SEMA 2011: Changing Landscape of Media | Automotive Marketing

Upload

carlos-a-folgarCategory

view

117download

2

I N N O V A T I O N I N E N G I N E S & F U E L

J U L Y 2 0 1 6

C O M P A N I E S A N A L Y S I S

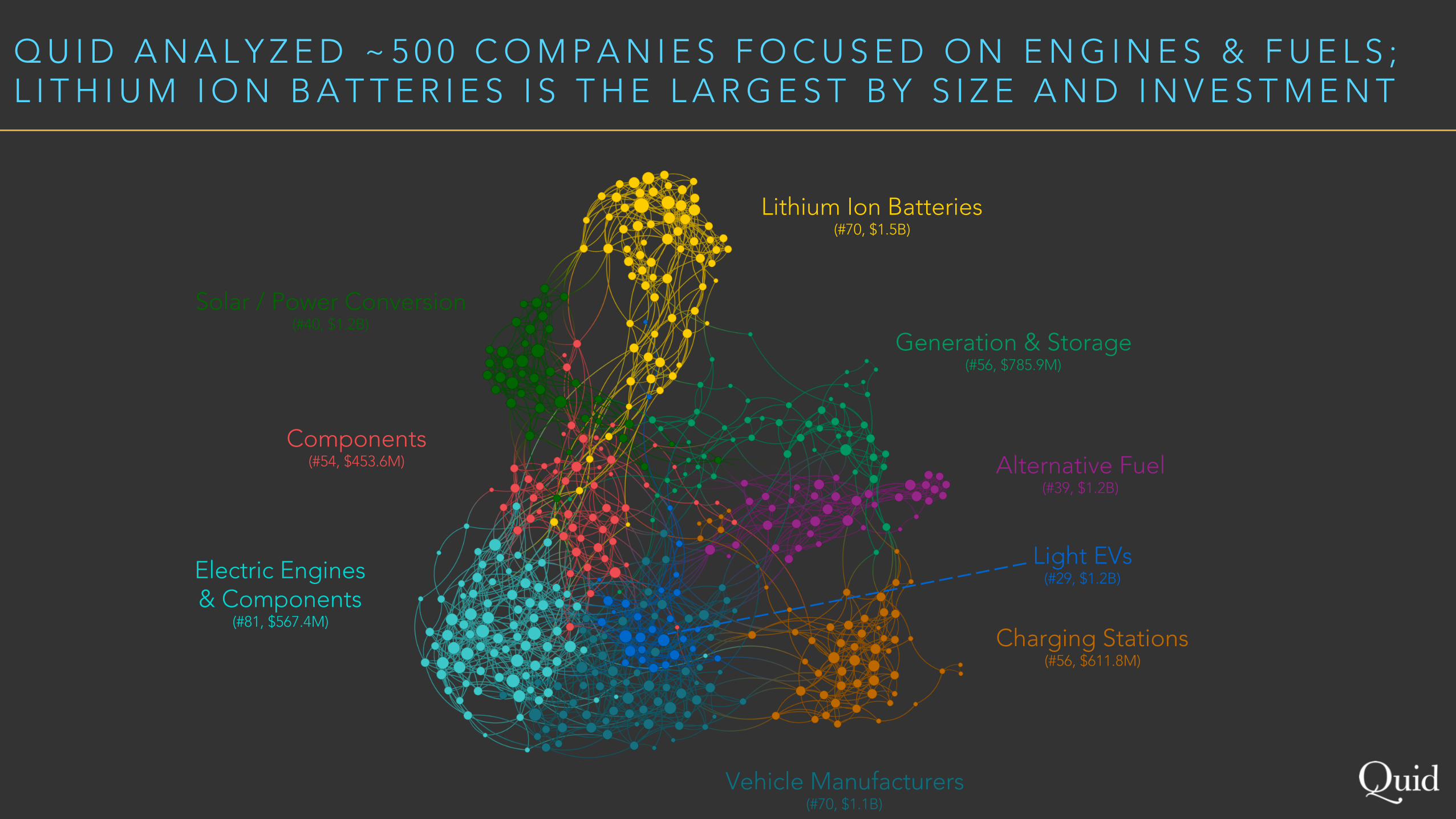

Q U I D A N A L Y Z E D ~ 5 0 0 C O M P A N I E S F O C U S E D O N E N G I N E S & F U E L S ; L I T H I U M I O N B A T T E R I E S I S T H E L A R G E S T B Y S I Z E A N D I N V E S T M E N T

Lithium Ion Batteries(#70, $1.5B)

Generation & Storage(#56, $785.9M)

Alternative Fuel(#39, $1.2B)

Charging Stations(#56, $611.8M)

Vehicle Manufacturers(#70, $1.1B)

Electric Engines & Components

(#81, $567.4M)

Components(#54, $453.6M)

Solar / Power Conversion(#40, $1.2B)

Light EVs(#29, $1.2B)

L I G H T E V S I S A N E W E R C L U S T E R W I T H F E W E R C O M P A N I E S B U T H A S S T I L L R A I S E D S I G N I F I C A N T F U N D I N G

AGE (Median Founded Year)

Inve

stm

ent R

ecei

ved

($M

)

Vehicle Manufacturers (70)

Electric Engines & Components (81)

Components (54)

Solar / Power Conversion (40)

Lithium Ion Batteries (70)

Generation & Storage (56)

Alternative Fuel (39)

Light EVs (29)

Charging Stations (56)

L I T H I U M I O N B A T T E R I E S A N D C H A R G I N G S T A T I O N S A R E C L U S T E R S T H A T H A V E R E C E I V E D A L A R G E N U M B E R O F F U N D I N G E V E N T S

11 10 10 2

12 15 15

9 5

12 5 12

3 3

5

5

9

8 3

7

4

7

4

7

10

12

9

5

2

8 11

9

14

6

11 9

12

9

4

5 11

6

3

4

0

25

50

75

100

2012 2013 2014 2015 2016 YTD

Vehicle Manufacturers

Solar / Power Conversion

Lithium Ion Batteries

Light EVs

Generation & Storage

Electric Engines & Components

Components

Charging Stations

Alternative Fuel

Num

ber

of e

vent

s

T H E F U N D I N G R E C E I V E D F O R T H E F I R S T H A L F O F 2 0 1 6 H A S A L R E A D Y O V E R T A K E N T H E F U N D I N G F O R A L L O F 2 0 1 4

179.1 67.6 101.3

1.2

103.1

3.0 49.8

36.6 57.8

48.5

3.7

40.3

32.6 3.0

31.0

51.1

69.0

88.0 107.7

55.5

25.1

71.1

41.0

162.2

46.9

70.8

166.8

26.6

24.3

50.6

80.1

141.0

179.9

169.6

61.7

42.0

132.5

214.5

285.4

1.8

27.8

24.8

513.0 21.2

200

400

600

800

1000

1200

2012 2013 2014 2015 2016 YTD

Vehicle Manufacturers

Solar / Power Conversion

Lithium Ion Batteries

Light EVs

Generation & Storage

Electric Engines & Components

Components

Charging Stations

Alternative Fuel

Includes $500M round in NextEV

Includes $234M round in Xiamen

San'an

Fund

ing

rece

ived

($M

)

A H E A T M A P O F T H E L A N D S C A P E D E M O N S T R A T E S I N T E R E S T I N G I N S I G H T S A B O U T E L E C T R I C E N G I N E S A N D C H A R G I N G S T A T I O N S

Segment Number of Companies

Total Exit Amount ($M)

Number of Exit Events

Total Private Investment

($M)

Number of Private Inv.

Median Private Inv.

($M)

Median Founding Year

Electric Engines & Components 81 907 25 567 31 6.0 2007

Lithium Ion BaAeries 70 1,227 13 1,513 41 8.3 2007.5

Vehicle Manufacturers 70 362 10 1,146 30 2.6 2008

Charging StaHons 56 140 15 612 36 1.6 2009

GeneraHon & Storage 56 151 11 786 30 2.0 2008

Components 54 20,753 16 454 22 1.8 2006

Solar / Power Conversion 40 275 6 1,185 26 4.0 2007

AlternaHve Fuel 39 825 14 1,192 29 2.9 2006

Light EVs 29 117 6 975 18 4.1 2009

Most exit events by far, but not highly

valued exits compared to other

segments

Not a high number of exits, comparatively, but an

extremely high value of exits

Second highest number of private investments,

but smallest median size.

Most private investment and highest median

investment

Smallest value Largest value

T H E F U T U R E O F T H E A U T O I N D U S T R Y M A Y 2 0 1 6

N E W S A N A L Y S I S

News articles on the future of cars Colored by topic, clustered by stories n = 2146

D R I V E R L E S S C A R S , E L E C T R I C C A R S , A N D I N C R E A S E D I N S T A N C E S O F P U B L I C T R A N S P O R T / R I D E S H A R I N G D O M I N A T E C O N V E R S A T I O N S

Autonomous/Driverless Cars, 10%

Public Transport/Ride Sharing, 9%

Electric Cars, 9%

Hybrids/Sports Cars, 8.6%

Mercedes/Luxury Cars, 8.4%

Hydrogen Powered, 6.4%

Apps, 6.1%

Flying Cars, 5.9%

Connectivity of Cars, 5.9%

Sensors, Automation, Self-Parking, 5.8%

Market Adaption, 5.8%Faraday Future, 5.4%

Future of Car Dealerships, 4.3%

Car Rental Markets, 3.8%

Car Materials, 3.6%

T O P A U T O M O B I L E C O M P A N I E S A R E H E A V I L Y V E S T E D I N S P A C E

Network for Emerging Tech in Auto

Google, 8.7% Toyota, 5.9% BMW, 4.8%

Ford, 4.3% Tesla, 3.0% Audi, 2.6%

Driverless cars Hydrogen-powered vehicles Sports cars/luxury cars

Electric cars*scattered Luxury cars/sensors, automation

C O N S U M E R S A N D P U B L I S H E R S A R E E Q U A L L Y E N G A G E D B Y D R I V E R L E S S C A R S , W H I L E M E D I A S O L E L Y F O C U S E S O N C O N N E C T I V I T Y O F C A R S

Engagement by count of shares, colored by topic

Autonomous/Driverless CarsPublic Transport/Ride Sharing

Connectivity of Cars

Mercedes/Luxury Cars

Faraday Future

Takeaways: -Media cares about “usage-based insurance, smartphone integration, and app-based home connectivity” more than consumers. -With the prevalence of Google’s driverless car, the media and consumers seem to be engaged and looking towards the future on the topic. -Luxury cars started entering the space towards Q4 of 2014. -Even sans the release of a car (2017), Faraday Future has created an aura of speculation around their car of the future, having already employed 750.

Patent Network for Google n = 1823

G O O G L E ’ S P A R T I C U L A R E F F O R T S I N T H E S E L F - D R I V I N G S P A C E A R E S U P P O R T E D B Y C O N S U M E R S ’ O P I N I O N S O F T H E M

Google Maps (geographic)

Wearables

Autonomous/lane detection

Sensors

Path detection

12.11% of overall network honed in on car space

WearablesGoogle Maps

Autonomous

Sensors

“Method for detecting driving with wearable computing device e.g. mobile phone, involves performing operation, based on determination that user of wearable computing

device is currently driving the moving vehicle.”

B M W I S W O R K I N G W I T H M A N Y D I F F E R E N T M A T E R I A L S T O M A K E T H E C A R L I G H T E R /F A S T E R , Y E T S T I L L T E C H N O L O G I C A L L Y A D V A N C E T O W A R D S T H E F U T U R E

Hybrid Vehicles

Fuel Cells

Batteries

Hydrogen Pressure Tank

Welding for Electrical Connector

Route Determination

Composite material for lighter car

BMW is working on:Cathode for lithium-ion batteryElectrical batteryFuel cell for hydrogen sensorCell contacting system for battery moduleElectrical-propelled motor car high-voltage batteryPower electronics apparatus (converts electrical

energy)Cryotank for storing hydrogen under pressureDevice for protecting high-pressure gas container

Composite Materials:Unidirectional fiber bundlesThermoplastic matrix & polymeric material3D composite material

Patent Network for BMWn = 1727

H Y D R O G E N - R E L A T E D I N N O V A T I O N I S M I N U S C U L E I N C O M P A R I S O N T O T H E R E S T O F T H E N E T W O R K

Takeaways:Everyone is discussing hydrogen-powered cells since it’s revolutionary, however, only 3.5% of the actual network is focused on this. (Probably due to most of the innovation being newer and tangibility; Toyota released the ‘Mirai,’ which is a fuel cell vehicle in 2014.)

Hybrid vehicles

Battery cooling duct

Lithium ion battery

Fuel cells

Non-aqueous electrolyte secondary battery

A P P L E ’ S P R O J E C T T I T A N I S S T I L L I N N A S C E N T S T A G E S O F D E V E L O P M E N TNews Network for Apple’s ‘Project Titan’ n = 688

Financial Stress of Apple Car, 13%

Reports of Apple making a car, 12%

2019 launch date, 10%

Speculation, 8.6%“Are Apple and BMW making a

car together?”

Elon Musk speculates, 6.7%

Apple meets with California to discuss

plans, 6.5%

Apple Execs, 6.4%

2020 launch date, 5.7%

A123 Lawsuit, 5.2%

Apple vs BMW i3, 4.9%

Hiring, 4.1%

Doug Betts, 3.9%

Patents, “Apple Watch keeping track of car…” 3.3%

Facility/land where car will be developed, 3.2%

“Apple set to build car…” 2.6%

Anonymity, 2.5%

Takeaways:With the car not being

launched until at least 2019/2020, there is still much speculation around the development/existence of the car.

Apple is in the R&D and conversation stage (in relation to hiring and setting up a new facility).

W H Y I S F A R A D A Y F U T U R E A M A J O R T O P I C I N T H E E M E R G I N G A U T O M O B I L E T E C H N E T W O R K ?News articles on Faraday Future Colored by topic, clustered by stories n = 1726

Aston Martin

“Tesla’s Rival”

Chinese ‘LeEco’ unveils new concept car, which

partners with FF

34% of network focused on competition

Other cars from the Consumer Electronics Show

BMW, Ford, Vanda Electric, Volkswagen, BAIC

Tesla, Elon Musk

S P E C I F I C S O F T H E I R N E T W O R K A L L O W U S T O G A U G E T H A T M O S T O F T H E C O N V E R S A T I O N I S R E L A T E D T O T H E I R C O M P E T I T O R S , S P E C I F I C A L L Y T E S L A A N D A S T O N M A R T I N

News Network for Faraday Future based on themes n = 1726

Only patent owned by FF: “Power inverter assembly for motor vehicles, has second direct current bus bar sub-assembly which electrically couples direct current link capacitor with power modules, cooling sub-assembly is associated with power modules.” (US9241428B1 - 2016-01-19)

K E Y T H E M E S

Competition 34%

Design/Product 19%

reputation 17%

Facility in nevada 16%

Key people involved 3.8%

Competitive Rivals 3.8%

Funding 3.1%

H O W I S F A R A D A Y F U T U R E A B L E T O I N V E S T $ 1 B I N T O A N E W N E V A D A F A C I L I T Y ?

Nick SampsonSenior VP of R&D and Engineering

(Previous Tesla Motors)

Jia YuetingFounder & CEO of Leshi

Brian SandovalGovernor of Nevada

Richard KimHead of Design

(prior made exterior of BMW i3)

Ding LeiCo-founder of Leshi’s Auto Division

Dag ReckhornVP of Manufacturing

(Ex-director of manufacturing, Tesla Model S)

Dan Schwartz Treasurer of Nevada

C O N S U M E R S T H I N K T O Y O T A I S O N L Y I N N O V A T I N G I N H Y D R O G E N - P O W E R E D C A R S , H O W E V E R , T H E Y A R E A C T U A L L Y W O R K I N G O N A N U M B E R O F B R E A K T H R O U G H S : S P A R K I G N I T I O N , E L E C T R O L Y T E B A T T E R I E S , A N D L I T H I U M C E L L S A M O N G O T H E R S

Hybrid vehicles/electrical storage

Battery cooling duct

Lithium ion battery

Charging device, power source

Welding of secondary battery

Semiconductors

Electrolyte batteries

Fuel cells

Non-aqueous electrolyte secondary battery

Spark Ignition

Patent Network for Toyotan = 1909

37.33% of their network is focused on innovation efforts in the automobile industry