Report Series Saudi Arabia: Macroeconomic Forecast Update · Macroeconomic Forecast Update ......

17

August 2017 Report Series Office of the Chief Economist Economics Department Samba Financial Group P.O. Box 833, Riyadh 11241 Saudi Arabia [email protected] +4420-7659-8200 (London) This and other publications can be Downloaded from www.samba.com Saudi Arabia: Macroeconomic Forecast Update Executive Summary Global economic activity is generally quite brisk, though hopes of a reflation- led surge in the US have faded as President Trump’s dysfunctional administration has become mired in scandal and intrigue. The hoped-for fiscal expansion has not materialised and inflation pressures remain subdued, indicating that the Federal Reserve’s tightening cycle is likely to be longer and shallower than previously expected. Meanwhile, the Eurozone economy is gathering speed as credit growth expands and unemployment falls, boosting consumption. Spain, France and Germany are at the forefront of this expansion. As the economy improves so the ECB is likely to begin withdrawing accommodation next year. Thus, whereas we had earlier assumed that the USD would strengthen in line with higher rates, it now seems likely that the euro will continue to gain ground against the dollar as monetary policy in the Eurozone and US slowly converge. The weaker dollar has boosted demand for oil (and all commodities) with the price of Brent pushing back above $50/b in recent weeks, though the uptick has also reflected the draw on US stocks as shale output shows signs of flagging. We expect balances to continue to tighten, though there are legitimate concerns about how OPEC might eventually exit its supply agreement. Assuming this is orderly, we expect prices to edge up to $56/b in 2018 from $54/b this year. Brent should move up to average $65/b in 2019 as the dearth of exploration activity in recent years begins to bite. The economic situation in Saudi Arabia has not changed significantly since January. The authorities remain committed to a substantial fiscal adjustment and have focused on trimming procurement spending and raising nonoil revenue (mainly through additional fees). That said, the stance has loosened somewhat in recent months, and with oil revenue set to be some 60 percent below the 2014 figure, we expect the deficit to be SR300bn or 14 percent of GDP (somewhat smaller than last year). The medium term outlook suggests a narrowing path for the fiscal deficit as oil revenue recovers, nonoil sources expand, and spending growth remains modest. Financing for these declining fiscal deficits will be secured from both domestic and external sources without much trouble, and by 2021 the government’s total debt stock is still only likely to be about a third of GDP. The price of this fiscal adjustment is a domestic economy that is contracting, in nominal terms at least. Households are retrenching in the face of rising unemployment, while private and public investment has stalled. Conditions should improve next year in line with an expected pickup in government spending. Growth should start to accelerate further once substantial amounts of foreign direct investment enter the country, which is likely to be later in the forecast period. As such, we see nonoil growth picking up to 4.5 percent in 2021 from just 0.6 percent this year. A large contraction in import spending indicates that the current account will return to surplus this year. Net foreign assets are expected to stabilise and we expect the peg to the dollar to remain in place.

Transcript of Report Series Saudi Arabia: Macroeconomic Forecast Update · Macroeconomic Forecast Update ......

PUBLIC

August 2017

Report Series

Office of the Chief Economist Economics Department Samba Financial Group P.O. Box 833, Riyadh 11241 Saudi Arabia [email protected] +4420-7659-8200 (London) This and other publications can be Downloaded from www.samba.com

Saudi Arabia:

Macroeconomic Forecast Update

Executive Summary

Global economic activity is generally quite brisk, though hopes of a reflation-led surge in the US have faded as President Trump’s dysfunctional administration has become mired in scandal and intrigue. The hoped-for fiscal expansion has not materialised and inflation pressures remain subdued, indicating that the Federal Reserve’s tightening cycle is likely to be longer and shallower than previously expected. Meanwhile, the Eurozone economy is gathering speed as credit growth expands and unemployment falls, boosting consumption. Spain, France and Germany are at the forefront of this expansion. As the economy improves so the ECB is likely to begin withdrawing accommodation next year. Thus, whereas we had earlier assumed that the USD would strengthen in line with higher rates, it now seems likely that the euro will continue to gain ground against the dollar as monetary policy in the Eurozone and US slowly converge.

The weaker dollar has boosted demand for oil (and all commodities) with the price of Brent pushing back above $50/b in recent weeks, though the uptick has also reflected the draw on US stocks as shale output shows signs of flagging. We expect balances to continue to tighten, though there are legitimate concerns about how OPEC might eventually exit its supply agreement. Assuming this is orderly, we expect prices to edge up to $56/b in 2018 from $54/b this year. Brent should move up to average $65/b in 2019 as the dearth of exploration activity in recent years begins to bite.

The economic situation in Saudi Arabia has not changed significantly since January. The authorities remain committed to a substantial fiscal adjustment and have focused on trimming procurement spending and raising nonoil revenue (mainly through additional fees). That said, the stance has loosened somewhat in recent months, and with oil revenue set to be some 60 percent below the 2014 figure, we expect the deficit to be SR300bn or 14 percent of GDP (somewhat smaller than last year). The medium term outlook suggests a narrowing path for the fiscal deficit as oil revenue recovers, nonoil sources expand, and spending growth remains modest. Financing for these declining fiscal deficits will be secured from both domestic and external sources without much trouble, and by 2021 the government’s total debt stock is still only likely to be about a third of GDP.

The price of this fiscal adjustment is a domestic economy that is contracting, in nominal terms at least. Households are retrenching in the face of rising unemployment, while private and public investment has stalled. Conditions should improve next year in line with an expected pickup in government spending. Growth should start to accelerate further once substantial amounts of foreign direct investment enter the country, which is likely to be later in the forecast period. As such, we see nonoil growth picking up to 4.5 percent in 2021 from just 0.6 percent this year. A large contraction in import spending indicates that the current account will return to surplus this year. Net foreign assets are expected to stabilise and we expect the peg to the dollar to remain in place.

August 2017

PUBLIC

2

The Global Economic Backdrop

Trump travails see reflation expectations fade

Six months ago there were concrete expectations that Donald Trump’s presidency would herald a period of fiscal-driven reflation in the US. His expansionary approach would push growth, prices and interest rates higher, and widen the divergence between the US and the Eurozone, where deep-rooted structural problems and anaemic credit growth were likely to keep activity subdued. In fact, it is almost the opposite that has occurred.

Six months in and Mr Trump’s chaotic and divided administration has yet to register its first policy success: Obamacare has not been dismantled and the White House’s tax plans have yet to see the light of day. Many Republican lawmakers, especially in the Senate, have found his leadership style irksome and his team remains under investigation for possible collusion with the Russian government during the election campaign—an issue that is unlikely to go away. The US economy is still creating jobs, but price pressures are subdued and the Fed’s language has returned to its dovish norm.

Eurozone activity gathers pace

The Eurozone, meanwhile, has seen economic activity accelerate, with star performers such as Spain now being joined by France, while German growth continues to chug along. Consumption appears to have been buoyed by gradually declining unemployment as well as electoral successes for pro-EU politicians such as Emanuel Macron in France. Brexit remains a headache, but mainly for Britain itself. The ECB is still in quantitative easing mode, but tapering is expected to begin next year, and many analysts expect the base rate to begin rising in 2019, with some anticipating late 2018.

Thus the “policy spread” between the US and Eurozone appears likely to narrow rather than diverge. Markets have of course already factored much of this in, and the euro has enjoyed a 13 percent surge against the dollar so far this year. Supported by fundamentals, we therefore think that the euro will continue to strengthen against the greenback during the next two years, though at a softer pace (and with inevitable periods of volatility)

Oil demand appears robust but supply issues weigh on prices

The weaker dollar has boosted demand for all commodities, including oil, and oil demand this year is likely to stay strong, with East Asia the locus. Persistently low prices have mainly reflected supply issues. Part of the equation is OPEC’s commitment to its supply agreement of November 2016. Initially, compliance

Donald Trump’s dysfunctional administration has so far failed to deliver any fiscal stimulus. The economy is ticking over but inflation remains subdued and the Fed’s tightening path is likely to be gentle

2014 2015 2016 2017f 2018f

World 3.1 3.0 2.9 3.2 3.2

US 2.4 2.4 1.6 2.0 2.3

Japan -0.1 0.5 1.0 1.4 1.1

Euro area 0.9 1.5 1.7 1.8 1.7

China 7.3 6.8 6.7 6.6 6.2

Emerging Markets 4.0 3.3 3.3 3.8 4.0

Saudi Arabia 3.7 4.1 1.4 -1.0 0.7

US 0.25 0.50 0.75 1.50 2.25

Japan 0.10 0.10 -0.10 -0.10 -0.10

Euro area 0.15 0.05 0.00 0.00 0.00

Brent 100.0 58.0 47.0 54.0 56.0

Samba estimates and forecasts

World Economic Outlook

Official policy rate (end period)

Oil Price ($/b period average)

Real GDP (percent change)

August 2017

PUBLIC

3

was good, but this has frayed in recent months, with some mid-ranking producers allowing output to edge up. However, the main reason for rising OPEC output is two member countries that were not part of the deal: Nigeria and Libya. They were allowed to opt out owing to apparently intractable political problems. These problems have eased and production from the two countries has climbed by an aggregate 450,000 b/d this year.

The other supply wildcard is US shale production, which has put on some 650,000 b/d this year. A couple of years ago many estimated the average shale producer’s marginal cost of production at around $60-70/b. At that time, OPEC assumed that by flooding the market with crude and pushing prices below this level, shale producers would be decimated. But in line with American firms’ uncanny ability to hammer down on costs, shale producers were quick to adapt to lower prices, with many of the more productive plays allowing producers to make a profit at $45/b or even less. This realisation led OPEC to reverse course in November 2016 and withdraw supply from the market

Shale growth beginning to plateau?

Yet not all shale producers survived unscathed. Many smaller operators in more challenging terrain have been driven to the wall by sub-$50/b prices, while others have faced diminishing marginal returns. Thus, shale oil production, while still rising at end-July, has been losing momentum recently, with flattening oil rig count growth indicating that production might continue to slow. Indeed, these dynamics are beginning to influence overall US crude stocks. Stocks are still elevated—they remain higher than at the turn of the year—but the trend since the second quarter has been down, suggesting that stocks have been drawn by the combined impact of robust demand, weakening shale growth, and reduced OPEC supply. Price spreads on various types of global crude are beginning to widen, which is associated with a tightening of supply.

Unwinding the OPEC agreement will need care

Despite this, OPEC could well decide to extend its supply agreement beyond March 2018, when it is currently scheduled to end. Some analysts worry how OPEC will finally end its agreement: a disorderly exit could see a flood of oil on to the market. This will indeed need to be carefully managed, but we think that balances will be significantly tighter by the time any such exit occurs. Shale production is also likely to recover in line with prices, which will clearly keep a check on price growth in the near term. For the moment, therefore, we expect prices to edge up slowly as the large stock overhang is gradually whittled away. We expect Brent to average $54/b this year, before edging up to an average $56/b in 2018. Assuming that the OPEC agreement

Unwinding OPEC’s supply agreement will need to be handled carefully

August 2017

PUBLIC

4

is successfully unwound, we project that Brent will average $65/b in 2019. This price gain partly reflects the impact of investment that was shelved by international oil companies from 2014 onwards as prices sagged. This will show up as tighter supply in the medium term.

The Outlook for Saudi Arabia

Reform efforts remain broadly on track

Events in the first six months of 2017 suggest that the government’s reform efforts remain broadly on track. Fiscal consolidation has continued, albeit with some relaxation of current spending, and financing sources have been expanded. Efforts to improve the investment environment—particularly for portfolio inflows—have been stepped up. The reform drive also appears more durable given recent political consolidation by its main sponsor, the Crown Prince. Less favourably, the regional political climate has deteriorated, which might be off-putting for potential foreign direct investors.

Oil income this year is likely to be lower than initially thought

Starting with the fiscal situation: we note that the government recorded a much-reduced fiscal deficit in the first quarter in year-on-year terms. However, this overwhelmingly reflects the very weak oil revenue performance in the first quarter of 2016. Moreover, the fiscal outlook has deteriorated moderately given the downward adjustment to our oil price forecast. In January we were expecting Brent to average $57/barrel this year and $62/b next; however, our new oil price assumptions—allied to the deepening of OPEC production cuts—indicates that oil revenue will be around SR390bn this year. This is still comfortably higher than last year’s SR330bn, but is less than the SR445bn recorded in 2015. In fact, we now project oil income to remain below the 2015 level in 2018 too. More positively, the ongoing rises in gasoline prices should help to soften domestic consumption of fuels, allowing additional crude to be freed up for export.

Note that we do not think that the change in Aramco’s taxation rate from 85 percent to 50 percent will have a material impact on government finances. The idea is that the “lost” 35 percent will be made up by dividends paid by Aramco to all shareholders, including the state. Of course, if the state does sell 5 percent of Aramco, then it will lose the flow of dividends on that stake. But this should, theoretically at least, be offset by flows generated by the Public Investment Fund (PIF) which will be capitalised by proceeds from the 5 percent sale. Clearly, the PIF’s investments

Fiscal consolidation has continued and political developments suggest that the reform drive is more durable

August 2017

PUBLIC

5

might not generate immediate—or equivalent—flows and that constitutes a modest risk to the fiscal outlook. But equally, the PIF could generate better flows in the future than Aramco—in fact that notion underpins the Vision 2030 project.

We have not included potential revenue from the proposed sale of 5 percent in Aramco, mainly because we cannot be sure of the likely valuation (estimates have ranged from $900bn to over $2 trillion). The 2018 timing of the sale could also be pushed back to coincide with the Tadawul’s inclusion in the MSCI EM, although this may be less of an issue if the majority of the listing is done in an overseas jurisdiction. These caveats aside, there is clearly significant upside potential to our revenue projections.

Nonoil income likely to make steady gains

Meanwhile, nonoil income is expected to gather pace. There was little yield from nonoil income in the first quarter, and there is unlikely to be much, if any, gain in customs revenue given a further steep fall in import spending this year. However, we do think that there will be more noticeable gains in nonoil revenue in the second half as various fees and charges are rolled out, and collection becomes more efficient. Next year sees the introduction of VAT, which should yield some SR35bn (around 5 percent of total projected revenue). Over the medium-term we expect that nonoil revenue will rise to some SR315 billion or a third of overall revenue by 2021.

Allowances are reinstated, but spending stance still tight

In terms of spending, the government’s tight fiscal grip was relaxed somewhat when it was announced that the cuts to public sector allowances (PSA) announced in October last year, would be reversed and retrospective payments made back to October. We also note that further cuts to fuel subsidies might well be delayed until 2018, though subsidies represent more of an opportunity cost than a direct financial outlay.

We do not think that the cuts to PSA signal a significant shift in policy: with a freeze in nominal salaries still in place spending on public sector employees is likely to be pretty much the same this year as last. Rather, the authorities will have seen that the cuts to disposable income were in danger of shrinking the domestic economy—through the multiplier effect—and hence the denominator for government deficits, debt etc. Instead, the authorities are likely to refocus on squeezing procurement costs. This is an area of spending that had grown almost exponentially in the early part of the decade and there is still plenty of scope to make savings.

August 2017

PUBLIC

6

Capital spending has been squeezed extremely hard in the past two years, falling by some 38 percent since 2014. As with procurement, capital spending had soared in the first half of this decade, growing by an average 17 percent a year up to 2014. The authorities have made great strides to rationalise investment spending mainly by improving oversight and tightening budgetary control. We have pencilled in some pickup in capital spending in the second half of this year, though this is very much oil price-dependent. Another drift down in oil prices towards $40/b would likely see the authorities keep public investment in check.

Spending set to shrink by around 3 percent this year

All told, we think that government spending will shrink by around 2.7 percent this year, with the reinstatement of allowances and the assumed uptick in capital spending being more than offset by the crackdown on procurement costs. This should mean an overall improvement in the fiscal position, but the deficit will remain large at more than 14 percent of GDP, down from some 17 percent in 2016.

We expect the fiscal squeeze to be relaxed in 2018, when current spending is expected to increase for the first time since 2014, and capital spending will see a further modest increase. The government will feel able to do this because of the likely increase in nonoil revenue (principally from VAT) and the assumed uptick in oil revenue as prices continue to recover. This should mean a deficit of some 12 percent of GDP.

Looking to the medium term, we expect the fiscal position to continue to improve as oil prices maintain their gentle ascent and nonoil revenue sources expand and deepen. Thus by 2021 the deficit should have narrowed to about 3.5 percent of GDP (SR100bn). This is slightly bigger than the Maastricht criteria limit (3 percent) but is well within bounds for an Emerging Market (or indeed an EU state).

Domestic and external sources will be tapped for financing

For the 2017-21 period the government will need to find almost SR1 trillion in fiscal financing. While substantial, the financing “intensity” should not be as severe as 2015-16 when a SR765bn gap needed to be closed in just two years. The government will

Saudi Arabia: Fiscal Projection (Samba)(SRbn) 2016 a 2017 2018 2019 2020 2021

Government revenue 528.1 601.3 664.0 775.2 878.8 959.9

(% change) -13.9 13.9 10.4 16.7 13.4 9.2

(% GDP) 22.0 28.1 30.1 32.8 34.8 36.2

of which, Oil 329.0 386.8 407.8 506.6 592.6 646.2

Government spending 929.6 904.6 931.3 961.7 1007.0 1055.7

(% change) -4.9 -2.7 3.0 3.3 4.7 4.8

(% GDP) 38.8 42.3 42.2 40.7 39.9 39.8

Balance -401.5 -303.3 -267.3 -186.4 -128.2 -95.8

a=actual -16.7 -14.2 -12.1 -7.9 -5.1 -3.6

Sources: MOF, SAMA, Samba

Fiscal financing needs over the next five years are likely to be sizeable. That said, financing pressure should not be as intense as it was in 2015 and 2016

August 2017

PUBLIC

7

continue to use the mix of domestic and external debt issuance, along with savings drawdown, to finance its position. There is likely to be a roughly equal split between domestic debt issuance to local banks and institutions such as the PIF and GOSI on the one hand, and sovereign issues (both conventional and sukuk) on the other. The local banking system remains in good shape, with strong capitalisation and good liquidity (especially given soft private sector credit demand). Note that the government’s debut local Islamic bond sale in July for SR17 billion generated offers of SR51 billion.

External creditors should continue to view the Kingdom positively

External appetite is also likely to remain strong. Granted, the flow of global liquidity is beginning to slow as various central banks begin (or begin to talk about) withdrawing accommodation. But the Kingdom is still likely to be viewed as a strong credit, given its energy resources and comfortable debt metrics. We therefore believe that the fiscal financing requirement will be met relatively comfortably, though we acknowledge that our forecast is underpinned by an assumption of gradually recovering oil prices. By the end of 2021 domestic debt is projected to be worth some SR485bn, or 18 percent of GDP, while external debt should have reached SR415bn or 16 percent of GDP.

Good progress has been made on capital market reform

Structural reform is the other major policy thrust. Most progress has been made on opening up the capital market. Foreign institutions with $1 billion assets under management can now trade equities directly, with a cap of 10 percent of any single stock. The Capital Markets Authority (CMA) has also shifted the settlement cycle to two days—so-called T+2—allowing traders to complete the transfer of funds within 48 hours, rather than the same day, bringing the Saudi exchange in line with international peers. It has also allowed short-selling.

Saudi Arabia: Fiscal Financing Outlook(SRbn) 2016 2017 2018 2019 2020 2021Fiscal financing requirement 401 303 267 186 128 96Financed by:Domestic debt issuance, of which: 112 80 83 51 37 35 to local banks 92 55 63 36 27 25 to GOSI, PIF, etc 20 25 20 15 10 10

External debt issuance 100 90 94 56 38 38

Total issuance 212 170 177 107 74 73

Change in government deposits -190 -133 -90 -80 -54 -23memoranda:Central Govt domestic debt 198 278 361 412 449 484 % GDP 8.3 13.0 16.4 17.5 17.8 18.2Central Govt external debt 100 190 284 340 377 415 % GDP 4.2 8.9 12.8 14.4 15.0 15.6Sources: MOF, SAMA, Samba

August 2017

PUBLIC

8

QFI ownership of Saudi stocks remains small, though this is mainly a reflection of a generally subdued market, which has been weighed down by the downward drift of oil prices and regional tensions. However, the Tadawul is now on the watch list for inclusion in MSCI’s Emerging Market index. With most criteria now met, inclusion will depend largely on QFI feedback to MSCI. Assuming that this is positive, then the Tadawul should be included in the index from mid-2018. This will mean an “automatic” inflow of foreign funds managed by a whole range of asset managers across the globe, who essentially track MSCI indices. Many will simply apportion their funds according to the Tadawul’s weighting in the overall index, which in turn will depend on the Tadawul’s market cap at the time of inclusion. We expect something around $40 billion in such inflows for 2018-21 (see balance of payments, below).

Broader investment environment needs improvement

There has been less progress in attracting foreign direct investment. FDI is more critical to the success of the Vision 2030 project as it provides non-debt-creating capital inflows and technology transfer which should, hopefully, nurture a private sector that is not wedded to government spending. FDI inflows eased to just $7.5 billion in 2016, consolidating a downward trend that partly reflects the completion of a number of large energy projects earlier in the decade, but also a deterioration in the business environment. The World Bank’s Ease of Doing Business ranking is an imperfect measure, but the trend is unmistakable. From number 11 in the global rankings in 2011 the Kingdom has slipped to number 94 in the latest survey. The most pressing weaknesses in the business environment are the ability to resolve insolvency (there is no bankruptcy law), contract enforcement, the number of procedures to start a business, and delays associated with ports. One way of short-cutting this problem is to create free zones for certain sectors (or even firms) such as in logistics. But the issues listed by the World Bank will need to be addressed in order to encourage a broader and deeper flow of investment that would benefit the whole private economy.

Domestic economy weighed down by fiscal correction

How has the domestic economy performed in the face of these fiscal and broader policy currents? While the medium- to long-term outlook now appears more sustainable, the current economic performance has been constrained by the sizeable fiscal adjustment. The private sector’s long-standing and well-entrenched reliance on public sector spending means that when the state effectively reduces its role in the economy, private sector activity also shrinks rather than fills the space. Thus, gross fixed capital formation declined by 3.9 percent year-on-year

target

August 2017

PUBLIC

9

in the first quarter (current prices). Higher frequency indicators confirm the downward trend: bank lending to the private sector was down by almost 2 percent in the 12 months to June (the largest such contraction since mid-2000), while private sector imports of building materials (new LCs) were down by a whopping 24 percent. In fact, overall private import spending was down 27 percent in the first half of 2017 compared with H1 2016. This follows a 22 percent contraction in total import spending for 2016 as a whole. Based on current trends, import spending is likely to be back to less than $100 billion this year—roughly the same level as in 2010. The Saudi economy is heavily dependent on imports and a large contraction points to a slowdown in activity rather than a change in investment or consumption preferences.

Households retrench as unemployment rises

The near-term outlook for private consumption, which accounts for 45 percent of GDP, is weak. The authorities’ decision to reverse the cuts to PSA (and backdate payments), and the reported plans to postpone a further cut to fuel subsidies, is clearly positive from a consumption point of view. Ordinarily, one might expect this to provide a fillip to retail sales in the second half. However, a major headwind is provided by the rise in unemployment, which reached 12.7 percent in the first quarter, up from 12.3 percent at end-2016. This large figure is in some senses skewed by the inclusion of women since they were until relatively recently economically inactive. Yet looking at just male unemployment shows a 1.3 percentage point increase during the quarter (from 5.9 percent to 7.2 percent). An increase of this size naturally leads households to be more cautious in their spending, regardless of whether their disposable income has been boosted or not.

This caution is already becoming apparent in retail sales. Retail sales (proxied by points of sale transactions) went into reverse in the 12 months to June. This should be treated with caution as the downturn was not large—just 0.8 percent—and the timing of Ramadan might have played a role. But our sense is that households are retrenching, and this trend is unlikely to unwind in the near term.

August 2017

PUBLIC

10

A mooted pick up in public investment should help to keep nonoil growth just about positive this year

Private investment might benefit from a mooted pickup in government capital spending in the second half of the year, but the latter remains very much oil-price dependent: another prolonged bout of sub-$50/b oil prices would likely lead the government to shelve its investment plans. Assuming this does not happen, we expect the nonoil economy to post growth of around 0.6 percent this year, roughly the same rate as in 2016, but risks are tilted to the downside given the oil price environment and fragile household confidence. Note that the overall economy is expected to contract by about 1 percent reflecting the cut to oil output.

Next year should see some pickup in activity, with a small increase in government spending allied to a moderate rise in foreign investment helping to revive private confidence somewhat. Consumption should also be supported through the wealth channel by the expected inclusion of the Tadawul in the MSCI EM index. That said, confidence will take a while to feed through and nonoil growth next year is likely to be held to around 1 percent in real terms.

The longer term outlook is dependent on the fiscal stance and foreign direct investment inflows

The medium-term growth outlook will continue to be influenced by the government’s fiscal stance. This is expected to remain tight by historical standards, but will begin to loosen as revenue (both oil and nonoil) picks up gradually. Private consumption might face some headwinds from the tax on expatriate dependents, which is set to be ramped up over the next five years. This is likely to push many dependents to leave the country which, according to one analysis, could see consumption fall by almost SR20bn by 2020 (roughly 1.2 percent of our projection for 2020 nominal nonoil GDP). However, the overall economic impact should be ameliorated by the boost to government spending allowed by the fee income and a broader improvement in household confidence.

Meanwhile, private investment, both domestic and foreign, is expected to play a bigger role in the years ahead as privatisation gathers pace and further deregulation is rolled out in line with the precepts of Vision 2030. As noted above, there are challenges to be overcome, and foreign investors will be looking in particular for a transparent, easily navigable business and legal

Saudi Arabia: GDP

(percent change) 2016 2017 2018 2019 2020 2021

Real GDP 1.4 -1.0 0.7 2.5 3.5 3.7

Real Nonoil GDP 0.7 0.6 0.9 2.2 3.9 4.5

Sources: General Authority for Statistics, Samba

A moderate increase in public investment in the next few months should keep nonoil growth in positive territory this year

August 2017

PUBLIC

11

environment, along with a reasonably stable regional situation. Domestic investment could well be led by the PIF, which is set to be fully capitalised by proceeds from the Saudi Aramco sale.

Clearly, not every element of the Vision 2030 programme will come to pass, but assuming that the general thrust of the programme remains on track, then we would expect real nonoil sector to accelerate gradually. Only in the latter stages of the forecast period, as FDI inflows deepen, is growth expected to pick up significantly. By 2021 we anticipate that growth will be pushing 5 percent. Following a sharp fall this year (owing largely to deflation—see below) GDP per head is expected to recover to some $19,300 by 2021, though note that this is still some $800 lower than last year’s level.

Deflation sets in, but some increase in prices is expected over the next 12 months

In a testament to the contraction of domestic demand, the economy experienced deflation in the first six months of the year. Consumer prices contracted by 0.4 percent year-on-year in June, consolidating the trend of the previous five months (the contraction would probably have been greater were it not for a scheduled increase in the price of tobacco products in June). Given that a further reduction of fuel subsidies appears to have been shelved for the time being, and given also the retrenchment of household spending, we think price growth will essentially stagnate this year.

The index will see a significant shift up in early 2018 as VAT is introduced at 5 percent. Second-round effects and the slight loosening of the government’s fiscal stance indicates that average inflation will be around 2 percent, but note that underlying price pressures will remain weak. Price growth should pick up in the 2019-21 period as subsidies continue to be removed, spending (both private and public) gathers pace, and the USD weakens. We expect consumer price inflation to average around 3.3 percent during this period.

Oil price fall brings current account back into focus

For many years the balance of payments has not been a concern for Saudi Arabia. Only in 1998 did the current account record a deficit, and that was reversed the following year. From then until 2014 the current account recorded hefty surpluses, allowing a

Saudi Arabia: Consumer Prices(percent change) 2016 2017 2018 2019 2020 2021

General index (2007=100) 137.6 137.6 140.4 144.5 149.5 154.9

CPI 2.2 0.1 2.0 2.9 3.5 3.6

Sources: SAMA, Samba.

The longer term growth outlook depends on both the trajectory of government spending, and the amount of foreign direct investment that can be attracted. From a structural point of view, the latter will be important in helping to nurture a genuinely autonomous private sector

Demand contraction saw prices decline in the first half. Programmed price increases will probably see inflation return in the months ahead, but underlying price pressures will remain weak

August 2017

PUBLIC

12

substantial accumulation of net foreign assets. NFA peaked in 2014 at $725 billion, or 96 percent of GDP. However, the oil price crash in mid-2014 meant that that year’s current account surplus was half of the preceding year’s, and by 2015 the current account had moved into deficit. At 8.2 percent of GDP this was quite sizeable, but the private sector’s rapid response to the deteriorating business environment (through a squeeze on import spending) meant that the deficit halved in size in 2016.

Nevertheless, the spectre of “twin deficits” (fiscal and current account) aroused the interest of speculators, who hypothesised that the draw on foreign assets might be enough to make the riyal’s peg to the US dollar unsustainable. Indeed, pressure on the peg in the forward market intensified in 2015, though this was exclusively from external speculators; local banks were happy to take the other end of the trade. Pressure has since eased, but has not fully abated. So what is the outlook for the balance of payments?

Import adjustment has kept trade balance in surplus

One notable feature of the visible trade account has been the remarkable squeeze in import spending, which fell by 22 percent in 2016 and is set for another substantial fall this year (see above). The elasticity of import spending has helped to keep the overall trade balance in surplus even as oil prices (and production) have fallen. The surplus should grow in the years ahead as oil revenue outpaces the expected recovery of import spending.

Nonoil exports should also show decent growth

Nonoil exports are a key element of the Vision 2030 programme. The idea is that foreign investment should enliven the nonoil tradeables sector, thereby creating jobs and boosting productivity. Most importantly, the nonoil export sector would provide a genuinely autonomous part of the economy, not reliant on government spending; indeed, it would provide the government with an alternative source of foreign exchange through taxation. Prospects for nonoil exports will depend in part on further efforts to improve the business environment. It might be that a flexible exchange rate is needed to really boost this sector and avoid the perils of “Dutch Disease”, but this is something for the much longer term; for the moment the authorities are concerned with ensuring macroeconomic stability. In the absence of any change to the exchange rate and assuming decent FDI inflows, we expect nonoil export earnings to be some $90 billion by 2021 up from some $50 billion in 2016.

August 2017

PUBLIC

13

Outlook for remittances unclear, but we expect the current account to post growing surpluses in years ahead

The biggest imponderable on the invisibles side of the current account is workers’ remittances. These outflows continued to grow over the past five years, but at a reduced pace as the economy slowed. Looking ahead, the recent implementation of the tax on expatriate families might encourage greater outflows as workers funnel more money back to families no longer living in the Kingdom. But a counter-current will be the general imperative for Saudiisation which will presumably mean fewer expatriate opportunities in many sectors. On balance, we see remittances outflows edging up gently in the years ahead, but at a slower pace than nominal GDP as their share of the economy moderates.

Despite this, we expect the current account to record growing surpluses in the years ahead. By 2021 the surplus should be in excess of $100bn, or 15 percent of GDP.

Financial account sees volatile private outflows

The financial account is somewhat opaque, but has typically been in deficit owing to hard-to-capture private capital outflows (net errors and omissions are usually large). As noted elsewhere, direct investment inflows have been modest, though we do expect them to start picking up. Portfolio inflows too should see more pronounced growth once the Tadawul is included in the MSCI EM index. However, for the moment the main dynamic on the financial account is private sector outflows, which are mainly recorded as “currency and deposits”. On a quarterly basis these have tended to average around $3 billion over the past few years, but there was a sharp spike in the first quarter of 2017 to $18bn.

Saudi Arabia: Current Account($ billion) 2016 2017 2018 2019 2020 2021Trade balance 59.7 93.1 107.3 145.3 177.0 197.8Exports 181.6 186.8 205.7 250.0 291.0 322.1 percent change -10.8 2.8 10.1 21.5 16.4 10.7of which, oil 120.2 134.0 145.0 180.1 210.7 229.7 nonoil 50.3 52.8 60.7 69.8 80.3 92.4Imports -121.9 -93.7 -98.4 -104.7 -114.0 -124.3 percent change -22.1 -23.1 5.0 6.4 8.9 9.0Invisibles balance -83.3 -63.4 -67.4 -73.1 -81.4 -90.7Services credit 16.0 16.5 17.0 17.5 18.0 18.9Services debit -71.2 -54.7 -57.5 -61.1 -66.6 -72.6Services balance -55.2 -38.3 -40.5 -43.6 -48.6 -53.7Income credit 23.5 24.7 25.9 28.0 30.5 33.2Income debit -8.3 -10.4 -13.0 -16.9 -21.9 -28.1Income balance 15.2 14.3 12.9 11.1 8.6 5.2Transfers balance -43.3 -39.4 -39.8 -40.6 -41.4 -42.2of which, workers' remittances -38.0 -35.7 -35.4 -36.1 -36.8 -37.2Current account balance -23.6 29.7 39.9 72.2 95.7 107.1 percent GDP -3.7 5.2 6.8 11.5 14.2 15.2Sources: SAMA, IMF, Samba

The first quarter saw sizeable private outflows. This helps to explain why NFA have taken a while to stabilise despite two successful external bond issues

August 2017

PUBLIC

14

This, and a large outflow on the net errors and omissions, is the main reason why official net foreign assets have not stabilised despite two successful sovereign bond/sukuk issues, and recent shift back to current account surplus. The first quarter spike may well reflect the repayment of domestic contractors by the government in the final quarter of 2016. The recipients of these repayments may in turn have had to meet external obligations, and/or invested the money abroad (exchanging SR for FX).

Second quarter banking data (there are no balance of payments data yet) are inconclusive: private depositors appear to have made quite a major shift from SR deposits (which fell by SR35bn) to foreign currency deposits in local banks (which rose by SR24bn) during the quarter, though this is not necessarily a prelude to capital outflows. In fact, SAMA’s NFA actually rose for the first time in over a year in June. This possibly relates to the repatriation of sukuk proceeds, though balance of payments data will be needed to get a clearer picture.

Net outflows should diminish in the years ahead

Looking ahead, these capital outflows should diminish as domestic investment opportunities become more plentiful. However, as noted elsewhere, to maximise the creation of such opportunities it will be important that improvements to the business environment proceed as planned. Absent these, private capital outflows could continue to create a draw on NFA, particularly as official outflows (through the PIF) are likely to be sizeable. In the medium- to long-term we expect both official and private outflows to be offset by private investment inflows as the country’s privatisation programme gathers pace, and by inflows on the current account as the PIF’s investments generate foreign earnings.

Saudi Arabia: Financial Account($ billion) 2016 2017 2018 2019 2020 2021Current account balance -23.6 29.7 39.9 72.2 95.7 107.1Direct investment -1.0 0.0 -2.0 -3.0 -2.0 -3.0Abroad -8.5 -7.0 -12.0 -15.0 -17.0 -20.0in KSA 7.5 7.0 10.0 12.0 15.0 17.0Portfolio investment -12.3 -6.5 0.1 -0.3 -1.8 3.5Abroad -29.8 -32.5 -30.9 -29.3 -27.8 -26.5in KSA 17.5 26.0 31.0 29.0 26.0 30.0Other investment -0.8 -27.0 -22.7 -19.4 -16.1 -14.0Abroad -9.9 -27.0 -25.7 -24.4 -23.1 -22.0in KSA 9.1 0.0 3.0 5.0 7.0 8.0Financial account balance -14.1 -33.5 -24.5 -22.7 -20.0 -13.4Net errors and omissions -42.8 -35.5 -24.1 -21.2 -14.4 -6.2Overall balance -80.5 -39.3 -8.7 28.3 61.2 87.5Change in reserves (- = increase) 80.3 39.3 8.7 -28.3 -61.2 -87.5Official NFA 528.6 489.4 480.7 508.9 570.2 657.7 percent GDP 82.6 86.1 82.0 81.1 84.9 93.2 import cover (months) 52.0 62.7 58.6 58.4 60.0 63.5

-5.0

10.0

15.0

20.0

The financial account deficit should gradually diminish and with the current account recording large and growing surpluses official NFA should begin to build again from 2019 onwards

August 2017

PUBLIC

15

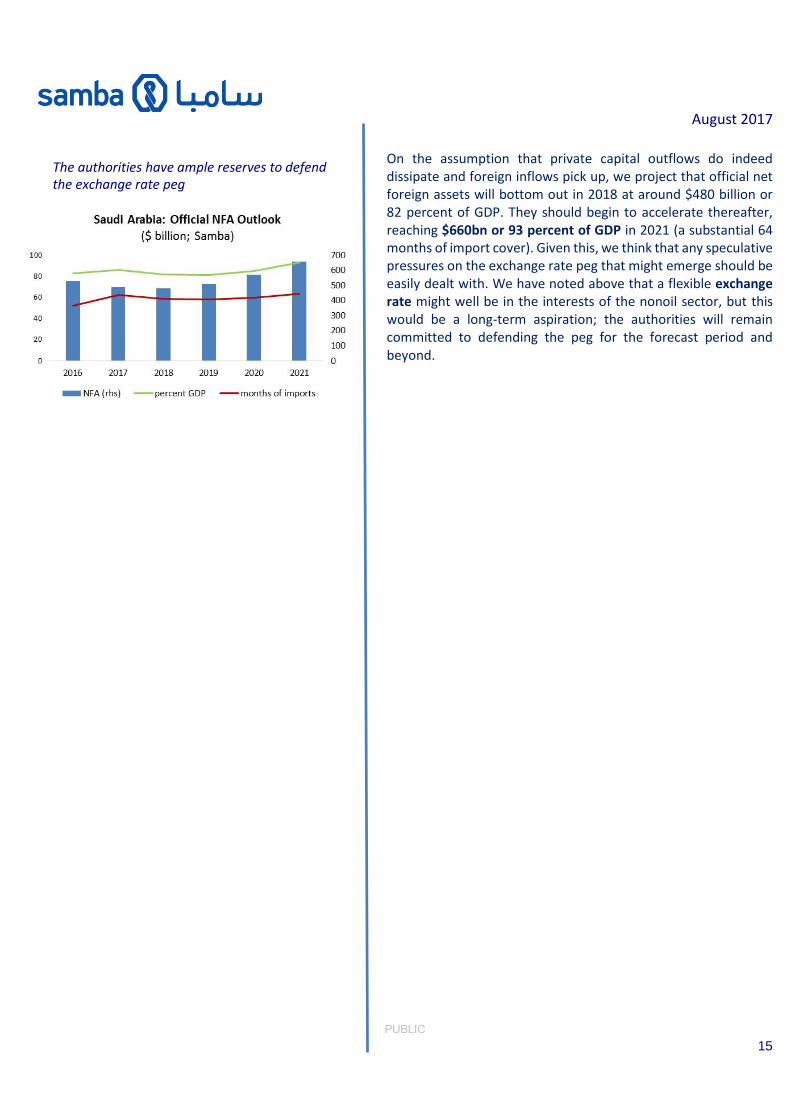

On the assumption that private capital outflows do indeed dissipate and foreign inflows pick up, we project that official net foreign assets will bottom out in 2018 at around $480 billion or 82 percent of GDP. They should begin to accelerate thereafter, reaching $660bn or 93 percent of GDP in 2021 (a substantial 64 months of import cover). Given this, we think that any speculative pressures on the exchange rate peg that might emerge should be easily dealt with. We have noted above that a flexible exchange rate might well be in the interests of the nonoil sector, but this would be a long-term aspiration; the authorities will remain committed to defending the peg for the forecast period and beyond.

The authorities have ample reserves to defend the exchange rate peg

August 2017

PUBLIC

16

Saudi Arabia: Baseline Macroeconomic Forecast 2016 2017f 2018f 2019f 2020f 2021f

Nominal GDP ($ bn) 639.6 568.2 585.9 627.5 671.7 705.3

% change -2.5 -11.2 3.1 7.1 7.0 5.2

GDP per capita ($ '000) 20,133 17,365 17,416 18,147 18,913 19,336

Real GDP (% change) 1.4 -1.0 0.7 2.5 3.5 3.7

Hydrocarbon GDP 2.4 -3.5 0.5 3.0 3.0 2.5

Non-hydrocarbon GDP 0.7 0.6 0.9 2.2 3.9 4.5

Money supply, M2 (SR bn) 1636.0 1610.0 1650.0 1750.0 1890.0 2003.4

% change 3.5 -1.6 2.5 6.1 8.0 6.0

Commercial bank loans to private sector (SR bn) 1337.0 1343.7 1397.4 1453.3 1540.5 1663.8

% change 2.2 0.5 4.0 4.0 6.0 8.0

3 month interbank rate (end year, percent) 2.0 1.47 1.8 2.1 2.6 2.9

CPI inflation (% change, average) 2.2 0.1 2.0 2.9 3.5 3.6

Hydrocarbon exports ($ bn) 120.2 134.0 145.0 180.1 210.7 229.7

% change -23.2 11.5 8.2 24.2 17.0 9.0

Current account balance ($ bn) -23.6 29.7 39.9 72.2 95.7 107.1

(% GDP) -3.7 5.2 6.8 11.5 14.2 15.2

Fiscal revenue (SR bn) 528.1 601.3 664.0 775.2 878.8 959.9

(% change) -13.9 13.9 10.4 16.7 13.4 9.2

Fiscal spending (SR bn) 929.6 904.6 931.3 961.7 1007.0 1055.7

(% change) -4.9 -2.7 3.0 3.3 4.7 4.8

of which, capital 235.0 239.7 251.7 264.3 288.1 311.1 (% change) -10.9 2.0 5.0 5.0 9.0 8.0 current 694.6 664.9 679.7 697.4 718.9 744.6 (% change) -2.7 -4.3 2.2 2.6 3.1 3.6

Fiscal balance (SR bn) -401.5 -303.3 -267.3 -186.4 -128.2 -95.8

(% GDP) -16.7 -14.2 -12.2 -7.9 -5.1 -3.6

Public sector gross deposits with banking system (SR bn) 972.6 839.5 749.1 669.5 615.4 592.2

(% GDP) 40.5 39.4 34.1 28.4 24.4 22.4

Public sector gross debt (SR bn) 346.8 519.5 695.8 802.2 875.8 947.9

(% GDP) 14.5 24.4 31.7 34.1 34.8 35.8

Other public sector domestic deposits (SR bn) 1098.0 1098.0 1098.0 1098.0 1098.0 1098.0

(% GDP) 45.8 51.5 50.0 46.7 43.6 41.4

Total net public sector deposits with banking system (SR bn) 1772.8 1469.5 1202.2 1015.7 887.5 791.7

(% GDP) 73.9 69.0 54.7 43.2 35.2 29.9

Memoranda:

Oil price (Brent; $/barrel) 47.0 54.0 56.0 65.0 72.0 75.0 Crude oil production ('000 b/d) 10500 10062 10080 10400 10700 10968 SAMA's net Foreign Assets ($ bn) 528.6 489.4 480.7 508.9 570.2 657.7

(% GDP) 82.6 86.1 82.0 81.1 84.9 93.2

Sources: SAMA; Ministry of Finance; General Statistics Authority; IMF; Samba.

August 2017

PUBLIC

17

James Reeve Deputy Chief Economist [email protected] Andrew Gilmour Deputy Chief Economist [email protected] Thomas Simmons Economist [email protected]

Disclaimer This publication is based on information generally available to the public from sources believed to be reliable and up to date at the time of publication. However, SAMBA is unable to accept any liability whatsoever for the accuracy or completeness of its contents or for the consequences of any reliance which may be place upon the information it contains. Additionally, the information and opinions contained herein: 1. Are not intended to be a complete or comprehensive study or to

provide advice and should not be treated as a substitute for specific advice and due diligence concerning individual situations;

2. Are not intended to constitute any solicitation to buy or sell any instrument or engage in any trading strategy; and/or

3. Are not intended to constitute a guarantee of future performance. Accordingly, no representation or warranty is made or implied, in fact or in law, including but not limited to the implied warranties of merchantability and fitness for a particular purpose notwithstanding the form (e.g., contract, negligence or otherwise), in which any legal or equitable action may be brought against SAMBA. Samba Financial Group P.O. Box 833, Riyadh 11421 Saudi Arabia