SEB Enskilda Finnish Blue Chip Seminar 2011 - UPMassets.upm.com/Investors/Documents/2011/SEB Finnish...

23

UPM SEB Enskilda Finnish Blue Chip Seminar 2011 Jussi Pesonen President and CEO 25 August, 2011

Transcript of SEB Enskilda Finnish Blue Chip Seminar 2011 - UPMassets.upm.com/Investors/Documents/2011/SEB Finnish...

UPM

SEB Enskilda Finnish Blue Chip Seminar 2011

Jussi Pesonen

President and CEO

25 August, 2011

FINANCIALS Q2 2011

| © UPM

FINANCIALS

Solid result despite challenging cost

environment

Gearing

44% -11 pp

EBITDA

EUR 751 m +110 m

Operating cash flow

EUR 446 m +135 m

Net debt

EUR 3,162 m -675 m

2

Sales

EUR 2,423 m +9%

EBITDA

EUR 372 m +5%

Operating profit (*

EUR 201 m +1%

EPS (*

EUR 0.26 -10%

*) excluding special items

Q2/2011 vs. Q2/2010 H1/2011 vs. H1/ 2010

| © UPM 3

0

50

100

150

200

250

300

350

400

450

500

EBITDA

Q1/11

EBITDA

Q2/11

FINANCIALS

Q2 2011 EBITDA increased from last year

0

50

100

150

200

250

300

350

400

450

500

EBITDA

Q2/10

EBITDA

Q2/11

EUR million

Prices,

currency

Fibre

costs

Other

variable

costs

Fixed

costs

Deliveries

Energy

costs

EUR million

Prices,

currency Fibre

costs

Other

variable

costs

Fixed

costs

Deliveries Energy

costs

353 15.9%

372 15.4%

379 16.1%

372 15.4%

Price and cost development

stabilised in Q2 vs. Q1 2011

Higher prices offset the rise

in costs in Q2 vs. Q2 2010

| © UPM

FINANCIALS

Operating profit was steady

4

-100

-50

0

50

100

150

200

250

300

EUR million

201 8.3%

199 9.0%

31 1.7%

Operating profit excluding special items

155 6.5%

| © UPM

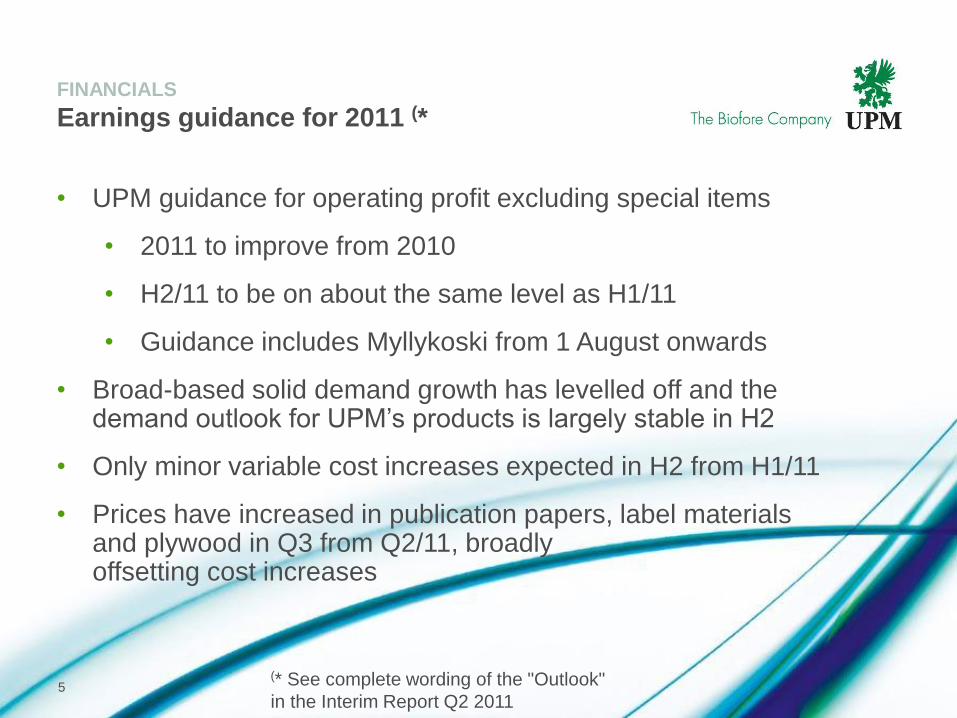

FINANCIALS

Earnings guidance for 2011 (*

(* See complete wording of the "Outlook"

in the Interim Report Q2 2011

• UPM guidance for operating profit excluding special items

• 2011 to improve from 2010

• H2/11 to be on about the same level as H1/11

• Guidance includes Myllykoski from 1 August onwards

• Broad-based solid demand growth has levelled off and the demand outlook for UPM’s products is largely stable in H2

• Only minor variable cost increases expected in H2 from H1/11

• Prices have increased in publication papers, label materials and plywood in Q3 from Q2/11, broadly offsetting cost increases

5

STRATEGIC FOCUS AREAS

| © UPM

8,3

3,5

5,4

8,3

7,2

6,0

8,2

0

2

4

6

8

10

12

2005 2006 2007 2008 2009 2010 H1 2011

Operating profit recovered to the pre-

recession level

% of sales Operating profit excluding special items

Target over 10%

7

| © UPM

8

Operating profit evenly distributed

– Paper is a major source of cash flow

Forest and Timber 3%

Pulp 23%

Energy 14%

Label 6%

Plywood 2%

Cumulative

EBITDA 2007 – H1 2011

Paper 53%

Forest and

Timber 13%

Pulp 35%

Energy 25%

Label 7%

Plywood 0%

Paper 19%

Cumulative

Operating profit 2007 – H1 2011

excluding special items

| © UPM

UPM's business portfolio and performance over the recession

9

0

20

40

60

80

100

120

140

160

180

200

220

Energy Pulp Label Paper Forest

and

timber

Plywood UPM

Total

0

5

10

15

20

25

30

35

40

Energy Pulp Label Paper Forest

and

timber

Plywood UPM

Total

Profitability

challenge

Average margins and returns over 2007 – H1 2011

Sales in H1 2011, as % of the economic peak year H1 2007

Operating margin % (** ROCE % (**

% %

**) excluding special items

WACC

100%

*) includes acquisition of the Uruguayan operations

(*

Myllykoski acquisition

| © UPM

MYLLYKOSKI ACQUISITION

Consolidation and restructuring are required

to create value in the Paper business

• UPM is determined to be the cost leader in the European paper

industry and the global leader in magazine papers

• A fundamental improvement in cost efficiency and value creation in

the Paper business are necessary. These are best achieved through

consolidation and restructuring

• The merits of the Myllykoski acquisition are clear. It creates UPM a

unique momentum for profitability improvement

UPM aims for a step change in its Paper business profitability

11

| © UPM

MYLLYKOSKI ACQUISITION

Myllykoski acquisition

UPM acquired Myllykoski Oyj and Rhein Papier GmbH

• Enterprise value EUR 900 million

• Publication paper production capacity of 2.8 million tonnes

• 0.8% stake in Pohjolan Voima Oy (PVO)

EU Commission approved the transaction on 13 July 2011

and it was completed on 1 August

Financing

• UPM issued 5 million new shares at the subscription price of

EUR 10.84 per share

• UPM raised bank loans of EUR 800 million

12

| © UPM

MYLLYKOSKI ACQUISITION

Summary of the financial impacts

Earnings and cash flow

• Preliminary estimate for annual cost synergies exceeds EUR 100 million

• Cash flow enhancing from the second half of 2011

• Earnings per share enhancing from 2012

Other

• UPM will book a one-off gain of approximately EUR 40 million in Q3 2011

• Preliminary estimate for restructuring costs and investments EUR 100-150m

Balance sheet

• Net debt increases by approximately EUR 800 million

• Gearing estimated to increase by 11 percentage points – UPM gearing on 30 June was 44%

13

| © UPM

14

Reported

1-6/2011

Adjustments Pro forma 1-6/2011

Sales, €m 4,779 722 5,501

EBITDA, €m 751 33 784

Operating profit, €m

‒ excl. special items, €m

487

399

-7

-7

480

392

Profit before tax, €m

‒ excl. special items, €m 511

355

-24

-24

487

331

Profit for the period 464 -17 447

MYLLYKOSKI ACQUISITION Pro forma financials – Group

| © UPM

MYLLYKOSKI ACQUISITION

Near term focus

• Customers and brand alignment

• UPM introduction to Myllykoski employees

– learning of best practices and achieving together

• Speed in integration and prompt capturing of

synergies

• Now access to detailed information.

The planning work to identify cost synergies is

proceeding towards announcement as soon as

possible, however latest by mid-September

15

| © UPM

16

Managing change

– UPM has a consistent track record

Restructuring and

efficiency

improvement

Cost competitiveness

and cash flow

Improved

financial flexibility

500

600

700

800

900

1000

2003 2004 2005 2006 2007 2008 2009 2010

tons/person

+28% in 5 years

Paper business group capacity per employee

closed

1.8mt (14%)

of capacity

| © UPM

17

Managing change

– UPM has a consistent track record

0 %

5 %

10 %

15 %

20 %

25 %

Q10

6

Q20

6

Q30

6

Q40

6

Q10

7

Q20

7

Q30

7

Q40

7

Q10

8

Q20

8

Q30

8

Q40

8

Q10

9

Q20

9

Q30

9

Q40

9

Q11

0

Q21

0

Q31

0

Q41

0

Q11

1

Q21

1

Norske Skog Stora Enso M-realHolmen Sappi SCAIP Lecta UPM

EBITDA margin compared with peers

Restructuring and

efficiency

improvement

Cost competitiveness

and cash flow

Improved

financial flexibility

| © UPM

18

Managing change

– UPM has a consistent track record

2 500

3 000

3 500

4 000

4 500

5 000

5 500

Q10

6

Q20

6

Q30

6

Q40

6

Q10

7

Q20

7

Q30

7

Q40

7

Q10

8

Q20

8

Q30

8

Q40

8

Q10

9

Q20

9

Q30

9

Q40

9

Q11

0

Q21

0

Q31

0

Q41

0

Q11

1

Q21

1

1,5

2,0

2,5

3,0

3,5

4,0

4,5

Net debt, € million Net debt / EBITDA (trailing 12 months)

Net debt

Net debt / EBITDA

Restructuring and

efficiency

improvement

Cost competitiveness

and cash flow

Improved

financial flexibility

| © UPM

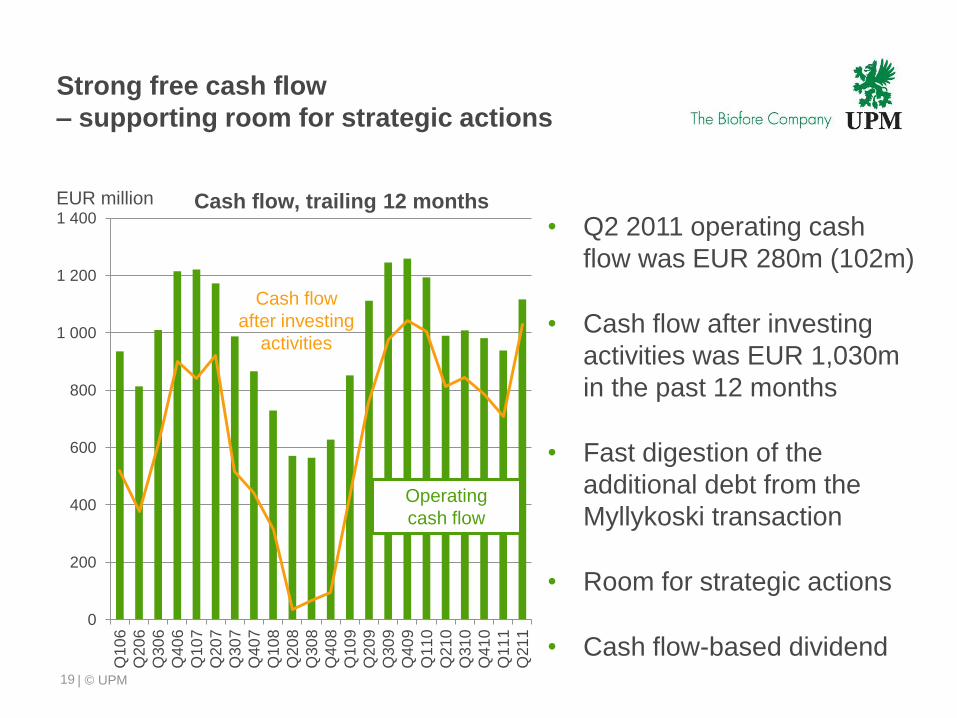

Strong free cash flow

– supporting room for strategic actions

19

0

200

400

600

800

1 000

1 200

1 400

Q10

6

Q20

6

Q30

6

Q40

6

Q10

7

Q20

7

Q30

7

Q40

7

Q10

8

Q20

8

Q30

8

Q40

8

Q10

9

Q20

9

Q30

9

Q40

9

Q11

0

Q21

0

Q31

0

Q41

0

Q11

1

Q21

1

Operating

cash flow

Cash flow

after investing

activities

EUR million Cash flow, trailing 12 months

• Q2 2011 operating cash

flow was EUR 280m (102m)

• Cash flow after investing

activities was EUR 1,030m

in the past 12 months

• Fast digestion of the

additional debt from the

Myllykoski transaction

• Room for strategic actions

• Cash flow-based dividend

| © UPM

Low operational investments – strategic capex

focused on value enhancing M&A

20

0

200

400

600

800

1 000

05 06 07 08 09 10 11e

€ million

Operational investments

350

Capital expenditure

Strategic investments

Depreciation

Uruguay

acquisition

20

Estimate

Myllykoski

acquisition

| © UPM

UPM has potential for increasing

shareholder value

21

Solid free cash flow

Competitive, valuable, cash-generative assets

Cash flow-based dividend

Improve profitability through

consolidation, cost synergies, restructuring

Case Myllykoski

Growth

Biofuels

Label, Paper in growth markets

Low emission Energy, competitive Pulp

New Biofore products

Strategic enabler

floor for share price

Short- to mid-term:

improvement

in profitability

and cash flow

Mid- to long-term:

increase valuation

multiples by growth

and reshaping

portfolio