Analisis pengembangan model bisnis properti pt hasta raya ...

1

PT Mega Manunggal Property Tbk

SEPTEMBER 2019

22

33

4

Disclaimer

The information contained in this presentation has been prepared by PT Mega Manunggal Property Tbk. (the “Company”) and is being furnished to you solely for your

information and may not be reproduced or redistributed to any other person, in whole or in part in any manners or for any purpose. In particular, neither the information

contained in this presentation nor any copy hereof may be, directly or indirectly, taken or transmitted into or distributed in any jurisdiction which prohibits the same except in

compliance with applicable securities laws.

This presentation does not contain all material information concerning the Company and the information set forth in these materials is subject to change without notice. The

third party information and statistical data in this presentation have been obtained from sources the Company believes to be reliable but there can be no assurance as to the

accuracy or completeness of the included information. No reliance should be placed on, the fairness, accuracy, completeness or correctness of the information, or opinions

contained herein.

None of the Company, its directors, officers, shareholders, advisors or representatives makes any representation or warranty, express or implied, as to the accuracy or

completeness of the information in this presentation, and nothing in this presentation is, or should be relied upon as, a promise or representation by any of them. None of the

Company, its directors, officers, shareholders, advisors or representatives shall have any responsibility or liability whatsoever (for negligence or otherwise) for any loss

howsoever arising from any use of this presentation or its contents or otherwise arising in connection with this presentation.

Certain statements in this presentation may constitute “forward-looking statements”, including statements regarding the Company’s expectations and projections for future

operating performance and business prospects. Such forward-looking statements are based on numerous assumptions regarding the Company’s present and future business

strategies and the environment in which the Company will operate in the future. Such forward-looking statements speak only as of the date on which they are made.

Accordingly, the Company expressly disclaims any obligation to update or revise any forward-looking statement contained herein to reflect any change in the Company’s

expectations with regard to new information, future events or other circumstances. The Company does not make any representation, warranty or prediction that the results

anticipated by such forward-looking statements will be achieved, and such forward-looking statements represent, in each case, only one of many possible scenarios and should

not be viewed as the most likely or standard scenario. Accordingly, parties reviewing this presentation should not place undue reliance on any forward-looking statements. The

information contained in this presentation should be considered in the context of the circumstances prevailing at the time and has not been, and will not be, updated to reflect

material developments which may occur after the date of the presentation.

This presentation is not intended to form basis any investment decision to purchase securities of the Company and does not constitute or form part of, and should not be

construed as, any offer for sale or subscription of or solicitation or invitation of any offer to buy or subscribe for any securities of the Company in any jurisdiction, including the

United States. The Company’s securities have not been and will not be registered under the United States Securities Act of 1933, as amended (the “Securities Act”), and may

not be offered, sold or delivered within the United States absent registration under or an applicable exemption from the registration requirements of the Securities Act and this

presentation does not constitute or form a part of any offer to sell or solicitation of an offer to purchase or subscribe for securities in Indonesia in which such offer, solicitation or

sale would be unlawful prior to registration and such registration being deemed effective by the Otoritas Jasa Keuangan.

By reviewing this presentation, you acknowledge this Disclaimer and agree to be bound by the foregoing limitations, and you acknowledge that you will be solely responsible for

your own assessment of the market and the market position of the Company and that you will conduct your own analysis and be solely responsible for forming your own view of

the potential future performance of the business of the Company.

5

Agenda Presentation

Section Pages

1 Who we are 6

2 Growth strategy 17

3 On the right track 23

4 Strong growth opportunity 28

5 Key financial 47

6 Assets in details 53

7 Other financial info 65

6

Section 1

Who We Are

7

Company At A Glance

Overview

PT. Mega Manunggal Property Tbk

(“MMP”) is a warehouse provider

that supports industrial property

needs in Indonesia focusing on

developing, owning and operating

logistic properties with a focus in

warehousing that specifically meet

international standards.

Established on mid 2010, currently

MMP has Net Leasable Area of

area total 321,395 m2 - including a

90,000 m2 NLA warehouse for PT

Unilever Indonesia, one of the

largest Unilever warehouses

globally.

Projects

Currently MMP has 9 assets in 5 different

strategic locations:

MM2100, Bekasi:

Unilever Mega DC

Li & Fung Logistic

Selayar

Block AE

Cikarang, Bekasi:

• Delta Silicon III

Halim Cililitan, East Jakarta:

Intirub Business Park

Tapos, Depok:

Lazada warehouse

Jababeka:

Cibatu warehouse

Cileungsi:

Cileungsi warehouse

MMP is currently developing Lazada

Phase 2 warehouse in Tapos, a

warehouse in Delta Silicon III Cikarang

Phase II & III, a warehouse in Pondok

Ungu Bekasi, a warehouse in Jababeka,

Bekasi, and a warehouse in Manyar, East

Java.

FacilitiesFacilities of PT. Mega Manunggal

Property Tbk are developed with

specifications which refer to

international standards to meet

the demand in the Indonesian

logistics services business while

keeping the specifications comply

to local regulations. MMP is

committed to give good quality

products and deliver added value

services to support the client’s

business.

8

Structure of PT Mega Manunggal Property Tbk

99.99%

MMP’s asset structure

PT Mega Manunggal

Property Tbk

Unilever

Mega DC

Li & Fung

Intirub Business

Park I & II

Selayar

PT Mega Khatulistiwa

Properti

PT Mega Tridaya

Properti

55.00%

PT Intirub

99.76%99.50%

45.00%

GIC

PT Mega

Properti

Logistik

Nusantara

99.99%

Cibitung

AirportCibitung

Cibatu

Depok

Cileungsi

Bekasi

Halim

Pondok Ungu

Manyar Jababeka

99.99%

99.99%

99.99% 99.99%

99.99%

99.99%

99.99%

95.00%

99.99%

Cikarang

PT Mega

Dharma

Properti

PT

Manunggal

Persada

Properti

PT Subang

HorisonProperti

PT Subang

Cakrawala

Properti

PT Mega

Buana

Properti

Logistik

PT

Manunggal

Timur

Properti

PT Bukit

Properti

Logistik

PT Mega

Cahaya

Properti

PT Mega

Angkasa

Properti

PT Ace

Dalle Mega

Properti

PT Mega Cakrawala

Internusa Properti

PT Mega Jaya

Lestari Properti

99.40%99.40%

99.62%

PT Mega Arga

Properti

99.62%

PT Mega

Surya

Properti

99.62%

PT Mega

Aruna

Nusantara

Properti

9

Board of Directors

Bonny Budi SetiawanPresident Director

Has been the Company’s Director since 2015 and appointed as the President Director in January 2017.Earned a Bachelor of Business Administration in Accounting and Finance from Simon Fraser University,Canada (1997). Previously served as Executive Director of PT UBS Securities Indonesia (2011-2015); SeniorVice President of PT Danareksa Sekuritas, Jakarta (2010 - 2011); Vice President of Research Division of PTDanareksa Sekuritas in Jakarta (2009 - 2010); Vice President of Research Division of Merrill Lynch, Jakarta(2007 - 2009); Vice President of Research Division of PT CIMB-GK Securities, Assistant Vice President ofresearch division of PT Danareksa Sekuritas (2005 - 2007); Supervisor Consultant Financial AdvisoryServices (FAS) of Prijohandojo Boentoro & Co. (2003 - 2005); Research Analyst of PT Panin Sekuritas (2002 -2003) and Export Supervisor of PT Pabrik Kertas Tjiwi Kimia (1998-2000).

Loa Siong LieDirector

Has been appointed as the Independent Director since 2017. He is in charge of technical and construction.He earned Civil Engineering Bachelor’s degree from University of Tarumanegara, Jakarta in 1996. He wasProject Manager for PT Sinar Menara Deli (2016 – 2017), Project Manager for PT Supra Megah Utama ( 2012 -2016), Site Manager for PT Pradani Sukses Abadi (2010 – 2012), Site Manager for PT Intersatria Budi KaryaPratama (2007 – 2010). Construction Manager for PT Praga Artamida ( 1996 – 2007).

10

Company Milestone

11

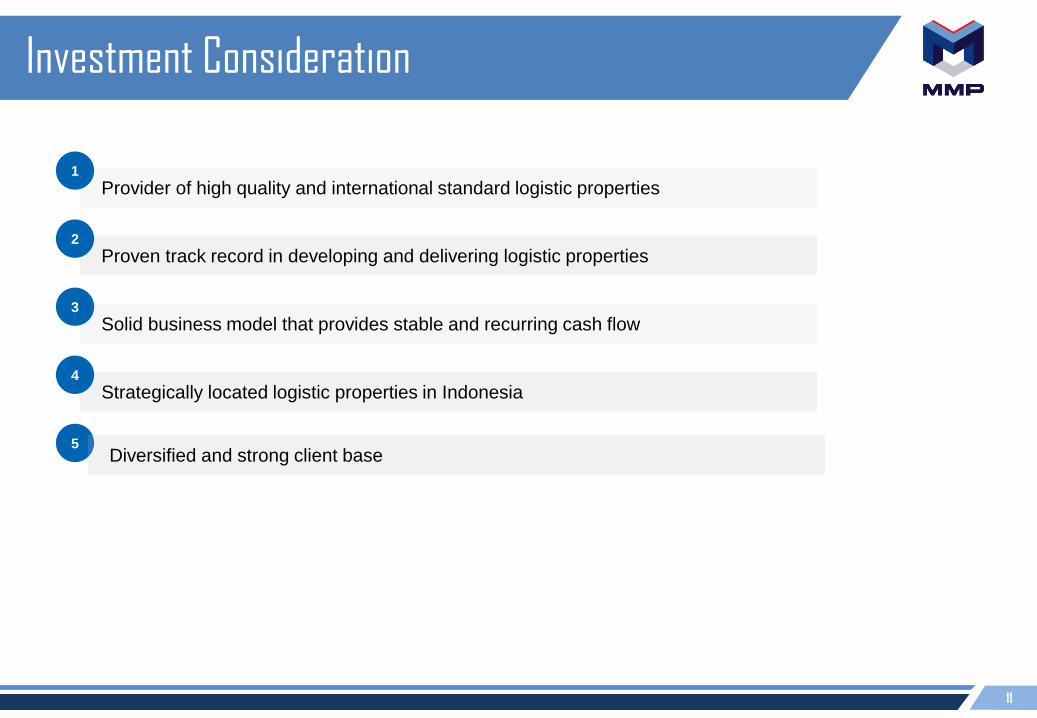

Investment Consideration

Provider of high quality and international standard logistic properties1

Proven track record in developing and delivering logistic properties2

Solid business model that provides stable and recurring cash flow 3

Strategically located logistic properties in Indonesia4

5Diversified and strong client base

12

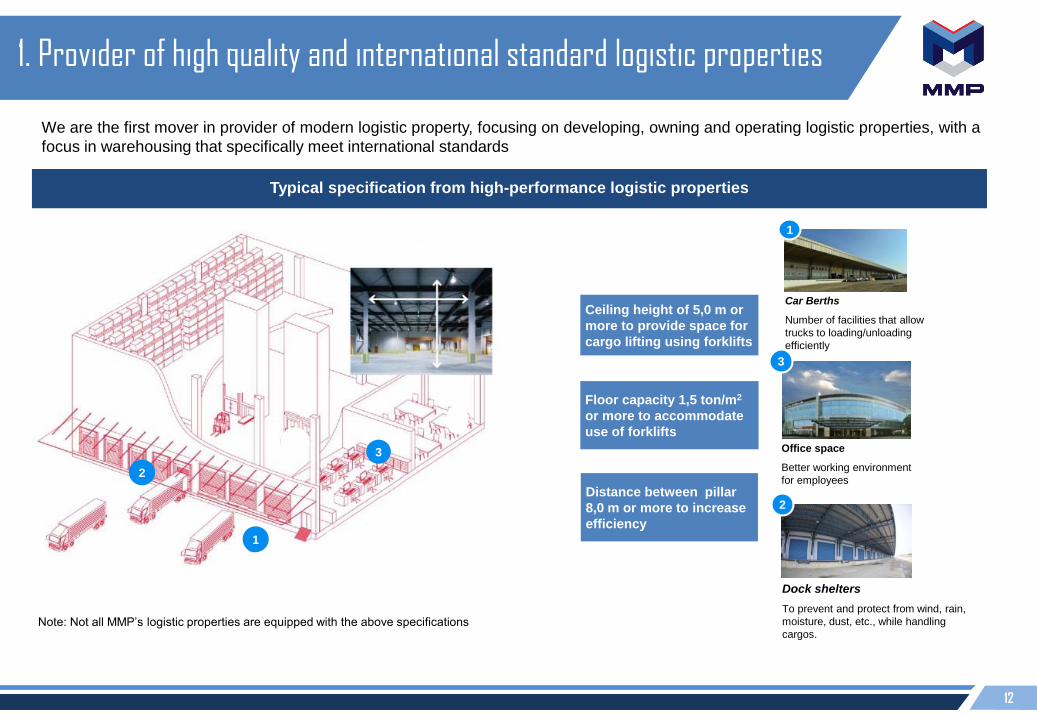

1. Provider of high quality and international standard logistic properties

Note: Not all MMP’s logistic properties are equipped with the above specifications

Typical specification from high-performance logistic properties

1

2

33 Office space

Better working environment

for employees

3

1

Car Berths

Number of facilities that allow

trucks to loading/unloading

efficiently

2

Dock shelters

To prevent and protect from wind, rain,

moisture, dust, etc., while handling

cargos.

Ceiling height of 5,0 m or

more to provide space for

cargo lifting using forklifts

Distance between pillar

8,0 m or more to increase

efficiency

Floor capacity 1,5 ton/m2

or more to accommodate

use of forklifts

We are the first mover in provider of modern logistic property, focusing on developing, owning and operating logistic properties, with a

focus in warehousing that specifically meet international standards

13

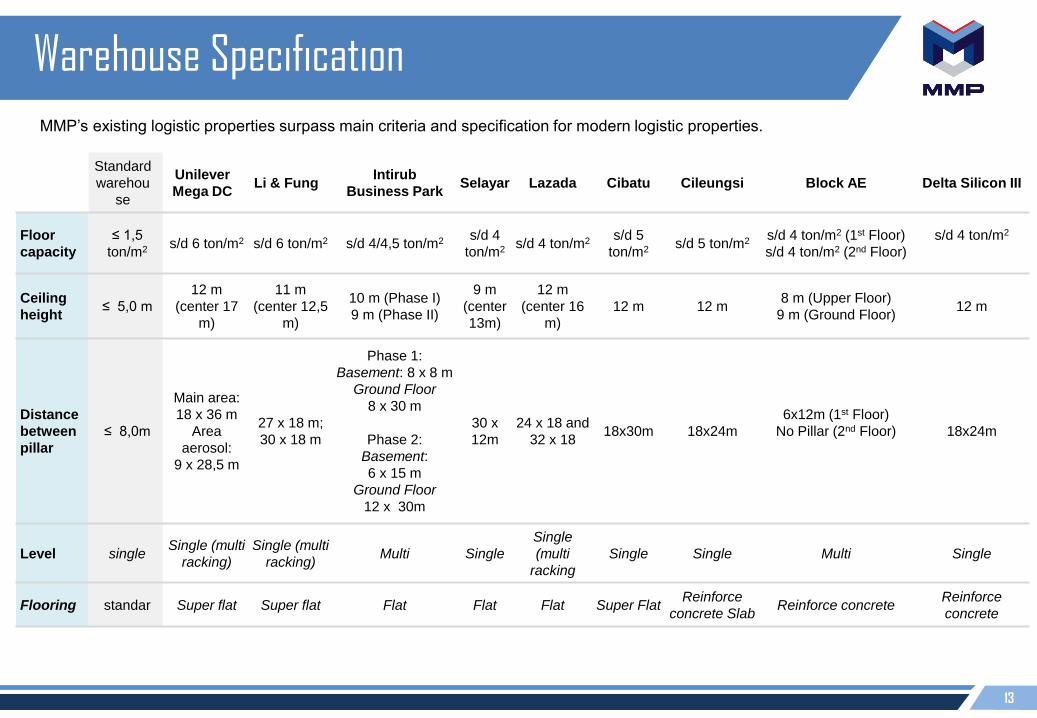

Warehouse Specification

Standard

warehou

se

Unilever

Mega DCLi & Fung

Intirub

Business ParkSelayar Lazada Cibatu Cileungsi Block AE Delta Silicon III

Floor

capacity

≤ 1,5

ton/m2 s/d 6 ton/m2 s/d 6 ton/m2 s/d 4/4,5 ton/m2 s/d 4

ton/m2 s/d 4 ton/m2 s/d 5

ton/m2 s/d 5 ton/m2 s/d 4 ton/m2 (1st Floor)

s/d 4 ton/m2 (2nd Floor)

s/d 4 ton/m2

Ceiling

height≤ 5,0 m

12 m

(center 17

m)

11 m

(center 12,5

m)

10 m (Phase I)

9 m (Phase II)

9 m

(center

13m)

12 m

(center 16

m)

12 m 12 m 8 m (Upper Floor)

9 m (Ground Floor)12 m

Distance

between

pillar

≤ 8,0m

Main area:

18 x 36 m

Area

aerosol:

9 x 28,5 m

27 x 18 m;

30 x 18 m

Phase 1:

Basement: 8 x 8 m

Ground Floor

8 x 30 m

Phase 2:

Basement:

6 x 15 m

Ground Floor

12 x 30m

30 x

12m

24 x 18 and

32 x 18 18x30m 18x24m

6x12m (1st Floor)

No Pillar (2nd Floor) 18x24m

Level singleSingle (multi

racking)

Single (multi

racking)Multi Single

Single

(multi

racking

Single Single Multi Single

Flooring standar Super flat Super flat Flat Flat Flat Super FlatReinforce

concrete SlabReinforce concrete

Reinforce

concrete

MMP’s existing logistic properties surpass main criteria and specification for modern logistic properties.

14

118,199 139,811 163,911 163,911

230,370

300,680 321,395

2013 2014 2015 2016 2017 2018 9M2019

2. Proven track record in developing and delivering logistic properties

MMP has proven track record in acquiring land and developing logistic properties, which generally takes around 15 to 18

months to complete construction.

Growth in NLA in the past years

Project Land Area Net Leasable Area Date of Contract Months to develop Delivery date

Unilever Mega DC 197,690 m2 90,288 m2 Dec 2010 16 months Apr 2012

Li & Fung 34,637 m2 21,612 m2 Jul 2012 11 months May 2013

Lazada Warehouse 90,041 m2 31,500 m2 Aug 2015 19 months Apr 2017

Cibatu 50,000 m2 36,335 m2 Jun 2016 15 months Dec 2017

Delta Silicon III (Ph 1) 100,000 m2 20,715m2 Mar 2018 24 months Jul 2019

Standard Warehouse Building

Project Land Area Net Leasable Area Date of ContractMonths to

developDelivery date

Intirub Business Park I 28,190 m2

36,622 m2 (warehouse) + 8,393 m2 (office)Dec 2011 9 months Jan 2012

Intirub Business Park II 32,380 m2 Dec 2013 18 months Apr 2014

Selayar 9,164 m2 5,620 m2 Apr 2015 12 months Apr 2015

Block AE 35,740 m2 38,854 m2 Sep 2016 18 months Feb 2018

Cileungsi 50,004 m2 31,456 m2 Sep 2016 18 months Feb 2018

Built-to-suit

m2

NLA

15

MMP focuses towards developing warehouse with size of 5.000 to 100.000 m2.

Stable operating cash flow with greater upside potential from improving economy cycle, while at the same time sheltered against

downside risks from economy slowing.

High operating leverage with high EBITDA margin.

Improve tenants’ efficiency and productivities through centralization of warehouses.

3. Solid business model that provides stable and recurring cash flow

Unilever Mega DC Li & Fung Intirub Business ParkSelayar

Operating assets that provide recurring and stable cash flow

Lazada

CibatuBlock AE Cileungsi DS III

16

Jakarta, Banten &

Jabar57%

Jateng6%

Jatim9%

Riau & Kep. Riau

9%

Sumut4%

Sumbar1%

Sulsel2%

Sulte…

Kaltim3%

Bangka Belitung

5%

Jakarta, Banten &

Jabar71%

Jateng5%

Jatim8%

Riau & Kep. Riau

8%

Sumut5%

Sumbar0%

Sulsel2%

Kaltim1%

4. Strategically located logistic property in Indonesia

Near centre of production and consumption

Easy access towards transportation network

Easy supply of labour workforce and convenient

transportation for employees

Provide benefits to tenants in reducing logistic costsSource: Himpunan Kawasan Industri% Industrial estate areas

% Industrial estates that are developed

Located in Java Island that is the centre for industries with the largest industrial estates in Indonesia

BESTCinere

Kunciran

Tangerang

CengkarengPenjaringan

Tanjung Priok

DKI

JakartaKebon

Jeruk

Ulujami

Veteran

(Pd Pinang)

Jagorawi

(Cimanggis)

Jawa Barat

Cibitung

Cikunir

Jatiasih

Hankam Raya

(Jatiwarana)Taman

Mini

Laut Jawa

Banten

Bekasi

Cakung

Cilincing

(Rorotan)

15

14

1312

9

8

765

3

2

1

16

17

11

4

10

Operational

In construction

Negotiation/tender

Contract signed

1 to 9 JORR I

10 to 17 JORR II

Located in Java Island that is the centre for industries with the largest industrial estates in Indonesia

17

36%

43%

16%

5%

Manufacture Logistics E-commerce Others

E-commerce

5. Diversified and strong client base

Logistic

Manufacturing

ClientsTenant profile of MMP’s logistic properties as of Sept 2019

18

Section 2

Growth Strategy

19

A strategy that focuses on three factors of success to reach scalable size

Three factors of success

Efficiency Funding

Volume

800,000 m2

NLA

To achieve our NLA target of 800,000 m2 by end of 2021

Continues to reduce construction cost to maximize yield

to cost

Sustainable of funding structure and recycle of cash

To accelerate growth and generate stable cash flow

Sustain profitability and greater EBITDA margin

Timely execution of development

To increase transparency and good corporate

governance

Our strategy is simplified into three factors – funding, efficiency and volume. Timely ability to seek flexible funding structure and continues effort to

reduce cost will maximize yield to cost. This will lead to greater profitability. Our initial scalable size to be achieved by end of 2021 is 800,000m2

NLA.

20

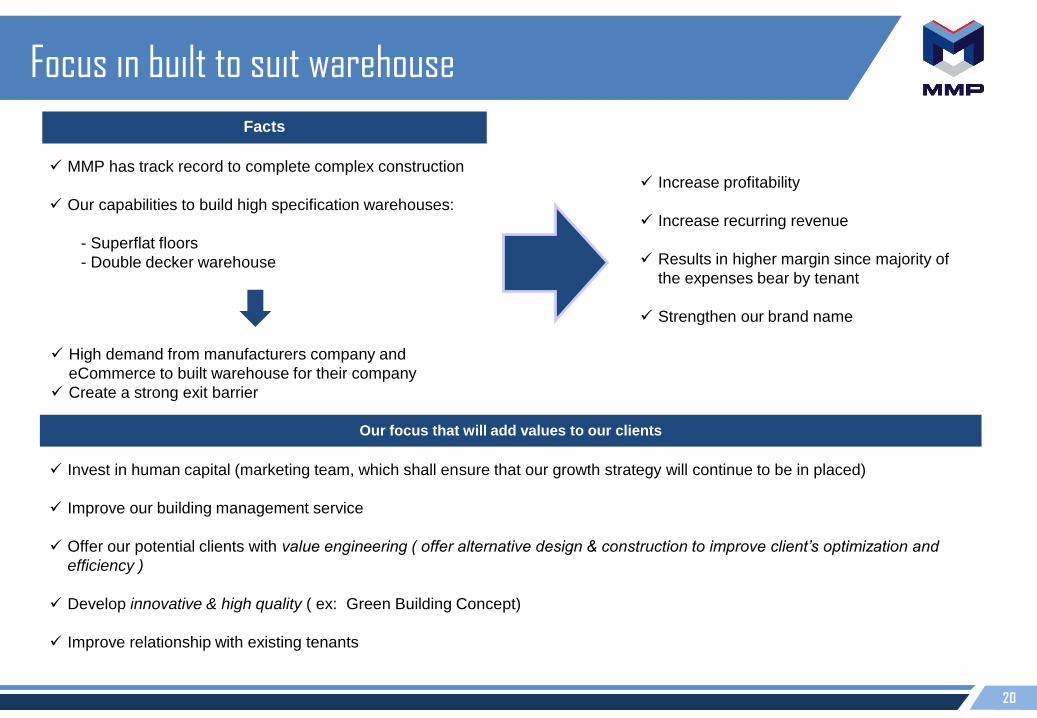

Focus in built to suit warehouse

Facts

MMP has track record to complete complex construction

Our capabilities to build high specification warehouses:

- Superflat floors

- Double decker warehouse

Increase profitability

Increase recurring revenue

Results in higher margin since majority of

the expenses bear by tenant

Strengthen our brand name

Invest in human capital (marketing team, which shall ensure that our growth strategy will continue to be in placed)

Improve our building management service

Offer our potential clients with value engineering ( offer alternative design & construction to improve client’s optimization and

efficiency )

Develop innovative & high quality ( ex: Green Building Concept)

Improve relationship with existing tenants

High demand from manufacturers company and

eCommerce to built warehouse for their company

Create a strong exit barrier

Our focus that will add values to our clients

21

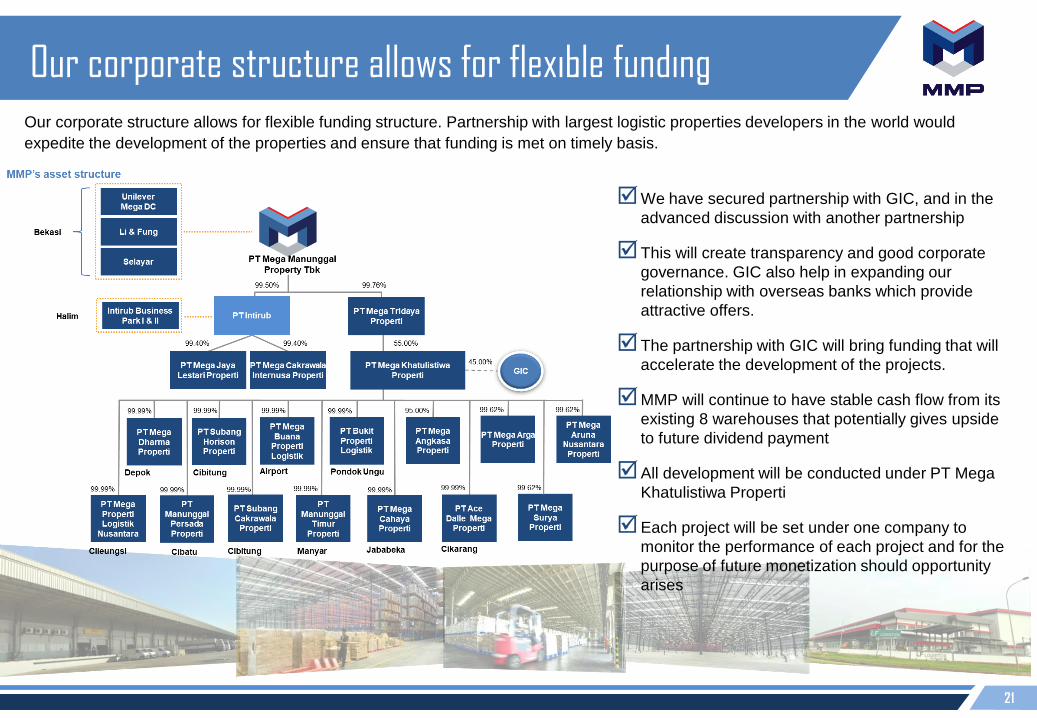

We have secured partnership with GIC, and in the

advanced discussion with another partnership

This will create transparency and good corporate

governance. GIC also help in expanding our

relationship with overseas banks which provide

attractive offers.

The partnership with GIC will bring funding that will

accelerate the development of the projects.

MMP will continue to have stable cash flow from its

existing 8 warehouses that potentially gives upside

to future dividend payment

All development will be conducted under PT Mega

Khatulistiwa Properti

Each project will be set under one company to

monitor the performance of each project and for the

purpose of future monetization should opportunity

arises

Our corporate structure allows for flexible fundingOur corporate structure allows for flexible funding structure. Partnership with largest logistic properties developers in the world would

expedite the development of the properties and ensure that funding is met on timely basis.

22

Continuous effort to cut costs amid aggressive capacity expansion

We have successfully cut down our construction cost by 10% on recent development plan

We set our yield to cost for at least of 9-10%

Our formula is to have land cost for 1/3 of total cost

We strengthen our engineers team to look for best possible design that will cut any

unnecessary cost

We continue to monitor construction progresses to align with existing budget

Efficiency

Volume CurPlan to construct 5 warehouses this year

rently under construction : Phase II warehouse for Lazada (35,000 m2) will be completed in

2019, DS-3 phase 1 project will be delivered as well in 2019.Pondok Ungu warehouse

(54,000 m2) will be delivered in 2021, Jababeka warehouse will be delivered in 2020, Manyar

Warehouse Phase II & III will be delivered in 2021.

23

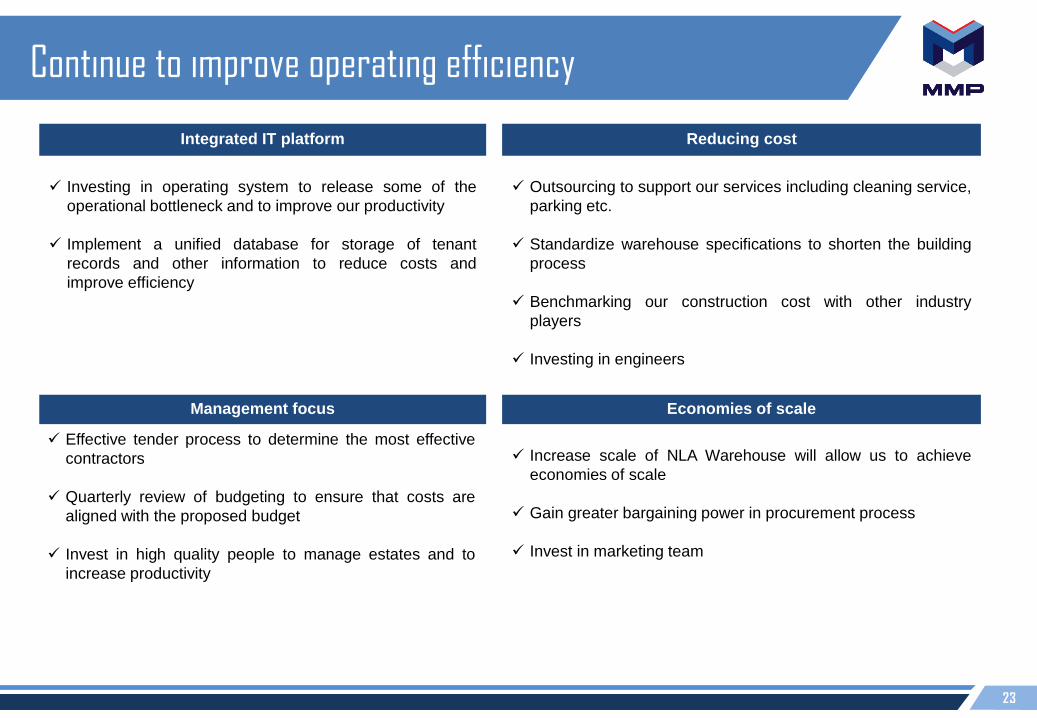

Continue to improve operating efficiency

Investing in operating system to release some of the

operational bottleneck and to improve our productivity

Implement a unified database for storage of tenant

records and other information to reduce costs and

improve efficiency

Increase scale of NLA Warehouse will allow us to achieve

economies of scale

Gain greater bargaining power in procurement process

Invest in marketing team

Integrated IT platform Reducing cost

Outsourcing to support our services including cleaning service,

parking etc.

Standardize warehouse specifications to shorten the building

process

Benchmarking our construction cost with other industry

players

Investing in engineers

Effective tender process to determine the most effective

contractors

Quarterly review of budgeting to ensure that costs are

aligned with the proposed budget

Invest in high quality people to manage estates and to

increase productivity

Management focus Economies of scale

24

Section 3

23

Projects Under Development

25

Projects Under Development

Currently we have 5 (five) projects under construction for approximately 253,195 m2 NLA warehouses, including DS III Phase I.

Location: Tapos, Depok (Phase III)

Land area : 50,000 m2

Net leasable area : 35,000 m2

Tenant : Lazada

Lease period : 10 years

Estimated completion : Q4 2019

Location : Delta Silicon III, Cikarang, Bekasi

Land area : 100,000 m2

Net leasable area : 67,475 m2

Tenant : DHL

Lease period : 10 years

Estimated full completion : 2021

Location : Pondok Ungu, Bekasi

Land area : 55,708 m2

Net leasable area : 52,398 m2

Tenant : Multi-tenant

Estimated full completion : 2021

Location: Jababeka, Bekasi

Land area : 49,351 m2

Net leasable area : 31,680 m2

Estimated completion : 2020

Location: Manyar, East Java

Land area : 114,614 m2

Net leasable area : 66,636 m2

Estimated completion : 2021

26

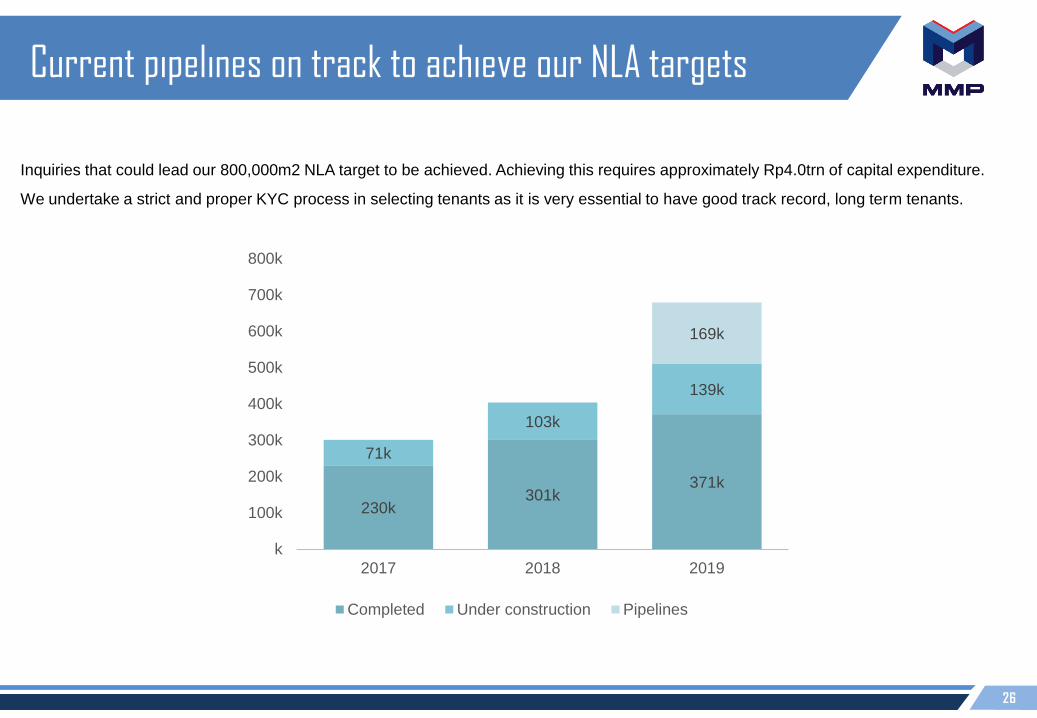

Current pipelines on track to achieve our NLA targets

Inquiries that could lead our 800,000m2 NLA target to be achieved. Achieving this requires approximately Rp4.0trn of capital expenditure.

We undertake a strict and proper KYC process in selecting tenants as it is very essential to have good track record, long term tenants.

230k301k

371k

71k

103k

139k

169k

k

100k

200k

300k

400k

500k

600k

700k

800k

2017 2018 2019

Completed Under construction Pipelines

27

Values created from existing assets

Existing operating assets generate high yield to cost

672 827 833 848

1,607

2,155

2,456

1,302

1,612 1,643 1,787

2,852

3,588

4,065 16.8%

15.2%

17.1%17.6%

13.3%

12.4%12.0%

8.7%

7.8%

8.7% 8.4%

7.5% 7.5% 7.2%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2013 2014 2015 2016 2017 2018 Q3 2019

IP at cost IP at fair value Yield to cost Yield to fair value

28

Section 4

Strong Growth Opportunity

29

The logistics sector in Indonesia remains nascent in comparison to other markets in the region, particularly compared to more

mature markets such as Singapore and Australia.

Notwithstanding this, the growth potential is huge and there are signs of a fundamental imbalance between available supply and

demand for modern logistics warehousing space. We expect to see the Indonesian logistics market evolve into a modern

logistics hub in the same way the sector has evolved in other markets regionally and globally.

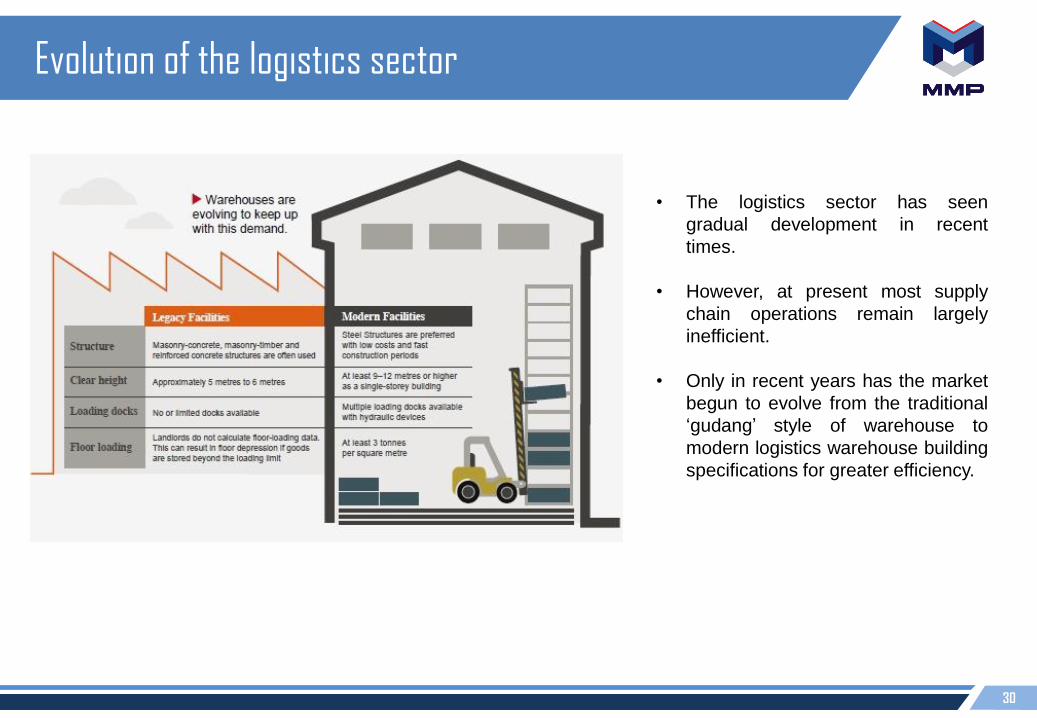

Evolution of the logistics sector

30

• The logistics sector has seen

gradual development in recent

times.

• However, at present most supply

chain operations remain largely

inefficient.

• Only in recent years has the market

begun to evolve from the traditional

‘gudang’ style of warehouse to

modern logistics warehouse building

specifications for greater efficiency.

Evolution of the logistics sector

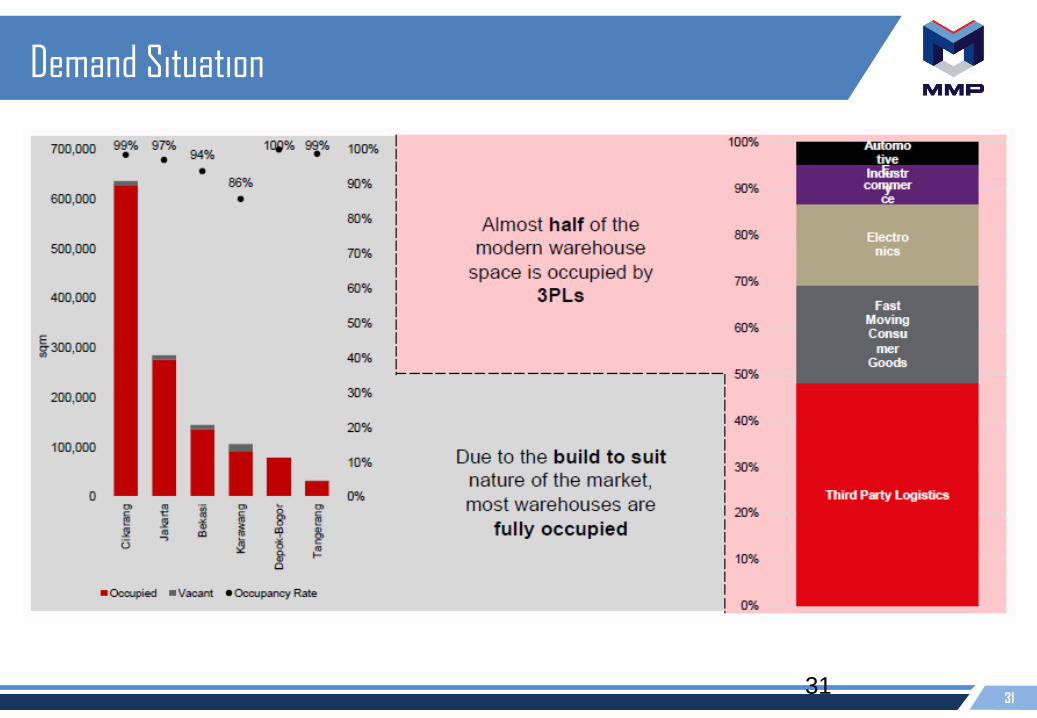

31

Demand Situation

31

32

A nascent industry to enter

26%

19%

9% 8%

14%

9%

13%

2016 2020 2035 Singapore Malaysia Japan South Korea

Logistic cost as % of total GDP

33

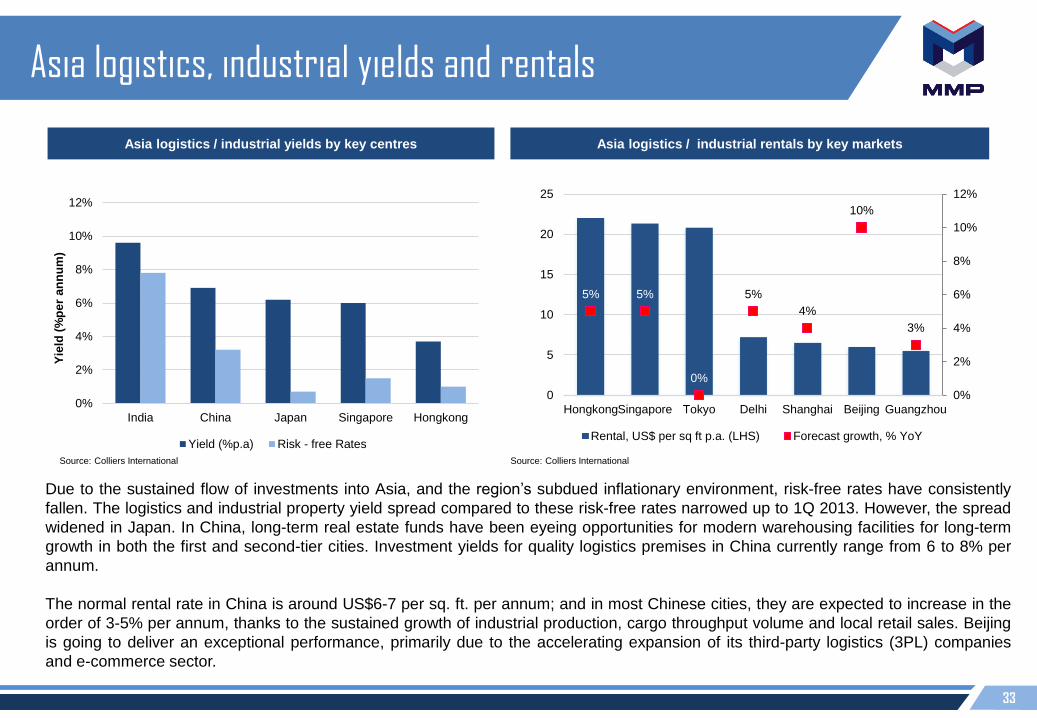

Asia logistics, industrial yields and rentals

Asia logistics / industrial yields by key centres Asia logistics / industrial rentals by key markets

0%

2%

4%

6%

8%

10%

12%

India China Japan Singapore Hongkong

Yie

ld (

%p

er

an

nu

m)

Yield (%p.a) Risk - free Rates

Source: Colliers International

5% 5%

0%

5%

4%

10%

3%

0%

2%

4%

6%

8%

10%

12%

0

5

10

15

20

25

HongkongSingapore Tokyo Delhi Shanghai Beijing Guangzhou

Rental, US$ per sq ft p.a. (LHS) Forecast growth, % YoY

Source: Colliers International

Due to the sustained flow of investments into Asia, and the region’s subdued inflationary environment, risk-free rates have consistently

fallen. The logistics and industrial property yield spread compared to these risk-free rates narrowed up to 1Q 2013. However, the spread

widened in Japan. In China, long-term real estate funds have been eyeing opportunities for modern warehousing facilities for long-term

growth in both the first and second-tier cities. Investment yields for quality logistics premises in China currently range from 6 to 8% per

annum.

The normal rental rate in China is around US$6-7 per sq. ft. per annum; and in most Chinese cities, they are expected to increase in the

order of 3-5% per annum, thanks to the sustained growth of industrial production, cargo throughput volume and local retail sales. Beijing

is going to deliver an exceptional performance, primarily due to the accelerating expansion of its third-party logistics (3PL) companies

and e-commerce sector.

34

Asia Logistics / Industrial Rental

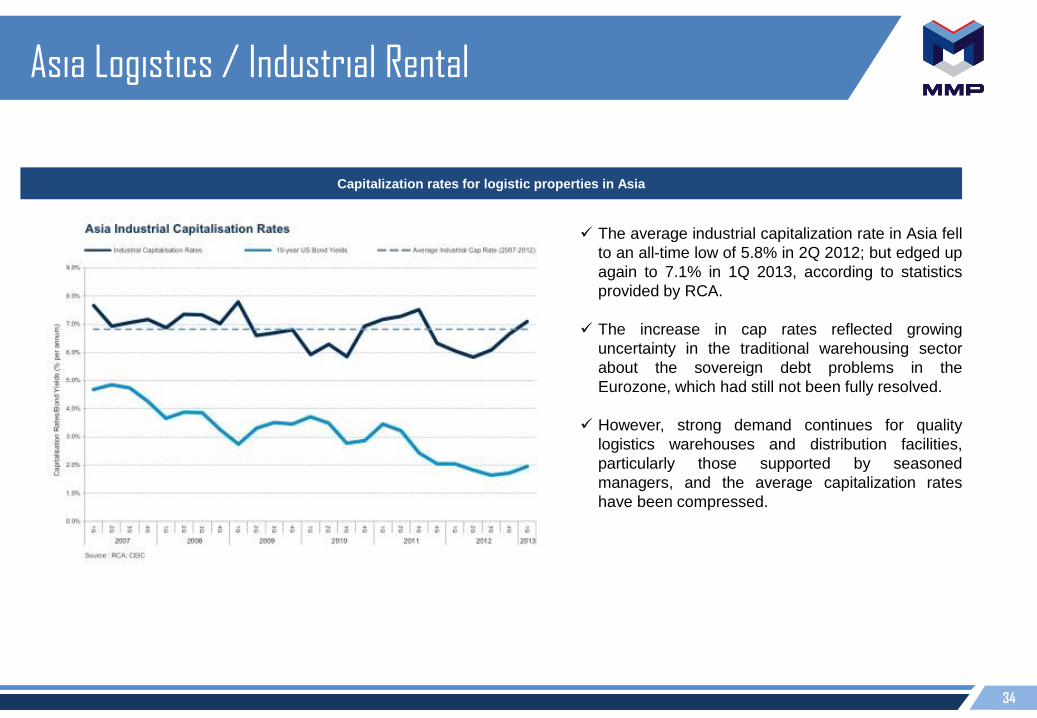

Capitalization rates for logistic properties in Asia

The average industrial capitalization rate in Asia fell

to an all-time low of 5.8% in 2Q 2012; but edged up

again to 7.1% in 1Q 2013, according to statistics

provided by RCA.

The increase in cap rates reflected growing

uncertainty in the traditional warehousing sector

about the sovereign debt problems in the

Eurozone, which had still not been fully resolved.

However, strong demand continues for quality

logistics warehouses and distribution facilities,

particularly those supported by seasoned

managers, and the average capitalization rates

have been compressed.

35

High logistic cost demand better infrastructures

“Besides the very high cost, logistic services in Indonesia are also bad like intervals in Indonesia for imported commodities

requiring 5.5 days and transportation is also very costly” – The Indonesia Chamber of Commerce and Industry (Kadin)

“Indonesia’s high logistic cost is due to under-utilized logistic assets, exacerbated by long and fragmented supply chains, low

port efficiency and road congestion” – World Bank

36

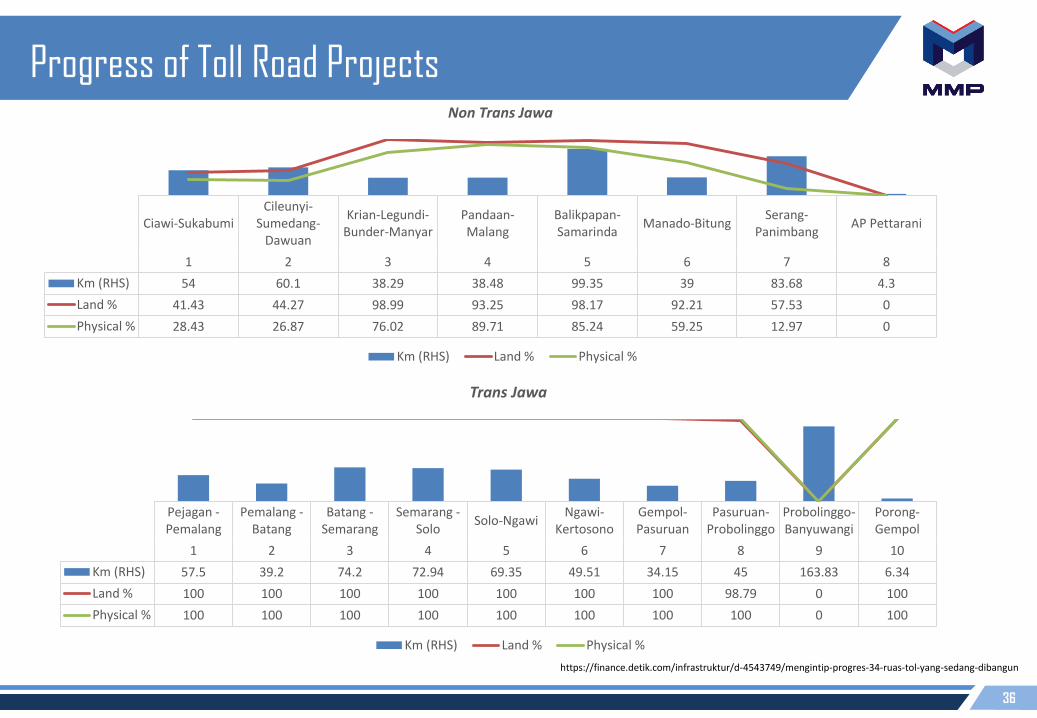

Progress of Toll Road Projects

Ciawi-SukabumiCileunyi-

Sumedang-Dawuan

Krian-Legundi-Bunder-Manyar

Pandaan-Malang

Balikpapan-Samarinda

Manado-BitungSerang-

PanimbangAP Pettarani

1 2 3 4 5 6 7 8

Km (RHS) 54 60.1 38.29 38.48 99.35 39 83.68 4.3

Land % 41.43 44.27 98.99 93.25 98.17 92.21 57.53 0

Physical % 28.43 26.87 76.02 89.71 85.24 59.25 12.97 0

020406080100120

020406080

100

Non Trans Jawa

Km (RHS) Land % Physical %

Pejagan -Pemalang

Pemalang -Batang

Batang -Semarang

Semarang -Solo

Solo-NgawiNgawi-

KertosonoGempol-Pasuruan

Pasuruan-Probolinggo

Probolinggo-Banyuwangi

Porong-Gempol

1 2 3 4 5 6 7 8 9 10

Km (RHS) 57.5 39.2 74.2 72.94 69.35 49.51 34.15 45 163.83 6.34

Land % 100 100 100 100 100 100 100 98.79 0 100

Physical % 100 100 100 100 100 100 100 100 0 100

020406080100120140160180

020406080

100

Trans Jawa

Km (RHS) Land % Physical %

https://finance.detik.com/infrastruktur/d-4543749/mengintip-progres-34-ruas-tol-yang-sedang-dibangun

37

Progress of Toll Road Projects

No Jabodetabek Km (RHS) Land % Physical %

1 Cengkareng-Kunciran 11 63.96 52.52

2 Kunciran-Serpong 10.14 98.7 88.76

3 Serpong-Cinere 11.19 79.23 56.55

4 Cinere-Jagorawi 14.64 65.73 62.6

5 Cimanggis-Cibitung 26.5 70.45 10.47

6 Cibitung-Cilincing 32.76 76.63 48.07

7 Depok-Antasari 21.54 56.6 38.94

8 Bekasi-Cawang-Kp Melayu 21.04 60.53 75.2

9 Semanan-Pulo Gebang 31.1 24.05 8.45

10Jakarta-Cikampek II Elevated

14.19 100 70.04

11 Japek II Sisi Selatan 62 0 0

https://finance.detik.com/infrastruktur/d-4543749/mengintip-progres-34-ruas-tol-yang-sedang-dibangun

38

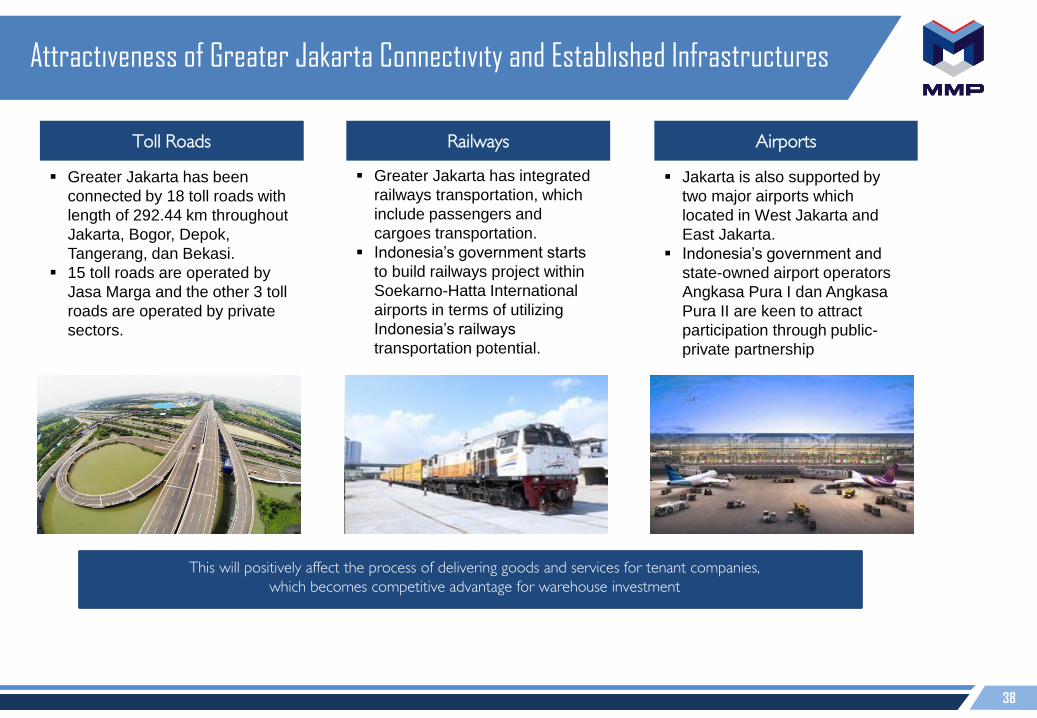

Attractiveness of Greater Jakarta Connectivity and Established Infrastructures

Toll Roads AirportsRailways

Greater Jakarta has been

connected by 18 toll roads with

length of 292.44 km throughout

Jakarta, Bogor, Depok,

Tangerang, dan Bekasi.

15 toll roads are operated by

Jasa Marga and the other 3 toll

roads are operated by private

sectors.

Greater Jakarta has integrated

railways transportation, which

include passengers and

cargoes transportation.

Indonesia’s government starts

to build railways project within

Soekarno-Hatta International

airports in terms of utilizing

Indonesia’s railways

transportation potential.

Jakarta is also supported by

two major airports which

located in West Jakarta and

East Jakarta.

Indonesia’s government and

state-owned airport operators

Angkasa Pura I dan Angkasa

Pura II are keen to attract

participation through public-

private partnership

This will positively affect the process of delivering goods and services for tenant companies,

which becomes competitive advantage for warehouse investment

39

Tanjung Perak Port

Juanda air Port

In the near future, Gresik, Sidoarjo, and Surabaya will become our expansion target

21 Km

22 Km

In terms of land prices and availability, Gresik and Sidoarjo seem potential for warehouse location. It offers

effective route to airport and port which could be added value for our future tenant.

35 Km

6 Km

Key Industry Served :FMCG, FnB, Electronic,

Chemicals

Greater Surabaya

Attractiveness of the locations - Connectivity

40

Industries driving the demand for logistics

Healthy Growth in FMCGs and Retail

Urbanisation and growing wealth is already translating into

growth in the FMCG sector and retail sales. This will

increase the appeal of the logistics real estate market to a

broader spectrum of modern international logistics players.

Indonesia has a robust manufacturing sector

Indonesia has a large manufacturing base driven by a large

domestic consumer market and low labour costs. The robust

manufacturing sector is another major driver of demand for

logistics services and associated real estate. In 2015,

manufacturing accounted for 22% of GDP.

Source: JLL

41

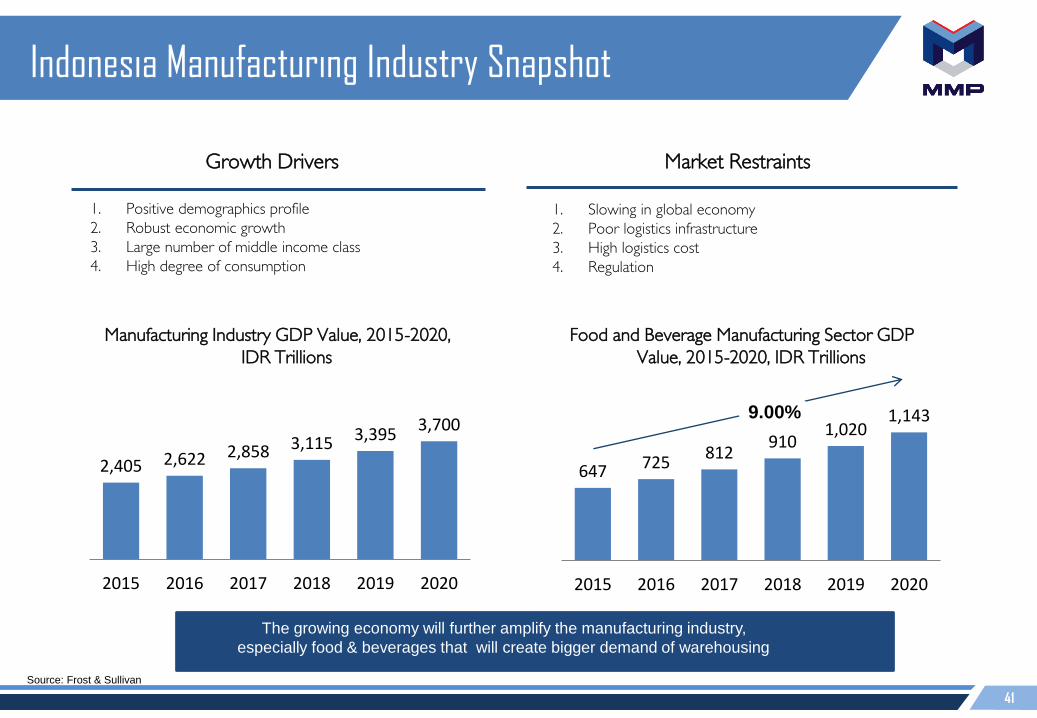

Indonesia Manufacturing Industry Snapshot

647 725812

9101,020

1,143

2015 2016 2017 2018 2019 2020

9.00%

Food and Beverage Manufacturing Sector GDP

Value, 2015-2020, IDR Trillions

2,405 2,622 2,858 3,115 3,3953,700

2015 2016 2017 2018 2019 2020

1. Positive demographics profile

2. Robust economic growth

3. Large number of middle income class

4. High degree of consumption

Growth Drivers Market Restraints

1. Slowing in global economy

2. Poor logistics infrastructure

3. High logistics cost

4. Regulation

Manufacturing Industry GDP Value, 2015-2020,

IDR Trillions

The growing economy will further amplify the manufacturing industry,

especially food & beverages that will create bigger demand of warehousing

Source: Frost & Sullivan

42

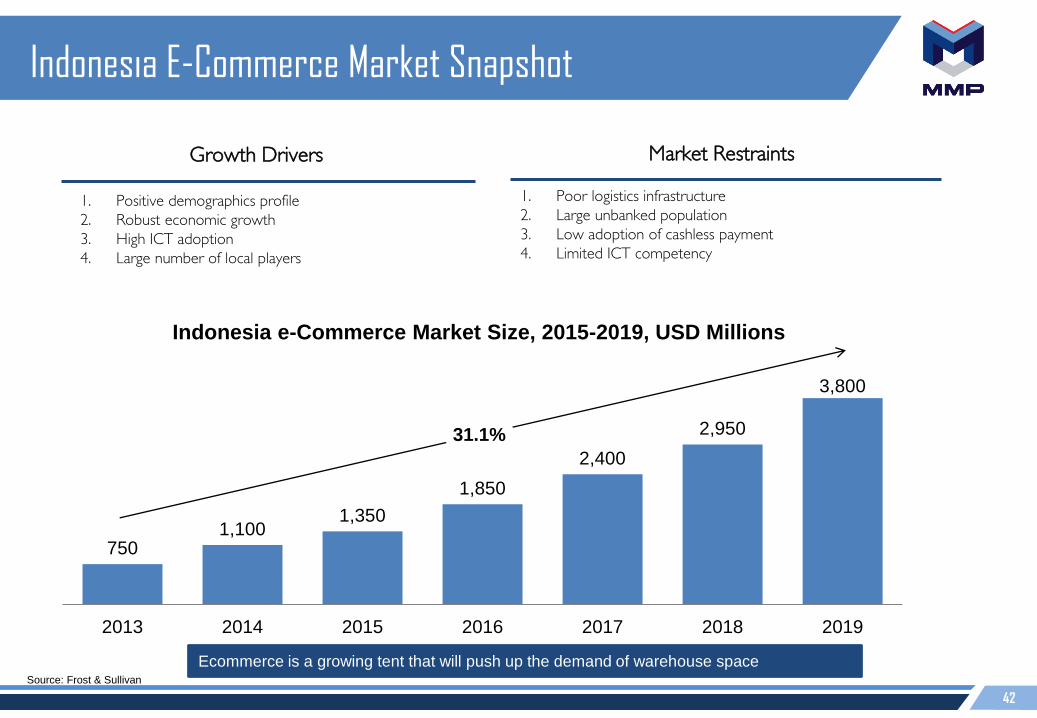

1. Positive demographics profile

2. Robust economic growth

3. High ICT adoption

4. Large number of local players

Growth Drivers Market Restraints

1. Poor logistics infrastructure

2. Large unbanked population

3. Low adoption of cashless payment

4. Limited ICT competency

7501,100

1,350

1,850

2,400

2,950

3,800

2013 2014 2015 2016 2017 2018 2019

31.1%

Indonesia e-Commerce Market Size, 2015-2019, USD Millions

Ecommerce is a growing tent that will push up the demand of warehouse spaceSource: Frost & Sullivan

Indonesia E-Commerce Market Snapshot

43

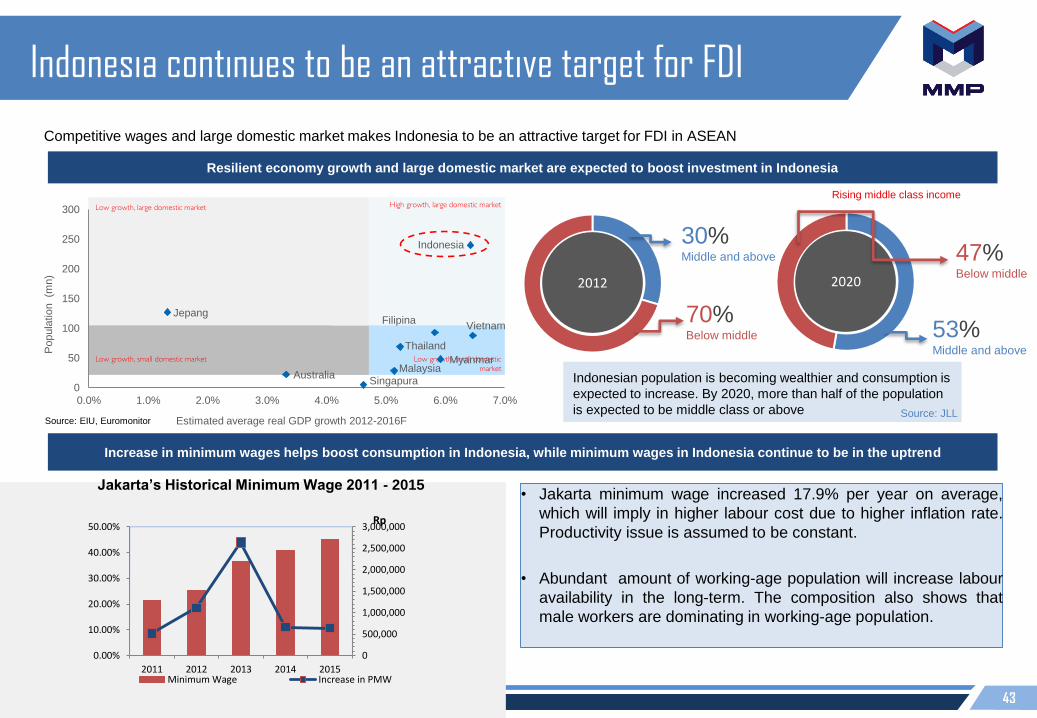

Source: EIU, Euromonitor

High growth, large domestic market

Low growth, small domestic

market

Low growth, small domestic market

Low growth, large domestic market

Indonesia

Singapura

Filipina

Thailand

Malaysia

Jepang

Australia

Vietnam

Myanmar

0

50

100

150

200

250

300

0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0% 7.0%

Popula

tio

n (m

n)

Estimated average real GDP growth 2012-2016F

Indonesia continues to be an attractive target for FDI

Competitive wages and large domestic market makes Indonesia to be an attractive target for FDI in ASEAN

Rising middle class income

• Jakarta minimum wage increased 17.9% per year on average,

which will imply in higher labour cost due to higher inflation rate.

Productivity issue is assumed to be constant.

• Abundant amount of working-age population will increase labour

availability in the long-term. The composition also shows that

male workers are dominating in working-age population.

Resilient economy growth and large domestic market are expected to boost investment in Indonesia

Increase in minimum wages helps boost consumption in Indonesia, while minimum wages in Indonesia continue to be in the uptrend

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

2011 2012 2013 2014 2015Minimum Wage Increase in PMW

Rp

Jakarta’s Historical Minimum Wage 2011 - 2015

Source: JLL

2012 2020

Indonesian population is becoming wealthier and consumption is

expected to increase. By 2020, more than half of the population

is expected to be middle class or above

30%Middle and above

70%Below middle 53%

Middle and above

47%Below middle

44

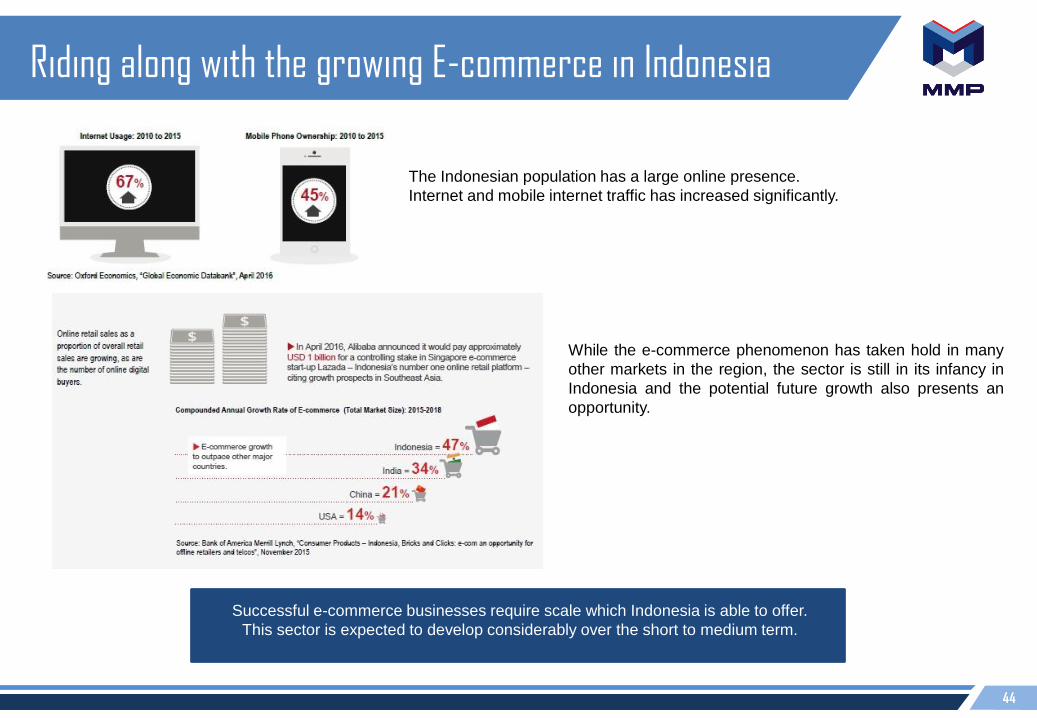

Riding along with the growing E-commerce in Indonesia

Successful e-commerce businesses require scale which Indonesia is able to offer.

This sector is expected to develop considerably over the short to medium term.

While the e-commerce phenomenon has taken hold in many

other markets in the region, the sector is still in its infancy in

Indonesia and the potential future growth also presents an

opportunity.

The Indonesian population has a large online presence.

Internet and mobile internet traffic has increased significantly.

45

Section 5

47

Key Financial

46

Solid revenues growth

Development of NLA and Occupancy Rate

MMP has successfully posted revenue Rp245.0 bn in 3Q19 supported by stable NLA and occupancy rate. Currently, our NLA stood at 321,395

sqm.

2013 2014 2015 2016 2017 2018 9M19

Net Leasable Area (sqm) 139,811 158,137 163,911 163,911 230,370 300,680 321,395

Leased area (sqm) 135,311 154,623 159,318 163,911 230,157 298,775 318,165

Occupancy Rate (%) 97.0% 94.0% 97.0% 100.0% 99.9% 99.4% 99.0%

139,811 158,137 163,911 163,911

230,370

300,680 321,395

96.8%94.0%

97.2%100.0% 99.9% 99.4% 99.0%

50.0%

55.0%

60.0%

65.0%

70.0%

75.0%

80.0%

85.0%

90.0%

95.0%

100.0%

2013 2014 2015 2016 2017 2018 9M19

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

47

261

65

323

217

144

107

-

142 163 175

209

299

245 220

2014 2015 2016 2017 2018 3Q19 3Q18

IDR

mili

ar

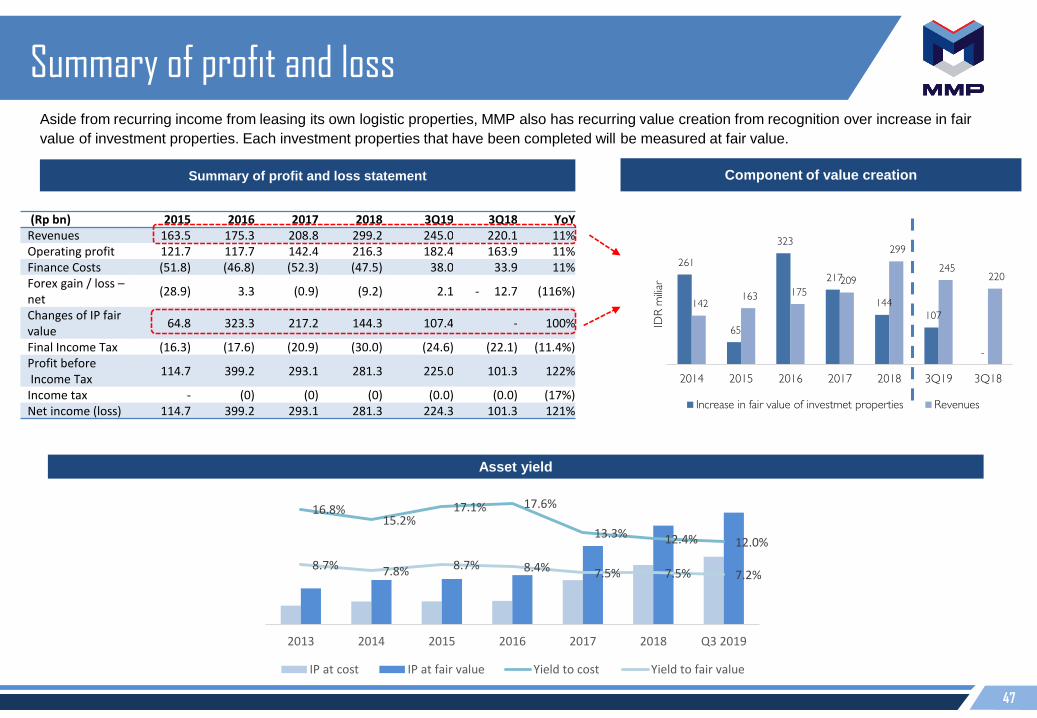

Increase in fair value of investmet properties Revenues

(Rp bn) 2015 2016 2017 2018 3Q19 3Q18 YoYRevenues 163.5 175.3 208.8 299.2 245.0 220.1 11%Operating profit 121.7 117.7 142.4 216.3 182.4 163.9 11%Finance Costs (51.8) (46.8) (52.3) (47.5) 38.0 33.9 11%Forex gain / loss –net

(28.9) 3.3 (0.9) (9.2) 2.1 - 12.7 (116%)

Changes of IP fair value

64.8 323.3 217.2 144.3 107.4 - 100%

Final Income Tax (16.3) (17.6) (20.9) (30.0) (24.6) (22.1) (11.4%)Profit beforeIncome Tax

114.7 399.2 293.1 281.3 225.0 101.3 122%

Income tax - (0) (0) (0) (0.0) (0.0) (17%)Net income (loss) 114.7 399.2 293.1 281.3 224.3 101.3 121%

Summary of profit and loss

Summary of profit and loss statement

Aside from recurring income from leasing its own logistic properties, MMP also has recurring value creation from recognition over increase in fair

value of investment properties. Each investment properties that have been completed will be measured at fair value.

Asset yield

Component of value creation

16.8%15.2%

17.1% 17.6%

13.3% 12.4% 12.0%

8.7% 7.8% 8.7% 8.4% 7.5% 7.5% 7.2%

0.0%

5.0%

10.0%

15.0%

20.0%

-

1,000

2,000

3,000

4,000

5,000

2013 2014 2015 2016 2017 2018 Q3 2019

IP at cost IP at fair value Yield to cost Yield to fair value

48

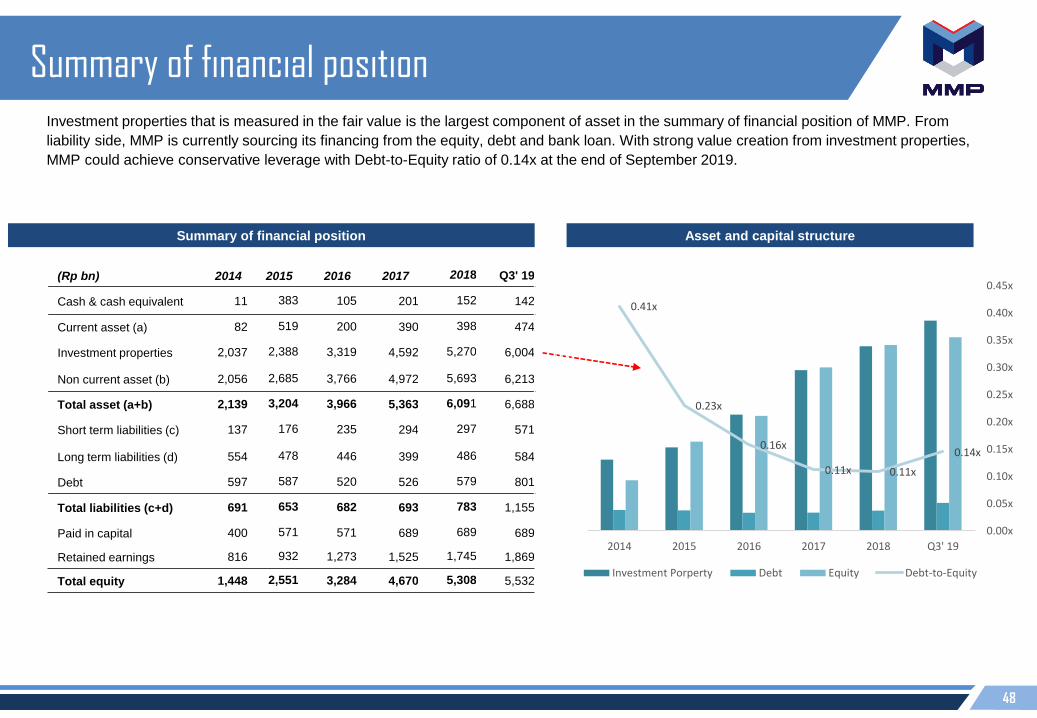

Summary of financial position

Summary of financial position Asset and capital structure

Investment properties that is measured in the fair value is the largest component of asset in the summary of financial position of MMP. From

liability side, MMP is currently sourcing its financing from the equity, debt and bank loan. With strong value creation from investment properties,

MMP could achieve conservative leverage with Debt-to-Equity ratio of 0.14x at the end of September 2019.

(Rp bn) 2014 2015 2016 2017 2018 Q3' 19

Cash & cash equivalent 11 383 105 201 152 142

Current asset (a) 82 519 200 390 398 474

Investment properties 2,037 2,388 3,319 4,592 5,270 6,004

Non current asset (b) 2,056 2,685 3,766 4,972 5,693 6,213

Total asset (a+b) 2,139 3,204 3,966 5,363 6,091 6,688

Short term liabilities (c) 137 176 235 294 297 571

Long term liabilities (d) 554 478 446 399 486 584

Debt 597 587 520 526 579 801

Total liabilities (c+d) 691 653 682 693 783 1,155

Paid in capital 400 571 571 689 689 689

Retained earnings 816 932 1,273 1,525 1,745 1,869

Total equity 1,448 2,551 3,284 4,670 5,308 5,532

0.41x

0.23x

0.16x

0.11x 0.11x

0.14x

0.00x

0.05x

0.10x

0.15x

0.20x

0.25x

0.30x

0.35x

0.40x

0.45x

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2014 2015 2016 2017 2018 Q3' 19

Investment Porperty Debt Equity Debt-to-Equity

49

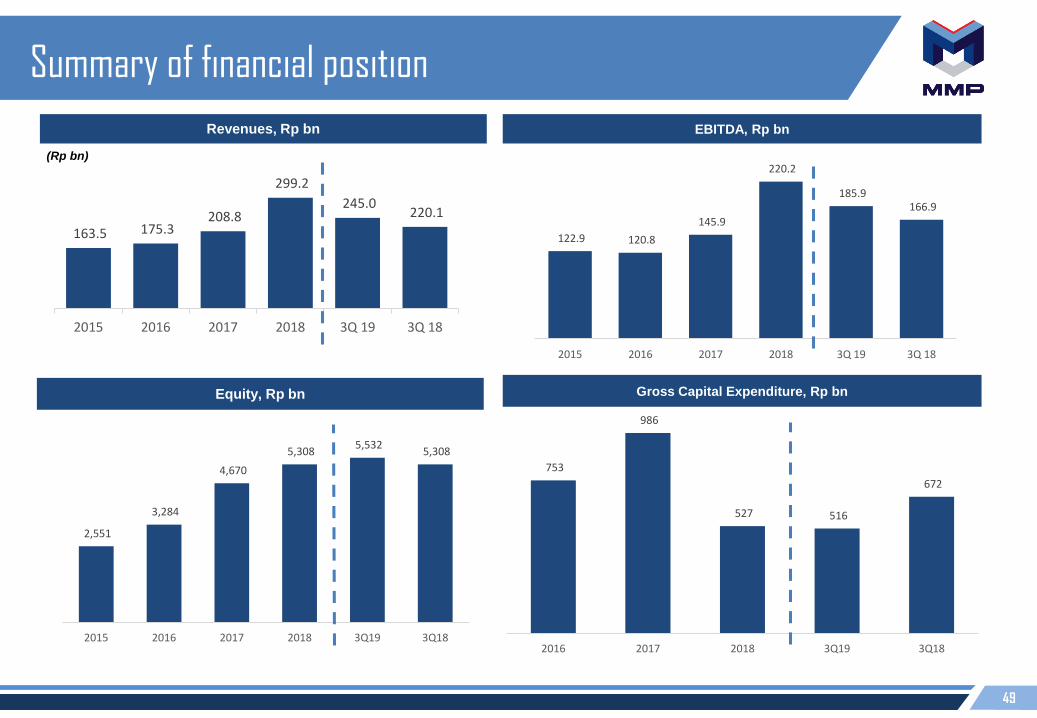

753

986

527 516

672

2016 2017 2018 3Q19 3Q18

2,551

3,284

4,670

5,308 5,532

5,308

-

1,000

2,000

3,000

4,000

5,000

6,000

2015 2016 2017 2018 3Q19 3Q18

122.9 120.8

145.9

220.2

185.9 166.9

-

50.0

100.0

150.0

200.0

250.0

2015 2016 2017 2018 3Q 19 3Q 18

163.5 175.3 208.8

299.2

245.0 220.1

2015 2016 2017 2018 3Q 19 3Q 18

Summary of financial position

Revenues, Rp bn EBITDA, Rp bn

Equity, Rp bn Gross Capital Expenditure, Rp bn

(Rp bn)

50

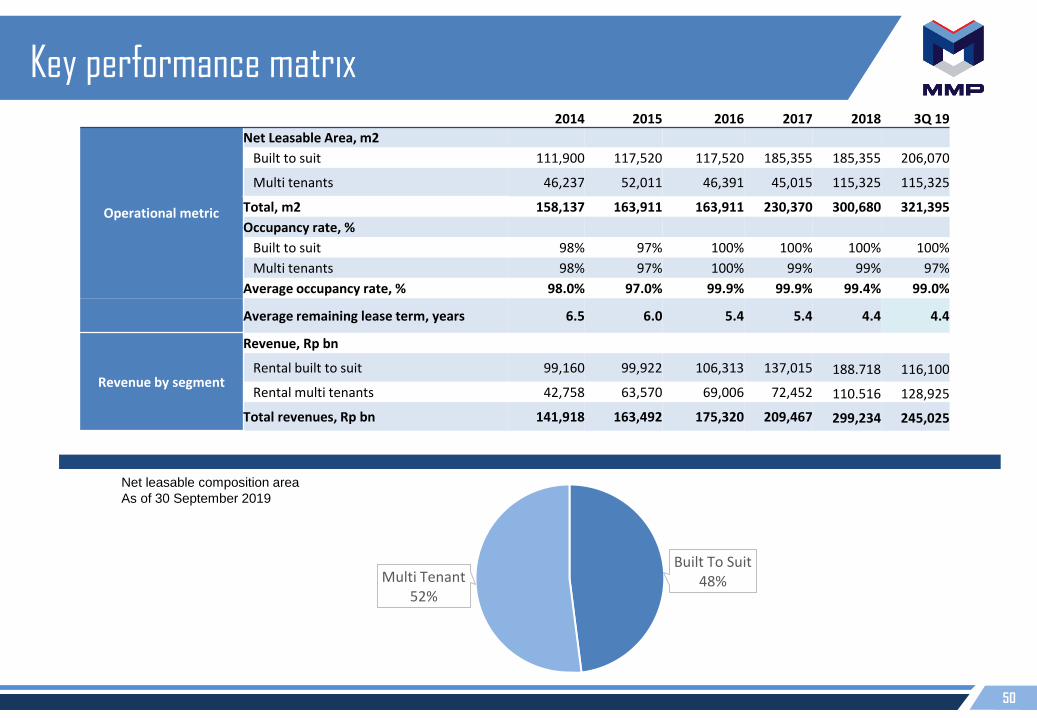

2014 2015 2016 2017 2018 3Q 19

Operational metric

Net Leasable Area, m2

Built to suit 111,900 117,520 117,520 185,355 185,355 206,070

Multi tenants 46,237 52,011 46,391 45,015 115,325 115,325

Total, m2 158,137 163,911 163,911 230,370 300,680 321,395

Occupancy rate, %

Built to suit 98% 97% 100% 100% 100% 100%

Multi tenants 98% 97% 100% 99% 99% 97%

Average occupancy rate, % 98.0% 97.0% 99.9% 99.9% 99.4% 99.0%

Average remaining lease term, years 6.5 6.0 5.4 5.4 4.4 4.4

Revenue by segment

Revenue, Rp bn

Rental built to suit 99,160 99,922 106,313 137,015 188.718 116,100

Rental multi tenants 42,758 63,570 69,006 72,452 110.516 128,925

Total revenues, Rp bn 141,918 163,492 175,320 209,467 299,234 245,025

Key performance matrix

Net leasable composition area

As of 30 September 2019

Built To Suit48%Multi Tenant

52%

51

Section 6

Assets in Details

52

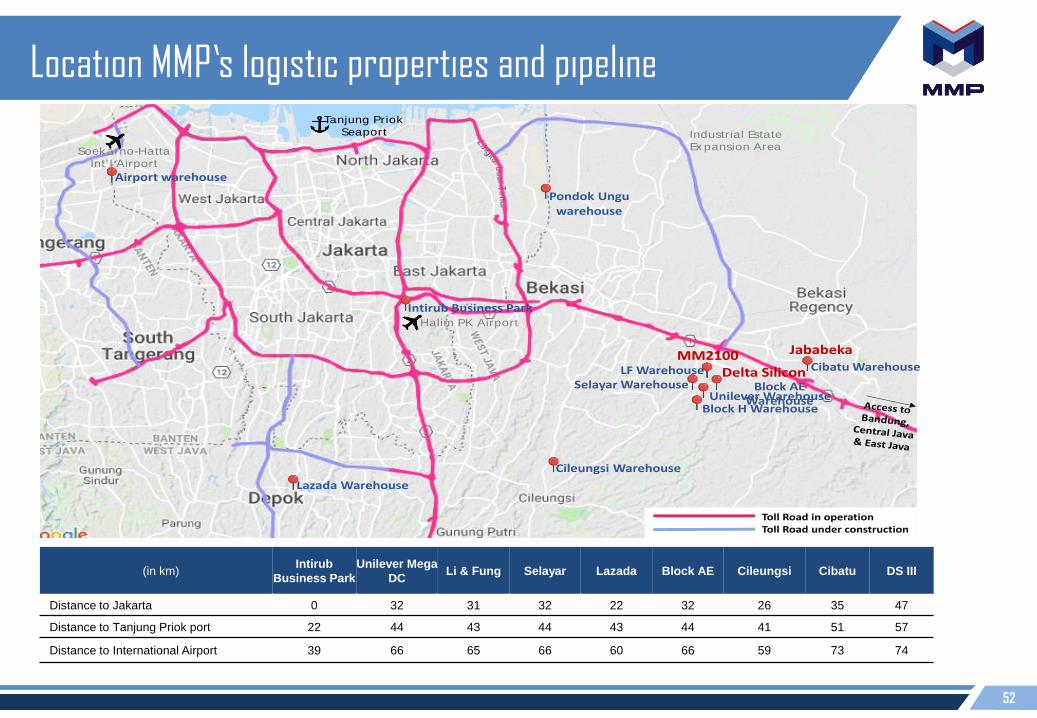

Location MMP’s logistic properties and pipeline

(in km)Intirub

Business Park

Unilever Mega

DCLi & Fung Selayar Lazada Block AE Cileungsi Cibatu DS III

Distance to Jakarta 0 32 31 32 22 32 26 35 47

Distance to Tanjung Priok port 22 44 43 44 43 44 41 51 57

Distance to International Airport 39 66 65 66 60 66 59 73 74

Tanjung Priok

Seaport Industrial Estate

Ex pansion Area

Halim PK Airport

Pondok Ungu warehouse

Lazada Warehouse

Cileungsi Warehouse

Intirub Business Park

JababekaMM2100Cibatu Warehouse

Block AE Warehouse

LF WarehouseSelayar Warehouse

Unilever WarehouseBlock H Warehouse

Delta Silicon

Airport warehouse

Soekarno-Hatta

Int’ l Airport

Toll Road in operation Toll Road under construction

53

Tanjung Perak Port

Juanda Air Port

Toll RoadsIn Operation

Under construction

Planning

In (Km) Manyar Warehouse

Distance to Surabaya 31

Distance to Airport 52

Distance to Tanjung Perak Port 29

Location MMP’s logistic properties and pipeline

MMP properties

54

Unilever Mega DC Warehouse

Location : MM2100 industrial estates, West

Cikarang, Bekasi

Land area : 197.690 m2

Gross floor area : 156.462 m2

NLA : 90.288 m2

Lease period : 10 years, with an option to extend

another 10 years

Operator : PT Linfox Logistics Indonesia

Floor capacity : 6 ton per m2

Ceiling height : 12 m (center 17 m)

Specification:

- Super flat floors (FF; Floor Flatness);

- Double deep pallet racking system;

- Heat shield;

- Parking area up to 104 truck;

- 85 loading doors;

- 8 loading dock levelers;

- Sprinkler on each rack, with immediate response;

- Fire extinguisher with standard of ULFM;

- Rental that include racking, sprinkler and office.

55

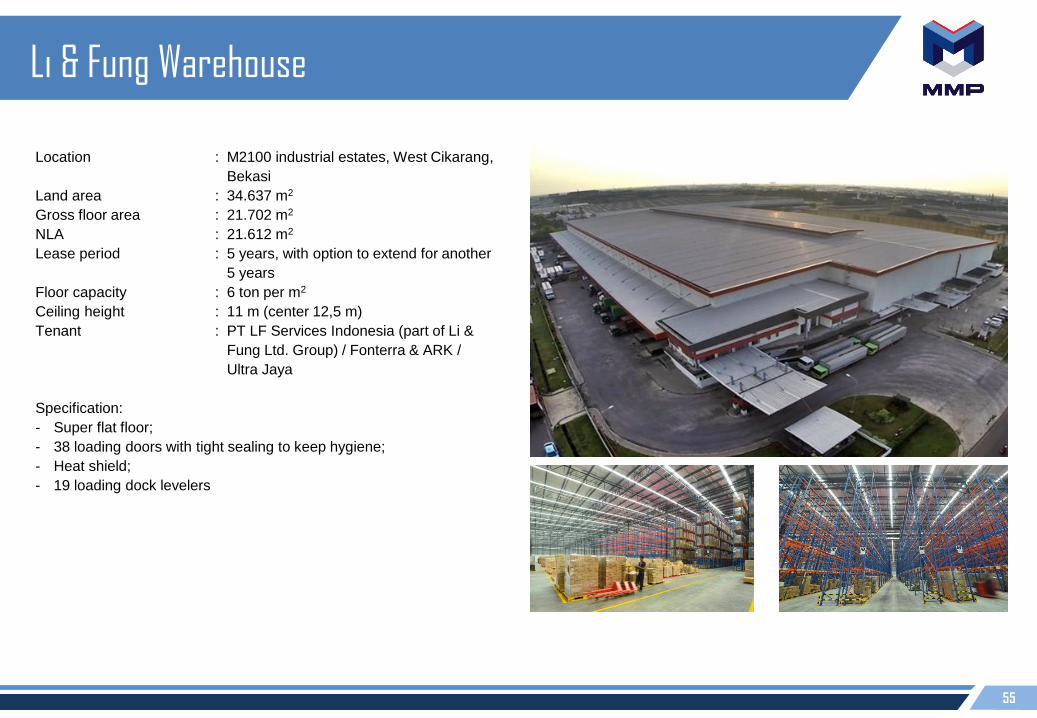

Li & Fung Warehouse

Location : M2100 industrial estates, West Cikarang,

Bekasi

Land area : 34.637 m2

Gross floor area : 21.702 m2

NLA : 21.612 m2

Lease period : 5 years, with option to extend for another

5 years

Floor capacity : 6 ton per m2

Ceiling height : 11 m (center 12,5 m)

Tenant : PT LF Services Indonesia (part of Li &

Fung Ltd. Group) / Fonterra & ARK /

Ultra Jaya

Specification:

- Super flat floor;

- 38 loading doors with tight sealing to keep hygiene;

- Heat shield;

- 19 loading dock levelers

56

Intirub Busines Park I & II Warehouse

Intirub Business Park

Location : Halim, East Jakarta

Land area : 60.575 m2

Gross floor area : 53.305 m2 (warehouse) + 11.151 m2 (office)

NLA : 36.622 m2 (warehouse) + 8.393 m2 (office)

Floor capacity : up to 4,5 ton per m2

Ceiling height : 10 m (IBP I)

9 m (IBP II)

Warehouse specification : warehouse with semi basement, 3 floor office

and parking area

Special specifications : 5 loading dock levelers (IBP I)

10 loading dock levellers (IBP II)

Tenants : DHL, ARK/Ingram, Yokogawa, aCommerce

(warehouse), Bank BNI46, DHL, Mahadasha,

Scan Global (office). Grundfos, DHL, ARK,

MHE-Demag (warehouse), Grundfos, Deraya,

MHE-Demag (office)

58

57

Selayar Warehouse

Location : MM2100 industrial estates, West

Cikarang, Bekasi

Land area : 9.164 m2

Gross floor area : 5.742 m2

NLA : 5.620 m2

Floor capacity : 4 ton per m2

Ceiling height : 9 m (center 13 m)

Special specifications : 6 loading doors with 2 loading dock

levelers

Tenants : Windu Persada Cargo

58

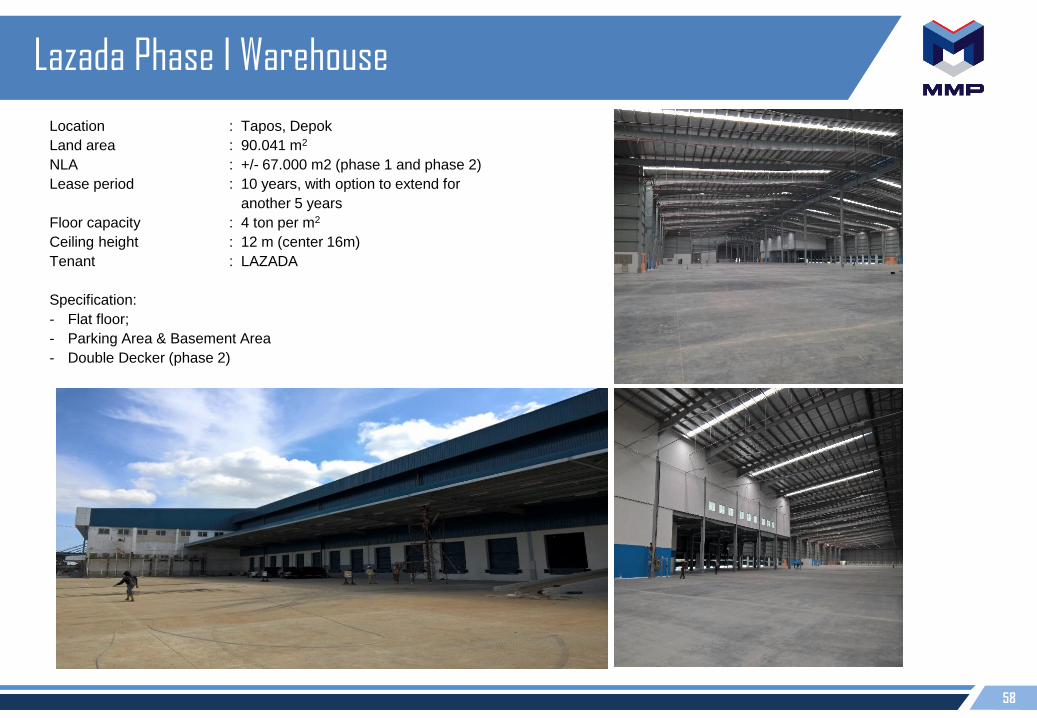

Lazada Phase I Warehouse

Location : Tapos, Depok

Land area : 90.041 m2

NLA : +/- 67.000 m2 (phase 1 and phase 2)

Lease period : 10 years, with option to extend for

another 5 years

Floor capacity : 4 ton per m2

Ceiling height : 12 m (center 16m)

Tenant : LAZADA

Specification:

- Flat floor;

- Parking Area & Basement Area

- Double Decker (phase 2)

59

Cibatu Warehouse

Location : Scientia Boulevard, Jababeka V

Cikarang

Land area : 50,000 m2

Net Leasable Area : 36,335 m2

Lease period : 10 years

Tenant : Ark Logistics

Estimated Completion Year : 2017

Architectural & Structural Specification:

- Floor Load Capacity : 4 ton/m2

- Foundation : Concrete Pile

- Floor : Reinforced Concrete

- Column : Tappered Steel Column

- Roof Structure : Tappered Steel Beam

- Floor Flatness : Superflat

- Effective Ceiling Height : 12 m

- Wall : AAC Wall + Metal Cladding

- Roof : Boltless Metal Roof + Insulation

- Loading Door : 19 Units

- Canopy Width : 13 m

Mechanical/Electrical Specification:

- Sprinkler : Yes

- Smoke Detector : Beam Detector

- Artificial Lighting : 100 lux (Warehouse)

- Generator Set : 400 KVA

60

Building value delivering result

From Abandoned Factory In progress to become the largest DC for LAZADA Indonesia

61

Block AE Warehouse

Location : MM2100 Industrial Estates, West Cikarang, Bekasi

Land Area : 35,740 m2

Net Leasable Area : 38,854 m2

Completion Year : 2018Cawang

Intersection Cikunir

Intersection

MM2100

Industrial Estate

Architectural & Structural Specification:

-Floor Load Capacity : 4 ton/m2 (Ground Floor)

3 ton/m2 (Upper Floor)

-Foundation : Concrete Pile

-Floor : Reinforced Concrete

-Column : Reinforced Concrete

-Roof Structure: Steel Truss

-Floor Flatness : Flat

-Effective Ceiling Height : 9 m (Ground Floor)

8 m (Upper Floor)

-Wall : AAC Wall + Metal Cladding

-Roof : Boltless Metal Roof + Insulation

-Loading Doors : 48 Units

-Canopy Width : 10 m (Ground Floor)

8 m (Upper Floor)

Mechanical/Electrical Specification:

- Sprinkler : Yes

- Smoke Detector : Beam Detector

- Artificial Lighting : 120 lux (Warehouse)

- Generator Set : 300 KVA

62

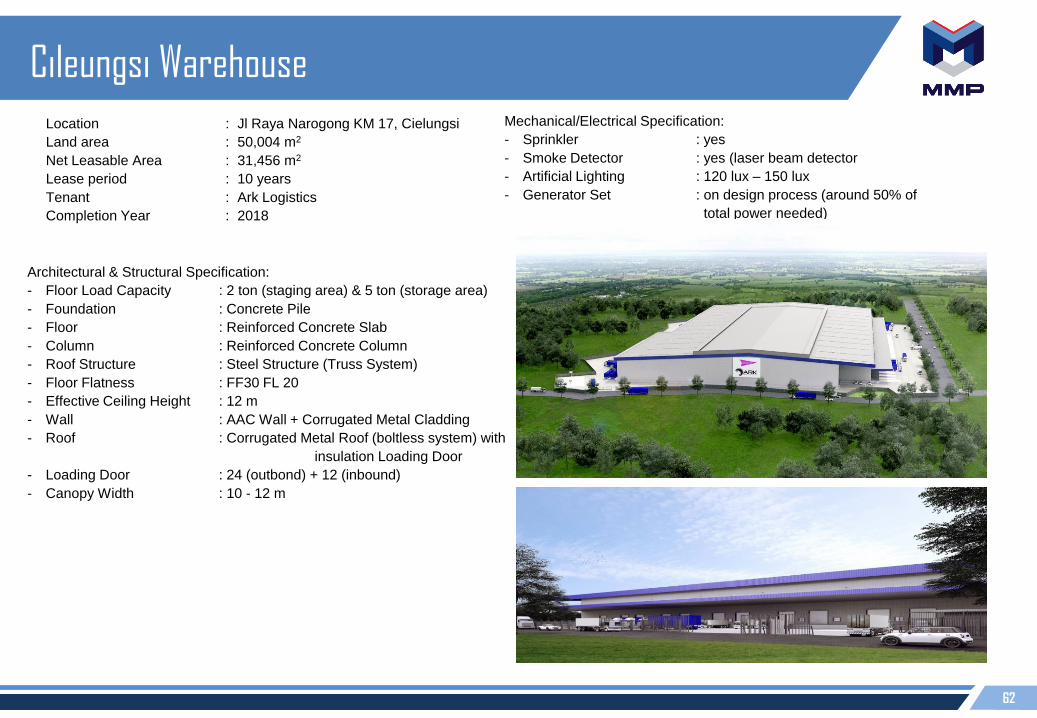

Cileungsi Warehouse

Location : Jl Raya Narogong KM 17, Cielungsi

Land area : 50,004 m2

Net Leasable Area : 31,456 m2

Lease period : 10 years

Tenant : Ark Logistics

Completion Year : 2018

Mechanical/Electrical Specification:

- Sprinkler : yes

- Smoke Detector : yes (laser beam detector

- Artificial Lighting : 120 lux – 150 lux

- Generator Set : on design process (around 50% of

total power needed)

Architectural & Structural Specification:

- Floor Load Capacity : 2 ton (staging area) & 5 ton (storage area)

- Foundation : Concrete Pile

- Floor : Reinforced Concrete Slab

- Column : Reinforced Concrete Column

- Roof Structure : Steel Structure (Truss System)

- Floor Flatness : FF30 FL 20

- Effective Ceiling Height : 12 m

- Wall : AAC Wall + Corrugated Metal Cladding

- Roof : Corrugated Metal Roof (boltless system) with

insulation Loading Door

- Loading Door : 24 (outbond) + 12 (inbound)

- Canopy Width : 10 - 12 m

63

Delta Silicon III

Location : Delta Silicon 3, Cikarang

Land area : 100.000 m2

NLA : +/- 67.475 m2 (phase 1, 2 and 3)

Lease period : 10 years

Floor capacity : 4 ton per m2

Ceiling height : 14 m

Tenant : DHL

Specification:

Floor : Reinforced Concrete, flatness FF30 FL 25

Foundation : Concrete pile with pile‐cap

Slab/Column/Beam : Steel Truss

Canopy : Steel Truss

64

Section 7

Other Financial Info

65

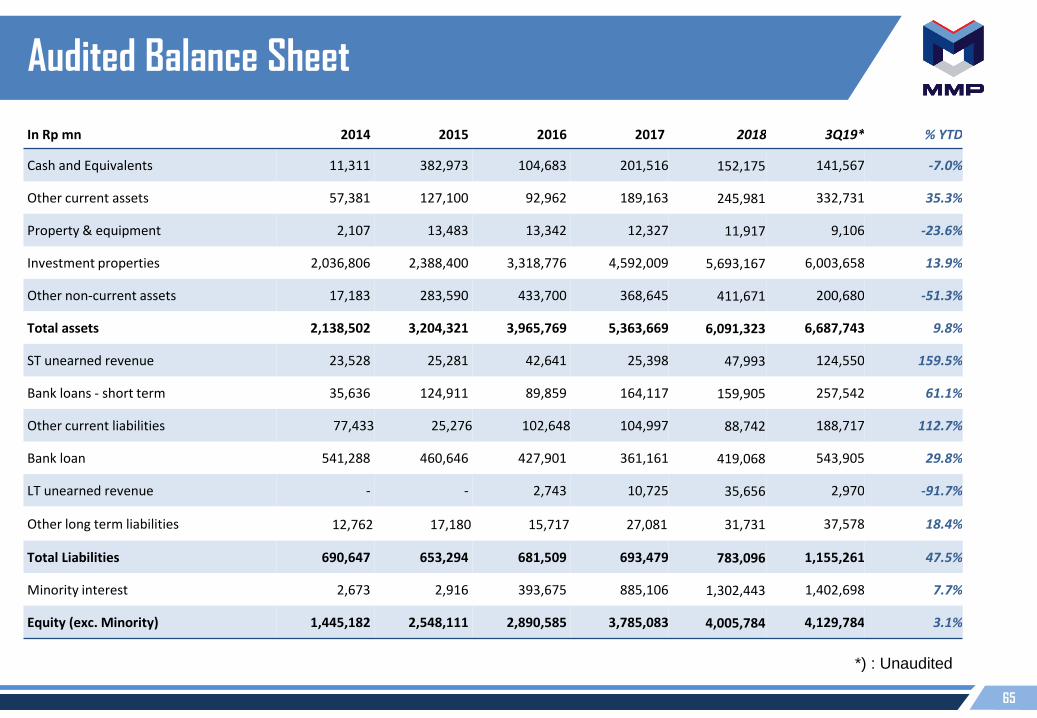

Audited Balance Sheet

In Rp mn 2014 2015 2016 2017 2018 3Q19* % YTD

Cash and Equivalents 11,311 382,973 104,683 201,516 152,175 141,567 -7.0%

Other current assets 57,381 127,100 92,962 189,163 245,981 332,731 35.3%

Property & equipment 2,107 13,483 13,342 12,327 11,917 9,106 -23.6%

Investment properties 2,036,806 2,388,400 3,318,776 4,592,009 5,693,167 6,003,658 13.9%

Other non-current assets 17,183 283,590 433,700 368,645 411,671 200,680 -51.3%

Total assets 2,138,502 3,204,321 3,965,769 5,363,669 6,091,323 6,687,743 9.8%

ST unearned revenue 23,528 25,281 42,641 25,398 47,993 124,550 159.5%

Bank loans - short term 35,636 124,911 89,859 164,117 159,905 257,542 61.1%

Other current liabilities 77,433 25,276 102,648 104,997 88,742 188,717 112.7%

Bank loan 541,288 460,646 427,901 361,161 419,068 543,905 29.8%

LT unearned revenue - - 2,743 10,725 35,656 2,970 -91.7%

Other long term liabilities 12,762 17,180 15,717 27,081 31,731 37,578 18.4%

Total Liabilities 690,647 653,294 681,509 693,479 783,096 1,155,261 47.5%

Minority interest 2,673 2,916 393,675 885,106 1,302,443 1,402,698 7.7%

Equity (exc. Minority) 1,445,182 2,548,111 2,890,585 3,785,083 4,005,784 4,129,784 3.1%

*) : Unaudited

66

Audited Profit and Loss Statement

In Rp mn 2014 2015 2016 2017 2018 3Q '19* 3Q '18 % Y/Y

Revenue 141,918 163,492 175,320 208,794 299,234 245,025 220,134 11.3%

Cost of revenue 13,084 16,059 18,444 20,146 25,396 20,341 18,856 7.9%

Gross profit 128,834 147,432 156,875 188,647 273,838 224,684 201,278 11.6%

G&A 14,616 25,754 39,143 46,202 57,539 20,341 37,352 -45.5%

Operating profit 114,218 121,677 117,732 142,445 216,299 204,343 163,926 24.7%

EBITDA 115,031 122,852 120,756 145,984 220,184 185,858 166,894 11.4%

Net interest income (expense) (42,818) (23,640) (29,262) (47,363) (39,377) (32,442) (27,116) 19.6%

Increase in fair value Invt Prop 261,127 64,787 323,288 217,211 144,270 107,388 - 0.0%

Other items (23,165) 31,822 5,073 (1,272) (668.9) (7,804) (13,157) -40.7%

Profit before tax 309,363 131,003 416,831 314,051 311,325 200,397 123,652 62.1%

Income Tax (14,192) (16,349) (17,624) (20,986) (30,011) (24,594) (22,388) 9.9%

Proforma adjustment (8,482) - - -

Net income (after NCI) 286,404 114,415 342,166 252,262 281,313 123,999 77,425 60.2%

*) : Unaudited

67

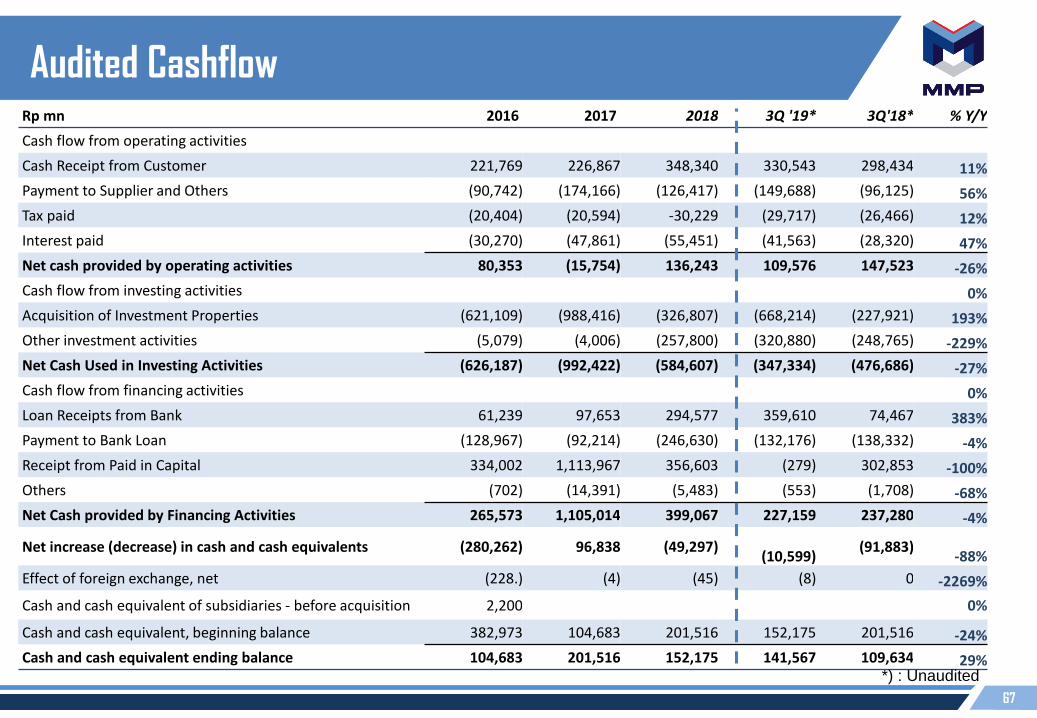

Audited CashflowRp mn 2016 2017 2018 3Q '19* 3Q'18* % Y/Y

Cash flow from operating activities

Cash Receipt from Customer 221,769 226,867 348,340 330,543 298,434 11%

Payment to Supplier and Others (90,742) (174,166) (126,417) (149,688) (96,125) 56%

Tax paid (20,404) (20,594) -30,229 (29,717) (26,466) 12%

Interest paid (30,270) (47,861) (55,451) (41,563) (28,320) 47%

Net cash provided by operating activities 80,353 (15,754) 136,243 109,576 147,523 -26%

Cash flow from investing activities 0%

Acquisition of Investment Properties (621,109) (988,416) (326,807) (668,214) (227,921) 193%

Other investment activities (5,079) (4,006) (257,800) (320,880) (248,765) -229%

Net Cash Used in Investing Activities (626,187) (992,422) (584,607) (347,334) (476,686) -27%

Cash flow from financing activities 0%

Loan Receipts from Bank 61,239 97,653 294,577 359,610 74,467 383%

Payment to Bank Loan (128,967) (92,214) (246,630) (132,176) (138,332) -4%

Receipt from Paid in Capital 334,002 1,113,967 356,603 (279) 302,853 -100%

Others (702) (14,391) (5,483) (553) (1,708) -68%

Net Cash provided by Financing Activities 265,573 1,105,014 399,067 227,159 237,280 -4%

Net increase (decrease) in cash and cash equivalents (280,262) 96,838 (49,297)(10,599)

(91,883)-88%

Effect of foreign exchange, net (228.) (4) (45) (8) 0 -2269%

Cash and cash equivalent of subsidiaries - before acquisition 2,200 0%

Cash and cash equivalent, beginning balance 382,973 104,683 201,516 152,175 201,516 -24%

Cash and cash equivalent ending balance 104,683 201,516 152,175 141,567 109,634 29%*) : Unaudited

68

PT Mega Manunggal Property Tbk