Shares Investment Malaysia Edition Issue 22

36

PP 14523/03/2010(023784) • MICA (P) 025/04/2009 Uncover the secrets to your wealth ™ ISSN 1793-7280 ISSUE 22 07/12/09 - 10/01/10 OTHER FEATURES Markets headed for consolidation The proposed 4% GST Banking on improved performance RESILIENT RUBBER: FROM PRODUCER TO MANUFACTURER

-

Upload

pcl-printers-pte-ltd -

Category

Documents

-

view

220 -

download

0

description

Shares Investment Malaysia Edition Issue 22

Transcript of Shares Investment Malaysia Edition Issue 22

PP 14523/03/2010(023784) • MICA (P) 025/04/2009

Uncover the secrets to your wealth™

I S S N 1 7 9 3 - 7 2 8 0

ISSUE 22 07/12/09 - 10/01/10

OTHER FEATURES

Markets headed for consolidation

The proposed 4% GST

Banking on improved performance

RESILIENT RUBBER:FROM PRODUCERTO MANUFACTURER

MSH_Cover22.indd 1 12/2/09 2:22:00 PM

MALAYSIA

Information in this guide has been obtained from sources believed to be reliable. However, its accuracy or completeness is not guaranteed. While every precaution is taken to ensure accuracy, the publisher accepts no liability for any error which may arise.The articles are based on the opinions of the various authors and do not represent the opinions of this publication and/or the opinions of the organisation he/she represents.In no event is SHARES INVESTMENT liable for all and/or any direct or indirect loss arising from any use or any reliance of any information provided.

FEATURES

p4 Resilient Rubber

p6 Markets Headed For Consolidation

p8 GST At 4%

p10 Momentum Weakening, Time For A Break?

p12 Introducing New Fuel Subsidy Scheme With Care

p14 Maximising A Return

p17 Banking On Improved Performance

p20 Christmas Comes Early For CapitaMalls Asia

■ CONTENTS ■ ■ Issue 22 ■ 07 Dec - 10 Jan 2010

PERSPECTIVE p4

All materials printed in SHARES INVESTMENT are protected under the copyright act. All rights reserved. No part of this publication may be reproduced in any form or by any means without the written permission of the publisher. Information in the publication should not be taken as offer/ advice to buy or sell securities.We, our associated companies and / or their officers, directors and employees may own or have positions in securities mentioned in the publication, and may from time to time, add on to or dispose of such securities.

p8

Malaysia used to be the world’s biggest producer of natural rubber. It lost its dominance as the supplier for one-third of the world’s output in 1985 with the country’s shift towards industrialization.

p14

MSHE_1-2_Content.indd 1 12/3/09 5:18:53 PM

p17

REGULARS

p23 Market Indices

p26 Foreign Indices

p28 Market Capitalisation

p30 Major Trades

p32 Most Active Shares

p34 Hitting 52-Week High

p35 Hitting 52-Week Low

p36 Top Gainers

p38 Top Losers

p40 Lowest P/E

p42 Highest Yield

p44 Highest Margins

p46 Highest ROA

p48 Profit & Loss

p50 Upcoming Results Announcements

p52 Entitlements (cd, xd, cb, xb…)

p54 Performance of Recent IPOs

p55 Discount to NAV

p56 Mainboard Companies A-Z

p246 ACE Market Companies A-Z

p247 Investment Trust

p251 Warrants A-Z

p256 Inactive Shares, Warrants & Loanstocks

p267 Companies Index A-Z

ShareS InveStment (malaySIa) is published once a month.

We welcome contributions from readers, as well as from finance professionals. Please fax or e-mail ([email protected]) should you also have any queries, remarks or suggestions.

Supported by

PUBlISherPioneers & leaders (malaysia) Sdn Bhd(Co. No. 660679-A)Unit 901, Level 9, City PlazaNo 21, Jalan Tebrau80300 Johor Bahru, MalaysiaTel : (03) 7875 6908 / (65) 6745 8733Fax: (65) 6745 8321

editor-in-chief Phan Tjun Serneditorial Director Lew Poh ChanSenior Consultant Dr Ho Kah Leongeditor Sang Ah Kewregional research editor Clement Kanresearch editor Stephen Chinresearch executives Aw Jie Sheng David Chung Donavan Lim Lai Wyai Kay Lee Szu Yung Soo Yin Ling Xavier Limtranslators Catherine Mak Choo Ai Loon Yong Chia Win

❖ executive Director Christopher Fun(Business Development) regional Business S. KrishnamoorthyDevelopment manager

Sales & marketing manager Clay FoomarKetInG rePreSentatIvenextvIeW Sdn Bhd(Co. No. 574271-D)Letter Box No. 8Level 8, Menara TM Asia Life189 Jalan Tun Razak, 50400 Kuala LumpurTel : (603) 2770 9388Fax : (603) 2770 9366PrIntervivar Printing Sdn Bhd (Co. No. 125107-D)Lot 25, Rawang Integrated Industrial Park 48000 Rawang Selangor Darul Ehsan Tel : (03) 6092 7818Fax : (03) 6092 8230DIStrIBUtInG aGentlife Publishers Berhad (10937-w)Tel : (603) 7620 2118 Fax : (603) 7620 2113

w w w . s h a r e s i n v . c o m

MSHE_1-2_Content.indd 2 12/3/09 5:19:14 PM

• editorial desk •

How time flies when you are having fun. It was not a lot of fun some 12 months ago when the world was in the throes

of a financial crisis. Economists and analysts tried to reassure everyone that in 1H09 things will bottom out and a recovery will be seen in 2H09.

As the year draws to a close, we are seeing a gradual recovery and the downslide did not seem to hurt as much as feared – though to many, it did hurt a lot, as unemployment data will attest. If only our economy is as resilient as rubber: it would bounce back in a jiffy!

This issue, we feature an exclusive interview with Minister for Plantation Industries and Commodities, Tan Sri Bernard Giluk Dompok, who shared his views on the rubber industry. It may interest you to know that Malaysia has no intention to regain its crown as the world’s top rubber producer. No, our land resources are too scarce and can be put to better use.

Yet, there are big plans for downstream

rubber industries, which is good news for the manufacturing sector, and in turn, investors in such companies. Find out more in our Perspec-tive article.

Fiscal reforms are also in the pipeline with the impending introduction of the Goods and Services Tax (GST). It will not be for at least another 18 months, but the government has al-ready let on that it will be a low 4% rate, and the GST will replace the current sales and service taxes, which are at a higher 5% to 10%.

Nonetheless, concerns linger regarding its implementation and businesses are particu-larly concerned since the tax is paid upfront for every transaction, and refunds must be claimed to prevent over-taxation. Will there be an adequate system in place to cope with this massive paperwork?

Happy investing and have a prosperous New Year! To our Christian readers, we also bid you a Merry and Blessed Christmas. May there be many great stocks in your stocking!

Clarification:In our November 2009 (#21) edition, the author of the article “What Are Shariah-Compliant Securities?” is the Securities Industry Develop-ment Corporation (SIDC) and not as published. In addition, the website of the Securities Com-mission should read as www.sc.com.my and not www.sc.org.my as printed. We deeply regret the error.

3

MSHE_3_Editorial.indd 3 12/3/09 5:03:47 PM

4

diversify rubber products from NR-base latex products to SR-based industrial rubber goods, especially in automotive and engineering components. Con-sumption of SR is expected to increase to 153,000 tonnes by 2010, 205,000 tonnes in 2015 and 270,000 by 2020.

The Third Industrial Master Plan (3IMP) envisaged the production of seismic bear-ings, rubber fender systems, automotive rubber-metal com-ponents and high-pressure hoses, for example. “The strat-egy is to manufacture high-end specialised products where Malaysia has the compara-tive advantage in research & development support and ex-pertise,” he said.

Since the 1970s, the Ma-laysian Rubber Board (MRB) has been developing rubber seismic bearing technology to be used in earthquake-prone countries. This would protect buildings, people and contents within buildings during earth-quakes. The effectiveness of such technology was evi-dent in Northridge (1994) and Kobe (1995): buildings with such technology withstood the quakes better than those that did not.

“The government is also actively implementing steps to further broaden applications into high value-added and high technology areas, such as engineering, marine, automo-tive, aeronautical and military

applications.“With the rubber products

industry entering a mature phase, and increasing com-petition from countries such as Thailand and China, issues such as creativity, innova-tion, efficiency, cost reduction and product designs will be a priority. Market access and penetration will depend not only on competitive pricing but customised products of high or improved quality,” Tan Sri Bernard explained.

To this end, the Ministry is encouraging R&D and pro-tecting intellectual property (IP). “Intellectual property reg-istration is the first priority. Our Technology Management Office (TMO) is looking for ways to protect our inventions, including the application of laws such as the Patents Act, 1983, Copyright Act 1987, In-dustrial Designs Act 1996 and the Trade Marks Act 1976.

Malaysia used t o be t he world’s big-gest produc-er of natural

rubber. It lost its dominance as the supplier for one-third of the world’s output in 1985 with the country’s shift towards industrialization. The lucrative prices of crude palm oil also led many plantation estates to change crops, favouring oil palm over rubber.

Yet, the rubber industry re-mains important to Malaysia, stressed Minister of Plantation Industries and Commodities, Tan Sri Bernard Giluk Dom-pok, in an exclusive inter-view with Shares Investment (Malaysia).

Malaysia does not aim to re-gain its position as the world’s top producer, he said. “We are constrained by a short-age of labour and competitive land use. Our direction is on value-added industrial and general rubber products,” he explained.

Malaysia is the largest pro-ducer of latex gloves. Global demand for gloves is expected to grow by 10%-12% annually, Tan Sri Bernard said. The de-mand for natural (NR) and syn-thetic (SR) latex is expected to grow in tandem.

In 2008, the domestic rubber industry consumed 603,191 tonnes of rubber, of which 77.7% was natural rubber. The government’s strategy is to

PersPectivetext : Stephen Chin & Paul Yeo

RESILIENT RUBBER

Tan Sri Bernard: The rubber industry remains important to Malaysia

MSHE_4-5_Perspective2.indd 4 12/3/09 5:18:27 PM

5

“The MRB also has an IP committee to ensure IP protection and facilitate the propagation of technologies to authorised stakeholders. The committee oversees IP registration for the MRB and works closely with IP agents to stay up-to-date and avoid ad-ministrative errors in the filing process,” he explained.

The MRB is also guided by the Ministry of Science, Technology and Innovation’s IP Policy which encourages scientists to protect their inven-tions and be rewarded when their R&D findings are suc-cessfully commercialised.

Investments in rubber man-ufacturing have been very encouraging, said Tan Sri Bernard. Investment grew at CAGR of 25.5% from RM328m in 2003 to RM812m in 2007, although total investments dipped to RM696m in 2008 due to unfavourable economic conditions, he explained.

The government offers vari-ous incentives to encourage investment in this sector, such as tax exemptions and allow-ances, incentives for investors producing certain rubber prod-ucts, and incentives for compa-nies setting up manufacturing plants in promoted areas such as Kelantan, Terengganu, Pa-hang, Perlis, Mersing in Johor, Sabah and Sarawak. For in-stance, imported raw materials and machinery or equipment not produced locally are ex-empted from import duty.

PLANTATION STILL A PRIORITY

Rubber planting and har-vesting are still important to

Tan Sri Bernard’s Ministry as they are a main source of income for about 250,000 smallholders in rural areas. “A rubber tree is a virtual Au-tomated Teller Machine. It generates income on tap. Rubber latex and sheet rubber can be stored and sold when needed, unlike palm oil which must be processed almost immediately,” he explained. “Therefore, the government will continue to improve tree and land productivity for areas planted with rubber. “

The MRB is responsible for the development of the Malay-sian rubber industry. Initially, its activities were centred on upstream activities. Since the 1950s, it produced a series of high latex-yielding clones. In recent years, it shifted its focus to produce clones called latex-timber clones that have a high latex yield and produce quality rubber wood.

“Consumers know that rub-ber wood comes from farmed trees. This is appealing to countries that are environ-mentally conscious and want to protect natural rainforests by avoiding hardwood timber,” Tan Sri Bernard explained.

The MRB also developed latex harvesting technology that uses gaseous or chemi-cal stimulation to prolong latex flow; improves tapper productivity; and prolongs the economic life of the trees. “So far, the application of the Low Intensity Tapping System has benefited 85,000 small-holders.

“Tappers can improve yields up to 1,500kg per hectare per annum with Ethephon,

and up to 2,500kg per hect-are per annum with gaseous stimulation,” Tan Sri Bernard explained.

The MRB promotes land and management consolida-tion programs to put uneco-nomic holding sizes under a central and more efficient management. “It is always our policy to encourage large-scale holdings to enjoy econo-mies of scale. Smallholdings are often developed as large blocks and placed under cen-tral management. FELDA, FELCRA, RISDA mini-estates and RRIM Panti are examples of such centralised manage-ment,” he said.

“We also encourage private plantation companies to go back to rubber, by replant-ing their hilly and marginal land (areas that are unsuit-able for oil palm planting) with rubber. Incentives such as Reinvestment Allowance, Accelerated Agricultural Al-lowance, Pioneer Status and Promoted Areas, and high rubber prices have attracted many plantation-based com-panies to do so.

“The government also promotes sustainable forest plantations with monetary and fiscal incentives. In such programs, rubber is the pre-ferred species. The wood can be harvested when the trees are 16-years-old, but from year nine onwards, latex can be tapped to generate income and provide additional raw material to rubber-based industries. This program is administered by Forest Plan-tation Development Sdn Bhd,” he said.

MSHE_4-5_Perspective2.indd 5 12/3/09 5:04:39 PM

6

Benny Lee is a private trader and chief market strategist for the NextVIEW Group. The NextVIEW Group is a group of companies in the Asian region that provides a leading real-time investment tool for both professional and retail investors. NextVIEW is also a leading Investor Education training provider. For more information, log on to www.nextview.com.

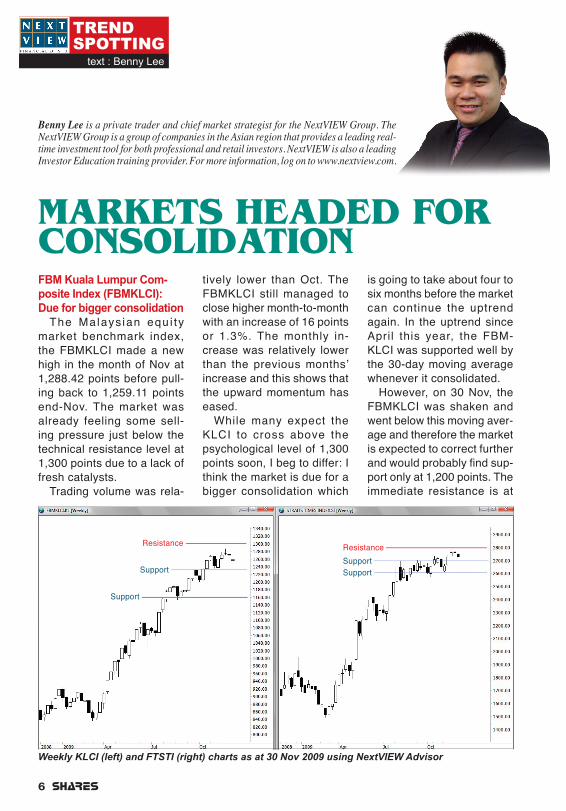

MARKETS HEADED FOR CONSOLIDATION

tively lower than Oct. The FBMKLCI still managed to close higher month-to-month with an increase of 16 points or 1.3%. The monthly in-crease was relatively lower than the previous months’ increase and this shows that the upward momentum has eased.

While many expect the KLCI to cross above the psychological level of 1,300 points soon, I beg to differ: I think the market is due for a bigger consolidation which

is going to take about four to six months before the market can continue the uptrend again. In the uptrend since April this year, the FBM-KLCI was supported well by the 30-day moving average whenever it consolidated.

However, on 30 Nov, the FBMKLCI was shaken and went below this moving aver-age and therefore the market is expected to correct further and would probably find sup-port only at 1,200 points. The immediate resistance is at

FBM Kuala Lumpur Com-posite Index (FBMKLCI): Due for bigger consolidation

The Malays ian equ i ty market benchmark index, the FBMKLCI made a new high in the month of Nov at 1,288.42 points before pull-ing back to 1,259.11 points end-Nov. The market was already feeling some sell-ing pressure just below the technical resistance level at 1,300 points due to a lack of fresh catalysts.

Trading volume was rela-

Weekly KLCI (left) and FTSTI (right) charts as at 30 Nov 2009 using NextVIEW Advisor

Trend spoTTing

text : Benny Lee

Resistance

Support

Support

ResistanceSupportSupport

MSHE_6-7_TrendSpotting.indd 6 12/3/09 5:05:13 PM

7

(Continues on Pg 9)

1,280 points.

FTSE Straits Times Index (FTSTI): Heading towards immediate support level

I n m i d - N o v, t h e F T-STI managed to test the 2,700-point immediate re-sistance level and rallied to the next resistance level at 2,800 points, climbing to as high as 2803.83 points. How-ever, the market fell steeply in the last two trading days of the month by falling about 70 points or 2.5% to close at 2732.12 points.

On a month- to -month basis, the benchmark in-dex still closed positively by an increase of 81 points or 3%. Trading volume de-clined slightly in the past few months. Investor con-fidence in the market has been weak.

The FTSTI is still in an uptrend and since April this year when the uptrend start-ed, it has been supported by the 60-day moving average.

The moving average is cur-rently at 2,685 points and this should be the immediate support level. The pattern from the chart shows that the market has strong support at 2,600 points.

The FTSTI is expected to head towards the immediate support level before continu-ing the trend. There is still a chance for the benchmark index to climb to the uptrend technical target of 3,000 points but this is unlikely to happen in the next four to six months. Immediate resis-tance level is 2,800 points.

Hong Kong Hang Seng Index (HSI): Stronger bearish pressure

As one of the major financial hubs in Asia, the Hong Kong equity market took a plunge after Dubai announced its problems in paying its debts and sparked fears of another financial crisis.

The HSI gapped down and fell slightly more than

1,000 points or 4.8% on 27 Nov to close at 21,134.50 points. However, the market rebounded at the end of the month to close at 21,821.50 points.

In the middle of Nov, the HSI peaked at 23,100 points, the highest since August last year. Trading volume, which continued to decline slightly in the past few months, was quite high in the last few days of Nov.

The HSI rebounded ex-actly on the 90-day moving average. Since April this year, the HSI was supported by the 60-day moving aver-age but the 27 Nov plunge broke this support level. However, the benchmark index climbed back above the 60-day moving average. The upward momentum for the past three months has been weak. The momentum indicators started its diver-gence from the uptrend since

Resistance

SupportSupport

Weekly HSI (left) and DJI (right) charts as at 30 Nov 2009 using NextVIEW Advisor

Resistance

MSHE_6-7_TrendSpotting.indd 7 12/3/09 5:05:30 PM

8

ness and make Malaysia a more attractive destination for foreign direct investments and businesses.

Whilst businesses gener-ally have the responsibility to account for GST and remit the taxes to the government, the man in the street bears the burden of the tax, Chew Theam Hock, executive di-rector of KPMG, told Shares Investment (Malaysia). “By introducing GST at a low rate, the impact can be softened or managed,” he added.

KPMG executive director, Tan Eng Yew, added that in principle, GST should apply across most goods and ser-vices. “Ideally, GST should not distort investment, production and consumption decisions. As such, it should generally not affect the stock market. Empirically, the introduction of GST In other countries has not had a significant impact on the stock markets,” he explained.

Asked on the likely tax treat-ment that would be applied to the stock market, Tan said the general treatment used in other countries could be adopted here as well:• The issue of shares or

securities – to exempt supply

• Brokerage and other fee-based services – taxable supply

• Late payment interest – exempt supply

Usually, Chew said, GST is

introduced as a package that includes a reduction of income taxes, particularly personal income taxes, and the aboli-tion of some other taxes. “The government has announced the replacement of sales tax and service tax, but has not indicated its plan on personal income tax,” he said.

An ideal GST structure should be broad-based single-rate regime for simplicity’s sake, Chew said. It should also be fixed at a low rate so as not to be too burdensome on the public, and exemption applied for essential items to further ease the burden on the public. However, he added, exemptions should be kept to a minimum as they have a tendency to create complexity and confusion.

Tan suggested that Free Zones or the equivalent be maintained to encourage ex-

After deferring the proposed broad-based G o o d s a n d Services Tax

(GST) during Tun Abdullah Badawi’s tenure as prime minister, the government is finally going ahead with its implementation. It plans to introduce a 4% GST in 2011 and expects to earn RM1b in the first year. The tax legisla-tion is expected to be tabled for first reading in Parliament this month, and may be imple-mented in mid-2011.

Second Finance Minis-ter, Dato’ Seri Ahmad Husni Hanadzlah told Bernama news agency that the GST will not put pressure on prices as it replaces the current sales and services tax, at 5% and 10% respectively. To ease the burden on consumers, staple foods such as rice, sugar, cooking oil and flour will be exempted.

Maybank Investment Bank’s chief economist, Suhaimi Ilias said the GST is needed to reduce the country’s growing dependence on petroleum-based revenues, and to ad-dress the imbalance in the tax structure caused by nar-row-based sales and service taxes; falling revenues from trade-related duties (due to multilateral and bilateral free trade agreements); and a low-ering of direct income taxes to boost economic competitive-

PersPectivetext : Stephen Chin

GST AT 4%

Chew: By introducing GST at a low rate, the impact can be softened or managed

MSHE_8-9_Perspective.indd 8 12/3/09 5:23:37 PM

9

port-based businesses.It is also important for the

government to provide clear transitional rules leading up to the GST’s implementation, he added.

Maybank IB’s Suhaimi said the public must also be edu-cated to ensure a buy-in. He also stressed the importance of having the right systems in place. “The customs depart-ment and corporations must have the right systems in place. So sufficient prepara-tion time is vital, especially for SMEs,” he said.

“Test runs must be done to ensure efficiency of process-ing claims for GST rebates as delays will hurt the cash flow of companies since they pay GST for their inputs and then

claim from the government,” he added.

The Federation of Malay-sian Manufacturers (FMM) voiced the same concerns when it issued a statement in October. “The greatest concern of businesses, in particular, exporters, was the efficiency of refunds. The International Monetary Fund identified the efficiency of the refund mechanism as the Achilles’ heel of any GST system,” it said.

Efficiency depends on the quantum of refunds, the man-power to process the claims and the level of confidence in clearing and issuing re-funds without carrying out pre-refund audits. “As Malay-sia is a highly export-oriented

economy, GST refunds can be as high as 58.3% based on FMM’s estimates in 2005. The promise of refunds within 14 days could be difficult to fulfill,” it said.

Tan: GST should not distort investment, production and consumption decisions

(From Pg 7)

Sept, which indicate stron-ger bearish pressure. This shows strong resistance and there is a little chance for the HSI to move higher above the recent peak of 23,100 points. The HSI may test the 90-day moving average support level again at 21,250 points and if this is broken, the market may continue to move further downwards to the next support level at 20,400 points.

US Dow Jones Industrial Average (DJI): Momentum indicators are neutral

Investors in the US were start led by Dubai ’s debt problems on their national holiday celebrating Thanks-

giving Thursday. The panic caused investors to sel l on Friday and forced the DJI to fall 154.48 points or 1.48% to close at 10,309.92 points. The DJI went as low as 10,231 points intraday before rebounding to close higher.

On the last day of Nov, the DJI slightly rebounded to close at 10,344.84 points. The selling pressure was not as bad as expected despite heavy losses in the Asian and European markets when the US was on holiday: it was buffered by improved consumer spending, jobless claims and home sales.

Trading volume was unex-pectedly low as investors did not rush to sell, but preferred to hold on and wait for further

developments. The DJI is currently still in an uptrend supported strongly by 60-day moving average. The 60-day moving average is currently at 9,900 points and the DJI is expected to pullback to this immediate support level.

Momentum ind ica to rs have gone into the neutral zone, but in the long term, the uptrend is still strong because these indicators are in convergence with the uptrend. If the immediate support level is broken, the DJI may fall further into cor-rection and find support at 9,700 points. However, if the immediate resistance level at 10,500 points is broken, the market may rally strongly to the next resistance level at 10,700 points.

MSHE_8-9_Perspective.indd 9 12/3/09 5:23:52 PM

10

Trend spoTTing

text : Benny Lee

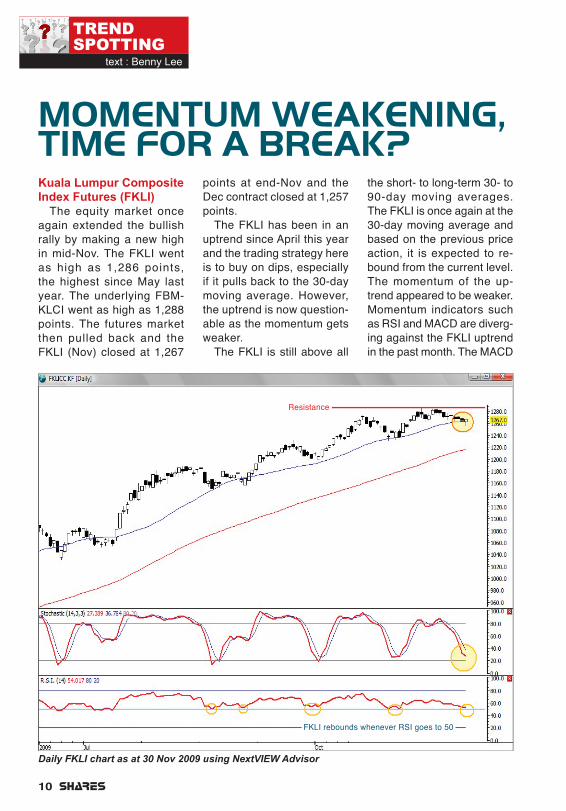

Kuala Lumpur Composite Index Futures (FKLI)

The equity market once again extended the bullish rally by making a new high in mid-Nov. The FKLI went as high as 1,286 points, the highest since May last year. The underlying FBM-KLCI went as high as 1,288 points. The futures market then pulled back and the FKLI (Nov) closed at 1,267

MOMENTUM WEAKENING, TIME FOR A BREAK?

points at end-Nov and the Dec contract closed at 1,257 points.

The FKLI has been in an uptrend since April this year and the trading strategy here is to buy on dips, especially if it pulls back to the 30-day moving average. However, the uptrend is now question-able as the momentum gets weaker.

The FKLI is still above all

the short- to long-term 30- to 90-day moving averages. The FKLI is once again at the 30-day moving average and based on the previous price action, it is expected to re-bound from the current level. The momentum of the up-trend appeared to be weaker. Momentum indicators such as RSI and MACD are diverg-ing against the FKLI uptrend in the past month. The MACD

Daily FKLI chart as at 30 Nov 2009 using NextVIEW Advisor

Resistance

FKLI rebounds whenever RSI goes to 50

MSHE_10-11_NextView.indd 10 12/3/09 5:06:31 PM

11

is currently at its lowest since July. The Stochastic indicator is currently oversold.

We may expect a rebound to happen in the very near term but it may not rally as strongly as before because of a strong resistance at 1,300 points. However, the market may face immediate resistance at 1,280 points. This provides a l itt le po-tential upside if the plan is to go long at current levels between 1,250 and 1,260 points. The immediate sup-port level is at 1,250 points and a stop should be placed below this level.

So, the plan to go long at, say 1,260 points, provides a

potential profit between 20 to 30 points, with a risk of 10 points. It is too early to have a short strategy as the uptrend is still intact.

The Average True Range (ATR) indicator reading is 11 points, which means a stop loss of 15 points should be sufficient. Therefore, trad-ing risk should be 15 points, or stop loss placed at 1,245 points if going long at 1,260 points. The potential reward-to-risk ratio may not be at-tractive in the current situ-ation and I would probably take a rest from trading this month. However, if I were still interested, I would think of going long.

Daily FCPO chart as at 30 Nov 2009 using NextVIEW Advisor

Crude Palm Oil Futures (FCPO)

Just a month ago, the FCPO was at RM2,200 per metric ton and the strategy was to go long with a RM2,400 price target. The price of FCPO went as high as RM2,482 with an intraday high of RM2,521 before pulling back to settle at RM2,472 end-Nov. The re-sistance in Aug was RM2,521 as well and the price fell to RM2,000 in Oct.

The price rally was mainly due to better than expected exports and a rebound in the US dollar. Now that the price has moved to the resistance

(Continues on Pg 13)

Resistance

Averages

MSHE_10-11_NextView.indd 11 12/3/09 5:06:42 PM

12

Just say ittext : Ameer Ali Mohamed

Ameer Ali Mohamed is Director, Financial Research of NextVIEW. He has a total of 20 years experience as a corporate journalist, investment analyst and fund man-ager, including as research head of two stockbroking firms and CEO/CIO of a funds management company.

INTRODUCE NEW FUEL SUBSIDY SCHEME WITH CARE

proper and stringent immigra-tion or check point procedure. In addition, any argument on the price disparity should also include income disparity.

The new fuel subsidy system should take into account its real objective. On one hand it is to reduce the government’s expenditure where RM10b has been allocated on fuel subsidies in the 2010 Budget, on the other it should not be done in a manner that the rich enjoys the benefits more than the poor.

The new system should not mirror the scheme introduced in June 2008 that spanned for one year, it would not serve the purpose in terms of wealth distribution. Under the scheme, those owning cars below 2,000 cc were entitled to a one-time rebate of RM625 when they re-newed their road tax. For those owning cars with 2-litre engines, a RM200 deduction on the road tax payable applied.

Can we assume that those owning motor vehicles of less than 2,000 cc are poorer than those owning cars above that threshold? Definitely not. Just consider these two facts: * A 2.0-litre BMW 320iSE costs

about 2.4 times the price of a 2.5-litre V6 Naza Ria GS (A);

* A 1.8-litre Mercedes Benz E200 costs about both Hon-da Accord 2.4 and Toyota Camry 2.4 combined!There are many more ex-

amples that can be listed. In addition, the rich normally have more than one car and based on the previous scheme, he was entitled to the rebate to as many cars as he owned so long as the engine capacity was less than 2 litres.

If a new subsidy scheme must be introduced, engine capacity should therefore not be the consideration, as it does not serve the purpose of benefiting the rakyat. There are other ways that can be considered.

One of them is the income bracket of car owners. One may argue it would delay the implementation if this approach is adopted due to the need for data accumulation. But the gov-ernment has the Inland Rev-enue Board (IRB) that would be able to provide, not the exact income, but the income range of all who submit their tax returns.

Such an approach would also

Consumers filling up petrol in Malaysia may no longer en-joy fuel subsidy in the present form

if a new subsidy system is in-troduced in the second quarter of next year. Many, especially Malaysians, are waiting to see whether the new system to be introduced is fair to everyone.

Finance Minister II Datuk Seri Ahmad Husni Hanadzlah recently was quoted as saying that the new structure of the fuel subsidy system would be ready by April 2010. The system would enable huge savings on the part of the government.

Among the possibilities, ac-cording to the Minister, are that those in the higher income bracket and tourists would not be eligible for the subsidy. An-other criterion being studied currently is a subsidy system that is benchmarked against the engine size of motor vehicles.

Granted, there is now a dis-parity between petrol and diesel prices in Malaysia and those in neighboring countries such as Thailand and Singapore, but not in Brunei. However, this should not be an issue with a

MSHE_12-13_JustSayIt.indd 12 12/3/09 5:20:14 PM

13

entice all salaried, non-salaried as well as small-, medium- and big-time entrepreneurs to submit tax returns to IRB, regardless whether they meet the minimum income to be tax payers. Non-submission would only mean that they will not be considered at all for the fuel subsidy scheme.

Exception should however be given to students at the un-dergraduate and post-graduate levels so long as they do not have income such as those taking full pay leave during their studies.

Each entitled Malaysian should however only be given

a certain maximum litre of fuel per month at subsidized price, and any consumption above the threshold to be determined should be at market rate. The entitlement should also be for-feited once every quarter or half year if it is not fully used. Hence the need to use MyKAD.

Such a scheme should also be extended to critical sectors if removal of the current subsidy would result in extreme pres-sure on inflation. Examples include public transport as well as companies involved in trans-porting essential goods and services. However, company cars should be excluded as

the companies have already benefited from some corporate tax advantages.

Non-Malaysians whether or not they live in Malaysia as expatriates or diplomats, as well as tourists should not enjoy such a subsidy scheme – they should pay the current rates.

Whatever being introduced April 2010, it should fair to all Malaysians and the economic principles in wealth distribution must be considered. It would be a respectable move if the committee tasked for this study seeks opinions from various parties before submitting its proposal to the Minister.

level, we should apply a new strategy.

With a strong rally in FCPO prices, all technical indicators will show strong bullish signals. Momentum indicators like RSI, Momentum and MACD con-tinue to make new highs and the price stays above the moving averages. However, the price is way above the averages which shows that it is overbought. The short- to long-term 30- to 90-day moving averages are currently between RM2,240 and RM2,290. It is clear that a cor-rection may soon take place.

A pullback is expected when

prices are overbought. A trading plan to go short may be applied. The FCPO is expected to move to the support level at the mov-ing averages, especially the short-term 30-day moving aver-age at RM2,290. A stop can be placed above RM2,520.

Therefore, a low-risk trading opportunity can be found when the price is between RM2,470 and RM2,500. To go long, traders should wait until the price finds support at around RM2,300.

Market volatility has slightly increased. The 14-period ATR indicator currently reads 53 points. A stop loss should be put

no less than the ATR to prevent being stopped out too early. A better and safer stop loss is 1.5x the ATR and it should be at least 70 points.

So, if I plan to short at the cur-rent price of RM2,470, I should place stop loss at 2,540 points (which is above the RM2,520 resistance level) and have a potential profit of RM170, based on a RM2,300 price target. This provides an average risk-to-reward ratio of more than two times. Therefore, going short above the current price level with the same stop loss of 70 points provides a better reward-to-risk ratio.

(From Pg 11)

Data Reference Month Scheduled Released DatesExternal Trade Oct 2009 4 Dec 2009International Reserves as at 30 Nov 2009 7 Dec 2009Index of Industrial Production Oct 2009 10 Dec 2009Salaries / Wages (manufacturing) Oct 2009 10 Dec 2009Consumer Price Index Nov 2009 16 Dec 2009International Reserves as at 15 Dec 2009 22 Dec 2009Producer Price Index Nov 2009 31 Dec 2009Malaysia Economic DiarySource: Websites of Department of Statistics of Malaysia and Bank Negara Malaysia

MSHE_12-13_JustSayIt.indd 13 12/3/09 5:20:29 PM

14

Corporate Digest

text : Stephen Chin

The investability weighting was surprising low, said OSK. “We had assumed a weight-ing of 70%. However, there may be some changes in the computation of this weighting in December and Maxis may be an early reflection of these changes,” it added.

For the relisting, Maxis of-fered 2.25b shares via an offer for sale by its majority shareholders. Institutional in-vestors received a lion’s share of 2.04b (90.7%) shares.

Unlike the previously listed vehicle which included over-seas ventures in India and Indonesia, Maxis Communi-cations Bhd (MCB), the new listed entity comprises only Maxis’ domestic mobile busi-nesses. While this deprives in-vestors of long-term revenue potential, it also removes the strain on Maxis’ cash flow which was previously used to fund overseas expansion, OSK said.

Maxis will be a stock that “provides sustainable and

strong dividend yields similar to listed mobile telcos in mar-kets where growth has leveled off,” OSK Research said.

Maxis chief financial officer, Rossana Annizah Ahmad Rashidi was quoted in the press as aiming to pay out 75% of net profit as dividend.

OSK pointed out that Maxis’ dividend policy is among the more aggressive of Malaysian telcos. TM has a two-pronged dividend payout guidance of a minimum RM700m or 90% of earnings, whichever is higher. Digi has a revised 80% payout target, which translates into respective yields of 7%-8%. “We expect Maxis and Digi to be pitted alongside each other in rewarding shareholders via generous dividends and po-tential capital management,” it said.

The Malaysian mobile tele-communications scene is fiercely competitive. Three major 3G operators, name-ly Celcom, Digi and Maxis, dominate the market with a

Maxis Bhd’s r e l i s t i n g on 19 Nov r a i s e d a great deal

of interest in the local equi-ties market. “It was the biggest IPO for Bursa Malaysia this year, boosting stock mar-ket velocity and breadth in a single stroke,” remarked OSK Research in a report.

Transactions for Maxis shares accounted for almost half of the total transaction value for the entire market on 19 and 20 Nov. On the first trading day, 305.8m Maxis shares worth RM1.6b changed hands.

The significance is not lost on Bursa, as it fast-tracked Maxis’ entry into the FBM KLCI, nudging out Malaysia Airlines. On 20 Nov, Maxis was included in the compos-ite index with an investability weighting of 30% and an im-plied weightage of 2.84%. It was the 11th largest compo-nent of the index.

MAXIMISING A RETURN

MSHE_14-15_CD.indd 14 12/3/09 5:21:05 PM

15

collective 95% market share. In recent years, mobile virtual network operators (MVNOs) have joined the fray but they lack coverage and marketing funds.

OSK projects mobile pen-etration to reach 109% by end-2009 and rising there-after to 118% and 122% in 2010 and 2011 respectively. It also expects subscriber growth to slow from 12% in 2009 to 7% by 2011. “Mobile revenue growth will deceler-ate to low-to-mid-single digit growth by 2011 from the mid-to-high single digit growth in 2009,” it added, citing weak subscriber growth and pres-sure on average revenue per user (ARPU).

The key growth catalyst will come from data and non-voice revenues, it predicted. The data revenue market is projected to grow by a compounded annual growth rate (CAGR) of 20.2% over the next three years, driven by the proliferation of smart phones, higher adoption of wireless broadband and in-creasing use of mobile In-ternet. Broadband market penetration is currently below 30%, said OSK.

Frost & Sullivan reported mobile data revenue in Ma-laysia grew from RM1.57b in 2004 to RM4.41b in 2008, at a CAGR of 29.4%. Over the same period, mobile data revenue doubled to represent 25.3% of the overall industry mobile revenue. OSK esti-mated a CAGR of 25.5% from FY09 to FY12.

Maxis’ overall market share for both prepaid and postpaid

services has been shrinking due to strong competition from Digi and Celcom. “Cel-com’s prepaid additions have overtaken Maxis since 3Q08 due to Celcom’s aggressive acquisition campaigns tar-geted at youths outside the Klang Valley,” OSK noted. Celcom increased its market share by 4%-points over the last eight quarters at Maxis’ expense, said OSK, gaining ground in the youth and en-terprise segments.

Despite voice revenue de-clining due to competitive tariff and a slowing market, Maxis’ data revenue grew by a CAGR of 29% between FY06 and FY08, due to the adoption of 3G mobile servic-es, mobile Internet and wire-less broadband services.

Maxis presently derives about 90% of its revenue from mobile services, with the remainder split between fixed line and international gate-way revenues. In FY08, voice and data revenues accounted for 71% and 29% of mobile revenues respectively.

By 1H09, data revenues grew to represent 31.1% of mobile revenue, compared to Celcom’s 2% and Digi’s 19%. OSK forecasts the proportion of data revenue to widen to 35%-40% over the next two years. “Maxis already has a sizeable proportion of high ARPU for enterprise and data subscribers to support strong growth,” it noted.

Despite being the f irst to launch wireless mobile broadband in Sept 2006, Maxis failed to capitalize on its first-mover advantage

due to network congestion problems. It also lost sub-scribers to competitors who offered cheaper packages and bundled modems, OSK noted. Maxis added 31,000 mobile broadband subscrib-ers in 1H09 compared to Celcom’s 192,000.

Competition is also heating up with the emergence of WiMAX broadband services. Packet One plans to double its subscriber base in the next 12 months with some 700 sites installed nationwide. TM is also due to roll out its high-speed broadband in 1Q10. To mitigate this, Maxis has been continuously upgrading the capacity of its core network and launching more aggres-sive customer retention initia-tives, OSK noted.

Maxis’ management is tar-geting to double its mobile broadband subscriber base (171,200 as at end-2Q09) by the end of 2009. It recently launched a new campaign – “Something for Everyone” with attractive plans ranging from RM8 per day to RM48 per month.

The telco may also mitigate eroding ARPUs by cross-selling voice and data prod-ucts through bundling pack-ages. Maxis is also eyeing the youth segment (15-24 years old) particularly for data services. The segment repre-sented 18.4% of Malaysia’s total population in 2008.

Mobile operators would do well to target areas where mobile penetration is still low, such as the rural markets in East Malaysia and the east coast.

MSHE_14-15_CD.indd 15 12/3/09 5:21:19 PM

Thank you for your support in 2009.

With the management and staff of the Pioneers & Leaders Group,

the Shares Investment family

wishes our readers and their families

a very blessed Christmas and Happy New Year!

Gearing You Towards Investment Success!

™

Full_Ad_2009.indd 3 12/3/09 4:17:06 PM

17

Net NPL was 2.19% (down from 2.44% in June 2009).

The improved outlook has prompted Maybank Investment Bank to upgrade its net profit growth forecasts to 9% p.a. The stock continues to offer good exposure to banking sector recovery, it said.

AMMB is proceeding with plans to acquire MAA’s gen-eral insurance business for RM180m, but will abort its planned 4.9% acquisition of MAA’s takaful insurance sub-sidiary. The deal will make AMMB’s 51%-subsidiary, AmG Insurance, one of Malaysia’s largest general insurers.

Malayan BankingMaybank recorded a 1Q10

net profit of RM881.8m (+54.1% y-o-y; -178.9% q-o-q), on rev-enue of RM3.2b (+54.1% y-o-y; -4.5% q-o-q). On an annualized basis, the 1Q10 results were 24.9% ahead of market con-sensus, said OSK.

The strong results were due

to a 28.7% increase in net inter-est income; a relatively robust annualized loans growth of 11%; a 130.7% y-o-y jump in non-interest income in tandem with an 807.9% surge in invest-ment and trading income; and a 36% increase in commission fee-based income. Therefore, operating profit grew y-o-y de-spite a 125.2% y-o-y increase in loan loss provision.

The results were also partially driven by trading gain of almost RM80m from the sale of gov-ernment securities. This may fall to more normalized levels in subsequent quarters. Maybank also enjoyed a one-off RM25m tax credit at its subsidiary, Bank Internasional Indonesia.

RHB CapitalRHB Capital reported a 3Q09

net profit of RM334.8m (+1.5% y-o-y, +11.0% q-o-q) on rev-enue of RM922.9m (+6.7% y-o-y, -0.5% q-o-q).

OSK said RHB’s annualized 9M09 earnings were 16.5%

AMMB HoldingsAMMB Holdings recorded

2Q10 net profit of RM240.2m (+4.4% y-o-y; -7.0% q-o-q), on revenue of RM845.9m (+25.6% y-o-y, -4.8% q-o-q) due to strong loans growth and low rate of non-performing loans (NPL). This brings 1H10 profit to RM498.4m (+15.1% y-o-y).

The q-o-q drop in revenue (4.8%) and net profit (7.0%) was attributed to 1Q’s surge in bond underwriting fees. The six-month 15.1% growth in net profit came from investment banking while income from retail and business banking was stable.

New loans in 2Q were more than double the previous quar-ter. Loans grew 6.3% in 1H10 from corporate and business segments, especially in bridg-ing loans for mergers and ac-quisitions, and construction projects.

Gross NPL shrank 3.9% in 2Q10 due to write-offs while the formation of new NPL slowed.

compiled : Stephen Chin

INVESTORS’ CORNER

Banking on improved performance

AMMB Holdings (FY Mar 2010) Maybank Investment Bank OSK ResearchResearch dated 18 Nov 2009 9 Nov 2009Forecast EPS 10 (sen) 32.8 30.8PER 10 (x) 14.8 15.7Forecast DPS 10 (sen) 10.2 9.0Div. Yield 10 (%) 2.1 1.9Call Buy BuyTarget price (RM) 5.20 5.35Share price as at 30 Nov, 2009: RM4.85

MSHE_17-19_InvCorner.indd 17 12/2/09 9:12:58 AM

18

and 8.2% above consensus and its own full-year estimates, respectively. This improved performance stemmed from a write-back of RM63m from excess general provisioning and effective cost containment measures. These helped limit RHB’s increase in operating expenses to just 1.9% y-o-y.

RHB’s underlying core per-formance remained robust, OSK noted, despite a chal-lenging macro environment. Pre-provision profits expanded 10.3% y-o-y. On a q-o-q basis, pre-provision profits were 8.6% lower because of 2Q09’s high Islamic income earnings base.

The bank also recorded a 10.0% growth in retail loans, largely on mortgage loans while loans in the corporate business segment grew by a slower 0.8%.

Eastern Pacific Industrial Corp (EPIC)

Despite a lackluster quarter

for the oil & gas sector, EPIC recorded better than expected 9M09 results. According to OSK, EPIC’s 9M09 net profit of RM32.6m (+24.7% y-o-y) on revenue of RM133.9m (-25.5% y-o-y) was 85% of consensus forecasts for the year, and 89% of its own forecasts.

The improved net profit de-spite a drop in revenue were mainly due to effective cost cutting measures by some of its divisions and a lower effective tax rate due to the recognition of some tax allowances. Neverthe-less the lethargy in O&G activi-ties in the quarter is reflected in a 22.1% q-o-q decline in 3Q09 net profit (RM10.8m).

OSK has upgraded EPIC’s FY09-10 earnings forecast by 12% and 13% respectively to reflect its 3Q results. It also anticipated a pick-up in O&G activities with the recent sta-bilization of crude oil prices to above US$70/barrel.

Maybank IB added that it

favored EPIC’s cash cow sup-ply base operations, which was largely unaffected by a slow-down in its 61%-owned Kema-man Port activities and poorer sales at its fabrication and pipe threading operations. Supply base operations accounted for almost 96% of the O&G divi-sion’s pre-tax profit. Valuations are also inexpensive on PER and PBV basis, it added.

Maybank IB noted that EPIC is still in negotiations to acquire IJM Corp’s West Wharf port operations to complement its East Wharf port activities, and that EPIC intends to build an offshore fabrication yard in the next 2-3 years. A budget of RM188m in capex has been allocation for the fabrication year and Phase 3 expansion program.

AirAsiaAirAsia recorded a 3Q09 net

profit of RM130.1m (-127.9% y-o-y, -6.5% q-o-q) on revenue

Malayan Banking (FY Jun 2010) Maybank Investment Bank OSK ResearchResearch dated 13 Nov 2009 13 Nov 2009Forecast EPS 10 (sen) 39.9 41.7PER 10 (x) 16.9 16.2Forecast DPS 10 (sen) 21.2 26.0Div. Yield 10 (%) 3.1 3.1Call Not rated NeutralTarget price (RM) - 6.95Share price as at 30 Nov, 2009: RM6.75

RHB Capital (FY Dec 2009) Maybank Investment Bank OSK ResearchResearch dated 19 Nov 2009 19 Nov 2009Forecast EPS 09 (sen) 53.1 49.1PER 09 (x) 10.0 10.8Forecast DPS 09 (sen) 20.2 21.3Div. Yield 09 (%) 3.8 4.0Call Buy BuyTarget price (RM) 6.40 6.00Share price as at 30 Nov, 2009: RM5.31

MSHE_17-19_InvCorner.indd 18 12/2/09 9:13:10 AM

19

of RM739.7m (+4.5% y-o-y, +12.5% q-o-q). Despite an im-provement in revenue for the quarter, AirAsia’s performance was dragged down by weak economic conditions; concerns over the A(H1N1) pandemic; lower average fares; and higher fuel costs.

Seasonally, 3Q is AirAsia’s weakest quarter but “we are sur-prised by the further contraction in average fares to RM141.60 (-11.5% q-o-q) against the back-drop of escalating fuel costs,” said OSK. The company’s fuel price averaged US$79.30/bar-rel in 3Q (+30.4% q-o-q).

The drop in average fares suggests that the price under-cutting had intensified despite signs of a recovery in the global economy. The continuing up-trend in fuel prices is also a concern as the company’s lat-est fuel hedging contract only covers approximately 20% of the group’s 4Q requirements,

OSK added.Maybank IB said AirAsia has

addressed several key con-cerns by deferring the delivery of 16 out of 45 new aircraft scheduled for 2010-11; raising RM505m from a 16% private placement; and seeking a dual listing in Thailand to raise eq-uity.

The airline is currently in discussions with lead arranger CIMB Group to work out its list-ing details. The exercise could see a separate listing of Thai AirAsia or a merger by inject-ing Thai AirAsia into AirAsia. “A merger would eventually rationalize the current RM438m in inter-company dues Thai AirAsia owes AirAsia,” Maybank IB said.

OSK said it believed the exercise would be a secondary listing without involving any changes to the existing group structure. In some instances, a dual listing may improve a

company’s valuation if it is in a market that offers significantly higher valuation than its pri-mary listed market. However, OSK noted that Thai Airways International is trading at only 16.1x FY09 and 6.9x FY10 EPS, which does not reflect a significant premium to Bursa Malaysia’s valuation.

“We think a direct listing of the Thai unit may be a better option,” OSK said. AirAsia owns 49% of Thai AirAsia and has thus been funding the purchase of the latter’s aircraft, which resulted in the group’s high gearing level. A direct listing would enable the Thai unit to independently secure its own financing in the future, it said. The only major hurdle for this type of listing is Thai AirAsia’s lack of a profit record, as it is still in the red although manage-ment is confident of turning it around by the end of this fiscal year.

EPIC (FY Dec 2009) Maybank Investment Bank OSK ResearchResearch dated 24 Nov 2009 24 Nov 2009Forecast EPS 09 (sen) 25.7 24.4PER 09 (x) 5.8 6.1Forecast DPS 09 (sen) 8.0 8.9Div. Yield 09 (%) 5.4 6.0Call Buy BuyTarget price (RM) 1.95 2.03Share price as at 30 Nov, 2009: RM1.48

AirAsia (FY Dec 2009) Maybank Investment Bank OSK ResearchResearch dated 20 Nov 2009 23 Nov 2009Forecast EPS 09 (sen) 21.0 13.9PER 09 (x) 6.1 9.1Forecast DPS 09 (sen) 0.0 0.0Div. Yield 09 (%) 0.0 0.0Call Hold SellTarget price (RM) 1.35 1.13Share price as at 30 Nov, 2009: RM1.27

MSHE_17-19_InvCorner.indd 19 12/2/09 4:28:58 PM

20

Assuming the over-allot-ment option is not exercised, net proceeds from the offering is expected to be $2.4b, mak-ing it Singapore’s largest IPO since the listing of SingTel. As at press time, the public tranche of the IPO was sub-scribed nearly 5 times.

The pure-play shopping mall company, one of the largest in Asia, will have a total of 59 completed retail properties in 2009 and 86 retail properties by the end of 2012, estimated to be worth $20.3b.

The principal strategy for CapitaMalls is to invest and manage a portfolio of real estate assets used for retail purpose in Asia. Operations

are carried out through 2 seg-ments, the property business whereby the company invests in properties through direct ownership, REITs, joint-ven-tures and private real estate funds and the management segment consisting of fund and mall management.

Upon listing, CapitaLand will retain 65.5% to 70% of CapitaMalls, allowing the latter to access the former’s expertise as well as wide business network.

String Of Pearls

Spanning 48 cities in the countries of Singapore, Ma-laysia, China, Japan and In-dia, CapitaMalls’ portfolio is diverse geographically and

Don’t tel l any-body, San ta Claus dropped by town last week, descend-

ing from his anachronistic transport onto Robinson Point, headquarters of CapitaMalls Asia (CapitaMalls).

Priced at $2.12 apiece or 1.55x P/BV, the initial public offering (IPO) of CapitaMalls attracted a great deal of pent-up demand from retail and institutional investors alike. According to CapitaLand President and Chief Executive Liew Mun Leong, demand for the IPO was robust with US and European institutional in-vestors clamouring for a slice of the pie.

Christmas Comes early For Capitamalls asia

text : Donavan Lim

Across the cAusewAy

MSHE_20-21_ipo.indd 20 12/2/09 9:21:16 AM

21

holds immense potential for development.

Insofar, Singapore with relatively low average retail space per capita (compared to developed economies) is expected to be the anchor market of the company. In time to come, however, top line growth will be fueled by the China and India card.

Initially, CapitaMalls will focus on the Middle Kingdom, accelerating development of malls and actively seeking out opportunities for expansion.

By December 2009, Capita-Malls will have 32 properties in China as compared to 16 in Singapore. In the year 2012, 58% of the company’s prop-erty will be in China.

Such aggressive expan-sion could easily heighten risk for the company. China’s Rmb4 trillion stimulus pack-age has lifted the economic performance of the country and there are valid concerns of a future downturn following the unwinding of the pack-age. In such a scenario, the

bursting of the bubble could drag earnings and in turn divi-dend payouts. FY08 dividend was $0.107 a share.

I n v e s t o r s looking for a sa fe i ncome play could park t h e i r m o n e y in CapitaMall Trust or other S i n g a p o r e -centric REITs such as Suntec REIT. For those seeking cred-i b l e g r o w t h , then Cap i ta -Malls is a bet-ter option.

Growing From Strength To Strength

During the 3 years, FY06 to FY08, CapitaMalls’ top line grew at a CAGR of 44.6%. Nonetheless, FY08’s bottom line was hit by a 48% increase in finance costs, owing to the impact of additional borrowings from CapitaLand in 4Q07 and 2Q08 for financing investment in CapitaRetail China Trust and the China Incubator Fund among other funds.

On an EBIT basis, Singa-pore accounted for the lion share (53.3%) followed by China (28%). For reasons discussed above, China is ex-pected to be the main revenue driver in the future.

9M09 was another bumper period for CapitaMalls. Turn-over rose marginally 5.1% to $206.3m as compared to $196.3m in the corresponding period. But the bottom line surged to $244.5m boosted by a 112% increase in contri-butions from associates and jointly-controlled entities.

Undoubtedly, the floatation of CapitaMalls is a much-need-ed boost for the local equity market in a year where notable listing is a rarity. Investors are advised to examine their port-folio and risk-return profile to assess the suitability of taking a stake in the company.

S$’000 FY06 FY07 FY08 9M08 9M09Revenue 130,843 169,698 273,776 196,332 206,328Gross Profit 53,029 97,575 184,468 132,108 135,621Net Profit 112,342 185,407 156,799 152,512 244,506GPM (%) 40.53 57.50 67.38 67.29 65.73NPM (%) 85.86 109.26 57.27 77.68 118.50

CapitaMalls Asia’s financial highlights

Aggressive expansion ahead

MSHE_20-21_ipo.indd 21 12/2/09 9:21:38 AM

45%Discounts

Up To

Raid / Shares_Msia / msh_fillers / SubscribeForm / SI-msia_msia_BW / SImis_msia_BW.indd

SubScription Form You can now subscribe online at subscribe.SharesInvestment.com

Name: (Dr/Mr/Mdm/Ms)

Company:

Address:

Tel: Fax:

Email:

If you are a current subscriber and would like to renew, please fill in your 6-digit Subscriber ID:

Subscription Term Retail Price Offer Price 4

6 issues (30% discount) RM 72 RM 50

12 issues (35% discount) RM 144 RM 93

24 issues (40% discount) RM 288 RM 172For subscriptions to East Malaysia, please add RM3 per issue for delivery · Shares Investment (Malaysia) is a monthly publication.

English Edition Chinese Edition Commencement Month / Year /

A mustfor serious investors

whicheverway the market goes

MalaysiaEdition

Mail or fax completed form to: Pioneers & Leaders (Malaysia) Sdn BhdLevel 16, Menara Hap SengJalan P. Ramlee50250 Kuala Lumpur, MalaysiaTel : (603) 2782 6865Fax : 03-9236 7333Attn : SI (Malaysia) Subscription

Cheques to be made payable to:Pioneers & Leaders (M) Sdn Bhdor bank directly into:United Overseas Bank (Malaysia) Bhd(A/C 319-3001-2866)A/C payable to: Pioneers & Leaders (M) Sdn Bhd

For bulk subscription & other enquiries:Tel : (603) 7877 8481 / 8482Fax : (603) 7877 8486Email : [email protected]*Overseas postage will be charged separately

SingaporeEdition

ChinaEdition

Subscribe Online and get additional Discounts!!!

SImsia_msia_BW_1.indd 1 12/3/09 4:21:06 PM

Raid / Advertisement / P&L / SH_Wanted / Wanted_Ad_Msia_1.indd

You will be: Writing investment/financial

articles for Shares Investment and SharesInvestment.com, with focus on equities investment.

Conducting interviews with top-managements, and interact with like-minded investors in the industry.

Working in a dynamic team to contribute ideas and drive content/focus for the different platforms.

You’reWanted

Email us your resume and your expected remuneration today to

[email protected]!(Please place “SI(M) -

Contributor” in the subject)

Website: www.sharesinvestment.com • Facebook: Shares Investment • Twitter : sharesinv • Magazine: subscribe.sharesinvestment.com

The only shares investment magazinein Malaysia with English and Mandarin editions,

we’re looking for dynamic, self-driven and

experienced writers

to contribute to Shares Investment as we grow in the region.

Wanted_Ad_Msia_1.indd 1 12/3/09 4:57:42 PM

aaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaa

MARKET CAPITALISATION

22 Close in RM, Vol (volume) in ‘00

2 wks Last Mkt CapPage Company...........................Vol Close (‘000)

2 wks Last Mkt CapPage Company...........................Vol Close (‘000)

196 Sime Darby.................................... 565,187 9.06 RM54,445,164149 Malayan Banking .......................... 488,368 6.92 RM48,977,42866 CIMB Group Hldgs ........................ 352,421 13.38 RM47,874,684

184 Public Bank.................................... 175,663 11.40 RM40,263,956151 Maxis ............................................. 415,874 5.33 RM39,975,000

110 IOI Corp.......................................... 840,552 5.59 RM37,247,568210 Tenaga Nasional ........................... 513,243 8.20 RM35,563,400260 MISC .................................................. 9,777 8.50 RM31,618,53893 Genting .......................................... 407,946 7.54 RM27,926,80359 Axiata Group ................................. 726,396 3.16 RM26,686,687

172 PPB Group ....................................... 54,193 16.60 RM19,679,300179 Petronas Gas ................................... 30,963 9.75 RM19,292,637125 Kuala Lumpur Kepong.................... 80,674 17.04 RM18,190,28579 Digi.Com .......................................... 22,195 21.92 RM17,042,80093 Genting M’sia ................................ 333,628 2.88 RM16,997,184

171 PLUS Expressways ....................... 383,301 3.27 RM16,350,00052 AMMB Hldgs ................................. 414,005 5.10 RM14,881,214

222 YTL Corp .......................................... 23,541 7.52 RM14,265,380258 Fraser & Neave Hldgs ....................... 4,357 11.00 RM14,224,584106 Hong Leong Bank............................ 44,623 8.35 RM13,193,893

223 YTL Power Int’l.............................. 375,229 2.20 RM13,002,616257 British American Tobacco ................. 6,096 43.00 RM12,277,790186 RHB Capital...................................... 65,737 5.34 RM11,499,557210 Telekom M’sia ............................... 358,456 3.11 RM10,748,160179 Petronas Dagangan ........................ 27,396 8.79 RM8,732,461

261 Nestlé ................................................ 1,294 34.50 RM8,090,112259 Hong Leong Financial Group........... 15,844 7.52 RM7,916,815146 MMC Corp...................................... 194,315 2.45 RM7,460,397216 UMW Hldgs ..................................... 80,563 6.45 RM7,044,329108 IJM Corp ........................................ 146,218 4.76 RM6,243,920

174 Parkson Hldgs ............................... 105,568 5.96 RM6,177,00458 Astro All Asia Networks PLC......... 121,459 3.21 RM6,163,20062 Berjaya Sports Toto...................... 136,181 4.37 RM5,904,00192 Gamuda ......................................... 886,547 2.84 RM5,706,290

131 Lafarge Malayan Cement ................ 14,183 6.18 RM5,251,115

208 Tanjong PLC .................................... 28,780 17.54 RM5,125,434143 M’sian Airline System ..................... 91,492 2.97 RM4,962,87694 Genting Plantations........................ 98,389 6.43 RM4,865,92881 EON Capital ..................................... 81,002 7.01 RM4,859,395

256 Batu Kawan ....................................... 4,481 10.72 RM4,673,395

256 Berjaya Land...................................... 1,575 3.96 RM4,534,885141 M’sia Airports Hldgs ....................... 66,346 3.98 RM4,378,00065 Bursa M’sia ...................................... 50,307 8.14 RM4,280,712

190 SP Setia............................................ 86,603 4.10 RM4,168,46562 Berjaya Corp.................................. 125,296 1.27 RM4,039,315

216 UEM Land Hldgs ........................... 358,496 1.57 RM3,812,23654 Affin Hldgs ....................................... 96,184 2.55 RM3,810,63656 Alliance Financial Group............. 1,458,021 2.42 RM3,746,41755 AirAsia............................................ 486,712 1.43 RM3,395,120

143 M’sian Bulk Carriers........................ 34,098 3.21 RM3,210,000

213 Top Glove Corp ............................... 55,662 10.52 RM3,195,534195 Shell Refining Co............................. 31,575 10.60 RM3,180,000259 KLCC Ppty Hldgs ............................. 13,383 3.39 RM3,166,51165 Boustead Hldgs ............................... 74,232 3.47 RM3,162,711

118 KNM Group................................. 1,897,754 0.79 RM3,127,168

108 IGB Corp ........................................155,909 1.97 RM2,935,883261 Oriental Hldgs ...................................6,469 5.66 RM2,926,039264 United Plantations ...........................1,115 13.98 RM2,909,713191 SapuraCrest Petroleum ................270,564 2.38 RM2,841,327109 IJM Land .........................................73,115 2.34 RM2,581,647

257 Bintulu Port Hldgs ............................1,439 6.25 RM2,500,000121 Kencana Petroleum ......................241,183 1.58 RM2,425,347263 Star Publications ..............................1,669 3.24 RM2,392,947125 Kulim ...............................................20,172 7.59 RM2,341,151204 TA Global ......................................478,150 0.485 RM2,335,275

207 Tan Chong Motor Hldgs ...............138,591 3.42 RM2,298,240213 Titan Chemicals Corp .....................74,554 1.31 RM2,296,037184 Proton Hldgs ...................................31,408 4.00 RM2,196,852219 WCT ...............................................190,289 2.79 RM2,152,479258 Guinness Anchor ..............................3,077 6.95 RM2,099,581

264 YTL Cement .........................................889 4.26 RM2,089,760109 IJM Plantations ..............................66,093 2.58 RM2,067,462259 Hap Seng Plantations Hldgs ...........35,458 2.50 RM2,000,000260 LPI Capital .........................................2,137 13.98 RM1,939,34878 Dialog Group ................................231,420 1.34 RM1,893,701

161 Multi-Purpose Hldgs ......................85,277 1.89 RM1,818,987256 Aeon Co .............................................9,143 5.15 RM1,807,650159 Mudajaya Group .............................62,955 4.80 RM1,795,20074 DRB-Hicom ......................................52,769 1.04 RM1,788,385

101 Hartalega Hldgs ..............................36,983 6.72 RM1,628,337

154 Media Prima ..................................142,664 1.90 RM1,622,241220 Wah Seong Corp ............................51,310 2.41 RM1,583,370256 Ann Joo Resources ........................13,144 3.01 RM1,573,348259 KFC Hldgs ..........................................5,619 7.88 RM1,562,407259 Hap Seng Consolidated ....................9,014 2.47 RM1,537,970

201 Sunway City ...................................30,461 3.25 RM1,527,338202 Supermax Corp ............................426,378 5.70 RM1,512,039162 NCB Hldgs .......................................30,772 3.10 RM1,457,784144 M’sian Resources Corp .................829,370 1.57 RM1,424,833260 Lingkaran Trans Kota Hldgs ...........10,297 2.85 RM1,416,450

118 KPJ Healthcare ...............................45,872 2.61 RM1,366,732262 QL Resources ..................................14,497 4.01 RM1,323,30060 BIMB Hldgs .....................................15,084 1.24 RM1,322,708

257 Carlsberg Brewery M’sia ..................7,771 4.63 RM1,314,883259 JT Int’l .............................................10,159 4.94 RM1,291,978

203 TA Enterprise ................................273,207 0.75 RM1,283,93376 Damansara Realty ..........................81,009 0.81 RM1,266,336

259 Hong Leong Industries .....................4,957 4.50 RM1,265,157185 Puncak Niaga Hldgs .......................36,697 3.05 RM1,253,986262 Sarawak Oil Palms ...........................3,365 2.92 RM1,248,031

260 M’sian Pacific Industries .................11,442 5.86 RM1,229,92064 Boustead Heavy Industries Corp ......12,427 4.92 RM1,222,413

256 Amway Hldgs ......................................676 7.31 RM1,201,662139 Lion Industries Corp .....................482,544 1.68 RM1,197,785264 UBG ...................................................1,822 2.39 RM1,195,946

148 Mah Sing Group .............................58,780 1.90 RM1,191,007167 OSK Hldgs .......................................90,784 1.76 RM1,184,601181 Pos M’sia .........................................11,149 2.20 RM1,181,457194 Selangor Ppties ................................8,298 3.37 RM1,157,989200 Sunrise ............................................35,482 2.20 RM1,089,858

MEa22_mcap.indd 2010-1-8, 18:021

aaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaa

LOWEST P/E

34 Close & EPS (earnings per share) in RM, Yield in %

139 Lion Forest Industries................. 1.29 0.795 --- 1.6221 XiDeLang Hldgs ........................ 0.49 --- --- 3.9105 Hock Lok Siew Corp................. 0.19 0.096 --- 4.0161 Multi Sports Hldgs ................. 0.515 --- --- 4.0221 Xingquan Int’l Sports Hldgs........... 1.18 0.583 --- 4.1

211 Teo Seng Capital .................... 0.465 0.113 3.4 4.1263 Tomei Consolidated ................. 0.51 0.120 4.9 4.2140 London Biscuits ........................ 1.02 0.205 2.9 5.0260 Khind Hldgs............................... 0.98 0.191 5.1 5.1264 Tradewinds ............................... 2.77 0.530 7.2 5.2

180 Poh Huat Resources Hldgs ........ 0.475 0.092 4.2 5.2264 Yee Lee Corp............................. 1.48 0.277 3.4 5.3197 Sinaria Corp .............................. 0.39 --- --- 5.5103 Hing Yiap Group ....................... 1.27 0.227 5.9 5.6260 Lay Hong ................................... 0.85 0.145 1.5 5.9

260 Malayan Flour Mills .................. 3.19 0.539 3.1 5.9263 Tafi Industries ......................... 0.375 0.064 6.0 5.9180 Poh Kong Hldgs ...................... 0.415 0.070 3.4 6.075 DXN Hldgs................................. 0.56 0.089 2.2 6.3

260 LTKM ......................................... 1.37 0.219 5.8 6.3

CONSUMER (15.1)*Last

Page Company.........................Close EPS Yield PE

187 Ranhill........................................ 0.89 0.383 1.1 2.3257 DKLS Industries ........................ 1.06 0.407 2.8 2.6261 Merge Energy............................ 0.38 0.102 --- 3.7258 Grand Hoover............................ 0.21 0.050 --- 4.2261 Melati Ehsan Hldgs................... 0.68 0.117 --- 5.8

263 TRC Synergy ............................. 1.38 0.240 4.3 5.8148 Magna Prima............................. 3.62 0.503 1.4 7.2257 Crest Builder Hldgs................. 0.765 0.099 3.9 7.788 Fajarbaru Builder Group.............. 1.07 0.132 1.4 8.1

262 SBC Corp ................................... 0.52 0.061 2.9 8.6

CONSTRUCTION (16.5)*Last

Page Company.........................Close EPS Yield PE

145 MBF Hldgs................................. 0.54 0.081 --- 3.3263 Syarikat Takaful M’sia ................ 1.35 0.240 5.4 5.6111 Insas .......................................... 0.63 0.075 --- 8.4167 OSK Hldgs ................................. 1.76 0.200 4.3 8.8256 Allianz M’sia.............................. 4.27 0.460 0.5 9.3

256 Aeon Credit Svcs ...................... 3.98 0.406 5.1 9.8186 RHB Capital ............................... 5.34 0.487 3.7 11.0260 Manulife Hldgs.......................... 2.62 0.232 5.0 11.360 BIMB Hldgs................................ 1.24 0.107 1.0 11.6

259 Hong Leong Financial Group ........ 7.52 0.600 3.1 12.5

54 Affin Hldgs................................. 2.55 0.196 2.0 13.0203 TA Enterprise ............................ 0.75 0.064 6.0 14.0106 Hong Leong Bank ..................... 8.35 0.573 2.9 14.6259 Hwang-DBS............................... 1.72 0.118 2.9 14.6184 Public Bank.............................. 11.40 0.731 4.8 15.6

FINANCE (20.7)*Last

Page Company.........................Close EPS Yield PE

132 Landmarks ................................ 1.28 0.131 --- 9.8258 Grand Central Enterprises ........... 0.70 0.066 4.3 10.7263 Shangri-La Hotels .................... 1.85 0.112 4.3 16.5

HOTEL (12.5)*Last

Page Company.........................Close EPS Yield PE

260 M’sia Steel Works .................... 1.02 0.407 2.5 2.5261 Minho ........................................ 0.32 0.121 --- 2.674 DRB-Hicom ............................... 1.04 0.384 2.4 2.7

256 Asia Poly Hldgs ........................ 0.18 0.060 --- 3.0261 Metrod ...................................... 3.30 1.082 3.6 3.0

261 Mentiga Corp ........................... 0.51 0.156 3.9 3.3257 Chuan Huat Resources ............ 0.61 0.182 9.0 3.3264 United U-Li Corp .................... 0.595 0.161 --- 3.7261 PMB Tech ................................. 0.43 0.117 3.5 3.7260 Kia Lim ...................................... 0.23 0.059 --- 3.9

99 HPI Resources .......................... 1.40 0.442 1.4 4.0262 Public Packages Hldgs ............. 0.235 0.057 --- 4.1258 Emas Kiara Industries ................ 0.52 0.128 2.9 4.1260 Lysaght Galvanized Steel ........... 1.43 0.341 3.5 4.2192 Scomi Group ............................ 0.49 0.114 1.0 4.3

264 Ya Horng Electronic ................. 0.71 0.165 7.0 4.3261 Metech Group .......................... 0.30 0.069 --- 4.3262 Seacera Tiles ............................ 0.36 0.076 2.8 4.7182 Prestar Resources .................. 0.605 0.124 2.5 4.9263 Sersol Tech ............................... 0.09 0.018 --- 4.9

261 Muda Hldgs ............................ 0.815 0.155 3.1 5.2133 Leader Universal Hldgs .............. 0.79 0.149 3.8 5.3262 Pelangi Publishing Group ......... 0.475 0.089 5.8 5.368 Cahya Mata Sarawak .............. 1.54 0.290 3.2 5.3

256 Ajiya .......................................... 1.70 0.318 --- 5.3

84 Eksons Corp ............................. 0.85 0.158 --- 5.4257 Bright Packaging Industry ........... 0.23 0.042 --- 5.4114 Jasa Kita ................................... 0.15 0.028 3.3 5.4

INDUSTRIAL PRODUCTS (11.9)*Last

Page Company.........................Close EPS Yield PE

256 Aliran Ihsan Resources .............. 1.30 0.221 --- 5.9260 Lingkaran Trans Kota Hldgs ......... 2.85 1.028 8.8 13.979 Digi.Com ................................. 21.92 1.467 5.0 14.9

223 YTL Power Int’l ........................ 2.20 0.106 6.3 20.8185 Puncak Niaga Hldgs ................ 3.05 0.239 3.3 50.9

INFRASTRUCTURE (17)*Last

Page Company.........................Close EPS Yield PE

MINING(No shares for this issue)

MEa34_pe.indd 2010-1-8, 18:0034

aaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaa

LOWEST P/E

35PE derived from company’s latest full year earnings, * denotes industry’s weighted average PE.

263 TDM .......................................... 1.65 0.455 8.5 3.6205 TH Plantations .......................... 1.53 0.345 8.2 4.4260 MHC Plantations....................... 1.22 0.269 2.5 4.580 DutaLand................................. 0.535 0.113 --- 4.769 Cepatwawasan Group ........... 0.985 0.191 2.5 5.2

260 Kurnia Setia............................... 2.60 0.482 5.8 5.465 Boustead Hldgs......................... 3.47 0.889 8.6 5.5

256 BLD Plantation.......................... 3.80 0.687 2.9 5.5261 NPC Resources.......................... 1.88 0.327 4.8 5.7125 Kulim ......................................... 7.59 1.180 2.0 6.4

264 Tradewinds Plantation ............... 1.66 0.252 3.6 6.6258 Far East Hldgs........................... 6.60 0.979 3.8 6.7100 Harn Len Corp......................... 0.795 0.113 2.5 7.0260 Malpac Hldgs ............................ 1.20 0.158 --- 7.6260 Kretam Hldgs ............................ 1.22 0.149 --- 8.2

PLANTATION (17.2)*Last

Page Company.........................Close EPS Yield PE

207 Talam Corp.............................. 0.105 0.031 --- 3.4258 Fima Corp.................................. 2.98 0.693 5.7 4.3256 Bina Darulaman ........................ 0.99 0.226 5.1 4.4262 Plenitude ................................... 2.71 0.591 5.2 4.6259 KSL Hldgs.................................. 1.21 0.257 4.1 4.7

72 Crescendo Corp ........................ 1.09 0.204 6.4 5.3259 KLCC Ppty Hldgs....................... 3.39 0.573 3.1 5.9258 Encorp........................................ 1.00 0.165 5.0 6.1200 Sunrise....................................... 2.20 0.315 1.4 7.0256 Bandar Raya Devts ................... 1.59 0.228 1.9 7.0

120 Keladi Maju ............................. 0.165 0.022 9.1 7.6222 YNH Ppty................................... 1.68 0.218 --- 7.7262 Paramount Corp ....................... 3.04 0.389 5.3 7.8156 Metro Kajang Hldgs.................. 1.44 0.185 3.5 7.8259 Hua Yang................................... 0.77 0.096 3.2 8.1

149 Majuperak Hldgs....................... 0.23 0.027 --- 8.7107 Hunza Ppties ............................. 1.64 0.183 3.4 9.063 Bertam Alliance ........................ 0.26 0.027 5.8 9.8

194 Selangor Ppties......................... 3.37 0.345 3.3 9.8260 Krisassets Hldgs ....................... 3.10 0.297 4.2 10.4

PROPERTY (13.2)*Last

Page Company.........................Close EPS Yield PE

256 AmFirst REIT ............................. 1.06 0.417 8.3 2.5249 Starhill REIT .............................. 0.86 0.302 8.0 2.8247 AL-Hadharah Boustead REIT......... 1.32 0.341 8.4 3.9250 Tower REIT................................ 1.14 0.237 8.2 4.8256 Amanahraya REIT................... 0.845 0.155 8.3 5.4

248 Hektar REIT ............................... 1.13 0.189 9.0 6.0256 Atrium REIT............................. 0.905 0.140 9.3 6.4248 Axis REIT ................................... 1.94 0.248 7.5 7.8

REIT (4.6)*Last

Page Company.........................Close EPS Yield PE

219 Vastalux Energy ..................... 0.175 0.091 5.7 1.9260 Mechmar Corp ......................... 0.19 0.103 --- 1.9130 LCL Corp ................................... 0.20 0.065 --- 3.1214 Tradewinds Corp ..................... 0.65 0.196 1.3 3.388 Fitters Diversified .................... 0.56 0.167 --- 3.4

259 Ipmuda ...................................... 0.67 0.193 4.5 3.5264 Yinson Hldgs ............................ 0.68 0.187 3.7 3.687 Faber Group ............................. 1.60 0.429 2.5 3.7

188 SAAG Consolidated ............... 0.175 0.047 --- 3.7226 Asia Bioenergy Technologies ........ 0.10 0.022 --- 4.5

263 TASCO ...................................... 0.87 0.184 --- 4.7126 Kumpulan Fima ........................ 0.84 0.177 3.6 4.7259 Hap Seng Consolidated ............. 2.47 0.504 4.9 4.9256 ATIS Corp ............................... 0.945 0.192 --- 4.9206 TSM Global .............................. 2.12 0.421 2.4 5.0

257 Complete Logistics Svcs ............. 0.54 0.106 11.1 5.1259 Kamdar Group ....................... 0.345 0.068 --- 5.1259 Harbour-Link Group ................ 0.74 0.144 2.7 5.1193 Scomi Marine ........................... 0.48 0.089 2.9 5.4260 MBM Resources ....................... 2.60 0.485 4.6 5.4