Quality at every step. - Polaris Bank Limited

187

Transcript of Quality at every step. - Polaris Bank Limited

Qualityat everystep.

MISSION

We will leverage our

knowledge of an ever -

changing world to

design innovative

solutions that

facilitate our customers'

enterprise

VISION

To be the preferred partner

providing superior financial

solutions for our customers

VALUES

Boldness

Sustainability

Innovative

Continous Learning

Trustworthy

POLARIS BANK ANNUAL REPORT & FINANCIAL STATEMENTS 2019

4

TABLE

of contents

NOTICE OF ANNUAL GENERAL MEETING 5

RESULTS AT A GLANCE 6

DIRECTORS AND ADVISERS 7

CORPORATE GOVERNANCE REPORT 9

SUSTAINABILITY REPORT 17

CHAIRMAN’S STATEMENT 26

MANAGING DIRECTOR’S STATEMENT 31

PROFILE OF DIRECTORS 39

REPORT OF THE DIRECTORS 44

REPORT OF THE INDEPENDENT CONSULTANT 47

STATEMENT OF DIRECTORS' RESPONSIBILITIES 48

INDEPENDENT AUDITOR’S REPORT 50

STATEMENT OF COMPREHENSIVE INCOME 56

STATEMENT OF FINANCIAL POSITION 57

STATEMENT OF CHANGES IN EQUITY 58-61

STATEMENT OF CASHFLOWS 62

NOTES TO THE FINANCIAL STATEMENTS 63-156

MANAGEMENT TEAM 159

PRODUCTS & SERVICES 162-174

CORPORATE DIRECTORY 176-182

PROXY FORM 183

POLARIS BANK ANNUAL REPORT & FINANCIAL STATEMENTS 2019

5

Date: May 28, 2020

Venue: The Head Office, Polaris Bank Limited 3, Akin Adesola Street, Victoria Island, Lagos.

Time: 11:00a.m.

ORDINARY BUSINESS

The following businesses will be transacted at the meeting as ordinary businesses:

1. To receive and consider the Audited Financial Statements for the period from September 21 to December 31,2018 and year

ended December 31,2019, together with the Reports of the Directors and Auditors, respectively

2. To re-elect Directors.

3. To appoint Messrs. PricewaterhouseCoopers as the Bank's Auditors.

4. To authorize the Directors to fix the remuneration of the Auditors.

SPECIAL BUSINESS

The following business will be transacted at the meeting as a special business:

5. To fix the Directors' fees for the year ending December 31, 2020 .

PROXY

A person entitled to attend and vote at the meeting is entitled to appoint a proxy to attend and vote in his / her stead. A proxy need not

be a member of the company. To be valid, the proxy form must be duly signed by the shareholder and stamped at the Stamp Duties

office and returned to the Company Secretariat of the Bank at 3, Akin Adesola Street, Victoria Island, Lagos, not less than 48 hours

before the date and time scheduled for the meeting.

NOTICE OF

annual generalmeeting

NOTICE IS HEREBY GIVEN to you that the Annual General Meeting of

Polaris Bank Limited will hold as follows:

BY THE ORDER OF THE BOARD

BABATUNDE OSIBODUGENERAL COUNSEL/COMPANY SECRETARYFRC/2016/NBA/000000154643, Akin Adesola Street, Victoria Island, Lagoswww.polarisbanklimited.com

POLARIS BANK ANNUAL REPORT & FINANCIAL STATEMENTS 2019

6

RESULTS AT A

glance

GROSS EARNINGS PROFIT BEFORE TAX PROFIT AFTER TAX

N150.36 billion N27.34 billion N26.29 billion

(All amounts in millions of Naira unless otherwise stated)

31 December

2019

21 September - 31

December

2018

31 December

2019

21 September - 31

December

2018

Major Income Statement items

Gross Earnings 150,361 37,392 150,848 37,392

Profit Before Tax 27,342 2,456 27,829 2,456

Profit After Tax 26,290 2,856 27,350 2,431

31 December

2019

31 December

2018

31 December

2019

31 December

2018

Major Statement of Financial Position items

Loans and Advances to customers 188,738 340,050 188,738 340,050

Deposits from customers 857,885 861,044 857,885 861,044

Total Assets 1,156,644 1,168,658 1,143,266 1,150,095

Total Liabilities 1,069,754 1,109,901 1,060,277 1,097,133

GROUP BANK

GROUP BANK

POLARIS BANK ANNUAL REPORT & FINANCIAL STATEMENTS 2019

7

DIRECTORS AND

advisersDIRECTORS APPOINTED BY CENTRAL BANK OF NIGERIA

DIRECTOR CAPACITY

1 Mr. Muhammad K. Ahmad, OON Chairman/Non-Executive Director

2 Mr. Adetokunbo M. Abiru Managing Director/CEO

3 Alhaji Abdullahi M. Umar Non-Executive Director

4 Mr. Austin E. Jo-Madugu Non-Executive Director

5 Mr. Bata G. Wakawa Non-Executive Director

6 Mr. Olu O. Odugbemi Non-Executive Director

7 Mr. Abdullahi S. Mohammed Executive Director

8 Mr. Innocent C. Ike Executive Director

GENERAL COUNSEL/

COMPANY SECRETARYMr. Babatunde Osibodu

FRC/2016/NBA/00000015464

REGISTERED OFFICE 3, Akin Adesola Street, Victoria Island,

Lagos

WEBSITE www.polarisbanklimited.com

TELEPHONE +(234) -1- 2701600

Landmark Towers

5B Water Corporation Drive,

Victoria Island, Lagos

www.pwc.com/ng

AUDITORS

PricewaterhouseCoopers

(Chartered Accountants)

CORPORATE GOVERNANCE REPORT

8

POLARIS BANK ANNUAL REPORT & FINANCIAL STATEMENTS 2019

9

As a private limited liability company, the Bank is required to

adhere to the CBN Code of Corporate Governance for Banks and

Discount Houses in Nigeria 2014, and more recently, the new

Nigerian Code of Corporate Governance 2018. As it continues to

institutionalise sound Corporate Governance, the Bank remains

committed to ensuring compliance with these Corporate

Governance regulations as well as other best practices.

Board Structure & Composition

The Board of Polaris Bank was appointed at the inception of the

Bank on September 21, 2018. As at December 31, 2019, the Board

was composed of eight (8) members. Five (5) of them were Non-

Executive Directors (NEDs) including the Chairman and the other

three (3) were Executive Directors (EDs), including the Managing

Director/Chief Executive Officer. Its members have varied

experiences in Finance and Accounting, Banking, Public Service,

Strategy & Innovation, Business Entrepreneurship, Risk

Management and Governance amongst others.

The positions of the Chairman and the Managing Director are

separate and held by two individuals, thereby ensuring that no

one individual has unfettered powers of decision making. The

Chairman provides overall leadership and direction to the Board.

His primary responsibility is to ensure effective operation of the

Board towards achieving the Bank’s strategic objectives,

including enhancing shareholder value. The Managing

Director/Chief Executive Officer is the Head of Management and

is responsible for the day-to-day management of the Bank

toward achieving its corporate objectives.

Furthermore, in the interest of safeguarding the objectivity and

independence of the Board, there are no two members of the

same family on the Board concurrently.

No changes took place in the structure of the Board during the

2019 Financial Year.

Roles and Responsibilities of the Board

The Board provides leadership and vision to the Company in a

manner that will enhance Shareholder value and ensure that the

Bank’s long-term vision is realised. Some decisions are reserved

for the Board, such as approval of corporate strategy and annual

budgets, approval of policies, risk management strategy,

succession planning and the appointment , training,

remuneration and replacement of Board members and senior

Management amongst others. The roles and responsibilities of

the Board are outlined below:

CORPORATE

governance reportFOR THE YEAR ENDED 31 DECEMBER 2019

A culture of alignment with sound Corporate Governance practices is pivotal to the success,and survival of an enterprise. Polaris Bank recognises this, and therefore ensures thatthere are effective governance policies, practices and structures in place to guide theaffairs of the enterprise. The activities of the organisation, including oversight byManagement and the Board of Directors are carried out in a manner consistent with theCorporate Governance principles of Fairness, Probity, Accountability, Responsibility, andTransparency.

The Chairman provides overall leadership and direction to the Board.

POLARIS BANK ANNUAL REPORT & FINANCIAL STATEMENTS 2019

10

. Defining levels of materiality, reserving specific powers

to itself and delegating other matters within authority

to Management;

. Retention of full and effective control over the Bank

and monitoring Management’s implementation of

Board plans and strategies;

. Ensuring ethical behaviour and compliance with

relevant laws and regulations, audit and accounting

principles, and the Bank’s governing documents;. Striving to act above and beyond the minimum

requirements and benchmark of international best

practices;

. Ensuring a healthy balance of the interests of all the

Bank’s relevant stakeholders;

. Being aware of, and committing to, the underlying

principles of good governance; and

. Approval of specific financial and non-financial

objectives and policies proposed by Management.

Appointment, Induction and Training of Board Members

The criteria for the appointment of members to the Board are laid

down in the Board Succession Planning Policy which is a formal,

transparent and rigorous process. New members are selected

based on their wealth of experience, relevant leadership skills,

integrity, meeting the fit and proper person criteria and

competence amongst others . The process of Board

appointments is not concluded until the nominees are duly

appointed/approved by the Central Bank of Nigeria (CBN) and

ratified by Shareholders in general meeting

Upon appointment to the Board, Directors are taken through a

formal induction process which is anchored by the Company

Secretary. The induction process is targeted at facilitating their

understanding of the Bank and the environment and markets in

which it operates. As part of the induction programme, Board

members are provided access to various materials such as

corporate information of the Bank, Minutes of Board and Board

Committee meetings, as well as Annual Reports and Accounts.

This is then followed by interactive sessions with key Senior

Management staff to deepen the Directors’ understanding of the

materials provided.

The Bank appreciates the crucial importance of continuous

learning to the effectiveness of the Board in the discharge of its

functions. Board members are therefore provided with relevant

training programmes.

Board Evaluation

In line with Corporate Governance regulations and best practices

in Corporate Governance, the Bank has a formal process for the

evaluation of the Board. Annually, an independent consultant is

engaged to conduct a performance evaluation of the Board as a

whole, its Committees, the Chairman and individual Directors.

The appraisal process involves a benchmark of the Bank’s

existing governance documentation, structure and practices,

with relevant Corporate Governance regulations and best

practices to enable the identification of governance gaps, one-

on-one interview sessions with the Directors, 360 degree

appraisal process for directors, and feedback sessions with the

Chairman, the Chief Executive Officer and the Company

Secretary.

The Board has engaged an independent consultant, KPMG

Professional Services, to carry out the annual Board and

Individual Performance Appraisal for the 2019 financial year.

The report of the Appraisal will be presented to the Bank’s

shareholders, and a copy will be sent to the Central Bank of

Nigeria (CBN) in line with regulation.

Shareholders

Polaris Bank is a private limited liability company, wholly owned

by the Assets Management Corporation of Nigerian, an agency of

the CBN.

The Board and Management of the Bank ensures an open line of

communication and full disclosure of all matters relating to the

Bank’s operations to AMCON and obtains approval of the agency

where required. The first Annual General Meeting (AGM) of the

Bank will be held in May 2020.

The Company Secretary

The Company Secretary is accountable to the Board as a whole

and advises the Board through the Chairman and the Managing

Director on all matters of governance, including their duties. He

ensures that the Board receives relevant information, including

agenda and documents for consideration at the Board and

Board Committee meetings. The Company Secretary ensures

that the Bank is in compliance with all regulatory and statutory

requirements.

CORPORATE GOVERNANCE REPORT

POLARIS BANK ANNUAL REPORT & FINANCIAL STATEMENTS 2019

11

Board Meetings

At the beginning of each financial year, meetings of the Board,

and its Committees are scheduled in advance for the entire year.

The agenda for each meeting and the supporting Board papers

are sent to Directors at least 7 days before the meeting to provide

them sufficient time to review the papers and request for

additional information, where necessary. For review at Board

meetings, the members receive reports on the implementation

of the corporate strategy and the financial performance of the

Bank. Directors have access to Management through the

Company Secretariat and take independent advice from

Consultants where required. The Board operates as a cohesive

team; thus, decisions are reached by consensus.

The membership of the Board during the 2019 financial year is as

shown below:

During the year, there were six (6) meetings of the Board of

Directors on January 24, March 6, May 7, August 8, November 7,

and December 12. The Board recorded 100% membership

attendance at these meetings as ALL Directors were present..

Board Committees

The Board Committees of the Bank as at December 31, 2019 were

as follows:

• Board Governance, Nominations & Compensation

Committee • Board Credit Committee • Board Finance & General Purposes Committee • Board Audit & Risk Management Committee

Board Governance, Nominations & Compensation

Committee (BGNCC)

The Committee is established to assist the Board in carrying out

its oversight responsibility with respect to the Bank’s compliance

with corporate governance best practices, nominations to the

Board, and implementation of appropriate compensation for the

Bank’s staff as well as Board members. The major terms of

reference of the Committee are:

• Assisting the Board in the identification of people

e l i g i b l e t o b e c o m e B o a r d m e m b e r s a n d

recommending the director nominees for approval.

• Recommending to the Board corporate governance

best practices applicable to the Bank and monitoring

compliance by the Bank with the approved corporate

governance codes and guidelines.

• Assisting the Board in fulfilling its responsibility with

respect to the design and implementation of

appropriate compensation and remuneration

packages for Directors.

• Assisting the Board in fulfilling its responsibility with

respect to the design and implementation of strategic

Human Capital Management policies, including

compensation and remuneration packages for staff.

• Coordinating the annual Board performance

evaluation; and

• Reviewing Board Committee Charters in collaboration

with the respective Committees and making

appropriate recommendations for changes,

periodically.

*The membership of the Committee during the 2019 Financial

year is as shown below:

During the 2019 financial year, there were seven (7) meetings of

the BGNCC on January 21, January 24, April 29, July 30,

September 6, October 29 and December 10. The Committee

recorded 100% attendance at these meetings as its Chairman

and ALL members were present.

*The MD/CEO is in attendance at the Committee's meetings.

CORPORATE GOVERNANCE REPORT

1. Mr. Muhammad K. Ahmad (OON) Chairman

2. Mr. Adetokunbo M. Abiru Managing Director/CEO

3. Mr. Abdullahi S. Mohammed Executive Director

4. Mr. Innocent C. Ike Executive Director

5. Alhaji Abdullahi M. Umar Non-Executive Director

6. Mr. Austin E. Jo-Madugu Non-Executive Director

7. Mr. Bata G. Wakawa Non-Executive Director

8. Mr. Olu O. Odugbemi Non-Executive Director

NAME CAPACITY

1. Mr. Austin E. Jo-Madugu Non-Executive Director (Chairman)

2. Mr. Bata G. Wakawa Non-Executive Director

3. Mr. Olu O. Odugbemi Non-Executive Director

NAME CAPACITY

POLARIS BANK ANNUAL REPORT & FINANCIAL STATEMENTS 2019

12

Board Credit Committee (BCC)

The Committee is established to assist the Board in carrying out

its oversight responsibility with respect to the Bank’s credit policy

and reviewing all credits in excess of the limits delegated to

Management. It also recommends those above its approval limit

to the Board for approval. The major terms of reference include

the following:

• Reviewing the Bank’s Credit Policy, including defining

levels and limits of lending authority, and making

recommendations accordingly to the Board for

approval.

• Considering and approving credits in excess of

Management limits but within the limits set by the

Board and recommending those above its limit to the

Board for approval.

• Considering and approving all insider-related credit

applications, irrespective of the size, up to its approval

limit and recommending those above its limit to the

Board for approval.

• Considering and approving write-offs in excess of

Management limits but within the limits set by the

Board and recommending those above its limit to the

Board for approval.

• Monitoring loan quality through the review of quarterly

reports on facilities and potential loss forecasts.

• Reviewing fully provisioned loans and loan recovery

efforts from time to time.

• Approving credit guidelines for strategic plans and

projects.

The membership of the Committee during the 2019 financial year

is as shown below:

During the 2019 financial year, there were six (6) meetings of the

BCC on January 21, March 4, April 29, July 30, September 6, and

October 29. The Committee recorded 100% attendance at these

meetings as its Chairman and ALL members were present.

Board Finance & General Purposes Committee (BF&GPC)

The Committee is established to assist the Board in fulfilling its

oversight responsibilities with respect to strategic, financial and

corporate development matters. Its major terms of reference

include the following:

• Defining the strategic business focus and plans of the

Bank.

• Determining the policies, strategies and financial

objectives of the Bank, and overseeing and monitoring

the pursuit of these policies, strategies and financial

objectives.

• Overseeing the acquisition and disposal of any

significant asset or business of the Bank, subject to the

approval of the Board.

• Defining capital expenditure limits and approving all

capital expenditure within its limit and recommending

those above its limit to the Board for consideration and

approval.

• Reviewing and recommending to the Board for

approval, the procurement strategy and policy for the

Bank.

• Approving and recommending to the Board for

approval, the acquisition, establishment, disposal or

closure of any branch, business outlet of the Bank.

• Ensuring that all major contracts are carried out

according to the terms and conditions of the contract

agreements.

• Oversight responsibility in respect of the Bank’s

corporate strategy and material, financial and other

significant matters relating to the Bank’s annual

budget, capital investment policies, mergers and

acquisitions, and the Bank’s performance review, dra�,

amongst others.

The membership of the Committee during the 2019 financial year

is as shown below:

1. Mr. Bata G. Wakawa Non-Executive Director (Chairman)

2. Alhaji Abdullahi M. Umar Non-Executive Director

3. Mr. Austin E. Jo-Madugu Non-Executive Director

4. Mr. Adetokunbo M. Abiru Managing Director/CEO

5. Mr. Abdullahi S. Mohammed Executive Director

6. Mr. Innocent C. Ike Executive Director

NAME CAPACITY

1. Alhaji Abdullahi M. Umar Non-Executive Director (Chairman)

2. Mr. Austin E. Jo-Madugu Non-Executive Director

3. Mr. Olu O. Odugbemi Non-Executive Director

4. Mr. Adetokunbo M. Abiru Managing Director/CEO

5. Mr. Abdullahi S. Mohammed Executive Director

6. Mr. Innocent C. Ike Executive Director

NAME CAPACITY

POLARIS BANK ANNUAL REPORT & FINANCIAL STATEMENTS 2019

13

During the 2019 financial year, there were five (5) meetings of the

BF&GPC on January 22, April 30, July 31, September 6, and

October 30. The Committee recorded 100% attendance at these

meetings as its Chairman and ALL members were present.

Board Audit and Risk Management Committee (BARMC)

The Committee is established to assist the Board in fulfilling its

responsibility with respect of Audit & Risk Management. Its major

terms of reference include the following:

. Reviewing the integrity of the Bank’s financial

reporting and overseeing the independence and

objectivity of the external auditors.

• Assisting in the oversight of compliance with

regulatory requirements, and assessing qualifications

and independence of external auditor, as well as,

performance of the Bank’s internal audit function.

• Ensuring the development of a comprehensive

internal control framework for the Bank, providing

o v e rs i g h t o f M a n a ge m e n t ’s p ro ce s s fo r t h e

identification of significant fraud risks across the Bank

and ensuring that adequate prevention, detection and

reporting mechanisms are in place.

• Reviewing and recommending to the Board, the

appropriate risk management policy and framework,

including risk appetite and risk strategy, for the Bank.

• Ensuring the adequacy and effectiveness of risk

management and the controls in place, clearly

delineating the Bank’s overall risk tolerance level by

reviewing and approving risk limits.

• M o n i to r i n g a n d re v i e w i n g p e r i o d i ca l l y, t h e

implementation of the Bank’s risk management

strategy.

• Making recommendations on the appointment and

removal of the Chief Compliance Officer and the Chief

Internal Auditor.

*The membership of the Committee during the 2019 financial

year is as shown below:

During the 2019 financial year, there were four (4) meetings of the

BARMC on January 22, April 30, July 31, and October 30. The

Committee recorded 100% attendance at these meetings as its

Chairman and ALL members were present.

*The MD/CEO and other Executives are in attendance at the

Committee’s meetings.

In addition to their individual meetings, the BF&GPC and BARMC

also held joint meetings to consider matters such as the Bank’s

Budget and Accounts. The joint meetings were held on January

22 and December 10.

Remuneration of Directors

Only Non-Executive Directors are entitled to Directors’ Annual

Fees as well as Sitting Allowances for attendance at Board and

Committee meetings. Remuneration for Executive Directors

comprises a basic salary, allowances, performance incentive,

tied to the Bank’s performance.

The schedule of annual fees (excluding withholding tax at 10%)

paid to Non-Executive Directors for the year ended December 31,

2019 is as follows:

CORPORATE GOVERNANCE REPORT

1. Mr. Olu O. Odugbemi Non-Executive Director (Chairman)

2. Alhaji Abdullahi M. Umar Non-Executive Director

3. Mr. Bata G. Wakawa Non-Executive Director

NAME CAPACITY

S/N Fees & Allowances Amount

1. Annual Fee for Board Chairman N5m

2. Annual Fee for Non-Executive Directors N3.5m

3. Sitting Allowance for Board Committee Meetings N250,000

4. Sitting Allowance for Chairman of Board Committee Meetings N300,000

5. Sitting Allowance for Board of Directors Meetings N350,000

6. Sitting Allowance for Board Chairman N550,000

POLARIS BANK ANNUAL REPORT & FINANCIAL STATEMENTS 2019

14

Whistle-Blowing Policy

The Bank has established and implements a whistle-blowing

Policy which is an avenue for employees of the Bank,

stakeholders and the general public to report suspected or

known acts of fraud, malpractice, or other unethical activity.

The whistle-blowing framework includes a dedicated and active

email address to reach the Bank’s Chief Internal Auditor (CIA),

phone lines to the CIA and the CBN, and a conspicuous whistle-

blowing channel on the Bank’s website. Information on the

whistle blowing procedure is available to staff and customers

and also published in conspicuous places in the banking halls.

The whistle-blowing facility has the assurance of confidentiality

to protect the identity and interest of the whistle-blower. Periodic

reports on whistleblowing are presented to the Board of

Directors and sent to the CBN.

Disclosures

The Board has a policy of openness and transparency. Director-

related facilities are disclosed during consideration, and the

related party does not participate in the consideration of the

facility or remain in the Board room during the consideration. NoDirector of the Bank currently provides professional services to

the Bank.

During the 2019 Financial Year, the Bank incurred a CBN penalty

of N2million for delay in implementing two of the prior year's

recommendations from the external auditor's management

letter. The Bank was also fined the sum of N4million by the CBN

for writing-off interest portion of N2,067,685.00 on a legacy

insider-related loan to Onas Farms without prior CBN approval.

Management Committees

The Board delegates to Management, through the Managing

Director/CEO, all authority necessary for the day-to-day

management of the Bank. The Managing Director is the Head of

the Management team and has the discretion to request

Management Committees to take Management decisions and

actions that promote the corporate objectives of the Bank, with

due regard to Management’s limits as approved by the Board.

The Management Committees, composed of Management staff

selected according to their roles and responsibilities, all have

their Terms of Reference. Each Management Committee is

headed by a Chairman and has a Secretary appointed to perform

the secretarial functions for the Committee.

The standing Management Committees of the Bank are as

follows:

The Executive Committee (EXCO)

It is the highest-level Management Committee. It comprises the

Managing Director/CEO, as the Chairman, Executive Directors,

and Directorate Heads. Some of its Terms of Reference include:

• M a k i n g re co m m e n d a t i o n s o n t h e s t ra teg i c

development of the Bank in the areas of branch

expansion, branding and market presence.

• Considering of the financial performance of the Bank.

• Considering internal policies and processes and

making recommendations to the Board for approval.

• Considering the performance evaluation of staff and

issues of manpower planning, human capital and non-

human capital optimization.

• Ensuring that laid-down internal control procedures

are adequate and duly observed.

• Providing oversight function for the Bank’s accounting

and financial reporting, and its internal and external

audit.

• Reviewing the findings of any examination by

regulatory agencies, and any auditor observation,

including investigations.

• Monitoring and reviewing the effectiveness of the

Bank’s risk management systems and processes to

confirm its consistency with the Bank’s strategy and

business plan.

Assets & Liabilities Committee (ALCO)

The Committee is responsible for coordinating the Bank’s

borrowing and lending strategy, and funds acquisition to meet

profitability objectives as interest rates change. It monitors

actions by the regulators that may affect interest rates, and

impact of any policy change on the Bank’s business.

Criticized Assets Review Committee (CARC)

The Committee monitors the effectiveness and application of

credit risk management and ensures that all relevant

documentation pertaining to credit application and collateral

security are effected. It also reviews reports on challenged

accounts and oversees the development of loan loss provision

policy. It ensures that the systems established by Management to

identify credit risks, assess, manage and monitor loans are

operating effectively.

CORPORATE GOVERNANCE REPORT

POLARIS BANK ANNUAL REPORT & FINANCIAL STATEMENTS 2019

15

Tenders Committee (TC)

The Tenders Committee reviews the Bank’s tendering and

procurement policies and practices to ensure that the operating

policies and procedures relating to tendering and procurement

are recognised as “best practices”, and all Tenders are conducted

in a fair and ethical manner and that no conflict of interest exists

with any Director or employee connected to the tendering and

procurement process.

Disciplinary Committee (DC)

The Committee is responsible for considering complaints made

against staff members on matters relating to misconduct of staff,

in accordance with the Bank’s disciplinary framework. It also

r e v i e w s t h e D i s c i p l i n a r y R e g u l a t i o n s a n d m a k e s

recommendations for changes to Management.

Appeal Disciplinary Committee (ADC)

The Committee is established to review appeals from staff or ex-

staff on cases decided by the Disciplinary Committee.

Management Credit Committee (MCC)

The Committee is established to approve credits within its limit,

approve write-offs on excess interest and refund of interest within

its limit, and review fully provisioned loans and loan recovery

efforts, reports on credit quality, and policy procedure

adherence.

IT Steering Committee (ITSC)

The Committee is established to review, monitor and prioritize

major IT projects. It ensures that IT strategy is aligned with the

strategic goals of the Bank and procures business solutions that

leverage technology.

General Purposes Committee (GPC)

The Committee is established to carry out the following

functions:

• Provide oversight and direction for execution of

Investor Relations strategy and program such as

Financial Reporting & Stakeholder Engagement.

• Establish firm reputation for timely, transparent, and

reliable financial reporting/disclosure.

• Attract investors with long-term stake and ensure an

expanded & sustained access to lower-cost capital

from local and foreign financial markets.• Review and approve recommended processes and

present to EXCO for ratification.

• Ensure that process improvement activities are clearly

and functionally linked to the regional peculiarities

and strategic imperatives are capable of achieving the

key objectives of cost containment, service quality and

regularity compliance amongst others.

• Consider the Bank’s strategy towards CSR &

Sustainability related issues and monitor relevant

external developments.

• Consider and approve resource allocation for

identified and recommended CSR investments and

projects.

Product Development Committee (PDC)

The Committee is established to oversee the product

development process in the Bank. It defines the product

development process and strategy, reviews new products to

ensure alignment with the Bank’s strategic goals and objectives,

m o n i to rs t h e p e r fo r m a n ce o f p ro d u c t s a n d m a ke s

recommendations to Executive Management.

Process Review Committee (PRC)

The Committee is established to carry out comprehensive review

of processes designed by the Bank’s Business Process Re-

Engineering Team and make recommendations to Executive

Management. The Committee reviews process initiatives to

ensure that objectives of cost, service quality, speed and

regulatory compliance are achieved.

Polaris Bank appreciates the immense importance of sound

Corporate Governance in delivering value to its stakeholders and

building a sustainable enterprise. It therefore remains

committed to upholding the highest standards of Governance in

all the processes of the enterprise.

BY ORDER OF THE BOARD

BABATUNDE OSIBODUGENERAL COUNSEL/COMPANY SECRETARYFRC/2016/NBA/00000015464

Lagos, Nigeria February 13, 2020

CORPORATE GOVERNANCE REPORT

SUSTAINABILITYREPORT

16

POLARIS BANK ANNUAL REPORT & FINANCIAL STATEMENTS 2019

17

We believe that organizations that are genuinely concerned

about the environment and take active steps to manage the

environmental and social governance aspects of their activities

are best positioned to minimize risks and costs, capitalizing on a

plethora of opportunities to attract capital hence ensuring long-

term success of the organization. Our business activities and

operations at Polaris Bank have shi�ed from the regular business

model that focuses only on shareholder value and brand

acceptance; they are designed to ensure that we lend

responsibly, promote financial inclusion, encourage diversity,

invest in our employees, adhere to health and safety standards,

and reduce (or eliminate where possible) negative impact on the

environment, while continuing to grow a profitable and

sustainable business. Polaris Bank’s 2019 edition of the

Sustainability report reveals how the Bank’s policy and

framework aligns with its plan of building a world class work

environment. It also shows the general progress the Bank has

made to improve its agenda across the three stakeholder groups

– clients, people and community. In the area of Environmental,

Social and Governance (ESG), the Bank has steadily maintained a

robust management system by reviewing its Risk Assessment

Toolkit to meet industry and international standards.

OUR STRATEGY

As a principal financial Institution, Polaris Bank will continue to

focus on the importance of Sustainability to execute its business

activities and operations. The Bank recognizes the irrefutable

relationship between increasing the quality of life of people, the

long-term sustainable growth of its business activities &

operations and the environment where it operates. Hence,

sustainable activities of the Bank are woven around three

cardinal guidelines as indicated below:

1. Responsible Banking

2. Sustainable Economic growth

3. Community investments

RESPONSIBLE BANKING

Governance

The business priorit ies of the Bank with regards to

environmental, social and ethical issues are determined by the

Board Governance, Nomination and Compensation Committee.

The committee (through the Board, Audit and Risk Management

C o m m i t t e e ) a l s o i n t e g ra t e s t h e m a n a g e m e n t a n d

implementation of the Environmental and Social Risk

Management policy into the Bank’s business decisions.

The Environmental & Social Risk Management Framework

(ESRMF) sets out the agenda for consistent and systematic

management of E&S risks at Polaris Bank. It was built based on

Polaris Bank’s business principles and underlying commitment

to respect human rights and the environment.

The assessment portal has been continuously updated and

enhanced to screen qualifying transactions for environmental

and social risk towards efficient business decision making. The

portal is guided to ensure that the Bank’s risk management

processes are aligned with international best practice through

efficient internal standards and external collaborations such as

UNEPFI, IFC, ILO, Equator principles etc.

SUSTAINABILITY

report

At Polaris Bank, our commitment to sustainability reflects our values. Our strategy is focused primarily on responsible business practices which drive our role in ensuring long term economic development through the provision of sustainable financial products and advisory services. We are in active pursuits of the triple bottom line which consists of the three Ps: People, planet and profit.

POLARIS BANK ANNUAL REPORT & FINANCIAL STATEMENTS 2019

18

Employees

Polaris Bank is committed to the wellbeing of its employees

through effective engagements such as: health programmes,

trainings, competitive benefits and adequate compensation to

promote staff retention. As an equal opportunity employer, we

are passionate about providing a safe and conducive work

environment for all our employees.

In line with the commitment to harnessing our employees’

potential through continuous learning and development, the

Bank invested in various capacity building and employee

empowerment programmes focused on providing the required

support , solutions, knowledge and skills to meet the

developmental needs of the work force. This was achieved

through a detailed training curriculum which included

assessments to determine the level at which learning took place

and if set objectives were met.

The immense engagement drive influenced the behaviour of the

work force which resulted in enhanced work performance. Based

on the training policy of the Bank, all employees are entitled to a

variety of capacity building initiatives to boost their distinct

abilities. The Bank’s robust e-learning portal with a combination

of classroom learning enhances its vision for continuous

knowledge acquisition and professional development.

Gender, Diversity and Inclusion

Polaris Bank celebrates individuality and diversity and treats its

workforce equally with respect, dignity and fairness. In line with

best practices, the Bank offers equitable remuneration and

capacity development opportunities for all regardless of gender,

ethnicity, ideology or creed. Polaris Bank also ensures that

applications for employment by persons with disabilities are

given utmost consideration. In the event that any staff member

becomes physically challenged, appropriate training and

counselling sessions will be organized to guarantee continuous

employment with the Bank as required.

Health and Safety

The Bank has been successful in achieving a safe and healthy

working environment which is solely based on the shared

responsibilities of its employees.

Over the years, the Bank has maintained an enviable Health,

Safety and Environment (HSE) framework. The Bank is held

accountable for the enforcement of the HSE framework which is

cascaded to employees, customers and other stakeholders on

the Bank’s premises. Polaris Bank ensures adequate practices

and procedures which provides an appropriate working

environment for the workforce to deliver their utmost ability.

Polaris Bank remains ISO 22301 certified and operates within the

protocols: A Business Continuity Management certification

which ensures the timely resumption of business operations in

the event of an incident occurring and the protection of

personnel and the organization.

Malaria and Other Serious Diseases

One of Polaris Bank’s main goal is to ensure consistent

improvement in the well-being of the Bank’s workforce thereby

ensuring that employees are fit mentally, physically, emotionally

and are subsequently productive at optimal levels.

The Bank in partnership with some Health Management

Organizations (HMO) operates a structure where employees are

registered with hospitals under the insurance scheme to

undertake various health management issues like malaria to

other more serious ailments for them and their listed

dependents. An annual Health assessment week also held in the

Bank to reiterate the importance of healthy living for all staff.

Various Health topics have been used as themes for the week;

ranging from Physical Health, Mental Health, Healthy Living, and

Nutrition to Consistent Health checks.

The annual health week was held in November 2019 with the

theme: “PHYSICAL ACTIVITY – KEY TO ALL ROUND

WELLNESS”. The objective was to empower employees with

information on the importance of physical activity to all-round

wellness, give insights into how to incorporate more physical

activity in their work life, encourage and inspire a healthy lifestyle,

inform and educate on the dangers of a sedentary lifestyle vis-a

vis how to combat same.

HIV Testing, Confidentiality and Disclosure

Polaris Bank is known to regularly contribute to events that

provide sensitization for the Human Immunodeficiency

Virus/Acquired Immune Deficiency Syndrome (HIV/AIDS). As an

institution that shows great concern for the well-being of its staff,

the Bank takes initiatives that promote awareness, prevention

and management of the disease and also supports any

individual who is affected. In addition, the Bank encourages

nondiscrimination on HIV/AIDS particularly in the workplace and

does not require employees, their dependents, job applicants or

other third parties to undergo HIV testing as a precondition for

employment or receipt of benefits.

SUSTAINABILITY REPORT

POLARIS BANK ANNUAL REPORT & FINANCIAL STATEMENTS 2019

19

Code of ethics

For Polaris Bank, Sustainability is necessary to attract and retain

dedicated employees with a strong service mind-set for business

continuity and long-term performance. The Bank’s core values

which are the foundation for its culture as well as its procedures

are described in the Bank’s Code of Conduct which focuses on

areas of ethical risk. The Code which is attested at the beginning

of each year by every employee, provides guidance to help

employees recognize and deal with ethical issues, availing

mechanisms for employees to report unethical conduct and

foster a culture of honesty and accountability amongst its

employees.

Human Rights

As a reputable financial institution, Polaris Bank aims to set a

positive example of how to respect and promote human rights.

T h e B a n k h a s f a i r r e c r u i t m e n t p r a c t i c e s t h a t a r e

nondiscriminatory.

In addition, as part of our Social and Environmental Management

System, questions bothering on human rights has been

integrated into the Environmental & Social Risk Assessment

Portal. The Bank’s site visitation team also note human rights

issues as part of the system’s checklist to ensure our clients are

not violating human rights.

In Polaris Bank, the rights of the individual is demonstrated in

accordance with the 1948 Universal Declaration of Human Rights

(UDHR) as well as the International Labor Organizations (ILO)

standards regarding child and forced labor, the rights to organize

and bargain collectively, freedom of association, enhance social

protection and strengthen dialogue on work-related issues.

Collaboration

Organisations sign up for Sustainability partnerships to attain

greater accomplishments from such associations. Polaris Bank

appreciates the importance of working jointly with local and

international institutions that promote environmentally and

socially responsible economic development, while ensuring that

its activities do not undermine the ability of future generations to

meet their needs.

To this end, Polaris Bank is a member of some of the leading

global organisations in sustainability, which include the United

Nations Environment Programme and financial Institutions

(UNEP FI), Global Reporting Initiative (GRI) and Child & Youth

Finance International (CYFI). Polaris Bank is also the only

Nigerian bank represented in the GRI G4 Pioneer Group.

Environmental Responsibility

The Bank’s attention to environmental preservation cannot be

over-emphasized. This reflects in its steady commitment to

mitigating and possibly bringing to the barest minimum the

impact on the environment arising from its business decisions.

Our commitment to continuous vendor monitoring and

management programmes has been beneficial to its

environmental sustainability motives. We engaged the Bank’s

vendors in a capacity building workshop to develop skills and

provide necessary education in Environmental & Social Risk

(E&S) Management. This is reflected in the improved compliance

by vendors and suppliers to ethical business practices.

The Bank has also continuously reduced its negative impact on

the environment by reducing pollution caused by diesel usage

through the use of alternative sources of energy. More business

offices are being solar powered whilst also maintaining a strict

closing time of 6pm across all branches nationwide to reduce

energy consumption and carbon emission.

As a Bank we are also committed to reducing our carbon

footprint by ensuring the use of recycled paper at the same time

tracking printing costs and paper usage.

SUSTAINABLE ECONOMIC GROWTH

Access to Finance

Polaris Bank is committed to developing products and services

that improve accessibility to finance. The Bank takes pleasure in

understanding its customer’s needs and strives to surpass them

by undertaking a proactive customer engagement process using

different channels, publications, email alert/SMS, social media,

focus group, written communications, marketing calls,

advertising and business seminars.

The Bank has also provided various channel choices for

customers to ensure substantial access to Banking services at all

times for both the advantaged and disadvantaged individuals. In

order to ensure that possessing a disability is not a hindrance to

accessing our services, the Bank is currently upgrading more of

its branches to accommodate wheelchair access for the

physically challenged customers.

Polaris Bank has continually enhanced its credit process to fully

integrate the Environmental and Social Risk Analysis into the

lending, monitoring and reporting process for specific project-

finance transactions within a stipulated threshold.

SUSTAINABILITY REPORT

POLARIS BANK ANNUAL REPORT & FINANCIAL STATEMENTS 2019

20

Products and Innovation

At Polaris Bank, we constantly improve and expand the retail

portfolio with emphasis on driving transactional banking while

delivering outstanding customer service through the provision of

fast, secure, reliable and convenient electronic and retail banking

products, platforms and services. We have innovative products

and services designed to cater for all classes in the society.

Our team of experts have also simplified our services with

technology driven processes to enable more people have access

to financial services which encourages a positive and rewarding

savings culture. Highlights of some of our distinct Products and

Innovations include:

• Polaris Flex Salary Account: This is an account targeted

at salaried individuals who earn a monthly income of

up to N50,000.

• Polaris Ease Salary Account: This is an account

targeted at salaried individuals who earn a monthly

income of up to N100,000.

• Health Loan: Gives opportunity for SMEs in the Health

Sector to access finance for the daily running of their

business.

• Market Loan: Grants access to short term working

capital loan to SMEs who deal in fast moving consumer

goods in preapproved market locations

• Education Loan: Reviewed existing product in tune

with current market realities. Beneficiaries of Education loans are private nursery,

primary, secondary and tertiary institution

• Launched a capacity building program in partnership

with Facebook to train SMEs to leverage social media

as an access to market tool. Trained over 500 SMEs in 9

locations across 6 regions.

• Digital Salary Advance: the product enables salaried

employees who are eligible to access salary advance

via their phones by dialing USSD code *833*12.

• Short Term Asset Finance: This product is designed to

enable customers acquire choice consumer

household assets from pre-qualified merchants of the

Bank and enjoy a flexible and convenient repayment

plan

• Successful integration of Polaris Collect with Infinity

Systems on Ebonyi State IGR Collections and

commenced sensitization to enhance our market

share in the State.

• Implementation of the digital banking gateway

• Commenced pilot of the agency banking platform

(Surepadi)

COMMUNITY INVESTMENTS

Financial Literacy

The Bank believes sustainable economic development cannot

be achieved without the ability of customers to make informed

and effective decisions. Polaris Bank dedicates time and

resources to helping customers with the knowledge, skills and

confidence required to make financial decisions.

To demonstrate Polaris Bank’s commitment, its Sustainability

team working with the Products & Markets group across the

different geopolitical zones have delivered Financial Literacy

seminars/classes in several schools (primary and secondary) in

clusters every quarter across the nation over a period, in addition

to contributing various educational materials to school visited.

To date, the team has been able to reach over 80,000 students in

over 180 schools across major cities in Nigeria.

The Bank will continue to work with the CBN and use its

employees through volunteerism schemes for greater impact

and coverage through various initiatives in the year ahead.

Corporate Social Responsibility

At Polaris Bank, we believe that beyond the benefits of our

business to society, we have a critical role to play in providing

support systems and structures that enable individuals,

institutions and communities reach their full potentials.

Our commitment to this ideal thus runs just as deep as our

passion for creating value and is driven by the belief that building

a strong business and making the world a better place are

essential ingredients for long-term success.

Consistent with our Sustainability and CSR policy, our

interventions are driven by strategic focus and significant

investments in Education, Health & Safety, Women & Youth

Empowerment, Environment, Social infrastructure, Sports and

Cultural & Civic Projects; six areas which are essential pillars to

building a sustainable society.

It is for this reason that we have fully integrated corporate social

responsibility into our business model and continue to maintain

a clearly defined CSR strategy focused on championing

humanitarian causes and fostering initiatives that transform lives

and upli� communities.

SUSTAINABILITY REPORT

POLARIS BANK ANNUAL REPORT & FINANCIAL STATEMENTS 2019

21

In 2019, we continued to deepen the impact of our initiatives;

funding developmental projects, championing humanitarian

causes, expanding access to quality education, promoting

cultural heritage and creating opportunities for economic

empowerment. In this report, you will find testimonials that

reflect our progressive impact in enriching people’s lives. Details

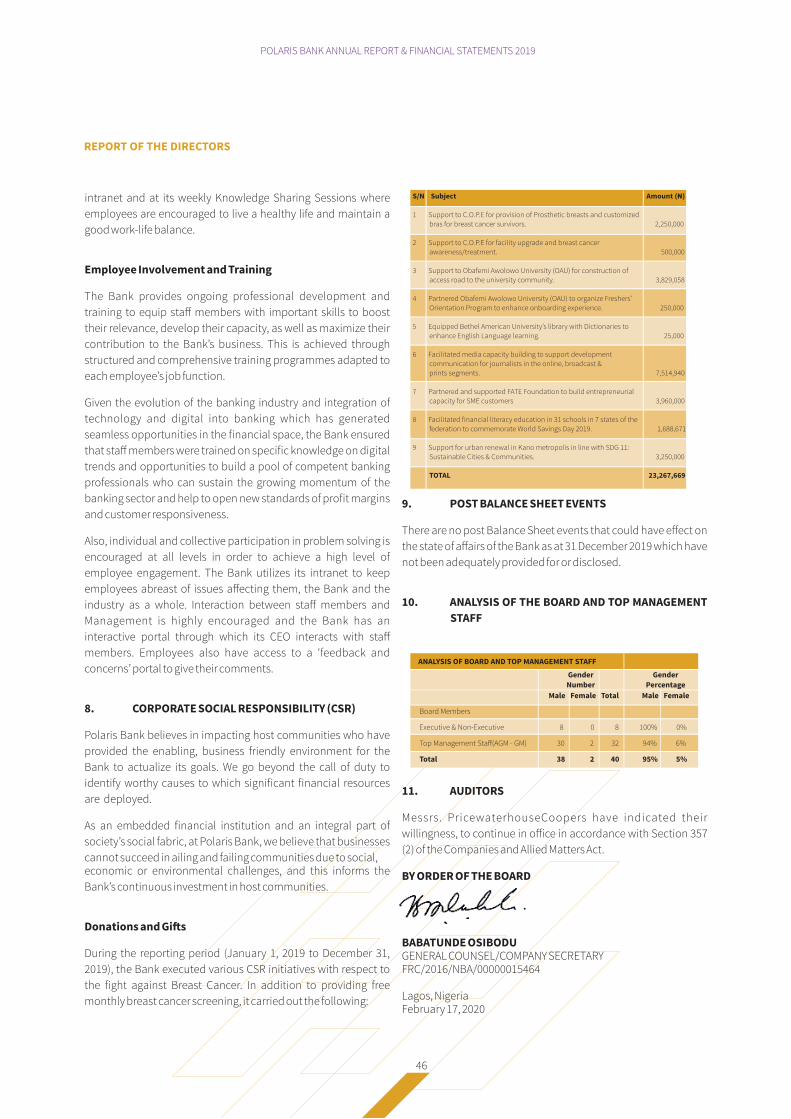

of our initiatives include:

• Provided Prosthetic breasts and customized bras for

registered breast cancer survivors to ameliorate the

plight of those who have lost their self-confidence and

self-esteem as a result of stigmatization, following

mastectomy.

• Construction of Bank Road at Obafemi Awolowo

University (OAU): Provided seamless access to over

36,000 estimated population in the university

community

• Facilitated a worthwhile on-boarding experience for

over 6,500 fresh undergraduates: Partnered with

Obafemi Awolowo University (OAU) to organise their

Freshers’ Orientation Programme

• Sponsored 8 of the Bank's customers to FATE

Foundation: Built entrepreneurial capacity for eight

young entrepreneurs in an all-expense paid business

empowerment training

• Sponsored Afroprom for graduating students drawn

from select public and private secondary schools:

Facilitated a semi-formal black tie dance and

gathering of 3,000 graduating students drawn from

popular public and private secondary schools in Lagos

on the threshold of pursuing their dreams of Higher

Education.

• Donated towards the WIMBIZ 2019 Conference which

had over 1,700 women in attendance across various

sectors. The Bank sponsored 10 female staff members

to reaffirm its support for women

• Sponsored the Sisters’ Keepers Initiative, Kano maiden

workshop in Kano for Social Impact and Awareness on

right of Women and Girl Child: Reached over 400

women spanning across education, business and

politics with several account opening

• Sponsored Nigerian Artisans & Technicians 2019

Conference: Over 6,000 artisans present with strong

SME stakeholders/regulators (SMEDAN, FIRS, CPC &

Ministry of Labour) in attendance

• Partnered with Guild of Corporate Online Publishers to

organise the Annual Conference of the association:

Beyond deepening the knowledge of the publishers, it

also reinforced brand partnership with a critical media

stakeholder.

• Sponsored the 4th Lagos Digital NIPR Summit: The

Bank got extensive visibility on the sponsorship which

reinforced the brand perception of Polaris as a

knowledge driver in a knowledge economy.

• Sponsored Sarius Palmetum Garden Abuja in support

of Botanical Gardening with over 1000 classes of plants

which include 250 species of palm trees

• Sponsored the Head of Service Games (HOS Games),

Alausa, Lagos

CUSTOMERS’ COMPLAINTS AND PETITIONS

At Polaris Bank, our customers are fundamental to our business

and our commitment is to ensure we deliver an enjoyable and

satisfying banking experience to them.

The Bank deployed various feedback and engagement initiatives

geared towards obtaining direct feedback from customers on

their experiences and satisfaction levels with our products and

services across all our channels. This greatly assisted us in

improving our customers’ experience as well as strengthening

our relationships with them.

To further close the gap between our service delivery and

customer expectations, we carried out several reviews of our

business processes and service standards to increase value

creation and ensure a rewarding banking experience.

The improvement is expected to continue, as Polaris Bank

maintains a strong focus on surpassing customers’ expectations

while ensuring the swi� resolution of customer complaints

through prompt, impartial and fair investigations.

Complaint/Feedback Channels:

The Bank’s dedicated channels for the receipt and processing of

complaints include:

• Our 24/7 Contact Centre- The Yes Centre• Our Branches and Head Office• Customer Experience Management Department• Consumer Protection Department• Social media platforms including Twitter and

Facebook.

SUSTAINABILITY REPORT

POLARIS BANK ANNUAL REPORT & FINANCIAL STATEMENTS 2019

22

The Complaint Management system in the Bank has been set up

to:

• Ensure that all customers complaints received are

resolved promptly and satisfactorily.

• Ensure that customers’ concerns and complaints are

handled in line with our customer experience strategy

and relevant legal/regulatory requirements.

• Minimize reasons for complaints by learning from

them and improving on our products and services

The Consumer Protection desk has continued to perform its

mediation role between the Bank and its customers, thus

ensuring fair hearing and right to compensation as necessary.

This has been achieved by managing redress issues

professionally towards amicable resolution and customer

retention as well as continuous education on our products and

services, hence ensuring full consumer knowledge and

education. The desk has maintained its commitment to the apex

bank in line with its guidelines on resolution of complaints and

pursuit of Consumer Protection.

Complaints Report/Breakdown

The Bank received a total of 547,926 (Five Hundred and Forty

Seven Thousand, Nine Hundred and Twenty Six) complaints

which comprise of complaints logged on the Consumer

Complaints Management System (CCMS) and redress

complaints from the CBN within the review period (January -

December 2019) across various channels including Branches, Yes

Centre, Complaint Management and Consumer Protection desk.

From the 547,926 complaints received which also include the 382

petitions brought forward from December 2018, a total of 542,796

(Five Hundred and Forty-Seven Thousand, Seven Hundred and

Ninety-Six) were resolved satisfactorily while 5130 (Five

Thousand, One Hundred and Thirty) remained unresolved with

resolution efforts ongoing. Percentage of resolved complaints as

at 31st December 2019 stands at 99.06%.

Analysis of Complaints

Graphical Representation of Complaints

During the period under review, the sum of N52,507,993,857.15

(Fi�y two Billion, Five hundred and Seven Million, Nine Hundred

and Nine Three Thousand, Eight Hundred and Fi�y Seven Naira,

Fi�een Kobo) was claimed by various customers from petitions

reviewed. However, complaints involving the sum of

N51,495,530,627.23 were resolved, while the sum of

N124,319,369.79 was paid out as refunds.

SUSTAINABILITY REPORT

S/N Narration Total No. of Complaints

Total No. Resolved

Total No. Unresolved

1 Total 547,926 542,796 5,130

2 Percentage

Distribution 100% 99.06 0.94

99.060.94

No. of Complaints Recieved

Total No. Resolved Total No. Unresolved

S/N DESCRIPTION NUMBER AMOUNT CLAIMED (NGN)

Jan-Dec 2019 Oct-Dec 2018 2019 2019

AMOUNT REFUNDED (NGN)

Pending

Complaints

B/F

382 4021

2

3

4

5

Received

Complaints 547,544 1,917 52,507,993,857.15

Resolved

Complaints 542,796 1,822 51,495,530,627.23 124,319,369.79

Unresolved

Complaints

escalated

to CBN for

intervention

126 115

Unresolved

complaints

pending

with the

bank C/F

5,004 382

Tabular Breakdown of Customers’ complaints and claims

POLARIS BANK ANNUAL REPORT & FINANCIAL STATEMENTS 2019

23

Customers’ complaints and petitions received for the

period include but not limited to the following:

• Card ser vices, including, Card issuance, ATM

withdrawals, POS transactions etc.

• Internet Banking related issues

• Contentious withdrawals and charges

• General Account complaints.

Analysis of Fraud and Forgeries Return

During the period under review, the bank recorded 102 fraud

cases. The total amount involved is N1,914,982,813.00 and

$321,132.85. However, a total of N99,662,635.76 and $30,991.95

were lost and these are analyzed below:

SUSTAINABILITY REPORT

S/N Nature of fraud No of cases 31 December

2019

31 December

2019

1 ATM 15 11,129,098.96 991.95 10.36

2 Internet Banking 8 16,157,007.17 - 14.56

3 Mobile 20 19,201,282.50 - 17.30

4 Impersonation 13 18,062,221.90 - 16.28

5 Cheque Related 12 4,672,942.46 - 4.21

6 Outright the� 21 1,540,740.00 - 1.39

7 Cyber Fraud 2 3,743,039.14 - 3.37

8 General 11 25,156,303.63 30,000.00 32.53

Total 102 99,662,635.76 30,991.95 100.00

Amount lost (N) Amount lost ($) % Total (N)

11,490,863.13

16,157,007.17

19,201,282.50

18,062,221.90

4,672,942.46

1,540,740.00

3,743,039.14

36,097,303.63

110,965,399.93

CHAIRMAN’SSTATEMENT

24

25

POLARIS BANK ANNUAL REPORT & FINANCIAL STATEMENTS 2019

26

Today, I am delighted to note that Polaris Bank is strong, stable

and not only firmly on a path to sustainable profitability but

strongly positioned to be a future determining bank in the fast-

changing Financial Service space. We have laid a solid

foundation for an enduring, effective, efficient, agile, innovative

and resilient Bank and the performance numbers do bear me

witness.

Our Humble Beginning

When, pursuant to intervening action by the CBN, I assumed the

Chairmanship of the Board of the defunct Skye Bank PLC on July

4th, 2016, the task ahead of us appeared daunting. The bank was

groaning under the weight of non-performing loans and liquidity

pressures, the prudential ratios were a far cry from regulatory

compliance, services were below par, the I.T Infrastructure was

obsolete, staff morale was at its lowest ebb there was immense

pressure from both local and foreign lenders by recalling their

funds. To cap it all, some of the Bank’s major customers along

with key mandates had also taken a walk, as a flight to safety.

However, with the staunch support of the CBN, we were able to

turn around the fortunes of that bank following the decision of

the regulators to incorporate Polaris Bank to take over the assets

and some liabilities of Skye Bank and retain the same Board and

Management.

Polaris Bank was birthed on September 21, 2018 as a private

limited company, wholly owned by the Asset Management

Corporation of Nigeria (AMCON), and on the same day, it took

over the assets and some liabilities of the defunct Skye Bank. As

attested by the financial results being approved today, the story

is completely different. Most prudential ratios, including Capital

Adequacy and Liquidity, are firmly in compliance, all matured

obligations across currencies have been discharged, service

levels have improved tremendously, the technology platforms

and infrastructure are being upgraded and the workforce is well

motivated. Although there are still a few of the legacy challenges

that we are dealing with, we are confident that with your usual

support and the commitment of the Board and Management,

they will also soon be resolved. The progress made so far will

suffice to stand Polaris Bank out for all of history in Financial

Services Industry and in Academia as a classical model for

successful regulatory intervention. While acknowledging the

valued critical and unrelenting support received from our

regulators, the CBN and AMCON our owners, I must also express

my appreciation to my colleagues on the Board and the

Management of the Bank for the completely different story we

are telling today.

Operating Environment, Business Strategy and Business

Overview

The business environment is increasingly becoming challenging

to navigate. Economic growth has been very sluggish, and

businesses are not having the best of times. Regulatory demands

kept mounting, from rising prudential requirements, to thinning

charges and margins. In addition, the sphere of competition is

also widening beyond traditional financial institutions to include

existential threats from FInTechs and other non-traditional

players. Amid all of these, we remain confident that Polaris will

find, defend and be among the leading innovative banks in the

evolving order of financial service offerings.

CHAIRMAN’S

statement

It is with great pleasure that I present the 2019 Annual Reports and Accounts of our Bank. This is

our first full year of operations since Polaris Bank came into being and acquired the assets and

some of the liabilities of the defunct Skye Bank.

POLARIS BANK ANNUAL REPORT & FINANCIAL STATEMENTS 2019

27

Given the foregoing, it became clear early on in this assignment

that an overhaul of the business processes and strategy including

digital transformation was critical to turning the fortunes of

Polaris around and compete effectively and efficiently in the fast-

changing banking space. Working with top rated industry

consultants across disciplines such as business development,

technology, strategy and brand, we carved out a medium-term

corporate transformation program. This includes digital

transformation / technology refresh, Business strategy, Brand

and culture realignment. The implementation of all the

components of the corporate strategy has commenced and in

less than a year on the journey, significant milestones have been

achieved. Indeed, I am pleased to announce that we are ahead of

timelines on many of our performance benchmarks.

Although we are still on the corporate transformation journey,

initial results are very encouraging, and we are confident of even

more impressive outcomes on both the quantitative and

qualitative fronts going forward. Our customer service is

improving, and our target is to rank among the very best in the

industry in the not-too-distant future. Also, our digital platforms

are more stable, the foundation of our IT infrastructure has been

solidified and is infinitely more robust, and our customers 'overall experience has witnessed strong improvement. We are

winning market share and have started getting unsolicited

corresponding banking business offers from foreign lenders.

The financial results we posted in our first full year of operation is

a testimony to the progress we have made in our goal of

transforming the Bank. We posted ₦150.4bn in gross earnings,

N27.34bn in Profit Before Tax and ₦26.29bn in Profit A�er Tax.

Our deposits stood at N857.8bn and loan book at N261bn. Return

on Equity was at 33.0% and Return on Assets at 2.4%. The results

compare favourably with the best in the industry and I must seize

this opportunity to appreciate and congratulate the Board,

Management and indeed the entire staff of the Bank for a job well

done.

Corporate Governance

One of our very first action points on coming on-board was to put

in place a strong and transparent corporate governance

framework that ensures adequate Board oversight and more

importantly Board transparency and accountability. The Board is

supported by four Board committees, namely the Board

Governance, Nominations and Compensations Committee,

Board Audit and Risk Management Committee, Board Credit

Committee and Board Finance and General Purpose Committee,

each with direct oversight over their respective areas of

responsibilities. All capital expenditure above N100m requires

the approval of the Board Finance and General purpose

committee, and the Board Credit Committee is required to

approve any credit facility in excess of N500m. Furthermore, all

policy documents underlying the Bank's operations require

Board approval to become effective. These are just a few of the

measures put in place to entrench corporate governance and

promote Board accountability.

Responsibility to Our Society

At Polaris, we are deeply committed to the well-being of the

society where we operate, and this is demonstrated by our robust

CSR budget. Our operations are wholly guided by strict

considerations for environmental protection and we do not

support any business whose activities are inimical to

environmental and societal well-being. The Bank is a signatory to

the United Nations Environmental Program – Financial Initiative

(UNEP-FI), the body responsible for coordinating sustainable

banking practices. The Chief Executive Officer, Mr. Tokunbo

Abiru, is also a nominated champion for gender equality,

�HeforShe” by the Lagos State Ministry for Women's Affairs in

collaboration with the United Nations. Our commitment to

promoting financial literacy is demonstrated through our annual

participation in the Global Money week campaign, an annual

financial awareness campaign which inspires children and

young people to learn about money, saving, creating livelihoods,

gaining employment and becoming entrepreneurs. Amid many

other Corporate Social Responsibility (CSR) activities we are

involved in, we supported government efforts toward fighting the

COVID-19 pandemic by donating fully accessorized hospital beds

to the Lagos state Government and Nigeria Centre for Decease

Control (NCDC). We also supported the Private Sector coalition

effort towards combating the virus.

CHAIRMAN’S STATEMENT

the progress we have made in our

goal of transforming the Bank.

We posted ₦150.4bn in gross

earnings, N27.34bn in Profit Before

Tax and ₦26.29bn in Profit A�er Tax.

POLARIS BANK ANNUAL REPORT & FINANCIAL STATEMENTS 2019

28

What the Future holds

The horizon was very hazy when we started this journey, but

today, you will agree with me that the future of this enterprise is

much more promising. We are advancing in our corporate

transformation Journey toward making Polaris a digital bank

that will not only compete but lead the frontier of innovations. We

will continue to invest in Technology, strengthen our Cyber

security capabilities and broaden product offerings to the unique

needs of the banking public. While acknowledging that COVID-

19 has dampened the business climate, casting a shadow of

recession on economic outlook, Polaris will continue to fashion

appropriate strategic responses to weather the storm of the

pandemic. We are optimistic about the evolving strength and

profile of the brand we are building for sustainable wealth

creation for maximum value realization.

On behalf of the Board and Management, I thank you for the

opportunity given to us to serve and the confidence reposed on

us. I also appreciate the immense contributions of our most

valued asset (our staff for their support, dedication and

productivity) during this reporting period.

Thank you all.

CHAIRMAN’S STATEMENT

While acknowledging that COVID-19

has dampened the business

climate, casting a shadow of

recession on economic outlook,

Polaris will continue to fashion

appropriate strategic responses to

weather the storm of the pandemic

MANAGING DIRECTOR’SSTATEMENT

29

30

POLARIS BANK ANNUAL REPORT & FINANCIAL STATEMENTS 2019

31

A Challenging beginning

When Polaris Bank took over the assets and some liabilities of the

defunct Skye Bank in September 2018 and we assumed its affairs,

we were clear on the enormity of task ahead of us and the

directions in which we must move. The defunct Bank was

challenged on many fronts; prudential ratios (including liquidity

and capital adequacy) were out of compliance, the financial

position statement was not in a good state, there were non-

performing loans (NPL) challenges , core technology

infrastructure and many related applications were obsolete,

customer’s experience was sub-optimal and staff morale could

be a lot better. Despite all these challenges, we also saw

possibilities, hidden potentials of a brand that could redefine the

banking landscape, compete and challenge the very best in the

in the industry and we set out on a journey to make that happen.

Our Vision - Corporate Transformation

We engaged leading consultants for clear and concise

articulation of the vision we have for Polaris Bank. This requires

complete enterprise transformation with a medium-term

strategy broken down into; revamping our information

technology infrastructure, redefining the business strategy, re-

projecting the brand and digital transformation. We have

achieved significant mileage on this Corporate Transformation

journey, and you will agree with me that the early signs are very

promising. While we are repositioning our I.T infrastructure to

world class standards, we are equally implementing a robust

digital transformation to actualize our vision of making Polaris a

truly digital Bank. Given the demographics of this environment,

we primarily pursued a retail banking strategy, with focus on

growth sectors in the commercial banking space with cautious

play in Corporate Banking. With all these transformational

initiatives ongoing, very soon, we are confident Polaris will

assume a pride of place in the industry, leading innovation and

delivering world-class customer experience leveraging cutting-

edge technology. We have also deepened our product offering to

address the unique needs of different customer segments across

age, geography, gender and business types. To further reinforce

the evolving brand value in the mind of the banking public, we

are re-projecting our brand identity both in the virtual and

physical environment.

Our Performance and Our Business

A review of the result shows positive performance across all

financial indices, an early validation of the corporate

transformation journey the Bank embarked upon. Amidst stiff

competition, challenging regulatory and harsh macro-economic

conditions, the Bank posted ₦150.4bn in gross earnings in its first

full year of operation. PBT stood at N27.34bn and PAT at N26.29n.

By refocusing on deposits sources, our deposit declined

marginally to N857.8billion from N861b at which we closed our

first three months of operation in December 2018 following our

resolve to rebalance the deposit portfolio toward more stable

and less expensive retail deposits.

MANAGING DIRECTOR’S

statement

Let me start by expressing my sincere gratitude to our primary regulator, the Central Bank of

Nigeria (CBN), and AMCON for the opportunity and privilege to lead the Management team of this

fledging institution. I am equally grateful to the Board, under the Chairmanship of Mr.

Muhammad Kabiru Ahmad, for its leadership and invaluable support that has helped to bring

Polaris to where it is today. I also commend the entire workforce of the Bank for commitment

and sense of dedication to duty and together we will continue to deepen Polaris footprints on

the history of corporate transformation in Nigeria.

Amidst stiff competition, challenging regulatory and

harsh macro-economic conditions, the Bank posted

₦150.4bn

POLARIS BANK ANNUAL REPORT & FINANCIAL STATEMENTS 2019

32

The loan book closed the year at N261bn. Our Return on Equity

(ROE) and while Return on Assets (ROA) were also very decent at

33.0% and 2.4% respectively (both are above industry average)

Underpinning our financial performance is the implementation

of our corporate transformation program. Thus, our retail

business is anchored on our capability to provide value to

individuals and small businesses. The retail products are