RI CorporatePresentation Agosto 2012 - GPA · Partner: Helbor 544 apartments, in 2 steps (1st step:...

22

CORPORATE PRESENTATION Grupo Pão de Açúcar and Viavarejo August 2012

Transcript of RI CorporatePresentation Agosto 2012 - GPA · Partner: Helbor 544 apartments, in 2 steps (1st step:...

CORPORATE PRESENTATION

Grupo Pão de Açúcar and Viavarejo

August 2012

ABOUT GRUPO PÃO DE AÇÚCAR

2

> Key Figures 2011>R$ 52.7 bi Sales

> #1 Retailer in Brazil

>Growth higher than the 2nd player’s

> Operational > 1.8k points of sales, located in 19 States and

the Federal District

> Multi-format distribution

> 635 million tickets per year

> 2.8 million m² of sales area

Net Profit(1)Net Profit(1)

EBITDAEBITDA

Gross SalesGross Sales

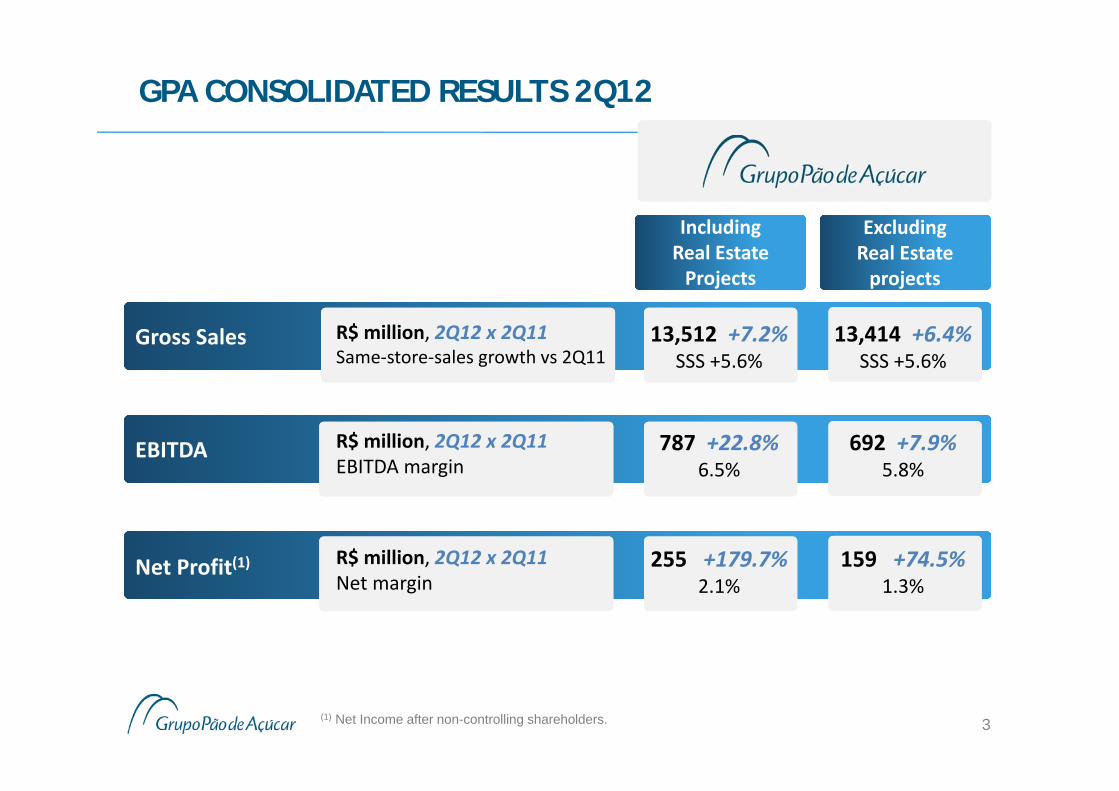

GPA CONSOLIDATED RESULTS 2Q12

3

R$ million, 2Q12 x 2Q11Same‐store‐sales growth vs 2Q11

13,512 +7.2%SSS +5.6%

13,414 +6.4%SSS +5.6%

R$ million, 2Q12 x 2Q11EBITDA margin

787 +22.8%6.5%

692 +7.9%5.8%

R$ million, 2Q12 x 2Q11Net margin

255 +179.7%2.1%

159 +74.5%1.3%

(1) Net Income after non-controlling shareholders.

Excluding Real Estate projects

Excluding Real Estate projects

Including Real Estate Projects

Including Real Estate Projects

GPA CONSOLIDATED - INDEBTEDNESS AND LEVERAGE

Net debt (R$ billion)Net debt (R$ billion) 4.84.8 4.94.9

Net debt /EBITDA(1)Net debt /EBITDA(1) 1.51x1.51x 1.50x1.50x

03/31/1203/31/12 06/30/1206/30/12

(1) EBITDA of the last twelve months 4

% of net sales

166 121

170164

2Q11 2Q12

3.0%2.4%

336285

Consolidated Net Financial Expenses (R$ mi)

Viavarejo

GPA Food

Capex(R$ million)Capex(R$ million)

1H126331H12633

2Q123922Q12392

Gross SalesGross Sales

2Q12 BUSINESSES RESULTS

Gross ProfitGross Profit

Operating ExpensesOperating Expenses

EBITDAEBITDA

Net Financial ExpensesNet Financial Expenses

Net Profit (1) Net Profit (1)

5

R$ million, 2Q12 x 2Q11Same‐store‐sales growth vs 2Q11

7,437 +7.3%SSS +4.7%

Gross margin, 2Q12 x 2Q11Δmargin 2Q12 x 2Q11

26.8% +14.8%+160 bps

% of net sales, 2Q12 x 2Q11Δ % of net sales 2Q12 x 2Q11

18.3% +6.7%‐20 bps

R$ million, 2Q12 x 2Q11EBITDA margin

574 +37.0%8.5%

% of net sales, 2Q12 x 2Q11Δ % of net sales 2Q12 x 2Q11

1.8% ‐27.4%‐90 bps

Net margin, 2Q12 x 2Q11Net margin

253 +171.3%3.8%

GPA Food

(1) Net Income after non-controlling shareholders.

6

6,9287,339

2Q11 2Q12

Gross Sales (R$ mi)

5.9%

Gross Profit (R$ mi)

1,5691,703

2Q11 2Q12

25.2% 25.7%

EBITDA (R$ mi)

419

479

2Q11 2Q12

14.2%6.7%

7.2%

% of net sales

Revenue recognition of R$ 98 million related to GPAMalls & Properties´s land swap for development andconstruction of real estate projects in partnership withdevelopers.

GPA Food excluding real estate projects results :

8.5%

GPA FOOD AND REAL ESTATE PROJECTS

Gross SalesGross Sales

2Q12 BUSINESSES RESULTS

Gross ProfitGross Profit

Operating ExpensesOperating Expenses

EBITDAEBITDA

Net Financial ExpensesNet Financial Expenses

Net Profit (1)Net Profit (1)

7

R$ million, 2Q12 x 2Q11Same‐store‐sales growth vs 2Q11

6,075 +7.0%SSS +6.7%

Gross margin, 2Q12 x 2Q11Δmargin 2Q12 x 2Q11

27.1% +1.5%‐100 bps

% of net sales, 2Q12 x 2Q11Δ % of net sales 2Q12 x 2Q11

23.1% +2.5%‐60 bps

R$ million, 2Q12 x 2Q11EBITDA margin

214 ‐3.5%4.0%

% of net sales, 2Q12 x 2Q11Δ % of net sales 2Q12 x 2Q11

3.1% ‐3,4%‐30 bps

R$ million, 2Q12 x 2Q11Net margin

5.4 n/c0.1%

GPA Non‐Food

(1) Net Income before non‐controlling shareholders.

8

100%Sold

93%Sold

SoonLaunching

TheraFariaLima

FiguéSantoAndré

GuarulhosBosqueMaia

GPA Mall & Properties: Grupo Pão de Açúcar's real estate unit, which is responsible for managesand explores the Company’s real estate assets, and looks at unlocking value in this market.GPA Mall & Properties: Grupo Pão de Açúcar's real estate unit, which is responsible for managesand explores the Company’s real estate assets, and looks at unlocking value in this market.

2012 OUTLOOK: GPA FOOD AND REAL ESTATE PROJECTS

Residential and Commercial Real EstatePartner: Cyrela399 residential apartments and 630 officesLand of 16,200 square meters Total PSV of R$ 502.0 million

Residential Real EstatePartner: RFM64 apartmentsLand of 2,000 square meters Total PSV of R$ 44.2 million

Residential Real EstatePartner: Helbor544 apartments, in 2 steps (1st step: 2012/ 2nd step: 2013)Land of 16,100 square metersExpected Total PSV of R$ 250.0 million

2012 OUTLOOK: GPA FOOD

9

Hyper: strengthen one‐stop‐shop concept (multi‐specialist in electro, home, baby and fashion)

Extra Super consolidation: investment rationalization

Increase the offering of organics, imported, regional e exclusive brands

Minimercado: new format, best convenience solution, resumption of expansion

Explore multichannel opportunities

Operational cost reduction

Logistic cost rationalization with higher inventory capacity at stores

Assortment rationalization focusing the new customer (reseller/foodservice/catering)

New format and resumption of expansion plan

Cash‐and‐carryCash‐and‐carry

RetailRetail

Fashion’s new approach, with renowned stylist and

new product line’s positioning

Perfumery investment on both industry’s lines and imported opportunities

Exclusive brands’ investment

Assaí’s new format

10

Focus on organic expansion

Capture synergies from already optimized processes and implement new initiatives throughout the year

One united culture as one of the priorities

Cash generation aiming at business strength

Expectations towards CADE’s final decision

EletroEletro

Addition of new categories

Explore multichannel opportunities

Deliver above market growth with profitability

Keep customer satisfaction indicator at high levels

E‐commerceE‐commerce

Categories addition in the e‐commerce

operation

New Ponto Frio’sconcept store

Store openings, specially atBrazil’s Northeast region

2012 OUTLOOK: GPA NON-FOOD

Kees customersatisfaction level at

Pontocom

Gross salesin R$ billion

2012 GUIDANCES

11

Net fin. expensesas % of net sales

EBITDA2012 margin

Capex¹ in R$ billion

Expansiongrowth vs Dec/11

FinancialsFinancials

OperationalOperational

New stores

¹ Maximum of R$1,966 million was approved at General Shareholders Meeting

GPA Non‐foodGPA Food

31.5

2.3%

25.7

3.3%

7.3% to 7.8% 5.2% to 6.5%

1.4 0.4

6.0% to 6.7%

57.2

2.8%

6.4% to 7.2%

1.8

70 to 80 50 to 60

Above

Below

Above

Below

Above

Below

-

12

GPA STORES AND FORMATS

*Stores as of 2Q12.

# Stores*

GPA

FO

OD

ELEC

TRO

NIC

S /

HO

ME

APP

LIA

NCESupermarkets

Cash & Carry

Hypermarket

Neighborhood

Gas stations and Drugstores

Specialized Stores

B2C

B2B

363

59

134

69

236

950

-

-

Malls & Properties -

RETAIL MOMENTUM IN BRAZILRETAIL MOMENTUM IN BRAZIL

Rise of the Purchasing Power

Focus on Middle Class Population

Informality Reduction

Distribution Channels Diversification

2014 World Cup

2016 Olympic Games

BRAZILIAN SCENARIO

ECONOMIC SCENARIOECONOMIC SCENARIO

GDP Growth

Social Rise

Greater Credit Offer

2014: 5th largest consumermarket of the world

2020: expense of Brazilianhomes: R$ 5,000 bn

13

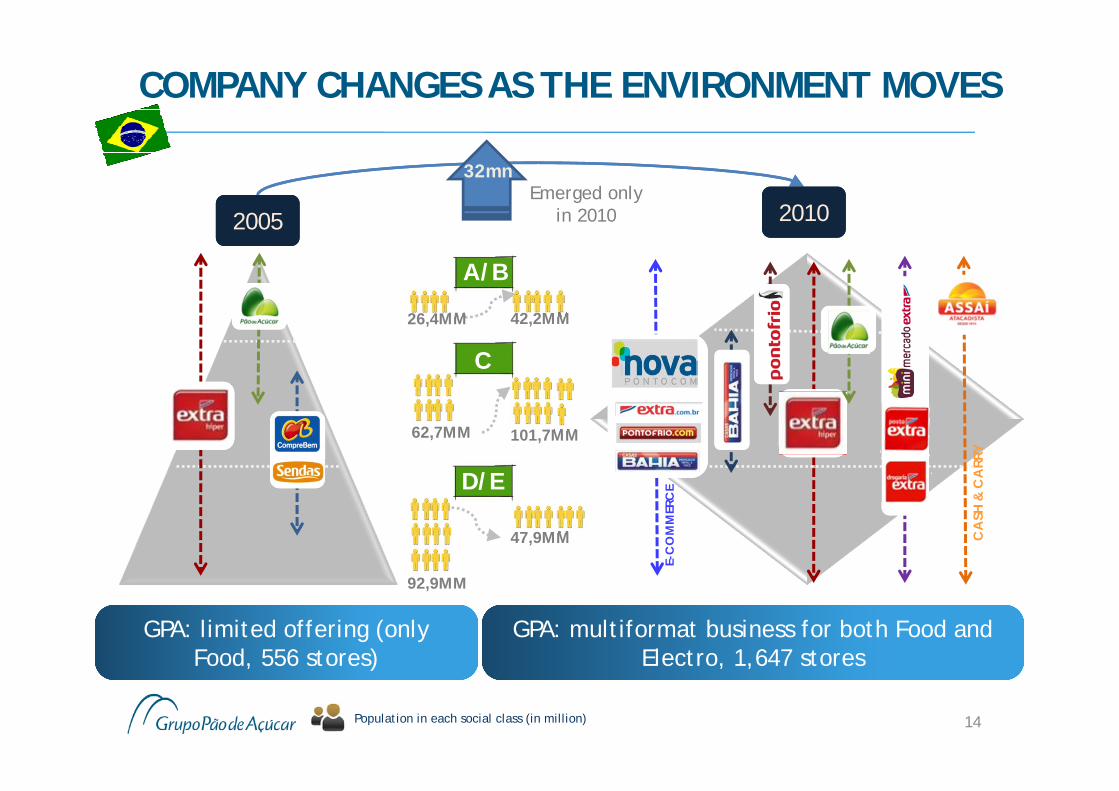

COMPANY CHANGES AS THE ENVIRONMENT MOVES

14Population in each social class (in million)

GPA: limited offering (only Food, 556 stores)

GPA: limited offering (only Food, 556 stores)

GPA: multiformat business for both Food and Electro, 1,647 stores

GPA: multiformat business for both Food and Electro, 1,647 stores

92,9MM

26,4MM

62,7MM 101,7MM

C

A/B

42,2MM

47,9MM

D/E

20052005 20102010

32mnEmerged only

in 2010

CA

SH &

CA

RRY

E-C

OM

MER

CE

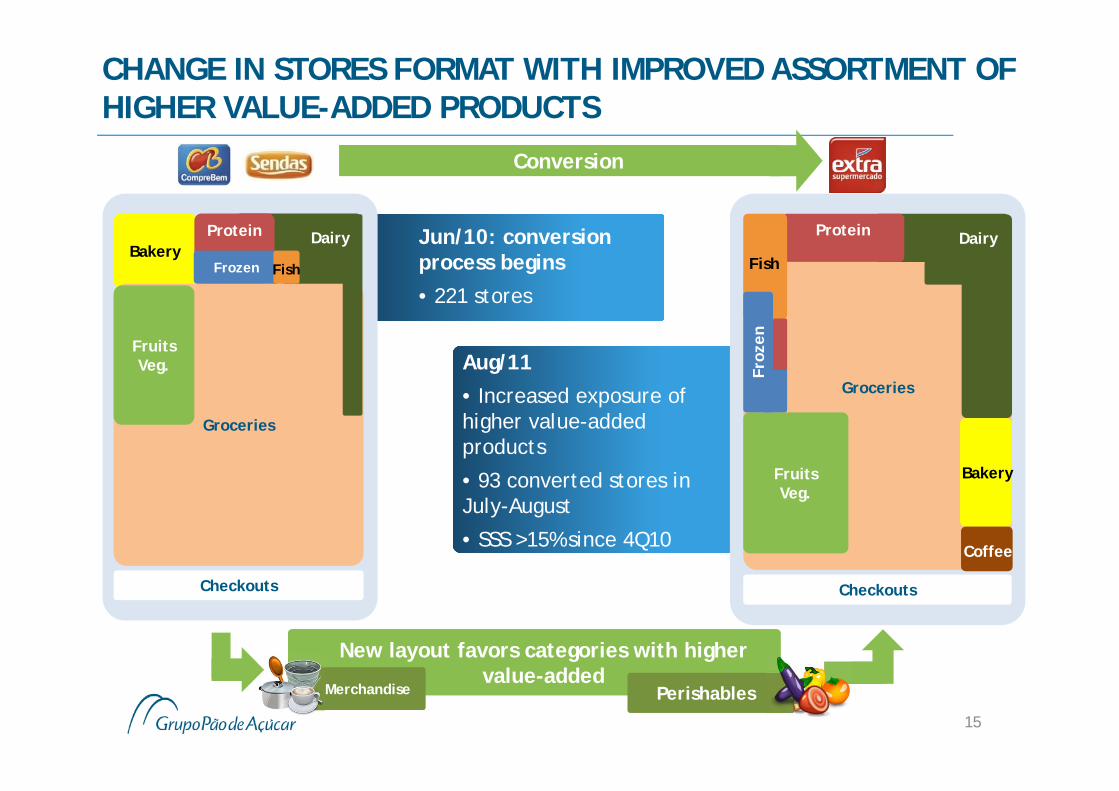

CHANGE IN STORES FORMAT WITH IMPROVED ASSORTMENT OF HIGHER VALUE-ADDED PRODUCTS

15

New layout favors categories with higher value-added

New layout favors categories with higher value-added

MerchandiseMerchandise PerishablesPerishables

Jun/10: conversion process begins

• 221 stores

Aug/11

• Increased exposure of higher value-added products

• 93 converted stores in July-August

• SSS >15% since 4Q10

Bakery

Checkouts

Groceries

FruitsVeg.

DairyProtein

Frozen Fish

Checkouts

Groceries

FruitsVeg.

DairyProtein

Fish

Bakery

Coffee

Froz

en

Conversion

16

Sales Area : from 200 to 300m²Bakery : services and broaden assortmentof productsSliced cheese/meat : sliced at thepurchase moment , self-service exposureand broaden assortmentButchery : customized servicesGroceries : refined products lineFruits/Vegetables : day-by-day productsbetter exposed.Differentiation AB/CD income classesSKUs: 3,600

Groceries: 2,600Perishables: 1,000

Sales Area: from 150 to 200m² Bakery: baken product (self-service)

Sliced cheese/meat: ready-to-go (fromindustry)

Butchery: vacuum packedGroceries: day-by-day productFruits/Vegetables: day-by-day product

Low differentiation AB/CD income classesSKUs: 3,600

Groceries: 2,800Perishables: 800

Previous Format(Focus: groceries, self-service)

Previous Format(Focus: groceries, self-service)

New modelNew model

Conversion

CHANGE IN STORES FORMAT WITH MORE PERISHABLES AND SERVICES

RETAIL INNOVATION AND PIONEERING GOES ON

Fashion in Extra• New positioning: near to specialized stores in terms of collection, communication and suppliers, but with hypermarket pricing strategy

Private Label Development• Strategic approach due to higher margin, profitability and customer loyalty

• Focus to increase share, with product life cycle management, quality control and more innovation

Perfumery • Scenario: Competition against Pharmacy, D2D and Beauty Salons• Actions: Exclusive products and exposition, reference for New product launch, beauty Consultant, growth in high penetration categories

17

18

GPA STORES CHARACTERISTICS

GPA FOOD Public Stores

Avg Sales Area (m2)

ABCD classes 134 6,000

AB classes 159 1,500

BCD classes 204 1,500

TransformersFood service 59 4,000

ABCD classes 69 300

Public Stores

ABC classes 403

CD classes 547

VIAVAREJO

Stores as of 2Q12.

*Stores as of 2Q12.Gas station and drugstores are not included.

NorthHyper: 1

Electro: 2

Total: 3

Middle-WestSuper: 14

Hyper: 12

Electro: 82

Cash & Carry: 3

Total: 111

North-EastSuper: 29

Hyper: 18

Electro: 36

Cash & Carry: 6

Total: 89

South-EastSuper: 316

Hyper: 101

Electro: 743

Cash & Carry: 50

Proximity: 69

Total: 1,279

SouthSuper: 4

Hyper: 2

Electro: 87

Total: 93

52 Distribution Centers in the country

GDP: 5.1%GDP: 5.1%

GDP: 9.2%GDP: 9.2%

GDP: 13.1%GDP: 13.1%

GDP: 56.0%GDP: 56.0%GDP: 16.6%GDP: 16.6%

REGIONAL PRESENCE (STORES*)

19

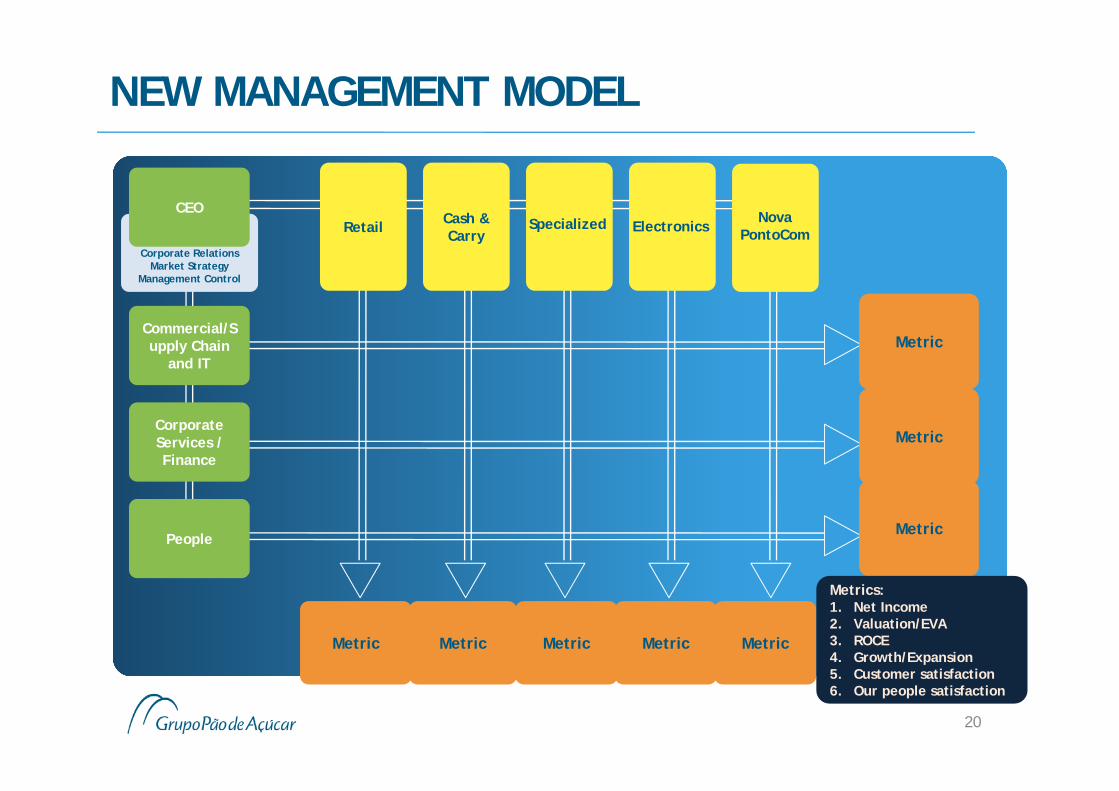

NEW MANAGEMENT MODEL

20

MetricCommercial/Supply Chain

and IT

Corporate Services / Finance

People

Retail Cash & Carry

Metric Metric Metric Metric Metric

Metric

Metric

Metrics:1. Net Income2. Valuation/EVA3. ROCE4. Growth/Expansion5. Customer satisfaction6. Our people satisfaction

Corporate RelationsMarket Strategy

Management Control

CEONova

PontoComSpecialized Electronics

21

OWNERSHIP STRUCTURE

37%

63%

47%53%

50% 6%

44%

FICFinancial JV 14%

36%

Banco Itaú

50%

Free Float

Controlling Group

Casas Bahia FoundersKlein Family

Management

As of March 31, 2012.

INVESTOR RELATIONS CONTACTS

Grupo Pão de Açúcar (GPA) | Viavarejo

Investor Relations TeamPhone: +55 (11) 3886‐0421 Fax: +55 (11) 3884‐2677

FORWARD‐LOOKING STATEMENTS> The forward‐looking statements contained herein are based on our management’s currentassumptions and estimates, which may result in material differences regarding future results,performance and events. Actual results, performance and events may differ substantially from thoseexpressed or implied in these forward‐looking statements due to a variety of factors, such as generaleconomic conditions in Brazil and other countries, interest and exchange rate levels, legal andregulatory changes and general competitive factors (whether global, regional, or national).

22