PTTEP Canada International Finance Limited -...

290

PTTEP Canada International Finance Limited (incorporated in the Province of Alberta, Canada with limited liability) Guaranteed by PTT Exploration and Production Public Company Limited (registered in the Kingdom of Thailand as a public company with limited liability) U.S.$700,000,000 5.692% Senior Notes due 2021 Interest Payable October 5 and April 5 Issue Price: 100.0% PTTEP Canada International Finance Limited, a company with limited liability incorporated under the laws of the Province of Alberta, Canada (the “Issuer”), is offering U.S.$700,000,000 aggregate principal amount of its 5.692% Senior Notes due 2021 (the “Notes”). The Notes will mature on April 5, 2021. Interest on the Notes will be payable semi-annually and interest will accrue from April 5, 2011, and the first payment date is October 5, 2011. The Notes will be unsecured, rank equally with all of the Issuer’s existing and future senior debt and senior to all of the Issuer’s existing and future subordinated debt. The Notes will be effectively subordinated to all of the Issuer’s future secured debt to the extent of the value of the assets securing such debt and effectively subordinated to all future debt of the Issuer’s subsidiaries. The Notes will be guaranteed (the “Guarantee”) on a senior basis by PTT Exploration and Production Public Company Limited (“PTTEP”). The Guarantee will be unsecured, rank equally with all of PTTEP’s existing and future senior debt and senior to all of PTTEP’s existing and future subordinated debt. The Issuer may redeem the Notes in whole, but not in part, at any time at a price equal to their principal amount plus any accrued but unpaid interest, in the event of certain tax changes as described under “Description of the Notes — Optional Tax Redemption.” For a more detailed description of the Notes, see “Description of the Notes” beginning on page 102. See “Risk Factors” beginning on page 14 for a discussion of certain risks that you should consider in connection with an investment in the Notes. The Notes and the related Guarantee have not been and will not be registered under the United States Securities Act of 1933, as amended (the “Securities Act”), or with any securities regulatory authority of any State or other jurisdiction of the United States. Accordingly, the Notes and the related Guarantee are being offered and sold to non-U.S. persons in offshore transactions in reliance on Regulation S under the Securities Act (“Regulation S”) and within the United States only to qualified institutional buyers (“QIBs”) in reliance on Rule 144A (“Rule 144A”) under the Securities Act. Prospective purchasers that are QIBs as defined under Rule 144A are hereby notified that the sellers of the Notes and the related Guarantee may be relying on the exemption from the provisions of Section 5 of the Securities Act provided by Rule 144A. The Notes may not be offered or sold in Canada or to or for the benefit of residents thereof except to “accredited investors” as defined in National Instrument (Canada) 45-106 “Prospectus and Registration Exemptions” (“Accredited Investors”) or, as the case may be, “permitted clients” as defined in National Instrument (Canada) 31-103 “Registration Requirements and Exemptions” (“Permitted Clients”). For a description of restrictions on offers, sales and transfers of the Notes and distribution of this Offering Memorandum, see “Plan of Distribution” and “Transfer Restrictions.” Application has been made to the Singapore Exchange Securities Trading Limited (“SGX-ST”) for the listing of the Notes on the Official List of the SGX-ST. Such approval will be granted when the Notes have been admitted to the Official List of the SGX-ST. The SGX-ST assumes no responsibility for the correctness of any statements made, reports contained or opinions expressed contained herein. Admission of the Notes to the Official List of the SGX-ST is not to be taken as an indication of the merits of the Notes, the Guarantee, the Issuer, the Guarantor or its subsidiaries. The Notes will be traded on the SGX-ST in a minimum board lot size of U.S.$200,000 for as long as the Notes are listed on the SGX-ST. The Issuer expects that delivery of the Notes will be made to investors in book-entry form through The Depository Trust Company (“DTC”) for the accounts of its direct and indirect participants, including Euroclear Bank S.A./N.V. and Clearstream, Banking, société anonyme (“Clearstream, Banking”), on or about April 5, 2011 (or such other time and date as the Issuer and Barclays Bank PLC may agree). Lead Manager and Bookrunner Barclays Capital The date of this Offering Memorandum is March 29, 2011.

-

Upload

truongnguyet -

Category

Documents

-

view

230 -

download

3

Transcript of PTTEP Canada International Finance Limited -...

PTTEP Canada International Finance Limited(incorporated in the Province of Alberta, Canada with limited liability)

Guaranteed by

PTT Exploration and Production Public Company Limited(registered in the Kingdom of Thailand as a public company with limited liability)

U.S.$700,000,000

5.692% Senior Notes due 2021

Interest Payable October 5 and April 5

Issue Price: 100.0%

PTTEP Canada International Finance Limited, a company with limited liability incorporated under the laws of theProvince of Alberta, Canada (the “Issuer”), is offering U.S.$700,000,000 aggregate principal amount of its 5.692% SeniorNotes due 2021 (the “Notes”). The Notes will mature on April 5, 2021. Interest on the Notes will be payable semi-annuallyand interest will accrue from April 5, 2011, and the first payment date is October 5, 2011.

The Notes will be unsecured, rank equally with all of the Issuer’s existing and future senior debt and senior to all of theIssuer’s existing and future subordinated debt. The Notes will be effectively subordinated to all of the Issuer’s future secureddebt to the extent of the value of the assets securing such debt and effectively subordinated to all future debt of the Issuer’ssubsidiaries. The Notes will be guaranteed (the “Guarantee”) on a senior basis by PTT Exploration and Production PublicCompany Limited (“PTTEP”). The Guarantee will be unsecured, rank equally with all of PTTEP’s existing and future seniordebt and senior to all of PTTEP’s existing and future subordinated debt.

The Issuer may redeem the Notes in whole, but not in part, at any time at a price equal to their principal amount plusany accrued but unpaid interest, in the event of certain tax changes as described under “Description of the Notes — OptionalTax Redemption.” For a more detailed description of the Notes, see “Description of the Notes” beginning on page 102.

See “Risk Factors” beginning on page 14 for a discussion of certain risks that you should consider in connection withan investment in the Notes.

The Notes and the related Guarantee have not been and will not be registered under the United States Securities Act of1933, as amended (the “Securities Act”), or with any securities regulatory authority of any State or other jurisdiction of theUnited States. Accordingly, the Notes and the related Guarantee are being offered and sold to non-U.S. persons in offshoretransactions in reliance on Regulation S under the Securities Act (“Regulation S”) and within the United States only to qualifiedinstitutional buyers (“QIBs”) in reliance on Rule 144A (“Rule 144A”) under the Securities Act. Prospective purchasers that areQIBs as defined under Rule 144A are hereby notified that the sellers of the Notes and the related Guarantee may be relyingon the exemption from the provisions of Section 5 of the Securities Act provided by Rule 144A. The Notes may not be offeredor sold in Canada or to or for the benefit of residents thereof except to “accredited investors” as defined in National Instrument(Canada) 45-106 “Prospectus and Registration Exemptions” (“Accredited Investors”) or, as the case may be, “permittedclients” as defined in National Instrument (Canada) 31-103 “Registration Requirements and Exemptions” (“PermittedClients”). For a description of restrictions on offers, sales and transfers of the Notes and distribution of this OfferingMemorandum, see “Plan of Distribution” and “Transfer Restrictions.”

Application has been made to the Singapore Exchange Securities Trading Limited (“SGX-ST”) for the listing of theNotes on the Official List of the SGX-ST. Such approval will be granted when the Notes have been admitted to the OfficialList of the SGX-ST. The SGX-ST assumes no responsibility for the correctness of any statements made, reports contained oropinions expressed contained herein. Admission of the Notes to the Official List of the SGX-ST is not to be taken as anindication of the merits of the Notes, the Guarantee, the Issuer, the Guarantor or its subsidiaries. The Notes will be traded onthe SGX-ST in a minimum board lot size of U.S.$200,000 for as long as the Notes are listed on the SGX-ST.

The Issuer expects that delivery of the Notes will be made to investors in book-entry form through The Depository TrustCompany (“DTC”) for the accounts of its direct and indirect participants, including Euroclear Bank S.A./N.V. and Clearstream,Banking, société anonyme (“Clearstream, Banking”), on or about April 5, 2011 (or such other time and date as the Issuer andBarclays Bank PLC may agree).

Lead Manager and Bookrunner

Barclays Capital

The date of this Offering Memorandum is March 29, 2011.

You should rely only on the information contained in this Offering Memorandum or to which the Issuer andthe Guarantor have referred you. The Issuer and the Guarantor have not authorized anyone to provide you withinformation that is different. This Offering Memorandum may only be used where it is legal to sell these securities.The information in this Offering Memorandum may only be accurate as of the date of this Offering Memorandum.

The Issuer and the Guarantor, to the best of their knowledge and belief, having made all reasonable enquires,confirm that (i) this Offering Memorandum contains all information with respect to the Issuer, the Guarantor andthe Notes which is material in the context of the issue and offering of the Notes, (ii) the statements containedherein relating to the Issuer and the Guarantor and the Notes are in every material particular true and accurate andnot misleading, (iii) the opinions and intentions expressed in this Offering Memorandum with regard to the Issueror the Guarantor are honestly held, have been reached after considering all relevant circumstances and are basedon reasonable assumptions, (iv) there are no other facts in relation to the Issuer and the Guarantor or the Notesthe omission of which would, in the context of the issue and offering of the Notes, make any statement in thisOffering Memorandum misleading in any material respect and (v) all reasonable enquiries have been made by theIssuer and the Guarantor to ascertain such facts and to verify the accuracy of all such information and statements.

The Issuer and the Guarantor accept responsibility for the information contained in this OfferingMemorandum. The Issuer and the Guarantor are furnishing this Offering Memorandum on a confidential basis inconnection with an offering exempt from registration under the Securities Act and applicable state securities lawssolely for the purpose of enabling a prospective investor to consider the purchase of the Notes. The informationcontained in this Offering Memorandum has been provided by the Issuer and the Guarantor and other sourcesidentified in this Offering Memorandum. None of the Trustee, Paying Agent, Registrar, Transfer Agents (each asdefined below) or Barclays Bank PLC (the “Initial Purchaser”) has independently verified the informationcontained in this Offering Memorandum. No representation or warranty, express or implied, is made by the InitialPurchaser of the Notes or by their respective U.S. selling agents as to the accuracy or completeness of suchinformation, and nothing contained in this Offering Memorandum and appendices is, or shall be relied upon as,a promise or representation by the Initial Purchaser or such agents and no responsibility or liability is accepted byany of them as to the accuracy or completeness of the information contained or incorporated in this OfferingMemorandum or any other information provided by the Issuer or the Guarantor in connection with the issue ofthe Notes and the Guarantee. None of the Trustee, Paying Agent, Registrar, Transfer Agents (each as definedbelow) or the Initial Purchaser accepts any liability in relation to the information contained or incorporated byreference in this Offering Memorandum or any other information provided by the Issuer or the Guarantor inconnection with the issue of the Notes. Advisers or consultants named in this Offering Memorandum have actedpursuant to the terms of their respective engagements and do not make, and should not be taken to have verified,any statement or information in this Offering Memorandum unless expressly stated otherwise. Any reproductionor distribution of this Offering Memorandum, in whole or in part, and any disclosure of its contents or use of anyinformation herein is prohibited, except to the extent such information is otherwise publicly available. You shouldbe aware that since the date of this Offering Memorandum there may have been changes in PTTEP’s or theIssuer’s business or otherwise that could affect the accuracy or completeness of the information set out in thisOffering Memorandum.

PTTEP’s consolidated financial statements as presented in this Offering Memorandum are prepared andpresented in accordance with generally accepted accounting principles in Thailand (“Thai GAAP”) and reportingpractices in Thailand, which differ in certain significant respects from International Financial Reporting Standards(“IFRS”). For a discussion of differences between Thai GAAP and IFRS that are relevant to PTTEP’s financialstatements, see “Summary of Principal Differences Between Thai GAAP and IFRS.” Potential investors shouldconsult their own professional advisors for an understanding of the differences between Thai GAAP and IFRS, andhow these differences affect the financial information contained in this Offering Memorandum. This OfferingMemorandum should not be considered as a recommendation by the Initial Purchaser that any recipient of thisOffering Memorandum should purchase the Notes.

The securities are subject to restrictions on transferability and resale and may not be transferred or resoldexcept as permitted under the Securities Act and applicable state securities laws pursuant to registration orexemption from registration. You should be aware that you may be required to bear the risk of an investment inthe Notes for an indefinite period of time.

i

Each person receiving this Offering Memorandum acknowledges that: (i) such person has not relied on theInitial Purchaser or any person affiliated with the Initial Purchaser in connection with any investigation of theaccuracy of such information or its investment decision; and (ii) no person has been authorized to give anyinformation or to make any representation concerning the Issuer and/or the Guarantor, their respective subsidiariesand affiliates, the Notes or the Guarantee (other than as contained herein and information given by the dulyauthorized officers and employees of the Issuer and/or the Guarantor in connection with investors’ examinationof the Guarantor and its subsidiaries (including the Issuer) and the terms of this offering of the Notes and theGuarantee (this “Offering”)) and, if given or made, any such other information or representation should not berelied upon as having been authorized by the Issuer, the Guarantor or the Initial Purchaser.

The Notes and the related Guarantee have not been approved or disapproved by any United Statesfederal or state securities commission or regulatory authority (including the United States Securities andExchange Commission) or any securities regulatory body in Canada, nor have any of the foregoingauthorities passed upon or endorsed the merits of this Offering or the accuracy or adequacy of this OfferingMemorandum. Any representation to the contrary is a criminal offense in the United States. Prospectivepurchasers are hereby notified that sellers of the Notes may be relying on the exemption from the provisionsof Section 5 of the Securities Act provided by Rule 144A.

The distribution of this Offering Memorandum and this Offering may in certain jurisdictions be restrictedby law. Persons into whose possession this Offering Memorandum comes are required by the Issuer, the Guarantorand the Initial Purchaser to inform themselves about and to observe any such restrictions. For a description of therestrictions on offers, sales and resales of the Notes and the distribution of this Offering Memorandum, see “Planof Distribution” and “Transfer Restrictions” below.

In making an investment decision, you must rely on your own examination of the Issuer and the Guarantorand the terms of this Offering, including the merits and risks involved. The Issuer and the Guarantor are notmaking any representation to you regarding the legality of an investment in the Notes or the Guarantee by youunder any legal, investment or similar laws or regulations. You should not consider any information in thisOffering Memorandum to be legal, business or tax advice. You should consult your own attorney, business advisorand tax advisor for legal, business and tax advice regarding an investment in the Notes and the Guarantee.

The Issuer and the Guarantor reserve the right to withdraw this Offering at any time, and the InitialPurchaser reserve the right to reject any commitment to subscribe for the Notes in whole or in part and to allotto any prospective purchaser less than the full amount of the Notes sought by such purchaser. The Initial Purchaserand certain related entities may acquire for their own account a portion of the Notes.

In connection with this Offering, certain persons participating in the Offering may engage in transactionsthat stabilize, maintain or otherwise affect the price of the Notes outside of Canada and on a financial marketoperated outside of Canada. Specifically, the Initial Purchaser may bid for and purchase Notes in the open marketto stabilize the price of the Notes. The Initial Purchaser may also over allot the Offering, creating a syndicate shortposition. In addition, the Initial Purchaser may bid for and may stabilize or maintain the market price of the Notesabove market levels that might otherwise prevail. The Initial Purchaser is not required to engage in these activities,and may end these activities at any time in their sole discretion without prior notice. These activities will beundertaken solely for the account of Initial Purchaser, and not for and on behalf of the Issuer or the Guarantor.

Notwithstanding anything in this Offering Memorandum to the contrary, each investor in the Notes (and anyemployee, representative, or other agent of any investor) may disclose to any and all persons, without limitationof any kind, the U.S. federal tax treatment and the U.S. federal tax structure of the transactions contemplated bythis Offering Memorandum and all materials of any kind (including opinions or other tax analyses) that areprovided to it relating to such U.S. federal tax treatment and U.S. federal tax structure.

ii

UNITED STATES INTERNAL REVENUE SERVICE CIRCULAR 230 DISCLOSURE

PURSUANT TO U.S. INTERNAL REVENUE SERVICE CIRCULAR 230, THE ISSUER HEREBYINFORMS YOU THAT THE DESCRIPTION SET FORTH HEREIN WITH RESPECT TO U.S.FEDERAL TAX ISSUES WAS NOT INTENDED OR WRITTEN TO BE USED, AND SUCHDESCRIPTION CANNOT BE USED BY ANY TAXPAYER, FOR THE PURPOSE OF AVOIDING ANYPENALTIES THAT MAY BE IMPOSED ON THE TAXPAYER UNDER THE UNITED STATESINTERNAL REVENUE CODE OF 1986, AS AMENDED. SUCH DESCRIPTION WAS WRITTEN TOSUPPORT THE PROMOTION OR MARKETING OF THE NOTES. TAXPAYERS SHOULD SEEKADVICE BASED ON THEIR PARTICULAR CIRCUMSTANCES FROM AN INDEPENDENT TAXADVISOR.

NO OFFERS OR SALES OF THE NOTES OFFERED PURSUANT TO THIS OFFERINGMEMORANDUM MAY BE MADE IN THAILAND.

NOTICE TO NEW HAMPSHIRE RESIDENTS

NEITHER THE FACT THAT A REGISTRATION STATEMENT OR ANAPPLICATION FOR A LICENSE HAS BEEN FILED UNDER CHAPTER 421-B OFTHE NEW HAMPSHIRE REVISED STATUTES WITH THE STATE OF NEWHAMPSHIRE NOR THE FACT THAT A SECURITY IS EFFECTIVELYREGISTERED OR A PERSON IS LICENSED IN THE STATE OF NEW HAMPSHIRECONSTITUTES A FINDING BY THE SECRETARY OF STATE OF NEWHAMPSHIRE THAT ANY DOCUMENT FILED UNDER RSA 421-B IS TRUE,COMPLETE AND NOT MISLEADING. NEITHER ANY SUCH FACT NOR THEFACT THAT AN EXEMPTION OR EXCEPTION IS AVAILABLE FOR A SECURITYOR A TRANSACTION MEANS THAT THE SECRETARY OF STATE HAS PASSED INANY WAY UPON THE MERITS OR QUALIFICATIONS OF, OR RECOMMENDEDOR GIVEN APPROVAL TO, ANY PERSON, SECURITY OR TRANSACTION. IT ISUNLAWFUL TO MAKE, OR CAUSE TO BE MADE, TO ANY PROSPECTIVEPURCHASER, CUSTOMER OR CLIENT ANY REPRESENTATION INCONSISTENTWITH THE PROVISIONS OF THIS PARAGRAPH.

AVAILABLE INFORMATION

To preserve the exemptions for resales and transfers pursuant to Rule 144A, the Issuer will furnish, upon therequest of a holder of the Notes, such information as is specified in paragraph (d)(4) of Rule 144A under theSecurities Act, to such holder or beneficial owner or to a prospective purchaser of the Notes or interest therein whois a “QIB” within the meaning of Rule 144A, in order to permit compliance by such holder or beneficial ownerwith Rule 144A in connection with the resale of such Notes or beneficial interest therein unless, at the time of suchrequest, the Issuer is subject to the reporting requirements of Section 13 or 15(d) of the United States SecuritiesExchange Act of 1934, as amended (the “Exchange Act”), or is included in the list of foreign private issuers thatclaim exemption from the registration requirements of Section 12(g) of the Exchange Act and therefore is requiredto furnish to the U.S. Securities and Exchange Commission certain information pursuant to Rule 12g3-2(b) underthe Exchange Act.

ENFORCEMENT OF CIVIL LIABILITIES

The Issuer is incorporated in the Province of Alberta, Canada and the Guarantor is incorporated in Thailand.The majority of the directors of the Issuer and all of the directors of the Guarantor are residents of Thailand. Asubstantial portion of the assets of the Issuer and the Guarantor, as the case may be, and the assets of theirrespective directors, are located in Canada or Thailand. As a result, you may not be able to:

• effect service of process upon the Issuer or the Guarantor or these persons outside Canada or Thailand;or

iii

• enforce against the Issuer or the Guarantor or their respective directors judgments obtained in courtsoutside of Canada or Thailand. These judgments include judgments relating to the federal securitieslaws of the United States.

The Issuer has been advised by its Canadian counsel, Stikeman Elliott LLP, that there is doubt as to theenforceability, in original actions in the courts of the Canada, of liabilities predicated solely on the federalsecurities law of the United Sates or any state thereof and as to the enforceability, in the courts of Canada, ofjudgments of U.S. courts obtained in actions predicated upon the civil liability provisions of the federal securitieslaw of the United States or any state thereof. Therefore, it may not be possible to enforce those judgments againstthe Issuer or its directors.

PTTEP’s Thai counsel, Allen & Overy (Thailand) Co., Ltd. has advised PTTEP that Thai courts will notenforce any judgment or order obtained outside Thailand, but a judgment or order from a foreign court, in thediscretion of a court in Thailand, may be admitted as evidence of an obligation in a new proceeding instituted inthat court, which will consider the issue or the evidence before it.

Under the Petroleum Act B.E. 2514 (1971) (as amended), the right to hold a petroleum concession shall notbe subject to execution of judgment. Thus, to the extent investors are entitled to bring a legal action againstPTTEP, they may be limited in their remedies or any recovery, and any Thai proceedings may be limiteddepending on the relevant court’s discretion.

FORWARD-LOOKING STATEMENTS

This Offering Memorandum includes forward-looking statements. These forward-looking statements relateto analyses and other information, which are based on forecasts of future results and estimates of amounts not yetdeterminable. These statements also relate to PTTEP’s future prospects, developments and business strategies.You are cautioned not to rely on these forward-looking statements.

These forward-looking statements include, without limitation, statements relating to:

• PTTEP’s future overall business development and economic performance;

• PTTEP’s estimated financial information regarding, and the future development and economicperformance of, its business;

• PTTEP’s future earnings, cash flow and financial position;

• PTTEP’s expansion plans;

• PTTEP’s business strategy;

• the amount and nature of future exploration, development and other capital expenditures required byPTTEP;

• wells to be drilled by PTTEP;

• future prices and demand for natural gas, crude oil and refined petroleum products;

• estimates of PTTEP’s proved reserves;

• Kai Kos Dehseh Oil Sands Project (“KKD”)’s future development plans, expansion and operations;and

• the liberalization of the Thai gas industry.

Although PTTEP’s management believes that its expectations as reflected by such forward-lookingstatements are reasonable based on information currently available to it, no assurances can be given that suchexpectations will prove to be correct. In addition, PTTEP’s management’s expectations with respect to itsexploration, production and development activities are subject to risks arising from the inherent difficulty ofpredicting the presence, yield or quality of oil and gas reserves, as well as unknown or unforeseen difficulties inextracting or transporting any oil or gas found, or doing so on a commercial basis.

iv

The forward-looking statements reflect PTTEP’s current views with respect to future events and are not aguarantee of future performance. Actual results may differ materially from information contained in theforward-looking statements as a result of a number of factors including:

• fluctuations in prices of natural gas, crude oil and condensate;

• change in estimates of reserves;

• the continued availability of capital and financing;

• general economic and business conditions both globally and regionally and energy demand and supplyin Thailand and Southeast Asia;

• the failure of PTTEP to continue to achieve exploration successes;

• failure or delays by PTTEP in achieving production from development projects or failure to achievetargeted production or sales volumes;

• the achievement of development plans and targets in relation to its projects, including KKD;

• liability for remedial actions and other damages under environmental regulations or associatedthird-party claims; and

• other factors beyond PTTEP’s control.

PTTEP’s risks are more specifically described in “Risk Factors.” If one or more of these risks oruncertainties materialize, or if the underlying assumptions prove incorrect, PTTEP’s actual results may varymaterially from those expected, estimated or projected. PTTEP does not undertake to update its forward-lookingstatements or risk factors to reflect future events or circumstances.

CERTAIN DEFINED TERMS AND CONVENTIONS

Market data and certain industry forecasts used throughout this Offering Memorandum were obtained frominternal surveys, market research, publicly available information and industry publications published by thirdparty sources that PTTEP believes are reliable. Such information has been accurately reproduced herein and, asfar as PTTEP is aware and is able to ascertain from information published by such third parties, no facts have beenomitted that would render the reproduced information inaccurate or misleading. Industry publications generallystate that the information that they contain has been obtained from sources believed to be reliable but that theaccuracy and completeness of that information is not guaranteed. Similarly, internal surveys, industry forecastsand market research, while believed to be reliable, have not been independently verified, and none of the Issuer,the Guarantor or the Initial Purchaser makes any representation as to the accuracy or completeness of thisinformation. The industry in which PTTEP operates is subject to a high degree of uncertainty and risks due to avariety of factors, including those described under “Risk Factors.” These and other factors could cause results todiffer materially from the information contained in such publications, surveys, forecasts and market research.

All references to “Thailand” or “Thai” herein are references to the Kingdom of Thailand. All references tothe “Government” herein are references to the Government of Thailand. All references to “Myanmar” arereferences to the Union of Myanmar, formerly known as Burma.

In this Offering Memorandum, unless otherwise specified or the context otherwise requires, “the Company,”“PTTEP” or “the Guarantor” refers to PTT Exploration and Production Public Company Limited and, unlessotherwise indicated or required by context, PTTEP’s consolidated subsidiaries.

All financial information, descriptions and other information in this Offering Memorandum regardingPTTEP’s activities, financial condition and results of operations are, unless otherwise indicated or required bycontext, presented on a consolidated basis.

v

In this Offering Memorandum, references to “$,” “U.S. dollars,” “U.S.$” and “dollars” are to the currencyof the United States of America, references to “Bt” and “Baht” are to the currency of Thailand and “CAD” and“Canadian dollar” are to the currency of Canada. PTTEP maintains its accounts in Baht and Statoil CanadaPartnership (“SCP”) maintains its accounts in Canadian dollars. This Offering Memorandum contains conversionsof certain amounts into dollars at specified rates solely for the convenience of the reader. Unless otherwiseindicated, all conversions of Baht to dollars have been made at the rate of Baht 30.296 = U.S.$1.00, the averageselling rate announced by the Bank of Thailand on December 30, 2010. See “Exchange Rate Information.” Norepresentation is made that the Baht or dollar amounts referred to herein could have been or could be convertedinto dollars or Baht, as the case may be, at this rate, at any particular rate or at all.

Any discrepancies in the tables included herein between totals and sums of the amounts listed are due torounding.

PRESENTATION OF OIL AND GAS RESERVES DATA

This Offering Memorandum includes estimates made by PTTEP of its gross proved reserves. Noindependent reserve report is available on the gross proved reserves of PTTEP. These estimates are based onPTTEP’s Classification of Petroleum Resources Guidelines, which is substantially similar to the standardsestablished by the Society of Petroleum Engineers (the “SPE”), the SPE Petroleum Resources ManagementSystem. Investors should note, however, that different reserves reporting systems employ different assumptions,and that, in particular, PTTEP’s Classification of Petroleum Resources Guidelines may differ from the standardsestablished by the United States Securities and Exchange Commission. In regards to the reserves and resourcesfigures provided for KKD, PTTEP references the figures from the independent report done by Sproule AssociatesLimited, which is based on the draft Canadian Oil and Gas Evaluation Handbook Vol. 3, Part 3 — DetailedGuidelines for Estimation and Classification of Bitumen and Steam Assisted Gravity Drainage (SAGD) Reservesand Resources, prepared jointly by the Society of Petroleum Evaluation Engineers (Calgary Chapter) and theCanadian Institute of Mining, Metallurgy & Petroleum (Petroleum Society) (the “COGE Handbook”). The COGEHandbook was reviewed in reference to the SPE Petroleum Resources Management System and there is nowbroad alignment between the COGE Handbook and the SPE definitions.

There are uncertainties inherent in estimating quantities of gross proved reserves and in the timing ofdevelopment expenditures and the projection of future rates of production. However, the proved reserve data setout in this Offering Memorandum represents estimates of a high confidence, which according to both the SPEPetroleum Resources Management System and the COGE Handbook, means at least a 90% chance that quantitiesactually recovered will equal or exceed the estimates.

There are numerous uncertainties inherent in estimating quantities of reserves, including many factorsbeyond the control of PTTEP. The reserve data set forth in this Offering Memorandum represent estimatesdetermined by PTTEP according to industry practice. In general, estimates of commercially recoverable oil andnatural gas reserves are based upon a number of variable factors and assumptions, such as geological andgeophysical characteristics of the reservoirs, historical production performance from the properties, the quality andquantity of technical and economic data, prevailing oil and gas prices applicable to a company’s production,engineering judgments, forward-looking commercial and market assumptions, the assumed effects of regulationby Government agencies and future operating costs. All such estimates involve uncertainties, and classificationsof reserves are only attempts to define the degree of likelihood that the reserves will result in revenue for PTTEP.For these reasons, estimates of the commercially recoverable oil and natural gas reserves attributable to anyparticular group of properties, classification of such reserves based on uncertainty of recovery and estimates offuture net revenues expected therefrom, prepared by different engineers or by the same engineers at differenttimes, may vary substantially. In addition, such estimates can be and will be subsequently revised as additionalpertinent data becomes available prompting revision. Actual recoverable reserves may vary significantly fromsuch estimates. See “Risk Factors — Risks Relating to PTTEP’s Business — The reserves data in this OfferingMemorandum are only estimates, there is no independent reserve report available for PTTEP and its actualproduction, revenues and expenditures with respect to its reserves may differ from these estimates.”

vi

When converting natural gas volumes to barrel of oil equivalent (“Boe”), PTTEP uses a formula where theBoe conversion is “volume (MMboe) = volume (BSCF) multiplied by the gross calorific value (“GCV”) of thepetroleum divided by 6,000.” The gross calorific values used to convert gas volume to barrels of oil equivalentare different and vary in each project depending on reservoir fluids composition. The gross calorific value usedfor BOE conversion in reserves estimations and annual production volumes are also different. Ones that used forreserves estimations are the estimated GCV of each project throughout its field life. The GCVs used for productionreports were the actual GCVs that were measured in each month. Generally, the assumed GCV is 1,000 BTU/Cf,so that 1 Boe is equal to 6 MSCF.

For a description of how certain terms relating to reserves and other data are used in this OfferingMemorandum, see “Glossary of Technical Terms.”

PRESENTATION OF FINANCIAL INFORMATION

PTTEP’s financial statements have been prepared in accordance with Thai GAAP. PTTEP’s reportingcurrency is the Thai Baht. After January 1, 2011, PTTEP’s financial statements will be prepared in accordancewith IFRS and the reporting currency will be U.S. dollars. See “Risk Factors — PTTEP may incur significant costsin preparing for and complying with IFRS and may not be able to fully comply with such standards.”

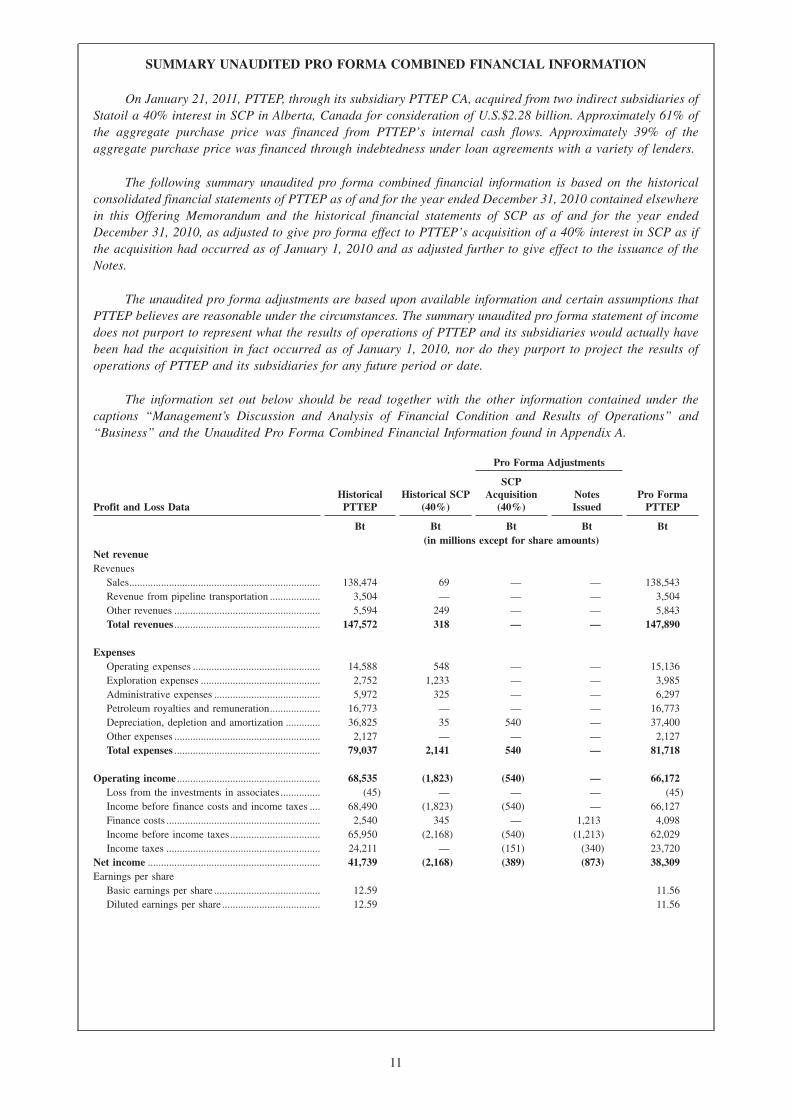

This Offering Memorandum includes unaudited pro forma combined financial information reflecting thecombined results of operations of PTTEP and PTTEP’s 40% interest in SCP, which owns KKD, acquired throughPTTEP’s subsidiary PTTEP Canada Limited (“PTTEP CA”) from two indirect subsidiaries of Statoil ASA(“Statoil”) on a pro forma basis as of and for the year ended December 31, 2010. All such pro forma financialinformation is unaudited and may not be indicative of the results of operations that actually would have beenachieved had PTTEP acquired its interest in SCP as of January 1, 2010 and do not purport to be indicative of futureresults. The audited financial statements of SCP as of and for the year ended December 31, 2010, were preparedin accordance with IFRS.

Certain numerical figures set out in this Offering Memorandum, including financial data presented inmillions or thousands, have been subject to rounding adjustments and, as a result, the totals of the data in thisOffering Memorandum may vary slightly from the actual arithmetic totals of such information. Percentages andamounts reflecting changes over time periods relating to financial and other data set forth in “Management’sDiscussion and Analysis of Financial Condition and Results of Operations” are calculated using the numerical datain PTTEP’s consolidated financial statements or the tabular presentation of other data (subject to rounding)contained in this Offering Memorandum, as applicable, and not using the numerical data in the narrativedescription thereof.

This Offering Memorandum contains supplemental non-GAAP financial measures and ratios that are notrequired by, or presented in accordance with, Thai GAAP.

The term “EBITDA” refers to earnings before interest expenses, taxes, depreciation and amortization.Earnings for calculating PTTEP’s EBITDA include sales revenue and revenue from pipeline transportation.

PTTEP believes that EBITDA is a widely accepted financial indicator of an entity’s operating performanceand an entity’s ability to incur and service debt. EBITDA should not be considered by an investor as alternativesto net income or income from operations, or as indicators of PTTEP’s operating performance or other combinedoperations or cash flow data prepared in accordance with generally accepted accounting principles, or as analternative to cash flows as a measure of liquidity. PTTEP’s computation of EBITDA may differ from similarlytitled computations of other companies.

Further, EBITDA is not a measurement of PTTEP’s financial performance or liquidity under Thai GAAPand should not be considered as an alternative to net income, gross revenues or any other performance measurederived in accordance with Thai GAAP or as an alternative to cash flow from operations or as a measure ofPTTEP’s liquidity.

The non-GAAP financial measures may not be comparable to other similarly titled measures of othercompanies and have limitations as analytical tools and should not be considered in isolation or as a substitute foranalysis of our operating results reported under Thai GAAP.

vii

TABLE OF CONTENTS

Page

OFFERING MEMORANDUM SUMMARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

THE OFFERING . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

SUMMARY HISTORICAL THAI GAAP CONSOLIDATED FINANCIAL DATA . . . . . . . . . . . . . 9

SUMMARY UNAUDITED PRO FORMA COMBINED FINANCIAL INFORMATION . . . . . . . . . 11

SUMMARY OPERATING, SALES AND ASSET DATA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

RISK FACTORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

USE OF PROCEEDS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

EXCHANGE RATE INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

THE ISSUER . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

CAPITALIZATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITIONAND RESULTS OF OPERATIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

THE PETROLEUM INDUSTRY IN THAILAND . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56

RELATIONSHIP WITH THE GOVERNMENT AND PTT AND REGULATORY MATTERS . . . . 61

PTTEP CORPORATE STRUCTURE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63

BUSINESS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64

PRINCIPAL SHAREHOLDERS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 96

MANAGEMENT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 97

DESCRIPTION OF THE NOTES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 102

TAXATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 115

PLAN OF DISTRIBUTION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 121

TRANSFER RESTRICTIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 126

LEGAL MATTERS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 129

INDEPENDENT ACCOUNTANTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 130

GENERAL INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 131

SUMMARY OF PRINCIPAL DIFFERENCES BETWEEN THAI GAAP AND IFRS . . . . . . . . . . . 132

GLOSSARY OF TECHNICAL TERMS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 140

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS AND AUDITOR’S REPORTS . . . . . F-1

viii

OFFERING MEMORANDUM SUMMARY

This summary may not contain all of the information that is important to you. You should read the entireOffering Memorandum, including the financial statements and related notes, before making an investmentdecision. You should pay special attention to the “Risk Factors” section beginning on page 13 of this OfferingMemorandum to determine whether an investment in the Notes is appropriate for you.

General

PTTEP’s principal activity is the petroleum exploration, production and development of interests in oil andnatural gas and crude oil properties and reserves in Thailand, in neighboring countries and elsewhereinternationally. PTTEP was incorporated in 1985 as the oil and natural gas exploration and production arm of PTT,a state enterprise established to develop and promote Thailand’s petroleum industry and to ensure the security ofThailand’s energy supply. PTT had a 65.32% ownership interest in the Company as of February 15, 2011.

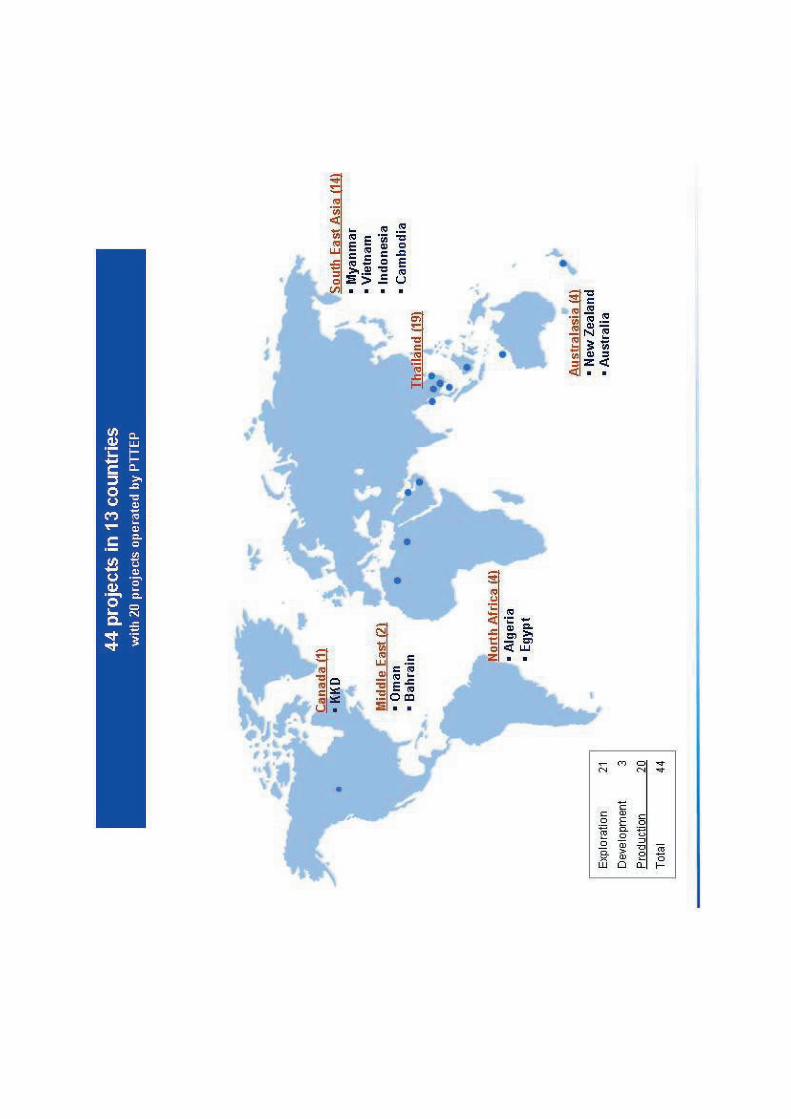

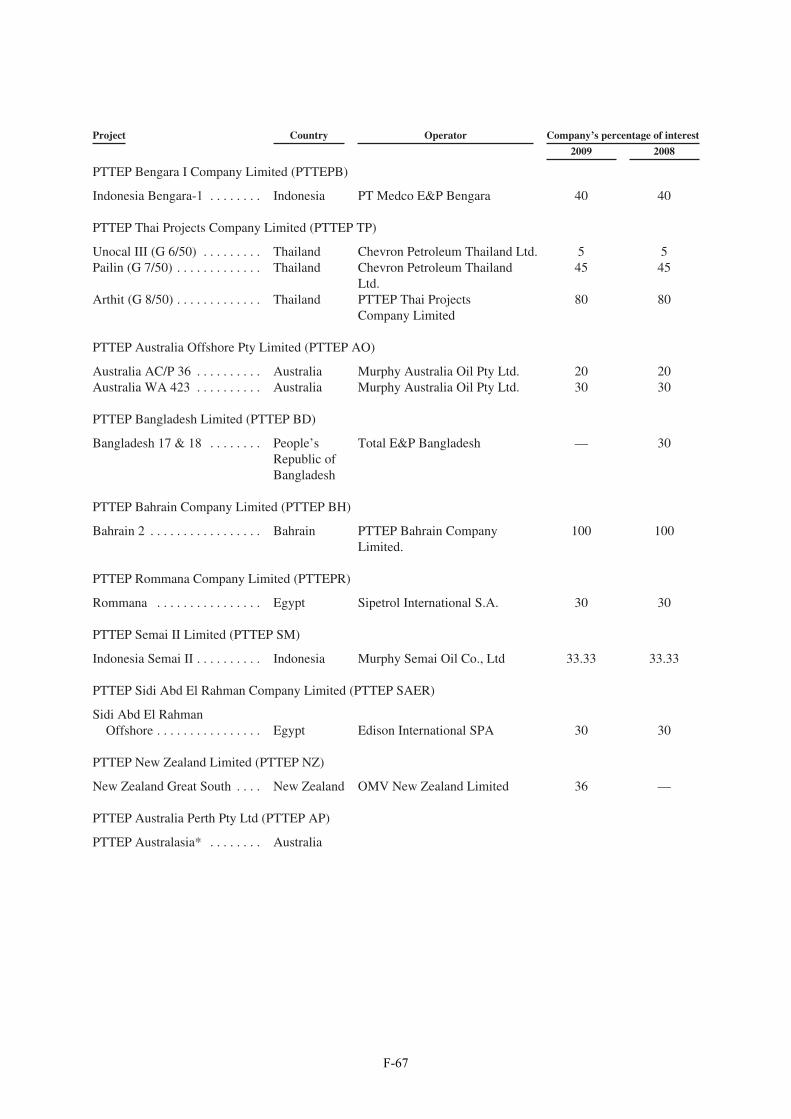

PTTEP conducts a substantial portion of its exploration and production activities through its workinginterests in petroleum concessions operated through joint ventures with international oil and gas companies. UnderPTTEP’s joint venture arrangements, one joint venture participant actively manages the concession as operator inaccordance with the terms of a joint venture agreement. As of January 31, 2011, PTTEP had participation interestsranging from 5.0% to 100.0% in 19 Thai projects, 14 regional projects in neighboring countries and 11international projects. Of these projects, PTTEP has participation interests ranging from 19.3% to 100.0% in fourinvestment projects in Myanmar. PTTEP is also the operator of seven Thai petroleum exploration and developmentprojects in which it holds a 100.0% interest.

PTTEP’s common stock was first listed on the Stock Exchange of Thailand in June 1993. PTTEP’s marketcapitalization as at February 28, 2011 was Baht 555,838 million, making it the second largest publicly tradedcompany in Thailand.

Competitive Strengths

PTTEP believes that its historical success and future prospects are directly related to a combination ofstrengths, including the following.

Leading regional exploration and production company with substantial international exposure

PTTEP is the largest publicly-listed oil and gas exploration and production company in Thailand and aleading oil and gas producer among publicly-listed oil companies in South East Asia. It is also one of the largestindependent exploration and production companies in South East Asia in terms of reserves and production, withgross proved reserves of 1,043 MMboe, as well as production of 304 Kboe/d for the year ended December 31,2010. Given its large size, the Company has the resources and expertise to serve as operator of many of its blocks.

PTTEP believes its large portfolio of blocks offers a diversification of reserves, production and explorationopportunities and risk. It has also diversified internationally, acquiring attractive assets in Australia, Canada, theMiddle East, and North Africa, in addition to acquiring assets in South East Asia. As of January 31, 2011, itsportfolio comprises a total of 44 projects, consisting of a combination of both oil and gas assets. The majority ofthe Company’s reserves are located in Thailand and nearby areas overlapping with Thailand’s neighbors (19blocks), out of which 14 are producing. The remaining 25 projects are located overseas across the Asia Pacific,North American, Middle Eastern and North African regions. The remaining projects, which are not currentlyproducing, are at various stages of exploration and development.

The Company believes its financial and operational strength allows it better access to the domestic andinternational capital markets to fund its acquisition and development costs, as demonstrated by its successfulprevious fund raisings in the capital markets.

Strong relationship with majority shareholder

PTTEP has a strong relationship with its majority shareholder, PTT. PTTEP was founded as the explorationand production arm of PTT in 1985. PTT had a 65.32% ownership interest in PTTEP as of February 15, 2011.Many of PTTEP’s directors and senior managers worked at PTT before working at PTTEP and several membersof PTT’s board of directors are also members of PTTEP’s board of directors.

1

PTT is Thailand’s national energy and petrochemical group and possesses a strong financial position andgovernment backing in the Thai petroleum markets. PTT also purchases substantially all of the natural gasproduction in Thailand, providing 98% of PTTEP’s natural gas sales revenue in 2010. PTT is the largest supplierof petroleum and petrochemical products in Thailand. The relationship with PTT also creates synergies betweenPTTEP and PTT in the natural gas value chain, ensuring access to petroleum production for PTT and a guaranteedcustomer relationship for PTTEP. PTT enjoys a natural monopoly as the owner and operator of Thailand’s entiregas transmission and distribution pipeline system, which PTTEP uses to transport natural gas to PTT. As agovernment corporation, PTT provides leverage and support for PTTEP’s relationships with other governmentbodies and agencies. PTTEP works closely and coordinates with PTT and related government agencies tocollectively outline and implement Thailand’s national petroleum supply plans and policies.

Experienced management team

PTTEP’s senior management team has extensive experience in the oil and gas industry, and most of itsexecutives have been with PTTEP or PTT since PTTEP’s inception in 1985. PTTEP’s management team and staffhave had the opportunity to work closely with foreign partners both within and outside Thailand. PTTEP has beenable to deploy experienced management team members across its geographic operations to implement projects andoversee operations. PTTEP believes that its management team has contributed significantly to its past success andwill continue to contribute to its future growth.

Well-positioned to benefit from Thailand’s increasing energy consumption

PTTEP’s role as the sole investment vehicle for the Government in undertaking exploration and productionactivities and developing a long-term natural gas supply for Thailand plays an important role in developingThailand’s hydrocarbon reserves. In 2010, PTTEP’s sales accounted for approximately 31% of total nationalproduction of petroleum products. In the year ended December 31, 2010, approximately 44% of Thailand’sprimary energy consumption was from natural gas and in that same period natural gas accounted for approximately72% of fuel for power generation by the Electricity Generating Authority of Thailand, independent powerproducers, and small power producers, PTT’s primary customers for natural gas. Natural gas consumption hasexperienced persistent growth, generating a growth rate of 13.1%, from 3,597 MMSCFD in 2009 to 4,039MMSCFD in 2010, according to EPPO.

Strong reserves base to support production growth

PTTEP’s proved undeveloped reserves accounted for approximately 55% of its 1,043 MMboe provedreserves as of December 31, 2010. PTTEP intends to utilize this proved undeveloped reserve base and otherreserve prospects to grow its production and sales. PTTEP has an established track record of growing its reservesand production: during 2010, PTTEP’s average daily sales volume increased approximately 13% compared to2009, while its compound average growth rate for the three years ended December 31, 2010 was 9.8%. Keyprojects for PTTEP’s growth include the development of Arthit North and MT-JDA.

Significant growth, stable margins and competitive cost structure

PTTEP’s sales volumes have increased at a compound annual growth rate of 9.8% over the past three years.This increase is due to contributions in the sales of petroleum from Arthit, which experienced its first full year ofproduction in 2009, Arthit North, which commenced production in 2009, and Malaysia-Thailand JointDevelopment Authority (“MTJDA”) project, which commenced production in February 2010. PTTEP’s EBITDAincreased in line with the sales growth, with a compound annual growth rate of 9.8% reaching Baht 101,708million (U.S.$3.4 billion) in 2010. Since 2008, PTTEP has also maintained EBITDA margins over 65.4%.PTTEP’s finding and development costs are low due to production sharing contracts with various foreign partners.In the years ended December 31, 2008, 2009 and 2010, PTTEP’s finding and development costs were U.S.$15.7per Boe, U.S.$11.1 per Boe and U.S.$13.6 per Boe, respectively. Low finding and development costs allow forthe capital-efficient growth of PTTEP’s business, while its low operating costs further enhance returns andoperating margins. In the years ended December 31, 2008, 2009 and 2010, PTTEP’s lifting costs were U.S.$2.46per Boe, U.S.$3.16 per Boe and U.S.$3.75 per Boe, respectively. PTTEP believes that this is significantly lowerthan the average lifting cost of most other exploration and production companies. Lifting costs consist of fieldoperating expenses. PTTEP kept its lifting costs low through various measures, including more efficient use ofoffshore infrastructure, the adoption of new technology in its operations, renegotiation of supply-chain costs,standardization among existing assets, as well as the adoption of an excellence program to further develop its

2

organizational capacity with a focus on organization restructuring, business process streamlining and optimizingresource allocation. PTTEP believes that its growth of EBITDA and maintenance of its EBITDA margin isevidence of PTTEP’s focused development objectives, synergies with PTT operations as well as its cost structure.These factors allow it to compete effectively, even in a low crude oil price environment.

Strategy

PTTEP’s primary objective as a leading exploration and production company is to enhance its position inthe Southeast Asian region and internationally. Significant elements of PTTEP’s strategy include the following:

Expanding its investment portfolio with a goal towards sustainable growth, and focus on growth by targetingselected acquisitions

PTTEP intends to capitalize on synergies with its subsidiaries and expand its investments and acquisitionsin particular areas including Southeast Asia, Canada and Australia. In addition, PTTEP plans to focus on areas orcountries that it believes have high petroleum potential and those where it has existing projects or interests tomaximize value, including Australia, Indonesia, Vietnam and Canada. PTTEP sees these developments as anopportunity to pursue acquisitions which would create value for it in the long term. PTTEP intends to focus mainlyon business development and transactions with respect to conventional exploration and production projects in thedevelopment and production phase and where the opportunities fit with PTTEP’s corporate culture. However, aswith the acquisition of SCP, PTTEP will also selectively pursue opportunities to invest in unconventionalexploration and production projects characterized by specialized technological expertise and high investment andunit costs (for example, oil sands, deepwater drilling and heavy oil). PTTEP is currently in the study phase ofdeveloping Floating Liquefied Natural Gas (“FLNG”) production, which is an emerging offshore productiontechnology to monetize stranded gas resources. The areas of commercial focus for FLNG production will be inthe Cash/Maple and Oliver fields in the Timor Sea. Both the oil sands and FLNG opportunities resulted fromPTTEP’s continued monitoring and research into “mega trends,” which may provide sustainable long-termgrowth.

Continuing to participate in key regional and international petroleum projects

Since PTTEP was founded as the exploration and production arm of PTT in 1985, PTTEP has benefited fromthe Government’s policy of encouraging Thai participation in exploration and production activities in the region.As a result, PTTEP has participated in key projects in its regional focus areas of the Gulf of Thailand and the Gulfof Martaban, which PTT believes are attractive exploration and development areas due to their reserve potential,relatively low geological risk and finding costs and a developing infrastructure network of gathering systems,pipelines and platforms.

In PTTEP’s early stages of development, working interests were acquired through Government rights.Subsequently, PTTEP successfully developed relationships with leading international oil and gas companies andhas independently negotiated interests in many of its projects. PTTEP has also been able to farm-in to numerousother projects in Thailand and internationally. To farm-in is to acquire an interest in a lease or concession ownedby another operator on which oil or gas has been discovered or is being produced.

PTTEP believes that with its growing regional knowledge base, technical capability and its closerelationships with PTT, the Government and international oil and gas companies, it is well positioned to continueto take advantage of favorable exploration and development opportunities in the region, particularly in Thailandand elsewhere in Southeast Asia, as well as internationally.

Maximize existing assets through production plateau extension initiatives and implementing supply chainsecurity

PTTEP’s sales volume averaged 264,575 Boe/d in 2010, approximately 13% higher than its average salesvolume of 233,756 Boe/d in 2009. From 2008 to 2010, the compound annual growth rate of petroleum sales byvolume was 9.8%. PTTEP intends to increase the production level, production plateau period and production lifeof its existing assets by focusing on maximizing the recovery at its producing projects. PTTEP intends to continueactively developing its large undeveloped proved reserves which accounted for 55% of its proved reserves as ofDecember 31, 2010. PTTEP also expects further resources to be discovered by continuing to explore the areas nearits existing projects. In 2010, PTTEP succeeded in discovering petroleum in 15 of 18 exploration and appraisalwells drilled, which is equivalent to a drilling success rate of 83%.

3

PTTEP is dedicated to ensuring that Thailand has a secure supply of energy to meet its current and futureneeds. To respond to the dynamics of energy demand, PTTEP has closely monitored petroleum demands and hasbeen coordinating with PTT and related government agencies to collectively outline the optimal supply plan.PTTEP also has reviewed and adjusted its production as well as project development plans to match energyrequirements. In 2010, PTTEP conducted a study, provided a detailed evaluation of PTTEP’s competitiveness inselected countries and business technologies, the result of which was integrated into PTTEP’s overall growthstrategy roadmap with prioritized countries and technology to be pursued.

Implementing cost savings initiatives to optimize value from existing assets

PTTEP periodically reviews investment plans for its existing assets and has rescheduled investments witha view toward optimizing asset value. In particular, PTTEP focuses on cost savings initiatives such asrenegotiating procurement spending, so that product quantities and procurement periods are clearly defined inorder to coincide with the prevailing market situation. PTTEP also plans to standardize these initiatives across itsexisting assets. Moreover, PTTEP has initiated programs to improve its project management performance and theoverall efficiency of its production and operation activities.

Strengthen the capability of its operating model through enhancing organizational excellence in accordancewith international standards

PTTEP is instituting programs to enhance the efficiency and productivity of its business operations includingmeasures to accelerate the recruitment process in support of its business expansion activities, as well as toaccelerate the development and improve the skills of its personnel. On the technological side, PTTEP strives tocontinually gain new drilling and exploration competencies. PTTEP will complement these initiatives bydeveloping its structured leadership development program. PTTEP hopes that their initiatives will allow PTTEPto maintain its high level of corporate governance. PTTEP is also strengthening its organizational support tobusiness expansion and long-term growth through reviews and streamlining of the procurement process, theinvestment process and the portfolio management process.

Recent Developments

Acquisition of an Interest in the Kai Kos Dehseh Project

On January 21, 2011, PTTEP, through its subsidiary, PTTEP CA, acquired from two indirect subsidiaries ofStatoil a 40% interest in SCP, a partnership that owns KKD in Alberta, Canada, for consideration of U.S.$2.28billion. Statoil owns the remaining 60% interest in SCP and is the managing partner. PTTEP and Statoil enteredinto several key agreements to govern the sale and their partnership. KKD is an oil sands project, which PTTEPestimates has 3.8 to 4.3 billion Bbls of recoverable Bitumen resources as independently verified by a leadingexternal petroleum consultant. The project is an in-situ oil sands project utilizing SAGD technology, and has anexpected project life of over 40 years. Commercial production began in January 2011. On March 19, 2011, PTTEPand Statoil entered into a memorandum of understanding to jointly investigate future collaboration opportunitiesinternationally.

Oil sands are composed of a mixture of sand, clay and other mineral matter, water and bitumen. The largestproven deposit of oil sands reserves is in Alberta, Canada although deposits also exist in Venezuela, Russia, theUnited States, Madagascar, Albania, Trinidad and Romania. The first oil sands project in Canada began in 1967.The Athabasca region, where KKD is located, is one of three oil sands regions in Alberta. The two extractionmethods used in Canadian oil sands projects are surface mining and in-situ methods. Surface mining is generallyused for oil sands located less than 75 meters from the surface. For deeper deposits, in-situ methods, whichresemble conventional oil drill projects, are used. There are several types of in-situ methods and KKD uses SAGD.The SAGD method injects steam into the earth to heat the bitumen and help separate it from the sand, then it ispumped to the surface. Bitumen extracted from oil sands is so viscous that it does not flow at normal temperatures.It has to be either blended with diluent to be able to flow through a pipeline and sold as blended bitumen orupgraded into synthetic crude oil by bitumen upgraders, which is a process of removing heavy components. Afterone of these two processes are complete, refineries can transform bitumen or synthetic crude oil into variouspetroleum products.

4

PTTEP has included unaudited pro forma combined financial information as of and for the year endedDecember 31, 2010, as well as the audited financial information of SCP as of and for the year ended December31, 2010 elsewhere in this Offering Memorandum to illustrate the pro forma combined results of operationsfollowing the acquisition and provide information on the historical results of operations of SCP. See, “UnauditedPro Forma Combined Financial Information.”

Project Description

KKD is located in Alberta, Canada, approximately 100 km southwest from Fort McMurray, Alberta, Canada.The project includes five fields, Leismer, Corner, Thornbury, Hangingstone, and South Leismer covering 257,200acres. When fully developed, KKD will include four hubs and a total planned project capacity of over 300,000Bbls/d. PTTEP CA has assessed KKD’s reserves using the COGE Handbook for estimating its resources andreserves, which is broadly aligned with the SPE guidelines. Accordingly, PTTEP estimates that the total expectedBitumen resources for the project will be between 3.8 and 4.3 billion Bbls as independently verified by a leadingexternal petroleum consultant. Statoil acquired its interest in the corporate entity holding KKD in June 2007 andhas since invested over U.S.$1.8 billion in the development of the project, exclusive of the acquisition cost.

The first phase of development was a demonstration plant for the Leismer field (“Leismer DemonstrationPlant”). The Leismer Demonstration Plant became operational in December 2010 and commercial productioncommenced in January 2011. It currently has an approved capacity of 40,000 Bbls/d of bitumen and built-inprocessing and well capacity sufficient to raise production to the commercial scale of 18,800 Bbls/d. The LeismerDemonstration Plant is connected via a 75 km pipeline to storage facilities in Cheecham, Alberta.

The KKD project is currently advancing plans for a second phase of development at the Leismer field. Inaddition, KKD is currently developing plans for the Corner field with a production capacity target of 40,000 Bbls/dof bitumen in the first phase.

For more information, see “Risk Factors — Risks Relating to the Acquisition of an interest in SCP.”

Material Agreements

PTTEP indirectly holds its interest in SCP through its wholly-owned subsidiary PTTEP CA. PTTEP CAholds a 40% interest in SCP, which wholly-owns KKD. PTTEP’s relationship with Statoil and SCP is governedby a Partnership Agreement dated January 21, 2011. Under the Partnership Agreement, Statoil is the initialmanaging partner in charge of oversight of the operations of SCP. However, unanimous approval of a managementcommittee representing each of the partners is required for many decisions, including approving changes to, andthe initiation of, project plans, accumulating debt, making expenditures over certain thresholds and othersignificant changes to the operations of KKD.

SCP sells its entire production volume of bitumen to Statoil under a sales agreement entered into as part ofthe acquisition process. The sales agreement is a long-term agreement for the life of SCP or until certainproduction volumes are reached. Once those volumes are reached, PTTEP can exercise its option to take its shareof production. The price of the bitumen is set according to a formula that references market benchmarks andpre-determined adjustments for adjustments for delivery costs, U.S. duties and marketing fees.

5

THE OFFERING

The following is a brief summary of some of the terms of the Notes. For a more detailed description of theterms of the Notes, see “Description of the Notes.” Terms used in this summary and not otherwise defined shallhave the meanings given to them in the Indenture.

Issuer PTTEP Canada International Finance Limited

Guarantor PTT Exploration and Production Public Company Limited.

Offering U.S.$700,000,000 aggregate principal amount of 5.692% Notes due2021 are being offered (i) in the United States to QIBs in reliance onRule 144A and (ii) outside of the United States to non-U.S. personsin reliance on Regulation S. See “Plan of Distribution.”

Issue Price 100.0% of the principal amount of the Notes, plus accrued interest,if any, from the issue date of the Notes.

Maturity Date April 5, 2021.

Interest The Notes will bear interest from and including April 5, 2011, at therate of 5.692% per annum payable semi-annually in arrear onOctober 5 and April 5 of each year up to and excluding the maturitydate, April 5, 2021, with the first interest payment to be made onOctober 5, 2011.

Status The Notes will be unsecured, rank equally with all of the Issuer’sexisting and future senior debt and senior to all of the Issuer’sexisting and future subordinated debt. The Notes will be effectivelysubordinated to all of the Issuer’s future secured debt to the extent ofthe value of the assets securing such debt and effectivelysubordinated to all future debt of the Issuer’s subsidiaries.

Guarantee The Notes will be guaranteed on a senior basis by PTTEP. TheGuarantee will be unsecured, rank equally with all of PTTEP’sexisting and future senior debt and senior to all of PTTEP’s existingand future subordinated debt.

Optional Redemption 100% of the principal amount of the Notes redeemed, plus theApplicable Premium and accrued and unpaid interest, if any, to theredemption date.

Optional Tax Redemption The Notes may be redeemed at the Issuer’s option, in whole but notin part, at a price equal to the principal amount thereof plus accruedand unpaid interest, in certain circumstances in which the Issuer orthe Company would become obligated to pay Additional Amounts.See “Description of the Notes — Optional Tax Redemption.”

Certain Covenants The indenture (the “Indenture”) under which the Notes will be issuedcontains certain covenants that limit (i) the incurrence of liens,mortgages, or pledges on certain of the Issuer’s assets and (ii) certainsale/leaseback transactions. However, these limitations andrestrictions are subject to important exceptions. See “Description ofthe Notes — Certain Covenants.”

6

Change of Control The interest rate payable on the Notes will be subject to an increaseof 1.00% upon the occurrence of a Change of Control TriggeringEvent (as defined herein). See “Description of the Notes — Principal,Maturity and Interest.”

Events of Default The Notes will be subject to certain events of default, including thefailure by the Issuer to pay principal of or interest on the Notes andacceleration of certain other indebtedness. See “Description of theNotes — Events of Default.”

Withholding Tax See “Description of the Notes — Additional Amounts,” “Taxation —Canadian Taxation” and “Taxation — Thailand Taxation.”

Further Issues The Issuer may, from time to time, without the consent of the holdersof the Notes, create and issue further notes having the same terms andconditions as the Notes in all respects so that such further issue shallbe consolidated and form a single series with the Notes; providedthat, if any further issue is not fungible with the Notes for U.S.federal income tax purposes, such further issue shall trade separatelyfrom such previously issued Notes under a separate CUSIP numberbut shall otherwise be treated as a single series with all other Notesissued under the Indenture. See “Description of Notes — FurtherIssuances.”

Use of Proceeds The net proceeds from the sale of the Notes, which are estimated tobe approximately U.S.$699,720,000 million after payment ofcommissions to the Initial Purchaser but before expenses payable bythe Issuer and the Company, will be used for general corporatepurposes, including, but not limited to, funding the Company’sexploration, development and production activities.

Listing Approval-in-principle has been received for the listing of the Noteson the Official List of the SGX-ST. The Notes will be traded on theSGX-ST in a minimum board lot size of U.S.$200,000 for as long asthe Notes are listed on the SGX-ST.

Transfer Restrictions; Absence ofPublic Market for the Notes

The Notes and the Guarantee have not been and will not be registeredunder the Securities Act or any applicable securities legislation inCanada and are subject to restrictions on transferability and resale.For more information, see “Transfer Restrictions.” The Notes are anew issue of securities and there is currently no established tradingmarket for the Notes. Accordingly, there can be no assurance as to thedevelopment or liquidity of any market for the Notes. The InitialPurchaser has advised the Issuer and the Company that it currentlyintends to make a market in the Notes. However, it is not obligatedto do so, and any market making with respect to the Notes may bediscontinued without notice. See “Risk Factors — Risks Related tothis Offering — There is no public market for the Notes.”

7

Form, Denomination and Registrationof Notes

The Notes offered hereby will be issued in fully registered form,issued in minimum denominations of U.S.$200,000 and integralmultiples of U.S.$1,000 in excess thereof. The Rule 144A Notesoffered in the United States to QIBs in reliance on Rule 144A will beevidenced by a Rule 144A Global Note deposited with the Trustee, ascustodian for, and registered in the name of a nominee of, DTC. Rule144A Notes evidenced by the Rule 144A Global Note will settle inDTC’s Same Day Funds Settlement System, and secondary markettrading activity in such Rule 144A Notes will therefore settle inimmediately available funds. Regulation S Global Notes offeredoutside the United States in reliance on Regulation S will beevidenced by a Regulation S Global Note deposited with the Trustee,as custodian for, and registered in the name of a nominee of, DTC forits direct and indirect participants, including Euroclear andClearstream, Banking.

Delivery of the Notes Delivery of the Notes, against payment in same-day funds, isexpected on or about April 5, 2011. See “Plan of Distribution —Delivery of the Notes.”

Risk Factors See “Risk Factors” beginning on page 16 for a discussion of certainrisks that you should consider in connection with an investment inthe Notes.

Trustee The Bank of New York Mellon will act as the Trustee under theIndenture for the Notes.

Governing Law The Notes and the Indenture are governed by, and construed inaccordance with, the laws of the State of New York.

Security Codes Rule 144A Notes: Regulation S Notes:

CUSIP No.: 74442A AA6 CUSIP No.: C75088 AA9ISIN: US74442AAA60 ISIN: USC75088AA97

8

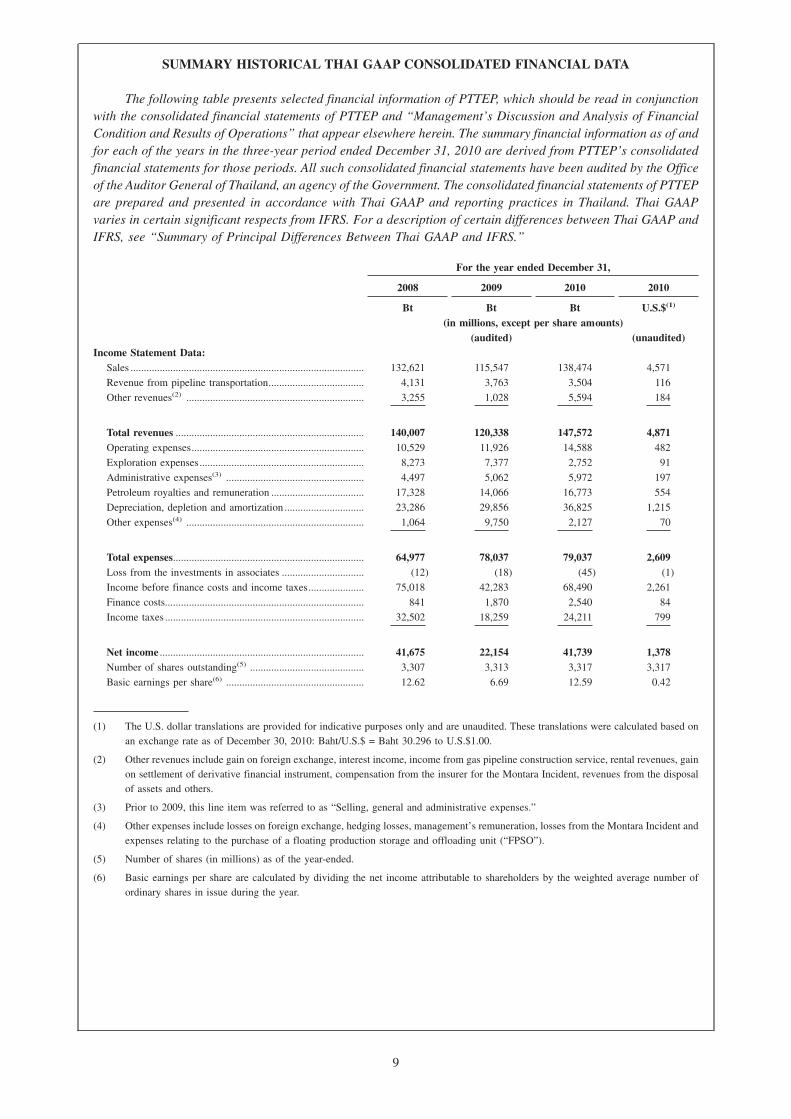

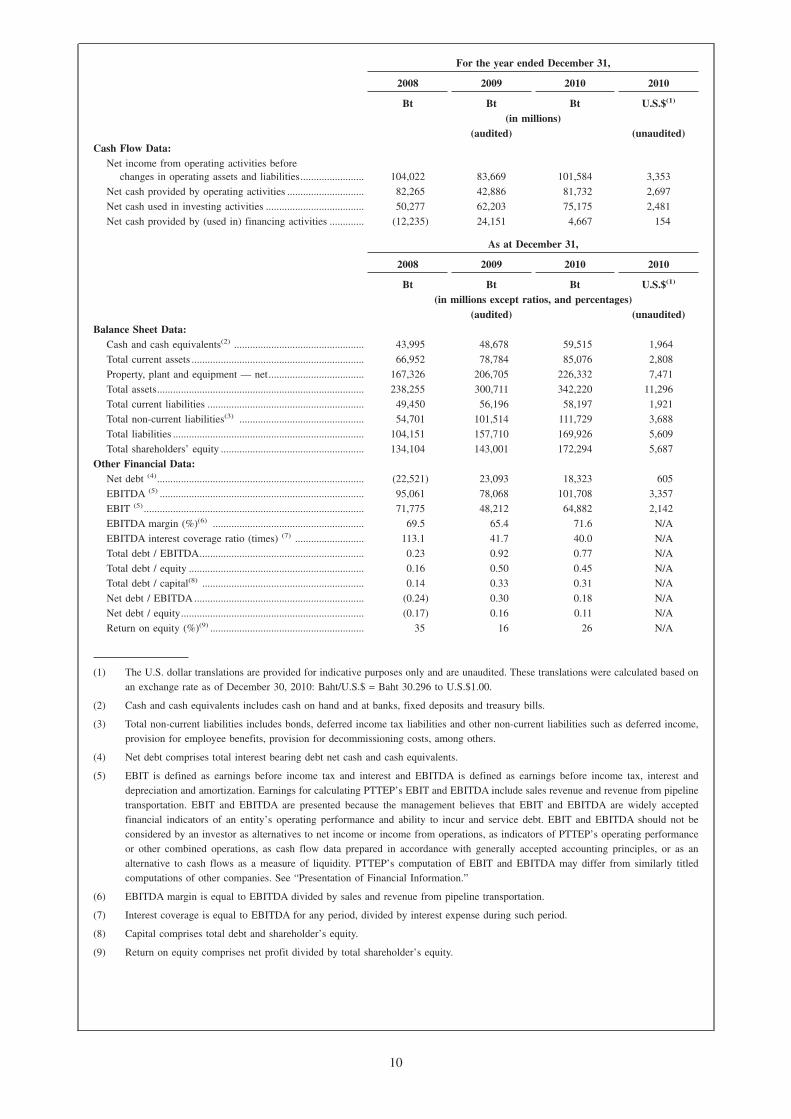

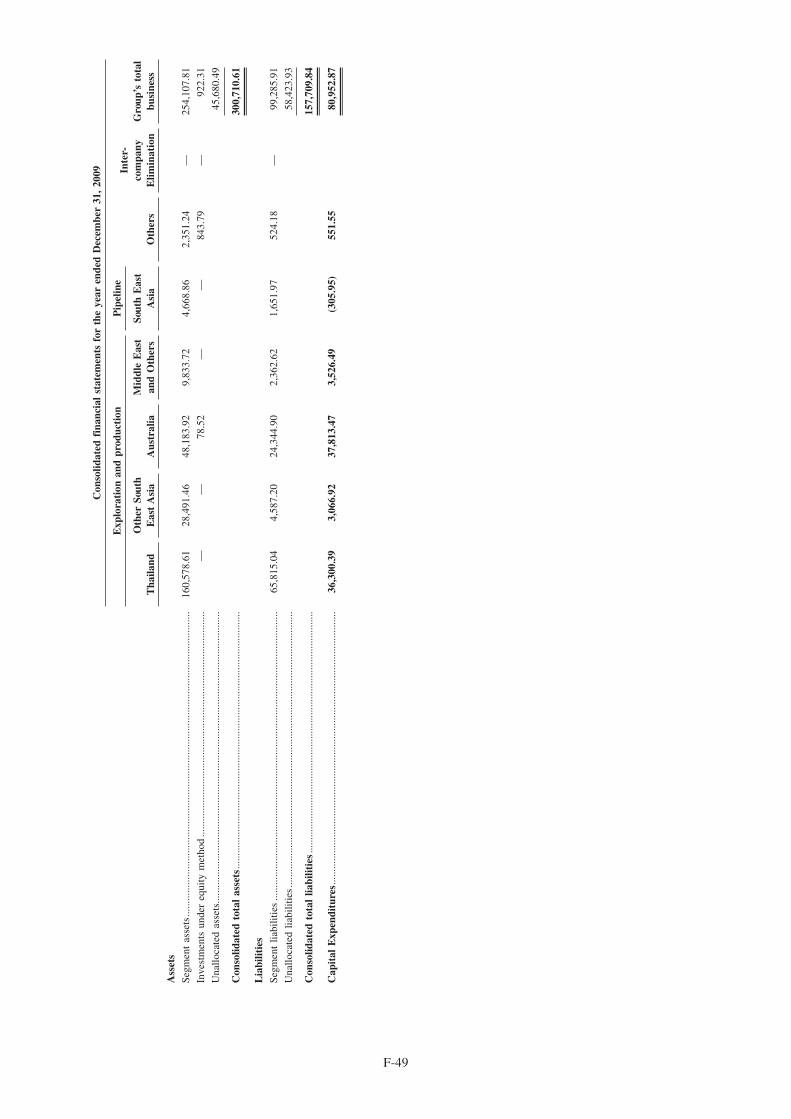

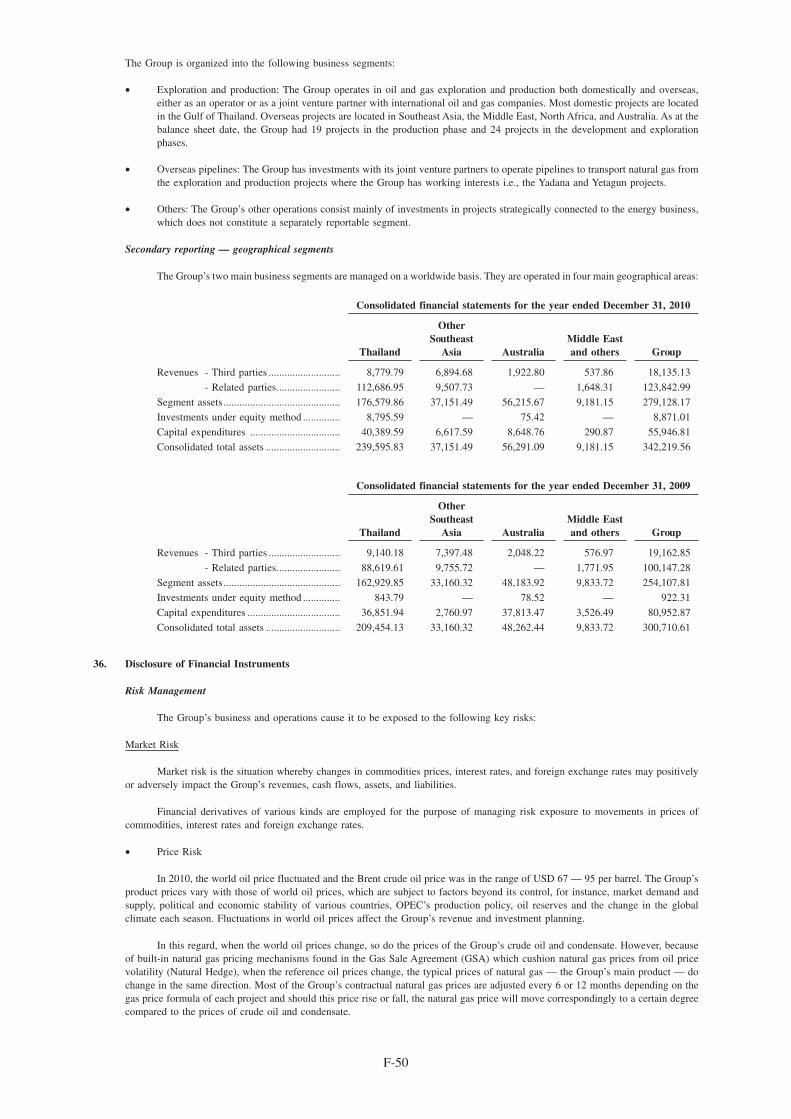

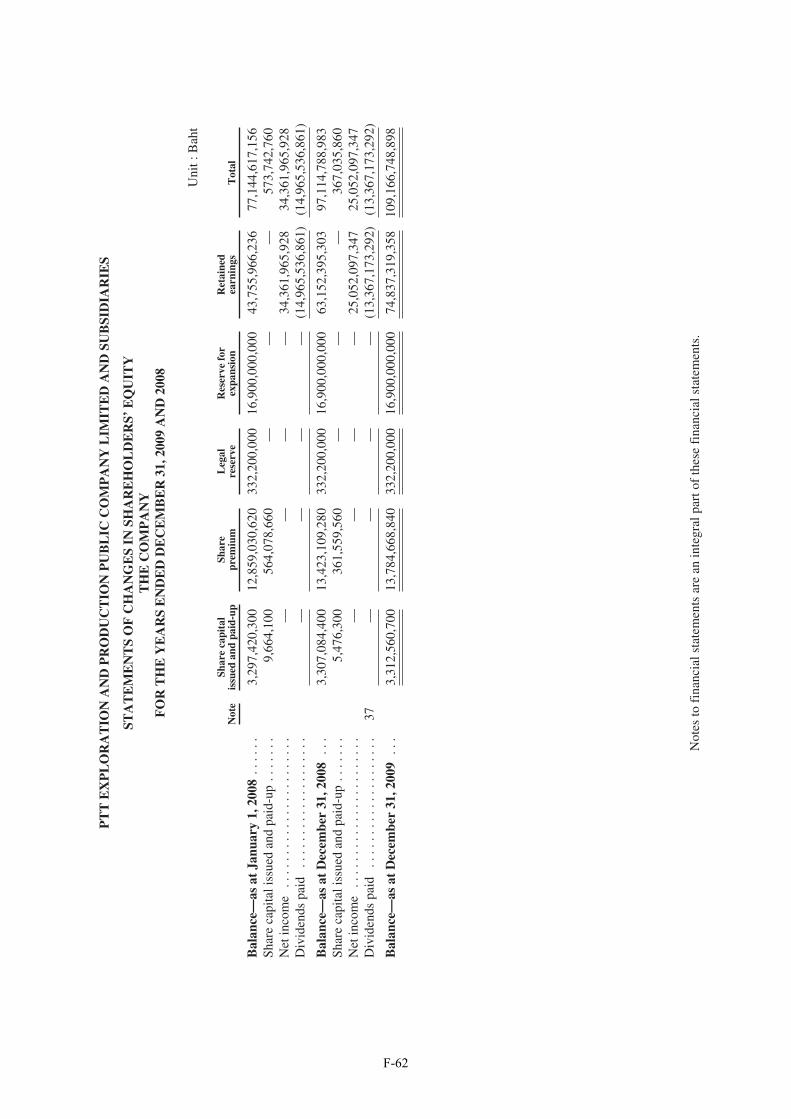

SUMMARY HISTORICAL THAI GAAP CONSOLIDATED FINANCIAL DATA

The following table presents selected financial information of PTTEP, which should be read in conjunctionwith the consolidated financial statements of PTTEP and “Management’s Discussion and Analysis of FinancialCondition and Results of Operations” that appear elsewhere herein. The summary financial information as of andfor each of the years in the three-year period ended December 31, 2010 are derived from PTTEP’s consolidatedfinancial statements for those periods. All such consolidated financial statements have been audited by the Officeof the Auditor General of Thailand, an agency of the Government. The consolidated financial statements of PTTEPare prepared and presented in accordance with Thai GAAP and reporting practices in Thailand. Thai GAAPvaries in certain significant respects from IFRS. For a description of certain differences between Thai GAAP andIFRS, see “Summary of Principal Differences Between Thai GAAP and IFRS.”

For the year ended December 31,

2008 2009 2010 2010

Bt Bt Bt U.S.$(1)

(in millions, except per share amounts)(audited) (unaudited)

Income Statement Data:Sales ........................................................................................ 132,621 115,547 138,474 4,571

Revenue from pipeline transportation.................................... 4,131 3,763 3,504 116

Other revenues(2) ................................................................... 3,255 1,028 5,594 184

Total revenues ....................................................................... 140,007 120,338 147,572 4,871Operating expenses................................................................. 10,529 11,926 14,588 482

Exploration expenses.............................................................. 8,273 7,377 2,752 91

Administrative expenses(3) .................................................... 4,497 5,062 5,972 197

Petroleum royalties and remuneration ................................... 17,328 14,066 16,773 554

Depreciation, depletion and amortization .............................. 23,286 29,856 36,825 1,215

Other expenses(4) ................................................................... 1,064 9,750 2,127 70

Total expenses........................................................................ 64,977 78,037 79,037 2,609Loss from the investments in associates ............................... (12) (18) (45) (1)

Income before finance costs and income taxes..................... 75,018 42,283 68,490 2,261

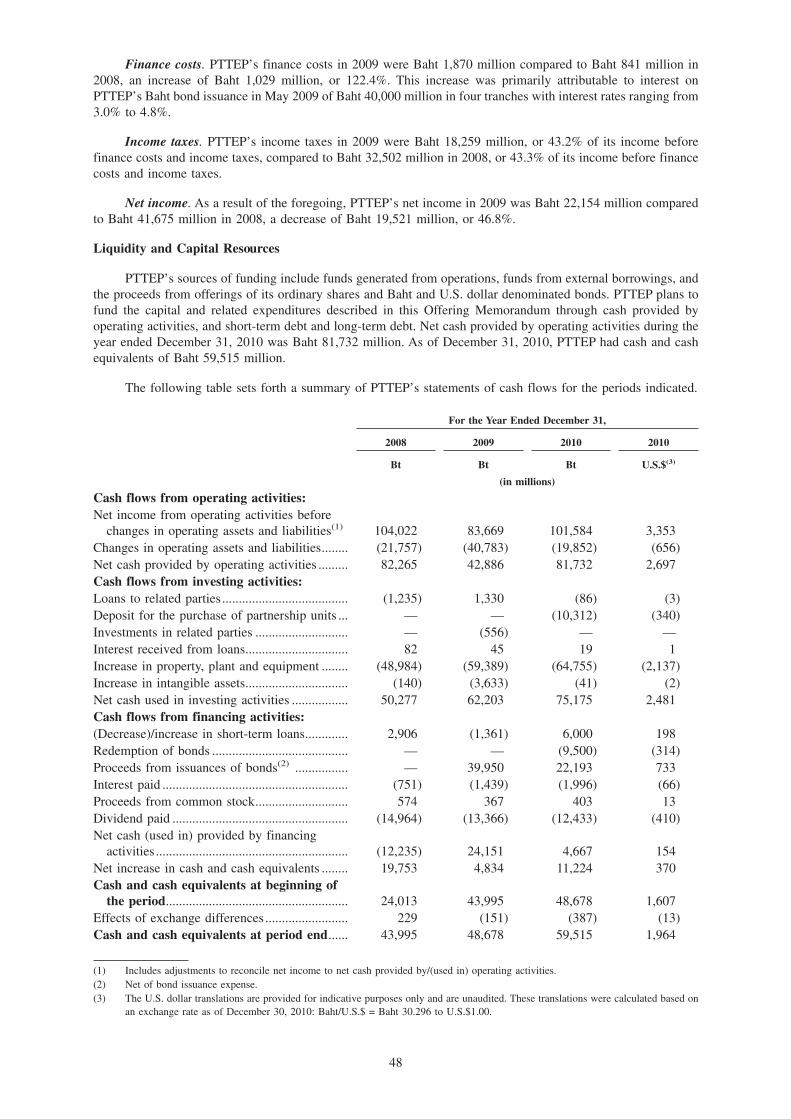

Finance costs........................................................................... 841 1,870 2,540 84

Income taxes ........................................................................... 32,502 18,259 24,211 799

Net income ............................................................................. 41,675 22,154 41,739 1,378Number of shares outstanding(5) ........................................... 3,307 3,313 3,317 3,317

Basic earnings per share(6) .................................................... 12.62 6.69 12.59 0.42

(1) The U.S. dollar translations are provided for indicative purposes only and are unaudited. These translations were calculated based onan exchange rate as of December 30, 2010: Baht/U.S.$ = Baht 30.296 to U.S.$1.00.

(2) Other revenues include gain on foreign exchange, interest income, income from gas pipeline construction service, rental revenues, gainon settlement of derivative financial instrument, compensation from the insurer for the Montara Incident, revenues from the disposalof assets and others.

(3) Prior to 2009, this line item was referred to as “Selling, general and administrative expenses.”

(4) Other expenses include losses on foreign exchange, hedging losses, management’s remuneration, losses from the Montara Incident andexpenses relating to the purchase of a floating production storage and offloading unit (“FPSO”).

(5) Number of shares (in millions) as of the year-ended.

(6) Basic earnings per share are calculated by dividing the net income attributable to shareholders by the weighted average number ofordinary shares in issue during the year.

9

For the year ended December 31,

2008 2009 2010 2010

Bt Bt Bt U.S.$(1)

(in millions)(audited) (unaudited)

Cash Flow Data:Net income from operating activities before

changes in operating assets and liabilities........................ 104,022 83,669 101,584 3,353

Net cash provided by operating activities ............................. 82,265 42,886 81,732 2,697

Net cash used in investing activities ..................................... 50,277 62,203 75,175 2,481

Net cash provided by (used in) financing activities ............. (12,235) 24,151 4,667 154

As at December 31,

2008 2009 2010 2010

Bt Bt Bt U.S.$(1)

(in millions except ratios, and percentages)(audited) (unaudited)

Balance Sheet Data:Cash and cash equivalents(2) ................................................. 43,995 48,678 59,515 1,964

Total current assets ................................................................. 66,952 78,784 85,076 2,808

Property, plant and equipment — net.................................... 167,326 206,705 226,332 7,471

Total assets.............................................................................. 238,255 300,711 342,220 11,296

Total current liabilities ........................................................... 49,450 56,196 58,197 1,921

Total non-current liabilities(3) ............................................... 54,701 101,514 111,729 3,688

Total liabilities ........................................................................ 104,151 157,710 169,926 5,609

Total shareholders’ equity ...................................................... 134,104 143,001 172,294 5,687

Other Financial Data:Net debt (4).............................................................................. (22,521) 23,093 18,323 605

EBITDA (5) ............................................................................. 95,061 78,068 101,708 3,357

EBIT (5) ................................................................................... 71,775 48,212 64,882 2,142

EBITDA margin (%)(6) ......................................................... 69.5 65.4 71.6 N/A

EBITDA interest coverage ratio (times) (7) .......................... 113.1 41.7 40.0 N/A

Total debt / EBITDA.............................................................. 0.23 0.92 0.77 N/A

Total debt / equity .................................................................. 0.16 0.50 0.45 N/A

Total debt / capital(8) ............................................................. 0.14 0.33 0.31 N/A

Net debt / EBITDA ................................................................ (0.24) 0.30 0.18 N/A