Programs Available to Farmers from Virginia Department of Agriculture and Consumer Services."...

23

-

Upload

nathaniel-lamb -

Category

Documents

-

view

214 -

download

0

Transcript of Programs Available to Farmers from Virginia Department of Agriculture and Consumer Services."...

Programs Available to Farmers from Virginia Department of Agriculture and Consumer Services."

• Marketing Services • Regulatory Services • News and Events • About VDACS • Special Programs and Quick Links • Charitable Gaming • • • • • • Consumer Portal - Access to the information and expertise of government agencies and consumer organizations to address consumer problems and guard

against fraud.

• CONSUMER SERVICES• OFFICE OF CONSUMER AFFAIRS

102 Governor StreetRichmond, Virginia 23219Consumer Protection HOTLINEToll free in Virginia: 1.800.552.9963 or within the Richmond, VA area 804.786.2042Fax: 804.225.2666Monday through Friday, 8:15 am to 5:00 pmE-mail: Webmaster

• GENERAL INFORMATION ABOUT THE PRICE OF GASOLINE• Office of Consumer Affairs• Fast Facts for Consumers• Price Gouging Complaint Form• Consumer Complaint Form • Publications & Resources• A Guide to Virginia’s Horse Country - To obtain a free copy of the guide, call 1.877.TROT 2 VA. To request the guide in quantity (5 or more), call Andrea Heid, Program

Manager for the Virginia Horse Industry Board, at 804.786.5842. • Ag Resources for Teachers - suggestions for fun classroom activities with pages to download and print. • Animal Care and Handling - frequently asked questions. • Food Safety - proper food handling information and tips; even a quiz for kids. • Organic Farming - lists operations alphabetically by county or major city. Read each listing carefully to learn about individual farms. • Virginia Christmas Trees - a guide to cut-your-own, freshly cut, and live Virginia-grown trees. • Virginia Wineries - a listing of Virginia wineries and vineyards. Enjoy world-class wine and exciting activities for the entire family. • Virginia’s Finest Products - look for the trademark that identifies top-quality Virginia-produced and processed agricultural products. • Now you can find many of Virginia's Finest products online at Shopvafinest.com. Traditional favorites and gourmet delights make great gifts for any occasion.• For information about food festivals and other events, see News & Events. • Copyright © 2009, Virginia Department of Agriculture and Consumer Services. For Comments or Questions Concerning this Web Site, contact the VDACS Webmaster.

WAI Level A Compliant

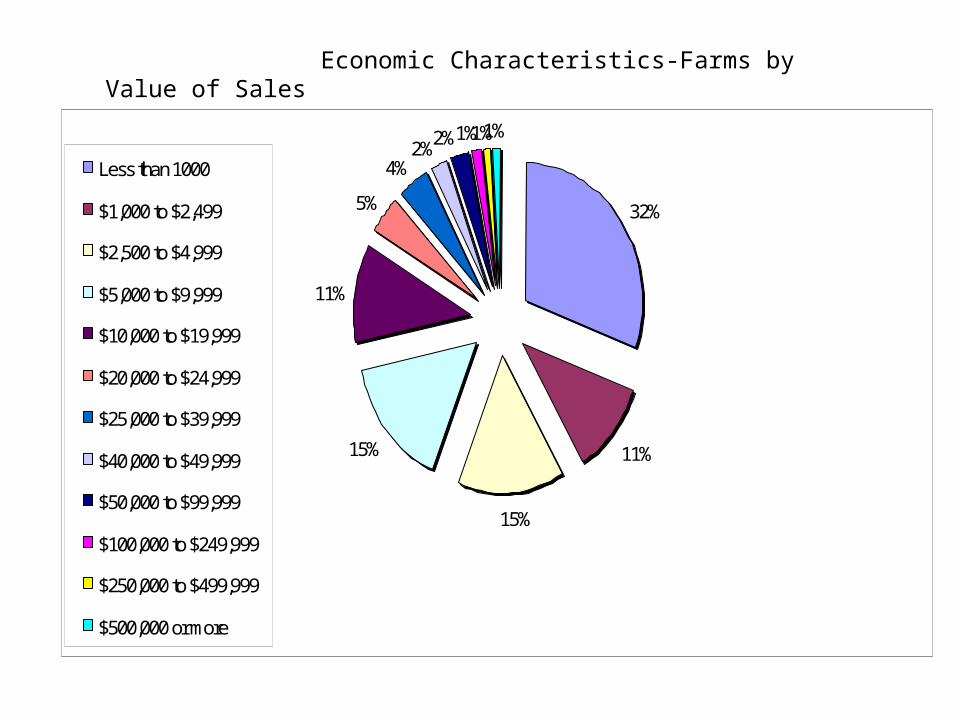

Economic CharacteristicsFarms by Value of Sales

Less than 1000

$1,000 to $2,499

$2,500 to $4,999

$5,000 to $9,999

$10,000 to $19,999

$20,000 to $24,999

$25,000 to $39,999

$40,000 to $49,999

$50,000 to $99,999

$100,000 to $249,999

$250,000 to $499,999

$500,000 or more

32%

11%

15%

15%

11%

5%

4%2%

2%1%1%1%

Less than 1000

$1,000 to $2,499

$2,500 to $4,999

$5,000 to $9,999

$10,000 to $19,999

$20,000 to $24,999

$25,000 to $39,999

$40,000 to $49,999

$50,000 to $99,999

$100,000 to $249,999

$250,000 to $499,999

$500,000 or more

Economic Characteristics-Farms by Value of Sales

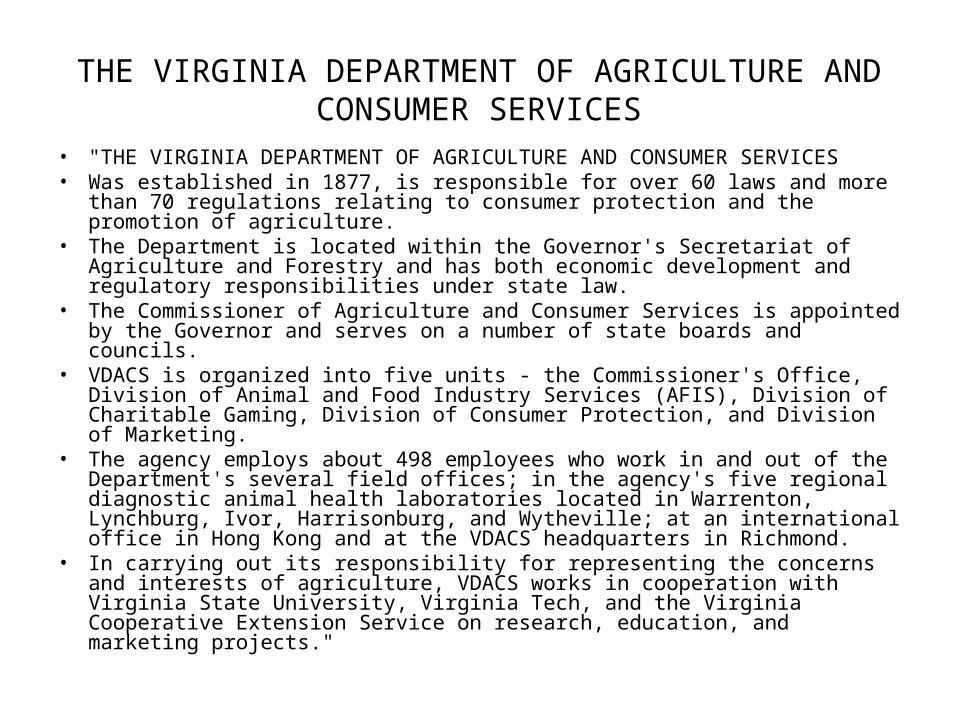

THE VIRGINIA DEPARTMENT OF AGRICULTURE AND CONSUMER SERVICES

• "THE VIRGINIA DEPARTMENT OF AGRICULTURE AND CONSUMER SERVICES

• Was established in 1877, is responsible for over 60 laws and more than 70 regulations relating to consumer protection and the promotion of agriculture.

• The Department is located within the Governor's Secretariat of Agriculture and Forestry and has both economic development and regulatory responsibilities under state law.

• The Commissioner of Agriculture and Consumer Services is appointed by the Governor and serves on a number of state boards and councils.

• VDACS is organized into five units - the Commissioner's Office, Division of Animal and Food Industry Services (AFIS), Division of Charitable Gaming, Division of Consumer Protection, and Division of Marketing.

• The agency employs about 498 employees who work in and out of the Department's several field offices; in the agency's five regional diagnostic animal health laboratories located in Warrenton, Lynchburg, Ivor, Harrisonburg, and Wytheville; at an international office in Hong Kong and at the VDACS headquarters in Richmond.

• In carrying out its responsibility for representing the concerns and interests of agriculture, VDACS works in cooperation with Virginia State University, Virginia Tech, and the Virginia Cooperative Extension Service on research, education, and marketing projects."

Services available to Farmers• MARKETING SERVICES• VDACS Marketing Services assists the state's varied agricultural community by enabling producers and

processors to locate the best markets for their products both here at home and abroad. The Division of Marketing serves producers, commodity boards and associations, retailers and buyers by providing marketing assistance. Field offices are located throughout the state as well as overseas in Hong Kong.

• BUY VIRGINIA GROWNVIRGINIA FOOD AND BEVERAGE EXPO VIRGINIA'S FINEST PROGRAM VIRGINIA ORGANIC PROGRAM Marketing Services

• Direct Marketing ServicesExport CertificationFarm-to-School Program Fruit, Vegetable and Peanut MarketingGrain MarketingInternational MarketingLivestock MarketingMarket News ServicePoultry and Egg MarketingPromotionsSales and Market DevelopmentVirginia's Finest Trademark ProgramEvents and Publications

• Consumer EventsTrade Events

• Virginia Grown Christmas Trees – Search Virginia Grown.com for Christmas trees and related products. You'll find directions, hours of operation, available products and special activities. You can also view a pdf version of the 2009 Virginia Grown Guide Choose and Cut Or Fresh Cut.

• Food & Beverage Directory - lists Virginia food producers and processors. Many of the products are available wholesale, as well as retail and through mail order. For a printed copy of the directory, call 804.786.3951.

• Gardening with the Virginia Green Industry Council

Services available to farmers (Cont)

• Virginia's Finest Directory - The best of the best in fresh and processed products.

• Virginia Organic Directory - Here you will find organic farm products, processed products made with certified organic ingredients, and organic livestock processors. All are Certified Organic by the U.S. Department of Agriculture. Listings are organized by product.

• Shippers Directory - lists suppliers of top-quality fresh fruits, vegetables and Christmas trees. Includes Virginia's Finest products. For a printed copy of the directory, call 804.786.3951.

• Federal/State Programs

• Ag StatisticsFood DistributionRisk Management AgencyUSDA Specialty Crop Competitive Grants

• Boards & Associations• Ag Industry Boards

Virginia Farmers Market SystemVirginia Nursery and Landscape Association Inc.Wine Growers Association

Land use valuation taxation relief is provided for in the Code of Virginia

• 58.1-3230

• 58.1-3231 Authority of counties, cities and towns to adopt ordinances; general reassessment following adoption ...

• 58.1-3232 Authority of city to provide for assessment and taxation of real estate in newly annexed are...

• 58.1-3233 Determinations to be made by local officers before assessment of real estate under ordinance ...

• 58.1-3234 Application by property owners for assessment, etc., under ordinance; continuation of assessment, e...

• 58.1-3235 Removal of parcels from program if taxes delinquent

• 58.1-3236 Valuation of real estate under ordinance

• 58.1-3237 Change in use or zoning of real estate assessed under ordinance; roll-back taxes

• 58.1-3237.1 Authority of counties to enact additional provisions concerning zoning classifications

• 58.1-3238 Failure to report change in use; misstatements in applications

• 58.1-3239 State Land Evaluation Advisory Committee continued as State Land Evaluation Advisory Council; member ...

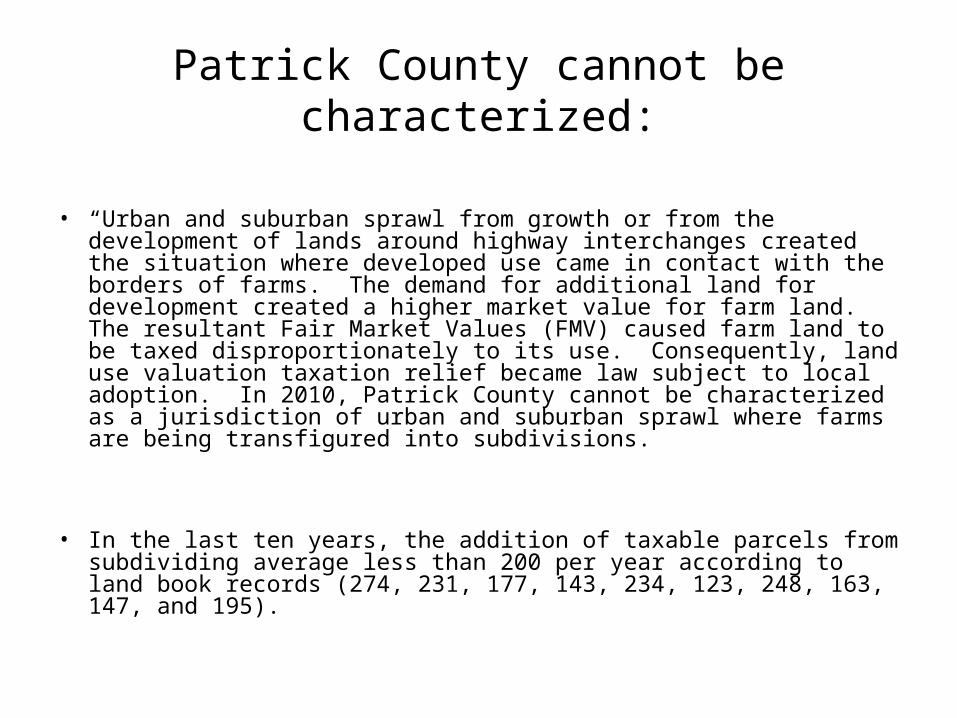

Patrick County cannot be characterized:

• “Urban and suburban sprawl from growth or from the development of lands around highway interchanges created the situation where developed use came in contact with the borders of farms. The demand for additional land for development created a higher market value for farm land. The resultant Fair Market Values (FMV) caused farm land to be taxed disproportionately to its use. Consequently, land use valuation taxation relief became law subject to local adoption. In 2010, Patrick County cannot be characterized as a jurisdiction of urban and suburban sprawl where farms are being transfigured into subdivisions.

• In the last ten years, the addition of taxable parcels from subdividing average less than 200 per year according to land book records (274, 231, 177, 143, 234, 123, 248, 163, 147, and 195).

2010 Use Value Legislation

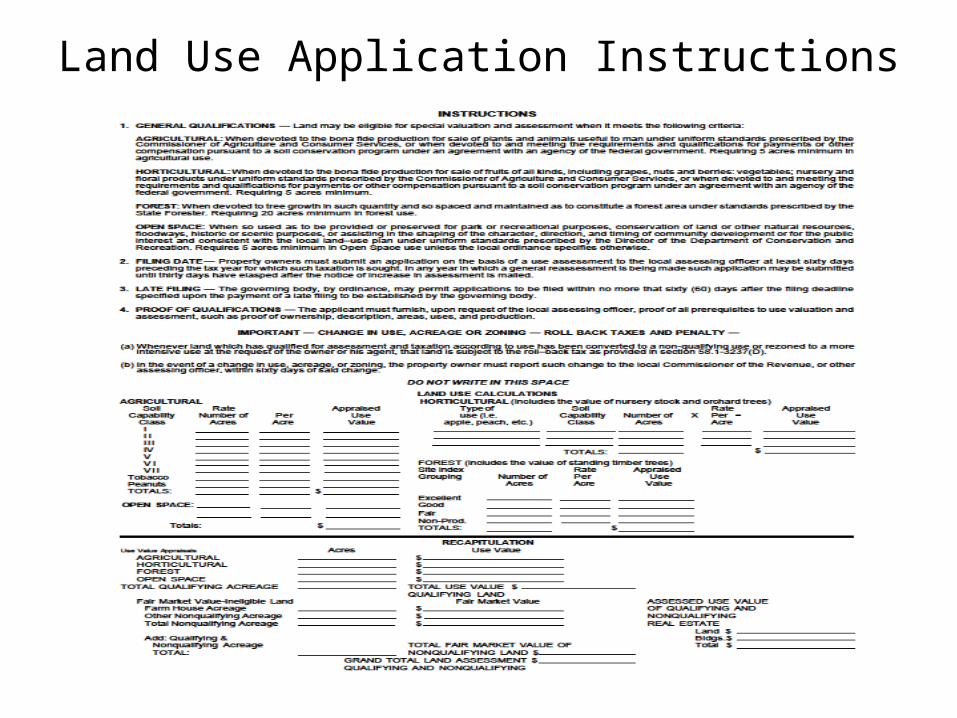

Land Use Application

Land Use Application Instructions

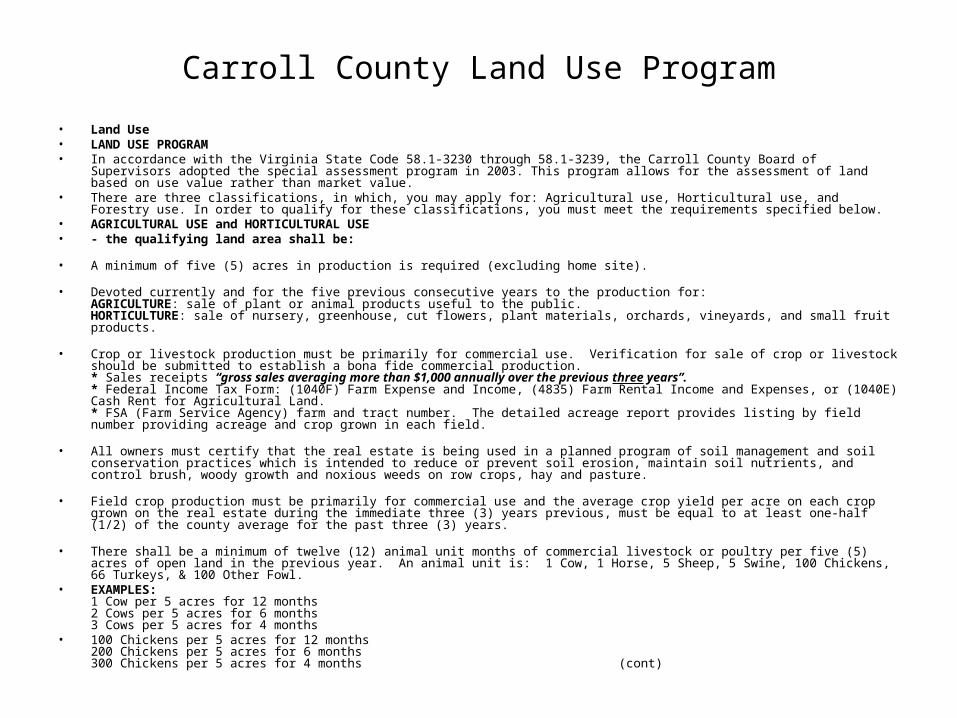

Carroll County Land Use Program

• Land Use• LAND USE PROGRAM • In accordance with the Virginia State Code 58.1-3230 through 58.1-3239, the Carroll County Board of Supervisors adopted the special

assessment program in 2003. This program allows for the assessment of land based on use value rather than market value. • There are three classifications, in which, you may apply for: Agricultural use, Horticultural use, and Forestry use. In order to qualify for

these classifications, you must meet the requirements specified below. • AGRICULTURAL USE and HORTICULTURAL USE • - the qualifying land area shall be:

• A minimum of five (5) acres in production is required (excluding home site).

• Devoted currently and for the five previous consecutive years to the production for: AGRICULTURE: sale of plant or animal products useful to the public. HORTICULTURE: sale of nursery, greenhouse, cut flowers, plant materials, orchards, vineyards, and small fruit products.

• Crop or livestock production must be primarily for commercial use. Verification for sale of crop or livestock should be submitted to establish a bona fide commercial production. * Sales receipts “gross sales averaging more than $1,000 annually over the previous three years”. * Federal Income Tax Form: (1040F) Farm Expense and Income, (4835) Farm Rental Income and Expenses, or (1040E) Cash Rent for Agricultural Land. * FSA (Farm Service Agency) farm and tract number. The detailed acreage report provides listing by field number providing acreage and crop grown in each field.

• All owners must certify that the real estate is being used in a planned program of soil management and soil conservation practices which is intended to reduce or prevent soil erosion, maintain soil nutrients, and control brush, woody growth and noxious weeds on row crops, hay and pasture.

• Field crop production must be primarily for commercial use and the average crop yield per acre on each crop grown on the real estate during the immediate three (3) years previous, must be equal to at least one-half (1/2) of the county average for the past three (3) years.

• There shall be a minimum of twelve (12) animal unit months of commercial livestock or poultry per five (5) acres of open land in the previous year. An animal unit is: 1 Cow, 1 Horse, 5 Sheep, 5 Swine, 100 Chickens, 66 Turkeys, & 100 Other Fowl.

• EXAMPLES: 1 Cow per 5 acres for 12 months 2 Cows per 5 acres for 6 months 3 Cows per 5 acres for 4 months

• 100 Chickens per 5 acres for 12 months 200 Chickens per 5 acres for 6 months 300 Chickens per 5 acres for 4 months (cont)

Carroll County Land Use Program

• FOREST USE -the qualifying land area shall be:

• A minimum of twenty (20) acres.

• The land must be growing a commercial forest crop that is physically accessible for harvesting when mature.

• The land must be devoted to forest use, which has a well-distributed, commercially valuable trees to compose at least 40% stocking.

• A planned program of Timber Management (Forest Management Plan) prepared by the Virginia Department of Forestry or a consultant forester is required.

• Before timber is sold, the landowner(s) shall consult with the Virginia Department of Forestry or a consultant forester to prepare a parcel plan for the unit to be sold.

• Each tract shall have a pre-harvest plan prepared prior to harvesting. The Virginia Department of Forestry’s BMP guidelines will be used as a reference for the plan. Recommendations in the pre-harvest plan should minimize stream and drainage crossings; pipe sizes and/or bridge recommendations; road, skid trail and log landing locations.

• The owner shall certify that the real estate is being used in a planned program of timber-management and soil-conservation practices

• • (Cont)

Carroll County Land Use Program

• APPLICATIONS To participate in the Special Assessment Program, the landowner must:

• Submit an application to the County Assessor’s Office for each parcel on the land book.

• There is a $25.00 application fee and $0.25 per acre for each application submitted. Checks should be made payable to: Treasurer, Carroll County.

• Applications must be submitted by November 1 prior to the preceding tax year or 30 days after notice of “increase” of assessment is mailed.

• A late filing fee of $25.00 per application and $0.25 per acre can be submitted between November 2 and December 31. An owner may file an application within no more than sixty (60) days after the filing deadline.

• Submit required documentation: * Sales receipts “gross sales averaging more than $1,000 annually over the previous three years”. * Federal Income Tax Form: (1040F) Farm Expense and Income, (4835) Farm Rental Income and Expenses, or (1040E) Cash Rent for Agricultural Land. * FSA (Farm Service Agency) farm and tract number. The detailed acreage report provides listing by field number providing acreage and crop grown in each field. * An Aerial Photo of the property, which may be obtained from the local FSA (Farm Service Agency).

• Applicant must furnish a count of the animals and the number of months they were located on the real estate for the previous three (3) years.

• Applicant must furnish a list of KIND of crops and the average yield per acre that were in production for the previous three (3) years.

• If land is leased, a certification from the property owner and lessee is required. • * A form is provided by the Carroll County Assessor’s Office.

*Federal Income Tax Form: Schedule E (Showing Pasture Rent) or Form (4835) Farm Rental Income and Expenses • State law requires that house sites be excluded from Land Use Assessment and be assessed on a fair market basis. Therefore all house

sites have been assessed at fair market value. If you have any true tenant houses on your property, you may furnish us with evidence of this fact and this house site acreage can be qualified for Land Use Assessment. Persons working only part time on the farm cannot qualify the house as a tenant house.

• No application will be accepted or approved if there are delinquent taxes on the property. • A new application is required whenever the use or acreage of previously approved land changes. •

(Cont)

Carroll County Land Use Program• DELINQUENT TAXES • In the event of delinquent taxes:

• The Treasurer shall notify all land use participants who have any prior year delinquent taxes, as of April 1. • If delinquent taxes for prior years are still owing as of June 1, the property will be removed from the Special

Assessment Program. • ROLLBACK TAX • -Rollback tax applies when land changes from a qualifying to a non-qualifying use.

• Real estate that no longer qualifies for the Land Use Assessment Program is subject to a roll back tax. • The rollback tax is calculated on the difference between the tax levied, based on a use-value assessment, and

the tax that would have been levied, based on a market value assessment. • The rollback tax shall be equal to the sum of the deferred tax for the current, and for each of the five most recent,

tax years, plus interest. • Any change in use must be reported to the Carroll County Assessor’s Office with 60 days of the date of change to

avoid having a penalty applied to the rollback tax. • On failure to report and pay within sixty (60) days following such change in use, such owner shall be liable for an

additional penalty equal to ten (10) percent of the amount of the roll-back tax and interest, which penalty shall be collected as a part of the tax. In addition to such penalty, there is imposed interest of one-half percent of the amount of the rollback tax, interest and penalty, for each month or fraction thereof during which the failure continues.

• Any change in the total acreage of real estate, which is assessed in accordance with the Land Use Assessment Law, requires the filing of a new application. This requirement is in accordance with 58-769.8 of the Code of Virginia Title “Taxation.” Therefore, it is of the utmost importance that when such change in acreage occurs, it must be reported to the Commissioner of the Revenue immediately.

• MATERIAL MISSTATEMENT • Any person making a material misstatement of fact in any application filed pursuant to this article shall be liable

for all taxes, in such amounts and at such times as if such property had been assessed on the basis for fair market value as applied to other real estate in the taxing jurisdiction, together with interest and penalties thereon, and the owner shall be further assessed with a additional penalty of one hundred percent of such unpaid taxes.

• (Cont)

Agriculture/Horticulture Requirements

• AGRICULTURAL USE and HORTICULTURAL USE • - the qualifying land area shall be: • A minimum of five (5) acres in production is required (excluding home site). • Devoted currently and for the five previous consecutive years to the production for:

AGRICULTURE: sale of plant or animal products useful to the public. HORTICULTURE: sale of nursery, greenhouse, cut flowers, plant materials, orchards, vineyards, and small fruit products.

• Crop or livestock production must be primarily for commercial use. Verification for sale of crop or livestock should be submitted to establish a bona fide commercial production. * Sales receipts “gross sales averaging more than $1,000 annually over the previous three years”. * Federal Income Tax Form: (1040F) Farm Expense and Income, (4835) Farm Rental Income and Expenses, or (1040E) Cash Rent for Agricultural Land. * FSA (Farm Service Agency) farm and tract number. The detailed acreage report provides listing by field number providing acreage and crop grown in each field.

• All owners must certify that the real estate is being used in a planned program of soil management and soil conservation practices which is intended to reduce or prevent soil erosion, maintain soil nutrients, and control brush, woody growth and noxious weeds on row crops, hay and pasture.

• Field crop production must be primarily for commercial use and the average crop yield per acre on each crop grown on the real estate during the immediate three (3) years previous, must be equal to at least one-half (1/2) of the county average for the past three (3) years.

• There shall be a minimum of twelve (12) animal unit months of commercial livestock or poultry per five (5) acres of open land in the previous year. An animal unit is: 1 Cow, 1 Horse, 5 Sheep, 5 Swine, 100 Chickens, 66 Turkeys, & 100 Other Fowl.

• EXAMPLES: 1 Cow per 5 acres for 12 months 2 Cows per 5 acres for 6 months 3 Cows per 5 acres for 4 months

• 100 Chickens per 5 acres for 12 months 200 Chickens per 5 acres for 6 months 300 Chickens per 5 acres for 4 months

Virginia Use Value Assessment Program

• Welcome to the home page for Virginia's Use Value Assessment Program. The purpose of this site is to provide information to those interested in use value assessment in Virginia.

• Virginia law allows eligible land in agricultural, horticultural, forest or open space to be taxed upon the land's value in use (use value) as opposed to the market value. The State Land Evaluation and Advisory Council (SLEAC) was created in 1973 with the mandate to estimate the use value of eligible land for each jurisdiction participating in the use-value taxation program. The SLEAC contracts annually with the Department of Agricultural and Applied Economics at Virginia Tech to develop an objective methodology for estimating the use value of land in agricultural and horticultural uses, with the Virginia Department of Forestry for the use value of land in forestry, and with the Department of Conservation and Recreation for the use value of land in open space. A Technical Advisory Committee (TAC), comprised of professionals familiar with Virginia agriculture, was established in 1998 to provided guidance on the technical aspects of developing an appropriate methodology for the estimation of use values for agricultural and horticultural uses. Section 58.1-3239 of Code of Virginia requires each participating jurisdictions' assessment office to consider the SLEAC estimates when assessing the use value of eligible land. However, the local assessing office is not required to use the estimates.

• To view the state application click here, this document is for informational purposes only. Please check with a local government agency to verify specific applications, eligibility, and reporting requirements.

• Click here to view a map and list of participating use-value jursidictions.• Recent Updates • TY2010 Use-Value Estimates • TY2010 Data Analysis • TY2010 Use-Value Estimates and Rental Rates Compared • • • • • © Department of Agricultural and Applied Economics, Virginia Tech. For problems or questions regarding this

website contact Lex Bruce. Last updated: Sept 28, 2009

•

SLEAC• The State Land Evaluation and Advisory Council

(SLEAC) was created in 1973 with the mandate to estimate the use value of eligible land for each jurisdiction participating in the use-value taxation program. The SLEAC contracts annually with the Department of Agricultural and Applied Economics at Virginia Tech to develop an objective methodology for estimating the use value of land in agricultural and horticultural uses, with the Virginia Department of Forestry for the use value of land in forestry, and with the Department of Conservation and Recreation for the use value of land in open space.

Fair Market Valuation

• The Fair Market Valuation is arrived at by certified and licensed appraisers working within guidelines approved by the Virginia Department of Taxation. The SLEAC value guidelines are arrived at through a highly scientific methodology. However, all this science can be dismissed and ignored, because Section 58.1-3239 of Code of Virginia requires each participating jurisdictions' assessment office to only consider the SLEAC estimates when assessing the use value of eligible land. However, the local assessing office is not required to use the estimates and can assign its own arbitrary values.

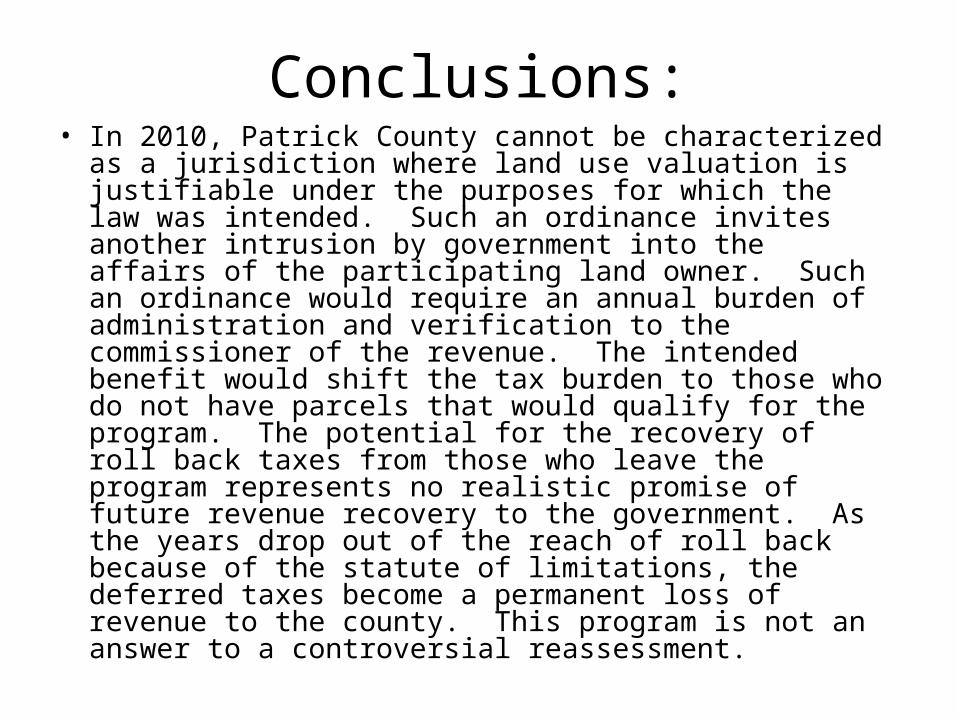

Conclusions:• In 2010, Patrick County cannot be characterized as a

jurisdiction where land use valuation is justifiable under the purposes for which the law was intended. Such an ordinance invites another intrusion by government into the affairs of the participating land owner. Such an ordinance would require an annual burden of administration and verification to the commissioner of the revenue. The intended benefit would shift the tax burden to those who do not have parcels that would qualify for the program. The potential for the recovery of roll back taxes from those who leave the program represents no realistic promise of future revenue recovery to the government. As the years drop out of the reach of roll back because of the statute of limitations, the deferred taxes become a permanent loss of revenue to the county. This program is not an answer to a controversial reassessment.