Quarterly report on the global and the spanish economy Q3 2016 Círculo de Empresarios

50

Quarterly report on the global and the Spanish economy Q3 2016 Círculo de Empresarios Madrid, November 2016

-

Upload

circulo-de-empresarios -

Category

Economy & Finance

-

view

42 -

download

0

Transcript of Quarterly report on the global and the spanish economy Q3 2016 Círculo de Empresarios

Quarterly report on the global

and the Spanish economyQ3 2016

Círculo de Empresarios

Madrid, November 2016

2016 GDP projections

Source: Círculo de Empresarios based on IMF (October), 2016

2016 2017

Global

3.1 3.4(3.2 previous) (3.5 previous)

-3,3

-1,8

-0,8

US

Argentina

Brazil

Eurozone Russia

India

Nigeria

-1,8

-0,8

1,7

1,8

UK

-3,3

1,6

-3,3

-1,7

6,6

7,6

2,9 Australia

0,5

Japan

China

3

Steady and moderate growth in an uncertainty global

environment (I)

In economic terms...

• Contagion effect

• Impact on the UE

• FED doubts

• FED’s credibility at risk

• Private debt problem

• Overcapacity

BREXITPAUSE IN RATE

HIKES

THE ECONOMIC DESACELERATION

CONTINUES

Source: Círculo de Empresarios, 2016

Risks

4

In geopolitical terms...

Political risk events calendar

2016 COUNTRY EVENT

8 November US General election

4 December Italy Constitutionalreferendum

4 December Austria Re-run of PresidentialElection

2017 COUNTRY EVENT

March UK Article 50

March Netherlands General election

April-May France Presidential election

September Germany General election

November China 19th National Party Congress

Source: Círculo de Empresarios, 2016

Steady and moderate growth in an uncertainty

global environment (II)

A growing level of protectionism and political climate that stalls structural reforms

5

Higher growth in emerging markets...

After 5 consecutive years of declining economic activity, growth in emerging markets is

expected to strengthen in 2016

Source: Círculo de Empresarios based on IMF (October), 2016

Economic sentiment has

improved:

Lower interest

rates in advanced

economies

Higher

commodity

prices

Due to

Recovery in capital flows

Currency appreciation

Therefore

8,58

5,77

2,88

7,46

6,27

5,314,96

4,574,02 4,17

4,6

-1

0

1

2

3

4

5

6

7

8

9

10

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Real GDP growth %

Emerging Global

Forecast

6

...Yet growth remains fragile in advanced

economies

Growth forecast revised down by 5 percentage points for 2016

2016 GDP projections

* July’s forecast: 1,8%

Source: Círculo de Empresarios based on IMF (October), 2016

1.6%

0.8%

1.7%

1.3%1.8%

0.5%

2,7

0,1

-3,4

3,1

1,71,2 1,2

1,9 2,1 1,6 1,8

5,7

3,0

-0,3

5,4

4,23,5 3,3 3,4 3,2 3,1

3,4

-4

-3

-2

-1

0

1

2

3

4

5

6

7

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Real GDP growth%

Advanced GlobalForecast

7

Weakness in global trade(I)

Source: Círculo de Empresarios based on WTO, 2016

18.5 tn$

Billion $

Global merchandise trade

16.4 tn$

2014

2015

Global trade volume 2015

-11,4%

8

Weakness in global trade(II)

World trade will grow at the slowest pace since the global financial crisis

Source: Círculo de Empresarios based on WTO, 2016

Forecast 2016:

1.7%(2.8% in April)

Lower relationship betweentrade growth and world GDP

Reasons for a global trade

contraction

Slowing GDP

Creeping protectionism

Note: Baltic Dry Index surged 100% since February minimums

-18,3

18,3

1,3

-25

-20

-15

-10

-5

0

5

10

15

20

25

07T1 08T1 09T1 10T1 11T1 12T1 13T1 14T1 15T1 16T2

Quarterly global trade evolutionAnnual change

9

China

China’s transition to a more consumption economy influences in global trade

slowdown

Source: Círculo de Empresarios based on Reuters, IMF, 2016

Chinese imports accounts 10% of global imports and has an impact on 80% of global trade

0

0,2

0,4

0,6

0,8

1

Asia Commodity

exporters

Advanced Eastern Europe Rest

Impact on exports of a 1 % shock to China's demand

after one year

Global average impact-11,2

-25,4

11,5

-1,8

-4,1 -4,8 -4,4-2,8

-10

-18,8

-13,8

-7,6

-10,9

-0,4

-8,4

-12,5

1,5

-1,9

-30

-25

-20

-15

-10

-5

0

5

10

15

Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16

Chinese external sectorAnnual change

Exports Imports

10

China

Forecast

GDP growth remained stable in Q3 at 6.7% (6.9% year

on year change Q2)

Consumption contributed 71% of GDP growth in the first 3

quarters of the year (66.4% in 2015):

Gradual transition continues

Improvements...

Manufacturing PMI

Industrial Production

Fixed Investment

Retail sales

51,2

6

8,2

10,7

Source: Círculo de Empresarios based on IMF, Bankia, 2016

Note: Chinese Government GDP target: 6,5%-7%

%

%

%

points

8,4

14,2

10,61

6,6 5,9

0

2

4

6

8

10

12

14

16

Real GDP growth

%

11

China

Higher financial imbalances

Chinese corporate debt (18 trillion

$) is equivalent to US GDP

Source: Círculo de Empresarios based on IMF (October), 2016

Total China’s debt to GDP ratio is

250%

Note: Actually, China requires 6 yuan debt to generate 1 yuan of GDP

Chinese non-perfoming loans

(NPLs) rose to 14% (IMF) vs 2.15

(Chinese government)

121,9

170

70,7

97

50

70

90

110

130

150

170

190

2010 2011 2012 2013 2014 2015 2016

Chinese corporate debt% GDP

China

Emerging

12

Latin America

Gradual recovery in economic activity

Source: Círculo de Empresarios based on IMF (October) and BBVA Research, 2016

LATIN

AMERICA

2016 GDP growth

PACIFIC ALLIANCE MERCOSUR

Great disparities in the region

2.6%

-0.9Pacific Alliance: Chile, Colombia, Mexico, Peru

Mercosur: Argentina, Brazil, Venezuela, Paraguay, Uruguay and Bolivia

3,14

-1,8

6,1

4,6

3 2,9

10

-0,6

1,6

-4

-2

0

2

4

6

8

Real GDP growth

%

%

13

Higher market confidence

Financial Markets

Recovery in exports

Brazil

Source: Círculo de Empresarios based on IMF, BBVA Research, 2016

The economy continues in contraction but recovery in 2017

Lack of reforms

Reduction in potential GDP

Deficit in public accounts

Weaknesses Strengths Challenges

Inflation

Debt

Confidence

14

Brazil

Source: Círculo de Empresarios based on BBVA Research, IBGE, 2016

Brazil’s economy will grow between 0.5-0.9% in 2017 underpinned by domestic

demand and exports

Lower inflation pressure but still above

inflation range (4.5%)

-20

-15

-10

-5

0

5

10

15

Fixed capital

investment

Private

consumption

Public

expenditure

Exports Imports GDP

GDP by components%

2015 2016 2017

0

0,3

-1

-2,3

-1,5-1,3

-0,4-0,6

-2,5

-2

-1,5

-1

-0,5

0

0,5

Q3-14 Q4-14 Q1-15 Q2-15 Q3-15 Q4-15 Q1-16 Q2-16

Real GDP growthQuarterly change %

15

Japan

Source: Círculo de Empresarios based on OECD, Caixabank Research, 2016

Economic growth remains fragile although new fiscal stimulus

Forecast

* The plan incorporates 13.5 trillion yen mainly aimed to infrastructure projects and demographics

%

GDP 2017: 5,1 tn $ (500 tn ¥)

Japan’s potential GDP is projected

to remain weak and unemployment

rate in minimums

Doubts to achieve inflation target

(2%)

-10,0

-8,0

-6,0

-4,0

-2,0

0,0

2,0

4,0

6,0

8,0

Real GDP growthAnnual change %

2014 2015 2016 2017

Unemployment rate 3,6 3,4 3,2 3,1

Employment 0,6 0,4 0,5 -0,2

Wages 0,8 0,7 1 2

Inflation 2,7 0,8 0,1 2,1

Real GDP 0 0,5 0,5 0,6

16

US

Source: Círculo de Empresarios based on Markit, Bloomberg, 2016

January-16 March-16 May-16 July-16 September-16 October-16

Positive leading indicators

Expansion

Contraction

New home sales surge

to 9 – year high

+3.1%

Durable godos orders*

+1.6%

* Non volatile sectors included

47

48

49

50

51

52

53

54

55

56

Manufacturing and services PMI's, 2016

Services Manufacturing

17

US

Source: Círculo de Empresarios based on Markit, Bloomberg, 2016

After loosing economic momentum between Q415-Q216, US GDP growth

picked up

4Q15-2Q16

+1% +1.4%

2Q-2016

+2.9%

3Q-2016

+1.6-2%

2016 Forecast

-1,2

4

5

2,32

2,62

0,9 0,81,4

2,9

-2

-1

0

1

2

3

4

5

6

1Q-14 2Q-14 3Q-14 4Q-14 1Q-15 2Q-15 3Q-15 4Q-15 1Q-16 2Q-16 3Q-16

Real GDP growthAnnual change %

-10

-5

0

5

10

15

1Q-14 2Q-14 3Q-14 4Q-14 1Q-15 2Q-15 3Q-15 4Q-15 1Q-16 2Q-16 3Q-16

GDP by componentsAnnual change %

Private consumption Private investment Exports

18

USStable net employment creation

+192,000 (average jul-sep*)

5%(sep)

Net employment creation

Unemployment rate

Wages

+2.6%

Source: Círculo de Empresarios based on BLS, BEA, 2016

149

295 280 271

168

233

186

144

24

271252

167 156

0

50

100

150

200

250

300

350

US net employment creationMonhly, thousands

62,2

62,4

62,6

62,8

63,0

63,2

63,4

4,0

4,5

5,0

5,5

6,0

6,5

7,0

Unemployment and labor force participation% labour force

Labor force (right axis)

Unemployment (left axis)

19

US

Financial markets anticipates a rate hike before the end of the year

Source: Círculo de Empresarios based on Berenberg, 2016

70% probability

Not in favor In favor

Indications to raise interests

0,5 0,5 0,5

0,75

1 1

1,25

1,5

0

0,2

0,4

0,6

0,8

1

1,2

1,4

1,6

1Q-16 2Q-16 3Q-16 4Q-16 1Q-17 2Q-17 3Q-17 4Q-17

Fed interest rates expectations%

20

Europe

Economic growth after Brexit

1.8% 1.8% 1.8%

Q1-2016 Q2-2016 Q3-2016

BREXIT

EU-28 real GDP growth Euro Area real GDP

1.7

Q3-2016

Q2-2016

Q1-2016

1.6

1.6

Source: Círculo de Empresarios based on Eurostat, OECD, 2016

Q3 GDP 2015, by countries(%)

+0.7 +0.3

(+0,8% T2) (+0,4% T2)

+0.5

(+0,7% T2)

+0.2(0% T2 )

+0.1(0% T2)

More ECB

measures

21

Eurozone

PMI’s showed economic expansion

Source: Círculo de Empresarios based on Eurostat, OECD, 2016

GERMANY

55SPAIN

53.3FRANCE

51.l8ITALY

50.9PMI > 50 = Expansion

PMI< 50 = Contraction

53.5

Eurozone Average

22

Unemployment rate by countries% labour force

Source: Círculo de Empresarios based on Eurostat, 2016

Eurozone: Labour market

Lowest rate recorded since July 2011

Youth unemployment

20.7%

Long-term unemployment*

51.5%

* > 12 months

23,2

18,91

10,8 11,510 9,9

7,78,6 8,4 7,9

5,7 6,2

4,1

0

5

10

15

20

25

23

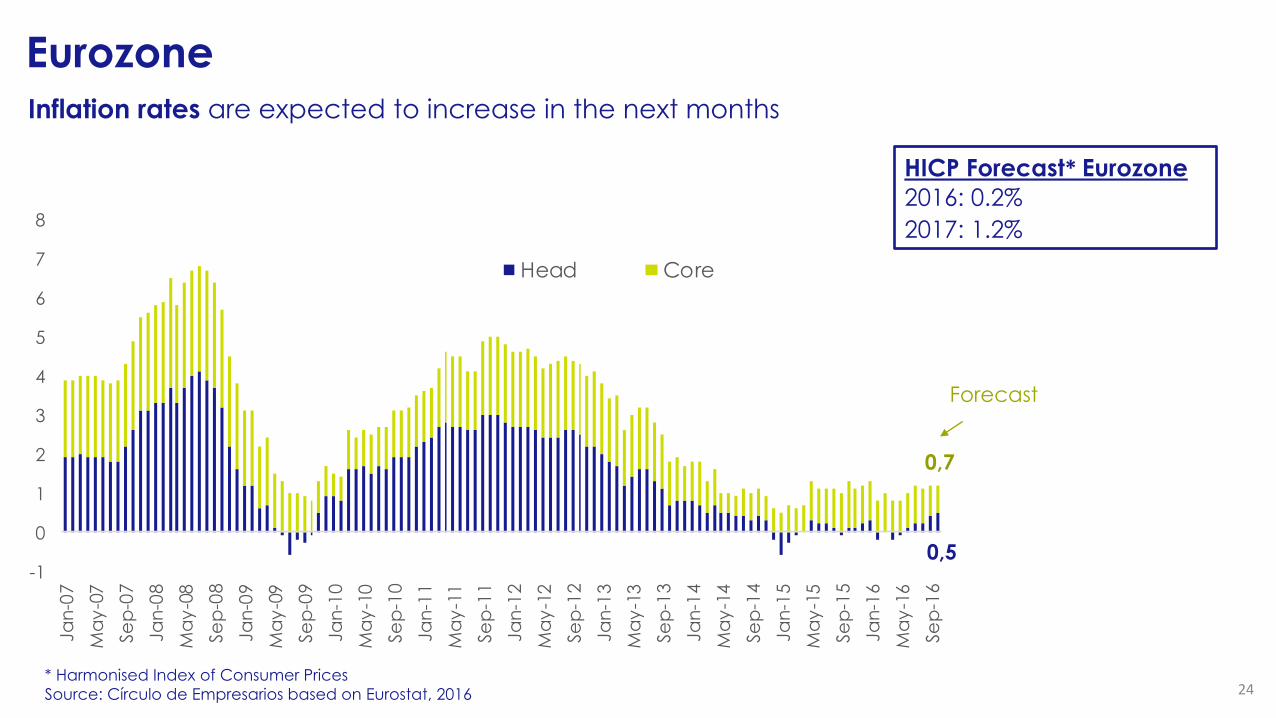

EurozoneInflation rates are expected to increase in the next months

* Harmonised Index of Consumer Prices

Source: Círculo de Empresarios based on Eurostat, 2016

Forecast

HICP Forecast* Eurozone

2016: 0.2%

2017: 1.2%

0,5

0,7

-1

0

1

2

3

4

5

6

7

8

Ja

n-0

7

Ma

y-0

7

Se

p-0

7

Ja

n-0

8

Ma

y-0

8

Se

p-0

8

Ja

n-0

9

Ma

y-0

9

Se

p-0

9

Ja

n-1

0

Ma

y-1

0

Se

p-1

0

Ja

n-1

1

Ma

y-1

1

Se

p-1

1

Ja

n-1

2

Ma

y-1

2

Se

p-1

2

Ja

n-1

3

Ma

y-1

3

Se

p-1

3

Ja

n-1

4

Ma

y-1

4

Se

p-1

4

Ja

n-1

5

Ma

y-1

5

Se

p-1

5

Ja

n-1

6

Ma

y-1

6

Se

p-1

6

Head Core

24

BREXIT

Source: Círculo de Empresarios based on Eurostat, OECD, 2016

Less impact than expected in financial markets but Brexit uncertainty remains

High degree of uncertainty about the exit process will reduce

investment in the next months

Brexit

Since the referendum, the poundplunged 15% and will push inflation up

to 0.7% in 2016 and 2.5% in 2016

BOE cuts

interest rates

to 0.25%

1,15

1,25

1,35

1,45

1,55

1,65

GBP/USD

25

BREXIT2017 GDP growth projections revised downwards

•EuropeanCommission

• BBVA

Research

• OECD• IMF

1,1

(2,2)

1

(2)

1,1

(1.9)

0,4

(1.9)

Source: Círculo de Empresarios based on IMF OECD, BBVA Research, S&P, Fitch, Moody`s, 2016

Note: In brackets pre-Brexit forecast

AA1 (negative)

AA1 (stable)

AA (negative)

AAA (negative)

AA+ (stable)

AA (negative)

Moody`s

S&P

Fitch

Before-Brexit

After Brexit

Ratings agencies credit score%

26

Commodities

Source: Círculo de Empresarios based on World Bank, 2016

World Bank forecasts

2016

43 $

2017

55 $

20

25

30

35

40

45

50

55

Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16

WTI evolution, 2016$

Oil Price increases after OPEC meeting in Algeria*

Upturn to $51 after OPEC agreement (1/3 of global

production) to reduce supply

* Uncertainty over the intention of cutting OPEC production in 1 mbd

27

Commodities

Source: Círculo de Empresarios based on IMF, 2016

Commodity prices evolution2005=100

Gradual increase of commodity prices

50

90

130

170

210

250

290 Total Non-fuel Energy Metals

28

Foreign Exchange market

Source: Círculo de Empresarios a based on Bloomberg, 2016

Change since 2016 against $%

-18,4

-15

-6,9

-4,5

-1,0

0,3

3,5

3,6

12,5

15,0

20,5

Argentine peso

Pound sterling

Turkish lira

Chinese yuan

Indian rupee

Euro

Australian dollar

Canadian dollar

Japanese yen

Russian ruble

Brazilian real

29

8,27,13

4

0,67

-0,06-1,17 -1,21

-2,1

-5

-8

-6

-4

-2

0

2

4

6

8

10

Shanghai

Composite

(China)

Ftse 100 (UK) Nikkei

(Japan)

Dax

(Germany)

Ibex 35

(Spain)

S&P 500 (US) Cac 40

(France)

Eurostoxx 50 FTSE MIB

(Italy)

Financial markets

Source: Círculo de Empresarios based on Bloomberg, 2016

-8,6

After temporary instability due to Brexit, Central Banks cause concern in stock markets

Brexit-3 Nov 2016

30

▼ Oil prices

▼Financial costs

Depreciation of the €

´Expansive fiscal policy

Growth boosts

1

2

3

56

Job creation

▲Exports to EU market

Domestic demand

4

7

32

At a moderate pace...

Remain broadly stable...

Forecasts: the recovery continues…

2017 2018

2.3%

2.1%

Source: Bank of Spain, Sept. 2016

… but at a moderate pace

3.2%

2016

The IMF has revised its forecasts upward for 2016 up to 3.1%

33

Forecasts 2016: composition of growth

GDP annual growth in 2016 = 3.2%

• Private consumption= 3.4%*

• Public consumption = 1%*

• GFCF = 4%*

* % annual change

• Exports = 5.3%*

• Imports = 5.4%*

* % annual change

Domestic demand

0.1 pp

3.1 pp

External demand

contribution to growth

contribution to growth

Source: Círculo de Empresarios, based on Bank of Spain data, Sept. 2016

34

Goods and services

Goods and services

GDP forecasts 2016 by regions% annual change

Galicia

2.7%

Asturias

2.6%

Cantabria

2.5%

Basque C.

2.7%

La Rioja

3.2%

Navarre

2.9%

Aragon

3.4%

Catalonia

3.3%

Valencian C.

3.3%

Murcia

3.4%

Andalusia

2.9%

Balearic I.

3.7%

Canary I.

3.2%

Extremadura

2.8%

Castile and Leon

2.7%

Madrid

3.5%

Castile-La Mancha

3.3%

Source: Círculo de Empresarios, based on BBVA Research, 2016

2.4 – 2.7%

≥ 3.3%

2.8 – 3.2%

Tourism and private consumption

boost growth in Canary Islands,

Balearic Islands, the East region and

Madrid

35

GDP growth

Domestic demand supports growth

Private consumption and investment

lead Spanish recovery

Despite national and internacional

uncertainties, Spain doubles OECD

and Eurozone growth rates

After 5 quarters, the external

demand contribution to growth has

become positive

36

3.2

-8

-6

-4

-2

0

2

4

6

2Q

200

7

3Q

200

7

4Q

200

7

1Q

200

8

2Q

200

8

3Q

200

8

4Q

200

8

1Q

200

9

2Q

200

9

3Q

200

9

4Q

200

9

1Q

201

0

2Q

201

0

3Q

201

0

4Q

201

0

1Q

201

1

2Q

201

1

3Q

201

1

4Q

201

1

1Q

201

2

2Q

201

2

3Q

201

2

4Q

201

2

1Q

201

3

2Q

201

3

3Q

201

3

4Q

201

3

1Q

201

4

2Q

201

4

3Q

201

4

4Q

201

4

1Q

201

5

3Q

201

5

3Q

201

5

4Q

201

5

1Q

201

6

2Q

201

6

3Q

201

6

GDP (annual change) and contribution of domestic and external demand (pp)

Domestic demand

External demand

GDP Spain

GDP Eurozone

GDP OECD

Source: Círculo de Empresarios, based on NSI, Bank of Spain and OECD data, 2016

Productivity and competitiveness

From 2014, low increase in productivity by

employee

37

Spain loses competitiveness in terms of

unit labour costs, converging towards

Eurozone average

0,9

2,9

1,8

1,7

1,5 1,3 0,4 0,3

-6,0

-5,0

-4,0

-3,0

-2,0

-1,0

0,0

1,0

2,0

3,0

4,0

2008 2009 2010 2011 2012 2013 2014 2015

GDP by employee 2008-2015

% annual change

Eurozone

Germany

Spain

Source:OECD, 2016

5,9

1,6

-1,6

-0,9

-2,8

-0,1

-0,9

0,2

-4,0

-2,0

0,0

2,0

4,0

6,0

8,0

2008 2009 2010 2011 2012 2013 2014 2015

Unit labour costs 2008-2015

% annual change

Germany

Eurozone

Spain

Source:OECD, 2016

Labour market

SEPE data – Oct. 2016:

▲ unemployed = 44,685 vs. Sep.

▲ affiliates = 101,335 vs. Sep.

▲ registered contracts = 1,867,360

Unemployment rate in Spain 3Q 2016 = 18.91% (EPA, NSI) vs. eurozone average = 10% (Eurostat)

38

16.393.866

17.813.356

4.763.680

3.764.982

0

1.000.000

2.000.000

3.000.000

4.000.000

5.000.000

6.000.000

16.000.000

16.500.000

17.000.000

17.500.000

18.000.000

18.500.000

19.000.000

19.500.000

20.000.000

2007

2008

2009

2010

2011

2012

2013

2014

2015

Jan

-16

Feb

-16

Ma

r-16

Ap

r-16

Ma

y-16

Jun

-16

Jul-16

Au

g-1

6Se

p-1

6O

ct-

16

Affilia

tes

Evolution of affiliation to Social Security and registered unemployed

Persons

Affiliates

Unemployed

Un

em

plo

ye

d

Source: Círculo de Empresarios based on Ministry of Employment data, Nov. 2016

Duality in the labour market

39

Temporary rate = 27% of dependent

employment (vs. 35% before 2008)

3Q 2016 → 46.7% of new job were permanent (vs.

33.2% in 2015)

154.900

-545.300

350.400

-600.000

-500.000

-400.000

-300.000

-200.000

-100.000

0

100.000

200.000

300.000

400.000

Ma

r-09

Jun

-09

Se

p-0

9

De

c-0

9

Ma

r-10

Jun

-10

Se

p-1

0

De

c-1

0

Ma

r-11

Jun

-11

Se

p-1

1

De

c-1

1

Ma

r-12

Jun

-12

Se

p-1

2

De

c-1

2

Ma

r-13

Jun

-13

Se

p-1

3

De

c-1

3

Ma

r-14

Jun

-14

Se

p-1

4

De

c-1

4

Ma

r-15

Jun

-15

Se

p-1

5

De

c-1

5

Ma

r-16

Jun

-16

Se

p-1

6

Permanent employment

Annual change, number of employees

Source:Círculo de Empresarios, based on NSI data, 2016

32

27

22

23

24

25

26

27

28

29

30

31

32

Ma

r-07

Se

p-0

7

Ma

r-08

Se

p-0

8

Ma

r-09

Se

p-0

9

Ma

r-10

Se

p-1

0

Ma

r-11

Se

p-1

1

Ma

r-12

Se

p-1

2

Ma

r-13

Se

p-1

3

Ma

r-14

Se

p-1

4

Ma

r-15

Se

p-1

5

Ma

r-16

Se

p-1

6

Temporary rate

% of dependent employment

Source: Círculo de Empresarios based on NSI data, 2016

Youth unemployment and NEETs by regions 2016% population between 15-29 years, 4Q 2015

Catalonia35.15%

18.4%

Valencian C.42.53%

18.6%

Murcia44.22%

22.5%Andalusia55.18%

24.1%

Balearic I.27.1%

19.6%

Canary I.51.42%

24.2%

Source: Círculo de Empresarios, based on NSI and Ministry of Employment data, 2016

< 40 %

50 ≥ %

40 – < 50 %

Galicia37.61%

16.4%

Asturias47.02%

17.8%

Cantabria29.32%

14.7%

Basque C.39.73%

12.8%

La Rioja35.48%

17.6%

Navarre32.53%

12.3%

Aragon39.23%

16.6%

Extremadura49.06%

23.3%

Castile and Leon34.14%

15.4%

Madrid37,75%

16%

Castile-La Mancha47.46%

22.4%

SPAIN

Youth unemployment:

41.94%

NEETs: 19.4%

40

Andalusia

Canary I .

Asturias

Extremadura

Castile-La

Mancha

Valencian C.

SPAIN

La Rioja

Murcia

Madrid

Galicia

Navarre

Castile and

Leon

Cantabria

Balearic I .

Aragon

basque C.

Catalonia

10

15

20

25

35 40 45 50 55 60

Youth unemployment and NEETs by regions, 2016

NEETs

%p

op

ula

tio

n 1

5-2

9 y

ea

rs

Youth unemployment

% total unemployment

Prices

In October 2016:

Interannual CPI increases to 0.7%,

mainly because the rise in energy prices

Above the average of the Eurozone

41

0.7 % (Oct)

0.8 % (Sep)

0.5 % (Oct)

-1,5

-1

-0,5

0

0,5

1

1,5

201

6M

10

201

6M

09

201

6M

08

201

6M

07

201

6M

06

201

6M

05

201

6M

04

201

6M

03

201

6M

02

201

6M

01

201

5M

12

201

5M

11

201

5M

10

201

5M

09

201

5M

08

201

5M

07

201

5M

06

201

5M

05

201

5M

04

201

5M

03

201

5M

02

201

5M

01

201

4M

12

201

4M

11

201

4M

10

201

4M

09

201

4M

08

201

4M

07

201

4M

06

General and core inflationAnnual change %

CPI Spain

Core inflation Spain *

CPI Eurozone

* without energy and non-processed food

Source:Círculo de Empresarios, based on NSI and Eurostat data, Oct. 2016

Financial conditions

Credit increases mainly in consumption

and agriculture

Default rate falls down while it is still

high in the construction and

developer sectors

42

Credit and default rate in Spain 2Q 2016

Bn € and %

Balance

2Q 2016

Annual

changeDefault rate

Households (housing) 544 -3,6 4,7

Households (consumption) 121 4,5 8,1

Productive activities 614 -7,2 14

Construction 42 -9,8 29,6

Developer 125 -9,8 26,9

Serv ices 319 -8,7 8,7

Industry 110 -0,2 9,5

Agriculture 19 6,3 9,1

Total* 1.279 -4,6 9,4

Source: CaixaBank based on Bank of Spain data, 2016

Public accounts – revenues, expenditures and balance

AIReF → the target of déficit for 2016 may be achieved = 4.6% of GDP

Estimated balance for 2016:

43

o Central Administration= - 2.2% of GDP

o Social Security = - 1.6% of GDP

o Autonomous Regions = - 0.8% of GDP

o Local units = + 0.4% of GDP

General Administration deficit Jan.-Aug. 2016 (without local units and

financial aid) = 3.3% of GDP

5,14,0

2,9 3,2 3,23,7

4,2 3,8

1,1

-3,6

0,0

-1,0

-2,6-1,7

1,4

3,2

-1,0-0,5 -0,4 -0,4 0,0

1,22,2 2,0

-4,4

-11,0

-9,4 -9,6-10,4

-6,9-5,9

-5,1

30

32

34

36

38

40

42

44

46

48

50

-12

-10

-8

-6

-4

-2

0

2

4

6

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Public revenues and expenditures

% GDP GDP growth Balance

Revenues Expenditures

Source: IMF, 2016

-1,5

-1

-0,5

0

0,5

1

Autonomous regions balance, Aug. 2016

% GDP

Source: Círculo de Empresarios based on Ministry of Finance data, 2016

Public and private debt

Public debt goes on increasing, 0.7% since 2Q 2015, above 100% of GDP

Households and companies reduce their debt at a more moderate pace

44

58,054,2

51,347,6

45,342,3

38,935,5

39,4

52,7

60,1

69,5

85,7

95,4100,4

99,8

101,2

101,0

2000200120022003200420052006200720082009201020112012201320142015 1Q

2016

2Q

2016

PPAA debt

%

Source: Bank of Spain, 2016

0

20

40

60

80

100

120

140

160

180

-10

-8

-6

-4

-2

0

2

4

6

8

10

Gross public debt 2Q 2016

% GDP and annual change% GDP 2Q 2016

Annual change

Source: Círculo de Empresarios based on Eurostat data, 2016

300.000

500.000

700.000

900.000

1.100.000

1.300.000

1.500.000

Se

p-0

7D

ec

-07

Ma

r-08

Jun

-08

Se

p-0

8D

ec

-08

Ma

r-09

Jun

-09

Se

p-0

9D

ec

-09

Ma

r-10

Jun

-10

Se

p-1

0D

ec

-10

Ma

r-11

Jun

-11

Se

p-1

1D

ec

-11

Ma

r-12

Jun

-12

Se

p-1

2D

ec

-12

Ma

r-13

Jun

-13

Se

p-1

3D

ec

-13

Ma

r-14

Jun

-14

Se

p-1

4D

ec

-14

Ma

r-15

Jun

-15

Se

p-1

5D

ec

-15

Ma

r-16

Jun

-16

Se

p-1

6

Non-financial sectors debtMillions of € PPAA

Non-financial companies

Households

Source:Bank of Spain, Nov. 2016

Exports of goods

January – August 2016 (annual change)

▲ 1.3% (167,053.6 M€)

Imports of goods ▼ -1.6% (178,049.9 M€)

Trade balance ▼ 31.6% del DEFICIT (-10,996.3 M€)

▼ 42.4% in energy deficit

Geographical distribution (%)TO

P 3

SEC

TOR

S

Exp

ort

sIm

po

rts

Source: Círculo de Empresarios, based on Ministry of Economy, Oct. 2016

External sector

45

Exportaciones % / total Importaciones % / total

Bienes de equipo 20,2 Bienes de equipo 21,6

Automóvil 17,9 Productos químicos 16

Alimentación, bebidas y

tabaco17,1 Automóvil 14

-94.159,9-24.173,9 -10.996,3

-100.000

-50.000

0

50.000

100.000

150.000

200.000

250.000

300.000

Evolución exportaciones, importaciones y saldo comercialMillones €

Exportaciones

Importaciones

Saldo

EUROPE72

EU

66,3

AMERICA10,5

ASIA9,4

AFRICA6,3

OTHER1,8

Exports

EUROPE62,6

EU

56,9

ASIA19,7

China8,8

AMERICA10,1

AFRICA7,3

OTHER0,3

Importaciones

Interet rates and risk premium

Brexit → German bond in negative values

Risk Premium has recovered to 2015 March levels

46

0

20

40

60

80

100

120

140

160

180

-0,5

0

0,5

1

1,5

2

2,5

3

3,5

Ten years bond yield. Spain adn Germany (%)Risk premium (bp)

Spain

Germany

Risk premium

Source: Círculo de Empresarios based on Bank of Spain data, 2016

Risk premiumInterest rate

Enterprise creation

Enterprise creation rate 2007 - 2Q

2016:

In Spain it remains below pre-crisis

rates at 28.5%.

In the United Kingdom, it has

increased by 31%.

47

-40

-30

-20

-10

0

10

20

30

40

Enterprise creation. Difference between 2007-2016

%

Source: OECD, 2016

Ibex 35

48

7.500

7.700

7.900

8.100

8.300

8.500

8.700

8.900

9.100

9.300

Source: Investing, 2016

Brexit

(23 Jun)

Elections USA

↑ Trump

(1 Nov)

Spain´s position in international rankings

Finland

Canada

Denmark

SPAIN

49

Hong Kong

Singapore

SPAIN

1

2

3

Health Care Efficiency Index 2016 Data 2014 (55 countries)

Source: Bloomberg, 2016

▲5(vs. 2009)

USA

Canada

Australia

SPAIN

1

2

3

12

Telefónica Index on Digital Life 2016 (34 countries)

Source: Telefónica, 2016

---(1st edition)

1

2

3

17

2016 Social Progress Index(130 countries)

Source: Social Progress Imperative

(Deloitte, Avina, Skoll), 2016

▲3(vs. 2015)

Estonia

New Zealand

Latvia

SPAIN

1

2

3

28

International Tax Competitiveness

Index 2016 (135 countries)

Source: Tax Foundation, 2016

▲1(vs. 2015)

Switzerland

Singapore

USA

SPAIN

1

2

3

32

Global Competitiveness Index

2016-17 (138 countries)

Source: IMD, 2016

▲1(vs. 2015-2016)

New Zealand

Singapore

Denmark

SPAIN

1

2

3

32

Doing Business 2017 (190 countries)

Source: World Bank, 2016

▲1(vs. 2016)

www.circulodeempresarios.org