September2016 Edition IV - Hazelton...

22

S S

Transcript of September2016 Edition IV - Hazelton...

S

S

2

Hazelton Capital PartnerSeptember2016 Edition IV

(C) ValueWalk 2016 - All rights Reserved

I. Intro to The Fourth EditionWelcome to the fourth edition of the Underrated Small-Cap Stocks premium newsletter. Our goal is to bring you small- and mid-cap stocks you wouldn’t normally hear about, as they fly under the radar. These types of stocks tend to have the most potential to become multi-baggers. Our last edition includ-ed an in investor who solely focuses on P&C insurers with little coverage. This issue brings a fund man-ager from Chicago who runs a concentrated portfolio and invests across market caps. We do a heavy deep dive into two micro/small caps the fund manager owns and is bullish on. Some of these holdings were not shared yet with anyone besides shareholders so you truly are in for a special treat.

3

September2016 Edition IV

(C) ValueWalk 2016 - All rights Reserved

Hazelton Capital Partner

II. Update From Our April & July 2016 EditionsNoh-Joon’s journey to the property and casualty (“P&C”) insurance industry has been part luck and part asking the question many fail to ask when it comes to Warren Buffett’s investment success: Where did Warren Buffett’s investment capital at Berkshire Hathaway come from? Indeed, Buffett deployed most of Berkshire’s capital first to its P&C insurance companies which then provided even more funds to finance many of Buffett’s most famous investments: Coca-Cola, Wells Fargo, Washington Post, American Express, Burlington Northern, etc.

Noh-Joon left the investment banking world with a background in distressed debt and restructuring, getting hired as an analyst for a start-up event-driven credit and equity hedge fund. After the hedge fund wound down, Noh-Joon started taking a hard look at Warren Buffett and how he funded his in-vestments. For most of his career, Buffett has not been subject to redemption pressures from investors and limited partners. “Why did he not have to perform on a monthly basis?” asked Noh-Joon. Most of the media, Wall Street and Main Street focus on Buffett’s investments, but they rarely ask, how did he fund these investments? Armed with the answer to this question, S&C Messina Capital was born.

Noh does not discuss positions but was nice enough to discuss one for our audience ProAssurance group (PRA). While our readers do not focus on short term performance the stock is up nicely since we sent the issue on June 21st to today (9/22) with slightly over an 8% gain - not bad!

Mark Spiegel was profiled in our April issue. Mark is killing it on his small cap picks this year. We re-cently sent out his monthly investor update and you can read some his picks which has helped lead to a 20.4% net return YTD.

4

Hazelton Capital PartnerSeptember2016 Edition IV

(C) ValueWalk 2016 - All rights Reserved

III. Hedge Fund Highlight: Barry Pasikov of Hazelton Capital Partners Barry Pasikov CONTACT INFO:

[email protected] (312) 970-9202

Barry Pasikov background:

Barry Pasikov is the founder and Managing Member of Hazelton Capital Partners, a value-oriented investment fund. The Fund is a distillation of Mr. Pasikov’s 25-plus years of experience in equities, currencies, commodities, options, portfolio and risk management. Launched in 2009, Hazelton Capital Partners employs two investing strategies: The Core Strategy constructs a concentrated portfolio of equity holdings that are selected based on a number of metrics, including sustainable revenue growth, margin expansion, the company’s balance sheet, and its management. The Overlay Strategy, through its use of options, commodities, currencies and risk arbitrage, complements the Core Strategy by pro-viding a hedge as well as short-term cash flows. Barry holds a Bachelor of Arts in Economics from the University of Michigan..Hazelton Capital Partners, LLC gained 3.2% from April 1, 2016 through June 30, 2016, gained 11.8% year-to-date, and has returned 93% since its inception in August 2009. Since last issue was more indus-try focused we decided to really deep dive even further into stocks in this edition.

5

September2016 Edition IV

(C) ValueWalk 2016 - All rights Reserved

Hazelton Capital Partner

IV. Stock Highlight:

How do you go about finding potential opportunities, where do you usually find your best ideas?

When I first started Hazelton Capital Partners, I relied primarily on stock screeners to generate my in-vesting ideas. I had specific metrics I was looking for, and this was a quick and easy way to create a list of companies to investigate. Over time, I quickly realized two things: My results were very similar to what many other investors were finding, and many of these stocks were cheap for a reason. Investing in these companies was profitable, overall, but it was not providing the long-term, sustainable, invest-ments I was seeking.

Today, Hazelton Capital Partners generates most of its investing ideas from wanting to better under-stand how businesses and industries operate. This curiosity has led to an education that I could not have achieved just by reading a company’s 10-K or only focusing on its financials. Many of our in-vestments are not in the “well known,” competitive segments of an industry but instead, in companies that operate in smaller, niche segments where market share, margins, and operational leverage have a meaningful impact on profitability and growth. Some of our most successful investments: Tellular, Michael Baker, Northern Tier and DreamWorks Animation have come from this investing process and would have never shown up on a stock screener.

I am also very fortunate to have built up a network of friends who are professional investors/hedge fund managers, whom I speak with regularly. Being able to share ideas with colleagues of this caliber helps me to distil my thoughts more quickly and identify some of the hidden risks associated with an investment I may have glossed over.

Aside from the figures, what do you look for in a prospective in-vestment, what makes you say, “yes we want that” or “no we don’t”? How do you approach valuation?

We begin our investing process by determining whether there is something unique about a company. Since we limit the number of holdings within the portfolio to around 15 to 20 positions, Hazelton Cap-ital Partners is very picky about the companies in which we invest. If there is nothing unique about the enterprise, we move on to the next idea. For those businesses that are distinctive, we then look for their area of expertise. This focuses on the company’s business model: How the company generates its revenues and turns those revenues into cash. A good amount of time is spent not only learning about the company, its business model, and management but the industry and industry segments in which it operates. This information helps us understand whether the company has a sustainable competitive edge, and if so, whether or not the company can maintain that competitive edge well into the future.

This in-depth process that I just outlined will only get the company onto a vetted watch list. The final determinant will be how the addition of this company complements the overall portfolio. A company’s

6

Hazelton Capital PartnerSeptember2016 Edition IV

(C) ValueWalk 2016 - All rights Reserved

stock price that is cheap in relation to our future intrinsic valuation is definitely a criterion we focus on, but just as important is how the addition of this company is going to impact the overall portfolio’s exposure to a particular industry or its industry segments, interest rates, and balance sheet metrics, like debt and cash levels.

The final step of our investment process is valuation. Hazelton Capital Partners probably approaches valuation a bit differently than most hedge funds because we are less concerned about what a company is worth and more focused on what a company is not worth. In other words, once we find a company that has met our vetting criteria, we spend less time at the beginning of the valuation process trying to determine the upside and more time trying to establish the company’s value if things were to go south. This is why we take the time to understand a company’s industry, area of expertise, and competitive edge, as it helps with the downside valuation. Once we have identified the potential downside and assuming the investment continues to make sense to us, we then begin to spend more time narrowing down the upside valuation. Often, we will invest in a company without having fully valued its potential upside. If we are confident with our downside assumptions, then, over time, the upside will more than take care of itself. Using this method to “stress test” our investments allows us to quickly recognize whether a downturn in the price of a stock is an investing opportunity or a roadblock to our investing thesis. Once an investment is added to the portfolio, it is reviewed at least four times a year and any-time there is significant company or industry news.

Since there are numerous ways to value a company, Hazelton Capital Partners is not fixated with a single valuation process and will often use a combination of multiples, discounted cash flows, and the balance sheet to arrive at a valuation range.

What are the qualities investors should be looking for when trying to identify the best companies?Every investor is going to have a different set of metrics that they focus on when searching for and valuing a company. The key to using metrics is to be consistent, honest, and unwilling to compromise. Hazelton Capital Partners focuses on businesses that we believe to have a sustainable, long-term com-petitive edge. We spend a good amount of time getting comfortable with a company’s balance sheet, operating metrics and its management. Of the three, management is the most challenging to evaluate but will also have the biggest impact on the company and its future prosperity. A starting point for me is to determine how management is incentivized. Knowing how someone is incentivized is a key ingredient in understanding what drives one’s behavior.

Overall, I feel more comfortable investing in companies whose management behaves like an owner op-erator and treats the company as a precious commodity instead of a piggy bank. Hazelton Capital Part-ners looks for management whose incentives are aligned with its shareholders. This is often reflected in the management team holding a significant portion of compensation in the equity of the company.

7

September2016 Edition IV

(C) ValueWalk 2016 - All rights Reserved

Hazelton Capital Partner

You run a relatively concentrated portfolio. Why did you choose this approach over diversification?The concept of portfolio diversification is based on minimizing risk. In theory, investments that are spread across a number of industries and or asset classes will provide protection against the unpredict-able and cyclical nature of markets; a downturn in one industry or asset class will be more than offset by the gains in others within the portfolio. Diversification is often seen as an insurance policy, and like an insurance policy, there is a cost involved. Instead of a policy premium, an investor pays for this insurance with lower yearly returns by focusing on variety instead of quality.

It is also important to remember that people carry insurance to cover a meaningful loss to assets like your home and car. Portfolio diversification is expected to provide the same level of protection, except during the 2008-2009 financial crisis this was not the case. Investors who maintained a diversified portfolio during this period found that nearly all stock industries, commodities, and foreign markets decreased in concert. In 2008, the S&P 500, along with the average diversified portfolio, lost approxi-mately 38% of its value. In essence, all those years of diversification ended up being a waste of time and money because when investors needed the insurance the most, nobody was there to settle the claim.

Investors are faced with two distinct forms of risk when making an investment: Business and market risk. Business risks are the uncertainties associated with a particular company or industry, whereas market risks are related to economic conditions impacting all asset classes. Without the conviction that comes from spending meaningful time researching companies, many investors decisions are driv-en by fear and greed. Fear that they will lose money on their investment and greed that they are missing out on a great opportunity. Hazelton Capital Partners is not trying to eliminate uncertainty; uncertainty is what provides the Fund its opportunities. Instead, the Fund seeks to exploit uncertainty by taking advantage of investors’ fear and greed.

At Hazelton Capital Partners, we focus on creating a concentrated portfolio of 15-20 uncorrelated in-vestments with our top five holdings representing between 35 & 50% of the assets under management. The portfolio is constructed not only on the merits of the individual equities it holds but also by how correlated these equities are to one another. A good example of the difference between diversification and correlation can be seen when comparing two companies like General Electric and Hanesbrand Inc.

Hanesbrand is a manufacturer of adult and children’s underwear and whose profitability is highly influenced by the rise and fall of cotton prices, rather than the general state of the economy. General Electric is an industrial conglomerate servicing industries including technology, energy, and aviation which are impacted by a number of economic factors. It would appear that an investment in these two companies is not only uncorrelated but would also provide diversity to your portfolio as the factors in-fluencing the profitability of Hanesbrand Inc. would have very little in common with General Electric.

In 2008, both Hanesbrand Inc and General Electric carried a significant amount of debt on their bal-ance sheets. In fact, both companies had a debt level that was multiples of their market capitalization and equity. Even though General Electric and Hanesbrand Inc. earn more than enough money to cover their yearly interest payments, they were highly dependent on the debt market, and if the credit market were to seize up, as it did in late 2008 early 2009, or if the companies found it challenging to issue new debt, then the value of both companies would be negatively impacted. If both companies

8

Hazelton Capital PartnerSeptember2016 Edition IV

(C) ValueWalk 2016 - All rights Reserved

were unable to “roll-over” or issue new debt, they could be forced into bankruptcy. As dramatic and unlikely as this may sound, this is nearly what happened to General Electric after the collapse of Leh-man Brothers in 2008. Just like diversification, reducing the correlation within a portfolio is not a form of insurance; it will not protect the portfolio against a precipitous decline in the equity markets. But, understanding how equities are correlated will help an investor fortify his portfolio.

At the end of your second quarter, another company the fund owned was Japanese conglomerate Softbank. Can you tell us a bit about this position?

Softbank is a holding company run by Masayoshi Son. Its main assets include: a domestic Japanese telecom business; an 80% stake in Sprint; a 43% stake in Yahoo Japan; and a 28% position in Alibaba, which Softbank recently reduced from 32%. Additionally, Softbank has some smaller investments/ownership stakes in ride sharing, internet & media, and e-commerce companies. It truly is a con-glomerate.

What first attracted Hazelton Capital Partners to Softbank was its assets, or to be more clear, the deep and widening discount between the value of Softbank’s assets and its market capitalization. At the time of our first investment, Hazelton Capital Partners believed that there was at least a 30% discount between the value of its four primary assets and the price that the market was assigning to Softbank’s stock. That gap grew even wider to what we believe was a 65% discount in the first quarter of this year when Hazelton Capital Partners added to its position. Today, Softbank’s investment in Alibaba is worth around $75 billion while Softbank’s market capitalization comes in around $80 billion, which means that its domestic telecom business, Sprint, its 43% stake in Yahoo Japan and its additional in-vestments together equals just $5 billion.

A lot of attention has been focused on Sprint debt and whether it can survive given its debt level. So, let’s assume that Sprint goes into bankruptcy and is worth zero. It is important to remember that all the debt held by Sprint, which is reflected on Softbank’s balance sheet, is non-recourse to Softbank and collateralized by Sprint’s assets. So, if Sprint goes away, so does about $35 billion of debt on Softbank’s balance sheet. I estimate Softbank’s 43% stake in Yahoo Japan to be conservatively worth around $10 billion based on valuations from the recent bidding process for some of Yahoo’s assets. As for Softbank’s domestic telecom business, that business has a range of $50 to $60 billion, again conservatively priced. And we have not even gotten into all of the investments and ownership stakes Softbank has in companies like Gung Ho. I feel strongly that there remains a meaningful discount

9

September2016 Edition IV

(C) ValueWalk 2016 - All rights Reserved

Hazelton Capital Partner

between what Softbank owns and its share price.

The main reasons for the deep discount is because of Sprint. Sprint has been a money pit that has forced Softbank to continuously spend billions of dollars to keep it alive. Eliminating Sprint from its portfolio would not only reduce Softbank’s debt and free up capital for future investments, but it would get rid of the uncertainty that has been plaguing the company, but I do not see that happening any time soon.

What do you think about the group’s recent $32 billion cash deal to buy ARM Holdings?At first blush, it is difficult to see the logic in the acquisition. There are no cost savings, overlapping technologies, or synergies between Softbank’s existing companies. However, that is not the reason Softbank purchased ARM Holdings. Masayoshi Son believes that the next technological wave will be the “Internet of Things,” where all mobile devices, home appliances, and automobiles will be connected and “communicating” with one another. Today, there are over 14 billion connected devices worldwide and that number is expected to more than quadruple by 2020. At the center of this disruption will be ARM Holdings, whose processor and graphics intellectual property has become the platform that other companies, like Apple, Samsung, Broadcom and Qualcom, license to design their proprietary chipset.

Of course, it’s hard to get around the $32 billion price tag which currently equates to 20x revenues and over 50x earnings. But those multiples should fall, especially if the “Internet of Things” and the con-nectivity of devices lives up to future expectations. The additional debt raised to finance the deal was denominated in Yen, so it will carry a low-interest rate that can be covered by ARM Holdings current earnings. The real question is: Will this investment be similar to Alibaba or Sprint?

One position I’d really like to talk about is your Micron holding. This is a company that’s attracted plenty of controversy in the past. What do you like about Micron and what’s your outlook for the com-pany over the next 12 to 24 months?

10

Hazelton Capital PartnerSeptember2016 Edition IV

(C) ValueWalk 2016 - All rights Reserved

By Mixabest (Own work) [Public domain], via Wikimedia Commons

Micron is another example of a company with a number of moving parts. The company is a manufac-turer of DRAM memory and NAND storage. Currently, the NAND industry is transitioning from a 2D to 3D platform, which will significantly expand not only the amount of storage available on a chip but the input/output speeds and durability as well. Converting to 3D NAND is not just a next-generation rollout, but a complete redesign of flash storage which requires a significant amount of time and capital from Micron to retool its production

During this transition, Micron has been negatively impacted by lower production levels, greater ex-penses, and the ongoing cyclicality of the market all of which has taken a toll on its earnings over the past few quarters. Additionally, the continued decline in sales of desktop computers over the past few years has been an ongoing headwind to the industry. However, as the revenue from Micron’s PC seg-ment has been in decline, its revenue from cloud and data centers along with mobile devices have been providing consistent growth, especially from mobile devices that continue to provide greater memory and storage capabilities.

The digital memory and storage industry has always been very cyclical. However, Micron’s downturn in its share price over the past six months has probably been exacerbated by the ongoing decline in PC sales along with the industry transition to 3D NAND. Given the recent industry consolidation in both DRAM and NAND witnessed over the past five years, combined with the increasing appetite consum-ers and businesses have for memory and storage, the demand for Micron’s products should continue to be in high demand over the long-run. The uncertainty that exists surrounds Samsung, the 800-pound gorilla in the room. Having a meaningful market share in both DRAM and NAND means that Sam-sung can negatively impact both volume level and pricing if they decide to be “irrational.”

11

September2016 Edition IV

(C) ValueWalk 2016 - All rights Reserved

Hazelton Capital Partner

Since May, Micron stock has rallied over 70% as both DRAM and NAND spot prices have recovered and competitors are reporting declining inventories while raising guidance going into the end of the year. Just like the downturn in its stock price from October 2015 till May of 2016 was exaggerated, my feeling is that the movement from May through its current share price has the makings of a snapback rally. I still think that there remains a meaningful gap between Micron’s current share price and its future intrinsic value, but given the strong rally we have witnessed in its share price over the past four months, I would not be surprised to see the stock sell off before it continues to close the gap.

Alongside Hazelton’s “Core Strategy” you also run an “Overlay Strategy”. What’s the purpose of the “Overlay Strategy”?Hazelton Capital Partners utilizes two investing strategies: The Core Strategy and an Overlay Strate-gy. The Core strategy, as we discussed earlier, creates a concentrated portfolio of 15-20 uncorrelated equity holdings. The Overlay Strategy is used to complement the core strategy by creating cash flow or providing a hedge for a particular name or segment within the portfolio. With the Overlay Strate-gy, Hazelton Capital Partners will invest in mergers and acquisitions, spinoffs, commodities, curren-cies and can short individual stocks or indexes. But options represent the lion share of our Overlay Strategy.

Can you give an example of a trade you might put on within the “Overlay Strategy”?One of our most commonly used option strategies is to sell a ratio call or put spreads to exit or enter a position. Let’s assume we have a long position in a stock that is currently trading around $34/share and our exit level is at $40/share. For the right price, Hazelton Capital Partners will execute a spread where we purchase the 35 strike calls and simultaneously sell the 37.5 strike calls in a ratio of 1 by 2. So, for every 35 strike call option we purchase, we will sell 2 of the 37.5 calls and receive a premium to do so. In other words, we are getting paid to put on this spread. Now, let’s consider the three scenar-ios that might happen when these options expire. The first scenario is that the stock price at expira-tion is below the $35/share. In this case, all of the options expire out of the money, Hazelton Capital Partners still has its original stock position and has banked the premium it received for putting on the ratio call spread. The second scenario is that at expiration, the stock price has risen above $35/share but is lower than $37.50/share. At this point, the 35 strike calls are now in-the-money, and the Fund is now long more shares of the stock at $35/share - the strike price of our long calls. Hazelton Capital Partners can quickly sell out of these newly acquired shares and bank that profit along with the premium received to put on the spread, while still maintaining the original position. In the last scenario, the stock price is above $37.50/share at the time of expiration. At this point, both the 35 and

12

Hazelton Capital PartnerSeptember2016 Edition IV

(C) ValueWalk 2016 - All rights Reserved

37.50 strike calls are both in the money, and the transaction looks like this: Hazelton Capital Partners gets long shares at $35/share - the strike price of our long calls and sells shares at $37.50/share - the strike price of our short calls. We do this in a ratio of 1 by 2. The shares we sell at $37.50/share will be offset by both the shares we got long at $35.00/share and the long shares of the stock we had before putting on the ratio spread. However, the shares sold at $37.50/share are now valued at over $40/share. When we simultaneously bought shares of the stock at $35 and sold them at $37.50, the fund made $2.50/share - the difference between $35/share and $37.50/share. When $2.50/share plus the original premium received is added to the $37.50/share, then the level at which we sold those shares becomes greater than $40/share. So, it is possible to sell shares at $40 even if the stock were never to reach that level. I probably made it sound a lot more complicated than it is, but the same strategy can be used with a ratio put spread to enter into position.

By Thomas J. O’Halloran, photographer [Public domain], via Wikimedia Commons

It is important to remember that there are risks associated with using options. Options are like insur-ance policies: They both have a set expiration date, a deductible, which for options is the strike price, and they both have a premium. The greater the chance of reaching the deductible, the higher the premium one must pay. When purchasing or selling an option, investors need to make sure that the premium paid or received is commensurate with the volatility of the stock. Paying too high a premium for an option could easily mean that an investor will lose money, even if the options are in the money at the time of expiration. But the biggest risk most investors do not consider is the cost of a missed op-portunity. In the earlier examples, I only talk about the stock price at expiration. Of course, as we have all witnessed over the past 12 months, a stock’s share price can become very volatile. It is likely that the stock’s share price could easily have rallied over $40/share before settling below $35/share at expiration.

13

September2016 Edition IV

(C) ValueWalk 2016 - All rights Reserved

Hazelton Capital Partner

If an investor did not sell his share at $40 because he felt “handcuffed” by the spread he had on, then the premium received will not make up for the missed opportunity. Other scenarios could lead to a lost opportunity, including a quick spike through $40 on a takeout offer or other news. The important thing to take away is that investors need to have a clear understanding of how options premiums react to changes in volatility, days to expiration, and overall market sentiment before putting on an option strategy, like a ratio call or put spread.

Are there any new positions that you’re looking are looking at right now for the “Core Strategy” or are you sitting on your hands as val-uations rise?Well, we are never sitting on our hands. Every morning, we wake with the singular goal of finding a new company to invest. Having a limit of 15-20 positions means that any company we wish to add to the portfolio will have to bring something to the table that is not already reflected in our current holdings. Being cheaply priced versus the company’s future value is, of course, a major criteria we look for, but as I have said before, we want to construct a portfolio of uncorrelated companies with a sustainable competitive edge.

At the moment, we have around a 22% cash position, which is up from the 7% cash level we had during the first quarter. So, we are finding more positions to sell or reduce at this time than names to purchase.

There are about five to seven companies that we have done a material amount of research and valu-ation on over the past few months. These companies are a number of different industries, including energy, and meet all of our criteria except for one: The price. So, we will be patient, and in the mean-time, continue to look for new investments.

You have over two decades of experience investing, what has been the most valuable lesson you’ve learned over the years?Patience. As we spoke about earlier, fear and greed are the key emotions influencing an investor’s be-havior. Since these emotions have been hardwired into our psyche, one cannot just turn them off any more than one can decide when to breathe. Left unchecked, fear and greed will hijack any investing process. However, with patience, an investor can have the time to deliberate, be thoughtful and cre-ative.

14

Hazelton Capital PartnerSeptember2016 Edition IV

(C) ValueWalk 2016 - All rights Reserved

Many investors have a short-term focus, and therefore are always reacting to the changes in a company’s share price. They are driven by the idea that greater activity leads to greater results. A patient investor with a long-term focus will have the discipline to remain objective, especially when markets become vol-atile. This allows him to turn uncertainty into opportunity. We are all familiar with the mantra: “Don’t Just Stand There, Do Something.” For the patient investor, the mantra is: “Don’t Just Do Something, Stand There.” Stand there with the fortitude to withstand criticism, uncertainty, and self-doubt until an opportunity presents itself.

What’s been your greatest mistake and what did you take away from the experience?There are some very brilliant investors whose expertise I hold in high regard. In the past, I have used their portfolio holdings as a starting point for my research, or as a confirmation of a recent investment. But as we have seen over the past year or so, even well-respected investors can make mistakes. Early on, I would outsource some of my research to these investors believing that given the amount of money they managed and the track record that had amassed, their vetting process was more evolved than mine. I still did research on the name before adding it to my portfolio, but it was not of the caliber it should have been or the in-depth process that I use today.

The problem I had when relying on other people’s portfolios was that my research was incomplete. I did not have a full understanding of the company, its key metrics, and all the risks involved. As you proba-bly have guessed, a few of the positions that I added to the portfolio that were based on other investors holdings ended up going south. It did not take me long to discover that I did not do enough research to make a qualified decision to invest in the company in the first place, let alone know whether a downturn in the stock price was an opportunity to add to or cut my losses.

Those mistakes made me refocus my efforts on doing my own homework and not take shortcuts by interpreting the value of a company based on what other investors were buying. I still pay attention to what other investors are adding or subtracting from their portfolios, but I am more conscientious about doing my own homework, and that has helped me gain more consistent results.

15

September2016 Edition IV

(C) ValueWalk 2016 - All rights Reserved

Hazelton Capital Partner

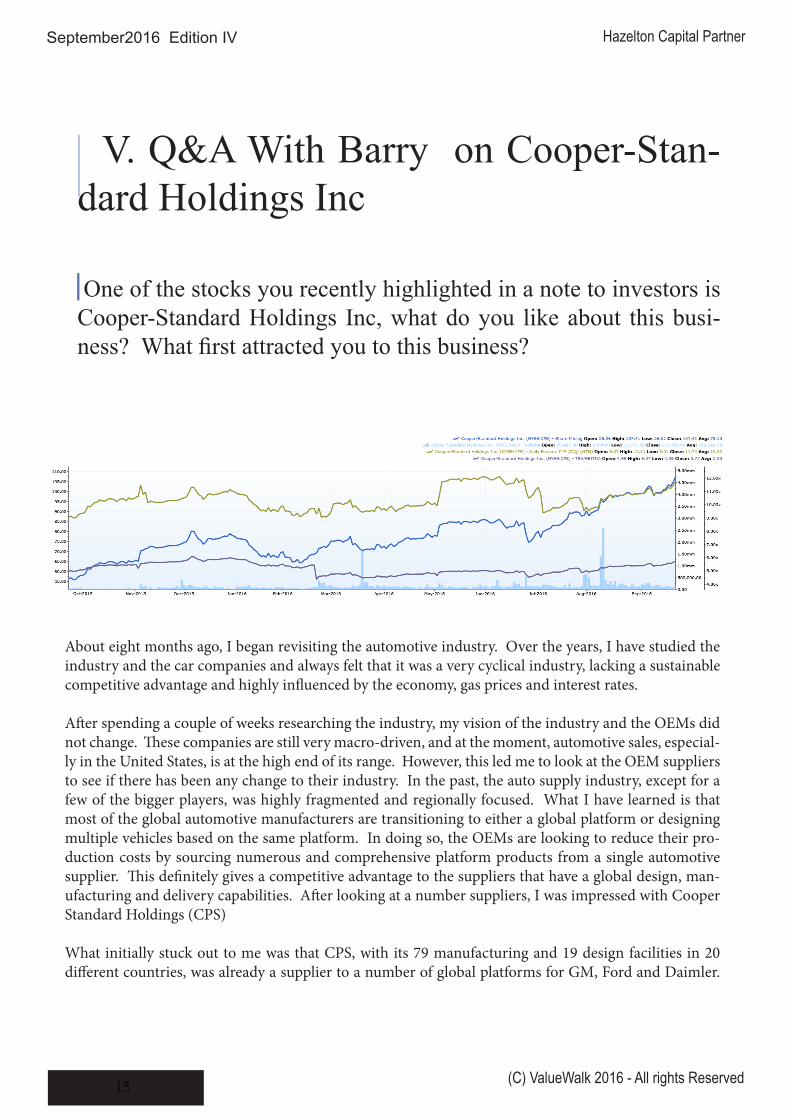

About eight months ago, I began revisiting the automotive industry. Over the years, I have studied the industry and the car companies and always felt that it was a very cyclical industry, lacking a sustainable competitive advantage and highly influenced by the economy, gas prices and interest rates.

After spending a couple of weeks researching the industry, my vision of the industry and the OEMs did not change. These companies are still very macro-driven, and at the moment, automotive sales, especial-ly in the United States, is at the high end of its range. However, this led me to look at the OEM suppliers to see if there has been any change to their industry. In the past, the auto supply industry, except for a few of the bigger players, was highly fragmented and regionally focused. What I have learned is that most of the global automotive manufacturers are transitioning to either a global platform or designing multiple vehicles based on the same platform. In doing so, the OEMs are looking to reduce their pro-duction costs by sourcing numerous and comprehensive platform products from a single automotive supplier. This definitely gives a competitive advantage to the suppliers that have a global design, man-ufacturing and delivery capabilities. After looking at a number suppliers, I was impressed with Cooper Standard Holdings (CPS)

What initially stuck out to me was that CPS, with its 79 manufacturing and 19 design facilities in 20 different countries, was already a supplier to a number of global platforms for GM, Ford and Daimler.

V. Q&A With Barry on Cooper-Stan-dard Holdings Inc

One of the stocks you recently highlighted in a note to investors is Cooper-Standard Holdings Inc, what do you like about this busi-ness? What first attracted you to this business?

16

Hazelton Capital PartnerSeptember2016 Edition IV

(C) ValueWalk 2016 - All rights Reserved

Since emerging from bankruptcy in 2010, Cooper Standard has been working on expanding its global footprint through acquisitions and joint ventures focused on gaining a stronger foothold in emerging markets, like China. Most supply contracts run about five years, but also include a two-year design segment where the company works directly with the automotive manufacturer’s design team. Since Cooper Standard’s products are specifically designed for a future automotive car model, it means that it will be very difficult for the OEM to transition to another supplier midstream without having to modify their current product design. Supplying automotive OEMs can become a very sticky business. Once a product is included in the automotive platform, the revenues and margins become predictable and sustainable for the life of the contract.

What’s the company’s main line of business?Cooper Standard Holdings is a supplier of Sealing Systems, Fuel & Brake Delivery Systems, Fluid Trans-fer Systems and Anti-Vibration Systems to the global automotive OEMs and holds a leadership position in each one of those segments. Its global footprint allows it to design, manufacture and distribute its products for automobiles and lightweight trucks worldwide. Approximately 80% of Cooper Standard’s sales are to global OEMs with the remaining sales going to Tier I and II automotive suppliers.

It seems Cooper is highly exposed to the global auto market. Are you not worried about macro headwinds impacting vehicle demand?I am not overly optimistic about the future growth of the automotive industry, especially the short-term outlook in the US. In February of 2009, seasonally adjusted US vehicle sales bottomed out around 9 million units. That number doubled to 18 million by October 2015, and as of July 2016, is still hovering around 17.8 million units, well above its 40 year average of 14.5 million units. Even though the average vehicle on the road today is about 11.5 years old, there are a number of headwinds facing the industry: A combination of low-interest rates, low oil prices, and government and dealer incentives have been driving North American vehicle sales, which currently is averaging over $34,000 per vehicle. What is more concerning is that car manufacturers are incentivizing auto sales with extremely attractive financ-ing. Recently, Ford announced its “Ford Freedom” plan which provides 0% APR for 72 months. With the average duration of a car loan now over 68 months, car loan delinquency rates rising, interest rates and oil prices expected to increase over time, and the overall economic growth lackluster, I would not be surprised to see a contraction in US auto sales. Outside the US, automobile sales are anticipated to be flat, at best. The only area of growth is expected to come from China and some emerging segments within Asia. Together, North America and Europe represent approximately 85% of CPS’ revenue. Hav-ing said all of that, I still believe that for a patient investor, CPS still represents a significant investment opportunity given its competitive advantages and future operational improvements that will lead to

17

September2016 Edition IV

(C) ValueWalk 2016 - All rights Reserved

Hazelton Capital Partner

higher revenue, margins and earnings.

The three main catalyst that I believe will drive Cooper Standard’s future growth are: 1) New/renewed contract wins leading to increased number of global platform and premium products per vehicle; 2) Ex-panding the company’s global footprint and revenues to reflect higher growth regions, especially China and Asia Pacific; and 3) Global adoption of Cooper Standard Operating System (CSOS), including cen-tralizing the company’s worldwide bidding process and cost structures, while restructuring European operations to reflect global OEM and regional changes.

It is important to remember that Cooper Standard Holdings emerged from bankruptcy in May 2010. At that time, the company was more focused on winning contracts and utilizing its manufacturing fa-cilities than it was on margins or profitability. And given that its balance sheet was still in recovery, the company was probably happy to get whatever contracts it could. Those contracts are now coming up for renewal along with a new request for a quote on redesigned platform models. With a more robust balance sheet and a new management team that took over in 2012, CPS is not only more focused on return on invested capital and profitability but has become a stronger and more dependable partner to the automotive industry. Cooper Standard is also adding a number of new premium products that are more durable and significantly lighter than their existing legacy products. These premium products carry a higher ASP and margins, as they help OEMs meet future CAFE standards by helping reduce the weight of the automobile.

Historically, Cooper Standard products have been underrepresented with Asian automotive manufac-turers like Toyota, Kia and Hyundai, partly because they did not meet the strict operational standards set forth by those OEMs and partly because CPS was not part of the OEM’s Keiretsu network. Cooper Standard is hoping its recent contract win with Honda will help it gain additional credibility and open future opportunities with Toyota, Kia, and Hyundai. The Honda win also highlights the operational changes that are taking place within the company and should continue to bolster it standings amongst European and North American OEMs, as well.

One of the areas that I think is overlooked by the market is the meaningful change that is occurring within Cooper Standard at the operating level. Since taking over as CEO in 2012, Jeff Edwards has refo-cused the operations of the company, making it more flexible and less dependent on volume to achieve profitability. He implemented the Cooper Standard Operating System to ensure global consistency in engineering, design, manufacturing and distribution across all facilities globally. These operating sys-tems are expected reduce waste, lower inventory needs, and produce positive changes to their working capital and cash flows.

The stock is up nearly a third year-to-date. Are you still bullish after this recent rally?For the long-run, absolutely. Most of the future revenue growth and margin expansion that I am ex-pecting will start to have an impact over the next 12 to 18 months as contracts go into production and operational leverage that the company has been paying for finally takes hold. In the meantime, with the

18

Hazelton Capital PartnerSeptember2016 Edition IV

(C) ValueWalk 2016 - All rights Reserved

stock up around 30% for the year, short-term investors will be looking for the next catalyst to drive the stock price higher. Absent of that catalyst, Cooper Standard’s stock price will be highly influenced by the strength or weakness of the automotive market. This company is always going to be painted with the same paintbrush as the rest of the automotive industry, but for the patient long-term investor, this is an opportunity because the company’s future profitability is not reliant on whether SAAR remains at 18 million units/year. In my view, a decline in the share price of auto manufacturers and suppliers will provide an even better entry level for CPS.

What about valuation? Do you have a price target for the stock and how long do you think it will before it hit this target? What’s your bull/bear case estimate of intrinsic value for the stock?

Given the impressive recovery we have seen in car sales since 2009 and the headwinds I spoke about, one could easily make the case that today, Cooper Standard’s stock is fairly priced. However, I am fo-cused on the CPS’ future revenue and margin growth opportunities, and that is the reason why I remain optimistic about the company. There are a number of moving parts when valuing this company, so Hazelton Capital Partners broke down the valuation into three outcomes: A Bear, Base, and Bull Case for the stock.

The bear case assumes North America’s revenues will decline over the next two years, before returning to growth in 2018 through 2020. Europe remains flat through 2018 and then grows around 3% from 2019-2020. Asia is the outlier, growing around 15% driven primarily by China. Overall EBITDA mar-gins will fall to 10.75% in 2017, recover to 11.75% in 2018, and begin to touch 13% by 2020. There is no change to current debt or cash levels, and the EV/EBITDA multiple will decline to 4.5x in 2017, before recovering to 5.5x by 2020. CPS’ share price falls to $65/share by 2017 and recovers to $130/share by 2020.

The base case conservatively values the company with the key assumptions beingthat North American revenue will grow around 5-6%, faster than the 3% projected for theautomotive industry. Europe’s growth will be flat until 2018, and then grow at 3%; Asia willgrow around 20%, and EBITDA margins will expand to 13.5% by 2020. Thereis no change to current debt or cash levels, and the EV/EBITDA multiple will increase to5.5x. This puts the CPS’ share price at around $105/share by early 2017, and $170/share by 2020.

The bull case is an optimistic outlook for the automotive industry and CPS’ opportunities to expand its global footprint. North America’s revenues grow steadily, hitting 10% revenue growth by 2020, driv-en by new contract wins and product mix. European operations and restructuring sees flat revenue through 2017 but growing to 7% by 2020, and Asia’s growth, driven mostly by China, comes in slightly above 20% by 2020. EBITDA margins expand from 11.5% to 14%, with a positive impact from North America’s contract wins and product mix, Europe’s restructuring, improved utilization in Asia, and suc-cessful implementation of CSOS. There is no change to current debt or cash levels, and the EV/EBITDA multiple will increase from 5.5x to 6.5x by 2020, reflecting CPS’ significant growth and in line with peer multiples. CPS’ share price rises to $120/share by 2017 and continues to grow to $220/share by 2020.

19

September2016 Edition IV

(C) ValueWalk 2016 - All rights Reserved

Hazelton Capital Partner

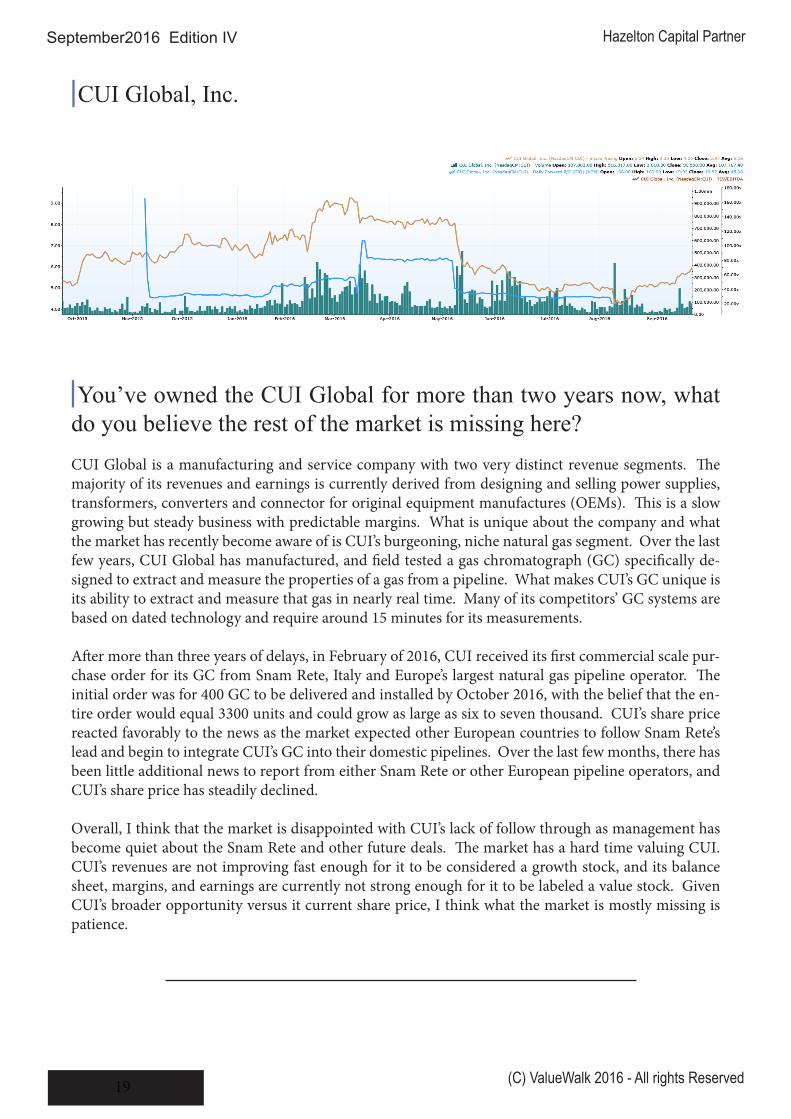

You’ve owned the CUI Global for more than two years now, what do you believe the rest of the market is missing here?CUI Global is a manufacturing and service company with two very distinct revenue segments. The majority of its revenues and earnings is currently derived from designing and selling power supplies, transformers, converters and connector for original equipment manufactures (OEMs). This is a slow growing but steady business with predictable margins. What is unique about the company and what the market has recently become aware of is CUI’s burgeoning, niche natural gas segment. Over the last few years, CUI Global has manufactured, and field tested a gas chromatograph (GC) specifically de-signed to extract and measure the properties of a gas from a pipeline. What makes CUI’s GC unique is its ability to extract and measure that gas in nearly real time. Many of its competitors’ GC systems are based on dated technology and require around 15 minutes for its measurements.

After more than three years of delays, in February of 2016, CUI received its first commercial scale pur-chase order for its GC from Snam Rete, Italy and Europe’s largest natural gas pipeline operator. The initial order was for 400 GC to be delivered and installed by October 2016, with the belief that the en-tire order would equal 3300 units and could grow as large as six to seven thousand. CUI’s share price reacted favorably to the news as the market expected other European countries to follow Snam Rete’s lead and begin to integrate CUI’s GC into their domestic pipelines. Over the last few months, there has been little additional news to report from either Snam Rete or other European pipeline operators, and CUI’s share price has steadily declined.

Overall, I think that the market is disappointed with CUI’s lack of follow through as management has become quiet about the Snam Rete and other future deals. The market has a hard time valuing CUI. CUI’s revenues are not improving fast enough for it to be considered a growth stock, and its balance sheet, margins, and earnings are currently not strong enough for it to be labeled a value stock. Given CUI’s broader opportunity versus it current share price, I think what the market is mostly missing is patience.

CUI Global, Inc.

20

Hazelton Capital PartnerSeptember2016 Edition IV

(C) ValueWalk 2016 - All rights Reserved

CUI Global looks to be a traditional contrarian bet; the stock is down by 27% this year. What do you like about the company?CUI Global is the type of company that Hazelton Capital Partners likes to buy. It operates is a niche seg-ment of large industry, flying below most investors’ radar. I feel the downside is identifiable and limited while the upside could be very significant with a number of positive events beyond its recent deal with Snam Rete. Given where the stock has currently been trading, it would not take a lot of new contracts to impact the company’s revenues and earnings positively. I, like other investors, have been disappointed at the cadence of new and current sales, but given the company’s disruptive technology that applies to a number of industries beyond just natural gas, I feel there is promising upside potential, especially when compared to its current share price.

Do you think the equity has a further near-term downside?Until CUI can show steady growth from new and/or existing purchase orders, I think that the uncer-tainty will weigh on the company’s share price. I would not be surprised to see the stock continue to languish at these levels or even decline further down to around the $4.25/share level.

If everything goes to plan how much do you think the company could be worth?That’s a good question. Just like with CPS, I think the easiest way to value the company is with a Bear, Base and Bull valuation for the company.

The Bear case for CUI is that there are delays with new and potential purchase orders. Instead of in-stalling approximately 1000 units per year, Snam Rete slows down its purchase orders and drags out the process. Additionally, potential customers from France, Germany, Spain, and Portugal also delay their request for quote and potential purchase orders. At this point, CUI continues to be dependent on its power supply business to support the entire company. The power supply business, based on past rev-enues and margins, I valued to be around $3.50 to $4.00 per share. Assuming CUI can maintain and or grow its power supply revenues, this should provide a baseline valuation for the company. CUI has openly talked about separating the two companies once the GC segment got stronger. Recently, there have been rumors floating that the company is rethinking its time table for separation.

21

September2016 Edition IV

(C) ValueWalk 2016 - All rights Reserved

Hazelton Capital Partner

The key assumption to the Base case is that the Snam Rete deal moves ahead with CUI winning the lion share of the 3300 units. Additionally, some of the other GC opportunities start to bear fruit as CUI re-ceives RFQ from countries like Germany, France, Spain, and Portugal. This would provide the company with a more certainty arounds its GC revenues and give investors more comfort as well. If this were to happen, I think we could easily see the company’s share price rebound to the $9/share level we saw initially after the Snam Rete announcement in February.

The Bull case is the Base case with the expansion of the Snam Rete deal from 3300 units to a total of 6 or 7 thousand units. It also includes more clarity around purchase orders for countries like Germany, France, Spain, and Portugal and conversion of trial projects in the LNG, Ethylene and other industries into RFQ and purchase orders. This is a bit more difficult to value because these ancillary industries vary by both size and scope. At the moment, some of CUI’s GC components are being used in LNG ter-minals at Chevron’s Gorgon facility in Australia and at a North American Ethylene Plant in South Texas. If all of these opportunities result in purchase orders, then CUI stock could easily be north of $15/share.

How long will it take to hit this stage?Unfortunately, CUI is dependent on other company’s schedules to generate its revenues. And many of its customers are bureaucratic operations. When Snam Rete provided its initial RFQ, it released its schedule surrounding its GC purchases to be about 1,000/year over the next three years. Assuming the next purchase order reflects that schedule, I think that should help investors become more comfortable with CUI’s future revenues.

Are there any major speed-bumps that could derail your investment thesis?There are some speed-bumps that could negatively impact CUI and our investment thesis. One of them is the company’s balance sheet. Currently, CUI has about $6 million in cash. This is down from $12 and $7 million in 2014 & 2015 respectively, as the company has been spending money to build out its infrastructure and support its growing GC operation. The fear is the company will not have enough cash or working capital to fulfill future orders. The good news is that CUI has a $4 million dollar line of credit from Wells Fargo and has also mentioned that it can borrow against future purchase orders.

There is also the risk that future demand for GC’s will not live up to the initial hype. However, I think the biggest uncertainty facing the company is the risk that one of its competitors can create a competing technology that will steal away CUI’s market share. Companies like ABB, Emerson and Elsters, who are active in the GC market, have the financial means to deploy hundreds of millions of dollars into GC research and could easily disrupt the industry. However, the GC market is currently about a $400 million dollar per year industry at best and that includes future growth from Europe. This is a meaning-

22

Hazelton Capital PartnerSeptember2016 Edition IV

(C) ValueWalk 2016 - All rights Reserved

ful number to CUI but remains either a subtle portion or a rounding error to one of CUI’s competitors yearly revenue. At CUI’s current $120 million market capitalization, or even at double that price, if one of CUI’s competitors felt strongly about having a strong foothold in the GC space, they could easily pur-chase the company outright. That purchase would probably equal the same amount of capital needed over a handful of years to disrupt the industry and steal market share, but with more certainty of success.

Charts with permission from S&P Capital IQ

By Rupert Hargreaves for (C) ValueWalk 2016 - All rights reserved. All materials in this PDF are pro-tected by United States and international copyright and other applicable laws. You may print the PDF website for personal or non-profit educational purposes only. All copies must include any copyright no-tice originally included with the material and a link to ValueWalk.com. All other uses requires the prior explicit written permission by ValueWalk