REVENUE RECOGNITION - bkd.com · CREATING A ONE-STOP SHOP FOR REVENUE LITERATURE Current Guidance 3...

32

experience clarity // CPAs & ADVISORS FASB/IASB Joint Project REVENUE RECOGNITION

Transcript of REVENUE RECOGNITION - bkd.com · CREATING A ONE-STOP SHOP FOR REVENUE LITERATURE Current Guidance 3...

experience clarity //

CPAs & ADVISORS

FASB/IASB Joint Project

REVENUE RECOGNITION

May 28, 2014 - ASU 2014-09, Revenue from Contracts with Customers, is released

Single, converged, comprehensive approach to revenue recognition, regardless of industry

Replaces virtually all existing U.S. GAAP for revenue recognition

Effective for public companies in 2017 with additional year for nonpublic entities

2

CREATING A ONE-STOP SHOP FOR REVENUE LITERATURE

3

Current Guidance New Principle

General Recognition Concepts

Ind

ust

ry-s

pec

ific

gu

idan

ce

So

ftw

are

(Su

bto

pic

98

5-6

05

)

Rea

l Est

ate

Sale

s (S

ub

top

ic 3

60

-20

)

Co

ntr

acto

rs -

Co

nst

ruct

ion

Rev

enu

e R

eco

gnit

ion

(S

ub

top

ic 9

10

-60

5)

Rea

l Est

ate

- G

ener

al R

even

ue

Rec

ogn

itio

n

(Su

bto

pic

97

0-6

05

)

Rea

l Est

ate

- R

etai

l Lan

d -

Rev

enu

e R

eco

gnit

ion

(S

ub

top

ic 9

76

-60

5)

The transfer of a promised good or service determines when revenue is recognized and occurs when (or as) the customer obtains control of the asset. Transfer can be made either at a point in

time or over time.

Persuasive evidence of an arrangement exists

Delivery has occurred or services have been rendered

Price is fixed or determinable

Collectibility is reasonably assured

Construction and production type contracts (Subtopic 605-35)

WHO’S IMPACTED

All entities that enter into contracts with customers

Public, private, not-for-profit

Regardless of industry

4

REASONS FOR THE CHANGE

Remove inconsistencies in existing requirements

Provide more robust framework

Improve comparability across companies, industries & capital markets

Enhance disclosure

Simplify financial statement preparation

Provide guidance for transactions that did not previously have authoritative guidance

5

SCOPE

Contracts with customers, except

Lease contracts

Insurance contracts

Financial instruments

Certain guarantees (other than product warranties)

Certain nonmonetary exchanges

6

CUSTOMERS VS. COLLABORATORS

Proposal does not apply to pure collaborative arrangements, that is

Parties share in risk of developing product

Not for sale of goods or services that are output of entity’s ordinary activities

Must determine if contract is with customer, collaborator or entity with elements of both

7

FIVE-STEP MODEL

Step 1 • Identify contract(s) with customer

Step 2 • Identify performance obligations

Step 3 • Determine transaction price

Step 4 • Allocate transaction price to performance obligations

Step 5 • Recognize revenue when (or as) performance obligation is satisfied

8

SOME ENTITIES WILL BE AFFECTED MORE THAN OTHERS

9

Industry Step 1 Identify Contract

Step 2 Identify Performance Obligations

Step 3 Determine Transaction Price

Step 4 Allocate Transaction Price

Step 5 Recognize Revenue

Contract Costs

Health Care X X X X X X

Finance - Asset Mgrs.

X X X X X X

Real Estate & Construction

X X X X X

Manufacturing X X X X X

10

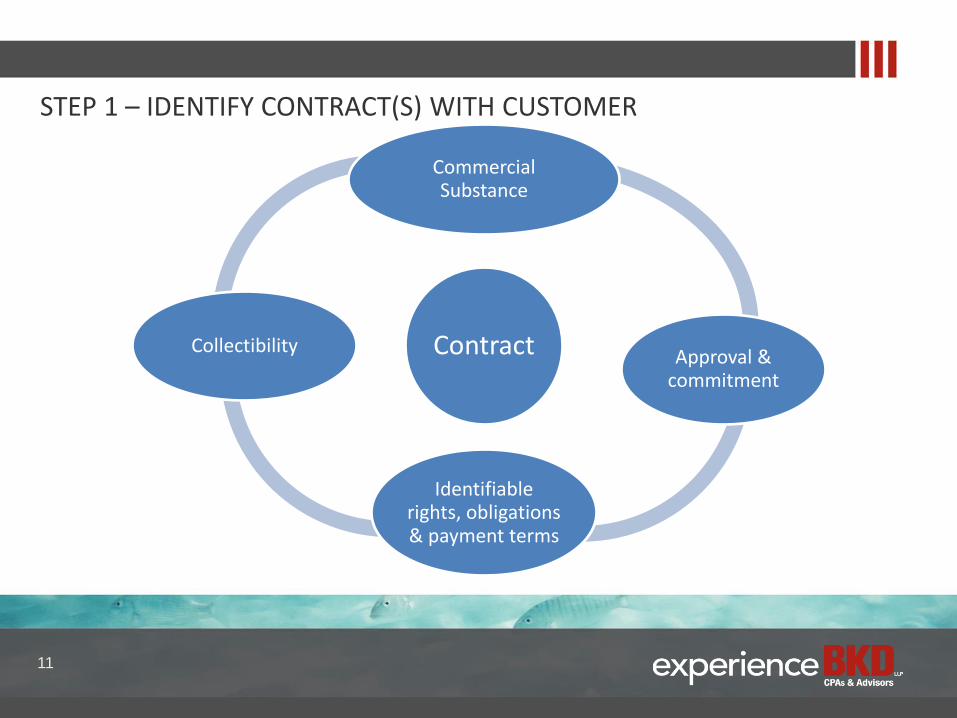

STEP 1 – IDENTIFY CONTRACT(S) WITH CUSTOMER

Contract = “agreement between two or more parties that creates enforceable rights & obligations” & meets following criteria

Commercial substance

Approval & commitment by all parties

Identifiable rights, obligations & payment terms

Collectibility threshold

Step 1: Identify Contract(s) with

Customer

Step 2: Identify Performance Obligations

Step 3: Determine

Transaction Price

Step 4: Allocate Transaction Price

Step 5: Recognize Revenue

11

STEP 1 – IDENTIFY CONTRACT(S) WITH CUSTOMER

Contract

Commercial Substance

Approval & commitment

Identifiable rights, obligations & payment terms

Collectibility

12

COLLECTIBILITY

Collectibility will be explicit threshold that must be assessed before applying revenue recognition model to contract. Entity must evaluate customer credit risk & conclude that it is “probable” that it will collect amount of consideration due in exchange for goods or services

Assessment is based on both customer’s ability & intent to pay as amounts become due

13

STEP 2 – IDENTIFY PERFORMANCE OBLIGATIONS

Performance obligation

Promise to transfer goods/services to customer

Can be explicitly identified in contract or implied by customary business practices

One contract could equal one or many performance obligations

Significant judgment may be required

Step 1: Identify Contract(s) with

Customer

Step 2: Identify Performance Obligations

Step 3: Determine

Transaction Price

Step 4: Allocate

Transaction Price

Step 5: Recognize Revenue

14

STEP 2 – IDENTIFY PERFORMANCE OBLIGATIONS

Separate performance obligations should be identified if good or services meet both of following

Customer can benefit from good/service on its own or with other readily available resources; &

Distinct within context of contract, i.e., not highly dependent on, or highly interrelated with, other promised goods/services in contract

Step 1: Identify Contract(s) with

Customer

Step 2: Identify Performance Obligations

Step 3: Determine Transaction

Price

Step 4: Allocate

Transaction Price

Step 5: Recognize Revenue

15

STEP 3 – DETERMINE TRANSACTION PRICE

Transaction price = amount of consideration entity expects to be entitled to (after collectibility threshold is met)

Contract terms

Customary business practices

Time value of money (if significant financing component)

Variable consideration (including consideration of constraint)

Cash & noncash consideration

Step 1: Identify Contract(s) with

Customer

Step 2: Identify Performance Obligations

Step 3: Determine Transaction

Price

Step 4: Allocate

Transaction Price

Step 5: Recognize Revenue

STEP 3 – DETERMINE TRANSACTION PRICE

Revenue from variable consideration constrained unless

Entity has experience with similar contracts & is able to estimate cumulative amount of revenue

Based on experience, significant reversal of revenue previously recorded is not probable

Step 1: Identify Contract(s)

with Customer

Step 2: Identify Performance Obligations

Step 3: Determine Transaction

Price

Step 4: Allocate

Transaction Price

Step 5: Recognize Revenue

16

STEP 4 – ALLOCATE TRANSACTION PRICE TO SEPARATE PERFORMANCE OBLIGATIONS

Step 1: Identify Contract(s) with

Customer

Step 2: Identify Performance Obligations

Step 3: Determine Transaction

Price

Step 4: Allocate

Transaction Price

Step 5: Recognize Revenue

Allocate based on relative standalone selling prices of separate performance obligations

Observable price when sold separately (best evidence)

Otherwise, estimate based on

Adjusted market assessment

Cost plus margin

Residual value - Only if highly variable or uncertain

Other

17

STEP 5 – RECOGNIZE REVENUE WHEN (OR AS) PERFORMANCE OBLIGATIONS ARE SATISFIED

Revenue recognized when (or as) control of good/service is transferred to customer

Transfer of control occurs when customer has ability to direct use of, & receive benefits from, good/service

Can be recognized over time or at a point in time, depending on how performance obligations are satisfied

Step 1: Identify Contract(s) with

Customer

Step 2: Identify Performance Obligations

Step 3: Determine Transaction

Price

Step 4: Allocate

Transaction Price

Step 5: Recognize Revenue

18

STEP 5 – RECOGNIZE REVENUE WHEN (OR AS) PERFORMANCE OBLIGATIONS ARE SATISFIED

Control is transferred over time if any of following criteria are met

Customer controls asset as it is created/enhanced

Customer receives & consumes benefits of entity’s performance as entity performs

Entity’s performance doesn’t create asset with alternative use to entity & customer doesn’t control asset created; however, entity has right to payment for performance completed to date & expects to fulfill contract

Step 1: Identify Contract(s) with

Customer

Step 2: Identify Performance Obligations

Step 3: Determine Transaction

Price

Step 4: Allocate

Transaction Price

Step 5: Recognize Revenue

19

STEP 5 – RECOGNIZE REVENUE WHEN (OR AS) PERFORMANCE OBLIGATIONS ARE SATISFIED

Measuring progress toward satisfaction of obligation

Output methods

Milestones reached

Units produced

Only used if value of WIP & value of units produced but not yet delivered is immaterial

Input methods

Costs incurred

Machine hours used

Time lapsed

Step 1: Identify

Contract(s) with Customer

Step 2: Identify Performance Obligations

Step 3: Determine Transaction

Price

Step 4: Allocate

Transaction Price

Step 5: Recognize Revenue

20

STEP 5 – RECOGNIZE REVENUE WHEN (OR AS) PERFORMANCE OBLIGATIONS ARE SATISFIED

Control transferred at a point in time indicated by following

Present right to payment from customer

Customer has legal title

Customer has physical possession

Customer has significant risks/rewards of ownership

Customer has accepted asset

Step 1: Identify Contract(s) with

Customer

Step 2: Identify Performance Obligations

Step 3: Determine Transaction

Price

Step 4: Allocate

Transaction Price

Step 5: Recognize Revenue

21

STEP 5 – RECOGNIZE REVENUE

22

Control transferred at a point in time

Present right to

payment Legal title

Physical possession

Significant risk &

rewards of ownership

Customer acceptance

STEP 5 – RECOGNIZE REVENUE WHEN (OR AS) PERFORMANCE OBLIGATIONS ARE SATISFIED

Licenses - Entity must first determine if license is distinct from other goods or services in arrangement. For licenses that are not distinct, entity would combine license with other goods & services in contract & recognize revenue when it satisfies combined performance obligation

Step 1: Identify Contract(s) with

Customer

Step 2: Identify Performance Obligations

Step 3: Determine

Transaction Price

Step 4: Allocate

Transaction Price

Step 5: Recognize Revenue

23

STEP 5 – RECOGNIZE REVENUE WHEN (OR AS) PERFORMANCE OBLIGATIONS ARE SATISFIED

For distinct licenses, entity would assess nature of promise before applying revenue recognition model to license arrangements

Right to use - License is promise to provide right to use entity’s IP as it exists at a

point in time when license was granted, which transfers to customer at a point in

time

Access - License that allows customer to access intellectual property as it exists

at time of access results in revenue recognition over time

Step 1: Identify Contract(s) with

Customer

Step 2: Identify Performance Obligations

Step 3: Determine

Transaction Price

Step 4: Allocate

Transaction Price

Step 5: Recognize Revenue

24

CONTRACT COSTS

Incremental Cost of Obtaining a Contract - Capitalized if recoverable

Direct response advertising would be expensed

Costs to Fulfill Contract - Entity would recognize asset only if costs meet all of following criteria

Relate directly to contract or specific anticipated contract, e.g., direct labor or materials

Generate or enhance resources that would be used to satisfy performance obligations in future

Are expected to be recovered

25

FINANCIAL STATEMENT DISCLOSURES

Significantly expanded disclosures

Quantitative & qualitative information about nature, amount, timing & uncertainty of revenue & cash flows

Limited relief offered to nonpublic companies on some of qualitative disclosures

26

EFFECTIVE DATE & TRANSITION

Public companies

First interim period within annual reporting periods beginning on or after December 15, 2016

Early application would not be permitted

Nonpublic entities

Additional year after public company effective date

Early application permitted as early as public company date

27

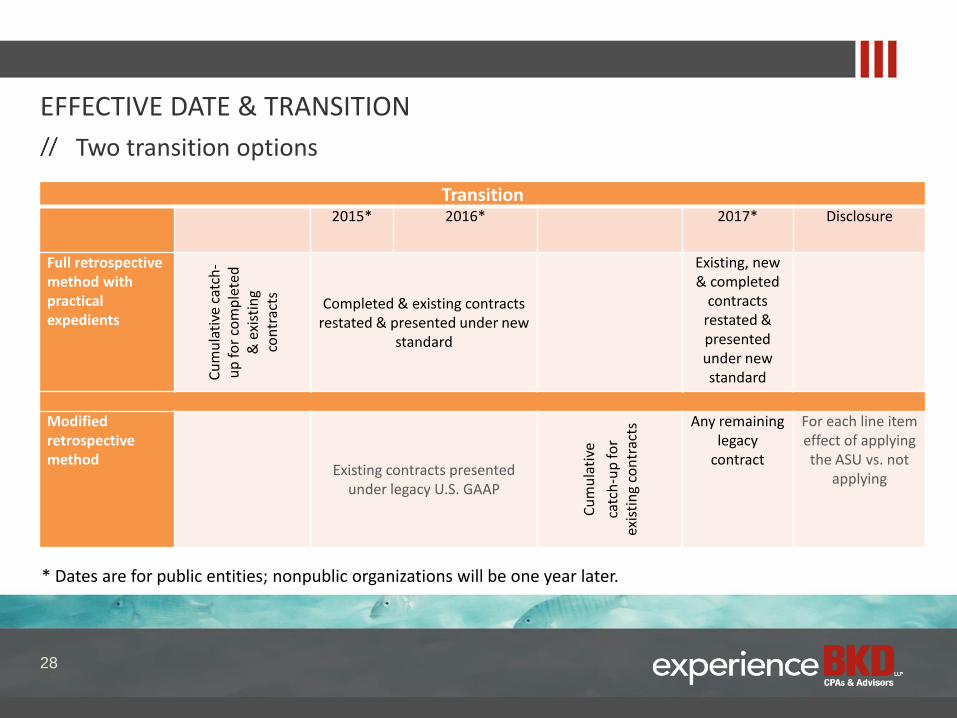

EFFECTIVE DATE & TRANSITION

Two transition options

Transition

2015*

2016*

2017*

Disclosure

Full retrospective method with practical expedients

Cu

mu

lati

ve c

atch

-u

p f

or

com

ple

ted

&

exi

stin

g co

ntr

acts

Completed & existing contracts restated & presented under new

standard

Existing, new & completed

contracts restated & presented under new standard

Modified retrospective method

Existing contracts presented under legacy U.S. GAAP

Cu

mu

lati

ve

catc

h-u

p fo

r ex

isti

ng

con

trac

ts Any remaining

legacy contract

For each line item effect of applying the ASU vs. not

applying

28

* Dates are for public entities; nonpublic organizations will be one year later.

CROSS-FUNCTIONAL IMPLEMENTATION TEAM REQUIRED

29

Department

Board of Directors Approve changes to compensation plans

Tax Impact of changing in timing of revenue recognition

Legal Redraft contract terms with customers

IT System updates

Internal Audit Review new internal controls & documentation

Investor Relations Communication strategy, manage analysts’ expectations

Treasury Review debt covenants for impact of changes in revenue timing

HR Review compensation & incentive plans

Marketing Review advertising plans & sales incentive programs

Operations Review contract fulfillment costs for capitalization

NEXT STEPS

Substantial additional implementation guidance & outreach from FASB expected in upcoming months

We plan to issue

White papers

General

Industry specific

C&RE

Health Care

M&D

Alerts on AICPA implementation guides

Webpage

30

JOINT TRANSITION RESOURCE GROUP (TRG)

First meeting July 18, 2014, with one additional meeting in October 2014 & four in 2015. All meetings will be public & co-chaired by vice chairmen of IASB & FASB

Members include financial statement preparers, auditors & users representing wide spectrum of industries, geographical locations & public & private companies & organizations

Anyone can submit potential implementation issue for discussion at TRG meetings. IASB & FASB will evaluate each submission & prioritize issues for discussion at TRG meetings

TRG will NOT issue guidance

31

THANK YOU

FOR MORE INFORMATION // For a complete list of our offices

and subsidiaries, visit bkd.com or contact:

Name, Credentials // Title [email protected] // 888.888.8888