PRESENTED BY Epoch’s Quarterly Capital Markets in this presentation are forward looking statements...

22

David N. Pearl Executive Vice President and Co-CIO William W. Priest Chief Executive Officer and Co-CIO PRESENTED BY Josepha Kaufman Managing Director Senior Research Analyst The information contained in this presentation is distributed for informational purposes only and should not be considered investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. The information contained in this presentation is accurate as of the date submitted, but is subject to change. Any performance information referenced in this presentation represents past performance and is not indicative of future returns. Any projections, targets, or estimates in this presentation are forward looking statements and are based on Epoch’s research, analysis, and assumptions made by Epoch. There can be no assurances that such projections, targets, or estimates will occur and the actual results may be materially different. Other events which were not taken into account in formulating such projections, targets, or estimates may occur and may significantly affect the returns or performance of any accounts and/or funds managed by Epoch. To the extent this presentation contains information about specific companies or securities including whether they are profitable or not, they are being provided as a means of illustrating our investment thesis. Past references to specific companies or securities are not a complete list of securities selected for clients and not all securities selected for clients in the past year were profitable. Epoch’s Quarterly Capital Markets Outlook July 23, 2014 | The webinar replay will be available on our website: www.eipny.com

-

Upload

phungkhanh -

Category

Documents

-

view

214 -

download

1

Transcript of PRESENTED BY Epoch’s Quarterly Capital Markets in this presentation are forward looking statements...

David N. Pearl

Executive Vice President and Co-CIO

William W. Priest

Chief Executive Officer and Co-CIO

PRESENTED BY

JosephaKaufman

Managing Director Senior Research Analyst

The information contained in this presentation is distributed for informational purposes only and should not be considered investment advice or a recommendation of any particular security, strategy orinvestment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. The information contained in this presentation is accurate as of the datesubmitted, but is subject to change. Any performance information referenced in this presentation represents past performance and is not indicative of future returns. Any projections, targets, orestimates in this presentation are forward looking statements and are based on Epoch’s research, analysis, and assumptions made by Epoch. There can be no assurances that such projections,targets, or estimates will occur and the actual results may be materially different. Other events which were not taken into account in formulating such projections, targets, or estimates may occur andmay significantly affect the returns or performance of any accounts and/or funds managed by Epoch. To the extent this presentation contains information about specific companies or securitiesincluding whether they are profitable or not, they are being provided as a means of illustrating our investment thesis. Past references to specific companies or securities are not a complete list ofsecurities selected for clients and not all securities selected for clients in the past year were profitable.

Epoch’s Quarterly Capital Markets Outlook

July 23, 2014 | The webinar replay will be available on our website: www.eipny.com

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

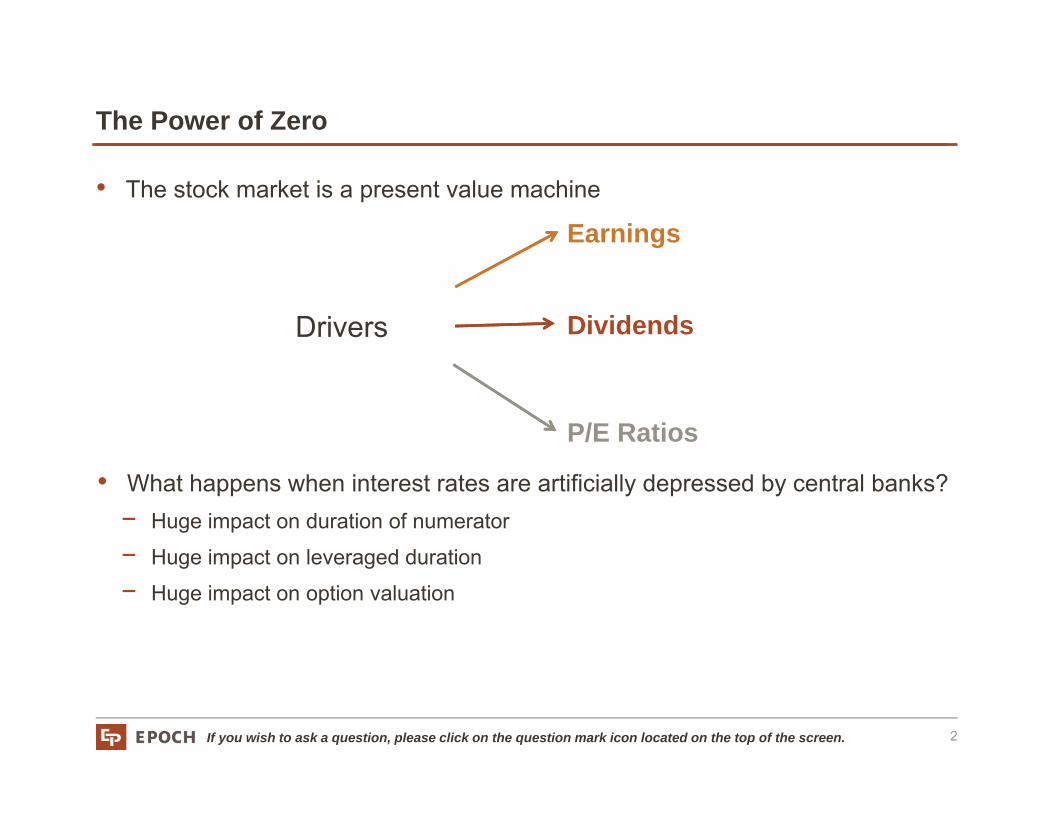

The Power of Zero

2

• The stock market is a present value machine

• What happens when interest rates are artificially depressed by central banks?− Huge impact on duration of numerator

− Huge impact on leveraged duration

− Huge impact on option valuation

Earnings

Dividends

P/E Ratios

Drivers

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

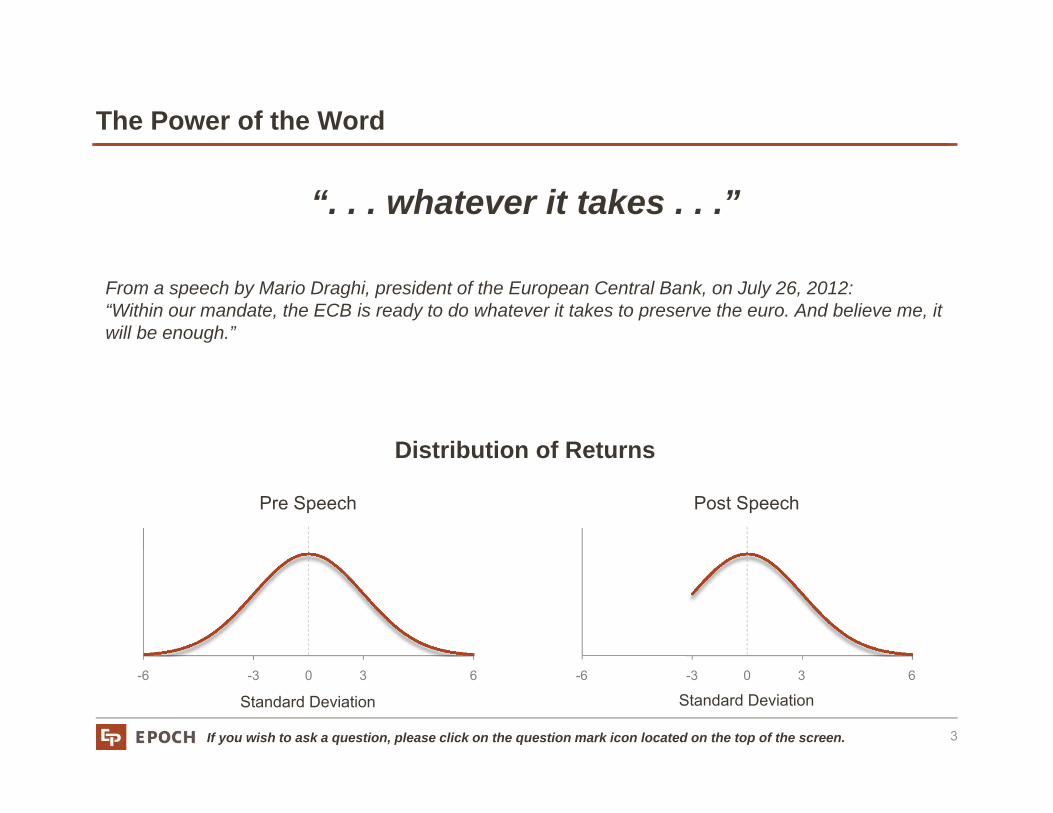

The Power of the Word

3

From a speech by Mario Draghi, president of the European Central Bank, on July 26, 2012: “Within our mandate, the ECB is ready to do whatever it takes to preserve the euro. And believe me, it will be enough.”

“. . . whatever it takes . . .”

Pre Speech Post Speech

Standard Deviation

Distribution of Returns

Standard Deviation0 3 6-3-6 0 3 6-3-6

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

1,250

1,350

1,450

1,550

1,650

1,750

1,850

1,950

2,050S&P 500

S&P 500 and Forward Earnings Multiples

Index

Source: Standard & Poors, Yardini Research, Epoch Investment Partners; June 2014

Quantitative Easing has Fueled Equity Markets

4

12x

13x

14x

15x

Extension of Twist

QE3

QE3 Expanded

Taper Tantrum

No Taper at Meeting

Yellen Nomination

16x

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

0

100

200

300

400

500

600

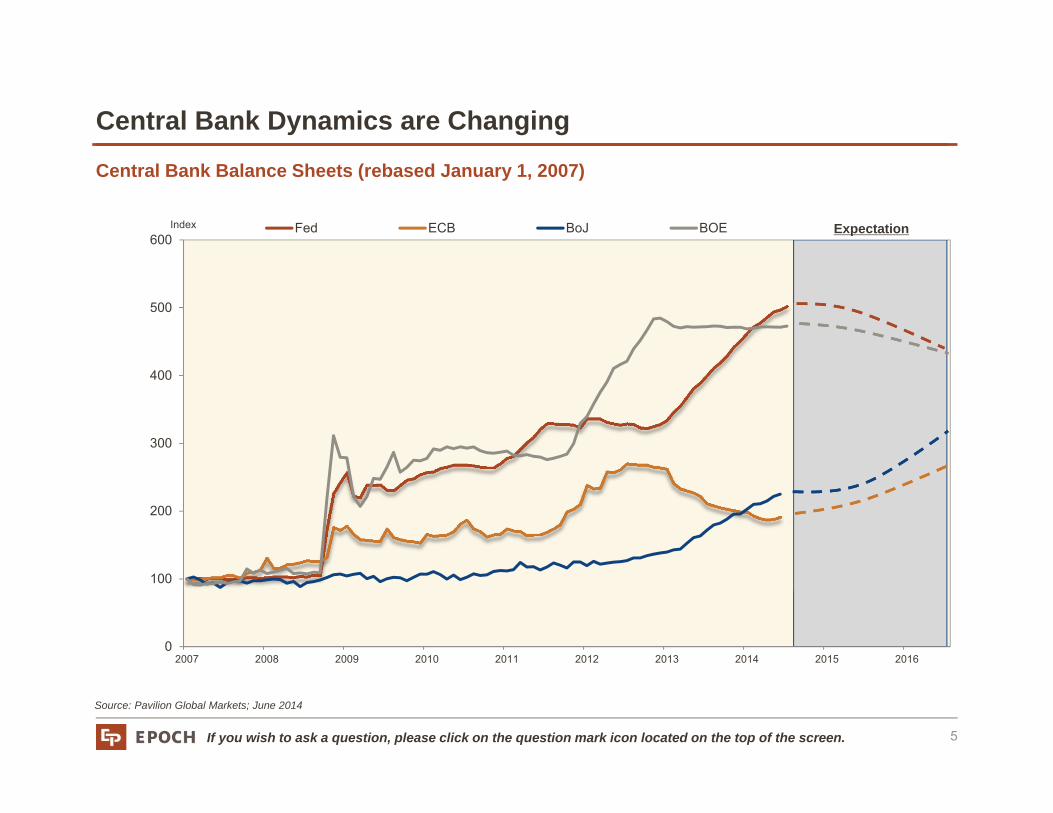

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Fed ECB BoJ BOE

Central Bank Balance Sheets (rebased January 1, 2007)

Source: Pavilion Global Markets; June 2014

Central Bank Dynamics are Changing

5

Index Expectation

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

0

10

20

30

40

50

60

70

80

90

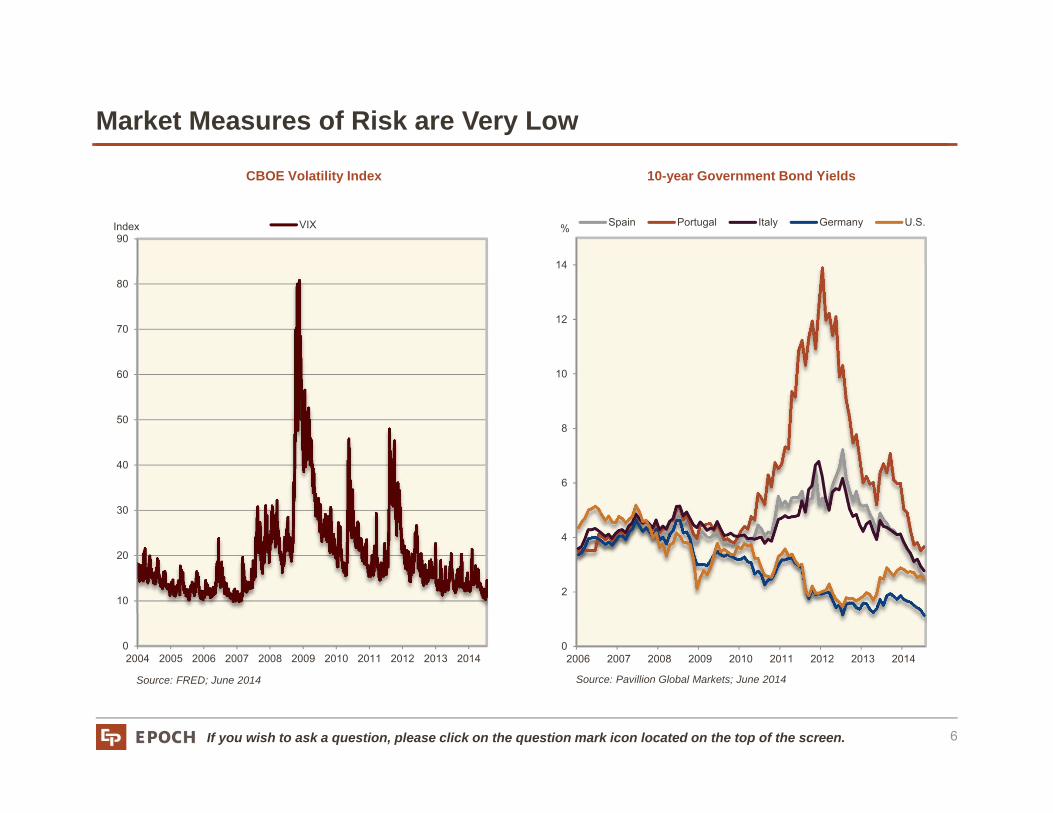

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

VIX

0

2

4

6

8

10

12

14

2006 2007 2008 2009 2010 2011 2012 2013 2014

Spain Portugal Italy Germany U.S.

CBOE Volatility Index

Source: FRED; June 2014

Market Measures of Risk are Very Low

6

%Index

10-year Government Bond Yields

Source: Pavillion Global Markets; June 2014

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

Geopolitical Risk a Growing Concern

Source: Council on Foreign Relations, Global Conflict Tracker

Red = Hi Risk, Orange = Medium Risk, Yellow = Low Risk

7

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

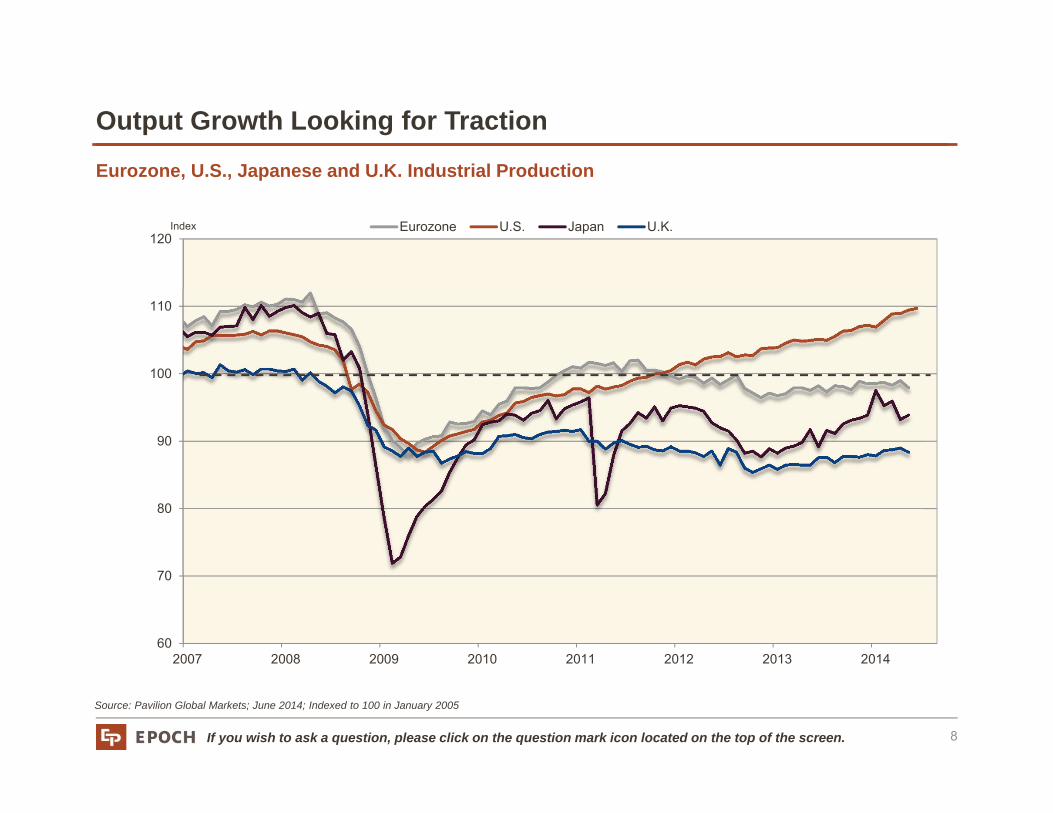

60

70

80

90

100

110

120

2007 2008 2009 2010 2011 2012 2013 2014

Eurozone U.S. Japan U.K.

Eurozone, U.S., Japanese and U.K. Industrial Production

Source: Pavilion Global Markets; June 2014; Indexed to 100 in January 2005

Output Growth Looking for Traction

8

Index

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

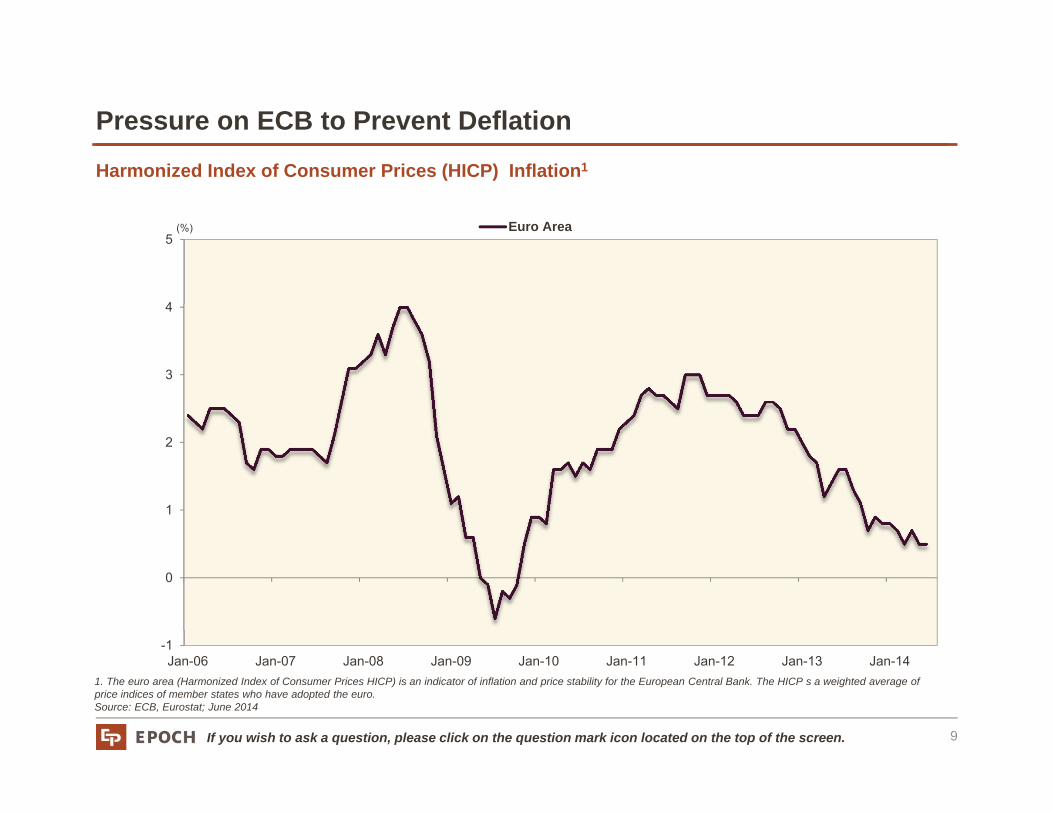

-1

0

1

2

3

4

5

Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

Euro Area

Harmonized Index of Consumer Prices (HICP) Inflation1

1. The euro area (Harmonized Index of Consumer Prices HICP) is an indicator of inflation and price stability for the European Central Bank. The HICP s a weighted average of price indices of member states who have adopted the euro. Source: ECB, Eurostat; June 2014

Pressure on ECB to Prevent Deflation

9

(%)

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

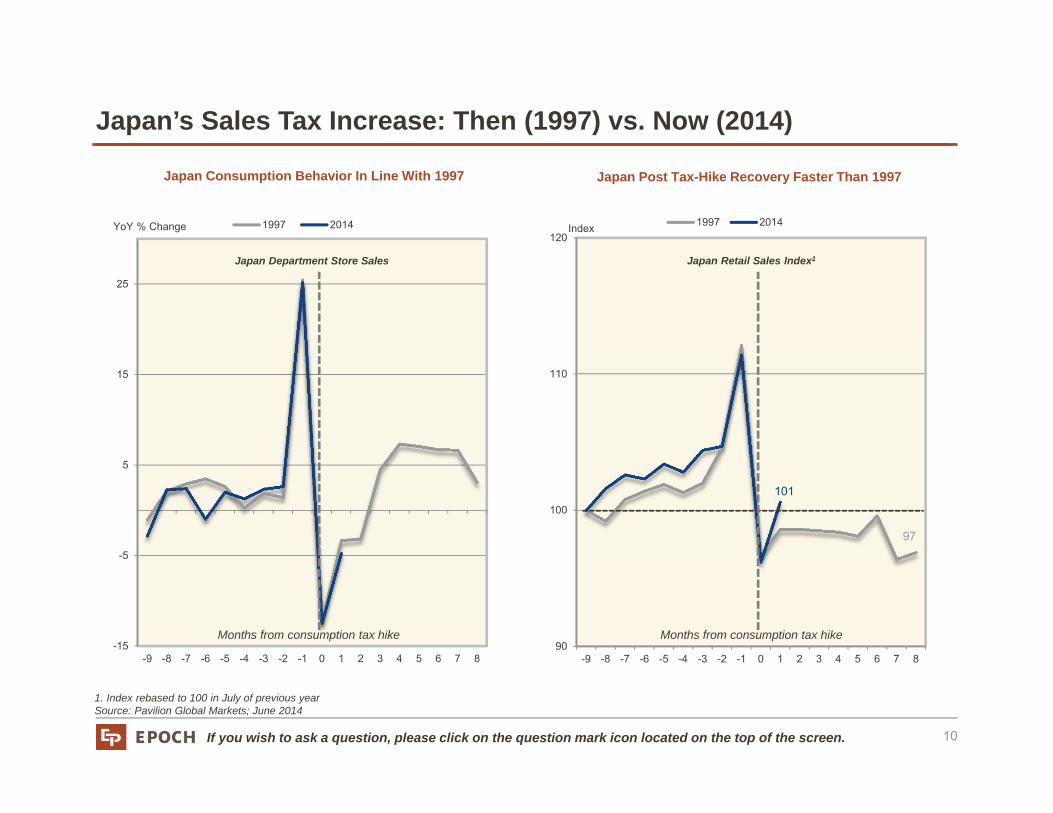

-15

-5

5

15

25

-9 -8 -7 -6 -5 -4 -3 -2 -1 0 1 2 3 4 5 6 7 8

1997 2014

90

100

110

120

-9 -8 -7 -6 -5 -4 -3 -2 -1 0 1 2 3 4 5 6 7 8

1997 2014

Japan Consumption Behavior In Line With 1997

1. Index rebased to 100 in July of previous year Source: Pavilion Global Markets; June 2014

Japan’s Sales Tax Increase: Then (1997) vs. Now (2014)

10

Index

101

97

Months from consumption tax hikeMonths from consumption tax hike

YoY % Change

Japan Post Tax-Hike Recovery Faster Than 1997

Japan Department Store Sales Japan Retail Sales Index1

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

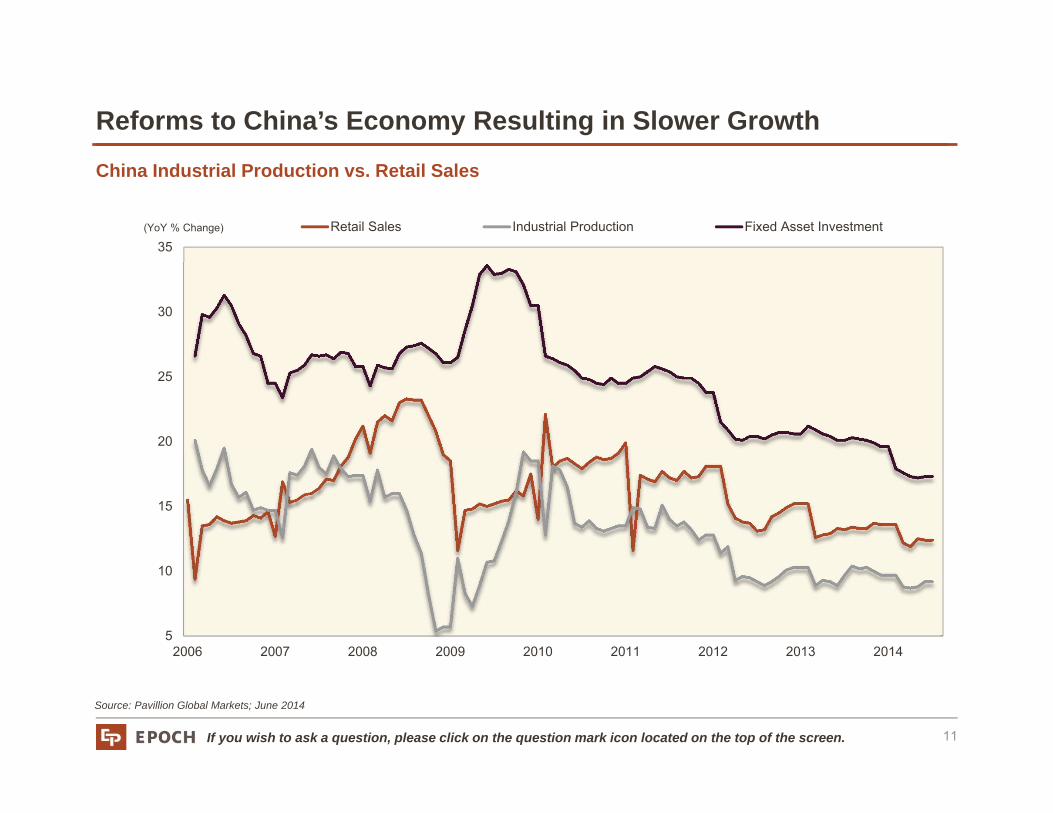

5

10

15

20

25

30

35

2006 2007 2008 2009 2010 2011 2012 2013 2014

Retail Sales Industrial Production Fixed Asset Investment

China Industrial Production vs. Retail Sales

Source: Pavillion Global Markets; June 2014

Reforms to China’s Economy Resulting in Slower Growth

11

(YoY % Change)

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

European Research Trip: Josepha Kaufman

12

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

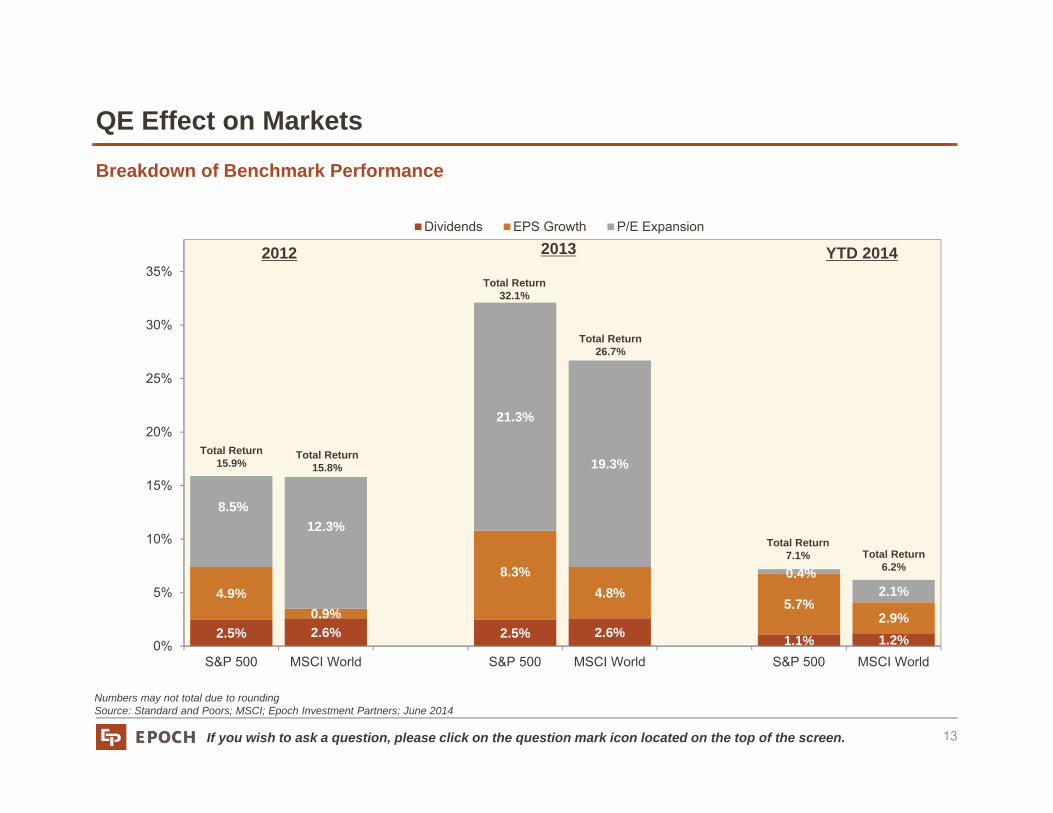

2.5% 2.6% 2.5% 2.6% 1.1% 1.2%

4.9%0.9%

8.3%4.8%

5.7%2.9%

8.5%12.3%

21.3%

19.3%

0.4%2.1%

0%

5%

10%

15%

20%

25%

30%

35%

S&P 500 MSCI World S&P 500 MSCI World S&P 500 MSCI World

Dividends EPS Growth P/E Expansion

Breakdown of Benchmark Performance

Numbers may not total due to roundingSource: Standard and Poors; MSCI; Epoch Investment Partners; June 2014

QE Effect on Markets

13

2012 YTD 20142013

Total Return15.9%

Total Return15.8%

Total Return32.1%

Total Return26.7%

Total Return7.1% Total Return

6.2%

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

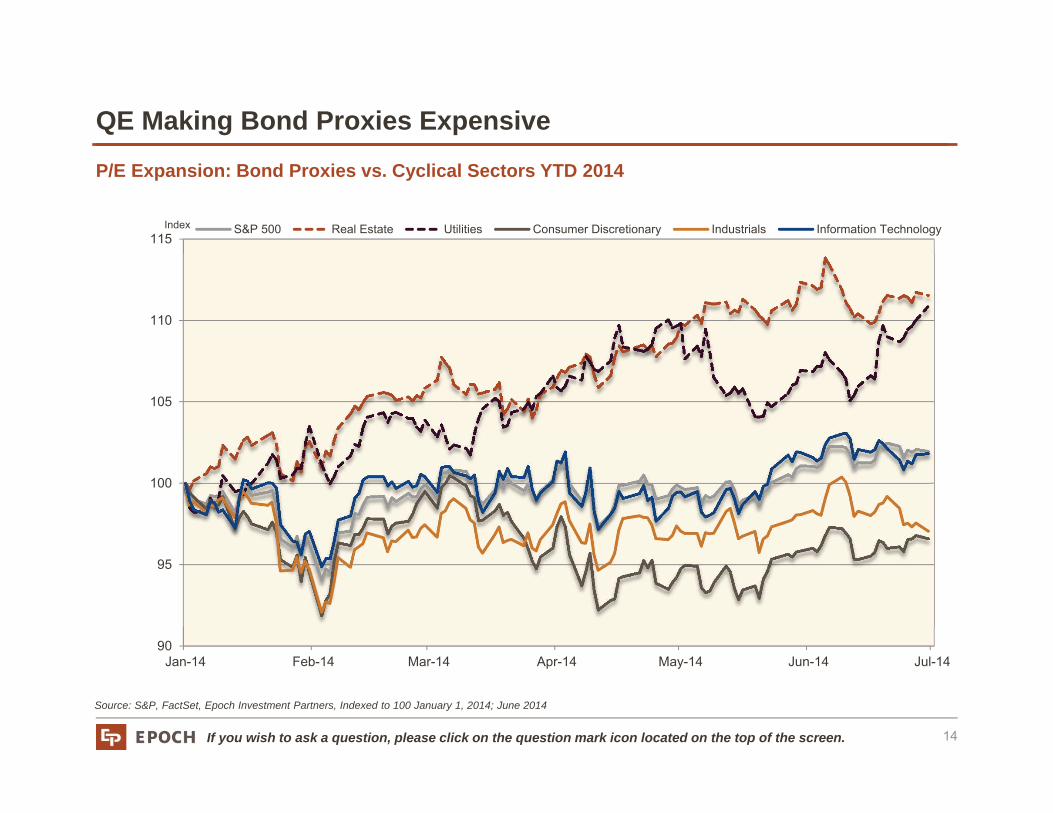

P/E Expansion: Bond Proxies vs. Cyclical Sectors YTD 2014

Source: S&P, FactSet, Epoch Investment Partners, Indexed to 100 January 1, 2014; June 2014

QE Making Bond Proxies Expensive

14

90

95

100

105

110

115

Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14

S&P 500 Real Estate Utilities Consumer Discretionary Industrials Information TechnologyIndex

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

58

59

60

61

62

63

64

65

66

67

68

1948 1958 1968 1978 1988 1998 2008

Workforce as a Percent of Working Age Population

Participation Rate Assuming No Change In Age Participation from 2004-2005 Average

U.S. Labor Participation Rate

Source: Bureau of Labor Statistics, Epoch Investment Partners; June 2014

Much of the Decline in the Participation Rate is Structural

15

(%)

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

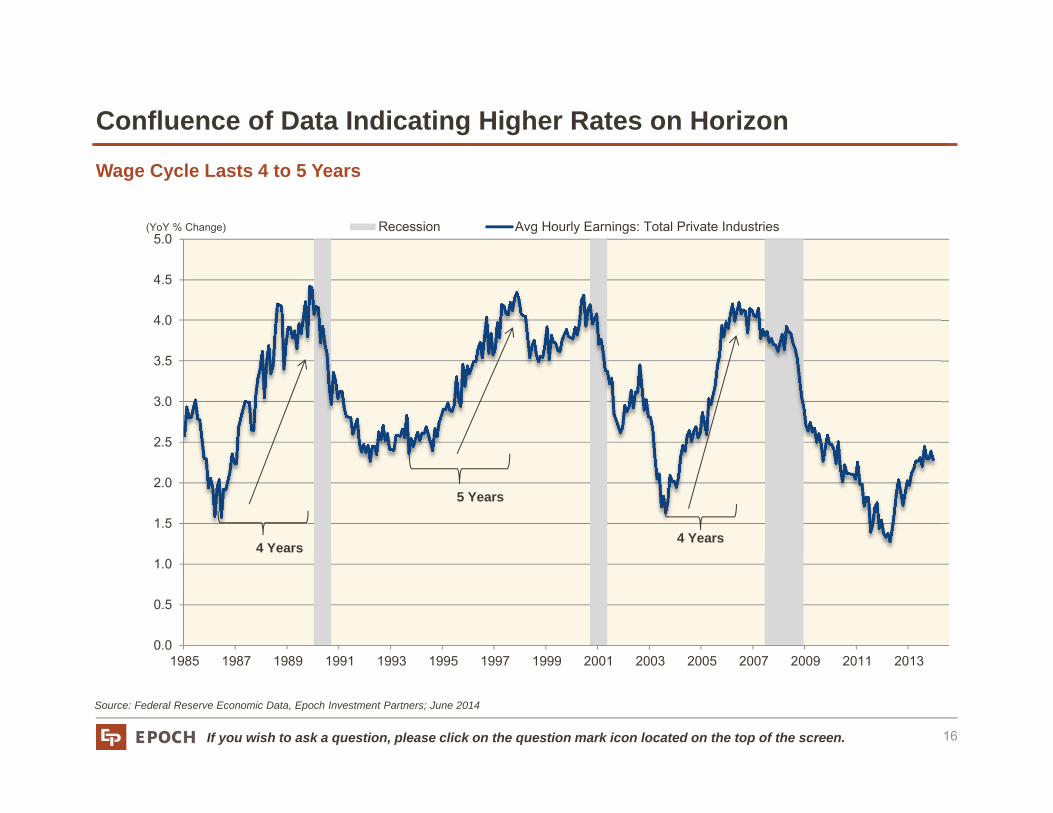

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Recession Avg Hourly Earnings: Total Private Industries

Wage Cycle Lasts 4 to 5 Years

Source: Federal Reserve Economic Data, Epoch Investment Partners; June 2014

Confluence of Data Indicating Higher Rates on Horizon

16

(YoY % Change)

4 Years

5 Years

4 Years

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

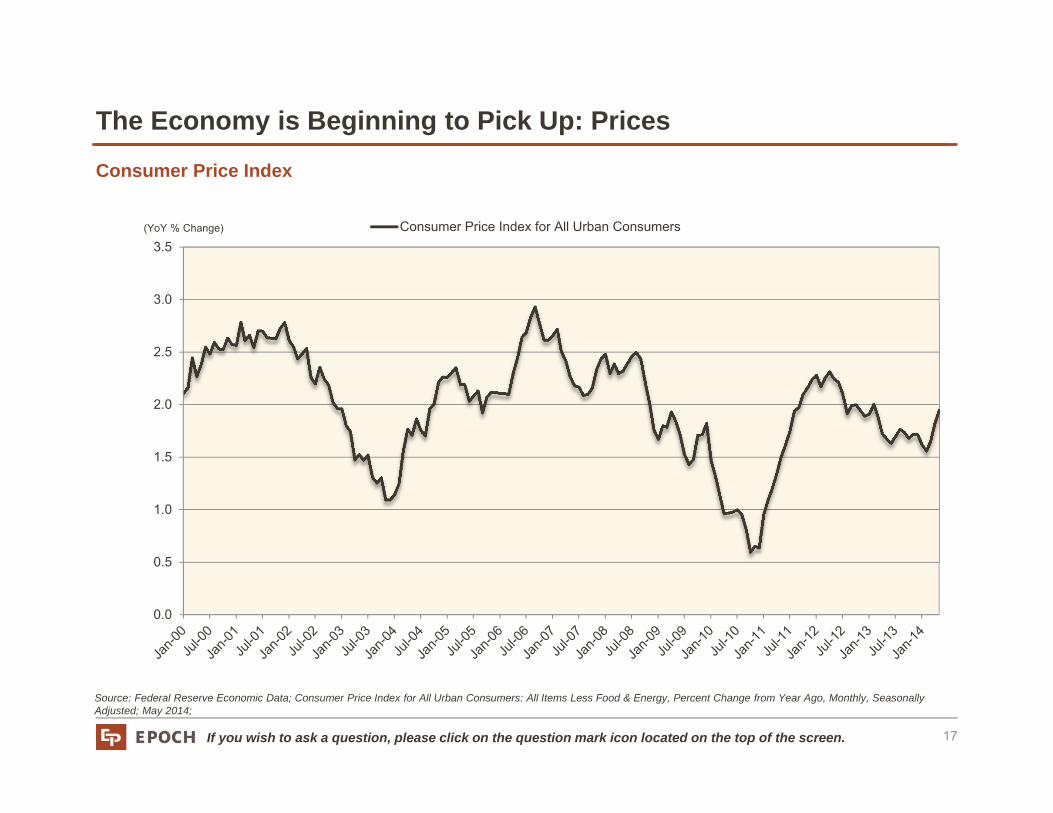

Consumer Price Index

Source: Federal Reserve Economic Data; Consumer Price Index for All Urban Consumers: All Items Less Food & Energy, Percent Change from Year Ago, Monthly, Seasonally Adjusted; May 2014;

The Economy is Beginning to Pick Up: Prices

17

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5Consumer Price Index for All Urban Consumers(YoY % Change)

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

1.0

1.5

2.0

2.5

3.0

3.5

4.0(%)

Sequence of the Tightening Thresholds on 10-year U.S. Yields

Source: Exane BNP Paribas, U.S. Treasury; June 2014

When Rates Rise, They Tend To Do So Quickly

18

1st Upward PhaseTrigger: Mention of reducing QE

2nd Upward PhaseTrigger: Coming end QE

3rd Upward PhasePotential Trigger: Rate hikes

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

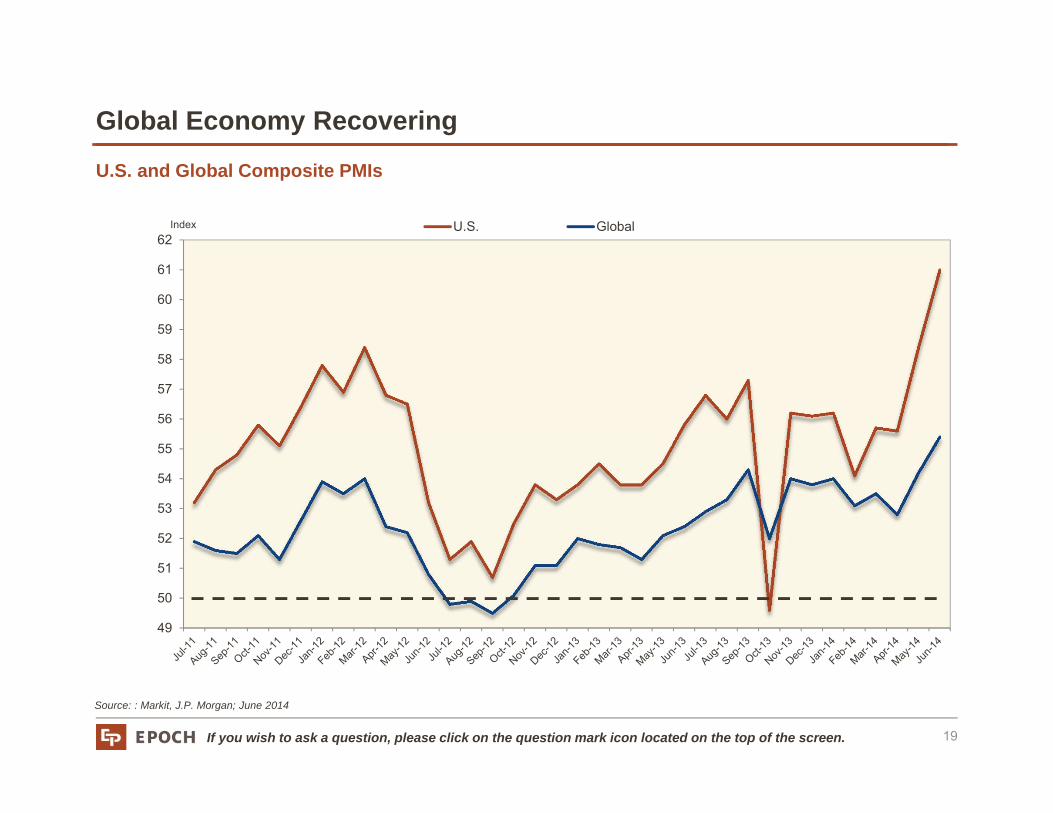

U.S. and Global Composite PMIs

Source: : Markit, J.P. Morgan; June 2014

Global Economy Recovering

19

49

50

51

52

53

54

55

56

57

58

59

60

61

62U.S. GlobalIndex

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

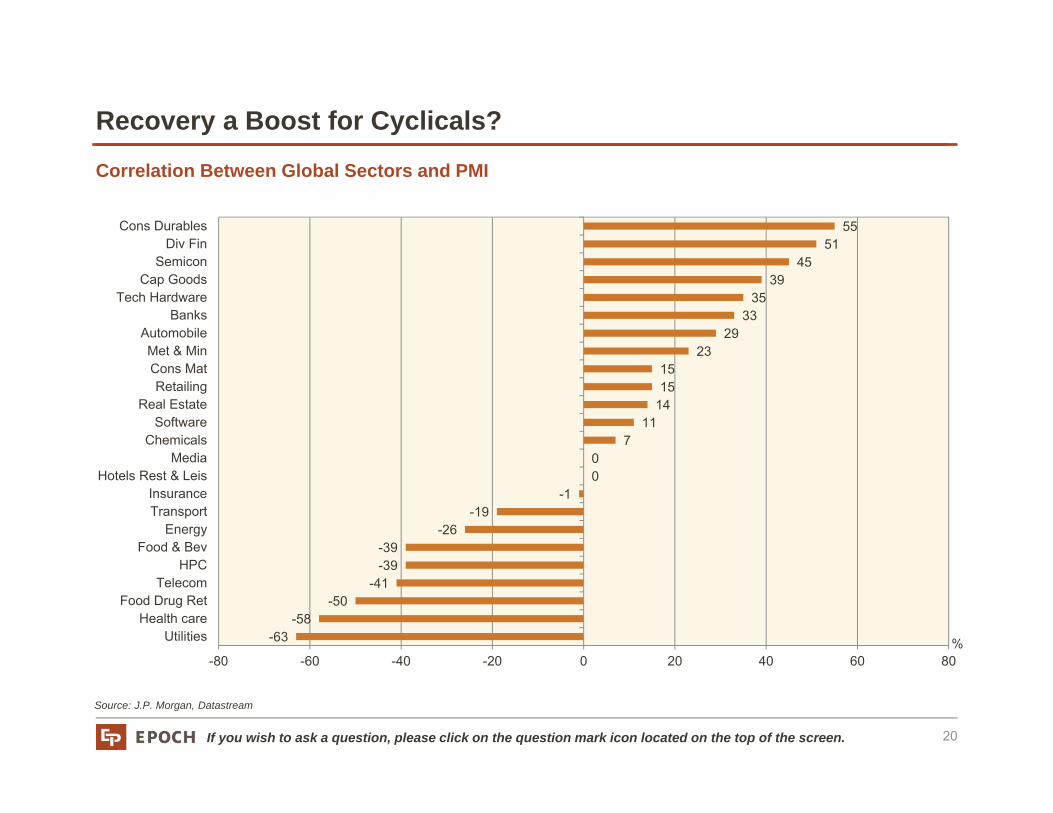

Correlation Between Global Sectors and PMI

Source: J.P. Morgan, Datastream

Recovery a Boost for Cyclicals?

20

-63-58

-50-41

-39-39

-26-19

-100

711

141515

2329

3335

3945

5155

-80 -60 -40 -20 0 20 40 60 80

UtilitiesHealth care

Food Drug RetTelecom

HPCFood & Bev

EnergyTransportInsurance

Hotels Rest & LeisMedia

ChemicalsSoftware

Real EstateRetailing

Cons MatMet & Min

AutomobileBanks

Tech HardwareCap Goods

SemiconDiv Fin

Cons Durables

%

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

Summary

Global Growth Expectations

• Financial health of most economies improving modestly

• Positive growth exists, but still below long-run trend rate

• Geopolitical risk an increasing concern

Effects of Monetary

Policy

• Central banks at different stages in policy cycle

• Growth still not self-sustaining in several regions

Sustainability of Recovery in Euro Zone

and Japan

• Deflation remains a threat in Europe

• Japan experiment continues

China and Emerging Markets

• Structural changes in China continue to be a drag

• Emerging markets continue to be adversely effected by the credit slowdown

U.S. Market Environment

• U.S. economy picking up steam

• Rising wages may foreshadow a rise in rates

• Cyclical sectors look attractive in this environment

As of June 30, 2014

21

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

A replay of this presentation will be available shortly on our website www.eipny.com

Please feel free to contact us at 212-303-7200

Question & Answer Section

22