Market Profiles and Competitiveness Inventory Report—Volume 2

STUDY ON MARKET

COMPETITIVENESS AND

FINANCIAL PATTERNS OF FARMER

PRODUCER ORGANISATIONS

(FPOs) IN TELANGANA AND

KARNATAKA

M.KANDEEBAN B.Sc., (Ag.)

MASTER OF BUSINESS ADMINISTRATION

(AGRIBUSINESS MANAGEMENT)

2015

STUDY ON MARKET COMPETITIVENESS

AND FINANCIAL PATTERNS OF FARMER

PRODUCER ORGANISATIONS (FPOs) IN

TELANGANA AND KARNATAKA

BY

M.KANDEEBAN B.Sc., (Ag)

PROJECT SUBMITTED TO THE

ACHARYA N.G. RANGA AGRICULTURAL UNIVERSITY

IN PARTIAL FULFILMENT OF THE REQUIREMENTS

FOR THE AWARD OF THE DEGREE OF

MASTER OF BUSINESS ADMINISTARTION (AGRIBUSINES MANAGEMENT)

CHAIRPERSON: Smt.Y.PRBHAVATHI

DEPARTMENT OF AGRIBUSINESS MANAGEMENT AGRICULTURAL COLLEGE, TIRUPATI

ACHARYA N.G. RANGA AGRICULTURAL UNIVERSITY

RAJENDRANAGAR, HYDERABAD – 500 030

2015

I

DECLARATION

I, Mr. M.KANDEEBAN, hereby declare that the project entitled “STUDY

ON MARKET COMPETITIVENESS AND FINANCIAL PATTERNS OF

FARMER PRODUCER ORGANISATIONS (FPOs) IN TELANGANA

AND KARNATAKA” submitted to Acharya N.G. Ranga Agricultural

University, Hyderabad for the award of degree of MASTER OF BUSINESS

ADMINISTARTION (ABM) is the result of original research work done by

me. I also declare that no material contained in this project has been published

earlier in any manner.

Place: (M.KANDEEBAN)

Date: I.D No- TMBA- 2013/09

II

CERTIFICATE

Mr. M.KANDEEBAN has satisfactorily prosecuted the course of research

and that the project entitled “STUDY ON MARKET COMPETITIVENESS

AND FINANCING PATTERNS OF FARMER PRODUCER

ORGANISATIONS (FPOs) in TELANGANA AND KARNATAKA”

submitted is the result of original research work and is of sufficiently high

standard to warrant its presentation to the examination. I also certify that

neither the project nor its part thereof has not been previously submitted by him

for a degree of any university.

Date :

(Smt. Y. PRABHAVATHI)

Assistant Professor

Department of Agricultural Business

Management

S.V. Agricultural College,

Tirupati.

III

CERTIFICATE

This is to certify that the project entitled “STUDY ON MARKET

COMPETITIVENESS AND FINANCIAL PATTERNS OF FARMER

PRODUCER ORGANISATIONS (FPOs) IN TELANGANA AND

KARNATAKA” submitted in partial fulfillment of the requirements for the award

of degree of ‘MASTER OF BUSINESS ADMINISTRATION (ABM) to the

Acharya N.G. Ranga Agricultural University, Hyderabad, is a record of the

bonafide research work carried out by Mr. M.KANDEEBAN under our

guidance and supervision. The subject of the project has been approved by the

Student’s Advisory Committee.

No part of the project has been submitted by the student for the award of

any other degree or diploma. The published part has been fully acknowledged.

All assistance and help received during the course of the investigations have been

duly acknowledged by the author of the thesis.

Thesis approved by the Student’s Advisory Committee

Chairperson : Smt. Y. PRABHAVATHI

Assistant Professor

Department of Agricultural Business

Management

S.V. Agricultural college,

Tirupati- 517502, A.P

______________

Member : Dr. B. APARNA

Assistant Professor

Department of Agricultural Economics

S.V. Agricultural college,

Tirupati- 517502, A.P.

______________

Member : Dr. G. MOHAN NAIDU

Assistant Professor and Head

Department of Statistics and

Mathematics

S.V. Agricultural college,

Tirupati- 517502, A.P.

______________

Date of final viva-voce:

IV

ACKNOWLEDGEMENT

There are no proper words to convey my deep gratitude and respect for my Project and research advisor, Smt. Y.PRABHAVATHI. She has inspired me to become an independent researcher and helped me realize the power of critical reasoning.

I am also indebted to Dr. P.RAGHURAM, who has been constant source of encouragement and enthusiasm, not only during this project work but also during the two years of my Masters program.

With deep respect and esteem regards I owe my indebtedness to Dr.I.BHAVANIDEVI, Professor and Head, Department of Agricultural Business Management, S.V. Agricultural College, Tirupati.

Special thanks must go to Professor C.S.SUNDARESAN who taught me the delight of studying farmer producer companies and encouraged me to pursue my interests in farmer producer companies.

I humbly offer my heartfelt thanks to Dr. G.MOHAN NAIDU and Smt. B.APARNA member of my Advisory Committee, for their unstinted help, support, suggestions and whole hearted co-operation during the execution of my research work.

I would like thank all the members of ALC, who constantly welcome me every time I visited their office and helped me all the way throughout my project.

I will never forget all chats and beautiful moments with my classmates. They were fundamental in supporting me during stressful and difficult moments in these two years. CHANDU, ANU, VINEEL, NARAYANA ANNA, PHANI, SHINY. And special thanks to ADHI for his support throughout my stay and especially during this project period.

V

I am very grateful to thank Smt. RAJALAKSHMI madam, Teaching Associate whom always helped in studies and constantly giving me advice which supported me largely. And I also thank Mr. MAHESH and Smt. POOJITHA, Teaching Associate for their strong support during my course period.

I owe my sincere thanks to my juniors PRASANTH, PRADEEP, VASU, ABHI, ANANAD and PRIYANKA for their generous help and unparallel affection.

I further extend my thanks to my seniors and friends in S.V.Agricultural college ARUNODHAYAM SIR, GOVARDHAN SIR,SURYA, SWATANTRA MISHRA,ROUTROY,MADHAN, AMAR, D.V, SOMU ,PEERU, VEDA, NARESH and LOKANATHAN for their constant encouragement and moral support were my strongest assets during the period of my study.

I cannot forget friends who went through hard times together, cheered me on, and celebrated each accomplishment: ANBU, GOKUL, ARTHEE, KANI, PREETHA, TAMIL, AMAR, MANI, KARTHICK SIR, SABARI AND PRASANTH.

I would like to express my gratitude to my love PRIYANGA for her unfailing emotional support. I also thank for heart-warming kindness from the family of my Sister’s GOMATHI, PRABA, KUMAR MAMA, SENTHIL MAMA AND RAJA MAMA.

Finally, my deepest gratitude goes to my parents MARAPPAN and SAKTHI for their unflagging love and unconditional support throughout my life and studies. You made me live the most unique, magic and carefree childhood that have made who I am now!

M.Kandeeban...

VI

CONTENTS

Chapter No. Title Page No.

I INTRODUCTION 1

II REVIEW OF LITERATURE 14

III MATERIAL AND METHODS 22

IV RESULTS AND DISCUSSIONS 36

V SUMMARY AND CONCLUSIONS 75

LITERATURE CITED 84

VII

LIST OF TABLES

Table

No

Title

Page

No

1.1

Difference between PCs and cooperatives

4

3.1

List of the sample FPCs

24

4.1

Volume of red gram sales business done by FPCs for two

years

38

4.2

Analysis of marketing costs under different channels in the

marketing of red gram (Rs/Qn)

45

4.3

Analysis of marketing margins under different channels in the

marketing of red gram (Rs/Qn)

46

4.4

Price spread under different marketing channels in the

marketing of red gram (Rs/Qn)

47

4.5

Indices of marketing efficiency in the selected marketing

channels

48

4.6

Redgram prices in various marketing scenario in Telangana

(2014-15)

55

4.7

Redgram prices in various marketing scenario in Karnataka

(2014-15)

55

4.8

Redgram prices in various marketing scenario in Telangana

(2013-14)

56

4.9

Redgram prices in various marketing scenario in Karnataka

(2013-14)

56

4.10

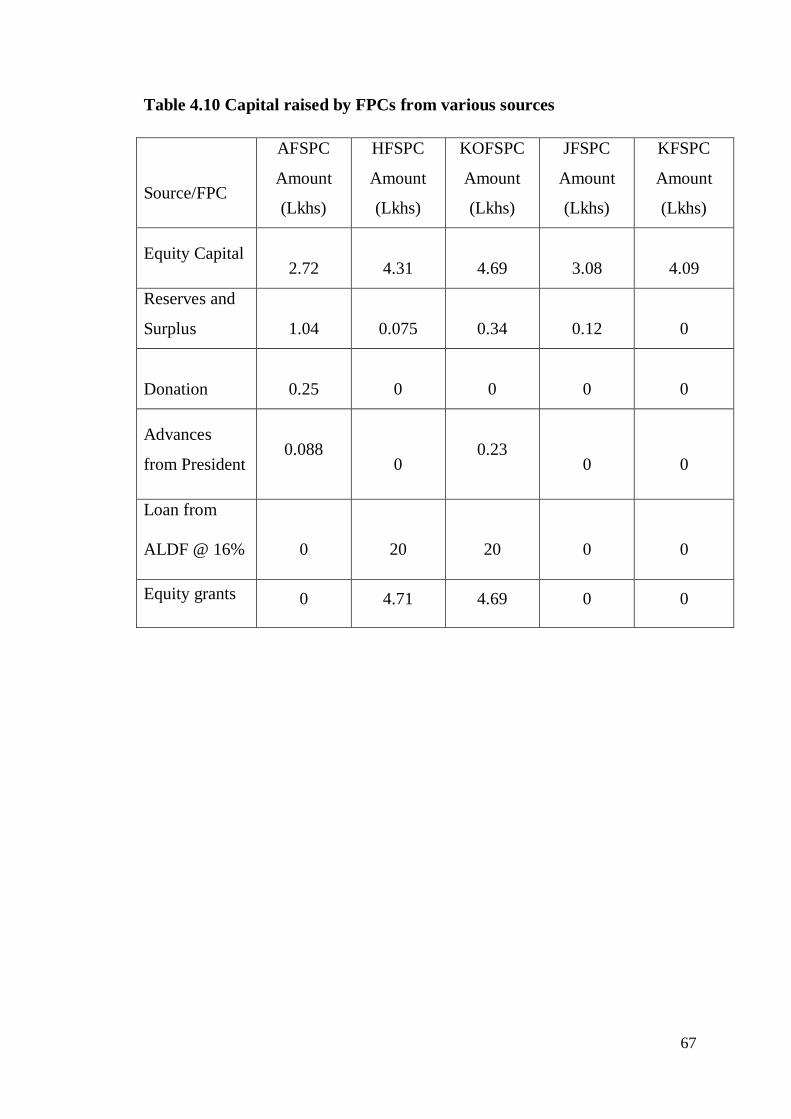

Capital raised by FPCs from various sources

67

4.11

Financial Ratios of the FPCs for 2013-14 and 2014-15

74

VIII

LIST OF ILLUSTRATIONS

Figure

No

Title

Page

No

4.1

Volumes of red gram sales done by FPCs in 2013

39

4.2

Volumes of red gram sales done by FPCs in 2014

39

4.3

Marketing costs incurred by various intermediaries in

channel I

49

4.4

Marketing costs incurred by various intermediaries in

channel II

50

4.5

Marketing margins earned by various intermediaries in

channel I

51

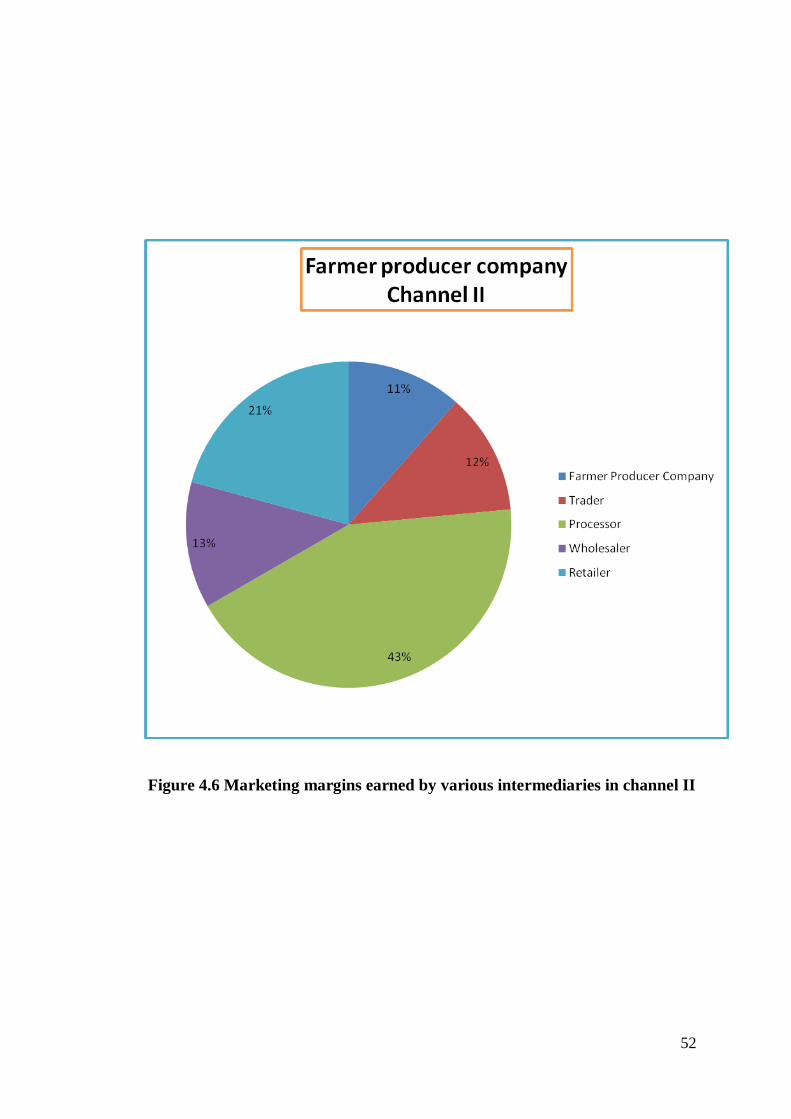

4.6

Marketing margins earned by various intermediaries in

channel II

52

4.7

Sources of Own Capital

59

4.8

Equity shares of selected FPCs

60

4.9

Sources of grant capital

62

4.10

Source of debt capital

63

4.11

Various schemes to assist FPCs

66

IX

LIST OF ABBREVIATIONS AND SYMBOLS

AFSPC - Angadiraichur Farmers Services Producer Company Limited

ALC - Access Livelihood Consultancy

ALDF - Access Livelihood Development Finance

APMC - Agricultural Produce Marketing Committee

BoD – Board of Director

CIGs - Common Interest Groups

e.g. - Example

EGCGFS - Equity Grant and Credit Guarantee Fund Scheme for Farmer

Producer Companies

et al – And others

FAGs – Farmer Affinity Groups

FAO - Food and Agriculture Organization

FPCs - Farmer Producer Companies

FPOs - Farmer Producer Organisations

GBY - Gramin Bhandaran Yojana

HFSPC - Hasnabad Farmers Services Producer Company Limited

i.e. - That is

JFSPC - Jalwad Farmers Services Producer Company Limited

KFSPC - Kalkeri Farmers Services Producer Company Limited

KOFSPC - Kodangal Farmers Services Producer Company Limited

lkhs – Lakhs

MC - Marketing cost

MDH - Mission for Integrated Development of Horticulture

MM- Marketing margin

MME - Index of Marketing Efficiency

X

MSP - Minimum support price

NABARRD – National Bank for Agriculture and Rural Development

NABFINS - NABARRD finance service limited

NFSM - National Food Security Mission

NGCs - New Generation Cooperatives

NGOs - Non-governmental organisations

PACS – Primary Agricultural Credit Society

PC - Producer Company

PODF - Producer Organisation Development Fund

PRADAN - Professional Assistance for Development Action

Qn – Quintal

ROE- Return on Equity

Rs – Rupees

SFAC - Small Farmers’ Agri-Business Consortium

SHGs - Self-Help Groups

tn – Tonnes

UN - United Nations

UNDP - United Nations Development Programme

VAPCOL - Vasundra Agri-horti Producer Company limited

VCA - Venture Capital Assistance Scheme

VIUC - Vegetable Initiative for Urban Cluster

viz. - Namely

XI

ABSTRACT

Title of the Project : STUDY ON MARKET COMPETITIVENESS

AND FINANCING PATTERNS OF FARMER

PRODUCER ORGANISATIONS (FPOS) IN

TELANGANA AND KARNATAKA

Name of the author : M. KANDEEBAN

Major Advisor : Smt. Y.PRABHAVATHI

Degree to which it is

submitted

: MASTER OF BUSINESS MANAGEMENT

(ABM)

Faculty : AGRICULTURE

Department : AGRIBUSINESS MANAGEMENT

University : Acharya N.G.Ranga Agricultural University

Year of submission : 2015

The present study entitled “Study on Market competitiveness and

Financing Patterns of Farmer Producer Organisations (FPOs) in Telangana and

Karnataka” was intended to examine the value chain, market competitiveness,

financial models and assessment of FPCs.

Two-stage purposive sampling technique was adopted to select the

ultimate sample units. The study was undertaken in five FPCs in Telangana and

Karnataka states. For the present study, Mahabubnagar district of Telangana

state and Bijapur district of Karnataka were selected as these were backward

districts in their respective states. Three FPCs in Telangana state and two FPCs

in Karnataka state were purposively selected since these FPCs were promoted

by the same promoter. Both conventional analysis and financial ratio

techniques were used to analyze the data and arrive at valid conclusions.

All the specified FPCs were involved in direct marketing and handled

single commodity i.e. redgram. In 2013, the maximum and minimum volume

XII

of produce was handled by KOFSPC (190 tonnes) and KFSPC (120 tonnes)

respectively. In 2014, maximum and minimum volume of produce was handled

by AFSPC (136 tonnes) and JFSPC (102 tonnes) respectively. The marketing

channel of redgram currently followed by specified FPCs: Farmers – Farmer

Producer Company - Traders - Miller – Wholesaler – Retailer – Consumer.

The cost incurred in marketing of redgram in channel I (Rs.2732) was

higher than channel II (Rs.2463). The marketing margins earned in marketing

of redgram through channel II (Rs.915) were less than channel I (Rs.948). The

price spread in the case of channel I (Rs.3440) was higher than channel-II

(Rs.3225). The producer’s share in consumer’s rupee (PSCR) in channel II

(64.560 per cent) was more than in channel I (62.198 per cent). The marketing

efficiency of channel I was 1.53 and that of channel II was 1.73. It infers that

channel II was more efficient than channel I.

The prices that are arranged by the five FPCs for redgram in 2013-14

and 2014-15 for the farmer members were relatively on the higher side when

compared to modal price (Tandur market in Telangana state and Gulbarga

market in Karnataka state) and MSP.

The leverage ratios, profitability ratios, debt ratio and earnings per share

of all but one i.e. KFSPC, indicated reasonably good performance of the FPCs

though they were hardly two years old.

CHAPTER I

Introduction

1

Chapter - I

INTRODUCTION

A majority of the world’s poor belong to agricultural based rural

households.Small and marginal farmers constitute the largest group of

cultivators in Indian agriculture. About 85 per cent of the operated holdings are

smaller than two hectares and amongst these holdings 66 per cent are less than

one hectare (Singh, 2012). The increasing number of agricultural suicides

among small and marginal farmers (National Crime Records Bureau, 2011) is

any indication that these farmers are struggling to survive. While indebtedness

is often cited as the immediate reason for distress (Reserve Bank of India 2006

and Satish, 2007), deeper issues are related to vulnerability to risk in

agricultural production. These issues include lower scale of operation, lack of

information, poor communication linkages with the wider markets and

consequent exploitation by intermediaries in procuring inputs and marketing

fresh produce, access to and cost of credit (Dev, 2005) and in isolated cases

aggressive loan recovery practices (Sriram, 2008).

Despite growing market opportunities, there is a danger that small

farmers will be squeezed out, even though they possess some competitive

advantage over larger producers, especially in their low cost in accessing

family labour and intensive local knowledge (Poulton et al., 2005). The

disadvantages they face are high unit transaction costs in almost all non-labour

transactions (Poulton et al., 2005). Furthermore, over the last two decades

structural adjustment programmes have led to a decline in state-funded

agricultural support, with the result that many farmers find it difficult to access

inputs, extension and training.

A variety of approaches have emerged in response to the problems faced

by the small and marginal farmers. The first approach is the facilitation of

collective action by small and marginal farmers. Agricultural cooperatives,

formed under the Co-operative Credit Societies Act, 1904, have long been the

2

dominant form of farmer collectives; however the experiences with

cooperatives point too many limitations that prevent effective collective action.

The co-operative form of organisation has been perceived and seen as a means

to achieving reduction in poverty and increase in well being of local people

(Birchall, 2003) in the presence of other structural constraints like small

holdings, lack of bargaining power of small sellers of produce or services and

competition from other forms of organizations. But, co-operatives across the

developing world have been more of a failure than success and are alleged to

have led to exclusion of really poor, elite capture of such bodies, promoting

differentiation instead of equity in rural communities like in the case of sugar

co-operatives in Gujarat (Ebrahim, 2000).

There is increasing recognition that the opportunity for smallholders to

raise their incomes from agricultural production, natural resource management

and related rural enterprises depends on their ability to participate successfully

in markets. As a consequence, the focus of research and development has

broadened from building up farmers’ production capabilities to facilitating

farmers’ access to markets (Shepherd, 2007).

At the market end of agricultural value-chain, private participation is

being promoted through contract farming, particularly after the amendment of

the Agricultural Produce Marketing Committee (APMC) Act in 2003. Contract

farming involves agricultural production based agreement between a

corporation and the farmer for production and supply of agreed quantities of a

product meeting certain quality standards (FAO, 2014). However, contract

farming arrangements tend to exclude small producers (e.g.,Gill, 2004; Hazell,

2005; Singh, 2009; Pritchard and Connell, 2011) and in many instances have

benefited the buyers at the expense of the producers (Hellin et al., 2009).

In India, there are many legal forms of organisations through which

primary producer can organise themselves. A producer organization is a

generic name that represents different forms of community organizations such

as large cooperatives, Primary Agricultural Credit Society (PACS), Self-Help

3

Groups (SHGs), Federation of SHGs, Common Interest Groups (CIGs),

Farmers Club, Producer Company, etc. However, a producer company is a

special case of producer organization that is registered under Section IXA of

the companies Act, 1956 (Sukhpal and Tarunvir , 2012).

In this context, there has been a constant search for alternative forms of

collectivization or co-operation to achieve the objectives of development of

poor people though some researchers also differentiate between collectivization

and co-operation in the sense that whereas former refers to organizing to avoid

exploitation in markets and the latter as organising in situations of missing

markets (Shah,1996).Cooperatives concept is one of the options available for

the farmers to get organized themselves to move up in the value-chain and

having business ownership. The below-par performance of cooperatives except

for certain commodities viz, milk and fertilizers, led to the emergence of ‘New

Generation Cooperatives (NGCs)’ with advanced member-friendly profile

(Singh 2008). Difference between cooperatives and PCs was given in Table

1.1.

Ironically, the concept of NGCs too could not overcome certain pulling

factors like preferred share premium, limited rights of members on internal

control mechanism, suitability only to large holders, functioning like closely-

held companies, risk of becoming investor-oriented company, off-market

purchases to meet contract terms, leasing of delivery rights by members and

dependency on non-producer member equity and non-member business.

A producer company (PC) is one such and relatively new legal entity of

the producers of any kind, viz., agricultural produce, forest produce, artisan

products, any other local produce where the members are primary producers.

PC as a legal entity was enacted in 2003 as per section IXA of the Indian

Companies Act 1956. Since the above enactment the PC has been hailed as an

organizational form that will empower and improve the bargaining power, net

income and quality of life of small and marginal farmers/producers in India.

4

Table 1.1: Difference between Co-operatives and Producer Companies

Feature Co-operatives Producer Companies

Registration under Co-operatives act Companies act

Membership Open to any individual or

co-operative

Only to producer

members and their

agencies

Professionals on

Board Not provided Can be co-opted

Area of operation Restricted Throughout India

Relation with other

entities Only transaction based

Can form joint ventures

and alliances

Shares Not tradable Tradable within

membership only

Member stakes No linkage with number of

shares held

Articles of Association

can provide for linking

shares and delivery rights

Voting rights

One person one vote but

Registrar of companies and

government have veto

power

Only one vote for one

member and non-member

can’t vote

Reserves Can be created when made

profit

Mandatory to create

reserves

Profit sharing

Limited divided on capital

Based on patronage but

reserves must and limit on

dividend

Role of government Significant Minimal

Disclosure and audit

requirements Annual report to regulator

Very strict as per the

companies act

Administrative

control

Excessive

None

Dispute settlement Through co-op system Through arbitration

5

While each member in a PC can have only one vote, he/she can

contribute different amounts of share capital to the PC. The shares of the PC

members cannot be transferred outside the membership. A PC should have a

minimum of ten members or two producer entities or a combination thereof. By

virtue of assigning equal voting rights to each member, the issue of

management control by small and marginal producers has been resolved in the

design of PC. In spirit, the current PC design also takes into account the

efficiency of the community of producers rather than the efficiency of

shareholders/financiers of a profit seeking company.

Primary producer’s organisations or collectivities are being argued to be

the only institution which can protect small farmers from ill-effects of

globalization or make them participate successfully in modern competitive

markets (Trebbin and Hassler, 2012).

In the recent years, the focus of the Government of India, state

governments and the various development agencies has been towards producer

companies. The international development agencies including the United

Nations (UN) agencies such as World Bank, United Nations Development

Programme (UNDP) and Food and Agriculture Organization (FAO) have been

showing their interest in investing in these organizations. Many of the non-

governmental organizations (NGOs) in the country had been facilitating

formation of producer organizations and in the recent years and some of them

have graduated to facilitate formation of producer companies on behalf of the

state governments and development funding agencies.

1.1 PROBLEM STATEMENT

Producer’s organization not only help farmers buy or sell better due to

scale benefits but also lowers transaction cost for sellers and buyers besides

providing technical help in production and creating social capital. In

Mozambique, where 80 percent farmers are small holders and only 7.3 percent

were members of farmer organisation in 2005, the membership in farmers’

6

organisations led to 50 percent increase in profits for small farmers from the

crops handled by the organization (Bachke, 2011). It is also argued that co-

operatives or such collectivities are needed for small farmers to help them

realize better output prices and credit terms and thus can help eliminate

interlocking of factor and product markets into which small farmers are

generally trapped (Patibandla and Sastry, 2004).

As on June 2015, there were over 445 PCs in India. The above PCs sell

their produce to any large national and international buyers/processors or to

their promoters. In its attempt to aggregate the produce from the small

producers, the above PC model focuses on the common interest groups (CIGs)

or self-help groups (SHGs) as the basic unit for aggregation with no limit on

the size of membership and size of cluster/operational area.

Farmers’ cooperatives in the erstwhile socialist economies worked

largely to bring together small farmers enabling them to pool their resources

and enhance their output. Currently farmer producer organisations (FPOs) work

in the dynamic and ever evolving market economies and promote the

entrepreneurial spirit. Most of the FPOs are either simple farmer producer

aggregator functioning to increase their share in the consumer price or work to

eliminate one or two intermediaries from the supply chain. Despite several

success stories, marketing still remains a challenge. Against this background, in

present study entitled “Study on Market competitiveness and Financing

patterns of Farmer Producer Organisations (FPOs) in Telangana and

Karnataka” has been undertaken with following specific objectives

1.2 OBJECTIVES OF INVESTIGATION

1. to identify the stage of the FPOs and its market readiness in terms of

products and volumes

2. to map the current value chain with existing FPOs value chain to single

&multi commodity

7

3. to estimate the market competitiveness of the FPOs

4. to identify the capital and credit availability models of the FPOs

5. to examine viability of FPOs in terms of capital and financing patterns

1.3 SCOPE OF THE STUDY

The study attempts to understand the current mode of operation, market

competitiveness and financial viability of the PCs with reference to the small

and marginal farmers/producers in the states of Karnataka and Telangana. This

in turn, helps to review the design of the PC and the amendments and policy

mechanisms that may be necessary to make the PC an effective institutional

arrangement of the small and marginal farmers/producers leading to

development of small producers in rural India.

1.4 LIMITATIONS OF THE STUDY

The study has the limitations of time, fund, other physical facilities

needed for the research and resources at the disposal of investigator. Marketing

information such as price, quantity and cost were obtained and presented in the

study is based on recall memory of different actors. Further financial

information obtained was not at required standard and validity of data in the

statements is also questionable. Besides these, single person research study is

always confronted with various bottlenecks and the present study is no

exception to these limitations. And hence the findings could be generalized to a

limited extent to compare PCs. But exhaustive care has been taken in

collection, analysis and presentation of the data.

1.5 PLAN OF THESIS

The thesis is presented in five chapters. The first chapter describes the

various producer organisations in India along with specific objectives. It also

describes the difference lies between PCs in the state of Karnataka and

Telangana. Within first chapter, the selected five FPCs profile in brief were

8

also discussed. Review of literature on Farmer Producer Companies and

marketing and finance related field is cited in the second chapter. The third

chapter presents the material and methods adopted in this study. The fourth

chapter encompasses a critical analysis of the results and discussion. The

summary and conclusion emerged from the study form the integral part of the

fifth chapter.

9

BREIF PROFILE OF FIVE FPCs

1. Angadiraichur Farmers Services Producer Company (AFSPC)

Angadiraichur Farmers Services Producer Company is located in

Angadiraichur village, Kodangal mandal, Mahabubnagar district of Telangana

state. The company was registered on 14-11-2013 with corporate Id

U01400AP213PT06484891. The producer company is located at a distance of

18 km away from the mandal and is remotely placed with no or less

communication and transportation facilities. The total number of shareholders

of the AFSPC is 503 in number residing in 10 villages namely Chitlapalli,

Angadiraichur, Ravalpalli, Tekulakoderu, Dharmapur, Boipallytanda,

Sangaipalli, Mothkulabanddatanda, Kasturpally and Indanoor.

The company has 10 Board of Director (BoD) members and 62

Representative General Body Leaders (RGB) members associated in 31

Farmers Affinity Groups (FAGs). The authorised capital of the company was

10 lakhs and the issued capital as on 31.03.14 was 2.83 lakhs. All the members

of the company were women farmers. In order to become a member of the

company individual farmer has to purchase a minimum of 50 shares each share

value being Rs.10.

ALC, social enterprise is playing a prominent role both in functioning of

FPC and also in improving the living standards of the farmers. As the district is

totally rainfed, most of the farmers in the study area grow redgram. The main

function of the FPC is procurement and effective marketing of redgram.

10

2. Hasnabad Farmers Services Producer Company (HFSPC)

Hasnabad Farmers Services Producer Company is located in Kodangal

mandal, Mahabubnagar district of Telangana state. The company was

registered on 27.3.2013 with corporate Id U01400AP2013PTC08666. The

producer company is located about 20 Km and 100 Km from Tandur and

Hyderabad respectively. The total number of shareholders of the HFSPC is 834

in number residing in 10 villages namely Hasnabad, Peddanandiganma,

Chinnanandigama, Neetur, Chitlapally, Hussianpur, Kudurumalla, Aledu,

Mysammathanda and Burjukhanpally. The farmers in these villages grow

mainly red gram.

The company has 10 Board of Director (BoD) members and 96

Representative General Body Leaders (RGB) members associated in 48

Farmers Affinity Groups (FAGs). The authorised capital of the company was

15 lakhs and the issued capital as on 31.03.14 was 4.32 lakhs. Only the women

farmers can be members of the company. In order to become a member of the

company individual farmer has to purchase minimum of 50 shares of each

share value being Rs.10.

Access Livelihoods Consulting India Ltd (ALC), a social enterprise,

initiated the farmers to take up and start - farmer producer organisation. With

the empanelment of Small Farmers Agribusiness Consortium (SFAC), ALC

has promoted the farmer producer organisations in Kodangal mandal of

Mahabubnagar district. As the area is majorly rainfed farmers mainly cultivate

redgram. The main function of the FPC is procurement and marketing of

shareholders produce (redgram).

11

3. Kodangal Farmers Services Producer Company (KOFSPC)

Kodangal Farmers Services Producer Company was registered on 3rd

April 2013, with its registered office at Kodangal mandal, Mahabubnagar

district. ALC India ltd, a social enterprise was instrumental in the formation of

KOFSPC. The company’s corporate Id is U01400AP2013P TC086781. In each

and every aspect of the business and operations, ALC has played a crucial role

in its functioning of producer company.

There are around 46 FAGs in KOFSPC and 92 representative general

body leaders with farmer shareholders 915. Most of the FAGs are located in the

villages Kodangal, Bulkapur, Kondareddypally, Regadimailaram,

Ashammakunta, Thandaparsapur and Udimaheshwaram. The farmers in these

villages grow mainly redgram. The authorised capital of the company was 15

lakhs and the issued capital as on 31.03.14 was 4.71 lakhs. As in the other

FPCs only the women farmers can become as member of the company. In order

to become a member of the company individual farmer has to purchase

purchase a minimum of 50 shares each share value being Rs.10.

12

4. Jalwad Farmers Services Producer Company (JFSPC)

Jalwad Farmers Services Producer Company is located in Sindagi taluk,

Bijapur district of Karnataka state. The company was registered on 18.12.2013

with corporate Id U01400KA2013P TC072632. The head office of the

company was located in a village namely Ashki. All the members of the FPC

were women farmers. The district is totally rainfed and the environment is

suitable for growing pulses. The total number of shareholders of the JFSPC is

948 in number residing in 5 villages namely Jalwad, Mannur, Devur, Koravur

and Imbrahimpur.

The company has 10 Board of Director (BoD) members and 102

Representative General Body Leaders (RGB) members associated in 51

Farmers Affinity Groups (FAGs). The authorised capital of the company was

10 lakhs and the issued capital as on 31.03.14 was 4.5 lakhs. Only the women

farmers can be members of the company. In order to become a member of the

company individual farmer has to purchase 50 shares of Rs.10 each.

Access Livelihoods Consulting India Ltd (ALC), a social enterprise,

initiated the farmers to take up and start - farmer producer organisation. With

the empanelment of Small Farmers Agribusiness Consortium (SFAC), ALC

has promoted the farmer producer organisations in Sindagi taluk of Bijapur

district. The main function of the FPC is procurement and marketing of

shareholders produce.

13

5. Kalkeri Farmers Services Producer Company (KFSPC)

Kalkeri Farmers Services Producer Company is located in Sindagi taluk,

Bijapur district of Karnataka state. The company was registered on 20.12.2013

with corporate Id U01400KA2013PTC07247. The producer company is

located about 60 Km and 50 Km from Sindagi and Bijapur respectively. All the

members of the FPC were women farmers. The district is totally rainfed and

suitable for growing pulses. Access Livelihoods Consulting India Ltd (ALC), a

social enterprise, initiated the farmers to take up and start - farmer producer

organisation.

The total number of shareholders of the KFSPC is 1023 in number

residing in 5 villages namely Ashki, Niralgi, Bekinal, Kalkeri and B.B.Jngalgi.

The company has 9 Board of Director members and 116 RGB Leaders

members associated in 58 Farmers Affinity Groups (FAGs). The authorised

capital of the company was 15 lakhs and the issued capital as on 31.03.14 was

4.8 lakhs. Only the women farmers can be members of the company. In order

to become a member of the company individual farmer has to purchase a

minimum of 50 each share value being Rs.10 each.

CHAPTER II

Review of Literature

14

Chapter- II

REVIEW OF LITERATURE

In this Chapter, an attempt has been made to critically review the

literature of the past research work done in relevance to the present study.

Comparatively a fewer number of studies were reported on the market

competitiveness and financial models in general and in FPCs in particular. An

account of previous research work done related to the present study and other

forms of farmer organisations is presented under the following heads,

2.1 Studies on producer organisations

2.2 Studies on marketing channels

2.3 Studies on marketing readiness

2.4 Studies on market competitiveness, and

2.5 Studies on financing of FPCs

2.1 STUDIES ON PRODUCER ORGANISATIONS

Rondot and Collion (2000) defined the producer organizations as formal

rural organizations whose members organized themselves with the objective of

improving farm income through improved production, marketing, and local

processing activities. Producer Organisations deal with policies on issues such

as pricing and export and import of agricultural products; improvement of

agricultural production practices; access to inputs and services, including

agricultural credit; marketing of agricultural production; and local processing

of agricultural production and its marketing.

Bijman and Wollni (2008) defined the producer organization is an

association, a society, a cooperative, a union, a federation, or even a firm that

has been established to promote the interests of farmers. The main goal of the

15

producer organisation was to provide services that support producers in their

farming activities, including the marketing of the farm products.

Shylendra (2009) explained producer company as a new answer to

rectifying the imperfect experiences of cooperatives and to answering the social

requirements of aggregating small and marginal farmers, strengthening their

leverage through collective means, and integrating their livelihoods into

remunerative markets.

Tanguy and David (2009) suggested that the poorest of the poor tended

to be excluded from membership in marketing cooperatives in Ethiopia.

However, they stood to benefit from the positive spillovers generated by some

types of cooperative activities, although these benefits were often limited when

compared to those accruing to members.

Dhakal (2013) concluded that farmers' organizations were collapsed due

to the lack of ownership, group management skill and inability to link with

market. The business skills, technical skills and organizational management

skills of ARC (Agricultural Resource centres) members were not promoted

parallel. Autonomy and adequacy of time given to select the enterprise for

groups has long term impact on ownership development. High level of external

influence lead ARCs for dependency and lack of problem solving ability

among members.

2.2 STUDIES ON MARKETING CHANNELS

Subbarao (1978) concluded that horizontal integration of wholesale

markets did not ensure competitive prices to the farmers. In villages

characterised by low level of infrastructure development coupled with low

staying power of farmers, competitive forces were weakened thus provided

opportunities to millers to make abnormal profit.

Deininger and Sur (2006) concluded that the ability to meet high food

safety and quality standards was lowest in smallholder agriculture because of

the scale economies. The most important reason was the inability of the

16

smallholder dominated production systems to meet the food safety and quality

requirements of the rich country markets.

Urban Poverty and Environment series report (2007) stated that to

minimize the cost of inputs and ensure proper handling of output by middle

men or command higher output prices, group negotiation through producers’

organizations’ was a valuable advantage. It also strengthened experience

sharing, and offered opportunities for inter-change programmes and training.

Gábor and Szabó (2009) proposed that producer-owned organisations

were good examples for the vertical integration based on the horizontal

coordination of farmers as initiators as they proved that by co-operation there

was an opportunity to significantly improve their countervailing power and to

establish ownership for farmers in the upper part of the food chain if they can

secure strict quality requirements, solid financing, loyalty and trust in their

organisations.

Trebbin and Hassler (2012) explained that the concept of producer

companies represented a tool for smallholder farmers to get organized and to

reap benefits - not only from joint action, but also from links to evolving high-

value markets in India's urban centres.

2.3 STUDIES ON MARKETING READINESS

Hellin et al. (2009) have suggested that the benefits of farmer

organization for market access were more evident in the vegetable sector,

characterized by high transaction costs. There was less incentive for farmers

producing an undifferentiated commodity such as maize to organize as the

transaction costs associated with market access were relatively low. Farmer

organizations that sold vegetables secured a very small percentage of the final

consumers’ price. Low volumes of product plus low margins meant that

ongoing subsidies were probably needed to cover operational costs.

The case study of the Vasundhara Agri-Horti Producer Company

(VAPCOL) show that producer companies can help smallholder farmers and

17

underprivileged rural communities to position themselves in a more demanding

market environment and to establish trading relations to modern retail

companies by conducting value adding processes and generate economies of

scale in output marketing. By selling larger quantities to a larger buyer, not

only transaction costs were reduced, but also the marketing risk. (2009)

Berdegué et al. (2008) concluded that for the producer organisations to

become viable, autonomous organizations, three factors seemed to explain their

success. The first was that they must act as vehicles for change. Producer

organizations’ can be effective for farmers who were willing to change their

practices, but not for those who wishes to maintain the status quo in the context

of traditional commodity production systems. The second factor was related to

the producer organisations’ networking capability. Effective organizations were

embedded in dynamic multi-agent networks that link their members to ideas,

resources, incentives and opportunities from beyond their rural communities.

Finally, a system of rules and incentives for the internal allocation of costs and

benefits, both among the members, and between the farmers as a group and the

organization itself, was key to success. With effective and sustainable producer

organisations’, these rules typically transmit undistorted market signals to

individual members, to which the members are able to respond.

Javier and Cavero (2012) argued that group of small producers through

producer organizations were capable of making strategic investments to gain

access to agro industrial markets where their produce was more profitable by

establishing more complex contractual arrangements with potential purchasers.

Lowering transactions costs through promoting producer organizations, will

not only make more likely that the less endowed small farmers enhance their

opportunities to access to agro industrial markets but also increase their net

incomes once they were able to access these markets.

Trebbin and Hassler (2012) concluded that Kabini Organics producer

company has helped farmers for the production of high-quality organic cotton

which was dependent on a seed supply alternative to the Bt cotton mainstream.

18

Getting organized into a producer company has helped these farmers overcome

the seed supply crisis and reach organic certification. The producer company

has been of great service to its members through a row of activities which

helped farmers tap till then unknown or unreachable sources of credit and

funding to stabilize their livelihood situation.

2.4 STUDIES ON MARKET COMPETITIVENESS

Estelle and Danies (2005) reported that competitiveness rests on cost

reduction strategies which can be achieved through economies of scale, either

in terms of input provision, technical assistance or commercial logistic through

farmer’s organization. It also relies on non-price factors such as reputation,

commercial efficiency, or specific quality attributes.

Rondot and Collion (2000) proposed that collective action and farmers’

organizations have gained renewed interest in recent years from governments,

donors and NGOs alike that see them as appropriate institutions for building

capacity among farmers by helping them participate in more competitive and

globalized market environments.

Barham and Chitemi (2009) studied and found that because of small size

of operation, small farmers were not only able to create scale economies, and

had low bargaining power because of low quantities of marketable surplus.

They also lacked capital, knowledge, information and market access, and

suffered from market imperfections, and poor infrastructure and

communications.

Fischer and Qaim (2012) concluded that collective action spurred

innovation through promoting efficient information flows and output price

advantages associated with collective marketing but relatively small in

magnitude.

Tita et al. (2013) argued that the group negotiated better prices

commensurate to the extra efforts made and so that members should be

19

satisfied with such prices. To be successful, producer groups should be able to

increase their bargaining power and one of such means was to have control

over members' produce. One way to do so may be to have access to micro-

credit in order to offer advanced payments to members to withhold produce

while waiting for an agreed market day, so that members are not tempted to sell

out of the group.

Varun Prasad (2013) proposed that the Farmer Producer Organization

(FPO) was the best of the structures, in terms of the express objective of

eliminating the “Moral Economy”, and argued for the same using the tools of

Transaction Cost Economics (TCE). He also argued that the problem of

individual farmers being unable to pursue litigation against corporate would

become less of an issue, because of the financial capacity of the FPO and

farmers, who were previously not exposed to any form of business

organization, have become “experts” in marketing their produce to the public, a

mere six months after their FPO was officially incorporated.

Robert and Peter (2014) inferred that farmer organisations have the

potential to improve services and reduce transaction costs but effective

mechanisms of downward accountability were necessary so that issues such as

poor management and elite capture can be addressed, and farmers are

motivated to invest in actions that have collective benefits. They also suggested

that for farmer organisations (and particularly for large farmer organisations) to

fulfil their potential roles in development, there needed to be a focus on

developing means of legitimising smallholder farmers’ rights, building their

capacity to challenge exclusion and moving from rights to obligations

regarding information provision.

Bernard and David (2015) concluded that many Rural Producer

Organisations (RPOs) still struggled to offer the type of commercialization

services that would lead to higher output prices for their members and it also

argued that trust in leaders’ motives and competence as well as trust in ordinary

members were crucial for successful collective commercialization as a form of

collective action.

20

2.5 STUDIES ON FINANCING OF FPCs

Braun and Immink (1994) proposed that the creation of producer

organizations is the most common solution to share the fixed costs necessary

for small holders to link to dynamic markets as the Rural Producer

Organisations is a form of collective action that improve both the farmers’

access to credit, information, and improved varieties of crops. And he also

stated that economies of scale, be it in production or marketing, producers will

have incentives for collective action, in the form of producer associations.

Bhattacharjee (2010) concluded that producer companies can be made

viable in the long run through provision of adequate support by the donor

agency and supportive environment and relaxing of the capital constraints and

as far as commodity based producer companies were concerned, there were

possibilities of both diversification of business, value addition possibilities and

integration with both input and output markets.

Marzena and Paul (2011) concluded that for the producer company to be

an influential and effective model for improving the livelihoods of small and

marginal producers, it has to overcome its credit constraints either with the help

of supporting policies and with an alteration of its design.

Pustovoitova (2011) proposed that the choice of company format and

business model should not limit farmers’ options, particularly in economic

sense. But, the working capital constraint in the initial stages locked the

producer company and its member farmers into a smaller scale, preventing the

company from engagement in value addition.

Catherine Ragasa (2012) concluded that membership commitment was

highly and positively correlated with performance of rural producer

organisations’ and in order to sustain financial contributions from members and

operations of rural producer organisations’, support will have to focus on the

economic viability and increasing incomes for the members. Marketing training

21

and extension approaches, including training on value chain approaches, is the

important strategy for supporting rural producer organisations’.

Jessop et al. (2012) identified that cooperatives or smallholder groups

can cooperate with public and private financial institutions in the mobilization

of smallholders to have a better education about financial services as well as

effective investments and risk management. Those initiatives from

smallholders’ cooperatives and groups would be crucial and useful for

achieving financial services and expanding their investment.

Bijiman and Wollni (2008) stated that monetary incentive to organise,

professionalise and innovate would support capacity building of producer

organisation. But, such a shift from direct payments to farmers towards

payments to producer associations also had negative aspects like subsidy-

dependence or making life more difficult for existing cooperatives.

Ampaire et al. (2013) suggested that promoting SACCOs as rural

financial institutions to support rural smallholder producers was a timely and

necessary solution to the current lack of credit in Uganda. He also suggested

policies guiding the establishment and loaning conditions should be reviewed

to match rural producers’ economic status.

CHAPTER III

Methodology

22

Chapter-III

METHODOLOGY

This chapter presents procedural details in selection of samples, method

of data collection and analytical techniques employed in attaining the stated

objectives of the study. The contents of the chapter are presented under the

following heads:

3.1. SAMPLING DESIGN

3.2. COLLECTION OF DATA

3.3. METHODS OF COMPUTATION

3.4. TOOLS OF ANALYSIS and

3.5. CONCEPTS AND TERMS USED IN THE STUDY

3.1. SAMPLING DESIGN

Two-stage purposive sampling technique was adopted to select the

ultimate sample units.

3.1.1. SELECTION OF STATE

Telangana and Karnataka states of Southern India were purposively

selected for the study as the producer companies located in these states are in

nascent stage.

3.1.2. SELECTION OF DISTRICT

Farmer Producer Companies (FPCs) prevailing in Mahabubnagar

district of Telangana and Bijapur district of Karnataka were selected

purposively for two reasons

The selected districts were backward compared to other districts in

respective states. (Source - Public Release: University of Hyderabad)

23

The existing FPCs in the above district were being promoted by single

promoter namely Access Livelihood Consultancy India Ltd (ALC).

3.1.3 SELECTION OF FPC

A list of 445 producer companies including cooperatives were identified

based on secondary data available from Small Famers Agribusiness

Consortium (SFAC) website. From the data obtained, producer companies are

classified based on the various promoters involved in it. There were totally 8

FPC’s in the state of Karnataka and 9 in the state of Telangana promoted by

several promoters. Taking into consideration of time and resources five FPCs

(two FPCs in Bijapur district of Karnataka state and three FPCs in

Mahabubnagar district of Telangana state) were purposively selected. The state

wise names of the selected FPCs were given in Table 3.1.

3.2 COLLECTION OF DATA

A set of pre-tested schedules were used to collect pertinent data from

farmer shareholders, FPC staff members, promoting agencies, other

stakeholders of FPC, other farmers, commission agents, traders , processors

and retailers. To examine the viability of FPCs secondary data were collected

from the annual financial statements maintained by each FPC. Other secondary

data includes collection of Minimum Support Price (MSP) of redgram from

Ministry of Agriculture website; modal prices of Tandur (Telangana) and

Gulbarga (Karnataka) market for redgram were collected from

agmark.net.nic.in. The data for the present study pertained to the financial year

2013-14.

24

Table 3.1: List of the sample FPCs

District

Name of the FPCS

Bijapur

(Karnataka)

1. Kalkeri Farmers services producer company

2. Jalwad Farmers services producer company

Mahabubnagar

(Telangana)

1. Angadiraichur Farmers services producer company

2. Hasnabad Farmers services producer company

3. Kodangal Farmers services producer company

25

3.3 METHODS OF COMPUTATION

The detailed procedure followed in computing the concepts is described

below.

3.3.1 Marketing costs

Marketing costs are the actual expenses incurred in bringing goods and

services from the producer to the consumers. The marketing costs normally

include

(i) Handling charges by various agencies involved

(ii) Assembling charges

(iii) Transport and storage costs

(iv) Expenses on secondary services like financing, risk taking and

market intelligence.

3.3.2 Marketing margin

Marketing margin is the summation of share earned by various market

intermediaries for moving the particular quantity of produce from producer to

consumer in particular marketing channel. And it includes

(i) Commission earned by commission agents

(ii) Margin earned by wholesaler

(iii) Margin earned by retailer

(iv) Margin earned by processor

3.3.3 Modal Price

Modal price is the price at which maximum quantity of produce has

been sold in a particular day in the particular market.

3.3.4 Price spread

It is the difference between the price paid by the consumer and the price

received by the producer for an equivalent quantity of the produce.

26

3.3.5 Producer’s share in consumer’s rupee

The percentage of amount that producer gets from the total amount paid

by consumer.

3.3.6 Inventories

Inventories include fertilizers, plant protection chemicals and unsold

produce maintained by FPC.

3.3.7 Trade receivables

These include the cash & cash equivalents to be received from the

farmer shareholders with in one accounting period.

3.3.8 Trade payables

These include the cash to be paid by the FPC to the input companies in

one accounting period.

3.3.9 Long term borrowings

These are loans availed by FPC to purchase fixed assets.

3.3.10 Short term borrowings

These are loans availed by FPC to meet working capital requirements.

3.3.11 Total Debt

Total Debt includes long-term borrowings and short-term borrowings.

3.3.12 Net worth

These include share capital, reserves and surplus.

3.3.13 Net assets

Net assets include net fixed assets and net current assets.

27

3.3.14 Net fixed assets

Fixed assets maintained by FPC minus depreciation.

3.3.15 Net current assets

It is current assets minus current liabilities

3.3.16 Other operating expenses

Other operating expenses include employee benefit expenses and other

selling and administrative expenses.

3.3.17 Cost of Goods sold

These include cost of materials consumed, purchase of stock-in-trade

and changes in inventories of finished goods, work in progress and stock-in-

trade.

3.3.18 Sales

The Company is making sales not only by selling fertilizers and

pesticide to farmers’ shareholders but also receiving commission by selling

members produce.

3.3.19 Gross profit

It is sales minus cost of goods sold by the FPC.

3.3.20 Net Profit

It is obtained when operating expenses, interest and taxes are subtracted

from the gross profit.

3.3.21 Number of shares outstanding

Total number of shares multiplied by number of shares each

shareholder is holding.

28

3.4. TOOLS OF ANALYSIS

3.4.1 Financial concepts utilized in the study

3.4.1.1 Balance sheet

In financial accounting, a balance sheet or statement of financial

position is a summary of a person's or organization's balances. A balance sheet

is often described as a snapshot of a company's financial condition. It

summarizes a company's assets, liabilities and shareholders' equity at a specific

point in time. These three balance sheet segments give investors an idea as to

what the company owns and owes, as well as the amount invested by the

shareholders. Of the four basic financial statements, the balance sheet is the

only statement which applies to a single point in time.

A company balance sheet has three parts: assets, liabilities and

ownership equity. The main categories of assets are usually listed first and are

followed by the liabilities. The difference between the assets and the liabilities

is known as equity or the net assets or the net worth or capital of the company.

It's called a balance sheet because the two sides balance out.

3.4.1.2 Current ratio

Current assets

Current ratio =

Current liabilities

It measures the liquidity position of a firm. A firm with a higher ratio

has better liquidity. A ratio of 2:1 is considered safe.

3.4.1.3 Quick ratio

Quick assets

Acid test or Quick ratio =

Current liabilities

29

It is an important index of firms’ liquidity. A ratio of 1:1 is considered

safe.

3.4.1.4 Debt ratio

Total debt

Debt ratio =

Net assets

It measures the share of the total assets financed by outside lenders. A

low ratio is desirable for creditors.

3.4.1.5 Debt- equity ratio

Total debt

Debt-equity ratio =

Net worth

This ratio indicates the relative proportion of debt and equity in

financing the assets of a firm. A ratio of 1:1 is considered safe.

3.4.1.6 Profit & loss statement

Income statement, also called profit and loss statement (P&L) or

statement of operations is financial statement that summarizes the revenues,

costs and expenses incurred during a specific period of time - usually a fiscal

quarter or year. These records provide information that shows the ability of a

company to generate profit by increasing revenue and reducing costs. The

purpose of the income statement is to show managers and investors whether the

company made or lost money during the period being reported. The important

thing to remember about an income statement is that it represents a period of

time. This contrasts with the balance sheet, which represents a single moment

in time.

30

3.4.1.7 Capital assets turnover ratio

Sales

Capital assets turnover ratio =

Net current assets

It measures the share of sales revenue from the net current assets. A high

ratio is better for creditors.

3.4.1.8 Operating expenses ratio

Cost of goods sold + other operating Expenses

Operating expenses ratio =

Sales

It measures the part of sales revenue consumed for meeting cost of

goods sold plus other operating expenses.

3.4.1.9 Gross profit margin ratio

Sales- cost of goods sold

Gross profit margin =

Sales

It measures the profit in relation to sales. The gross profit margin

reflects the efficiency with which FPCs produces each unit of produce. A high

gross profit margin is a good sign of investment and a low gross profit margin

reflects the higher cost of the goods sold.

3.4.1.10 Net profit margin ratio

Profit after tax

Net profit margin =

Sales

It measures the net profit of a firm with respect to sale. It indicates

management efficiency in manufacturing, administrating and selling the

31

produce. A firm with high net profit margin will survive in adverse economic

conditions.

3.4.1.11 Return on equity

Profit after Tax

Return on equity (ROE) =

Net worth

This indicates the share of owners’ profit from the total net profit.

Maximum value indicates maximum returns to the equity share holders.

3.4.1.12 Earnings per share ratio

Profit after tax

Earnings per share (EPS) =

Number of shares outstanding

It measures the profit available to the equity holders on a per share basis.

3.4.2 Marketing concepts utilized in the study

3.4.2.1 Marketing cost

The Marketing cost was estimated with the help of following formula

C = CF + Cm1 + Cm2 + Cm3 + .................. + Cmi

Where,

C = Total cost of marketing (Rs/Qn)

CF = Cost paid by the producer (Rs/Qn)

Cmi = Cost incurred by the ith

middle in the process of marketing (Rs/Qn)

3.4.2.2 Marketing efficiency

The Marketing efficiency of different Marketing channels considered

under the study was estimated by Acharya and Agarwal’s Approach

32

ME = FP / (MC + MM)

Where,

ME = Index of marketing efficiency

FP = Price received by the farmer

MC = Total marketing costs

MM = Net marketing margins

3.4.2.3 Producers share in consumers’ rupee

It is the price received by the produce expressed as percentage of the

retail price (price paid by the consumer). If Pr is the retail price and Pf is the

producers’ price, then the producers’ share in consumers’ rupee (Ps) may be

worked out as follows;

Ps = (Pf / Pr) * 100

Where,

Ps = Producers’ share in consumers’ rupee

Pf = Price received by the producer

Pr = Price paid by the consumer

3.5 CONCEPTS AND TERMS USED IN THE STUDY

3.5.1 Market competitiveness

It is the ability of a firm to offer products and services that meet the

quality standards of the local and world markets at prices that are competitive

and provide adequate returns on the resources employed.

33

3.5.2 Marketing channel

It is the path which a commodity is passed through from producer to the

ultimate consumer.

3.5.3 Marketing efficiency

Marketing efficiency is the measure of availability of information to all

the participants in a market that provides maximum opportunities to buyers and

sellers to effect transaction with minimum transaction costs.

3.5.4 Transaction costs

The costs associated with exchange of goods or services and incurred in

overcoming market imperfections.

3.5.5 Producer

One who actually produces the product by cultivating the land and

brings the surplus to the market to dispose and by their earn cash income.

3.5.6 Processor

Processor is the one who adds value to the produce by doing required set

of activities.

3.5.7 Wholesaler

One who makes the buying activity in large quantity and sell the goods

to the retailers in required quantities.

3.5.8 Retailer

Retailer is the one who finally disposes the produce to the consumer

after purchasing at the wholesale market.

34

3.5.9 Consumer

One who actually buy and utilises the produce.

3.5.10 Price spread

It is the difference between the price paid by the consumer and the price

received by the producer for an equivalent quantity of the produce.

3.5.11 Marketing costs

The total marketing cost is summation of cost involved in moving the

particular quantity of produce from producer to consumer

3.5.12 Marketing margin

The total marketing margin is summation of share earned by various

market intermediaries for moving the particular quantity of produce from

producer to consumer in particular marketing channel.

3.5.13 Current assets

Current assets are cash and other assets expected to be converted to

cash, sold, or consumed either in a year or in the operating cycle. These assets

are continually turned over in the course of a business during normal business

activity.

3.5.14 Current liabilities

Current liabilities are short-term financial obligations that are paid off

within one year or one current operating cycle. These liabilities are reasonably

expected to be liquidated within a year.

35

3.5.15 Long-Term liabilities

Liabilities that are not paid off within a year, or within a business's

operating cycle, are known as long-term or non-current liabilities. These

liabilities are reasonably expected not to be liquidated within a year.

3.5.16 Turnover

The main source of income for a company is its turnover, primarily

comprised of sales of its products and services to third-party customers.

3.5.16 Sales

Sales are normally accounted for when goods or services are delivered

and invoiced, and accepted by the customer, even if payment is not received

until sometime later, even in a subsequent trading period.

CHAPTER IV

Results & Discussion

36

Chapter - IV

RESULTS AND DISCUSSION

In attempt is made in this chapter to discuss critically the results

obtained from the study. The important findings of the study along with

relevant discussion are presented under the following heads in accordance with

the objectives of the study.

4.1 Market readiness of farmer producer companies in terms of products and

volumes

4.2 Mapping channels of farmer producer companies

4.3 Marketing efficiency of farmer producer companies

4.4 Market competitiveness of farmer producer companies

4.5 Credit availability models farmer producer companies and

4.6 Financial assessment of farmer producer companies

4.1 Market readiness of FPCs in terms of products and volumes

The market readiness of FPCs provides comprehensive understanding of

FPCs ability to capture market opportunities and to address changing market.

This section furnishes data on products handled; volume and size of business

made by FPCs in addition to addressing changing market needs are also

discussed.

4.1.1 Products Handled

Since all the FPCs are promoted by the same non-governmental

organisation (Access Livelihood Consultancy) the major decisions taken were

quite similar in all FPCs. The common crops cultivated in the study area during

kharif under rain fed condition are redgram, groundnut, sunflower, pearl millet,

maize and castor.

37

Though there are 4 to 5 major crops cultivated in the study area during

kharif season, FPCs limited their operation to redgram. This is because most of

the farmers in the study area are growing redgram due to prevailing rainfed

condition. This in turn shifted farmers towards growing redgram.

Presently, redgram is the major farm produce procured and sold by all

the selected FPCs. The other reason for FPC handling a single commodity is

the fact that it is in the initial stage of establishment. It is quite obvious that it is

difficult to handle many commodities which require huge capital and man

power.

The other reason behind single commodity business is the risk that lies

behind maintaining quality of the produce like groundnut and cotton which

needs specialised structures to store and maintain quality. Compared to the

other crops, red gram procurement involves less risk coupled with greater

volume of output which helps to have links with other market with relative

ease.

4.1.2 Volume of business

Market readiness of the farmers through FPCs exhibited different

scenarios. Normally, the presence of FPCs provides a particular mechanism

while procuring and arranging for sale. So the farmers were convinced about

the probable benefits they are going to receive once they become members of

FPCs. It is only two years since the FPCs have been registered; the data shows

certainly that there is an element of enthusiasm by members to sell their

produce through the FPCs.

From Table 4.1 we can observe that in 2013, produce of redgram that was

brought to FPCs was of 180 tonnes, 190 tonnes, 180 tonnes, 127 tonnes and

120 tonnes for Angadiraichur Farmers Services Producer Company Limited

(AFSPC), Kodangal Farmers Services Producer Company Limited (KOFSPC),

Hasnabad Farmers Services Producer Company Limited (HFSPC),

38

Table: 4.1 Volume of redgram sales business done by FPCs for two years

Year

AFSPC KOFSPC HFSPC JFSPC KFSPC

Qn

(tn)

Amnt

(lkhs)

Qn

(tn)

Amnt

(lkhs)

Qn

(tn)

Amnt

(lkhs)

Qn

(tn)

Amnt

(lkhs)

Qn

(tn)

Amnt

(lkhs)

2013

180

77.40

90

38.70

180

77.40

127

54.61

120

51.60

2014

136

73.49

127

69.97

107

56.67

102

53.92

110

58.15

39

Figure 4.1 Volumes of redgram sales done by FPCs in 2013

Figure 4.2 Volumes of redgram sales done by FPCs in 2014

40

Jalwad Farmers Services Producer Company Limited (JFSPC) and Kalkeri

Farmers Services Producer Company Limited (KFSPC) respectively. Volume

of quantities handled in the year 2013 has been illustrated in Figure 4.1.

In the following year i.e., 2014 there was a uniform reduction in the

quantities that was brought for the sale with the reference to all FPCs barring

Kodangal farmers services producer company limited. Volume of quantities

handled in the year 2013 has been illustrated in Figure 4.2. The same trend

could be noticed in value of produce a well. During the survey, it is understood

that only15 percent – 30 percent of the redgram grown by farmer share holders

of the companies only being brought their produce to the FPCs, others

preferred to dispose the produce on their own. The financial commitments of

the farmers to the non institutional financing agencies like money lenders,

relatives might have compelled them to do so. The same continued in the 2014

as well.

Another sound reason was the price line that prevailed in 2014 was

similar to that are in 2013 which was not all that encouraging leading to the

reduction in area. A point to be highlighted here is that all the farmer members

were well convinced about the role that FPCs played in their lives but yet that

those initial hiccups played their role that could be observed from the

percentage of produce brought to the FPCs as detailed in Table 4.1.This

scenario will be changed once the farmers get to used to this new system in the

coming years and strongly believe that they are the best market after natives for

them. However, the FPCs must redefine their products for the market, taking as

the role of market leader rather than just a follower of established marketing

practices.

41

4.1.3 Addressing Changing Market

FPCs have helped to enhance farmers’ competitiveness and gave them a

level playing field in emerging market and prevented exploitation by

middlemen. It was a challenge to overcome the competition by traditional

middlemen and brokers in this business by offering a more competitive price

and fair procurement than the prevailing market conditions.

FPCs through their ability to respond market dynamics and flexibility to

address changing needs helped shareholders to get more prices for their

produce than the other farmers. Its vast external linkage helped in finding

external marketing opportunities.

It could be observed from the Table 4.8 and Table 4.9 in the year 2013-

14 red gram open market prices was only Rs.3979.84/quintal and Rs.3975.17/

quintal in Telangana and Karnataka states respectively. But FPC made

arrangements to sell the produce through small farmers’ agribusiness

consortium (SFAC) at MSP of Rs.4300/quintal. And also it could be observed

from the Table 4. 6 and Table 4.7 in the year 2014-15 redgram was sold by

FPC at a price of Rs.5323.33/ quintal in the state of Telangana and at

Rs.5321.6/ quintal in the state of Karnataka which is more than that of open

market price (Rs.5233.37/quintal and 5287.21/ quintal in Telangana and

Karnataka states respectively – Table 4.6 and Table 4.7) to traders as FPC

ensures quality of produce.

4.2 Mapping channels of FPC

This study provides detailed information regarding flow of redgram

through different channels in the study area.

Channels of Marketing:

The important link in the marketing of redgram is the regulated market.

Most of the crop output is sold either directly by the farmers or with the help of

village traders, produce flows to millers through the regulated market. Village

42

traders were also found to have a lot of variation in their mode of operation. In

some cases, they were approaching the farmers, while in others they were

operating through their own collection centres i.e. local private markets.

As redgram is consumed in the dal (split) form; the millers have an

important presence in the marketing of the pulses. In order to ensure smooth

supply of raw material for the dal mill, some of the millers have vertically

expanded their operations by participating in the marketing of pulses as traders.

Though there are many marketing channels exist in the study only few

were operating efficiently.

(i). Farmers – Commission Agent – Trader – Miller – Wholesaler – Retailer –

Consumer

(ii). Farmers – Farmer Producer Company - Traders - Miller – Wholesaler –

Retailer – Consumer

Since most of the produce was found to be flowing through channel I

and channel II only these two channels have been considered for the detailed

analysis of marketing costs and margins.

4.3 Marketing efficiency of FPC

This chapter provides understanding regarding availability of

information that provides maximum opportunities to buyers and sellers to

effect transactions with minimum transaction costs. In this section, marketing

costs, marketing margins, producer’s share in consumer’s rupee and marketing

efficiency are discussed. Five FPCs identified in the study area are selling the

produce to a single processor. Moreover, the data collected and analysed were

quite similar to all the FPCs in the study area the results presented in the Table

4.2 represents to all FPCs identified for the study.

43

4.3.1 Marketing cost

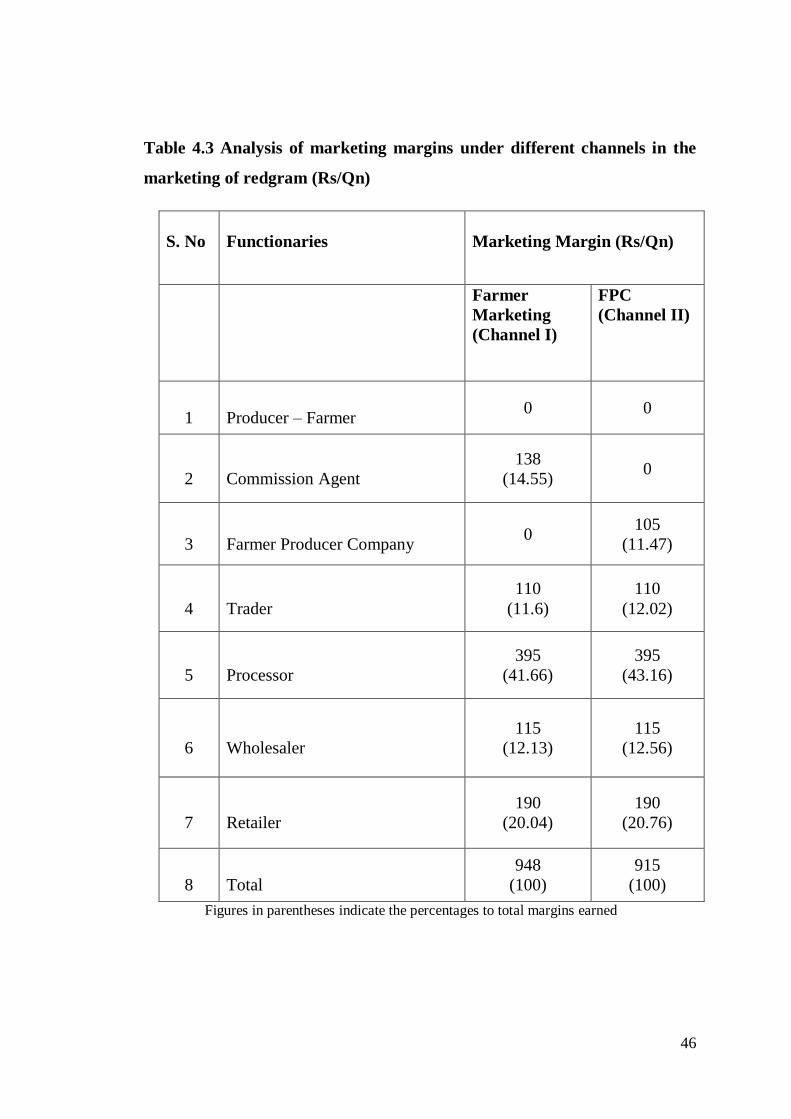

It is observed from Table 4.2 that total marketing cost incurred for

redgram in channel I was Rs. 2732 per quintal and in channel II was Rs. 2463

per quintal. Thus the cost incurred in marketing of redgram in channel I

(Rs.2732) was higher than channel II (Rs.2463). It implies that farmers who

disposed the produce on their own incurred relatively more costs compared to

the FPC shareholder farmers. Within the channel, marketing cost incurred by

the processor was more compared to other market functionaries.

Comparing the total marketing the costs incurred by different

intermediaries in the marketing of redgram are concerned; the highest cost was

incurred by the processor followed by retailer, trader, wholesalers and