Solar Monthly Update for Print -...

12

SOLAR MONTHLY UPDATE Issue II January 2016 Vol. I

Transcript of Solar Monthly Update for Print -...

SOLARMONTHLY UPDATE

Issue II January 2016Vol. I

CERC BENCHMARK SOLAR PV CAPITAL

COSTS FALL BY MORE THAN 25% IN 2 YEARS

The Central Electricity Regulatory Commission (CERC) passed an order for determination of benchmark capital cost for solar PV projects for FY 2016-17 dated 23 December 2015. The order estimates capital cost including cost of equipment, construction, land, transmission and pre-operative expenses of solar PV projects for the upcoming financial year at ̀ 50.1 million/MW (USD 0.76 million). Based on inputs from the industry due by 10th January 2016, final benchmark capital cost and solar tariff is expected to be notified on 31st March 2016).

CLEAN ENERGY INVESTMENT JUMPS TO

RECORD USD 329BN IN 2015

Clean energy investment in 2015 rose to the record-high USD 329.3 billion (EUR 303bn), thanks to growth in China India, Africa, the US and Latin America.

A new report by Bloomberg New Energy Finance (BNEF) shows that investment in the past year was 4% above 2014 figures. It also beat by 3% the previous record of USD 318.3 billion set in 2011. That happened despite falling fossil fuel commodity prices, the continued weakness of the European economy, the declining cost of PV and the strong US currency, which is reducing the dollar value of investments. This means that despite these factors, more capacity could be installed for the same price, and despite the strength of the US currency, which is reducing the dollar value of non-dollar investment.

Preliminary calculations show that, thanks to utility-scale and small-scale activity, the world installed roughly 64 GW of wind and 57 GW of solar PV in 2015, marking a rise of around 30% on 2014. This combined total of 121 GW will have made up around half of the net capacity added in all generation technologies globally last year.

SOLAR POWER TARIFF AT RECORD LOW,

DROPS TO ̀ 4.34/UNIT

Foreign firms have bid record low solar power tariffs of `4.34 per unit in the latest auction, making green energy even more competitive and brightening the prospects of India adding 1 lakh mw of solar power capacity by 2022.Companies from Finland and South Africa have won projects in a solar park in Rajasthan, offering tariffs that are actually lower than some new coal-fired plants although older thermal units like those operated by NTPC charge less than `2.00 per unit. Analysts believe high solar radiation at the location and assured availability of land at the park would have attracted aggressive bids from foreign firms.

lSolar News Round Up

lSolar State Focus - Rajasthan

lCompany Limelight - Jakson Group

lSolar Financing & Falling Solar Tariffs

lTechnology Update

lSolar Tracker December - January

2015

Inside this Issue:

SOLAR NEWS ROUND UP

SOLAR MONTHLY UPDATE January 2016| 2

SOLAR MONTHLY UPDATE | January 2016 3

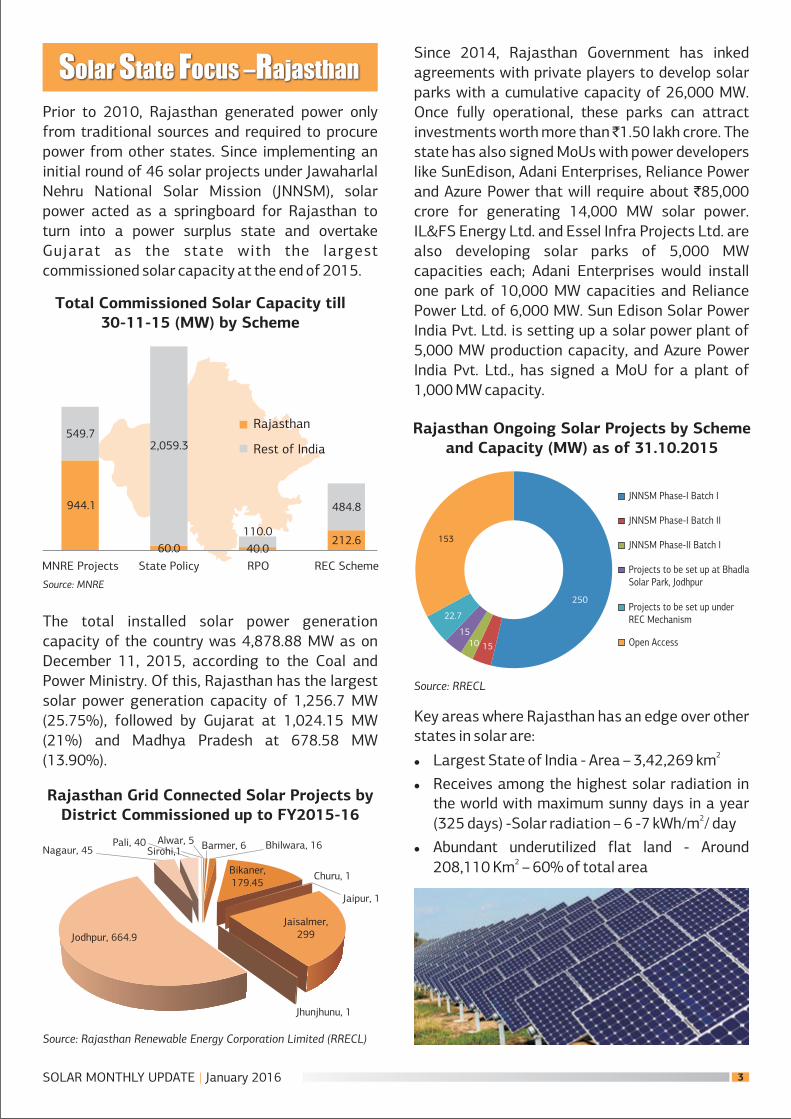

Since 2014, Rajasthan Government has inked agreements with private players to develop solar parks with a cumulative capacity of 26,000 MW. Once fully operational, these parks can attract investments worth more than ̀ 1.50 lakh crore. The state has also signed MoUs with power developers like SunEdison, Adani Enterprises, Reliance Power and Azure Power that will require about `85,000 crore for generating 14,000 MW solar power. IL&FS Energy Ltd. and Essel Infra Projects Ltd. are also developing solar parks of 5,000 MW capacities each; Adani Enterprises would install one park of 10,000 MW capacities and Reliance Power Ltd. of 6,000 MW. Sun Edison Solar Power India Pvt. Ltd. is setting up a solar power plant of 5,000 MW production capacity, and Azure Power India Pvt. Ltd., has signed a MoU for a plant of 1,000 MW capacity.

Prior to 2010, Rajasthan generated power only from traditional sources and required to procure power from other states. Since implementing an initial round of 46 solar projects under Jawaharlal Nehru National Solar Mission (JNNSM), solar power acted as a springboard for Rajasthan to turn into a power surplus state and overtake Gujarat as the state with the largest commissioned solar capacity at the end of 2015.

The total installed solar power generation capacity of the country was 4,878.88 MW as on December 11, 2015, according to the Coal and Power Ministry. Of this, Rajasthan has the largest solar power generation capacity of 1,256.7 MW (25.75%), followed by Gujarat at 1,024.15 MW (21%) and Madhya Pradesh at 678.58 MW (13.90%).

Solar State Focus –Rajasthan

Total Commissioned Solar Capacity till30-11-15 (MW) by Scheme

Source: MNRE

Rajasthan Grid Connected Solar Projects byDistrict Commissioned up to FY2015-16

Source: Rajasthan Renewable Energy Corporation Limited (RRECL)

MNRE Projects State Policy

212.6

484.8

110.0

2,059.3549.7

944.1

RPO REC Scheme

Rajasthan

Rest of India

40.060.0

Rajasthan Ongoing Solar Projects by Schemeand Capacity (MW) as of 31.10.2015

Source: RRECL

Key areas where Rajasthan has an edge over other states in solar are:

2lLargest State of India - Area – 3,42,269 km

lReceives among the highest solar radiation in the world with maximum sunny days in a year

2(325 days) -Solar radiation – 6 -7 kWh/m / day

lAbundant underutilized flat land - Around 2208,110 Km – 60% of total area

JNNSM Phase-I Batch I

JNNSM Phase-I Batch II

JNNSM Phase-II Batch I

Projects to be set up at BhadlaSolar Park, Jodhpur

Projects to be set up underREC Mechanism

Open Access

153

250

22.7

15

1510

Jodhpur, 664.9

Nagaur, 45Pali, 40 Alwar, 5 Barmer, 6

Bikaner,179.45

Jaisalmer,299

Bhilwara, 16

Churu, 1

Jaipur, 1

Jhunjhunu, 1

Sirohi,1

SOLAR MONTHLY UPDATE | January 2016 4

Rajasthan Solar Policy 2014-Highlights

Source: Reconnect Energy

The Flip Side

Rajasthan is saddled with the highest Discom losses. At present, the state has a financial burden of

around ̀ 85,000 crore to lending institutions. The state, along with other loss-making states, is already

on notice by the RBI to clear its debts or it will be debarred from receiving financial aid.

Rajasthan State Discoms have tried debt restructuring twice…..

During the last five years, all state-owned power firms in Rajasthan have resorted to taking short- term working capital loans, owing to growing demand for electricity, though they have been unable to increase tariffs adequately. Now, by being the first state to adopt the Government's latest UDAY (Ujwal Discom Assurance Yojana), a financial restructuring programme for the loss-making power utilities, it has now bought time for a turnaround. Under UDAY, power distribution companies have to reduce their technical and commercial losses to 15 percent by FY2018-19 against existing national average 22 percent and eliminate the gap between Average Revenue Realised (ARR) & Average Cost of Supply (ACS) by FY2018-19.

Rajasthan Solar Policy 2014 w.e.f 08.10.2014 (till modification or newer policy supersedes it);Nodal Agency: RREC Target Capacity: 25 GW

Particulars Rajasthan Solar Policy 2014

1. Setting up of Solar plants under guidelines of MNRE or JNNSM.

2. Setting up of Solar plants in Rajasthan for sale to Discoms.

3. Setting up plants for sale through REC mechanism.

4. Projects for Captive use or sale to 3rd party or sale to other states through open Access.

5. Solar Rooftop Systems through Net Metering mechanism.

6. Decentralized & Off grid Solar Applications - Hybrid Systems, SPV Pumping Systems, Standalone Solar Systems.

7. Development of Solar parks in the state.

1. Projects of capacities more than 500 MW will be directly placed before State Level Empowered Committee (SLEC) for consideration.

2. Such projects will be eligible for benefits/concessions available under Rajasthan Investment Promotion Scheme.

1. Incentives as per Rajasthan Industrial Policy.

2. Availability of Water for Power Generation.

3. Clearance from Rajasthan State Pollution Control Board.

4. Banking will be allowed as per RERC Regulations and orders.

The solar power producer will have to submit an application to RREC, and will be required to deposit processing fee defined under the Policy.

The govt. land will be alloted to Solar park developer or a project developer as per the provisions of Rajasthan Land and Revenue Rules 2007. The setting up of Solar projects on private lands will also be promoted.

Rs. 10 Lac/MW in form of Bank Guarantee.

Open access will be granted to beneficiaries, provided that they will have to pay OA charges asas approved by RERC through its orders.

The drawal of reactive power shall be charged by Transmission companies as per the RERCorders.

The Transmission and Distribution companies will ensure the availability of powerevacuation network. The solar power producer will have to pay grid connectivity chargesas finalized by RERC.

Projects to bepromoted under the

Policy

Registration of SolarProjects

Land Allotment

Incentives

Security Deposits

Special Provision forMega Solar Power

Projects

Open Access for ThirdParty

Reactive EnergyCharges

Power Evacuation andGrid interfacing

SOLAR MONTHLY UPDATE | January 2016 5

COMPANY LIMELIGHT – JAKSON GROUP

About Jakson Group

Jakson Group is a diversified power solutions provider group with multiple business interests ranging from power generation, solar and power distribution to generators, EPC, IPP and hospitality. Founded in 1947, the company has over 7 decades of engineering experience. Jakson occupies a leading market position with its business activities in the following key areas:

lPower Generation.

lSolar & Power Distribution division

lEPC division.

lIPP

lInternational Business – Bangladesh, UK, Nepal, Singapore and Bangladesh, Africa.

lHospitality

The Jakson group represents:

lOver 1 million sq. ft. of combined manufacturing space, 3 manufacturing plants

lOver 2000 employees pan India

lGlobal Training Centre and 2 Service Centers

l22 offices in India, overseas Offices in Nepal, Bangladesh & Singapore, upcoming office in Dubai

lGrowing into a USD 300 million (`1800 crore) enterprise, as of 2016.

lSatish Kumar Gupta - Founder & Chairman

lSameer Gupta - Managing Director

Management

Growth Story: Jakson Group Turnover (` Crore), FY2009-2016

Source: Jakson

Director's Quote:

From the perspective of an India based solar solutions provider, what do you perceive as a key challenge in the solar market today?

The key challenge for domestic solar companies are definitely, the drastically falling tariffs in the recent PV grid connected solar bids auctioned during the course of 2015. Here, companies with external funding and those that manufacture components and cells have a temporary advantage over others in bidding for PV projects. Vertical integration and ensuring an optimum financing mix in the long run is thus, the key to sustaining low tariffs in the sector.

Group and Company Performance Highlights

2015-2016(E

)

Tur

nove

r (`

Cro

re) 1500

1000

500

2009-2010

2010-2011

2011-2012

2012-2013

2013-2014

2014-2015

0

2000

1,301.88

1,800.00

1,438.771,362.25

1,088.591,113.19

887.07

SOLAR MONTHLY UPDATE | January 2016 6

lSundeep Gupta - Jt. Managing Director

lSunil Narang - Sr. Director

lRakesh Kumar Sharma (Group CFO)

lAtul Gupta (Strategic Head-Finance)

lSudershan Kumar Gupta (Board Advisor & Solar IPP Head)

lAshish Sethi (Solar EPC Head)

lSandip Ghosh (Solar Products Head)

lPraveen Pai (Power Solutions Head)

lGagan Chanana (Commercail Genset Head)

lAparajitha Ramadyani (HR and Admin)

In 2011, the Jakson group diversified its business operations in solar power, extending its experience in power generation to serve the solar markets. Its solar portfolio includes the following key solutions:

1. Solar IPPs: Selling power to Govt. entities and

private customers through long term PPAs

2. Solar EPC & Components:

a. Turnkey EPC for Utility scale & Rooftop power plants

b. On-grid & Off-grid solar systems

c. PV plant components

3. Solar Products & Systems:

a. Mini/Micro Grids

b. Solar Pumping Systems

c. Solar Street Lighting Systems

d. Solar Home Lighting Systems

Jakson has also laid foundation for its 25 MW solar power plant (with plans to scale it upto 100MW) to address growing power needs of India and provide a clean renewable source of energy.

lSetting up of MW scale land based Solar Power Plants under long term PPAs to sell power to Government entities.

lSetting up rooftop solar power plants on BOOT/ BOO basis under long term PPAs to sell power to private customers.

Current Land Based IPP's

l20 MW Solar Power Plant in Bap, Rajasthan

in operation since March 2012: Set up with

About Jakson Solar Projects

1. Solar IPP

an investment of 200 crore under Government's Jawaharlal Nehru National Solar Mission (JNNSM) policy Phase 1 Batch 2. The solar power plant is built on an approximately 100 acres land using high efficiency crystalline solar cells technology. It is the largest single location solar power farm in India based on crystalline cell technology. Commissioned in March 2013, executed in 10 months. Current CUF:19%

l10 MW Solar Plant in Uttar Pradesh commissioned in March 2015

l30 MW Solar plant in UP Plant to be commissioned by June 2016

Current Rooftop IPP's

l200kWp in Chennai

l250 kWp for Delhi Metro Rail Corporation

l100kWp for Airport Authority of India, Raipur.

Jakson plans to own 200 MW solar power plants in the next three years

lTurnkey EPC and O&M for Rooftop solar power plants

lSupply of Solar Power Plant Components for MW projects

lSolar Inverter Sub-station (SISS)- Introduced in 2012

lString Combiner Box ( SCB)- Introduced in 2012

lModule Mounting Structures (MMS)- Introduced in 2014

lPV Modules- Introduced in Aug 2015

Current Land Based EPC & Components

Projects

l20 MW, JPPL- Bap, Rajasthan

uDesign, Engineering, Equipment Supply, Installation, Commissioning and O&M for 25 yrs

l10 MW, NTPC- Talcher, Orissa

uDesign, Engineering, Equipment Supply (except PV Modules) , Insta l lat ion , Commissioning and O&M for 1 year

uThree different design of civil foundation used on Ash fill land

l20 MW EPC Solution for Solar Power plant in Rajasthan

`

2. Solar EPC and Components

SOLAR MONTHLY UPDATE | January 2016 7

1.05 MWp

23.0 MWp

10 MWp

33.5 MWp

148.5

81 MWp under execution

Table 1 : Jakson Solar EPC Projects Executed/Under Execution, FY2012-2016

F. Y. Land Rooftop Turnover ( Cr.)`

2011-12

2012-13

2013-14

2014-15

TOTAL

2015-16

-

300 KWp

600 KWp

3.1 MWp

17.2

13.2 MWp under execution

11

152

38

130

831

481.705 Cr orders in handunder execution, 500 Cr total

expected

Source: Jakson

l20 MW EPC Solution for Vikram Solar in Rajasthan

l1 MW EPC for Ganges Enterprises in Khetri, Rajasthan

3. Solar Products and Systems

Design & manufacture of innovative solar power products for various applications being marketed both directly and through Channel Partners

lNetwork of 22 channel partners and 160 dealers Expected 60 channel partners and 600 dealers by end of 2016

lDeveloping a channel of distributors in Africa & Middle East

SOLAR PROJECT FINANCING- FALLING TARIFFS AND ITS IMPLICATIONS

Falling Solar Costs

The January 2016 update of CERC, outlined how the major components of capital costs associated

with solar PV projects in India have witnessed drastic reductions, resulting in a clear fall in overall cost of solar PV utility scale projects in India.

26.13 48.5 60 80 80

Table 1 : Capital Cost Norm Proposed (` lakhs/MW) for Solar PV Projects, FY2013-17

Cost Component

PV Modules

Land Cost

Civil and General Works

Mounting Structures

Power Conditioning Unit (Inverter)

Evacuation Cost up to Inter-connection Point(Cables and Transformers)

Preliminary and Pre-Operative Expensesincluding IDC and Contingency

2016-17(Proposed)

310.19

25

35

35

30

40

2015-16

332.35

25

50

50

45

55

2014-15

365.8

25

60

50

50

60

2013-14

335.71

16.8

94.5

105

60

105

2012-13

344.5

16.8

94.5

105

60

105

Total Capital Cost 501.32 605.85 670.8 797.01 805.8

Source: CERC

Source: Energy Trend, Jan 2016

Market/Country Installation Target Share ofRenewable Generation

150GW by 2020 20%(non-fossil fuel by 2030)

64GW by 2030 22-24% by 2030

- 20% by 2030

66GW by 2030 50% by 2030

22GW by 2020 15% by 2020

100GW by 2022 40%(non-fossil fuel) by 2030

8.7GW by 2030 13.3% by 2030

China

Japan

US

Germany

UK

India

Taiwan(current Government)

Taiwan(Opposition party)

13GW by 2025 20% by 2025

Table 2 : Installation targets of major markets and LCOE for utility-scale systems

Current LCOE(min), $/kWh

0.08

0.10

0.07

0.11

0.12

0.08

0.09

0.09

Current LCOE(max), $/kWh

0.14

0.14

0.12

0.17

0.20

0.11

0.14

0.14

SOLAR MONTHLY UPDATE | January 2016 8

Global Trends contributing to the

Falling costs

Globally installed cost of PV is expected to fall by over 15%, driving demand for solar PV installations worldwide. In the US with increased deployment

and new technological advances, installed costs could drop to around US$1.15/W in 2016 and by 15% by the end of 2017. Such a decrease would drive down the Levellised Cost Of Electricity (LCOE) to under US$0.07/kWh in some areas.

Falling Domestic Tariffs amid

Aggressive Bidding in Auctions

Questions Solar Viability

Massive scaling up of solar targets, global fall in solar panel prices, combined with aggressive bidding in the auctioned solar projects in 2015 have raised the question of whether the solar projects in India would remain financially viable in the future.

The lowest tariffs in the portfolio obviousy have been quoted for solar parks, where ready and free availability of land, water, transmission and grid connectivity infrastructure would translate to lower costs compared to other solar projects where the onus is on the bidder to procure the relevant infrastructure. Alternatively, power bundling schemes also provide leeway for lower tariffs in a market, where grid parity has yet to be achieved.

Table 3 : Trend in Solar PV Auction Bid Results by Project/Scheme, 2010-2015

NSM Batch 1

NSM Batch 2

Orissa Phase 1

Orissa Phase 2

Karnataka

Dec '10

Dec '11

Mar '12

Dec '12

Apr '12

Project/ Scheme Year Capacity onOffer (MW)

Highest Bid(`/KWh)

Lowest(`/KWh)

Bid Weighted Avg.Price (`/KWh)

150

350

25

25

60

12.76

9.39

8.98

9.50

8.50

10.95

7.49

7.00

7.28

7.94

12.16

8.79

8.36

8.73

8.34

Madhya Pradesh

Tamil Nadu

Rajasthan

Andhra Pradesh

Punjab Phase 1

Jun '12

Mar '13

Mar '13

Apr '13

June '13

125

150

75

226

270

12.45

14.50

8.25

15.99

8.75

7.90

5.97

6.45

6.49

7.20

8.05

6.48*

6.45 (L1)

6.49 (L1)

8.41

Uttar Pradesh Phase 1

Karnataka Phase 2

Madhya Pradesh Phase 2

Aug '13

Aug '13

Jan '14

Oct '14

130

130

100

500

9.33

8.05

6.97

5.99** (7.03Levelized)

8.01

5.50

6.47

5.25**(6.17 Level.)

8.90

6.87

6.86

5.75**(6.75 Level.)

Andhra Pradesh Phase 2

Karnataka

Telangana

Punjab (Capacity 5-24 MW)

Punjab (Capacity 25-100 MW)

NTPC Anantapur

Uttar Pradesh Phase 2

Madhya Pradesh

Telangana Group 1****

Telangana Group 2****

Punjab

Uttarakhand

AP-500 MW Bundling scheme******

Rajasthan Solar Park

Nov '14

Nov '14

Feb '15

Feb '15

May '15

Jun '15

Jun '15

Aug '15

Aug '15

Sep '15

Oct '15

Nov '15

Jan '16

500

500

100

100

250

215

300

500

1500

500

170

500

420

7.12

6.90

7.45

7.56

-

8.60

5.64

5.87

5.89

5.98

5.57

4.63

5.60

6.71

6.46

6.88

6.88

-

7.02

5.05

5.50

5.17

5.09

5.99

4.63

4.34

6.94

6.72

7.17

7.16

6.16*** (L1)

8.04

5.36

5.73

5.62

5.65

5.76

4.63

5.00

* 5% escalation for 10 years** 3% escalation for 10 years. Separate L1 for 9 districts*** EPC Bids with Domestic content requirement. Capital subsidy of `1 Cr/MW**** Results for the lowest bid for 500 and 1500 MW respectively. The sub-station wise final list to be declared soon****** Online reverse action concluded on 03.11.2015. Entire capacity has been won by Sun Edison.

Source: MNRE

SOLAR MONTHLY UPDATE | January 2016 9

Project/ Scheme Year Capacity onOffer (MW)

Highest Bid(`/KWh)

Lowest(`/KWh)

Bid Weighted Avg.Price (`/KWh)

The lowest price quoted so far in the Rajasthan Solar Park tender on January 19, 2016 is an example. Moreover, according to the MNRE, the weakest link in the value chain is distribution, wherein discoms in the country have accumulated losses of approximately `3.8 lakh crore and outstanding debt of approximately ̀ 4.3 lakh crore (as on March, 2015). The Government has come out with a clear cut action plan called UDAY (Ujjwal Discom Assurance Yojana) to tackle the problem of debt-ridden discoms head on over the next two to three years. This could level the playing field and eliminate bottlenecks in distribution across the market in the future and make the equations on tariffs less complex and easier to compare.

Innovative Financing of solar projects and availability of funding

According to credit rating agency CRISIL, the wind and solar sectors will require approximately `3 trillion in the next five years to double capacity. Of this, about 70 percent (`2 trillion) will have to be funded through debt. Bank financing is likely to

remain poor given the low appetite for financing renewable projects, asset-liability mismatch constraints and crowding-out by conventional power sources.

CRISIL recommends innovative financing as a means of widening financing avenues and reducing costs. There are various credit enhancements available, which can be deployed to match the needs, such as:

lPartial guarantee

lSecuritization of renewable project cash flows

lInfrastructure debt funds (IDFs), and

lPartial credit enhancement facility for renewable energy bonds

Government initiatives to fund renewable energy projects

The Ministry of Finance incubated the idea of an infrastructure debt fund (IDF) as a trust or mutual fund that can supplement bank finance by taking over a substantial share of outstanding loans.

lEnergy Storage Systems

lIndia Needs to Make Silicon for Solar Power

Energy Storage Systems

Energy storage is tightly linked with renewable energy generation and lower costs. This requires the integration of storage mechanisms into existing grids and other distribution systems in ways that manage peak loads and thus contribute to reducing the necessary generating costs. According to Greentech Media analysis forecasts, the cost of installing an energy storage system will drop by some 41% by 2020.

Battery costs have fallen 50 per cent in the past five years. The balance-of-system cost (hardware, labor and customer acquisition, etc.) suggests installing energy storage will drop to $400 a kilowatt by 2020, down from the current average of $670. This suggests advances in storage could rapidly overturn established business models.

The biggest price cut will be seen in inverters — the most complicated piece of machinery in the storage system, besides the battery.

Storage Technologies and their Applications:

lPumped hydro systems - enable us to manage the use of flows of water. It has been in use for centuries

lBatteries - can balance power loads and help manage the challenges of energy supplies that are intermittent and also at the production and

TECHNOLOGY UPDATE

SOLAR MONTHLY UPDATE | January 2016 10

Currently, two IDF-NBFCs (L&T Infra Debt Fund Ltd and India Infradebt Ltd, both rated CRISIL AAA/Stable) are operational. IREDA is a NBFC which was created to finance renewable energy. Government had allowed IREDA to raise `2,000 crore through tax-free bonds. Besides, it has also asked Power Finance Corporation, Rural Electrification Corporation and NTPC Ltd to raise `1,000 crore through tax-free renewable energy bonds.

The RBI is considering allowing banks to provide credit enhancement to corporate bonds either as a subordinated loan facility or as a non-funded contingent line of credit.

at the consumption ends of the supply chain. While technologies such as lithium ion batteries, are not yet commercially viable, costs are falling at an impressive pace, which could soon make it an attractive alternative.

India Needs to Make Silicon for Solar Power

Market research firm GTM Research expects around 130,000MT of polysilicon production to come on stream in the next few years, equivalent of 25GW, which could impact pricing. GTM Research stated that cumulative global polysilicon supply capability was expected to reach 437,000MT by 2016, enough to support 85GW of c-Si module production. Silicon is the material at the base of modern electronics and IT, be it computers, television, mobile phones which all depend on silicon chips for their operation. Semiconductor silicon is now used in 85 per cent of all the photovoltaic (PV) cells in commercial use. India however, does not manufacture silicon on a significant scale!

One MW capacity of solar modules requires 3-7 tons of highly pure semiconductor grade silicon. Thus for 1,00,000 MW, India requires about 3,00,000 – 7,00,000 tons of silicon. Though we have plenty of sand as raw material, we don't have the technology to process it into silicon wafers for solar cells or panels.

lPolysilicon production involves chemical processes using chlorination followed by fractional distillation to eliminate impurities such as B, P and As and metallic impurities down to less than 1 part per billion.

2013 2014E 2015E 2016E 2018E2017E

Siemens FBR UMG

550

50

100

150

200

250

300

350

400

450

500

550

KM

T

72

374 395 404

Ramped Polysillicon Capacity byProduction Technology, 2013-2018E

555

5

2

260 278325

7258

46

2620

Source: Polysillicon 2015-2018: Supply, Demand, Cost and Pricing

SOLAR MONTHLY UPDATE | January 2016 11

There are now only 6-8 major producers of electronic-grade silicon in the world, Germany, Norway and Taiwan being the other three. All are vigorously expanding their production capacity in view of the worldwide shortage of silicon, which is expected to become even more critical with the rapid expansion of the PV industry, especially in developing economies.

Indian Scenario

India manufacture of silicon is limited to SCL

Chandigarh, while BEL and ITI in Bangalore all

depend on imported wafers. In India, Polysillicon

production leading to Si wafers at a commercial

level started at Mettur Chemicals in the 80's, but

did not achieve viable economies of scale and used

outdated processes.

A plan to import technology from USA and

considerable R&D did not result in technology

transfer. Thus all Si device production at SCL, BEL,

BHEL and ITI has depended on imported wafers.

Indigenous production of silicon is thus the key to

lowering costs of PV projects in India viable.

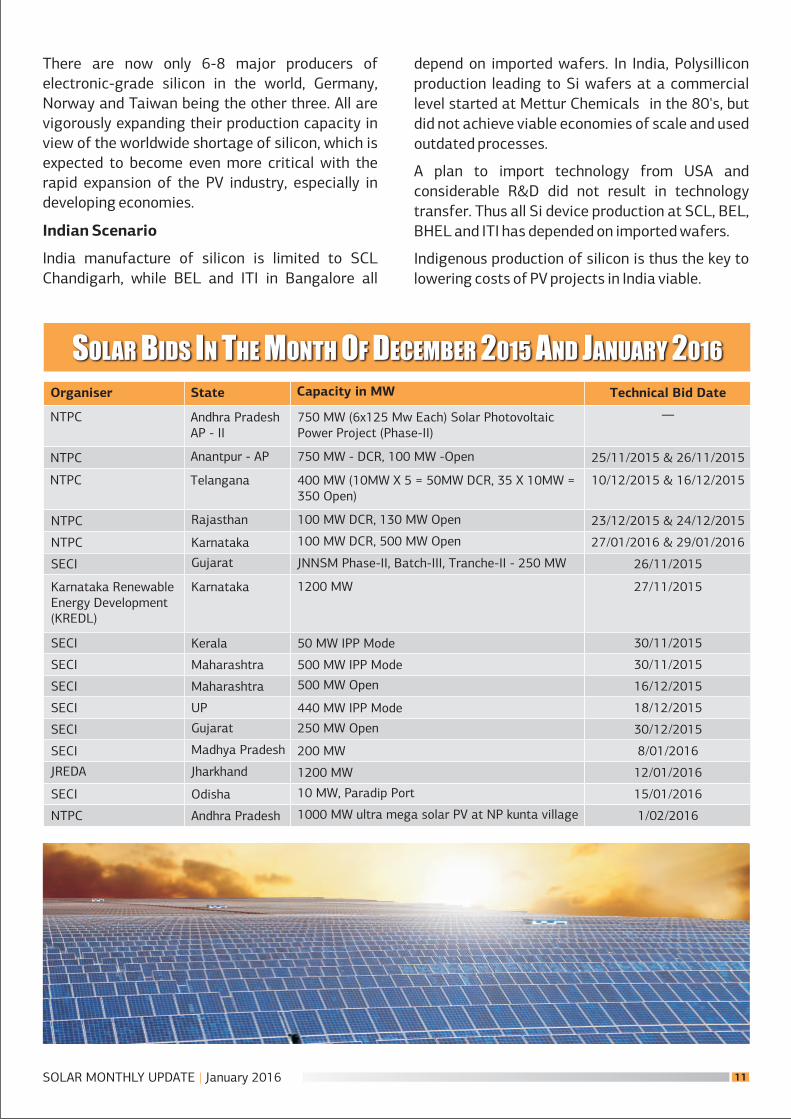

SOLAR BIDS IN THE MONTH OF DECEMBER 2015 AND JANUARY 2016

750 MW (6x125 Mw Each) Solar PhotovoltaicPower Project (Phase-II)

750 MW - DCR, 100 MW -Open

400 MW (10MW X 5 = 50MW DCR, 35 X 10MW =350 Open)

100 MW DCR, 130 MW Open

100 MW DCR, 500 MW Open

JNNSM Phase-II, Batch-III, Tranche-II - 250 MW

1200 MW

Technical Bid Date

—

25/11/2015 & 26/11/2015

10 15 & 16 15/12/20 /12/20

23 15 & 24 15/12/20 /12/20

27/01/2016 & 29 16/01/20

Capacity in MWState

Andhra PradeshAP - II

Anantpur - AP

Telangana

Rajasthan

Karnataka

Gujarat

Karnataka

Organiser

NTPC

NTPC

NTPC

NTPC

NTPC

SECI

Karnataka RenewableEnergy Development(KREDL)

50 MW IPP Mode

500 MW IPP Mode

500 MW Open

440 MW IPP Mode

250 MW Open

200 MW

1200 MW

10 MW, Paradip Port

1000 MW ultra mega solar PV at NP kunta village

8 16/01/20

12 16/01/20

15 16/01/20

1 16/02/20

Kerala

Maharashtra

Maharashtra

UP

Gujarat

Madhya Pradesh

Jharkhand

Odisha

Andhra Pradesh

SECI

SECI

SECI

SECI

SECI

SECI

JREDA

SECI

NTPC

26/11/2015

27 15/11/20

30 15/11/20

30 15/11/20

16 15/12/20

18 15/12/20

30 15/12/20

New Delhi

P FE

1201, 12th Floor, Chiranjiv Tower

43, Nehru Place, New Delhi 110019 011 46628817 011 46628851 [email protected]

Kolkata

P FE

Sagar Trade Cube 5th Floor

104, S P Mukherjee Road, Kolkata 700026 033 24863815 033 24863816 [email protected]

Mumbai

P FE

Unit 8, 4th Floor, Trade World B Wing

Kamala Mills Compound, Lower Parel, Mumbai 400013 022 66702000/04 022 66702005 [email protected]

www.lsifinance.com