SEMI Equipment and Materials Market Updatesemieurope.omnibooksonline.com/2015/semicon_europa... ·...

31

SEMI Equipment and Materials Market Update Clark Tseng, Sr. Manager SEMI Industry Research & Statistics October 2015

Transcript of SEMI Equipment and Materials Market Updatesemieurope.omnibooksonline.com/2015/semicon_europa... ·...

SEMI Equipment and Materials Market Update

Clark Tseng, Sr. ManagerSEMI Industry Research & Statistics

October 2015

Outline

• 2015 Year-to-Date Trends

• Equipment Market Outlook

• Materials Market Outlook

• Summary

Year-to-Date Trends

2015 Semiconductor Revenue Forecasts

2.3%

5.0%

3.4%

3.0%

2.0%

4.3%

0% 1% 2% 3% 4% 5% 6%

WSTS (Aug 15)

IDC (Sep 15)

Cowan LRA (Aug 15)

TSMC (Jul 15)

IC Insights (Aug 15)

Semico Research (Sep 15)

Source: Compiled by SEMI

Year to Date…

• Growing uncertainty in the global economic condition – Slower growth from emerging markets; mediocre

European market; Japan 2Q GDP contraction; China stock market…

• Semiconductor revenue forecasts lowered– Generally, from mid-single digit to low-single digit– Japan and Europe currency devaluation – Inventory issue, PC/tablet market down, high-end smart

phone market growth slowing…– Declining DRAM pricing

• Some companies reduced capex for 2015 Yet…

Unit Trends-Strong Year-over-Year growth for 1H

Source: SEMI and WSTS

Silicon Area Shipment Index

100

120

140

160

180

200

220

240

260

280

Jan-

12

Ap

r-12

Jul-

12

Oct

-12

Jan-

13

Ap

r-13

Jul-

13

Oct

-13

Jan-

14

Ap

r-14

Jul-

14

Oct

-14

Jan-

15

Ap

r-15

Jul-

15

Ind

ex V

alu

e

Worldwide Wafer Area Shipment Index(Three-month Moving Average)

Source: SEMI Silicon Manufacturers Group August 2015

Silicon shipments are up 7% year to date through July

0.90

0.95

1.00

1.05

1.10

1.15

Jan

-14

Feb

-14

Mar

-14

Ap

r-1

4

May

-14

Jun

-14

Jul-

14

Au

g-1

4

Sep

-14

Oct

-14

No

v-1

4

De

c-1

4

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5

May

-15

Jun

-15

Jul-

15

(f)

15

-Au

g (p

)

Bo

ok-

to-B

ill R

atio

$800$1,000$1,200$1,400$1,600$1,800

Jan

-14

Feb

-14

Mar

-14

Ap

r-1

4

May

-14

Jun

-14

Jul-

14

Au

g-1

4

Sep

-14

Oct

-14

No

v-1

4

De

c-1

4

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5

May

-15

Jun

-15

Jul-

15

(f)

Au

g-1

5…US$

Mil

lio

ns

North American Headquartered Manufacturers Global Capital Equipment Book-to-Bill

(based on three month averages)

Bookings Billings

SEMI North America Book-to-Bill-Steady booking and billings trends thru August

Source: SEMI August 2015

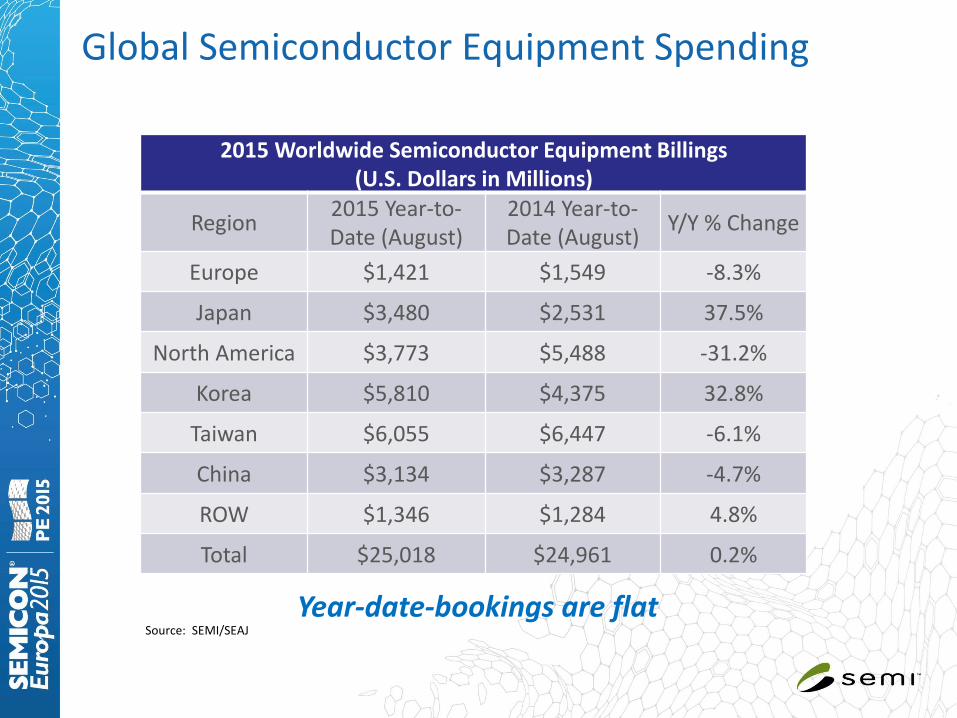

Global Semiconductor Equipment Spending

Source: SEMI/SEAJ

2015 Worldwide Semiconductor Equipment Billings(U.S. Dollars in Millions)

Region2015 Year-to-Date (August)

2014 Year-to-Date (August)

Y/Y % Change

Europe $1,421 $1,549 -8.3%

Japan $3,480 $2,531 37.5%

North America $3,773 $5,488 -31.2%

Korea $5,810 $4,375 32.8%

Taiwan $6,055 $6,447 -6.1%

China $3,134 $3,287 -4.7%

ROW $1,346 $1,284 4.8%

Total $25,018 $24,961 0.2%

Year-date-bookings are flat

Equipment Market Outlook

66%

14%

-7%5%

-9%

28%40%

66%

10%5%

-21%

17%

87%

-41%-30%

12%

67%

-11%

23%6%

-31%-46%

150%

9%

-15%-14%

18%3%

5%

-100%

-50%

0%

50%

100%

150%

200%

$0

$10

$20

$30

$40

$50

$60

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

F20

16F

An

nu

al G

row

th(%

)

Ca

pit

al E

qu

ipm

en

t($

US

Bil

lio

n)

Capital Equipment Annual Growth

Capital Equipment Cycles

Source: SEMI/SEAJ. SEMI 2015 Mid-Year Forecast, August update

Regional Semiconductor Equipment Markets

China12% Europe

6%

Japan11%

Korea18%

North America

22%

ROW6%

Taiwan25%

2014 = $37.50 billion

Region 2014$US B

2015F$US B

%Change

China $4.37 $4.56 4%

Europe 2.38 2.50 5%

Japan 4.18 5.29 27%

Korea 6.84 8.13 19%

North America 8.16 6.26 -23%

SEA/ROW 2.15 2.14 -1%

Taiwan 9.41 9.56 2%

Total $37.50 $38.44 3%

Source: SEMI/SEAJ August 2015 update

Totals may not add due to rounding

Fab Equipment Spending-Driven by Memory and Foundry

The Return of 200mm Capacity

Foundries-Ramping 200mm capacity in 2015 and 2016

2010 2011 2012 2013 2014E 2015F 2016F

Foundry only- 200mm 2.12 2.19 2.27 2.29 2.28 2.37 2.43

1.95

2.00

2.05

2.10

2.15

2.20

2.25

2.30

2.35

2.40

2.45

2.50

2010 2011 2012 2013 2014E 2015F 2016F

Inst

alle

d C

apac

ity

(Mill

ion

s w

pm

)

Installed 200mm Foundry Capacity

Source: SEMI World Fab Forecast

Materials Market Outlook

Global Silicon Wafer Shipment Trends

Source: Rose Associates 1991to 1994; SEMI SMG 1995 to 2013; SEMI Forecast

Worldwide Wafer Fab Materials Forecast

Totals may not add due to roundingSource: SEMI August 2015

Actual Forecast

2013US$ M

2014US$ M

2015US$ M

2016US$ M

Silicon Wafers1 $7,932 $7,990 $7,954 $8,278

Photomasks2 3,136 3,220 3,342 3,442

Photoresist 1,220 1,374 1,354 1,413

Photoresist Ancillaries3 1,428 1,711 1,777 1,850

Wet Chemicals4 995 1,059 1,121 1,104

Gases 3,319 3,481 3,577 3,721

Sputter Targets4 598 629 653 696

CMP Slurry & Pads5 1,436 1,569 1,618 1,722

Other/New Materials 2,588 2,945 3,178 3,415

Total $22,652 $23,977 $24,574 $25,641

% Growth 6% 2% 4%

Wafer Fab Materials Forecast Notes

1. Silicon wafers include merchant sales value only; includes SOI wafers; no reclaim wafers

2. Includes captive market3. Includes resist removal chemicals, developers, anti-reflective coatings,

contrast enhancers, edge bead removers, adhesion promoters, etc.4. Source is Linx Consulting LLC, Sputter Targets includes precious metals5. Estimates for IC applications only6. Includes low k dielectrics, copper plating solutions, dielectric

precursors, organometallic precursors, etc.7. All forecasts in current dollars8. Source for all data is SEMI, unless otherwise indicated

Photomask Market

Source: SEMI March 2015$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

2005 2007 2010 2015F 2016F

US$

Mill

ion

Taiwan ROW North America Korea Japan Europe China

0%

20%

40%

60%

80%

100%

2005 2015F

Pe

rcen

t of

Mar

ket

Merchant Captive

Source: SEMI March 2015

Regional Fab Materials Markets

China7%

Europe10%

Japan18%

Korea19%

North America

18%

SEA/ROW 6%

Taiwan22%

2015F = $24.6 billion

Region 2015F$US B

2016F$US B

%Change

China $1.77 $1.89 6%

Europe 2.49 2.57 3%

Japan 4.39 4.50 2%

Korea 4.65 4.95 6%

North America 4.46 4.59 3%

Taiwan 5.47 5.73 5%

SEA/ROW 1.34 1.42 7%

Total $24.57 $25.64 4%

Source: SEMI August 2015

Totals may not add due to rounding

Worldwide Packaging Materials Forecast

Totals may not add due to roundingSource: SEMI August 2015

Actual Forecast

2013US$ M

2014US$ M

2015US$ M

2016US$ M

Leadframes $3,342 $3,461 $3,350 $3,346

Organic Substrates1 7,408 7,612 8,196 8,586

Ceramic Packages 2,006 2,075 2,157 2,174

Encapsulation Resins 2,451 2,712 2,922 3,187

Bonding Wire2 4,151 3,385 3,176 3,099

Die Attach Materials3 666 704 734 752

Others 374 409 451 500

Total $20,398 $20,358 $20,986 $21,644

% Growth -0.2% 3% 3%

Packaging Materials will be 46% of the 2015 Total Semiconductor

Materials Market

Major update coming in November

Semiconductor Packaging Materials Forecast Notes

1. Source is TechSearch International. Includes PBGA, PPGA, LGA, and CSP laminate substrates and flex BGA and CSP substrates

2. Assume gold value of $1,480/trz for 2013; $1,260/trz for 2014; $1,190/trz for 2015 - 2016

3. Includes die attach film (tape) materials4. Other includes solder balls and wafer level package

dielectrics5. Source for all data is SEMI, unless otherwise indicated6. All forecasts in current dollars

Packaging Material Market Trends

• CSP laminate substrates, CSP leadframes, and WLP are driven by explosive growth in mobile computing and communications

• Flip chip and copper pillar continue to expand the market for underfillmaterials.

• Need more development for WLP dielectrics used in multi-layer structures

• Mold compounds- warpage control/package reliability (MSL1); withstand high flexing for wearable applications

• QFN- cost optimization through design (including strip size) and reduced plating area (also improves MSL); higher lead counts (routable); improved power dissipation

• Transition from gold wire to copper and silver

Source: SEMI and TechSearch International- Global Semiconductor Packaging Materials Outlook

Regional Packaging Materials Markets

China21%

Europe3%

Japan13%

Korea13%

North America

3%

SEA/ROW26%

Taiwan21%

2015F = $21.0 billion

Region 2015F$US B

2016F$US B

%Change

China $4.34 $4.54 5%

Europe 0.72 0.75 3%

Japan 2.69 2.82 4%

Korea 2.66 2.72 2%

North America 0.66 0.66 0%

Taiwan 4.43 4.56 3%

SEA/ROW 5.50 5.60 2%

Total $20.99 $21.64 3%

Source: SEMI August 2015Totals may not add due to rounding

Regional Semiconductor Materials Markets

China13%

Europe7%

Japan16%

Korea16%

North America

11%

SEA/ROW15%

Taiwan22%

2015F = $45.5 billion

Region 2015F$US B

2016F$US B

%Change

China $6.11 $6.43 5%

Europe $3.21 $3.32 3%

Japan $7.08 $7.32 3%

Korea $7.31 $7.67 5%

North America $5.12 $5.25 3%

Taiwan $9.90 $10.29 4%

SEA/ROW $6.84 $7.02 3%

Total $45.56 $47.28 4%

Source: SEMI August 2015Totals may not add due to rounding

Summary

Europe Market Summary

2016 Outlook

Installed Fab Capacity 1.84 million 200mm-equiv. wafers/monthSEMI is tracking 180 front-end facilities in

Europe/Mideast Region

Packaging & Test >60 production facilities; including focus on wafer bumping, WLP, and 3D

Semiconductor Materials ~$2.5+ billion

Semiconductor Equipment Estimating $2.5 to $3.0 billion in spending

Source: SEMI World Fab Forecast, WWSEMS, & MMDS

Europe Manufacturers

• Intel: 14nm related investments at its Ireland & Israel fabs

• Infineon: Expansion of power IC at Dresden 300mm

• ST Microelectronics: Expansions and upgrades to Crolles 2 Fab lines (including investments related to Nano2017 and Horizon 2020 Vision)

• GlobalFoundries: On-going upgrades in Dresden, 22nm FD-SOI manufacturing to start in 2016.

• IMEC: Spending on Fab 3

Summary

• Uncertainty with the near-term outlook• Industry inventory correction shall come to an end in 4Q15.

• Year-to-Date Trends Silicon shipments are up through July Equipment bookings and billings are comparable to 2014 levels

• Memory and Foundry lead fab investment this year and next

• Semiconductor Equipment & Materials Outlook Materials market is expected to increase 3% in 2015 and 4% in 2016 Equipment market is expected to increase 3% in 2015 and 5% in 2016

Thank YouFor SEMI Market Data and Information, Please Visit:www.semi.org/marketinfowww.semi.org/fabswww.slideshare.net/ehallSEMIwww.youtube.com/user/SEMImktstats

Sign-up for the Monthly SEMI Global Update e-newsletter:www.semi.org/About/SEMIGlobalUpdate/