Six Sigma helps a company create a culture of...

15

JOURNAL OF ORGANIZATIONAL EXCELLENCE / Summer 2004 © 2004 Wiley Periodicals, Inc. Published online in Wiley InterScience (www.interscience.wiley.com) DOI: 10.1002/npr.20019 SIX SIGMA HELPS A COMPANY CREATE A CULTURE OF ACCOUNTABILITY EXPECTATIONS–REWARDS ALIGNMENT How do you make employees feel more accountable for results? With many opin- ions but no hard facts about how to achieve this, one company turned to Six Sigma to find the answer. Six Sigma methodology, no longer confined to production de- partments, helped this company discover that a culture of accountability, first and foremost, is a function of strategically aligned employee expectations and an ef- fective system of rewards and consequences. © 2004 Wiley Periodicals, Inc. Peter C. Brewer Peter C. Brewer is an associate professor in the Department of Accountancy at Miami University, Oxford, Ohio. He can be reached at [email protected]. * * * 45 S ix Sigma, a process improvement methodol- ogy with its genesis in the manufacturing arena, has gained wide acceptance in U.S. companies; a recent study suggests that at least 25 percent of Fortune 200 companies are using it. Lately the methodology has been proving itself effective in nonmanufacturing applications as a customer- driven, data-based approach that provides an ob- jective framework for improving essentially qual- itative processes. When Amdell Inc. (a fictitious name for an ac- tual company) faced the need to create a “culture of accountability” (COA) within its organization, it encountered divergent opinions about how to achieve this. But rather than relying on anecdotal observations and personal opinions, the company chose the Six Sigma methodology to guide the process of culture change. Six Sigma enabled the project team to select the two processes that could most greatly affect employees’ sense of account- ability, to identify gaps between how these processes should operate and how they currently functioned, and to design and implement specific improvements to close the gaps as quickly as pos- sible. Six Sigma helped the Amdell project team not only focus its efforts in the most meaningful areas but also find the best triggers for making employees more accountable for results. WHO IS ACCOUNTABLE FOR RESULTS? With more than $750 million in annual sales, Amdell Inc., a wholly owned subsidiary of a Fortune 100 company, develops and markets a

Transcript of Six Sigma helps a company create a culture of...

JOURNAL OF ORGANIZATIONAL EXCELLENCE / Summer 2004

© 2004 Wiley Periodicals, Inc. Published online in Wiley InterScience (www.interscience.wiley.com) DOI: 10.1002/npr.20019

SIX SIGMA HELPS A COMPANY CREATE ACULTURE OF ACCOUNTABILITY

EXPECTATIONS–REWARDS ALIGNMENT

How do you make employees feel more accountable for results? With many opin-ions but no hard facts about how to achieve this, one company turned to Six Sigmato find the answer. Six Sigma methodology, no longer confined to production de-partments, helped this company discover that a culture of accountability, first andforemost, is a function of strategically aligned employee expectations and an ef-fective system of rewards and consequences. © 2004 Wiley Periodicals, Inc.

Peter C. Brewer

Peter C. Brewer is an associate professor in the Department of Accountancy at Miami University, Oxford, Ohio. He can be reached [email protected].

* * *

45

Six Sigma, a process improvement methodol-ogy with its genesis in the manufacturing arena,

has gained wide acceptance in U.S. companies; arecent study suggests that at least 25 percent ofFortune 200 companies are using it. Lately themethodology has been proving itself effective innonmanufacturing applications as a customer-driven, data-based approach that provides an ob-jective framework for improving essentially qual-itative processes.

When Amdell Inc. (a fictitious name for an ac-tual company) faced the need to create a “cultureof accountability” (COA) within its organization,it encountered divergent opinions about how toachieve this. But rather than relying on anecdotalobservations and personal opinions, the companychose the Six Sigma methodology to guide the

process of culture change. Six Sigma enabled theproject team to select the two processes that couldmost greatly affect employees’ sense of account-ability, to identify gaps between how theseprocesses should operate and how they currentlyfunctioned, and to design and implement specificimprovements to close the gaps as quickly as pos-sible. Six Sigma helped the Amdell project teamnot only focus its efforts in the most meaningfulareas but also find the best triggers for makingemployees more accountable for results.

WHO IS ACCOUNTABLE FOR RESULTS?

With more than $750 million in annual sales,Amdell Inc., a wholly owned subsidiary of aFortune 100 company, develops and markets a

JOURNAL OF ORGANIZATIONAL EXCELLENCE / Summer 2004

46 Peter C. Brewer

broad portfolio of automotive electronic compo-nents. Looking for better ways to sustain and im-prove on a tradition of strong financial perfor-mance, Amdell hired a high-profile consultingfirm in 2000 to take a fresh look at the company’sbusiness operations. One of the firm’s findingswas that the overwhelming majority of employ-ees were receiving overall performance evalua-tions of “3” or “4” (on a 5-point scale, with 1 �poor and 5 � outstanding) despite the fact thatthe company was regularly missing its revenuetargets and overspending its budget. Who atAmdell, the firm asked, is responsible for unac-ceptable financial performance? The firm recom-mended that one way Amdell could improve itsresults was to increase the sense of accountabil-ity that each employee has for those results, i.e.,to strengthen its culture of accountability (COA).

Amdell’s senior managers accepted the rec-ommendation but quickly discovered there wasno internal consensus on just how to achieve astronger COA. Some managers felt it was a func-tion of organizational processes and structures;others believed senior management effective-ness, human resource policies and practices, fis-cal responsibility, or individual commitment wasthe primary lever. All these opinions reflectedpersonal beliefs rather than any objective, cus-tomer-driven data. More importantly, each wouldlead to dramatically different courses of actionfor culture change. For example, a focus on in-dividual commitment could have a goal to elim-inate employees’ “I deserve it” mentality, whichcontributed to the inefficient use of resources. Ifsenior management effectiveness was the focusof the culture change process, then the goalmight be to eliminate the bureaucratic activitiesand in-house committees that some people be-lieved were an inefficient use of senior man-agers’ time.

In the absence of objective data, many com-panies rely upon political and personal agendas toselect a course of action. Financially astute seniormanagers often struggle with qualitative change

processes, frequently pursuing ill-advised coursesof action that demoralize their employees.

Amdell’s senior managers knew in their “gut”that Amdell needed a culture change that would in-crease everyone’s accountability, but without aclear consensus, they did not know how to facil-itate the process. They turned to Amdell’s ProcessImprovement Department for ideas.

The staff of the Process Improvement De-partment suggested using a Six Sigma frame-work known as DMAIC (Define, Measure, An-alyze, Improve, and Control) to provide astructure for the process of creating a COA (seeExhibit 1). The senior managers were intriguedby the customer focus, objectivity, and data-driven nature of the DMAIC process. They em-braced the Six Sigma approach and establisheda nine-member cross-functional project team,which included representatives from finance,human resources, sales, and research and devel-opment, as well as a Six Sigma Black Belt anda Green Belt (individuals trained and experi-enced in Six Sigma methodology and tools). Thesteps Amdell took to create a COA are discussedbelow according to each of the five DMAICstages employed in the project.

THE DEFINE STAGE

The accountability issues at Amdell related to theorganization’s ability, or inability, to meet the busi-ness plan and financial targets developed by theAmdell board of directors. The project team thusdefined its customer for this initiative as the boardof directors.

In order to make its efforts manageable, theteam also set project boundaries that limited thescope of the COA initiative to one location. SinceCleveland, the headquarters, had been the site ofthe consulting study that surfaced the accounta-bility problem, it was the logical candidate. Fur-thermore, if the accountability problem existedin other parts of Amdell as well, a successfulCleveland prototype would be helpful in devel-oping and implementing solutions elsewhere.

The project team created for the board of di-rectors’approval the Critical-to-Quality (CTQ) treeshown in Exhibit 2. The CTQ tree captured the“voice of the customer” (the board) in the form of26 outputs, or CTQs, that should be realized if

In the absence of objective data, manycompanies rely upon political and personal

agendas to select a course of action.

Six Sigma Helps a Company Create a Culture of Accountability

JOURNAL OF ORGANIZATIONAL EXCELLENCE / Summer 2004

47

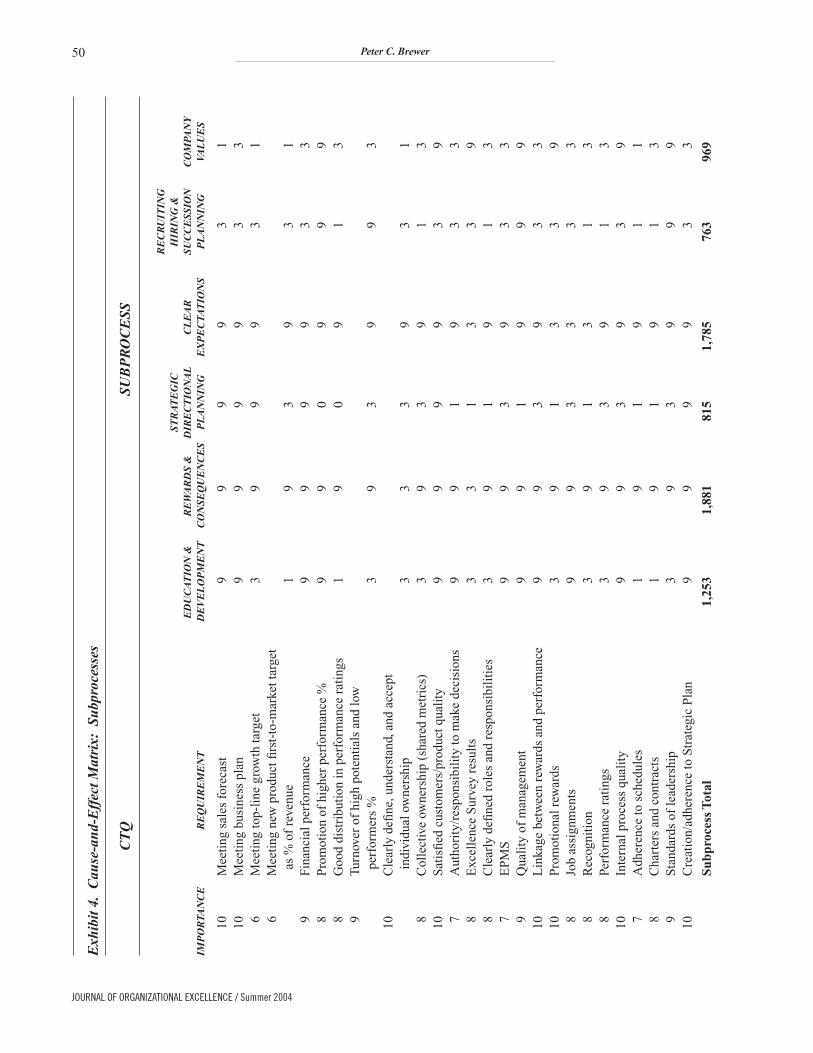

Next, the project team sought to “managescope” by focusing its efforts on the two processesout of the six that have the greatest impact on cre-ating a culture of accountability. To establish therelative influence of the six processes, the teamhad its customer, the board of directors, completetwo cause-and-effect matrices. The first of thesematrices, shown in Exhibit 3, lists the 26 CTQrequirements (in rows) and the six processes (incolumns). The board used the following steps tocomplete the matrix:

1. Board members weighted each CTQ re-quirement for its relative “importance to the

Amdell succeeds in creating a culture of account-ability. For example, greater accountability wouldmean that Amdell meets the business plan, linksrewards to performance, and adheres to schedules,to name just three of the 26 outcomes. The teamalso identified six processes—“Drivers” in the CTQtree —that influence the accountability CTQs:

• Financial performance• Performance management• Ownership• Rewards/consequences• Commitment• Quality of leadership

Exhibit 1. The Six Sigma DMAIC Framework

STAGE/OBJECTIVE TOOLS/OUTPUT

DEFINE

Define the project’s purpose and scope. • Project charter: project’s scope, goals, milestones, team members,and customer benefits

• High-level process map, a SIPOC (Suppliers, Inputs, Process,Outputs, and Customers) diagram

• Critical-to-Quality Tree: translates the “voice of the customer”into specific requirements

MEASURE

Gather information regarding existing process • Control Charts • Prioritization Matricesconditions to provide a baseline assessment of • Frequency Plots • FMEA (Failure Mode and current performance levels and narrow the scope • Pareto Charts Effect Analysis) Chartsof inquiry to the most important problems. • SIPOC Diagrams

ANALYZE

Identify the root causes of the problems that • Affinity Diagrams • Regression Analysis were clarified in the Measure Stage. • Cause-and-Effect Diagrams • Design of Experiments

• Control Charts

IMPROVE

Develop, implement, and evaluate solutions • Brainstorming • Hypothesis Testsintended to eliminate the root causes of • FMEA • Consensus Buildingproblems identified in the Analyze Stage. • Flow Diagrams

CONTROL

Ensure that problems remain fixed and that • Pareto Charts • Quality Control Process Chartsthe new methods can be improved over time. • Control Charts • Other data collection methods

• Flow Diagrams

JOURNAL OF ORGANIZATIONAL EXCELLENCE / Summer 2004

48 Peter C. Brewer

customer” by assigning it a rating between1 and 10 (the first column of the matrix).

2. Board members selected one of the fol-lowing four numbers to reflect how im-portant they thought each process is indriving improvement in each CTQ re-quirement: 0 (no importance), 1 (minimalimportance), 3 (medium importance), and9 (high importance). The number wasrecorded in the cell of the matrix that cor-responds to the intersection of the specificprocess and the specific CTQ requirement.

3. The value in each cell was then multipliedby the weighting factor of its respectiveCTQ requirement (from the first column)to yield a weighted score.

4. All the weighted scores in a process’s col-umn were summed and recorded in thelast row of the matrix to produce a totalscore for each process.

Through this exercise, Amdell’s board of di-rectors gave Performance Management the high-est score (1,989) and Quality of Leadership thesecond highest score (1,917), establishing themas the two most important processes for satisfyingthe accountability CTQs. Interestingly, FinancialPerformance was rated the lowest (1,017) of allsix processes by the board. Although some mem-bers of the project team had initially believed thatmanaging financial results was a key driver of ac-countability, the “customer” most likely saw it asmore an outcome than a driver.

To further refine the meaning of the top-ratedprocesses, the project team broke down Perfor-mance Management and Quality of Leadershipinto six component processes for the board of di-rectors to assess in a second cause-and-effect ma-trix, shown in Exhibit 4. Although Rewards andConsequences was not among the highest scor-ing processes in Exhibit 3, the project team felt

Exhibit 2. Critical-to-Quality Tree

Six Sigma Helps a Company Create a Culture of Accountability

JOURNAL OF ORGANIZATIONAL EXCELLENCE / Summer 2004

49

Exh

ibit

3.

Cau

se-a

nd-

Eff

ect M

atri

x:P

roce

sses

CT

QP

RO

CE

SS

FIN

AN

CIA

LP

ER

FO

RM

AN

CE

RE

WA

RD

S &

QU

AL

ITY

OF

IMP

OR

TAN

CE

RE

QU

IRE

ME

NT

PE

RF

OR

MA

NC

EM

AN

AG

EM

EN

TO

WN

ER

SH

IPC

ON

SE

QU

EN

CE

SC

OM

MIT

ME

NT

LE

AD

ER

SH

IP

10M

eeti

ng s

ales

for

ecas

t9

99

99

910

Mee

ting

bus

ines

s pl

an9

99

99

96

Mee

ting

top-

line

gro

wth

targ

et3

93

93

36

Mee

ting

new

pro

duct

firs

t-to

-mar

ket t

arge

t as

% o

f re

venu

e3

93

93

39

Fina

ncia

l per

form

ance

99

99

99

8P

rom

otio

n of

hig

her

perf

orm

ance

%3

93

91

98

Goo

d di

stri

buti

on in

per

form

ance

rat

ings

09

19

39

9Tu

rnov

er o

f hi

gh p

oten

tial

s an

d lo

w

perf

orm

ers

%3

93

90

910

Cle

arly

defi

ne, u

nder

stan

d, a

nd a

ccep

t in

divi

dual

ow

ners

hip

09

93

99

8C

olle

ctiv

e ow

ners

hip

(sha

red

met

rics

)3

99

99

910

Sat

isfi

ed c

usto

mer

s/pr

oduc

t qua

lity

99

99

99

7A

utho

rity

/res

pons

ibil

ity

to m

ake

deci

sion

s3

99

99

98

Exc

elle

nce

Sur

vey

resu

lts

09

03

99

8C

lear

ly d

efine

d ro

les

and

resp

onsi

bili

ties

09

99

99

7E

PM

S3

99

99

99

Qua

lity

of

man

agem

ent

99

39

99

10L

inka

ge b

etw

een

rew

ards

and

per

form

ance

99

39

99

10P

rom

otio

nal r

ewar

ds3

93

99

98

Job

assi

gnm

ents

39

39

99

8R

ecog

niti

on3

93

99

98

Perf

orm

ance

rat

ings

99

39

99

10In

tern

al p

roce

ss q

uali

ty3

99

39

97

Adh

eren

ce to

sch

edul

es

39

99

99

8C

hart

ers

and

cont

ract

s3

99

99

99

Sta

ndar

ds o

f le

ader

ship

39

99

99

10C

reat

ion/

adhe

renc

e to

Str

ateg

ic P

lan

99

93

99

Pro

cess

Tot

al1,

017

1,98

91,

361

1,76

11,

724

1,91

7

JOURNAL OF ORGANIZATIONAL EXCELLENCE / Summer 2004

50 Peter C. Brewer

Exh

ibit

4.

Cau

se-a

nd-

Eff

ect M

atri

x:S

ubp

roce

sses

CT

QS

UB

PR

OC

ES

S

RE

CR

UIT

ING

ST

RA

TE

GIC

HIR

ING

&E

DU

CA

TIO

N &

RE

WA

RD

S &

DIR

EC

TIO

NA

LC

LE

AR

SU

CC

ES

SIO

NC

OM

PAN

Y

IMP

OR

TAN

CE

RE

QU

IRE

ME

NT

DE

VE

LO

PM

EN

TC

ON

SE

QU

EN

CE

SP

LA

NN

ING

EX

PE

CTA

TIO

NS

PL

AN

NIN

GVA

LU

ES

10M

eeti

ng s

ales

for

ecas

t9

99

93

110

Mee

ting

bus

ines

s pl

an9

99

93

36

Mee

ting

top-

line

gro

wth

targ

et3

99

93

16

Mee

ting

new

pro

duct

firs

t-to

-mar

ket t

arge

t as

% o

f re

venu

e1

93

93

19

Fina

ncia

l per

form

ance

99

99

33

8P

rom

otio

n of

hig

her

perf

orm

ance

%9

90

99

98

Goo

d di

stri

buti

on in

per

form

ance

rat

ings

19

09

13

9Tu

rnov

er o

f hi

gh p

oten

tial

s an

d lo

w

perf

orm

ers

%3

93

99

310

Cle

arly

defi

ne, u

nder

stan

d, a

nd a

ccep

t in

divi

dual

ow

ners

hip

33

39

31

8C

olle

ctiv

e ow

ners

hip

(sha

red

met

rics

)3

93

91

310

Sat

isfi

ed c

usto

mer

s/pr

oduc

t qua

lity

99

99

39

7A

utho

rity

/res

pons

ibil

ity

to m

ake

deci

sion

s9

91

93

38

Exc

elle

nce

Sur

vey

resu

lts

33

13

39

8C

lear

ly d

efine

d ro

les

and

resp

onsi

bili

ties

39

19

13

7E

PM

S9

93

93

39

Qua

lity

of

man

agem

ent

99

19

99

10L

inka

ge b

etw

een

rew

ards

and

per

form

ance

99

39

33

10P

rom

otio

nal r

ewar

ds3

91

33

98

Job

assi

gnm

ents

99

33

33

8R

ecog

niti

on3

91

31

38

Perf

orm

ance

rat

ings

39

39

13

10In

tern

al p

roce

ss q

uali

ty9

93

93

97

Adh

eren

ce to

sch

edul

es

19

19

11

8C

hart

ers

and

cont

ract

s1

91

91

39

Sta

ndar

ds o

f le

ader

ship

39

39

99

10C

reat

ion/

adhe

renc

e to

Str

ateg

ic P

lan

99

99

33

Subp

roce

ss T

otal

1,25

31,

881

815

1,78

576

396

9

Six Sigma Helps a Company Create a Culture of Accountability

JOURNAL OF ORGANIZATIONAL EXCELLENCE / Summer 2004

51

derstanding of the Clear Expectations and the Re-wards and Consequences processes, and (2) itmeasured key aspects of the two processes in orderto establish a baseline assessment of their currenteffectiveness. The baseline assessment often cre-ates a sense of urgency regarding the need to im-prove, and it provides a reference point for quan-tifying the extent of future improvements.

A SIPOC Diagram for Rewards and Conse-quences. The project team created a SIPOC (Sup-pliers, Inputs, Process, Outputs, and Customer)diagram for the two processes under study. Byway of example, the SIPOC diagram for the Re-wards and Consequences process is shown in Ex-hibit 5. Although the SIPOC diagram for the ClearExpectations process has not been included here,it is important to note that this process precedesRewards and Consequences and thus acts uponelements shown in Exhibit 5—e.g., each supplierto Rewards and Consequences should share clearlyaligned expectations.

that it should be considered a component of Per-formance Management and thus included in thesecond matrix. Indeed, in this second assessment,the board of directors identified Rewards and Con-sequences (score � 1,881) and Clear Expecta-tions (score � 1,785) as the two most importantcomponent processes for a COA.

While all the processes assessed in Exhibits 3and 4 could potentially improve Amdell’s COA,the Define Stage of the DMAIC framework es-tablished a customer-driven prioritization. Thisdistilled the somewhat nebulous concept of COAinto an actionable equation: Clear Expectations �Rewards and Consequences � Accountability.This result would set the focus for the culturechange efforts to follow.

THE MEASURE STAGE

The Measure Stage proceeded in two steps: (1)the project team developed a more detailed un-

Exhibit 5. SIPOC Diagram: Rewards and Consequences

JOURNAL OF ORGANIZATIONAL EXCELLENCE / Summer 2004

52 Peter C. Brewer

Suppliers and Inputs. The Suppliers and Inputscolumns of Exhibit 5 depict three key relationships:

• Amdell’s parent company supplies two im-portant inputs: (1) the high-level financialbudget for the forthcoming period, whichprovides a target or benchmark for judg-ing actual performance, and (2) an allo-cation of resources for training, which isnecessary if employees are to be held ac-countable for their performance.

• External customers, other employees, andeach individual achieve (supply) the indi-vidual and collective business results.Comparison of these actual results withthe budget—i.e., to assess performance—is important input to the determination ofrewards and consequences.

• Each individual and his or her immediatesupervisor supply information needed forthree Amdell programs that are importantinputs because they directly link results tohow employees are evaluated, rewarded,and promoted:

• The Employee Performance Manage-ment System (EPMS) documents mu-tually agreed-upon goals for the forth-coming year and actual performancerelative to those goals.

• The Salary Planning Tool establishesstandards that equalize salary rangeswithin job levels across departmentsand provides parameters that enableemployees to understand how their payraises are determined.

• The Succession Planning Tool ensuresthat employees receive appropriate train-ing commensurate with their level ofresponsibility, which justifies holdingthem accountable for their performance.

Process. The Process column in Exhibit 5shows six steps that constitute a detailed process

map for Rewards and Consequences, which be-gins after clear expectations have been establishedthrough the other COA process under study:

1. Information feedback requires gatheringall relevant information regarding thebudget, actual results, and the mutuallyagreed-upon information from the EPMS,the Salary Planning Tool, and the Succes-sion Planning Tool.

2. The immediate supervisor compiles theinformation from Step 1.

3. The supervisor makes a judgment regard-ing the subordinate’s performance.

4. The supervisor seeks approval of this judg-ment from his or her boss.

5. The supervisor communicates the feed-back and associated consequences to thesubordinate.

6. The subordinate can accept the feedback,and then receive the associated conse-quences, or reject the feedback, therebyinitiating another loop through the Re-wards and Consequences process.

Outputs. The project team identified five keyoutputs in the Rewards and ConsequencesSIPOC diagram:

1. Supervisors assign each subordinate a per-formance rating.

2. The positive or negative feedback is sharedwith the subordinate.

3. The consequences manifest themselvesin the form of each subordinate’s com-pensation, future job assignments, andpromotions.

4. The effectiveness of the Rewards and Con-sequences process drives each employee’slevel of job satisfaction.

5. The process’s effectiveness ultimately in-fluences the level of business performance.

Customers. Three customers—beneficiariesof the Rewards and Consequences process—were identified in the SIPOC diagram: Amdell’sboard of directors, all Amdell employees, andAmdell stockholders.

Baseline Assessment. Using the measurableinputs and outputs highlighted in the SIPOC dia-

External customers, other employees,and each individual achieve (supply) the

individual and collective business results.

Six Sigma Helps a Company Create a Culture of Accountability

JOURNAL OF ORGANIZATIONAL EXCELLENCE / Summer 2004

53

• Superiors and subordinates did not clearlyarticulate the relative importance of de-fined performance goals.

• Employees lacked a unified understand-ing of the organization’s most importantstrategic goals.

Written comments also spotlighted problemswith the output side of both processes:

• Performance ratings and pay raises did notadequately discriminate between strongand weak performers.

• Performance was not reviewed oftenenough.

• The annual bonus was not linked to strate-gic objectives.

In addition to the survey, the project teamgleaned one additional piece of baseline datafrom the earlier consultant’s report that had rec-ommended a stronger COA. The report foundthat 35 percent of Amdell’s divisional objectiveswere not aligned with the company’s overallstrategic objectives—a clear problem on the out-put side of the Clear Expectations process.

gram for each process, the project team performeda baseline assessment of how well each processwas currently functioning. To do this, the teamsought employee feedback through a questionnaireadministered to all Amdell employees at the Cleve-land location (16 questions for nonmanagement em-ployees and 27 questions for managers). Exhibit 6summarizes a portion of the survey’s findings.

Most significantly, the survey revealed thatthe inputs for the Rewards and Consequencesprocess were failing, with a specific need to im-prove the following:

• EPMS training, usage, and clarity of goalsand objectives

• Salary Planning Tool training and usage• Succession Planning Tool awareness, train-

ing, and usage• Performance feedback training

Employees’ written comments highlightedseveral weaknesses regarding the key inputs ofthe Clear Expectations process. For example:

• Superiors and subordinates established toomany performance goals.

Exhibit 6. Baseline Assessment Survey Results—January 2001

% FAVORABLE RESPONSE

QUESTION MANAGERS NONMANAGERS

1. Have you been trained on how to use the EPMS? 69 532. Are you currently using the EPMS for your associates? 68 -3. Have you used the EPMS for your annual goals and objectives? 85 754. How well does the EPMS clarify your annual goals and objectives?

[5-point scale, 5 = highest] 2.8 2.45. Are you aware of your department’s succession planning process? 72 446. Have you received any training on the succession planning process? 38 -7. Have you seen the results of and discussed your personal succession

planning ratings? 53 398. Have you been trained on how to use the salary planning tool to create a

career development plan? 35 179. Do you have a general understanding of the compensation model used by Amdell? 63 35

10. Have you received any training on compensation planning and the various available compensation options? 25 -

11. Have you received training on giving effective performance feedback? 58 -

No value in cell indicates question was not asked to nonmanagement employees.

JOURNAL OF ORGANIZATIONAL EXCELLENCE / Summer 2004

54 Peter C. Brewer

The baseline data thus pointed to numerousopportunities for improvements in the Clear Ex-pectations and the Rewards and Consequencesprocesses, but in the opinion of the project team,it was unlikely that all the issues could be suc-cessfully addressed simultaneously. Accordingly,the team narrowed its scope to what it saw as thetwo most critical issues:

• The lack of strategic alignment (in theClear Expectations process)

• The weaknesses with the EPMS (in theRewards and Consequences process)

The project team would tackle the other is-sues later.

THE ANALYZE STAGE

To understand the extent of the deficiencies in thetwo areas selected in the Measure Stage, the proj-ect team conducted a gap analysis between thecurrent (“as is”) and the desired state. The gapanalysis done on strategic alignment is presentedhere to illustrate the team’s approach.

Exhibit 7 shows the “as is” process map forAmdell’s existing method of communicating itsstrategic vision and aligning its employees’ ef-forts with that vision. The project team concludedthat this approach suffered from three weaknesses:

• Although all employees learn of the Strate-gic Plan at an annual off-site “state of the

company” meeting, there was no feedbackmechanism to verify that divisional, de-partmental, and individual goals thatemerged from the “as is” process werealigned with the priorities reflected in thecompany’s Strategic Plan. Thus, vice pres-idents and departmental managers couldestablish goals that, while seemingly im-portant from a functional perspective, werenot important or optimal from a compa-nywide strategic perspective.

• With no prioritization mechanism in the“as is” approach, an employee with bothstrategically aligned goals and function-ally aligned goals would be more likely tofocus on the functional goals because theywere consistent with the immediate su-pervisor’s agenda.

• The board of directors’ strategic visionwas not supported by specific measuresthat clarified the most important im-provement targets.

The project team designed a new process—the desired state—shown in Exhibit 8. Thisprocess cascades the strategic goals down fromthe board of directors to the divisions, depart-ments, and individuals in a sequential manner. Inaddition to the development of goals and objec-tives, the new process requires that the divisions,departments, and individuals also define measures,prioritize the goals and objectives, and verify theiralignment with the strategic direction and mea-

Exhibit 7. Strategic Alignment: “As Is” Process Map

Six Sigma Helps a Company Create a Culture of Accountability

JOURNAL OF ORGANIZATIONAL EXCELLENCE / Summer 2004

55

• Create a new performance measurementsystem that aligned everyone’s prioritieswith the strategic goals of the company.

• Redesign the EPMS so that it held em-ployees accountable for supporting thestrategic goals of the company.

sures in the board of directors’ business plan, withdiscrete feedback steps to assure this happens.

The project team realized that to fully imple-ment this revised process would require two newsolutions, which became the focus for the nextstage of the project:

Exhibit 8. Strategic Alignment: Recommended Process Design

JOURNAL OF ORGANIZATIONAL EXCELLENCE / Summer 2004

56 Peter C. Brewer

THE IMPROVE STAGE

Adoption of a Balanced Scorecard. The team pro-posed—and Amdell adopted—a Balanced Score-card (BSC) to improve the strategic alignment ofefforts throughout the company. Shown in Ex-hibit 9, the BSC translates Amdell’s strategic vi-sion— “redefining customer satisfaction throughinnovation”—into four broad strategic objectives:profitable growth, customer-defined quality inproducts and services, innovation, and leadershipdevelopment. These four strategic objectives arebroken down into seven business plan objectives,which in turn are supported by 15 more specificcompany initiatives. The BSC also contains 30measures for the 15 initiatives (omitted from theexhibit for confidentiality reasons).

Each division within Amdell was required tocreate its own BSC that dovetailed with the com-pany’s BSC. A Divisional Alignment Matrix aided

divisional managers in this task. Exhibit 10 con-tains an excerpt from the consolidated alignmentmatrix for all divisions. (The matrix is similar instructure to the cause-and-effect matrices used inthe Define Stage of the project.) The nomenclaturefor the measures shown in the excerpt—i.e., PG1through PG9—indicates the specific strategic ob-jective to which a company initiative and its mea-sures relate—in this case, profitable growth (PG).

For each of the 30 measures in the company’sBSC, a divisional manager assessed the degree ofinfluence that his or her division had on that mea-sure and recorded it in the corresponding matrixcell as either a 0 (none), 1 (minimal), 3 (medium),or 9 (strong). (The board of directors could chal-lenge a division’s cell values if deemed neces-sary.) Each cell value was multiplied by the mea-sure’s Importance Rating (from Column 1), whichhad been assigned to the measure by the board ofdirectors to indicate its importance in Amdell’s

Exhibit 9. Amdell’s Balanced Scorecard

VISION: REDEFINING CUSTOMER SATISFACTION THROUGH INNOVATION

STRATEGIC OBJECTIVE BUSINESS PLAN OBJECTIVE COMPANY INITIATIVE

Profitable growth Achieve revenue targets • Drive market share, market expansion, and new markets

Drive free cash flow • Margin improvement• Efficient capital spending• Efficient use of working capital

Customer-defined quality in Create a customer-centric culture • Customer relationship managementproducts and services

Drive toward Six Sigma through process • Design excellenceexcellence • Proactive quality

Innovation Drive product and process breakthrough • First-to-market productsimprovements • Deploy process excellence

• Implement e-business strategy• Continue to expand product

development capability

Leadership development Create a culture of accountability • Implement companywide bonus plan, balanced scorecard, and revised EPMS

Recruit, develop, and retain top talent • Retention strategy• Implement robust staffing strategy• Succession and development planning

Six Sigma Helps a Company Create a Culture of Accountability

JOURNAL OF ORGANIZATIONAL EXCELLENCE / Summer 2004

57

that superiors and subordinates were es-tablishing too many goals and that 35 per-cent of those goals were not strategicallyaligned. Fewer goals would sharpen eachemployee’s focus on strategic priorities.)

• Each goal documented on an individual’sEPMS had to support a strategic objec-tive from the Amdell BSC. Individual ordepartmental goals not tied to the BSCwere forbidden.

• The EPMS evaluation time frame wasreduced from one year to quarterly,which required each supervisor and sub-ordinate to sign off on quarterly perfor-mance reviews.

• The EPMS’s 5-point performance ratingscale was expanded to a 9-point scale.(The baseline data indicated that morethan 95 percent of employees were ratedeither a “3” or “4” on a 5-point scale. Anexpanded 9-point scale—coupled withadditional performance feedback train-ing—would enable greater discrimina-tion among employees’ performance.)

BSC. The product of the two values indicated therelative priority of that measure for that division.The highest priority for a division was any mea-sure with a score of 90—i.e., the highest Influ-ence Rating of 9 and the highest Importance Rat-ing of 10; its importance to the company’s strategicobjectives and the strong influence the divisionhad on the measure signaled that it should be acritical component of the division’s own BSC.

Each division’s BSC was cascaded down toits departments and to individuals, in the sensethat each employee’s goals as stated in the EPMShad to be connected to Amdell’s BSC. Further-more, the annual employee bonus plan was con-nected to a subset of six to ten measures from thecompany’s BSC.

Modification of the EPMS. The project teammade five primary changes to the Employee Per-formance Management System (EPMS) to ad-dress the problems identified in the Measure Stage:

• The number of an individual’s EPMSgoals was reduced from 15 to 5. (The base-line data from the Measure Stage revealed

Exhibit 10. Simple Divisional Alignment Matrix

JOURNAL OF ORGANIZATIONAL EXCELLENCE / Summer 2004

58 Peter C. Brewer

• Amdell committed additional resources totraining its managers how to give con-structive performance feedback.

THE CONTROL STAGE

Subsequent to the changes made in the ImproveStage, Amdell developed a three-part strategy toinstitutionalize the BSC and the new version of theEPMS and to implement monitoring plans that pre-vent reverting to old practices. As the first and mostimportant element of this strategy, the Amdell pres-ident now frames her communication to Amdellemployees about the progress of the company interms of the four pillars—strategic objectives—ofthe Balanced Scorecard. Furthermore, she clearlycommunicates the importance of linking each em-ployee’s EPMS goals to the BSC.

The Finance Department now maintains adashboard of BSC metrics that is electronicallyavailable to all employees. The message from thepresident, coupled with the visibility of the dash-

board, ensures that the BSC becomes the languageof the organization.

As the third leg of the Control Stage strat-egy, the Human Resources Department now an-nually administers what Amdell calls its Excel-lence Survey. The questions in the survey aredesigned to gauge employee perceptions aboutthe policies, processes, and practices that shouldsupport a culture of accountability. By monitor-ing survey results and taking action where im-provement is needed, Amdell ensures that it con-tinuously improves upon its COA rather thanreverting to prior patterns and practices.

CONCLUSION

Nine months after its baseline assessment surveyand four months after the changes were made inthe Improve Stage, Amdell again conducted thesurvey first used for the baseline assessment. Theresults of the two surveys are compared in Exhibit11. There were significant improvements in both

Exhibit 11. Follow-Up Survey Results Compared with Baseline Assessment

% FAVORABLE RESPONSE

MANAGERS NONMANAGERS

QUESTION JAN 2001 OCT 2001 JAN 2001 OCT 2001

1. Have you been trained on how to use the EPMS? 69 90 53 832. Are you currently using the EPMS for your associates? 68 86 - -3. Have you used the EPMS for your annual goals

and objectives? 85 97 75 954. How well does the EPMS clarify your annual goals

and objectives? [5-point scale, 5 = highest] 2.8 3.5 2.4 3.25. Are you aware of your department’s succession

planning process? 72 80 44 606. Have you received any training on the succession

planning process? 38 55 - -7. Have you seen the results of and discussed your

personal succession planning ratings? 53 52 39 398. Have you been trained on how to use the salary

planning tool to create a career development plan? 35 44 17 329. Do you have a general understanding of the

compensation model used by Amdell? 63 65 35 4310. Have you received any training on compensation

planning and the various available compensation options? 25 32 - -

11. Have you received training on giving effective performance feedback? 58 73 - -

No value in cell indicates question was not asked to nonmanagement employees.

Six Sigma Helps a Company Create a Culture of Accountability

JOURNAL OF ORGANIZATIONAL EXCELLENCE / Summer 2004

59

Managers are better able to award pay andpromotions that more closely reflect em-ployees’ actual levels of performance andcontributions to the company, which inturn motivates employees to sustain goodperformance where it already exists andimprove performance where it is needed.

• The more frequent quarterly EPMS reviews(rather than annual reviews) with supervi-sor/subordinate sign-offs increase each em-ployee’s understanding of how his or herperformance supports the strategic goalsof the company. More frequent and targetedfeedback reinforces behavioral change. Thisalso provides a richer source of feedbackdata that can be used to more finely dis-criminate between strong and weak per-formance, which enables more targeted andequitable use of rewards and consequences.

With the aid of the Six Sigma DMAIC frame-work and tools, Amdell clarified the nature of itsproblems with accountability, focused its effortsin the most productive directions, and configuredand implemented solutions that will sustain pos-itive change into the future. Six Sigma principlesthus proved very useful to Amdell in making twoqualitative processes more effective in order tocreate a stronger culture of accountability.Amdell’s experience demonstrates that Six Sigmacan be used effectively in nonmanufacturing,highly qualitative contexts. For organizations thathave had to rely upon anecdotal opinions and po-litical influence to drive qualitative strategicchanges, Six Sigma holds promise for lending thecustomer’s voice, as well as structure and objec-tivity, to these types of management challenges. �

the managers’and nonmanagers’perceptions aboutthe EPMS (Questions 1–4 and 11)—a main areaof the COA project focus—including wider use ofthe EPMS for goal setting and greater clarity aboutgoals. Future efforts of the COA project team willaddress issues related to salary planning and ca-reer development (Questions 7–10).

The use of Six Sigma led to the implementa-tion of a Balanced Scorecard and revisions to theEmployee Performance Management System,which were significant improvements to the twoprocesses at Amdell most important for a COA—Clear Expectations and Rewards and Conse-quences. These changes supported a stronger cul-ture of accountability in five ways:

• The BSC clarifies and communicatesAmdell’s performance expectations to allof its employees.

• The revised EPMS requires each employeeto prioritize and be held accountable forfive performance goals that are linked tothe BSC, thereby directing employee ef-forts toward those areas most likely to pro-duce good business performance and long-term success for the company.

• Six to ten measures from the BSC are usedto determine the bonus pool for all Amdellemployees, thereby forging a direct linkbetween a significant reward for employ-ees and the achievement of results impor-tant to the company.

• The revised 9-point EPMS grading scale,coupled with the investment in construc-tive feedback training, improves Amdellmanagers’ ability to discriminate betweenstrong, average, and weak performers.

ADDITIONAL RESOURCESHammer, M. (2002). Process management and the future of Six Sigma. MIT Sloan Management Review, Winter, 26–32.