Solar Rooftop in India & its Financial Viability

63

1 | Page DECLARATION I, K. Naveen Kumar, ROLL NO -------------, student of MBA (POWER MANAGEMENT) at National Power Training Institute, Faridabad hereby declare that the Training Report entitled “project tittle” is an original work and the same has not been submitted to any other institute for the award of any degree. A seminar presentation of the training report was made on_______________________________ and the suggestions as approved by the faculty were duly incorporated. Mr K.P Singh Parmar K. Naveen Kumar Project In charge MBA (Power Mgmt.) NPTI NPTI Faridabad Counter Signed Director/Principal of the Institute

Transcript of Solar Rooftop in India & its Financial Viability

1 | P a g e

DECLARATION

I, K. Naveen Kumar, ROLL NO -------------, student of MBA (POWER

MANAGEMENT) at National Power Training Institute, Faridabad hereby

declare that the Training Report entitled “project tittle” is an original work and

the same has not been submitted to any other institute for the award of any degree.

A seminar presentation of the training report was made

on_______________________________ and the suggestions as approved by the

faculty were duly incorporated.

Mr K.P Singh Parmar K. Naveen Kumar

Project In charge MBA (Power Mgmt.)

NPTI NPTI Faridabad

Counter Signed

Director/Principal of the Institute

2 | P a g e

ACKNOWLEDGEMENT

Learning experience is like no other, but to learn one seeks a teacher, a guide, a

mentor and I found all of these in Mr. Rajat Malhan, (AGM-Business

Development) who was my project guide during my intern at Moser Baer Project

Pvt Ltd . His guidance and support made the learning easy and enjoyable. Thank

you for all things.

I also express gratitude toward Mr. Subodh singh, Head HR and HR team of

Moser Baer project pvt ltd. for coordinating administrative activities and other

efforts.

I thank Mrs. Manju Mam, Dy. Director-CAMPS NPTI for giving me an

opportunity to learn at Moser Baer project pvt ltd and for always being there when

I needed her.

I thank Mr. K.P Singh Parmar, (Asst. Director)-NPTI, my internal project

guide, for imparting useful knowledge and helping me refine this report. The help

and support given by you has made my understanding better and can never be

repaid.

The guidance given by entire team of Moser Baer project pvt ltd , especially

Mr.Ghei,CEO and by Mr. Sumit Pandey, General Manager–Business

Development, was instrumental and I thank them for providing the necessary

guidance and support.

I thank Mr. J.S.S Rao, Principal Director–NPTI and Mr. S.K. Chaudhry,

Principal Director–NPTI for all the administrative support provided by them to

make this internship programme successful.

K. Naveen Kumar

3 | P a g e

LIST OF FIGURES

Fig No Particular Pg.No I Off Grid Rooftop solar PV system 15

Ii Grid Interacted Rooftop solar PV system 16

Iii Sewa Bhawan rooftop system 20

Iv Regen power Australia rooftop system 23

V Shahwat Greenfuels & Technology (L) Pvt. 24

Vi BSNL, Shimla Rooftop system 25

vii Azure power, Ghandinagar Rooftop system 26

viii Bar-graph of Future installations 38

Ix Different types of solar PV 42

X Solar PV market share 43

Xi Bangalore, BIPV technology rooftop system 45

4 | P a g e

LIST OF TABLES

Table

No

Particular Pg No

1 Area required in Sq.Mts 27

2 Annual Electricity generation in KWh 28

3 Incentives provided by JNNSM 30

4 Present status of RPSSGP 30

5 EPC Cost for 100KW with subsidy 35

6 Net Metring Tariff of different states 36

7 FiT of different states 37

8 Future installations in Rooftop 39

9 Comparison on rooftop schemes of states 40

10 RPSSGP target under JNNSM Phase2 41

11 Conversion efficiencies of different solar PV

technologies

44

12 P&L sheet of subsidised solar rooftop system 46

13 Cash flows of subsidised solar rooftop system 49

14 IRR sensitivity of Cap Ex with Tariff after subsidy 50

15 IRR sensitivity of Cap Ex with interest rate after

subsidy

51

16 P&L sheet of FiT rooftop solar system 52

17 Cash flows of FiT rooftop solar system 56

18 IRR sensitivity of Cap Ex with Tariff 58

19 IRR sensitivity of Cap Ex with interest rate 58

5 | P a g e

ABBREVIATIONS

AC Alternate Current

APPC Average Pooling Purchase Cost

BAPV Building Applied Photovoltaic

BIPV Building Integrated Photovoltaic

Cap Ex Capital Expenditure

CERC Central Electricity Regulatory Commission

CUF Capacity Utilisation Factor

Cum P&L Cumulative P&L

Cum Cash Cumulative Cash

DC Direct Current

DISCOM Distribution Company

EBT Earnings Before Tax

EBTID Earnings Before Tax Interest and Depreciation

EMC Electromagnetic Compatibility

EPC Engineering Procurement Construction

FiT Feed in Tariff

GBI Generation Based Incentive

GERC Gujarat Electricity Regulatory Commission

HT High Tension

IREDA Indian Renewable Energy Development Agency

IRR Internal Rate of Return

JNNSM Jawaharlal Nehru National Solar Mission

Km Kilometre

KW Kilo Watt

KWh Kilo Watt Hour

KWp Kilo Watt Peak

m2 Metre square

MNRE Ministry of New and Renewable Energy

MW Mega Watt

MWh Mega Watt Hour

O&M Operations & Maintains

PAT Profit After Tax

PCU Power Conditioning Unit

P&L Profit & Loss

PV Photovoltaic

RAPS Remote Area Power Supply System

Rs Rupees

RTPV Rooftop Photovoltaic

RPSSGP Rooftop PV & Small Solar Generation

Programme

SAPS Stand Alone Power System

SECI Solar energy Corporation of India

SPV Solar Photovoltaic

6 | P a g e

Sq.Mts Square Metres

7 | P a g e

Table of Contents

S.No Particulars Pg No Declaration 1

Acknowledgement 2

List of Figures 3

List of Tables 4

Abbreviations 5

Table of Contents 7

Executive Summary 09

1 Organisation Details 10

2 Introduction to the Project 13

3 Introduction to Rooftop Solar 14

3.1 what is Rooftop Solar 14

3.2 Types of rooftop solar 14

3.3 Off Grid Rooftop Solar 14

3.4 Grid Interacted Rooftop solar 16

3.5 Net Metering System 17

3.6 Feed in Tariff System 17

4 Case Studies 18

4.1 Sewa Bhawan 19

4.2 Sri Nripendranath Girls High School 21

4.3 Regen Power 22

4.4 Shahwat Green Fuel & Technology Pvt 24

4.5 BSNL, Shimla 25

4.6 Azure Power 26

5 Generation 27

6 Policies & Incentives 29

6.1 Central Policies 29

6.1.1 RPSSGP 29

6.1.2 JNNSM Phase II 31

6.2 State Policies 32

6.2.1 West Bengal 32

6.2.2 Gujarat 32

6.2.3 Karnataka 32

6.2.4 Andhra Pradesh 33

6.2.5 Tamil Nadu 33

6.2.6 Chhattisgarh 33

6.2.7 Kerala 34

7 Business Models 35

7.1 Pure Play EPC Model 35

7.2 Net Metering Model 36

7.3 Feed in Tariff Model 37

8 Target 38

8.1 Current Installation 38

8 | P a g e

8.2 Future Installations 39

9 Technology 42

9.1 Conversion efficiencies 44

9.2 BIPV 44

9.3 Case studies 45

10 Financial Viability of Rooftop Solar with Subsidy

and FiT

46

10.1 Financial Viability of Rooftop Solar

with Subsidy

46

10.1.1 P&L Sheet 46

10.1.2 Cash Flows 49

10.1.3 IRR Sensitivity 50

10.2 Financial Viability of Rooftop Solar

with FiT

52

10.2.1 P&L Sheet 52

10.2.2 Cash Flows 55

10.2.3 IRR Sensitivity 58

11 Challenges 59

11.1 Availability of Rooftop 59

11.2 Financial 59

11.3 Regulatory/Policy 59

11.4 Infrastructural 59

11.5 Other Challenges 60

12 Conclusion & Recommendations 62

13 Bibliography 63

9 | P a g e

Executive Summary

Energy plays a considerable role in the Socio-Economic development of a

country. This century‘s global challenge is energy: how to increase the generation,

how to make it equitable and affordable, and also how to keep the environment

pristine without warming the planet or polluting the atmosphere. Among the

renewable, sustainable and carbon-free energy generation options, solar stands

out. One hour of sunshine on our planet, if stored adequately, can meet the global

needs for an entire year. Regrettably, however, it remains largely unviable

because of low collection efficiency and the large area required receiving

sunshine.

India is endowed with rich solar energy resource. With a geographical area of

3.287 million square km, India accounts for 657.4 million MW. However, only

12.5% of the land area amounting to 0.413 million km square can, in theory, be

used for solar energy installations. Even if 10% of this area can be used, the

available solar energy would be 8 million MW per year at least on paper.

This report highlights the details of types of solar rooftop PV systems in India,

different metering systems which are used in the country, generation capacity of

rooftop with respect to area required, different business models used in the

country, economic viability of the subsidised rooftop and FiT (Feed in Tariff),

incentives given by the state government as well as central government, current

and future size of the market size in India and technologies & technological

developments in rooftop system.

This report has briefly explained about the grid interactive and off grid solar

rooftop system along with the Net-metring and Feed in Tariff systems.

This report also contains six different case studies of rooftop systems along with

their interaction with grid and metering system in India as well as abroad.

Also this report gives the area required for the generation of electricity for

different capacity of rooftop solar PV system.

10 | P a g e

Report also explains the different types of business models which are success-

fully existing in the current market scenario along with the target market and

future market according to present situation in the country.

This report gives all the financial incentives, schemes given by the different states

and along with the central government in rooftop solar PV system.

This report also shows the different technologies used in the rooftop solar PV

system and their future developments for increasing efficiency as well as to

reduce cost of solar system.

The financial viability of the rooftop solar PV system with subsidy as well as Feed

in Tariff is been included in this report.

11 | P a g e

1.ORGANISATION DETAILS

Established in 1983 in New Delhi, Moser Baer is one of India’s leading

technology companies. Moser Baer's flagship company, Moser Baer India

Limited (MBIL) has successfully developed cutting edge technologies to

become the world’s leader in optical storage media and successful

manufacturer of Solar PV cells & modules.

Moser Baer is an Indian Multinational Company with more than 25 years of

experience in delivering high technology products and services, over 7,000

employees, revenues of over USD 500 million and asset base of over USD 1

billion. Our products are manufactured at its state-of-the-art manufacturing

facilities in the suburbs of New Delhi

Moser Baer Clean Energy (MBCEL) has rapidly progressed to become India’s

largest solar power development company with a presence in Indian and key

strategic international markets, viz., Germany and Italy. MBCEL has

commissioned solar PV projects aggregating to more than 300 MWp across

India and in International Markets. Moser Baer has the distinction of

developing and implementing India’s first 5 MW solar farm in Sivagangai in

Tamil Nadu in December 2010. The Company has also commissioned Asia’s

first 30 MW solar farm at Banaskhantha, Gujarat in October 2011.

Moser Baer is an integrated player having presence across all segments of the

solar value chain – manufacturing of panels, developing of rooftop and ground

mount projects, financing, project implementation and O&M. This cross

presence gives us a unique insight in to the technical and operational aspects of

solar PV farms.

Moser Baer Solar limited (MBSL), our solar panel manufacturing facility at

Greater Noida, has a capacity of 215 MW and is the largest cell and module

12 | P a g e

manufacturing facility in India. We have been a front runner in introducing

state-of-art solar PV cells and modules manufacturing technologies in the

country.

Strategic Rationale:

To build portfolio across multiple fuel typed and regions to serve both base load

and peaking demand.

Solar/wind – 800MW (~ 325 MW commissioned & 500MW in pipeline)

Building low cost solar and wind power plants in India and

globally with an objective of meeting peaking power demand.

Thermal 4000mw in construction and advance deployment

Close to coal source and owned merchant coal mines

Low delivered cost of energy to key load centers.

Hydel – 1000MW

Key run of river hydel assets with large storage to meet seasonal

and evening peaking requirements.

Moser Baer has manufacturing facilities for high grade solar PV modules across

various technologies. Present manufacturing capacity of 170MW crystalline cell,

150 MW of Crystalline silicon modules, 50MW of thin film modules.

13 | P a g e

2. INTRODUCTION TO THE PROJECT

The goal of the report explores the opportunity of Solar Roof Top in India. This

report analyses

1. Generation potential

2. Policies or framework by Government of India

3. Economic viability of rooftop solar

4. Current status and future market size of rooftop solar

5. Technological developments

14 | P a g e

3. INTRODUCTION TO ROOFTOP SOLAR

3.1 WHAT IS ROOFTOP SOLAR

Rooftop solar power plants are those power plants which are present on the outer

surface of a building's roof and generate electricity using natural energy produced

by the sun.

The sub-segments in the Rooftop Solar Category can be defined into Medium and

small based on the capacity:

Medium Capacity: Rooftop Solar PV projects to be connected at HT

level (below 33 kW level) of distribution network with installed capacity

of 100 kW and up to 2 MW.

Small Capacity: Rooftop Solar PV projects connected at LT level of

distribution network with installed capacity lower than 100 kW.

3.2 TYPES OF ROOFTOP SOLAR

There are two types of Rooftop solar systems globally

1. Off grid rooftop solar

2. Grid interacted rooftop solar

3.3 Off grid Rooftop solar system

In the off grid type of solar system; the system is not interacted to the grid and

continuous reliable power supply is maintained through batteries.

The Energy produced by the solar module is used to charge the Lead Acid

Battery. The Load is powered using the energy stored in the battery through

Electronic circuitry.

15 | P a g e

The Electronic circuitry consists of Charge Control Unit and Inverter. The Charge

Control Unit is used to control the overcharging and deep discharging of the

battery, which in turn increases the Life of the battery. Inverter is used to convert

the DC to 230 V AC with 50 Hz Frequency.

In off grid roof top solar PV system, the system interacted to main bus but only in

one way transmission of electricity is possible from main bus to the building. If

there is any malfunctioning in the system by this connectivity continuous

reliable supply is maintained.

If the off grid electricity supply system is located where there is no grid

connectivity to the residential, commercial and for industrial use, at this area the

system is called as stand-alone power system (SAPS) or remote area power supply

system(RAPS).

Fig (i)

16 | P a g e

3.4. Grid Interacted Roof top solar system

In grid connected or interacted Rooftop solar PV system, solar modules will

convert solar energy into electricity in the form of direct current (DC).

The direct current produced in the system is converted to alternating current (AC)

by an inverter or by power conditioning unit.

From this the system is interacted to grid through AC distribution board. Output is

measured by a meter which is present at the grid.

Fig (ii)

There are two types metering system in Roof Top solar Grids interacted system.

They are

1. Net metering system

2. Feed in Tariff metering

17 | P a g e

3.5. Net metering system

Net metering is the one which allows two-way flow of electricity, where

consumer is billed only for the net electricity he has consumed from the

DISCOM.

3.6. Feed in Tariff metering

Feed-in-Tariff which is minimum guaranteed price per unit of produced electricity

as approved by the regulator, to be paid to the producer. In feed in Tariff metering

system they have two uni-directional meters one records the electricity drawn

from the grid and other records the excess energy generated and fed into the grid.

The source pays retail rate for the energy they used and the power provider

purchases their excess generation at its Feed in Tariff.

For example Maharashtra Electricity Regulatory Commission (MERC) has fixed a

price of Rs. 11.66/kWh and Gujarat Electricity Regulatory Commission (GERC)

has fixed it at Rs. 12.44/kWh as FiT.

18 | P a g e

4. Case studies

In India we have a total installed capacity of 18811.11MW under Solar PV. Out of

which 1686.44MW is grid interacted solar PV system and 124.67MW is off grid

solar PV system. Under Rooftop PV &Small Solar Generation Programme

(RPSSGP) we have achieved 88.25MW rooftop solar out of 98MW signed PPAs.

Below are list of 6 different case studies of net metering and FiT of both Grid

connected and Off Grid system.

19 | P a g e

4.1. Sewa Bhawan

Location : West block Area, R.K Puram, New Delhi

Client : Central Electricity Authority (CEA)

Type : Grid-interacted rooftop solar system

Metering system : FiT

Area covered : 331.5 Sq.Mts

System size : 25KW

Modules : 150

Technology : poly crystalline

Rooftop angle : 28.32 degrees south

Inverters : 1*27KWp

Output : 440 V, 50HZ, 3ph

Annual generation : 42000KWh

CUF : 19.2%

Cost of generation per kwh : RS 10.54

Installation cost : Rs42.5 lakhs

Levelised tariff per kWh : Rs18.45

EPC Cost per KW : 1.7 lakhs

20 | P a g e

Fig (iii)

21 | P a g e

4.2. Sri Nripendranath Girls High School

Client : Sri Nripendranath Girls High School

Location : Kudghat, kolkatta

Type : Grid interacted system

Metering system : Net metering system

Used for : lights, fans, computers

Project cost : Rs8 lakhs

Rooms : 26

System size : 12KW

Expected Generation : 19970KWh

22 | P a g e

4.3. Regen Power (Australia)

Location : New South Wales, Australia

Client : Smithfield

Type : Grid interacted system

Metering system : Net metering

EPC : Regen Power

Module : 400*250watts

Inverters : 6*SMA Tri power

CUF : 18%

System size : 100KW

Technology : polycrystalline

Rooftop angle : 30 degrees north

Annual electricity generation : 157000KWh

Carbon dioxide savings : 122 Metric Tons

Units Generated Annually (in Kwh) = System Size in Kw * CUF * 365 * 24

157000=100*CUF*365*24

CUF (Capacity Utilisation Factor) = 18%

23 | P a g e

Fig(iv)

24 | P a g e

4.4. Shashwat Green Fuels & Technologies (I) Pvt.

Location : Kapadvanj, Gujarat

EPC : Shashwat Green Fuels & Technologies (I)

Pvt.

Type : Off grid system

Batteries : 21series*2parllel

Rooftop angle : 33 degrees toward south

No of modules : 84*240W

System size : 20kWp

Annual Generation : 30,000 units

CUF : 19%

Inverters : one

Output : 3ph 415V 50Hz

Fig(v)

25 | P a g e

4.5. BSNL

Location : Shmila, Himachal pradesh

Client : Bharat Sanchar Nigam Ltd.

EPC : Gensol Consultants Pvt Ltd.

Type : Off-Grid system

Solar Potential : 5.05 kWh/ m2/ day

System size : 10KW

CUF : 19%

Annual Generation : 16,600 units

Rooftop angle : 30 degrees toward south

Total project cost : Rs21.5 lakhs

Fig(vi)

26 | P a g e

4.6. Azure Power

Location : Ghandinagar, Gujarat

Client : Households (Rooftop Owners)

EPC : Azure Power

Type : Grid Connected system

Solar Potential : 6.0 kWh/ m2/ day

System size : 2.5MW

CUF : 19%

Annual Generation : 4.61MU

FiT : Rs11.21/Kwh

Rent to Rooftop area : Rs3/KWh

Fig(vii)

27 | P a g e

5. Generation

The proposed Solar Photovoltaic Power plant operates on the principle of the

photoelectric phenomenon - direct conversion of light to electricity. The solar

radiation incident upon a silicon-based semiconductor photovoltaic cell produces

direct electric current. Photovoltaic cells are integrated into modules with a

voltage of 6 - 12 V; the electrically interconnected modules form solar systems

with an output voltage of 230 V. The 100 KWp Grid Feeding Power Plant is

designed to export 167 MWh/year, 415 V, 3-phase power to the local load,

considering efficiency of the solar module as 16%, Inverter/ Power Conditioning

Unit (PCU) as 94% and losses as 3% in the DC and AC system. The Plant would

operate at an annual capacity utilization factor of 19%.

The amount of energy generated by a Rooftop solar is mainly depending on

capacity utilisation factor and capacity of the system. The annual generation of a

rooftop system is calculated by

Units Generated Annually (in Kwh) = System Size in Kw * CUF * 365 * 24

Table1: Area required in sq.mts

PV Module Efficiency

(%)

PV Capacity Rating(Kilo Watts)

10 50 100 200 300 500 1000

4 278.

7

1393.

5

2787 5574 8361 1393

5

2787

0

8 139.

4

697 1394 2788 4182 6970 1394

0

12 92.9 464.5 929 1858 2787 4645 9290

16 74.3

2

371.6 743.

2

1486.

4

2229.

6

3716 7432

For example, a 12% efficient solar module of capacity 100000watts or 100KW

will require a area of 929 Sq.Mts.

28 | P a g e

Table2: Annual Electricity generation in KWh

For example, 100KW capacity solar module will produce 166440KWh of

electricity per annum at 19% CUF (Capacity Utilisation Factor).

Units Generated Annually (in Kwh) = System Size in Kw * CUF * 365 * 24

Units Generated=100*0.19*365*24=166440KWh

Pv rating

capacity in KW CUF

16 17 18 19 20

10 14016 14892 15768 16644 17520

50 70080 74460 78840 83220 87600

100 140160 148920 157680 166440 175200

200 280320 297840 315360 332880 350400

300 420480 446760 473040 499320 525600

500 700800 744600 788400 832200 876000

1000 1401600 1489200 1576800 1664400 1752000

29 | P a g e

6. Policies and Incentives

6.1. Central Policies

6.1.1. Rooftop PV & Small Solar Power Generation

Programme (RPSSGP)

Programme : Jawaharlal Nehru National Solar Mission, Phase 1

Voltage level : below 33KV

Determination of tariff : Respective SERC

Incentive : Generation Based Incentive or Accelerated

Depreciation

GBI paid by : Distribution utility for 25 years

Capacity : 100MW

HT capacity : 90MW (0.1 to 2MW)

LT capacity : 10MW (<100KW)

Administrator : IREDA

IREDA has selected 12 states namely Rajasthan, Madhya Pradesh, Andhra

Pradesh, Tamil Nadu, Maharashtra, Odisha, Uttar Pradesh, Punjab, Haryana,

Uttarakhand, Chhattisgarh and Jharkhand for 78 Rooftop projects to install of

98MW.

Financial incentives for Off-grid projects:

There is subsidy of 30% on capital expenditure in Off-grid projects of grid

connected areas till capacity of 100KW.

Where grid connection is not available it is applicable till 250KW.

Low interest rate loans were also provided to projects at 5% interest on 50%

capital expenditure for 5 years is available for off grid projects.

30 | P a g e

For non-commercial entity both of the incentives are applicable.

For commercial entities any one of the financial incentive either capital subsidy or

soft loan is applicable.

Table 3: Financial Incentives

S.No Particulars Capacity Subsidy

1 Individuals

A All applications except 1B 1KWp Capital

subsidy &

Soft loan B Pumps for irrigation & community drinking water 5KWp

2 Non Commercial Entities

A All applications except 2B 100KWp Capital

subsidy &

Soft loan B Mini grid for rural electrification 250KWp

3 Industrial/commercial entities

A All applications except 3B 100KWp Capital

subsidy or

soft loan B Mini grid for rural electrification 250KWp

Table 4: Present status for Rooftop PV& Small Solar Generation

Programme:

Present status of the Rooftop PV & Small Solar Generation Programme under

JNNSM Phase 1

STATE PP

A

Sig

ned

M

W

Commissi

oned MW

Bala

nce

MW

Industrial

Tariff(Rs/

Kwh)

Andhra

Pradesh

10.5 9.5 1.0 8.00

Chhattisg

arh

4.0 4.0 0 5.00

31 | P a g e

Haryana 8.8 7.8 1.0 5.70

Maharas

htra

5.0 5.0 0 8.50

Odisha 8.0 7.0 1.0 6.00

Punjab 8.5 6.0 2.5 6.91

Rajastha

n

12 10.0 2.0 7.00

Tamil

Nadu

7.0 5.0 2.0 7.00

Uttarakha

nd

5.0 5.0 0 5.00

Uttar

Pradesh

8.0 7.0 1.0 7.50

Jharkhan

d

16.0 16.0 0 4.50

Madhya

Pradesh

5.25 5.25 0 6.00

Total 98.0

5

87.80 10.25

6.1.2. JNNSM, Phase II:

Initiatives for Off-grid projects

Capacity : 25-100KW

Capital subsidy : 30% on capital expenditure

Bench mark cost : Rs81/W with battery backup and Rs57/W

for without battery

Debt: Equity ratio : 80:20

Low interest :5% for 5 years on 50% of capital

expenditure

Target Capacity : 200MW

Time period : 2013-1015

32 | P a g e

6.2 STATE POLICIES

6.2.1. West Bengal:

The state has initiated a net metering solar rooftop model promoting self-

consumption. The grid-integrated rooftop PV is allowed only for institutional

consumers like government departments, academic institutions, etc. The system

size limited to 2-100 kW. Connectivity is allowed at Low Voltage or Medium

Voltage, or 6 KV or 11 KV. Solar injection is permitted only up to 90% of the

annual electricity consumption, and the net energy supplied by the utility would

be billed as per existing slab tariffs. West Bengal Renewable Energy Policy,

buildings with a certain minimum load will have to 20 meet some electricity

needs through RTPV. The policy targets 16MWof rooftop and small PV

installations by 2017. These rooftop projects are getting 30% capital subsidy from

MNRE.

6.2.2. Gujarat:

The state has initiated a 5 MW rooftop PV programme based on a FiT /sale to

utility model. 4MWs of this would come up on government buildings, while 1

MW would be installed on private homes. Two projects each have been selected

through the process of reverse competitive bidding. The local utility, Torrent

Power, will purchase the entire solar power at the discovered price. Torrent

Power, a private utility, will buy power from Azure at 11.21 rupees per kilowatt-

hour for 25 years. Azure, in turn, will pass on 3 rupees per kilowatt-hour to

rooftop owners'. Thus, the effective price of solar without the rooftop rent is only

Rs8.21/kWh.

6.2.3. Karnataka:

The new Karnataka Renewable Energy Policy 2009-14, promotes rooftop PV with

net-metering. The system size range is 5-100 kWp, and interconnection at 415 V,

3phase or 11 kV. Maximum energy injection is allowed only up to 70% of the

33 | P a g e

customer’s energy usage from the DISCOM. The policy encourages rooftop PV

with a net-metering facility to feed surplus power to the grid. The policy is

targeted for 25000 Solar Roof Tops of 5 to 10 kWp with Net-Metering during the

next 5 years with net metering tariff value of Rs3.40/- with 30% capital subsidy

from MNRE.

6.2.4. Andhra Pradesh:

The state has initiated a net metering solar rooftop model for promoting self-

consumption. The state government is providing 50% capital subsidy on capital

expenditure (with combing 30% central subsidy). The system size is limited to

1KW. Special Purpose Vehicle Generators will pay cost of the excess power from

the rooftop at a fixed tariff of Rs3.50/-.

6.2.5. Tamil Nadu:

The state has recently released solar policy 2012, a target of 350 MWs of RTPV

to be installed in three years from 2013-15 has been approved. 50 MW of RTPV

would be supported through a generation based incentive (GBI) of Rs2/kWh for

the first two years, Re.1/kWh for the next two and Rs0.5/kWh for the subsequent

two years will be provided for all. State government is providing Rs20, 000/kw as

subsidy along with 30% capital subsidy from MNRE.

6.2.6. Chhattisgarh:

The state has initiated the Off-grid rooftop PV system with a target of 15MW on

private and public buildings. The tariff period for these systems is 25 years. These

projects are going to get 30% capital subsidy from MNRE. This has to be

achieved by 2017.

34 | P a g e

6.2.7. Kerala:

The state has initiated the 10000 rooftops with each capacity of 1KW. The state

has providing a subsidy of Rs39, 000/- per KW along with 30% capital subsidy

from MNRE for these projects. The state has a target of 10MW under this

programme. This policy is mainly applicable for Households and Cottage

industries.

35 | P a g e

7. Business Models

As we can see currently there are three types of business models that exists

1. Pure play EPC Model

2. Developer builds Rooftop solar with Net Metering

3. Feed in Tariff

This section explains above business models and its economics

7.1. Pure play EPC Model

This is basic model, where in an EPC player develops solar Rooftop. The key

players in the market are

1. L&T

2. Tata Solar

3. Moser Baer

4. Lanco

EPC Cost for 100KW

This table shows the cost involved while developing a rooftop solar PV system.

The capital subsidies taken by the owner or EPC depending on the contract or

negotiation.

Table5: EPC Cost for 100KW with subsidy

Particulars Cost in Lakhs Cost after subsidy in

Lakhs

Photovoltaic Module 36 25.2

Inverters 8 5.6

Module Mounting Cost 5.2 3.4

Building and Civil works 5.2 3.4

Isolation Transformer 4.6 3.0

Wires and Electricals 1 0.7

Engineering and Procurement

Management

1 0.7

Contingency 6 4

Total 67 46

36 | P a g e

7.2. Net Metering Tariffs:

This is a system where the developer develops the rooftop solar system and takes

net metering benefit.

We have already given the EPC cost with subsidies. Below are the Net Metering

Tariff in various states.

Table 6: Net metering tariff values of different states

State Consumer Tariff in

Rs/KWh

Industrial Tariff in

Rs/Kwh

Andhra Pradesh 4.15 8.00

Arunachal Pradesh 3.8 4.00

Assam 4.66 4.50

Bihar 3.85 7.00

Chhattisgarh 2.95 5.00

Delhi 4.92 8.50

Goa 2.00 4.00

Gujarat 4.75 5.00

Haryana 4.00 5.70

Himachal Pradesh 2.4 5.50

Jammu & Kashmir 2.60 3.60

Jharkhand 2.50 4.40

Karnataka 4.30 5.50

Kerala 4.00 4.60

Madhya Pradesh 6.60 6.30

Maharashtra 5.00 8.50

Manipur 3.40 4.00

Mizoram 3.70 3.20

Meghalaya 3.00 4.10

Nagaland 4.20 4.50

Odisha 3.60 6.00

Punjab 5.20 6.91

Rajasthan 4.80 7.00

Sikkim 2.60 4.50

Tamil Nadu 3.70 7.00

Tripura 3.70

Uttar Pradesh 4.40 7.50

Uttarakhand 2.80 4.70

West Bengal 5.70 7.32

37 | P a g e

7.3. Feed in Tariff or Grid Connected Tariff:

This is a system where the developer develops the rooftop solar and takes the

benefit of Feed in Tariff.

Below are the Feed in Tariff in various states.

Table 7: Feed in Tariff values of different stares

State Tariff in Rs/KWh Industrial Tariff

Gujarat 12.44 5.00

Maharashtra 11.66 8.50

Chhattisgarh 8.87 5.00

Rajasthan 9.63 7.00

Kerala 12.49 7.00

38 | P a g e

8. Target Market

8.1. Current installations:

At present we have total installed capacity of 88MW in solar Rooftop system.

This table and graph gives the year wise target installations in Rooftop solar

systems.

Year

Target Capacity in

MW

2010-2012 100

2012-2013 200

2013-2014 350

2014-2015 525

2015-2016 750

2016-2017 1000

Fig (viii)

X-axis in MW

Y-axis years

0

200

400

600

800

1000

1200

39 | P a g e

8.2. Future Installations for Roof Top Solar

This table shows the policies of central and state, their excepted capacity addition

and timeline along with subsidies provided by their governments.

Table 8: Future Installations in Rooftop

S.No Policies Expected

Capacity

addition in

MW

Timeline Subsidies

1 SECI 16.6 2017 30% capital subsidy from

MNRE

2 JNNSM phase

2

200

1000

2015

2017

30% capital subsidy from

MNRE

3 Gujarat 30 2017 Feed in Tariff of Rs12.44/KWh

4 Karnataka 25,000

Rooftops

2017 30% capital subsidy from

MNRE

5 Kerala 85,000

Rooftops

2017 30% capital subsidy from

MNRE.

Rs39000/system from state

government

6 Tamil Nadu 350 2015 30% capital subsidy from

MNRE.

Rs20, 000/KW from state

government.

GBI of Rs2/KWh for first 2

years

Rs1/KWh for next 2 tears

Rs0.50/KWh for next 2 years

7 Chhattisgarh 15 2017 30% capital subsidy from

MNRE

8 West Bengal 16 2017 30% capital subsidy from

MNRE

9 Andhra Pradesh 30% capital subsidy from

MNRE.

20% capital subsidy from state.

government

Rs3.50/KWh as Net Metering

Tariff.

10 Maharashtra Feed in Tariff of Rs11.66/KWh

11 Rajasthan Feed in Tariff of Rs9.63/KWh

40 | P a g e

Table 9: Comparison of Rooftop Schemes of states

41 | P a g e

Table 10: RPSSGP targets under JNNSM Phase2

S.No State Target in MW Industrial Tariff

(Rs/KWh)

1 Arunachal Pradesh 1

2 Assam 5 5.00

3 Bihar 3 7.00

4 Delhi 5 8.50

5 Goa & Uttarakhand 5 5.00

6 Gujarat 5 5.00

7 Himachal Pradesh 5 5.50

8 Jammu & Kashmir 5 4.00

9 Karnataka 5 5.70

10 Kerala 5 4.70

11 Manipur 1 4.00

12 Mizoram 1 3.50

13 Meghalaya 3 4,20

14 Nagaland 1 4.30

15 Sikkim 1 4.50

16 Tripura 1.5

17 West Bengal 5 7.32

Total 59.5

Based on the relived, we feel that Rooftops solar is most attractive in the following

states

1. Gujarat: They are providing FiT along with rooftop rent.

2. Kerala: They are providing subsidy for small households along with MNRE

subsidies.

3. Andhra Pradesh: They are providing Net metering tariff along with MNRE

subsidy.

4. Tamil Nadu: They are providing state subsidy along with MNRE incentives

including GBI.

5. Karnataka: They are providing Net metering tariff along with MNRE subsidies.

42 | P a g e

9. Technology

A solar PV system mainly powered by crystalline or thin film PV modules.

Crystalline is basically divided into two type mono and poly crystalline. The

family tree of PV cell types is shown below.

Fig (ix)

Crystalline Silicon Technology

Crystalline silicon (c-Si) made of ultra-pure silicon material of one fifth of

millimetre size.

Mono crystalline, produced by slicing wafers (up to 150mm diameter and 350

microns thick) from a high-purity single crystal

Multi crystalline silicon is made by sawing a cast block of silicon first into bars

and then wafers. The main trend in crystalline silicon cell manufacture is toward

multi crystalline technology.

Thin film Technology

The materials costs are significantly reduced. The thin film semiconductor layers

are deposited on to either coated glass or stainless steel sheet.

Solar PV Technology

Crystalline Silicon

Mono Crystalline

Poly Crystalline

Thin film

Amorphous Silicon a-si

Cadmium Telluride

Copper Indium(Gallium)

Diselenide

43 | P a g e

Amorphous silicon

It is the well-developed of the thin film technologies. Thin film cells are laminated

to produce a weather resistant and environmentally robust module. They can

reduce the cost by as much as 60% of C-Si. Amorphous silicon has an interesting

avenue of further development through the use of "microcrystalline" silicon

which seeks to combine the stable high efficiencies of crystalline Si technology

with the simpler and cheaper large area deposition technology of amorphous

silicon.

However, conventional C-Si manufacturing technology has continued its steady

improvement year by year and its production costs are still falling too. Thin films

have long held a niche position in low power (<50W) and consumer electronics

applications, and may offer particular design options for building integrated

applications.

Fig (x)

44 | P a g e

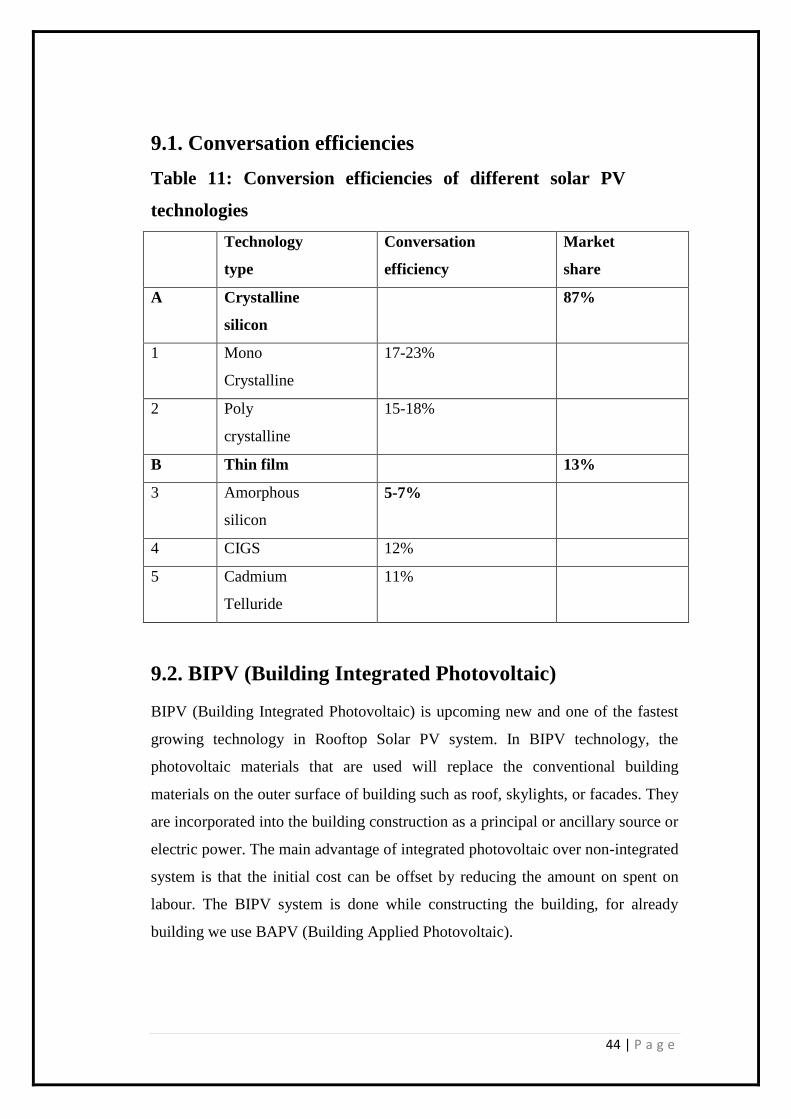

9.1. Conversation efficiencies

Table 11: Conversion efficiencies of different solar PV

technologies

Technology

type

Conversation

efficiency

Market

share

A Crystalline

silicon

87%

1 Mono

Crystalline

17-23%

2 Poly

crystalline

15-18%

B Thin film 13%

3 Amorphous

silicon

5-7%

4 CIGS 12%

5 Cadmium

Telluride

11%

9.2. BIPV (Building Integrated Photovoltaic)

BIPV (Building Integrated Photovoltaic) is upcoming new and one of the fastest

growing technology in Rooftop Solar PV system. In BIPV technology, the

photovoltaic materials that are used will replace the conventional building

materials on the outer surface of building such as roof, skylights, or facades. They

are incorporated into the building construction as a principal or ancillary source or

electric power. The main advantage of integrated photovoltaic over non-integrated

system is that the initial cost can be offset by reducing the amount on spent on

labour. The BIPV system is done while constructing the building, for already

building we use BAPV (Building Applied Photovoltaic).

45 | P a g e

9.3. CASE STUDY

Client : Glass manufacturing plant

Location : Bengaluru

Solar potential : 259KWp

Technology : poly and mono-crystalline

EPC : Emmvee Photovoltaic Power Pvt Ltd.

Module angle : 65 degrees to south

No of modules : 169*230Wp

Fig (xi)

46 | P a g e

10. Financial Viability of Rooftop solar with

subsidy and FiT

10.1 Financial viability of Rooftop Solar with Subsidy

In this financial viability of solar rooftop, we have taken the subsidy into account

along with APPC. All the assumptions we have taken from the CERC and from

MNRE.

10.1.1. P&L sheet of subsidised solar rooftop system

Table 12: P&L sheet of subsidised rooftop

Particulars Year 1 2 3 4 5 6 7 8

Months Operations 6 12 12 12 12 12 12 12

Units Generated KWh

83,012

1,65,19

4

1,64,36

8

1,63,54

6

1,62,72

8

1,61,91

5

1,61,10

5

1,60,30

0

Tariff Rs/KWh 4.92 5.17 5.42 5.70 5.98 6.28 6.59 6.92

Revenues

Rs

Lakhs 4.08 8.53 8.92 9.31 9.73 10.17 10.62 11.10

Revenues

Rs

Lakhs 4.08 8.53 8.92 9.31 9.73 10.17 10.62 11.10

O&M Rs Lakhs 0.40 0.84 0.88 0.93 0.97 1.02 1.07 1.13

EBTID

Rs

Lakhs 3.68 7.69 8.03 8.39 8.76 9.15 9.55 9.97

EBTID Rs Lakhs 3.68 7.69 8.03 8.39 8.76 9.15 9.55 9.97

Interest on Debt

Rs

Lakhs 4.47 4.14 3.76 3.39 3.01 2.63 2.26 1.88

Interest on WC Rs Lakhs 0.20 0.23 0.24 0.25 0.26 0.27 0.28 0.30

Dep

Rs

Lakhs 1.45 2.89 2.89 2.89 2.89 2.89 2.89 2.89

EBT

Rs

Lakhs

-2.43 0.43 1.14 1.86 2.59 3.35 4.11 4.90

-2.43 -2.00 -0.86 0.99 3.59 6.93 4.11 4.90

EBT

Rs

Lakhs 0.00 0.00 0.00 0.99 3.59 6.93 4.11 4.90

Tax

Rs

Lakhs 0.00 0.00 0.00 0.20 0.72 1.39 0.82 0.98

PAT

Rs

Lakhs 0.00 0.00 0.00 0.80 2.87 5.55 3.29 3.92

Cum.P&L

Rs

Lakhs 0.00 0.00 0.00 0.80 3.67 9.21 12.50 16.42

47 | P a g e

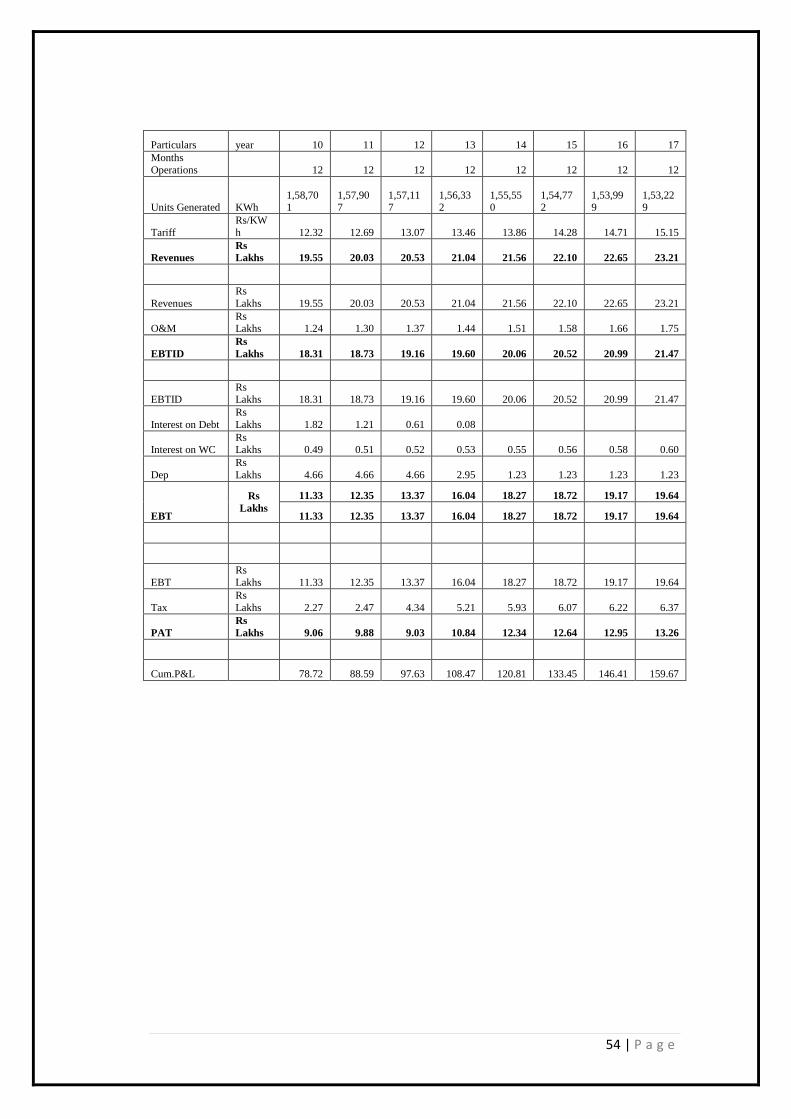

Particulars Year 9 10 11 12 13 14 15 16 17

Months

Operations 12 12 12 12 12 12 12 12 12

Units

Generated KWh

1,59,4

98

1,58,7

01

1,57,9

07

1,57,1

17

1,56,3

32

1,55,5

50

1,54,7

72

1,53,9

99

1,53,2

29

Tariff Rs/KWh 7.27 7.63 8.01 8.41 8.84 9.28 9.74 10.23 10.74

Revenues

Rs

Lakhs 11.59 12.11 12.65 13.22 13.81 14.43 15.08 15.75 16.46

Revenues Rs Lakhs 11.59 12.11 12.65 13.22 13.81 14.43 15.08 15.75 16.46

O&M

Rs

Lakhs 1.18 1.24 1.30 1.37 1.44 1.51 1.58 1.66 1.75

EBTID

Rs

Lakhs 10.41 10.87 11.35 11.85 12.38 12.92 13.49 14.09 14.71

EBTID

Rs

Lakhs 10.41 10.87 11.35 11.85 12.38 12.92 13.49 14.09 14.71

Interest on

Debt

Rs

Lakhs 1.51 1.13 0.75 0.38 0.05

Interest on WC

Rs

Lakhs 0.31 0.33 0.34 0.36 0.37 0.39 0.41 0.43 0.44

Dep

Rs

Lakhs 2.89 2.89 2.89 2.89 1.83 0.77 0.77 0.77 0.77

EBT

Rs

Lakhs

5.70 6.52 7.36 8.23 10.13 11.77 12.32 12.90 13.50

5.70 6.52 7.36 8.23 10.13 11.77 12.32 12.90 13.50

EBT

Rs

Lakhs 5.70 6.52 7.36 8.23 10.13 11.77 12.32 12.90 13.50

Tax

Rs

Lakhs 1.14 1.31 1.47 1.65 2.03 3.82 4.00 4.18 4.38

PAT

Rs

Lakhs 4.56 5.22 5.89 6.58 8.10 7.95 8.32 8.71 9.12

Cum.P&L Rs Lakhs 20.98 26.20 32.09 38.67 46.77 54.72 63.05 71.76 80.88

48 | P a g e

Particulars Year 18 19 20 21 22 23 24 25 26

Months

Operations 12 12 12 12 12 12 12 12 6

Units Generated KWh

1,52,462

1,51,700

1,50,942

1,50,187

1,49,436

1,48,689

1,47,945

1,47,206

73,235

Tariff

Rs/K

Wh 11.28 11.84 12.43 13.05 13.71 14.39 15.11 15.87 16.66

Revenues

Rs

Lakhs 17.19 17.96 18.77 19.61 20.48 21.40 22.36 23.36 12.20

Revenues

Rs

Lakhs 17.19 17.96 18.77 19.61 20.48 21.40 22.36 23.36 12.20

O&M Rs Lakhs 1.83 1.93 2.02 2.12 2.23 2.34 2.46 2.58 1.35

EBTID

Rs

Lakhs 15.36 16.04 16.74 17.48 18.25 19.06 19.90 20.78 10.85

EBTID Rs Lakhs 15.36 16.04 16.74 17.48 18.25 19.06 19.90 20.78 10.85

Interest on

Debt

Rs

Lakhs

Interest on WC

Rs Lakhs 0.47 0.49 0.51 0.53 0.56 0.58 0.61 0.64 0.33

Dep

Rs

Lakhs 0.77 0.77 0.77 0.77 0.77 0.77 0.77 0.77 0.38

EBT

Rs

Lakhs

14.13 14.79 15.47 16.19 16.93 17.71 18.53 19.38 10.13

14.13 14.79 15.47 16.19 16.93 17.71 18.53 19.38 10.13

EBT

Rs

Lakhs 14.13 14.79 15.47 16.19 16.93 17.71 18.53 19.38 10.13

Tax

Rs

Lakhs 4.58 4.80 5.02 5.25 5.49 5.75 6.01 6.29 3.29

PAT

Rs

Lakhs 9.54 9.99 10.45 10.93 11.44 11.97 12.52 13.09 6.84

Cum.P&L

Rs

Lakhs 90.42

100.4

1 110.9 121.8 133.2 145.2 157.7 170.8 177.7

49 | P a g e

10.1.2. Cash flows of subsidised solar rooftop

Table 13: Cash flows of subsidised rooftop system

Particulars Year

Dec-

13

Dec-

14

Dec-

15

Dec-

16

Dec-

17

Dec-

18

Dec-

19

Dec-

20

Dec-

21

EBTID

Rs

Lakhs 3.68 7.69 8.03 8.39 8.76 9.15 9.55 9.97 10.41

Interest on Debt

Rs

Lakhs 4.47 4.14 3.76 3.39 3.01 2.63 2.26 1.88 1.51

Interest on Wc

Rs

Lakhs 0.20 0.23 0.24 0.25 0.26 0.27 0.28 0.30 0.31

Loan Repayment

Rs

Lakhs 1.45 2.90 2.90 2.90 2.90 2.90 2.90 2.90 2.90

Net Cash Flows before

Tax

Rs

Lakhs -2.43 0.43 1.14 1.86 2.59 3.34 4.11 4.90 5.70

Net Cash Flows Before Tax

Rs Lakhs -2.43 0.43 1.14 1.86 2.59 3.34 4.11 4.90 5.70

Tax

Rs

Lakhs 0.00 0.00 0.00 0.20 0.72 1.39 0.82 0.98 1.14

Net Cash Flows After

Tax -14.89

-

17.32 0.43 1.14 1.66 1.87 1.96 3.29 3.92 4.56

Cash

Rs

Lakhs -2.43 0.43 1.14 1.66 1.87 1.96 3.29 3.92 4.56

Cash in Bank Rs Lakhs -2.43 -2.00 -0.87 0.79 2.66 4.62 7.91 11.83 16.38

Cumm Cash

Rs

Lakhs 0 0 0 0.79 2.66 4.62 7.91 11.83 16.38

Particulars Year

Dec-

22

Dec-

23

Dec-

24

Dec-

25

Dec-

26

Dec-

27

Dec-

28

Dec-

29

EBTID

Rs

Lakhs 10.87 11.35 11.85 12.38 12.92 13.49 14.09 14.71

Interest on Debt Rs Lakhs 1.13 0.75 0.38 0.05 0.00 0.00 0.00 0.00

Interest on Wc Rs Lakhs 0.33 0.34 0.36 0.37 0.39 0.41 0.43 0.44

Loan Repayment Rs Lakhs 2.90 2.90 2.90 1.45 0.00 0.00 0.00 0.00

Net Cash Flows before

Tax

Rs

Lakhs 6.52 7.36 8.23 10.51 12.53 13.09 13.66 14.27

Net Cash Flows Before

Tax Rs Lakhs 6.52 7.36 8.23 10.51 12.53 13.09 13.66 14.27

Tax Rs Lakhs 1.31 1.47 1.65 2.03 3.82 4.00 4.18 4.38

Net Cash Flows After

Tax

5.22 5.89 6.58 8.48 8.72 9.09 9.48 9.89

Cash

Rs

Lakhs 5.22 5.89 6.58 8.48 8.72 9.09 9.48 9.89

Cash in Bank Rs Lakhs 21.60 27.49 34.07 42.55 51.27 60.36 69.83 79.72

Cumm Cash Rs Lakhs 21.60 27.49 34.07 42.55 51.27 60.36 69.83 79.72

50 | P a g e

Particulars Year

Dec-

30

Dec-

31

Dec-

32

Dec-

33

Dec-

34

Dec-

35

Dec-

36

Dec-

37

Dec-

38

EBTID

Rs

Lakhs 15.36 16.04 16.74 17.48 18.25 19.06 19.90 20.78 10.85

Interest on Debt

Rs

Lakhs 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Interest on Wc Rs Lakhs 0.47 0.49 0.51 0.53 0.56 0.58 0.61 0.64 0.33

Loan Repayment

Rs

Lakhs 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Net Cash Flows before

Tax

Rs

Lakhs 14.89 15.55 16.24 16.95 17.70 18.48 19.29 20.14 10.51

Net Cash Flows Before

Tax

Rs

Lakhs 14.89 15.55 16.24 16.95 17.70 18.48 19.29 20.14 10.51

Tax Rs Lakhs 4.58 4.80 5.02 5.25 5.49 5.75 6.01 6.29 3.29

Net Cash Flows After

Tax

10.31 10.75 11.22 11.70 12.20 12.73 13.28 13.86 7.23

Cash

Rs

Lakhs 10.31 10.75 11.22 11.70 12.20 12.73 13.28 13.86 7.23

Cash in Bank

Rs

Lakhs 90.03

100.7

8

112.0

0

123.7

0

135.9

0

148.6

3

161.9

1

175.7

7

183.0

0

Cumm Cash Rs Lakhs 90.03

100.78

112.00

123.70

135.90

148.63

161.91

175.77

183.00

IRR-19%

10.1.3. IRR sensitivity

Table 14: IRR sensitivity of Cap Ex with Tariff

Cap Ex excluding Subsidy

Ta

riff

42 44 46 48 50 52

3.00 11.2% 10.5% 9.9% 9.3% 8.7% 8.2%

3.50 14.3% 13.5% 12.7% 12.0% 11.4% 10.8%

4.00 17.4% 16.4% 15.5% 14.7% 14.0% 13.3%

4.50 20.7% 19.5% 18.4% 17.5% 16.6% 15.8%

5.00 24.1% 22.7% 21.4% 20.3% 19.3% 18.3%

5.50 27.8% 26.1% 24.6% 23.2% 22.0% 21.0%

6.00 31.8% 29.7% 28.0% 26.4% 25.0% 23.7%

51 | P a g e

Table 15: IRR sensitivity of Cap Ex with interest rate

Cap Ex Excluding Subsidy

Inte

rest

Ra

te

42 44 46 48 50 52

10% 26% 24% 23% 22% 21% 20%

11% 25% 24% 22% 21% 20% 19%

12% 24% 23% 22% 20% 19% 18%

13% 24% 22% 21% 20% 19% 18%

14% 23% 21% 20% 19% 18% 17%

15% 22% 21% 20% 19% 18% 17%

16% 21% 20% 19% 18% 17% 16%

52 | P a g e

10.2 Financial viability of rooftop solar with FiT

These viability sheets we have taken into consider the feed in tariff system where

the value of FiT is 12.44Rs/KWh out of which 3Rs/KWh is paid to rooftop owner.

The remaining amount is taken by the developer

10.2.1. P&L sheet of rooftop solar of FiT

Table 16: P&L sheet of rooftop solar of FiT

53 | P a g e

Particulars Year 1 2 3 4 5 6 7 8 9

Months

Operations 6 12 12 12 12 12 12 12 12

Units Generated KWh

83,012

1,65,194

1,64,368

1,63,546

1,62,728

1,61,915

1,61,105

1,60,300

1,59,498

Tariff

Rs/KW

h 9.44 9.72 10.01 10.32 10.62 10.94 11.27 11.61 11.96

Revenues

Rs

Lakhs 7.84 16.06 16.46 16.87 17.29 17.72 18.16 18.61 19.07

Revenues

Rs

Lakhs 7.84 16.06 16.46 16.87 17.29 17.72 18.16 18.61 19.07

O&M Rs Lakhs 0.40 0.84 0.88 0.93 0.97 1.02 1.07 1.13 1.18

EBTID

Rs

Lakhs 7.44 15.22 15.58 15.94 16.32 16.70 17.09 17.49 17.89

EBTID Rs Lakhs 7.44 15.22 15.58 15.94 16.32 16.70 17.09 17.49 17.89

Interest on

Debt

Rs

Lakhs 7.21 6.67 6.07 5.46 4.85 4.25 3.64 3.03 2.43

Interest on WC

Rs Lakhs 0.37 0.40 0.41 0.42 0.43 0.44 0.45 0.47 0.48

Dep

Rs

Lakhs 2.33 4.66 4.66 4.66 4.66 4.66 4.66 4.66 4.66

EBT

Rs

Lakhs

-2.47 3.49 4.44 5.40 6.37 7.34 8.33 9.32 10.32

-2.47 1.02 5.45 10.85 17.22 24.57 8.33 9.32 10.32

EBT

Rs

Lakhs 0.00 1.02 5.45 10.85 17.22 24.57 8.33 9.32 10.32

Tax

Rs

Lakhs 0.00 0.20 1.09 2.17 3.45 4.92 1.67 1.86 2.06

PAT

Rs

Lakhs 0.00 0.81 4.36 8.68 13.78 19.65 6.66 7.46 8.26

Cum.P&L 0.00 0.81 5.18 13.86 27.63 47.29 53.95 61.40 69.66

54 | P a g e

Particulars year 10 11 12 13 14 15 16 17

Months

Operations 12 12 12 12 12 12 12 12

Units Generated KWh

1,58,701

1,57,907

1,57,117

1,56,332

1,55,550

1,54,772

1,53,999

1,53,229

Tariff

Rs/KW

h 12.32 12.69 13.07 13.46 13.86 14.28 14.71 15.15

Revenues

Rs

Lakhs 19.55 20.03 20.53 21.04 21.56 22.10 22.65 23.21

Revenues

Rs

Lakhs 19.55 20.03 20.53 21.04 21.56 22.10 22.65 23.21

O&M Rs Lakhs 1.24 1.30 1.37 1.44 1.51 1.58 1.66 1.75

EBTID

Rs

Lakhs 18.31 18.73 19.16 19.60 20.06 20.52 20.99 21.47

EBTID Rs Lakhs 18.31 18.73 19.16 19.60 20.06 20.52 20.99 21.47

Interest on Debt

Rs

Lakhs 1.82 1.21 0.61 0.08

Interest on WC Rs Lakhs 0.49 0.51 0.52 0.53 0.55 0.56 0.58 0.60

Dep

Rs

Lakhs 4.66 4.66 4.66 2.95 1.23 1.23 1.23 1.23

EBT

Rs

Lakhs

11.33 12.35 13.37 16.04 18.27 18.72 19.17 19.64

11.33 12.35 13.37 16.04 18.27 18.72 19.17 19.64

EBT

Rs

Lakhs 11.33 12.35 13.37 16.04 18.27 18.72 19.17 19.64

Tax

Rs

Lakhs 2.27 2.47 4.34 5.21 5.93 6.07 6.22 6.37

PAT

Rs

Lakhs 9.06 9.88 9.03 10.84 12.34 12.64 12.95 13.26

Cum.P&L 78.72 88.59 97.63 108.47 120.81 133.45 146.41 159.67

55 | P a g e

Particulars year 18 19 20 21 22 23 24 25 26

Months

Operations 12 12 12 12 12 12 12 12 6

Units Generated KWh

1,52,462

1,51,700

1,50,942

1,50,187

1,49,436

1,48,689

1,47,945

1,47,206

73,235

Tariff

Rs/KW

h 15.60 16.07 16.55 17.05 17.56 18.09 18.63 19.19 19.77

Revenues

Rs

Lakhs 23.79 24.38 24.99 25.61 26.24 26.89 27.56 28.25 14.48

Revenues

Rs

Lakhs 23.79 24.38 24.99 25.61 26.24 26.89 27.56 28.25 14.48

O&M Rs Lakhs 1.83 1.93 2.02 2.12 2.23 2.34 2.46 2.58 1.35

EBTID

Rs

Lakhs 21.95 22.45 22.96 23.48 24.01 24.55 25.11 25.67 13.12

EBTID Rs Lakhs 21.95 22.45 22.96 23.48 24.01 24.55 25.11 25.67 13.12

Interest on

Debt

Rs

Lakhs

Interest on WC

Rs Lakhs 0.61 0.63 0.65 0.67 0.69 0.71 0.73 0.75 0.38

Dep

Rs

Lakhs 1.23 1.23 1.23 1.23 1.23 1.23 1.23 1.23 0.62

EBT

Rs

Lakhs

20.11 20.59 21.08 21.58 22.09 22.62 23.15 23.69 12.12

20.11 20.59 21.08 21.58 22.09 22.62 23.15 23.69 12.12

EBT

Rs

Lakhs 20.11 20.59 21.08 21.58 22.09 22.62 23.15 23.69 12.12

Tax

Rs

Lakhs 6.52 6.68 6.84 7.00 7.17 7.34 7.51 7.69 3.93

PAT

Rs

Lakhs 13.58 13.91 14.24 14.58 14.93 15.28 15.64 16.00 8.19

Cum.P&L 173.25 187.16 201.41 215.99 230.91 246.19 261.83 277.83 286.02

56 | P a g e

10.2.2. Cash flows of FiT viable sheet

Table 17: Cash flows of FiT viable sheet

Particulars Year

Dec-

13

Dec-

14

Dec-

15

Dec-

16

Dec-

17

Dec-

18

Dec-

19

Dec-

20

Dec-

21

EBTID

Rs

Lakhs 7.44 15.22 15.58 15.94 16.32 16.70 17.09 17.49 17.89

Interest on Debt

Rs

Lakhs 7.21 6.67 6.07 5.46 4.85 4.25 3.64 3.03 2.43

Interest on Wc Rs Lakhs 0.37 0.40 0.41 0.42 0.43 0.44 0.45 0.47 0.48

Loan Repayment

Rs

Lakhs 2.33 4.67 4.67 4.67 4.67 4.67 4.67 4.67 4.67

Net Cash Flows before

Tax

Rs

Lakhs -2.47 3.48 4.44 5.40 6.37 7.34 8.33 9.32 10.32

Net Cash Flows Before

Tax

Rs

Lakhs -2.47 3.48 4.44 5.40 6.37 7.34 8.33 9.32 10.32

Tax Rs Lakhs 0.00 0.20 1.09 2.17 3.45 4.92 1.67 1.86 2.06

Net Cash Flows After

Tax -24.00

-

26.48 3.28 3.35 3.23 2.92 2.43 6.66 7.45 8.25

Cash

Rs

Lakhs -2.47 3.28 3.35 3.23 2.92 2.43 6.66 7.45 8.25

Cash in Bank

Rs

Lakhs -2.47 0.81 4.15 7.38 10.30 12.72 19.38 26.84 35.09

Particulars Year

Dec-

22

Dec-

23

Dec-

24

Dec-

25

Dec-

26

Dec-

27

Dec-

28

Dec-

29

EBTID

Rs

Lakhs 18.31 18.73 19.16 19.60 20.06 20.52 20.99 21.47

Interest on Debt Rs Lakhs 1.82 1.21 0.61 0.08 0.00 0.00 0.00 0.00

Interest on Wc Rs Lakhs 0.49 0.51 0.52 0.53 0.55 0.56 0.58 0.60

Loan Repayment Rs Lakhs 4.67 4.67 4.67 2.33 0.00 0.00 0.00 0.00

Net Cash Flows before

Tax

Rs

Lakhs 11.33 12.34 13.37 16.66 19.51 19.95 20.41 20.87

Net Cash Flows Before Tax Rs Lakhs 11.33 12.34 13.37 16.66 19.51 19.95 20.41 20.87

Tax Rs Lakhs 2.27 2.47 4.34 5.21 5.93 6.07 6.22 6.37

Net Cash Flows After

Tax

9.06 9.87 9.03 11.45 13.58 13.88 14.18 14.50

Cash

Rs

Lakhs 9.06 9.87 9.03 11.45 13.58 13.88 14.18 14.50

Cash in Bank Rs Lakhs 44.15 54.02 63.05 74.50 88.08 101.96 116.14 130.64

57 | P a g e

Particulars Year

Dec-

30

Dec-

31

Dec-

32

Dec-

33

Dec-

34

Dec-

35

Dec-

36

Dec-

37

Dec-

38

EBTID

Rs

Lakhs 21.95 22.45 22.96 23.48 24.01 24.55 25.11 25.67 13.12

Interest on Debt

Rs

Lakhs 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Interest on Wc Rs Lakhs 0.61 0.63 0.65 0.67 0.69 0.71 0.73 0.75 0.38

Loan Repayment

Rs

Lakhs 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Net Cash Flows before

Tax

Rs

Lakhs 21.34 21.82 22.32 22.82 23.33 23.85 24.38 24.92 12.74

Net Cash Flows Before

Tax

Rs

Lakhs 21.34 21.82 22.32 22.82 23.33 23.85 24.38 24.92 12.74

Tax Rs Lakhs 6.52 6.68 6.84 7.00 7.17 7.34 7.51 7.69 3.93

Net Cash Flows After

Tax

14.82 15.14 15.48 15.81 16.16 16.51 16.87 17.24 8.80

Cash

Rs

Lakhs 14.82 15.14 15.48 15.81 16.16 16.51 16.87 17.24 8.80

Cash in Bank

Rs

Lakhs

145.4

6

160.6

0

176.0

8

191.8

9

208.0

5

224.5

6

241.4

3

258.6

7

267.4

8

IRR-21%

58 | P a g e

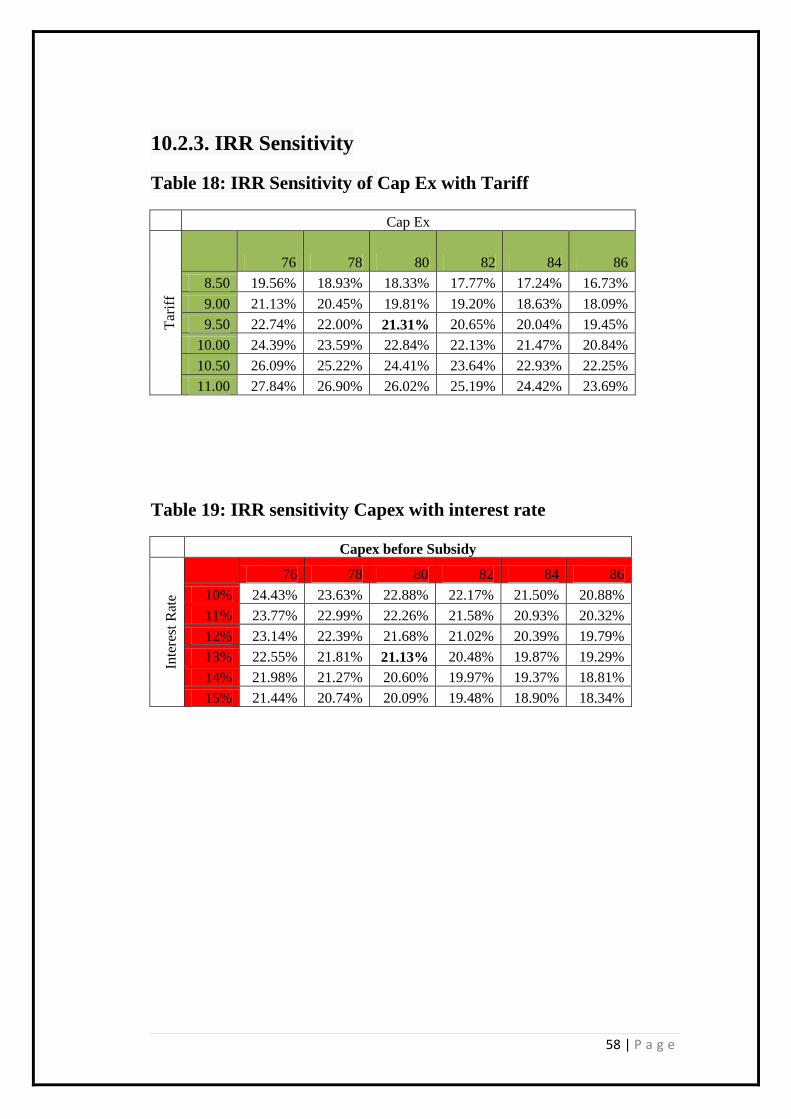

10.2.3. IRR Sensitivity

Table 18: IRR Sensitivity of Cap Ex with Tariff

Cap Ex

Tar

iff

76 78 80 82 84 86

8.50 19.56% 18.93% 18.33% 17.77% 17.24% 16.73%

9.00 21.13% 20.45% 19.81% 19.20% 18.63% 18.09%

9.50 22.74% 22.00% 21.31% 20.65% 20.04% 19.45%

10.00 24.39% 23.59% 22.84% 22.13% 21.47% 20.84%

10.50 26.09% 25.22% 24.41% 23.64% 22.93% 22.25%

11.00 27.84% 26.90% 26.02% 25.19% 24.42% 23.69%

Table 19: IRR sensitivity Capex with interest rate

Capex before Subsidy

Inte

rest

Rat

e

76 78 80 82 84 86

10% 24.43% 23.63% 22.88% 22.17% 21.50% 20.88%

11% 23.77% 22.99% 22.26% 21.58% 20.93% 20.32%

12% 23.14% 22.39% 21.68% 21.02% 20.39% 19.79%

13% 22.55% 21.81% 21.13% 20.48% 19.87% 19.29%

14% 21.98% 21.27% 20.60% 19.97% 19.37% 18.81%

15% 21.44% 20.74% 20.09% 19.48% 18.90% 18.34%

59 | P a g e

11. Challenges

11.1. Availability of rooftop – While the number of rooftops in the country is

very high, a big part of them are not suitable for installing PV systems.

11.2. Financial - The high upfront investment is often a major deterrent in rooftop

PV deployment.

11.3. Regulatory/policy

At present, only capital subsidies and tax benefits in the form of accelerated

depreciation are provided for PV systems (up to 500kWp).

The process of getting approval for the projects and getting the capital subsidy

disbursed takes long time. The slow turn-around times and some uncertainty about

getting the payments is a challenge in adoption of the rooftop PV.

11.4. Infrastructural

Implementing a Feed-in-Tariff system for rooftop PV, along the lines of major

European countries, is a powerful mechanism to stimulate growth in this segment.

However, challenges like prevention of abuse of the mechanism like feeding in

power to the grid from cheaper source of power (perhaps subsidized kerosene)

and getting higher feed-in-tariff needs to be addressed in order to make this model

successful. In fact, the Government of Delhi had to scrap its rooftop policy

because of the perceived challenge in this area.

In addition to these issues, Pune based Think-tank Prayas group has come up with

a study that highlights the challenges in implementing a Feed-in-Tariff approach

which include:

Higher burden on utility – due to the smaller sizes of rooftop PV (RTPV),

the unit cost of electricity from these systems tend to be higher, making

60 | P a g e

power purchase from them uncompetitive in comparison to power

purchase from utility scale projects.

Difficulty in estimating FiT – With the rapid fall in PV system prices,

arriving at a FiT has been a challenge not only for utility scale projects,

but also for RTPV.

The study argues that due to these challenges in the FiT based approach, a net-

metering based approach, as adapted by the Tamil Nadu Solar policy should be

promoted. In order to promote net-metering, the study recommends the following

steps.

Progressively increase the tariff for high-end consumption in residential

and commercial sectors, thereby bringing RTPV power generation cost

close to the price of grid-electricity.

Provide interconnection to the grid and banking facility for rooftop PV

systems.

Instead of providing payouts for the net electricity exported to the grid, the

credit can be rolled over to the next billing cycle and upto a year.

11.5. Other Challenges

Structural Constraints: Roofs of a certain age or construction may be

less desirable for a solar installation and may require a significant

refurbishment before such an installation is possible. Ideal conditions

include roofs with 10-20 years remaining before significant maintenance

or overhaul is required.

Limit on single phase generation: If there are many such micro

generators (as we can call small solar PV panel installations) and their

supply is not balanced among the phases, the network can become

imbalanced.

Quality of electricity: There are strict criteria so that having multiple

generation sources does not impact the quality of electricity available in

61 | P a g e

the grid. This includes the issue of harmonics (distortion of the Sine wave

AC signal) and EMC (Electromagnetic Compatibility) requirements.

62 | P a g e

12. Conclusion & Recommendations:

Rooftop solar under subsidy scheme

APPC tariff to industries is at Rs7/- in states Andhra Pradesh, Delhi,

Maharashtra, Tamil Nadu, and Rajasthan. Considering a project cost of

Rs7cr/MW will get an attractive IRR of 19%-22%, hence would

recommend Moser Baer to target industries under Rooftop subsidy in these

states Andhra Pradesh, Delhi, Tamil Nadu, Maharashtra and Rajasthan.

Feed in Tariff

Under FiT only Gujarat has come out with a tariff of Rs12.44/KWh which

gives a healthy return on investment of 22%

Project levers

For every 10% decrease in project cost we can see IRR increase of 2.5%

For every 1% change in interest rate we can see IRR jump of 0.5%.

I believe rooftop solar is currently is an immediate opportunity in the

Indian solar space and would recommend Moser Bare to invest in this

sector in big way. Considering attractive returns of 20% plus.

63 | P a g e

13. BIBILOGRAPHY

http://wberc.org

http://www.gercin.org

http://aperc.gov.in

http://www.kerc.org

http://cserc.gov.in

http://www.cercind.gov.in

http://www.cea.nic.in

http://www.mnre.gov.in

http://www.re-solve.in

http://seci.gov.in/content/

http://tnerc.tn.nic.in

http://www.eai.in

http://www.mercindia.org.in

http://rerc.rajasthan.gov.in

http://www.azurepower.com

http://www.regenpower.com

Prayas Group Pune, India