Price setting and the steady-state effects of inflation

23

DOI: 10.1007/s10108-004-0084-4 Span. Econ. Rev. 6, 267–289 (2004) c Springer-Verlag 2004 Price setting and the steady-state effects of inflation Miguel Casares Departamento de Econom´ ıa, Universidad P´ ublica de Navarra, 31006 Pamplona, Spain (e-mail: [email protected]) Abstract. This paper examines how price setting plays a key role in explain- ing the steady-state effects of inflation in a monopolistic competition economy with transactions-facilitating money. Three pricing variants (optimal prices, in- dexed prices, and unchanged prices) are introduced through a generalization of the Calvo-type setting that allows price indexation. We found that in an economy with less indexed prices, the steady-state negative impact of inflation on output is higher. Regarding welfare analysis, our results support a long-run monetary policy aimed at price stability with a close-to-zero inflation target. This finding is robust to any price setting scenario. JEL Classification: E13, E31, E50 Key words: Price setting, superneutrality, welfare cost of inflation 1 Introduction The purpose of this paper is to study the impact of different pricing specifications in the steady-state analysis of inflation. Our framework will be a closed-economy opti- mizing monetary model with monopolistic competition and transactions-facilitating money. The steady-state solution will be computed under several price setting vari- ants. Following early contributions by Hicks (1935), Baumol (1952) and Sidrauski (1967), most optimizing monetary models coincide in featuring a money demand The writing of this paper commenced during the time I spent on the Research Visitors Programme 2001 of the European Central Bank and an earlier version of the paper became ECB Working Paper No. 140. I would like to thank Bennett T. McCallum, Frank Smets, and Oscar Bajo-Rubio for their valuable comments and suggestions, and the Ministerio de Ciencia y Tecnolog´ ıa of Spain for its financial support (Research Project 2002/00954).

-

Upload

miguel-casares -

Category

Documents

-

view

213 -

download

0

Transcript of Price setting and the steady-state effects of inflation

DOI: 10.1007/s10108-004-0084-4Span. Econ. Rev. 6, 267–289 (2004)

c© Springer-Verlag 2004

Price setting and the steady-state effects of inflation

Miguel Casares

Departamento de Economıa, Universidad Publica de Navarra, 31006 Pamplona, Spain(e-mail: [email protected])

Abstract. This paper examines how price setting plays a key role in explain-ing the steady-state effects of inflation in a monopolistic competition economywith transactions-facilitating money. Three pricing variants (optimal prices, in-dexed prices, and unchanged prices) are introduced through a generalization of theCalvo-type setting that allows price indexation. We found that in an economy withless indexed prices, the steady-state negative impact of inflation on output is higher.Regarding welfare analysis, our results support a long-run monetary policy aimedat price stability with a close-to-zero inflation target. This finding is robust to anyprice setting scenario.

JEL Classification: E13, E31, E50

Key words: Price setting, superneutrality, welfare cost of inflation

1 Introduction

The purpose of this paper is to study the impact of different pricing specifications inthe steady-state analysis of inflation. Our framework will be a closed-economy opti-mizing monetary model with monopolistic competition and transactions-facilitatingmoney. The steady-state solution will be computed under several price setting vari-ants.

Following early contributions by Hicks (1935), Baumol (1952) and Sidrauski(1967), most optimizing monetary models coincide in featuring a money demand

The writing of this paper commenced during the time I spent on the Research Visitors Programme 2001of the European Central Bank and an earlier version of the paper became ECB Working Paper No.140. I would like to thank Bennett T. McCallum, Frank Smets, and Oscar Bajo-Rubio for their valuablecomments and suggestions, and the Ministerio de Ciencia y Tecnologıa of Spain for its financial support(Research Project 2002/00954).

268 M. Casares

based upon the role of money as a medium of exchange.1 Money is employedby economic agents as a means of facilitating daily transactions. More explicitly,a transaction costs function can be incorporated into the model with real moneybalances as one of its arguments. Here we will do the same by including a shoppingtime technology as in McCallum and Goodfriend (1987).

In this paper, producers will decide prices in a standard monopolistic compe-tition setup. Price rigidities arise when market circumstances prevent producersfrom choosing their optimal price. Following Calvo (1983), producers will be ableto set the selling price optimally only with some fixed probability. Producers whocannot price optimally will have two possibilities in our model. They can eithermaintain the price unchanged (as in the original Calvo setup), or raise the priceby the long-run rate of inflation (the price indexation scheme that departs from theCalvo setup). The choice between indexing the price or keeping it unchanged isexogenously determined by a fixed probability. As a result, there are three typesof prices in the economy: optimal, indexed, and unchanged. The distribution ofproducers according to their price setting behavior will be defined when calibratingthe probabilities of both price stickiness and price indexation.

The economic intuition behind price indexation is the presence of high evalua-tion costs when determining the optimal price (information costs, processing costs,computational costs, etc.).2 If these costs are unaffordable the price indexation rulemay be the best way to set prices as it is the optimal one on a steady-state basis.

Unchanged prices may be set because of the existence of menu costs.3 In a state-dependent model with fixed costs of changing prices, Dotsey, King, and Wolman(1999) find that more producers will adjust prices when the rate of inflation ishigher. In our paper we will calculate the welfare loss associated with leavingprices unchanged in a more inflationary economy. This amount might be comparedwith some measure of menu costs in order to decide whether or not to use priceindexation, and thus endogenize price indexation behavior.

The long-term effects of inflation and its welfare cost in optimizing monetarymodels have received much attention in the last few years (recent contributionsinclude Dotsey and Ireland 1996; Wolman 1997; Chadha et al. 1998; Wu and Zhang2000; Lucas 2000). These papers carry out the inflation analysis when economicagents take market-clearing prices in a perfect competition setup.4 By contrast,this paper shows how both monopolistic competition and price rigidities have aconsiderable influence on the long run effects of inflation.

1 There are two approaches that recognize only the store-of-value role of money, namely the portfolioapproach ofTobin (1958) and the overlapping generations approach ofWallace (1980). Since these ignorethe medium-of-exchange function, they imply that no money would be demanded if there were otherassets (of equal riskiness) yielding positive interest earnings to their holders.

2 Christiano et al. (2001) have already put forth this argument in their model and cite a paper byZbaracki et al. (2000) to provide some empirical evidence supporting it.

3 Menu costs should be understood in the broad sense so as to include the direct costs of re-labellingtogether with all the indirect costs associated with new prices (information costs, consumers’ dislike,adjustment costs, etc.).

4 Except for the paper by Wu and Zhang (2000), where there is a monopolistic competition marketwithout price rigidities. Their model is solved in a symmetric equilibrium with all firms setting theoptimal price.

Price setting and the steady-state effects 269

The rest of the paper is organized as follows. Section 2 describes the model.Section 3 is devoted to determining the transmission mechanisms from nominal toreal variables in steady state. Next, baseline calibration is carried out in Sect. 4.Section 5 deals with the implications of several price setting scenarios in the steady-state analysis of inflation. Section 6 concludes the paper by stating the main resultsobtained.

2 The model

Let the economy contain a continuum of households indexed by i ∈ [0, 1]. Thepreferences of a representative infinitely-lived household at time t are expressed inan intertemporal utility function whose arguments are a consumption index c andleisure time l

Et

∞∑

j=0

βjU (ct+j , lt+j)

(1)

where the discount factor is β = 11+ρ , with ρ > 0 as the rate of time preference.

The rational expectation operator in period t is denoted by Et[.] and it takes intoconsideration all the information available for that period. We assume positive firstderivatives and negative second derivatives of the instantaneous utility functionwith respect to both consumption and leisure (Uc > 0, Ul > 0, Ucc < 0, andUll < 0). In addition, we assume that the utility function (1) is additive separable,i.e. without cross marginal effects (Ucl = 0), as is standard practice in the RBCliterature. Consumption units are an aggregate of many goods. Indices were chosenfor both consumption and the aggregate price level as in Dixit and Stiglitz (1977).

Households are also producers. In period t, the household production functionf(nd

t , kt) gives the amount produced yt as a function of the stock of capital kt,and the quantity of labor demanded nd

t . In particular, a Cobb-Douglas technologyrepresents the production possibilities

yt = f(ndt , kt) =

[nd

t

]1−α[kt]

α, (2)

with 0 < α < 1. This technology shows decreasing marginal returns on both labor(fnn < 0) and capital (fkk < 0), positive cross-marginal productivity (fnk > 0),and constant returns to scale. Households decide how much to produce accordingto the Dixit-Stiglitz demand function5

f(ndt , kt) =

[Pt

PAt

]−θ

yAt , (3)

5 We are implicitly assuming that any household could also produce the aggregate output good byusing the Dixit-Stiglitz output aggregator technology defined in the text. If so, the profit-maximizationcriterion leads to demand Eq. (3), and the zero-profit condition leads to the Dixit-Stiglitz price leveldefinition.

270 M. Casares

in which the amount of output depends negatively on the selling price Pt, andpositively on the Dixit-Stiglitz aggregate price level PA

t and on the Dixit-Stiglitzaggregate output yA

t .Households produce a differentiated single good and consume a bundle of

goods. In this scenario, they take advantage of monetary services when carrying outtransactions. A time-cost transactions technology gives the amount of transactionscosts (shopping time), which depends positively on the level of consumption andnegatively on the amount of real money balances.6 Thus, the shopping time st spentin period t is given by

st = s(ct,mt), (4)

wheremt is the amount of real money balances in period t.The first and second orderderivatives have the signs sc > 0, sm < 0, scc > 0, smm > 0, and scm < 0. Thetransactions-facilitating property of money as a medium of exchange is representedthrough the signs sm < 0 and scm < 0, which imply that the use of more monetaryservices reduces the total and marginal transactions costs.

Thus, in period t households will split their total time T between work, leisure,and shopping

T = nst + lt + st, (5)

where nst is the labor supply in period t. The budget constraint imposed in period

t on a representative household expressed in aggregate output units is

Pt

PAt

yt + gt = ct + kt − (1 − δ)kt−1 + wt(ndt − ns

t ) +mt (6)

−(1 + πt)−1mt−1 + (1 + rt)−1bt − bt−1,

where gt are government lump-sum transfers, δ is the capital depreciation rate, wt

is the market-clearing real wage, πt is the rate of inflation, rt is the real interestrate, and (1 + rt)−1bt are purchases of government bonds in period t.

Income is obtained from selling production in the market Pt

P Atyt and from re-

ceiving lump-sum government transfers gt. Income is spent on consumption goodsct, on net investment kt−(1−δ)kt−1, on payments for net labor hiredwt(nd

t −nst ),

on increasing the demand for real money holdings mt − (1 + πt)−1mt−1, and onnet purchases of government bonds (1 + rt)−1bt − bt−1. Regarding the purchasesof bonds, (1+rt)−1bt is the amount bought in the current period that will be sold atthe value bt in the next period, yielding a risk-free real interest rate rt. The following

6 Alternatively, an output-cost transactions technology would measure transaction costs in terms ofoutput and would be included in the budget constraint (see Casares 2000 for a survey of optimizingmodels with transactions-facilitating money).

Price setting and the steady-state effects 271

definitions were used for real money balances, inflation, and the real interest rate:

mt =Mt

PAt

, (7)

πt =PA

t

PAt−1

− 1, (8)

1 + rt =1 +Rt

1 + Etπt+1, (9)

where Mt is the stock of nominal money and Rt is the nominal interest rate. Inaddition, the nominal money growth rate µt is defined as follows

µt =Mt

Mt−1− 1. (10)

Without loss of generality, it is assumed that both monetary and fiscal policies areconducted by applying a constant rule to money growth and lump-sum real transfersrespectively

µt = µ, (11)

gt = g. (12)

The lump-sum transfers of the government are financed either by increasing themoney supply or by selling bonds to households. In turn, the government budgetconstraint becomes in aggregate output terms

gt = mt − (1 + πt)−1mt−1 + (1 + rt)−1bt − bt−1. (13)

The optimal choices of ct, kt, ndt , n

st , lt, mt, bt, and Pt are those that maximize

(1) subject to constraints (2)–(6) in period t and future periods. Following Calvo(1983), the optimal selling price Pt can be set only upon receiving a market signalthat comes up with a constant probability 1−η. For those who cannot optimize theselling price, there will be two possibilities. First, with a constant probability χ,they will get a market signal to increase the price by the long-run rate of inflation.7

Second, they will leave the price unchanged with a probability 1 − χ.The price indexation rule was chosen because it is consistent with the optimal

dynamic pricing decision in a time-evolving steady state. The reason behind thisis that in steady state the ratio Pt

P At

is constant and, therefore, both optimal and

indexed prices grow at the steady-state rate of inflation π.8 After incorporatingprice rigidities, the Dixit-Stiglitz aggregate price level results in

PAt =

[(1−η) [Pt]

1−θ +η[(1−χ)+χ(1+π)1−θ

] [PA

t−1]1−θ

]1/(1−θ). (14)

7 Examples of models using such a non-optimal pricing scheme are Yun (1996), and Erceg et al.(2000). For the steady-state purposes of this paper, the price adjustment rule selected would be equivalentto Pt = (1 + πt−1)Pt−1 which has been used in Christiano et al. (2001).

8 See Eq. (A2) in the Appendix for details regarding this result.

272 M. Casares

A Competitive Equilibrium (CE) model can be defined by jointly considering thethirteen first order conditions of the optimizing program described above, Defini-tions (7)–(10), the fiscal and monetary policies (11)–(12), the government budgetconstraint (13), the Dixit-Stiglitz aggregate price level Eq. (14), and the labor mar-ket equilibrium condition

∑∞j=0(1 − η)ηj

[(1 − χ)(1 + π)θ + χ

]jnd

t = nst . In

turn, there are twenty two equations that determine dynamic paths for the seven-teen endogenous variables ct, kt, n

dt , n

st , lt, mt, bt, Pt, yt, wt, µt, gt, Mt, rt, Rt,

πt, PAt , and the five Lagrange multipliers of constraints (2)–(6).

2.1 Aggregate variables

Now we will take a look at the aggregate magnitudes. Assuming complete markets,all the variables are identical among households except for those that depend onthe specific price setting conditions of the household: the selling price, output,capital, and the demand for labor. Thus, only the aggregate magnitudes for thesefour variables need to be spelled out. The aggregate price level definition wasintroduced above in Eq. (14). For the other three, average values were calculatedin steady state in order to represent aggregate magnitudes.9 Thus, the steady-stateaverage labor and capital are related to their respective amounts under optimalpricing as follows

nt =[

1−η1−η[(1−χ)(1+π)θ+χ]

]nd

t , (15)

kt =[

1−η1−η[(1−χ)(1+π)θ+χ]

]kt. (16)

Similarly, aggregate output yt in steady state can be expressed in terms of both av-erage labor and capital entering the production function. As shown in the Appendix,there is a steady-state linear relationship between y and f(n, k):

yt =[

1−η1−η[(1−χ)(1+π)θ−1+χ]

]θ/(θ−1) [1−η

1−η[(1−χ)(1+π)θ+χ]

]−1f(nt, kt). (17)

The link factor depends on the steady-state rate of inflation π, the Dixit-Stiglitzelasticity θ, and the price stickiness parameters η and χ.10

The steady state solution of the model is obtained from the CE defined aboveand Eqs. (15)–(17). A reduced system of twelve equations is included at the end ofthe Appendix.

3 Non-superneutrality channels

This section is intended to provide a theoretical explanation of the long-run real ef-fects of changing the monetary conditions. In this model without economic growth,

9 The Appendix to the paper shows how this calculation was done.10 Note that y = f(n, k),when either η = 0.0 (fully flexible prices),χ = 1.0 (full price indexation),

or π = 0.0 (constant prices in steady state).

Price setting and the steady-state effects 273

the steady-state nominal money growth rate µ determines the steady-state rate ofinflation π because real money balances m = M

P A are constant in steady state. Inturn, growth rates for nominal money and prices must be equal, yielding µ = π.Thus, we will indistinctly refer to the long-run effects of either inflation or moneygrowth.

In a monopolistic competition model featuring sticky prices, there are two trans-mission channels from inflation to the real variables in steady state: the monetaryservices channel and the ”capital tax” channel. Let us study them separately.

3.1 Monetary services channel (the Friedman channel)

A rise in steady-state inflation π will increase the steady-state nominal interest rateR. This is due to the fact that in steady state the real interest rate r is equal tothe household rate of time preference ρ, and therefore does not vary with a newsteady-state rate of inflation.As a result we have r = ρ and the steady-state nominalinterest rate is R = r + π(1 + r) = ρ+ π(1 + ρ) ∼= ρ+ π.

If the nominal interest rate goes up, the money demand behavior of the house-holds will lead to lower real money balancesm held.11 Moreover, the transactions-facilitating role of money gives rise to a negative first derivative sm < 0 in theshopping time function. Accordingly, lower real money balances resulting from amore inflationary scenario will bring about more shopping time s spent on carry-ing out transactions. Therefore, if the only effect of high inflation were rising s,labor supply would shrink through the time constraint and we would find less laborentering the production function.12

Assuming complementarity between labor and capital in the production tech-nology fnk > 0, a fall in labor will reduce marginal productivity of capital. In turn,the amount of capital demanded will also fall. With both labor and capital falling,output will also fall. Superneutrality does not hold and there is a negative long-runrelationship between output and inflation.

We could refer to this channel as the Friedman channel because it implies anoptimal rate of inflation that drives nominal interest rates down to 0%, as pointedout by Friedman (1969). If the nominal interest rate is at 0%, there is no opportunitycost of holding money and the amount of real money balances held is at the satiationpoint on monetary services. On the contrary, any positive nominal interest rate givesrise to some loss of monetary services that will bring about more transaction costs.Some resources will then be withdrawn from the productive processes to be usedin carrying out transactions. As a result, there will be a negative impact on outputthat will originate some welfare cost of inflation. The Chicago rule says that pricesmust be decreasing at a deflation rate π∗ approximately equal to the real interest

11 In the time-cost transactions technology model at hand, the money demand equation derived fromthe first order conditions says that real money balances depend positively upon the current level ofconsumption and the real wage, and negatively upon the nominal interest rate (see the Appendix for theexplicit money demand expression).

12 Note that lower real money balances also drive up marginal transaction costs (scm < 0). Inturn, consumption becomes more costly and households also shift part of their labor supply to leisure.Nonetheless, this effect seems to be quantitatively fairly negligible.

274 M. Casares

rate: π∗ = −r/(1 + r). That will yield the optimal 0% nominal interest rate whichguarantees monetary satiation.

3.2 The ”capital tax” channel in monopolistic competition with sticky prices

Capital-labor allocation is optimal when the ratio of marginal productivity to itsfactor price is the same for capital as for labor. In steady-state magnitudes, we have

fn

w=

fk

(ρ+ δ)/(1 + ρ), (18)

where we used the steady-state result r = ρ. Let us introduce the mark-up in realterms denoted as ψ = fn

w = fk

(ρ+δ)/(1+ρ) . The real mark-up is the inverse of the

real marginal cost.13 Let us relate ψ to the steady state capital k in order to see theinfluence of the monopolistic competition setup on capital (and output). When theCobb-Douglas technology is incorporated, Eq. (18) determines that k is equal to

k = n

[α(1 + ρ)ψ(ρ+ δ)

]1/(1−α)

, (19)

where it can be appreciated that a higher ψ leads to a lower k. This creates adistortion that shapes capital accumulation and leads to the well-known efficiencyloss with respect to perfect competition. In perfect competition models,ψ is alwaysequal to 1. However, if the economy is in monopolistic competition, the mark-up isgreater than one (ψ > 1). For this reason, it is said that monopolistic competitiongives rise to a tax on capital accumulation interpreted as the higher opportunity costin terms of current production return.

The value of ψ, obtained in the Appendix, is

ψ = θθ−1

1−βη[(1−χ)(1+π)θ−1+χ]1−βη[(1−χ)(1+π)θ+χ]

[1−η

1−η[(1−χ)(1+π)θ−1+χ]

]1/(1−θ)(20)

which is fully determined by the steady state rate of inflation π, and the parametersβ, θ, η, and χ. If either prices are fully flexible (η = 0) or there is full priceindexation (χ = 1.0), expression (20) simplifies to ψ = θ

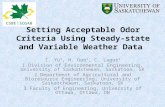

θ−1 and there is no long-run effect of inflation on the real mark-up. However, if prices are sticky withoutfull price indexation, there is a steady-state link between π and ψ. Any steady-statechange in π will affect capital and output as jointly implied by (20), (19) and (2).Moreover, the long-run effect of π onψ describes a u-shaped curve. In other words,the sign of the effect of π on ψ changes from negative to positive as inflation getshigher. Figure 1 displays this u-shape effect.14 Thus, the real mark-up ψ can beaffected by both the particular price setting conditions of the economy (defined bythe parameters η and χ), and the level of inflation π. This result will give rise tosignificant long-run welfare effects as documented in Section 5.

13 Taking into account the Cobb-Douglas production technology at hand the real marginal cost can

also be expressed as a function of the factor prices: ψ−1 =(

w1−α

)1−α (ρ+δ

α(1+ρ)

)α.

14 The calibration of parameters used in Fig. 1 is β = 0.995, and θ = 10.0, which corresponds to thebenchmark calibration carried out below. The price indexation parameter χ takes three different valuesin Fig. 1 so as to represent various price setting scenarios.

Price setting and the steady-state effects 275

Fig. 1. The ”capital tax” channel. Steady-state relationship between annual inflationπ and the real mark-up ψ at full price indexation (χ = 1.0), partial price indexation (χ = 0.5), and no price indexation(χ = 0.0)

4 Calibration

The model is intended to give quarterly observations for a modern large economy.In the baseline calibration both nominal money and prices grow 1% per quarter insteady state (µ = π = 0.01), i.e. 4% per year. The rate of time preference is setat 0.5% per quarter (ρ = 0.005), i.e. 2% per year, which implies β = 0.995. Thesteady-state nominal interest rate is 1.5% per quarter (R = 0.015), i.e. 6% per year,obtained as the sum of the real interest rate and the rate of inflation.

The instantaneous utility function is given by the constant relative risk aversionspecification:

U(ct, lt) =c1−σt

1 − σ+ Υ

l1−γt

1 − γ

with σ, γ, Υ > 0.

The consumption risk aversion coefficient σ is set at σ = 4 so as to imply anelasticity of intertemporal substitution of consumption equal to 0.25. As for theleisure risk aversion coefficient, we tookγ = 8which led to a rather low labor supplyelasticity to the real wage (+0.25) consistent with the microeconomic empiricalevidence reported by Pencavel (1986) in the US. The leisure scale parameter in theutility function Υ takes the value that implies that labor time is one-third of totaltime.

276 M. Casares

The existing transactions technology is described by a functional form verysimilar to that described in Den Haan (1990)

s(ct,mt) =

0 if ct = 0

a0 + cta1

[ctmt

]a2/(1−a2)

+ a3mt, if ct > 0

,

with a0, a1, a3 ≥ 0, and 0≤ a2 ≤ 1. The constant term a0 was calibrated byconsidering shopping time s to be 2% of the total time in steady state. The value a1implies a baseline steady-state ratiom/c equal to 1.5 as roughly observed in moderneconomies, whereas a2 = 0.75 implies a -0.25 nominal interest rate elasticity inthe money demand function.

The specification selected for the transactions technology implies the existenceof a satiation point in real money balances, due to the presence of linear storagecosts expressed as a3mt. Thus, if the nominal interest rate were zero (Chicagorule), households would not demand infinite real money balances. We decided tocalibrate the storage cost coefficient a3 in order to imply that monetary servicessatiation occurs when the amount of real money balances held is equal to 3 timesthe quarterly consumption level in steady state (that is, precisely twice what is heldin the baseline steady-state solution).

In the Cobb-Douglas production technology the capital share parameter is α =0.36. The depreciation rate for capital δ will be 2.5% per quarter (δ = 0.025). TheDixit-Stiglitz monopolistic competition parameter is set at θ = 10.0, following themicro-level empirical results on US companies by Basu and Fernald (1994), andBasu (1996). It implies that the steady-state real mark-up when prices are fullyflexible is 11.1%.

As for the price setting calibration, the next section analyzes several variantsranging from the fully flexible price case to the sticky price case with no priceadjustment.15

5 Price setting and the steady-state effects of inflation

Four alternatives are initially proposed for the price setting distribution:

i) Fully flexible prices (η = 0.0). All the selling prices can be adjusted optimallyin each period.

ii) Sticky prices (0.0 < η < 1.0) with full price indexation (χ = 1.0). There isa fraction η of households that cannot set the price optimally in each period.All of them will adjust the price by indexing it to steady-state inflation.

15 For the sake of consistency among pricing variants, the parameters Υ , a0, a1, and a3 will be setdifferently in order to maintain the baseline calibration assumptions. Hence, the calibration of theseparameters will always imply that at the (baseline) steady-state rate of inflation of 4% per year: 1/3 ofthe time is devoted to work, 2% of the time is devoted to shopping, m/c = 1.5, and money satiationoccurs when m/c = 3.0.

Price setting and the steady-state effects 277

iii) Sticky prices (0.0 < η < 1.0) with partial price indexation (0.0 < χ < 1.0).There is a fraction η of households that cannot set the price optimally in eachperiod. Some of them, a fraction ηχ, will index the price. The remaininghouseholds, the fraction η(1 − χ), will maintain the price unchanged.

iv) Sticky prices (0.0 < η < 1.0) with no price adjustment (χ = 0.0). There isa fraction η of households that cannot set the price optimally in each period.All of them will keep the price unchanged.

Regarding the long-run analysis at hand, the four price setting cases presentedcorrespond to only three different models because cases i) and ii) have the samesteady-state properties. If all the non-optimal prices are fully indexed, all the pricesof the economy will be growing at the rate of inflation in steady state. Therefore,case ii) is identical to case i) on a steady-state basis (see the Appendix for details),and we refer indistinctly to both cases as Model 1. The sticky-price economy withpartial price indexation will be Model 2, whereas the sticky-price economy withno price indexation (the original assumption in Calvo 1983) will be Model 3.

The analysis will consist of a case-by-case examination of the different steady-state implications found when altering the inflation rate. The rates will start at theChicago-rule rate (roughly -2% per year) and rise to 10% per year.16 Figures 2–4 and Tables 1–3 display the results for Models 1–3. The variables reported are:real money balances (m), shopping time (s), the mark-up (ψ), the real wage (w),average capital (k), average labor (n), consumption (c), leisure (l), average output(y), and the welfare cost of inflation (welfare cost). The welfare cost of inflation wascalculated as the percentage of output required to gain sufficient utility to renderthe household indifferent with respect to the optimal inflation case.

5.1 Model 1. Fully flexible prices or sticky prices with full price indexation

This ”capital tax” channel vanishes when prices are either fully flexible to adjustoptimally (η = 0.0) or sticky with all the non-optimal prices following the in-dexation rule (0.0 < η < 1.0 and χ = 1.0). In both cases, expression (20) yieldsψ = θ

θ−1 and the inflation-markup link disappears. Figure 2 shows this result as thehorizontal line in the plot of the real mark-upψ. When inflation changes, there is nochange in the mark-up tax on capital accumulation coming from the monopolisticcompetition setup.

Hence, the only way of explaining departures from superneutrality is through theFriedman-type channel. The two most important effects of any increase in steady-state inflation are the decline in real money balances and the increase in transactioncosts (shopping time) due to the loss of monetary services. The examples in Table1 show that real money falls by 50% when inflation rises from −2% per year to4% per year and by close to 60% when inflation reaches 10% per year. Shoppingtime, in turn, goes up by 12.9% when annual inflation rises from −2% to 4% andby nearly 24% when inflation reaches 10%.

16 The Chicago-rule rate of inflation in annualized percentage terms is π∗ = 400∗( −ρ

1+ρ

). Inserting

the calibrated figure ρ = 0.005, we obtain π∗ = −1.99%.

278 M. Casares

Fig. 2. Model 1. Level effects of increasing steady-state annual inflation from the Chicago rule to 10%

Table 1. Model 1. Effects of increasing annual inflation from the Chicago rule

Percent changes in relevant variables Welfare cost

π m s ψ k w n c l y0% −36.4 4.18 0 −0.25 0 −0.25 −0.25 0.01 −0.25 0.164% −50.3 12.9 0 −0.68 0 −0.68 −0.68 0 −0.68 0.50

10% −58.0 24.0 0 −1.20 0 −1.20 −1.20 −0.03 −1.20 0.91

This increase in shopping time s will bring about a fall in average labor n.This fall in labor will drive capital down as implied by (19). Average output willalso fall as a consequence of the decline in both labor and capital. These are onlyminor reductions in average labor, average capital, average output, and consumption(see Fig. 2). In fact, they all undergo the same decrease in percentage units. Twoexamples reported in Table 1 show that when annual inflation moves up from theChicago rule figure to 4%, all these variables drop by 0.68%, and if steady-stateinflation reaches 10% per year, they all fall by 1.20%.

Finally, the estimates of the welfare cost of inflation are also quite low: whenprices are constant (0% inflation) the welfare cost is 0.16% of output, 4% annualinflation produces a welfare cost of 0.50% of output, and 10% inflation has a welfarecost equal to 0.91%. The optimal rate of inflation is at the Chicago rule (−1.99%per year).

Price setting and the steady-state effects 279

Fig. 3. Model 2. Level effects of increasing steady-state annual inflation from the Chicago rule to 10%

5.2 Model 2. Sticky prices with partial price indexation

Figure 3 and Table 2 show the steady state effects of inflation in an economy withsticky prices (η = 0.75), and partial price indexation. Prices are set optimally onlywith a probability equal to 1 − η = 0.25. This means that on average the sellingprice will be adjusted optimally only once per year. However, there exists anotherform of price adjustment through the indexation rule. We examined the resultsat three different levels of price indexation according to their probabilities: high(χ = 0.75), medium (χ = 0.50), and low (χ = 0.25).

Similarly to what occurs in the flexible-price economy, the most significantresponses to higher inflation are a fall in real moneym and an increase in transactioncosts s. This result is robust to any price indexation level.

However the other variables show different patterns depending on the value ofχ. In the economy with a high level of price indexation (χ = 0.75), the steady-stateeffects of inflation are quantitatively much weaker than in the economy with lowprice indexation (χ = 0.25). Figure 3 reveals that the real mark-up ψ increaseswith higher inflation. The absence of full price indexation (0.0 ≤ χ < 1.0) in asticky-price economy (0.0 < η < 1.0) gives rise to a steady-state link betweeninflation π and the real mark-up ψ, as shown in (20). Consequently, the capitaltax channel matters in the steady-state analysis of inflation. This response is muchstronger when there is little price indexation (χ = 0.25). Put differently, the capital

280 M. Casares

Table 2. Model 2 with χ = 0.75. Effects of increasing annual inflation from the Chicago rule

Percent changes in relevant variables Welfare cost

π m s ψ k w n c l y0% −36.4 4.18 −0.02 −0.22 0.03 −0.25 −0.22 0.01 −0.22 0.154% −50.4 12.9 0.04 −0.69 −0.06 −0.64 −0.73 −0.02 −0.72 0.5610% −58.3 24.0 0.54 −1.67 −0.83 −0.84 −1.77 −0.22 −1.75 1.54

Model 2 with χ = 0.50. Effects of increasing annual inflation from the Chicago rule

π m s ψ k w n c l y0% −36.3 4.17 −0.05 −0.18 0.08 −0.27 −0.20 0.03 −0.20 0.124% −50.5 12.9 0.15 −0.79 −0.23 −0.56 −0.86 −0.06 −0.84 0.7010% −59.3 23.9 2.31 −3.22 −3.50 0.29 −3.57 −0.80 −3.84 3.54

Model 2 with χ = 0.25. Effects of increasing annual inflation from the Chicago rule

π m s ψ k w n c l y0% −36.2 4.16 −0.09 −0.15 0.15 −0.30 −0.18 0.04 −0.17 0.084% −50.5 12.9 0.37 −0.97 −0.57 −0.40 −1.10 −0.15 −1.06 0.9610% −62.2 23.8 7.67 −7.66 −10.9 3.64 −8.72 −2.53 −8.43 9.77

tax channel is more influential with a low level of price indexation, and capital,output and consumption fall very heavily. As Table 2 informs, when steady-stateannual inflation moves from −2% to 10%, capital, output and consumption fall byaround 8% in the low-indexation economy (χ = 0.25), whereas they decrease byless than 2% in the high-indexation economy (χ = 0.75).

It is also interesting that the effect of inflation on labor differs in directiondepending on the level of indexation χ. Since the impact on consumption is muchstronger with low indexation we observe a positive response of labor at high ratesof inflation. Labor supply shifts far enough to the right to outweigh the contractionof labor demand. Thus, the labor market clears with a greater quantity of labor anda fall in real wages (seew and n in Fig. 3). The increase in labor is more noticeablewhen the economy features little price indexation (χ = 0.25).

Regarding the welfare cost of inflation, the two arguments of the utility function,consumption and leisure, undergo larger falls in response to higher inflation whenthe economy exhibits a low level of price indexation, especially within the high-inflation range. Thus, the welfare cost is also larger (see Fig. 3). For example, a10% rate of inflation has a welfare cost equal to 1.54% of output when χ = 0.75and equal to 9.77% of output when χ = 0.25.

With partial price indexation the optimal rate of inflation is no longer at theChicago rule. The reason behind this result is that the initial increments of inflationfrom the Chicago rule produce slight falls in the real mark-up. In other words, thereexists a u-shaped response of the real mark-up to inflation as shown in Fig. 1 for thecase χ = 0.50. Unfortunately we cannot observe this in Fig. 3 because the figuresare very low compared to the positive impact reported at positive rates of inflation.What we have there is a negative change in ψ as inflation moves from −2% to 0%.This drop is more significant for a lower level of price indexation. A decrease in

Price setting and the steady-state effects 281

Fig. 4. Model 3. Level effects of increasing steady-state annual inflation from the Chicago rule to 10%

Table 3. Model 3. Effects of increasing annual inflation from the Chicago rule

Percent changes in relevant variables Welfare cost

π m s ψ k w n c l y0% −36.1 4.14 −0.14 −0.09 0.22 −0.31 −0.12 0.05 −0.11 0.054% −50.7 12.8 0.74 −1.29 −1.15 −0.14 −1.49 −0.28 −1.43 1.42

10% −71.9 22.9 30.6 −22.7 −34.1 17.4 −27.1 −9.59 −25.9 52.61

the capital tax is an incentive for capital accumulation. Hence, the optimal rate ofinflation was found to be −1.71% when χ = 0.25, −1.90% when χ = 0.50, and−1.98% when χ = 0.75.

5.3 Model 3. Sticky prices with no price indexation (Calvo economy)

An economy without price indexation is now analyzed. The seminal paper by Calvo(1983) assumed the absence of any price adjustment when prices cannot be setoptimally. Thus, we refer to this case as the Calvo economy. Taking η = 0.75 andχ = 0.0, a fraction 1− η = 0.25 of the households set the price optimally whereasthe rest of the households, the fraction η = 0.75, leave the price unchanged.

Figure 4 and Table 3 show that two major effects of higher inflation are a fall inreal money balances and an increase in transaction costs, as previously observed in

282 M. Casares

both Model 1 and Model 2. Nevertheless, it is also seen that other variables respondto higher inflation much more aggressively than in those models. In particular,capital, output and consumption drop dramatically when inflation rates rise to 10%per year. The origin of these sharp falls is the strong response of the real mark-up to increasing rates of inflation. Some numbers illustrate this result in Table 3.When inflation rises from −2% to 10% in steady state, the real mark-up ψ alsorises by more than 30%. The stock of capital is dramatically affected as it falls bynearly 23%. Output and consumption also decline sharply. They both fall by morethan 25% when inflation moves from −2% to 10%. Such a wide departure fromsuperneutrality seems very unrealistic.

The explanation of this strong negative effect is rather intuitive. If there is noprice indexation and the rate of inflation reaches moderately high figures, producersbecome more aggressive when adjusting the price optimally. They know that theymight face a long period without being able to change the price. Their optimalprice is set substantially higher than the marginal cost. This implies a very highreal mark-up. In turn, the capital tax channel exerts a very harmful effect on capitalaccumulation. Capital, output, and consumption fall dramatically.

When inflation rises, labor reacts in the opposite direction to capital. There is asignificant increase in labor when inflation approaches 10% per year. This result wasalready discussed in Model 2 for the case of low indexation. The Calvo economycan be viewed as the extreme case of no indexation. The significant decrease inconsumption shifts the labor supply curve to the right, i.e. households wish to workmore and average labor increases.

Meanwhile, figures for the welfare cost of inflation are also very high as bothconsumption and leisure fall in response to higher rates of inflation.Annual inflationof 4% has a welfare cost equal to 1.42% of output. There is a very rapid increasein the welfare cost at higher rates. A 10% rate of inflation per year produces awelfare cost of 52.6% of output, more than one-half of the total output producedper year! This is indeed very unrealistic and would push producers to use someprice indexation scheme to defend themselves from inflation.

Finally, the optimal rate of inflation is −1.32%. As discussed in Model 2, thereis an initial negative impact on the real mark-up when π departs from the Chicagorule. This creates a positive welfare effect that means that the optimal inflation isno longer at the Chicago rule.

6 Conclusions

There are two different channels of deviation from superneutrality in an optimizingmonetary model with monopolistic competition and sticky prices: the monetaryservices channel and the ”capital tax” channel. The monetary services channelcorresponds to the classic Friedman analysis of inflation. Higher inflation bringsabout substantial reductions in monetary services that can have a negative impacton output. In the ”capital tax” channel, higher inflation affects the monopolisticcompetition mark-up term, which acts as a tax on capital accumulation decisions.

The price setting characteristics of the economy play a significant role in thesteady-state analysis of inflation. If prices are fully flexible or there is price sticki-

Price setting and the steady-state effects 283

ness with full price indexation, the monetary services channel is the only mechanismthat can explain superneutrality deviations. The optimal steady-state rate of inflationis at the Chicago rule, which guarantees satiation on monetary services.

By contrast, if prices are sticky and there is not full price indexation, the ”cap-ital tax” channel becomes the driving force governing the steady-state effects ofinflation because it is quantitatively more significant than the monetary serviceschannel. In addition, the optimal rate of inflation is no longer at the Chicago rule.

This paper has also shown that the level of price indexation in the economyis crucial in determining the size of the steady-state effects of inflation. Thus, aneconomy with a low level of price indexation is more severely affected by a rise inthe steady-state rate of inflation than an economy where most of the non-optimalprices are indexed. Output falls more sharply and the welfare cost is higher whensteady-state inflation rises. Under the original Calvo model assumption of no priceindexation, the steady-state effects of inflation simply are unrealistically large interms of output falls and welfare cost of inflation.

Our results support a long-run monetary policy aimed at price stability witha close-to-zero inflation target. Low-inflation economies (from the Chicago rule−2% to 4% per year) report low estimates of the welfare cost of inflation. Thisresult is robust to any pricing specification.

Appendix

• The steady-state relationship between the optimal price P and the Dixit-Stiglitzaggregate price level PA.

Both Calvo-type price stickiness and price indexation imply that in period t theDixit-Stiglitz aggregate price level PA

t is

PAt = [(1 − η) [Pt]

1−θ +(1−η)ηχ [(1+π)Pt−1]1−θ +(1−η)η(1−χ) [Pt−1]

1−θ +

(1−η)η2χ2 [(1+π)2Pt−2

]1−θ+2(1−η)η2χ(1−χ) [(1+π)Pt−2]

1−θ +

(1 − η)η2(1 − χ)2 [Pt−2]1−θ + ...]1/(1−θ),

wherePt−j is the optimal price in period t−j. This expression can be written morebriefly as

PAt =

[(1−η) [Pt]

1−θ +η[(1−χ)+χ(1+π)1−θ

] [PA

t−1]1−θ

]1/(1−θ). (A1)

Equation (A1) in steady state implies the following relationship between the priceoptimally adjusted in the current period P and the aggregate price level PA

P

PA=

[1−η[(1−χ)(1+π)θ−1+χ]

1−η

]1/(1−θ)

. (A2)

Particular cases worth noting are

η = 0.0 (flexible prices) → P = PA

η > 0, χ = 1.0 (full indexation) → P = PA

η > 0, χ = 0.0 (Calvo economy) → P = PA[

1−η(1+π)θ−1

1−η

]1/(1−θ)

284 M. Casares

• The steady-state relationship between average output y and f(n, k).The Calvo price setting distribution at hand gives rise to the following definition

of average output in steady state y

y =∞∑

j=0

[(1 − η)ηjy−j

], (A3)

where y−j is the average output produced by the fraction of producers that last setits price optimally j periods ago. The value of y−j is expressed in Dixit-Stiglitzaggregate output units. Taking into consideration the nominal rigidities and therespective Dixit-Stiglitz demand functions for each set price, the steady state valueof y−j is

y(j) =

[j∑

k=0

j!(j − k)!k!

χj−k(1 − χ)k(1 + π)(1−θ)(j−k)

] [P−j

P A

]1−θ

yA,

where P−j is the steady-state optimal price set j periods ago. The previous expres-sion is equivalent to

y(j) =[1 + ((1 + π)1−θ − 1)χ

]j[

P−j

P A

]1−θ

yA. (A4)

The ratio P−j/PA can be decomposed into

P−j

P A = P−j

PP

P A . (A5)

Since P/PA is constant (see A2), the optimal selling price must grow at the samerate as the aggregate price level. In turn, the steady-state condition that drives thechange in optimal prices for the last j periods is

P = (1 + π)jP−j . (A6)

Inserting this result into the price decomposition (A5) and substituting it in Eq. (A4)yields, after some algebra,

y−j =[(1 − χ)(1 + π)θ−1 + χ

]j [P

P A

]1−θyA. (A7)

The value of y−j given by (A7) is introduced into (A3) to obtain

y =∞∑

j=0

(1 − η)ηj[(1 − χ)(1 + π)θ−1 + χ

]j PP A

[P

P A

]−θyA, (A8)

where the introduction of y, the amount of output produced at P , implies

y =∞∑

j=0

(1 − η)ηj[(1 − χ)(1 + π)θ−1 + χ

]j P

PAy.

Price setting and the steady-state effects 285

By computing the sum over j, we obtain

y =[

1−η1−η[(1−χ)(1+π)θ−1+χ]

] P

PAy,

Now P/PA is replaced by its steady state value obtained in (A2) to give

y =[

1−η1−η[(1−χ)(1+π)θ−1+χ]

] [1−η[(1−χ)(1+π)θ−1+χ]

1−η

]1/(1−θ)

y,

which implies the following steady-state expression relating y to y

y =[

1−η1−η[(1−χ)(1+π)θ−1+χ]

]θ/(θ−1)y. (A9)

So far, we have found a steady-state relationship between y and y. We will nowderive the analogous steady-state expression relating f(n, k) to y in order to deducea steady-state relationship between y and f(n, k). The value given by f(n, k) is theamount of output produced by plugging the steady-state average labor and capitaln and k in the Cobb-Douglas production function

f(n, k) = [n]1−α [k]α. (A10)

Under the Calvo setup, the steady-state average labor and capital are

n =∑∞

j=0(1 − η)ηjnd−j ,

k =∑∞

j=0(1 − η)ηjk−j ,(A11)

where nd−j and k−j are the steady-state average demand for labor and capital

decided by the fraction of producers that was last able to set the price optimallyj periods ago. Taking the price indexation probabilities into consideration, therespective Dixit-Stiglitz demand functions for each price set and the constant returnsto scale production technology, nd

−j and k−j are given in steady state by

nd−j =

[∑jk=0

j!(j−k)!k!χ

j−k(1 − χ)k(1 + π)−θ(j−k)]nd

−j ,

k−j =[∑j

k=0j!

(j−k)!k!χj−k(1 − χ)k(1 + π)−θ(j−k)

]k−j ,

(A12)

where nd−j and k−j are the steady-state amounts decided at the selling price P−j .

Expression (A12) is equivalent to

nd−j =

[1 + ((1 + π)−θ − 1)χ

]jnd

−j ,

k−j =[1 + ((1 + π)−θ − 1)χ

]jk−j .

(A13)

286 M. Casares

Now our intention is to write nd−j and k−j as a function of nd and k, the amounts

decided at the optimal selling price in the current period P . The constant returns toscale property of the production function implies

nd−j =

[P−j

P

]−θ

nd,

k−j =[

P−j

P

]−θ

k.

Recalling (A6) yields

nd−j = (1 + π)jθnd,

k−j = (1 + π)jθk.(A14)

Substituting (A14) into (A13) gives after some algebra

nd−j =

[(1 − χ)(1 + π)θ + χ

]jnd,

k−j =[(1 − χ)(1 + π)θ + χ

]jk.

(A15)

Now by substituting the values obtained from (A15) into (A11)

n =∑∞

j=0(1 − η)ηj[(1 − χ)(1 + π)θ + χ

]jnd,

k =∑∞

j=0(1 − η)ηj[(1 − χ)(1 + π)θ + χ

]jk,

where, after solving the sum over j, we have

n =[

1−η1−η[(1−χ)(1+π)θ+χ]

]nd,

k =[

1−η1−η[(1−χ)(1+π)θ+χ]

]k.

(A16)

The values of n and k implied by (A16) enter the production function (A10)

f(n, k) =[

1−η1−η[(1−χ)(1+π)θ+χ]

] [nd

]1−α[k]α ,

which in terms of y yields

f(n, k) =[

1−η1−η[(1−χ)(1+π)θ+χ]

]y. (A17)

The amount of average output y as a function of ywas given by Eq. (A9). Combining(A9) with (A17) leads to the following steady-state relationship between y andf(n, k)

y =

[1−η

1−η[(1−χ)(1+π)θ−1+χ]

]θ/(θ−1)

[1−η

1−η[(1−χ)(1+π)θ+χ]

] f(n, k) (A18)

Price setting and the steady-state effects 287

Particular cases worth noting are

η = 0.0 (flexible prices) → y = f(n, k)η > 0, χ = 1.0 (full indexation) → y = f(n, k)

η > 0, χ = 0.0 (Calvo economy) → y =

[1−η

1−η(1+π)θ−1

]θ/(θ−1)

[1−η

1−η(1+π)θ

] f(n, k)

• The steady-state real mark-up ψ.

Under pricing conditions a la Calvo, the selling price first order condition is givenin steady state by

P =θ

θ − 1

∑∞j=0 β

jηj[(1 − χ)(1 + π)θ + χ

]jψ−1PAyA∑∞

j=0 βjηj [(1 − χ)(1 + π)θ−1 + χ]j yA

, (A19)

where ψ−1 is the inverse of the real mark-up. The previous expression can besimplified to

P =θ

θ − 11 − βη

[(1 − χ)(1 + π)θ−1 + χ

]1 − βη [(1 − χ)(1 + π)θ + χ]

ψ−1PA. (A20)

Solving (A20) for the steady-state mark-up ψ yields

ψ =θ

θ − 11 − βη

[(1 − χ)(1 + π)θ−1 + χ

]1 − βη [(1 − χ)(1 + π)θ + χ]

PA

P. (A21)

Finally, the steady-state ratio PA/P implied by (A2) is inserted in (A21) to obtain

ψ =θ

θ−11−βη [

(1−χ)(1+π)θ−1+χ]

1−βη [(1−χ)(1+π)θ+χ]

[1 − η

1 − η [(1−χ)(1+π)θ−1+χ]

]1/(1−θ)

.

(A22)

Particular cases worth noting are

η = 0.0 (flexible prices) → ψ =θ

θ − 1

η > 0, χ = 1.0 (full indexation) → ψ =θ

θ − 1η > 0, χ = 0.0 (Calvo economy) → ψ =

θ

θ−11−βη(1+π)θ−1

1−βη(1+π)θ

[1 − η

1 − η(1+π)θ−1

]1/(1−θ)

288 M. Casares

• The steady-state solution of the model in a twelve-equation reduced form.

π = µ,

r = ρ,

R = r + π(1 + r),

y =[

1 − η

1−η [(1−χ)(1+π)θ−1+χ]

]θ/(θ−1) [1−η

1−η [(1−χ)(1+π)θ+χ]

]−1

n1−αkα,

ψ =θ

θ−11−βη [

(1−χ)(1+π)θ−1+χ]

1−βη [(1−χ)(1+π)θ+χ]

[1−η

1−η [(1−χ)(1+π)θ−1+χ]

]1/(1−θ)

,

k = n

[α(1 + ρ)ψ(ρ+ δ)

]1/(1−α)

,

w = (1 − α)[k

n

]α

ψ−1,

c = y − δk,

m = c

[a1a2w

1 − a2

(R

(1 +R)+ a3w

)−1]1−a2

,

n = T − l − s,

s = a0 + a1c1/(1−a2)m−a2/(1−a2) + a3m,

l =

w c−σ

Υ(1 + w a1

1−a2

[cm

]a2/(1−a2))

−1/γ

.

The twelve-equation system provides a solution for the twelve variables π, r,R, y,ψ, k, w, c, m, n, s, and l, given some calibrated value for the parameters ρ, σ, Υ ,γ, a0, a1, a2, a3, δ, α, θ, η, χ, and µ.

References

Basu, S., Fernald, J.G. (1994) Constant Returns and Small Markups in the US Manufacturing. Interna-tional Finance Discussion Paper 483, Board of Governors of the Federal Reserve System

Basu, S. (1996) Procyclical Productivity: Increasing Returns or Cyclical Utilization? Quarterly Journalof Economics 111: 719–751

Baumol, W.J. (1952) The Transactions Demand for Cash: An Inventory Theoretic Approach. QuarterlyJournal of Economics 66: 545–556

Calvo, G.A. (1983) Staggered Pricing in a Utility-Maximizing Framework. Journal of Monetary Eco-nomics 12: 383–396

Casares, M. (2000) Long-Run Analysis in Alternative Optimizing Monetary Models. Working paper0107, Universidad Publica de Navarra. Pamplona, Spain

Chadha, J.S., Haldane, A.G., Janssen, N.G.J. (1998) Shoe-Leather Costs Reconsidered. Economic Jour-nal 108: 363–382

Christiano, L.J., Eichenbaum, M., Evans, C.L. (2001) Nominal Rigidities and the Dynamic Effects ofa Shock to Monetary Policy. NBER Working Paper Series, 8403

Den Haan, W.J. (1990) The Optimal Inflation Path in a Sidrauski-Type Model with Uncertainty. Journalof Monetary Economics 25: 389–409

Price setting and the steady-state effects 289

Dixit, A.K., Stiglitz, J.E. (1977) Monopolistic Competition and Optimum Product Diversity. AmericanEconomic Review 67: 297–308

Dotsey, M., Ireland, P.N. (1996) The Welfare Cost of Inflation in General Equilibrium. Journal ofMonetary Economics 37: 29–47

Dotsey, M., Ireland, P.N., King, R.G., Wolman, A.L. (1999) State Dependent Pricing and the GeneralEquilibrium Dynamics of Money and Output. Quarterly Journal of Economics 114(2): 655–690

Erceg, C.J., Henderson, D.W., Levin, A.T. (2000) Optimal Monetary Policy with Staggered Wage andPrice Contracts. Journal of Monetary Economics 46: 281–313

Friedman, M. (1969) The Optimum Quantity of Money. In: The Optimum Quantity of Money and OtherEssays. Aldine Publishing Company, Chicago

Hicks, J.R. (1935) A Suggestion for Simplifying the Theory of Money. Economica 2: 1–19Lucas, R.E. (2000) Inflation and Welfare. Econometrica 68(2): 247–274McCallum, B.T., Goodfriend, M.S. (1987) Demand for Money: Theoretical Studies. In: The New Pal-

grave: A Dictionary of Economics. London, Macmillan Press. Reprinted in Federal Reserve Bankof Richmond Economic Review (1988) 74: 16–24

Pencavel, J.H. (1986) Labor Supply of Men: A Survey. In: Ashenfelter, O., Layard, R. (eds.) Handbookof Labor Economics. North Holland, Amsterdam

Sidrauski, M. (1967) Rational Choice and Patterns of Growth in a Monetary Economy. AmericanEconomic Review Papers and Proceedings 57: 534–544

Tobin, J. (1958) Liquidity Preference as Behavior Toward Risk. Review of Economic Studies 25: 65–86Wallace, N. (1980) The Overlapping Generations Model of Fiat Money. In: Kareken, J.H., Wallace, N.

(eds.) Models of Monetary Economics. Federal Reserve Bank of Minneapolis, MinneapolisWolman, A.L. (1997) Zero Inflation and the Friedman Rule: A Welfare Comparison. Federal Reserve

Bank of Richmond Economic Quarterly Fall 1997Wu, Y., Zhang, J. (2000) Monopolistic Competition, Increasing Returns to Scale, and the Welfare Costs

of Inflation. Journal of Monetary Economics 46: 417–440Yun, T. (1996) Nominal Price Rigidity, Money Supply Endogeneity, and Business Cycles. Journal of

Monetary Economics 37: 345–370Zbaracki, M.J., Ritson, M., Levy, D., Dutta, S., Bergen, M. (2000) The Managerial and Customer

Costs of Price Adjustment: Direct Evidence from Industrial Market. Manuscript, Wharton School,University of Pennsylvania