Presentation to American Australian Association

26

Presentation to American Australian Association New York 10 June 2002 John McFarlane, Chief Executive Officer Australia and New Zealand Banking Group Limited

Transcript of Presentation to American Australian Association

Presentation to American Australian Association

New York10 June 2002

John McFarlane, Chief Executive OfficerAustralia and New Zealand Banking Group Limited

Page 2

AgendaAgenda

1. The Australian economy – from boom/bust to a moreresilient foundation.

2. The emergence of financial services as a cornerstoneof the economy

3. Culture and intangible factors increasingly drivingvalue creation

Page 3

0.0

1.0

2.0

3.0

4.0

5.0

6.0

1950s 1960s 1970s 1980s 1990s

Australia Rest of the OECD

% per annum

Australia’s apparently superior growth rate in the Australia’s apparently superior growth rate in the 1950s and 1960s was largely due to immigration1950s and 1960s was largely due to immigration

Real GDP growth

Source: GGDC Total Economy Database; Economics@ANZ.

Population growth

0.0

0.5

1.0

1.5

2.0

2.5

1950s 1960s 1970s 1980s 1990s

Australia Rest of the OECD

% per annum

Page 4

Australia ‘opted out’ of postAustralia ‘opted out’ of post--war war globalizationglobalization--led growth, until the midled growth, until the mid--1980s1980s

Exports as a share of GDP

Sources: Angus Maddison, Monitoring the World Economy 1820-1992 (OECD); IMF, World EconomicOutlook database; ABS.

0

5

10

15

20

25

1870 1913 1929 1950 1973 1985 2000

Australia World

% of GDP

Page 5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

1950s 1960s 1970s 1980s 1990s

Australia US OECD average

% per annum

Only in the past 10 years has Australian per capita Only in the past 10 years has Australian per capita GDP grown faster than for the US and OECD as a GDP grown faster than for the US and OECD as a wholewhole

Per capita GDP growth

Source: GGDC Total Economy Database; Economics@ANZ.

Page 6

Australian productivity growth exceeded the OECD Australian productivity growth exceeded the OECD (and US) average in the 1990s(and US) average in the 1990s

Sources: Productivity Commission; GGDC Total Economy Database 2002.

Labour productivity growth

01122334455

1960-1973 1973-1990 1990-2001

Australia USA OECD

Average annual rate of growth, %

Page 7

The terms on which Australia trades with the world The terms on which Australia trades with the world have been improving since the midhave been improving since the mid--1980s1980s

Ratio of Australian export prices to import prices

Source: ABS.

85

95

105

115

125

135

145

61 66 71 76 81 86 91 96 01

1999-2000 = 100(4-qtr moving average)

Page 8

Australia’s export markets have changed Australia’s export markets have changed significantly over the last forty yearssignificantly over the last forty years

Share of exports -1960

Source: DFAT

Share of exports -2001

United Kingdom

Japan

FranceUnited StatesNew

Zealand

Other Other

New Zealand

United States

Japan

Korea

China

Page 9

0.0

2.0

4.0

6.0

8.0

10.0

12.0

1950s 1960s 1970s 1980s 1990s

Australia OECD

% per annum

Australia’s inflation rate has been lower than the Australia’s inflation rate has been lower than the OECD average for the first time since the 1960sOECD average for the first time since the 1960s

Inflation

Sources: Dresdner Bank; OECD; ABS. OECD excludes Turkey.

Page 10

-2

-1

0

1

2

3

4

5

6

7

91 93 95 97 99 01

% change from year earlier

US

Australia

After years of growing in sync, the US and After years of growing in sync, the US and Australian economies have diverged recently Australian economies have diverged recently

Sources: Datastream

Real GDP growth

Page 11

-2

-1

0

1

2

3

4

5

6

7

96 97 98 99 00 01 02 03

% change from year earlier

GDP

NZ has also weathered the tougher international environment well and is well positioned for continued reasonable growth

NZ real GDP growth

Sources: Statistics NZ; NZ Economics@ANZ

l NZ has also experienced a strong upswing in housing activity in response to last year’s interest rate reductions and a striking turn-around in net immigration (also supporting consumer spending)

l The stronger NZ$ and lower agricultural commodity prices (especially for dairy products) will result in a fall in export incomes this year

l Lower rural incomes, higher interest rates and, eventually, some tapering off in net immigration will lead to softer growth in domestic spending

l Overall growth is expected to slow from 3½% in 2002 to 2¾% in 2003

Page 12

0

1

2

3

4

5

6

7

96 97 98 99 00 01 02 03

% change from year earlier

GDP

GDP excl. housing

Source: ABS Cat. 5206.0, ANZ

The sources of growth in the Australian economy The sources of growth in the Australian economy are likely to change over the next twelve months are likely to change over the next twelve months

Australian economic growth

Page 13

-100

0

100

200

300

400

92 94 96 98 00 02

A weak US dollar and wider interest differentials A weak US dollar and wider interest differentials have supported the Australian dollarhave supported the Australian dollar

Interest rate spread

Source: Datastream; Reserve Bank; Economics@ANZ.

A$ vs US$

40

45

50

55

60

65

70

75

80

85

92 94 96 98 00 02

US centsbasis points

Difference betweenUS and Aus 3minterest rates

Page 14

Financial services play an increasingly Financial services play an increasingly important role in the Australian marketimportant role in the Australian market

BHP

NAB

CRA

NewsCorp

Coles Myer

BTR Nylex

Western Mining

Pacific Dunlop

Westpac

Fosters

22.98

9.92

8.70

8.20

7.02

6.51

5.06

4.88

4.61

4.50

12.3%

5.3%

4.6%

4.4%

3.7%

3.5%

2.7%

2.6%

2.5%

2.4%

NAB

NewsCorp

CBA

BHP

ANZ

Telstra

Westpac

AMP

RIO

Woolworths

56.79

49.33

42.65

38.50

29.73

29.21

28.98

19.08

17.49

13.78

14.20

12.47

10.47

9.55

7.42

7.37

7.13

4.71

4.28

3.45

Market Cap $b

Market Cap $b

% of index

% of index

1992 2002

1992 ANZ - $4.4b & 2.3%

1

2

3

4

5

6

7

8

9

10

1

2

3

4

5

6

7

8

9

10

Page 15

Australian banks are well placed in the Australian banks are well placed in the second tier of global bankssecond tier of global banks

0

5

10

15

20

25

30

35

NAB

Royal Ban

k Can

ada CB

A

Abbe

y Nation

al ANZ

WBC

Mellon

Finan

cial TD

Stand

ard Ch

artere

d CIBC

Bank of

Mon

treal

Market CapitalisationUSD $b

Page 16

Intangible factors are increasingly driving value Intangible factors are increasingly driving value creationcreation

Unique strategySustainable leadership

Growth opportunities

Return on equityCost of capital

Strong brand

Talented peopleVibrant culture

$4.98$7.21

$4.04

$12.68

$0

$5

$10

$15

$20

$25

1998 Today

$9.02

$19.89

Share price

Compound growth rate

33%

Compound growth rate

9%Intangible net assets per shareTangible net assets per share

Page 17

-1000

0

1000

2000

3000

4000

5000

6000

7000

8000

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 Mar-02* 0

200

400

600

800

1000

1200

Revenue (LHS)Expenses (LHS)Provisions (LHS)Profit (LHS)TSR (RHS)

ANZ Bank - repositioning, then new momentum

* Mar-02 annualised

$mValu

e of $

100 in

vested in

1992

Page 18

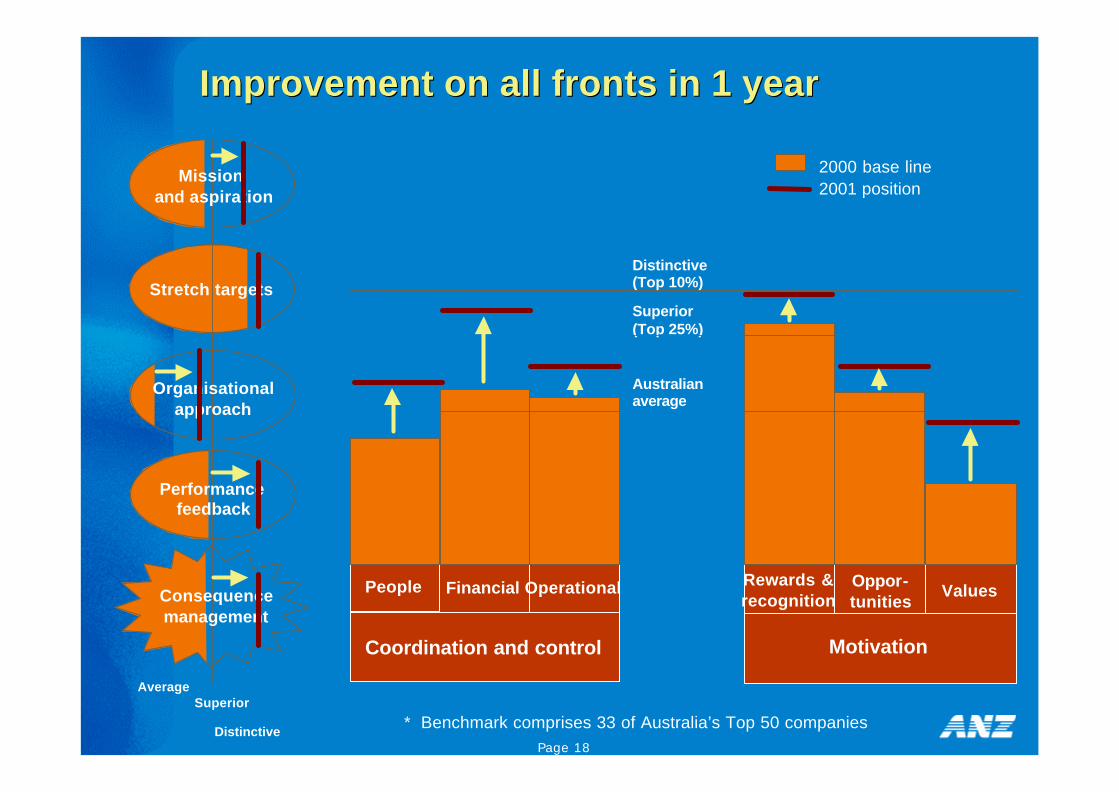

Improvement on all fronts in 1 yearImprovement on all fronts in 1 year

AverageSuperior

Distinctive* Benchmark comprises 33 of Australia’s Top 50 companies

Coordination and control

Financial OperationalPeople

Distinctive (Top 10%)

Superior (Top 25%)

Australian average

Motivation

Rewards &recognition

Oppor-tunities

Values

2000 base line2001 position

Stretch targets

Consequencemanagement

Missionand aspiration

Organisationalapproach

Performance feedback

Page 19

Our culture is changing dramatically Our culture is changing dramatically --improvement in ANZ Valuesimprovement in ANZ Values

InAccountabilityAchievementCustomer focusContinuous improvement

OutBureaucracyHierarchyControlShort-term focus

Cost reductionShareholder valueResults drivenProfitLow riskGoals orientation

Maintained

Page 20

Our people are engagedOur people are engaged

0

10

20

30

40

50

60

70

80

Overall satisfaction with ANZ Recommend ANZ as a place to work

1999 2000

2001 2002

Staff satisfaction survey

Page 21

AAllll stakeholders key to value creationstakeholders key to value creation

Shareholders

• EPS double-digit

• Cost-Income mid 40’s

• ROE above 20%

• Intangible value

• Distinctive disclosure

Customers

• Restoring customer faith

• Simplified accounts and fees

• Ten charter promises

Community

• Maintaining rural branches

• Seniors and welfare banking

• ANZ Community Fund

Our People

• Performance ethic

• Breakout transformation

• Freedom with accountability

• Stretch incentives

Page 22

Copy of presentation available on

www.anz.com

Page 23

The material in this presentation is general background information about the Bank’s activities current at the date of the presentation. It is information given in summary form and does not purport to be complete. It is not intended to be relied upon as

advice to investors or potential investors and does not take into account the investment objectives, financial situation or needs of any particular investor. These

should be considered, with or without professional advice when deciding if an investment is appropriate.

For further information visit

www.anz.comor contact

Philip GentryHead of Investor Relations

ph: (613) 9273 4185 fax: (613) 9273 4091 e-mail: [email protected]

Page 24

PE Ratio

0

5

10

15

20

25

30

35

1993 1994 1995 1996 1997 1998 1999 2000 2001 Mar-02

Asian crisis and emerging market losses – damaged confidence in ANZ

Page 25

PE Ratio

0

2

4

6

8

10

12

14

16

18

May

-94

May

-95

May

-96

May

-97

May

-98

May

-99

May

-00

May

-01

May

-02

ANZ

Average

PE Ratio

0

5

10

15

20

25

May

-94

May

-95

May

-96

May

-97

May

-98

May

-99

May

-00

May

-01

May

-02

Share PricePE Ratio $ AUD

Page 26

Comparative PE ratios

10

11

12

13

14

15

16

17

AN

Z

Aust

ralia UK

Can

ada

US

Reg

ional

s

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

10

11

12

13

14

15

16

17

AN

Z

Aust

ralia UK

Can

ada

US

Reg

ional

s

Current year PE’s Prospective PE’s

Dividend yield

Source – JB Were 3 June 2002