STATE OF NORTH CAROLINA COUNCIL OF …osbm2.osbm.state.nc.us/files/pdf_files/OIA_Meeting...STATE OF...

57

STATE OF NORTH CAROLINA COUNCIL OF I NTERNAL A UDITING Mailing Address: 20320 Mail Service Center Raleigh, NC 27699-0320 www. osbm.state.nc.us 919-807-7000 ** FAX: 919-733-0640 An EEO/AA Employer Office location: 5200 Administration Building 116 West Jones Street David T. McCoy State Controller, Chair Andy Willis State Budget Director Moses Carey Jr. Secretary of Administration Roy Cooper Attorney General David W. Hoyle Secretary of Revenue Beth Wood State Auditor Agenda October 10, 2012 Reading of Ethics Awareness Reminder A. Approval of Minutes – April 11, 2012 (Action item) B. Staff Updates C. Objectives 1. Award of Excellence 2. Training 3. Quality Assurance Review 4. Audit Plan (Action item) 5. Annual Activity Report (Action item) D. Council Reports 1. Obstruction (Action item) 2. External Audit Services

Transcript of STATE OF NORTH CAROLINA COUNCIL OF …osbm2.osbm.state.nc.us/files/pdf_files/OIA_Meeting...STATE OF...

STATE OF NORTH CAROLINA COUNCIL OF INTERNAL AUDITING

Mailing Address: 20320 Mail Service Center

Raleigh, NC 27699-0320

www. osbm.state.nc.us 919-807-7000 ** FAX: 919-733-0640

An EEO/AA Employer

Office location: 5200 Administration Building

116 West Jones Street

David T. McCoy

State Controller, Chair

Andy Willis

State Budget Director

Moses Carey Jr.

Secretary of Administration

Roy Cooper

Attorney General

David W. Hoyle

Secretary of Revenue

Beth Wood

State Auditor

Agenda

October 10, 2012

Reading of Ethics Awareness Reminder

A. Approval of Minutes – April 11, 2012 (Action item)

B. Staff Updates

C. Objectives

1. Award of Excellence

2. Training

3. Quality Assurance Review

4. Audit Plan (Action item)

5. Annual Activity Report (Action item)

D. Council Reports

1. Obstruction (Action item)

2. External Audit Services

COUNCIL OF INTERNAL AUDITING ETHICS AWARENESS

AND CONFLICT OF INTEREST REMINDER It is the duty of every Council member to avoid both conflicts of

interest and the appearances of conflict.

If any Council member has any known conflict of interest or is

aware of facts that might create the appearance of such conflict, with

respect to any matters coming before the Council today, please identify

the conflict or the facts that might create the appearance of a conflict to

ensure that any inappropriate participation in that matter may be

avoided. If at any time, any new matter that raises a conflicts issue

arises during the meeting, please be sure to identify it at that time.

STATE OF NORTH CAROLINA COUNCIL OF INTERNAL AUDITING

Page 1 of 3

David T. McCoy

State Controller, Chair

Andy Willis

State Budget Director

Moses Carey, Jr.

Secretary of Administration

Roy Cooper

Attorney General

David W. Hoyle

Secretary of Revenue

Beth Wood

State Auditor

Minutes

April 11, 2012

Call to Order

The Council of Internal Auditing held its regular meeting, Wednesday,

April 11, 2012 in the Commission Room, Administration building.

Director Willis presiding.

The following Council of Internal Audit members were present:

Andy Willis, State Budget Director

Nels Roseland representing Roy Cooper, Attorney General

Beth Wood, State Auditor

David Hoyle, Secretary of Revenue

Moses Carey, Jr., Secretary of Administration

Director Willis called the meeting to order at 9:08 a.m. and read the Ethics

Awareness and Conflict of Interest Reminder. Members had no conflicts.

Chairman David T. McCoy was absent from the proceedings.

A. Approval of Minutes

On a motion by Secretary Hoyle, seconded by Mr. Roseland, the

Council unanimously approved the minutes of January 11, 2012.

Secretary Carey recommended making spell check corrections to the

minutes.

B. Staff Update

Barbara Baldwin gave a brief update on the new employees within the

office which are:

Peggy Gill-Started 3-1-2012 is a Race to the Top auditor

Jeani Allen is an ITS auditor

Jenny Addison is an ITS auditor

Both Jeani and Jenny worked for OSBM as ARRA auditors

in the past. ITS is supporting these positions through a

memorandum of understanding.

OIA has one (1) vacant position for Race to the Top ARRA. OIA is

conducting interviews this week.

Page 2 of 3

C. Objectives

Training

OIA is offering two training opportunities. Quality Assurance Review Workshop

held on May 14, 2012. This is a 1 day; 8 CPE hours workshop.

Performance Measurement in Government Workshop held on May 17, 2012.

This is a 6 CPE hours workshop.

D. Council Reports

Council Meeting Schedule FY 2012-13

Barbara Baldwin discussed a schedule for the 3rd

quarter council meeting from

January 9, 2013 to January 23, 2013. This change occurred four years ago due to

Government election changes. On a motion made by Secretary Carey and

seconded by Secretary Hoyle, the Council unanimously approved the schedule

change.

External Audit Services

Barbara Baldwin worked with the Division of Purchase and Contract which

suggested establishing a work group to develop a request for information for

external audit service. Director Willis recommended assigning someone from the

State Auditor’s office to the group. Director Willis requested Barbara Baldwin to

continue working with P& C, set-up a work group, and notify the Council

members of the individuals serving on the workgroup.

Compliance Report

Barbara Baldwin presented the draft of the Internal Audit Compliance and

Challenges Report to the council.

Director Willis recommended Barbara Baldwin draft a transmittal letter for

Chairman McCoy to sign. This transmittal letter should be circulated to each

council member for review. State Auditor Wood suggested including an

executive summary in the report. Director Willis requested the report be

completed and submitted to legislature before the short session begins on May 16,

2012.

Interference Amendment

An amendment to the Act for interfering with an internal audit was presented.

Discussion was held to determine the penalty attached to obstructing an audit. A

discussion was made to attach a class II misdemeanor penalty. On a motion by

Secretary Carey and seconded by Director Willis, the Council unanimously

Page 3 of 3

approved the amendment. Mr. Roseland said Department of Justice will support

the package with all the approved amendments, but does not agree with the

confidential work papers amendment. Barbara explained how Chairman McCoy

submits each amendment separately to the legislature not as a package.

There being no further business, at 9:45a.m., a motion to adjourn was made by

Secretary Carey and seconded by Mr. Roseland. The meeting was adjourned.

This is to certify that the foregoing comprises the minutes of the Council of

Internal Auditing at the meeting held April 11, 2012.

Witness my hand, this ______ day of _____________________.

____________________________

David T. McCoy, Chair Secretary

State Budget Director

Council of Internal Auditing Internal Audit Director

Research Assistant Coordinator

Internal Auditor

Internal Auditor

Information System Auditor

Internal Auditor(Race to the Top ARRA)*

Internal Auditor(Race to the Top ARRA)*

Internal Auditor(Early Learning Challenge)**

Internal Auditor (ITS)***

* Time limited positions term August 31, 2012** Time limited positions term December 31, 2012*** Receipts supported position through a MOU with ITS

The Council of Internal Auditing is seeking nominations for the

2013 AWARD of EXCELLENCE

To express its appreciation for excellence in the field of internal auditing, this award is presented annually to honor a State internal auditor or a group of internal auditors who has made extraordinary contributions that promotes excellence in internal auditing Eligible individuals are full-time, part-time, or time-limited current or past (retired or deceased) State employees. Nominations may be made for an individual or a group. If you know of an internal auditor or group of internal auditors that goes above and beyond normal expectations of their job requirements to improve, or promote internal auditing they would qualify for nomination. This may include but is not limited to:

Dedication going beyond the normal requirements of an internal auditor’s job responsibilities. This could include internal auditors that perform duties outside of their job requirements, mentoring or assisting junior internal auditors, or performing at a level above and beyond expectations.

Contribution to promoting the internal audit profession. This could include participation with professional organizations, promoting the profession of internal auditing to individuals including students, or educating others as to the benefits of internal auditing within an organization.

Innovation to improve the processes related internal audit functions. This could include improvements to better administer audits, reduce auditing time, or improve communication of audit results.

Attached is the nomination form you can complete and return to [email protected] by October 1, 2012. If you have any questions, please call Donald Crooke at 919-807-4729 or Barbara Baldwin at 919-807-4721.

Participants

Agencies 16 162

Universities 10 37

City Government 7

County Government 3

Community College 2

Other* 4

Total Number of Participants 26 215

Total Cost 1,290.52$ 2,710.41$

Cost per Participant 49.64$ 12.61$

CPE hours 8 5

Training Information

* Rex Healthcare, Biotech Center, Licensing Board

Quality Assurance

Review

May 14, 2012

Performance Measures

in Government

May 17, 2012

Participants 26

Response Received 21

Response Rate 81%

Questions Excellent Very Good Average Fair Poor No Response

Were the facilities appropriate? 6 13 1 0 1 0

Were audio and technological equipment effective? 8 11 2 0 0 0

Were the stated learning objectives met? 10 8 2 1 0 0

If, applicable, were prerequisite requirements appropriate? 3 7 2 1 0 8

Were program materials accurate? 5 12 3 0 0 1

Were materials relevant and contributed to the achievement of learning objectives? 4 12 4 0 0 1

Was time allotted to the learning activity appropriate? 4 14 3 0 0 0

Was the instructor effective? 5 10 5 1 0 0

Were the handout and/or advance preparation materials satisfactory? 4 12 3 0 0 2

Average Response 5.4 11.0 2.8 0.3 0.1 1.3

Quality Assurance Review ResponsesTraining Held May 14, 2012

26%

52%

13%

2%

1%

6%

Quality Assurance Review Training

Average Survey Response

Excellent

Very Good

Average

Fair

Poor

No Response

Participants 215

Response Received 128

Response Rate 60%

Questions Excellent Very Good Average Fair Poor

No

Response

Were the facilities appropriate? 70 46 12 0 0 0

Were audio and technological equipment effective? 75 48 2 0 0 0

Were the stated learning objectives met? 71 50 6 0 0 1

Were program materials accurate? 66 47 11 0 0 3

Were materials relevant and contributed to the achievement of learning objectives? 69 51 5 0 0 2

Was time allotted to the learning activity appropriate? 67 51 8 1 0 0

Was the instructor effective? 80 43 4 0 0 0

Were the handout and/or advance preparation materials satisfactory? 70 45 5 0 3 2

Average Response 71.0 47.6 6.6 0.1 0.4 1.0

Preformance Measures in Government ResponsesTraining Held May 17, 2012

56%

38%

5%

1%

Performance Measures in Government Training

Average Survey Responses

Excellent

Very Good

Average

No Response

Quality Assurance Program

North Carolina State University

Review underway

There were two individuals on the review team

Completed review and finalized the report

Remaining step: OIA must review all work papers and report

Estimated completion date early October

Fayetteville State University

Requested a review

Selected two individuals for the review team

Remaining: Execute MOU and conduct review

Estimated completion date late fall

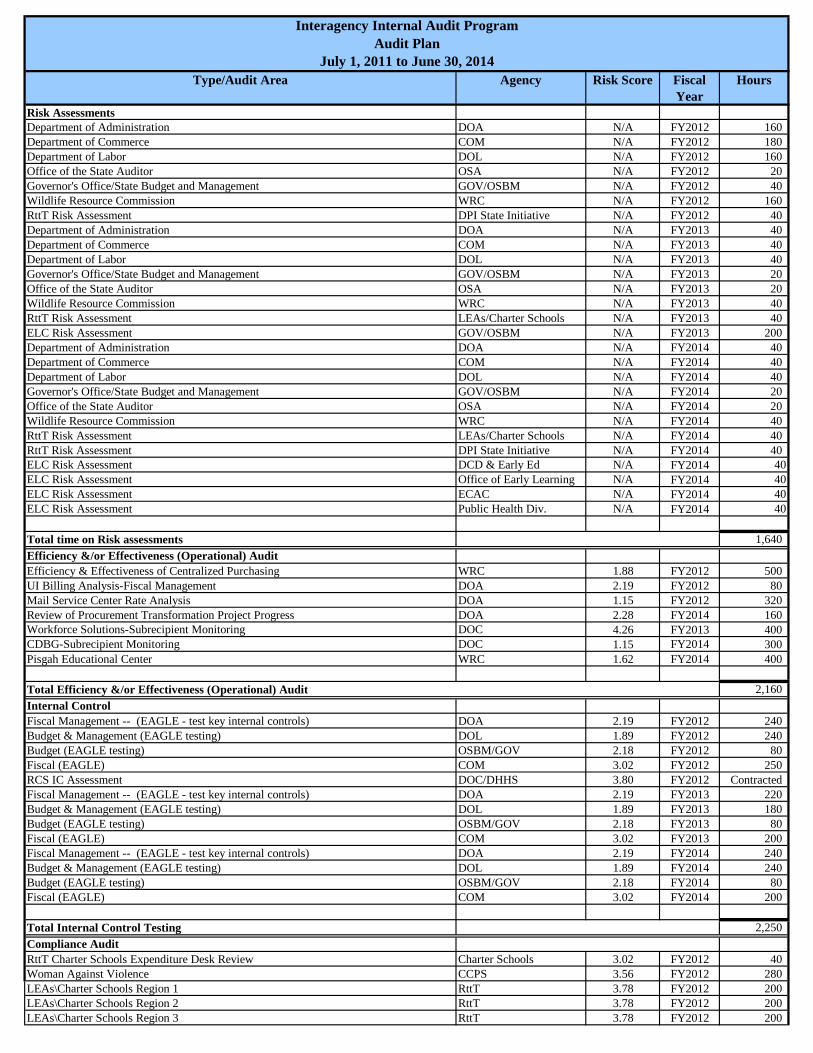

Type/Audit Area Agency Risk Score Fiscal

Year

Hours

Risk Assessments

Department of Administration DOA N/A FY2012 160

Department of Commerce COM N/A FY2012 180

Department of Labor DOL N/A FY2012 160

Office of the State Auditor OSA N/A FY2012 20

Governor's Office/State Budget and Management GOV/OSBM N/A FY2012 40

Wildlife Resource Commission WRC N/A FY2012 160

RttT Risk Assessment DPI State Initiative N/A FY2012 40

Department of Administration DOA N/A FY2013 40

Department of Commerce COM N/A FY2013 40

Department of Labor DOL N/A FY2013 40

Governor's Office/State Budget and Management GOV/OSBM N/A FY2013 20

Office of the State Auditor OSA N/A FY2013 20

Wildlife Resource Commission WRC N/A FY2013 40

RttT Risk Assessment LEAs/Charter Schools N/A FY2013 40

ELC Risk Assessment GOV/OSBM N/A FY2013 200

Department of Administration DOA N/A FY2014 40

Department of Commerce COM N/A FY2014 40

Department of Labor DOL N/A FY2014 40

Governor's Office/State Budget and Management GOV/OSBM N/A FY2014 20

Office of the State Auditor OSA N/A FY2014 20

Wildlife Resource Commission WRC N/A FY2014 40

RttT Risk Assessment LEAs/Charter Schools N/A FY2014 40

RttT Risk Assessment DPI State Initiative N/A FY2014 40

ELC Risk Assessment DCD & Early Ed N/A FY2014 40

ELC Risk Assessment Office of Early Learning N/A FY2014 40

ELC Risk Assessment ECAC N/A FY2014 40

ELC Risk Assessment Public Health Div. N/A FY2014 40

Total time on Risk assessments 1,640

Efficiency &/or Effectiveness (Operational) Audit

Efficiency & Effectiveness of Centralized Purchasing WRC 1.88 FY2012 500

UI Billing Analysis-Fiscal Management DOA 2.19 FY2012 80

Mail Service Center Rate Analysis DOA 1.15 FY2012 320

Review of Procurement Transformation Project Progress DOA 2.28 FY2014 160

Workforce Solutions-Subrecipient Monitoring DOC 4.26 FY2013 400

CDBG-Subrecipient Monitoring DOC 1.15 FY2014 300

Pisgah Educational Center WRC 1.62 FY2014 400

Total Efficiency &/or Effectiveness (Operational) Audit 2,160

Internal Control

Fiscal Management -- (EAGLE - test key internal controls) DOA 2.19 FY2012 240

Budget & Management (EAGLE testing) DOL 1.89 FY2012 240

Budget (EAGLE testing) OSBM/GOV 2.18 FY2012 80

Fiscal (EAGLE) COM 3.02 FY2012 250

RCS IC Assessment DOC/DHHS 3.80 FY2012 Contracted

Fiscal Management -- (EAGLE - test key internal controls) DOA 2.19 FY2013 220

Budget & Management (EAGLE testing) DOL 1.89 FY2013 180

Budget (EAGLE testing) OSBM/GOV 2.18 FY2013 80

Fiscal (EAGLE) COM 3.02 FY2013 200

Fiscal Management -- (EAGLE - test key internal controls) DOA 2.19 FY2014 240

Budget & Management (EAGLE testing) DOL 1.89 FY2014 240

Budget (EAGLE testing) OSBM/GOV 2.18 FY2014 80

Fiscal (EAGLE) COM 3.02 FY2014 200

Total Internal Control Testing 2,250

Compliance Audit

RttT Charter Schools Expenditure Desk Review Charter Schools 3.02 FY2012 40

Woman Against Violence CCPS 3.56 FY2012 280

LEAs\Charter Schools Region 1 RttT 3.78 FY2012 200

LEAs\Charter Schools Region 2 RttT 3.78 FY2012 200

LEAs\Charter Schools Region 3 RttT 3.78 FY2012 200

Interagency Internal Audit Program

Audit Plan

July 1, 2011 to June 30, 2014

Type/Audit Area Agency Risk Score Fiscal

Year

Hours

LEAs\Charter Schools Region 4 RttT 3.78 FY2012 200

LEAs\Charter Schools Region 5 RttT 3.78 FY2012 200

LEAs\Charter Schools Region 6 RttT 3.78 FY2012 200

LEAs\Charter Schools Region 7 RttT 3.78 FY2012 200

LEAs\Charter Schools Region 8 RttT 3.78 FY2012 200

ARRA Complaince/Monitoring Professional Development RttT DPI State Initiative 3.78 FY2012 360

Teacher and Principal Evaluation Tool RttT DPI State Initiative 3.78 FY2012 140

Instruction Improvement System RttT DPI State Initiative 3.78 FY2012 140

Indian Affairs Commission-Section 8 Housing Choice Vouchers DOA 2.19 FY2013 320

State Aid Contracts From DENR DOC 2.29 FY2013 300

LEAs\Charter Schools Region 1 RttT 3.78 FY2013 200

LEAs\Charter Schools Region 2 RttT 3.78 FY2013 200

LEAs\Charter Schools Region 3 RttT 3.78 FY2013 200

LEAs\Charter Schools Region 4 RttT 3.78 FY2013 200

LEAs\Charter Schools Region 5 RttT 3.78 FY2013 280

LEAs\Charter Schools Region 6 RttT 3.78 FY2013 200

LEAs\Charter Schools Region 7 RttT 3.78 FY2013 200

LEAs\Charter Schools Region 8 RttT 3.78 FY2013 200

STEM RttT DPI State Initiative 3.78 FY2013 Contracted

Technology Infrastructure RttT DPI State Initiative 3.78 FY2013 Contracted

Effective Teachers via Virtual/Blended Courses RttT DPI State Initiative 3.78 FY2013 Contracted

RttT Induction Support Program for New Teachers in High Need Schools RttT DPI State Initiative 3.78 FY2013 350

RttT RttT Management RttT DPI State Initiative 2.52 FY2013 350

ELC Compliance/Monitoring DCD and Early Ed 4.92 FY2013 310

ELC Compliance/Monitoring Office of Early Learning 4.00 FY2013 250

ELC Compliance/Monitoring ECAC 3.87 FY2013 240

ELC Compliance/Monitoring Divison of Public Health 3.35 FY2013 200

LEAs\Charter Schools Region 1 RttT 3.78 FY2014 200

LEAs\Charter Schools Region 2 RttT 3.78 FY2014 200

LEAs\Charter Schools Region 3 RttT 3.78 FY2014 200

LEAs\Charter Schools Region 4 RttT 3.78 FY2014 200

LEAs\Charter Schools Region 5 RttT 3.78 FY2014 200

LEAs\Charter Schools Region 6 RttT 3.78 FY2014 200

LEAs\Charter Schools Region 7 RttT 3.78 FY2014 200

LEAs\Charter Schools Region 8 RttT 3.78 FY2014 200

RttT Teach for America Expansion RttT DPI State Initiative 2.52 FY2014 Contracted

RttT Evaluation of RttT Initiatives RttT DPI State Initiative 2.52 FY2014 Contracted

RttT Regional Leadership Academics RttT DPI State Initiative 2.52 FY2014 Contracted

RttT North Carolina Teacher Corps RttT DPI State Initiative 2.52 FY2014 350

RttT Turning Around the Lowest Achieving Schools RttT DPI State Initiative 2.52 FY2014 350

RttT Performance Incentives: Low Achieving Schools,Teacher,Principal Effectiveness RttT DPI State Initiative 2.52 FY2014 350

RttT Strategic Staffing Incentives RttT DPI State Initiative 2.52 FY2014 350

ELC Compliance/Monitoring DCD and Early Ed 4.92 FY2014 310

ELC Compliance/Monitoring Office of Early Learning 4.00 FY2014 250

ELC Compliance/Monitoring ECAC 3.87 FY2014 240

ELC Compliance/Monitoring Divison of Public Health 3.35 FY2014 200

Total Compliance Audit 10,560

Information System Audit

General Control DOA 1.41 FY2012 180

General Control DOC 1.97 FY2012 180

General Control DOL 1.44 FY2012 180

General Control WRC 1.53 FY2012 180

General Control OSBM 1.95 FY2013 200

General Control OSA 1.65 FY2014 200

Total Information System 1,120

Audit Follow-Up

Teacher and Principal Evaluation Tool RttT DPI State Initiative N/A FY2013 50

LEAs\Charter Schools Region 1 RttT N/A FY2013 50

LEAs\Charter Schools Region 2 RttT N/A FY2013 50

LEAs\Charter Schools Region 3 RttT N/A FY2013 50

LEAs\Charter Schools Region 4 RttT N/A FY2013 50

LEAs\Charter Schools Region 5 RttT N/A FY2013 50

LEAs\Charter Schools Region 6 RttT N/A FY2013 50

LEAs\Charter Schools Region 7 RttT N/A FY2013 50

LEAs\Charter Schools Region 8 RttT N/A FY2013 50

Teacher and Principal Evaluation Tool RttT DPI State Initiative N/A FY2013 50

Type/Audit Area Agency Risk Score Fiscal

Year

Hours

Instruction Improvement System RttT DPI State Initiative N/A FY2013 50

ELC Follow-up GOV N/A FY2013 160

Audit follow-up for IIAP agencies FY11 &FY12 projects N/A FY2013 140

IS follow-up DOL and WRC DOL & WRC N/A FY2013 80

ITS Follow-up ITS N/A FY2013 120

Follow-up for work conducted in FY2013 N/A FY2014 50

ELC -- DCD and Early Ed DCD and Early Ed N/A FY2014 50

ELC -- Office of Early Learning Office of Early Learning N/A FY2014 50

ELC -- Early Childhood Advisory Council ECAC N/A FY2014 50

ELC -- Divison of Public Health Divison of Public Health N/A FY2014 50

RttT ARRA N/A FY2014 80

Total Audit Follow-Up 1,380

Contingency for Consulting Services/Special Requests/Invesigations

Early Childhood System Building GOV N/A FY2012 120

Gaston Community Action Group Weatherization DOC N/A FY2012 80

Community Development Block Grant Investigation-Hobbs DOC N/A FY2012 40

US Dept of Labor/ESC audit follow-up DOC N/A FY2012 80

ESC/DOC Merger (rapid response) OSBM N/A FY2012 25

Statewide Compliance with IIA Standard 1321 Statewide N/A FY2012 35

WSSU/UNC-GA Employee OERI N/A FY2012 50

Contract Discrimination DOC N/A FY2012 80

Public Safety DPS N/A FY2012 8

Occupational Boards OSBM N/A FY2012 10

Use of State Resources investigations DOA N/A FY2012 150

P&C Contract Monitoring Guide DOA N/A FY2012 20

OSA Performance Audit of ITS ITS N/A FY2012 100

Hosting/No Match ITS N/A FY2012 300

Network Services ITS N/A FY2012 300

ITS Fiscal Unit Staff Analsyis ITS N/A FY2012 25

Hoke County Domestic Violence OSBM N/A FY2012 80

ITS Complaint review ITS N/A FY2012 80

E-Procurement ITS N/A FY2012 250

Billing procress ITS N/A FY2012 250

Employee Time Allocation by Cost Center ITS N/A FY2013 280

DES Staffing Analysis/OSBM Mgmt Study OSBM N/A FY2013 400

QAR NCSU NCSU N/A FY2013 120

QAIP self assessment OSBM N/A FY2013 80

QAR OSBM-OIA Internal audit function OSBM N/A FY2013 600

CIA RFP Audit Service CIA N/A FY2013 200

Consulting DPI Internal Audit with EAGLE DPI N/A FY2013 10

Weatherization Assistance Program DOC N/A FY2013 100

ELC Monitoring Plans ELC N/A FY2013 80

ELC Expenditure Tracking Tool ELC N/A FY2013 80

Contingency for Consulting/Special Requests/Investigations N/A FY2013 600

RttT ARRA Consulting Services/Special Requests/Investigations DPI, OSBM, GOV N/A FY2013 210

ITS consulting services/special request/investigations ITS N/A FY2013 900

ELC consulting services/special request/investigations GOV, DHHS, DPI N/A FY2013 500

QAIP self assessment OSBM N/A FY2014 120

ITS consulting services/special request/investigations ITS N/A FY2014 1,300

Contingency for Consulting/Special Requests/Investigations N/A FY2014 800

ELC consulting services/special request/investigations GOV, DHHS, DPI N/A FY2014 300

RttT ARRA consulting services/special request/investigations DPI, OSBM, GOV N/A FY2014 210

Total Consulting Services/Special Requests/Invesigations 8,973

Total FY2012 7,833

Total FY2013 10,930

Total FY2014 9,320

Grand Total Hours 28,083

STATE OF NORTH CAROLINA

COUNCIL OF INTERNAL AUDITING

INTERNAL AUDIT

ACTIVITY REPORT

As Required by G.S. 143-747(c)(12)

October 2012

Prepared By:

Office of Internal Audit

Office of State Budget and Management

DRAFT

[THIS PAGE INTENTIONALLY LEFT BLANK]

DRAFT

Table of Contents

Introduction ..........................................................................................................................1

Council of Internal Auditing ................................................................................................1

Membership, Programs and Staff ...............................................................................1

Efforts and Accomplishments .....................................................................................3

Proposed Legislative Changes ....................................................................................4

State Agency Internal Audit Functions ................................................................................5

Audit Resources ..........................................................................................................5

Efforts and Accomplishments ...................................................................................10

Compliance ...............................................................................................................12

Appendices

Appendix A – North Carolina Internal Audit Act ....................................................15

Appendix B – Fiscal Year 2011 Staffing Recommendation .....................................19

Appendix C – Legislative Amendments ...................................................................23

DRAFT

[THIS PAGE INTENTIONALLY LEFT BLANK]

DRAFT

1

INTRODUCTION

The North Carolina Internal Audit Act1 (the Act) was signed into law on August 31, 2007. The

Act established the Council of Internal Auditing (Council) and required State agencies and

universities (agencies) to establish a program of internal auditing. The Council of Internal

Auditing is mandated to report on service efforts and accomplishments of these programs and

propose legislation for consideration by the Governor and General Assembly. This report

documents the service efforts and accomplishments from July 2011 through June 2012, of State

agencies and the Council of Internal Auditing in fulfilling the mandates of the legislation.

COUNCIL OF INTERNAL AUDITING

Membership, Programs and Staff

The Council membership is set by statue as shown in Table 1. The Council meets quarterly to

provide guidance, set policies, and assess progress of internal auditing efforts within State

government.

The Council is mandated to administer programs and activities which:

Promulgate guidelines, develop technical manuals and suggest best practices;

Conduct statewide internal audit staffing analysis;

Provide training and professional development opportunities;

Report on statewide internal audit service efforts and accomplishments;

Develop and administer a peer review program;

Develop and administer an internal audit recognition program;

Develop and administer a shared internal audit program; and

Maintain a report and audit plan repository.

The Office of State Budget and Management (OSBM) support the Council and established the

Office of Internal Audit (OIA) to house the staff to the Council. The organizational structure of

the OIA is shown in Exhibit 1 on page 2. There are five permanent positions and five time-

limited positions. The time-limited positions focus their efforts on the programs/agency that

funds the position. The professional credentials held by the internal audit staff include:

Three Certified Public Accountants;

Three Certified Internal Auditors;

Two Certified Internal Control Auditors;

Two Certified Fraud Examiners;

One Certified Government Auditing Professionals; and

One Certified Government Financial Manager.

1 Entire Internal Audit Act is located in Appendix A.

Table 1 Council of Internal Auditing

Members

David T. McCoy, Chair State Controller

Andy Willis State Budget Director

Moses Carey Jr. Secretary of Administration

Roy Cooper Attorney General

David Hoyle Secretary of Revenue

Beth Wood State Auditor (nonvoting)

DRAFT

2

The Office of Internal Audit had a 15% reduction in expenditures during FY2011-12 compared

to the prior year. The decrease is related to the loss of State Fiscal Stabilization Funds which

terminated September 30, 2011. The federal funds were used to hire six internal auditors whose

primary purpose was to audit and provide technical assistance to agencies receiving ARRA

funds. In addition, two different federal grants fund three auditor positions which are: two Race

to the Top (RttT) and one Early Learning Challenge (ELC) auditors. These positions are strictly

for auditing RttT and ELC funds. Finally, two auditor positions are funded through a

memorandum of understanding (MOU) to provide audit services to Information Technology

Services (ITS). The combined general and federal funds expenditures for FY2007-08 through

FY2011-12 are shown in Table 2 on the next page.

Exhibit 1

Office of Internal Audit

Organizational Structure

June 30, 2012

State Budget Director

Council of Internal Auditing Internal Audit Director

Research Assistant

Coordinator

Internal Auditor

Internal Auditor

Information System Auditor

Internal Auditor

(Race to the Top ARRA)*

Internal Auditor

(Race to the Top ARRA)*

Internal Auditor

(Early Learning

Challenge)**

Internal Auditor

(ITS)***

Internal Auditor

(ITS)***

* Time-limited positions term August 31, 2014

** Time-limited position term December 31, 2015

*** Receipt supported through MOU with ITS

DRAFT

3

As the economic downturn prolonged, the Office diligently continued to reduce spending. The

Office of Internal Audit general fund reduction was 31% between FY2008/09 and FY2011/12.

The effect of the reduction was elimination of the program administrator position, delays in

filling vacant positions, reduction in training, postponement of audits requiring travel and delays

in purchasing professional materials and software.

Efforts and Accomplishments

Over the last five years the Council complied with all the mandated requirements in the Act.

Guidelines and manuals were published in May 2008 and communicated to all internal auditors.

The peer review, internal audit recognition, and shared internal audit programs are developed and

operating. The staffing analysis is conducted every three years (See Appendix B for details) and

annual activity report is published every year. Below is specific accomplishment during

FY2011-12.

Training and Professional Development Opportunities

To maintain proficiency, audit standards require internal auditor participate in professional

development. During May 2012, two training sessions were conducted. The, one day, Quality

Assurance Review training session educated 26 internal auditors on how to conduct a quality

assurance review. These internal auditors agreed to participate in the peer review program. The

Performance Measures in Government training session was opened to employees in State

government, licensing boards, and local government. There were 215 attending this one day

training session.

In addition to the two training sessions, throughout the year, other free or low cost training is

identified and communicated to all internal auditors. Communication takes place via email and

Table 2

FY2011/12 FY2010/11 FY2009/10 FY 2008/09 FY 2007/08

Expenditures

Personal Services 718,992 867,475$ 562,759$ 466,451$ 161,526$

Purchased Services

Central Database Dev. & Maintenance - - 96,215 -

Training & Development 14,460 7,662 3,760 11,205 24,500

Information Technology Services 13,272 10,720 1,415 40,545 6,000

Travel, Telephone, Miscellaneous 12,743 8,327 923 996 543

Total Purchased Services 40,475 26,709 6,098 148,961 31,043

Supplies 100 710 1,232 129 2,425

Property, Plant, & Equipment 550 580 872 516 10,042

Other - - 60 110 358

Total Expenditures 760,117 895,474 571,021 616,167 205,394

Carry Forward - - - - 200,985

Grand Total Expenditures 760,117 895,474 571,021 616,167 406,379

BREAKDOWN BY FUND SOURCE

General Fund 425,146 429,948 469,126 616,176 406,379

ARRA State Fiscal Stabilization Fund 116,832 443,483 101,895

ARRA Race to the Top Fund 150,079 22,042

Early Learning Challenge 8,479

Information Technology Services 59,583

Office of Internal Audit

Expenditures

DRAFT

4

posting on OSBM website. Over the past year, approximately 50 professional development

opportunities were identified and communicated.

Peer Review Program

The Peer Review program is a cooperative effort to establish a method to comply with the

Institute of Internal Auditor’s external quality assurance requirement. All internal audit functions

are required to have an external quality assurance review every five years. This program enables

agencies and universities to obtain their external assessment in a cost-effective method. North

Carolina State University requested a peer review during FY2012. The process started in late

June 2012 and is estimated to be completed by October 2012.

Internal Audit Recognition Program

The recognition program consists of two activities. First, in the quarterly newsletter an internal

auditor or audit group is profiled. Second, the Award of Excellence is bestowed upon an internal

auditor or group of internal auditors that goes above and beyond normal expectations of their job

requirements to improve or promote internal auditing. The first award was presented to James

Bruce Dillard Department of Transportation, Inspector General, Retired.

Shared Internal Audit Program

The internal audit program provides audit services to small State agencies. The guideline for

State agencies to use the internal audit program for compliance with the Act is:

1. Has an annual operating budget exceeds ten million dollars but is less than seventy

million dollars; or

2. Has less than 100 full-time equivalent employees; or

3. Receives and processes more than ten million dollars but less than seventy million

dollars in cash in a fiscal year; or

4. Is deemed appropriate by the Council of Internal Auditing.

In addition, the program will provide audit assistance to small2 internal audit functions upon

request. Services are dependent upon resource availability of the program.

For accomplishment of this program see the State Agency Internal section titled Efforts and

Accomplishments on page 10.

Report and Audit Plan Repository

Audit reports are submitted to the office throughout the year. Also, by September 30th of each

year, agencies must submit their audit plans. For more details on compliance with requirements

and the number and types of reports see the State Agency Internal section titled Efforts and

Accomplishments on page 10.

Proposed Legislation Changes

The Council has approved four separate amendments to the Internal Audit Act. The most recent

amendment relates to the obstruction of an audit. The other three amendments have been

provided to the Governor and General Assembly in prior years. Amendments include:

2 Small internal audit functions is define as one or two auditor positions.

DRAFT

5

1. Technical Correction. Major changes included: adding a University System

representative to the Council; expanding the reporting requirement of the internal audit

director; and allowing the Office of State Personnel to develop auditor qualification.

2. Confidential Work Papers. Provides consistency within the General Statute regarding

audit work papers. The Offices of the State Auditor and Controller, and the Department

of Health and Human Service Internal Audit function has full confidential work paper

law. The University system law provides work paper confidentially on a time-limited

basis. All other internal audit functions have no confidential laws.

3. Subject to the Act. Provides consistency by requiring all Executive Branch and Council

of State agencies to comply with the requirements in the Act. There are five agencies not

subject to the Act.

4. Obstruction of Audit. Stipulates the penalty for willfully attempting to hinder, interfere

or obstruct an audit.

Amendments can be seen in their entirety in Appendix C.

STATE AGENCY INTERNAL AUDIT FUNCTIONS

Audit Resources

Personnel Resources

As shown in Table 3, on page 7, there are 139.25 internal auditor positions, which are spread

across 34 State agencies. There was a net loss of one position throughout the State over the past

year. Significant changes over the last year included:

Department of Transportation gained five positions but still has taken a 29% reduction in

positions over five years;

Department of Public Safety has three less positions compared to the Departments of

Correction, Crime Control and Public Safety, and Juvenile Justice and Delinquency

Prevention combined positions before consolidation;

OSBM lost six SFSF3 time-limited positions and gained one ELC

4 and two positions

funded by the Office of Information Technology Services.

There are twelve agencies with no internal auditor positions. Four of these agencies use the

OSBM’s Office of Internal Audit as their internal audit program and five agencies are not subject

to the Internal Audit Act. Three university contract for audit service as follows:

North Carolina School of the Arts contracts with Winston-Salem State University for

audit services;

North Carolina School of Science and Math contracts with the University of North

Carolina General Administration; and

Fayetteville State University utilizes contracted auditors.

The information in Table 3, on page 7, provides data on positions regardless of filled or vacant

status.

3 Federal State Fiscal Stabilization Fund grant supported these positions.

4 Federal Early Learning Challenge grant funds this position and terminates December 31, 2015.

DRAFT

6

Internal auditors can demonstrate proficiency by obtaining professional certification and advanced

degrees. Overall, internal auditors hold 111 professional certifications in 15 different audit areas;

78% of these being either Certified Public Accountants, Certified Internal Auditors, Certified

Information Systems Auditors or Certified Fraud Examiners. The number and type of professional

certifications held by the agency’s internal auditors are shown in Chart 1on page 8.

In addition, Chart 2, on page 8, shows advanced degrees held by the agency’s internal auditors.

Combined, the auditors hold 49 advanced degrees with 73% of these being Masters in Business

Administration, Accounting or Accounting and Finance Management.

DRAFT

7

Table 3

2012 2011 2010 2009 2008 2012 2011 2010 2009 2008

Administrative Office of the Courts 4

3 3 3 3 3 Office of Administrative Hearings4

0 0 0 0 0

Community College System Office 1 1 1 0 0 Office of Lieutenant Governor4

0 0 0 0 0

Department of Administration1

0 0 0 0 0 Office of State Controller4

0 0 0 1 1

Department of Agriculture & Consumer Services 1 1 1 1 1 Office of the Governor/Office State Budget and Management1, 3

8 11 10 4 0

Department of Commerce2

3 0 0 0 2 Office of the State Auditor1

0 0 0 0 0

Department of Commerce, Employment Security Division2

N/A 2 2 1 0 State Board of Elections4

0 0 1 4 4

Department of Cultural Resources 1 1 1 1 1 Wildlife Resources Commission1

0 0 0 0 0

Department of Environment and Natural Resources 2 2 2 2 1 Appalachian State University 4 5 4 5 5

Department of Health and Human Services 8 8 8 8 8 East Carolina University 7 7 7 6 6

Department of Insurance 1 1 1 1 0 Elizabeth City State University 2 2 2 2 2

Department of Justice 1 1 1 1 0 Fayetteville State University5

0 2 2 2 2

Department of Labor1

0 0 0 0 0 North Carolina Agriculture and Technical State University 5 4 4 4 4

Department of Public Instruction 1 2 1 1 1 North Carolina Central University 3 3 3 3 4

Department of Public Safety9

19 N/A N/A N/A N/A North Carolina School of Science and Math7

0 1 1 1 1

Department of Correction9

N/A 18 18 18 19 North Carolina School of the Arts6

0 0 1 1 1

Department of Crime Control and Public Safety9

N/A 1 1 1 1 North Carolina State University 6.25 4.25 6 7 7

Department of Juvenile Justice and Delinquency Prevention9

N/A 3 3 3 4 University of North Carolina Hospitals 5 4 5 5 5

Department of Revenue 2 2 2 2 2 University of North Carolina - Asheville 1 1 1 1 1

Department of Secretary of State 1 1 1 1 1 University of North Carolina - Chapel Hill 6 6 6 6 6

Department of State Treasurer 3 2 2 1 1 University of North Carolina - Charlotte 4 4 4 4 4

State Health Plan8

N/A 0 0 0 0 University North Carolina - General Administration 1 1 1 1 1

Department of Transportation 22 17 25 31 31 University of North Carolina - Greensboro 2 2 2 3 2

Housing Finance Agency4

0 0 0 0 0 University of North Carolina - Pembroke 1 1 1 1 1

Indigent Defense Services4

1 1 1 1 1 University of North Carolina - Wilmington 4 4.5 4 4 4

Information Technology Services4

2 3 2 2 1 Western Carolina University 2 2 2 2 2

North Carolina Education Lottery4

2 2 2 2 2 Winston-Salem State University 4 4 3 3 3

Total 139.25 140.75 148.00 151.00 146.00

Positions

AgencyAgency

Statewide Internal Auditor Position Level Comparison

1. Utilizes the Interagency Internal Audit program

2. The Employment Security Commission merged with Department of Commerce in FY2012, Division of Employment Service has federal funded internal audit position and the remaining Department of Commerce is utilizes the

Interagency Internal Audit program

3. Council of Internal Auditing Interagency Internal Audit Program, housed in the Office of State Budget and Management

4. Agency is not subject to the Internal Audit Act

5. Uses contract auditors

6. Contracts with Winston-Salem State University

7. Contracts with UNC-General Administration

8. State Health Plan merged with Department of State Treasurer in FY2012

9. Departments of Correction, Crime Control and Public Safety, and Juvenile Justice and Delinquency Prevention consolidated as of January 1, 2012

Positions

DRAFT

8

Chart 1

CPA, 38

CIA, 18CFE, 17

CISA, 14

CICA, 7

CGFM, 5

CPM, 2

CGAP, 2

CISSP, 2 Other, 6

Agency Internal Auditors

Professional Certifications

CPA/Certified Public Accountant

CIA/Certified Internal Auditor

CFE/Certified Fraud ExaminerCISA/Certified Information Systems Auditor

CICA/Certified Internal Controls Auditor

CGFM/Certified Government Financial ManagerCGAP/Certified Government Audit Professional

CPM/Certified Public Manager

CISSP/Certified IT Security

Other:

CBA/Certified Business Analyst

CBRM/Certified Business Resilience ManagerCEH/Certified Ethical Hacker

CHC/Certified Healthcare Compliance

CProjM/Certified Project ManagerITIL-F/Information Technology Infrastructure

Library-Foundation

Chart 2

MBA, 25

MAC, 8

MAFM, 3

M.Ed., 2

MEA, 2

MPA, 2

MSA, 2

Other , 5

Agency Internal Auditors

Advanced Degrees

MAC/Masters of Accounting

MBA/Master of Business Administration

MAFM/Masters of Accounting & Financial Mgmt.M.Ed./Master of Education

MEA/Master of Agricultural Economics

MPA/Master of Public AdministrationMSA/Master of Science/Accounting

Other:

MTAX/Masters of Taxation

MAM/Masters of Accounting/ManagementMIS/Master of Information Sciences

MS/Masters of Science

MSIE/Masters of Science Industrial Engineering

DRAFT

9

Computer Assisted Audit Tools

In addition to personnel, internal audit functions use computer assisted audit tools (CAATs) to

improve the efficiency and effectiveness of administrative and audit tasks. Automated tools

range from basic office productivity software such as spreadsheet, word processors and text

editing programs to more advanced software packages involving the use of statistical analysis and

business intelligence tools.

The advanced software products are typically productivity tools or generalized audit software.

Productivity tools aid with the administrative and management of the audit processes such as

Teammate and SharePoint. Generalized audit software tools assist with data extract and analyze

such as ACL, IDEA and SAS.

Table 4 shows all internal audit functions use the Microsoft Office products to enhance

productivity through automation. In addition, fifteen agencies use generalized audit software

tools for data extraction and analysis; and six agencies use productivity tools to automate work

papers and work flow processes.

Table 4

State Agency

Spreadsheet or

Word Documents1

Generalized

Audit Software2

Productivity

Tools3

Community College Central Office

Department of Agriculture and Consumer Services

Department of Commerce-Division of Employment Services

Department of Cultural Resources

Department of Environment and Natural Resources

Department of Health and Human Services

Department of Insurance

Department of Justice

Department of Public Instruction

Department of Public Safety

Department of Revenue

Department of Secretary of State

Department of State Treasurer

Department of Transportation

Office of the Governor/Office of State Budget and Management

Appalachian State University

East Carolina University

Elizabeth City State University

North Carolina Agriculture and Technical State University

North Carolina Central University

North Carolina State University

University of North Carolina - Asheville

University of North Carolina - Chapel Hill

University of North Carolina - Charlotte

University of North Carolina - General Administration

University of North Carolina - Greensboro

University of North Carolina - Pembroke

University of North Carolina - Wilmington

University of North Carolina Hospitals

Western Carolina University

Winston-Salem State University

Computer Assisted Audit Tools Usage

3. Streamline process to managing audits through electronic work papers and work flows. Some products are Teammate and SharePoint.

2. Perform routine task for data extract and analysis. Some products are ACL, IDEA, and EZ-R Stats.

1. Microsoft Office products.

DRAFT

10

Efforts and Accomplishments

Internal audit functions conduct various activities designed to add value and improve a State

agency’s operations. For the period July 1, 2011 through June 30, 2012, the majority of activities

conducted by the internal auditors were compliance audits. Chart 3 shows the percentage of

internal audit reports prepared by type. In addition to the audit work shown here, most internal

audit functions provide technical assistance throughout the year. During the same time period,

internal auditors provided assistance to their agency’s management on 578 different activities

which did not result in report issuance.

The audit projects by State agency are shown in Table 5 on the next page. The Table depicts the

efforts of each internal audit function. Efforts are directly related to the size of the audit function.

There are many State agencies that have one internal auditor which limits the number of audits

that can be accomplished throughout the year.

Chart 3

Agency Engagements

July 1, 2011 through June 30, 2012

Compliance

51%

Special Review

12%

Internal Controls

Assessment

8%

Investigative

7%

Follow Up

6%

Financial

5%

Risk Assessment

4%

Performance/

Operational

3%

Special

Projects

2%

Information

Systems

2%

DRAFT

11

Table 5

Agency

Financial

Performance/

Operational Investigative Compliance

Internal

Controls

Assessment

Information

Systems

Risk

Assessment

Follow

Up

Special

Review

Special

Projects

Community College Central Office 1 3

Department of Agriculture & Consumer Services 8 2 8 2

Department of Commerce-Division of Employment Security 3 41 1 1 32

Department of Cultural Resources 4

Department of Environment & Natural Resources 5 3 3 2 1

Department of Health & Human Services 1 2 35 3 1

Department of Insurance 1 2 1 2 1

Department of Justice 1 1 1 1

Department of Public Instruction 1 1 1

Department of Public Safety2

3 2 10 53 12 38 24 74 4

Department of Revenue 6 12 1 49

Department of Secretary of State 1 6

Department of State Treasurer 2 2 3 1 9

Department of Transportation 33 37 740 1 3

OIA's Interagency Internal Audit Program1

2 2 14 5 4 8 5 12

Appalachian State University 6 5 3 4 37 12 1 2 4

East Carolina State University 5 20 2 2 2 14 4

Elizabeth City State University 1 2 1

Fayetteville State University 1 3 1 1 1 1 1

North Carolina Agriculture & Technical State University 5 1 3 3 1 1 1

North Carolina Central University 2 2 2 2 4 1 1 5

North Carolina School of Science & Math 2 4 9

North Carolina School of the Arts 1 1 1 1

North Carolina State University 10 1 1 9

University North Carolina - Asheville 1 1 1 1 1 1 5 1

University of North Carolina - Chapel Hill 1 3 2 4

University of North Carolina - Charlotte 4 2 1 4 1 2 1 3

University of North Carolina - General Administration 1 1 1

University of North Carolina - Greensboro 2 4 4 1 2

University of North Carolina - Pembroke 2 1 1 2 4

University of North Carolina - Wilmington 1 3 4 3 3 1 7 4

University of North Carolina Hospitals 2 17 4 14 6 6 1 5 2 2

Western Carolina University 4 1 4 1 1 1 15 1

Winston-Salem State University 2 5 2 1 2 3

Totals 86 55 123 894 145 31 64 103 219 38

1. Using OIA Interagency Internal Audit Program: Department of Administration, Department of Commerce, Department of Labor, Department of State Auditor, Wildlife Resource Commission,

Office of the Governor, and OSBM

2. Departments of Correction, Crime Control and Public Safety, and Juvenile Justice and Delinquency Prevention consolidated as of January 1, 2012

Agency Engagements

July 1, 2011-June 30, 2012

D

RAFT

12

Compliance

Internal Audit Act and Council Requirements

The Internal Audit Act and the North Carolina Internal Audit Manual require internal audit

functions to submit the following documents and reports to the Office of Internal Audit: internal

audit charter, organizational chart, audit plan and engagement reports. Table 6 shows compliance

with document submission and overall compliance rates for all 35 internal audit functions.

Table 6

Community College System Office

Department of Agriculture & Consumer Services

Department of Correction

Department of Crime Control and Public Safety

Department of Juvenile Justice and Delinquency Prevention

Department of Public Safety1

N/A

Department of Cultural Resources

Department of Environment and Natural Resources

Department of Health and Human Services2

Department of Insurance

Department of Justice

Department of Public Instruction3

Department of Revenue

Department of Secretary of State3

Department of State Treasurer3

Department of Transportation

OIA's Interagency Internal Audit Program4

Appalachian State University3

East Carolina University

Elizabeth City State University

Fayetteville State University

North Carolina A&T State University

North Carolina Central University

North Carolina School of the Arts

North Carolina School of Science and Math

North Carolina State University

University of North Carolina - Asheville

University of North Carolina - Chapel Hill

University of North Carolina - Charlotte

University of North Carolina - General Administration

University of North Carolina - Greensboro

University of North Carolina - Pembroke

University of North Carolina - Wilmington

University of North Carolina Hospitals

Western Carolina University

Winston-Salem State University

TOTAL 35 36 29 30

Compliance rate 97% 100% 81% 83%

Compliance with Internal Audit Act and Statewide Internal Audit Manual

1. The Departments of Correction, Crime Control and Public Safety and Juvenile Justice and Delinquency Prevention consolidated on January 1, 2012.

2. Follows Government Auditing Standards which does not require an audit charter.

3. Internal audit position was vacant.

4. Using OIA Interagency Internal Audit Program: Department of Administration, Department of Commerce, Department of Labor, Office of State

Auditor, Wildlife Resources Commission, Office of the Governor, and Office of State Budget and Management.

ReportsAgency Charter Org Chart

Annual

Plan

DRAFT

13

Internal Audit Director

The Internal Audit Act requires State agencies to appoint a Director of Internal Audit (Director)

who must report to the head of the agency. The Act defines head as Governor, Council of State

member, Cabinet Secretary, the President of the University System or the Superintendent of

Public Instruction. Table 7 shows all State agencies have appointed a director but only 39% of

the director’s report to the head of the State agency as defined in the Act. The low reporting

compliance rate is most likely due to the strict definition of ‘agency head’ which has lead to one

of the proposed legislative changes located on page 27.

Table 7

Community College Central Office Yes

Department of Administration Yes

Department of Agriculture and Consumer Services Yes

Department of Commerce No

Department of Cultural Resources Yes

Department of Environment and Natural Resources Yes

Department of Health and Human Services Yes

Department of Insurance Yes

Department of Justice Yes

Department of Labor No

Department of Public Instruction Yes

Department of Public Safety No

Department of Revenue Yes

Department of State Treasurer Yes

Department of the Secretary of State Yes

Department of Transportation Yes

Office of the Governor/Office of State Budget and Management Yes

Office of the State Auditor Yes

Wildlife Resources Commission No

Appalachian State University No

East Carolina University No

Elizabeth City State University No

Fayetteville State University No

North Carolina Agriculture and Technical State University No

North Carolina Central University No

North Carolina School of Science and Math No

North Carolina School of the Arts No

North Carolina State University No

University of North Carolina - Asheville No

University of North Carolina - Chapel Hill No

University of North Carolina - Charlotte No

University of North Carolina - General Administration No

University of North Carolina - Greensboro No

University of North Carolina - Pembroke No

University of North Carolina - Wilmington No

University of North Carolina Hospitals No

Western Carolina University No

Winston-Salem State University No

Compliance rate 100% 39%

Compliance with Internal Audit Director Appointment and Reporting

Agency

Director

Appointed

Meets Reporting

Requirement

DRAFT

14

External Quality Assurance Review (Peer Review)

Quality assurance reviews are required either every three or five years, depending on which audit

standard is followed. Thirteen internal audit functions are currently being developed and are not

required to have a review. Of the 23 internal audit functions established, only two have received

external quality assurance reviews within the required time period as shown in Table 8. It can

take 6 months to prepare for an external quality assurance review. North Carolina State

University’s peer review began June 2012 and should be completed in October 2012.

Fayetteville State University completed the self-assessment and requested a peer review. This

review is expected to begin in November 2012.

Table 8

Agency/University

Agency

Establishment Date Date of Last QAR

Deadline For First

Required QAR

Compliant

University of North Carolina - Wilmington 1983 June 2011

East Carolina University May 2011

Non-Compliant

Department of Agriculture & Consumer Services 1969 None

Department of Health and Human Services 1994 March 2004

Department of Transportation December 2002

Appalachian State University 1965 None

Elizabeth City State University 1994 None

Fayetteville State University 1998 None

North Carolina A&T State University 1969 July 1997

North Carolina Central University 1997 None

North Carolina School of the Arts 2004 None

North Carolina State University 1963 None

University of North Carolina - Asheville 2001 None

University of North Carolina - Chapel Hill 1963 None

University of North Carolina - Charlotte 1973 None

University of North Carolina - Greensboro 1984 None

University of North Carolina - Pembroke 1984 None

University of North Carolina Hospitals 1988 None

Western Carolina University 1975 None

Winston-Salem State University 1992 None

Not Required

North Carolina School of Science and Math November 2007 None November 2012

Department of Public Safety1

None December 2012

Department of Cultural Resources January 2008 None January 2013

Department of Insurance June 2008 None June 2013

Department of Secretary of State July 2008 None July 2013

OIA Internal Audit Interagency program2

September 2008 None September 2013

Department of Environment and Natural Resources October 2008 None October 2013

Department of Revenue October 2008 None October 2013

Department of Justice February 2009 None February 2014

Department of State Treasurer April 2009 None April 2014

Department of Public Instruction June 2009 None June 2014

Community College System Office September 2009 None September 2014

University of North Carolina - General Administration August 2010 None August 2015

Agency Establishment Date and

Compliance with Quality Assurance Review (QAR) Requirement

1. Departments of Correction, Crime Control and Public Safety, and Juvenile Justice and Delinquency Prevention consolidated on January 1,

2012. Council allowed the new Department until the end of the year to comply with this requirement.

2. Using OIA Interagency Internal Audit Program: Department of Administration, Department of Commerce, Department of Labor, Office

of State Auditor, Wildlife Resources Commission, Office of the Governor, and Office of State Budget and Management.

DRAFT

15

APPENDIX A

NORTH CAROLINA INTERNAL AUDIT ACT

DRAFT

16

[THIS PAGE INTENTIONALLY LEFT BLANK]

DRAFT

17

Appendix A

Internal Audit Act

Article 79.

Internal Auditing.

§ 143-745. Definitions; intent; applicability.

(a) For the purposes of this section:

(1) "Agency head" means the Governor, a Council of State member, a cabinet

secretary, the Chief Justice of the Supreme Court, the President of The

University of North Carolina, and the Superintendent of Public Instruction.

(2) "State agency" means each department created pursuant to Chapter 143A or

143B of the General Statutes, the Judicial Branch, The University of North

Carolina, and the Department of Public Instruction.

(b) This Article applies only to a State agency that:

(1) Has an annual operating budget that exceeds ten million dollars

($10,000,000);

(2) Has more than 100 full-time equivalent employees; or

(3) Receives and processes more than ten million dollars ($10,000,000) in cash in

a fiscal year. (2007-424, s. 1.)

§ 143-746. Internal auditing required.

(a) Requirements. – A State agency shall establish a program of internal auditing that:

(1) Implements an effective system of internal controls that safeguards public

funds and assets and minimizes incidences of fraud, waste, and abuse.

(2) Ensures programs and business operations are administered in compliance

with federal and state laws, regulations, and other requirements.

(3) Reviews the effectiveness and efficiency of agency and program operations

and service delivery.

(4) Periodically audits the agency's major systems and controls, including:

a. Accounting systems and controls.

b. Administrative systems and controls.

c. Electronic data processing systems and controls.

(b) Internal Audit Standards. – Internal audits shall comply with current Standards for the

Professional Practice of Internal Auditing issued by the Institute for Internal Auditors or, if

appropriate, Government Auditing Standards issued by the Comptroller General of the United

States.

(c) Appointment and Qualifications of Internal Auditors. – Any internal auditor employed

by a State agency shall at a minimum have a bachelor's degree from an accredited college or

university and:

(1) Certification or licensure as a certified public accountant, certified internal

auditor, certified fraud examiner, certified information systems auditor,

professional engineer, or attorney; or

(2) A minimum of five years' experience in internal or external auditing,

management consulting, program evaluation, management analysis,

economic analysis, industrial engineering, or operations research.

(d) Director of Internal Auditing. – The agency head shall appoint a Director of Internal

Auditing who shall report to the agency head and shall not report to any employee subordinate to

the agency head. (2007-424, s. 1.)

DRAFT

18

§ 143-747. Council of Internal Auditing.

(a) The Council of Internal Auditing is created, consisting of the following members:

(1) The State Controller who shall serve as Chair.

(2) The State Budget Officer.

(3) The Secretary of Administration.

(4) The Attorney General.

(5) The Secretary of Revenue.

(6) The State Auditor who shall serve as a nonvoting member. The State Auditor

may appoint a designee.

(b) The Council shall be supported by the Office of State Budget and Management.

(c) The Council shall:

(1) Hold its first meeting before November 1, 2007, and thereafter at the call of

the Chair or upon written request to the Chair by two members of the

Council.

(2) Keep minutes of all proceedings.

(3) Promulgate guidelines for the uniformity and quality of State agency internal

audit activities.

(4) Recommend the number of internal audit employees required by each State

agency.

(5) Develop internal audit guides, technical manuals, and suggested best internal

audit practices.

(6) Administer an independent peer review system for each State agency internal

audit activity; specify the frequency of such reviews consistent with

applicable national standards; and assist agencies with selection of

independent peer reviewers from other State agencies.

(7) Provide central training sessions, professional development opportunities, and

recognition programs for internal auditors.

(8) Administer a program for sharing internal auditors among State agencies

needing temporary assistance and assembly of interagency teams of internal

auditors to conduct internal audits beyond the capacity of a single agency.

(9) Maintain a central database of all annual internal audit plans; topics for review

proposed by internal audit plans; internal audit reports issued and individual

findings and recommendations from those reports.

(10) Require reports in writing from any State agency relative to any internal audit

matter.

(11) If determined necessary by a majority vote of the council:

a. Conduct hearings relative to any attempts to interfere with,

compromise, or intimidate an internal auditor.

b. Inquire as to the effectiveness of any internal audit unit.

c. Authorize the Chair to issue subpoenas for the appearance of any

person or internal audit working papers, report drafts, and any other

pertinent document or record regardless of physical form needed for

the hearing.

(12) Issue an annual report including, but not limited to, service efforts and

accomplishments of State agency internal auditors and to propose legislation

for consideration by the Governor and General Assembly. (2007-424, s. 1.)

DRAFT

19

APPENDIX B

Staffing Recommendation

DRAFT

20

[THIS PAGE INTENTIONALLY LEFT BLANK]

DRAFT

21

Appendix B

Staffing Recommendation

Agency

Total Internal

Audit Positions

Needed

Current Internal

Audit Positions

Recommended

Number of New

Positions

Estimated Cost of

New Internal

Audit Positions

Department of Administration 3 0 3 279,000

Department of Agriculture and Consumer Services 3 1 2 186,000

Department of Commerce 5 0 5 465,000

Department of Correction 18 18 - -

Department of Crime Control & Public Safety 5 1 4 372,000

Department of Cultural Resources 2 1 1 93,000

Department of Environment and Natural Resources 8 2 6 558,000

Department of Health and Human Services 19 8 11 1,023,000

Department of Insurance 2 1 1 93,000

Department of Justice 3 1 2 186,000

Department of Juvenile Justice and Delinquency Prevention 3 3 - -

Department of Labor Shared Pool 0 - -

Department of Public Instruction 3 1 2 186,000

Department of Revenue 2 2 - -

Department of State Treasurer 2 2 - -

Department of the Secretary of State Shared Pool 1 - -

Department of Transportation 31 25 6 558,000

Office of Administrative Hearings n/a 0 - -

Office of Lieutenant Governor n/a 0 - -

Office of the Governor /Office of State Budget and Management Shared Pool 4 - -

Office of the State Auditor Shared Pool 0 - -

Wildlife Resource Commission Shared Pool 0 - -

North Carolina Community College Central Office 3 1 2 186,000

Appalachian State University 4 4 - -

East Carolina University 7 7 - -

Elizabeth City State University 2 2 - -

Fayetteville State University 2 2 - -

North Carolina A&T State University 4 4 - -

North Carolina Central University 3 3 - -

North Carolina School of Science & Math 1 1 - -

North Carolina School of the Arts 1 1 - -

North Carolina State University 7 6 1 93,000

University of North Carolina Hospitals 7 5 2 186,000

University of North Carolina-Asheville 1 1 - -

University of North Carolina-Chapel Hill 8 6 2 186,000

University of North Carolina-Charlotte 4 4 - -

University of North Carolina-General Administration 3 1 2 186,000

University of North Carolina-Greensboro 3 2 1 93,000

University of North Carolina-Pembroke 1 1 - -

University of North Carolina-Wilmington 4 4 - -

Western Carolina University 2 2 - -

Winston-Salem State University 3 3 - -

Subtotal 179 131 53 4,929,000

Agencies Not Subject to Legislation

Administrative Office of the Courts 6 3 - -

Employment Security Commission 10 2 - -

Housing Finance Agency Shared Pool 0 - -

Information Technology Services 3 2 - -

North Carolina Education Lottery 6 2 - -

Office of State Controller Shared Pool 0 - -

State Board of Elections Shared Pool 1 - -

State Health Plan 18 0 - -

Subtotal 43 10 0 0

Grand Total 222 141 53 4,929,000

2 - Six time-limited positions within the Office of Budget and Management are not included. The positions terminate September 30, 2011 and

are only used to audit American Recovery and Reinvestment Act funds through State government.

Council of Internal Auditing

State Agency Internal Audit Staffing Level Recommendation

October 2010

1 - Agencies with an established internal audit function with one position may utilize the shared pool for support.

DRAFT

22

[THIS PAGE INTENTIONALLY LEFT BLANK]

DRAFT

23

APPENDIX C

Proposed Legislation

DRAFT

24

[THIS PAGE INTENTIONALLY LEFT BLANK]

DRAFT

25

Appendix B

Proposed Legislation

The Council of Internal Auditing voted to propose four amendments to the Internal Audit Act,

one being a revision and the other an addition to the Act.

AMENDMENT 1: Revisions to the Internal Audit Act

The Council of Internal Auditing successfully introduced House Bill 393 (see below) during the

2011-2012 General Assembly Session. House Bill 393 passed the House of Representatives and

the Senate sent the Bill to the Program Evaluation Committee receiving a favorable vote, then to

the Committee on Finance where no action was taken.

GENERAL ASSEMBLY OF NORTH CAROLINA

SESSION 2011

HOUSE BILL 393

Short Title: Modify Internal Auditing Statutes. (Public)

Sponsors: Representatives Hastings and McGee (Primary Sponsors).

For a complete list of Sponsors, see Bill Information on the NCGA Web Site.

Referred to: Government.

March 17, 2011

A BILL TO BE ENTITLED

AN ACT TO MODIFY THE INTERNAL AUDITING STATUTES APPLICABLE TO LARGE

STATE DEPARTMENTS AND THE UNIVERSITY SYSTEM.

The General Assembly of North Carolina enacts:

SECTION 1. Article 79 of Chapter 143 of the General Statutes reads as rewritten:

"Article 79.

"Internal Auditing.

"§ 143-745. Definitions; intent; applicability.

(a) For the purposes of this section:

(1) "Agency head" means the Governor, a Council of State member, a cabinet

secretary, the President of The University of North Carolina, and the

Superintendent of Public Instruction.

(2) "State agency" means each department created pursuant to Chapter 143A or

143B of the General Statutes, The University of North Carolina, and the

Department of Public Instruction.

(b) This Article applies only to a State agency that:

(1) Has an annual operating budget that exceeds ten million dollars

($10,000,000);

(2) Has more than 100 full-time equivalent employees; or

DRAFT

26

(3) Receives and processes more than ten million dollars ($10,000,000) in cash

in a fiscal year.

"§ 143-746. Internal auditing required.

(a) Requirements. – A State agency shall establish a program of internal auditing that:

(1) Implements Promotes an effective system of internal controls that safeguards

public funds and assets and minimizes incidences of fraud, waste, and abuse.

(2) Ensures Determines if programs and business operations are administered in

compliance with federal and state laws, regulations, and other requirements.

(3) Reviews the effectiveness and efficiency of agency and program operations

and service delivery.

(4) Periodically audits the agency's major systems and controls, including:

a. Accounting systems and controls.

b. Administrative systems and controls.

c. Electronic data processing Information technology systems and

controls.

(b) Internal Audit Standards. – Internal audits shall comply with current Standards for the

Professional Practice of Internal Auditing issued by the Institute for Internal Auditors or, if

appropriate, Government Auditing Standards issued by the Comptroller General of the United

States.

(c) Appointment and Qualifications of Internal Auditors. – Any internal auditor

employed by a State agency shall at a minimum have a bachelor's degree from an accredited

college or university and:Any state employee who performs the internal audit function shall meet

the minimum qualifications for internal auditors established by the Office of State Personnel.

(1) Certification or licensure as a certified public accountant, certified internal

auditor, certified fraud examiner, certified information systems auditor,

professional engineer, or attorney; or

(2) A minimum of five years' experience in internal or external auditing,

management consulting, program evaluation, management analysis,

economic analysis, industrial engineering, or operations research.

(d) Director of Internal Auditing. – The agency head shall appoint a Director of Internal

Auditing who shall report to (i) the agency head and shall not report to any employee subordinate

to the agency head. head, (ii) the chief deputy or chief administrative assistant, or (iii) the agency

governing board, or subcommittee thereof, if such a governing board exists. The Director of

Internal Auditing shall be organizationally situated in a manner that avoids impairments to

independence as defined in the auditing standards referenced in subsection (b) of this section.

"§ 143-747. Council of Internal Auditing.

(a) The Council of Internal Auditing is created, consisting of the following members:

(1) The State Controller Controller, who shall serve as Chair.

(2) The State Budget Officer.

(3) The Secretary of Administration.

(4) The Attorney General.

(5) The Secretary of Revenue.

(6) The President of The University of North Carolina, who may appoint a

designee.

(7) The State Auditor Auditor, who shall serve as a nonvoting member. The State

Auditor may appoint a designee.

(b) The Council shall be supported by the Office of State Budget and Management.

(c) The Council shall:

(1) Hold its first meeting before November 1, 2007, and thereafter meetings at

the call of the Chair or upon written request to the Chair by two members of

the Council.

DRAFT

27

(2) Keep minutes of all proceedings.

(3) Promulgate guidelines for the uniformity and quality of State agency internal

audit activities.

(4) Recommend the number of internal audit employees required by each State

agency.

(5) Develop internal audit guides, technical manuals, and suggested best internal

audit practices.

(6) Administer an independent peer review system for each State agency internal

audit activity; specify the frequency of such reviews consistent with

applicable national standards; and assist agencies with selection of

independent peer reviewers from other State agencies.

(7) Provide central training sessions, professional development opportunities,

and recognition programs for internal auditors.

(8) Administer a program for sharing internal auditors among State agencies

needing temporary assistance and assembly of interagency teams of internal

auditors to conduct internal audits beyond the capacity of a single agency.

(9) Maintain a central database of all annual internal audit plans; topics for

review proposed by internal audit plans; internal audit reports issued and

individual findings and recommendations from those reports.

(10) Require reports in writing from any State agency relative to any internal audit

matter.

(11) If determined necessary by a majority vote of the council:

a. Conduct hearings relative to any attempts to interfere with,

compromise, or intimidate an internal auditor.

b. Inquire as to the effectiveness of any internal audit unit.

c. Authorize the Chair to issue subpoenas for the appearance of any

person or internal audit working papers, report drafts, and any other

pertinent document or record regardless of physical form needed for

the hearing.

(12) Issue an annual report including, but not limited to, service efforts and

accomplishments of State agency internal auditors and to propose legislation

for consideration by the Governor and General Assembly."

SECTION 2. This act is effective when it becomes law.

AMENDMENT 2: Confidential Work Papers

The Council approved the following amendment to the Internal Audit Act.

N.C. Gen Stat. § 143-748

An internal auditor shall maintain, for 10 years, a complete file of all audit reports and reports of