REAL INTERES RATT E PARITY

22

REAL INTEREST RATE PARITY: DECOMPOSITION OF FINANCIAL AND COMMERCIAL COMPONENTS I N T H E CASE OF COLOMBIA Sergio Clavijo* Minister of Finance of Colombia Resumen: Este trabajo profundiza en el concepto de paridad inter- nacional de las tasas de interés, cuyo análisis en nuestro medio ha estado limitado al diferencial de tasas nominales de interés, ajustado por la devaluación. Dicho diferencial nominal sólo se aproximaría al real en la medida en que se hubiese mantenido la regla de paridad del poder adquisitivo, lo cual no ha ocurrido en todo momento. Abstract: The concept of interest rate parity is here revisited, emphasizing the different results that are obtained when the analysis is made either using a nominal interest rate difference, adjusted by the actual or expected rate of depreciation, or using a real interest rate difference. The results vary according to deviations from "purchasing power parity". ntroduction •uring the 1980s, analytical efforts were made to distinguish between ominal determinants of the interest rates (i.e. to isolate the inflation ffect) from its real determinants (i.e. components of the cost of use of ipital). For example, in the case of Colombia, Olivera (1993) found that hile nominal interest rates had descended from an average of 35% to 1% per annum in the period 1980-1991/1992-1993, the cost of use of * The author is indebted to A. Carrasquilla for helpful comments on an earlier draft. ;sponsibility for opinions and remaining errors rests only with the author and do not cessarily represent the points of view of the Colombian Government. Eco, 11, 1, 1996 117

Transcript of REAL INTERES RATT E PARITY

R E A L I N T E R E S T R A T E P A R I T Y : D E C O M P O S I T I O N O F F I N A N C I A L A N D C O M M E R C I A L C O M P O N E N T S I N T H E

C A S E O F C O L O M B I A

Sergio Clavijo* M i n i s t e r of F i n a n c e of Colombia

R e s u m e n : Este trabajo profundiza en el concepto de paridad internacional de las tasas de interés, cuyo análisis en nuestro medio ha estado limitado al diferencial de tasas nominales de interés, ajustado por la devaluación. Dicho diferencial nominal sólo se aproximaría al real en la medida en que se hubiese mantenido la regla de paridad del poder adquisitivo, lo cual no ha ocurrido en todo momento.

A b s t r a c t : The concept of interest rate parity is here revisited, emphasizing the different results that are obtained when the analysis is made either using a nominal interest rate difference, adjusted by the actual or expected rate of depreciation, or using a real interest rate difference. The results vary according to deviations from "purchasing power parity".

ntroduction

•uring the 1980s, analytical efforts were made to distinguish between ominal determinants of the interest rates (i.e. to isolate the inflation ffect) from its real determinants (i.e. components of the cost of use of ipital). For example, in the case of Colombia, Olivera (1993) found that hile nominal interest rates had descended from an average of 35% to 1% per annum in the period 1980-1991/1992-1993, the cost of use of

* The author is indebted to A. Carrasquilla for helpful comments on an earlier draft. ;sponsibility for opinions and remaining errors rests only with the author and do not cessarily represent the points of view of the Colombian Government.

E c o , 11, 1, 1996 117

118 ESTUDIOS ECONÓMICOS

capital had been reduced from 30% to nearly 13% per annum. The driving force in the reduction of the nominal interest rate was the deceleration of inflation, which fell from an average of 29.8% per annum during 1990¬1992 to 22.4% during 1993. The dramatic reduction in the cost of use of capital had to do with the liberalization of trade, which implied both the abolition of most quantitative restrictions levied on imported goods and the reduction of effective tariffs from an average of nearly 75% in 1989 to 7% in 1993 (including the abolition of the surcharge). The reduction in the cost of use of capital was further reinforced by the creation of tax incentives in the imports of capital goods.

Additionally, it has become important to distinguish between internal and external components of the interest rate differentials. External components are usually approximated by compounding the effect of external interest rates with the actual or the expected rate of depreciation of the peso against the dollar. This kind of analysis has empirical support in the findings that internal interest rates are influenced by the nominal interest rate parity condition. In fact, Edwards (1984) concluded that the Colombian economy could be characterized as a "small and semiopen economy" during the 1970s and early 1980s due to such influence of the external return on the domestic interest rates. Clavijo (1986) and Herrera (1990), among others, corroborated such findings, in spite of the presence of a rigid system of exchange controls instituted in 1967. Additionally, Correa (1992) found, using an error correction model, that causality runs fundamentally from the external to the internal rate of return.

Since the liberalization of the Colombian economy, in early 1990, it has become more apparent the role of the external returns in determining the domestic interest rates. Law 9 of 1991 dismounted many of the exchange controls, including the obligation of surrendering to the Central Bank proceeds from all exports, and also abolished the imposition of strict limits for contracting foreign debt. These deregulations have been complemented by Resolutions 57/91, 21/93, 28/93 and 2/94 of the Central Bank by which the traditional crawling-peg system has been substituted by a semiflexible exchange system, including the adoption of wide bands of intervention.

In this paper we readdress the issue of decomposition of the real interest rate parity, in the spirit of the papers of Frankel and MacArthur (1988) and Branson (1988). The role of the integration of market of

REAL INTEREST RATE PARITY 119

goods and factors is highlighted by assessing the behavior of the real exchange rate behavior in determining the real interest rate differential between Colombia and the us A . 1

Such real differential has behaved differently from that of the nominal interest rates due to the fact that the PPP rule has not been maintained. In fact, the real exchange rate targeting made by the Central Bank has changed the rule in several occasions during the period 1976-1993, due to the correct perception that the PPP level has also changed dynami-;ally, as external debt and real growth of the economy have altered their path.2 While the uncovered interest rate differential was favorable to Colombia during the period 1977-1982, the commercial component (cor--esponding to the real exchange rate effect) was unfavorable to Colombia due to the sharp appreciation of the peso. Important capital outflows occurred during such period. In the period 1983-1987 the effects were eversed, as the real differential reached 10 percentage points in favor of ;apital flows towards Colombia. The period 1991-1993 was of great volatility in the components of the real interest rate differential, but by the ;nd of 1993 it had converged to nearly zero differential as the process of apertura" consolidated.

. Uncovered Interest Rate Differential between the Colombian Peso and the us Dollar

Tie simplest version of interest rate parity postulates that financial larkets wi l l equilibrate the return on domestic assets / with that of areign assets, which is usually measured by the compounding effect f the foreign interest rate i* and the actual or expected rate of epreciation + e or appreciation - e. This statement is known in the nancial literature as the "uncovered interest rate parity condition", jmrnarized in equation ( l ) . 3

1 This decomposition could be traced back to the synthesis made by Dornbusch 976) of the monetary approach to the balance of payments, based on the long-run PPP, id the assets approach, based on short-term capital flows.

2 See, for example, Echavarrfa and Gaviria (1992). 3 We shall make abstraction of the effects of residents vs. non-resident taxes.

Dwever, it should be said that in certain countries and at particular periods they are lite important in determining the direction of capital flows.

120 ESTUDIOS ECONÓMICOS

i-{?+e)~0 (1)

Graph 1 illustrates, first, the path of the domestic component i and, secondly, that of the external component ( f + e ) , where e corresponds to the actual rate of depreciation. (See appendix regarding data and sources) 4 Note that, during the period 1976-1982, the domestic component was, on average, about 5 percentage points above the external component. Graph 2 illustrates the nominal difference between the return on savings held in Colombian pesos and the return on savings in us-dollars, converted to pesos at the actual exchange rate. The positive interest difference observed in the period 1976-1982 is consistent with the decrease of about US$3.5 billion in the stock of financial assets held by the private Colombian sector in USA during such period (Rennhack and Mondino, 1989). Such amount of capital inflows represented about 1.8% of the GDP generated in that period.

In contrast, during the period 1983-1987, the acceleration of the crawling peg-rule, which determined the nominal rate of depreciation, turned the nominal differential negative for Colombian savings. In fact, such differential reached up to 20 percentage points by the end of 1985 (see graph 2). This reversion in the sign of the differential with respect to the previous period also coincides with a change in the direction of the capital flows. It has been documented that in the years 1983-1985 took place capital outflows estimated at us$4 billion (Rennhack and Mondino, 1989; Gomez, 1990).5 This amount of capital outflows represented about 3.6% of the GDP generated during the period 1983-1985.

With the exception of the end of 1987 and the beginning of 1988, such nominal differential was unfavorable to financial savings in Colombia, reaching extreme values of -10 percentage points by the end of 198 8

4 In computing the differentials, we have taken into account the compounding effect of i and e, which could represent up to 3 percentage points when, for example, the annual rate of depreciation was at 40% and the foreign interest rate was 8%, i.e. [(1.40* 1.08) - 1 ] - [0.40 + 0.08] = 0.032.

5 Based on data from the Bank of International Settlements, Gomez (1990) estimated capital outflows of nearly us$4.2 billion during the period 1981-88, representing about 1.3% of the G D P generated during those years. It is important to mention that such capital flows are not necessarily connected with those of drug traffiking, as documented by Correa (1984) and Urrutia (1990). However, deregulation of the rigid exchange controls, that prevailed up to 1991, could have altered this situation.

REAL INTEREST RATE PARITY 121

0.80-1 0.75-0.70-0.65-0.60-0.55-0.50-

a 0.45-u 0.40-

0.35-0.30-0.25-0.20-0.15-o.io -0.05" 0.00

76

Graph 1 yVo/wma/ I n t e r e s t Rates

( I n c l u d i n g N o m i n a l D e p r e c i a t i o n )

76 77 78 79 80 81 82 83 '84 85 86 ' 87 '88 '¿9 90'' 91 ' 92 ' 93 Colombia USA

Graph 2 N o m i n a l Difference ( C o l o m b i a vs. U S A )

0.201

-0.35 --0.40 ' ,, ,

76 77 78 79 80 81 82 83 84"85 '86' 87 ' '¿8' 89 'ÓÒ' '91' '92' ' Difference

122 ESTUDIOS ECONÓMICOS

and -8 percentage points at the beginning of 1990. This situation changed during 1990, as external interest rates fell and the domestic ones escalated. The behavior of the nominal differential could then help explaining the lingering of financial deepening indicators, such as M2/GDP or M 3 / G D P , during the second part of the 1980s (Clavijo, 1992b).

Beginning in 1991, the nominal differential reversed again, as domestic interest rates increased, reaching 39.4% per annum in the third quarter, the external interest rates fell to 5.6% and the rate of depreciation decelerated to 23.5% per annum (Banco de la Republica, 1991). The differential registered 9.7 percentage points in the third quarter of 1991 and climbed up to 19.5 percentage points by the end of 1992. During 1993, the uncovered interest rate differential was finally reduced to 5-10 percentage points, as domestic interest rates fell down to 26% per annum.

In short, it would be difficult to argue that, during the period 1976¬1993, there has been convergence of Colombian nominal interest rates and USA interest rates, adjusted by the actual rate of depreciation of the peso against the dollar, as postulated by equation (1). The internal-external difference was much higher than 5 percentage points during 1976¬1983 and turned negative and larger than -5 during 1984-1987. During 1991-1993, it has been again positive and higher than 5 percentage points. In spite of the rigid exchange controls dating from 1967, this wide fluctuations of the interest rate differential induced important capital flows. In fact, it has been documented that the premium of the black-market exchange rate is deeply associated with fundamental macro-variables, among others with the interest rate differential (Ocampo, 1985; Herrera, 1990). The capital flows have become more evident since the opening of the capital account began with the enactment of Law 9 of 1991 and its regulation through decrees 57/91, 21/93 y 28/93.

2. Real Interest Rate Differential: Financial and Commercial Components

Under a crawling-peg system, the real exchange rate is targeted by adjusting the nominal rate of depreciation e to close the gap between domestic inflation p and the external inflation p * . If the Central Bank succeeds in setting the rule e = p - p * , then equation (1) could also be interpreted as a rule of real interest rate parity, as shown in equation (2).

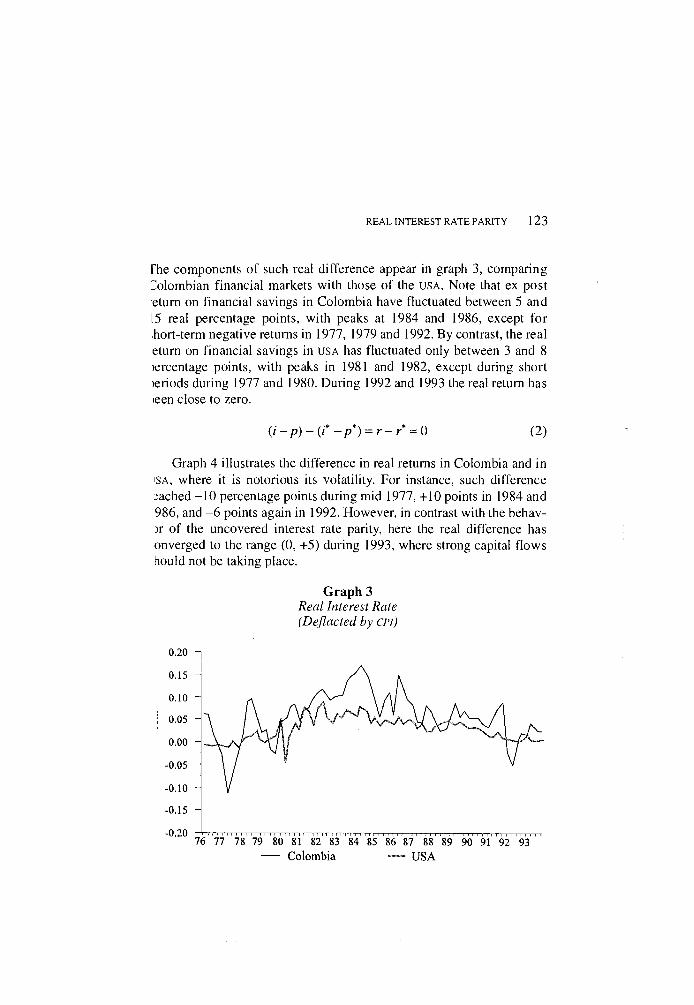

REAL INTEREST RATE PARITY 123

rhe components of such real difference appear in graph 3, comparing :olombian financial markets with those of the USA. Note that ex post •eturn on financial savings in Colombia have fluctuated between 5 and 15 real percentage points, with peaks at 1984 and 1986, except for :hort-term negative returns in 1977, 1979 and 1992. By contrast, the real eturn on financial savings in USA has fluctuated only between 3 and 8 >ercentage points, with peaks in 1981 and 1982, except during short >eriods during 1977 and 1980. During 1992 and 1993 the real return has ieen close to zero.

( i - p ) - { t - p * ) = r - r * ~ Q (2)

Graph 4 illustrates the difference in real returns in Colombia and in ISA, where it is notorious its volatility. For instance, such difference ;ached -10 percentage points during mid 1977, +10 points in 1984 and 986, and - 6 points again in 1992. However, in contrast with the behav->r of the uncovered interest rate parity, here the real difference has onverged to the range (0, +5) during 1993, where strong capital flows tiould not be taking place.

Graph 3 R e a l I n t e r e s t Rate ( D e f l a c t e d by CPl)

0.20 n

-0.15 -

76"77"78 79 '¿0' 8! 82 83 84 85 86 87 88 89 90 91 92 "93 ' ' Colombia — USA

124 ESTUDIOS ECONÓMICOS

The contrast between the uncovered interest rate differential, which do not exhibit convergence towards zero, and the real difference, which does converge to zero, is explained by the fact that the criteria e = p - p * did not hold for the Colombian peso during the period 1990¬93. Right at the outset of the liberalization program in 1990, the Colombian Central Bank accelerated e, which later spilled into higher inflation and led to an appreciation of the real exchange rate with respect to the 1990 level.

This conclusion could, nevertheless, be easily altered if such differentials are computed based on proxies for the expected rate of depreciation of the peso against the dollar, as we shall illustrate it later. For the moment, it is worth concentrating in the decomposition of this difference in real returns.

2 A . D e c o m p o s i t i o n of t h e R e a l I n t e r e s t Rate Differential

When taking into account the futures market of a given currency, it becomes possible to decompose the real difference of interest rates between its financial, commercial and currency risk factors, as shown in

REAL INTEREST RATE PARITY 125

equation (3), following Frankel and MacArthur (1988) and Branson ;i988). Such expression is just a reaccommodation of terms previously ihown in (2), only that we now have added the currency discount of the rational currency in the futures market /v is -á-v is the expected rate of iepreciation e.

Real Parity Bonds Goods Currency r - r* = (( - i * - f ) + ( e - p + p * ) + i f - e) (3)

This expression portraits the real interest rate difference as deter-nined by: 1) a difference of nominal interest rates covered by the utures currency market (i.e. the covered interest parity), which wi l l be ddressed as t h e bonds effect; 2) a difference in the prices of traded oods and services, which is determined by the real exchange rate, /hich is here referred to as t h e goods effect; and 3) a differential which ; associated to the local currency risk.

Given the fact that the Colombian peso is not traded in the money tarkets due to its condition of "weak" currency, we do not have data for te discount/shown in equation (3). Some newly industrialized coun-ies, such as Hong Kong, Malaysia, Singapur and Mexico, have devel-ped a market of futures for their currencies. This could help to a better inctioning of their financial markets. For instance, Mexico exhibited a avered interest rate differential of nearly -17 points, with respect to the uro-bond market, during 1982-1987. In spite of strict exchange con-ols, Mexico experienced massive capital outflows during the interna-anal debt crises (see Frankel and MacArthur, 1988).

Provided tha t /=0 for Colombia, equation (3) could be altered to ke the form shown in (4).6 This implies that the currency effect disap-;ars from the expression and that the bonds effect is really uncovered, s we shall see, in some cases e wil l take values referred to the actual te of depreciation (although in different markets) and in other cases it i l l refer to the expected rate of depreciation + e or appreciation - e >mputed both from a static and a dynamic point of view.

6 Note that unless we define different values for e in each component, the bond and : goods effects will mirror each other. This assumption will be altered later.

128 ESTUDIOS ECONÓMICOS

closing the RER gap. Note, in graph 6, the convergence of the lines showing the actual rate of depreciation and the expected rate required to attain the 1975 RER goal. During the period 1987-1989, the domestic rate of inflation was slightly reduced and the nominal rate of depreciation maintained in the 25-30% annual range. This caused the expected rate of depreciation to be reduced from 50% at the end of 1986 to only 12% at the of 1989.

Graph 6 N o m i n a l D e p r e c i a t i o n

( A n n u a l Rate) 0.80 -1 0.75 -

76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 Observed 1975 RER Goal — 1986 RER Goal

However, due to the high levels of external indebtedness and to the need of promoting nonprimary goods exports, the Central Bank continued to pursue an active RER targeting. We have estimated that, by the end of 1989, the nominal rate of depreciation of the peso surpassed in nearly 10 percentage points the rate required to maintain an static equilibrium of the RER . Although such policy did permit in the 1987-1989 period a real depreciation of nearly 12 points with respect to the 1975 RER level, its long-term effect on the inflation rate was costly and this strategy postponed badly needed structural changes leading to the opening of the economy.

A n alternative measurement of the expected rate of depreciation arises when one considers the need of implementing structural changes

REAL INTEREST RATE PARITY 129

and the sustainability of the RER , for example with respect to the 1975 level 7. The implicit (dynamic) equilibrium of the RER could then be :aken as the one that prevailed during 1986 and the expected rate of depreciation as the one required to close the gap between domestic and ;xternal CPI inflation from then onwards. Note, in graph 6, that the tctual rate of depreciation followed very closely this (dynamic) expec-ations, beginning in mid-1990 with the opening of the economy. The ictive real exchange rate targeting pursued a goal of maintaining 12 >ercentage points of real depreciation with respect to the RER of 1975.

It is important to detail two episodes of "misalignment" of the R E R vith respect to the 1986 level. The first one occurred in 1990, when a ominal depreciation of 32% per annum was adopted as a precautionary xchange policy to counterbalance the expected increase of imports due 3 the abolition of quantitative restrictions and the rapid reduction of nport tariffs. We have estimated, ex post, that the nominal rate of epreciation could have been about 10 percentage points lower, due to te fact that imports did not pick-up as expected and that the internatio-al reserves precautionary component was actually never needed. As a suit of the acceleration of the nominal rate of depreciation, Colombian iflation accelerated, reaching nearly 32% per annum in late 1990.

The second episode of "misalignment" took place in mid-1991, hen a de facto nominal appreciation of nearly 10% was adopted by eans of introducing a floor of 12.5% discount on the official exchange te set by the Central Bank. By the end of 1992, we have estimated that e nominal rate of depreciation required to maintain the RER of 1986 as around 10%, while the actual rate was running at 4.6% per annum, lis RER appreciation, with respect to the level of 1986, prevailed ring 1993 as the required nominal depreciation was around 19.5%, lile the actual rate was only 11%. Note, however, that such nominal preciation still granted 5 percentage points of depreciation with reset to the parity held in 1975 (the static equilibrium).

How are these results to be compared with the multilateral-RER mputed by the Colombian Central Bank, in which trade and currency

7 There exists at least another proxy for the expected rate of depreciation, indeed y popular among Colombian entrepreneurs, consisting in annualizing the monthly rate depreciation. Although it is often argued that this alternative has the advantage of ing "forward looking" elements in it, we consider that it lacks an economic anchor, as other alternatives do.

130 ESTUDIOS ECONÓMICOS

movements of about 18 countries are taken into account? By the end of 1993, the multilateral-RER index was in the range 102-104, where 1986= 100, irrespectively of using CPI'S, whole-sale prices or wages indices as deflators. This means that a 4% real depreciation was still held with respect to our "dynamic equilibrium" at the end of 1993, result which is basically explained by the real depreciation of the dollar with respect to other hard-currencies.

In fact, it has been estimated that the us-dollar was about 30% undervalued with respect to its equilibrium rate of the early 1970s against a basket of other hard-currencies, which obviously helped depreciate the peso with respect to other hard-currencies, as the Central Bank adopted a rule of pegging the peso to the us-dollar. In consequence, the multilateral-RER reveals a higher depreciation than the one computed only against the dollar. Additionally, this effect was reinforced by a trend of real appreciation of most Latin American currencies during the early 1990s (Calvo e t a l , 1993).

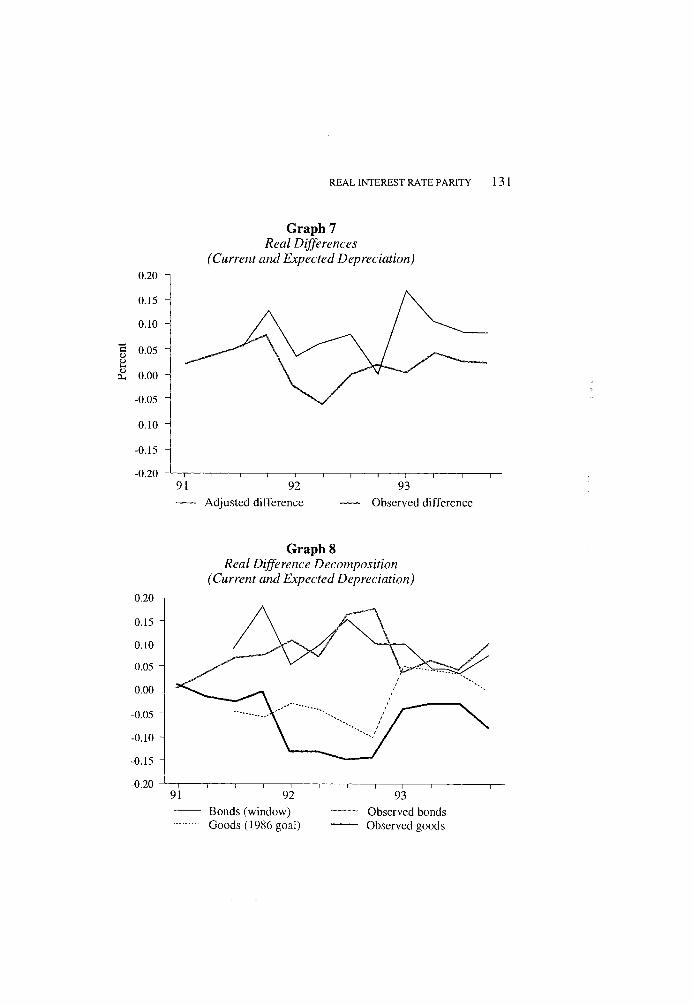

These alternatives of expected rates of depreciation generate different goods and bonds effects on the real interest rate differential. For instance, medium-term decisions could consider the expected rate of depreciation as the rate required to close the RER with respect to the 1986 level, while short-term decisions could consider the actual rate of depreciation observed in the exchange houses. The result of this hypothetical exercise is depicted in graph 7, where it can be observed that the real interest rate differential would have been 5 percentage points in favor of Colombia during 1992, but it would have reached 10 points during 1993. This outcome is quite different from the parity observed when the real interest rate differential was computed using the actual rate of nominal depreciation.

Graph 8 compares the real interest rate decomposition when actual and expected rates of depreciation are used. The higher real differential obtained when using expected rates of depreciation could be interpreted as a result of having a lower current account deficit and a more depreciated RER, given the assumption that private agents could have expected no gap against the RER level of 1986. During the first quarter of 1993, this effect would have been reinforced by a higher bond effect, that would have induced more capital inflows into Colombia. However, this effect would have ceased by the end of the year.

REAL INTEREST RATE PARITY 13 1

Graph 7 R e a l D i f f e r e n c e s

( C u r r e n t a n d E x p e c t e d D e p r e c i a t i o n )

0.20 -

0.15 -

0.10 -

| 0.05 -

£ o.oo -

-0.05 -

-0.10 -

-0.15 -

-0.20 - L - 1 1 1 1 1 1 1 1 1 1 , —

91 92 93

Adjusted difference Observed difference

Graph 8 R e a l Difference D e c o m p o s i t i o n

( C u r r e n t a n d E x p e c t e d D e p r e c i a t i o n )

0.20 -,

0.15 -

o.io -

0.05 -

0.00 -

-0.05 -

-0.10 -

-0.15 "

-0.20 i i i i i i i 1 1 1

91 92 93 Bonds (window) — _ Observed bonds Goods (1986 goal) Observed goods

132 ESTUDIOS ECONÓMICOS

3. Conclusions

We have concentrated our analysis in the concept of real interest rate differential and its decomposition between its bond effect (i.e. uncovered interest rate differential) and its goods effect (i.e. the RER effect). We have also focused on the role of exchange rate expectations by considering different alternatives of static and dynamic exchange rate equilibriums for the Colombian peso during the period 1976-1993.

Using simple computations of interest rate differentials between Colombia and USA , it has been shown that uncovered interest rate differentials are not a good approximation to the behavior of real interest rates differentials due to the fact that "purchasing power parity" has not been held in several years during such period, particularly in 1977¬1978, 1983-1987 and again in 1991-1993.

When the decomposition of such real differential was performed, it was found that the bonds effect (or the uncovered interest rate) was favorable to capital inflows into Colombia for up to 10 percentage points during the period 1977-1978, while the goods effect (or the RER) was appreciated in about 20 percentage points. The net result was a differential of about 10 points against the peso, hence inducing capital flows out of Colombia.

In the period 1983-1987 there was a reversal of effects as the goods effect turned positive by about 25 points (indicating a real depreciation of the peso against the dollar) and the bonds effect turned negative by about 20 points (showing unfavorable conditions for financial savings in Colombia). In consequence, the real interest rate differential was around 5 percentage points in favor of Colombia during this period.

More recently, during the period 1991-1993, such real differential fluctuated between -5 and +5, and experienced another reversion of effects. The RER has appreciated with respect to the 1990 level and the uncovered interest rate turned highly positive, attracting short-term capitals into Colombia. These effects have balanced each other and the ex post differential have converged to almost zero by the end of 1993.

Finally, we explained how the interpretation of the bonds and goods effect could be drastically altered by assuming different proxies for the expected rate of depreciation. For example, if exchange rate expectations corresponded to the rate that would have close the gap with respect to the 1986-RER level, private agents would have had incentives to arbitrage capital flows by moving into Colombian pesos.

REAL INTEREST RATE PARITY 133

I 1 S •<

g l i S 5 5

I S

N M N M (N fi M ri N fi M M N N N D tn m M «

C O ~

MMrNrmnc^r rif f)rnr rir fiTr\t^r'1'^fTr ,tir)

in oo ^ - - • ^ j - v i o o - ^ o o ' i o r - o o i n r ^ i r i O N

^ v o > n v i i n v d ^ ^ ' ^ ^ r ^ o o o s d « ( s W ^ N f S

-Nr, Tr-tNcnTr-iCNrn-i-H ci m rr -< rJ M

34 ESTUDIOS ECONÓMICOS

<o 3 c o

U

s s

3 í ^

a. <$,

>n r- m \o vi oo —< c-í -<t O — h ^ ^ i n v i ' o c y i i n ^ - < w-i

00 U-i fS O0 O) - - oí . , -. .. T ¡ v i - h r ¡ a i \ ¿ r ¡ ^f ' rS '^-ooc j s—'

— - h ITI in ir, i/i T I >n - í ^

OO U-) es oo o\ r - o o o o — n o N r ^ - ^ D O o o oo in a ^ \0 T ¡

C~- ^ ^ O ^ o o o < ^ o o o O f N O N O ^ r ^ i o - i r - - 0 iri »ri w-i "O S rS

00 VC — í t 0~i OO CJÍ Tt 'í ^ m

^O^oscov r jO'«OcnciO-ooo\ 'OniriCO —• < <N —• Tf ov

oo rji "n —I o< o OÑ

\o h m in - \o m m r i rn r i -

r i r n , t ' - - t N c n ' í - H ( N ( < i ' T t - - i c i m ' t cN en cN

REAL INTEREST RATE PARITY 135

_ „ i —, [s. X* n - ci \0 »o • o o \c m

c i m e-, m r i N N - -1 — — , _ _ H _

r- ~ m O N O o o m — « vo « D - o o o u - i ^ o c i u - i o v o o i n v , ^ i r i O r j ^

o o » . « o i o o t n o - n e » i - i o O N « M O o i » - - « - H i i < i - M N N r i c i r i m N N r i r i r i n N ri ^ ^ M r*ì r i <N <N <N n <N <N <N <N

C7\

ESTUDIOS ECONÓMICOS

§•8

£ es

•*i tu B- "o"

•Ü 3

O fe.

s ü 3

•a fe

5 £

3 «

.5 ¡ s Ta w £• ai r*

3 as =3-

"s ¿ a s

¡&1

T3 O

¡a fes

s

oo en en en oq ON ON

oq vi -o CS vi CS

OO (N « C< r> r f rf' -*t"

t~- oo m in en es es rn

i/-¡ iñ vi vi vi vi ví vi o en vd cScScscscSíSescsenenmen

r> q •« o) rn ^ . . . _ . ^ v ¡ v i v i v í v i v ) v i v ¡ v i v i v i v i v Í v i v i O e n es es es es es rs es es ^ ' ^ ' ' v * - - - - -

t~~ tr~ oc ir, Tt O oo vi vi en d d o i v i h d - - i N N K o N r - r ¡

O) q o> c o - r s ^ ' * ^ o m o N O s ^ t ' < t — • ' t i n d ^ r ^ - O M ¿ r n * ' q ™ q ^ O < r i l ¿ r ¡ cS O —'

q ^ - q ^ ^ q ^ ^ - ^ ^ ^ i r i T t q n o o . - o v a \ T iri co o r¡ -W' - co rn n rn r) - r¡ ri

inrnr-~ f;,oONr-íJvr>vi — r vio^oor-.O' vi ^ ^ M d r s a ^ d d h o o ' d - ^ r i ^ d o v \ o ^ '

^ ^ c s © e n ' © ^ r ^ « O ^ C \ v i c s r n ~ - 4 c s •f ' K oó

o o o d o o o t ^ d — — c ido VO — - H O —'

— ' M m - es en eSen'íf — esen -— esen-rj-

REAL INTEREST RATE PARITY 137

— - ü - m O o o u - 1 1 - v o o o c i t - . o o o v o o q o — o --o m — r^mooo^D'ncA^ ' • ' l ' i ' — . r ^ t N r - l ^ - 1 ' 1 ' 1 ' —

^ ^ o d o o ° o ' ° d r ~ ' * £ W ^ m m ' ^ ^ ^ ^ ^ ^ ^ . r < d d d d d d d c < W « r i -rf\ rr-i r<\ rr\ r n r*", r*l r*~i r*~i r*"i m f i r<ì r*"i r*~\ m r*"i rrì m ro rr-, rn m m r*-i r*i i-n r*-i rr~i r<i

f^l ITI 1/1 N oc « ö — d ö d

^ ^ o o v i v - , v i r ^ N D o o O N V i r ^ r n O O N O V i « . - r - —« N O 1

O O - I CO - ^ ^ r i C> N O NO v i ^ T i OO OO (v| (sj I ^ _ „ _ „ , - ( N N N (S -

O oq rri vi

mqDOTfMGc^^riOTi'jri-- OvDC Ov ONVirnor r rMvìfnoi'id-vi- N«-i/iri«^iritNONMTi^iCrlrfdw |/ÌMHh

d ON co r~~ d co T—« oo TJ- c*l c*l NO c i oo 3" t~~~ NO v f O oo «—« o — M M t—• v i o v i r** ^ ON

v i N O t ^ O < ^ « O O N - O O r n ^ v j N D v i r n O < v i ^

- d c o T t v i N o r ^ o o

ESTUDIOS ECONÓMICOS

T3

u 3 G

"•4—» C O

U

te Q

a 3 a » te

=3 S-?

w -a °-3 S » f u i

^ - IJ

*¡ B- o 1

° fe-oí §•

-2 S?

G

£ E

"8 g

Q

s ¡S. 3 s te «

« J "1

T3 O U

CN| -« oq ON NO — ; m ^ rn -<t Tt vd m m en en m m

O O ^ O - | C N M N O C O • v, v . v , ~ O al ON O r>i r i r i M iri ^' O co r i r i

O 0 \ i ; oo c ) i r i oo q N

v i r v i r n N d r ^ d v d d o d r ^

"ÑT u~Í C N en N ¿ O Ñ Tt TÍ-' O

^ • N o o N o o ^ ^ r i f i f i o o i o O N c o ' i n a i n d d ' n r n K

© N O e n t S ^ c o e n N D e n r ^ o o — i n r ^ T t O o o N O e n ^ i " NO oo vi r~~ oo ND ND j" o o" es oí "í" en oi oí r~~

^ O N o o o o ^ » n r ^ ^ N o c N i a N N O r > r - - N D O o > o r - - o ^ n m m v n T t ' r n n d ^ N D V d t ^ N O o O T f N D ^ d

- f ó r ¡ r s N - ^ ^ n u i r ^ c n N o d ^ d r n c s «

m T Í oo a t ^ N O q >Ti O r i h m r i rs q oo N >o ' t v r i o d i r i N O v - i i n u i - ^ f n ^ r ^ c o r N i n d

r ^ - H i n r N l N O N q T í ; ^ ^ o o o o - e r i n r > T t m N o d d d d - ^ d d d

- ^ ( N m ^ f — • eN en —i M c^i - n n - N m

oí

REAL INTEREST RATE PARITY 139

References

Banco de la República (1991). "Notas editoriales", Revista del Banco de l a República, December.

Branson, W. H. (1988). "Comments to 'Political vs. Currency Premia in International Real Interest Differentials' by Frankel and MacArthur", E u r o p e a n Economic Review, no. 32.

Calvo, G., C. Reinhart, and C. Vegh (1993). "Targeting the Real Exchange Rate: Theory and Evidence", IMF, working paper, May.

Clavijo, S. (1986). "International Reserves and Foreign Exchange Black-Market Under 'Crawling-Peg': Theoretical and Empirical Issues", N a t i o n a l B u r e a u of Economic Research, W o r k i n g Paper N o . 8, Special-Series, Department of Economics, University of Illinois at Urbana-Champaign.

(1992a). "Overcoming Financial Crisis During Transition from a Repressed to a Market-Based System: Colombia 1970-89", in A. Cohen and F. R. Gunter (eds.), T h e Colombian Economy: Issues of T r a d e and Development, Westview Press.

(1992b). "Footprints of Financial Repression and Strategies for Liberalization: Colombia 1970-1990", Money Affairs, CEMLA, July-December.

(1992c). "Permanent and Transitory Components of Colombia's Real GDP: The 'Over-Consumption' Hypothesis Revisited", J o u r n a l of Development Economics, vol.38.

Zorrea, P. (1984). "Determinantes de la cuenta de servicios de la balanza cambiaría (colombiana)", Ensayos sobre Política Económica, 6.

(1992). "Paridad en las tasas de interés real interna y externa", C o y u n t u r a Económica, Fedesarrollo, April.

:uddington, J. T., and C. M. Urzúa (1989). "Trends and Cycles in Colombia's Real GDP and Fiscal Deficit", J o u r n a l of Development Economics, vol. 30, no. 2.

)ornbusch, R. (1976). "Expectations and Exchange Rate Dynamics", J o u r n a l of P o l i t i c a l Economy, December.

ichavarria, J.J., and A. Gaviria. (1992). "Los determinantes de la tasa de cambio y la coyuntura actual", C o y u n t u r a Económica, Fedesarrollo, December.

idwards, S. (1984). "Coffee, Money and Inflation in Colombia", W o r l d Development, vol. 12, no. 11 and 12.

rankel, J. A., and A. T. MacArthur (1988). "Political vs. Currency Premia in International Real Interest Differentials", E u r o p e a n Economic Review, no. 32.

lómez, H. J. (1990). "El tamaño del narcotráfico y su impacto económico", Economía C o l o m b i a n a , February-March,

terrera, S. (1990). "Eficiencia y determinantes del funcionamiento del mercado paralelo de divisas en Colombia", Ensayos sobre Política Económica, June,

ommes, R. (1993). "En la senda del crecimiento acelerado", C a r t a F i n a n c i e r a , December.

140 ESTUDIOS ECONÓMICOS

Langebaek, A. (1992). "Colombia y los flujos de capital privado en América Latina", Archivos de Macroeconomía, DNP, February.

Montenegro, A. (1994). "Una nota sobre entradas de capital", DNP, January. Ocampo, J. A. (1985). "El impacto macroeconómico del control de impor

taciones", Ensayos sobre Política Económica, December. Olivera, M. (1993). "El costo del flujo de capital: una nueva estimación",

Archivos de Macroeconomía, DNP, March. Rennhack, R., and G. Mondino (1989). "Movilidad de capitales y política

monetaria en Colombia", Ensayos sobre Política Económica, June. Steiner, R., et al. (1993). "Flujos de capitales y expectativas de devaluación", in

M. Cárdenas and L. J. Garay (eds.), Macroeconomía de los flujos de capital, Tercer Mundo.

Urrutia, M. (1990). "Análisis costo-beneficio del tráfico de drogas para la economía colombiana", C o y u n t u r a Económica, October.

, and A. Pontón (1993). "Entrada de capitales, diferenciales de intereses y narcotráfico en Colombia", in M. Cárdenas y L. J. Garay (eds.), M a c r o economía de los flujos de capital, Tercer Mundo.