Study Objectives - CPA Diary · PDF fileUnderstand the benefits and limitations of...

59

Study Objectives

Transcript of Study Objectives - CPA Diary · PDF fileUnderstand the benefits and limitations of...

Study ObjectivesStudy Objectives

Study ObjectivesStudy ObjectivesCHAPTER 4

Activity-Based Costing

Managerial Accounting, Fourth Edition

Study ObjectivesStudy Objectives

1. Recognize the difference between traditional costing and activity based costing.

2. Identify the steps in the development of an activity-based costing system.

3. Know how companies identify the activity cost pools used in activity-based costing.

Study ObjectivesStudy Objectives

Study ObjectivesStudy Objectives

4. Know how companies identify and use cost drivers in activity-based costing.

5. Understand the benefits and limitations of activity-based costing.

6. Differentiate between value-added and non-value-added activities.

Study ObjectivesStudy Objectives

Study ObjectivesStudy Objectives

7. Understand the value of using activity levels in activity-based costing.

8. Apply activity-based costing to service industries.

Study ObjectivesStudy Objectives

Study ObjectivesStudy ObjectivesPREVIEW OF CHAPTER 4

Traditional Costing and Activity-Based CostingTraditional costing systemsThe need for a new approachActivity-based costing

Illustration of Traditional Costing versus ABCUnit costs under traditional costingUnit costs under ABCComparing unit costs

Study ObjectivesStudy ObjectivesPREVIEW OF CHAPTER 4

Activity-Based Costing: A Closer LookBenefits/Limitations of ABCWhen to use ABCValue-added vs. Non-value-added activitiesClassification of activity levels

Activity-Based Costing in Service IndustriesTraditional costing exampleActivity-based costing example

Appendix: Just-in-time ProcessingObjective – Elements - Benefits

Study ObjectivesStudy ObjectivesACTIVITY-BASED COSTING VERSUS TRADITIONAL COSTING

Traditional Costing Systems

Allocates overhead using a single predetermined rate.

Job order costing: direct labor cost is assumed to be the relevant activity base.

Process costing: machine hours is the relevant activity base.

Assumption was satisfactory when direct labor was a major portion of total manufacturing costs.

Wide acceptance of a high correlation between direct labor and overhead costs.

Study ObjectivesStudy ObjectivesTraditional Costing Systems

Direct labor is still often the appropriate basis for assigning overhead costs when:

Direct labor constitutes a significant part of total product cost and

High correlation exists between direct labor and changes in overhead costs

Overhead Direct Labor ProductsCosts Hours/Dollars

Study ObjectivesStudy ObjectivesNeed for a New Approach

Tremendous change in manufacturing and service industries.

Decrease in amount of direct labor usage.

Significant increase in total overhead costs.

May be inappropriate to use plant-wide predetermined overhead rates based on direct labor or machine hours when a lack of correlation exists.

Complex manufacturing processes may require multiple allocation bases; this approach is called Activity-Based Costing (ABC).

Study ObjectivesStudy ObjectivesActivity-Based Costing (ABC)

An overhead cost allocation system that allocates overhead to multiple activity cost pools

andAssigns the activity cost pools to products or services by means of cost drivers that represent the activities used.

Study ObjectivesStudy ObjectivesActivity-Based Costing (ABC)Terms

Activity: any event, action, transaction, or work sequence that causes a cost to be incurred in producing a product or providing a service.

Activity Cost Pool: a distinct type of activity.For example: ordering materials or setting up machines.

Cost Drivers: any factors or activities that have a direct cause-effect relationship with the resources consumed.

Study ObjectivesStudy ObjectivesThe Logic Behind ABC

Products consume activities,and

activities consume resources.

Study ObjectivesStudy ObjectivesActivity-Based Costing (ABC)

ABC allocates overhead costs in two stages:

Stage 1: Overhead costs are allocated to activity cost pools.

Stage 2: The overhead costs allocated to the cost pools is assigned to products using cost drivers.

The more complex a product’s manufacturing operation, the more activities and cost drivers likely to be present.

Study ObjectivesStudy ObjectivesActivities and Related Cost Drivers

Study ObjectivesStudy ObjectivesABC System Design – Lift Jack Company

Study ObjectivesStudy ObjectivesTraditional Costing vs. ABC

ABC does not replace an existing job order/process cost system.

ABC does segregate overhead into various cost pools to provide more accurate cost information.

ABC, thus, supplements – it does not replace –the traditional cost system.

Study ObjectivesStudy ObjectivesTraditional Costing vs. ABCAn Illustration

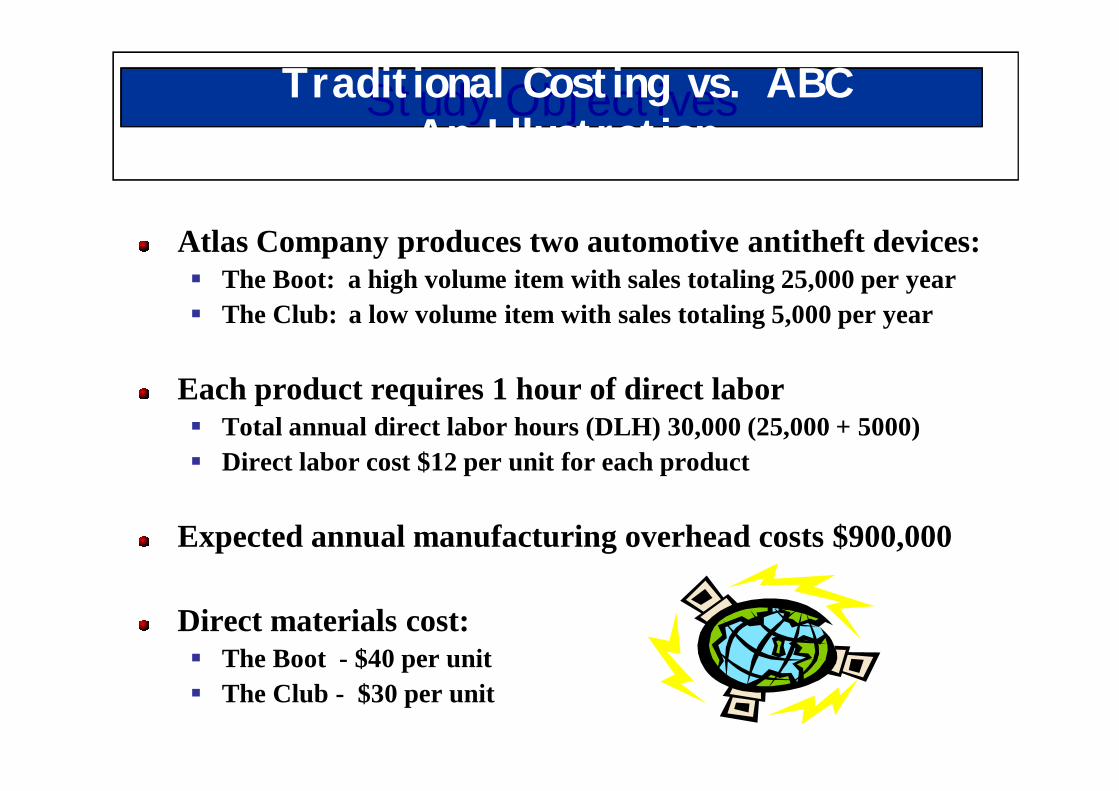

Atlas Company produces two automotive antitheft devices: The Boot: a high volume item with sales totaling 25,000 per year The Club: a low volume item with sales totaling 5,000 per year

Each product requires 1 hour of direct labor Total annual direct labor hours (DLH) 30,000 (25,000 + 5000) Direct labor cost $12 per unit for each product

Expected annual manufacturing overhead costs $900,000

Direct materials cost: The Boot - $40 per unit The Club - $30 per unit

Study ObjectivesStudy ObjectivesUnit Costs Under Traditional Costing

Products

Manufacturing Costs The Boot The ClubDirect Materials $40 $30Direct Labor 12 12Overhead 30* 30*Total unit cost $82 $72

* Predetermined overhead rate: $900,000/30,000 DLH = $30 per DLHOverhead = predetermined overhead rate times direct labor hours

($30 X 1 hr. = $30)

STEPS IN ACTIVITY-BASED COSTING SYSTEM

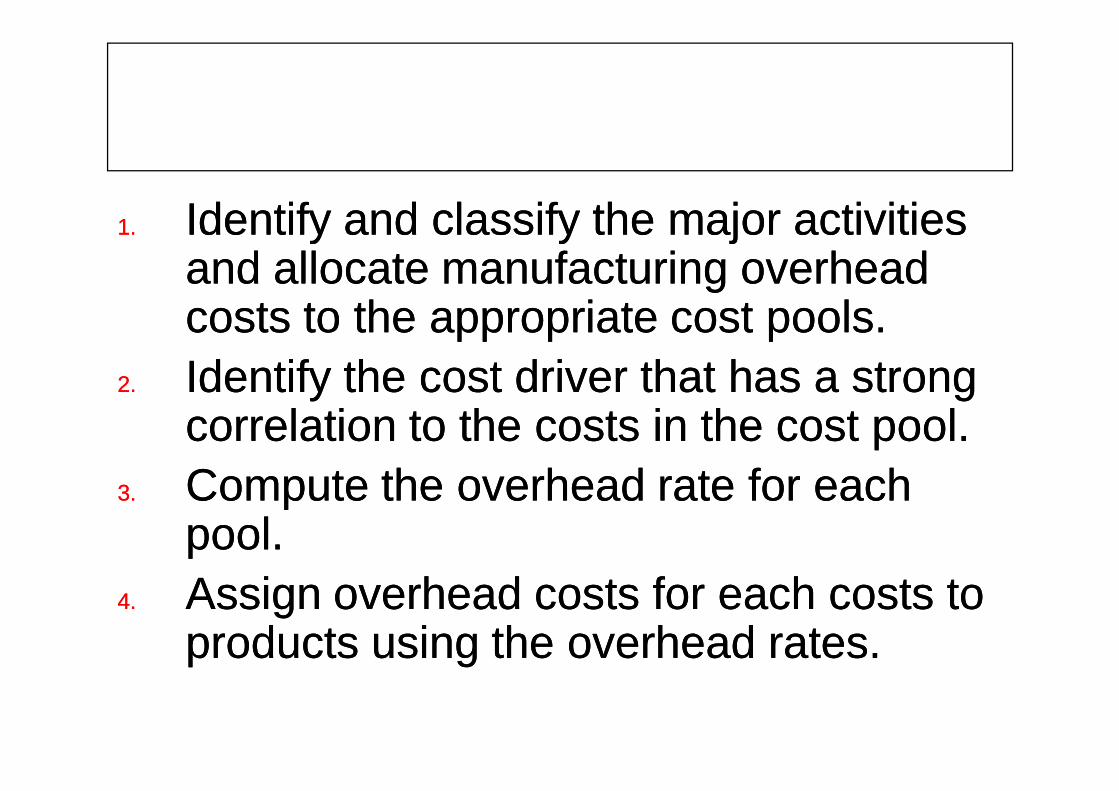

1.1. Identify and classify the major activities Identify and classify the major activities and allocate manufacturing overhead and allocate manufacturing overhead costs to the appropriate cost pools.costs to the appropriate cost pools.

2.2. Identify the cost driver that has a strong Identify the cost driver that has a strong correlation to the costs in the cost pool.correlation to the costs in the cost pool.

3.3. Compute the overhead rate for each Compute the overhead rate for each pool.pool.

4.4. Assign overhead costs for each costs to Assign overhead costs for each costs to products using the overhead rates.products using the overhead rates.

Study ObjectivesStudy ObjectivesUnit Costs Under ABC:Step 1: Identify and Classify Activities and

Allocate Overhead to Cost Pools

Activity Cost Pools Estimated OverheadSetting up machines $300,000Machining 500,000 Inspecting 100,000Total $900,000

Study ObjectivesStudy ObjectivesUnit Costs Under ABC:Step 2: Identify Cost Drivers

Expected Useof Cost Drivers

Activity Cost Pools Cost Drivers Per ActivitySetting up machines Number of setups 1,500 Machining Machine hours 50,000 Inspecting Number of

Inspections 2,000

Study ObjectivesStudy ObjectivesUnit Costs Under ABC:Step 3: Compute Overhead Rates

Formula for Computing Activity-Based Overhead Rate:

Estimated Overhead Per Activity Activity-Based

Expected Use of Cost Drivers Per Activity Overhead Rate

Expected UseEstimated of Cost Drivers Activity-Based

Activity Cost Pools Overhead Per Activity Overhead RatesSetting up machines $300,000 1,500 setups $200 per setupMachining 500,000 50,000 machine hrs. $ 10 per mach. hourInspecting 100,000 2,000 inspections $ 50 per inspectionTotal $900,000

Study ObjectivesStudy ObjectivesUnit Costs Under ABC:Step 4: Assign Overhead Costs to ProductsPart 1: Expected Use of Cost Driver Per Product

Expected Useof Cost Drivers

per ProductExpected Use

Activity Cost of Cost DriversPools Cost Driver Per Activity The Boot The Club

Setting up Number ofmachines setups 1,500 setups 500 1,000

Machining Machine hours 50,000 hours 30,000 20,000Inspecting Number of

inspections 2,000 inspections 500 1,500

Study ObjectivesStudy ObjectivesUnit Costs Under ABC:Step 4: Assign Overhead Costs to Products

Part 2: Assign Cost Pools to Products

The Boot

Expected Use of Activity-BasedActivity Cost Drivers X Overhead = Cost Cost Pools per Product Rates AssignedSetting up machines 500 $200 $100,000Machining 30,000 10 300,000Inspecting 500 50 25,000Total costs assigned $425,000Units produced 25,000Overhead cost per unit $17

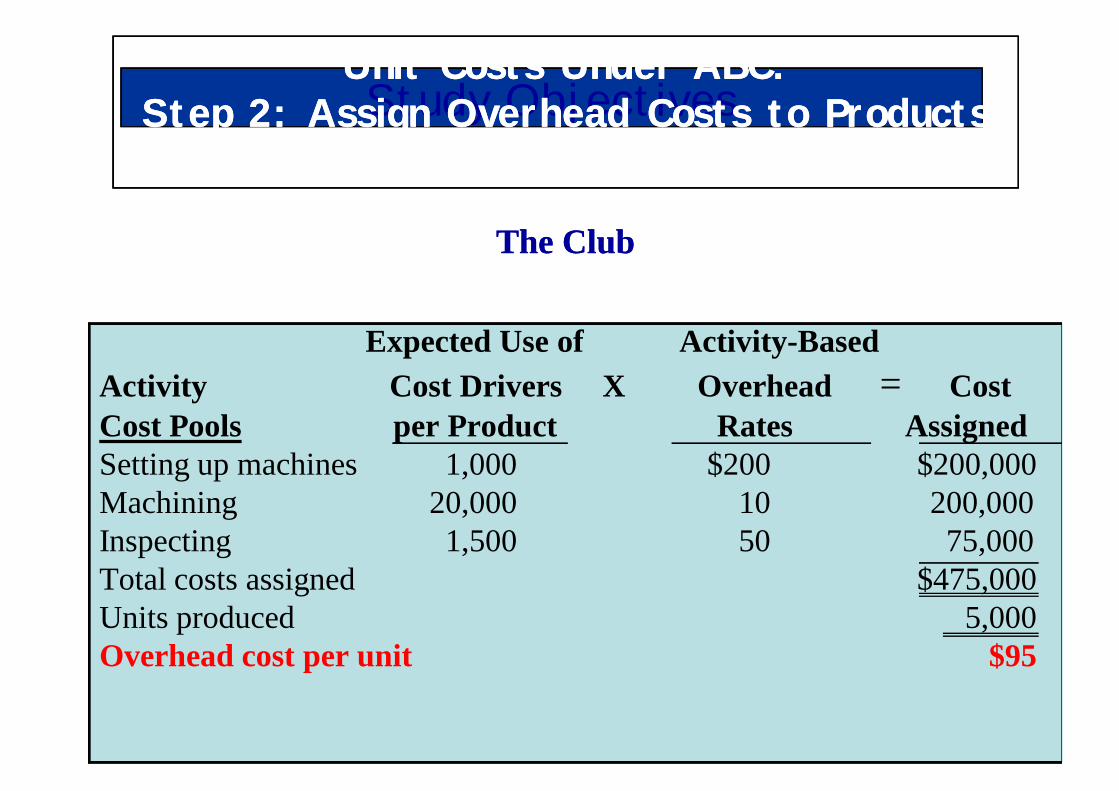

Study ObjectivesStudy ObjectivesUnit Costs Under ABC:

Step 2: Assign Overhead Costs to ProductsPart 2: Assign Cost Pools to Products

The Club

Unit Costs Under ABC:Step 2: Assign Overhead Costs to Products

Part 2: Assign Cost Pools to Products

The Club

Expected Use of Activity-BasedActivity Cost Drivers X Overhead = Cost Cost Pools per Product Rates AssignedSetting up machines 1,000 $200 $200,000Machining 20,000 10 200,000Inspecting 1,500 50 75,000Total costs assigned $475,000Units produced 5,000Overhead cost per unit $95

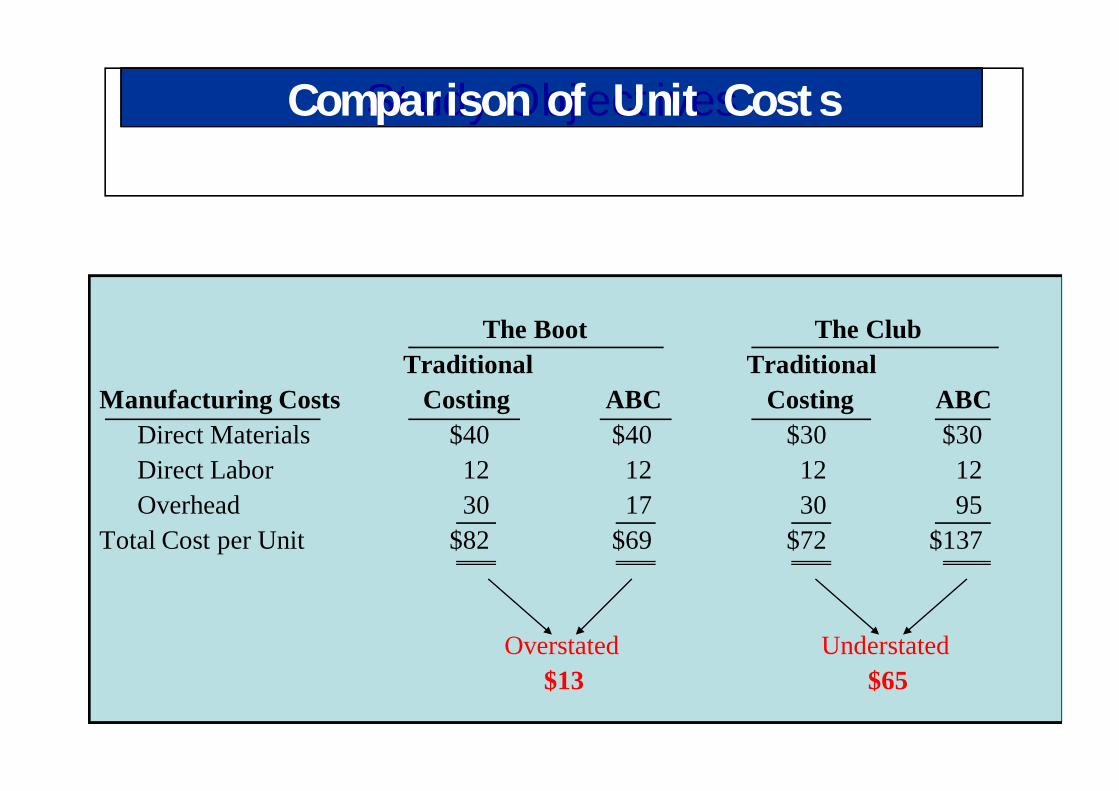

Study ObjectivesStudy ObjectivesComparison of Unit CostsTraditional vs. ABC

The Boot The ClubTraditional Traditional

Manufacturing Costs Costing ABC Costing ABCDirect Materials $40 $40 $30 $30Direct Labor 12 12 12 12Overhead 30 17 30 95

Total Cost per Unit $82 $69 $72 $137

Overstated Understated$13 $65

Study ObjectivesStudy ObjectivesComparison of Unit CostsTraditional vs. ABC

Note that under ABC, overhead costs are shifted from the high volume product (The Boot) to the low volume product (The Club) because:

1. Low volume products often require more special handling.

2. Assigning overhead using ABC will usually increase the cost per unit of low volume products.

Study ObjectivesStudy ObjectivesActivity-Based Costing:A Closer Look

More accurate product costing through:Use of more cost pools to assign overhead costsEnhanced control over overhead costsBetter management decisions

Study ObjectivesStudy ObjectivesActivity-Based Costing: A Closer Look

Limitations of ABC

• Can be expensive to use• Some arbitrary allocations continue

Study ObjectivesStudy ObjectivesActivity-Based Costing:

A Closer Look

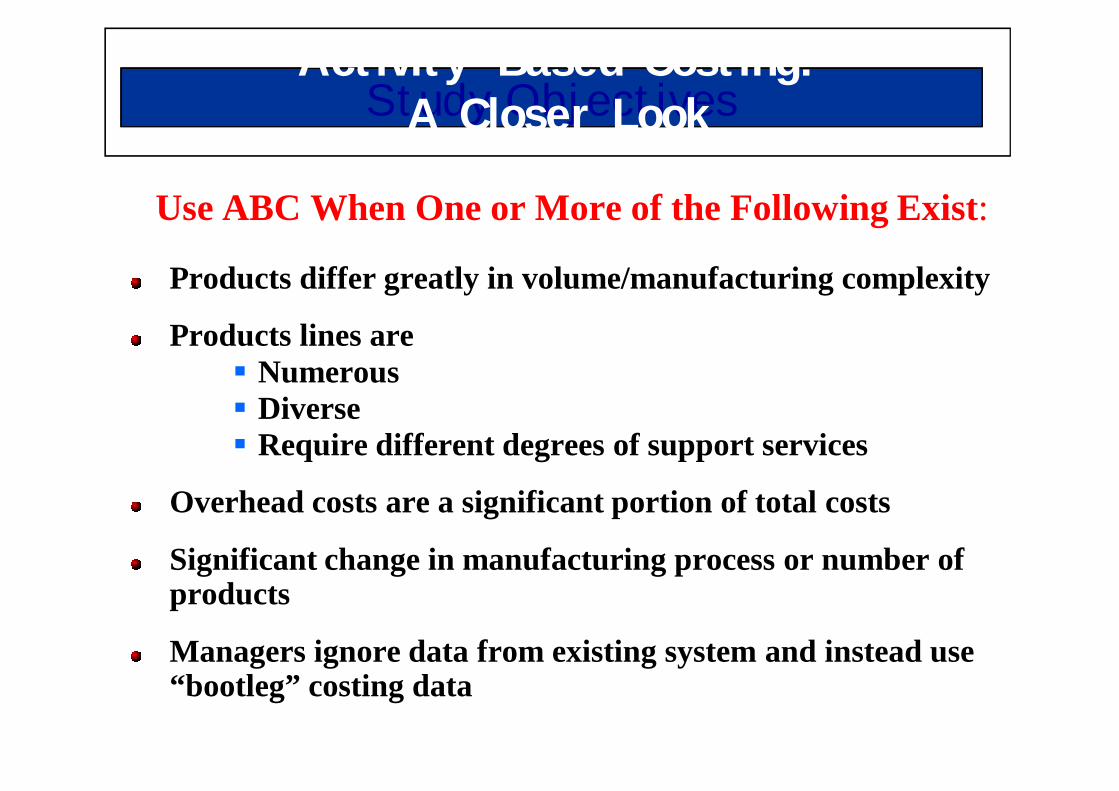

Use ABC When One or More of the Following Exist:

Products differ greatly in volume/manufacturing complexity

Products lines are Numerous Diverse Require different degrees of support services

Overhead costs are a significant portion of total costs

Significant change in manufacturing process or number of products

Managers ignore data from existing system and instead use “bootleg” costing data

Study ObjectivesStudy ObjectivesLet’s ReviewLet’s Review

Activity-based costing (ABC):

a. Can be used only in a process cost systemb. Focuses on units of productionc. Focuses on activities performed to

produce a productd. Uses only a single basis of allocation

Study ObjectivesStudy ObjectivesLet’s ReviewLet’s Review

Activity-based costing (ABC):

a. Can be used only in a process cost systemb. Focuses on units of productionc. Focuses on activities performed to

produce a productd. Uses only a single basis of allocation

Study ObjectivesStudy ObjectivesValue-Added vs.Non-Value-Added Activities

Activity Based Management (ABM):

An extension of ABC from a product costing system to a management function

that focuses on reducing costs and improving processes and decision making

A refinement of ABC used in ABM classifies activities as either value-added or non-value-added.

Study ObjectivesStudy ObjectivesValue-Added vs.Non-Value-Added Activities

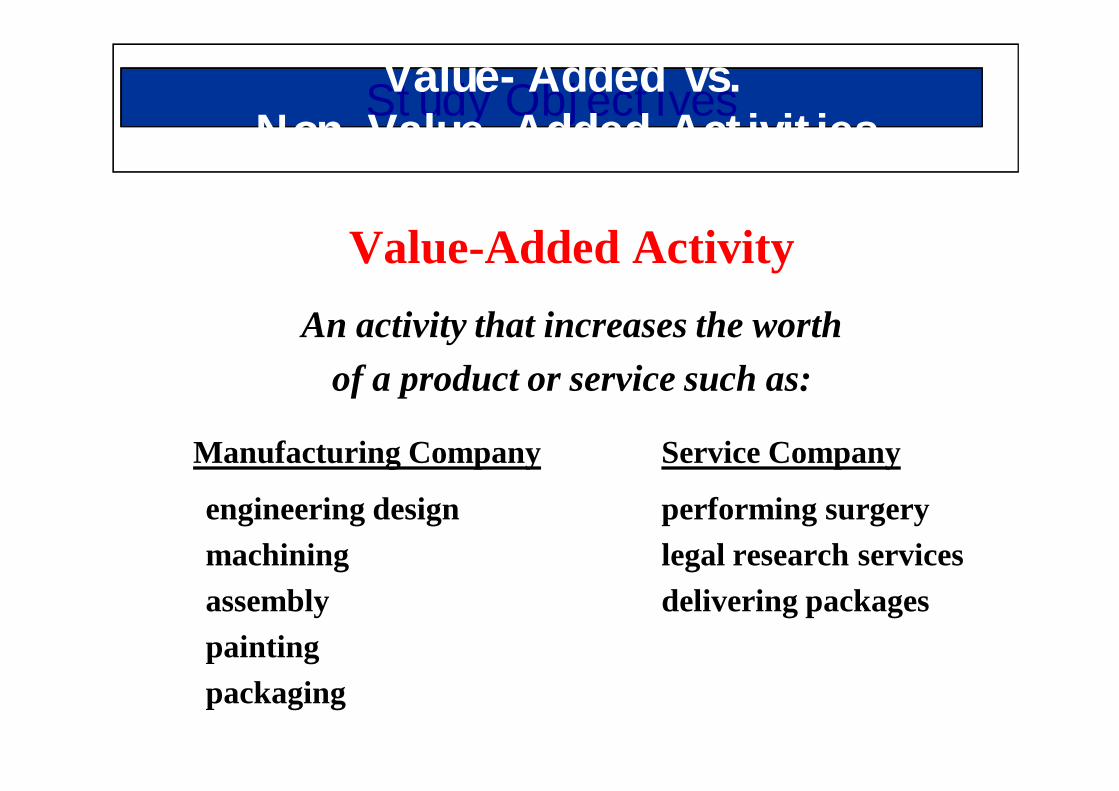

Value-Added ActivityAn activity that increases the worth

of a product or service such as:

Manufacturing Company Service Company

engineering design performing surgerymachining legal research servicesassembly delivering packagespaintingpackaging

Study ObjectivesStudy ObjectivesValue-Added vs.

Non-Value-Added Activities

Non-Value-Added ActivitiesAn activity that adds cost to, or increases the time spent on, a product/service without increasing its

market value such as:Manufacturing Company Service CompanyRepair of machines Taking appointmentsStorage of inventory ReceptionMoving of raw materials, Bookkeeping/billingassemblies, and finished goods TravelingBuilding maintenance Ordering suppliesInspectionsInventory Control

Study ObjectivesStudy ObjectivesCLASSIFICATION OF ACTIVITY LEVELS

Unit-level activities:Performed for each unit of production

Batch-level activities:Performed for each batch of product

Product-level activities:Performed in support of an entire product line, but not always performed every time a new unit or batch is produced

Facility-level activities:Required to support or sustain an entire productionprocess

Study ObjectivesStudy ObjectivesHierarchy of Activity Levels

Four Levels Types of Activities Cost DriversUnit-Level Activities Machine-related: Machine Hours

Drilling, cutting, millingLabor-related Direct labor hours/cost

Assembling, paintingBatch-Level Activities Equipment setups Number of setups/setup time

Purchase ordering Number of purchase ordersInspection Number of inspections or

inspection timeMaterial handling Number of material moves

Product-Level Activities Product design Number of product designsEngineering changes Number of changes

Facility-Level Activities Plant management Number of employees salaries managed

Plant depreciation Square footageProperty taxes Square footageUtilities Square footage

Study ObjectivesStudy ObjectivesActivity-Based Costing in Service Industries

Similarities with Manufacturing Firms

Overall objective:Identify key cost-generation activities and keep track of quantity of activities performed for each service provided

General approach is to identify activities, cost pools, and cost drivers

Labeling of activities as value-added or non-value-added

Reduction of non-value-added activities

Study ObjectivesStudy ObjectivesHEARTLAND MANUFACTURING COMPANY

Activity Flowchart

Activities

NVA NVA NVA NVA VA VA NVA NVA VA NVA NVA NVA VA

Remove Move and Move Materials Move Inspect Move Store Package

and Inspect Store to Production Set-Up Machining Inspect and Assembly and to Finished and

Materials Materials and Wait Machines Drill Lathe Wait Test Storage Goods Ship

Current

Days 1 12 2.5 1.5 2 1 0.2 6 2 0.3 0.5 14 1

<-------------------------------------------------------- Total Current Average Time = 44 days -------------------------------------------------------- ------------>

Proposed

Days 1 4 1.5 1.5 2 1 0.2 2 2 0.3 0.5 10 1

<-------------------------------------------------------- Total Proposed Average Time = 27 days ------------------------------------------------------ ------------->

Study ObjectivesStudy ObjectivesActivity-Based Costing in Service Industries

Major difficulty to implementing ABC:

A larger proportion of overhead costs are company-wide costs

that cannot be directly traced to specific services.

Study ObjectivesStudy ObjectivesActivity-Based Costing in Service Industries: Traditional Costing Example

CHECK AND DOUBLECHECK, CPAsAnnual Budget

Revenue $2,000,000Direct labor $ 600,000Overhead (expected) 1,200,000Total Costs 1,800,000Operating income $ 200,000

Estimated overhead= Predetermined overhead rate

Direct labor cost

$1,200,000= 200%

$600,000

Study ObjectivesStudy ObjectivesActivity-Based Costing in Service Industries: Traditional Costing Example

CHECK AND DOUBLECHECK, CPAs

Plano Molding Company Audit

Revenue $260,000Less: Direct professional labor $ 70,000

Applied Overhead (200% x $70,000) 140,000 210,000Operating Income $ 50,000

Study ObjectivesStudy ObjectivesActivity-Based Costing in Service Industries: ABC Costing Example

CHECK AND DOUBLECHECK, CPAs

Annual Overhead BudgetExpected Use

Activity Cost Estimated ÷ of Cost Drivers = Activity-BasedPools Cost Drivers Overhead Per Activity Overhead Rates

Secretarial support Direct Prof. hours $ 210,000 30,000 $7 per hourDirect labor Fringe benefits Direct labor cost 240,000 $ 600,000 $0.40 per $1 labor Printing and photocopying Working paper pages 20,000 20,000 $1 per pageComputer support CPU minutes 200,000 50,000 $4 per minuteTelephone and postage None (traced directly) 71,000 N/A Based on usage Legal support Hours used 129,000 860 $150 per hour Insurance Revenue billed 120,000 $2,000,000 $0.06 per $1 rev. Recruiting and training Direct Prof. Hours __210,000 30,000 $7 per hour

$1,200,000

Study ObjectivesStudy ObjectivesActivity-Based Costing in Service Industries: ABC Costing Example

CHECK AND DOUBLECHECK, CPAs

Plano Molding Company AuditActivity-Based-

Activity Cost Actual Use Overhead Pools Cost Drivers of Drivers Rates Cost Assigned

Secretarial support Direct Professional hours 3,800 $ 7.00 $ 26,600 Direct labor Fringe benefits Direct labor cost $ 70,000 $ 0.40 28,000 Printing and photocopying Working paper pages 1,800 $ 1.00 1,800Computer support CPU minutes 8,600 $ 4.00 34,400Telephone and postage None (traced directly) 8,700 Legal support Hours used 156 $150.00 23,400 Insurance Revenue billed $260,000 $ 0.06 15,600 Recruiting and training Direct Prof. Hours 3,800 $ 7.00 26,600

$165,100

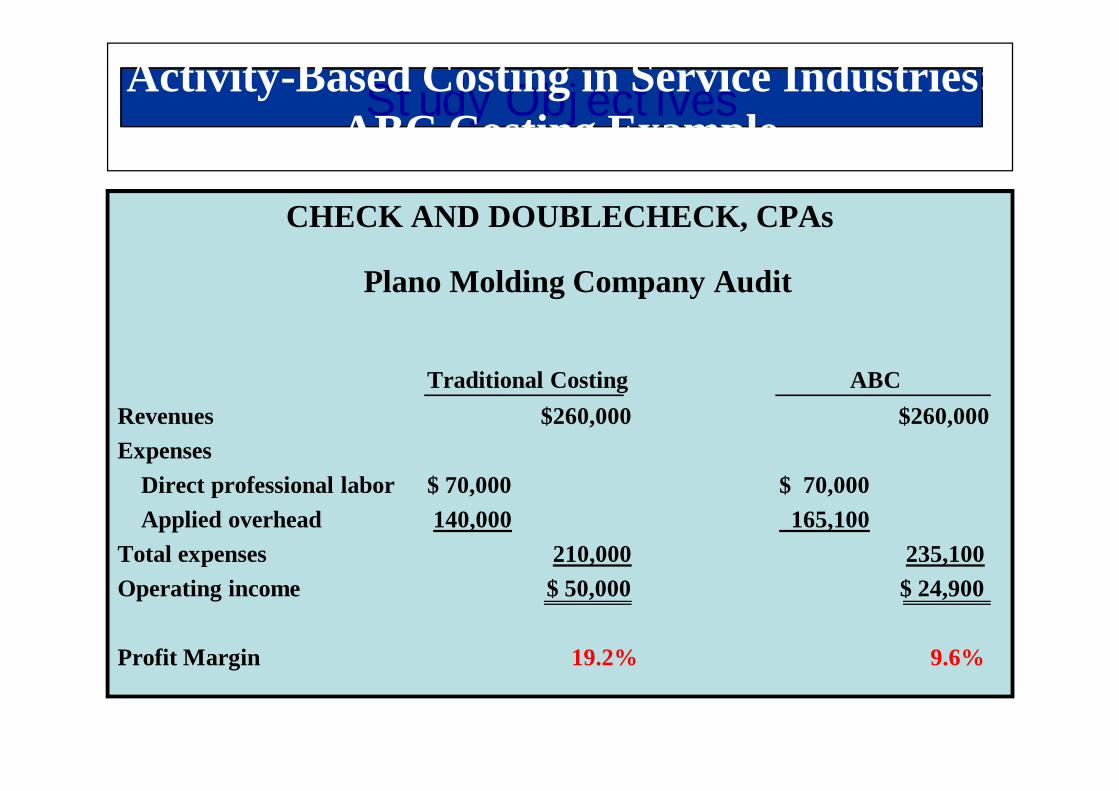

Study ObjectivesStudy ObjectivesActivity-Based Costing in Service Industries: ABC Costing Example

CHECK AND DOUBLECHECK, CPAs

Plano Molding Company Audit

Traditional Costing ABCRevenues $260,000 $260,000Expenses

Direct professional labor $ 70,000 $ 70,000Applied overhead 140,000 165,100

Total expenses 210,000 235,100Operating income $ 50,000 $ 24,900

Profit Margin 19.2% 9.6%

Study ObjectivesStudy ObjectivesSummary of Study Objectives

Recognize the difference between traditional and activity-based costing.

Traditional system allocates overhead to products using predetermined unit-based output rate.

ABC allocates overhead to activity cost pools and assigns costto products using cost drivers.

Identify the steps in the development of an activity-based costing system.

Step 1: Identify the major activities and allocate the overhead costs to cost pools.

Step 2: Identify the cost driver highly correlated to the cost pool.Step 3: Compute the overhead rate per cost driver.Step 4: Assign cost pools to products or services using the overhead

rates.

Study ObjectivesStudy ObjectivesSummary of Study Objectives

Know how companies identify cost pools used in ABC.Analyze each operation or process, document and time every task, action, or transaction.

Know how companies identify and use cost drivers in ABC.Cost drivers identified for assigning activity cost pools must:

Accurately measure the consumption of the activity Have related data easily available.

Understand the benefits and limitations of ABCBenefits:

Enhanced control over overhead costs Better management decisions

Limitations: Higher costs accompany multiple activity centers and cost

drivers Some costs must still be allocated arbitrarily

Study ObjectivesStudy ObjectivesSummary of Study Objectives

Differentiate between value-added and non-value-added activities.

Value-added activities increase the worth of a product or service.Non-value-added activities add cost to, or increase the time spent

on, a product or service without increasing its market value.

Understand the value of using activity levels in ABCActivities may be classified as: Unit-level Batch-level Product-level Facility-level

Failure to recognize this classification can resultin distorted product costing.

Study ObjectivesStudy ObjectivesSummary of Study Objectives

Apply ABC to service industries.Same objective – improved costing of services

provided.

The general approach to costing is also the same: analyze operations identify activities accumulate overhead costs by activity

cost pools identify and use cost drivers to assign

cost to services

Study ObjectivesStudy ObjectivesAppendixJust-In-Time Processing (JIT)

A processing system dedicated to having the right amount of materials, products, or partsarrive as they are needed, thereby reducing

the amount of inventory.

Study ObjectivesStudy Objectives.

Goods Manufactured

Sales Order Received

100 pairs of sneakers...

got it!

Send rubber and shoe laces directly

to the factory.

JUST IN TIME PROCESSING

Study ObjectivesStudy ObjectivesJIT Processing

Objective of JIT:Eliminate all manufacturing inventories

Elements of JIT: Dependable suppliers Multi-skilled work force Total quality control system

Benefits of JIT:Reduced inventory Enhanced product qualityReduced rework and storage costs Savings from improved flow of goods

Study ObjectivesStudy ObjectivesLet’s ReviewLet’s Review

An activity that adds costs to the product but does not increase market value is a

a. Value-added activity

b. Cost driver

c. Cost-benefit activity

d. Nonvalue-added activity

Study ObjectivesStudy ObjectivesLet’s ReviewLet’s Review

An activity that adds costs to the product but does not increase market value is a

a. Value-added activity

b. Cost driver

c. Cost-benefit activity

d. Nonvalue-added activity

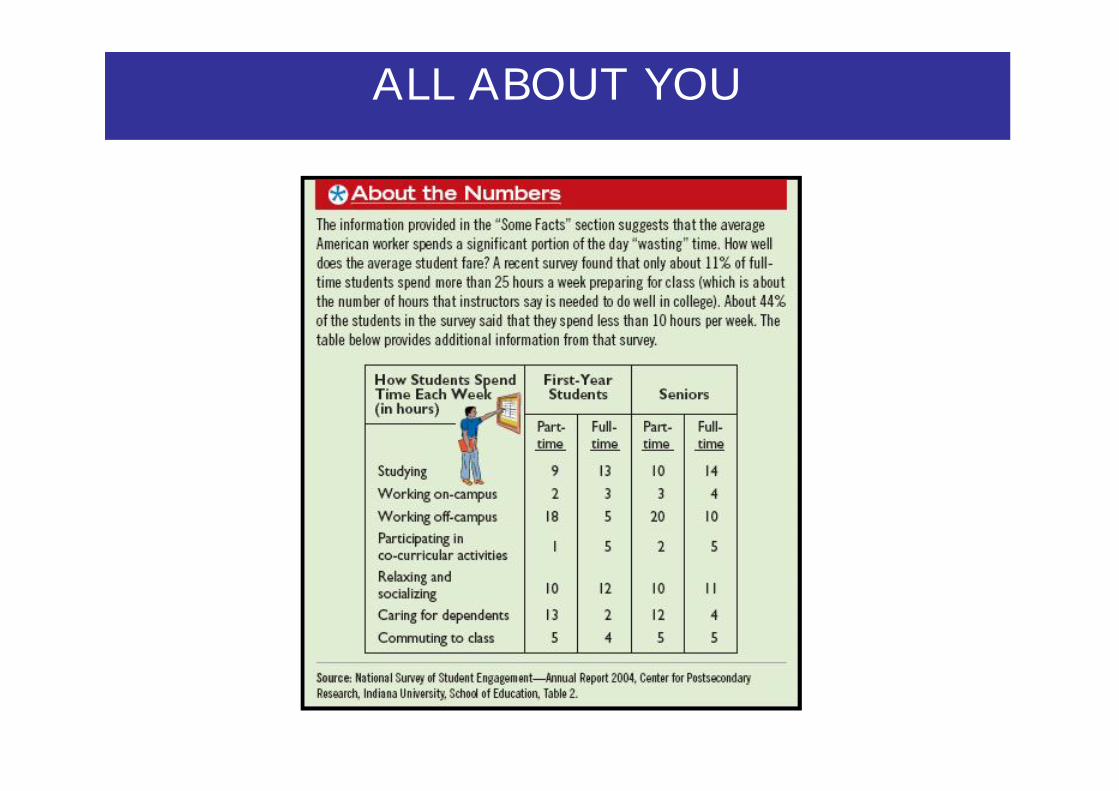

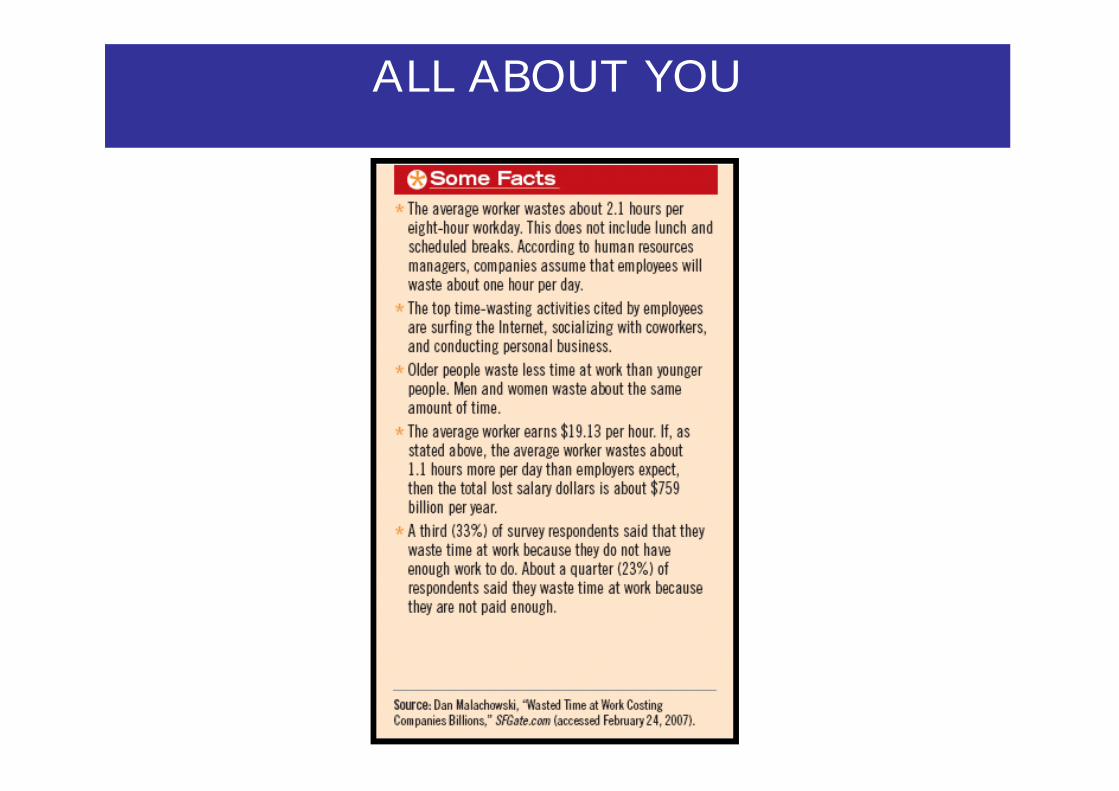

Study ObjectivesStudy ObjectivesALL ABOUT YOU

Study ObjectivesStudy ObjectivesALL ABOUT YOU

Study ObjectivesStudy ObjectivesALL ABOUT YOU

Study ObjectivesStudy ObjectivesCOPYRIGHT

Copyright © 2008 John Wiley & Sons, Inc. All rights reserved. Reproduction or translation of this work beyond that permitted in Section 117 of the 1976 United States Copyright Act without the express written consent of the copyright owner is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons, Inc. The purchaser may make back-up copies for his/her own use only and not for distribution or resale. The Publisher assumes no responsibility for errors, omissions, or damages, caused by the use of these programs or from the use of the information contained herein.