1.10) Revenue Recognition - Miles Education · 2019-12-27 · FAR-1 Miles CPA Review F1-521.10)...

28

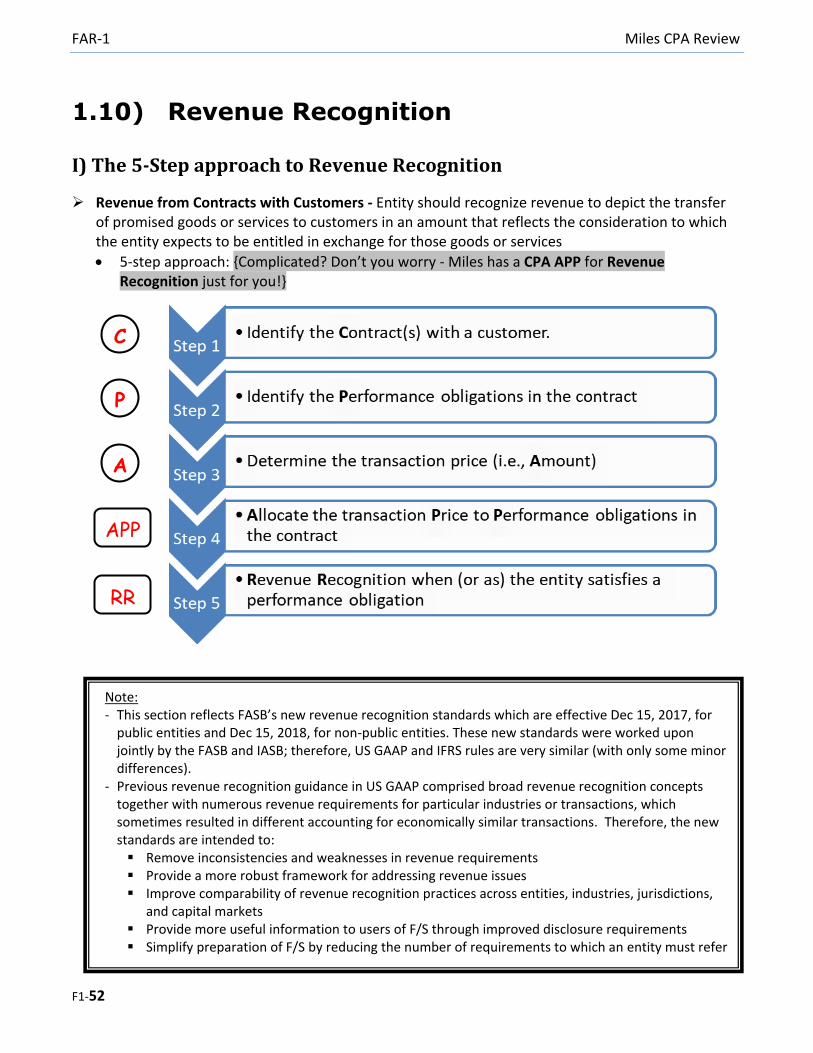

FAR-1 Miles CPA Review F1-52 1.10) Revenue Recognition I) The 5-Step approach to Revenue Recognition Revenue from Contracts with Customers - Entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services 5-step approach: ,Complicated? Don’t you worry - Miles has a CPA APP for Revenue Recognition just for you!} C APP P A RR Note: - This section reflects FASB’s new revenue recognition standards which are effective Dec 15, 2017, for public entities and Dec 15, 2018, for non-public entities. These new standards were worked upon jointly by the FASB and IASB; therefore, US GAAP and IFRS rules are very similar (with only some minor differences). - Previous revenue recognition guidance in US GAAP comprised broad revenue recognition concepts together with numerous revenue requirements for particular industries or transactions, which sometimes resulted in different accounting for economically similar transactions. Therefore, the new standards are intended to: Remove inconsistencies and weaknesses in revenue requirements Provide a more robust framework for addressing revenue issues Improve comparability of revenue recognition practices across entities, industries, jurisdictions, and capital markets Provide more useful information to users of F/S through improved disclosure requirements Simplify preparation of F/S by reducing the number of requirements to which an entity must refer

Transcript of 1.10) Revenue Recognition - Miles Education · 2019-12-27 · FAR-1 Miles CPA Review F1-521.10)...

FAR-1 Miles CPA Review

F1-52

1.10) Revenue Recognition

I) The 5-Step approach to Revenue Recognition

Revenue from Contracts with Customers - Entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services

5-step approach: ,Complicated? Don’t you worry - Miles has a CPA APP for Revenue Recognition just for you!}

C

APP

P

A

RR

Note: - This section reflects FASB’s new revenue recognition standards which are effective Dec 15, 2017, for

public entities and Dec 15, 2018, for non-public entities. These new standards were worked upon jointly by the FASB and IASB; therefore, US GAAP and IFRS rules are very similar (with only some minor differences).

- Previous revenue recognition guidance in US GAAP comprised broad revenue recognition concepts together with numerous revenue requirements for particular industries or transactions, which sometimes resulted in different accounting for economically similar transactions. Therefore, the new standards are intended to: Remove inconsistencies and weaknesses in revenue requirements Provide a more robust framework for addressing revenue issues Improve comparability of revenue recognition practices across entities, industries, jurisdictions,

and capital markets Provide more useful information to users of F/S through improved disclosure requirements Simplify preparation of F/S by reducing the number of requirements to which an entity must refer

Miles CPA Review FAR-1

F1-53

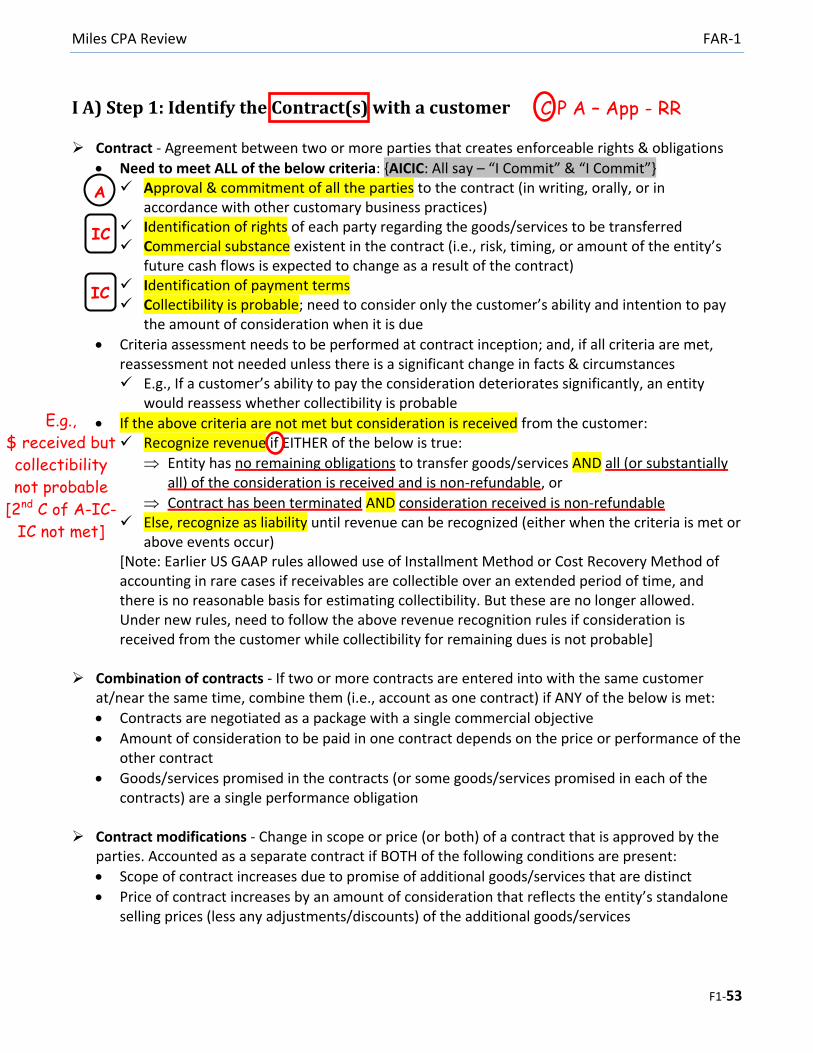

I A) Step 1: Identify the Contract(s) with a customer

Contract - Agreement between two or more parties that creates enforceable rights & obligations

Need to meet ALL of the below criteria: {AICIC: All say – “I Commit” & “I Commit”- Approval & commitment of all the parties to the contract (in writing, orally, or in

accordance with other customary business practices) Identification of rights of each party regarding the goods/services to be transferred Commercial substance existent in the contract (i.e., risk, timing, or amount of the entity’s

future cash flows is expected to change as a result of the contract) Identification of payment terms Collectibility is probable; need to consider only the customer’s ability and intention to pay

the amount of consideration when it is due

Criteria assessment needs to be performed at contract inception; and, if all criteria are met, reassessment not needed unless there is a significant change in facts & circumstances E.g., If a customer’s ability to pay the consideration deteriorates significantly, an entity

would reassess whether collectibility is probable

If the above criteria are not met but consideration is received from the customer: Recognize revenue if EITHER of the below is true:

Entity has no remaining obligations to transfer goods/services AND all (or substantially all) of the consideration is received and is non-refundable, or

Contract has been terminated AND consideration received is non-refundable Else, recognize as liability until revenue can be recognized (either when the criteria is met or

above events occur) [Note: Earlier US GAAP rules allowed use of Installment Method or Cost Recovery Method of accounting in rare cases if receivables are collectible over an extended period of time, and there is no reasonable basis for estimating collectibility. But these are no longer allowed. Under new rules, need to follow the above revenue recognition rules if consideration is received from the customer while collectibility for remaining dues is not probable]

Combination of contracts - If two or more contracts are entered into with the same customer

at/near the same time, combine them (i.e., account as one contract) if ANY of the below is met:

Contracts are negotiated as a package with a single commercial objective

Amount of consideration to be paid in one contract depends on the price or performance of the other contract

Goods/services promised in the contracts (or some goods/services promised in each of the contracts) are a single performance obligation

Contract modifications - Change in scope or price (or both) of a contract that is approved by the

parties. Accounted as a separate contract if BOTH of the following conditions are present:

Scope of contract increases due to promise of additional goods/services that are distinct

Price of contract increases by an amount of consideration that reflects the entity’s standalone selling prices (less any adjustments/discounts) of the additional goods/services

A

IC

IC

E.g.,

$ received but

collectibility

not probable

[2nd C of A-IC-

IC not met]

C P A – App - RR

FAR-1 Miles CPA Review

F1-54

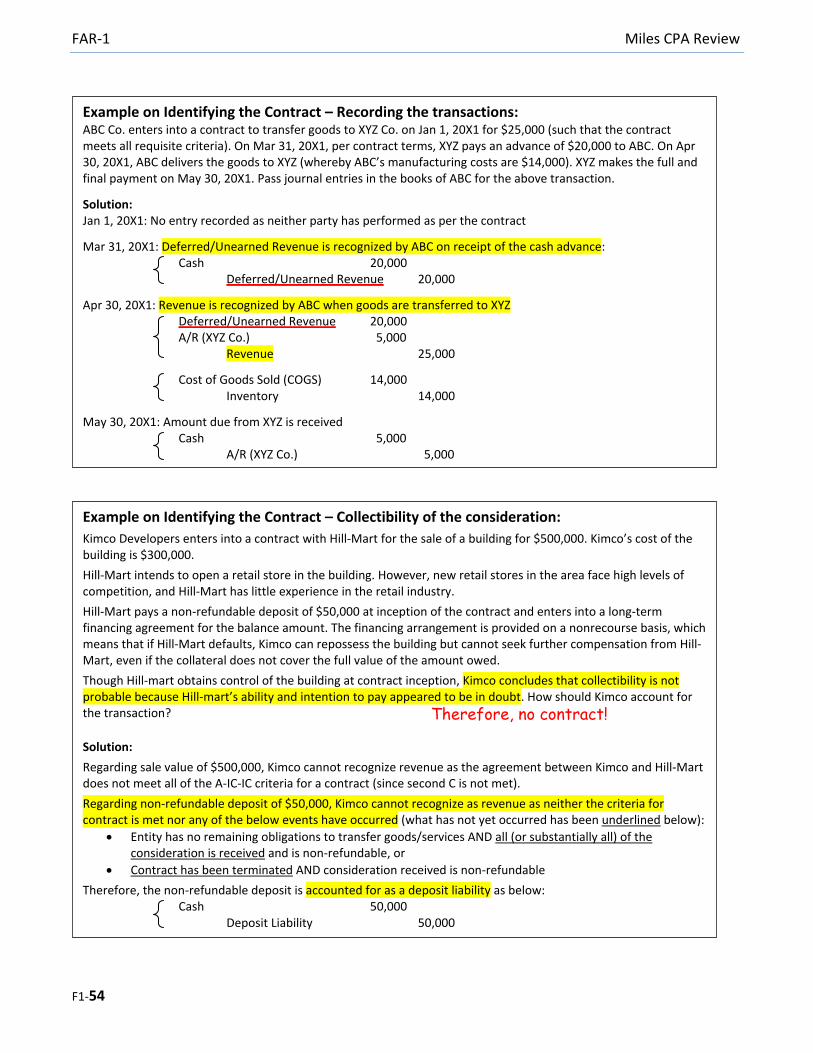

Example on Identifying the Contract – Recording the transactions: ABC Co. enters into a contract to transfer goods to XYZ Co. on Jan 1, 20X1 for $25,000 (such that the contract meets all requisite criteria). On Mar 31, 20X1, per contract terms, XYZ pays an advance of $20,000 to ABC. On Apr 30, 20X1, ABC delivers the goods to XYZ (whereby ABC’s manufacturing costs are $14,000). XYZ makes the full and final payment on May 30, 20X1. Pass journal entries in the books of ABC for the above transaction.

Solution: Jan 1, 20X1: No entry recorded as neither party has performed as per the contract

Mar 31, 20X1: Deferred/Unearned Revenue is recognized by ABC on receipt of the cash advance: Cash 20,000

Deferred/Unearned Revenue 20,000

Apr 30, 20X1: Revenue is recognized by ABC when goods are transferred to XYZ Deferred/Unearned Revenue 20,000 A/R (XYZ Co.) 5,000 Revenue 25,000

Cost of Goods Sold (COGS) 14,000 Inventory 14,000

May 30, 20X1: Amount due from XYZ is received Cash 5,000

A/R (XYZ Co.) 5,000

Example on Identifying the Contract – Collectibility of the consideration:

Kimco Developers enters into a contract with Hill-Mart for the sale of a building for $500,000. Kimco’s cost of the building is $300,000.

Hill-Mart intends to open a retail store in the building. However, new retail stores in the area face high levels of competition, and Hill-Mart has little experience in the retail industry.

Hill-Mart pays a non-refundable deposit of $50,000 at inception of the contract and enters into a long-term financing agreement for the balance amount. The financing arrangement is provided on a nonrecourse basis, which means that if Hill-Mart defaults, Kimco can repossess the building but cannot seek further compensation from Hill-Mart, even if the collateral does not cover the full value of the amount owed.

Though Hill-mart obtains control of the building at contract inception, Kimco concludes that collectibility is not probable because Hill-mart’s ability and intention to pay appeared to be in doubt. How should Kimco account for the transaction?

Solution:

Regarding sale value of $500,000, Kimco cannot recognize revenue as the agreement between Kimco and Hill-Mart does not meet all of the A-IC-IC criteria for a contract (since second C is not met).

Regarding non-refundable deposit of $50,000, Kimco cannot recognize as revenue as neither the criteria for contract is met nor any of the below events have occurred (what has not yet occurred has been underlined below):

Entity has no remaining obligations to transfer goods/services AND all (or substantially all) of the consideration is received and is non-refundable, or

Contract has been terminated AND consideration received is non-refundable

Therefore, the non-refundable deposit is accounted for as a deposit liability as below: Cash 50,000 Deposit Liability 50,000

Therefore, no contract!

Miles CPA Review FAR-1

F1-55

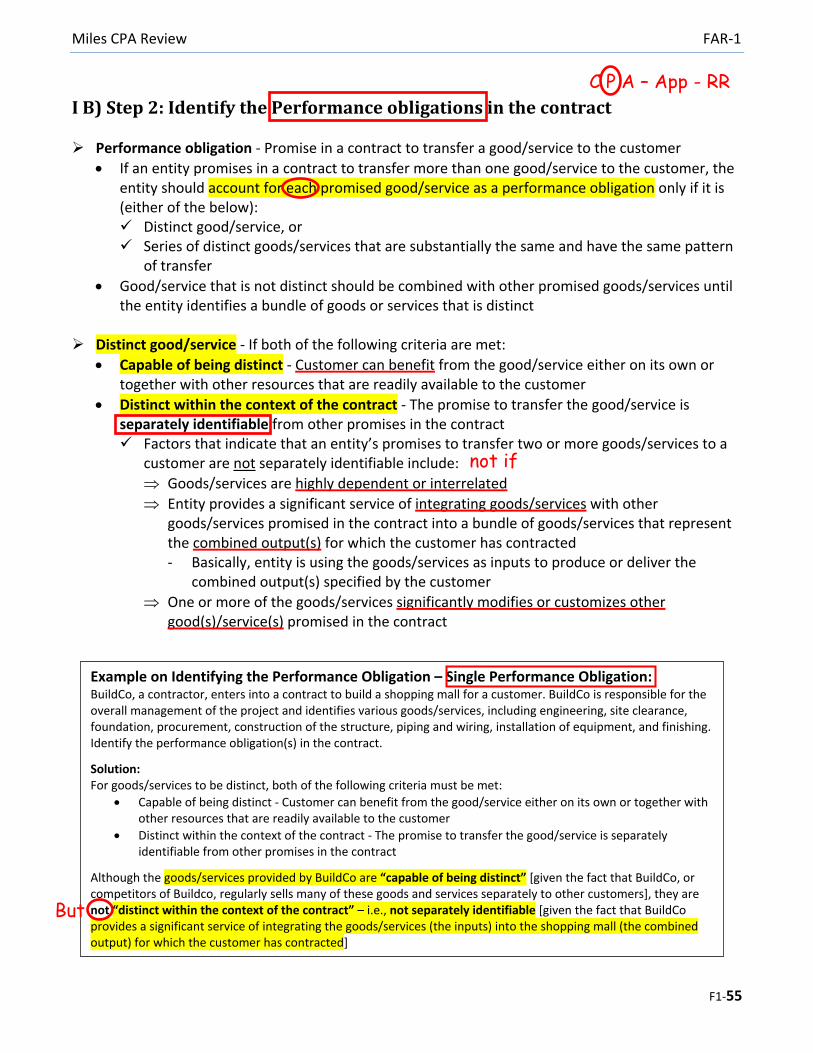

I B) Step 2: Identify the Performance obligations in the contract

Performance obligation - Promise in a contract to transfer a good/service to the customer

If an entity promises in a contract to transfer more than one good/service to the customer, the entity should account for each promised good/service as a performance obligation only if it is (either of the below): Distinct good/service, or Series of distinct goods/services that are substantially the same and have the same pattern

of transfer

Good/service that is not distinct should be combined with other promised goods/services until the entity identifies a bundle of goods or services that is distinct

Distinct good/service - If both of the following criteria are met:

Capable of being distinct - Customer can benefit from the good/service either on its own or together with other resources that are readily available to the customer

Distinct within the context of the contract - The promise to transfer the good/service is separately identifiable from other promises in the contract Factors that indicate that an entity’s promises to transfer two or more goods/services to a

customer are not separately identifiable include:

Goods/services are highly dependent or interrelated

Entity provides a significant service of integrating goods/services with other goods/services promised in the contract into a bundle of goods/services that represent the combined output(s) for which the customer has contracted - Basically, entity is using the goods/services as inputs to produce or deliver the

combined output(s) specified by the customer

One or more of the goods/services significantly modifies or customizes other good(s)/service(s) promised in the contract

C P A – App - RR

not if

Example on Identifying the Performance Obligation – Single Performance Obligation: BuildCo, a contractor, enters into a contract to build a shopping mall for a customer. BuildCo is responsible for the overall management of the project and identifies various goods/services, including engineering, site clearance, foundation, procurement, construction of the structure, piping and wiring, installation of equipment, and finishing. Identify the performance obligation(s) in the contract.

Solution: For goods/services to be distinct, both of the following criteria must be met:

Capable of being distinct - Customer can benefit from the good/service either on its own or together with other resources that are readily available to the customer

Distinct within the context of the contract - The promise to transfer the good/service is separately identifiable from other promises in the contract

Although the goods/services provided by BuildCo are “capable of being distinct” [given the fact that BuildCo, or competitors of Buildco, regularly sells many of these goods and services separately to other customers], they are not “distinct within the context of the contract” – i.e., not separately identifiable [given the fact that BuildCo provides a significant service of integrating the goods/services (the inputs) into the shopping mall (the combined output) for which the customer has contracted]

But

FAR-1 Miles CPA Review

F1-56

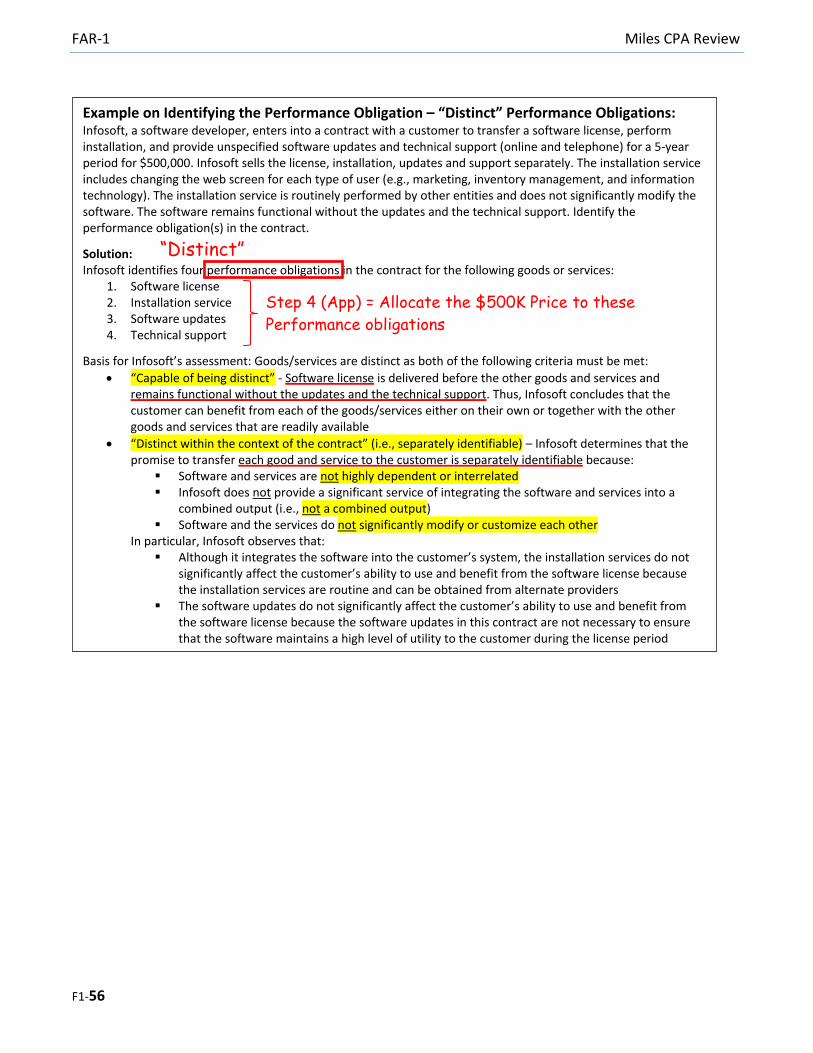

Example on Identifying the Performance Obligation – “Distinct” Performance Obligations: Infosoft, a software developer, enters into a contract with a customer to transfer a software license, perform installation, and provide unspecified software updates and technical support (online and telephone) for a 5-year period for $500,000. Infosoft sells the license, installation, updates and support separately. The installation service includes changing the web screen for each type of user (e.g., marketing, inventory management, and information technology). The installation service is routinely performed by other entities and does not significantly modify the software. The software remains functional without the updates and the technical support. Identify the performance obligation(s) in the contract.

Solution: Infosoft identifies four performance obligations in the contract for the following goods or services:

1. Software license 2. Installation service 3. Software updates 4. Technical support

Basis for Infosoft’s assessment: Goods/services are distinct as both of the following criteria must be met:

“Capable of being distinct” - Software license is delivered before the other goods and services and remains functional without the updates and the technical support. Thus, Infosoft concludes that the customer can benefit from each of the goods/services either on their own or together with the other goods and services that are readily available

“Distinct within the context of the contract” (i.e., separately identifiable) – Infosoft determines that the promise to transfer each good and service to the customer is separately identifiable because:

Software and services are not highly dependent or interrelated Infosoft does not provide a significant service of integrating the software and services into a

combined output (i.e., not a combined output) Software and the services do not significantly modify or customize each other

In particular, Infosoft observes that: Although it integrates the software into the customer’s system, the installation services do not

significantly affect the customer’s ability to use and benefit from the software license because the installation services are routine and can be obtained from alternate providers

The software updates do not significantly affect the customer’s ability to use and benefit from the software license because the software updates in this contract are not necessary to ensure that the software maintains a high level of utility to the customer during the license period

“Distinct”

Step 4 (App) = Allocate the $500K Price to these

Performance obligations

Miles CPA Review FAR-1

F1-57

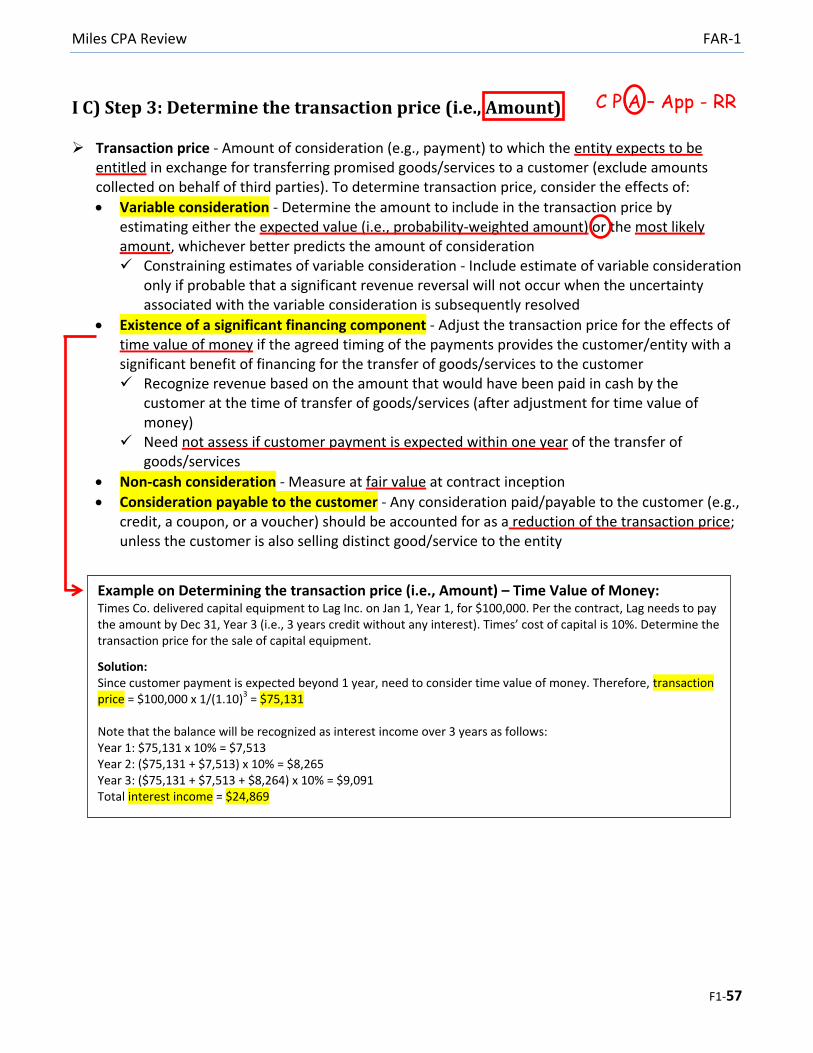

I C) Step 3: Determine the transaction price (i.e., Amount)

Transaction price - Amount of consideration (e.g., payment) to which the entity expects to be entitled in exchange for transferring promised goods/services to a customer (exclude amounts collected on behalf of third parties). To determine transaction price, consider the effects of:

Variable consideration - Determine the amount to include in the transaction price by estimating either the expected value (i.e., probability-weighted amount) or the most likely amount, whichever better predicts the amount of consideration Constraining estimates of variable consideration - Include estimate of variable consideration

only if probable that a significant revenue reversal will not occur when the uncertainty associated with the variable consideration is subsequently resolved

Existence of a significant financing component - Adjust the transaction price for the effects of time value of money if the agreed timing of the payments provides the customer/entity with a significant benefit of financing for the transfer of goods/services to the customer Recognize revenue based on the amount that would have been paid in cash by the

customer at the time of transfer of goods/services (after adjustment for time value of money)

Need not assess if customer payment is expected within one year of the transfer of goods/services

Non-cash consideration - Measure at fair value at contract inception

Consideration payable to the customer - Any consideration paid/payable to the customer (e.g., credit, a coupon, or a voucher) should be accounted for as a reduction of the transaction price; unless the customer is also selling distinct good/service to the entity

Example on Determining the transaction price (i.e., Amount) – Time Value of Money: Times Co. delivered capital equipment to Lag Inc. on Jan 1, Year 1, for $100,000. Per the contract, Lag needs to pay the amount by Dec 31, Year 3 (i.e., 3 years credit without any interest). Times’ cost of capital is 10%. Determine the transaction price for the sale of capital equipment.

Solution: Since customer payment is expected beyond 1 year, need to consider time value of money. Therefore, transaction price = $100,000 x 1/(1.10)3 = $75,131 Note that the balance will be recognized as interest income over 3 years as follows: Year 1: $75,131 x 10% = $7,513 Year 2: ($75,131 + $7,513) x 10% = $8,265 Year 3: ($75,131 + $7,513 + $8,264) x 10% = $9,091 Total interest income = $24,869

C P A – App - RR

FAR-1 Miles CPA Review

F1-58

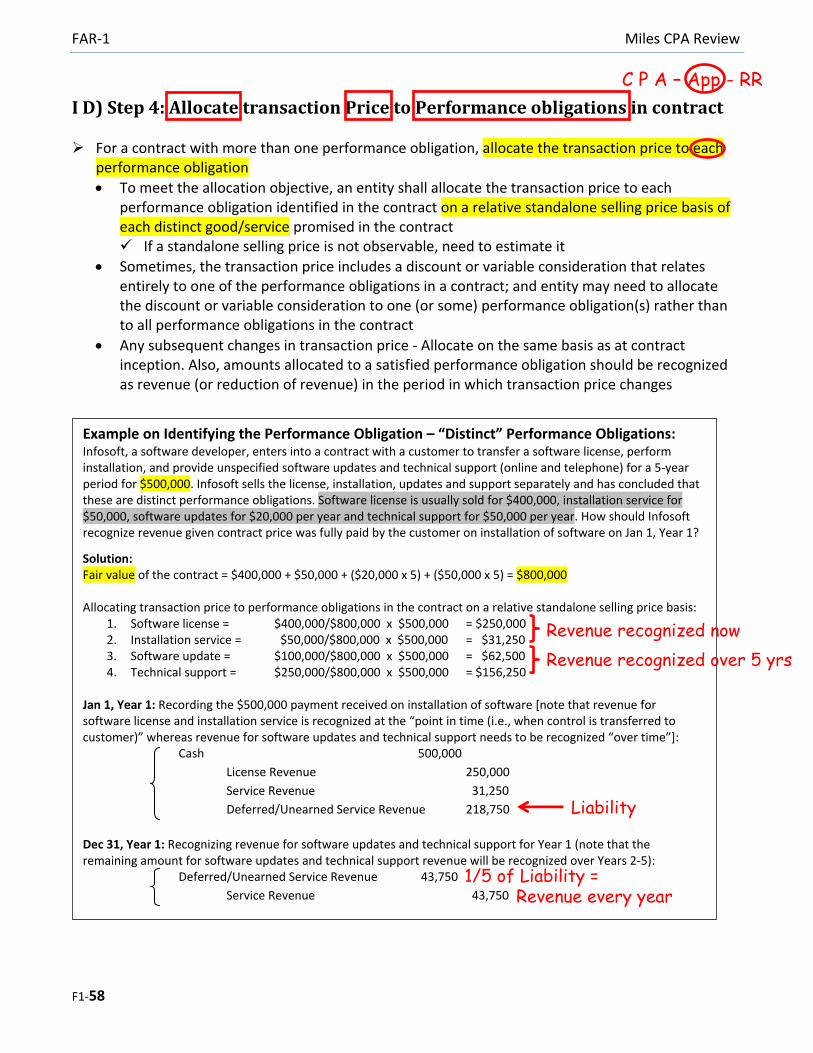

I D) Step 4: Allocate transaction Price to Performance obligations in contract

For a contract with more than one performance obligation, allocate the transaction price to each performance obligation

To meet the allocation objective, an entity shall allocate the transaction price to each performance obligation identified in the contract on a relative standalone selling price basis of each distinct good/service promised in the contract If a standalone selling price is not observable, need to estimate it

Sometimes, the transaction price includes a discount or variable consideration that relates entirely to one of the performance obligations in a contract; and entity may need to allocate the discount or variable consideration to one (or some) performance obligation(s) rather than to all performance obligations in the contract

Any subsequent changes in transaction price - Allocate on the same basis as at contract inception. Also, amounts allocated to a satisfied performance obligation should be recognized as revenue (or reduction of revenue) in the period in which transaction price changes

Example on Identifying the Performance Obligation – “Distinct” Performance Obligations: Infosoft, a software developer, enters into a contract with a customer to transfer a software license, perform installation, and provide unspecified software updates and technical support (online and telephone) for a 5-year period for $500,000. Infosoft sells the license, installation, updates and support separately and has concluded that these are distinct performance obligations. Software license is usually sold for $400,000, installation service for $50,000, software updates for $20,000 per year and technical support for $50,000 per year. How should Infosoft recognize revenue given contract price was fully paid by the customer on installation of software on Jan 1, Year 1?

Solution: Fair value of the contract = $400,000 + $50,000 + ($20,000 x 5) + ($50,000 x 5) = $800,000 Allocating transaction price to performance obligations in the contract on a relative standalone selling price basis:

1. Software license = $400,000/$800,000 x $500,000 = $250,000 2. Installation service = $50,000/$800,000 x $500,000 = $31,250 3. Software update = $100,000/$800,000 x $500,000 = $62,500 4. Technical support = $250,000/$800,000 x $500,000 = $156,250

Jan 1, Year 1: Recording the $500,000 payment received on installation of software [note that revenue for software license and installation service is recognized at the “point in time (i.e., when control is transferred to customer)” whereas revenue for software updates and technical support needs to be recognized “over time”+: Cash 500,000

License Revenue 250,000

Service Revenue 31,250

Deferred/Unearned Service Revenue 218,750

Dec 31, Year 1: Recognizing revenue for software updates and technical support for Year 1 (note that the remaining amount for software updates and technical support revenue will be recognized over Years 2-5): Deferred/Unearned Service Revenue 43,750

Service Revenue 43,750

C P A – App - RR

Revenue recognized now

Revenue recognized over 5 yrs

Liability

1/5 of Liability = Revenue every year

Miles CPA Review FAR-1

F1-59

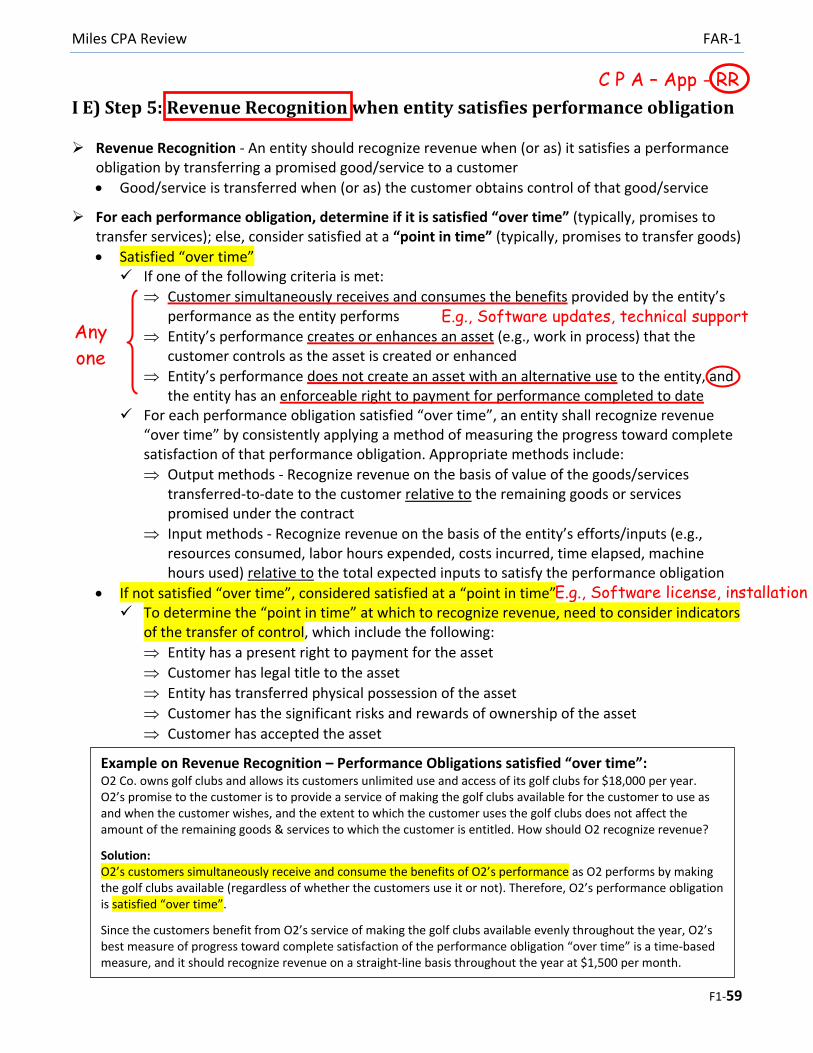

I E) Step 5: Revenue Recognition when entity satisfies performance obligation

Revenue Recognition - An entity should recognize revenue when (or as) it satisfies a performance obligation by transferring a promised good/service to a customer

Good/service is transferred when (or as) the customer obtains control of that good/service

For each performance obligation, determine if it is satisfied “over time” (typically, promises to transfer services); else, consider satisfied at a “point in time” (typically, promises to transfer goods)

Satisfied “over time” If one of the following criteria is met:

Customer simultaneously receives and consumes the benefits provided by the entity’s performance as the entity performs

Entity’s performance creates or enhances an asset (e.g., work in process) that the customer controls as the asset is created or enhanced

Entity’s performance does not create an asset with an alternative use to the entity, and the entity has an enforceable right to payment for performance completed to date

For each performance obligation satisfied “over time”, an entity shall recognize revenue “over time” by consistently applying a method of measuring the progress toward complete satisfaction of that performance obligation. Appropriate methods include:

Output methods - Recognize revenue on the basis of value of the goods/services transferred-to-date to the customer relative to the remaining goods or services promised under the contract

Input methods - Recognize revenue on the basis of the entity’s efforts/inputs (e.g., resources consumed, labor hours expended, costs incurred, time elapsed, machine hours used) relative to the total expected inputs to satisfy the performance obligation

If not satisfied “over time”, considered satisfied at a “point in time” To determine the “point in time” at which to recognize revenue, need to consider indicators

of the transfer of control, which include the following:

Entity has a present right to payment for the asset

Customer has legal title to the asset

Entity has transferred physical possession of the asset

Customer has the significant risks and rewards of ownership of the asset

Customer has accepted the asset

Example on Revenue Recognition – Performance Obligations satisfied “over time”: O2 Co. owns golf clubs and allows its customers unlimited use and access of its golf clubs for $18,000 per year. O2’s promise to the customer is to provide a service of making the golf clubs available for the customer to use as and when the customer wishes, and the extent to which the customer uses the golf clubs does not affect the amount of the remaining goods & services to which the customer is entitled. How should O2 recognize revenue?

Solution: O2’s customers simultaneously receive and consume the benefits of O2’s performance as O2 performs by making the golf clubs available (regardless of whether the customers use it or not). Therefore, O2’s performance obligation is satisfied “over time”.

Since the customers benefit from O2’s service of making the golf clubs available evenly throughout the year, O2’s best measure of progress toward complete satisfaction of the performance obligation “over time” is a time-based measure, and it should recognize revenue on a straight-line basis throughout the year at $1,500 per month.

Any

one

E.g., Software updates, technical support

C P A – App - RR

E.g., Software license, installation

FAR-1 Miles CPA Review

F1-60

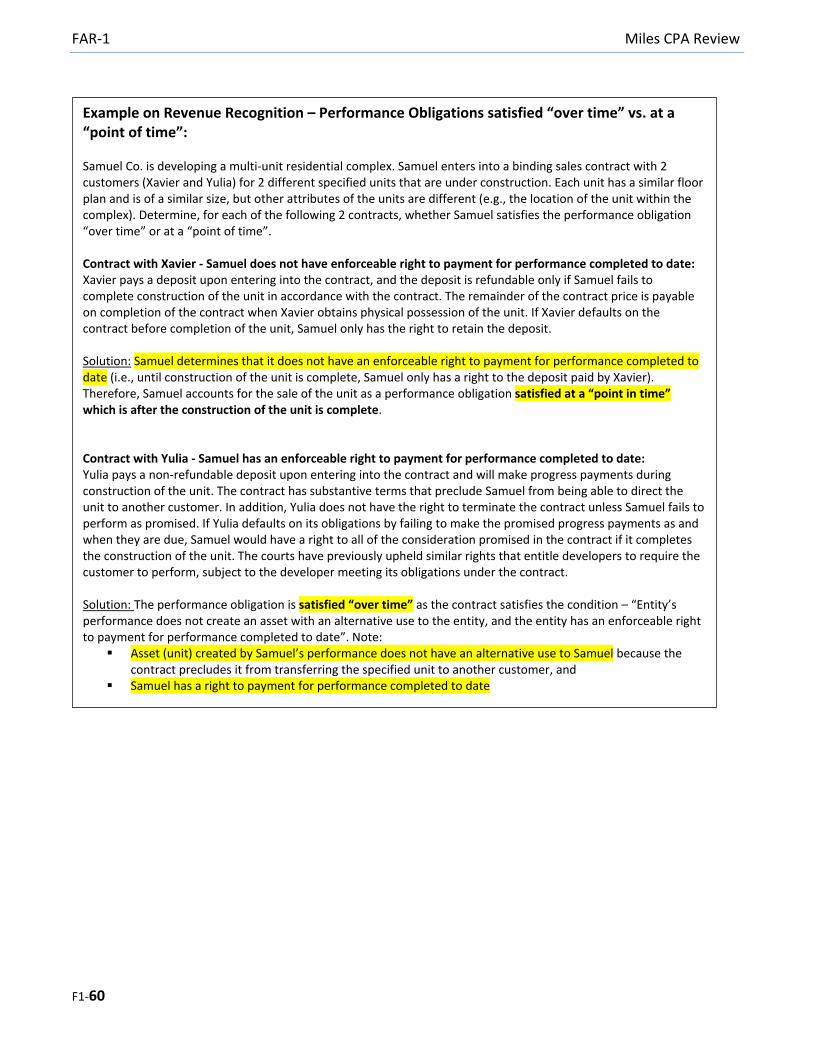

Example on Revenue Recognition – Performance Obligations satisfied “over time” vs. at a “point of time”: Samuel Co. is developing a multi-unit residential complex. Samuel enters into a binding sales contract with 2 customers (Xavier and Yulia) for 2 different specified units that are under construction. Each unit has a similar floor plan and is of a similar size, but other attributes of the units are different (e.g., the location of the unit within the complex). Determine, for each of the following 2 contracts, whether Samuel satisfies the performance obligation “over time” or at a “point of time”. Contract with Xavier - Samuel does not have enforceable right to payment for performance completed to date: Xavier pays a deposit upon entering into the contract, and the deposit is refundable only if Samuel fails to complete construction of the unit in accordance with the contract. The remainder of the contract price is payable on completion of the contract when Xavier obtains physical possession of the unit. If Xavier defaults on the contract before completion of the unit, Samuel only has the right to retain the deposit. Solution: Samuel determines that it does not have an enforceable right to payment for performance completed to date (i.e., until construction of the unit is complete, Samuel only has a right to the deposit paid by Xavier). Therefore, Samuel accounts for the sale of the unit as a performance obligation satisfied at a “point in time” which is after the construction of the unit is complete. Contract with Yulia - Samuel has an enforceable right to payment for performance completed to date: Yulia pays a non-refundable deposit upon entering into the contract and will make progress payments during construction of the unit. The contract has substantive terms that preclude Samuel from being able to direct the unit to another customer. In addition, Yulia does not have the right to terminate the contract unless Samuel fails to perform as promised. If Yulia defaults on its obligations by failing to make the promised progress payments as and when they are due, Samuel would have a right to all of the consideration promised in the contract if it completes the construction of the unit. The courts have previously upheld similar rights that entitle developers to require the customer to perform, subject to the developer meeting its obligations under the contract. Solution: The performance obligation is satisfied “over time” as the contract satisfies the condition – “Entity’s performance does not create an asset with an alternative use to the entity, and the entity has an enforceable right to payment for performance completed to date”. Note:

Asset (unit) created by Samuel’s performance does not have an alternative use to Samuel because the contract precludes it from transferring the specified unit to another customer, and

Samuel has a right to payment for performance completed to date

Miles CPA Review FAR-1

F1-61

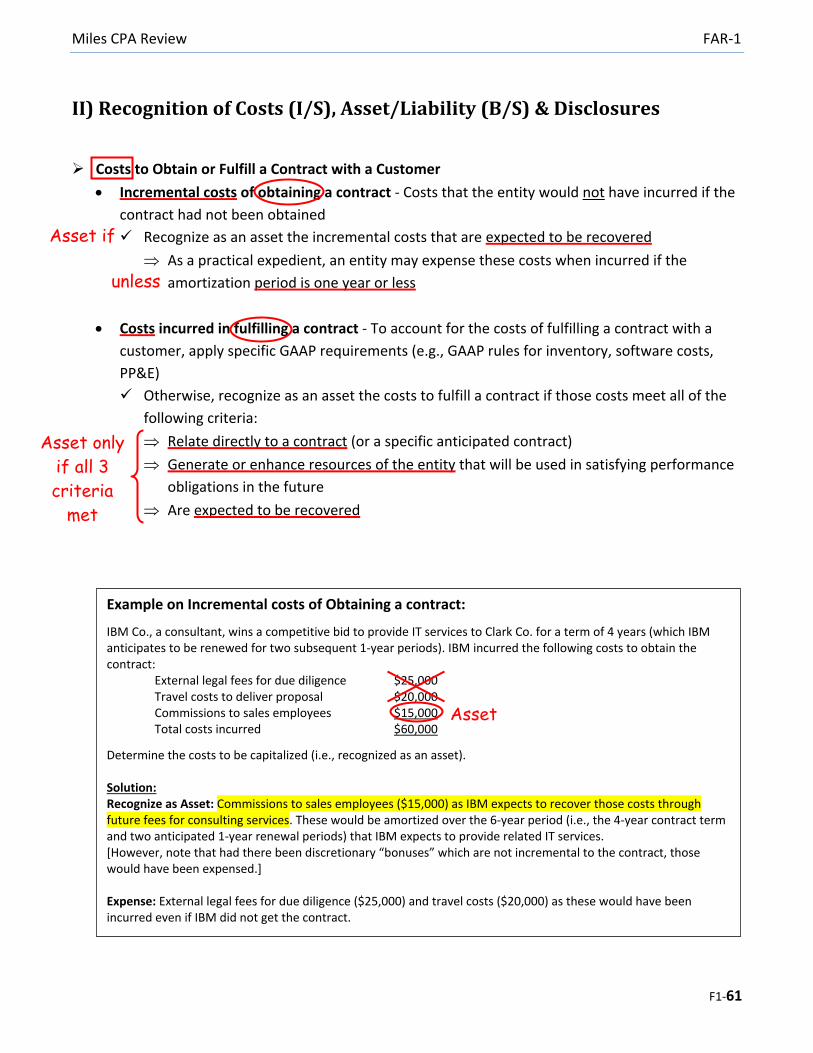

II) Recognition of Costs (I/S), Asset/Liability (B/S) & Disclosures

Costs to Obtain or Fulfill a Contract with a Customer

Incremental costs of obtaining a contract - Costs that the entity would not have incurred if the

contract had not been obtained

Recognize as an asset the incremental costs that are expected to be recovered

As a practical expedient, an entity may expense these costs when incurred if the

amortization period is one year or less

Costs incurred in fulfilling a contract - To account for the costs of fulfilling a contract with a

customer, apply specific GAAP requirements (e.g., GAAP rules for inventory, software costs,

PP&E)

Otherwise, recognize as an asset the costs to fulfill a contract if those costs meet all of the

following criteria:

Relate directly to a contract (or a specific anticipated contract)

Generate or enhance resources of the entity that will be used in satisfying performance

obligations in the future

Are expected to be recovered

Example on Incremental costs of Obtaining a contract:

IBM Co., a consultant, wins a competitive bid to provide IT services to Clark Co. for a term of 4 years (which IBM anticipates to be renewed for two subsequent 1-year periods). IBM incurred the following costs to obtain the contract: External legal fees for due diligence $25,000

Travel costs to deliver proposal $20,000 Commissions to sales employees $15,000 Total costs incurred $60,000

Determine the costs to be capitalized (i.e., recognized as an asset). Solution: Recognize as Asset: Commissions to sales employees ($15,000) as IBM expects to recover those costs through future fees for consulting services. These would be amortized over the 6-year period (i.e., the 4-year contract term and two anticipated 1-year renewal periods) that IBM expects to provide related IT services. *However, note that had there been discretionary “bonuses” which are not incremental to the contract, those would have been expensed.] Expense: External legal fees for due diligence ($25,000) and travel costs ($20,000) as these would have been incurred even if IBM did not get the contract.

Asset only

if all 3

criteria

met

Asset if

Asset

unless

FAR-1 Miles CPA Review

F1-62

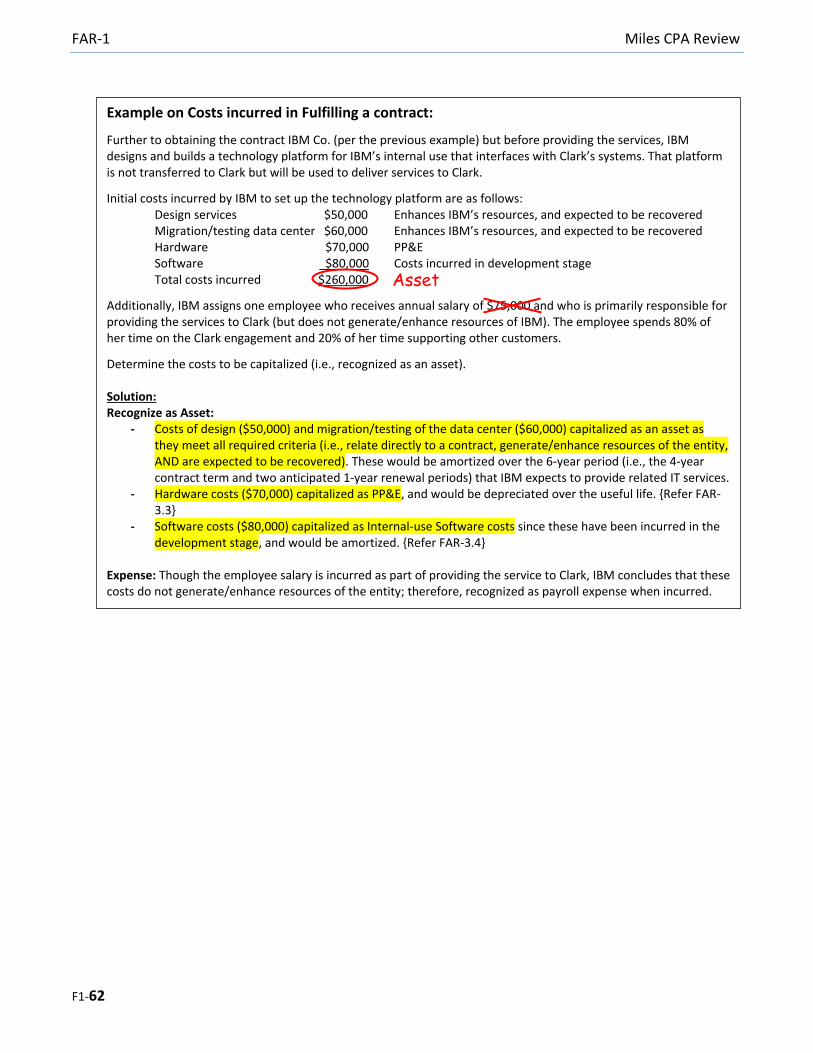

Example on Costs incurred in Fulfilling a contract:

Further to obtaining the contract IBM Co. (per the previous example) but before providing the services, IBM designs and builds a technology platform for IBM’s internal use that interfaces with Clark’s systems. That platform is not transferred to Clark but will be used to deliver services to Clark.

Initial costs incurred by IBM to set up the technology platform are as follows: Design services $50,000 Enhances IBM’s resources, and expected to be recovered Migration/testing data center $60,000 Enhances IBM’s resources, and expected to be recovered Hardware $70,000 PP&E Software $80,000 Costs incurred in development stage Total costs incurred $260,000

Additionally, IBM assigns one employee who receives annual salary of $75,000 and who is primarily responsible for providing the services to Clark (but does not generate/enhance resources of IBM). The employee spends 80% of her time on the Clark engagement and 20% of her time supporting other customers.

Determine the costs to be capitalized (i.e., recognized as an asset). Solution: Recognize as Asset:

- Costs of design ($50,000) and migration/testing of the data center ($60,000) capitalized as an asset as they meet all required criteria (i.e., relate directly to a contract, generate/enhance resources of the entity, AND are expected to be recovered). These would be amortized over the 6-year period (i.e., the 4-year contract term and two anticipated 1-year renewal periods) that IBM expects to provide related IT services.

- Hardware costs ($70,000) capitalized as PP&E, and would be depreciated over the useful life. {Refer FAR-3.3}

- Software costs ($80,000) capitalized as Internal-use Software costs since these have been incurred in the development stage, and would be amortized. {Refer FAR-3.4}

Expense: Though the employee salary is incurred as part of providing the service to Clark, IBM concludes that these costs do not generate/enhance resources of the entity; therefore, recognized as payroll expense when incurred.

Asset

Miles CPA Review FAR-1

F1-63

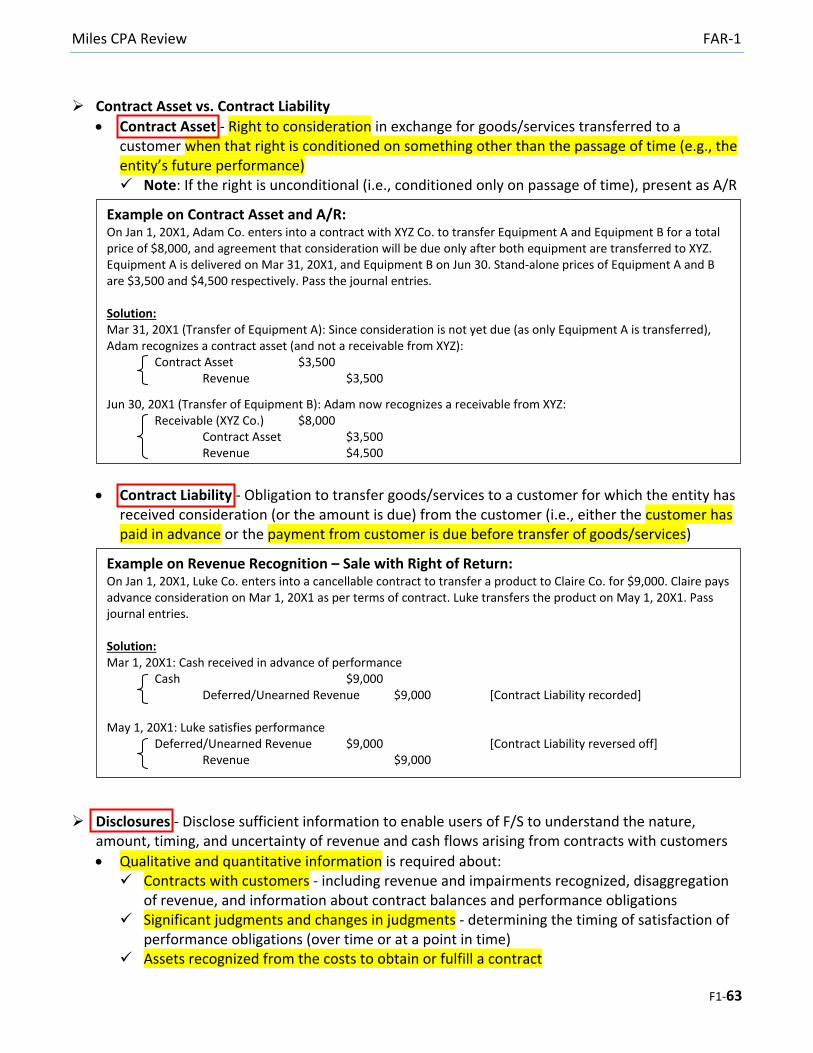

Contract Asset vs. Contract Liability

Contract Asset - Right to consideration in exchange for goods/services transferred to a customer when that right is conditioned on something other than the passage of time (e.g., the entity’s future performance) Note: If the right is unconditional (i.e., conditioned only on passage of time), present as A/R

Contract Liability - Obligation to transfer goods/services to a customer for which the entity has received consideration (or the amount is due) from the customer (i.e., either the customer has paid in advance or the payment from customer is due before transfer of goods/services)

Disclosures - Disclose sufficient information to enable users of F/S to understand the nature, amount, timing, and uncertainty of revenue and cash flows arising from contracts with customers

Qualitative and quantitative information is required about: Contracts with customers - including revenue and impairments recognized, disaggregation

of revenue, and information about contract balances and performance obligations Significant judgments and changes in judgments - determining the timing of satisfaction of

performance obligations (over time or at a point in time) Assets recognized from the costs to obtain or fulfill a contract

Example on Contract Asset and A/R: On Jan 1, 20X1, Adam Co. enters into a contract with XYZ Co. to transfer Equipment A and Equipment B for a total price of $8,000, and agreement that consideration will be due only after both equipment are transferred to XYZ. Equipment A is delivered on Mar 31, 20X1, and Equipment B on Jun 30. Stand-alone prices of Equipment A and B are $3,500 and $4,500 respectively. Pass the journal entries. Solution: Mar 31, 20X1 (Transfer of Equipment A): Since consideration is not yet due (as only Equipment A is transferred), Adam recognizes a contract asset (and not a receivable from XYZ):

Contract Asset $3,500 Revenue $3,500

Jun 30, 20X1 (Transfer of Equipment B): Adam now recognizes a receivable from XYZ: Receivable (XYZ Co.) $8,000

Contract Asset $3,500 Revenue $4,500

Example on Revenue Recognition – Sale with Right of Return: On Jan 1, 20X1, Luke Co. enters into a cancellable contract to transfer a product to Claire Co. for $9,000. Claire pays advance consideration on Mar 1, 20X1 as per terms of contract. Luke transfers the product on May 1, 20X1. Pass journal entries. Solution: Mar 1, 20X1: Cash received in advance of performance

Cash $9,000 Deferred/Unearned Revenue $9,000 [Contract Liability recorded] May 1, 20X1: Luke satisfies performance

Deferred/Unearned Revenue $9,000 [Contract Liability reversed off] Revenue $9,000

FAR-1 Miles CPA Review

F1-64

III) Certain Customer’s Rights & Obligations

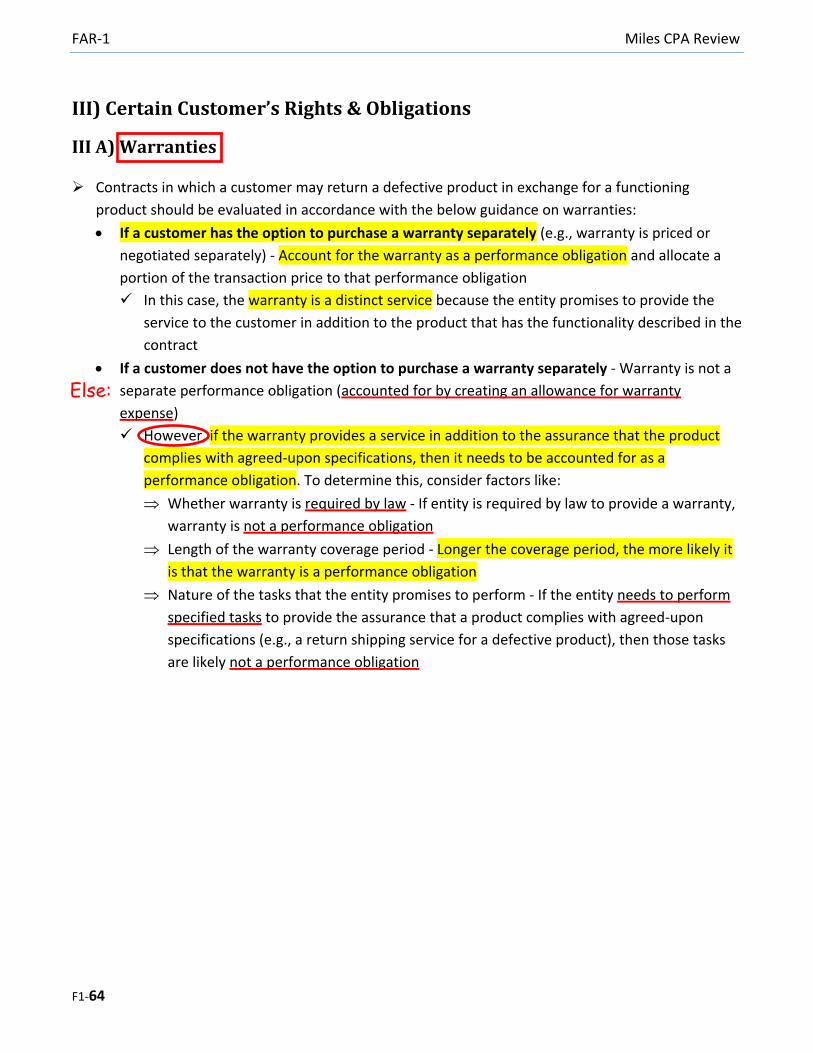

III A) Warranties

Contracts in which a customer may return a defective product in exchange for a functioning

product should be evaluated in accordance with the below guidance on warranties:

If a customer has the option to purchase a warranty separately (e.g., warranty is priced or

negotiated separately) - Account for the warranty as a performance obligation and allocate a

portion of the transaction price to that performance obligation

In this case, the warranty is a distinct service because the entity promises to provide the

service to the customer in addition to the product that has the functionality described in the

contract

If a customer does not have the option to purchase a warranty separately - Warranty is not a

separate performance obligation (accounted for by creating an allowance for warranty

expense)

However, if the warranty provides a service in addition to the assurance that the product

complies with agreed-upon specifications, then it needs to be accounted for as a

performance obligation. To determine this, consider factors like:

Whether warranty is required by law - If entity is required by law to provide a warranty,

warranty is not a performance obligation

Length of the warranty coverage period - Longer the coverage period, the more likely it

is that the warranty is a performance obligation

Nature of the tasks that the entity promises to perform - If the entity needs to perform

specified tasks to provide the assurance that a product complies with agreed-upon

specifications (e.g., a return shipping service for a defective product), then those tasks

are likely not a performance obligation

Else:

Miles CPA Review FAR-1

F1-65

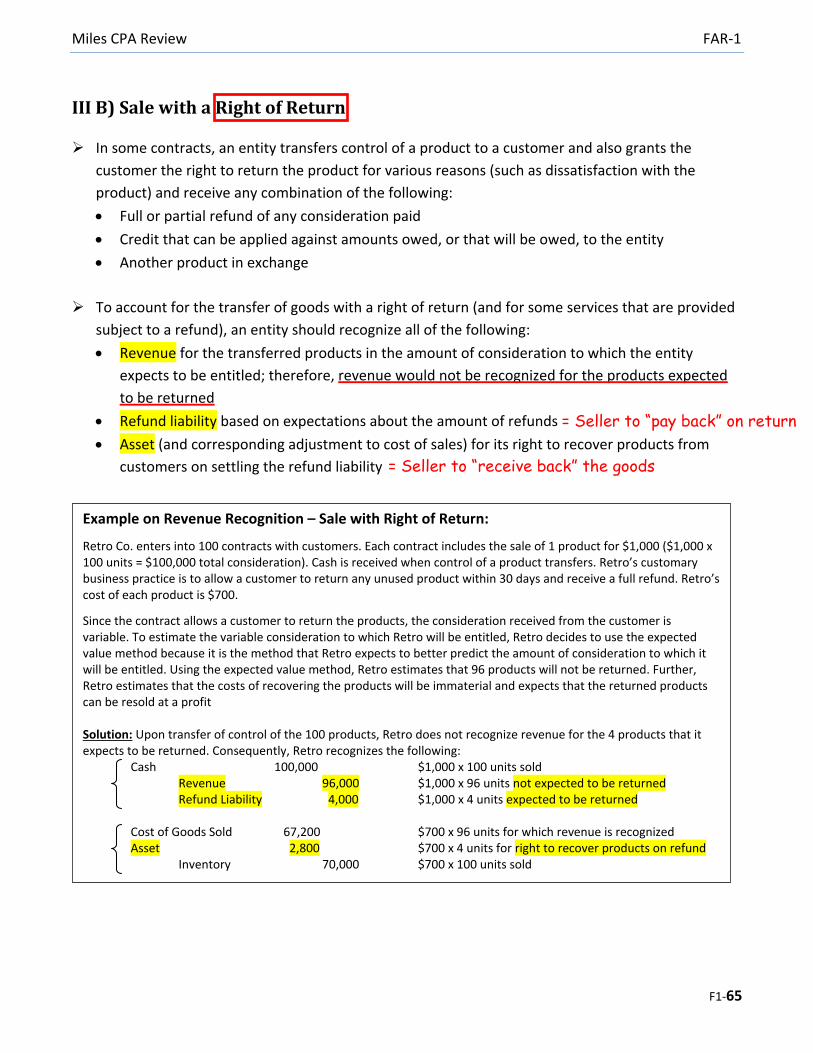

III B) Sale with a Right of Return

In some contracts, an entity transfers control of a product to a customer and also grants the

customer the right to return the product for various reasons (such as dissatisfaction with the

product) and receive any combination of the following:

Full or partial refund of any consideration paid

Credit that can be applied against amounts owed, or that will be owed, to the entity

Another product in exchange

To account for the transfer of goods with a right of return (and for some services that are provided

subject to a refund), an entity should recognize all of the following:

Revenue for the transferred products in the amount of consideration to which the entity

expects to be entitled; therefore, revenue would not be recognized for the products expected

to be returned

Refund liability based on expectations about the amount of refunds

Asset (and corresponding adjustment to cost of sales) for its right to recover products from

customers on settling the refund liability

Example on Revenue Recognition – Sale with Right of Return:

Retro Co. enters into 100 contracts with customers. Each contract includes the sale of 1 product for $1,000 ($1,000 x 100 units = $100,000 total consideration). Cash is received when control of a product transfers. Retro’s customary business practice is to allow a customer to return any unused product within 30 days and receive a full refund. Retro’s cost of each product is $700.

Since the contract allows a customer to return the products, the consideration received from the customer is variable. To estimate the variable consideration to which Retro will be entitled, Retro decides to use the expected value method because it is the method that Retro expects to better predict the amount of consideration to which it will be entitled. Using the expected value method, Retro estimates that 96 products will not be returned. Further, Retro estimates that the costs of recovering the products will be immaterial and expects that the returned products can be resold at a profit Solution: Upon transfer of control of the 100 products, Retro does not recognize revenue for the 4 products that it expects to be returned. Consequently, Retro recognizes the following: Cash 100,000 $1,000 x 100 units sold Revenue 96,000 $1,000 x 96 units not expected to be returned Refund Liability 4,000 $1,000 x 4 units expected to be returned Cost of Goods Sold 67,200 $700 x 96 units for which revenue is recognized Asset 2,800 $700 x 4 units for right to recover products on refund Inventory 70,000 $700 x 100 units sold

= Seller to “pay back” on return

= Seller to “receive back” the goods

FAR-1 Miles CPA Review

F1-66

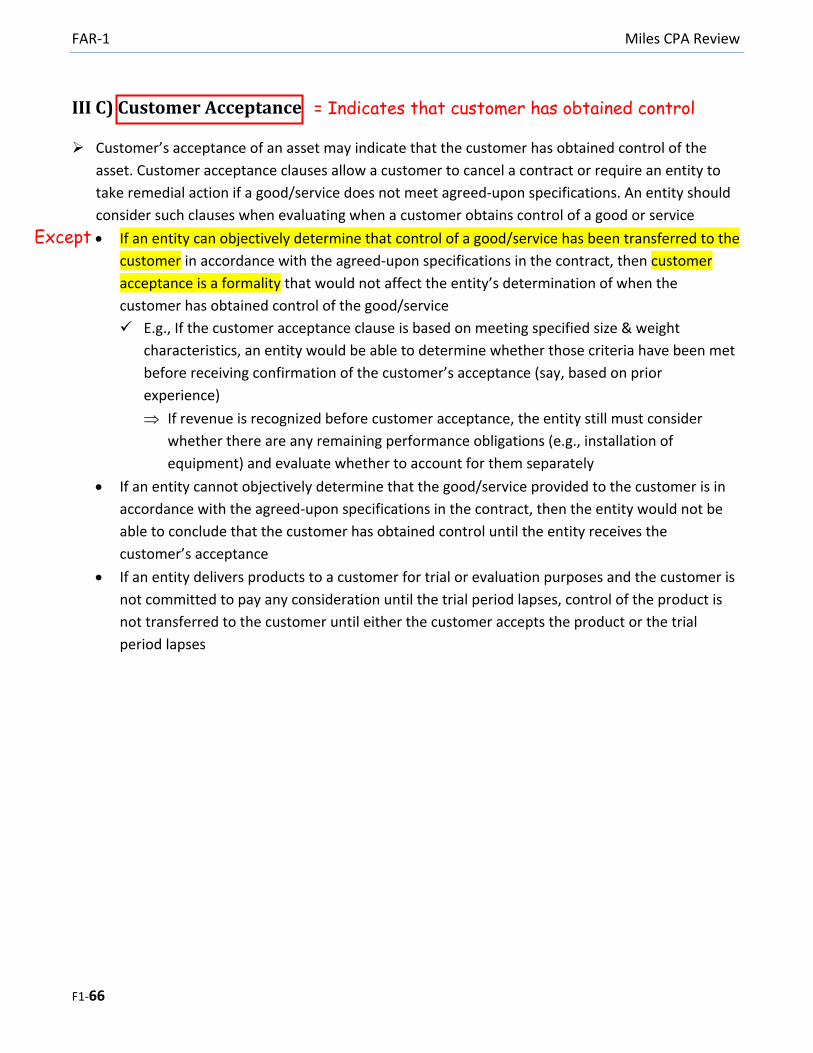

III C) Customer Acceptance

Customer’s acceptance of an asset may indicate that the customer has obtained control of the

asset. Customer acceptance clauses allow a customer to cancel a contract or require an entity to

take remedial action if a good/service does not meet agreed-upon specifications. An entity should

consider such clauses when evaluating when a customer obtains control of a good or service

If an entity can objectively determine that control of a good/service has been transferred to the

customer in accordance with the agreed-upon specifications in the contract, then customer

acceptance is a formality that would not affect the entity’s determination of when the

customer has obtained control of the good/service

E.g., If the customer acceptance clause is based on meeting specified size & weight

characteristics, an entity would be able to determine whether those criteria have been met

before receiving confirmation of the customer’s acceptance (say, based on prior

experience)

If revenue is recognized before customer acceptance, the entity still must consider

whether there are any remaining performance obligations (e.g., installation of

equipment) and evaluate whether to account for them separately

If an entity cannot objectively determine that the good/service provided to the customer is in

accordance with the agreed-upon specifications in the contract, then the entity would not be

able to conclude that the customer has obtained control until the entity receives the

customer’s acceptance

If an entity delivers products to a customer for trial or evaluation purposes and the customer is

not committed to pay any consideration until the trial period lapses, control of the product is

not transferred to the customer until either the customer accepts the product or the trial

period lapses

Except

= Indicates that customer has obtained control

Miles CPA Review FAR-1

F1-67

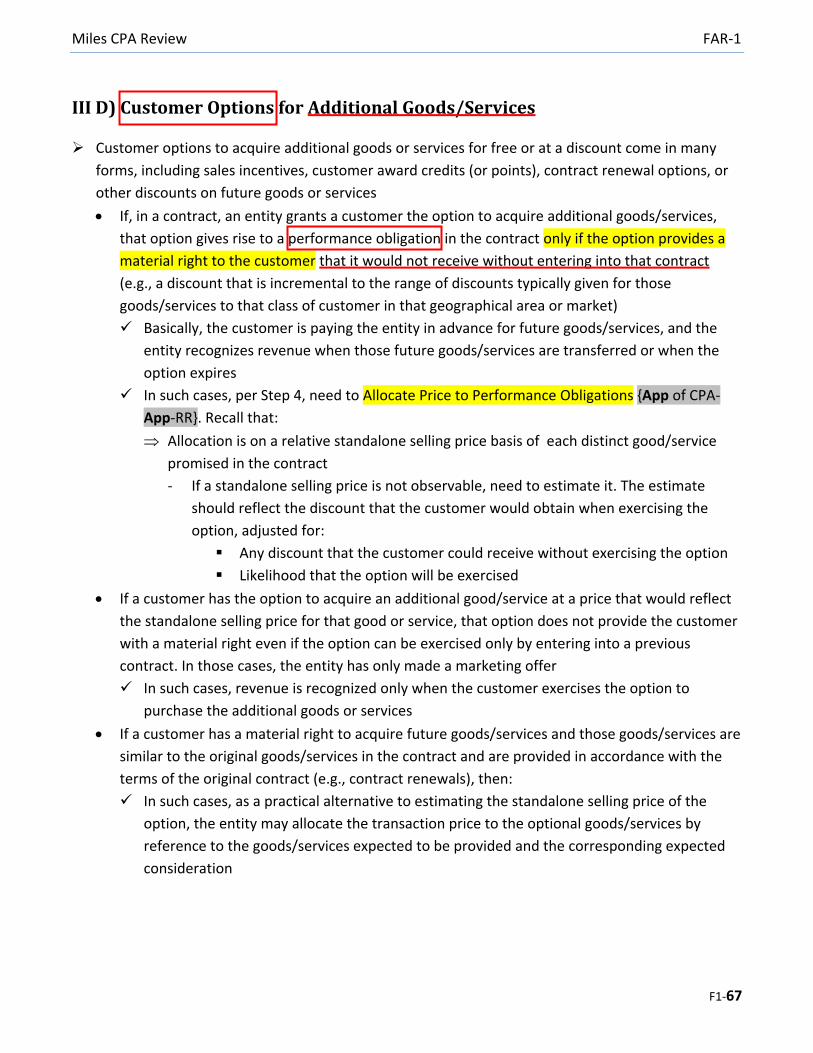

III D) Customer Options for Additional Goods/Services

Customer options to acquire additional goods or services for free or at a discount come in many

forms, including sales incentives, customer award credits (or points), contract renewal options, or

other discounts on future goods or services

If, in a contract, an entity grants a customer the option to acquire additional goods/services,

that option gives rise to a performance obligation in the contract only if the option provides a

material right to the customer that it would not receive without entering into that contract

(e.g., a discount that is incremental to the range of discounts typically given for those

goods/services to that class of customer in that geographical area or market)

Basically, the customer is paying the entity in advance for future goods/services, and the

entity recognizes revenue when those future goods/services are transferred or when the

option expires

In such cases, per Step 4, need to Allocate Price to Performance Obligations {App of CPA-

App-RR}. Recall that:

Allocation is on a relative standalone selling price basis of each distinct good/service

promised in the contract

- If a standalone selling price is not observable, need to estimate it. The estimate

should reflect the discount that the customer would obtain when exercising the

option, adjusted for:

Any discount that the customer could receive without exercising the option

Likelihood that the option will be exercised

If a customer has the option to acquire an additional good/service at a price that would reflect

the standalone selling price for that good or service, that option does not provide the customer

with a material right even if the option can be exercised only by entering into a previous

contract. In those cases, the entity has only made a marketing offer

In such cases, revenue is recognized only when the customer exercises the option to

purchase the additional goods or services

If a customer has a material right to acquire future goods/services and those goods/services are

similar to the original goods/services in the contract and are provided in accordance with the

terms of the original contract (e.g., contract renewals), then:

In such cases, as a practical alternative to estimating the standalone selling price of the

option, the entity may allocate the transaction price to the optional goods/services by

reference to the goods/services expected to be provided and the corresponding expected

consideration

FAR-1 Miles CPA Review

F1-68

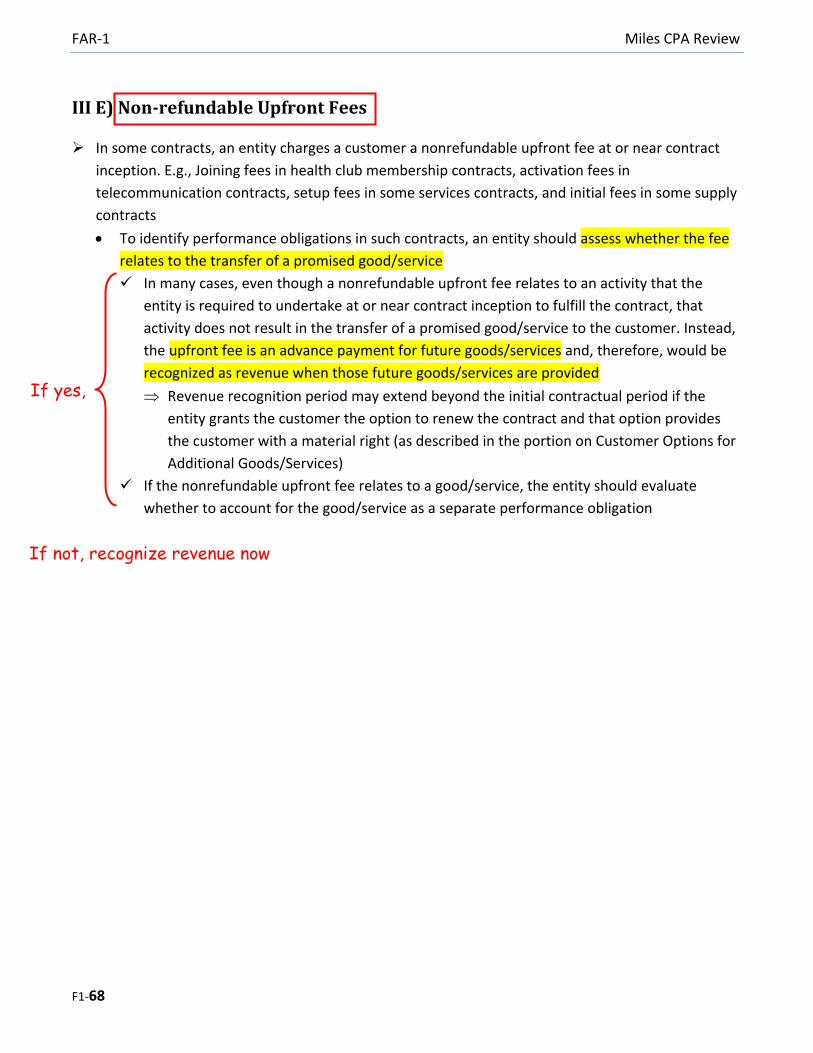

III E) Non-refundable Upfront Fees

In some contracts, an entity charges a customer a nonrefundable upfront fee at or near contract

inception. E.g., Joining fees in health club membership contracts, activation fees in

telecommunication contracts, setup fees in some services contracts, and initial fees in some supply

contracts

To identify performance obligations in such contracts, an entity should assess whether the fee

relates to the transfer of a promised good/service

In many cases, even though a nonrefundable upfront fee relates to an activity that the

entity is required to undertake at or near contract inception to fulfill the contract, that

activity does not result in the transfer of a promised good/service to the customer. Instead,

the upfront fee is an advance payment for future goods/services and, therefore, would be

recognized as revenue when those future goods/services are provided

Revenue recognition period may extend beyond the initial contractual period if the

entity grants the customer the option to renew the contract and that option provides

the customer with a material right (as described in the portion on Customer Options for

Additional Goods/Services)

If the nonrefundable upfront fee relates to a good/service, the entity should evaluate

whether to account for the good/service as a separate performance obligation

If not, recognize revenue now

If yes,

Miles CPA Review FAR-1

F1-69

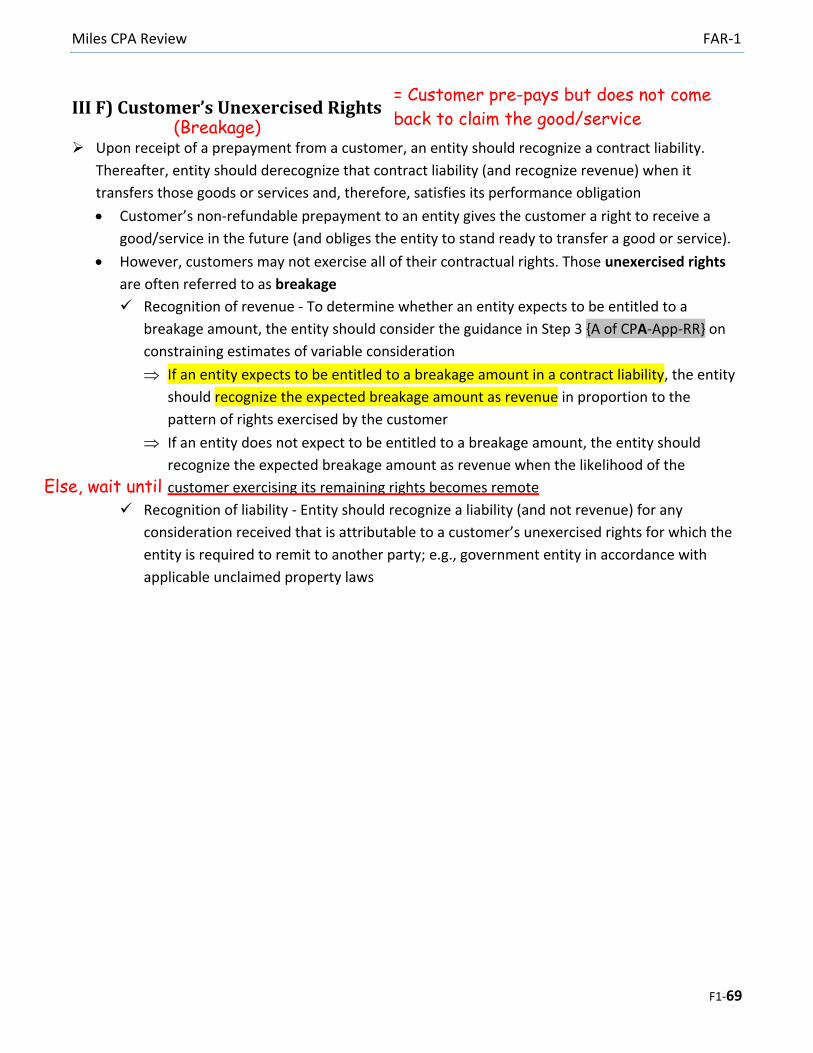

III F) Customer’s Unexercised Rights

Upon receipt of a prepayment from a customer, an entity should recognize a contract liability.

Thereafter, entity should derecognize that contract liability (and recognize revenue) when it

transfers those goods or services and, therefore, satisfies its performance obligation

Customer’s non-refundable prepayment to an entity gives the customer a right to receive a

good/service in the future (and obliges the entity to stand ready to transfer a good or service).

However, customers may not exercise all of their contractual rights. Those unexercised rights

are often referred to as breakage

Recognition of revenue - To determine whether an entity expects to be entitled to a

breakage amount, the entity should consider the guidance in Step 3 {A of CPA-App-RR} on

constraining estimates of variable consideration

If an entity expects to be entitled to a breakage amount in a contract liability, the entity

should recognize the expected breakage amount as revenue in proportion to the

pattern of rights exercised by the customer

If an entity does not expect to be entitled to a breakage amount, the entity should

recognize the expected breakage amount as revenue when the likelihood of the

customer exercising its remaining rights becomes remote

Recognition of liability - Entity should recognize a liability (and not revenue) for any

consideration received that is attributable to a customer’s unexercised rights for which the

entity is required to remit to another party; e.g., government entity in accordance with

applicable unclaimed property laws

(Breakage)

= Customer pre-pays but does not come

back to claim the good/service

Else, wait until

FAR-1 Miles CPA Review

F1-70

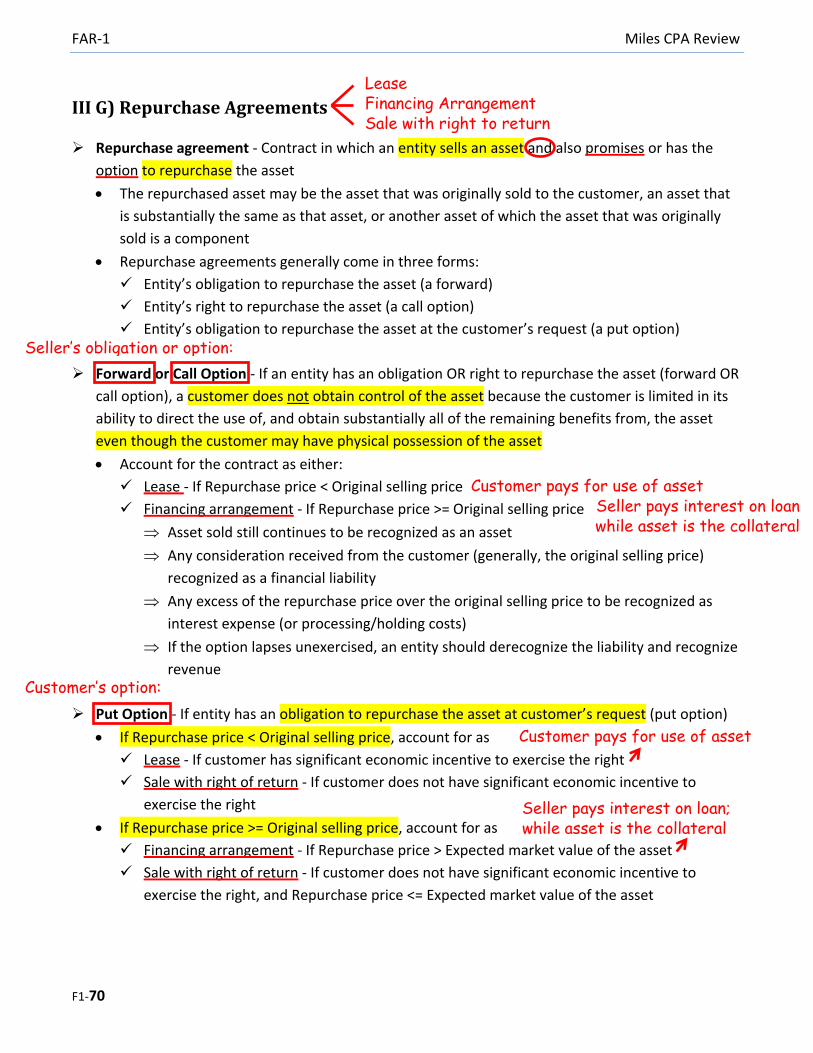

III G) Repurchase Agreements

Repurchase agreement - Contract in which an entity sells an asset and also promises or has the

option to repurchase the asset

The repurchased asset may be the asset that was originally sold to the customer, an asset that

is substantially the same as that asset, or another asset of which the asset that was originally

sold is a component

Repurchase agreements generally come in three forms:

Entity’s obligation to repurchase the asset (a forward)

Entity’s right to repurchase the asset (a call option)

Entity’s obligation to repurchase the asset at the customer’s request (a put option)

Forward or Call Option - If an entity has an obligation OR right to repurchase the asset (forward OR

call option), a customer does not obtain control of the asset because the customer is limited in its

ability to direct the use of, and obtain substantially all of the remaining benefits from, the asset

even though the customer may have physical possession of the asset

Account for the contract as either:

Lease - If Repurchase price < Original selling price

Financing arrangement - If Repurchase price >= Original selling price

Asset sold still continues to be recognized as an asset

Any consideration received from the customer (generally, the original selling price)

recognized as a financial liability

Any excess of the repurchase price over the original selling price to be recognized as

interest expense (or processing/holding costs)

If the option lapses unexercised, an entity should derecognize the liability and recognize

revenue

Put Option - If entity has an obligation to repurchase the asset at customer’s request (put option)

If Repurchase price < Original selling price, account for as

Lease - If customer has significant economic incentive to exercise the right

Sale with right of return - If customer does not have significant economic incentive to

exercise the right

If Repurchase price >= Original selling price, account for as

Financing arrangement - If Repurchase price > Expected market value of the asset

Sale with right of return - If customer does not have significant economic incentive to

exercise the right, and Repurchase price <= Expected market value of the asset

Seller’s obligation or option:

Customer’s option:

Customer pays for use of asset Seller pays interest on loan while asset is the collateral

Customer pays for use of asset

Lease Financing Arrangement Sale with right to return

Seller pays interest on loan; while asset is the collateral

Miles CPA Review FAR-1

F1-71

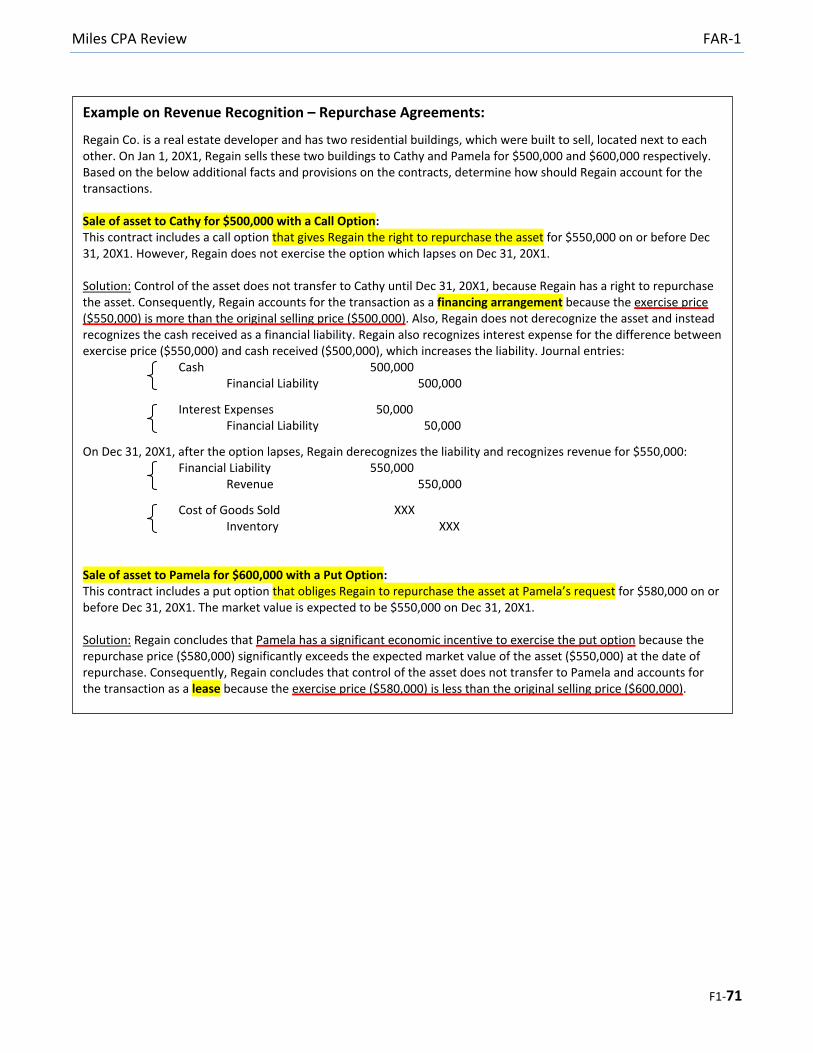

Example on Revenue Recognition – Repurchase Agreements:

Regain Co. is a real estate developer and has two residential buildings, which were built to sell, located next to each other. On Jan 1, 20X1, Regain sells these two buildings to Cathy and Pamela for $500,000 and $600,000 respectively. Based on the below additional facts and provisions on the contracts, determine how should Regain account for the transactions. Sale of asset to Cathy for $500,000 with a Call Option: This contract includes a call option that gives Regain the right to repurchase the asset for $550,000 on or before Dec 31, 20X1. However, Regain does not exercise the option which lapses on Dec 31, 20X1. Solution: Control of the asset does not transfer to Cathy until Dec 31, 20X1, because Regain has a right to repurchase the asset. Consequently, Regain accounts for the transaction as a financing arrangement because the exercise price ($550,000) is more than the original selling price ($500,000). Also, Regain does not derecognize the asset and instead recognizes the cash received as a financial liability. Regain also recognizes interest expense for the difference between exercise price ($550,000) and cash received ($500,000), which increases the liability. Journal entries: Cash 500,000 Financial Liability 500,000

Interest Expenses 50,000 Financial Liability 50,000

On Dec 31, 20X1, after the option lapses, Regain derecognizes the liability and recognizes revenue for $550,000: Financial Liability 550,000 Revenue 550,000

Cost of Goods Sold XXX Inventory XXX Sale of asset to Pamela for $600,000 with a Put Option: This contract includes a put option that obliges Regain to repurchase the asset at Pamela’s request for $580,000 on or before Dec 31, 20X1. The market value is expected to be $550,000 on Dec 31, 20X1. Solution: Regain concludes that Pamela has a significant economic incentive to exercise the put option because the repurchase price ($580,000) significantly exceeds the expected market value of the asset ($550,000) at the date of repurchase. Consequently, Regain concludes that control of the asset does not transfer to Pamela and accounts for the transaction as a lease because the exercise price ($580,000) is less than the original selling price ($600,000).

FAR-1 Miles CPA Review

F1-72

IV) Specific Arrangements

IV A) Principal vs. Agent Considerations

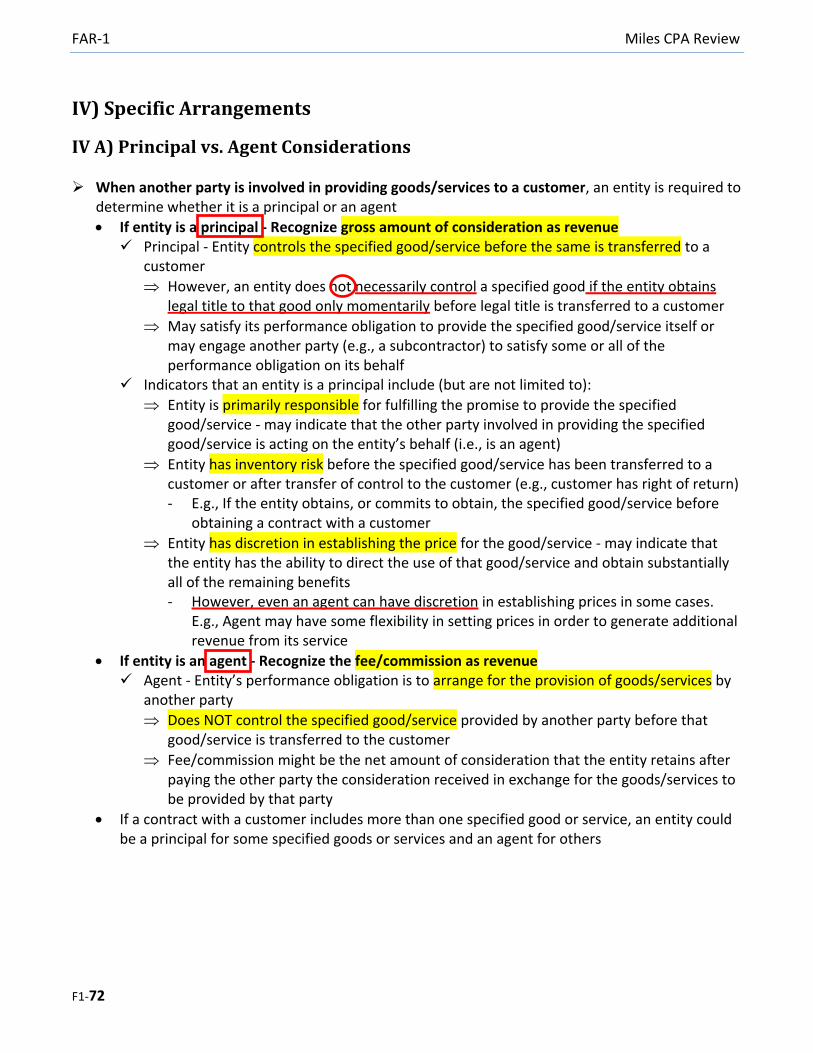

When another party is involved in providing goods/services to a customer, an entity is required to determine whether it is a principal or an agent

If entity is a principal - Recognize gross amount of consideration as revenue Principal - Entity controls the specified good/service before the same is transferred to a

customer

However, an entity does not necessarily control a specified good if the entity obtains legal title to that good only momentarily before legal title is transferred to a customer

May satisfy its performance obligation to provide the specified good/service itself or may engage another party (e.g., a subcontractor) to satisfy some or all of the performance obligation on its behalf

Indicators that an entity is a principal include (but are not limited to):

Entity is primarily responsible for fulfilling the promise to provide the specified good/service - may indicate that the other party involved in providing the specified good/service is acting on the entity’s behalf (i.e., is an agent)

Entity has inventory risk before the specified good/service has been transferred to a customer or after transfer of control to the customer (e.g., customer has right of return) - E.g., If the entity obtains, or commits to obtain, the specified good/service before

obtaining a contract with a customer

Entity has discretion in establishing the price for the good/service - may indicate that the entity has the ability to direct the use of that good/service and obtain substantially all of the remaining benefits - However, even an agent can have discretion in establishing prices in some cases.

E.g., Agent may have some flexibility in setting prices in order to generate additional revenue from its service

If entity is an agent - Recognize the fee/commission as revenue Agent - Entity’s performance obligation is to arrange for the provision of goods/services by

another party

Does NOT control the specified good/service provided by another party before that good/service is transferred to the customer

Fee/commission might be the net amount of consideration that the entity retains after paying the other party the consideration received in exchange for the goods/services to be provided by that party

If a contract with a customer includes more than one specified good or service, an entity could be a principal for some specified goods or services and an agent for others

Miles CPA Review FAR-1

F1-73

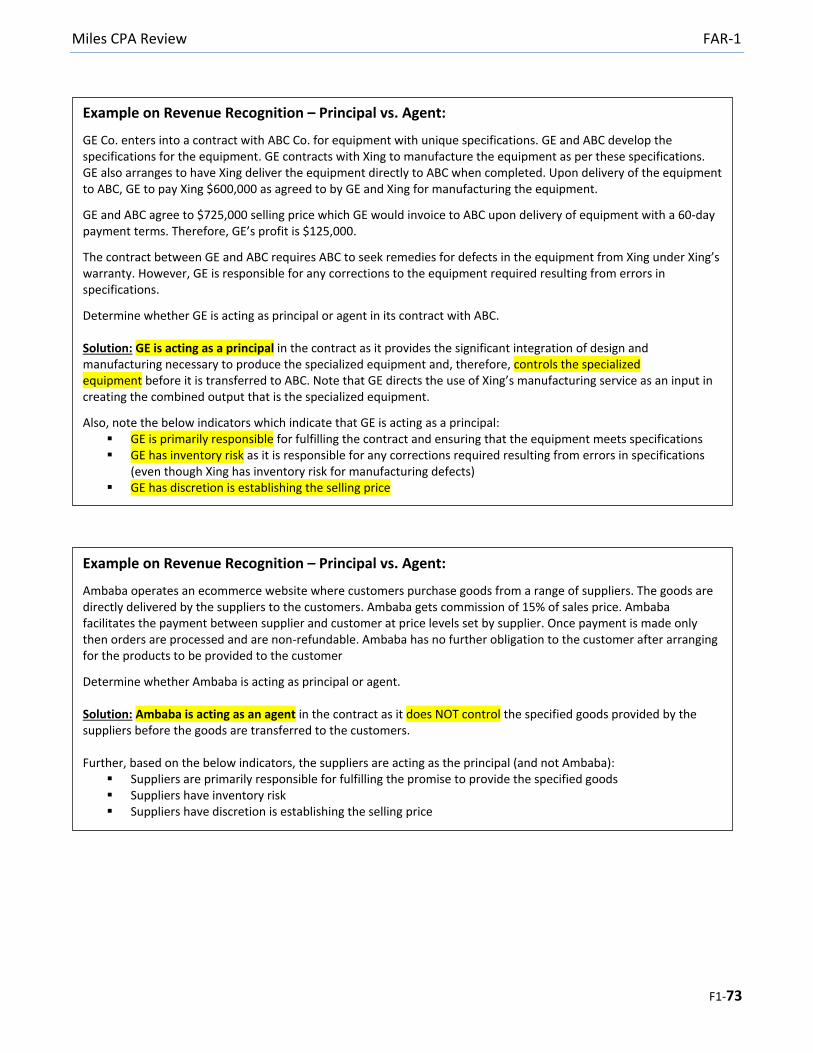

Example on Revenue Recognition – Principal vs. Agent:

GE Co. enters into a contract with ABC Co. for equipment with unique specifications. GE and ABC develop the specifications for the equipment. GE contracts with Xing to manufacture the equipment as per these specifications. GE also arranges to have Xing deliver the equipment directly to ABC when completed. Upon delivery of the equipment to ABC, GE to pay Xing $600,000 as agreed to by GE and Xing for manufacturing the equipment.

GE and ABC agree to $725,000 selling price which GE would invoice to ABC upon delivery of equipment with a 60-day payment terms. Therefore, GE’s profit is $125,000.

The contract between GE and ABC requires ABC to seek remedies for defects in the equipment from Xing under Xing’s warranty. However, GE is responsible for any corrections to the equipment required resulting from errors in specifications.

Determine whether GE is acting as principal or agent in its contract with ABC. Solution: GE is acting as a principal in the contract as it provides the significant integration of design and manufacturing necessary to produce the specialized equipment and, therefore, controls the specialized equipment before it is transferred to ABC. Note that GE directs the use of Xing’s manufacturing service as an input in creating the combined output that is the specialized equipment.

Also, note the below indicators which indicate that GE is acting as a principal: GE is primarily responsible for fulfilling the contract and ensuring that the equipment meets specifications GE has inventory risk as it is responsible for any corrections required resulting from errors in specifications

(even though Xing has inventory risk for manufacturing defects) GE has discretion is establishing the selling price

Example on Revenue Recognition – Principal vs. Agent:

Ambaba operates an ecommerce website where customers purchase goods from a range of suppliers. The goods are directly delivered by the suppliers to the customers. Ambaba gets commission of 15% of sales price. Ambaba facilitates the payment between supplier and customer at price levels set by supplier. Once payment is made only then orders are processed and are non-refundable. Ambaba has no further obligation to the customer after arranging for the products to be provided to the customer

Determine whether Ambaba is acting as principal or agent. Solution: Ambaba is acting as an agent in the contract as it does NOT control the specified goods provided by the suppliers before the goods are transferred to the customers. Further, based on the below indicators, the suppliers are acting as the principal (and not Ambaba):

Suppliers are primarily responsible for fulfilling the promise to provide the specified goods Suppliers have inventory risk Suppliers have discretion is establishing the selling price

FAR-1 Miles CPA Review

F1-74

IV B) Consignment Arrangements

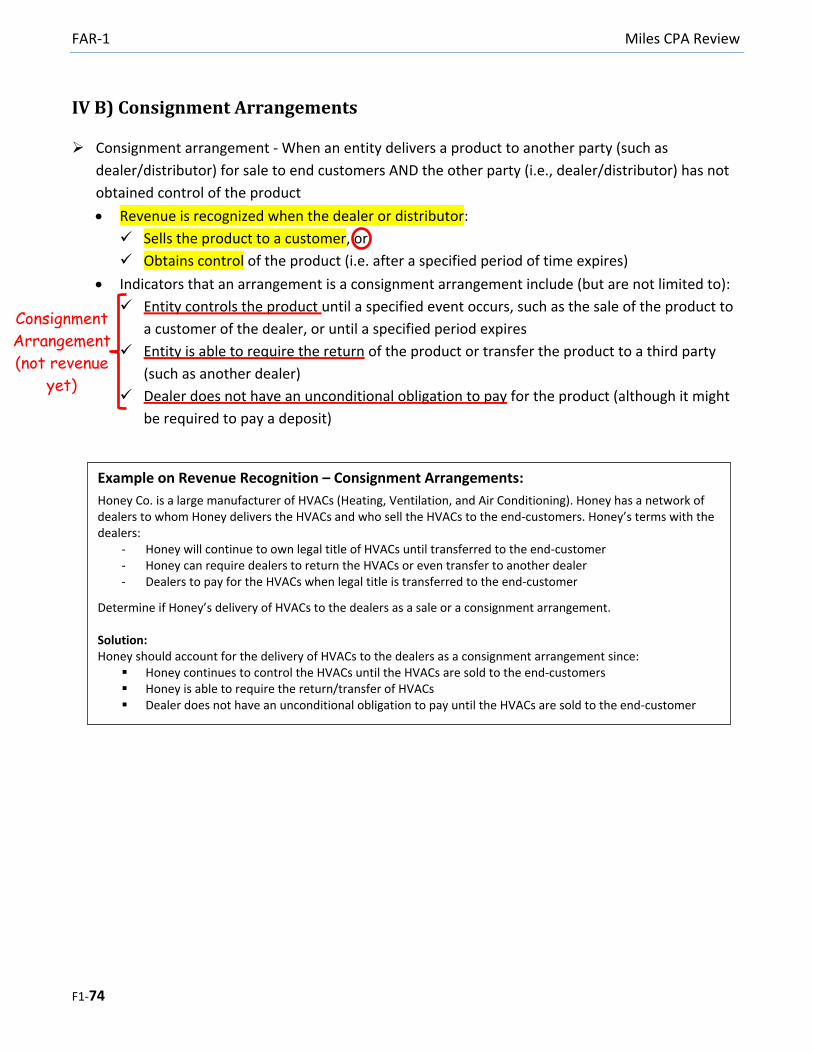

Consignment arrangement - When an entity delivers a product to another party (such as

dealer/distributor) for sale to end customers AND the other party (i.e., dealer/distributor) has not

obtained control of the product

Revenue is recognized when the dealer or distributor:

Sells the product to a customer, or

Obtains control of the product (i.e. after a specified period of time expires)

Indicators that an arrangement is a consignment arrangement include (but are not limited to):

Entity controls the product until a specified event occurs, such as the sale of the product to

a customer of the dealer, or until a specified period expires

Entity is able to require the return of the product or transfer the product to a third party

(such as another dealer)

Dealer does not have an unconditional obligation to pay for the product (although it might

be required to pay a deposit)

Example on Revenue Recognition – Consignment Arrangements:

Honey Co. is a large manufacturer of HVACs (Heating, Ventilation, and Air Conditioning). Honey has a network of dealers to whom Honey delivers the HVACs and who sell the HVACs to the end-customers. Honey’s terms with the dealers:

- Honey will continue to own legal title of HVACs until transferred to the end-customer - Honey can require dealers to return the HVACs or even transfer to another dealer - Dealers to pay for the HVACs when legal title is transferred to the end-customer

Determine if Honey’s delivery of HVACs to the dealers as a sale or a consignment arrangement. Solution: Honey should account for the delivery of HVACs to the dealers as a consignment arrangement since:

Honey continues to control the HVACs until the HVACs are sold to the end-customers Honey is able to require the return/transfer of HVACs Dealer does not have an unconditional obligation to pay until the HVACs are sold to the end-customer

Consignment

Arrangement

(not revenue

yet)

Miles CPA Review FAR-1

F1-75

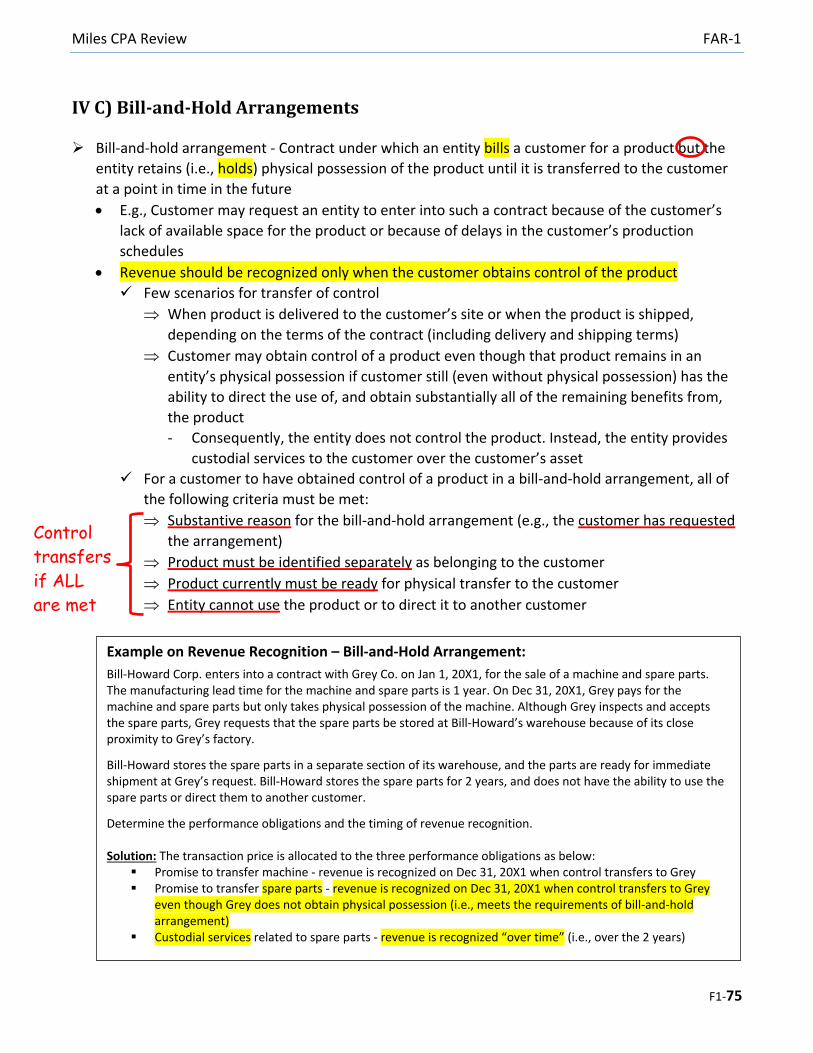

IV C) Bill-and-Hold Arrangements

Bill-and-hold arrangement - Contract under which an entity bills a customer for a product but the

entity retains (i.e., holds) physical possession of the product until it is transferred to the customer

at a point in time in the future

E.g., Customer may request an entity to enter into such a contract because of the customer’s

lack of available space for the product or because of delays in the customer’s production

schedules

Revenue should be recognized only when the customer obtains control of the product

Few scenarios for transfer of control

When product is delivered to the customer’s site or when the product is shipped,

depending on the terms of the contract (including delivery and shipping terms)

Customer may obtain control of a product even though that product remains in an

entity’s physical possession if customer still (even without physical possession) has the

ability to direct the use of, and obtain substantially all of the remaining benefits from,

the product

- Consequently, the entity does not control the product. Instead, the entity provides

custodial services to the customer over the customer’s asset

For a customer to have obtained control of a product in a bill-and-hold arrangement, all of

the following criteria must be met:

Substantive reason for the bill-and-hold arrangement (e.g., the customer has requested

the arrangement)

Product must be identified separately as belonging to the customer

Product currently must be ready for physical transfer to the customer

Entity cannot use the product or to direct it to another customer

Example on Revenue Recognition – Bill-and-Hold Arrangement:

Bill-Howard Corp. enters into a contract with Grey Co. on Jan 1, 20X1, for the sale of a machine and spare parts. The manufacturing lead time for the machine and spare parts is 1 year. On Dec 31, 20X1, Grey pays for the machine and spare parts but only takes physical possession of the machine. Although Grey inspects and accepts the spare parts, Grey requests that the spare parts be stored at Bill-Howard’s warehouse because of its close proximity to Grey’s factory.

Bill-Howard stores the spare parts in a separate section of its warehouse, and the parts are ready for immediate shipment at Grey’s request. Bill-Howard stores the spare parts for 2 years, and does not have the ability to use the spare parts or direct them to another customer.

Determine the performance obligations and the timing of revenue recognition. Solution: The transaction price is allocated to the three performance obligations as below:

Promise to transfer machine - revenue is recognized on Dec 31, 20X1 when control transfers to Grey Promise to transfer spare parts - revenue is recognized on Dec 31, 20X1 when control transfers to Grey

even though Grey does not obtain physical possession (i.e., meets the requirements of bill-and-hold arrangement)

Custodial services related to spare parts - revenue is recognized “over time” (i.e., over the 2 years)

Control

transfers

if ALL

are met

FAR-1 Miles CPA Review

F1-76

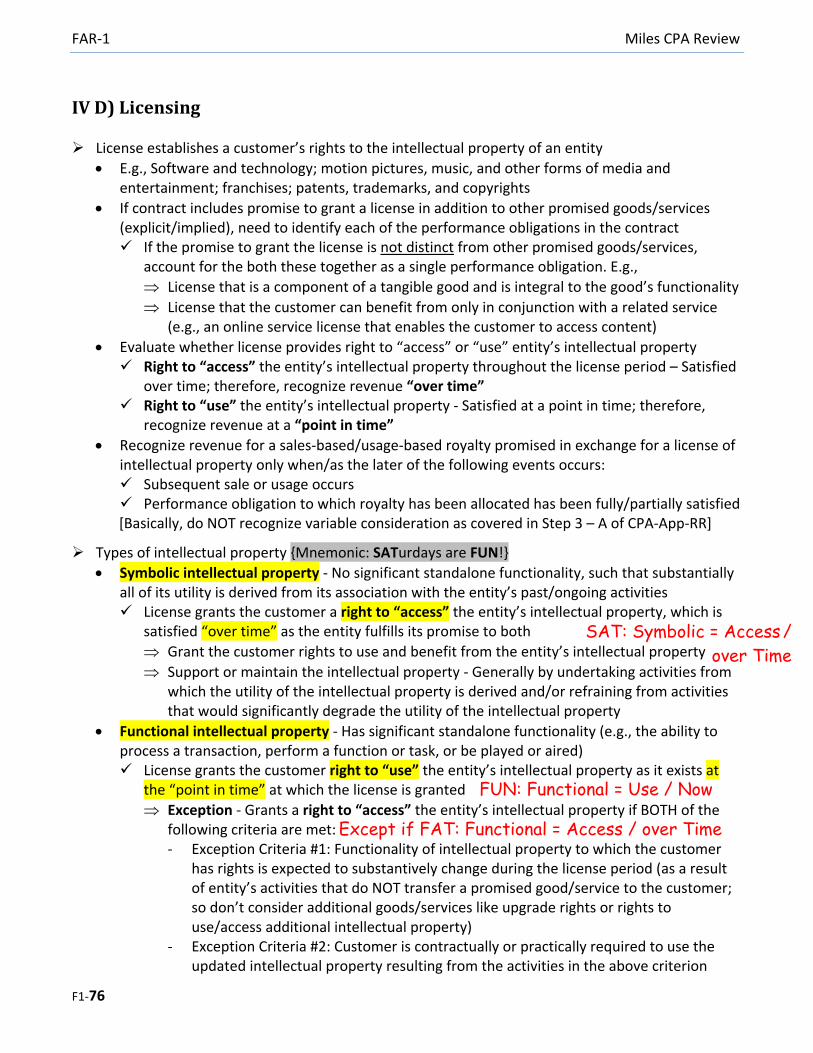

IV D) Licensing

License establishes a customer’s rights to the intellectual property of an entity

E.g., Software and technology; motion pictures, music, and other forms of media and entertainment; franchises; patents, trademarks, and copyrights

If contract includes promise to grant a license in addition to other promised goods/services (explicit/implied), need to identify each of the performance obligations in the contract If the promise to grant the license is not distinct from other promised goods/services,

account for the both these together as a single performance obligation. E.g.,

License that is a component of a tangible good and is integral to the good’s functionality

License that the customer can benefit from only in conjunction with a related service (e.g., an online service license that enables the customer to access content)

Evaluate whether license provides right to “access” or “use” entity’s intellectual property Right to “access” the entity’s intellectual property throughout the license period – Satisfied

over time; therefore, recognize revenue “over time” Right to “use” the entity’s intellectual property - Satisfied at a point in time; therefore,

recognize revenue at a “point in time”

Recognize revenue for a sales-based/usage-based royalty promised in exchange for a license of intellectual property only when/as the later of the following events occurs: Subsequent sale or usage occurs Performance obligation to which royalty has been allocated has been fully/partially satisfied [Basically, do NOT recognize variable consideration as covered in Step 3 – A of CPA-App-RR]

Types of intellectual property {Mnemonic: SATurdays are FUN!}

Symbolic intellectual property - No significant standalone functionality, such that substantially all of its utility is derived from its association with the entity’s past/ongoing activities License grants the customer a right to “access” the entity’s intellectual property, which is

satisfied “over time” as the entity fulfills its promise to both

Grant the customer rights to use and benefit from the entity’s intellectual property

Support or maintain the intellectual property - Generally by undertaking activities from which the utility of the intellectual property is derived and/or refraining from activities that would significantly degrade the utility of the intellectual property

Functional intellectual property - Has significant standalone functionality (e.g., the ability to process a transaction, perform a function or task, or be played or aired) License grants the customer right to “use” the entity’s intellectual property as it exists at

the “point in time” at which the license is granted

Exception - Grants a right to “access” the entity’s intellectual property if BOTH of the following criteria are met: - Exception Criteria #1: Functionality of intellectual property to which the customer

has rights is expected to substantively change during the license period (as a result of entity’s activities that do NOT transfer a promised good/service to the customer; so don’t consider additional goods/services like upgrade rights or rights to use/access additional intellectual property)

- Exception Criteria #2: Customer is contractually or practically required to use the updated intellectual property resulting from the activities in the above criterion

FUN: Functional = Use / Now

SAT: Symbolic = Access /

over Time

Except if FAT: Functional = Access / over Time

Miles CPA Review FAR-1

F1-77

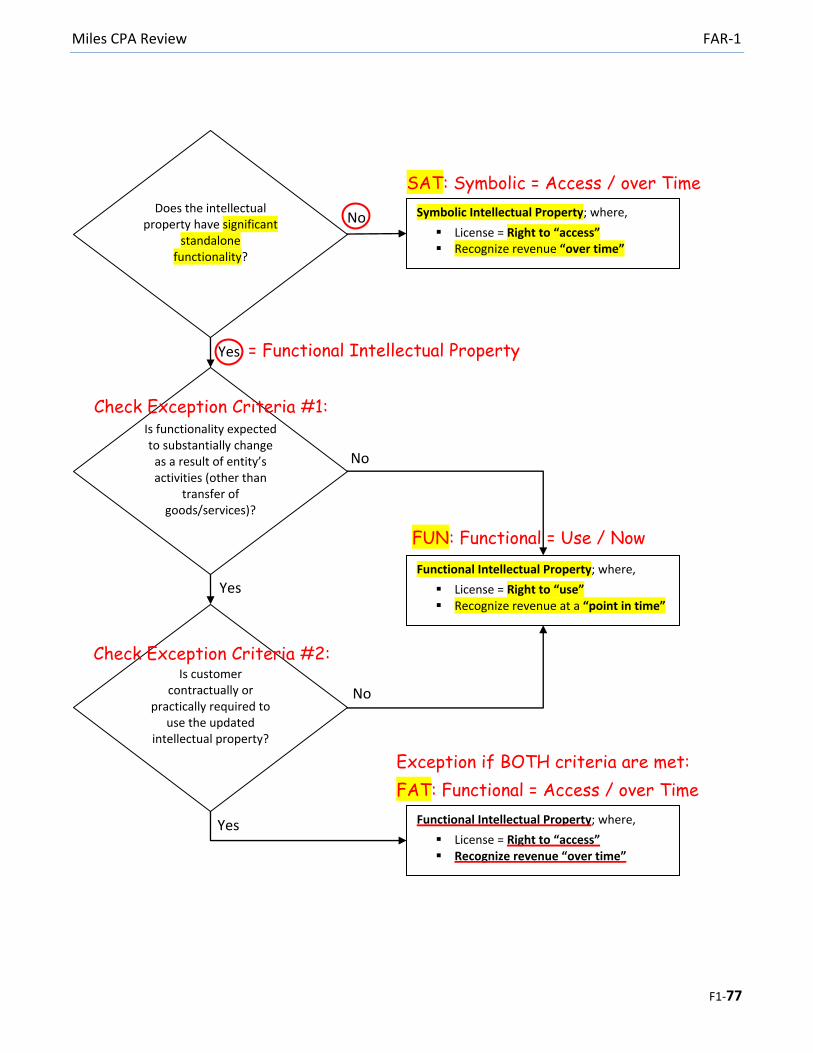

Does the intellectual property have significant

standalone functionality?

Is functionality expected to substantially change

as a result of entity’s activities (other than

transfer of goods/services)?

Is customer contractually or

practically required to use the updated

intellectual property?

Symbolic Intellectual Property; where,

License = Right to “access” Recognize revenue “over time”

Functional Intellectual Property; where,

License = Right to “use” Recognize revenue at a “point in time”

Functional Intellectual Property; where,

License = Right to “access” Recognize revenue “over time”

Yes

No

No

Yes

Yes

Exception if BOTH criteria are met:

FAT: Functional = Access / over Time

Check Exception Criteria #1:

= Functional Intellectual Property

Check Exception Criteria #2:

SAT: Symbolic = Access / over Time

FUN: Functional = Use / Now

No

FAR-1 Miles CPA Review

F1-78

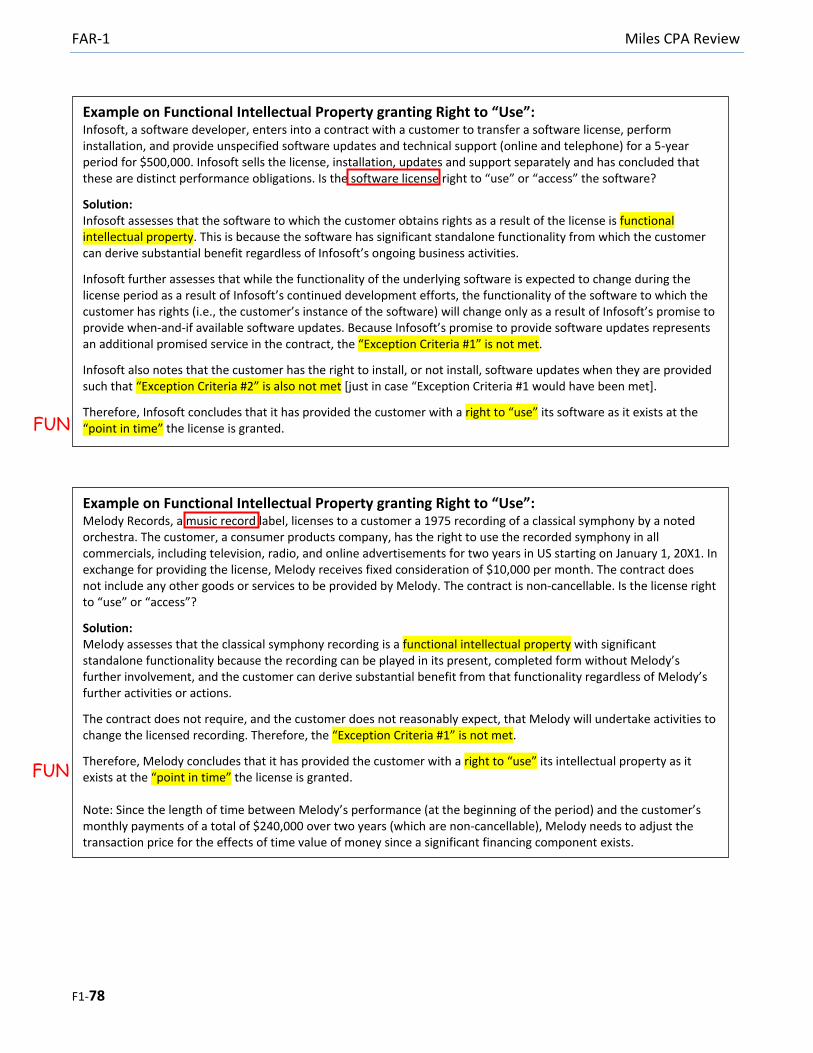

Example on Functional Intellectual Property granting Right to “Use”: Infosoft, a software developer, enters into a contract with a customer to transfer a software license, perform installation, and provide unspecified software updates and technical support (online and telephone) for a 5-year period for $500,000. Infosoft sells the license, installation, updates and support separately and has concluded that these are distinct performance obligations. Is the software license right to “use” or “access” the software?

Solution: Infosoft assesses that the software to which the customer obtains rights as a result of the license is functional intellectual property. This is because the software has significant standalone functionality from which the customer can derive substantial benefit regardless of Infosoft’s ongoing business activities.

Infosoft further assesses that while the functionality of the underlying software is expected to change during the license period as a result of Infosoft’s continued development efforts, the functionality of the software to which the customer has rights (i.e., the customer’s instance of the software) will change only as a result of Infosoft’s promise to provide when-and-if available software updates. Because Infosoft’s promise to provide software updates represents an additional promised service in the contract, the “Exception Criteria #1” is not met.

Infosoft also notes that the customer has the right to install, or not install, software updates when they are provided such that “Exception Criteria #2” is also not met *just in case “Exception Criteria #1 would have been met].

Therefore, Infosoft concludes that it has provided the customer with a right to “use” its software as it exists at the “point in time” the license is granted.

Example on Functional Intellectual Property granting Right to “Use”: Melody Records, a music record label, licenses to a customer a 1975 recording of a classical symphony by a noted orchestra. The customer, a consumer products company, has the right to use the recorded symphony in all commercials, including television, radio, and online advertisements for two years in US starting on January 1, 20X1. In exchange for providing the license, Melody receives fixed consideration of $10,000 per month. The contract does not include any other goods or services to be provided by Melody. The contract is non-cancellable. Is the license right to “use” or “access”?

Solution: Melody assesses that the classical symphony recording is a functional intellectual property with significant standalone functionality because the recording can be played in its present, completed form without Melody’s further involvement, and the customer can derive substantial benefit from that functionality regardless of Melody’s further activities or actions.

The contract does not require, and the customer does not reasonably expect, that Melody will undertake activities to change the licensed recording. Therefore, the “Exception Criteria #1” is not met.

Therefore, Melody concludes that it has provided the customer with a right to “use” its intellectual property as it exists at the “point in time” the license is granted. Note: Since the length of time between Melody’s performance (at the beginning of the period) and the customer’s monthly payments of a total of $240,000 over two years (which are non-cancellable), Melody needs to adjust the transaction price for the effects of time value of money since a significant financing component exists.

FUN

FUN

Miles CPA Review FAR-1

F1-79

Example on Symbolic Intellectual Property granting Right to “Access”: Forever Co. enters into a contract with a customer and promises to grant a franchise license that provides the customer with the right to use Forever’s trade name and sell Forever’s products for 10 years. In exchange for granting the license, Forever receives a fixed fee of $700,000, as well as a sales-based royalty of 5% of the customer’s monthly sales for the term of the license. Is the franchise license right to “use” or “access”?

Solution: Forever assesses that its trade name and logo have limited standalone functionality; and, the utility of the products developed by Forever are derived largely from the products’ association with the franchise brand. Substantially all of the utility inherent in the trade name, logo, and product rights granted under the license stems from Forever’s past and ongoing activities of establishing, building, and maintaining the franchise brand. The utility of the license is its association with the franchise brand and the related demand for its products.

Therefore, Forever concludes that the nature of its promise is to provide a right to access Forever’s symbolic intellectual property. Consequently, the license provides the customer with a right to “access” Forever’s intellectual property and Forever’s performance obligation to transfer the license is satisfied “over time”:

- Fixed $700,000 fees: Recognize revenue “over time” (i.e., over 10 years) - Sales-based royalty: Recognize revenue as and when the sales occur

Example on Symbolic Intellectual Property granting Right to “Access”: Catilla Creative Cohort, a creator of comic strips, licenses the use of the images and names of its comic strip characters in two of its comic strips to a customer for a 3-year term. There are main characters involved in each of the comic strips. However, newly created characters appear and disappear regularly and the images of the characters evolve over time. The customer, an operator of cruise ships, can use Catilla’s characters in various ways, such as in shows or parades, within reasonable guidelines. In exchange for granting the license, Catilla receives a fixed payment of $250,000 in each year of the 3-year term.

Solution: Catilla assesses that the license has no standalone functionality (the names and images cannot process a transaction, perform a function or task, or be played or aired separate from significant additional production that would, for example, use the images to create a movie or a show) and the utility of those names and images is derived from Catilla’s past and ongoing activities such as producing the weekly comic strip that includes the characters.

Therefore, Catilla concludes that the nature of its promise is to provide a right to access Catilla’s symbolic intellectual property. Consequently, the license provides the customer with a right to “access” Catilla’s intellectual property and Catilla’s performance obligation to transfer the license is satisfied “over time”:

- Annual $250,000 fees: Recognize revenue “over time” (i.e., $250,000/year over the 3-year term)

SAT

SAT