Providing Creditor Protection for Inherited IRAs After the Clark Decision Continuing Education...

75

Providing Creditor Protection for Inherited IRAs After the Clark Decision Continuing Education Conference August 14, 2015 Presented by Richard L. Randall Attorney & Counsellor at Law, Randall Law Offices, P.C. (Chairman and CEO, National Network of Estate Planning Attorneys)

-

Upload

clarence-mason -

Category

Documents

-

view

221 -

download

0

Transcript of Providing Creditor Protection for Inherited IRAs After the Clark Decision Continuing Education...

Providing Creditor Protection for Inherited IRAs After the Clark Decision

Continuing Education ConferenceAugust 14, 2015

Presented by Richard L. RandallAttorney & Counsellor at Law,

Randall Law Offices, P.C.(Chairman and CEO,

National Network of Estate Planning Attorneys)

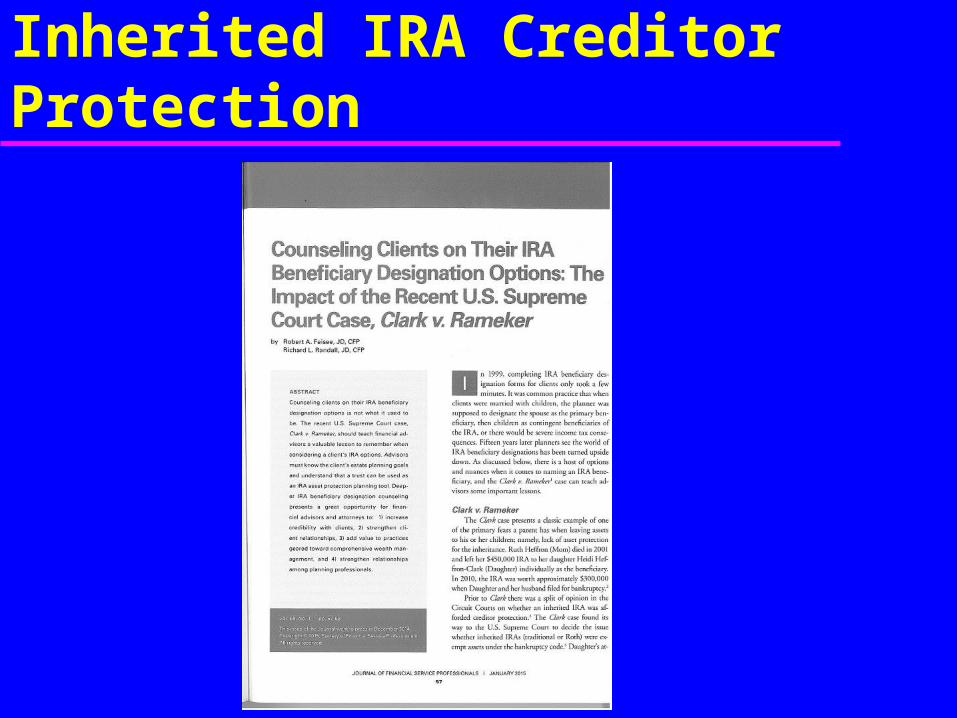

Inherited IRA Creditor Protection

Program OverviewGeneral Outline

Historically, Why Pay Distributions to Trust?A Contrarian Approach: The Trust as Primary BeneficiaryImpact of the Clark v. Rameker DecisionPayment to Trust Can Be Done Without Negative Impact on Tax Deferral

Retirement Plan Distributions

Why Pay Distributions to a Trust?

Provide Instructions to Beneficiaries (Applies to Everyone)

Provide Protections to Beneficiaries (Applies to Everyone)

Death Tax Planning for Married Couples

Key Stories to Master

School Bus

Trip to the IRS Supermarket

Hit Parade

Limited Power of Appointment

The “Hit Parade”

Kid Hits the School Bus School Bus Hits the Kid Marriage Hits the Rocks Kid Hits the Bottle Kid Hits the Books Kid Hits the Lottery Kid Hits the Skids

Retirement Plan Distributions

Why Pay Distributions to a Trust?

Hit Parade Many Clients Want Flexibility Provided by Limited

Power of Appointment Order of Beneficiaries Affects Whether Power of

Appointment Can be Retained by Surviving Spouse

Retirement Plan Distributions

Why Pay Distributions to a Trust?

Hit Parade To Make this Work, We Must Name the Trust

as Primary Beneficiary and Disclaim to the Spouse if Rollover is Desired

The Trust Must be Drafted to Qualify for Life Expectancy Distributions

Limited Power of Appointment

Naming the Trust Primary and the Spouse Contingent Beneficiary

A Spouse Can Disclaim and Still Receive Benefits In Trust (No One Else Can!)

BUT NO ONE (Not Even a Spouse!) May Disclaim and Retain a Right to Direct Property

Limited Power of Appointment

Naming the Trust Primary and the Spouse Contingent Beneficiary

Spouse as Primary Beneficiary Must Disclaim the IRA and the Power of Appointment to Add Proceeds to TrustOur Clients Say They Want Flexibility (“the Hit Parade” Power) TRUSTEE Can Keep Property AND the “Hit Parade” Power OR Can Disclaim to Spouse

Limited Power of Appointment

Naming the Trust Primary and the Spouse Contingent Beneficiary

The “Shirley Memo”

Available to You on Request!

Let’s Begin With How We Introduce Retirement Distribution/Estate Planning

Integration Concepts to Clients

The Truth About Estate Planning™ for Clients With Large Retirement

Plan Balances

Estate Planning Overview

Most Estate PlansJust Don’t Work!

Estate Planning Overview

“The Snapshot Test”

Estate Planning Overview

Definition of Estate Planning

I Want to Control My Property While I’m Alive and Well

Plan for Me and My Loved Ones if I Become Disabled

Estate Planning Overview

Definition of Estate Planning

• Give What I Have• To Whom I Want• When I Want• The Way I Want

All While Assuring My Wisdom is Transferred Along with the Rest of My Wealth

SAVE TAXES

EXPAND WEALTHPRESERVEWEALTH

FAMILY

ME

“I want to control my property while alive and well, plan for me and my loved ones if I become mentally disabled,

and then give what I have to whom I want, when I want and the way I want--

all while assuring my wisdom is transferred along with the rest of my wealth.”

THE PLANNING PYRAMID™

Estate Planning Overview

The Planning Pyramid™

Focuses on Client Goals

Solutions Make Planning Easier

Exposes Traditional Planning as “Upside Down”

Estate Planning Overview

Three Step Strategy™

• DEVELOP Your Plan with Counselling Oriented Planning Partners• COMMIT Yourself and Your Family to a Formal Continuing Maintenance and Education Program • SECURE Appropriate Assistance for You and Your Family to Transfer Your Wisdom along With the Rest of Your Wealth

Retirement Plan Minimum Distribution Rules Under

the IRS

Final Regulations

Minimum Distribution Rules

The MYTH of Immediate Taxation!

(The Mistaken Belief that the Entire Retirement Plan Must Be

Taxed at Participant’s Death)

Retirement Plan Distributions

You Know More Than You Think!

Who Owns Account? When Do You Pay Income Tax? Penalty for Early Distribution When You HAVE to Withdraw

Retirement Plan Distributions

A Simple Illustration:

Inherit the Money vs.

Inherit the Account!

Retirement Plan Distributions

Why is all this so important?

Income Tax Deferral Income Tax Deferral Income Tax Deferral

Retirement Plan Distributions

The Advantage of Tax Deferral

Dollar Doubled Every Year for 20 Years

Taxed at 28% Tax Deferred

Retirement Plan Distributions

The Advantage of Tax Deferral

Dollar Doubled Every Year for 20 Years

Taxed at 28% $51,353.37 Tax Deferred

Retirement Plan Distributions

The Advantage of Tax Deferral

Dollar Doubled Every Year for 20 Years

Taxed at 28% $51,353.37 Tax Deferred $1,048,576

Retirement Plan Distributions

Why Pay Distributions to a Trust?

Provide Instructions to Beneficiaries (Applies to Everyone)

Provide Protections to Beneficiaries (Applies to Everyone)

Death Tax Planning for Married Couples

Retirement Plan Distribtions

Remember, Minimums are Minimums!

For You

For Your Beneficiaries!

Retirement Plan Distributions

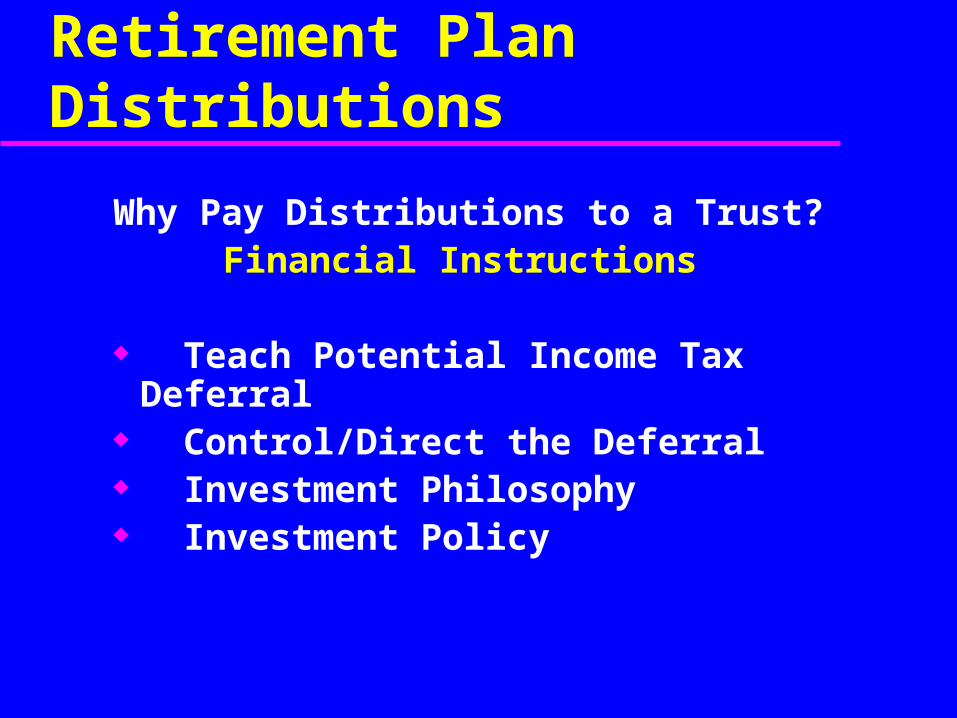

Why Pay Distributions to a Trust?Financial Instructions

Teach Potential Income Tax Deferral

Control/Direct the Deferral Investment Philosophy Investment Policy

Retirement Plan Distributions

Why Pay Distributions to a Trust?

Provide Instructions to Beneficiaries (Applies to Everyone)

Provide Protections to Beneficiaries (Applies to Everyone)

Death Tax Planning for Married Couples

Retirement Plan Distributions

So Why Pay Distributions to a Trust? To Provide Potential

“School Bus” Protections!

Potential Creditor Protection Potential Divorce Protection Potential Illness Protection

Wealth Reception Planning™

Our Experience

Initial Mindset is Normally a Barrier With Education, Client’s “Snapshot”

Changes Need for Active Family Involvement Is

Clear

Trust Design

Access and Control Mindset (Client’s)

“Don’t Want to ‘Pull Strings’ From the Grave” “They’re Independent” “It’s Their Job to Take Care of the Kids”

Trust Design

Trust Protections Mindset

When is it OK for:

Ex-Spouse to get the inheritance you leave in a divorce proceeding?

Medicaid to require “spend down” of the inheritance you leave?

Catastrophic Creditor to get inheritance you leave?

Trust Design

Access and Control Mindset(Beneficiary)

How Much Do I Get?

When Do I Get It?

Trust Design

Strength of Personal Protections Is Affected By Beneficiary’s

Access and Control:

Demand

Ask

Trust Design

Dual Planning Goals

Protection Against Outsiders

Practical Control by Beneficiary

Retirement Plan Creditor Protection

Plans at Work Protected By Supreme Court Decision

Protection Extended to IRAs

Inherited IRAs Under Attack

Retirement Plan Creditor Protection

Inherited IRAs Under Attack

Split Decisions Two States Had Negative Decisions Indiana (Klipsch) and Florida

(Robertson)

Retirement Plan Creditor Protection

Inherited IRAs Under Attack

The Clark Decision

Estate Planning Overview

Clark v. Rameker

June 2014 U.S. Supreme Court Case

Retirement Plan Creditor Protection

“Retirement Funds” Receive Protection

Mom’s funds were in an IRA

Question: is an INHERITED IRA a “Retirement Fund” as to an Inheritor?

Retirement Plan Creditor Protection

The Court’s Rationale:

The holder of an inherited IRA:– may never invest additional money in the

account.– is required to withdraw money from the account,

no matter how many years they may be from retirement

– may withdraw the entire balance of the account at any time-and for any purpose-without penalty

Retirement Plan Creditor Protection

Inherited IRAs Under Attack

Solution is to Pay Distributions Into Trust

IRA Can Still Be Attacked “School Bus” Trust Protects IRA Like

Any Other Asset!

Federal Estate Tax Reduction

Other Planning Goals Potential State Inheritance Tax PlanningEstate Growth in Survivor’s Estate

Could Cause Estate TaxDisability PlanningCreditor and Predator PlanningRemarriage ProtectionPlanning for Blended Familiesetc., etc.

Retirement Plan Distributions

For All These Reasons, We Find Clients Would Like to Pay Distributions Into Trust. What They Don’t Want to do is Lose Income Tax Deferral!!

Retirement Plan Distributions

Ten Minute

“Technical” Review

Retirement Plan Distributions

Just Three Things to Remember:

“As Easy as Blue, Yellow, Green”

Retirement Plan Distributions

“TRUE BLUE”

Uniform Table for

Withdrawals During Lifetime

Retirement Plan Distributions

YELLOW MEANS

CAUTION!!

If you name a Trust as Your Beneficiary, You Must Take a Test to Determine

How Fast Distributions Are Required

Retirement Plan Distributions

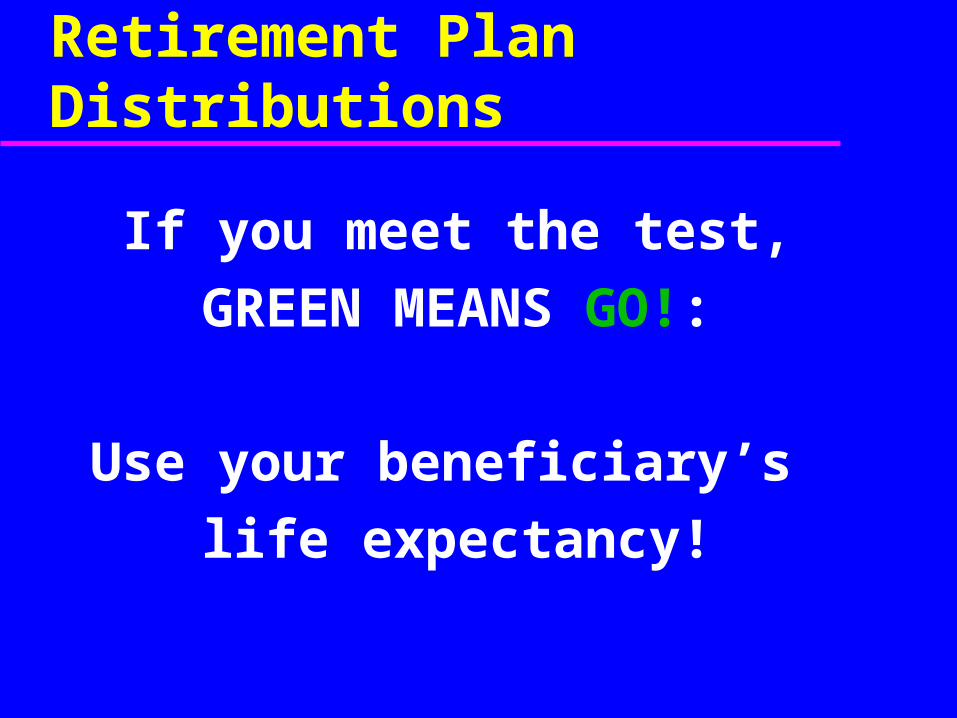

If you meet the test,

GREEN MEANS GO!:

Use your beneficiary’s

life expectancy!

Retirement Plan Distributions

If you fail the test,

GREEN MEANS GO!:

Use your own

life expectancy!

Retirement Plan Distributions

Remember why is all this so important to us?

Income Tax Deferral Income Tax Deferral Income Tax Deferral

Retirement Plan Distributions

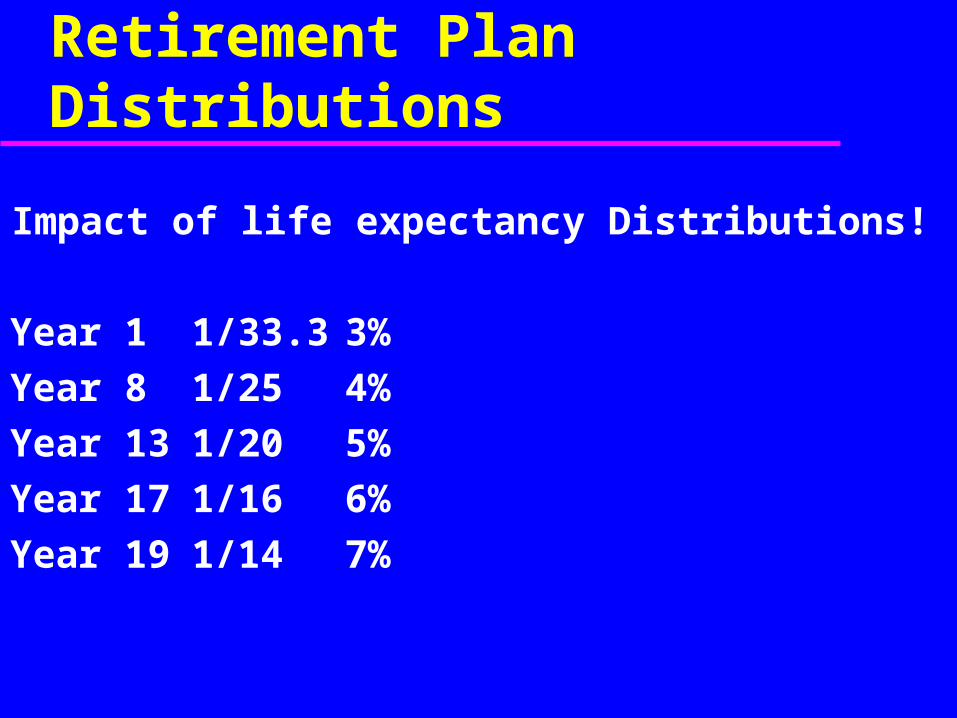

Impact of life expectancy Distributions!

Year 1 1/33.3 3%

Year 8 1/25 4%

Year 13 1/20 5%

Year 17 1/16 6%

Year 19 1/14 7%

Retirement Plan DistributionsImpact of life expectancy Distributions!

The account is still growing two decades after original owner’s death! Even though the beneficiary has enjoyed use of all the minimum

distributions The account’s actual after tax value is roughly double the value on date

of death! This is true IF only minimums are withdrawn!

Minimum Distribution Rules

Designated Beneficiary Test

Five Part Test To Qualify Trust as Designated Beneficiary

(The “Heartbeat Test” )

Minimum Distribution Rules

Designated Beneficiary Test

(aka “The Heartbeat Test”)

Corporation?

Charity?

Estate?

Individual?

Trust?

Minimum Distribution Rules

Designated Beneficiary Test

(aka “The Heartbeat Test”) No, a Trust Does NOT have a Heartbeat The General Rule is NO, It Won’t Qualify as

a Designated Beneficiary But there’s an EXCEPTION!

Minimum Distribution Rules

DESIGNATED BENEFICIARY EXCEPTION FOR TRUSTS

1. Valid Under State Law

2. Individual Beneficiaries

3. Identifiable Beneficiaries

4. Trust Delivered to Administrator

5. Trust Irrevocable Upon Death

Minimum Distribution RulesDesignated Beneficiary Test

If Trust Meets the Test, We “Look Through” the Trust To Determine Which Heart Is Used

All Beneficiaries Are Considered If All are Designated Beneficiaries the Oldest

Must be Used (“Oldest Heart” Rule) If Any Beneficiary is non-designated, the

Trust Fails the Test (“No Heart” Problem)

Minimum Distribution Rules

Designated Beneficiary Test

The Determination Date for the Designated Beneficiary Test is September 30 of Year Following Participant’s Death

Retirement Plan Distributions

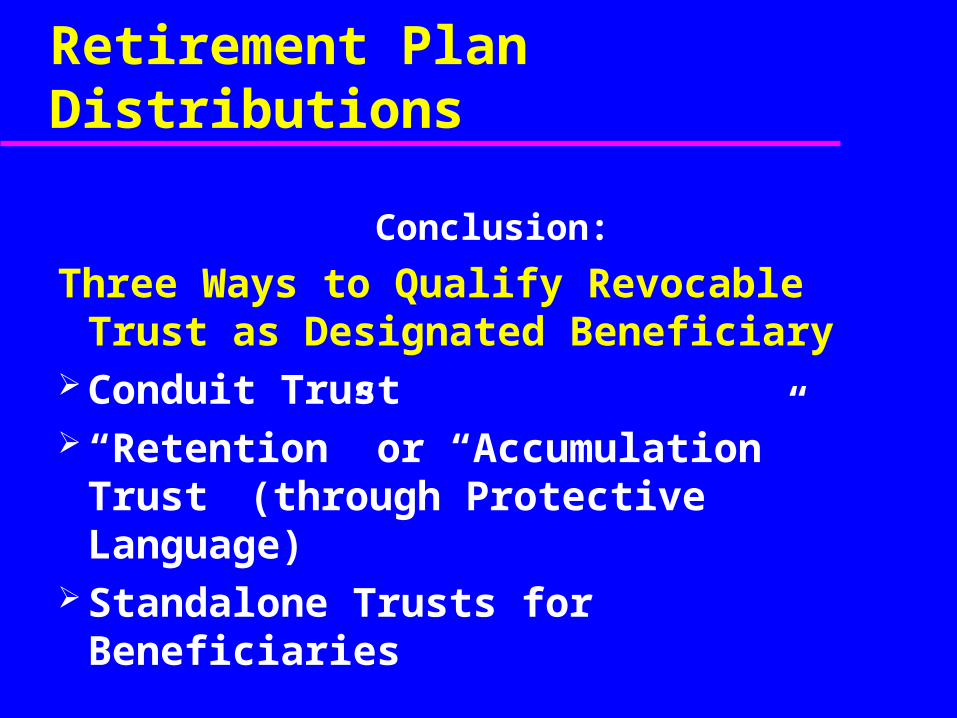

Three Ways to Qualify Revocable Trust as Designated Beneficiary

Conduit Trust “Retention” or “Accumulation” Trust

(through Protective Language) Standalone Trusts for Beneficiaries

Retirement Plan Distributions

The Three Doors™

Of Retirement Plan Distributions

Client Counselling Tool That Explains Balance Between Protections and Three Life Expectancy Distribution Drafting Strategies

Unique Counseling and Integration Tools

TM

TM

™ & © 2005 LifeSpan, L.L.C. All Rights Reserved. This integral concept of LifeSpan, L.L.C., may not be reproduced in any form or by any means without written permission from the publisher. Made in U.S.A. 3/23/2005. Used with permission.

The Three Doors™

1 CONDUIT

BASE TRUST with SPECIAL RP LANGUAGE

STANDALONE RP TRUST

RP distributions on beneficiary’s L.E. (oldest)

RP distributions on desired beneficiary’s life expectancy

RP distributions on beneficiary’s OWN LE

Protections &

Instructions

Protections &

Instructions

RP= Retirement Plan LE = Life Expectancy

FOR RETIREMENT PLAN DISTRIBUTIONS

2

3

Minimum Distribution Rules

Common Obstacles• Naming Non-Designated Beneficiary (“No

Heart” Problem)• Naming the Wrong Designated Beneficiary

• Older Beneficiary (“Bad Heart” Problem)

• Multiple Beneficiaries (“Oldest Heart” Problem)

Retirement Plan Distributions

Passing The Test

• “No Heart”: Distribution Strategy• “Bad Heart”: Disclaimer Strategy• “Oldest Heart”: Division Strategy

Retirement Plan Distributions

Passing The Test

“Oldest Heart”: Division Strategy 2002 Regulations Interpreted to Mean Any

Distribution to Any Part of a Trust Results in Oldest Heart Calculation

This Means Sub-Trusts Named on Beneficiary Form Will Not Avoid Oldest Heart Treatment

Retirement Plan Distributions

Passing The Test

“Oldest Heart”: Division Strategy

Standalone Trusts with Single Beneficiaries Will Allow for Use of Individual Life Expectancies

Retirement Plan Distributions

Passing The Test

“Oldest Heart”: Division Strategy

2005 PLR Approves Use of Individual Life Expectancies for Distributions Payable Directly to Sub-Trusts

Retirement Plan Distributions

Passing The Test

“Oldest Heart”: Division Strategy

• Standalone Trusts Still Useful for Administrative Clarity and Isolation of Retirement Planning Issues

• Standalone Trusts can now be designed for Multiple Beneficiaries

Retirement Plan Distributions

Conclusion:

Three Ways to Qualify Revocable Trust as Designated Beneficiary

Conduit Trust “Retention” or “Accumulation” Trust

(through Protective Language) Standalone Trusts for Beneficiaries

Unique Counseling and Integration Tools

TM

TM

™ & © 2005 LifeSpan, L.L.C. All Rights Reserved. This integral concept of LifeSpan, L.L.C., may not be reproduced in any form or by any means without written permission from the publisher. Made in U.S.A. 3/23/2005. Used with permission.

The Three Doors™

1 CONDUIT

BASE TRUST with SPECIAL RP LANGUAGE

STANDALONE RP TRUST

RP distributions on beneficiary’s L.E. (oldest)

RP distributions on desired beneficiary’s life expectancy

RP distributions on beneficiary’s OWN LE

Protections &

Instructions

Protections &

Instructions

RP= Retirement Plan LE = Life Expectancy

FOR RETIREMENT PLAN DISTRIBUTIONS

2

3

Retirement Plan DistributionsRemaining Challenge:

Compressed Income Tax Rate Levels (Pay Higher Rate on Less Income)

We’ve Developed Approach to Allow Funds to Stay in Trust (Protected) While Being Taxed at Individual Rates (And Financial Advisors are Key!)

To Be continued…