Presented by Ginger Baker Eileen Campbell. Cost Principles for Educational Institutions found in 2...

27

THE FACILITIES AND ADMINISTRATIVE RATE CALCULATION PROCESS – SIMPLIFIED METHOD Presented by Ginger Baker Eileen Campbell

-

Upload

martin-jaggard -

Category

Documents

-

view

215 -

download

1

Transcript of Presented by Ginger Baker Eileen Campbell. Cost Principles for Educational Institutions found in 2...

THE FACILITIES AND ADMINISTRATIVE RATE CALCULATION PROCESS –

SIMPLIFIED METHOD

Presented byGinger Baker

Eileen Campbell

OMB Circular A-21

Cost Principles for Educational Institutions found in

2 CFR Part 220

The Federal Government guidelines for calculating the facilities and administrative rate using either Long Form or Short Form methodologies.

Educational institutions that receive federal awards subject to A-21 of less than $10 million are required to calculate their F&A cost rate using a simplified method known as a short form (Section H).

Educational institutions that wish to be reimbursed for institutional wide administrative and facility costs associated with federal contracts and grants need to develop an F&A cost rate.

Objectives of the A-21 Cost Principles

Sets uniform standards of allocation Sets uniform standards of allowability Allows schools to identify full cost of

federal programs Provides that the federal government

bear its fair share of total costs Simplifies intergovernmental relations Encourages consistent costing

What the Cost Principles Require:

The six “B’s” for costs: Be allowable Be allocable Be reasonable Be treated consistently Be necessary to perform the program Be permissible under the law

What is the F&A Rate Proposal?

The documentation prepared by an institution in accordance with the federal cost principles in OMB Circular A-21 to substantiate its claim for the reimbursement of F&A costs. If you don’t want to be reimbursed for F&A

costs, you don’t have to prepare a proposal. The proposal should to be submitted six

months after the fiscal year end.

What is the F&A Rate Proposal?

The proposal needs to be reconciled to the audited financial statements.

Needs to be clear explanation of adjustments and reclassifications.

Base period normally coincides with fiscal year.

Short form institutions follow Section H of OMB Circular A-21.

What is the F&A Rate Proposal?

The proposal and supporting documentation becomes the basis for negotiating your institution’s F&A rate.

Remember, this is your proposal and you must defend it.

What are Facilities and Administrative (F&A) Costs?

Costs that are incurred for common or joint objectives and therefore cannot be identified readily and specifically with a particular sponsored project, instructional activity or any other institutional activity.

Often referred to as indirect or overhead costs.

What are Facilities and Administrative (F&A) Costs?

Not directlyassignableto any one

activity.

ExecutiveManagement

Building and Equipment Depreciation/

Use Allowance

Payroll orPurchasing

Repair & Maintenance Utilities

Human Resources

Accounting &Financial

Management

Budgeting

The Short Form

Advantages Relatively easy to prepare and negotiate Uses institutional financial statements Uses formula approach -1 pool and 1 base

(OH) Does not need a space study Does not need a library allocation Does not need a DCE calculation Does not need sub-pooling for GA or O&M Administration is not subject to the 26 point

cap that is imposed on long-form institutions

The Short Form

Disadvantages Does not always result in optimizing F&A cost

recovery. Establishes one rate for all sponsored activity,

rather than on and off campus rates and special rates where appropriate.

The F&A Calculation Process

Download operating expenses Functional expenses need to be broken into

salaries, fringe, and other expenses Reconcile

Expenses to the Financial Statements by NACUBO functional category

Decide on Distribution Basis MTDC Salaries and Wages

Reclassify financial expenses Into the function groups and ultimately indirect cost

pool and direct cost base

The F&A Calculation Process Exclude certain costs

MTDC exclusions Unallowable costs

Make adjustments to ensure consistency Calculate the rate

Reconcile Extract current fund operating expenses Reconcile to expenditures reported in the

notes to the financial statements by NACUBO category

Can take longer than you think

Reclassification Short form institutions need to reclassify

their financial expenses into the F&A function groups and ultimately either the indirect cost pool or direct cost base needed to compute the F&A rate under the simplified method.

This initial review of expenses for F&A classification purposes can be done at the department, object code, or account level.

ReclassificationReclassifications Include: Scrub Expenses Unallowable Activities Sponsored Accounts Catalogs, Commencement, and

Convocations Department Paid Operations and

Maintenance Library Department Administration Specialized Service Facilities

Reclassification Auxiliary Assessments for Institutional

Support and/or Operations and Maintenance

Academic Support Student Services Administration Institutional Support

ExclusionsExclusions Include: College Work Study Modified Total Direct Cost Exclusions

Capitalized Equipment Subcontracts > $25K Financial Aid Long Term Facilities Rental Patient Care Costs

Unallowable Expenses Bad Debt Entertainment

Cost of Goods Sold in Auxiliaries

AdjustmentsAdjustments Include: Applicable Credits O&M Expenses Allowable Building Depreciation Allowable Equipment Depreciation Interest Expense Gain/Loss on Disposal of Depreciable Assets

The F&A Calculation Process

Financial Statement Functional Category F&A Function Group Indirect or DirectInstruction Department Administration

InstructionIndirectDirect

Research Department AdministrationResearch

IndirectDirect

Public Service Department AdministrationPublic Service

IndirectDirect

Academic Support Department AdministrationLibrarySpecialized Service FacilitiesOther Direct Costs

IndirectIndirectDirectDirect

Student Services Administration Other Direct Costs Direct

Institutional Support General Administration Indirect

Operation and Maintenance of Plant Operations and Maintenance of Plant Indirect

Scholarships and Fellowships Eliminated from Proposal

Auxiliary Enterprises Auxiliary Enterprises Direct

Building Depreciation Indirect

Equipment Depreciation Indirect

Interest Expense Indirect

How is the Rate Developed?

Step 1. Develop the F&A cost pool:- Administrative salaries/wages $350,000- Associated fringe benefits 75,000 - Finance and accounting costs 25,000- Supplies, materials and expenses 17,000- Space related (O&M) 27,000- Administrative travel 6,000

- Total pool costs $500,000

How is the Rate Developed?

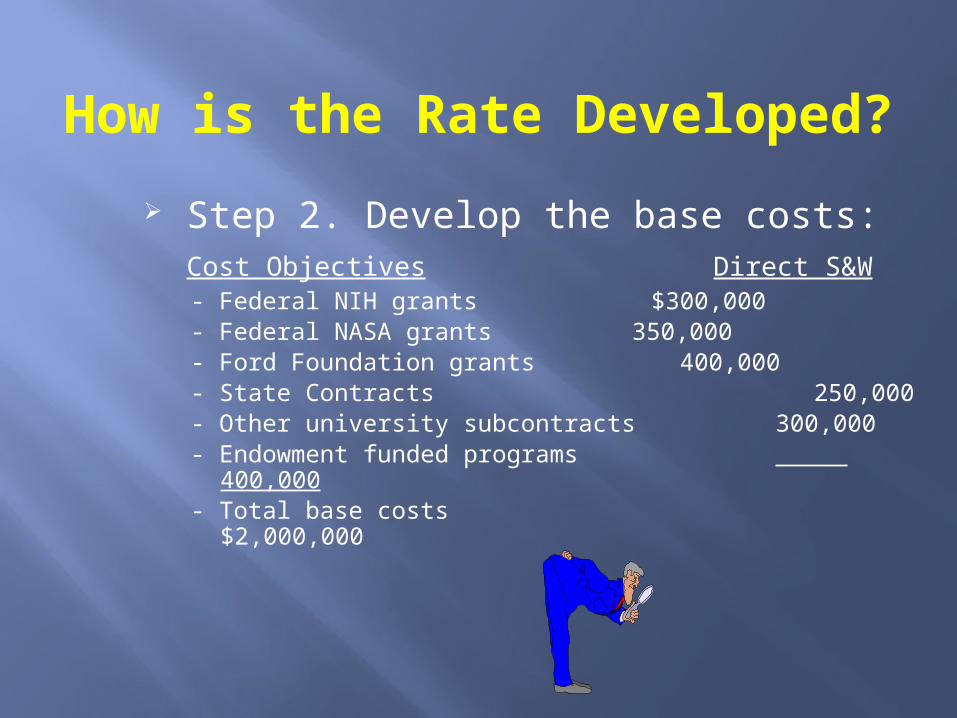

Step 2. Develop the base costs: Cost Objectives Direct S&W

- Federal NIH grants $300,000- Federal NASA grants 350,000- Ford Foundation grants 400,000- State Contracts 250,000- Other university subcontracts 300,000- Endowment funded programs 400,000- Total base costs $2,000,000

How is the Rate Developed?

Step 3. Calculate the rate:

F&A cost pool $ 500,000 Direct cost base $2,000,000

= 25%

How is the Rate Developed?

Step 4. Apply the rate:

Federal NIH grants $300,000 x 25% = $75,000Federal NASA 350,000 x 25% = 87,500Foundation grants 400,000 x 25% = 100,000State contracts 250,000 x 25% = 62,500Subcontracts 300,000 x 25% = 75,000Endowment 400,000 x 25% = 100,000

Total reimbursement $500,000

Questions?

Resources:DCA Short Form Sample:http://rates.psc.gov/fms/dca

A-21:http://www.whitehouse.gov/omb/circulars_a021_2004

Contact Information

Ginger BakerSenior Manager(702) [email protected]

Eileen CampbellManager(435) [email protected]

![THE GINGER GUIDE · PDF file · 2017-09-27GINGER GUIDE THE [ORIGINS OF FLAVOR ] ... omes of ginger ingiber officinale) ... ORGANIC GINGER SYRUP #25400 INGREDIENTS: Organic ginger,](https://static.fdocuments.net/doc/165x107/5aadf2a57f8b9a22118b6437/the-ginger-guide-guide-the-origins-of-flavor-omes-of-ginger-ingiber-officinale.jpg)