Setting credit limits

32

1 Setting Credit Limits© Presented by: Jim Menard, CCE Presented by: Jim Menard, CCE email: email: [email protected] [email protected] Webinar Webinar

-

Upload

credit-management-association -

Category

Business

-

view

371 -

download

0

Transcript of Setting credit limits

1

Setting Credit Limits©

Presented by: Jim Menard, CCEPresented by: Jim Menard, CCEemail: email: [email protected]@charter.net

WebinarWebinar

2

Credit is like a puzzle…

…the more pieces you have, the clearer the picture

3

The Credit Puzzle

The pieces fit together to form a picture The more pieces you have, the clearer the

picture It is possible to understand the essence of

the picture without having all of the pieces in place

Although no one piece is enough to make you comfortable, you can become uncomfortable based on a single item.

4

Establishing Credit Lines

The credit line is:An investmentA loanBut most of all – a privilege

5

Credit Line

A credit line must coincide with your firm’sTerms of saleDesired level of market

penetrationAppetite for risk

6

Extension of Credit

Your credit extensions will be linked to your customer’s: Capacity for growth Ability to withstand adversity in the

economy and the market place Credit worthiness Need for your product matched to the

ability to repay the debt

7

Granting a line of Credit

Percentage of Net Worth Percentage of Cash Flow from Operations Percentage of Working Capital Based upon Dun & Bradstreet rating Supplier references Bank references Personal / Corporate guaranty Security

8

SOME FACTORS INFLUENCING LENDERS’ COMFORT LEVEL

QUALITATIVE Character / credibility . past payment history . support from present lenders . reputation with past customers . moral standing and integrity . business style

9

SOME FACTORS INFLUENCING LENDERS’ COMFORT LEVEL -2 Proven ability to grow / adapt . successful problem identification /

resolution . strategies to keep abreast of the

times . ability to manage complexity . balance of key managerial functions

10

SOME FACTORS INFLUENCING LENDERS’ COMFORT LEVEL -3 Depth of experience / talent . degree of competence in critical

areas what must they do well ? what is company’s real business ? . competent to manage in adversity as

well as prosperity

11

Industry

Inherent risk compared to other industries State of maturity

. growing . flat . declining Present Stage of Industry Cycle Position within industry

. market share . trend Competition within industry

. domestic / international . entry / exit barriers . cost structure . energy sensitivity

12

Industry - 2

Margins within the industry Seasonality Vulnerability to inflation Vulnerability to business cycle Vulnerability to sources of supply Vulnerability to obsolescence

. stage of product maturity

13

QUANTITATIVE - Financial

Cash Flow - pays loans . income . non cash expenses consistency diversity Liquidity - ease of converting assets to cash . working capital Leverage - varies by industry . total liabilities vs: tangible net worth overstated understated relative to transaction Performance during hard / difficult times

14

SECONDARY FACTORS - QUALITATIVE Access to additional financial resources Proven ability to raise equity . return on equity in excess of capital

costs Other lenders’ present willingness to

make commitments Liquid net worth of corporate parent or

major stockholders Prevailing phase of business cycle

15

Environmental factors

Vulnerability to change . regulatory . social . political

16

SECONDARY FACTORS - QUANTITATIVE (Collateral) Ease of perfecting security interest Degree of equity in real property . loan to quick sale value ratio Historic value fluctuations over the term . vulnerability to cyclicality . risk of technological obsolescence Ease of liquidity / remarket ability . mobility . market . identifiable . measurable

17

SECONDARY FACTORS - QUANTITATIVE (Collateral) - 2 Incremental revenue / profit expectations

attributable to acquisition Diversity of customer base . dependence on limited number of

customers . dependence on limited number of

industries Lenders exposure to similar credits Need for portfolio diversity

18

LIKELY DEAL KILLERS - OBJECTIVE Fire history Large tax liens Creditor judgments Criminal conviction Negative tangible worth Qualified auditors opinion Viability as on-going concern Speculative business practices Recent Chapter 11 re-organization Major litigation threatened or pending

19

LIKELY DEAL KILLERS - SUBJECTIVE

Name dropping Lack of openness Disreputable affiliates Low morale / high turnover Pressure for rapid credit decision Arrogance rather than cooperation Unavailability of internal information Criticism of present lenders or auditors Evasive answers regarding performance High style personal corporate living habits

20

REASONS FOR CAUTION

Rapid growth Changing banks Heavy cash usage Debt rescheduling Changes in auditors Slow trade payment

21

REASONS FOR CAUTION 2

No dominant lead bank Deteriorating financial ratios No regional bank involvement Acquisitions (friendly / unfriendly) Change in ownership / management

Previous turndowns

22

REASONS FOR CAUTION 3

Continuous restating of previous year’s statements.

Previously troubled credits that appear to have turned around

Reported payment history inconsistent with trade reference comments

Criminal indictment

23

SUBJECTIVE

Poorly managed Absentee management Family dominated company Anything out of the ordinary Company with one person rule Significant changes in operations Heavy fixed costs or other operating rigidities Alterations in corporate emphasis and objectives Large, complex corporate and financial structures Marginal borrowers with down market positions in their

industries

24

Example of a Policy

Exhibit “A” Company Policy on establishing a Credit limit

for your customers…

25

ABC, INC. Policy #CC1002

CREDIT & COLLECTION POLICY/PROCEDURES Page 1 of 7 Effective Date: September 21, 2007

Subject: CREDIT LIMIT CRITERIA Approved by: Joe Credit

I. Scope - ABC, Inc. and all subsidiaries, worldwide

II. Objective - To establish a consistent procedure in approving open account credit lines.

Example – Credit Limit Policy

26

III. Procedure

It is the responsibility of the individual Credit Representative to assign credit limits and terms of sale to each customer within their own account assignment. The accounts are to be reviewed, minimally on an annual basis.

A. Establishing credit lines:1. The credit line is an investment, a loan, but most of all a privilege.

2. The Five "C's" of Credit a. Character - who is the business owner / does he pay b. Capital - the financial strength of a risk c. Capacity - the ability to pay when due d. Conditions – the general economic conditions e. Collateral – is there backup should the capacity fail

Example – Credit Limit Policy - 2

27

3. A credit line must coincide with our firm's terms of sale, desired level of market penetration and appetite for risk.

4. Credit extensions will be linked to our customer's capacity for growth, ability to withstand adversity in the economy and in the market place.

5. To properly control your total credit extensions in the majority of our customer's cases, their credit lines should not be greater than their need for your product - the credit line should cover the customers needs during the next 6-12 months.

6. The credit line is based upon the customer's ability to repay - not their product needs.

Example – Credit Limit Policy - 3

28

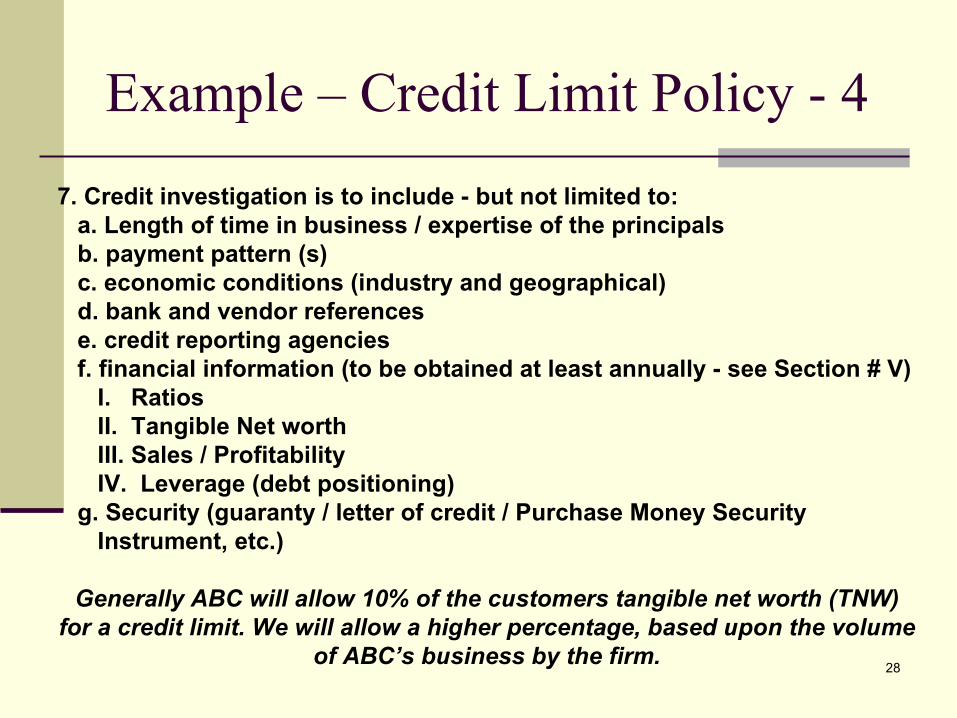

7. Credit investigation is to include - but not limited to: a. Length of time in business / expertise of the principals b. payment pattern (s) c. economic conditions (industry and geographical) d. bank and vendor references e. credit reporting agencies f. financial information (to be obtained at least annually - see Section # V) I. Ratios II. Tangible Net worth III. Sales / Profitability IV. Leverage (debt positioning) g. Security (guaranty / letter of credit / Purchase Money Security Instrument, etc.)

Generally ABC will allow 10% of the customers tangible net worth (TNW) for a credit limit. We will allow a higher percentage, based upon the volume

of ABC’s business by the firm.

Example – Credit Limit Policy - 4

29

B. ABC will add to the base credit limit for the following:1. Stand By Letter of Credit 100%2. Purchase Money Security Agreement (UCC) without subordination -or- + 20% TNW with subordination to the bank + 10% TNW3. Blanket Security Agreement (UCC) First position + 25% TNW Second position + 15% TNW Third or more + 5% TNW4. Personal guaranty of principals & spouse + 15% TNW (required on new or closely held corporations to include personal financial statements)5. Prompt Pay - pays within terms of Net 30 + 10% TNW6. In business more than 5 years + 10% TNW7. Debt to Worth greater than 2:1 - 10% TNW8. International - local financial standards +10% to +40%TNW

Example – Credit Limit Policy - 5

30

C. Financial Statements:1. To be obtained a least annually from our customers whose credit limit is >$20k.2. Audited statements on all customers, where possible, unaudited statements have limited value.3. International financial statements to be obtained within 60 days of publication.4. Domestic financial statements to be obtained within 30 days of publication.5. Domestic public companies to furnish quarterly as well as annual reports (10Q / 10K / Prospectus - SEC reports). 6. Parent company financial statements should be obtained at the same time as the subsidiary's.7. High Risk Accounts* - monthly financial statements. (* as determined by the Credit Manager)

Example – Credit Limit Policy - 6

31

For Further Consideration

Future webinars On Line Classes Western Regional Credit Conference in Las Vegas (10/14-16)

We are always open to your comments and suggestions for future programs … please contact your rep at CMA

32

Question time………..

Time to ask your questions…

I can email you a copyof this policy if youwould like…

Thank you for joining us today…Jim Menard, CCEYou can contact me at [email protected]