Project finance presentation ppp conference- south africa 2015

41

2/26/2016 Presented by Audrey Mwala, Director Project Finance & Risk Analysis, The PPPC, Malawi 1 Project Finance PPP Conference March 2015

-

Upload

audrey-mwala -

Category

Presentations & Public Speaking

-

view

563 -

download

1

Transcript of Project finance presentation ppp conference- south africa 2015

2/26/2016Presented by Audrey Mwala, Director Project Finance & Risk Analysis, The PPPC, Malawi 1

Project Finance

PPP Conference March 2015

In SADCs to spend US$64bn between

2013 to 2017

Energy USD12.3bn

Transport USD16.8bn

Water USD13.5bn

ICT USD21.4bn

Other USD 0.5bn

Source: SADC Short-term Plan 2013 – 17

2/26/2016 Presented by Audrey Mwala, Director Project Finance & Risk Analysis, The PPPC, Malawi

2

2/26/2016Presented by Audrey Mwala, Director

Project Finance & Risk Analysis, The PPPC, Malawi

3

• Infrastructure demand growth rate > traditional finances

• Traditional finance not enough for operations

• Need for Project Finance

What’s not Project Finance

•Corporate finance

•Angel finance

•Sovereign finance

•Structured finance

2/26/2016 4Presented by Audrey Mwala, Director

Project Finance & Risk Analysis, The PPPC, Malawi

Corporate Finance

Trend Analysis

2/26/2016Presented by Audrey Mwala, Director

Project Finance & Risk Analysis, The PPPC, Malawi

5

• Loan against exiting balance sheet

• A going concern status

• Often unsecured

• Extrapolate from past performance

• Management has full control

• Recourse to company balance sheet;

Sovereign Finance

• Government borrows to finance public infrastructure.

• Govt. may contribute its own equity

• Analyze govt.’s ability to raise funds

• Shows up as a liability on Government

2/26/2016Presented by Audrey Mwala, Director

Project Finance & Risk Analysis, The PPPC, Malawi

6

Angel Finance

2/26/2016Presented by Audrey Mwala, Director

Project Finance & Risk Analysis, The PPPC, Malawi

7

• Rich individuals or a group

• Retired entrepreneurs or executives

• Seed capital

• Management advice & contacts

• Bear extremely high risks

• A higher reward

• Invest beyond monetary return

• Equity or convertible debt

• A defined exit strategy

Structured Finance

2/26/2016Presented by Audrey Mwala, Director

Project Finance & Risk Analysis, The PPPC, Malawi

8

• Existing Company borrows• Finance brown field project• Full recourse on borrower • Creditworthiness - historical &

future • Limited security perfection • Pay interest in construction

Definitionby E. R. Yescombe, 2007

Means of raising long term non-recourse debtfinancing for major projects based on lendingagainst the project’s future cash flows and dependson a detailed evaluation of project’s construction,operating and revenue risks, their allocationbetween the investors, lenders and other partiesthrough contractual and other arrangements.

2/26/2016 9Presented by Audrey Mwala, Director

Project Finance & Risk Analysis, The PPPC, Malawi

Project Finance

• Contractual structure where the lender only looks at the project cash flows & earnings

• The project finance structure affects the cost of finance

• Security is the project asset

• Multiple parties & multiple contracts

• Lenders control

• 70 % of infrastructure is financed through project finance

2/26/2016Presented by Audrey Mwala, Director

Project Finance & Risk Analysis, The PPPC, Malawi

10

Why project finance

• Its clean- project finance lenders avoid exposure to various risks of the sponsors balance sheet

• Magnitude of the project is too large normal corporate finance arrangement

• Diversification –risk spread• Off-balance sheet financing• Protection of Govt. interest in the

asset• Lenders have more control

2/26/2016Presented by Audrey Mwala, Director

Project Finance & Risk Analysis, The PPPC, Malawi

11

Why project finance

• Lower agency costs- lender monitor managers

• Extensive due diligence of by lenders

• In distress lenders can manage situation through step in rights

• Lower financing costs

• Ring fencing of project assets

2/26/2016Presented by Audrey Mwala, Director

Project Finance & Risk Analysis, The PPPC, Malawi

12

Disadvantages

• High transaction costs

• Complex structures

• Slower to arrange financing

• Not appropriate for small projects less than $10 million

• It increases equity return

2/26/2016Presented by Audrey Mwala, Director

Project Finance & Risk Analysis, The PPPC, Malawi

13

Sources of project finance

• Commercial banks-

– banks

– Pension funds

– Insurance

• Multilateral lenders

• Regional development banks

• Export crediot Agency

2/26/2016Presented by Audrey Mwala, Director

Project Finance & Risk Analysis, The PPPC, Malawi

14

Project Finance

2/26/2016Presented by Audrey Mwala, Director

Project Finance & Risk Analysis, The PPPC, Malawi

15

• High upfront capital intensive assets, long lives.

• Greenfield project• Used in most PPP’s• Special Purpose Vehicle borrows • Highly leveraged structure• Non or limited recourse• Bankability- NPV of future cash

flows• Capitalise interest in construction

Sources of Project Finance

• Equity- for new or same line of business

– Pure equity or Quasi equity, Preferred equity, Shareholder loans

• Pension funds- matches with pension obligations

• A 'syndicate' of lending institutions

– Senior debt, Second lien debt, Mezzanine debt, Convertible debt

• Bank loans (usually short term)

• Construction companies @ risk capital

• Infrastructure Bonds- based on project cash flows

• Revenue Bonds- used by municipals

• Securitization – receivables used to float a bond

2/26/2016Presented by Audrey Mwala, Director

Project Finance & Risk Analysis, The PPPC, Malawi

16

Typical Stages in Project Finance

2/26/2016Presented by Audrey Mwala, Director

Project Finance & Risk Analysis, The PPPC, Malawi

17

Stage 1

Stage 2

Stage 3

• Construction

• Service delivery

Preliminary negotiations (Business Plan, Cash flow projections

Due diligence (affordability, technical, Economic, Environmental, legal, financial,

commercial)

Procurement/BiddingContract negotiationsContract Signing Financial closure (Sale and Purchase Agreement, concession,

Construction, FM agreement, Conditions precedent, Architects, Contractors, Project Management team, Marketing team)

Bankability

• A projects attractiveness to raise private finance

• Attractiveness to both attract equity & debt

• Project cash flows can service debt

• For cash flow variation- a margin to still service debt

• Risks allocated to private sector not excessive

• Enough returns to give the equity holders a return

2/26/2016Presented by Audrey Mwala, Director

Project Finance & Risk Analysis, The PPPC, Malawi

18

Bankability- Not an isolated component

• Need for balance that private party risks not to undermine:

• lenders interests

• Sponsors interest or

• burden users or

• Govt. with excessive fees

• Govt. looks at projects technical and financial viability

2/26/2016Presented by Audrey Mwala, Director

Project Finance & Risk Analysis, The PPPC, Malawi

19

Bankability

Project Finance Pricing

• During Construction Period: LIBOR + X%

• During Project Operation: LIBOR + X% -1%

• Typical Upfront Fees : X

• Arrangement Fee – Once off Documentation Fees

• Legal Fees

• Commitment Fees –X% p.a. on un-drawn amount ™

• Administration Fees2/26/2016

Presented by Audrey Mwala, Director Project Finance & Risk Analysis, The PPPC,

Malawi20

Financing Agreement

• Disbursements-lender’s consent.

• Lenders monitoring

• Step in rights

• In large projects financiers appoint manager

• Lien-project assets, paid from project cash flows

• Debt repaid before the end of project life.

2/26/2016Presented by Audrey Mwala, Director

Project Finance & Risk Analysis, The PPPC, Malawi

21

Special Purpose Vehicle

• A special entity created for project, shields other sponsor’s assets from project failure.

• Has no assets besides the project. • Sponsors capital contribution assures lenders of the sponsors'

commitment.• Limited recourse- Limits the borrowers loans to the project

assets• Assignment of all contracts (insurance, off take & supply

contracts)• Pledge of SPV shares• Assignment & pledge of revenue to collateral accounts

2/26/2016Presented by Audrey Mwala, Director

Project Finance & Risk Analysis, The PPPC, Malawi

22

Special Purpose Vehicle

The Special Purpose Vehicle Construction

firm

Project sponsors Contract

Monitoring

Government contracted certifier

Contracting Authority

fees

Marriagecontract

Unitary payments

Payment

2/26/201623

Presented by Audrey Mwala, Director Project Finance & Risk Analysis, The PPPC, Malawi

Other suppliers

Project Financing Risks

• Infrastructure projects are inherently risky.

• A project may be subject technical, environmental, economic and political risks.

• Risk identification and allocation is a key.

• Project financing is distributed among multiple parties, so as to distribute the project risk.

• Financiers institutions at times conclude that the risks in a project are unbankable

• Riskier projects may require limited recourse financing, a surety from sponsors

2/26/2016Presented by Audrey Mwala, Director

Project Finance & Risk Analysis, The PPPC, Malawi

24

Public Sector Base Comparator

• Hypothetical, risk adjusted, cost of govt. doing a project.

• Expressed in present value

• Testing private party bid for value for money.

• Helpful for negotiation

• Helps to ascertain full life cycle cost of the project.

2/26/2016Presented by Audrey Mwala, Director

Project Finance & Risk Analysis, The PPPC, Malawi

25

PPP Shadow Bid

• Hypothetical, risk adjusted, cost of private party. doing a project.

• Expressed in present value

• Helpful to understand assumptions

• Helpful for negotiation

2/26/2016Presented by Audrey Mwala, Director

Project Finance & Risk Analysis, The PPPC, Malawi

26

2/26/2016Presented by Audrey Mwala, Director

Project Finance & Risk Analysis, The PPPC, Malawi

27

Affordability

• PV of Govt.’s future revenue versus:

• present value of future capital &

• current expenditure

• Affordable to:

• Government

• Users

• Whole life cycle costs but may vary:• Brazil – 10 years fiscal analysis

• UK- procuring authority

• France- ministerial programme

• Colombia- cash transfer to contingent fund

• State of Victoria- PSC

2/26/2016Presented by Audrey Mwala, Director

Project Finance & Risk Analysis, The PPPC, Malawi

28

Gap funding

• Viability Gap fund

• Initial funding or

• Operational

• Output Based aid

• Contract period extension

• Guarantees, loan

• Availability payments

• Concessional loans

Financial Modeling

• Lending based on financial modeling of investment, cost & revenues.

• bankability based on key assumptions

• Sensitivity & scenario analysis used to draw the comfort lines

2/26/2016Presented by Audrey Mwala, Director

Project Finance & Risk Analysis, The PPPC, Malawi

29

Key Inputs of a financial model• Project duration

• Initial Capital plus additional capital Demand volume

• Price

• Unit cost

• Overheads

• Inflation

• Discount rate- Cost of total capital

• Interest rate

• Debt repayment

2/26/2016Presented by Audrey Mwala, Director

Project Finance & Risk Analysis, The PPPC, Malawi

30

Present Value of O & M

2/26/2016Presented by Audrey Mwala, Director

Project Finance & Risk Analysis, The PPPC, Malawi

31

Risk Impact Assessment

2/26/2016Presented by Audrey Mwala, Director

Project Finance & Risk Analysis, The PPPC, Malawi

32

Risk Probability

2/26/2016Presented by Audrey Mwala, Director

Project Finance & Risk Analysis, The PPPC, Malawi

33

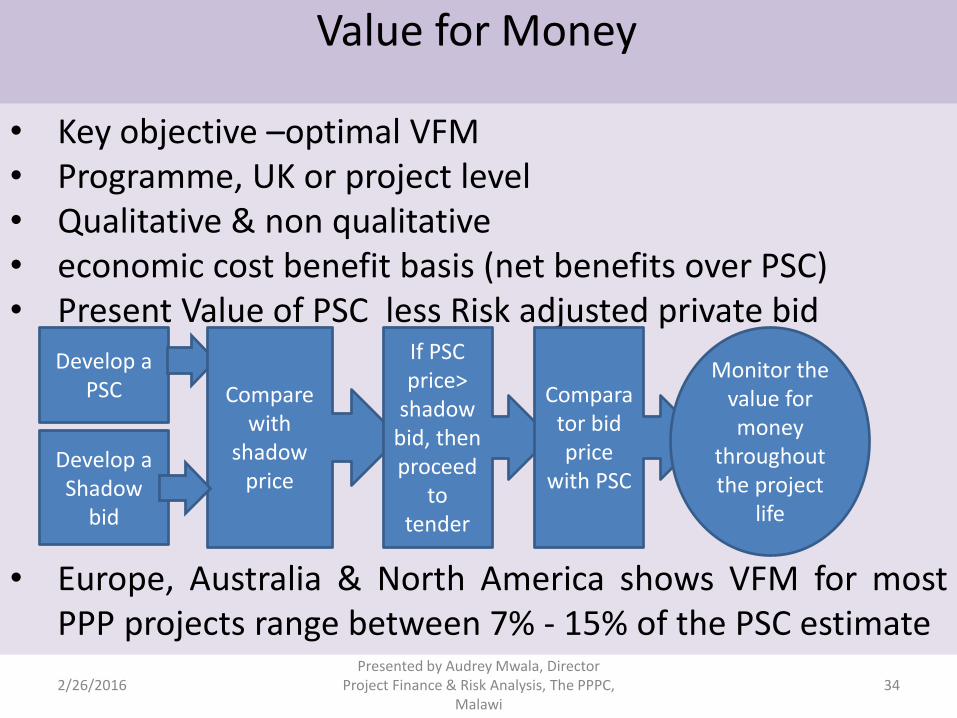

Value for Money

• Key objective –optimal VFM• Programme, UK or project level• Qualitative & non qualitative• economic cost benefit basis (net benefits over PSC)• Present Value of PSC less Risk adjusted private bid

• Europe, Australia & North America shows VFM for mostPPP projects range between 7% - 15% of the PSC estimate

2/26/2016Presented by Audrey Mwala, Director

Project Finance & Risk Analysis, The PPPC, Malawi

34

Develop a PSC

Develop a Shadow

bid

Compare with

shadow price

If PSC price>

shadow bid, then proceed

to tender

Comparator bid price

with PSC

Monitor the value for money

throughout the project

life

Optimal Value for Money

2/26/2016Project Finance Presentation- A. Mwala

Sept. 201435

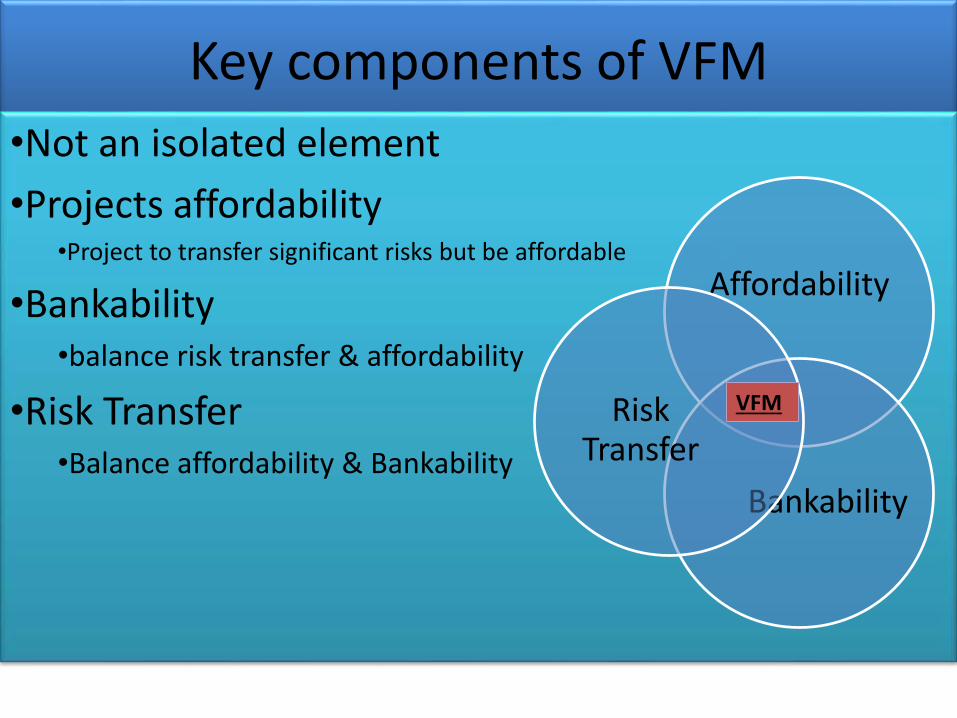

Key components of VFM

•Not an isolated element

•Projects affordability•Project to transfer significant risks but be affordable

•Bankability•balance risk transfer & affordability

•Risk Transfer•Balance affordability & Bankability

Affordability

Bankability

Risk Transfer

VFM

Value for Money assessment

2/26/2016Presented by Audrey Mwala, Director Project Finance & Risk Analysis, The PPPC,

Malawi37

Value for Money= • NPV of PSC $149.9m less• NPV of PPP bid $121.1m = $28.8m

Summary

2/26/2016Presented by Audrey Mwala, Director Project Finance & Risk Analysis, The PPPC,

Malawi38

$100

$149.9

$121.1

$135

$170

$28.8m

$14.9m

2/26/2016Presented by Audrey Mwala, Director

Project Finance & Risk Analysis, The PPPC, Malawi

39

•Monitor VM during in all stages:•Tender •Construction & •Service delivery•Transfer

• Significant shift of VM might be ground for renegotiation

VFM Monitoring

2/26/2016Presented by Audrey Mwala, Director

Project Finance & Risk Analysis, The PPPC, Malawi

40

•Direct financial VFM can be negative•Subsequent economic impact might be enormous e.g. Airlines, high speed trains•can be both quantifiable and non quantifiable

•Taxes•Employment, •New business

Economic Impact

2/26/2016Presented by Audrey Mwala, Director

Project Finance & Risk Analysis, The PPPC, Malawi

41