Sopot - Mozambique Financial Market - EFCongress Financial Market 4th European Financial Congress...

35

Mozambique Financial Market 4 th European Financial Congress Sopot - Poland June 2014

Transcript of Sopot - Mozambique Financial Market - EFCongress Financial Market 4th European Financial Congress...

Mozambique Financial Market

4th European Financial CongressSopot - Poland

June 2014

Presentation Structure

I. About Mozambique

II. Economic Overview

III. Capital Markets Structure and Products

IV. Capital Market Performance

V. Capital Market: Challenges and Perspectives

• Mozambique is located in the Southern Africa

• Has an area of 799.380 Km2, of which 2.515 Km constitutes the Indian ocean coast line

• Language: Portuguese

• Population: 23,5 millions

Geographic Location and Language

About Mozambique

• Mozambique follows a multi-party political system with general election in every 5 years

• After the 1992 Peace agreement that marked the end of the civil war thecountry has been enjoying a political stability

• The democratic governance and the national reconciliation have been contributing enjoy a good business environment

• As per the Global Peace Index of 2013, the country was ranked at 48th position inthe world in terms of political stability

Political & Demographic Review

About Mozambique

Presentation Structure

I. About Mozambique

II. Economic Overview

III. Capital Markets Structure and Products

IV. Market Segmentation and Performance

V. Capital Market: Challenges and Perspectives

Presentation Structure

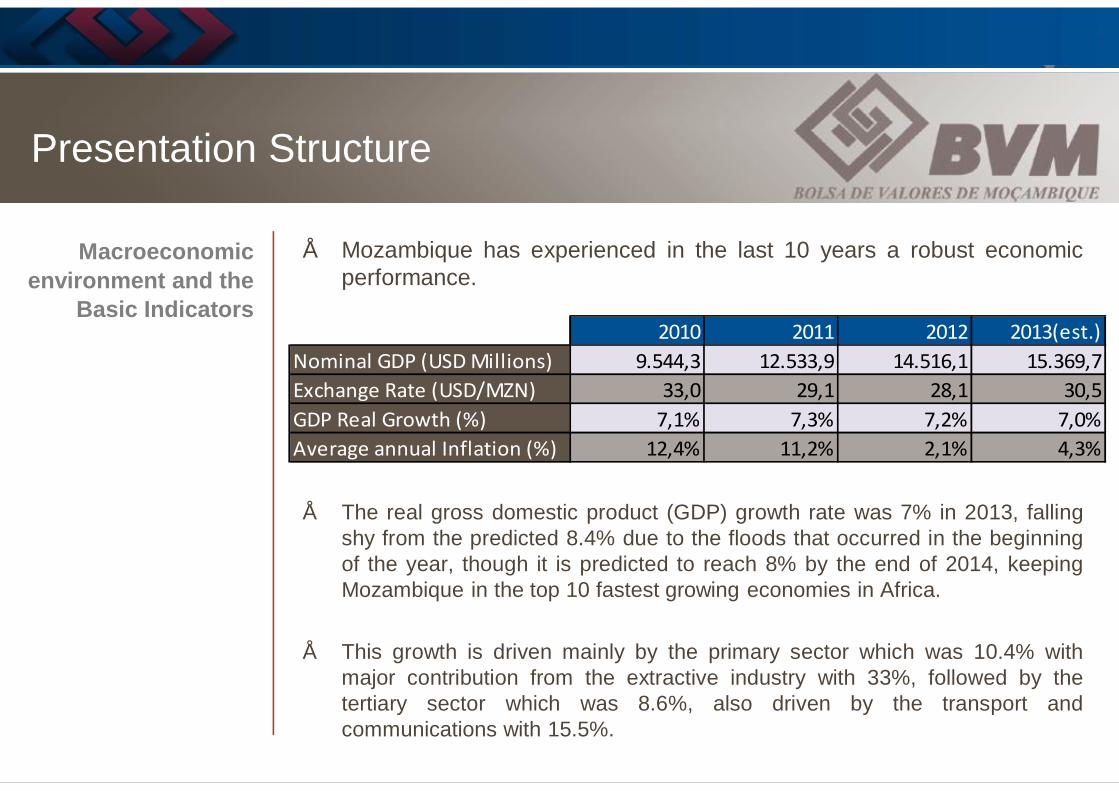

• Mozambique has experienced in the last 10 years a robust economicperformance.

• The real gross domestic product (GDP) growth rate was 7% in 2013, fallingshy from the predicted 8.4% due to the floods that occurred in the beginningof the year, though it is predicted to reach 8% by the end of 2014, keepingMozambique in the top 10 fastest growing economies in Africa.

• This growth is driven mainly by the primary sector which was 10.4% withmajor contribution from the extractive industry with 33%, followed by thetertiary sector which was 8.6%, also driven by the transport andcommunications with 15.5%.

Macroeconomic environment and the

Basic Indicators 2010 2011 2012 2013(est.)

Nominal GDP (USD Millions) 9.544,3 12.533,9 14.516,1 15.369,7Exchange Rate (USD/MZN) 33,0 29,1 28,1 30,5GDP Real Growth (%) 7,1% 7,3% 7,2% 7,0%Average annual Inflation (%) 12,4% 11,2% 2,1% 4,3%

Macroeconomic environment and the

Basic Indicators

Economic Overview

• The secondary sector also had a positive growth because of the construction sector, contributing with 8.6% of the GDP;

• Inflation rate also tend to remain below 10% in the coming years since it dropped to one digit in 2012;

• This is meanly due to the implementation of sound and prudent macroeconomic policies, political stability and the structural reforms being undertaken;

• The agriculture is one of the major economic sector contributing to around GDP with 20%. Others are industry trade and transports and communications;

• Mozambique grew at an average annual rate of 6%-8% in the decade up to 2013, one of Africa's strongest performances;

Macroeconomic environment and the

Basic Indicators(cont.)

Economic Overview

• The strong and sustained economic growth, has relationshipwith natural resources, specifically coal, gas and aluminium.Electricity, cotton, tobacco, and shrimp are also otherimportant export resources;

• According to the World Bank, the emerging extractive industrycould provide the means for Mozambique to reach the statusof a middle-income country by 2025;

• Additionally, it is expected that revenues from these vastresources, including natural gas, coal, titanium andhydroelectric capacity, could overtake donor assistance withinfive years;

• The government is now focusing on boosting the rest of theeconomy.

Macroeconomic environment and the

Basic Indicators(cont.)

Economic Overview

• Being a member of the Southern African DevelopmentCommunity (SADC) and one of the signatories of the SADCfree trade protocol, together with the privileged geographicallocation of the country, Mozambique is well placed in to furthereconomic development;

• Though agriculture sector has been contributing to theeconomy in the recent years in around 20% to 25% of theGDP, in recent years sectors like mining and banking aregrowing in a steady rate;

• Foreign Direct Investment reached USD 5.9 billion in 2013;

• International reserves increased by USD 404 million over theyear;

Financial System Structure in

Mozambique

Economic Overview

Macroeconomic environment and the

Basic Indicators(cont.)

Economic Overview

Looking at the financial system as whole:

• There are efforts by the government to make credit more accessible,access to credit by the private sector and individuals remains difficultand expensive;

• Currently, interest rates for loans range between 17% and 22% perannum;

However:

• Despite the lack of depth in the financial industry, the financial sectorhas been growing, and overall financial intermediation has deepenedas banks’ branch networks have expanded to sub-urban and ruralareas. There are currently 20 commercial banks, including 2 newbanks that came into the market through acquisition of already existingbanks.

Presentation Structure

I. About Mozambique

II. Economic Overview

III. Capital Markets Structure and Products

IV. Market Segmentation and Performance

V. Capital Market: Challenges and Perspectives

The Mozambique Stock Exchange

- Background

Capital Markets Structure and Products

• Opening: October 1999

• Public entity under the umbrella of the Ministry of Finance

• Supervised by the Central Bank of Mozambique designated the Capital Markets Authority

• Managed by a Board of Directors and an Audit Committee

• Responsible for the management of the secondary securities market, and has sought, throughout its existence, to develop, broaden, consolidate and empower the Mozambican capital market on an on-going basis.

The Mozambique Stock Exchange

- Market Segmentation and Products Treaded

Capital Markets Structure and Products

• Objectives:

ü Diversify the existing financing alternatives;

ü Promotion of savings and its conversion into productive investment.

• Type of securities comprise of:

ü Shares and bonds issued by national or foreign entities;

ü Domestic and foreign public funds and similar securities;

ü Any other securities which by their nature and characteristics, may be admitted to listing:

§ Commercial Paper§ Participating Securities

The Mozambique Stock Exchange

-Key Milestones

Capital Markets Structure and Products

The Mozambique Stock Exchange

- Market Share

and Products Traded

Capital Markets Structure and Products

The Mozambique Stock Exchange

- Autonomous Services

Capital Markets Structure and Products

• Central Securities Depository:

• Established in 2006;

• To be operational in the beginning of the second semester of 2014;

• Main Innovation: registration and centralization of listed and non-listed securities in the country;

• In this first stage it will work as a service provided by the BVM, hence, also falling under the umbrella of the Central Bank as the Capital Market’s supervisory authority;

• In 2013, the BVM was designated the National Numbering Agency of Mozambique;

The Mozambique Stock Exchange

- Major partnerships and cooperation

Capital Markets Structure and Products

• Multilateral Partners

• ASEA – African Securities Exchanges Association;• CoSSE – Committee of SADC Stock Exchanges;• WFE – World Federation of Exchanges;• World Exchange Congress;• OIC Exchanges;• World Exchange Congress.

• Bilaterals Partners

• SADC Stock Exchanges• Euronext Lisbon;• Comittee of Angola Capital Market;• Perspectives: London Stock Exchange, Brasil

(BMF&Bovespa), South Korea, Japan (Tokyo), Poland.

The Commodities Exchange

Capital Markets Structure and Products

• Established in 2012;

• Main objectives: create a chain of products potentially tradable;

• Assure food security in the country;

• Improve the quality of commodities domestically produced;

• Help in the price discovery process;

• Diversification of markets.

Capital Market Performance

I. About Mozambique

II. Economic Overview

III. Capital Markets Structure and Products

IV. Capital Market Performance

V. Capital Market: Challenges and Perspectives

Current market Capitalization

Evolution

- Mozambique(1999 – June 10th, 2014

Capital Market Performance

Market Capitalization (1999 – June 10th, 2014)(MZN Millions)

Capital Market PerformanceMarket Capitalization Dimension

The Mozambique Stock Exchange

- Market Capitalization: World versus

Emerging Markets

Capital Markets Structure and Products

• Market Capitalization: Global and Emerging Markets

Market Capitalization Dimension

Mozambique Emerging Markets

World(% of GDP)

Capital Market Performance

Potential Market Capitalization Trend

Capital Market Performance

Source: Global Finance Stability Report, April 2013

Presentation Structure

I. About Mozambique

II. Economic Overview

III. Capital Markets Structure and Products

IV. Capital Market Performance

V. Capital Market: Challenges and Perspectives

Key Success Factors and Challenges

Capital Market: Challenges and Perspectives

• Macroeconomic Stability;• Development of the Financial Sector;• Quality of the Institutions;• Protection of the Investors;• Automation of Financial and Banking processes;• Demutualization of organizations;• Companies Profitable Strategy;• Development of Regulation and Supervision of Financial

Market;• Interconnection of Regional Markets;• Attracting Investment by Institutional Investors and Foreign

Investors.

Key Success Factors and Challenges

(cont.)

Capital Market: Challenges and Perspectives

Key Success Factors and Challenges

(cont.)

Capital Market: Challenges and Perspectives

Opportunities Drivers • In 2011 the Public-Private Partnership Law was approved by the

Government, and established that all megaprojects inMozambique should be listed at the Mozambique Stock Exchangeat least 5% to 20% of the shares;

• Mainly, these megaprojects shares are intended to be acquired byMozambican investors, looking for the empowerment ofMozambican people;

• It is expected that by the end of 2014, a Brazilian miningcompany, VALE Moçambique, will be the first megaprojectcompany to be listed at the Mozambique Stock Exchange with10% of the capital shares, representing a market capitalization ofaround USD 400 Millions.

Capital Market: Challenges and Perspectives

Capital Market: Challenges and PerspectivesThe Major Opportunities’ Drivers

In 2013, emerging markets, Sub-Saharian Africa in particular, 5.6%, detach in the context of the the world economic growth

Estimated growth of GDP and its Weight, 2013

GDP Growth

1.6% 8%

8%

2%

World3.3%

2%3.0%

4%

USA and CanadaLatin America and CaribbeanEuropean UnionNorth Africa and Middle EastSub-Saharian AfricaCEIAsian Countries in developmentJapanAustralia

24% 22%

0.0%

4%

3.4%

7.1%

19%3.1%

5.6%

1.9%

3.4%

Weight in the World GDP

The Major Opportunities’ Drivers

GDP Growth, 1992-2017

Capital Market: Challenges and Perspectives

The Major Opportunities’ Drivers

- PotentialSector Growth in

Africa,2013-2015

(%)

Capital Market: Challenges and Perspectives

The Major Opportunities’ Drivers

- Top 10 African destinations with the IDE highest

growth, 2007-2012

Capital Market: Challenges and Perspectives

THANK YOU !

4th European Financial CongressSopot - Poland

June 2014