Resultados Grupo Pão de Açúcar - GPA · ABOUT GRUPO PÃO DE AÇÚCAR 2 1 2011 Estimated 2 In the...

54

CORPORATE PRESENTATION Grupo Pão de Açúcar and Globex Utilidades October, 2011

Transcript of Resultados Grupo Pão de Açúcar - GPA · ABOUT GRUPO PÃO DE AÇÚCAR 2 1 2011 Estimated 2 In the...

CORPORATE

PRESENTATION

Grupo Pão de Açúcar and Globex Utilidades

October, 2011

ABOUT GRUPO PÃO DE AÇÚCAR

2

1 2011 Estimated 2 In the past 12 quarters, according to Brazilian Supermarket Association (ABRAS)

> Key figures

> R$ 50+ bi Sales1

> #1 Retailer in Brazil

> Growth higher than

the 2nd player’s2

> 160k employees

> Operational

> 1.8k points of sales, located in

19 States and the Federal District

> Multi-format distribution

> 600 million tickets per year

> 2.8 million m² of sales area

NEW MANAGEMENT MODEL ADJUSTED IN 2011

3

Metric Commercial/

Supply Chain

and IT

Corporate

Services /

Finance

People

Retail Cash &

Carry

Metric Metric Metric Metric Metric

Metric

Metric

Metrics: 1. Net Income

2. Valuation/EVA

3. ROCE

4. Growth/Expansion

5. Customer satisfaction

6. Our people satisfaction

Corporate Relations

Market Strategy

Management Control

CEO Nova

PontoCom Specialized Electronics

MAIN INDICATORS

4

1 Nova Casas Bahia consolidation as of Nov, 2010. Annualized gross sales of R$44 billion.

ECONOMIC-FINANCIAL 2006 2007 2008 2009 2010 (1)

(R$ million)

Gross Sales 16,460.3 17,642.6 20,856.8 26,219.1 36,144.4

Same-store growth -0.1% 2.8% 8.5% 9.6% 12.1%

EBITDA 886.4 992.4 1,322.5 1,504.1 2,068.1

EBITDA margin 6.4% 6.7% 7.3% 6.5% 6.4%

Net income 85.5 185.7 260.4 644.7 722.4

Gross margin 28.2% 28.0% 26.4% 24.8% 24.5%

Net margin 0.6% 1.3% 1.4% 2.8% 2.3%

Net debt/EBITDA 0.7x 1.3x 0.6x 0.4x 0.6x

EPS (R$/thousand shares) 0.8109 0.8151 1.1070 2.5333 2.8051

OPERATIONAL 2006 2007 2008 2009 2010

Total stores (number) 549 575 597 1,080 1,647

Selling area (m2) 1,217,984 1,338,329 1,360,706 1,744,653 2,811,103

Area increase 1.0% 9.9% 1.7% 28.2% 61.1%

Number of employees 63,607 66,165 70,656 85,244 144,914

COMPANY CHANGES AS THE ENVIRONMENT

MOVES

5

Brazil

2005

Population in each social class (in million)

GPA: limited

offering (only

Food, 556 stores)

GPA: multiformat

business for both Food

and Electro, 1,646 stores

Brazil 2010 32mn emerged

only in 2010

2005 2010

92,9MM

D/E

101,7MM

C

A/B

26,4MM

62,7MM

C

A/B

42,2MM

47,9MM

D/E

E-C

OM

MER

CE

FO

OD

CA

SH

& C

AR

RY

COMPANY CHANGES AS THE ENVIRONMENT

MOVES

6

Source: IBGE, BACEN, Ipsos/Cetelem, Exame

magazine - June 29, 2011

10,1% 10,3% 9,6% 8,0% 8,4%

6,7%

2005 2006 2007 2008 2009 2010

Unemployment rate

Credit available to population (As % of GDP)

8,8% 9,7% 11,2% 12,8% 15,0% 15,7%

2005 2006 2007 2008 2009 2010

1,2%

4,0% 3,2% 3,4% 3,2% 3,5%

2005 2006 2007 2008 2009 2010

Real income growth

Available income1 (monthly)

Social Class

2009 2010 % Change

A/B R$ 680 R$ 991 46%

C R$ 204 R$ 243 19%

D/E R$ 61 R$ 104 70%

Total R$ 230 R$ 368 60%

1 Total income less all family expenses

Social Class Income (monthy)

A Above R$9,050

B From R$6,941 to R$9,050

C From R$1,610 to R$6,941

D From R$1,008 to R$1,610

E Below R$1,008

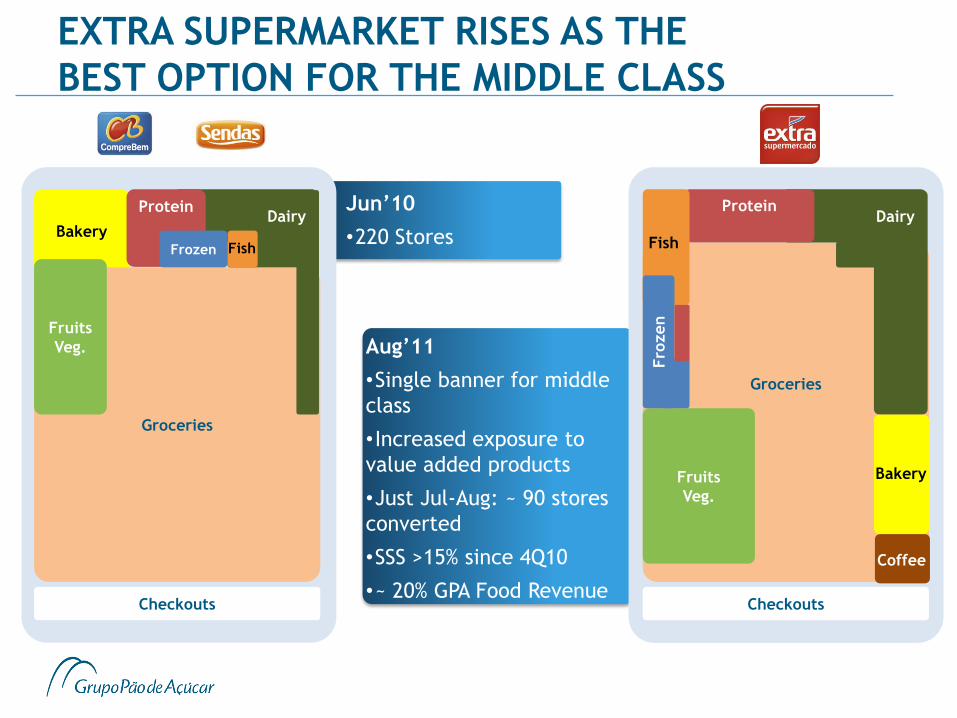

EXTRA SUPERMARKET RISES AS THE

BEST OPTION FOR THE MIDDLE CLASS

Bakery

Checkouts

Groceries

Fruits

Veg.

Dairy Protein

Frozen Fish

Jun‟10

•220 Stores

Checkouts

Groceries

Fruits

Veg.

Dairy Protein

Fish

Bakery

Coffee

Fro

zen

Aug‟11

•Single banner for middle

class

• Increased exposure to

value added products

•Just Jul-Aug: ~ 90 stores

converted

•SSS >15% since 4Q10

•~ 20% GPA Food Revenue

R$25.0 BN OF GROSS SALES IN 1H11

8

• 2010: 24.5%

Nova Casas Bahia consolidation as of Nov, 2010

• 1H11: 26.4%

GPA Food1: 25.4%

Globex2: 27.5%

• 2010: R$ 36.1 bn

„Same-store‟ sales moved up by 12.1%

Nova Casas Bahia consolidation as of Nov, 2010

• 1H11: R$25.0 bn

„Same-store‟ sales increased by 8.5%

Gross

Sales

Gross

Margin

1 Refers to GPA consolidated excluding Globex 2 Includes Nova Casas Bahia and Nova Pontocom

EBITDA OF R$1,2 BN IN 1H11

9

EBITDA

Net Income

• 2010: R$2.1 bn 37.5% (margin of 6.4%)

Nova Casas Bahia consolidation as of Nov, 2010

• 1H11: R$1.2 bn 50.8% (margin of 5.5%)

GPA Food1:R$841.3 mn (margin of 6.9%)

Globex2: R$382.7 mn (margin of 3.9%)

• 2010: R$722.4 mn (margin of 2.3%)

Nova Casas Bahia consolidation as of Nov, 2010

• 1H11 adjusted net income: R$296.6 mn (margin of 1.3%)

1 Refers to GPA consolidated excluding Globex 2 Includes Nova Casas Bahia and Nova Pontocom

GROWTH HIGHER THAN THE 2ND PLAYER

10

Same Store Sales

8.5%

4.3%

10.3% 10.4%

4.6%

13.2%

9.7%

10.6%

15.0%

9,9%

12,5%

11,5%

6,8%

10,1%

7.1%

8.6% 8.4%

7.8%

2.3%

7.2%

3.9% 4.8%

8.7%

2,9%

5,2%

5,6%

5,0%

7,1%

1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11

2nd player

12 Quarters

11

GUIDANCE FOR NEW GLOBEX ELECTRO – BRICKS AND MORTAR OPERATION

GROSS SALES (R$) Above

R$ 20 billion

Growth (SSS)

above the market

GROSS MARGIN(1)

EBITDA MARGIN(1) (2) 4.0 to 5.5% Higher than 7.0%

Higher than 25.5% Higher than 26.5%

CAPEX R$ 100 mn to

R$ 120 mn

FINANCIAL RESULT(1) -3.5 to -4.5% Up to -4.0%

1 of net sales. Projections include estimated synergies. 2 The guidance for EBITDA margin was adjusted due to reclassification of “profit sharing” expenses in

the 2Q11. Under the previous accounting criterion, the guidance for 2011 would be between 4.5% and

6.0%, and for year model it would be 7.5%, as disclosed in 2H10.

2011E Year Model

12

MAIN SYNERGIES ELECTRO1

1 – Commercial and operating

management

2 – Management of infrastructure and

back-office

3 – Management of

financial and capital

structure

‣ Integrate the Ponto Frio operating management to Casas Bahia model

with margin and sales gains

‣ Centralization of purchase management with margin gains;

‣ Improvement of sales and pricing mix;

‣ Increase the penetration of services sales;

‣ Repositioning of Ponto Frio brand and maintaining strong the Casas Bahia

brand

‣ Centralization of the companies’ inventories and stock ups;

‣ Utilization of GPA’s back-office platform with Shared Services Center and

total integration among Casas Bahia, Ponto Frio and the other areas;

‣ Refine the operational processes;

‣ Take advantage of other synergies with GPA (logistics, IT etc);

‣ Manage the cash / Working Capital inside GPA platform;

‣ Reduction in funding costs / negotiation of financing instruments and

lines at GPA cost;

1 Includes Electronics, Home Appliance and Furniture operations

13

SYNERGIES GLOBEX

1.0% - 2.0%

(R$ 170 - 340 mn)

1.5% - 2.0%

(R$ 255 - 340 mn)

0.5% - 1.0%

(R$ 85 - 170 mn)

3.0% - 5.0%

(R$ 510 - 850 mn)

Potential per year – after total capture of synergies(1)

1 Synergy calculated over the net sales. 2 Includes Electronics, Home Appliance and Furniture operations

1 – Commercial and operating management

2 – Management of infra-structure and back-office

3 – Management of

financial and capital

structure

Total

14

OWNERSHIP STRUCTURE

32%

68%

47% 53%

50%

Globex

NovaPontoCom

6%

44%

Nova Casas

Bahia

100%

FIC Financial JV

14%

36%

Banco Itaú

50%

Free Float

Controlling Group

Casas Bahia Founders

Klein Family

Management

As of October 06, 2011.

Formats

16

GPA STORES AND FORMATS G

PA F

OO

D

ELEC

TR

ON

ICS /

HO

ME

APPLIA

NC

E

Supermarkets (*)

Cash & Carry

Hypermarket

Proximity

Gas stations and

Drugstores

Specialized

Stores

B2C B2B

374

59

115

67

231

989

# Stores

(*) Includes the Sendas and CompreBem stores still not converted.

Stores as of 2Q11.

17

GPA FOOD RETAIL STORES CHARACTERISTICS GPA FOOD

Public Stores 2Q11

Additions

Avg Sales Area

(m2)

ABCD classes 115 +1 6,000

AB classes 151 - 1,500

BCD classes 129 +11 1,500

Transformers Food service

59 - 4,000

ABCD classes 67 - 300

18

GLOBEX STORES COUNT ELECTRONICS1

Public Stores 2Q11

Additions

ABC classes 456 +3

CD classes 533 +9

1 Includes Electronics, Home Appliance and Furniture operations

19

REGIONAL PRESENCE (STORES)

North

Super: 0

Hyper: 1

Electro: 0

Cash & Carry: 1

Proximity: 0

Total: 2

GDP: 5.1%

Middle-West

Super: 13

Hyper: 11

Electro: 83

Cash & Carry: 3

Proximity: 0

Total:11017 GDP: 9.2%

Stores as of 2Q11

GDP: 13.1%

GDP: 56.0%

GDP: 16.6%

North-East

Super: 29

Hyper: 16

Electro: 29

Cash & Carry: 6

Proximity: 0

Total: 80

South-East

Super: 328

Hyper: 85

Electro: 762

Cash & Carry: 49

Proximity: 67

Total: 1,291

South

Super: 4

Hyper: 2

Electro: 115

Cash & Carry: 0

Proximity: 0

Total: 121

20

REGIONAL PRESENCE (DISTRIBUTION CENTERS)

Distribution Centers - Total

SP - São Paulo 18

RJ - Rio de Janeiro 5

DF - Distrito Federal 4

PR - Paraná 4

MG - Minas Gerais 3

PE - Pernambuco 3

BA - Bahia 2

ES - Espírito Santo 2

GO - Goiás 2

MT - Mato Grosso 2

SC - Santa Catarina 2

CE - Ceará 1

MS - Mato Grosso do Sul 1

RS - Rio Grande do Sul 1

Total 50 As of 2Q11

Nova Pontocom

BRAZILIAN MARKET IN EXPANSION

22

44% 56%

2010

67%

33%

2014 E

Access

No Access

Internet access – “C” class

E-commerce revenue in R$ billion

Source: e-Bit and Estado de SP July 31, 2011

1.7 2.7

Nova Pontocom annualized

Brazilian e-commerce

1 E-bit estimate

16% 18% 19%

Nova Pontocom mkt share

23

CONSISTENT SALES GROWTH NOVA PONTOCOM

24

IMPROVEMENT IN OPERATING PROFITABILITY NOVA PONTOCOM

* Amounts without Stock Option non-cash expenses.

Gross Profit (R$ Mn)

100

328

2009 2010

18,6% 19,2%

Operating Expenses (R$ Mn)*

17,6%

14,5%

95

248

2009 2010

Gross margin has grown, despite VAT tax

change (“Substituição Tributária”)

• Better negotiations / beginning of the

expansion of the assortment

• Still little synergy from groups commercial

conditions

Expenses reduction of more than 3 p.p. in 2010

• Strong fixed expenses dilution

• Greater variable expenses efficiency

• Synergies with the group

25

INCREASING EBITDA AND BREAK-EVEN IN NET INCOME

NOVA PONTOCOM

EBITDA (R$ Mn)*

EBITDA has approached 5% in 2010 with

gains in both margin and expenses

5

80

2009 2010

1,0%

4,7%

Net income (R$ Mn)**

Operation in the break-even point

of net income

0,2

0,0%

-2,3%

2009

2010

* Amounts without Stock Option non-cash expenses.

** Amounts without Stock Option non-cash expenses; 2009 pro-forma: adjusted amounts for the

current deferral accounting practice.

26

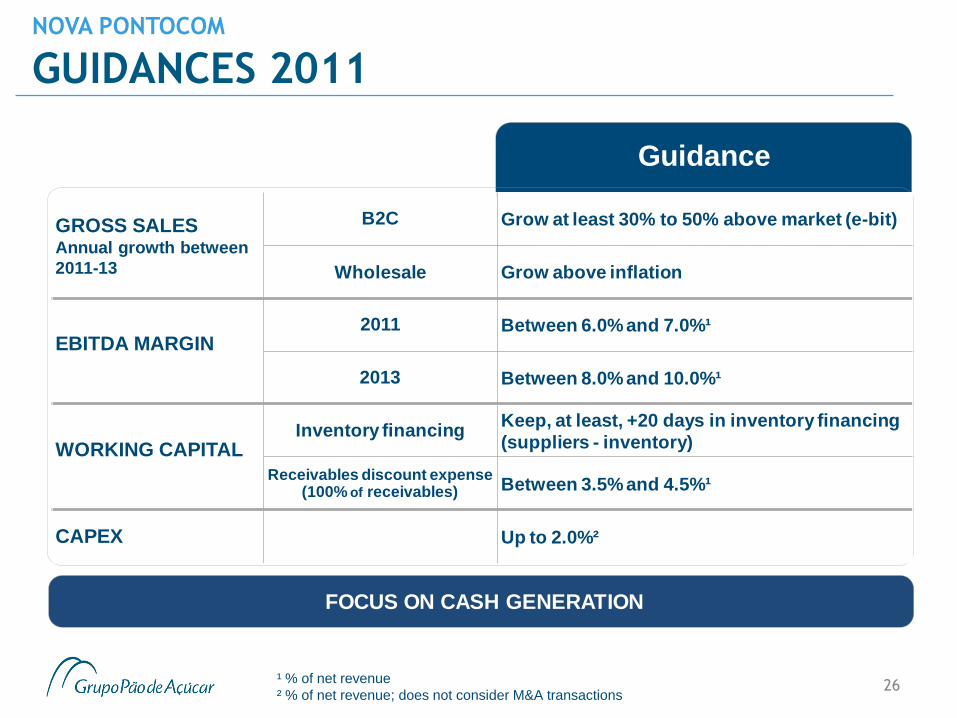

GUIDANCES 2011 NOVA PONTOCOM

Guidance

GROSS SALESAnnual growth between

2011-13

B2C Grow at least 30% to 50% above market (e-bit)

Wholesale Grow above inflation

EBITDA MARGIN2011 Between 6.0% and 7.0%¹

2013 Between 8.0% and 10.0%¹

WORKING CAPITALInventory financing

Keep, at least, +20 days in inventory financing

(suppliers - inventory)

Receivables discount expense (100% of receivables) Between 3.5% and 4.5%¹

CAPEX Up to 2.0%²

FOCUS ON CASH GENERATION

¹ % of net revenue

² % of net revenue; does not consider M&A transactions

2Q11 Results

2Q11 HIGHLIGHTS

> IPCA 12 months: +6.7%

> GPA Food real growth: +2.3%

> Increase in Selic1 rate from 11.75% to 12.25%

> „Same-store‟ growth:

> GPA Food2: +9.3%, Globex2:+17.6%

> Results: increase in market share, profitability with

competitiveness and permanent control of expenses

> EBITDA: +20% Food, +38% Globex

> EPS: +64% Consolidated

28

Macroeconomic impact

1 End of periods 1Q11 and 2Q11, respectively 2 Net Sales

Performance in businesses

GPA CONSOLIDATED IN THE 2Q11: GROSS

SALES OF R$ 12.6 BN

29

>GROSS SALES: R$ 12.6 bn + 61.3% vs. 2Q10

GPA Food1: Same-store growth of 9.1% in 2Q11

Globex2: Same-store growth of 14.1% in 2Q11

>GROSS PROFIT: R$ 3.0 bn +82.8% vs. 2Q10

Margins: GPA Food1: 25.2% +40 bps vs. 2Q10

Globex2: 28.1% +130 bps vs. 1Q11

>EBITDA: R$ 641 mn +66.3% vs. 2Q10

Margins: GPA Food1: 6.7% +50 bps vs. 2Q10

Globex2: 4.4% +110 bps vs. 1Q11

1 Refers to GPA Consolidated without Globex. 2 Considers Ponto Frio and e-commerce, excluding Casasbahia.com.br

The figures presented in this document already reflect the IFRS change in 2010 and 2011 and it

changes Company’s already published figures.

Globex’s numbers are not comparable between 2Q11 and 2Q10 due to the consolidation of Casas

Bahia as of November, 2010.

AGENDA – 2Q11 RESULTS

30

GPA F

OO

D

Supermarkets

Cash & Carry

Hypermarket

Proximity

Gas Stations and Drugstores

GROSS SALES OF R$ 6.9 BN, SAME-STORE SALES INCREASE

9.1% IN THE QUARTER

31

> Same-store growth

> In the 2Q11, higher than the 2nd player

for 3 years in a row

> In the 1H11, +7.4%, the upward trend

observed in previous quarters is

maintained

GPA FOOD

6,286 6,928

12,629 13,569

2Q10 2Q11 1H10 1H11

Gross Sales (R$ mn)

(without Globex)

7.7% 7.2%

5.7%

9.1%

3Q10 4Q10 1Q11 2Q11

Same-store growth (without Globex)

Highlights with same-

store growth > 15%

10.2%

7.4%

7.4%

1H11

The shopping period for Easter took place

in the 1Q10 and 2Q11. The analysis of

growth in the first 6 months isolates this

effect.

GROSS PROFIT CLIMBS BY 12.3%

32

> Margin expansion is related mainly to : > Product mix with higher margin

GPA FOOD

1 Cash-and-carry operation share in GPA Food net sales.

1,397 1,569

2,803 3,106

2Q10 2Q11 1H10 1H11

12.3%

Aligned with the strategy of

conversion to Extra

Supermercado, which allocates

larger area for these categories

10.8%

General

Merchandise and Perishables

% of Net Sales

25.2% 24.8%

Cash & Carry1

11.9% 14.8%

25.4% 24.7%

Gross Profit (R$ mn)

(without Globex)

33

GPA FOOD

Operating Expenses (R$ mn)

(without Globex)

1,047 1,150

2Q10 2Q11

18.5% 18.6%

% of Net Sales

OPERATING EXPENSES OF R$ 1.1 BN IN THE 2Q11

> Maintenance of the same level

of operating expenses as a

percentage of net sales in 2Q10

Creation of the

Management Control with

the administration of the

expenses groups

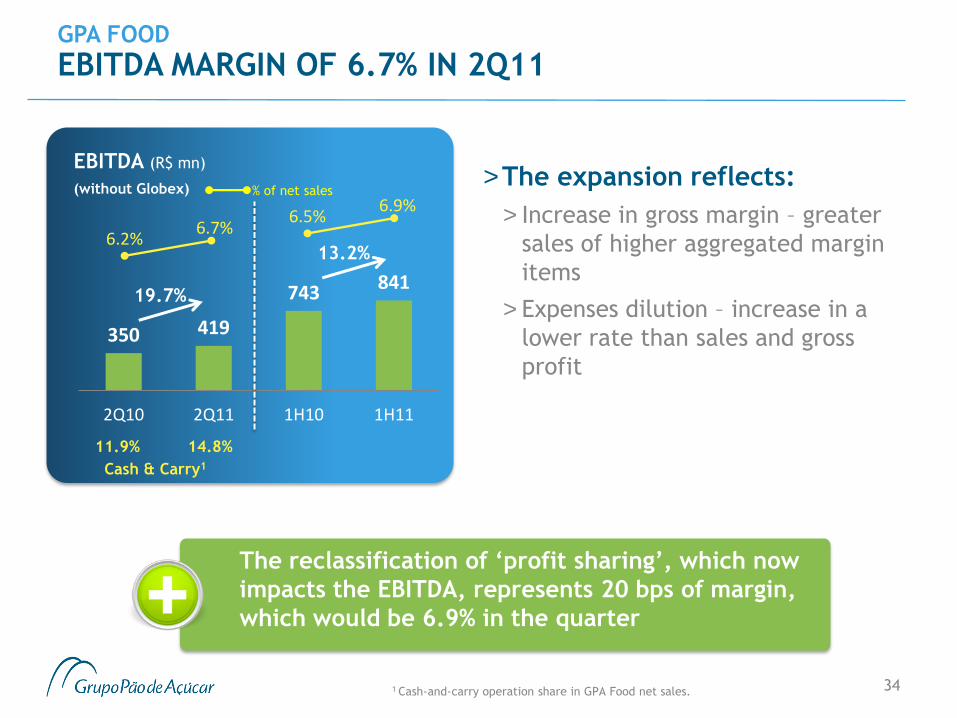

EBITDA MARGIN OF 6.7% IN 2Q11

34

GPA FOOD

EBITDA (R$ mn)

(without Globex)

350 419

743 841

2Q10 2Q11 1H10 1H11

19.7%

The reclassification of „profit sharing‟, which now

impacts the EBITDA, represents 20 bps of margin,

which would be 6.9% in the quarter

13.2%

6.7% 6.2%

6.9% 6.5%

% of net sales >The expansion reflects:

> Increase in gross margin – greater

sales of higher aggregated margin

items

> Expenses dilution – increase in a

lower rate than sales and gross

profit

11.9% 14.8%

Cash & Carry1

1 Cash-and-carry operation share in GPA Food net sales.

NET FINANCIAL EXPENSE KEEPS REPRESENTING

2.7% OF SALES

35

GPA FOOD

>Maintained level of 2.7% of

net sales, despite the higher

Selic rate

>Breakdown:

> 1.1%: Charges on bank net debt

(R$67.6 mn)

> 0.6%: Charges of discounted

receivables (R$34.3 mn)

> 1.0%: Adjustment by CDI of other

assets and liabilities(R$64.4 mi)

Net Financial Expense (R$ mn)

(without Globex)

162 166

1Q11 2Q11

2.7% 2.7%

% of net sales

AGENDA – 2Q11 RESULTS

36

Due to the consolidation of Casas Bahia’s results as of November, 2010, we use the 1Q11 as a

reference for better comparison.

Expenses from “profit sharing”, previously recognized after “operating profit before income

tax”, are now recognized in the “general and administrative expenses” line, as part of the

adjustment to the new accounting standards (IFRS).

ELEC

TR

ON

ICS

Specialized Stores

E-commerce B2B

37

PERSPECTIVE OF THE CONSUMER ELECTRONICS

MARKET IN BRAZIL

Market with high growth rate for electronics, home

appliances and furniture > Increasing access to credit

> Urban population growth and reduction of electric exclusion –

“Programa Luz para Todos” (Light for All Program)

> Maturation of the age pyramid with more participation of the

economically active population in total population

> Higher real incomes in all social classes - especially with the growth of

“C” class

> Lower unemployment level – with increase in the number of women in

the work place

GLOBEX 2Q11 HIGHLIGHTS

> Positive results of the integration process:

> Commercial margin gains

> Control of non-interest-bearing sales and increased

interest-bearing sales

> Maintenance of financial expense

> Return of organic growth (12 new stores)

38

The Company will consistently deliver the

guidance presented to the market

GLOBEX 2Q11 HIGHLIGHTS

39

> Nova Pontocom (2Q11 vs 2Q10):

> Sales 1 : growth of 58.0%

> 50% higher than the market growth

> Highlight for CasasBahia.com.br, 3-digit growth

> EBITDA: growth above 50%

> Margin between 6% and 7%

> SAC 2.0

> Logistics 2020

(1) In addition to the PontoFrio.com.br and Extra.com.br websites and the wholesale

operation, this figure includes the pro-forma of CasasBahia.com.br and is the basis

for the guidance given for the year.

GLOBEX 2Q11 HIGHLIGHTS

40

Before

GLOBEX 2Q11 HIGHLIGHTS

41

After

NET SALES OF R$ 5.0 BN, SAME-STORE CLIMB BY 17.6%

42

GLOBEX

1 Comparable basis (Casasbahia.com.br and wholesale are not included)

HIGHLIGHTS

SAME-STORE

gross sales

4,884 5,041

1Q11 2Q11

Net Revenue (R$ mn)

Globex

> Same-store growth vs. 2Q10:

>Even vs. World Cup period (2Q10)

>Control of non-interest-bearing sales

and increased interest-bearing sales

e-commerce 1

:

+39.4%

3.2%

Bricks-and-mortar:

+8.1%

43

> Gains in commercial efficiency:

> Better price policy

> Better commercial conditions

associated with a better

product mix

GLOBEX

Gross Profit (R$ mn)

Globex

1,312 1,418

1Q11 2Q11

+8.1%

Reduction of logistics

expenses : Result of

the combination of two

operations under a

single structure

% of Net Sales

26.9%

28.1%

GROSS PROFIT OF R$ 1.4 BN IN THE 2Q11, MARGIN OF 28.1%

1.151 1.196

1Q11 2Q11

OPERATING EXPENSES REPRESENTED 23.7% OF NET

SALES IN THE 2Q11

44

GLOBEX

„Profit sharing‟ is now considered

Operating Expense under IFRS

Operating Expenses (R$ mn)

Globex % of Net Sales

23.6% 23.7%

> Maintenance of the expenses level

> Impact of non-recurring items

(R$ 25.7 mn): > Software maintenance agreement, R$11.5

mn

> Adjustment of benefits and charges

R$10,0 mn

> Adjustment of provisions for profit

sharing, R$4.2 mn

> Excluding the items above, expenses

would have come to 23.2% of net

sales

23.2%

Adjusted by non-recurring items

> The process of synergies gains in

expenses advances in the 2H11

45

> Advance in EBITDA margin

> Gross margin increase

GLOBEX

EBITDA (R$ mn)

Globex % of Net Sales

161

222

1Q11 2Q11

EBITDA in 2011:

We reaffirm the margin

guidance

EBITDA OF R$ 222 MN IN THE 2Q11, WITH MARGIN OF 4.4%

+38.2%

Reclassification of „profit

sharing‟, which starts to

impact EBITDA, represents

0.6% of the margin

3.3% 4.4%

Adjusted by IFRS

3.6% 5.0%

2011 EBITDA Margin

guidance, now in IFRS

basis, is equivalent to

margin between 4.0%

and 5.5%

NET FINANCIAL EXPENSE REPRESENTED 3.4%

OF NET SALES

46

GLOBEX

> Maintenance of financial

expenses level, even with the

Selic increase in the period

> Maintenance in the average

payment period

> Greater use of FIDC (Nova

Pontocom)

> Increase in the share of interest-

bearing sales

Net Financial Expense1 (R$ mn)

Globex % of net sales

3Q10 4Q10 1Q11 2Q11

4.9%

3.4%

5.9%

The financial expense as net sales percentage

remains below the guidance for 2011 (between 3.5%

and 4.5%)

3.4%

1 NCB is included as of November, 2010.

AGENDA – 2Q11 RESULTS

47

GPA F

OO

D

ELEC

TR

ON

ICS

Supermarkets

Cash & Carry

Hypermarket

Proximity

Gas Stations and Drugstores

Specialized Stores

E-commerce B2B

FIC IN 2Q11

48

Private label share in sales

GRUPO PÃO DE AÇÚCAR

Globex % of net sales

4.1% 4.6%

9.3% 10.5%

1Q11 2Q11

13.4% 15.1%

No interest

With interest

> Equity income result: R$ 2.7 mn

in 2Q11

> GPA Food: R$ (1.0) mn

> Globex (Ponto Frio): R$ 3.7 mn

> The change into cards with chip

generated R$9.2 mn (non-recurring)

Globex interest-free

sales represented in

the 2Q11 less than

50% of sales 1 The best credit tool:

> Longer term

> Lower comission cost

> Discount of receivables at FIDC cost

2Q11 CONSOLIDATED NET RESULT

49

GRUPO PÃO DE AÇÚCAR

1 End of period.

Adjusted Net Income (R$ mn)

93

158

2Q10 2Q11

% of net sales

> Adjusted net income grows by 70.2%,

totaling R$158 mn

> Considering non-recurring effects with

REFIS, adoption of IFRS and integration

expenses

> Operational strengthening and EBITDA

margin advance in Food

> Recovery of the Globex’s operation,

which comes close to break-even

> Accounting net income climbs by 64%

(R$56 mn in the 2Q10 to R$91 mn)

> Growth despite the increase in

financial expenses (Selic advances

from 10.25% to 12.25% p.a.1)

1.3% 1.4%

+70.2%

CONSOLIDATED NET DEBT

50

GRUPO PÃO DE AÇÚCAR

> The reduction on net debt is

associated with:

> Reduction of debt in Globex’s

operation

> Debt level maintenance in GPA

Food

Evolution of Consolidated Net Debt (R$ bn)

2.3 2.0

1Q11 2Q11

Net Debt / EBITDA

1.05x 0.81x

2Q11 INVESTMENTS

51

GRUPO PÃO DE AÇÚCAR G

PA FO

OD

New stores and lands

AMOUNT INVESTED STORES

12 c

onvers

ions

> 10 CompreBem to Extra

Supermercado

> 1 CompreBem to Extra

Hipermercado

> 1 Sendas to Extra

Supermercado

ELEC

TR

ON

ICS

Infrastructure > Fleet

> Technology

12 n

ew

sto

res

> 9 Casas Bahia

> 3 Ponto Frio

1H11: +03 stores, 35 conversions

1H11: +12 traditional stores

R$ 21.7 mn

2Q11 1H11

Total R$ 205.7 mn R$ 454.8 mn

Infrastructure and other

Total

Renovations and conversions R$ 88.6 mn

R$ 95.4 mn

R$ 84.4 mn

R$ 224.9 mn

R$ 145.4 mn

New stores and lands

Renovations and conversions

Other

R$ 10.5 mn

R$ 84.1 mn R$ 118.0 mn

R$ 17.9 mn

R$ 40.4 mn

R$ 26.2 mn

R$ 20.2 mn

R$ 52.2 mn R$ 15.9 mn R$ 19.4 mn

R$ 24.5 mn R$ 32.7 mn

R$ 15.3 mn R$ 19.4 mn

WHAT LIES AHEAD

52

> A multibusiness company with sales over R$50 billion

> Right people in the correct places with processes and systems

> Integration with synergy‟s capture of Ponto Frio and Nova Casas Bahia

reaching guidance

> Consolidation and expansion of cash-and-carry, supermarkets,

hypermarkets, proximity stores, specialized businesses, electronics

stores and e-commerce formats taking advantage of the Brazilian

middle class growth

MAIN ECONOMIC INDICATORS

53 Source: CDI, IGP-M and IPCA: FGV / Selic and Dólar: Bacen / TJLP: BNDES

2009

2010

Last 12 months (jul/10 - jun/11)

Interbank Deposit Certificate (CDI) 9.88% 9.75% 11.05%

General Price Index - Market (IGP-M) -1.72% 11.32% 8.64%

IPCA 4.3% 5.9% 6.7%

Federal Government Long-Term Interest Rate (TJLP) 6.2% 6.0% 6.1%

Dec 2009 Dec 2010 Jun 2011

Basic Selic Rate Copom 8.75% 10.75% 12.25%

Dollar Exchange Rate - in R$ 1.74 1.67 1.56

Dollar Exchange Rate - variation in 12 months -25.5% -4.3% -13.3%

54

Grupo Pão de Açúcar (GPA)

Globex Utilidades S.A.

Investor Relations Team

Phone: +55 (11) 3886-0421

Fax: +55 (11) 3884-2677

www.gpari.com.br

> FORWARD –LOOKING STATEMENTS

The forward-looking statements contained herein are based on our management’s current assumptions and estimates, which may result in material differences regarding future results, performance and events. Actual results, performance and events may differ substantially from those expressed or implied in these forward-looking statements due to a variety of factors, such as general economic conditions in Brazil and other countries, interest and exchange rate levels, legal and regulatory changes and general competitive factors (whether global, regional, or national).

CONTACT – INVESTOR RELATIONS