Savings Rates and Tax Structure Nancy J. Burnett, UW – Oshkosh Lee Van Scyoc, UW – Oshkosh.

32

Savings Rates and Tax Structure Nancy J. Burnett, UW – Oshkosh Lee Van Scyoc, UW – Oshkosh

-

date post

21-Dec-2015 -

Category

Documents

-

view

221 -

download

2

Transcript of Savings Rates and Tax Structure Nancy J. Burnett, UW – Oshkosh Lee Van Scyoc, UW – Oshkosh.

Savings Rates and Tax Structure

Nancy J. Burnett, UW – OshkoshLee Van Scyoc, UW – Oshkosh

US Net National Savings

Savings Rates and Tax Structure

• Literature: From the classics of Friedman and Modigliani to “9-9-9”– Agreement on importance of personal savings– Theoretical analysis of consumption v. income tax– Empirical evidence mixed• International studies• Time series studies• Suffer from cross cultural and/or changing environment

State by State Analysis

• Eliminate the environment differences• Eliminate (mostly) the cultural differences• State residents all have access to the same R

and pay the same Federal Tax• State have different tax regimes– Sources of state income

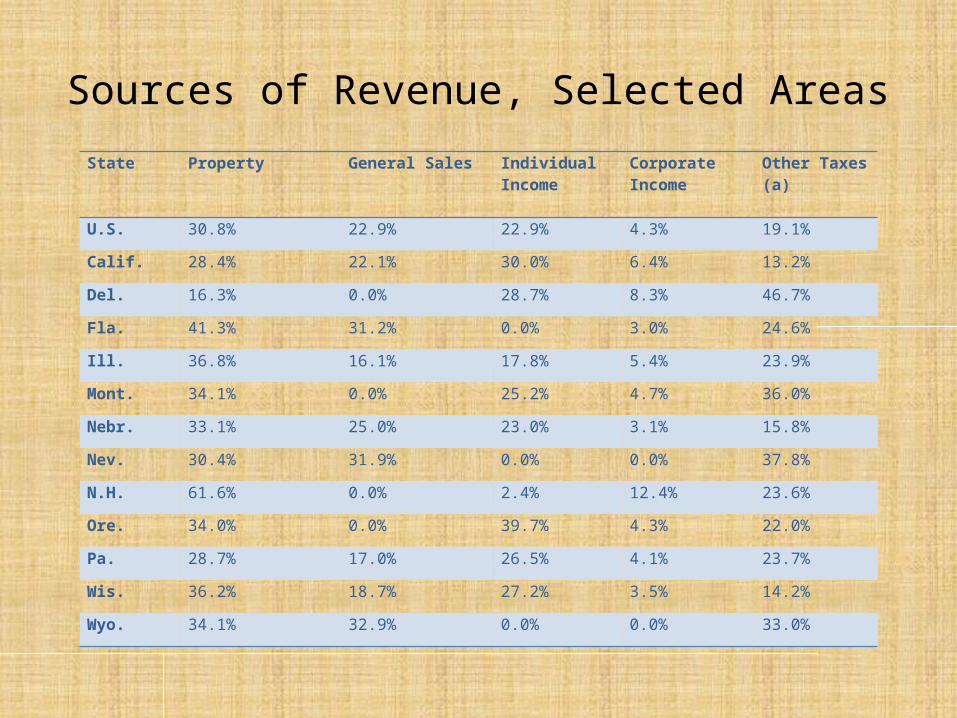

State Property General Sales Individual Income

Corporate Income

Other Taxes (a)

U.S. 30.8% 22.9% 22.9% 4.3% 19.1%

Calif. 28.4% 22.1% 30.0% 6.4% 13.2%

Del. 16.3% 0.0% 28.7% 8.3% 46.7%

Fla. 41.3% 31.2% 0.0% 3.0% 24.6%

Ill. 36.8% 16.1% 17.8% 5.4% 23.9%

Mont. 34.1% 0.0% 25.2% 4.7% 36.0%

Nebr. 33.1% 25.0% 23.0% 3.1% 15.8%

Nev. 30.4% 31.9% 0.0% 0.0% 37.8%

N.H. 61.6% 0.0% 2.4% 12.4% 23.6%

Ore. 34.0% 0.0% 39.7% 4.3% 22.0%

Pa. 28.7% 17.0% 26.5% 4.1% 23.7%

Wis. 36.2% 18.7% 27.2% 3.5% 14.2%

Wyo. 34.1% 32.9% 0.0% 0.0% 33.0%

Sources of Revenue, Selected Areas

9876543210

9

8

7

6

5

4

3

2

1

0

salesT

Avg T

ax

Scatterplot of Avg Tax vs salesT

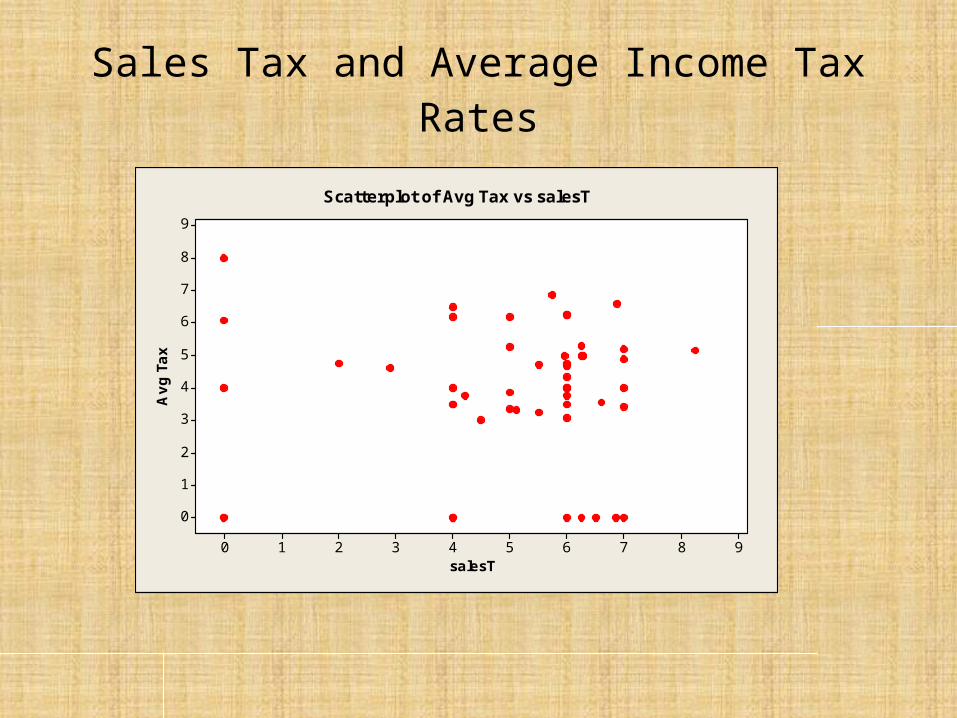

Sales Tax and Average Income Tax Rates

The Zero States… 0% Sales Tax Rate 0% State Income Tax Rate

AK – Alaska AK - Alaska

DE - Delaware NH* - New Hampshire

MT - Montana SD – South Dakota

NH – New Hampshire WY - Wyoming

OR - Oregon FL - Florida

TX – Texas

WA – Washington

NY – New York

TN - Tennessee

Interesting Period?

• Current political climate (“9-9-9”, etc) makes this topic important now

• Looking at data from period since the ‘credit crunch’ – 2009.

• Will the economic miasma of the period overwhelm results?

Data

• Changes in Personal Income by State– BEA

• Average Income Tax Rate– Federation of Tax Administrators

• State Sales Tax Rate– Federation of Tax Administrators

• Savings Rate?– Interest Income by state: IRS.gov – Adult Population by state: US Stat Abstract

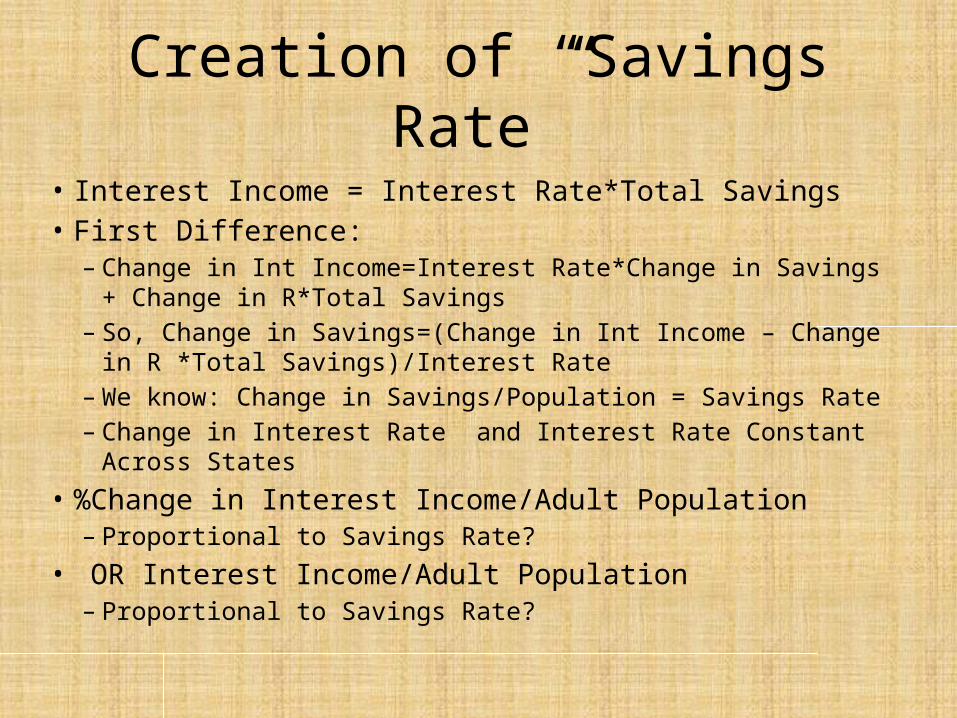

Creation of “Savings Rate”

• Interest Income = Interest Rate*Total Savings• First Difference:

– Change in Int Income=Interest Rate*Change in Savings + Change in R*Total Savings

– So, Change in Savings=(Change in Int Income – Change in R *Total Savings)/Interest Rate

– We know: Change in Savings/Population = Savings Rate– Change in Interest Rate and Interest Rate Constant Across States

• %Change in Interest Income/Adult Population– Proportional to Savings Rate?

• OR Interest Income/Adult Population– Proportional to Savings Rate?

Data Summary, 2009

Variable Mean StDev Minimum Maximum

AvgTax 3.863 2.106 0.000 8.000

SalesTax 5.031 2.044 0.000 8.250

%ChangeSave/Pop -.001682 .003660 -.02391 .006686

IncomeChange -2.124 1.544 -5.900 1.800

InterestIncome/Pop643.7 174.8 384.9 1186.1

Income/Pop32128 5903 23080 49325

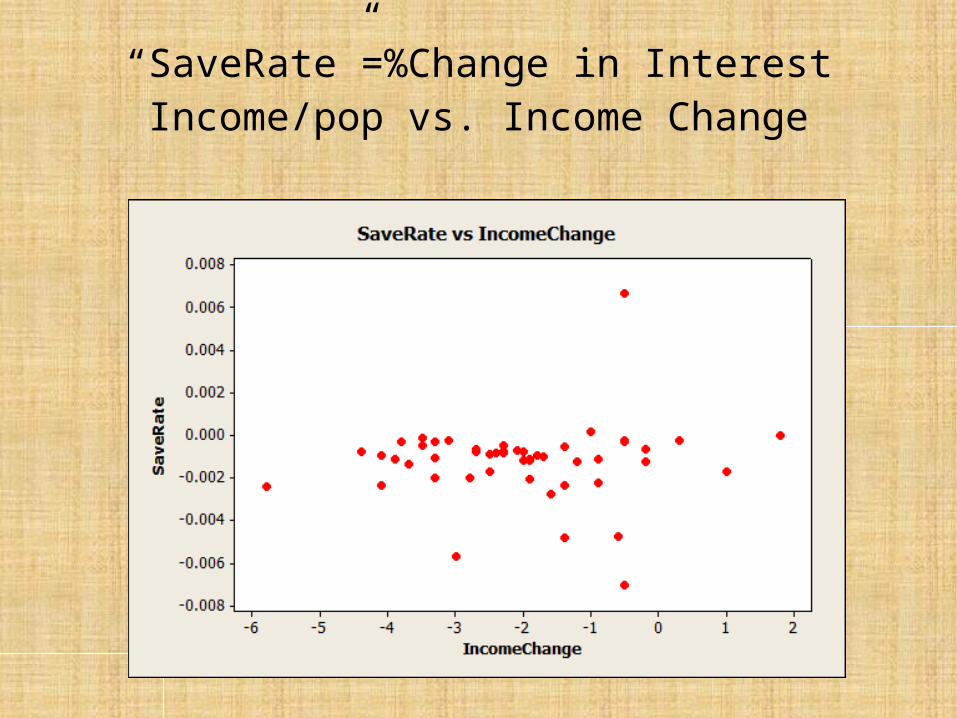

“SaveRate”=%Change in Interest Income/pop vs. Income Change

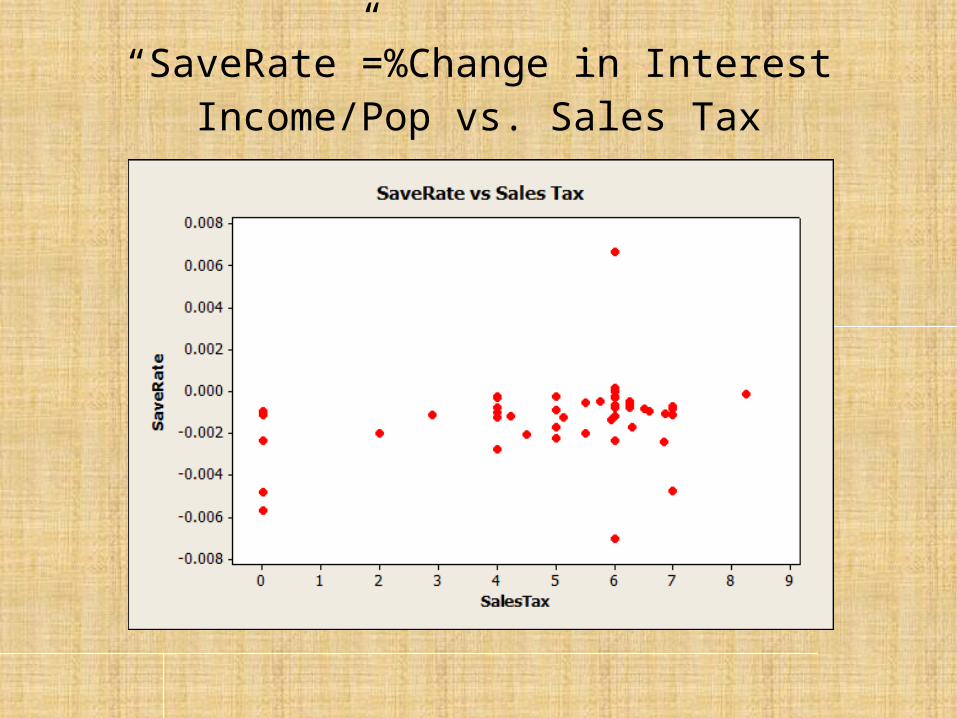

“SaveRate”=%Change in Interest Income/Pop vs. Sales Tax

“SaveRate”=% Change in Interest Income/Pop vs. Income Tax Rate

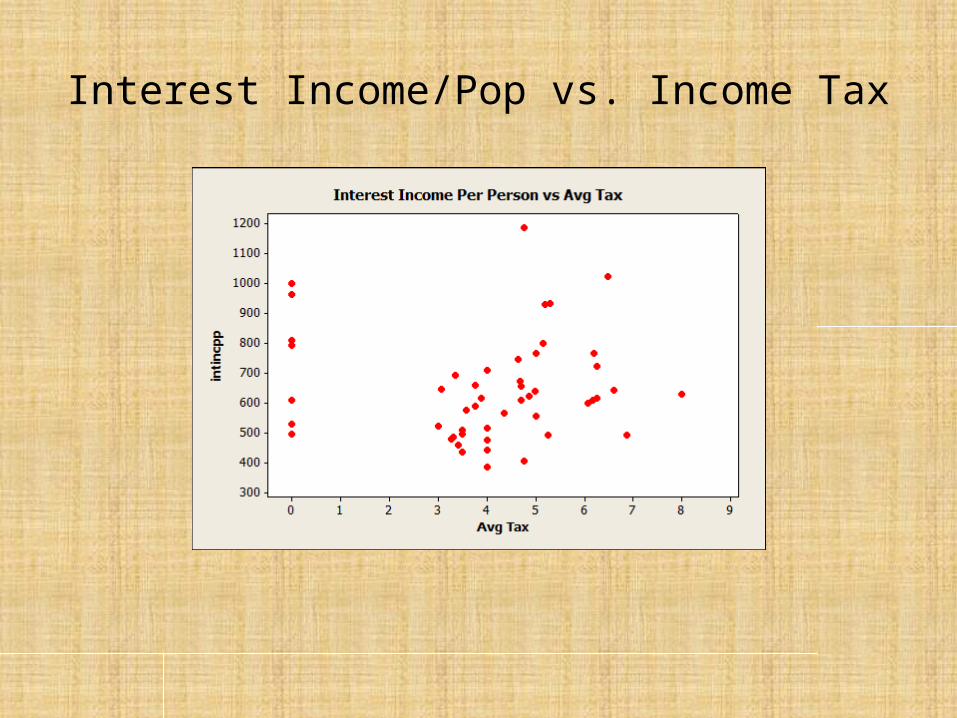

Interest Income/Pop vs. Income Tax

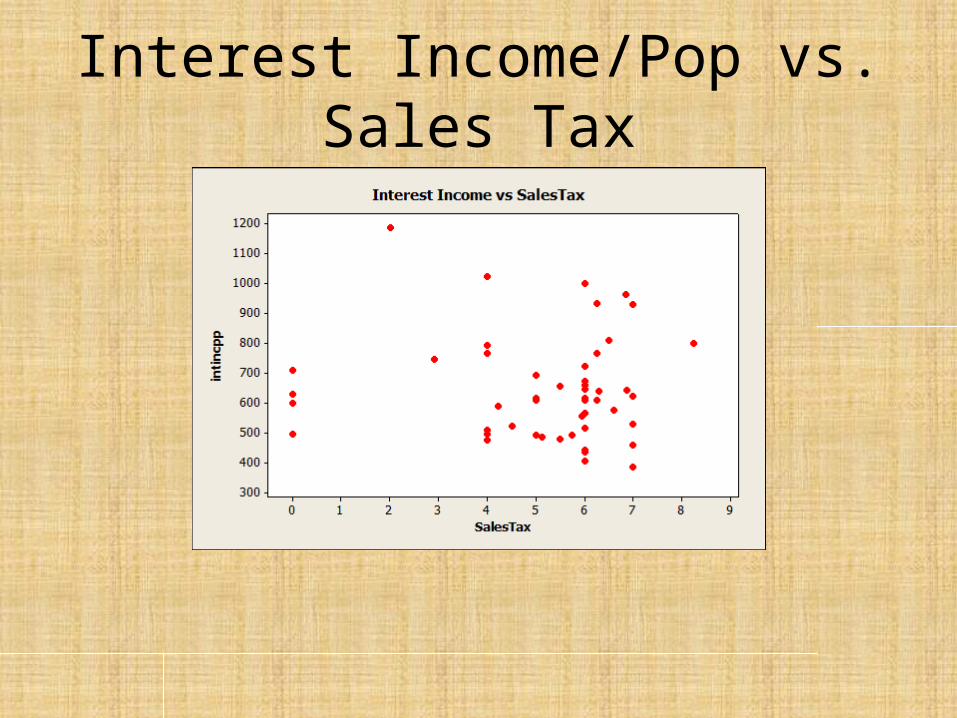

Interest Income/Pop vs. Sales Tax

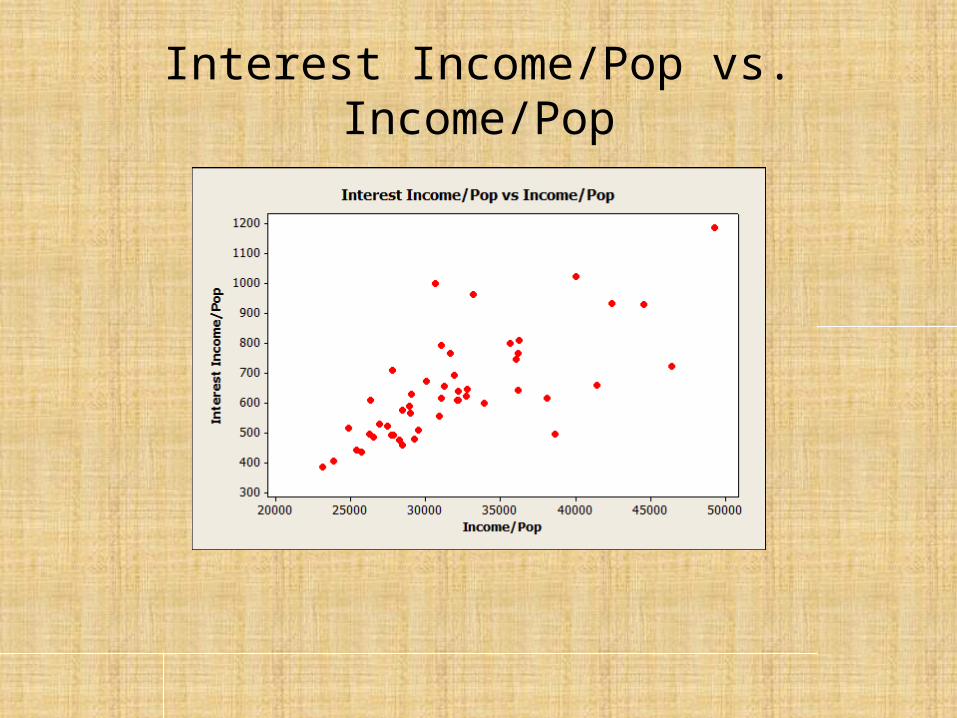

Interest Income/Pop vs. Income/Pop

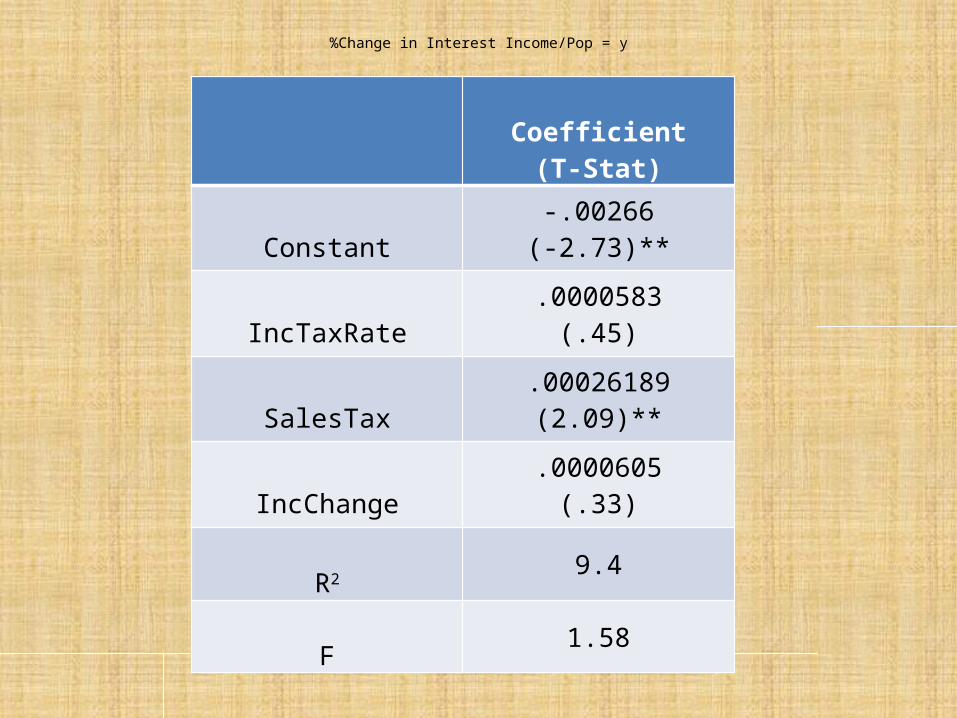

%Change in Interest Income/Pop = y

Coefficient(T-Stat)

Constant-.00266(-2.73)**

IncTaxRate.0000583(.45)

SalesTax.00026189(2.09)**

IncChange.0000605(.33)

R2 9.4

F1.58

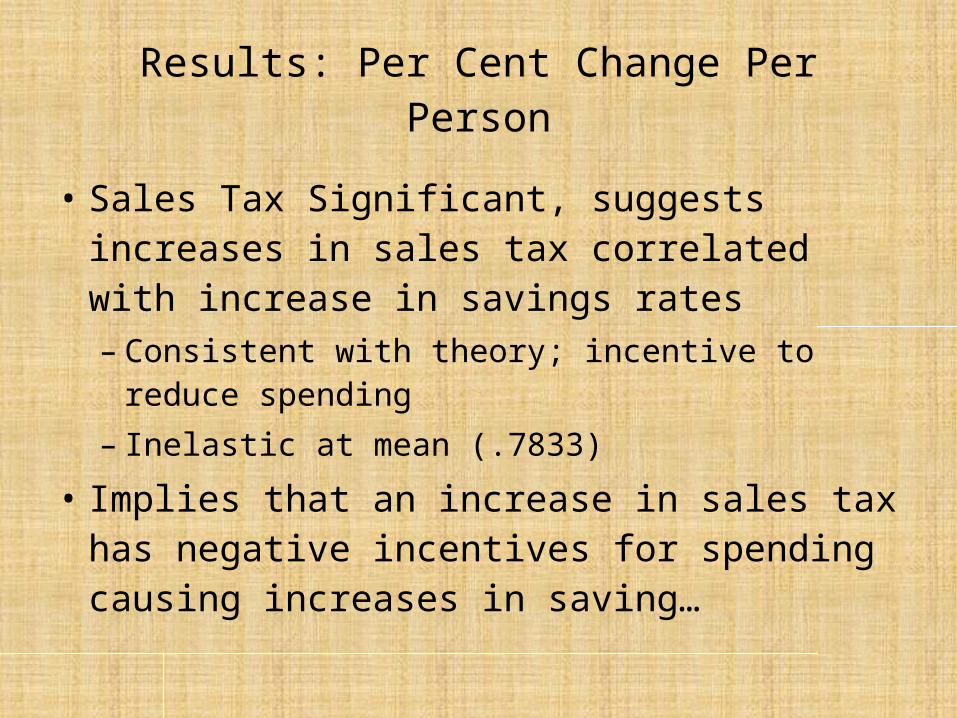

Results: Per Cent Change Per Person

• Sales Tax Significant, suggests increases in sales tax correlated with increase in savings rates– Consistent with theory; incentive to reduce

spending– Inelastic at mean (.7833)

• Implies that an increase in sales tax has negative incentives for spending causing increases in saving…

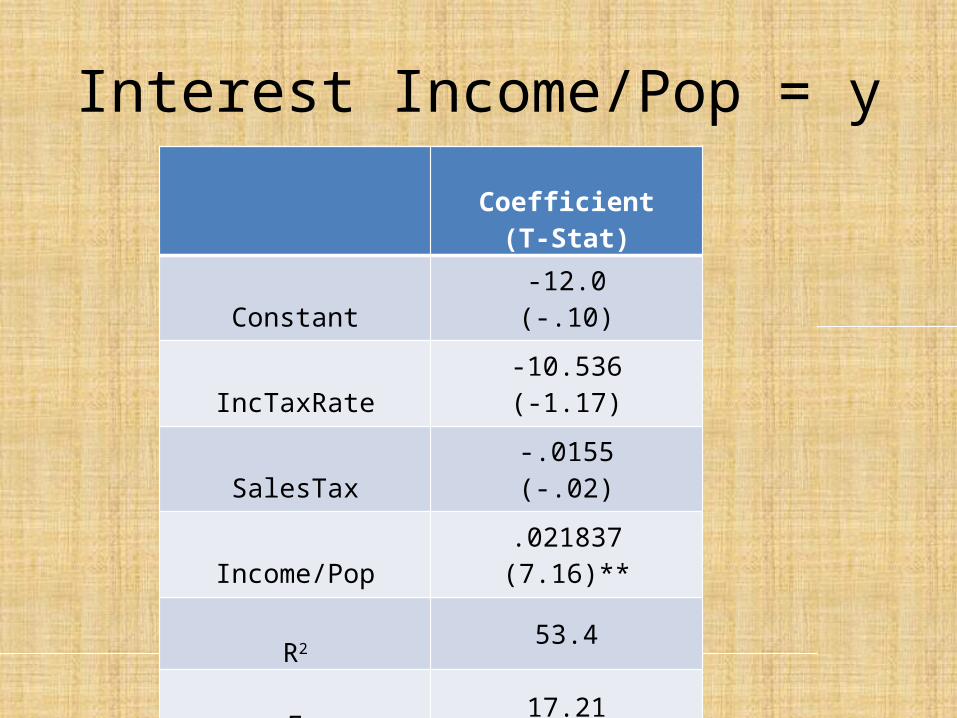

Interest Income/Pop = yCoefficient

(T-Stat)

Constant-12.0(-.10)

IncTaxRate-10.536(-1.17)

SalesTax-.0155(-.02)

Income/Pop.021837(7.16)**

R2 53.4

F17.21

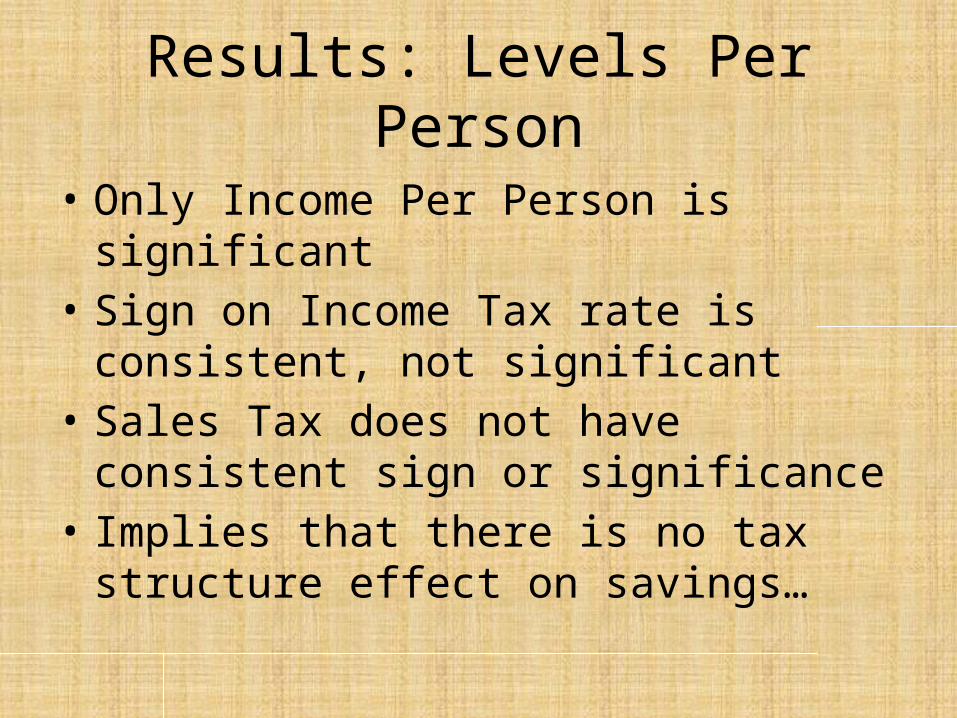

Results: Levels Per Person

• Only Income Per Person is significant• Sign on Income Tax rate is consistent, not

significant• Sales Tax does not have consistent sign or

significance• Implies that there is no tax structure effect on

savings…

Now What?

• 2009 was unusual year – economic miasma• Levels or Percentage Changes?

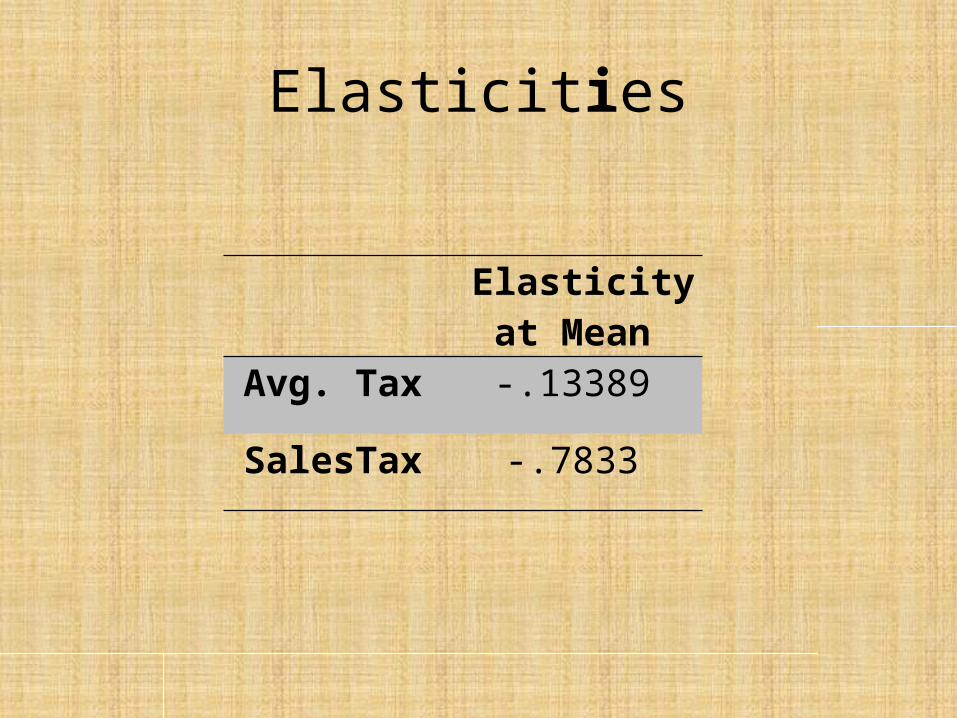

Elasticities

Elasticity at Mean

Avg. Tax -.13389

SalesTax -.7833