Real Estate Lori Chapman Principals of. Virginia Real Estate Who must have a license: Any person who...

235

Real Estate Lori Chapman Principa ls of

-

Upload

clarence-fossett -

Category

Documents

-

view

214 -

download

0

Transcript of Real Estate Lori Chapman Principals of. Virginia Real Estate Who must have a license: Any person who...

Real EstateLori

Chapman

Principals of

Virginia Real Estate

• Who must have a license: Any person who or business entity that performs or advertises brokerage services must be licensed by the REB (Real Estate Board)

• Real Estate Broker &

• Real Estate Salesperson

Virginia Real Estate

• Real Estate Broker- …any person or business entity, including, but not limited to, a partnership, association, corporation, or limited liability corporation, who for compensation or valuable consideration(i) sells or offers for sale, buys or offers to buy, or negotiates the purchase or sale or exchange of real estate, including units or interest in condominiums, cooperative interest… for time shares in a time-share program…or(ii) who leases or offers for lease, or rents or offers for rent any real estate or

the improvements thereon for others.

Virginia Real Estate

• Real Estate Salesperson- ..any person, or business entity of not more than two persons unless related by blood, or marriage, who for compensation or valuable consideration is employed either directly or indirectly by, or affiliated as an independent contractor with, a real estate broker, to sell, or offer for sell, to buy or offer to buy, or to negotiate the purchase, sale, or exchange of real estate, or to lease, rent or offer for rent, any real estate, or to negotiate leases thereof, or of the improvements thereon.

Virginia Real Estate

• Firm- sole proprietorship (nonbroker owned) that is not owned by a principal broker.

• Principal Broker- individual broker designated to assure firm compliance & communication with the Real Estate Board

• Supervising Broker- or a managing broker that supervise the office activities

• Associate Broker- one that practices as a salesperson but holds a brokers license

• Sole Proprietor- an individual who owns a real estate firm, if licensed then acts as principal broker if not then must designate a licensed broker to be principal broker.

• Licensee- any person…. That holds a license issued

by the REB to act a broker or salesperson • Standard Agent- a broker or salesperson that acts or

represents a client.

• Independent Contractor- broker/salesperson that acts for or represents a client with a written contract- not to be confused w/tax purposes.

Introduction toReal Estate

CHAPTER 1

• Real Estate Specialization

• Professional Organizations

• Types of Real Estate

• The Real Estate Market

Real Estate Specialization

• Brokerage-bringing people together

• Appraisal- estimating the value of real property

• Property Management- managing & protecting an owner’s investment/return

• Financing- arranging/providing funds to purchaser real property

• Subdivision & Development- splitting a larger parcel into smaller pieces & improving

• Counseling- competent,independent information & advice

• Education- opportunities to practitioners & consumers

• Others- practice of law, corporations,government agencies

Professional Organizations

• NAR-National Association of REALTORS• NAREB-National Association of Real

Estate Brokers• AIREA-American Institute of Real Estate

Appraisers• ASA-American Society of Appraisers• NAIFEA-National Association of

Independent Fee Appraisers• REEA-Real Estate Educators Association• REBAC-Real Estate Buyer’s Agent

Council• NAEBA-National Association of Exclusive

Buyer’s Agents• BOMA-Building Owners & Managers• IREM-Institute of Real Estate Management• CIREI-Commercial Investment Real Estate

Institute• ASREC-American Society of Real Estate

Counselors

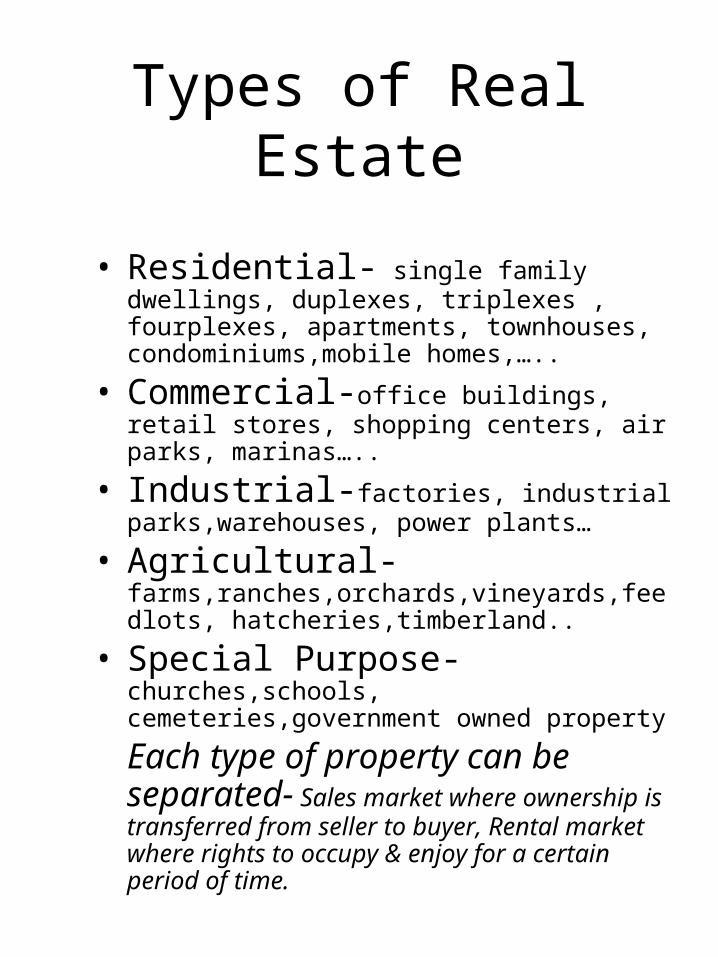

Types of Real Estate

• Residential- single family dwellings, duplexes, triplexes , fourplexes, apartments, townhouses, condominiums,mobile homes,…..

• Commercial-office buildings, retail stores, shopping centers, air parks, marinas…..

• Industrial-factories, industrial parks,warehouses, power plants…

• Agricultural-farms,ranches,orchards,vineyards,feedlots, hatcheries,timberland..

• Special Purpose- churches,schools, cemeteries,government owned property

Each type of property can be separated- Sales market where ownership is transferred from seller to buyer, Rental market where rights to occupy & enjoy for a certain period of time.

The Real Estate Market

• Market Place- where goods are bought & sold

• Supply & Demand are economic forces that set prices

1. Characteristics of real estate effecting supply & demand:

a. Uniqueness

b. Immobility

c. Effect of natural disasters/changes in markets

2. Prices drop with increased supply

3. Prices raise with decreased supply

Factors affectingSupply / Demand

• Supply1. Labor force

2.Construction cost

3. Government controls at all levels

4. Government fiscal & monetary policies

• Demand1. Population

2. Demographics- make up of population

3. Employment & wages- where & how money is spent/ perceived job security

Real Property LawCHAPTER 2

• Land- to the earth’s center & upward to infinity (including trees & water)

• Real Estate-the land & all things permanently attached by nature & man (improvements)

• Real Property- the real estate plus interest, benefits & rights inherent in the ownership of real estate

• Surface rights- may be sold/ leased to others

• Subsurface rights- substances in the ground/may be sold or leased

• Air rights-may be sold or leased. Solar &/or sunlight have become issues in recent years.

• Personal property- All property that does not fit the definition real property .

– An item of real property may be changed to personal property through severance AND an item or personal property may become real property by annexation

Ownership of Real Property/Bundle of legal

rights

• The concept comes from old English law

• The Bundle of legal rights include the rights of:– Possession- the right to occupy– Control-the right to determine certain

interest for others– Enjoyment- possession without

harassment– Exclusion- legally refusing to create

interest for others/keep others from entering

– Disposition-determining how the property is disposed of

• Title to real property- right to ownership – Deed – the actual paper that

shows ownership- where title is passed

• Personal Property / ChattelsAll property that is not and/or do not fit the

description of real property

Classification of Fixtures

Fixtures

&

Trade Fixtures

Fixtures

An article that was once personal property but has been affixed to land or building so long that the law recognizes it as part of the real estate

• Legal test: – The intention of the annexure– The method of the annexation– The adaptation to real estate– The existence of an agreement

Trade fixture

An article owned by a tenant & attached to rental space or a building for operating a business

– Tenant’s personal property– Must remove on or before the last end

of lease– Not removed becomes the owners real

property

Importance in a real estate transaction- to avoid confusion items that are to be included or excluded should be clarified in the listing agreement and/or the sales agreement

Characteristics of Real Estate that affect its

Nature & Use• Economic characteristics

SIPA

SCARCITY –Land of a particular quality or location may be limited

IMPROVEMENTS-They can affect the improved or surrounding parcels either favorably or unfavorably

PERMANENCE OF INVESTMENT- improvements are considered to create fixed investments

AREA PREFERENCE-or situs-peoples choice of area- the most important economic characteristic

Physical Characteristics Immobile Indestructible Unique

Immobile – the geographic location of land

Indestructible – land is durable & indestructible

Unique – nonhomogeneity or heterogeneity – no two piece of land are alike

IIU

Laws Affecting Real Estate

Specific areas of law important to Real Estate Practitioners

• Law of Contracts• General Property Law• Law of Agency• State Real Estate License Law• Federal Regulations• Zoning & Land Use Laws• Environmental regulations• Federal, state & local tax laws

Real Estate license law• To protect the public interest by promoting confidence• All 50 states, D.C. & Canadian provinces require

licensing• State laws are similar but differ in details• Specific education & personal requirements for

licensure• Exam required• Certain standards of ethical & personal conduct

required• Some state require continuing education for renewal

Real Estate Practitioners may not act as attorneys

• Reason– Sign of financial stability– Investment- appreciation/depreciation: income

tax deduction/exclusion of gain from tax– Intangible benefits

• Ownership- single, married with children, “empty nesters”…..

• Types of housing-Single family, Apartments, Condominiums,Cooperatives,Planned urban development (PUD), Converted use, retirement communities, High rise developments, Mobile homes, Modular homes, Time-shares

Home OwnershipCHAPTER 3

Housing Affordability

• Mortgage terms, including types of loans, availability, interest rates and monthly payments– Ownership expenses: insurance,real estate

taxes, utilities & maintenance

– Ability to meet mortgage payment/ Most important economic consideration

– PITI/PMI

Qualifying for a loan: 28/36

Gross income $54,000 : 12 = $4,500

x 28%

$1,260

$1,260 + Total monthly debt $650 =$1,910

needs to be <36%

$4,500 x 36%= $1,620

in this case the persons debt is too high, needs to be $360 or less

Investment considerations

– Tax benefits: Income deductions, Mortgage interest, Real estate taxes,certain loan origination/discount fees, loan prepayment penalties

– Capital gain: Lifetime exclusion of $250,000/ $500,000 married couples/must have lived there for 2 years, keep good records

– In Practice- Real estate practitioners should tell their clients to consult a tax professional

Homeowner’s insurance

• Basic policy: fire, lighting, vandalism, theft, lose…

• Broad-form: falling objects (weight of ice/snow), collapse, water/steam-plumbing….

• Comprehensive: further available coverage• Condo/apartment: unit & contents not the

structure• Most policies have a coinsurance clause

80% of replacement• Loss settlement of actual cash value

(replacement less depreciation) or prorated by dividing the % of replacement cost actually covered by policy

Federal Flood Insurance Program• Administered by the Emergency Management

Agency (FEMA)• Program subsidized flood damage insurance• Required on all properties located in flood

prone areas (flood plains) that have federally related financing

• Maps of flood probe areas prepared by the Army Corps of Engineers

Prior to entering into a brokerage relationship the licensee must advise a person of the following:

-Types of available Brokerage relationships-Brokers compensation

-Whether the commission will be shared with another broker

Buyer BrokerReal Estate agent represents

the interest of the buyer

Designated AgentReal estate agents of the same

company represent the buyer/seller or tenant/landlord ,

Broker remains Dual agent

Dual AgentReal estate agent represents

the interest of both, buyer/seller or tenant/landlord

Sub-AgentReal Estate agent that is not a buyer broker or listing agent, is working with the buyer/tenant but has no writing agreement but is an agent of the seller.

Non-AgentReal Estate agent that

represents neither buyer/seller or tenant/landlord, but is

facilitator in the real estate transaction

Virginia Real EstateCHAPTER 1

VIRGINIA IS A STATUTORY STATE

• Common Source Information Company- person or entity that gathers or distributes real estate information, MLS or REALTOR.com, etc…

• In Virginia , compensation nor use of an information center creates a brokerage relationship

Virginia Real EstateCHAPTER 1

• Agency- any relationship when a real estate licensee acts for or represents a person by that person’s express authority

in a real estate transaction. This can be changed by entering into a written agreement that alters the relationship, specifies the duties.

• Brokerage relationship- contractual relationship between broker and client.

• Client- a person that has entered into a brokerage agreement.

• Customer- anyone else involved in the buying/selling/renting/exchanging… of real estate.

END OF CLASS

See you

Chapter 4 of the yellow book

&

Chapter 1 of the maroon book

Goodnight

Designated

Client Client

Agent Agent

Broker

Law of Agency

• Common Law

-Rules of society

• Statutory Law - Enacted by legislatures &

other governing bodies

AgencyCHAPTER 4

• Agent-the individual who is authorized & consents to represent the interest of another, in real estate the firm is the agent

• Subagent-the agent of the agent

• Principal-the individual who hires & delegates to the agent the responsibility representing his/her interest

• Agency- the fiduciary relationship between the principal & the agent

• Fiduciary- the agent is held in a position of special trust & confidence by the principal

• Client-the principal

• Customer-the third party, some sort of service is provided

• Non-agent-facilitator, transaction broker…..

• Consensual agreement-

Fiduciary dutiesCOALD

A fiduciary relationship is one of trust & confidence between employer

(principal) and employee (agent)Difference between client & customer

• Common law of agency duties:– Care- by use of skill– Obedience- obeying the principal’s

instructions– Accounting- financial (deposits), files

(3yrs), conversion/commingling/illegal– Loyalty- interest above all/

Confidentiality– Disclosure- offers,interest of parties,

value, pricing

Creation of Agency

• The principal delegates & the agent consents to act

• Express agency- Listing Agreement– The parties state the terms of the

agreement & express their intentions either orally or in writingIn real estate normally in written rather than orally: listing agreement or buyer-agency

• Implied Agency-Buyer Agency Agreement– By actions– Unintentionally, inadvertently or

accidentally could create an undisclosed dual agency

• Compensation– Does not determine agency– Keep in mind that although a person

pays the compensation to an agent does not mean that person is the principal

Termination of Agency

• Death or incapacity• Destruction or condemnation of the

property• Expiration of terms of the agreement• Mutual agreement• Breach by either party• By operation of law- (bankruptcy)• Completion or fulfillment• Exception: agency coupled with

interest-the agent has an interest in the subject of the agency (such as the property being sold)– Cannot be revoked by the principal– Does not automatically terminate at the

principal’s death

Types of Agency Relationships

Limitations on an Agent’s authority• Universal agent-no limits on

authority/power of attorney/attorney in fact

• General agent-one that represents the principal in a range of matters

– Receives power to enter into contracts on behalf of the principal within the scope of authority(property manager)

• Special agent-Limited agent-special power of attorney- one who represents the principal in one specific transaction under detailed instruction: Agent cannot bind principal– Created by the terms of the listing

agreement/buyer-agency

• Designated agent- one who is authorized by the broker to act as the agent of a specific principal

– Others in the office free to act for another party– Broker may be in position of dual agency, disclosure

required– Varies from state to state

Single agency… continued

• Single agency-the broker represents one party, either the seller or the buyer, a third party is a customer

• Seller as principal-• The broker becomes the agent of the

seller• The relationship is established by a

listing agreement• The buyer is the customer• The broker may utilize other brokers

who become subagents• Sub agency- the broker appoints other

cooperating brokers who have fiduciary responsibilities as the listing broker

• Offered through MLS• Created by offer of cooperation and/or

compensation• Other brokers may accept or reject

subagency offer

– Buyer as principal• The broker becomes the agent of the

seller• The relationship is established by a

buyer-agency contract• Broker is responsible to the buyer to

locate real estate

– Owner as principal• The broker is responsible to the owner

to manage or lease the owner’s real estate

• The relationship is established by a property management agreement or listing contract

Dual Agency

The broker represents two principals in the same transaction

• Disclosed dual agency-both principal must be informed and consent to dual representation.

• Undisclosed dual agency- the action of the parties can create an agency relationship where none was intended

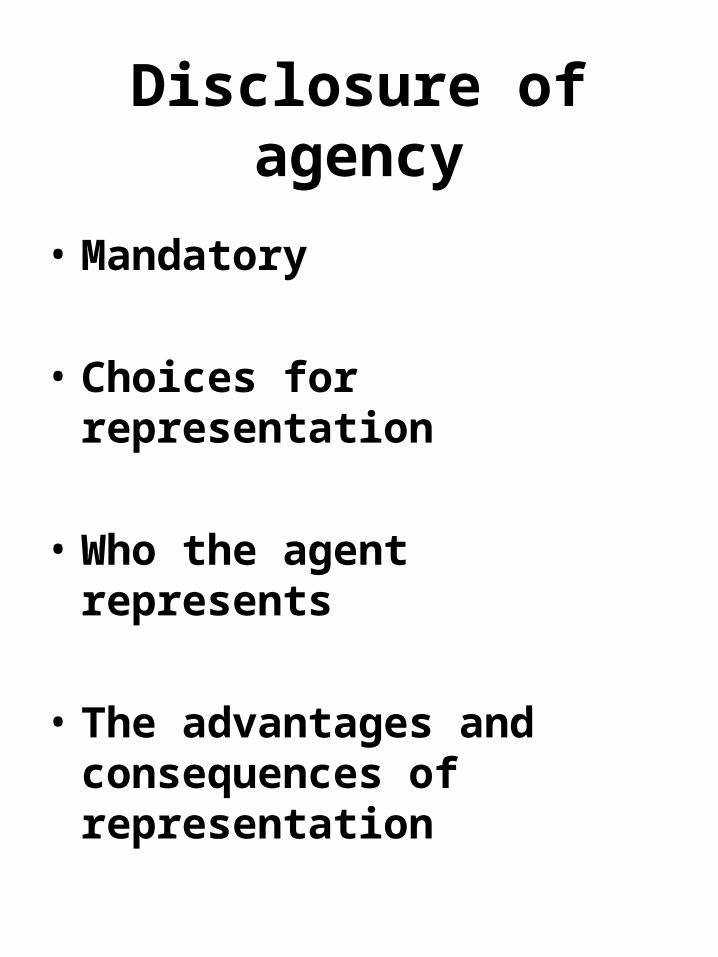

Disclosure of agency

• Mandatory

• Choices for representation

• Who the agent represents

• The advantages and consequences of representation

Agency Statue

• Exercise reasonable care & skill in performing duties

• Obey client’s specific instructions

• Account for all money & property received

• Disclose material facts

• Perform according to brokerage agreement terms

• Keep confidential all confidential information received from client

• Generally comply with terms of statue

Customer- Level of Services

• Duties to the customer– Reasonable care & skill– Honest & fair– Disclosure of all facts known to agent that

materially affect the property• Disclosure of environmental hazards

– Lead paint, asbestos, toxic waste, contaminated soil/water,etc…

• Opinion versus fact– Opinions must be stated as agent’s opinion – Facts must be accurate

• Fraud- intentional misrepresentation• Puffing- exaggeration, it’s legal provided the

statement is not considered fraudulent• Negligent misrepresentation- if the broker is

ignorant of a fact but should have known• Latent defects

– A hidden structural defect that wouldn’t be found under ordinary inspection

• Stigmatized properties

– Virginia prohibits disclosure of HIV-positive, AIDS

Virginia Real EstateCH 1

Since 1995VIRGINIA IS A STATUTORY STATE

• Prior to entering into a brokerage relationship the licensee must advise a person of the following:-Types of available Brokerage relationships-Brokers compensation-Whether the commission will be shared with another broker

• Common Source Information Company- person or entity that gathers or distributes real estate information, MLS or REALTOR.com, etc…

• In Virginia , compensation nor use of an information center creates a brokerage relationship

Virginia Real Estate

• Agency – any relationship in which an agent acts or represents a person’s express authority in a real estate transaction. The parties can enter into another type of relationship with a written agreement (independent contractor)

• Brokerage relationship- contractual relationship between client and broker

• Designated agent• Dual agent• Client- contractual agreement• Customer- non contractual agreement

Virginia Real EstateDuties

• To Client– Perform to the terms of the contract– Promote the interest by 1. seeking

sale/lease for the terms of the contract 2. Present all offers 3. Disclose all material facts 4. Accountability

– CONFIDENTIALITY- FOREVER– Ordinary care– Comply with all laws & regulations

• To Customer– Must treat honestly– Can’t knowingly give false information– Must disclose all material adverse facts of

the property

Virginia Real Estate

• Additional Disclosure:– Buyer Broker- whether buyer will

occupy the property as main residence

– Property Management- same as a client duties other than agent is a general agent to the owner

Oral agreements are legal in Virginia but they are not enforceable

Virginia Real EstateChapter 1

• Brokerage Relationship– Establishing:

• Type of brokerage relationship/buyer broker,dual, -designated, non –agent

• Broker’s compensation• Whether broker will share commission

with another broker

- Termination:- expiration date (90 day default)

- mutual agreement to terminate- default by either party - Agents withdrawal when client

refuses to consent to disclose dual agency

• CONFIDENTIALITY- FOREVER

Virginia Real Estate Chapter 1

Disclosure requirements• Agency law requires full disclosure of any

existing brokerage relationship

• First substantive discussion about specific property

• Only the person who is not the client has to sign “The Disclosure of Brokerage Relationship” form

• Dual Representation must be made to all parties

• Imputed Knowledge- client nor broker is liable for misrepresentations of the other, provided they didn’t know or shouldn't have known of the information

Monday

March 22, 2004

Chapter #5

Chapter 1,2,3,4

Math THE DRESS

What is the % of profit

$80

$100

: :

X

: :X

BUY A DRESS

FOR $80

SELL IT FOR $100

25%

Profit

% of Cost

Profit$10025 %

$80

Math

: :

X

PART

(Equivalent to Rate)

RATE (% of Whole)

WHOLE (100 %)

MathCommission

Net price

: .94 (6% comm)

List Price

$200,000

.94

6% comm.

$212,765

: :

X

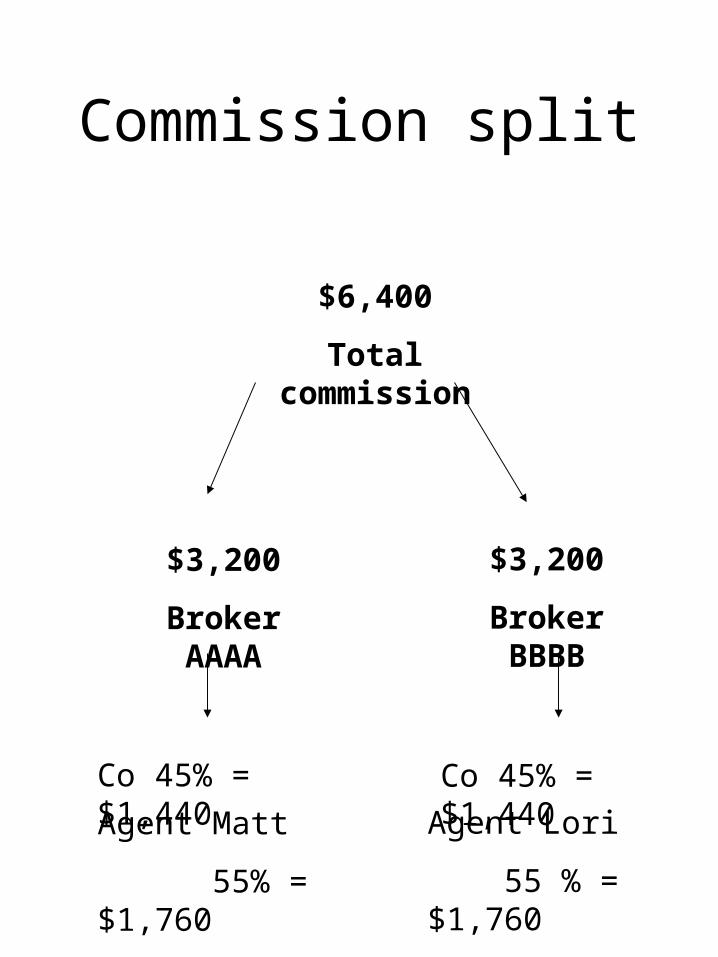

Commission split

$6,400

Total commission

$3,200

Broker AAAA

$3,200

Broker BBBB

Co 45% = $1,440

Agent Matt

55% = $1,760

Co 45% = $1,440

Agent Lori

55 % = $1,760

Math28/36

GROSS YEARLY INCOME

:

12 = MONTHLY INCOME

MONTHLY INCOME

X 28% = PITI/PMI

MONTHLY DEBT + PITI/PMI < 36%

Real Estate Brokerage Chapter 5/63

History of Brokerage1. Formerly, one-office, family –

run operation

2. Common law dictates caveat emptor was the rule

3. MLS became the widely used industry service

4. Buyers began to question & demand representation

Real Estate Brokerage Chapter 5

Purpose:

• Establish basic & continuing education requirements

• Define actives requiring licensing

• Describing acceptable standards of conduct & practice

• Enforce standards through disciplinary system……..

License Laws

Real Estate Brokerage Chapter 5/64

• Each state has a licensing authority/commission/board with the power to :– Issue license– Make real estate information

available to licensee & public– Enforce the statutory real estate

law

AND adopt a set of rules & regulations that have the same force & effect as any law

License Laws

Real Estate Brokerage Chapter 5/65-70

• Brokerage- Bringing people together in a real estate transaction– Broker- One who is licensed to sell,

buy, exchange or lease real property for others & charge a fee for service

• Business form– Sole proprietorship– Corporation– Partnership– Independent– Franchise………………….

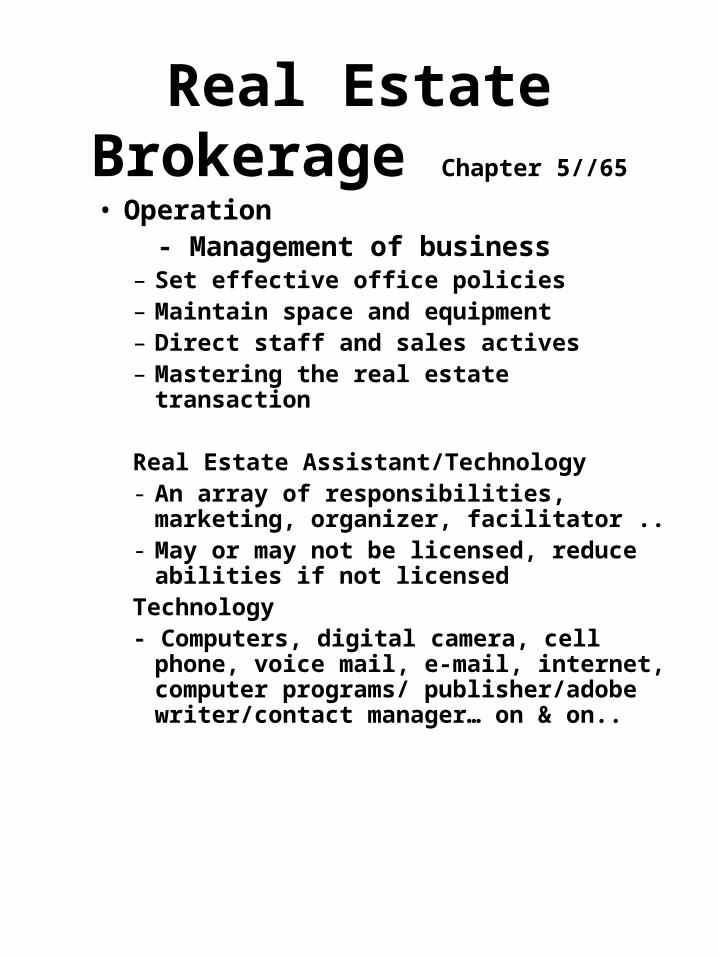

Real Estate Brokerage Chapter 5//65

• Operation - Management of business– Set effective office policies– Maintain space and equipment– Direct staff and sales actives – Mastering the real estate transaction

Real Estate Assistant/Technology- An array of responsibilities, marketing,

organizer, facilitator ..- May or may not be licensed, reduce

abilities if not licensedTechnology- Computers, digital camera, cell phone,

voice mail, e-mail, internet, computer programs/ publisher/adobe writer/contact manager… on & on..

Real Estate Brokerage Chapter 5/67

• Broker-Salesperson relationship– The employing Broker is directly

responsible for supervising all salesperson’s real estate activities

– The salesperson is responsible only to his/her employing broker. All activities must be performed in the name of the employing broker

– Salesperson cannot receive compensation from anyone other than own broker

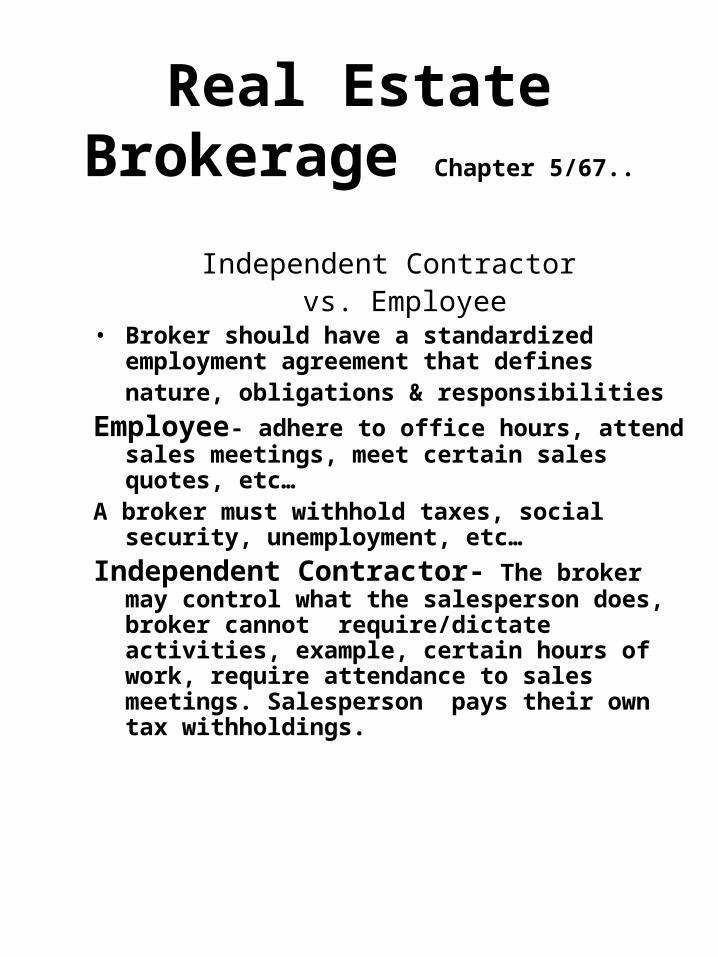

Real Estate Brokerage Chapter 5/67..

Independent Contractor vs. Employee

• Broker should have a standardized employment agreement that definesnature, obligations & responsibilities

Employee- adhere to office hours, attend sales meetings, meet certain sales quotes, etc…

A broker must withhold taxes, social security, unemployment, etc…

Independent Contractor- The broker may control what the salesperson does, broker cannot require/dictate activities, example, certain hours of work, require attendance to sales meetings. Salesperson pays their own tax withholdings.

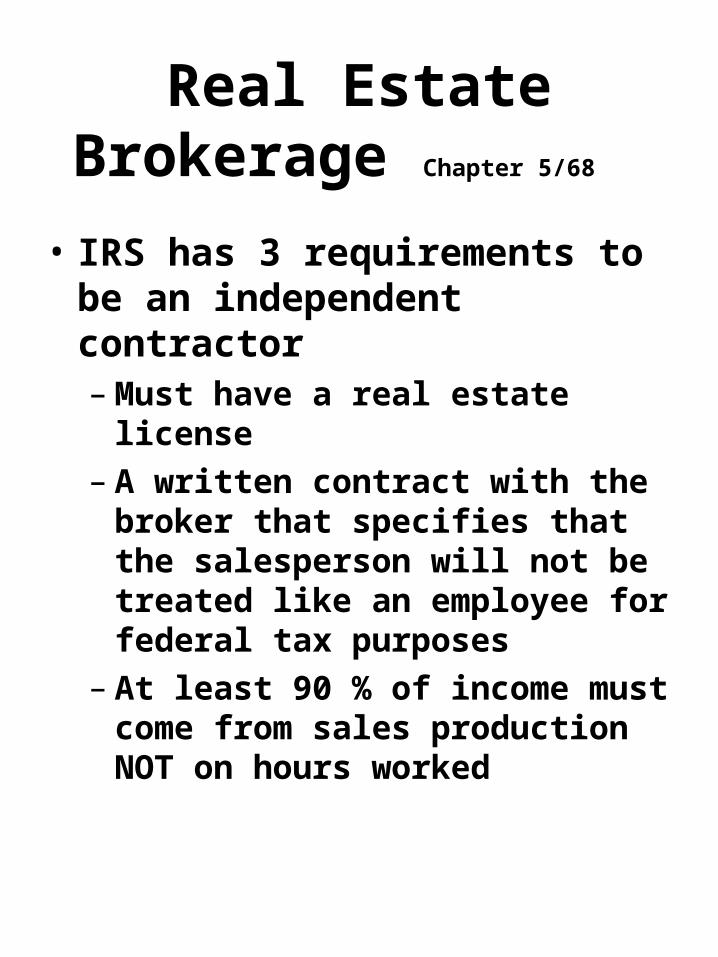

Real Estate Brokerage Chapter 5/68

• IRS has 3 requirements to be an independent contractor– Must have a real estate license– A written contract with the

broker that specifies that the salesperson will not be treated like an employee for federal tax purposes

– At least 90 % of income must come from sales production NOT on hours worked

Real Estate Brokerage Chapter 5/68

• Broker’s compensation– Must be negotiated between the

principal and the broker– Usually a % of the sales price/rent

or could be a fixed dollar amount– Broker is entitled to compensation

when:• The sales contract has been ,

executed(signed) by a ready, able and willing buyer

• The contract has been accepted and executed (signed) by the seller

• Copies of the contract are in the hands of all parties

If the seller defaults the broker is entitled to a commission

Real Estate Brokerage Chapter 5/69

• To be entitled to a commission an individual must be:– A licensed broker– Procuring cause of the sale – Employed by the buyer or seller

under a valid contract

Procuring cause- started an unbroken chain of events

Ready, Able & Willing Buyer:To buy on the seller’s terms & ready

to complete the transaction

Real Estate Brokerage Chapter 5/69-70

• Salesperson’s compensation– Must be contained in an

agreement between broker & salesperson

– May be a fixed salary, % of commission, draw from or graduated spilt

– 100 % program w/monthly fees

Math examples

Real Estate Brokerage Chapter 5

• Transactional brokerage: not an agent to either buyer or seller– Referred as Non-Agent,

facilitator, coordinator,or contract broker

Real Estate Brokerage Antitrust

Chapter 5/71-73

Brokers/salespeople are PROHIBLTED to:

• Price fixing- setting prices

• Group Boycotting-conspire against another business or withhold patronage

• Allocations of customers- divide the market place

• Tie-in agreements – tie first sale to the purchase of another

Penalties: -Maximum $100,000 3 years in prison-Corporation: Up to $1,000,000-Civil Suit: Suffered party may collect triple the actual damages & attorney fees

Real Estate Brokerage Chapter 5/73

Fee-for-Service

Various duties, bundle of services, on stop shopping, etc…

Math THE DRESS

What is the % of profit

$20

$80

: :

X

: :X

BUY A DRESS

FOR $80

SELL IT FOR $100

25%

Profit

% of Cost

Profit$8025 %

$20

PART is a portion of the WHOLE - Your office spaceWHOLE – BuildingRATE -- % of your office space to the building

: :

X

PART(Equivalent to Rate)

RATE (% of Whole)

WHOLE (100 %)

Math

: :

X

PART

(Equivalent to Rate)

RATE (% of Whole)

WHOLE (100 %)

MathCommission

Net price

: .94 (6% comm)

List Price

$200,000

.94

6% comm.

$212,765

: :

X

Commission split

$6,400

Total commission

$3,200

Broker AAAA

$3,200

Broker BBBB

Co 45% = $1,440

Agent Matt

55% = $1,760

Co 45% = $1,440

Agent Lori

55 % = $1,760

Math28/36

GROSS YEARLY INCOME

:

12 = MONTHLY INCOME

MONTHLY INCOME

X 28% = PITI/PMI

MONTHLY DEBT + PITI/PMI < 36%

Employment Contracts

CHAPTER 6

• Listing1. Listings are personal

service contracts between the broker & seller(principal)

2. Creates an employment contract

3. Most state require them to be in writing to be enforceable in court

ListingChapter 6/79

• Exclusive right to sell– One Broker is appointed as sole agent for

seller & is entitled to compensation regardless of who procurers the buyer

• Exclusive agency– One Broker is appointed as sole agent for

seller & is entitled to compensation regardless of who procurers the buyer, EXCEPT the seller

• Open– Non-exclusive, any number of brokers

including the seller can procure the buyer

Special Provisions/Issues

Chapter 6/80

Listing

MLS- Multiple listing service

Option listing- Broker has right to

purchaser property

Net listing- Broker may claim all proceeds

above the net amount to seller ( illegal in

most state/unethical in most others ,

ILLEGAL in VA)

Option Listing- Gives the Broker the the

right to purchase the property

TerminationChapter 6/81

• Fulfillment of purpose

• Expiration of date stated in agreement

• Destruction of property

• Change in property use

(zoning/eminent domain)

• Transfer of title by operation law

(bankruptcy)

• Mutual consent

• Death/incapacity of either party

• Breach/cancellation by either party

(party may later be liable for damages)

• Bold where listing & Buyer are same

• Underline only listing

Expiration Chapter 6/81

• Must state a definite termination date

• Automatic extension clauses & the wording of some contracts are prohibited by licensing authorities in some jurisdictions

• Some provided broker protection clauses, for procuring cause

Listing ProcessChapter 6/82-83

• www.realestateiii.com • www.caarmls.comCma- Competitive market analysis-

comparison of similar properties, sold, for sale & that didn’t sell

Net- the amount the seller will receive at closing

Market Value- what the market will bear

MathCommission

Net price

: .94 (6% comm)

List Price

$200,000

.94

6% comm.

$212,765

: :

X

Listing Process Chapter 6/85-92

Listings

REIII

ZIP FORMS

Buyer

• Employment

1. Broker-Buyer Agent

2. Principal- Buyer

3. Purpose- to find suitable property

4. Fiduciary relationship(Statutory in Virginia)

Buyer

• Exclusive– completely exclusive agreement

– Buyer legally bound to compensate whether property is located or not

• Exclusive agency– Limits Broker’s right to compensation– Buyer free to find property

• Open– Non-exclusive– Buyer may enter into similar agreement

with other Brokers

Buyer Broker agreement

Chapter 6/94-96

Special Provisions/Issues

BuyerExplain agency agreementParties rights & responsibilitiesCompensation

Flat feeRetainerSource- either party/seller or buyer

Always negotiable

Buyer financial information

Virginia Specific Chapter 2/14-17

Net listings are illegal in Virginia

Listing agreements:• Sellers must receive a copy of

the signed listing agreement & all blanks need to be filled in

• Must have a termination date• Must clearly state commission

rate

Virginia Specific Chapter 2/17/22

• Disclosure/DisclaimerA seller/landlord of a 1-4 unit property

must supply a purchaser, tenant,….. With either.

• Purchase/tenant….may terminate the contract: – within 3 days of receipt– within 5 days of postmark– prior to settlement – prior to occupancy

– prior mortgage application calls for

Virginia Specific Chapter 2/22

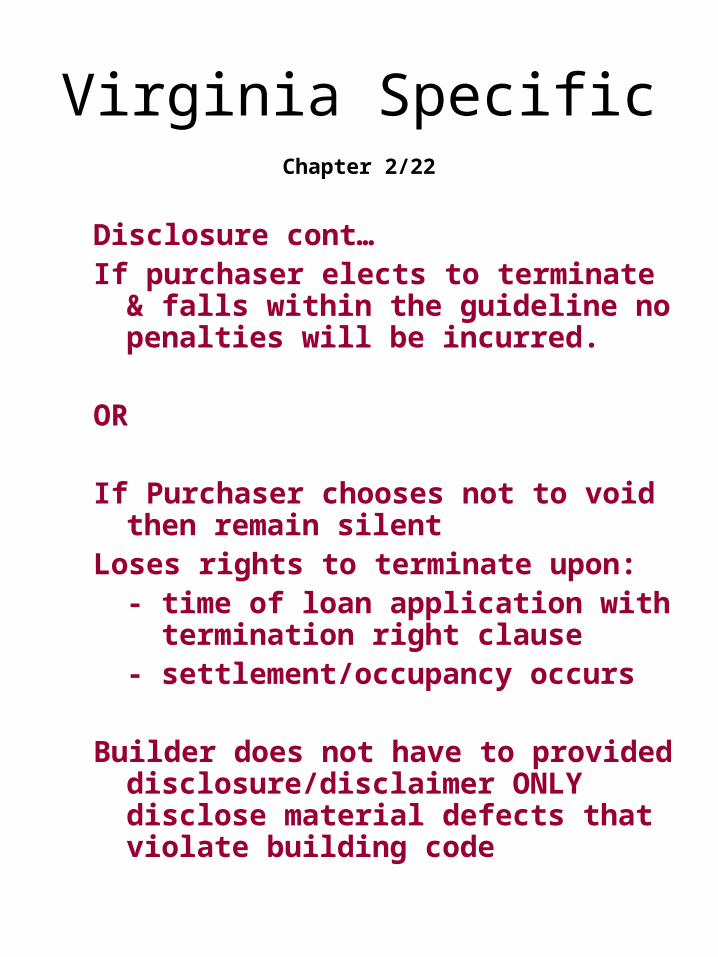

Disclosure cont…If purchaser elects to terminate & falls

within the guideline no penalties will be incurred.

OR

If Purchaser chooses not to void then remain silent

Loses rights to terminate upon:- time of loan application with termination right clause- settlement/occupancy occurs

Builder does not have to provided disclosure/disclaimer ONLY disclose material defects that violate building code

Virginia Specific Chapter 2/26

Disclosure/Disclaimer forms must contain Megan's Law notice

EXEMPTIONS FROM DISCLOSURE:

COURT ODERED TRANSFER

- to settle an estate

- a writ of execution

-foreclosure

-trustee in bankruptcy

-condemnation by way of eminent domain

-suit of specific performance

Virginia Specific Chapter 2/26

• EXEMPTIONS FROM DISCLOSURE: cont….

• Voluntary transfer:

– Between co-owners

– Relatives

– Divorce settlement

– To /from governmental entity,

housing authority/agency

– Sale due to failure to pay,

Fed/State/Lo Taxes

– First sale of a home

Virginia Specific Chapter 2/26-27

• DISCLOSURE: cont….

Buyers recourse-Any action must be commenced within 1 year from date the disclosure was delivered or if no delivery then within 1 year of settlement/occupancy

Owner not liable for reliable 3rd party information or what the owner reasonably believed to be true.

Agents like owner.

Virginia Specific Chapter 2/27

Stigmatized property

Refers to any property that is made to be undesirable by an event or circumstances that has not actual effects on the physical property.

VIRGINA prohibits the disclosure of any discussion of HIV-positive or AIDS

Interest in Real EstateCHAPTER 7

• Government Powers– Government

– Interest– Encumbrances

– Water

4 Government PowersPETE

Chapter 7/103-105

Police power- Preserve order,protect the public health & safety, and promote the general welfare of the citizens. ( protection laws, zoning ordinance& building codes…..)

Eminent domain- the right to acquire privately owned property for public use. Condemnation is the process by which the Gov’t exercises the right

Taxation- A charge on real estate to raise funds for public use

Escheat- when the owner dies & having no heirs or will property goes to the state, intended to prevent abandon/ownerless property

Estates in LandChapter 7/105

defines the degree of quantity,nature & extent of owner’s interest in real

property To be an estate in land , an

interest must allow possession (either now or in the future) & must be measurable by duration

• Freehold- indeterminable length of time (lifetime or forever)/ indefeasible fee

• Leasehold- fixed period of time

• Fee Simple estate- or fee simple absolute/estate of inheritance/fee ownership- the HIGHEST interest in real estate recognized by law- Holder is entitled to all rights to the property, only limited by PETE

Contin…

Estates in LandChapter 7/106-107

• Fee simple defeasible/ defeasible fee-

– condition subsequent new owner must NOT perform some action or activity(owner retains right to reentry), need to go to court

– Special limitation or fee simple determinable- if violated, reverts back to former owner no need to reenter or go to court

Both considered future interest & can be passed on to heirs

Contin….

Estates in LandChapter 7/107-109

• Life Estate- limited in duration to the life of the owner or some the designated person(s), that person(s) may sell their interest in the life estate , it passes to future owners based on provisions of the life estate

– Conventional life estate- by deed during owners life or will upon death, life tenant has the rights to the property until their death, then passes on to another as stipulated in the owners will or back to owner

– Pur autre vie- similar to a conventional life estate other than it’s measured by another life

Estates in LandChapter 7/108

Creator of a life estate plans for the future ownership by naming a:

• Remainder- Remainderman is the person to whom the property will pass to when the life estate ends

• Reversion- Reverts back to the owner of the property when life estate ends

Estates in LandChapter 7/109

• Legal life estate- Dower/Curtsey- Wife/Husband-Not created voluntarily by owner, by the state,for the nonowner spouse after the death of the owning spouse. Receives 1/3 to ½ interest of the property(doesn’t apply in community property states).

• Homestead- depending upon the state, a certain portion of the home/property is protected from creditors. Mortgages, real estate taxes or loans for improvements to the house.

Encumbrances

• Liens

• Easements

• Licenses

• Encroachments

EncumbrancesLiensChapter 7/110

Encumbrance is a right or interest in a property by another than

that of the fee owner

• Lien- Monetary, security for a debt or obligation. If not repaid then property maybe sold to satisfy the lien.

• Deed Restrictions- covenants, restrictions & conditions, private agreements typically made by the owner of the land. Can effect the use of the land.

Encumbrances Easements

Chapter 7/111-113

Easement is the right to use the land of another for a purpose

• Appurtenant easement- Annexed to the ownership of one parcel & used for its benefit on the land of another

--Servient tenement- owns the lands in which the easement is on--Dominant tenement- owns the land that benefits from the easement

• Easement in gross- an individual interest in or a personal right to use the land of another

• Party wall easement- used for a wall that straddles the property lines of adjacent properties w/different owners

• Easement by necessity- arising because owners must have e ingress and egress from their land

Encumbrances Easements

Chapter 7/113

• Easement by prescription- arising from continuous, exclusive use of the property without the owner’s approval– Open, notorious, visible– Tacking

• Easement by condemnation- acquired for a public purpose, requires compensation for loss in property value

Encumbrances Easements

Chapter 7/112

• Creating an easement- BY:

– Expressed grant in a deed from the owner of the property

– Express reservation by the grantor in a deed of conveyance

– Use

– Implication

Encumbrances Easements

Chapter 7/113-114

Terminating an easement-BY:– When the purpose fro which it was created no

longer exists

– The owner of either the dominant or servient tenement becoming the owner of both properties(merged)

– Release of the right of easement to the servient tenement

– Abandonment of the easement

– The nonuse of a prescriptive easement by it’s owner

– Adverse possession by the owner of the servient tenemt

– Destruction of the servient tenement(party wall)

– Court decision of a quiet title action against someone claiming an easement

– Excessive use (change in property use)

Above isn’t automatic

Chapter 7/114

License- The privilege to use another’s land for a specific purpose

Encroachment- anything extending from one property across the property line onto another parcel or beyond legal building setback lines

WaterChapter 7/115-116

end of Chapter

• Riparian rights- rights granted to owners along a non-navigable river or stream

• Littoral rights- rights granted to an owner along an ocean or large lake

• Accretion- increase in land resulting from deposit of soil

• Erosion- Loss of soil by gradually wearing away

• Avulsion- sudden removal of soil due to an act of nature

• Prior appropriation- the right to use water is controlled by the state rather than by the adjacent landowner. A person must show a beneficial use for the water, such as crop irrigation, in order to secure water rights

• Doctrine of prior appropriation-the right to use any water, except for limited domestic use, is controlled by the state

Virginia SpecificChapter 3/30-32

• Eminent Domain-also referred to as “taking”, just compensation must be paid to the owner, that is considered as fair market value. Payment of just compensation is a prerequisite to passing of the title. A genuine but ineffectual effort to purchase the property needs to occur prior to condemnation proceedings- DISCLOSE

• Curtsey/Dower- does not exist in Virginia- NO WILL descent & distribution is used, where property passes to the surviving spouse and others

• Intestate- If no will is left then the property goes to the

The spouse receives 1/3 & remainder is distributed amongst the decedent’s child or their decedents

Virginia SpecificChapter 3/33-34

• Augmented Estate- When the surviving spouse objects to how the property is left

• Homestead- UNSECURED DEBTS One can hold real or personal property exempted from unsecured loans. Total value not to exceed up to $5,000 plus $500 for each dependent….. The exemption does not apply against:– Claims for purchase price of the

homestead property– Mechanics liens– Claims for taxesClaim must be made by deed in case of real

property & inventory list under oath for personal property

A few things may be withheld, family bible, wedding rings, burial plots..

Virginia SpecificChapter 3/33-34

• Easements-

• Easement by Prescription- 20 yrs– In a court action to establish :– Adverse, under a claim of

right,exclusive,continuous, uninterrupted, with knowledge and acquaintance of owner

Forms of Real Estate Ownership

CHAPTER 8

• Severalty

• Co-Ownership

• Trust

• Severalty– Title is held by one

individual

• Co-Ownership– Tenancy in common– Joint Tenancy– Tenancy by the entirety– Community Property

• Trust– Living & Testamentary– Land Trust

Tenancy In Common

• 2 or more owners

• Undivided fractional interest

• Unity of possession

• Each may encumber or

convey their interest

• Each is inheritable

Joint Tenancy

• Right of survivorship(common law)

• 4 unities- required to create a Joint Tenancy– Possession– Interest– Time– Title

• To terminated if you can’t agree then you have to file a court action to partition the property

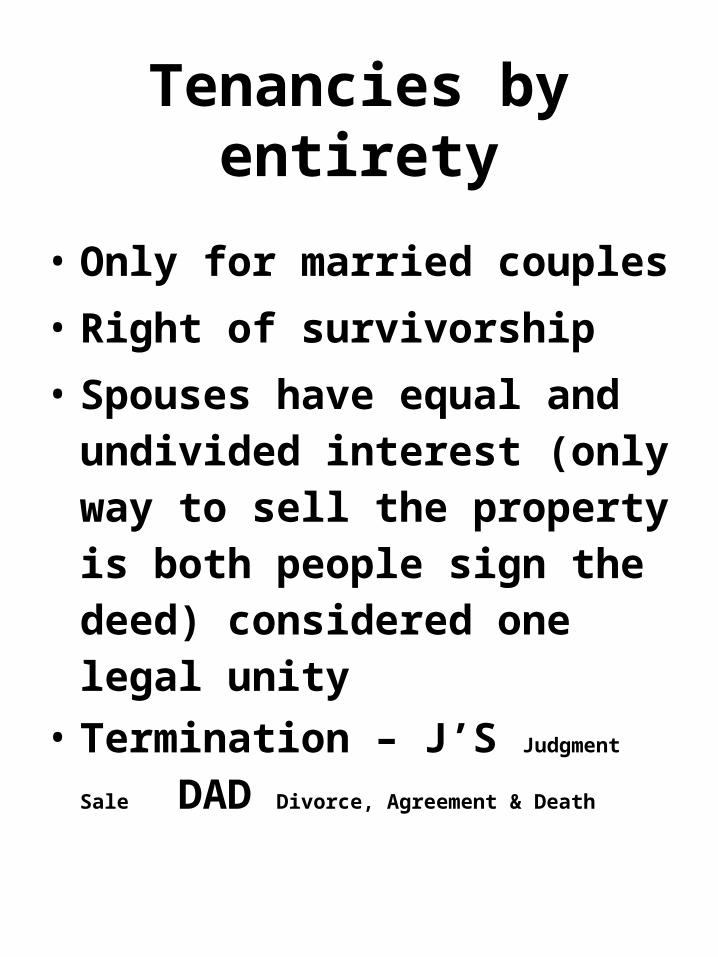

Tenancies by entirety

• Only for married couples

• Right of survivorship

• Spouses have equal and undivided interest (only way to sell the property is both people sign the deed) considered one legal unity

• Termination – J’S Judgment Sale DAD Divorce, Agreement & Death

Community Property

• Spouses are Equal Partner

• Anything acquired during the marriage is community property- Both Real & Personal Property

• Anything you have before the marriage or received during the marriage by gift or inheritance is separate property

• No right to Survivorship – Death of 1 spouse leaves ½ to surviving spouse and other ½ according to will

Trust

Parties to a Trust

• Trustor – creates the Trust

• Trustee – Manages the Trust

• Beneficiary – Receives the benefits

Living Trust

• Put something into Trust while your alive

Testamentary Trust

• The will puts the Trust into effect going upon your death

Land Trust

• Only asset

• Usually the Trustor & Beneficiary are the same person

Legal Descriptions

Legal description- used to identify a property

3 Methods of describing Real Estate

Metes and Bounds

Rectangular survey

Lot and block

Chapter 9/140

• Mete and Bounds-oldest way legally describe property.

• POB- point of beginning and continue to the next boundary. Use linear measurements, natural & artificial landmarks ( monuments) and directions always end back at the POB.

The actual distance between a monument over rides any linear measurement description.

Rectangular surveyGovernment Survey

CHAPTER 9

• Principal meridian lines– Run North to

South

• Base lines– Run West to

East

•The rectangular survey system affects specific land areas within the boundaries

•Both are located in reference to degree of longitude & latitude

•Each principal meridian is named & is crossed by its own base line

Base line

Meridian line

TOWNSHIP TIERS

• Run East and West ,parallel to the base line and are 6 miles apart

• 6 miles wide stripes of townships that are numbered North to South of the base line

RANGE

• 6 miles apart and run North & South parallel to the principal meridian

• 6 miles wide of townships that are numbered East & West of the principal meridian

Township Squares

• The intersection of a township stripe & a range strip

• 6 miles square & contains 36 square miles

township 6 north , Range 2 east of the principal meridian

Township Square(s)

6 miles square

Contain

36 square miles

6 5 4 3 2 1

7 8 9 10 11 12

18 17 16 15 14 13

19 20 21 22 23 24

30 29 28 27 26 25

31 32 33 34 35 36

Section in a Township

SECTIONS

• 36 sections in a township• Numbered 1 – 36, starting upper right corner• Each section is 1 mile square & contain 640

acres• By law Section 16 is reserved for school

purposes• Sections are divided by Halves (320) &

Quarters (160)• Correction lines • - are required to overcome the effect of

the earth’s curvature on range lines• - every 4th township line is a correction

line• - guide meridians run North & South at

24-mile intervals from the principal meridian• - adjustments are made on the North &

West boundaries of a township (sections 1-7,18,19,30)

• Fractional sections & government lots

- Undersized or oversized sections are classified as Fractional lots

- Areas smaller than full quarter-sections are designated as Government lots

- They are used to correct survey errors and physical disparities

• Reading a government survey legal description and calculating the size of a tract of land

- Start at the end of the description and work backwards to the beginning

- Begin size calculations from the right hand side with section containing 640 acres, then divide by each fraction given as you move to the left (the beginning of description)

• Metes & Bounds descriptions within the rectangular survey system

- tracts are too small to be described by quarter sections

- When tract does not follow the lot or block lines of recorded subdivision

- When a tract does not follow the section, quarter-section or fractional section lines

Lot and Block systemrecorded plat

• Identified properties may later be re-subdivided

• This system uses a recorded subdivision plat map• It requires a survey plat by a licensed surveyor or land engineer

• The system is used in all states, sometimes in conjunction with other legal descriptions

Preparing a Survey

• Used to locate a given parcel of land & can also amend a legal description– Shows the location & dimensions of

the parcel– Spot survey includes the location of

buildings on the land

• Requires the use of a licensed surveyor or land engineer

Measuring Elevations

• Condominium laws require a legal definition of the horizontal property rights included with each unit (air lots), air lots specific boundaries above land

• Datum – defined as the mean sea level at New York Harbor, a point, line or surface from which elevations are measured

• Benchmark – permanent reference point throughout the United States, primarily used for marking datums, embossed brass markers

Land Units & Measurements

• Area x Cost per sq. ft. or per acre

Convert the acreage to square feet before multiplying

1 acre = 43,560

Insert examples

Real Estate Taxes &Other Liens

Chapter 10/158

• Lien- a charge against property that provides security for a debt of the property owner

• Encumbrance- any charge or claim that burdens the title to real property, lessens its value or impairs its use. Including liens & claims

Liens may be voluntary or involuntary

Statutory or equitable & general or specific

Real Estate Taxes &Other Liens

Chapter 10/158-159

• Voluntary Lien- created intentionally– mortgage

• Involuntary – Not created by choice:

– Statutory lien- created by statue- real estate tax

– Equitable- created by common law- based on court of fairness

• Vendor lien- belongs to a vendor for the unpaid balance of a purchase price for land

Real Estate Taxes &Other Liens

Chapter 10/159

VISE - 4 ways ways to create a liens, Voluntary, Involuntary, Statutory, Equitable

• General lien- Judgments, inheritance taxes, IRS taxes.. effect all property, real and personal property-on real property the lien attaches the moment it is filed, personal property attaches once the property is seized.

• Specific liens- secured by specific property & effects only the specific property, mortgage, mechanic’s lien….

Real Estate Taxes &Other Liens

Chapter 10/159-160

Liens run with the PROPERTY not the person when properly established

• Priority of liens- typically it’s 1st come 1st served. Real estate tax and special assessment taxes don’t apply to this rule, those are paid 1st, then as the time the lien is recorded in a public place is the order of placement.

• Subordination agreement- when one lien hold gives up their place in line (order) of recording.

General Tax– Ad Valorem Tax specific, involuntary, statutory liens. Imposed by: – States, counties…….Some state exempt cities, state & federal

governments, hospitals….. senior citizens, veterans….

Real Estate Tax Liens Chapter 10/162-163

Assessment-the valuation of the property’s worth, based on fair market value

• Equalization-used to achieve uniformity throughout statewide tax assessments

• Tax rate- “mill” usually 1/1,000 of a dollar or $.001, can be mill-per dollar or in dollars per hundred or in dollars per thousand

• Tax bill- amount due, calculate the tax assessment x tax rate

• Enforcement of tax lien- Lien placed against the property, if not paid then a tax sale is enforced, the owner has the EQUITABLE RIGHT OF REDEMPTION, to pay the taxes along with additional cost to the property prior to the sale.

Real Estate Taxes &Other Liens

Chapter 10/166-167

• Special Assessment- not used much anymore, however if assessed, the cost of the improvement is divided amongst those that benefit

• Mortgage liens-or in some states called a Deed of Trust –involuntary, used to secure the purchase of a property. Lenders usually require a preferred lien, 1st mortgage lien, all others would be junior liens.

• Mechanic's lien- when improvements have been made to the property and the person that performed the work wasn’t paid. Varies from state to state.

• Judgments- a decree issued by a court. Normally used to satisfy a debt that is delinquent. Creditor obtains a writ of execution, where then a sheriff is allowed to enter the property and seize property, real or personal.

Real Estate Taxes &Other Liens

Chapter 10/167

• Lis pendens – puts people on notice that litigation is pending and could effect the title of property.

• Attachment- prevents a debtor from selling the property until a suit is settled, the creditor must post a bond if creditor doesn’t win the debtor received the bond

• Estate and Inheritance tax- are general, involuntary & statutory

• Municipal Utilities- imposes a specific, equitable involuntary lien on the property

Real Estate Taxes &Other Liens

Chapter 10/167-168

• Bail Bond Lien- specific,statutory, voluntary lien against property, no show in court, property is sold.

• Corporation Franchise Lien- general,statutory, involuntary lien against property owned by the corporation

• IRS tax lien- general,statutory, involuntary lien against real and personal property. Does not supercede other liens.

Virginia Real EstateChapter 4/37-38

Co-Ownership• Tenancy in Common- can be

created as follows:– Express limitation- 2 or more

people– Grant- interest– Devise/grant- equal shares– Breakup- in joint tenants– Dissolving- of tenancy by the

entirety- divorce or mutual agreement

Virginia Real EstateChapter 4/37-38

Joint tenancy-similar to other states, everyone has to share the same interest- Virginia has abolished automatic right to survivorship, unless THE DEED expressly creates the right to survivorship

Tenancy in Partnership-Subject to partnership agreementPartner’s rights are not individually assignablePartners rights are not subject to creditors

On the death of a partner his share passes to the other Partners

Partner can transfer property behave of the Partnership

Virginia Real EstateChapter 5/54-55

An incorrect description of a property does not invalidate the deed IF after enough information is available it the property can be identified

4 types of surveys1) Subdivision plat

2) Boundary survey

3) House location

4) Physical or as – built

Virginia Real EstateChapter 6/58

TAX LIENS Uniform taxation- Tax rate and mode of

assessing be same for like properties

Exemptions:

Burial grounds & cemetery lots owned by a company &/or individual

Religious groups

Public libraries & non profit educational institutes………….

Assessment- Taxes run with the land. Responsible from the date of purchase to the end of the year, at closing taxes are prorated.

Virginia Real EstateChapter 6/59

Past-due

Taxes currently due & payable

At closing the above 2 will be collected from the seller and paid.

Taxes not yet due- The seller will be charged the prorated amount and the buyer will be credited the amount

Prepaid – The seller will receive a credit for the amount not used and the buyer will be charged that amount

Virginia Real EstateChapter 6/59-61

New construction- Taxes are based on the time a certificate of occupancy is issued, then prorated

Leases- a perpetual leaseholder/owner pays the taxes & normally in a net lease the tenant pays the taxes

Tax lien- Over rides ALL liens. Virginia allows any unpaid US tax take priority to other liens.

On 3rd anniversary of non payment property may be sold

30 days before action is taken, a notice is mailed to last known address, notice of the sale must be placed in newspaper for 30 to 60 days prior to sale.

Property owner may pay the taxes plus…….. Prior to the sale DATE

Special Assessment…. Notice must be sent to adjacent property owners

Real Estate ContractChapter 11/173

STATUTE OF FRAUDS- MUST BE IN WRITING TO BE ENFORCEABLE

• Contract- a voluntary agreement,a promise between competent parties, supported by legal compensation, to perform or reframe some legal act.

VOLUNTARY- Can not be forced

AGREEMENT/PROMISE- legally enforceable

LEGALLY COMPETENT PARTIES- considered legally capable

LEGAL CONSIDERATION- something of value & legal

LEGAL ACT- can’t be illegal

Real Estate ContractChapter 11/173-174

Contract – Depending upon how it’s created:

EXPRESSED- parties state the terms and show there intentions in WORDS. Maybe oral or written

IMPLIED- the agreement between parties by acts or conduct

BILATERAL- Both parties agree to do something listing/sales

UNILATERAL- One side agrees to do something Option

EXECUTED- When all parties have completely performed all requirements

Property has closed

EXECUTORY- Property has not closed, an act still to perform- contingency

Real Estate ContractChapter 11/174-176

VAILD CONTRACT- elementsOFFER & ACCEPTANCE- An offer has to be

made by one party (offeror) & accepted by the other party (offeree) Mutual assent/meeting of the minds

- A counteroffer voids the 1st offer

- An offer maybe revoked at anytime prior to receiving the acceptance

- Both parties must be notified of the acceptance in order for their to be a contract

CONSIDERATION- something of value (money)

LEGALLY COMPETANCT PARTIES- mentally competent & over the age of 18

CONSENT- No undue duress, fraud…

LEGAL PURPOSE- Can’t be for illegal purposes

Real Estate ContractChapter 11/176-177

VALID- it becomes enforceable- meet all legal elements

VOID- lacks legal elements/ not enforceable/ no meetings of the minds

VOIDABLE- A contract that appears to be valid but where one party may void based on sometime period of a condition or the contract lacks a legal principle (minor, mentally ill, drunk)

UNENFORCEABLE – seems valid but is unenforceable, typically an oral contract

Real Estate ContractChapter 11/177-178

Discharged of ContractsTERMINATED

Performance “time is of the essence” MUST close within that time frame. Otherwise should have a time frame if not then “act” should be performed in a reasonable time frame

Assignment- pass your rights/obligations (delegated) onto another 3rd party (assignee) , you may still be reasonable for the terms of the contract unless specified

Novation – replacing the original contract with another contract, could be same parties or a new party, must have both parties consent……….

Discharged of ContractsTERMINATED

Chapter 11/178-179

Breach- one party doesn’t perform to the contract, non- defaulting party may sue the defaulting party

Buyer may sue the seller- Suit for specific performance- to convey the property OR Damages- for cost & hardship

Seller may sue the buyer- for damages or the purchase price, where the seller tenders the deed

Statute of limitations – time

limitation to bring suit against a party

Real Estate ContractChapter 11/178-179

OTHER REASONS:

Partial performance

Substantial performance

Impossibility of performance- an act cannot be legally performed

Mutual agreement- Both agree

Operation of law- altered, minor, fraud

Rescission- on party may terminate and all monies (deposit) returned

Real Estate ContractChapter 11/179

The Sales ContractThe ESSENTAIL ELEMENTS Offer &

acceptance, Consideration, Legally competent parties, Consent, Legal purpose

Sales Price

Legal description

Statement of type of title/deed (general,special)

Kind of title evidence (title search)

Terms & Conditions

Real Estate ContractChapter 11/180-182

Offer

Counteroffer

Acceptance

Binder

Earnest Money deposits &(accounts)

Equitable title Quickclaim deed

Destruction of premises

Liquidated damages

Real Estate ContractChapter 11/183

….Parts of a contract…Purchaser’s name

Description-Address & Legal descript.

Seller’s name

Purchase price, financing

Amount of deposit & down payment

Closing date

Evidence of title policy (search)

Condition (damaged/destroyed)

Default (liquidated/specific)

Contingencies

Signatures & dates of signatures

Disclosure of agency……………

Real Estate ContractChapter 11/184

….Parts of a contract…

Personal property & real property

Warranties on systems & personal prop.

Identifying any leased equipment

Who & where closing will take place

Distribution of escrow funds

Payment of any outstanding debts

Walk Thru/ final inspection

Agreement of documents and delivery of

Real Estate ContractChapter 11/184

Contingencies- Additional conditions in a contract. Mortgage, inspections, property sale, etc..

Action Time frame Who’s responsible

Escape clause or Kick out clause- Seller retains right to continue to market property, purchaser may have right to satisfy contingency

Amendments & Addendums-

Amendments- agreed upon changes after the contract is ratified

Addendums- agreed upon additions during negotiating a contract

Disclosures- Agency of relationship & property Disclaimer/Disclosure

Real Estate ContractChapter 11/185-186

OPTION- Where owner (optionor) gives the purchasers/lessee(optionee) the right to buy/lease at a certain price for a certain time

LAND CONTRACT- very similar to owner financing BUT, Seller retains title and buyer take possession and gets equitable title to the property

LEASE-Between tenant/landlord or lessor/lessee- exclusive possession of land/property for a specified time and cost

ESCROW AGREEMENT- an agreement between buyer/seller & escrow holder- a contract with a deposit/escrow

Virginia Real EstateChapter 7/67/78

Statue of Frauds- Must be in writing to be enforceable, transferable.

Can be oral, statue doesn’t invalidate an oral contract. Unenforceable after a year.

Power of attorney –Must be specify the transaction and parties, must be notarized & recorded with the deed

Title- A buyer should expect marketable title to the property

Equitable title- gives the buyer an insurable interest- VA places the risk of loss on the buyer.

Warranties- VA caveat emptor buyer beware

Existing: New Construction:

Transfer of TitleChapter 12/192

Title – the rights to or ownership of land/ evidence of ownership

Voluntary alienation- sale, gift or will

DEED is the document that is recorded that transfer ownership

The OWNER/GRANTOR signs the deed & the GRANTEE acquires title

Transfer of TitleChapter 12/192-194

Requirements for a valid Deed

Grantor- Of age(18), sound mind, correct spelling of name(s)

Grantee- Must state a full name

Consideration- some type of $ or gift

Granting clause- for how long, life… this is when the type of interest is stated, joint tenancy, tenants in common…

Habendum clause- used to clarify what type of ownership is being conveyed

Transfer of TitleChapter 12/194-195

Legal consideration-accurate legal description

Exceptions& reservations- must be recorded with deed, covenants, easements, special conditions…..

Signature- all grantors must sign/ power of attorney is possible

Acknowledgement- stating that the grantor voluntarily signs and is normally done so in front of a notary .

Delivery & acceptance- Title hasn’t transferred until the deed is delivered from the Grantor to have been accepted by the Grantee

Execution of Corp. deed- Conveyed only by authority of bylaws &/or BOD, if all or large portion is being transferred, may need to have shareholders approval & ONLY authorized officer can sign deed

DEEDS Chapter 12/196

GENERAL WARRANTY- THE GREATEST protection to the buyer. The warranties include: Grantor has…..

- Covenant of seisin: the rights to convey title- Buyer can recover full purchase price if broken.

-Covenant against encumbrances: that the property is free from liens, encumbrances, other than normal &/or what’s recorded. Purchaser may sue to recover cost to remedy.

- Covenant of quiet enjoyment: free from 3rd party interest, if title is inferior then grantor could be held liable for damages

- Covenant of further assurance- provide to buyer necessary documents to provide good title

-Covenant of warranty forever- to compensate grantee forever the loss sustained

Transfer of TitleChapter 12/197-198

SPECIAL WARRANTY- Grantor received title & not encumbered while they held title

BARGIN & SALE- Grantee has little recourse to recover damages, grantor is release their rights…. Bankruptcy sale

QUITCLAIM- Grantor receives the very least protection from the Grantor, to clear a title quickly

DEED IN TRUST- Deed from Trustor to Trustee for the beneficiary

RECONEYANCE- when the trustee transfer the title back to the Trustor

TRUSTEE’S- the trustee conveys real estate held in the trust to anyone other than the Trustor

DEED EXECUTED PURSUANT TO A COURT ORDER- court ordered or will full consideration vs. &10 & other….

Transfer of TitleChapter 12/199

Grantors tax- a tax charged to record the deed into public records, there are some exemptions, gifts, government bodies,charitable organizations…

In this case the rate is .50 per $500 of value

Value ($324,000) : Unit($500)

X Rate per Unit (.50 cents)

648 x .50= $324

Transfer of TitleChapter 12/200

Involuntary alienation- property transfer against owners consent- condemnation, delinquent taxes, dies intestate w/no heirs….

Transfer by adverse PossessionAnother form of involuntary transfer, a person

makes claim,takes possession and makes claim of the title. Usually ALL of the following must happen:

1. Open- obvious to everyone2. Notorious-known by others3. Continuous & uninterrupted4. Hostile- w/o true owner’s consent5. Adverse to the true owner’s possession

Statutory time frame can be from 5-30 years, from state to state

Transfer of TitleChapter 12/201-203

By Will – An instrument used upon ones death to convey real & personal property. The testator( person who makes the will) leaves the “gift” of real property by will is the(devise) and the person who receives it is the devisee.

For title to pass to the devisee, upon the death of the testator the will must be filed in court and probated.

Probate- legal procedure to verify the validity of the will and accounting of assets.

A will cannot supercede dower/curtsey rights

Legal requirements of a will-Only a valid and probated will can transfer title of property. Testator must be of legal age and sound mind

Probate proceedings- - Person who possess the will is the executor - To see that all assets are distributed correctly - Debts are paid - Distributes property to heirs - In the state in which the deceased resided &/or

another county where property is owned

Virginia Real EstateChapter 8/80

Requirements for a valid deedGrantor w/legal capacity

Grantee

Consideration

Granting clause

Accurate legal description of property

Any relevant exceptions or reservations

Signature of Grantor

Delivery & acceptance

Grantor can sometimes be a grantee as well

Grantee- Legally competent, full name & can be to a nonexistent person

Virginia Real EstateChapter 8/80-81

Competence – A minor may convey property BUT may be repudiated after he/she attains majority.

Habendum Clause- rarely used

Power of Attorney- Acceptable BUT affidavits & sworn statements cannot be signed by POA, lender may not allow POA because of truth in lending requirements

MUST BE RECORDED if not it’s as if the deed wasn’t signed

Virginia Real EstateChapter 8/81-82

Transfer taxes & fees-Recordation fee- Deed State fee

is $.15/$100 & county/city is 1/3 of that $.05/$100

Grantor Tax- $.50/$500Tax on deed of trust- calculated the same

way as recording fee, use applicable rate for area.

Transfer & clerk fees- a fee for miscellaneous papers to be recorded.

Rule of thumb- Buyer pays for “new” items & seller pays

for “old” items* Recording fees are based on Purchaser

price or value of grantor’s equity

Virginia Real EstateChapter 8/82-83

Adverse Possession- Necessary to show actual, hostile, exclusive, visible and continuous possession for 15 years

Must be hostile and without true owner’s permission

Transfer of deceased’s propertyNo will is valid unless it is in writing. Must

be signed by the testator or by someone under the direction of the testator & state clearly that it is to be in his/her name.

Can be in the testator’s handwriting (holographic will) if witnessed in the presence of at least 2 witness, they must sign it as well. Testamentary intent must be on the face of the paper itself.

Virginia Real EstateChapter 8/84

Va is silent on an oral or deathbed will

All heirs and spouses must sign as grantors

SELLER’S NET

AMOUNT SELL WANTS TO NET

$300,000

.94 (94%)

$319,148.93 Equals the amount the property needs to be listed for

Round up to $319,150

Original Cost

SALES PRICE : % OF PROFIT = ORIGINAL COST

$125,000 : 1.3% =

$96,153 IS ORIGIANL COST

To double check yourself:

$96,153 X 1.3% =$124,998.90

ROUND UP

Mortgage Qualifying Ratios

28/36

PITI/PMI- Principal, interest, taxes, insurance & private mortgage insurance

PITI/PMI no more than 28% of total gross monthly income

Total housing allowance (28%) plus monthly debts cannot exceed 36% of monthly gross income

$60,000 yearly income : 12 months =

$5,000 monthly income

X 28% maximum monthly housing allow.

$1,400 PITI/PMI

+ $400 monthly debt

$1,800 : 36% = $5,000 OKAY

Real Estate Commission split with agent & company on a 55agent /45 company split

Sales price $364,000

Commission rate x 7%

Commission $25,480

Commission $25,480

Agent share x 55%

$14,014

Company share $25,480

x 45%

$11,466

Important #’s to remember

1 acre = 43,560 square feet

1 mile = 5,280 feet

1 mile = 320 rods

1 square yards = 9 square feet

1 square mile= 1 section= 640 acres

1 cubic yard = 27 cubic feet

Title Records

Chapter 13/209

Recording – Any written document that affects any estate , right, title, or interest in land MUST BE recorded in the county where the land is located to serve public notice. To be eligible for recording a document must be drawn & executed according to the recording acts of the state

Notice – Giving notice 3 types

CONSTRUCTIVE – diligent inquiry – Properly recorded documents serves as notice to the worldACTUAL- direct knowledge someone that has searched the public records & inspected the property/ they can’t use lack of constructive notice to justify a claimINQUIRY- law assumes a reasonable person would inquiry more into the property

Priority – Order of rights in time who recorded 1st, who has possession……. 1-800-attorney @ law

Title Records

Chapter 13/211

Unrecorded - ????? Example ???????

Chain of title – the order in which tile is recorded (passed) Trace ownership through the years, if there is an unbroken chain then (gap) then there’s a cloud on the title that needs to be resolved, court action, a suit to quiet title, each claimant is allowed to present evidence then the judge rules.

Title search & Abstract of Title – Title search- examination of all public records to determine if there are any defects in the chain of title. Starts with present owner & goes back 40-60 years. Some states have adopted the Marketable Title Act this extinguishes certain interest & cures certain defects, goes back to

Title Records

Chapter 13/212

Marketable Title – Disclose no serious defects & does not depend upon doubtful questions of law or fact to prove its valid-Doesn’t expose purchaser to hazards of litigation or threaten the quiet enjoyment of the property-Convinces a reasonably well-informed & prudent person that he/she could, in turn,sell or mortgage the property-Unmarketable title can still be transferred but its defects may limit or restrict its ownership-Typical sales contract requires the seller to deliver marketable title to the buyer-Customary for a preliminary title search be conducted after sales contract is signed to give the buyer opportunity to review & seller time to cure defects before settlement

It’s important to sure any defects/restriction before closing, a buyer cannot be forced to accept what they didn’t bargain for in the contract.

Title Records

Chapter 13/212

Proof of Ownership- evidence of title: deed by itself not sufficient

Certificate of Title- Statement of opinion of the title’s status as of the date of the certificate-Based on a title search-Prepared by a title company, licensed abstractor or attorney-Imperfect because unrecorded liens, rights of parties in possession & hidden defects such as forged deeds, marital interest or fraud cannot be detected.

Abstract & attorney’s opinion- May be used in some areas as sufficient evidence-An opinion issued on basis of abstract-Imperfect because of the same conditions that affect a certificate of title

Title RecordsChapter 13/213-214

Title Insurance- Insures the policyholder against loss due to defects in the title other than those exceptions identified in the policy (unlike other insurance policies, title insurance insure against past occurrences)- Based on the title search-Preliminary report of title(commitment to issue policy) issued describing policy to be issued & includes: Name of party

Legal description of property Estate or interest covered Condition & stipulations Schedule of exemptions

-Premium paid (one time @ closing)-Insurer’s liability cannot exceed face amount ofpolicy unless there is an inflation rider-When the title company makes a payment it

generally acquires the rights to any remedy or damages available to insurer- SUBROGATION

SEE PAGE 214 TABLE

Title RecordsChapter 13/214

COVERAGE- Standard coverage- Normally insures the title as it is

known from public record & hidden defects as forged documents, conveyance by incompetent grantors, incorrect marital statements & improperly delivered deeds

Extended coverage- As provided by the American land Title Association policy, includes standard items & protects the homeowner against defects that maybe discovered upon inspection of the property, rights of parties in possession, examination of survey & certain unrecorded liens

Exclusions- not everything is covered, zoning, water rights, easements, taxes…

TYPES OF POLICIES- -Owner’s- Owners, heirs equityLender’s- Mortgage amount, reduces as principal

amount is paid down-Leaseholder’s- the tenantCertificate of sale- property purchased in a court

sale

Title RecordsChapter 13/214-215

Torrens System- A legal registration system used to verify ownership & encumbrances . Provides evidence of title verses searching the public records. Owner submits an application, it is submitted to the courts clerk, if applicant proves they are the owner then a certificate of title is issued.

UNIFORM COMMERCIAL CODE-

DOES NOT APPLY TO REAL PROPERTY UCC , Governs the documents when personal property is used as collateral. A lender requires that a security agreement be signed & a financial statement be given, it identifies any real property that may be involved.

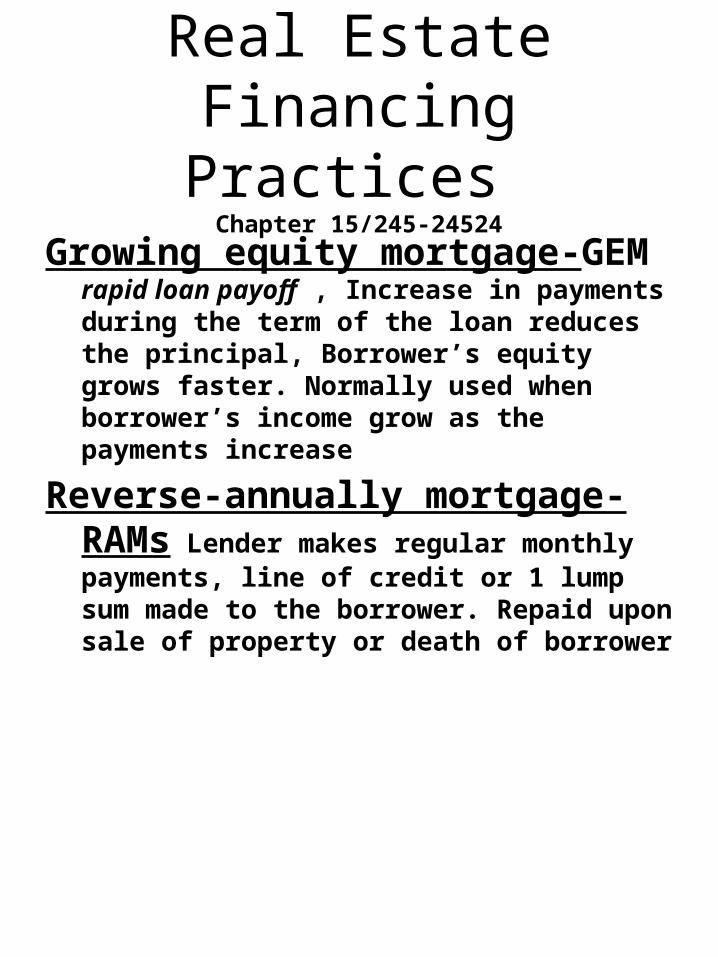

Real Estate FinancingChapter 14/221-222

Mortgage- is a voluntary liens on the real estate, the Mortgagor (borrower) pledges the property as collateral to the Mortgagee

(lender) (for money)

Title theory- Mortgagor gives title to the Mortgagee and he/she keeps equitable title

Lien theory-Mortgagor keeps the legal and equitable title to the property, Mortgagee has a lien on the property, if Mortgagor defaults then Mortgagee must foreclose, offer property for sale. Some states allow the Mortgagor (owner) the right to redeem the property for a certain amount of time after the sale.

Intermediate theory-Similar to title theory but Mortgagor must foreclose to obtain legal title

Real Estate FinancingChapter 14/222-223

One cannot convey anymore than what one owns. Interest/ fee simple, condo & the same goes for a

mortgage…..The are TWO parts to a mortgage

Mortgage loan instruments:Promissory note- otherwise known as the note or

financing instrument, The Mortgagor executes(signs) the note as a promise to pay back.

Mortgage- or otherwise known as deed of trust, security instrument , creates the lien on the property.

Hypothecation- the pledging of property, must have a debt to secure in order to have an effective deed of trust

Deed of trust- Title without the right to possession, the deed is given as security for a loan to a third party called a trustee. Trustee holds title on behalf of the lender beneficiary, the holder of the note. The conveyance establishes the actions that will be taken if the Trustor, borrower defaults.

Real Estate FinancingChapter 14/224

Provisions of the note- promissory note executed by the borrower/maker/payor is a contract in itself. Normally it states the debt, time & method of payment and interest rate.

If it’s not tied to a mortgage or deed of trust then it’s called an unsecured note, normally a short term loan.

A REAL ESTATE LOAN is a SECURED loan & ALWAYS includes security… a mortgage or deed of trust.

A note is a negotiable instrument the bank or whomever holds the note is the payee, it may be transferred to a third party, 1. Assigning or 2. Delivery

DATES SHOULD BE CLEARLY STATED

Real Estate FinancingChapter 14/224-225

Interest- The charge for using money.

Arrears-due at the end of the monthAdvance- due at the beginning of the month