Public’DebtSustainability’Analysisfor’...

27

Public Debt Sustainability Analysis for Market Access Countries (MACs): The IMF’s Framework September 2015 1 S. Ali Abbas International Monetary Fund

Transcript of Public’DebtSustainability’Analysisfor’...

Public Debt Sustainability Analysis for Market Access Countries (MACs):

The IMF’s Framework

September 20151

S. Ali AbbasInternational Monetary Fund

Outline

Risk -‐ Based Approach

Lower Scrutiny DSA (Basic DSA)

Realism of Baseline Assumptions

Motivation for 2013 “MAC DSA” reform

Higher Scrutiny DSA (Additional modules)

Heat Map: Stress Tests and Debt Profile

Fan Charts

DSA Write Up

2

Traditionally, the focus was mainly on debt trajectories….

3

Key Features of the MAC DSA

• More analysis for countries with potentially greater vulnerabilities

Risk -‐ based approach

• Realism of underlying assumptions• Risks to debt level, gross financing needs, and debt profile, macro-‐fiscal nexus, and bank-‐sovereign nexus

Multifaceted analysis

• Standardized charts and tables, fan charts, heat map, write-‐up

Clear and transparent presentation of results

4

Risk assessment based on benchmarks derived from early warning model

Toolkit is flexible and can be tailored to country-‐specific circumstances

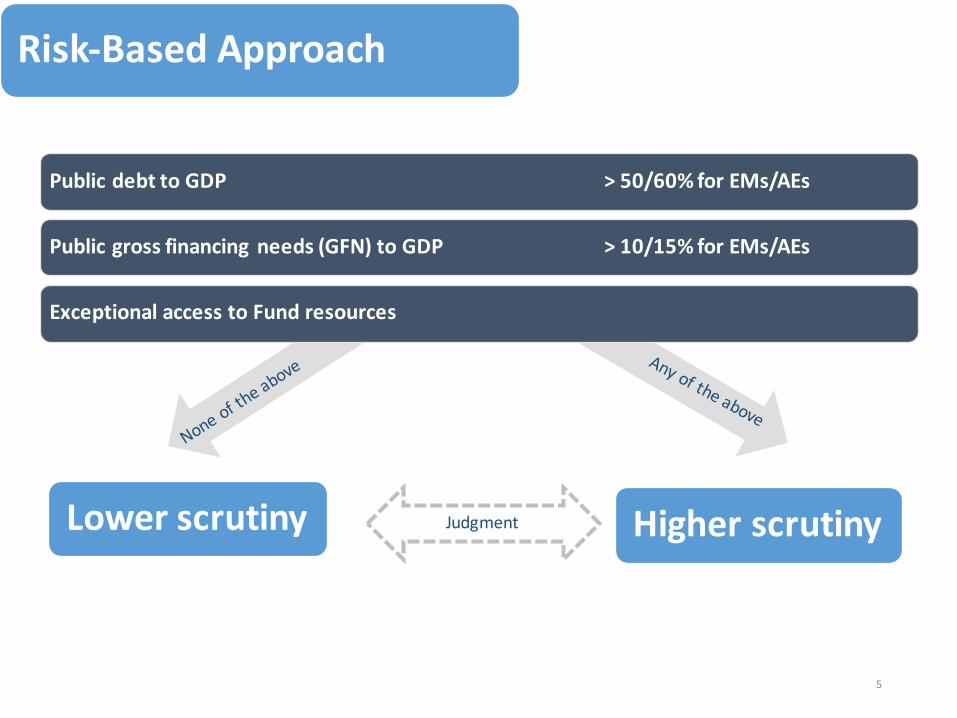

Risk-‐Based Approach

Public debt to GDP > 50/60% for EMs/AEs

Public gross financing needs (GFN) to GDP > 10/15% for EMs/AEs

Exceptional access to Fund resources

Lower scrutiny Higher scrutinyJudgment

5

6

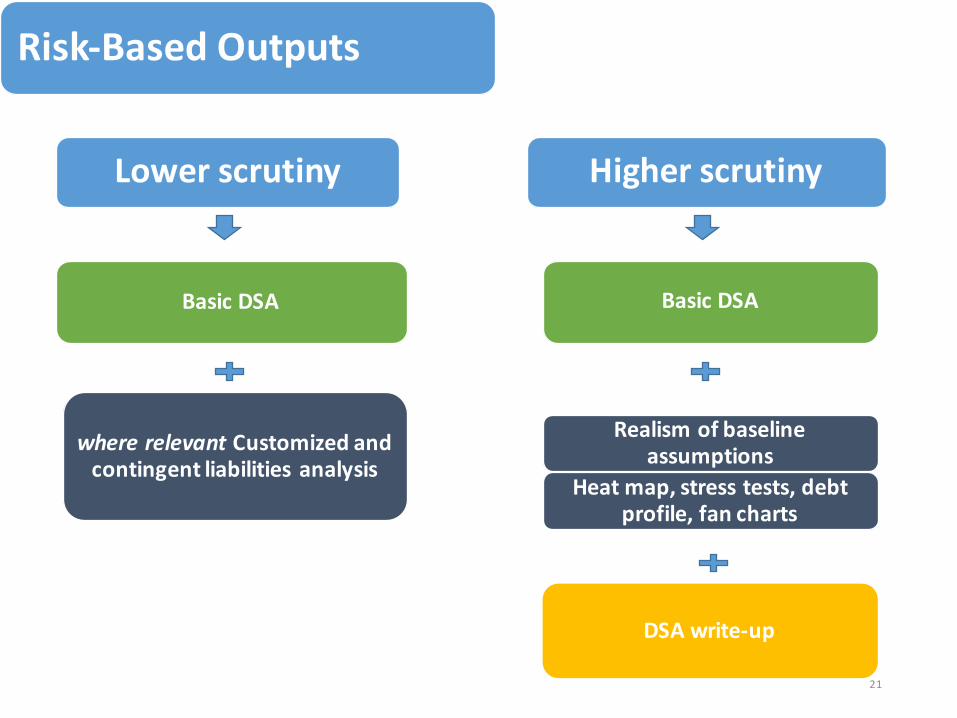

Risk-‐Based Outputs

Basic DSA

DSA write-‐up

Basic DSA

Realism of baseline assumptions

Heat map, stress tests, debt profile, fan charts

where relevant Customized and contingent liabilities analysis

Lower scrutiny Higher scrutiny

6

Basic DSA -‐ 1

As of June 15, 20142/ 2012 2013 2014 2015 2016 2017 2018 2019 Sovereign Spreads

Nominal gross public debt 48.9 85.9 94.0 98.7 101.2 102.3 102.3 101.3 99.8 EMBIG (bp) 3/ 160

Public gross financing needs 11.1 22.0 20.8 20.5 20.0 19.4 18.7 18.0 17.4 5Y CDS (bp) 90

Real GDP growth (in percent) 1.6 -‐1.6 -‐1.2 1.2 1.6 1.7 1.8 1.9 2.0 Ratings Foreign LocalInflation (GDP deflator, in percent) 2.5 0.0 0.6 -‐0.1 0.8 1.0 1.1 1.4 1.4 Moody's Baa2 Baa2Nominal GDP growth (in percent) 4.2 -‐1.6 -‐0.6 1.1 2.3 2.7 3.0 3.3 3.4 S&Ps BBB BBBEffective interest rate (in percent) 4/ 4.3 4.3 4.0 3.8 3.7 3.6 3.6 3.6 3.7 Fitch BBB+ BBB+

Debt, Economic and Market Indicators 1/

Projections2003-‐2011

Actual

-‐10

-‐5

0

5

10

15

20

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Debt-‐Creating Flows

Primary deficit Real GDP growth Real interest rate Exchange rate depreciation Other debt-‐creating flows ResidualChange in gross public sector debt

projection

(in percent of GDP)

-‐15

-‐10

-‐5

0

5

10

15

20

cumulative

7

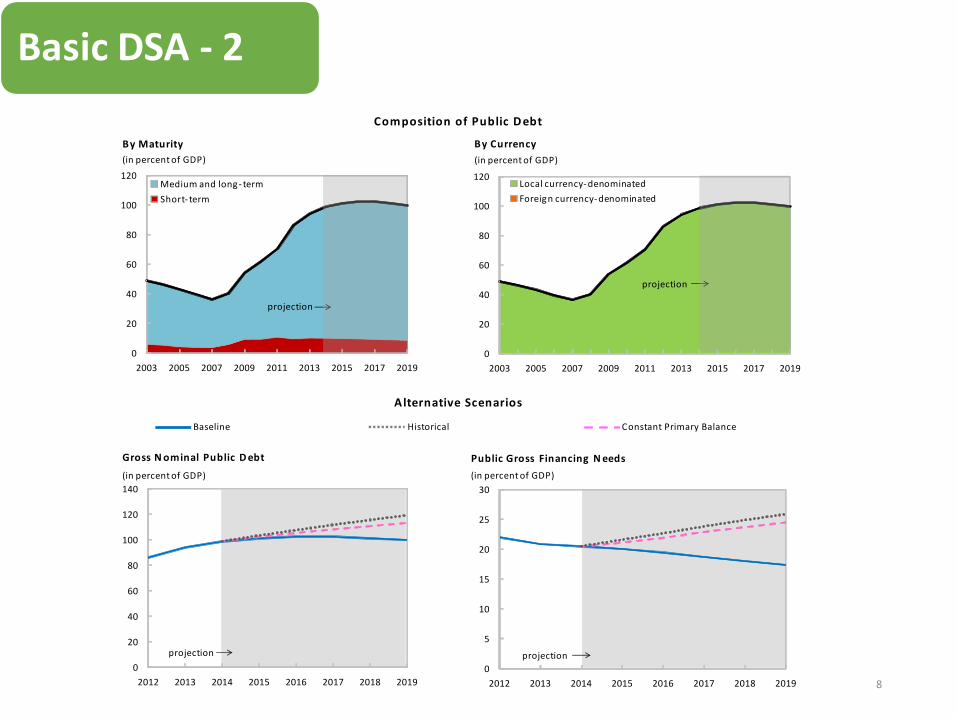

Basic DSA -‐ 2

Alternative Scenarios

Composition of Public Debt

Baseline Historical Constant Primary Balance

0

20

40

60

80

100

120

140

2012 2013 2014 2015 2016 2017 2018 2019

Gross Nominal Public Debt(in percent of GDP)

projection0

5

10

15

20

25

30

2012 2013 2014 2015 2016 2017 2018 2019

Public Gross Financing Needs(in percent of GDP)

projection

0

20

40

60

80

100

120

2003 2005 2007 2009 2011 2013 2015 2017 2019

By Maturity

Medium and long-‐ termShort-‐ term

projection

(in percent of GDP)

0

20

40

60

80

100

120

2003 2005 2007 2009 2011 2013 2015 2017 2019

By Currency

Local currency-‐denominatedForeign currency-‐denominated

projection

(in percent of GDP)

8

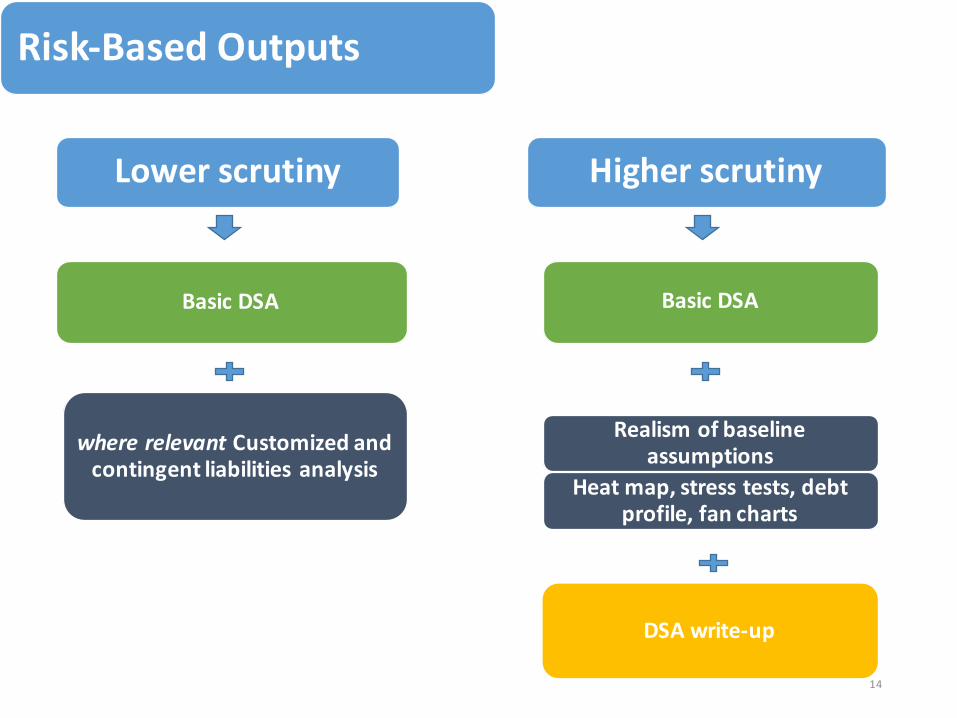

Risk-‐Based Outputs

Basic DSA

DSA write-‐up

Basic DSA

Realism of baseline assumptions

Heat map, stress tests, debt profile, fan charts

where relevant Customized and contingent liabilities analysis

Lower scrutiny Higher scrutiny

9

Realism of Baseline: Higher Scrutiny Cases

10

Realism of Baseline

Source : IMF Staff.1/ Plotted distribution includes surveillance countries, percentile rank refers to all countries.2/ Projections made in the spring WEO vintage of the preceding year.3/ Not applicable for Italy.4/ Data cover annual obervations from 1990 to 2011 for advanced and emerg ing economies with debt g reater than 60 percent of GDP. Percent of sample on vertical axis. 5/ For Italy the bulk of the adjustment already occurred in 2012 and the pace of consolidation slows to 1 percent of GDP in 2013.

Italy Public DSA -‐ Realism of Baseline Assumptions

Forecast Track Record, versus surveillance countries

Boom-‐Bust Analysis 3/Assessing the Realism of Projected Fiscal Adjustment

-‐10

-‐8

-‐6

-‐4

-‐2

0

2

4

6

2004 2005 2006 2007 2008 2009 2010 2011 2012Year 2/

Real GDP Growth

Interquartile range (25-‐75)MedianItaly forecast error

-‐ 1.467%Has a percentile rank of:

Italy median forecast error, 2004-‐2012:

Distribution of forecast errors: 1/

(in percent, actual-‐projection)

-‐10

-‐8

-‐6

-‐4

-‐2

0

2

4

2004 2005 2006 2007 2008 2009 2010 2011 2012Year 2/

Primary Balance

Interquartile range (25-‐75)MedianItaly forecast error

0.4968%Has a percentile rank of:

Italy median forecast error, 2004-‐2012:

Distribution of forecast errors: 1/

(in percent of GDP, actual-‐projection)

-‐6

-‐4

-‐2

0

2

4

6

8

10

2004 2005 2006 2007 2008 2009 2010 2011 2012Year 2/

Inf lation (Deflator)

Interquartile range (25-‐75)MedianItaly forecast error

-‐ 0.1713%Has a percentile rank of:

Italy median forecast error, 2004-‐2012:

Distribution of forecast errors: 1/

(in percent, actual-‐projection)

pessim

istic

optim

istic

-‐6

-‐4

-‐2

0

2

4

6

8

t-‐5 t-‐4 t-‐3 t-‐2 t-‐1 t t+ 1 t+ 2 t+ 3 t+ 4 t+ 5

Real GDP g rowth

Italy(in percent)

0

2

4

6

8

10

12

14

Less -‐4 -‐3 -‐2 -‐1 0 1 2 3 4 5 6 7 8

D istribution 4/

Italy

3-‐Year Adjustment in Cyclically-‐Adjusted Primary Balance (CAPB) 5/(Percent of GDP)

More

3-‐year CAPB adjustment g reater than 3 percent of

GDP in approx. top quartilehas a percentile rank of 18%

0

2

4

6

8

10

12

Less -‐4 -‐3 -‐2 -‐1 0 1 2 3 4 5 6 7 8

D istribution 4/

Italy

3-‐Year Averag e Level of Cyclically-‐Adjusted Primary Balance (CAPB)(Percent of GDP)

More

3-‐year average CAPB level g reater than 3.5 percent of GDP in approx. top quartilehas a percentile

rank of 9%

11

Forecast Track Record

-‐10

-‐8

-‐6

-‐4

-‐2

0

2

4

6

2005 2006 2007 2008 2009 2010 2011 2012 2013Year 2/

Real GDP Growth

Interquartile range (25-‐75)MedianExample forecast error

-‐ 1.4910%Has a percentile rank of:

Example median forecast error, 2005-‐2013:

Distribution of forecast errors: 1/

(in percent, actual-‐projection)

-‐10

-‐8

-‐6

-‐4

-‐2

0

2

4

2005 2006 2007 2008 2009 2010 2011 2012 2013Year 2/

Primary Balance

Interquartile range (25-‐75)MedianExample forecast error

0.4975%Has a percentile rank of:

Example median forecast error, 2005-‐2013:

Distribution of forecast errors: 1/

(in percent of GDP, actual-‐projection)

12

Projected Fiscal Adjustment

0

2

4

6

8

10

12

14Less -‐4 -‐3 -‐2 -‐1 0 1 2 3 4 5 6 7 8

D istribution 4/

Example

3-‐Year Adjustment in Cyclically-‐Adjusted Primary Balance (CAPB)(Percent of GDP)

More

13

Risk-‐Based Outputs

Basic DSA

DSA write-‐up

Basic DSA

Realism of baseline assumptions

Heat map, stress tests, debt profile, fan charts

where relevant Customized and contingent liabilities analysis

Lower scrutiny Higher scrutiny

14

Three additional modules: Heat Map, Debt Profile, Fan Charts

15

Heat Map

Heat Map

16

Heat Map

17

Stress Tests

18

Snap Shot of recent DSAs for G20 Countries: Debt Level

AE/EM Scrutiny Country

Debt to GDP Growth Shock

Primary Balance Shock

Interest Rate Shock

Exchange Rate Shock

Conting ent Liability Shock

AM Higher Canada 86.8 3 3 3 3 0AM Higher France 94.3 3 3 3 3 0AM Higher Germany 75.1 1 1 1 1 0AM Higher Italy 135.2 3 3 3 3 3AM Higher Japan 243.2 3 3 3 3 3AM Higher Spain 98.7 3 3 3 3 3AM Higher United Kingdom 92.0 3 3 3 3 3AM Higher United States 107.3 3 3 3 3 3AM Lower Australia 31.2 1 1 1 1 1AM Lower Korea 37.7 1 1 1 1 0

EM Higher Brazil 72.0 3 3 3 3 3EM Higher India 67.3 2 1 1 1 2EM Higher Mexico 47.8 1 1 1 1 0EM Higher South Africa 43.8 1 1 1 1 0EM Higher Turkey 35.4 1 1 1 1 1EM Lower China 18.3 1 1 1 1 1EM Lower Indonesia 26.8 1 1 1 1 0EM Lower Russia 15.5 1 1 1 1 0EM Lower Saudi Arabia 2.6 1 1 1 1 019

Snap Shot of recent DSAs for G20 Countries: Gross Financing Needs

AE/EM Scrutiny Country

GFN to GDP Growth Shock

Primary Balance Shock

Interest Rate Shock

Exchange Rate Shock

Conting ent Liability Shock

AM Higher Canada 18.3 3.0 3.0 3.0 3.0 0.0AM Higher France 8.8 1.0 1.0 1.0 1.0 0.0AM Higher Germany 15.4 1.0 1.0 1.0 1.0 0.0AM Higher Italy 23.8 3.0 3.0 3.0 3.0 3.0AM Higher Japan 54.8 3.0 3.0 3.0 3.0 3.0AM Higher Spain 20.5 3.0 3.0 3.0 3.0 3.0AM Higher United Kingdom 11.7 1.0 1.0 1.0 1.0 2.0AM Higher United States 22.9 3.0 3.0 3.0 3.0 3.0AM Lower Australia 3.7 1.0 1.0 1.0 1.0 2.0AM Lower Korea 6.4 1.0 1.0 1.0 1.0 0.0

EM Higher Brazil 14.4 3.0 3.0 3.0 3.0 3.0EM Higher India 13.1 2.0 1.0 1.0 1.0 2.0EM Higher Mexico 10.9 1.0 1.0 1.0 1.0 0.0EM Higher South Africa 12.0 2 2 1 1 0EM Higher Turkey 10.4 1 1 1 1 2EM Lower China 1.0 1 1 1 1 2EM Lower Indonesia 4.0 1 1 1 1 0EM Lower Russia 2.0 1 1 1 1 0EM Lower Saudi Arabia -‐2.5 1 2 1 1 0

20

Risk-‐Based Outputs

Basic DSA

DSA write-‐up

Basic DSA

Realism of baseline assumptions

Heat map, stress tests, debt profile, fan charts

where relevant Customized and contingent liabilities analysis

Lower scrutiny Higher scrutiny

21

DSA Write Up

Presents overall assessment of debt sustainability risks

Highlights vulnerabilities and country specific circumstances that mitigate or amplify risks

Discusses background and key assumptions including realism of the baseline

22

Thank you!

23

Additional slides

24

Fan Charts: Stochastic Simulations of Debt Paths

Evolution of Predictive Densities of Gross Nominal Public Debt(in percent of GDP)

0

20

40

60

80

100

120

140

2012 2013 2014 2015 2016 2017 2018 2019

10th-‐25th 25th-‐75th 75th-‐90thPercentiles:Baseline

Symmetric Distribution

0

20

40

60

80

100

120

140

160

2012 2013 2014 2015 2016 2017 2018 2019

Restricted (Asymmetric) Distribution

no restriction on the g rowth rate shockno restriction on the interest rate shock0 is the max positive pb shock (percent GDP)no restriction on the exchange rate shock

Restrictions on upside shocks:

25

Debt Profile

Example Upper early warningLower early warning(Indicators vis-‐à-‐vis risk assessment benchmarks, in 2013)

Debt Profile Vulnerabilities

1 2

400

600

165 bp

1 2

17

25

35%

1 2

1

1.5

-‐0.4%1 2

Bond spreadExternal Financing

Requirement

Annual Chang e in Short-‐Term Public

Debt

Public Debt in Foreig n Currency

(in basis points) 4/ (in percent of GDP) 5/ (in percent of total) (in percent of total)

30

4535%

1 2

Public Debt H eld by Non-‐Residents

(in percent of total)

26

Snap Shot of recent DSAs for G20 Countries: Debt Profile

AE/EM Scrutiny Country

Market Perception

External Financing Requirement

Change in the Share of ST Debt

Public Debt Held by Non-‐Residents

Foreig n Currency Debt

AM Higher Canada 1 3 1 1 0AM Higher France 1 1 1 3 0AM Higher Germany 1 0 1 3 0AM Higher Italy 1 3 1 1 0AM Higher Japan 1 1 1 1 0AM Higher Spain 1 3 1 2 0AM Higher United Kingdom 1 1 1 1 0AM Higher United States 1 3 1 2 0AM Lower Australia 1 0 1 3 0AM Lower Korea 1 0 1 1 0

EM Higher Brazil 2 2 1 2 1EM Higher India 2 2 1 1 1EM Higher Mexico 1 2 2 3 2EM Higher South Africa 2 2 1 2 1EM Higher Turkey 2 3 2 2 2EM Lower China 1 1 1 1 1EM Lower Indonesia 2 0 2 3 2EM Lower Russia 0 2 1 1 1EM Lower Saudi Arabia 1 0 1 0 1

27