RMB: Going Global - HSBCnet | HSBC · PDF fileRMB: Going Global Prepared by: RMB Business...

46

RMB: Going Global Prepared by: RMB Business Development, Asia-Pacific, HSBC Global Markets Date: May 2012

Transcript of RMB: Going Global - HSBCnet | HSBC · PDF fileRMB: Going Global Prepared by: RMB Business...

RMB: Going Global

Prepared by: RMB Business Development, Asia-Pacific, HSBC Global Markets

Date: May 2012

2

Agenda

RMB Internationalisation

Page 3

RMB Trade Settlement Page 7

Development of Offshore RMB

Page 11

Offshore RMB Markets Page 17

RMB FX and Money Market

Page 19

Offshore RMB Bond Market (Dim Sum bonds)

Page 26

RMB Interest Rate Derivatives Market

Page 33

Offshore RMB Initial Public Offering (IPO)

Page 36

HSBC RMB Capabilities and Credentials

Page 38

RMB Internationalisation

4

China and RMB – Rise of the redback

China has 1.3 billion (bn) people1, the 2nd

largest economy2

and is the largest exporter

at $1.899 trillion (tn)3

RMB could become the 3rd highest turnover

currency in the world if RMB were fully

convertible 0

500

1000

1500

2000

2500

2009 2010 2011

EU China US Japan UK

Source: HSBC estimate, BIS(1)

Central Intelligence Agency World

Factbook(2)

CEIC, HSBC(3)

Central Intelligence Agency World Factbook; 2011 EU exports The World Trade Organisation(4)

Ministry of Commerce (MOFCOM) –

http://english.mofcom.gov.cn/aarticle/statistic/BriefStatistics/201201/20120107927531.html(5)

Estimate of RMB daily average FX turnover is based on a turnover-to-trade ratio of 0.3, which is lower than 0.32 for EUR, 0.4 for YEN and 0.46 for GBP. The rise in use of RMB will offset the use of USD, EUR, YEN, and GBP at a share of 40%, 30%, 20% and 10%

Nominal GDP (USDbn)2 Exports (USDbn)3

Daily Average Turnover (USDbn)3 Daily Average Turnover (USDbn)3

0

2,0004,000

6,000

8,000

10,00012,000

14,000

16,000

1995 1997 1999 2001 2003 2005 2007 2009 2011

US China Japan EUA 17

$

USD

EUR

RMB GBPJPY

¥

€

¥

0

500

1,000

1,500

2,000

2,500

3,000

3,500

£

2010 Bank for International Settlement (BIS) Data

$

USD

EUR

RMBGBPJPY

¥€

¥0

500

1,000

1,500

2,000

2,500

3,000

3,500

£

2010 BIS Data (if RMB fully convertible)

5

RMB Internationalisation: A three-stage process

Source: HSBC* Details of some measures to be announced(1)

PBoC

–

http://www.pbc.gov.cn/publish/goutongjiaoliu/524/2012/20120108170351045302718/20120108170351045302718_.html(2)

CNH is the name used in the market to refer to offshore deliverable RMB(3)

Actual implementation date to be confirmed(4)

http://online.wsj.com/article/SB10001424052970203986604577257190163679120.html(5)

http://www.centralbanking.com/central-banking/news/2117966/rmb-s-rise-reserve-currency-status-accelerates

More symbolic than material

Accepted across world:

for investment, financing, and payment purposes

as a reserve, intervention and anchor currency

Nigeria has added the equivalent of US$500m in RMB to its reserves4

Chile, Thailand, Brazil and Venezuela are understood to have begun efforts to include RMB in reserve portfolio5

Multi-decade process

A Top GlobalReserve Currency3

JUNE 2009

Pilot launch of cross-border RMB trade settlement scheme

JUNE 2010

Expansion of cross-border RMB trade settlement scheme

AUGUST 2011

Announcement on further expansion of the scheme to nationwide

Trade settled in RMB totaled RMB2.08tn1

in 2011

MARCH 2012

Expansion of RMB export trade settlement from businesses on the Mainland Designated Enterprises (MDEs) list to all companies qualified for external trade3

JULY 2010

Establish of the offshore RMB (CNH2) market in HK

AUGUST 2010

China inter-bank bond market (CIBM) opened to selected offshore RMB Financial Institutions and central banks

JANUARY 2011

Mainland Enterprises can make overseas investment in RMB in the form of ODI

AUGUST 2011Mainland corporate can issue RMB bonds in Hong Kong

OCTOBER 2011

Formalisation

of RMB Foreign Direct investment (FDI)

RMB21bn for 110 projects approved by end December

DECEMBER 2011RMB QFII launched allowing HK subsidiaries of Chinese asset management and securities firms to invest in onshore securities

APRIL 2012

RMB QFII expanded by RMB50bn and allowed to be used in issuing A-share ETFs*

CIBM eligible investors expanded to supranationals, sovereign wealth funds and insurers

MAY 2012Formalisation

of RMB bond issuance in Hong Kong by Mainland non-financial firms

A Top GlobalInvestment Currency2A Top Global

Trading Currency1

6

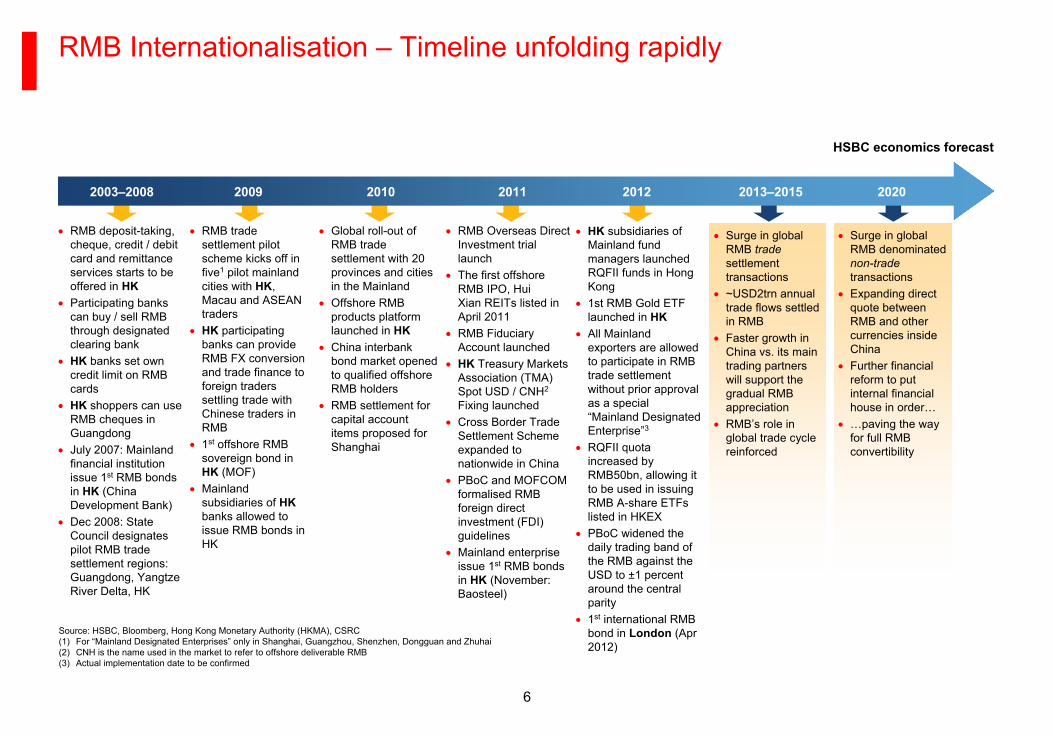

RMB Internationalisation – Timeline unfolding rapidly

Source: HSBC, Bloomberg, Hong Kong Monetary Authority (HKMA), CSRC(1)

For “Mainland Designated Enterprises”

only in Shanghai, Guangzhou, Shenzhen, Dongguan and Zhuhai(2)

CNH is the name used in the market to refer to offshore deliverable RMB(3)

Actual implementation date to be confirmed

HSBC economics forecast

RMB deposit-taking, cheque, credit / debit card and remittance services starts to be offered in HK

Participating banks can buy / sell RMB through designated clearing bank

HK

banks set own credit limit on RMB cards

HK

shoppers can use RMB cheques in Guangdong

July 2007: Mainland financial institution issue 1st

RMB bonds in HK

(China Development Bank)

Dec 2008: State Council designates pilot RMB trade settlement regions: Guangdong, Yangtze River Delta, HK

RMB trade settlement pilot scheme kicks off in five1

pilot mainland cities with HK, Macau and ASEAN traders

HK

participating banks can provide RMB FX conversion and trade finance to foreign traders settling trade with Chinese traders in RMB

1st

offshore RMB sovereign bond in HK

(MOF)

Mainland subsidiaries of HK

banks allowed to issue RMB bonds in HK

Global roll-out of RMB trade settlement with 20 provinces and cities in the Mainland

Offshore RMB products platform launched in HK

China interbank bond market opened to qualified offshore RMB holders

RMB settlement for capital account items proposed for Shanghai

Surge in global RMB denominated non-trade transactions

Expanding direct quote between RMB and other currencies inside China

Further financial reform to put internal financial house in order…

…paving the way for full RMB convertibility

Surge in global RMB trade

settlement transactions

~USD2trn annual trade flows settled in RMB

Faster growth in China vs. its main trading partners will support the gradual RMB appreciation

RMB’s role in global trade cycle reinforced

RMB Overseas Direct Investment trial launch

The first offshore RMB IPO, Hui Xian REITs listed in April 2011

RMB Fiduciary Account launched

HK Treasury Markets Association (TMA) Spot USD / CNH2

Fixing launched

Cross Border Trade Settlement Scheme expanded to nationwide in China

PBoC and MOFCOM formalised RMB foreign direct investment (FDI) guidelines

Mainland enterprise issue 1st

RMB bonds in HK (November: Baosteel)

2003–2008 2009 2010 2011 2012 2013–2015 2020

HK

subsidiaries of Mainland fund managers launched RQFII funds in Hong Kong

1st RMB Gold ETF launched in HK

All Mainland exporters are allowed to participate in RMB trade settlement without prior approval as a special “Mainland Designated Enterprise”3

RQFII quota increased by RMB50bn, allowing it to be used in issuing RMB A-share ETFs listed in HKEX

PBoC widened the daily trading band of the RMB against the USD to ±1 percent around the central parity

1st

international RMB bond in London

(Apr 2012)

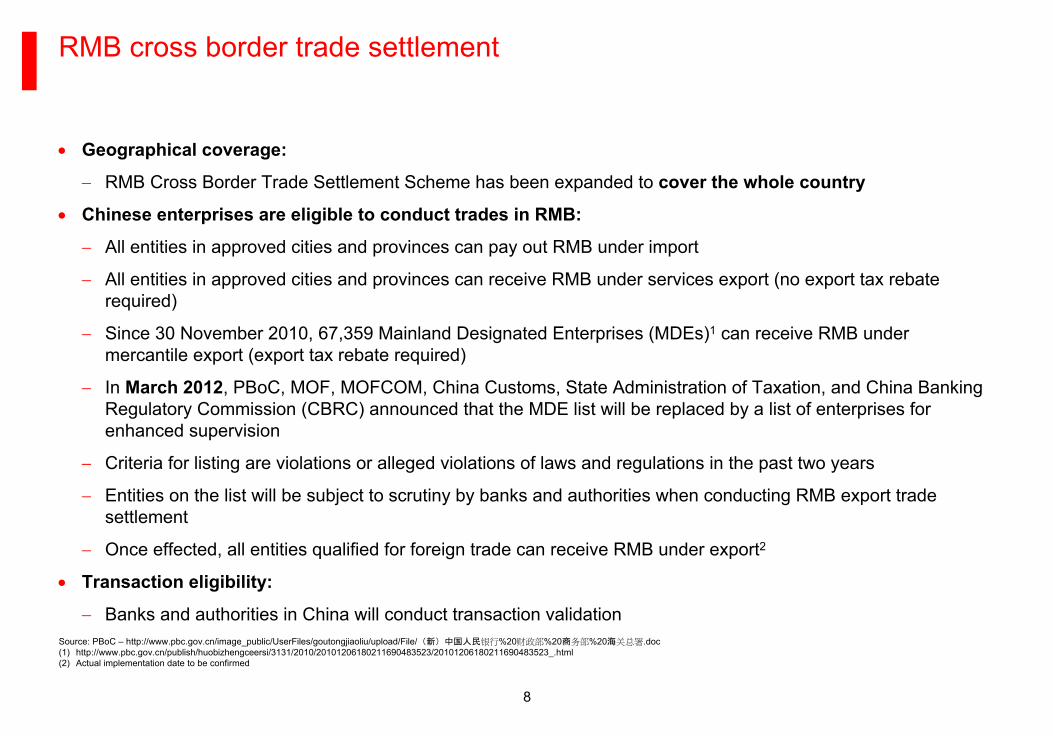

RMB Trade Settlement

8

RMB cross border trade settlement

Geographical coverage:

RMB Cross Border Trade Settlement Scheme has been expanded to cover the whole country

Chinese enterprises are eligible to conduct trades in RMB:

All entities in approved cities and provinces can pay out RMB under import

All entities in approved cities and provinces can receive RMB under services export (no export tax rebate required)

Since 30 November 2010, 67,359 Mainland Designated Enterprises (MDEs)1

can receive RMB under mercantile export (export tax rebate required)

In March 2012, PBoC, MOF, MOFCOM, China Customs, State Administration of Taxation, and China Banking Regulatory Commission (CBRC) announced that the MDE list will be

replaced by a list of enterprises for enhanced supervision

Criteria for listing are violations or alleged violations of laws and regulations in the past two years

Entities on the list will be subject to scrutiny by banks and authorities when conducting RMB export trade settlement

Once effected, all entities qualified for foreign trade can receive RMB under export2

Transaction eligibility:

Banks and authorities in China will conduct transaction validationSource: PBoC –

http://www.pbc.gov.cn/image_public/UserFiles/goutongjiaoliu/upload/File/(新)中国人民银行%20财政部%20商务部%20海关总署.doc(1) http://www.pbc.gov.cn/publish/huobizhengceersi/3131/2010/20101206180211690483523/20101206180211690483523_.html(2) Actual implementation date to be confirmed

9

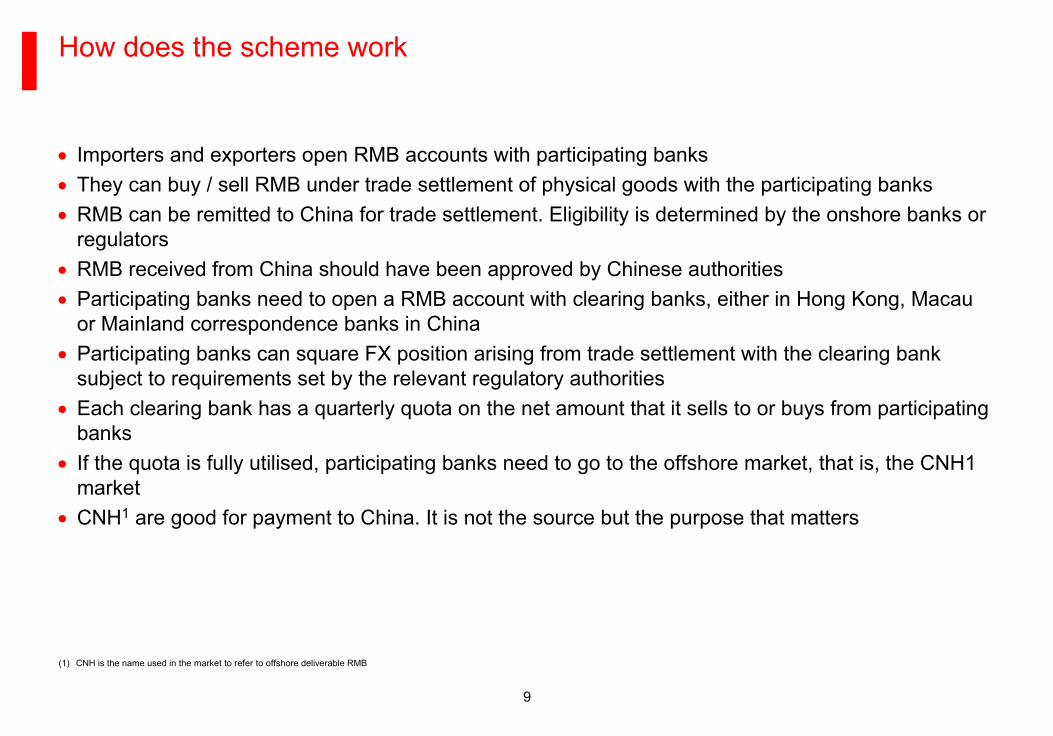

How does the scheme work

(1)

CNH is the name used in the market to refer to offshore deliverable RMB

Importers and exporters open RMB accounts with participating banks

They can buy / sell RMB under trade settlement of physical goods

with the participating banks

RMB can be remitted to China for trade settlement. Eligibility is determined by the onshore banks or regulators

RMB received from China should have been approved by Chinese authorities

Participating banks need to open a RMB account with clearing banks, either in Hong Kong, Macau or Mainland correspondence banks in China

Participating banks can square FX position arising from trade settlement with the clearing bank subject to requirements set by the relevant regulatory authorities

Each clearing bank has a quarterly quota on the net amount that it sells to or buys from participating banks

If the quota is fully utilised, participating banks need to go to the offshore market, that is, the CNH1 market

CNH1

are good for payment to China. It is not the source but the purpose that matters

10

RMB accounts

Offshore corporate can now open RMB account(s) with banks worldwide, for both trade and general purposes

Transfer of RMB funds (limited to offshore only) between different accounts are allowed in Hong Kong

RMB exchange / risk management

As offshore corporates seeking to use RMB as one of the currencies for their operations, foreign exchange risk management will be important

Due to the need for participating banks to adhere to the conditions stipulated under the Clearing Agreement, offshore corporates will need to be aware that a two-tier exchange market for RMB now exists; one market rate for RMB exchange for trade settlement purposes (subject to the quota of the clearing bank) and the other rate for general purposes

RMB Non-deliverable forward (NDF) and Non-deliverable option (NDO) continue to exist but offshore RMB deliverable forward (DF) and deliverable option market have started to take off with steady improvement in liquidity. Price level between NDF and DF are increasingly converging, but the latter has already become the tool of choice for many investors seeking to hedge against RMB volatility

RMB borrowing / financing

Besides the RMB trade financing facilities, all other type of loans in RMB are also available to corporates. Offshore corporates can also issue bonds denominated in RMB

Note that the RMB proceeds obtained from all non-trade financing related facilities including loans and bonds can be remitted back for use in China when the offshore corporates have obtained approval from the relevant authorities in China

RMB investment

There is no restriction with regards to the use of the accumulated RMB funds by offshore corporate provided the funds are not remitted back into the Mainland China

In terms of banking products, the accumulated RMB in the offshore RMB accounts can be invested in bank deposits, RMB bonds or certificate of deposits (CDs) issued offshore, FX-linked structured deposits, commodity-linked structured deposits, equity-linked structured deposits, interest rate-linked structured deposits, RMB-

denominated funds, RMB equities products and exchange-traded funds

Implications for offshore corporate

Development of Offshore RMB

12

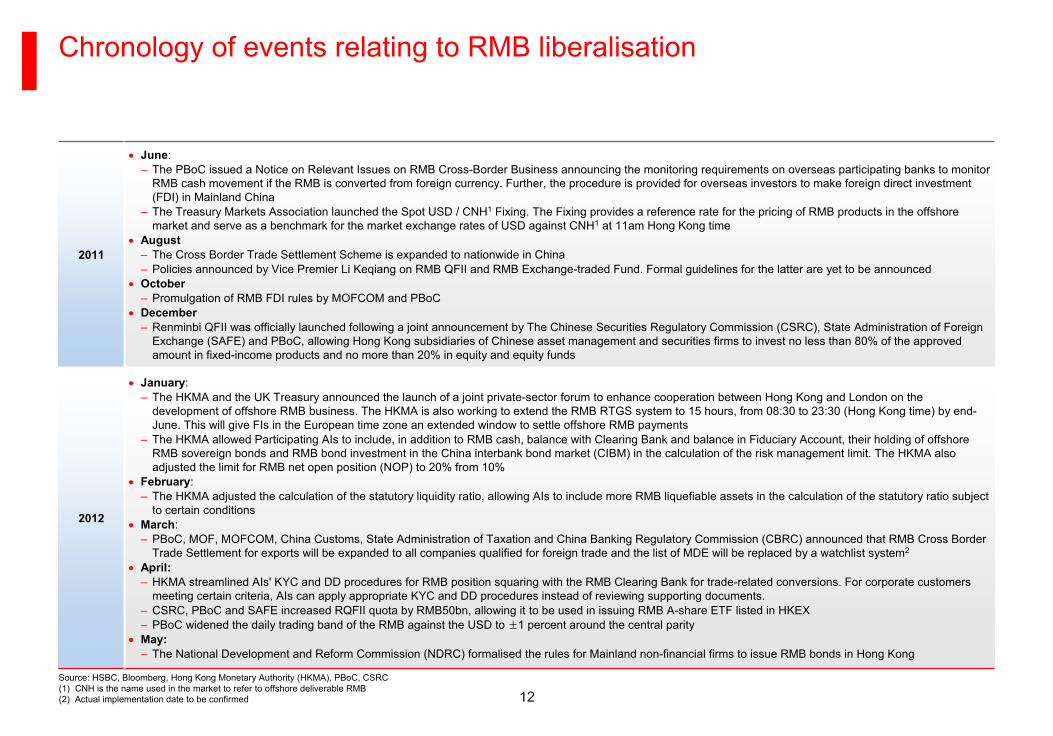

Chronology of events relating to RMB liberalisation

Source: HSBC, Bloomberg, Hong Kong Monetary Authority (HKMA), PBoC, CSRC(1)

CNH is the name used in the market to refer to offshore deliverable RMB(2)

Actual implementation date to be confirmed

2011

June: –

The PBoC issued a Notice on Relevant Issues on RMB Cross-Border Business announcing the monitoring requirements on overseas participating banks to monitor RMB cash movement if the RMB is converted from foreign currency.

Further, the procedure is provided for overseas investors to make foreign direct investment (FDI) in Mainland China

–

The Treasury Markets Association launched the Spot USD / CNH1

Fixing. The Fixing provides a reference rate for the pricing of

RMB products in the offshore market and serve as a benchmark for the market exchange rates of

USD against CNH1

at 11am Hong Kong time

August–

The Cross Border Trade Settlement Scheme is expanded to nationwide in China–

Policies announced by Vice Premier Li Keqiang on RMB QFII and RMB Exchange-traded Fund. Formal guidelines for the latter are yet to be announced

October–

Promulgation of RMB FDI rules by MOFCOM and PBoC

December–

Renminbi QFII was officially launched following a joint announcement by The Chinese Securities Regulatory Commission (CSRC), State Administration of Foreign Exchange (SAFE) and PBoC, allowing Hong Kong subsidiaries of Chinese asset management and securities firms to invest no less than 80% of the approved amount in fixed-income products and no more than 20% in equity and equity funds

2012

January: –

The HKMA and the UK Treasury announced the launch of a joint private-sector forum to enhance cooperation between Hong Kong and London

on the development of offshore RMB business. The HKMA is also working to extend the RMB RTGS system to 15 hours, from 08:30 to 23:30 (Hong Kong time) by end-

June. This will give FIs in the European time zone an extended window to settle offshore RMB payments–

The HKMA allowed Participating AIs to include, in addition to RMB cash, balance with Clearing Bank and balance in Fiduciary Account, their holding of offshore RMB sovereign bonds and RMB bond investment in the China interbank bond market (CIBM) in the calculation of the risk management limit. The HKMA also adjusted the limit for RMB net open position (NOP) to 20% from 10%

February: –

The HKMA adjusted the calculation of the statutory liquidity ratio, allowing AIs to include more RMB liquefiable assets in the calculation of the statutory ratio subject to certain conditions

March: –

PBoC, MOF, MOFCOM, China Customs, State Administration of Taxation and China Banking Regulatory Commission (CBRC) announced that

RMB Cross Border Trade Settlement for exports will be expanded to all companies qualified for foreign trade and the list of MDE will be replaced by a watchlist system2

April:–

HKMA streamlined AIs' KYC and DD procedures for RMB position squaring with the RMB Clearing Bank for trade-related conversions. For corporate customers meeting certain criteria, AIs can apply appropriate KYC and DD procedures instead of reviewing supporting documents.

–

CSRC, PBoC and SAFE increased RQFII quota by RMB50bn, allowing it to be used in issuing RMB A-share ETF listed in HKEX–

PBoC widened the daily trading band of the RMB against the USD to ±1 percent around the central parity

May:–

The National Development and Reform Commission (NDRC) formalised

the rules for Mainland non-financial firms to issue RMB bonds in Hong Kong

13

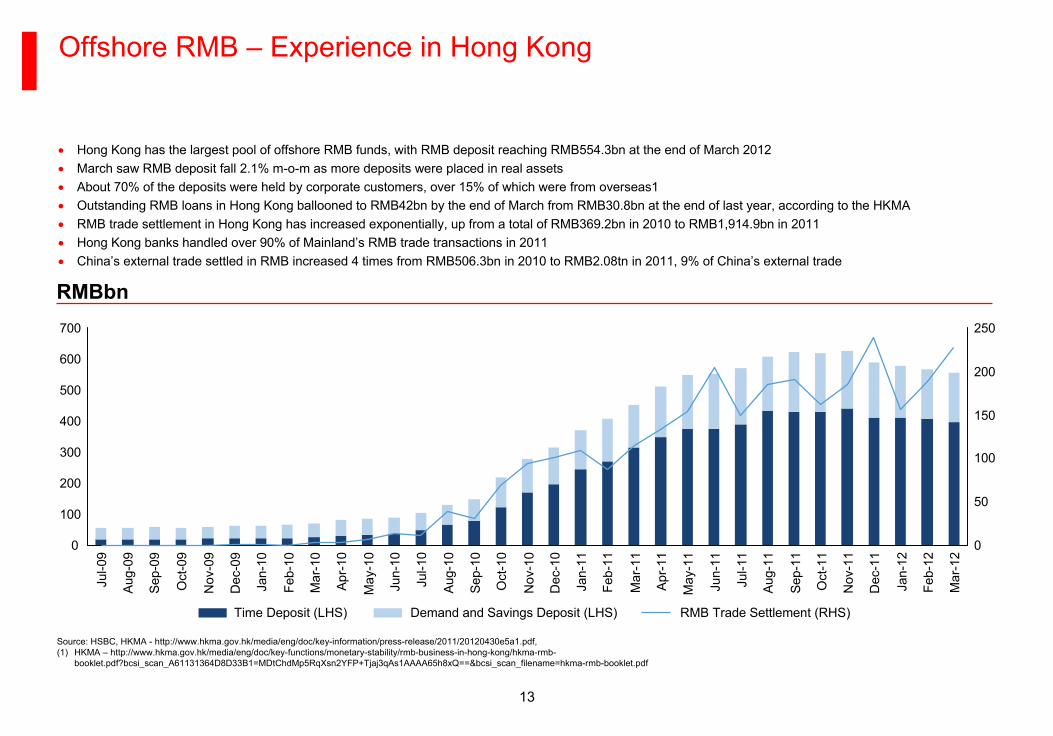

Offshore RMB – Experience in Hong Kong

Source: HSBC, HKMA -

http://www.hkma.gov.hk/media/eng/doc/key-information/press-release/2011/20120430e5a1.pdf, (1)

HKMA –

http://www.hkma.gov.hk/media/eng/doc/key-functions/monetary-stability/rmb-business-in-hong-kong/hkma-rmb-

booklet.pdf?bcsi_scan_A61131364D8D33B1=MDtChdMp5RqXsn2YFP+Tjaj3qAs1AAAA65h8xQ==&bcsi_scan_filename=hkma-rmb-booklet.pdf

Hong Kong has the largest pool of offshore RMB funds, with RMB deposit reaching RMB554.3bn at the end of March 2012

March saw RMB deposit fall 2.1% m-o-m

as more deposits were placed in real assets

About 70% of the deposits were held by corporate customers, over

15% of which were from overseas1

Outstanding RMB loans in Hong Kong ballooned to RMB42bn by the end of March from RMB30.8bn at the end of last year, according to the HKMA

RMB trade settlement in Hong Kong has increased exponentially, up from a total of RMB369.2bn in 2010 to RMB1,914.9bn in 2011

Hong Kong banks handled over 90% of Mainland’s RMB trade transactions in 2011

China’s external trade settled in RMB increased 4 times from RMB506.3bn in 2010 to RMB2.08tn in 2011, 9% of China’s external trade

RMBbn

100

200

300

400

500

600

700

0

Jul-0

9

Aug-

09

Sep-

09

Oct

-09

Nov

-09

Dec

-09

Jan-

10

Feb-

10

Mar

-10

Apr-

10

May

-10

Jun-

10

Jul-1

0

Aug-

10

Sep-

10

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Feb-

11

Mar

-11

Apr-

11

May

-11

Jun-

11

Jul-1

1

Aug-

11

Sep-

11

Oct

-11

Nov

-11

Dec

-11

Jan-

12

Feb-

12

Mar

-12

0

50

100

150

200

250

Time Deposit (LHS) Demand and Savings Deposit (LHS) RMB Trade Settlement (RHS)

14

Mainland China

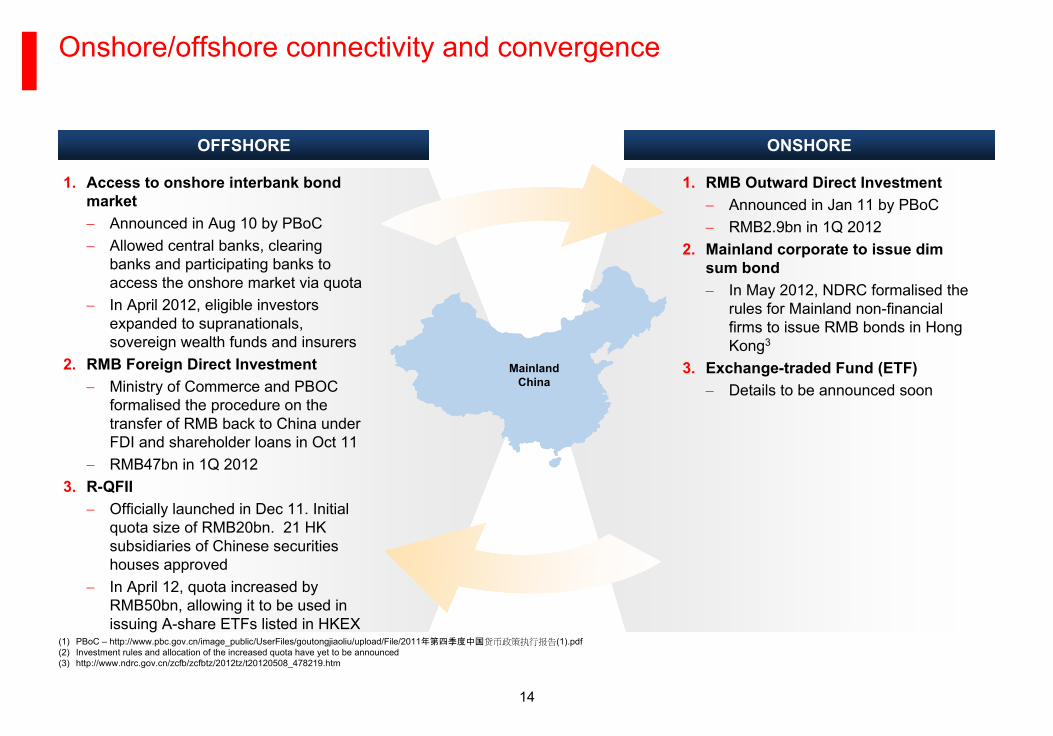

Onshore/offshore connectivity and convergence

1.

Access to onshore interbank bond market

Announced in Aug 10 by PBoC

Allowed central banks, clearing banks and participating banks to access the onshore market via quota

In April 2012, eligible investors expanded to supranationals, sovereign wealth funds and insurers

2.

RMB Foreign Direct Investment

Ministry of Commerce and PBOC formalised the procedure on the transfer of RMB back to China under FDI and shareholder loans in Oct 11

RMB47bn in 1Q 20123.

R-QFII

Officially launched in Dec 11. Initial quota size of RMB20bn. 21 HK subsidiaries of Chinese securities houses approved

In April 12, quota increased by RMB50bn, allowing it to be used in issuing A-share ETFs listed in HKEX

1.

RMB Outward Direct Investment

Announced in Jan 11 by PBoC

RMB2.9bn in 1Q 20122.

Mainland corporate to issue dim sum bond

In May 2012, NDRC formalised the rules for Mainland non-financial firms to issue RMB bonds in Hong Kong3

3.

Exchange-traded Fund (ETF)

Details to be announced soon

(1)

PBoC

–

http://www.pbc.gov.cn/image_public/UserFiles/goutongjiaoliu/upload/File/2011年第四季度中国货币政策执行报告(1).pdf(2)

Investment rules and allocation of the increased quota have yet to be announced(3)

http://www.ndrc.gov.cn/zcfb/zcfbtz/2012tz/t20120508_478219.htm

OFFSHORE ONSHORE

15

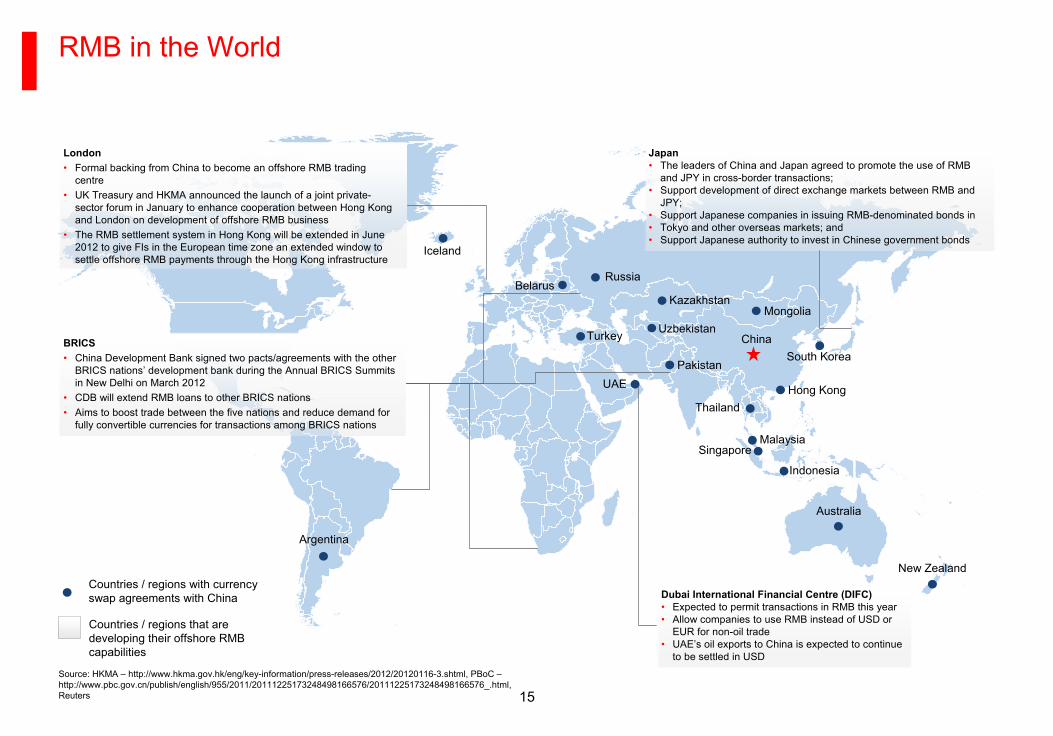

RMB in the World

UAE

Belarus

Indonesia

Iceland

SingaporeMalaysia

New Zealand

UzbekistanMongolia

Kazakhstan

South Korea

Hong KongThailand

Pakistan

Turkey

Argentina

London•

Formal backing from China to become an offshore RMB trading centre

•

UK Treasury and HKMA announced the launch of a joint private-

sector forum in January to enhance cooperation between Hong Kong

and London on development of offshore RMB business•

The RMB settlement system in Hong Kong will be extended in June 2012 to give FIs in the European time zone an extended window to

settle offshore RMB payments through the Hong Kong infrastructure

Japan•

The leaders of China and Japan agreed to promote the use of RMB and JPY in cross-border transactions;

•

Support development of direct exchange markets between RMB and JPY;

•

Support Japanese companies in issuing RMB-denominated bonds in•

Tokyo and other overseas markets; and•

Support Japanese authority to invest in Chinese government bonds

Dubai International Financial Centre (DIFC)•

Expected to permit transactions in RMB this year •

Allow companies to use RMB instead of USD or EUR for non-oil trade

•

UAE’s oil exports to China is expected to continue to be settled in USD

Countries / regions with currency swap agreements with China

Countries / regions that are developing their offshore RMB capabilities

Source: HKMA –

http://www.hkma.gov.hk/eng/key-information/press-releases/2012/20120116-3.shtml, PBoC –

http://www.pbc.gov.cn/publish/english/955/2011/20111225173248498166576/20111225173248498166576_.html, Reuters

Russia

BRICS•

China Development Bank signed two pacts/agreements with the other BRICS nations’

development bank during the Annual BRICS Summits in New Delhi on March 2012

•

CDB will extend RMB loans to other BRICS nations•

Aims to boost trade between the five nations and reduce demand for fully convertible currencies for transactions among BRICS nations

China

Australia

16

What has happened to RMB?

RMB band widening

PBoC widened the daily trading band of the USD-CNY exchange rate to +/-1% from a previous width of +/-0.5%

The last time the band was widened was in May 2007, when the band was increased from +/-0.3%

HSBC Comments:–

Unlikely to see the market respond by increasing expectations for greater appreciation–

Gradual increase in intraday volatility, though it may not necessarily utilise

the full newly expanded range–

Lower CNY-CNH divergence as onshore USD-CNY now has more flexibility to follow USD-CNH

Less appreciation, more volatility

Cyclically inflation has come weaker than market had expected (March CPI remains below Beijing’s 4% target)

Structural surplus is rapidly narrowing, latest trade-surplus-to-GDP read falling to new low of 1.9% on latest print

HSBC Forecast: –

Cyclical and structural forces for appreciation have weakened further–

Adjust our year-end 2012 forecast of USD-CNY to 6.18 or less than 2% appreciation from 3% over the calendar year

Faster liberalisation

RQFII quota expanded to RMB70bn from RMB20bn

Abolishment of the Mainland Designated Enterprise (MDE) white list, fully opening cross-border RMB trade settlement channel

HSBC Comments:–

Authorities appear to be taking advantage of relative equilibrium in USD-RMB to accelerate liberalisation–

Wider and more numerous cross-border channels mean less CNY-CNH divergence but more variability in offshore CNH deposit base growth

Source: HSBC Global Research "Asian FX : RMB band widening -

even more flexibility, 14 April 2012“, “Asian FX : RMB... even less appreciation, 11 April 2012”, “China March CPI: Edgingup temporarily, 9 April 2012”, “Asian FX : RMB -

faster liberalisation, 5 April 2012”

Offshore RMB Markets

18

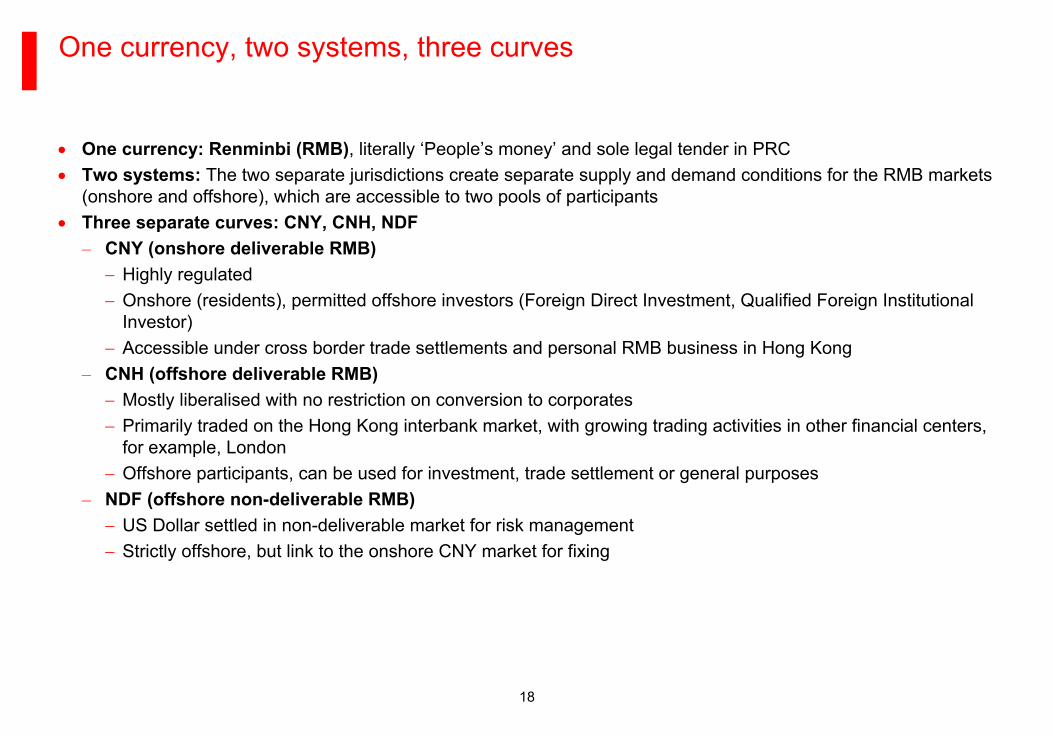

One currency, two systems, three curves

One currency: Renminbi (RMB), literally ‘People’s money’

and sole legal tender in PRC

Two systems:

The two separate jurisdictions create separate supply and demand conditions for the RMB markets (onshore and offshore), which are accessible to two pools of participants

Three separate curves: CNY, CNH, NDF–

CNY (onshore deliverable RMB)

Highly regulated

Onshore (residents), permitted offshore investors (Foreign Direct Investment, Qualified Foreign Institutional Investor)

Accessible under cross border trade settlements and personal RMB

business in Hong Kong–

CNH (offshore deliverable RMB)

Mostly liberalised

with no restriction on conversion to corporates

Primarily traded on the Hong Kong interbank market, with growing

trading activities in other financial centers, for example, London

Offshore participants, can be used for investment, trade settlement or general purposes–

NDF (offshore non-deliverable RMB)

US Dollar settled in non-deliverable market for risk management

Strictly offshore, but link to the onshore CNY market for fixing

RMB FX and Money Market

20

Offshore market is often being referred as CNH1

Market turnover increased gradually to around

USD1.4bn daily

Recent RMB band widening helps to a lower CNY-

CNH divergence2

Widening of the USDCNY daily trading band

allowed more flexibility with increased volatility

During periods of risk off and particular USD

demand, onshore USDCNY has more

flexibility to move upwards

CNY-CNH divergence under such circumstances may be more limited

FX spot

Note:(1)

CNH is the name used in the market to refer to offshore deliverable RMB(2)

HSBC Global Research "Asian FX : RMB band widening -

even more flexibility, 14 April 2012“Source: HSBC, Reuters

6.26

6.31

6.36

6.41

6.46

6.51

6.56

6.61

6.66

6.71

6.76

6.81

21-J

ul

18-A

ug

15-S

ep

13-O

ct

10-N

ov

08-D

ec

05-J

an

02-F

eb

02-M

ar

30-M

ar

27-A

pr

25-M

ay

22-J

un

20-J

ul

17-A

ug

14-S

ep

12-O

ct

09-N

ov

07-D

ec

04-J

an

01-F

eb

29-F

eb

28-M

ar

25-A

pr

Offshore Onshore

Mid-October 2010: CNH1

was traded at a premium as much as 3% at one point due to speculation of RMB reveluation

22 September 2011: CNH1 was traded at a discount as much as 2.5% due to USDCNH1 short-

covering on risk aversion

21

FX forward market – Mechanics of three different curves

CNY

–

Onshore deliverable forward

Restricted access by onshore entities under

current account transactions

CNY forward curve now is in line with the interest

differentials as SAFE removed the amount of FX

forwards that a bank can hold

NDF –

Offshore

non-deliverable forward

Expectation of RMB depreciation (currently

build-in 0.7% in 1 year’s time)

Accessible by any individuals and entities

outside China

CNH1

–

Offshore

deliverable forward

Behaved like a standard liberalised

FX forward curve, reflecting USD and

offshore RMB interest rate differentials

Improved efficiency and growing market liquidity

Data as of 10 May 2012Note:(1)

CNH is the name used in the market to refer to offshore deliverable RMBSource: HSBC, Reuters

6.30

6.32

6.34

6.36

6.38

6.40

SPOT 1M 2M 3M 6M 9M 12M

DF NDF Offshore DF

22

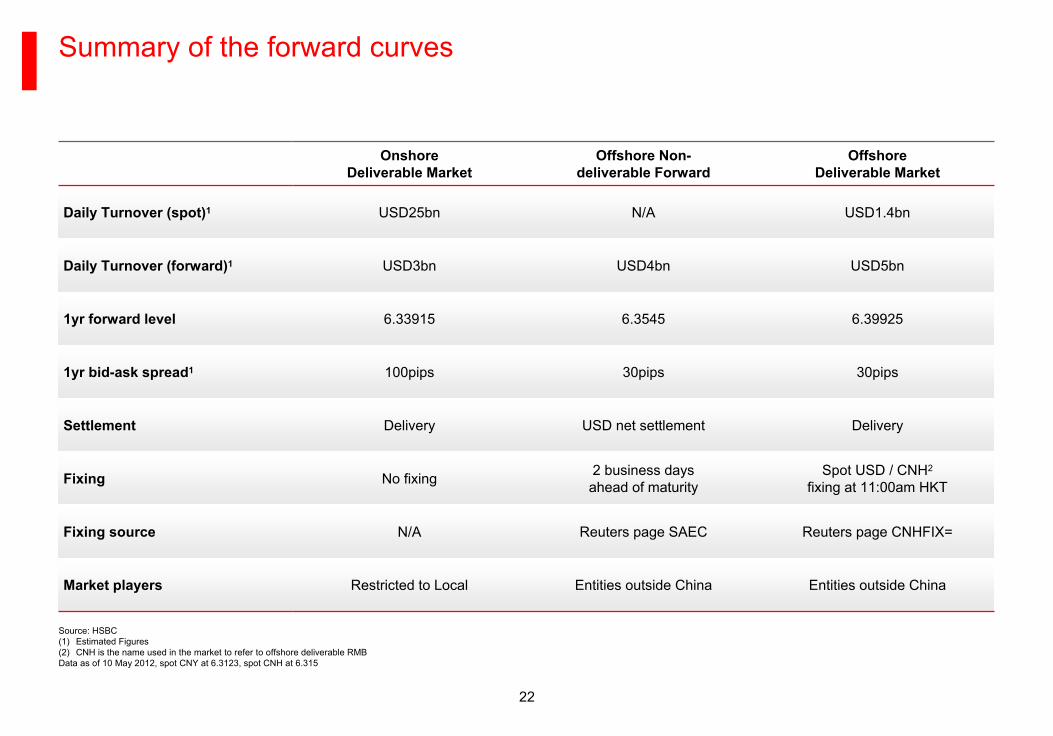

Onshore Deliverable Market

Offshore Non-

deliverable Forward

Offshore Deliverable Market

Daily Turnover (spot)1 USD25bn N/A USD1.4bn

Daily Turnover (forward)1 USD3bn USD4bn USD5bn

1yr forward level 6.33915 6.3545 6.39925

1yr bid-ask spread1 100pips 30pips 30pips

Settlement Delivery USD net settlement Delivery

Fixing No fixing 2 business days ahead of maturity

Spot USD / CNH2

fixing at 11:00am HKT

Fixing source N/A Reuters page SAEC Reuters page CNHFIX=

Market players Restricted to Local Entities outside China Entities outside China

Source: HSBC(1)

Estimated Figures(2)

CNH is the name used in the market to refer to offshore deliverable RMBData as of 10 May 2012, spot CNY at 6.3123, spot CNH at 6.315

Summary of the forward curves

23

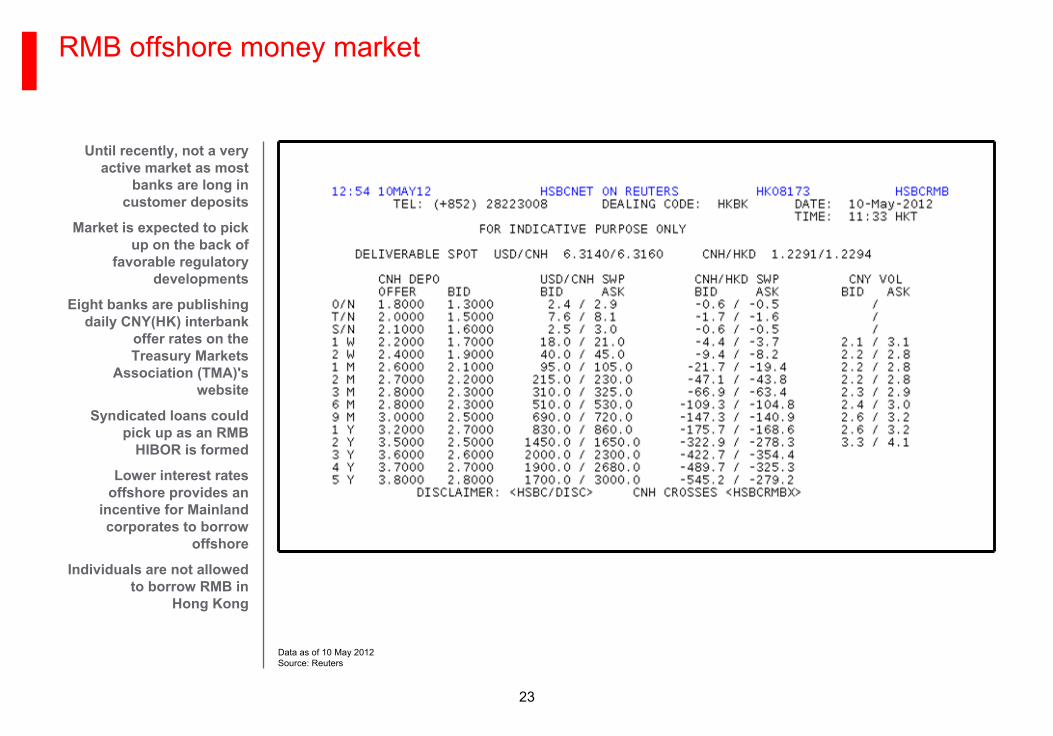

RMB offshore money market

Until recently, not a very active market as most

banks are long in customer deposits

Market is expected to pick up on the back of

favorable regulatory developments

Eight banks are publishing daily CNY(HK) interbank

offer rates on the Treasury Markets

Association (TMA)'s website

Syndicated loans could pick up as an RMB

HIBOR is formed

Lower interest rates offshore provides an

incentive for Mainland corporates to borrow

offshore

Individuals are not allowed to borrow RMB in

Hong Kong

Data as of 10 May 2012

Source: Reuters

24

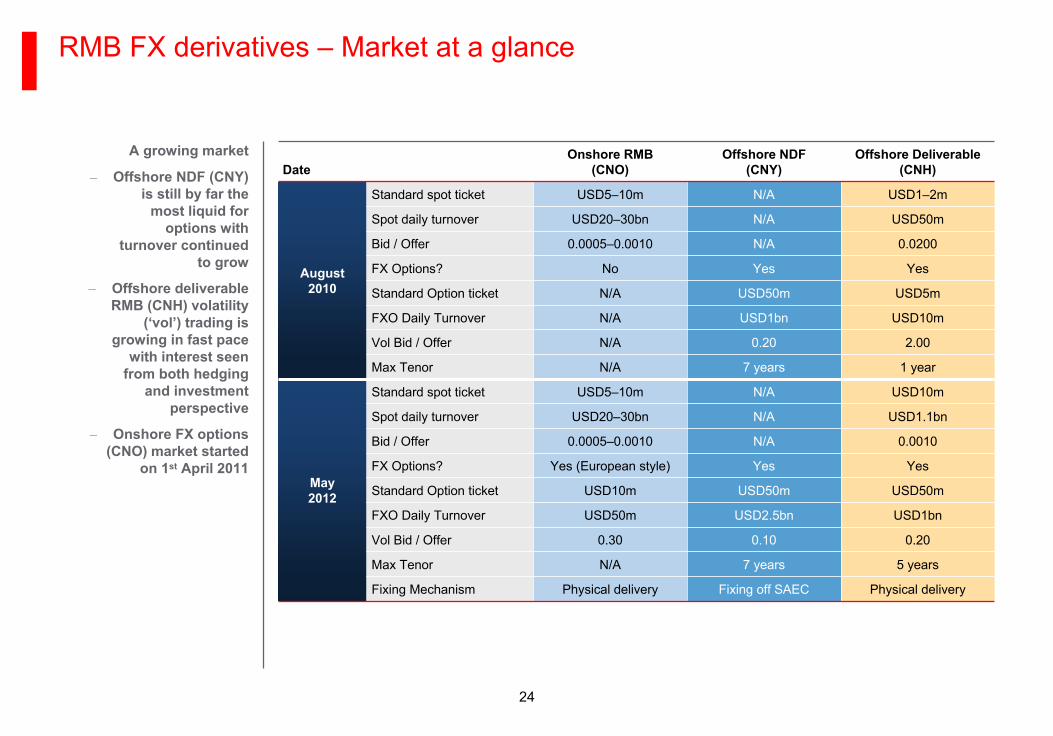

RMB FX derivatives – Market at a glance

A growing market

–

Offshore NDF (CNY) is still by far the

most liquid for options with

turnover continued to grow

–

Offshore deliverable RMB (CNH) volatility

(‘vol’) trading is growing in fast pace

with interest seen from both hedging

and investment perspective

–

Onshore FX options (CNO) market started

on 1st

April 2011

DateOnshore RMB

(CNO)Offshore NDF

(CNY)Offshore Deliverable

(CNH)

August

2010

Standard spot ticket USD5–10m N/A USD1–2m

Spot daily turnover USD20–30bn N/A USD50m

Bid / Offer 0.0005–0.0010 N/A 0.0200

FX Options? No Yes Yes

Standard Option ticket N/A USD50m USD5m

FXO Daily Turnover N/A USD1bn USD10m

Vol

Bid / Offer N/A 0.20 2.00

Max Tenor N/A 7 years 1 year

May

2012

Standard spot ticket USD5–10m N/A USD10m

Spot daily turnover USD20–30bn N/A USD1.1bn

Bid / Offer 0.0005–0.0010 N/A 0.0010

FX Options? Yes (European style) Yes Yes

Standard Option ticket USD10m USD50m USD50m

FXO Daily Turnover USD50m USD2.5bn USD1bn

Vol

Bid / Offer 0.30 0.10 0.20

Max Tenor N/A 7 years 5 years

Fixing Mechanism Physical delivery Fixing off SAEC Physical delivery

25

Deliverable RMB Products Non-deliverable RMB Products

FX Product Components

Spot FX (for trade as well as for general purposes)

Deliverable Forward (for general purpose)

Deliverable Option (for general purpose)

Non-deliverable Forward

Non-deliverable Option

Product Capabilities

Vanilla, European and discrete barriers, callable variations, target redemption variations and any structured forwards offered by HSBC

Baskets

Vanilla and Barrier options on other currencies quanta to CNH1

(e.g. AUD/USD DNT quanta to CNH1)

FX Indices

Vanilla, European and discrete barriers, callable variations, target redemption variations and any structured forwards offered by HSBC

Baskets

Vanilla and Barrier options on other currencies quanta to CNY (e.g. AUD/USD DNT quanta to CNY)

FX Indices

Wrappers

OTC in HK, London & selected centers*

Structured Deposit in HK, London & selected centers*

Structured Note using HSBC HK or London as issuer

OTC

Structured Deposit

Structured Note using HSBC HK or London as issuer

Selected Credentials

1st spot USDCNH1

deal in market

1st CNH1

FX option traded in market (Oct 2010)

Amongst the 1st

globally to trade deliverable RMB structured deposit

1st CNH1

Multicallable Forward traded in market (Jun 2011). Over CNH1

20bn of volume traded of multicallable and target redemption variations

1st FX-linked index with CNH1

as component traded in market (with European client)

HSBC’s offshore RMB FX capabilities

HSBC played a leading role in driving the rapid

product development in CNH1

market

HSBC offers a complete panel of solutions to

match clients’

investments, financing and risk management

needs

*Availability varies based on transacting HSBC entity (1)

CNH is the name used in the market to refer to offshore deliverable RMB

Offshore RMB Bond Market (Dim Sum bonds)

27

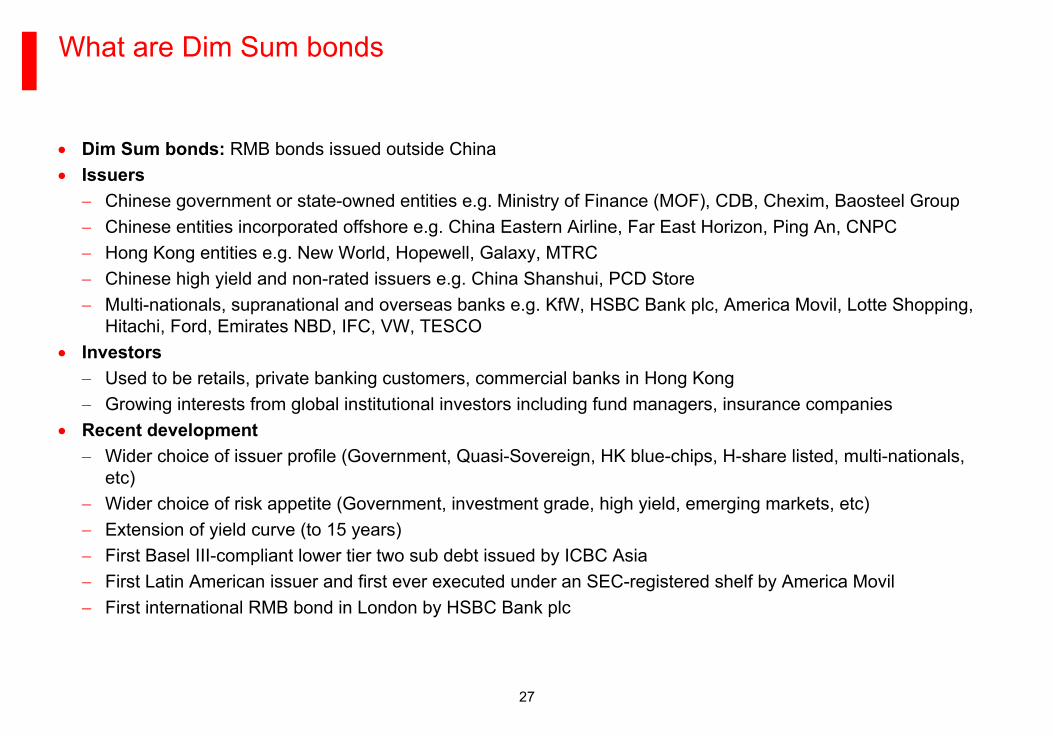

What are Dim Sum bonds

Dim Sum bonds:

RMB bonds issued outside China

Issuers

Chinese government or state-owned entities e.g. Ministry of Finance (MOF), CDB, Chexim, Baosteel Group

Chinese entities incorporated offshore e.g. China Eastern Airline, Far East Horizon, Ping An, CNPC

Hong Kong entities e.g. New World, Hopewell, Galaxy, MTRC

Chinese high yield and non-rated issuers e.g. China Shanshui, PCD Store

Multi-nationals, supranational and overseas banks e.g. KfW, HSBC Bank plc, America Movil, Lotte Shopping, Hitachi, Ford, Emirates NBD, IFC, VW, TESCO

Investors

Used to be retails, private banking customers, commercial banks in Hong Kong

Growing interests from global institutional investors including fund managers, insurance companies

Recent development

Wider choice of issuer profile (Government, Quasi-Sovereign, HK blue-chips, H-share listed, multi-nationals, etc)

Wider choice of risk appetite (Government, investment grade, high yield, emerging markets, etc)

Extension of yield curve (to 15 years)

First Basel III-compliant lower tier two sub debt issued by ICBC Asia

First Latin American issuer and first ever executed under an SEC-registered shelf by America Movil

First international RMB bond in London by HSBC Bank plc

28

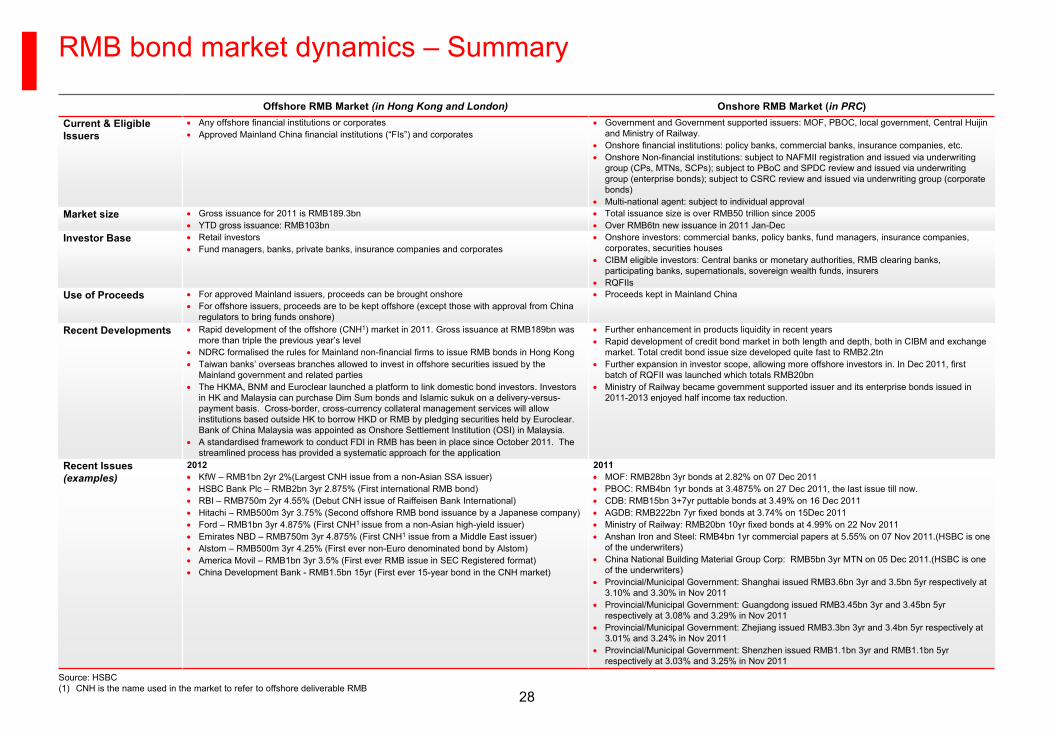

RMB bond market dynamics – Summary

Offshore RMB Market (in Hong Kong and London) Onshore RMB Market (in PRC) Current & Eligible Issuers

Any offshore financial institutions or corporates

Approved Mainland China

financial institutions (“FIs”) and corporates

Government and Government supported issuers: MOF, PBOC, local government, Central Huijin

and Ministry of Railway.

Onshore financial institutions: policy banks, commercial banks, insurance companies, etc.

Onshore Non-financial institutions: subject to NAFMII registration and issued via underwriting group (CPs, MTNs, SCPs); subject to PBoC

and SPDC review and issued via underwriting group (enterprise bonds); subject to CSRC review and issued via underwriting group (corporate bonds)

Multi-national agent: subject to individual approvalMarket size

Gross issuance for 2011 is RMB189.3bn

YTD gross issuance: RMB103bn

Total issuance size is over RMB50 trillion since 2005

Over RMB6tn new issuance in 2011 Jan-DecInvestor Base

Retail investors

Fund managers, banks, private banks, insurance companies and corporates

Onshore investors: commercial banks, policy banks, fund managers, insurance companies, corporates, securities houses

CIBM eligible investors: Central banks or monetary authorities, RMB clearing banks, participating banks, supernationals, sovereign wealth funds, insurers

RQFIIsUse of Proceeds

For approved Mainland issuers, proceeds can be brought onshore

For offshore issuers, proceeds are to be kept offshore (except those with approval from China regulators to bring funds onshore)

Proceeds kept in Mainland China

Recent Developments

Rapid development of the offshore (CNH1) market in 2011. Gross issuance at RMB189bn was more than triple the previous year’s level

NDRC formalised the rules for Mainland non-financial firms to issue RMB bonds in Hong Kong

Taiwan banks’

overseas branches allowed to invest in offshore securities issued by the Mainland government and related parties

The HKMA, BNM and Euroclear launched a platform to link domestic

bond investors. Investors in HK and Malaysia can purchase Dim Sum bonds and Islamic sukuk on a delivery-versus-

payment basis. Cross-border, cross-currency collateral management services will allow institutions based outside HK to borrow HKD or RMB by pledging securities held by Euroclear. Bank of China Malaysia was appointed as Onshore Settlement Institution (OSI) in Malaysia.

A standardised

framework to conduct FDI in RMB has been in place since October

2011. The streamlined process has provided a systematic approach for the application

Further enhancement in products liquidity in recent years

Rapid development of credit bond market in both length and depth, both in CIBM and exchange market. Total credit bond issue size developed quite fast to RMB2.2tn

Further expansion in investor scope, allowing more offshore investors in. In Dec 2011, first batch of RQFII was launched which totals RMB20bn

Ministry of Railway became government supported issuer and its enterprise bonds issued in 2011-2013 enjoyed half income tax reduction.

Recent Issues (examples)

2012

KfW –

RMB1bn 2yr 2%(Largest CNH issue from a non-Asian SSA issuer)

HSBC Bank Plc –

RMB2bn 3yr 2.875% (First international RMB bond)

RBI –

RMB750m 2yr 4.55% (Debut CNH issue of Raiffeisen Bank International)

Hitachi –

RMB500m 3yr 3.75% (Second offshore RMB bond issuance by a Japanese company)

Ford –

RMB1bn 3yr 4.875% (First CNH1 issue from a non-Asian high-yield issuer)

Emirates NBD –

RMB750m 3yr 4.875% (First CNH1

issue from a Middle East issuer)

Alstom –

RMB500m 3yr 4.25% (First ever non-Euro denominated bond by Alstom)

America Movil –

RMB1bn 3yr 3.5% (First ever RMB issue in SEC Registered format)

China Development Bank -

RMB1.5bn 15yr (First ever 15-year bond in the CNH market)

2011

MOF: RMB28bn 3yr bonds at 2.82% on 07 Dec 2011

PBOC: RMB4bn 1yr bonds at 3.4875% on 27 Dec 2011, the last issue

till now.

CDB: RMB15bn 3+7yr puttable

bonds at 3.49% on 16 Dec 2011

AGDB: RMB222bn 7yr fixed bonds at 3.74% on 15Dec 2011

Ministry of Railway: RMB20bn 10yr fixed bonds at 4.99% on 22 Nov

2011

Anshan Iron and Steel: RMB4bn 1yr commercial papers at 5.55% on 07 Nov 2011.(HSBC is one of the underwriters)

China National Building Material Group Corp: RMB5bn 3yr MTN on 05 Dec 2011.(HSBC is one of the underwriters)

Provincial/Municipal Government: Shanghai issued RMB3.6bn 3yr and 3.5bn 5yr respectively at 3.10% and 3.30% in Nov 2011

Provincial/Municipal Government: Guangdong issued RMB3.45bn 3yr and 3.45bn 5yr respectively at 3.08% and 3.29% in Nov 2011

Provincial/Municipal Government: Zhejiang issued RMB3.3bn 3yr and 3.4bn 5yr respectively at 3.01% and 3.24% in Nov 2011

Provincial/Municipal Government: Shenzhen issued RMB1.1bn 3yr and RMB1.1bn 5yr respectively at 3.03% and 3.25% in Nov 2011

Source: HSBC(1)

CNH is the name used in the market to refer to offshore deliverable RMB

29

Overview of offshore RMB bond market

Under the favorable regulatory and interest

rate environment, the offshore RMB bond

market has developed rapidly in

recent years

Tenors less than 3 years account for 95% of new issuance indicating the

strong demand for short tenors

HSBC forecasts RMB260-

310bn gross issuance

and RMB400-450bn market size by the end

of 2012

In terms of issuer type, HSBC believes Chinese

entities, including sovereigns, banks, and

corporates, will continue to dominate issuance in

this space

(1)

Excluding synthetic RMB bond issuances

2007-2012 RMB Bonds/CD Issuance, by country New issuances by Issuer Typre

(2011)1

Issuance Size (RMBbn)

New issuances by Tenor (2012 YTD)1 New issuances by Issuer Typre

(2012 YTD)1

Less than 1-year (33%)

1-year (33%)

2-year (10%)

3-year (19%)

5-year (2%)

More than 10-year (3%)

Sovereigns (0%)

Supranationals (0%)

Chinese Fis (76%)

Corporates (4%)

Foreigns Fis (9%)

MNC (11%)

Sovereigns (11%)

Supranationals (0%)

Chinese Fis (42%)

Corporates (32%)

Foreigns Fis (5%)

MNC (10%)0

50

100

150

200

250

300

2007 2008 2009 2010 2011

Mainland China Hong Kong Non-Chinese Entity Expected

Announcement Date2012

30

Issuer qualification

Any offshore entity as long as it qualifies the general bond issuing criteria in the Hong Kong/international bond market

Any onshore Chinese entity should obtain relevant regulators’

approvals

Use of proceeds

If the issuer intends to bring back onshore for capex and / or general working capital purpose, the remittance exercise is subject to Mainland authorities approvals

If the issuer intends to use the proceeds outside of Mainland China:

For trade settlement: the issuer needs to figure whether it has receivables in RMB for natural hedge, otherwise, it will be exposed to foreign exchange risk

For swap into USD: the USDCNH1

Cross Currency Swap (“CCS”) market is liquid up to 3 years with monthly turnover approaching USD3bn and a maximum possible tenor of 10 years with reduced liquidity

Issue Ratings

Preferred

Listing

Preferred

Marketing

It is recommended that the issuer could meet the key potential investors in Hong Kong and Singapore via marketing roadshow

For high quality names, the issuer could also choose to conduct investor calls with regional investors if travel is not convenient

HSBC will also help the issuer to upload the roadshow presentation to NetRoadshow to maximise the investor coverage

Documentation

Standalone Regulation S documentation or off EMTN programme

Necessary changes should be made to EMTN programme to include settlement via Central Moneymarket Unit (CMU)

Clearing system

CMU

Euroclear

Issuer’s considerations

Key considerations for issuers looking to tap the international RMB

bond market

(1)

CNH is the name used in the market to refer to offshore deliverable RMB

31

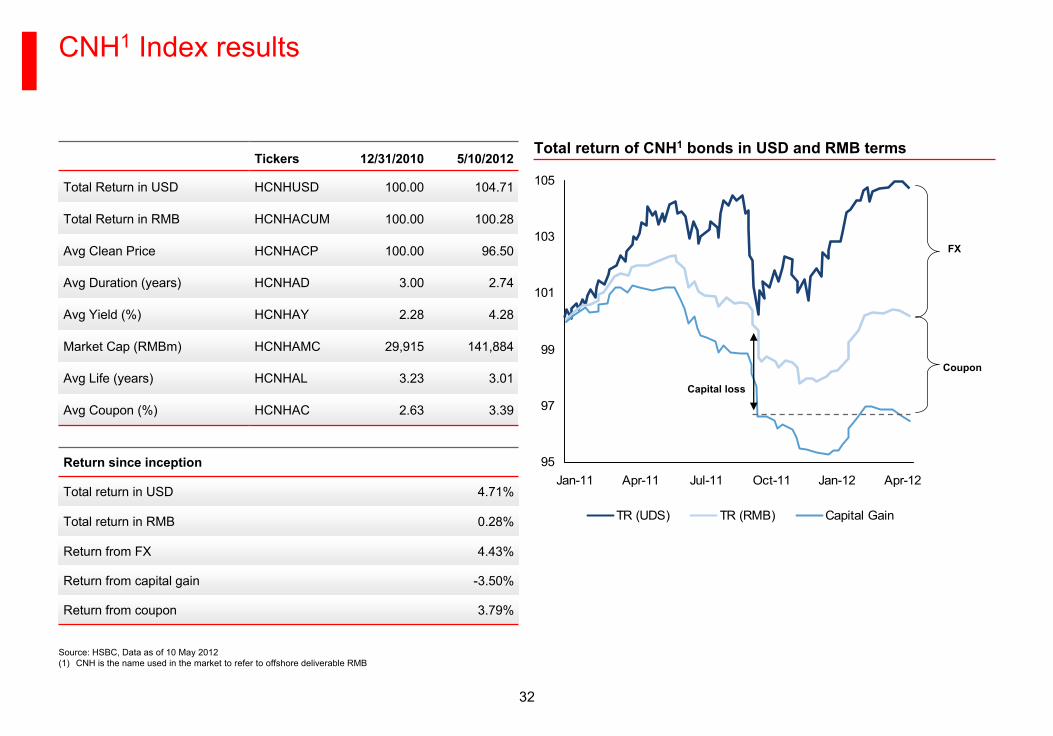

Introducing HSBC offshore RMB bond index (CNH1

Index)

HSBC CNH1

index is launched as part of the HSBC Asian Local Bond Index (ALBI)

CNH1

Index tracks total return performance of RMB-

denominated and settled bonds and certificates of deposit issued outside of the PRC

The index accounts for slightly over 10% of the ALBI-

China sector and 1% or the overall ALBI

Inception date: 31 December 2010

Inclusion criteria:

Fixed rate straight bonds and CDs (ie exclude synthetic bonds / floaters / bonds with embedded options)

At least one year remaining to maturity

Minimum outstanding amount: RMB500m

Institutional tranches only (ie exclude retail bonds)

As of May 2012Source: HSBC(1)

CNH is the name used in the market to refer to offshore deliverable RMB

Included in HSBC CNH index (51%)

Retail bonds (3%)

Floaters (exclude Retail) (1%)

Other (45%)

32

95

97

99

101

103

105

Jan-11 Apr-11 Jul-11 Oct-11 Jan-12 Apr-12

TR (UDS) TR (RMB) Capital Gain

CNH1

Index results

Source: HSBC, Data as of 10 May 2012(1)

CNH is the name used in the market to refer to offshore deliverable RMB

Tickers 12/31/2010 5/10/2012

Total Return in USD HCNHUSD 100.00 104.71

Total Return in RMB HCNHACUM 100.00 100.28

Avg Clean Price HCNHACP 100.00 96.50

Avg Duration (years) HCNHAD 3.00 2.74

Avg Yield (%) HCNHAY 2.28 4.28

Market Cap (RMBm) HCNHAMC 29,915 141,884

Avg Life (years) HCNHAL 3.23 3.01

Avg Coupon (%) HCNHAC 2.63 3.39

Return since inception

Total return in USD 4.71%

Total return in RMB 0.28%

Return from FX 4.43%

Return from capital gain -3.50%

Return from coupon 3.79%

Total return of CNH1

bonds in USD and RMB terms

Capital loss

FX

Coupon

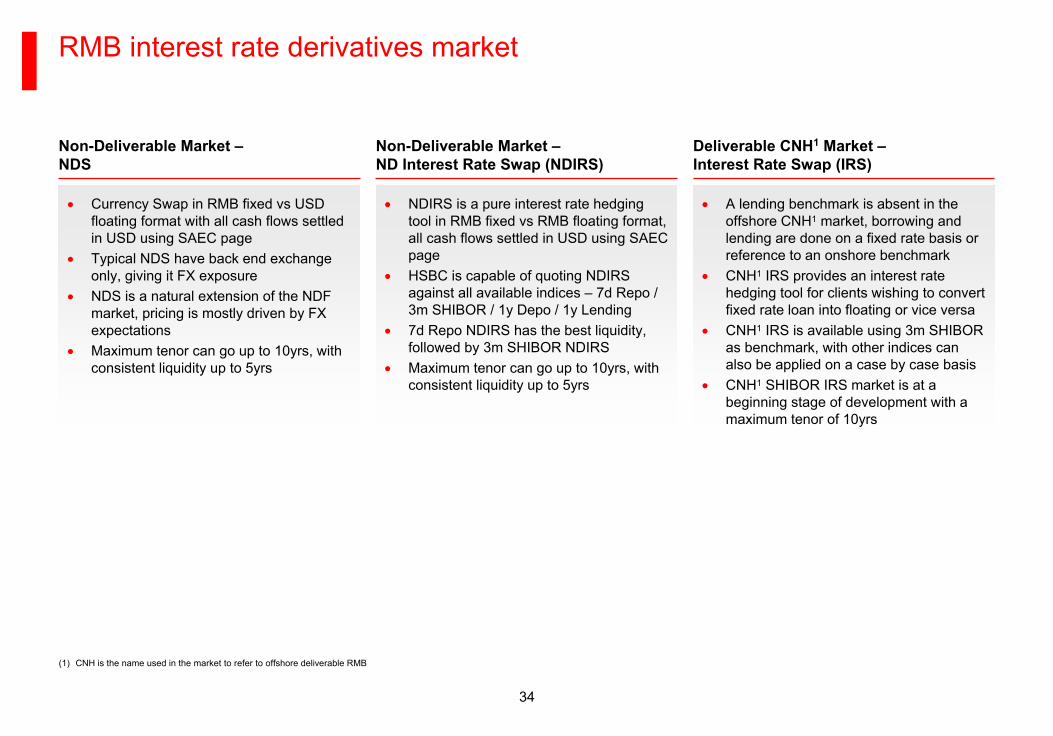

RMB Interest Rate Derivatives Market

34

A lending benchmark is absent in the offshore CNH1

market, borrowing and lending are done on a fixed rate basis or reference to an onshore benchmark

CNH1

IRS provides an interest rate hedging tool for clients wishing to convert fixed rate loan into floating or vice versa

CNH1

IRS is available using 3m SHIBOR as benchmark, with other indices can also be applied on a case by case basis

CNH1

SHIBOR IRS market is at a beginning stage of development with a maximum tenor of 10yrs

Currency Swap in RMB fixed vs USD floating format with all cash flows settled in USD using SAEC page

Typical NDS have back end exchange only, giving it FX exposure

NDS is a natural extension of the NDF market, pricing is mostly driven by FX expectations

Maximum tenor can go up to 10yrs, with consistent liquidity up to 5yrs

NDIRS is a pure interest rate hedging tool in RMB fixed vs RMB floating format, all cash flows settled in USD using SAEC page

HSBC is capable of quoting NDIRS against all available indices –

7d Repo / 3m SHIBOR / 1y Depo / 1y Lending

7d Repo NDIRS has the best liquidity, followed by 3m SHIBOR NDIRS

Maximum tenor can go up to 10yrs, with consistent liquidity up to 5yrs

RMB interest rate derivatives market

(1)

CNH is the name used in the market to refer to offshore deliverable RMB

Non-Deliverable Market –

NDS

Non-Deliverable Market –

ND Interest Rate Swap (NDIRS)

Deliverable CNH1

Market –

Interest Rate Swap (IRS)

35

Data as of 10 May 2012

Source: HSBC(1)

CNH is the name used in the market to refer to offshore deliverable RMB

Deliverable CNH1

Market –

USDCNH1

CCS curve

Currency Swap based on RMB fixed vs. USD float

format, with physical settlement of CNH1

vs

USD

USDCNH1

CCS have both front end and back end

exchange

The CCS market is an extension of the USDCNH1

FX Swap market, driven by interest rate differential and

the supply and demand of bond / loan hedging

activities

The USDCNH1

CCS market has experienced strong

growth since its inception in 2010, with monthly

turnover approaching USD 3bn, market is liquid up to

3yr, with a maximum possible tenor of 10yr with

reduced liquidity 1.50%

1.60%

1.70%

1.80%

1.90%

2.00%

2.10%

2.20%

2.30%

6M 9M 12M 18M 24M 30M 36M

USDCNH CCS

Offshore RMB Initial Public Offering (IPO)

37

Offshore RMB IPO

An RMB equity product refers to an equity product that is priced, traded and settled in RMB. Its price and dividends/distributions are denominated and paid in RMB

HSBC is one of the joint listing agents of the first RMB IPO listed on the main board of the Stock Exchange of Hong Kong in April 2011. Upon the listing of the first RMB IPO, most of the participants of an RMB IPO have their systems enhanced and are ready in dealing and / or clearing transactions in RMB securities in Hong Kong. In anticipation of RMB appreciation in the near future, higher demand for RMB equity products is expected

Superior distribution platform, consistently outselling in IPO transactions

Long standing track record of executing RMB denominated products

Lead bank who has pioneered the first RMB IPO

Capabilities to provide a total solution to both issuers and investors

Team of committed and highly experienced senior industry professionals

Introduction HSBC –

your partner of choice for RMB IPOs

HSBC RMB Capabilities and Credentials

39

HSBC trades GBP CNH3

structured forward with UK corporate client

First CNH3

dual currency investment offered to retail investors in Singapore

First FX index linked to CNH3

traded with European fund manager

Acted as joint listing agent for first offshore RMB IPO Hui Xian REIT

First CNH3

Multicallable Forward traded in the market

First CNH3

Dual Currency deposit traded in Japan

HSBC trades CNH3

FX option in Germany

Offshore RMB Products1 Onshore RMB Products (China)2

Payments and Cash Management

No restriction on account opening

No restriction on account opening

Custody

RMB Custody and Funds Administration Services

RMB Custody and ClearingExchange Services and Risk Management Products

Spot FX (for trade / general purposes)

Deliverable FX Forward, FX Option and FX Swap

Deliverable Interest Rate Swap, Cross Currency Swap and Interest Rate Swaptions

Non Deliverable Forward

Non Deliverable Option

Spot FX

Forward FX

FX swaps

Interest Rate Swap and Cross Currency Swap

Credit Risk Mitigation Agreement / Warrant

FX optionsBorrowing / Financing Products

Trade financing facilities and commercial loans

Issuance of offshore RMB bonds / certificate of deposits (CDs)

Trade financing facilities and commercial loans

Money MarketInvestment Products

Time deposit, CDs

Primary and secondary RMB bonds trading

FX linked structured deposit

Interest rate linked structured deposit

Equity linked structured deposit

Gold linked structured deposit

RMB investment funds

RMB equities

RMB RQFII funds

RMB gold ETF

Time deposit

Call deposit

Structured deposit

Bonds

Non-financial bonds

HSBC’s RMB capability

RMB ‘Going Out’

–

HSBC –

your bank of choice in international RMB business

(1)

Offshore RMB products currently available in HSBC Hong Kong. Products may vary in other regions(2)

There are certain restrictions on the types of clients to which the products can be offered(3)

CNH is the name used in the market to refer to offshore deliverable RMB

March 2011 March 2011 April 2011 June 2011 July 2011 Aug 2011 Nov 2011

40

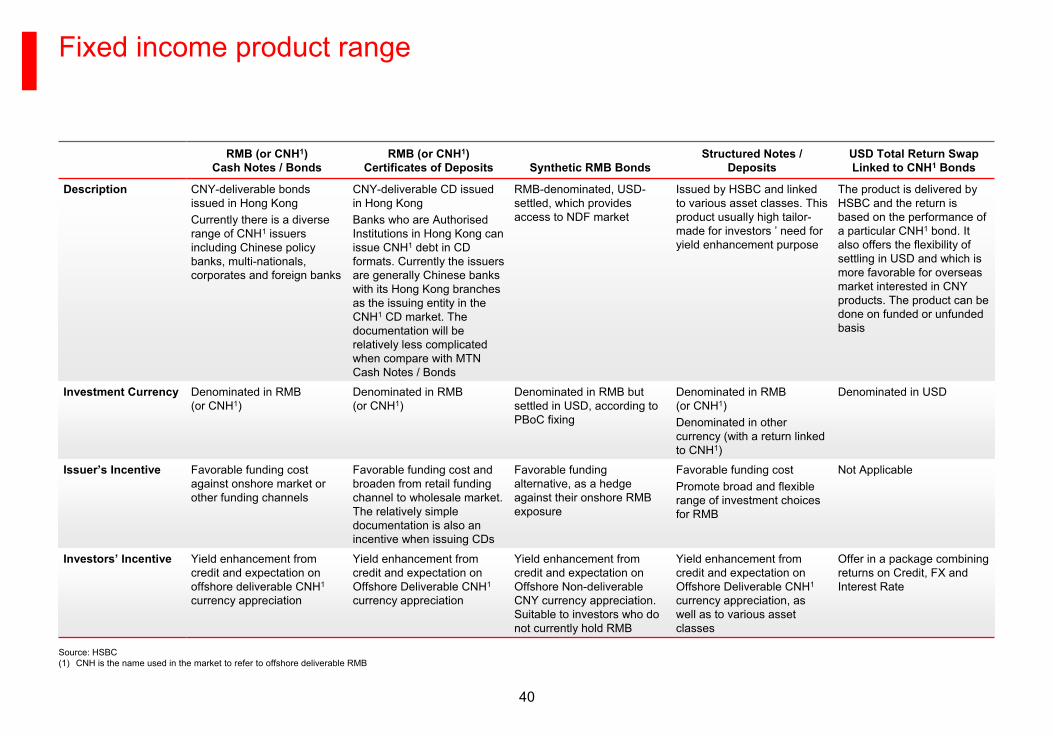

Fixed income product range

Source: HSBC(1)

CNH is the name used in the market to refer to offshore deliverable RMB

RMB (or CNH1) Cash Notes / Bonds

RMB (or CNH1) Certificates of Deposits Synthetic RMB Bonds

Structured Notes / Deposits

USD Total Return Swap Linked to CNH1

Bonds

Description CNY-deliverable bonds issued in Hong KongCurrently there is a diverse range of CNH1

issuers including Chinese policy banks, multi-nationals, corporates and foreign banks

CNY-deliverable CD issued in Hong KongBanks who are Authorised

Institutions in Hong Kong can issue CNH1

debt in CD formats. Currently the issuers are generally Chinese banks with its Hong Kong branches as the issuing entity in the CNH1

CD market. The documentation will be relatively less complicated when compare with MTN Cash Notes / Bonds

RMB-denominated, USD-

settled, which provides access to NDF market

Issued by HSBC and linked to various asset classes. This product usually high tailor-

made for investors ’

need for yield enhancement purpose

The product is delivered by HSBC and the return is based on the performance of a particular CNH1

bond. It also offers the flexibility of settling in USD and which is more favorable for overseas market interested in CNY products. The product can be done on funded or unfunded basis

Investment Currency Denominated in RMB (or CNH1)

Denominated in RMB (or CNH1)

Denominated in RMB but settled in USD, according to PBoC fixing

Denominated in RMB (or CNH1)Denominated in other currency (with a return linked to CNH1)

Denominated in USD

Issuer’s Incentive Favorable funding cost against onshore market or other funding channels

Favorable funding cost and broaden from retail funding channel to wholesale market. The relatively simple documentation is also an incentive when issuing CDs

Favorable funding alternative, as a hedge against their onshore RMB exposure

Favorable funding costPromote broad and flexible range of investment choices for RMB

Not Applicable

Investors’

Incentive Yield enhancement from credit and expectation on offshore deliverable CNH1

currency appreciation

Yield enhancement from credit and expectation on Offshore Deliverable CNH1

currency appreciation

Yield enhancement from credit and expectation on Offshore Non-deliverable CNY currency appreciation. Suitable to investors who do not currently hold RMB

Yield enhancement from credit and expectation on Offshore Deliverable CNH1

currency appreciation, as well as to various asset classes

Offer in a package combining returns on Credit, FX and Interest Rate

41

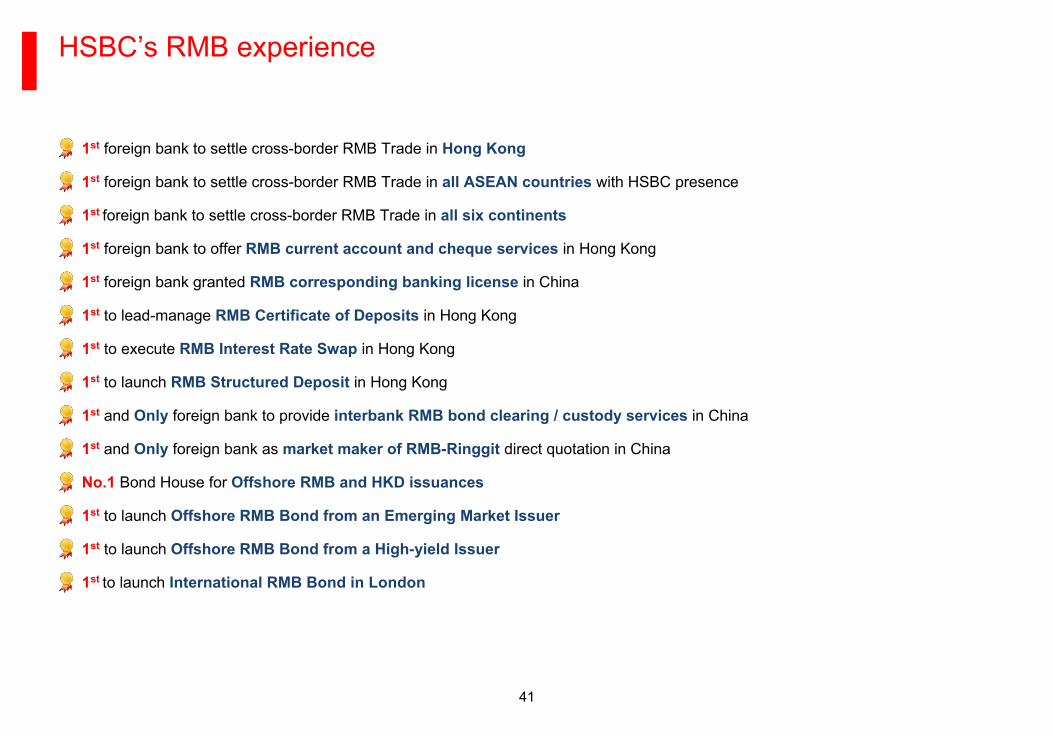

HSBC’s RMB experience

1st

foreign bank to settle cross-border RMB Trade in Hong Kong

1st

foreign bank to settle cross-border RMB Trade in all ASEAN countries

with HSBC presence

1st

foreign bank to settle cross-border RMB Trade in all six continents

1st

foreign bank to offer RMB current account and cheque services

in Hong Kong

1st

foreign bank granted RMB corresponding banking license

in China

1st

to lead-manage RMB Certificate of Deposits

in Hong Kong

1st

to execute RMB Interest Rate Swap

in Hong Kong

1st

to launch RMB Structured Deposit

in Hong Kong

1st

and Only

foreign bank to provide interbank RMB bond clearing / custody services

in China

1st

and Only

foreign bank as market maker of RMB-Ringgit

direct quotation in China

No.1

Bond House for Offshore RMB and HKD issuances

1st

to launch Offshore RMB Bond from an Emerging Market Issuer

1st

to launch Offshore RMB Bond from a High-yield Issuer

1st to launch International RMB Bond in London

42

HSBC made a clean sweep of all the major Asian regional Debt House awards for 2011,

across both G3 and local currency bonds

HSBC – Award-Winning #1 Bond House in Asia

Best Bookrunner

of Asia Pacific Bonds

Best Bookrunner

of G3 Bonds

2011

Bond House of the Year

Domestic Bond House of the Year

Dim Sum Bond House of the Year

2011

Best International Bond House

Best Local Currency Bond House

Best Sovereign Bond House

Best Offshore RMB Bond House2011

Best Debt Arranger

Best Loans Arranger

2011

Best Debt House in Asia

2011

Best Debt House

Best Bond House

Best Dim Sum Bond House

Best Loan House

2011

“HSBC’s G3 tally was a record, both in terms of volume and of issues… All told, the bank’s consistent performance across every cross-section of Asia’s international bond markets represented as close to complete market domination as anyone is ever likely

to get”IFRAsia

“HSBC took a near clean sweep of the awards this year thanks to its unprecedented dominance in both the G3 and local currency markets...”

FinanceAsia

“HSBC was clearly the best performer in Asia ex-Japan in terms of volumes and deals completed...the sheer depth and diversity of the deals HSBC played a role in, far outweighs its competitors in the space”

Asiamoney

“HSBC’s debt franchise cuts across G3, local currency, loans and securitisation

to become once more the go-to bank for debt deals ...... it reached out to Asian issuers across the region arranging some of the year’s landmark deals”

The Asset

43

CNH Bond League Table (2012YTD) HSBC executed ground-breaking transactions

Source: Bloomberg as of 7

May

2012

CNH Bonds

Bank CNYm Issues %

1 HSBC 17,553 54 29.1

2 Standard Chartered 7,464 28 12.4

3 Bank of China 6,743 8 11.2

4 Barclays 5,411 17 9.0

5 RBS 4,191 14 6.9

6 BNP Paribas 3,367 10 5.6

7 Deutsche Bank 3,299 13 5.5

8 ANZ 2,370 15 3.9

9 UBS 2,166 6 3.6

10 Citi 1,323 6 2.2

Total 60,381 165

March 2012

Ford Motor Company

RMB1bn Fixed Rate Notes due 2015

Joint Lead Manager and Bookrunner

March 2012

Ford Motor Company

RMB1bn Fixed Rate Notes due 2015

Joint Lead Manager and Bookrunner

March 2012

Alstom

RMB500m Fixed Rate Notes due 2015

Sole Lead Manager and Bookrunner

March 2012

Alstom

RMB500m Fixed Rate Notes due 2015

Sole Lead Manager and Bookrunner

February 2012

Mitsui & Co., Ltd.

RMB500m Fixed Rate Notes due 2017

Sole Lead Manager and Bookrunner

February 2012

Mitsui & Co., Ltd.

RMB500m Fixed Rate Notes due 2017

Sole Lead Manager and Bookrunner

March 2012

Emirates NBD

RMB750m Fixed Rate Notes due 2015

Joint Lead Manager and Bookrunner

March 2012

Emirates NBD

RMB750m Fixed Rate Notes due 2015

Joint Lead Manager and Bookrunner

February 2012

Lotte

Shopping

RM750mn due 2015Fixed Rates Notes

Joint Lead Manager and Bookrunner

February 2012

Lotte

Shopping

RM750mn due 2015Fixed Rates Notes

Joint Lead Manager and Bookrunner

November 2011

Baosteel

Group Corporation

RM1bn due 2013RMB2.1bn due 2014RMB500mn due 2016

Fixed Rates Notes

Joint Global Coordinator, Sole Rating Advisor, Joint Lead Manager and Bookrunner

November 2011

Baosteel

Group CorporationRM1bn due 2013RMB2.1bn due 2014RMB500mn due 2016

Fixed Rates NotesJoint Global Coordinator, Sole Rating Advisor, Joint Lead Manager and Bookrunner

September 2011

BSH Bosch & SiemensRMB850mn due 2014

RMB750mn due 2016 RMB400mn due 2018

Fixed Rates Notes

Joint Lead Manager and Bookrunner

September 2011

BSH Bosch & SiemensRMB850mn due 2014

RMB750mn due 2016 RMB400mn due 2018

Fixed Rates NotesJoint Lead Manager and Bookrunner

February 2012

America Movil

RM1bn due 2015Fixed Rates Notes

Sole Lead Manager and Bookrunner

February 2012

America Movil

RM1bn due 2015Fixed Rates Notes

Sole Lead Manager and Bookrunner

September 2011

Air Liquide

FinanceRMB1.75bnFixed Rate Notes due 2016RMB850mnFixed Rate Notes due 2018Joint Lead Manager and Bookrunner

September 2011

Air Liquide

FinanceRMB1.75bnFixed Rate Notes due 2016RMB850mnFixed Rate Notes due 2018Joint Lead Manager and Bookrunner

August 2011

Tesco PLC

RMB725mnFixed Rate Notes due 2014

Joint Lead Manager and Bookrunner

August 2011

Tesco PLC

RMB725mnFixed Rate Notes due 2014

Joint Lead Manager and Bookrunner

June 2011

Fonterra Co-operative Group Limited

RMB300mn Fixed Rate Notes due 2014

Sole Lead Manager and Bookrunner

June 2011

Fonterra Co-operative Group LimitedRMB300mn Fixed Rate Notes due 2014

Sole Lead Manager and Bookrunner

September 2011

BP Capital Markets PLC

RMB700mnFixed Rate Notes due 2014

Joint Lead Manager and Bookrunner

September 2011

BP Capital Markets PLC

RMB700mnFixed Rate Notes due 2014

Joint Lead Manager and Bookrunner

May 2011

Volkswagen

RMB1.5bnFixed Rate Notes due 2016

Joint Lead Manager and Bookrunner

May 2011

Volkswagen

RMB1.5bnFixed Rate Notes due 2016

Joint Lead Manager and Bookrunner

January 2011

International Finance Corporation

RMB150m Fixed Rate Notes due 2016

Sole Lead Manager and Bookrunner

January 2011

International Finance CorporationRMB150m Fixed Rate Notes due 2016

Sole Lead Manager and Bookrunner

January 2011

World Bank

RMB300m Fixed Rate Notes due 2013

Sole Lead Manager and Bookrunner

January 2011

World Bank

RMB300m Fixed Rate Notes due 2013

Sole Lead Manager and Bookrunner

March 2011

Unilever N.V.

RMB300m Fixed Rate Notes due 2014

Joint Lead Manager and Bookrunner

March 2011

Unilever N.V.

RMB300m Fixed Rate Notes due 2014

Joint Lead Manager and Bookrunner

HSBC – Undisputed Leader in the Dim Sum Bond Market

44

Of the 20 Multinational Corporations (“MNCs”)

which have accessed the Dim Sum bond market since 2011, HSBC was

Bookrunner on transactions from 18 issuers

HSBC’s unrivalled knowledge on the

repatriation of funds onshore and our universal distribution platform mean issuers can rely on a “safe pair of hands”

during their maiden CNH bond issue

HSBC MNC Credentials

March 2012

Raiffeisen

Bank International

RMB750mn Fixed Rate Notes due 2014Joint Lead Manager and Bookrunner

March 2012

Raiffeisen

Bank International

RMB750mn Fixed Rate Notes due 2014Joint Lead Manager and Bookrunner

February 2012

Mitsui & Co., Ltd.

RMB500m Fixed Rate Notes due 2017

Sole Lead Manager and Bookrunner

February 2012

Mitsui & Co., Ltd.

RMB500m Fixed Rate Notes due 2017

Sole Lead Manager and Bookrunner

September 2011

BSH Bosch & SiemensRMB850mn due 2014

RMB750mn due 2016 RMB400mn due 2018

Fixed Rates Notes

Joint Lead Manager and Bookrunner

September 2011

BSH Bosch & SiemensRMB850mn due 2014

RMB750mn due 2016 RMB400mn due 2018

Fixed Rates NotesJoint Lead Manager and Bookrunner

June 2011

Fonterra Co-operative Group Limited

RMB300mn Fixed Rate Notes due 2014

Sole Lead Manager and Bookrunner

June 2011

Fonterra Co-operative Group LimitedRMB300mn Fixed Rate Notes due 2014

Sole Lead Manager and Bookrunner

March 2012

Hitachi Capital Corporation

RMB500mn Fixed Rate Notes due 2015Sole Lead Manager and Bookrunner

March 2012

Hitachi Capital Corporation

RMB500mn Fixed Rate Notes due 2015Sole Lead Manager and Bookrunner

February 2012

Lotte

Shopping

RM750mn due 2015Fixed Rates Notes

Joint Lead Manager and Bookrunner

February 2012

Lotte

Shopping

RM750mn due 2015Fixed Rates Notes

Joint Lead Manager and Bookrunner

September 2011

Yum! Brands, Inc

RMB350mn Fixed Rate Notes due 2014

Joint Lead Manager and Bookrunner

September 2011

Yum! Brands, Inc

RMB350mn Fixed Rate Notes due 2014

Joint Lead Manager and Bookrunner

May 2011

Volkswagen

RMB1.5bnFixed Rate Notes due 2016

Joint Lead Manager and Bookrunner

May 2011

Volkswagen

RMB1.5bnFixed Rate Notes due 2016

Joint Lead Manager and Bookrunner

March 2012

Ford Motor Company

RMB1bn Fixed Rate Notes due 2015

Joint Lead Manager and Bookrunner

March 2012

Ford Motor Company

RMB1bn Fixed Rate Notes due 2015

Joint Lead Manager and Bookrunner

February 2012

America Movil

RM1bn due 2015Fixed Rates Notes

Sole Lead Manager and Bookrunner

February 2012

America Movil

RM1bn due 2015Fixed Rates Notes

Sole Lead Manager and Bookrunner

September 2011

Air Liquide

FinanceRMB1.75bnFixed Rate Notes due 2016

RMB850mn

Fixed Rate Notes due 2018Joint Lead Manager and Bookrunner

September 2011

Air Liquide

FinanceRMB1.75bnFixed Rate Notes due 2016

RMB850mnFixed Rate Notes due 2018Joint Lead Manager and Bookrunner

March 2011

Unilever N.V.

RMB300m Fixed Rate Notes due 2014

Joint Lead Manager and Bookrunner

March 2011

Unilever N.V.

RMB300m Fixed Rate Notes due 2014

Joint Lead Manager and Bookrunner

March 2012

Emirates NBD

RMB750m Fixed Rate Notes due 2015

Joint Lead Manager and Bookrunner

March 2012

Emirates NBD

RMB750m Fixed Rate Notes due 2015

Joint Lead Manager and Bookrunner

November 2011

IDBI Bank Limited

RMB650mn due 2014Fixed Rates Notes

Sole Lead Manager and Bookrunner

November 2011

IDBI Bank Limited

RMB650mn due 2014Fixed Rates Notes

Sole Lead Manager and Bookrunner

September 2011

BP Capital Markets PLC

RMB700mnFixed Rate Notes due 2014

Joint Lead Manager and Bookrunner

September 2011

BP Capital Markets PLC

RMB700mnFixed Rate Notes due 2014

Joint Lead Manager and Bookrunner

August 2011

Tesco PLC

RMB725mnFixed Rate Notes due 2014

Joint Lead Manager and Bookrunner

August 2011

Tesco PLC

RMB725mnFixed Rate Notes due 2014

Joint Lead Manager and Bookrunner

March 2012

Alstom

RMB500m Fixed Rate Notes due 2015

Sole Lead Manager and Bookrunner

March 2012

Alstom

RMB500m Fixed Rate Notes due 2015

Sole Lead Manager and Bookrunner

November 2011

Lafarge Shui

On Cement

RMB1.5bn due 2014Fixed Rates Notes

Joint Lead Manager and Bookrunner

November 2011

Lafarge Shui

On Cement

RMB1.5bn due 2014Fixed Rates Notes

Joint Lead Manager and Bookrunner

Many firsts for HSBC

45

HSBC continued to re-define the Dim Sum Bond market landscape by executing ground-breaking transactions

First Dim Sum Bond from an emerging market issuer

First Dim Sum Bond issue in 2011 and from the World Bank

First PRC Property Developer and first H-share company to tap the Dim Sum Market

First Dim Sum Bond by a European corporate

First Dim Sum Bond from a public wind energy issuer

First Dim Sum Bond from a Hong Kong blue chip corporate

First Dim Sum Bond from a German corporate and first international Auto Dim Sum Bond

First Dim Sum Bond issued by an insurance company

First Dim Sum Bond issued from

an Australasian corporate

First Dim Sum Bond issued from an International Retailer

Largest Dim Sum Bond by a Western Corporate and largest 7 year offshore RMB Bond ever

First Triple Tranche Deal Priced in a single day

First Dim Sum Bond by a PRC Incorporated Corporate Issuer

First Dim Sum Bond by a Latin American Issuer and in Sec Registered Format

First Dim Sum Bond Issuance From Mena Region

First International RMB Bond

VTB BankRMB1bn Fixed Rate notes due 2013

World BankRMB500m Fixed Rate notes due 2013

Beijing Capital LandRMB1.15bn Fixed Rate notes due 2014

UnileverRMB300m Fixed Rate notes due 2014

China WindPowerRMB750m Fixed Rate notes due 2014

TowngasRMB1bn Fixed Rate notes due 2016

VolkswagenRMB1.5bn Fixed Rate notes due 2016

China Ping An Insurance Overseas (Holdings) Limited RMB2bn Fixed Rate notes due 2014

Fonterra Co-Operative GroupRMB600m Fixed Rate notes due 2014

Tesco plc

RMB725m Fixed Rate notes due 2014

Air Liquide

Finance

RMB1.75bn Fixed Rate notes due 2016,

RMB850m Fixed Rate notes due 2018

BSH Bosch & Siemens RMB2bn triple tranche Fixed Rate Note

Baosteel

Group CorporationRMB3.6bn triple tranche Fixed Rate Note

America MovilRMB1bn Fixed Rate Note

Emirates NBDRMB750m Fixed Rate Note

HSBC Bank plcRMB2bn Fixed Rate Note

Dec

2010

Jan

2011

Feb 2011

Mar 2011

Mar 2011

Mar 2011

May2011

May2011

Jun 2011

Aug 2011

Sep 2011

Sep 2011

Nov

2011

Feb

2012

Mar

2012

Apr

2012

Groundbreaking Dim Sum Bond Transactions

46

Disclaimer

Renminbi (RMB) is currently not freely convertible and conversion of RMB through banks in Hong Kong is subject to certain restrictions. Clients should be reminded of conversion risk in RMB products. In addition, there is a liquidity risk associated with RMB products, especially if such investments do not have an active secondary market and their prices have large bid/offer spreads. RMB products in Hong Kong are denominated and settled in RMB deliverable in Hong Kong, which represents a

market which is different from that from that of RMB deliverable

in Mainland China. For individual clients, conversion of RMB is

subject to daily limit in Hong Kong, the clients may have to allow time for conversion of RMB from/to

another currency of an amount exceeding the daily limit.

This document is issued by The Hongkong and Shanghai Banking Corporation Limited (HSBC). The information contained herein is derived from sources we believe to be reliable, but which we have not independently verified. HSBC makes no representation or warranty (express or implied) of any nature nor is any responsibility of any kind accepted with respect to the completeness or accuracy of any information, projection, representation or warranty (expressed or implied) in, or omission

from, this document. No liability is accepted whatsoever for any

direct, indirect or consequential loss arising from the use of this document. Any examples given are for the purposes of illustration only. The opinions in this document constitute our present judgement, which is subject to change without notice. This document does

not constitute an offer or solicitation for, or advice that you should enter into, the purchase or sale of any security, commodity or other investment product or investment agreement, or any other contract, agreement or structure whatsoever and is intended for institutional customers and is not intended for the use of private customers. The document is intended to be distributed in its entirety. No consideration has been given to the particular investment objectives, financial situation or particular needs of any recipient. Unless governing law permits otherwise, you must contact a HSBC Group member in your home jurisdiction if you wish to use

HSBC Group services in effecting a transaction in any investment

mentioned in this document. This document, which is not for public circulation, must not be copied, transferred or the content disclosed, to any third party and is not intended for use by any person other than the intended recipient or the intended recipient's

professional advisers for the purposes of advising the intended recipient hereon.

Copyright. The Hongkong and Shanghai Banking Corporation Limited

2006. ALL RIGHTS RESERVED. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of

The Hongkong and Shanghai Banking Corporation Limited.