Risk assessments of retail investment products in hong kong and mainland china

67

1 RZ130 Risk assessments of retail investment products in Hong Kong and mainland China 3 IFPHK CE credits 3 SFC CPT hours 3 MPFA non-core CPD hours Speaker: Dr. LAM Yat Fai (林日辉 博士) Doctor of Business Administration (Finance) CFA CAIA FRM PRM MCSE MCNE 6:30pm to 9:30pm Friday 19 th July 2013

-

Upload

quan-risk -

Category

Economy & Finance

-

view

40 -

download

0

Transcript of Risk assessments of retail investment products in hong kong and mainland china

1

RZ130 Risk assessments of retail investment

products in Hong Kong and mainland China

3 IFPHK CE credits3 SFC CPT hours

3 MPFA non-core CPD hours

Speaker: Dr. LAM Yat Fai (林日辉 博士)Doctor of Business Administration (Finance)CFA CAIA FRM PRM MCSE MCNE

6:30pm to 9:30pm Friday 19th July 2013

2

Outline

Suitability of investment products

Major investment products

Qualitative risk assessment

Quantitative risk assessment

Practical issues

Private banking and corporate banking

3

What is this investment product?

Excellent investment product

High return

Low risk

Huge growth potential

Very stable income

As reliable as deposits

4

What is this investment product?

Very popular investment product

Mr. LAM acquired HK$ 100,000 yesterday

Mrs. LEE further brought HK$ 500,000 this

morning

Subscription to be closed by this end of

today

Limited offer to very few VIPs like you

5

What is this investment product?

Today the market is going up

The price will be more expensive

tomorrow

6

What is this investment product?

Today the market is going down

The price is very attractive today

7

Sure win selling strategy

HK$ 100 Parknshop gift coupon for every

HK$ 100,000 subscription

8

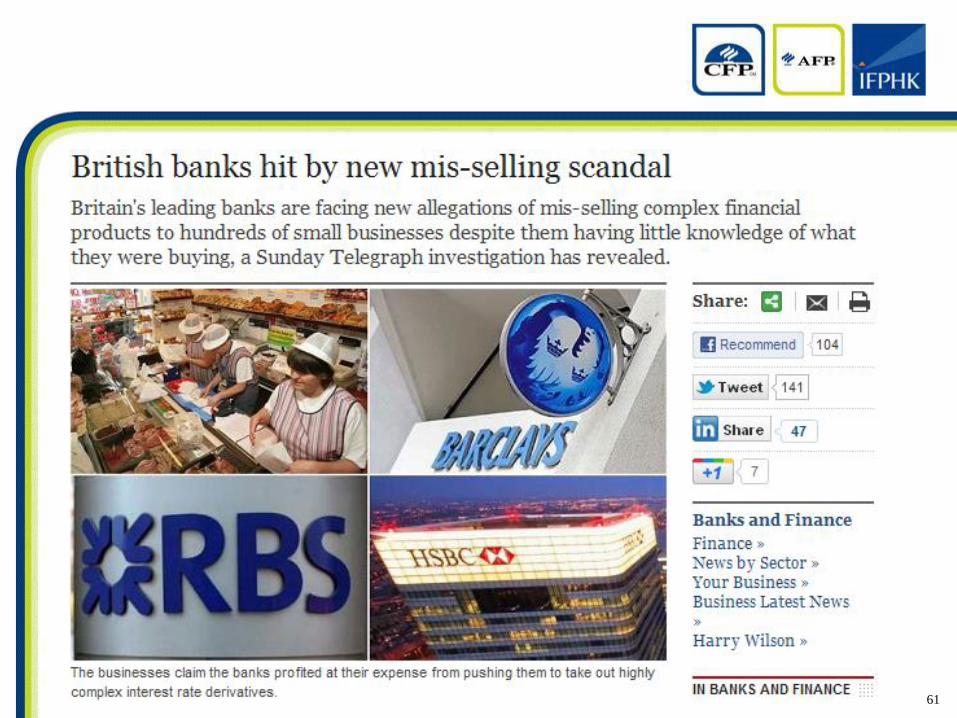

Very familiar conversions

9

Whom are you talking to?

10

Whom are you talking to?

11

Lehman Brothers minibonds

12

13

Supervisory framework

Zoning

No gift

Audio recording

Code of conducts

Investor education

Key fact sheet

Suitability assessment

and many more

14

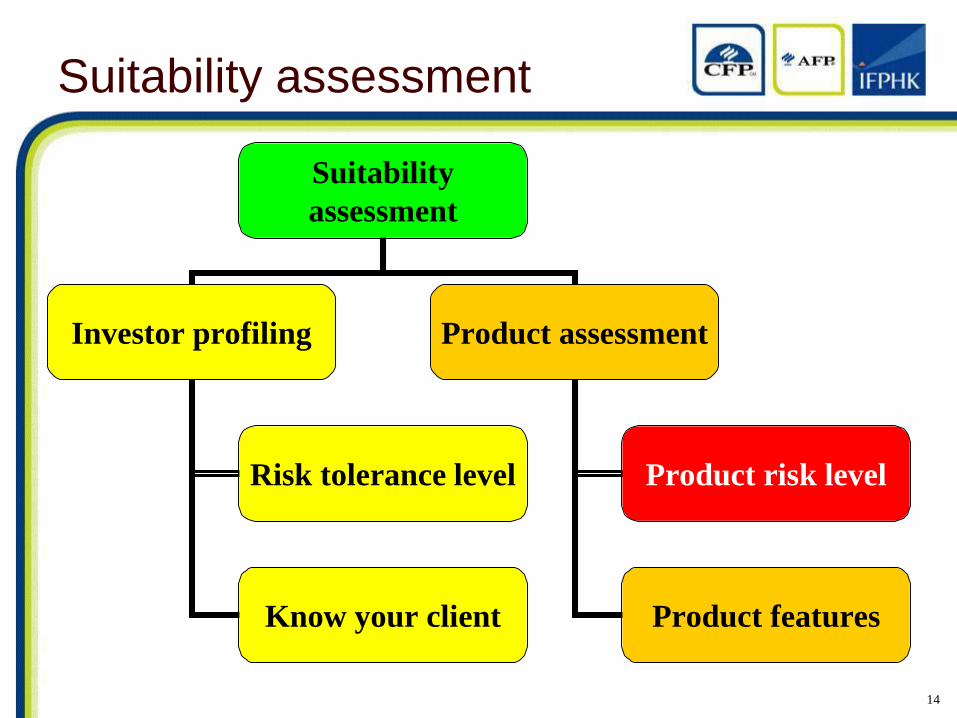

Suitability assessment

Suitability

assessment

Investor profiling Product assessment

Product risk level

Product features

Risk tolerance level

Know your client

15

Outline

Suitability of investment products

Major investment products

Qualitative risk assessment

Quantitative risk assessment

Practical issues

Private banking and corporate banking

16

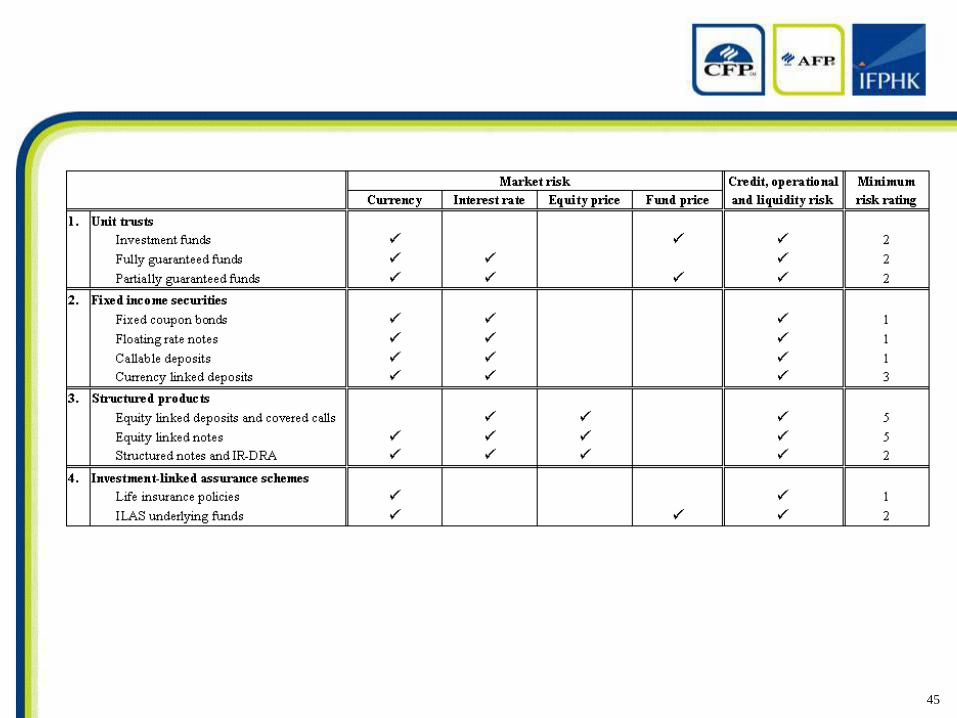

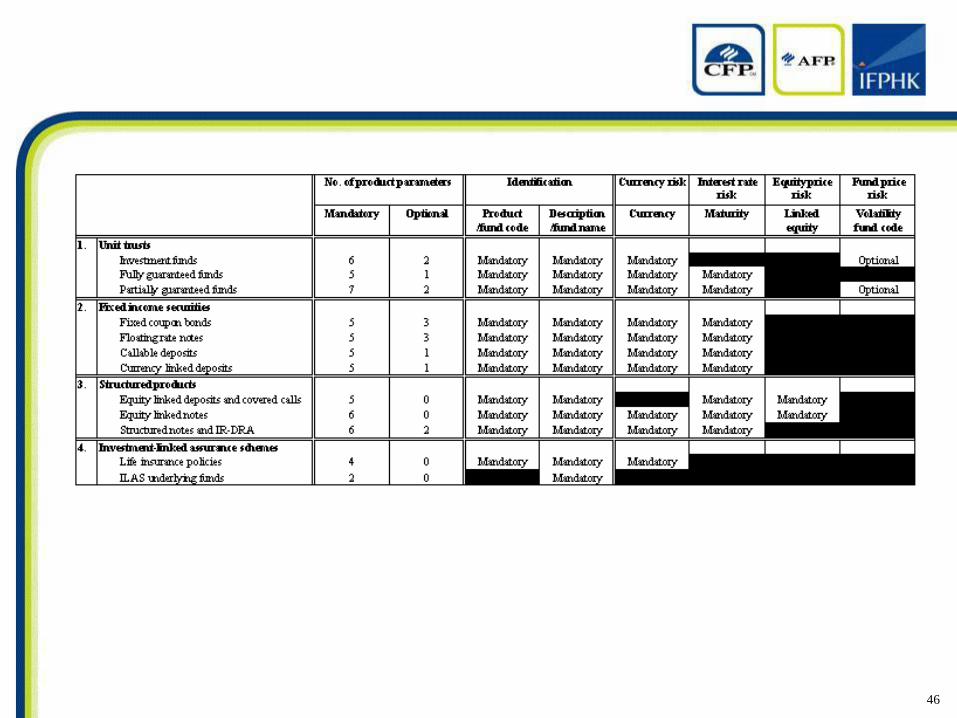

Common investment

products in Hong Kong

Retail

Investment funds

Hedge funds

Bonds

Structured notes

Principal protected notes

Currency linked deposits

Equity linked deposits

Insurance linked investment schemes

17

Common investment

products in Hong Kong

Private banking and corporate banking

Accumulator

Decumulator

Target redemption

Pivot

Currency linked notes with multiple

underlying and fixing

18

Investment products in China

Private placement lending

Asset backed securities

19

20

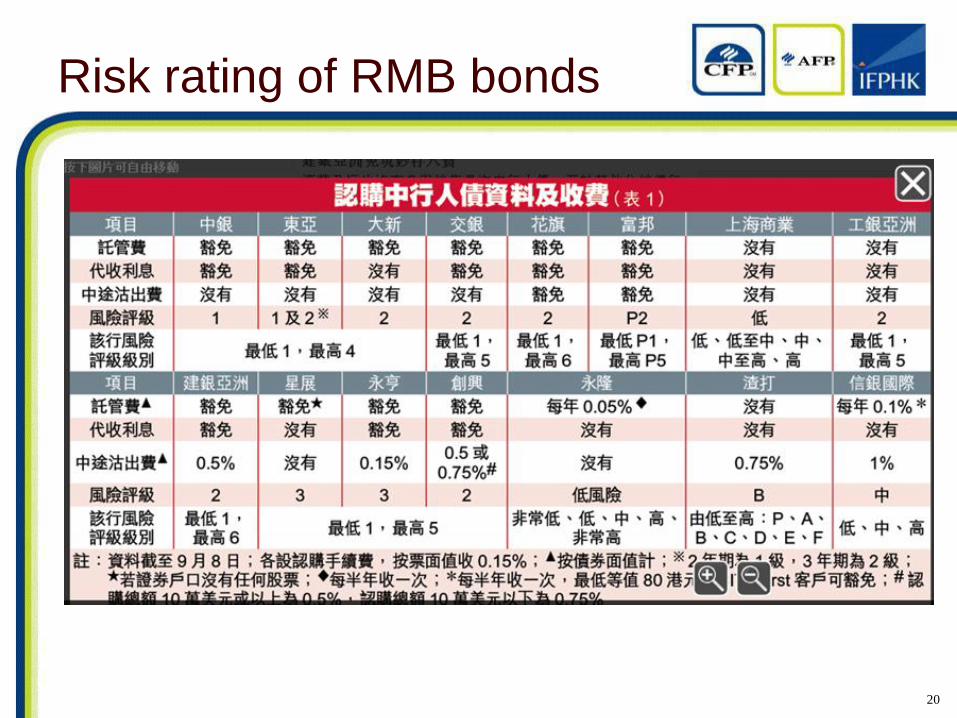

Risk rating of RMB bonds

21

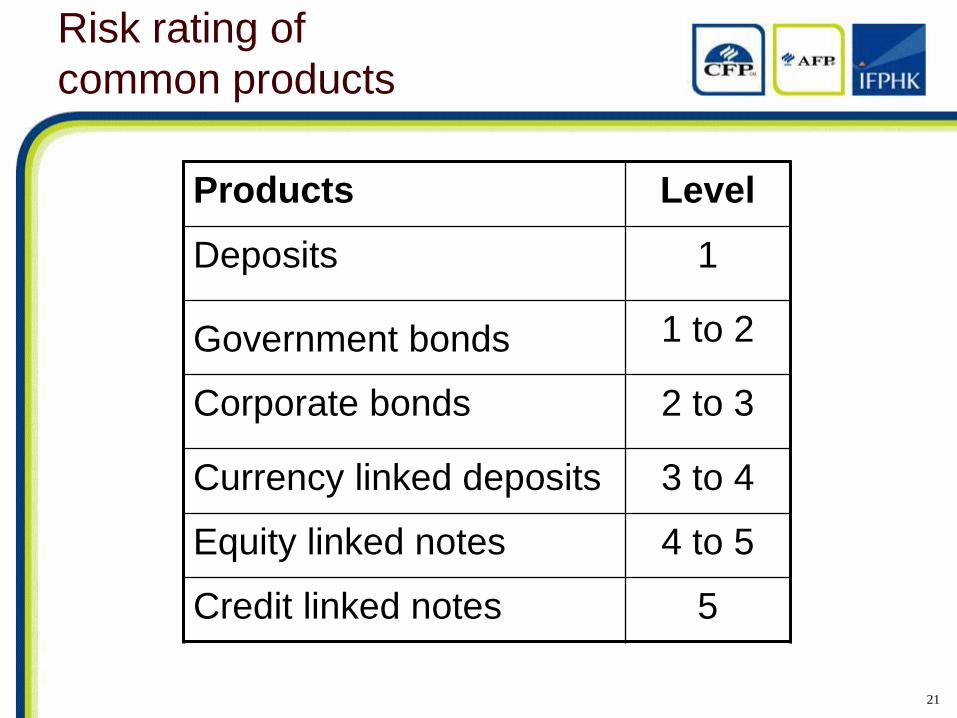

Risk rating of

common products

Products Level

Deposits 1

Government bonds 1 to 2

Corporate bonds 2 to 3

Currency linked deposits 3 to 4

Equity linked notes 4 to 5

Credit linked notes 5

22

Outline

Suitability of investment products

Major investment products

Qualitative risk assessment

Quantitative risk assessment

Practical issues

Private banking and corporate banking

23

Product risk assessment

Qualitative

Expert judgment

Subjective

Time consuming

Less consistent

Very flexible

Quantitative

Model based

Objective

Automated

Consistent

Less flexible

24

Regulatory risk factors

SFC’s key facts statement

http://www.sfc.hk/web/EN/regulatory-

functions/products/product-

authorization/products-key-facts-

statements.html

HKMA’s important facts statement

http://www.hkma.gov.hk/media/eng/doc/key-

information/guidelines-and-

circular/2011/20110418e1.pdf

25

Descriptive report

Many lengthy paragraphs

broken down by risk type

to conclude a risk rating

Several pages to several lines

Very similar reports among similar

investment products

26

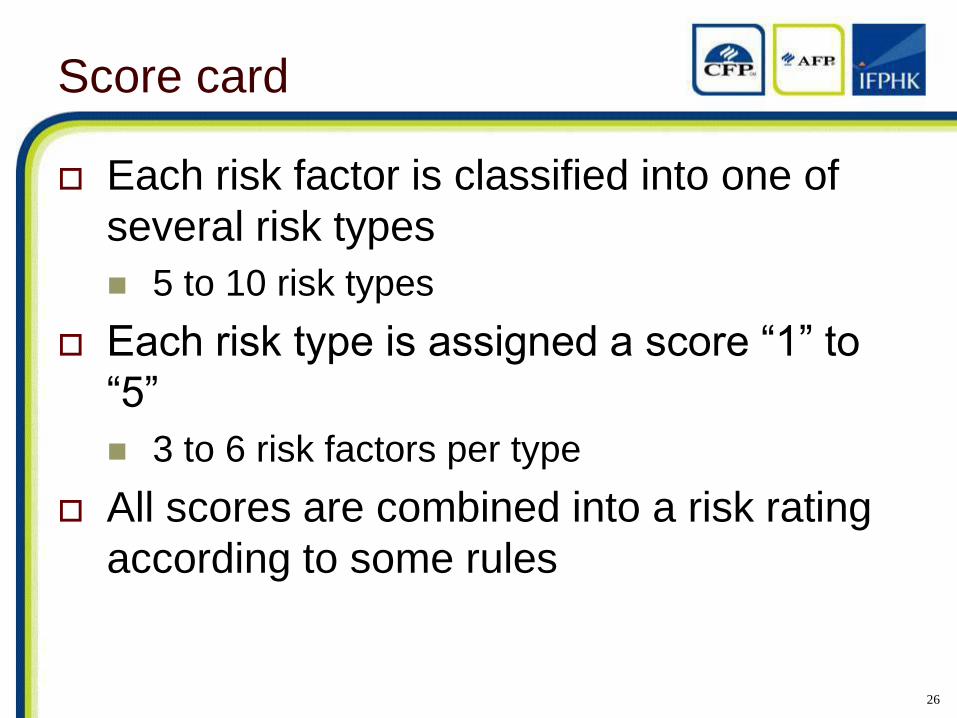

Score card

Each risk factor is classified into one of

several risk types

5 to 10 risk types

Each risk type is assigned a score “1” to

“5”

3 to 6 risk factors per type

All scores are combined into a risk rating

according to some rules

27

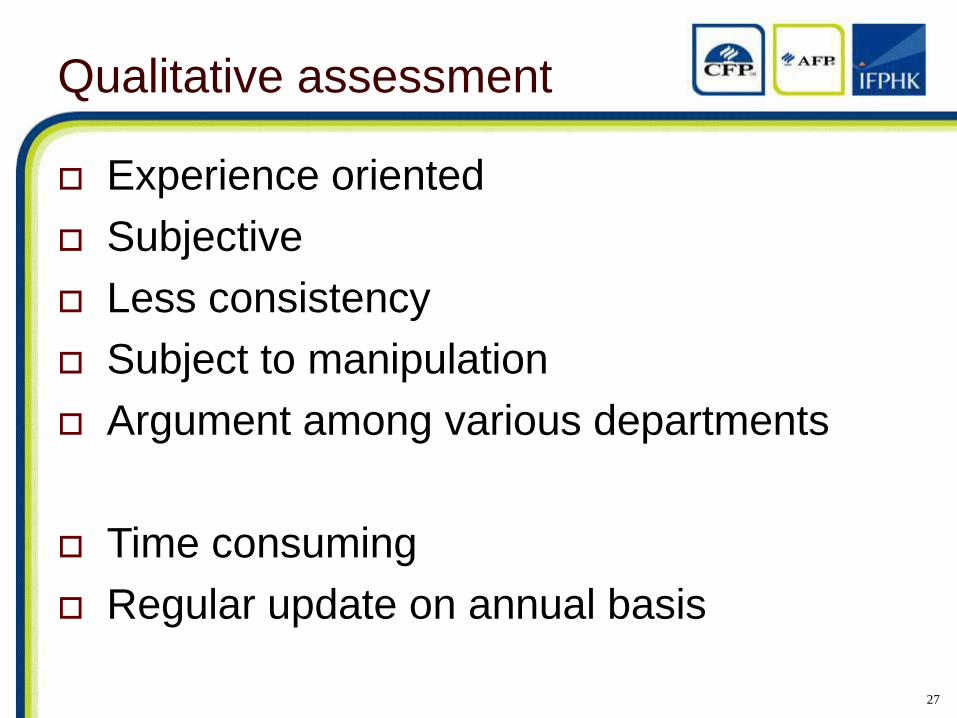

Qualitative assessment

Experience oriented

Subjective

Less consistency

Subject to manipulation

Argument among various departments

Time consuming

Regular update on annual basis

28

Outline

Suitability of investment products

Major investment products

Qualitative risk assessment

Quantitative risk assessment

Practical issues

Private banking and corporate banking

29

Basel III framework

Market risk Currency rate

Interest rate

Equity price

Commodity price

Credit risk

Operational risk

Liquidity risk

Reputation risk

Legal risk

Strategic risk

30

Assumptions

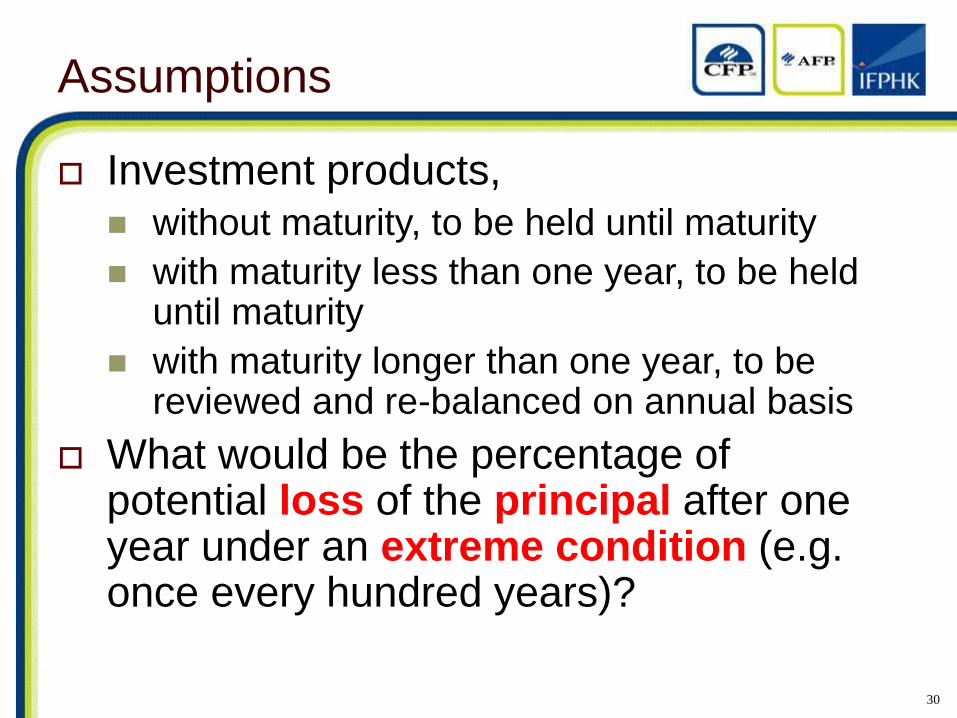

Investment products,

without maturity, to be held until maturity

with maturity less than one year, to be held until maturity

with maturity longer than one year, to be reviewed and re-balanced on annual basis

What would be the percentage of potential loss of the principal after one year under an extreme condition (e.g. once every hundred years)?

31

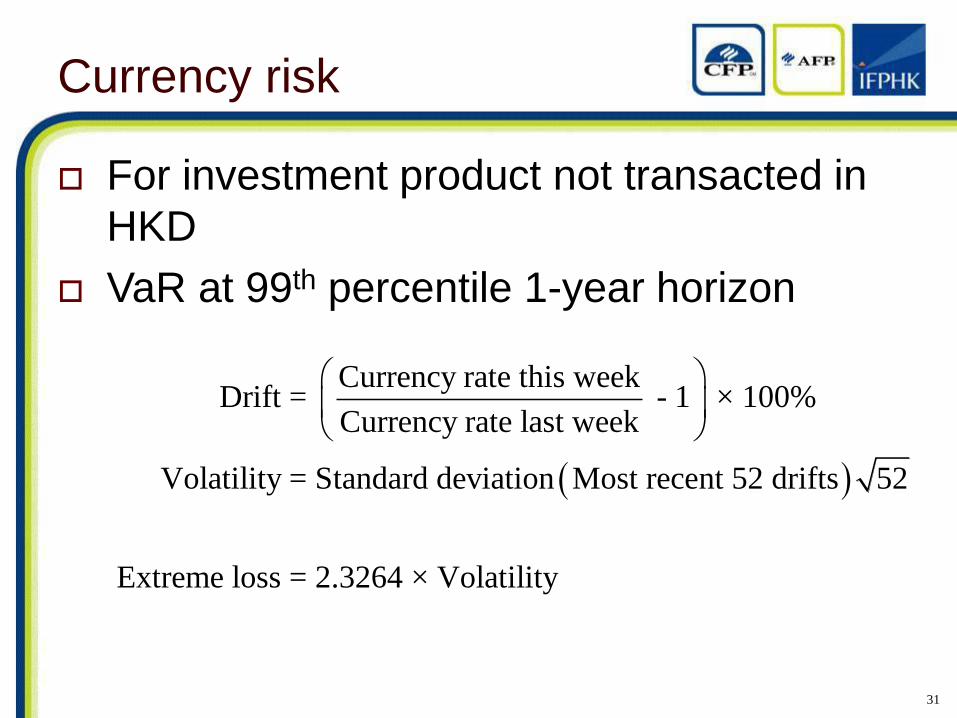

Currency risk

For investment product not transacted in

HKD

VaR at 99th percentile 1-year horizon

Currency rate this weekDrift = - 1 × 100%

Currency rate last week

Volatility = Standard deviation Most recent 52 drifts 52

Extreme loss = 2.3264 × Volatility

32

Annualized drift

at 99th percentile

-2.3264

volatility

99%

33

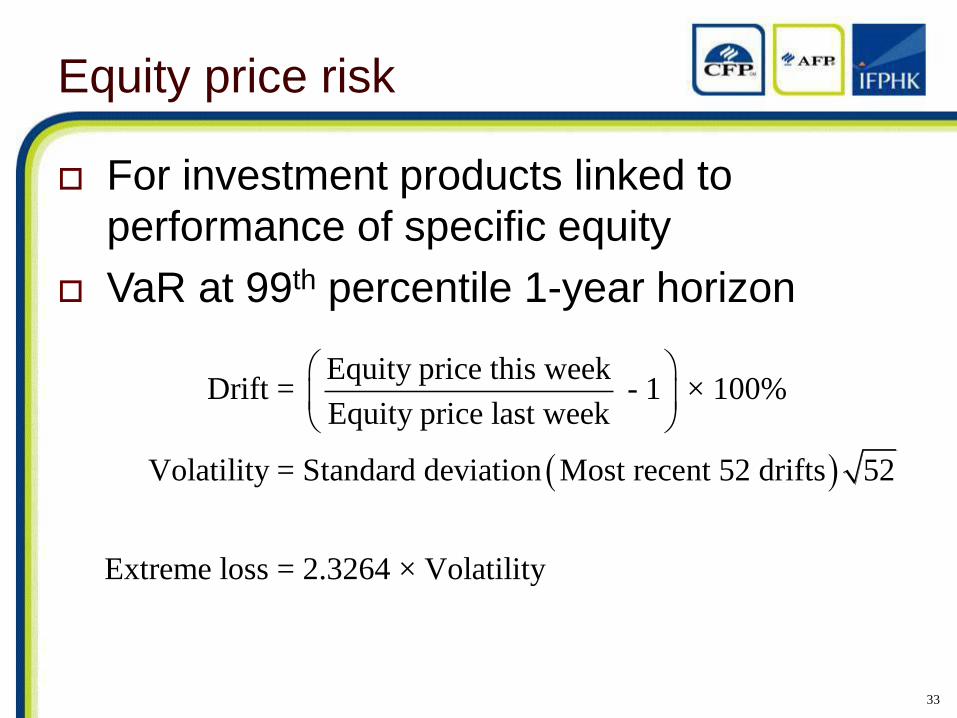

Equity price risk

For investment products linked to

performance of specific equity

VaR at 99th percentile 1-year horizon

Equity price this weekDrift = - 1 × 100%

Equity price last week

Volatility = Standard deviation Most recent 52 drifts 52

Extreme loss = 2.3264 × Volatility

34

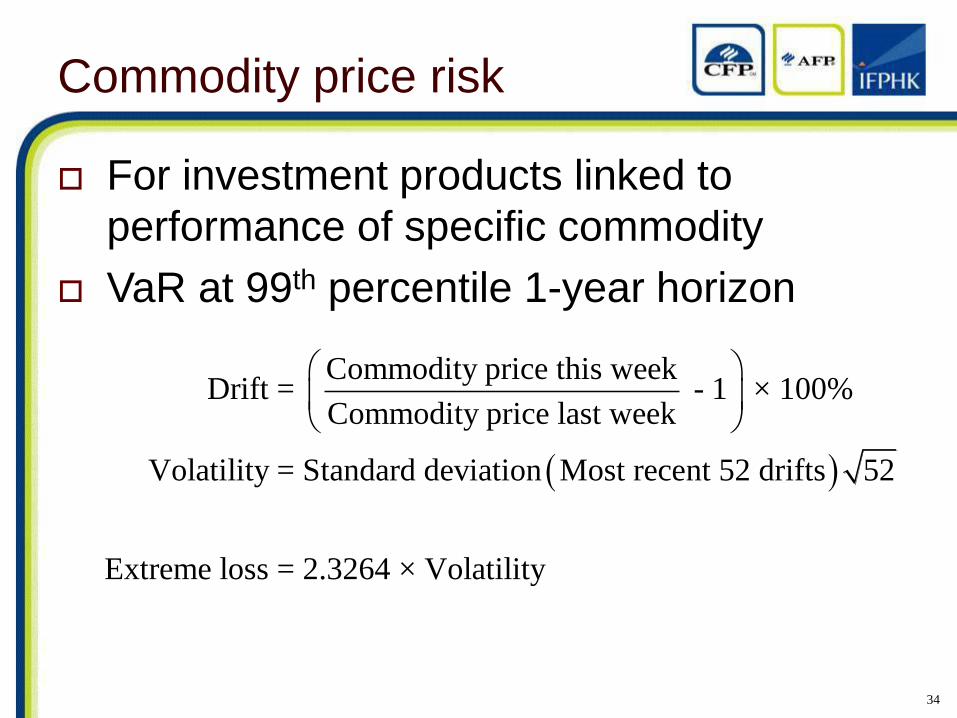

Commodity price risk

For investment products linked to

performance of specific commodity

VaR at 99th percentile 1-year horizon

Commodity price this weekDrift = - 1 × 100%

Commodity price last week

Volatility = Standard deviation Most recent 52 drifts 52

Extreme loss = 2.3264 × Volatility

35

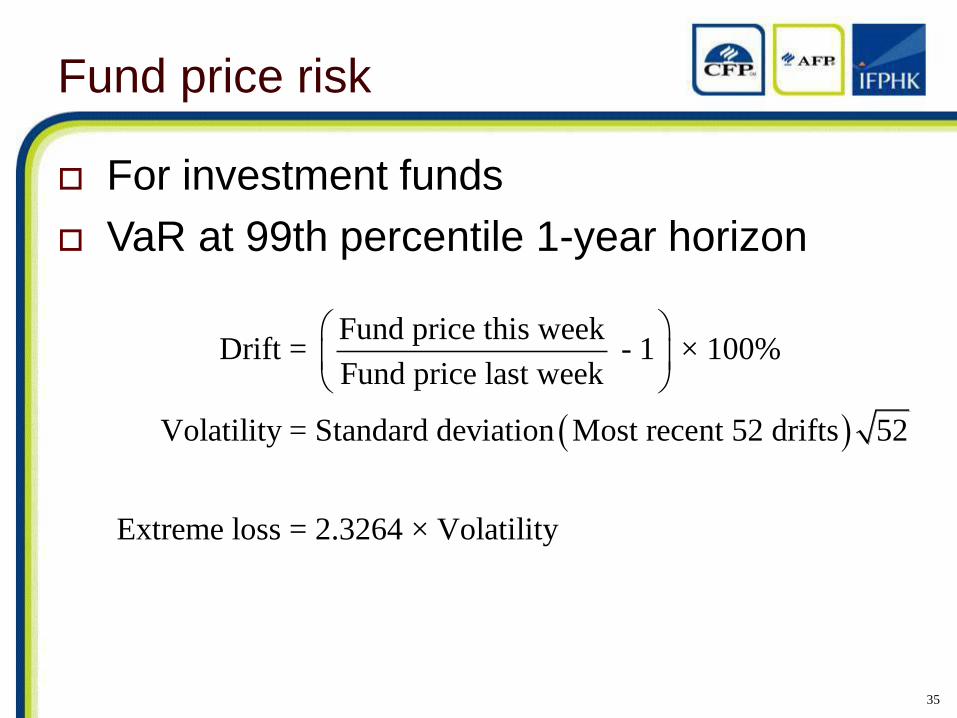

Fund price risk

For investment funds

VaR at 99th percentile 1-year horizon

Fund price this weekDrift = - 1 × 100%

Fund price last week

Volatility = Standard deviation Most recent 52 drifts 52

Extreme loss = 2.3264 × Volatility

36

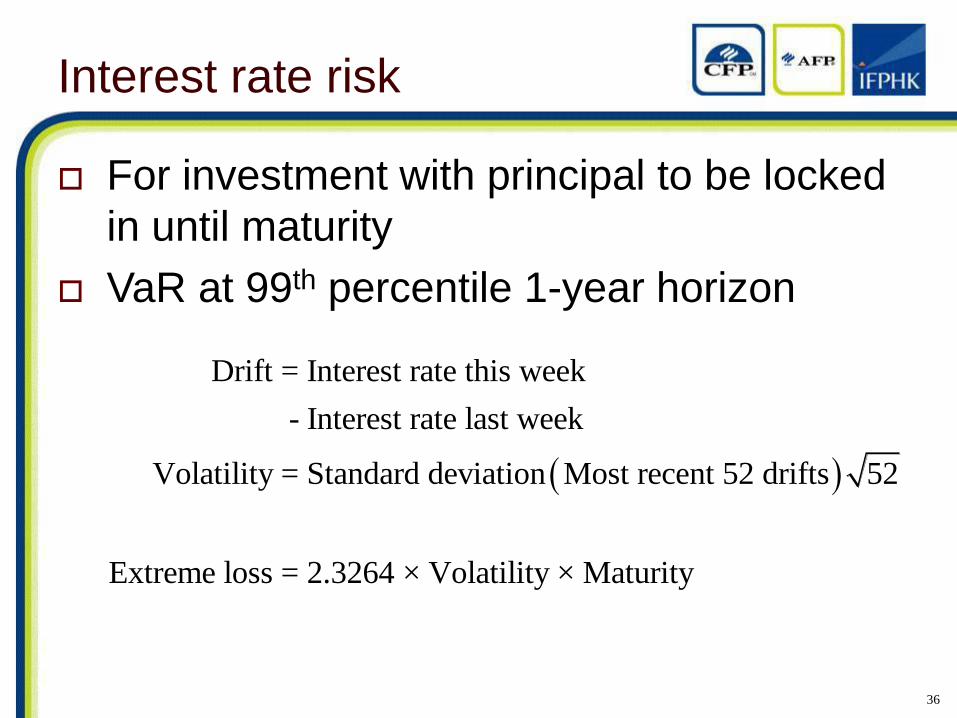

Interest rate risk

For investment with principal to be locked

in until maturity

VaR at 99th percentile 1-year horizon

Drift = Interest rate this week

- Interest rate last week

Volatility = Standard deviation Most recent 52 drifts 52

Extreme loss = 2.3264 × Volatility × Maturity

37

Credit risk

Rating Corp (%) Bank (%) Gov’t (%)

AAA, AA 1.6 1.6 0

A 4 4 1.6

BBB 4 4 4

BB 8 8 8

B 12 8 8

CCC to C 12 12 12

Unrated 12 12 12

38

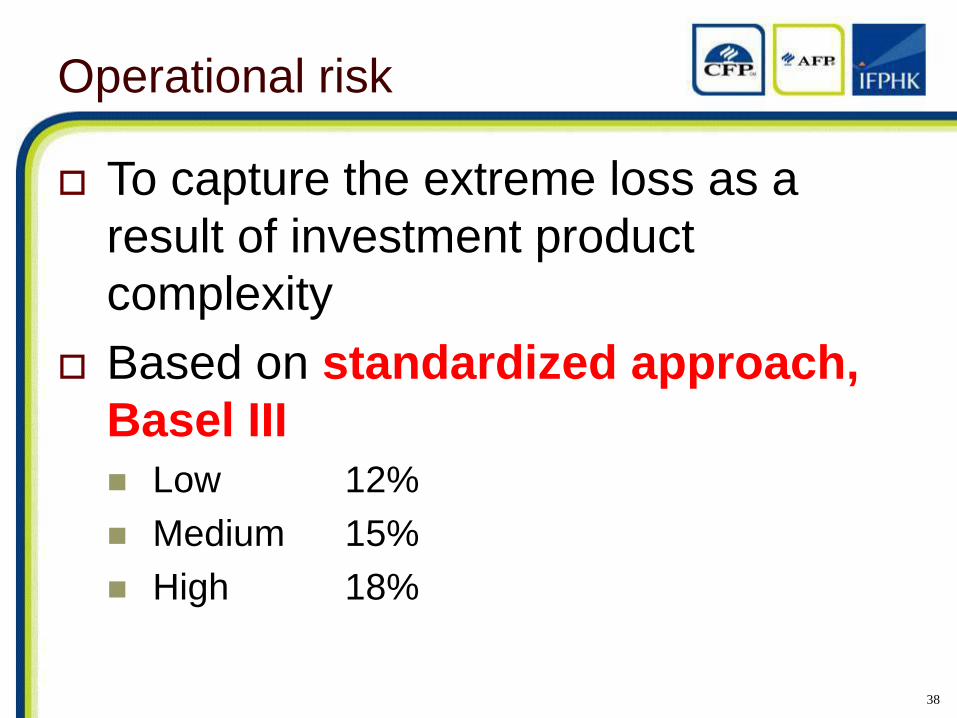

Operational risk

To capture the extreme loss as a

result of investment product

complexity

Based on standardized approach,

Basel III Low 12%

Medium 15%

High 18%

39

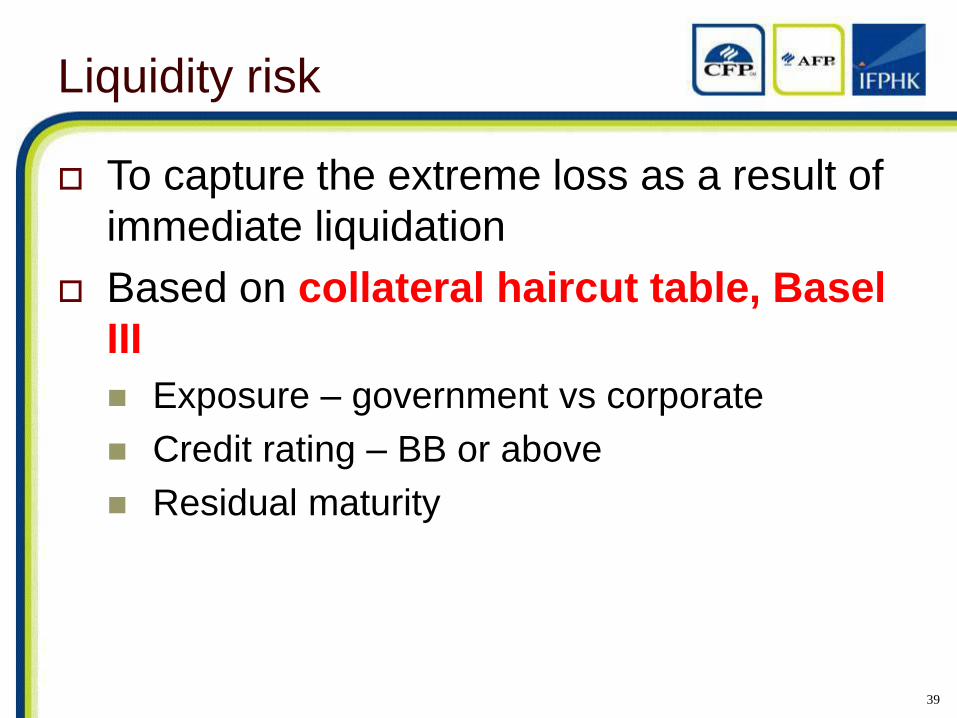

Liquidity risk

To capture the extreme loss as a result of

immediate liquidation

Based on collateral haircut table, Basel

III

Exposure – government vs corporate

Credit rating – BB or above

Residual maturity

40

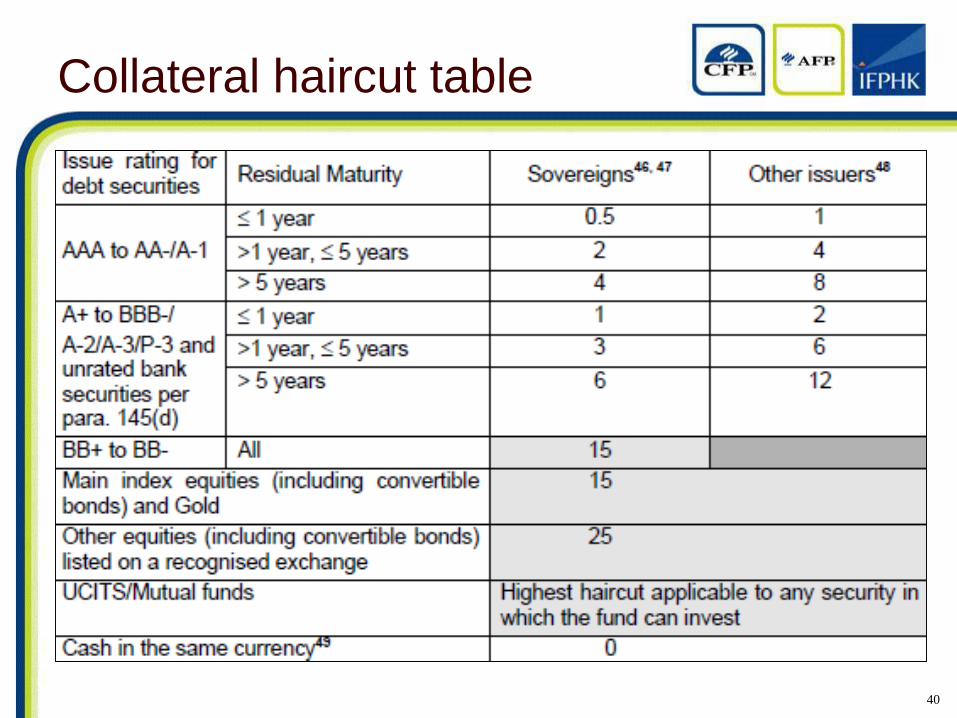

Collateral haircut table

41

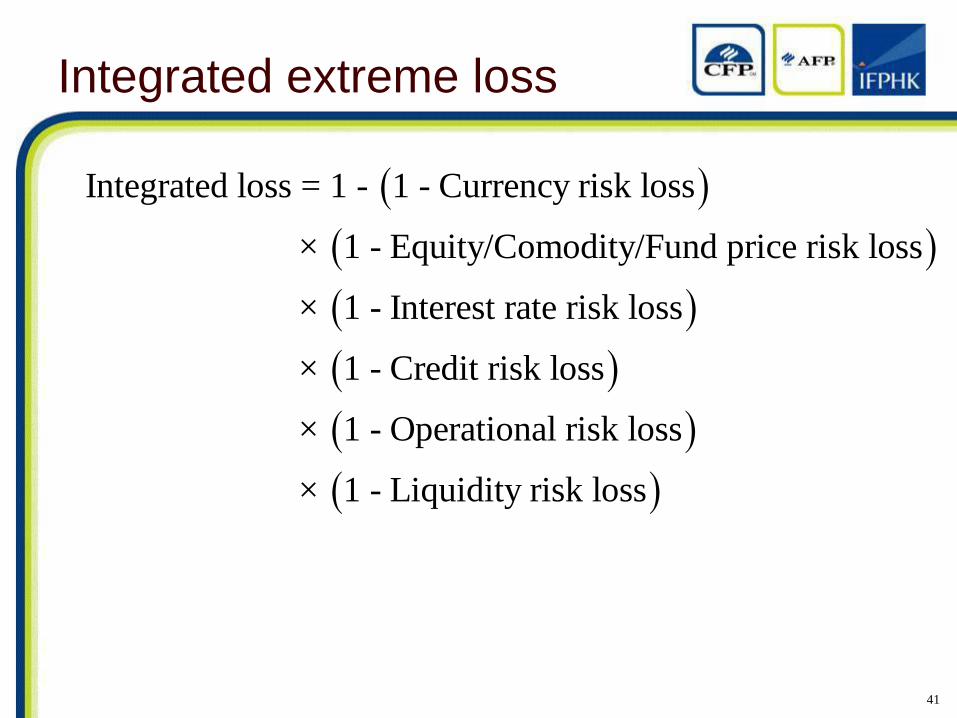

Integrated extreme loss

Integrated loss = 1 - 1 - Currency risk loss

× 1 - Equity/Comodity/Fund price risk loss

× 1 - Interest rate risk loss

× 1 - Credit risk loss

× 1 - Operational risk loss

× 1 - Liquidity risk loss

42

Calibration products

1 – US treasury fund

2 – Fixed income fund

3 – Blue chip equity fund

4 – Commodity fund

5 – Statistically sufficiently above “4”

43

Minimum risk level

To capture

Factors not incorporated in the model

Qualitative factors

Industry consents

Regulatory expectations

44

Minimum risk level

Fixed income fund 2

Corporate bond 2

Developed market equity fund 3

Currency linked deposits 3

Emerging market equity fund 4

Hedge fund 4

Equity linked notes 4

Credit linked notes 5

45

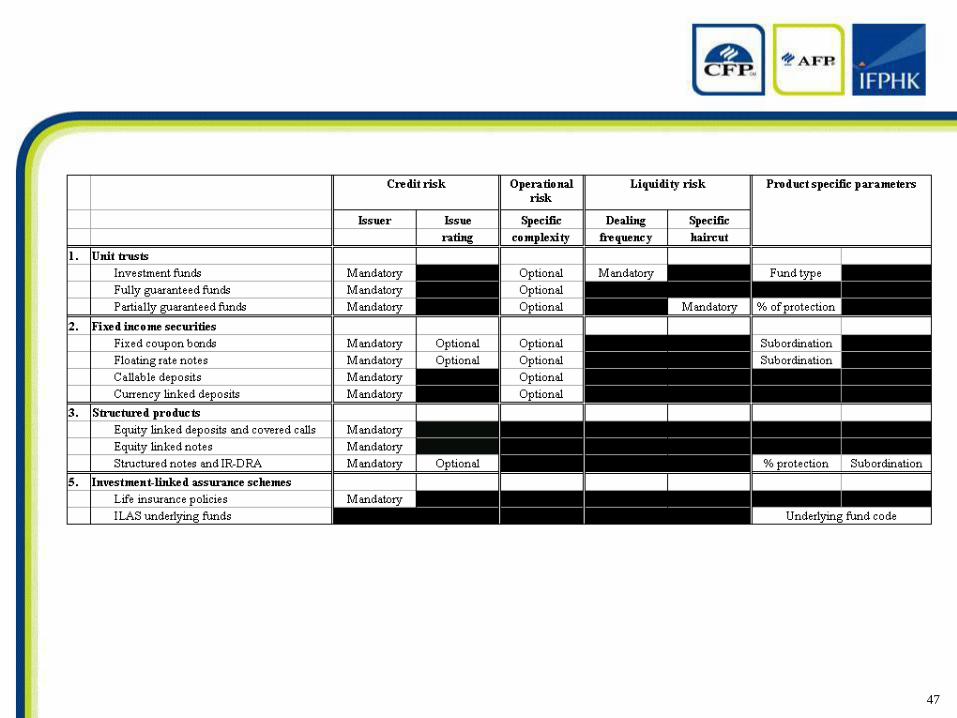

46

47

48

Outline

Suitability of investment products

Major investment products

Qualitative risk assessment

Quantitative risk assessment

Practical issues

Private banking and corporate banking

49

Practical issues

Peer group comparison

Sensitivity vs stability

Product decomposition

2-dimensional rating

New product

New product category

Marketing vs risk management

Data

Transition gap

50

Peer comparison

HSBC

Hang Seng Bank

DBS(HK)

Wing Lung Bank

Wing Hang Bank

Bank of Communications

ICBC(Asia)

ANZI(HK)

51

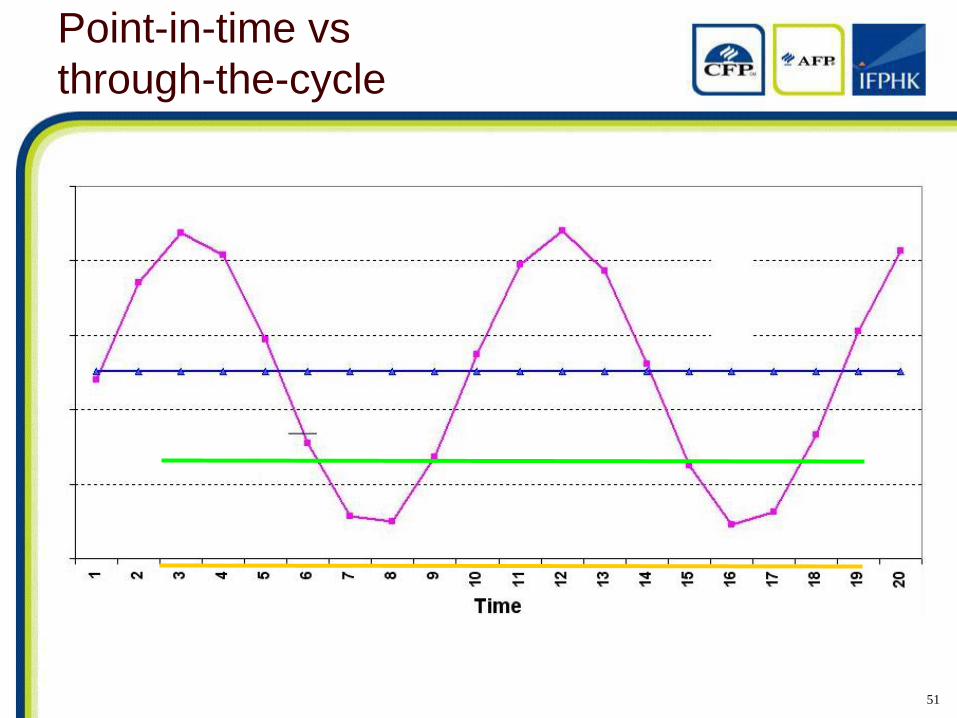

Point-in-time vs

through-the-cycle

52

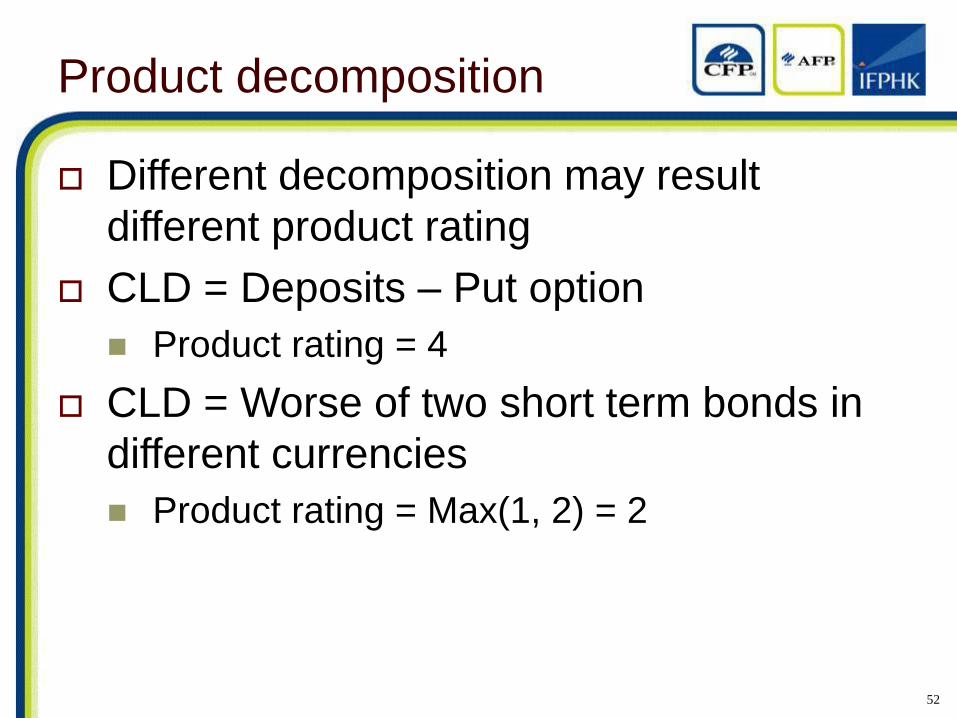

Product decomposition

Different decomposition may result

different product rating

CLD = Deposits – Put option

Product rating = 4

CLD = Worse of two short term bonds in

different currencies

Product rating = Max(1, 2) = 2

53

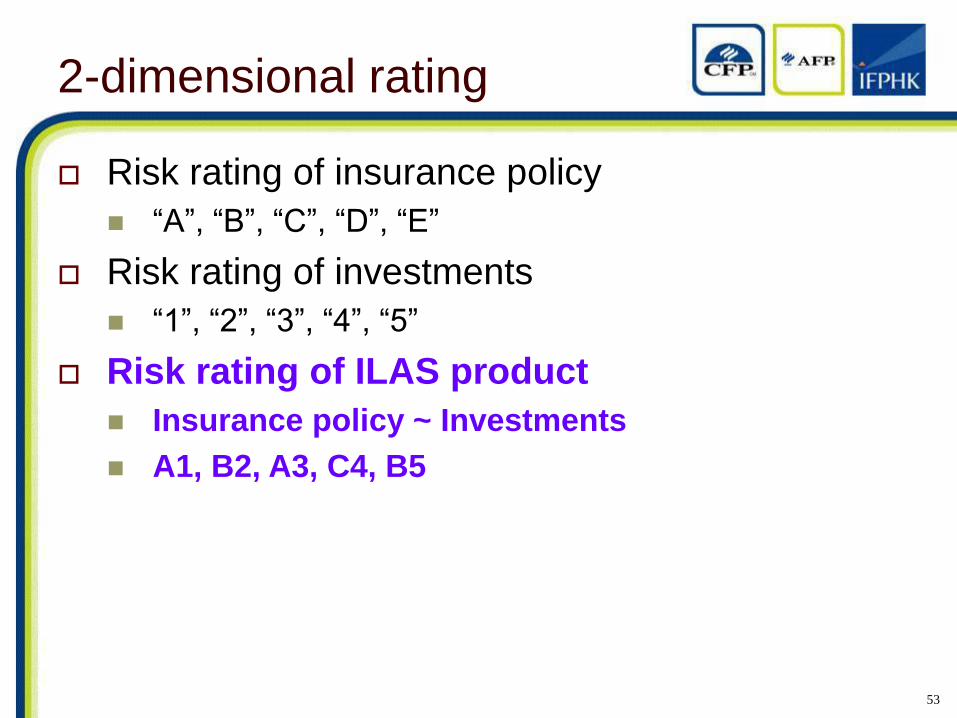

2-dimensional rating

Risk rating of insurance policy

“A”, “B”, “C”, “D”, “E”

Risk rating of investments

“1”, “2”, “3”, “4”, “5”

Risk rating of ILAS product

Insurance policy ~ Investments

A1, B2, A3, C4, B5

54

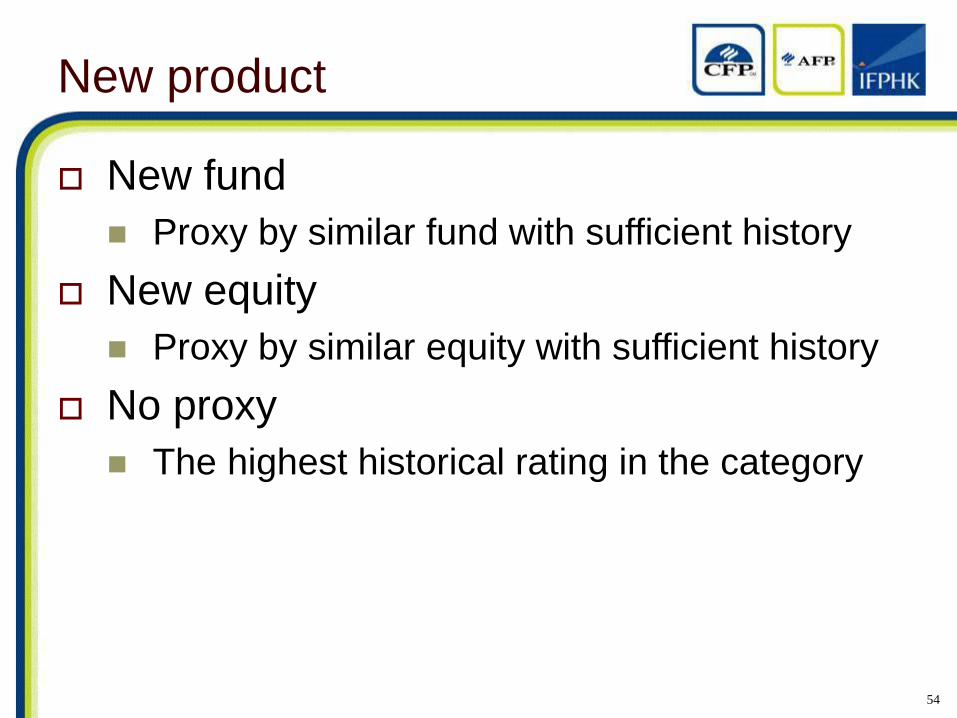

New product

New fund

Proxy by similar fund with sufficient history

New equity

Proxy by similar equity with sufficient history

No proxy

The highest historical rating in the category

55

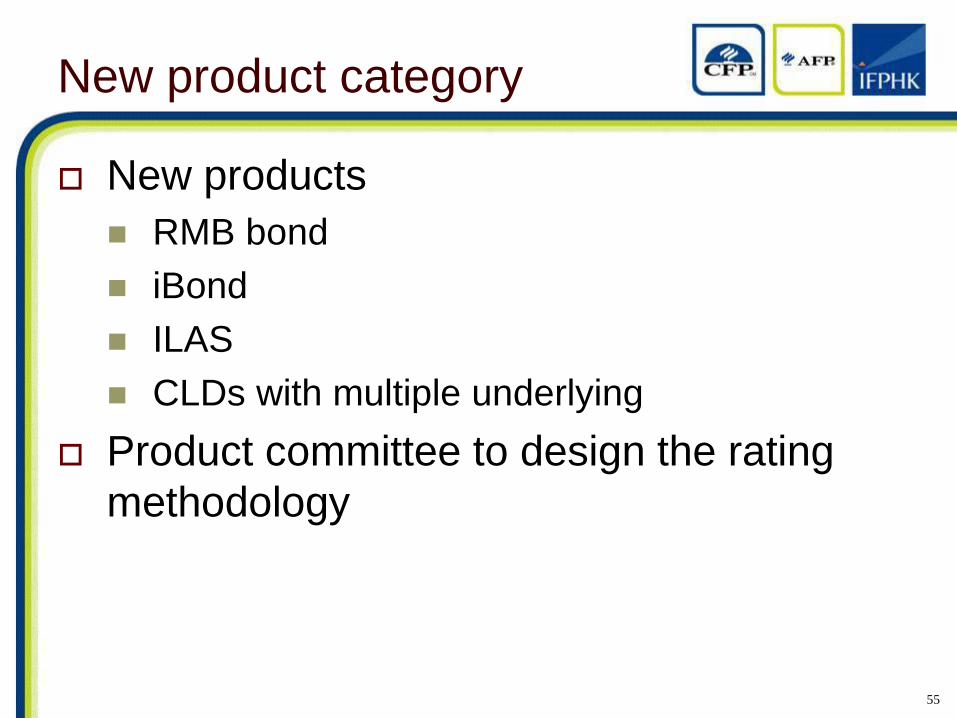

New product category

New products

RMB bond

iBond

ILAS

CLDs with multiple underlying

Product committee to design the rating

methodology

56

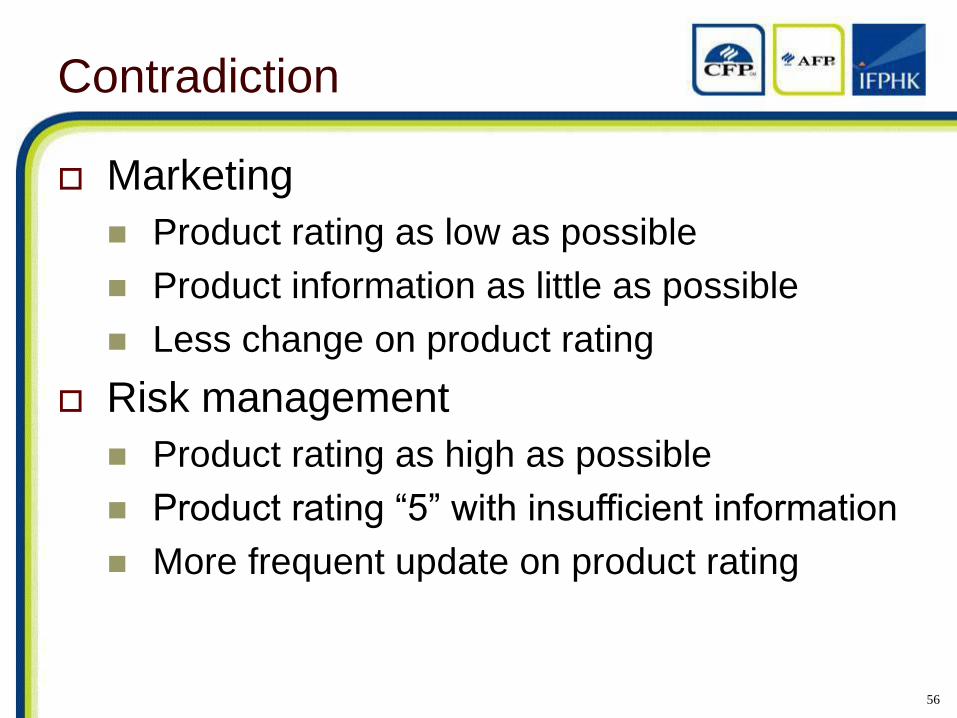

Contradiction

Marketing

Product rating as low as possible

Product information as little as possible

Less change on product rating

Risk management

Product rating as high as possible

Product rating “5” with insufficient information

More frequent update on product rating

57

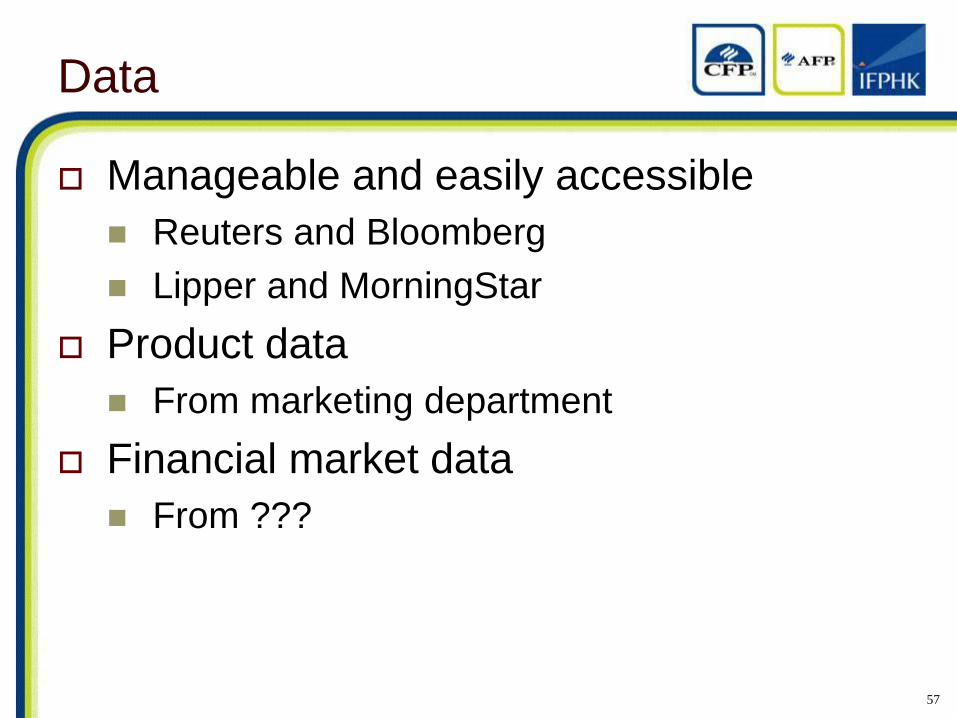

Data

Manageable and easily accessible

Reuters and Bloomberg

Lipper and MorningStar

Product data

From marketing department

Financial market data

From ???

58

Transition gap

New risk ratings materially deviating from

existing ratings

Lower new ratings – Good

Higher new ratings – What to do?

Should the sold products with mis-

matches be liquidated?

Should I inform the mis-match to

customers

59

Outline

Suitability of investment products

Major investment products

Qualitative risk assessment

Quantitative risk assessment

Practical issues

Private banking and corporate banking

60

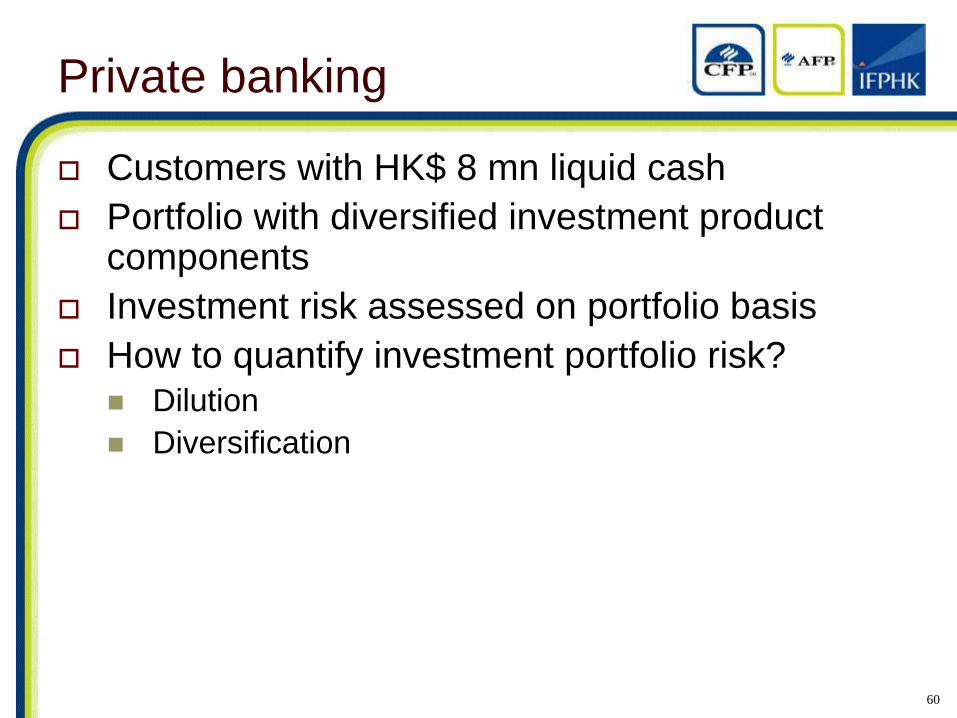

Private banking

Customers with HK$ 8 mn liquid cash

Portfolio with diversified investment product components

Investment risk assessed on portfolio basis

How to quantify investment portfolio risk? Dilution

Diversification

61

62

Corporate banking

Corporate customers with higher risk in their financial profile essentially demand correspondingly higher risk hedging strategies in offsetting direction so as to bring their financial profile back to affordable risk levels

Only corporate customers with sufficient knowledge in financial instruments, who know clearly the costs and benefits of different types of hedging instruments, may choose to adopt more complex hedging instruments, in order to reduce the risk of their financial profile more efficiently at a minimum cost

63

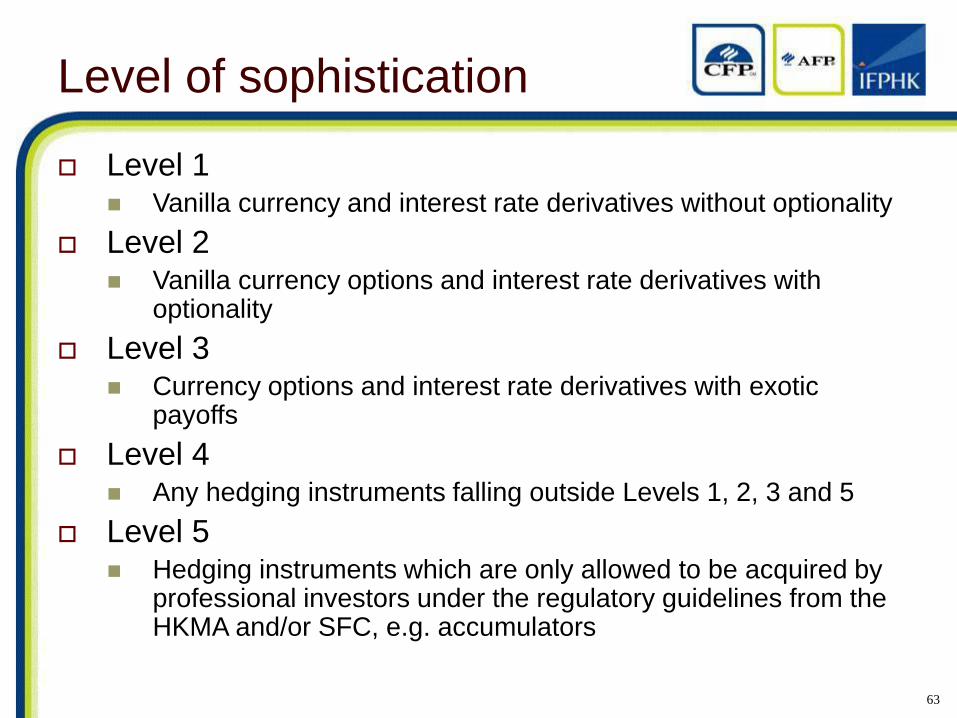

Level of sophistication

Level 1 Vanilla currency and interest rate derivatives without optionality

Level 2 Vanilla currency options and interest rate derivatives with

optionality

Level 3 Currency options and interest rate derivatives with exotic

payoffs

Level 4 Any hedging instruments falling outside Levels 1, 2, 3 and 5

Level 5 Hedging instruments which are only allowed to be acquired by

professional investors under the regulatory guidelines from the HKMA and/or SFC, e.g. accumulators

64

Further complication

Asset class

Short selling

Credit line

Collateral

65

Q & A

66

Thank You

67

Upcoming IFPHK Continuing Education Programs:

http://www.ifphk.org/CEP/ce-calendar

Institute of Financial Planners of Hong Kong

13/F, Causeway Bay Plaza 2,

463 - 483 Lockhart Road, Hong Kong

Tel: 2982 7888

Fax: 2982 7777

Email: [email protected]

Website: www.ifphk.org