![FINAL TERMS SKANDINAVISKA ENSKILDA BANKEN AB (publ) … · 2017. 4. 26. · 1 (49) FINAL TERMS 30 May 2017 SKANDINAVISKA ENSKILDA BANKEN AB (publ) Issue of EUR [] Autocallable EquityLinked](https://static.fdocuments.net/doc/165x107/60dec2a4433ef46fb147bc22/final-terms-skandinaviska-enskilda-banken-ab-publ-2017-4-26-1-49-final.jpg)

Skandinaviska Enskilda Banken AB (publ) - SEB Group · Skandinaviska Enskilda Banken AB (publ) ......

13

Skandinaviska Enskilda Banken AB (publ) Primary Credit Analyst: Sean Cotten, Stockholm (46) 8-440-5928; [email protected] Secondary Contact: Alexander Ekbom, Stockholm (46) 8-440-5911; [email protected] Table Of Contents Major Rating Factors Outlook Rationale Related Criteria And Research WWW.STANDARDANDPOORS.COM/RATINGSDIRECT AUGUST 29, 2014 1 1355876 | 300288388

Transcript of Skandinaviska Enskilda Banken AB (publ) - SEB Group · Skandinaviska Enskilda Banken AB (publ) ......

Skandinaviska Enskilda Banken AB(publ)

Primary Credit Analyst:

Sean Cotten, Stockholm (46) 8-440-5928; [email protected]

Secondary Contact:

Alexander Ekbom, Stockholm (46) 8-440-5911; [email protected]

Table Of Contents

Major Rating Factors

Outlook

Rationale

Related Criteria And Research

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT AUGUST 29, 2014 1

1355876 | 300288388

Skandinaviska Enskilda Banken AB (publ)

SACP a-

Anchor a-

Business

PositionAdequate 0

Capital and

EarningsAdequate 0

Risk Position Adequate 0

Funding Average

0

Liquidity Adequate

+ Support +2

GRE Support 0

GroupSupport 0

SovereignSupport +2

+AdditionalFactors 0

Issuer Credit Rating

A+/Negative/A-1

Major Rating Factors

Strengths: Weaknesses:

• Well-diversified revenue base by geography and

business area.

• Entrenched Nordic franchise in core business areas,

particularly merchant banking.

• Stable earnings from Swedish retail and merchant

banking business.

• Concentration of comparably large single-name

exposures.

• Improving but still relatively low cost efficiency

compared with peers.

Outlook

Standard & Poor's Ratings Services' outlook on Sweden-based Skandinaviska Enskilda Banken AB (publ) (SEB) is

negative, indicating that we could lower the ratings on SEB by year-end 2015 if we believe there is a greater likelihood

that senior unsecured creditors could incur losses if the bank fails. Specifically, we could lower the long-term

counterparty credit rating by up to two notches if we consider that extraordinary government support is less

predictable under the new EU legislative framework.

We could revise the outlook to stable if we consider that potential extraordinary government support for SEB's senior

unsecured creditors is unchanged in practice, despite the introduction of bail-in powers and international efforts to

increase banks' resolvability; or if we believe that other rating factors, such as a large buffer of subordinated

instruments, would provide substantial additional flexibility to absorb losses while the bank remains a going concern.

We will pay particular attention to the bank's ability to use a Swedish krona (SEK) 50 billion stability fund managed by

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT AUGUST 29, 2014 2

1355876 | 300288388

the national debt office to support senior creditors in our assessment of available government support for SEB.

Rationale

Our ratings on SEB reflect its 'a-' anchor and our assessment of its business position, capital and earnings, risk position,

and liquidity as "adequate," and funding as "average," as our criteria define these terms. The ratings also factor in the

bank's "high" systemic importance in the Kingdom of Sweden (AAA/Stable/A-1+).

Anchor: 'a-', reflecting Swedish headquarters and geographic lending portfolio

Our bank criteria use our Banking Industry Country Risk Assessment's (BICRA) economic risk and industry risk scores

to determine a bank's anchor, the starting point in assigning an issuer credit rating. Our anchor for SEB is 'a-', reflecting

the bank's regulatory base in Sweden and its combination of credit exposure to Sweden, other Nordic countries,

Germany, and the Baltics states of Estonia, Latvia, and Lithuania. The anchor is derived from a weighted economic risk

score of '2' and an industry risk score of '3'.

We view Sweden as a highly competitive and diverse economy, with high household debt levels and a history of

appreciating housing prices. Despite relatively high economic imbalances, we believe the private sector represents low

credit risk. In terms of industry risk, the Swedish banking sector benefits, in our view, from its institutional framework,

relatively conservative regulatory environment, and a high level of industry stability. A low degree of deposit funding

and a high degree of reliance on cross-border funding are partly offset by a deep domestic debt capital market and the

authorities' capacity and propensity to provide support to the domestic covered bond market.

Table 1

Skandinaviska Enskilda Banken AB (publ) Key Figures

--Year-ended Dec. 31--

(Mil. SEK) 2014* 2013 2012 2011 2010

Adjusted assets 2,294,794.0 2,152,144.0 2,157,519.0 2,074,856.0 1,898,001.0

Customer loans (gross) 1,275,514.0 1,212,658.0 1,155,987.0 1,112,873.0 1,022,375.0

Adjusted common equity 101,343.0 94,114.0 83,428.0 81,043.9 75,389.1

Operating revenues 21,504.0 41,569.0 39,248.0 37,959.0 36,893.0

Noninterest expenses 10,857.0 22,287.0 24,076.0 23,366.0 22,941.0

Core earnings 8,058.0 14,789.0 12,142.0 12,299.0 8,584.0

*Data as of June 30. SEK--Swedish krona.

Business position: Universal bank with leading Nordic merchant banking franchise

We assess SEB's business position as adequate, reflecting its broad business activities, strong position among large

Nordic corporates, and anticipated stable revenues from its merchant banking and retail operations. SEB continues to

demonstrate stable revenues due to its diverse revenue and business lines. The bank's expanded Nordic and German

merchant banking business has supported increasing revenues despite low growth and corporate investment in most

of its markets. SEB has also made use of additional scale and cost controls to improve the efficiency of the retail

operations closer to that of the bank's more efficient Nordic peers. If these trends continue, we could consider revising

upward our assessment of the bank's business position over the next two years, which could fully or partly offset any

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT AUGUST 29, 2014 3

1355876 | 300288388

Skandinaviska Enskilda Banken AB (publ)

reduction of government support.

SEB's revenue sources are diverse and it continues to generate a larger share of its revenues from fees than most

Nordic peers. The bank earns just over 40% of its pre-provision profits from merchant banking, above 30% from retail

banking, and the remaining 25%-30% spread evenly between wealth management, life insurance, and the Baltic

division. Since 2013, SEB has been reaping larger returns from a three-year effort to improve its Nordic and German

merchant banking units and should continue to benefit from these opportunities, given the resurgence of corporate

investment and increase in capital market activity.

SEB continues to demonstrate stable non-interest income despite volatile markets, reflecting its large share of

recurring fee-based income, especially from lending activities, custody, mutual funds, payments, and cards. SEB does

not operate a proprietary trading desk, so most of its trading income is dependent on customer flows, in particular

foreign exchange flows, rather than more volatile trading results.

Despite its traditional merchant banking roots, the bank has increased its focus on the domestic retail market in recent

years. As of June 2014, SEB had a domestic mortgage market share of 16%, placing it ahead of Nordea Bank AB as the

third-largest mortgage lender in Sweden. The development of household deposits has been somewhat slow given

much higher deposit rates offered by SBAB Bank AB, Landshypotek Bank AB, and other smaller players. Similarly, SEB

is making greater efforts to expand in the Swedish small and midsize enterprise (SME) market more than in the past,

which has contributed to improving the efficiency of the bank's retail operations.

SEB's management team has remained largely intact since before the recent financial crisis and has increased its

emphasis on core operations, improved the stability of its revenues and its balance sheet, prioritized cost efficiency,

and improved penetration of its existing markets. Despite significant improvements in cost efficiency and the improved

scale of its retail business, the bank remains a step behind its domestic peers in this respect (see chart 1).

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT AUGUST 29, 2014 4

1355876 | 300288388

Skandinaviska Enskilda Banken AB (publ)

Chart 1

Table 2

Skandinaviska Enskilda Banken AB (publ) Business Position

--Year-ended Dec. 31--

(%) 2014* 2013 2012 2011 2010

Loan market share in country of domicile 15.2 14.9 14.3 13.6 12.4

Deposit market share in country of domicile 15.8 15.4 15.9 16.0 15.8

Total revenues from business line (currency in millions) 21,504.0 41,569.0 39,248.0 37,959.0 36,893.0

Commercial banking/total revenues from business line 42.8 40.2 40.4 46.2 46.4

Retail banking/total revenues from business line 38.0 37.7 36.9 33.3 30.9

Commercial & retail banking/total revenues from business line 80.8 77.9 77.2 79.4 77.4

Insurance activities/total revenues from business line 11.0 11.0 11.8 11.8 12.3

Asset management/total revenues from business line 10.6 10.2 10.3 11.7 11.9

Other revenues/total revenues from business line (2.5) 0.9 0.7 (2.9) (1.6)

Return on equity 13.1 12.7 10.7 10.7 6.8

Capital and earnings: Adequate capital levels supported by stable earnings

We view SEB's capital and earnings as adequate. We expect SEB's capital generation of 20-30 basis points (bps) per

annum remain somewhat slower than that of its large Nordic peers, leading to an expected risk-adjusted capital (RAC)

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT AUGUST 29, 2014 5

1355876 | 300288388

Skandinaviska Enskilda Banken AB (publ)

ratio approaching 9% over the next 18-24 months. We do not include any hybrid capital in our total adjusted capital or

capital projections for SEB. We expect the Swedish regulator to finalize its requirements for additional Tier 1

instruments and related buffers in 2014, after which we expect SEB to issue some hybrid capital, which in turn could

improve its RAC ratio towards 10%.

At year-end 2013, SEB's RAC ratio was 8.3% excluding diversification and concentration adjustments, a strong

improvement over 7.8% at end-2012, particularly considering the bank's dividend of 59% of net profit. We expect the

bank to continue to pay out at least 50% of profits, which should provide room for risk-weighted asset growth

approaching 4% per annum while improving existing capital ratios by 20-30 bps per year.

We expect the bank to continue to focus on cost reduction and to improve its cost-to-income ratio to below 50%, a

significant improvement from our previous expectations and a reduction from over 60% in 2012. This development

should be supported by upward pressure on domestic mortgage margins following the Swedish regulator's expected

implementation of a 25% risk weight floor. SEB's three-year average earnings buffer, our measure of the capacity of a

bank's earnings to cover normalized losses, is expected to improve to 100-110 bps. This reflects SEB's ability to

generate capital even if losses approach our modeled, risk-based expected loss level of 35 bps, given the bank's

geographic and business line credit portfolio.

Table 3

Skandinaviska Enskilda Banken AB (publ) Capital And Earnings

--Year-ended Dec. 31--

(%) 2014* 2013 2012 2011 2010

Tier 1 capital ratio 17.9 17.1 17.5 15.9 14.2

S&P RAC ratio before diversification N.M. 8.3 7.7 7.7 8.0

S&P RAC ratio after diversification N.M. 8.9 8.3 8.3 8.6

Adjusted common equity/total adjusted capital 95.8 95.5 93.1 92.4 85.2

Double leverage 63.5 62.7 69.1 75.3 84.4

Net interest income/operating revenues 45.4 45.3 44.9 44.5 43.4

Fee income/operating revenues 36.9 35.3 34.7 37.3 38.4

Market-sensitive income/operating revenues 8.9 10.8 11.6 9.6 9.3

Noninterest expenses/operating revenues 50.5 53.6 61.3 61.6 62.2

Preprovision operating income/average assets 0.8 0.8 0.6 0.6 0.6

Core earnings/average managed assets 0.6 0.6 0.5 0.5 0.4

*Data as of June 30.

Table 4

Skandinaviska Enskilda Banken AB (publ) Risk-Adjusted Capital Framework Data

(Mil. SEK) Exposure* Basel II RWA

Average Basel II

RW (%)

Standard & Poor's

RWA

Average Standard &

Poor's RW (%)

Credit risk

Government and central

banks

358,411 4,365 1 16,069 4

Institutions 138,188 24,271 18 31,240 23

Corporate 807,509 298,321 37 600,123 74

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT AUGUST 29, 2014 6

1355876 | 300288388

Skandinaviska Enskilda Banken AB (publ)

Table 4

Skandinaviska Enskilda Banken AB (publ) Risk-Adjusted Capital Framework Data (cont.)

Retail 565,710 122,638 22 192,738 34

Of which mortgage 486,333 86,928 18 127,715 26

Securitization 13,675 4,827 35 23,604 173

Other assets 11,008 8,708 79 15,949 145

Total credit risk 1,894,500 463,129 24 879,723 46

Market risk

Equity in the banking book¶ 5,625 5,452 100 43,094 766

Trading book market risk -- 56,578 -- 84,775 --

Total market risk -- 62,030 -- 127,869 --

Insurance risk

Total insurance risk -- -- -- 74,738 --

Operational risk

Total operational risk -- 39,542 -- 105,840 --

(Mil. SEK) Basel II RWA

Standard & Poor's

RWA

% of Standard & Poor's

RWA

Diversification adjustments

RWA before diversification 918,181 1,188,169 100

Total adjustments to

RWA

-- (84,411) (7)

RWA after diversification 918,181 1,103,758 93

(Mil. SEK) Tier 1 capital Tier 1 ratio (%)

Total adjusted

capital

Standard & Poor's RAC

ratio (%)

Capital ratio

Capital ratio before

adjustments

108,119 11.8 98,562 8.3

Capital ratio after

adjustments§

108,119 11.8 98,562 8.9

*Exposure at default. ¤Securitization exposure includes securitization tranches deducted from capital in the regulatory framework. ¶Exposure

and Standard & Poor's risk-weighted assets for equity in the banking book include minority equity holdings in financial institutions. §Adjustments

to Tier 1 ratio are additional regulatory requirements (e.g. transitional floor or Pillar 2 add-ons). RWA--Risk-weighted assets. RW--Risk weight.

RAC--Risk-adjusted capital. SEK--Sweden krona. Sources: Company data as of Dec. 31, 2013, Standard & Poor's.

Risk position: Increasing focus on core markets in the Nordic countries and Germany

In our view, SEB's risk position is adequate when compared with that of banks with similar weighted economic risk.

We believe that economic imbalances and credit risk in Sweden are likely to remain stable over the next two years,

which supports our expectations of relatively low credit losses in SEB's loan book.

We expect that SEB's overall asset quality and loss experience will be generally in line with that of its peers. The bank's

credit profile has become increasingly focused on its core markets in the Nordic countries, in particular the household

and residential real estate sectors, and German corporates. We consider SEB's corporate and retail exposures to be

representative of its primary markets, given its high market shares, and we are expecting stability in credit losses in

Sweden at very low levels. We project loan loss provisions of about 10 bps in our base-case scenario, a level consistent

with SEB's performance in 2012 and 2013. In our view, future credit losses will be more balanced between Nordic and

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT AUGUST 29, 2014 7

1355876 | 300288388

Skandinaviska Enskilda Banken AB (publ)

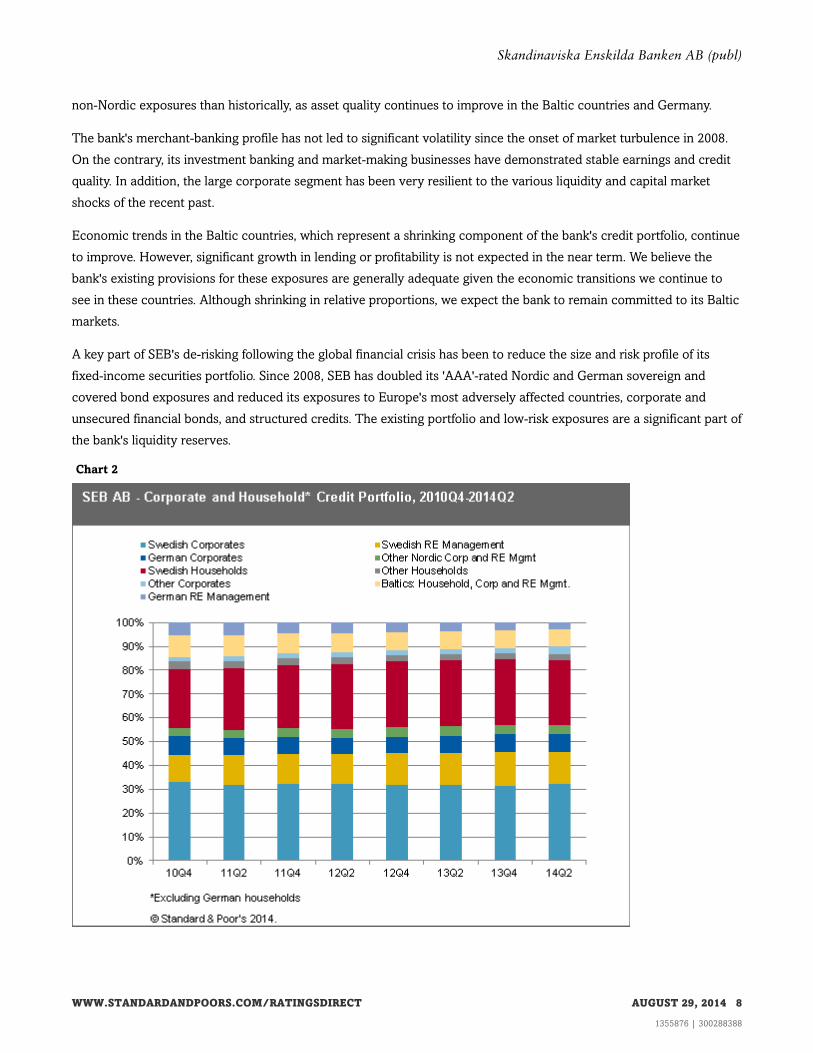

non-Nordic exposures than historically, as asset quality continues to improve in the Baltic countries and Germany.

The bank's merchant-banking profile has not led to significant volatility since the onset of market turbulence in 2008.

On the contrary, its investment banking and market-making businesses have demonstrated stable earnings and credit

quality. In addition, the large corporate segment has been very resilient to the various liquidity and capital market

shocks of the recent past.

Economic trends in the Baltic countries, which represent a shrinking component of the bank's credit portfolio, continue

to improve. However, significant growth in lending or profitability is not expected in the near term. We believe the

bank's existing provisions for these exposures are generally adequate given the economic transitions we continue to

see in these countries. Although shrinking in relative proportions, we expect the bank to remain committed to its Baltic

markets.

A key part of SEB's de-risking following the global financial crisis has been to reduce the size and risk profile of its

fixed-income securities portfolio. Since 2008, SEB has doubled its 'AAA'-rated Nordic and German sovereign and

covered bond exposures and reduced its exposures to Europe's most adversely affected countries, corporate and

unsecured financial bonds, and structured credits. The existing portfolio and low-risk exposures are a significant part of

the bank's liquidity reserves.

Chart 2

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT AUGUST 29, 2014 8

1355876 | 300288388

Skandinaviska Enskilda Banken AB (publ)

Table 5

Skandinaviska Enskilda Banken AB (publ) Risk Position

--Year-ended Dec. 31--

(%) 2014* 2013 2012 2011 2010

Growth in customer loans 10.4 4.9 3.9 8.9 (10.7)

Total diversification adjustment / S&P RWA before diversification N.M. (7.1) (6.8) (8.3) (6.6)

Total managed assets/adjusted common equity (x) 26.2 26.4 29.4 29.2 28.9

New loan loss provisions/average customer loans 0.1 0.1 0.1 (0.1) 0.2

Net charge-offs/average customer loans 0.1 0.3 0.2 0.2 0.2

Gross nonperforming assets/customer loans + other real estate owned 0.7 0.8 1.2 1.6 2.4

Loan loss reserves/gross nonperforming assets 73.8 69.1 64.1 62.2 63.9

*Data as of June 30. N.M.--Not meaningful.

Funding and liquidity: Less wholesale funding and more corporate deposits than peers

We consider SEB's funding to be average and its liquidity adequate, given the strong structural support for the high

share of wholesale funding in the Swedish banking system. However, we believe that the bank has room to extend the

duration of its stable funding sources to better support its illiquid assets.

As we expect SEB to further enhance its funding profile, we view funding as neutral for the ratings. SEB's stable

funding ratio of 90% at the end of 2013, compared with a three-year average of 92%, demonstrates some weakness in

the bank's funding structure, given our expectations that banks should fund their long-term assets with appropriate

forms of stable long-term funding. This is especially important considering SEB's large share of corporate deposit

funding, accounting for 63% of customer deposits. Despite an observable history of stable relationships and corporate

deposits, we see room for further improvement in the bank's use of stable funding sources to support its illiquid assets

(according to our definitions) and anticipate medium-term improvements as the bank prepares for eventual

compliance with the regulatory net stable funding ratio.

In our view, SEB has a somewhat more liquid balance sheet than its domestic peers and has shown improvements in

managing short-term and longer term liquidity. By our measures, SEB's one-year liquidity ratio, comparing broad liquid

assets with short-term wholesale funding, was 92% at the end of 2013 and below the three-year average of 98%.

Despite this decline in our one-year measure, we note that SEB has subtly increased the durations of its largely U.S.

dollar/euro short-term wholesale funding positions, improving its ability to manage short-term liquidity below one

year.

In our view, SEB is exposed to some refinancing risk. However, we consider that the dependence of the bank and its

domestic peers on foreign and wholesale funding partly stems from structural factors, including tax incentives and

repatriation of capital associated with the large proportion of Swedish investments abroad. Consequently, we believe

the Swedish government would be willing and able to provide ongoing liquidity support to banks and support the

functioning of the covered bond market if a new funding crisis were to emerge. In our view, such support is unlikely to

be withdrawn in full despite restrictions on government support outlined in the European Bank Resolution and

Recovery Directive.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT AUGUST 29, 2014 9

1355876 | 300288388

Skandinaviska Enskilda Banken AB (publ)

Chart 3

Table 6

Skandinaviska Enskilda Banken AB (publ) Funding And Liquidity

--Year-ended Dec. 31--

(%) 2014* 2013 2012 2011 2010

Core deposits/funding base 44.2 44.7 46.5 47.1 45.0

Customer loans (net)/customer deposits 146.1 147.0 137.9 133.5 145.0

Long term funding ratio 66.7 67.8 68.6 68.1 64.0

Stable funding ratio 89.6 90.2 93.2 92.5 77.7

Short-term wholesale funding/funding base 35.2 34.1 33.1 33.7 38.2

Broad liquid assets/short-term wholesale funding (x) 0.9 0.9 1.0 1.0 0.7

Net broad liquid assets/short-term customer deposits (9.4) (6.4) 3.9 (2.8) (23.9)

Short-term wholesale funding/total wholesale funding 62.8 61.5 61.4 63.3 68.4

Narrow liquid assets/3-month wholesale funding (x) 1.1 1.3 1.5 1.1 0.9

*Data as of June 30.

External support: Two notches of government support

The long-term rating on SEB is two notches higher than the bank's stand-alone credit profile. This reflects our

assessment under our criteria that SEB has "high" systemic importance in Sweden and that the Swedish government is

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT AUGUST 29, 2014 10

1355876 | 300288388

Skandinaviska Enskilda Banken AB (publ)

"supportive" of the country's banking sector.

Within Europe, we note a move toward avoiding bank bail-outs (government support) by using bail-ins (burden sharing

with investors, potentially including senior unsecured obligations). It is our view that there is a chance that we could

remove the explicit notches of government support by the end of 2015, a factor that drives our negative outlook.

Related ratings: SEB AG

We define SEB's German subsidiary SEB AG as highly strategically important given its primary role within the bank's

merchant banking division. The rating on SEB AG is 'A/A-1', one notch below that on the parent, in line with our

group rating criteria.

Additional rating factors: None

No additional factors affect this rating.

Related Criteria And Research

Related criteria

• Group Rating Methodology, May 7, 2013

• Banks: Rating Methodology And Assumptions, Nov. 9, 2011

• Banking Industry Country Risk Assessment Methodology And Assumptions, Nov. 9, 2011

• Bank Hybrid Capital Methodology And Assumptions, Nov. 1, 2011

• Bank Capital Methodology And Assumptions, Dec. 6, 2010

Related research

• Ratings On Sweden-Based Bank SEB Affirmed At 'A+/A-1' Following Government Support Review; Outlook

Remains Negative, April 29, 2014

• Various Rating Actions Taken On Nine Swedish Banks On Stabilizing Economic Risks And Government Support

Review, April 29, 2014

• Standard & Poor's Takes Various Rating Actions On European Banks Following Government Support Review, April

29, 2014

• Various Rating Actions Taken On Five Swedish Banks After Review Of Funding And Liquidity, And Capital Trends,

July 19, 2013

• Swedbank Outlook Revised To Stable On Improving Capitalization; 'A+/A-1' Ratings Affirmed, July 19, 2013

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT AUGUST 29, 2014 11

1355876 | 300288388

Skandinaviska Enskilda Banken AB (publ)

Anchor Matrix

Industry

Risk

Economic Risk

1 2 3 4 5 6 7 8 9 10

1 a a a- bbb+ bbb+ bbb - - - -

2 a a- a- bbb+ bbb bbb bbb- - - -

3 a- a- bbb+ bbb+ bbb bbb- bbb- bb+ - -

4 bbb+ bbb+ bbb+ bbb bbb bbb- bb+ bb bb -

5 bbb+ bbb bbb bbb bbb- bbb- bb+ bb bb- b+

6 bbb bbb bbb- bbb- bbb- bb+ bb bb bb- b+

7 - bbb- bbb- bb+ bb+ bb bb bb- b+ b+

8 - - bb+ bb bb bb bb- bb- b+ b

9 - - - bb bb- bb- b+ b+ b+ b

10 - - - - b+ b+ b+ b b b-

Ratings Detail (As Of August 29, 2014)

Skandinaviska Enskilda Banken AB (publ)

Counterparty Credit Rating A+/Negative/A-1

Commercial Paper

Foreign Currency A-1

Junior Subordinated BBB-

Senior Unsecured A+

Short-Term Debt A-1

Subordinated BBB+

Counterparty Credit Ratings History

20-Nov-2012 Foreign Currency A+/Negative/A-1

01-Dec-2011 A+/Stable/A-1

23-Feb-2010 A/Stable/A-1

20-Nov-2012 Local Currency A+/Negative/A-1

01-Dec-2011 A+/Stable/A-1

23-Feb-2010 A/Stable/A-1

Sovereign Rating

Sweden (Kingdom of) (Unsolicited Ratings) AAA/Stable/A-1+

Related Entities

SEB AG

Issuer Credit Rating A/Negative/A-1

*Unless otherwise noted, all ratings in this report are global scale ratings. Standard & Poor's credit ratings on the global scale are comparable

across countries. Standard & Poor's credit ratings on a national scale are relative to obligors or obligations within that specific country.

Additional Contact:

Financial Institutions Ratings Europe; [email protected]

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT AUGUST 29, 2014 12

1355876 | 300288388

Skandinaviska Enskilda Banken AB (publ)

S&P may receive compensation for its ratings and certain analyses, normally from issuers or underwriters of securities or from obligors. S&P

reserves the right to disseminate its opinions and analyses. S&P's public ratings and analyses are made available on its Web sites,

www.standardandpoors.com (free of charge), and www.ratingsdirect.com and www.globalcreditportal.com (subscription) and www.spcapitaliq.com

(subscription) and may be distributed through other means, including via S&P publications and third-party redistributors. Additional information

about our ratings fees is available at www.standardandpoors.com/usratingsfees.

S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respective

activities. As a result, certain business units of S&P may have information that is not available to other S&P business units. S&P has established

policies and procedures to maintain the confidentiality of certain nonpublic information received in connection with each analytical process.

To the extent that regulatory authorities allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certain

regulatory purposes, S&P reserves the right to assign, withdraw, or suspend such acknowledgement at any time and in its sole discretion. S&P

Parties disclaim any duty whatsoever arising out of the assignment, withdrawal, or suspension of an acknowledgment as well as any liability for any

damage alleged to have been suffered on account thereof.

Credit-related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed and

not statements of fact. S&P's opinions, analyses, and rating acknowledgment decisions (described below) are not recommendations to purchase,

hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security. S&P assumes no obligation to

update the Content following publication in any form or format. The Content should not be relied on and is not a substitute for the skill, judgment

and experience of the user, its management, employees, advisors and/or clients when making investment and other business decisions. S&P does

not act as a fiduciary or an investment advisor except where registered as such. While S&P has obtained information from sources it believes to be

reliable, S&P does not perform an audit and undertakes no duty of due diligence or independent verification of any information it receives.

No content (including ratings, credit-related analyses and data, valuations, model, software or other application or output therefrom) or any part

thereof (Content) may be modified, reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval

system, without the prior written permission of Standard & Poor's Financial Services LLC or its affiliates (collectively, S&P). The Content shall not be

used for any unlawful or unauthorized purposes. S&P and any third-party providers, as well as their directors, officers, shareholders, employees or

agents (collectively S&P Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Parties are not

responsible for any errors or omissions (negligent or otherwise), regardless of the cause, for the results obtained from the use of the Content, or for

the security or maintenance of any data input by the user. The Content is provided on an "as is" basis. S&P PARTIES DISCLAIM ANY AND ALL

EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR

A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT'S FUNCTIONING

WILL BE UNINTERRUPTED, OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no

event shall S&P Parties be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential

damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs or losses caused by

negligence) in connection with any use of the Content even if advised of the possibility of such damages.

Copyright © 2014 Standard & Poor's Financial Services LLC, a part of McGraw Hill Financial. All rights reserved.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT AUGUST 29, 2014 13

1355876 | 300288388

![FINAL TERMS SKANDINAVISKA ENSKILDA BANKEN AB (publ) … · SKANDINAVISKA ENSKILDA BANKEN AB (publ) Issue of EUR [xx] Equity Linked Securities under the Structured Note and Certificate](https://static.fdocuments.net/doc/165x107/60612ec2a00200288c22a5bf/final-terms-skandinaviska-enskilda-banken-ab-publ-skandinaviska-enskilda-banken.jpg)