PRESENTATION MYTIL JUNE 2010 AGII eng ... - mytilineos.gr · 165,300 0 100,000 200,000 300,000...

25

Group Presentation Association of Greek Institutional Investors June 2010

Transcript of PRESENTATION MYTIL JUNE 2010 AGII eng ... - mytilineos.gr · 165,300 0 100,000 200,000 300,000...

Group Presentation

Association of Greek Institutional InvestorsJune 2010

2

DISCLAIMER

These preliminary materials and any accompanying oral presentation (together, the “Materials”) have been prepared by Mytilineos Holdings SA (the “Company”) and are intended solely for the information of the Recipient. The Materials are in draft form and the analyses and conclusions contained in the Materials are preliminary in nature and subject to further investigation and analysis. The Materials are not intended to provide any definitive advice or opinion of any kind and the Materials should not be relied on for any purpose. The Materials may not be reproduced, in whole or in part, nor summarised, excerpted from, quoted or otherwise publicly referred to, nor discussed with or disclosed to anyone else without the prior written consent of the Company.

The Company has not verified any of the information provided to it for the purpose of preparing the Materials and no representation or warranty, express or implied, is made and no responsibility is or will be accepted by the Company as to or in relation to the accuracy, reliability or completeness of any such information. The conclusions contained in the Materials constitute the Company’s preliminary views as of the date of the Materials and are based solely on the information received by it up to the date hereof. The information included in this document may be subject to change and the Company has no obligation to update any information given in this report. The Recipient will be solely responsible for conducting its own assessment of the information set out in the Materials and for the underlying business decision to effect any transaction recommended by, or arising out of, the Materials. The Company has not had made an independent evaluation or appraisal of the shares, assets or liabilities (contingent or otherwise) of the Company .

All projections and forecasts in the Materials are preliminary illustrative exercises using the assumptions described herein, which assumptions may or may not prove to be correct. The actual outcome may be materially affected by changes in economic and other circumstances which cannot be foreseen. No representation or warranty is made that any estimate contained herein will be achieved.

3

Group Overview

Financial Review

Areas of ActivityMetallurgy & Mining EnergyEngineering Procurement Construction (EPC)

Stock Data

Summary

AGENDA

4

Group Overview

5

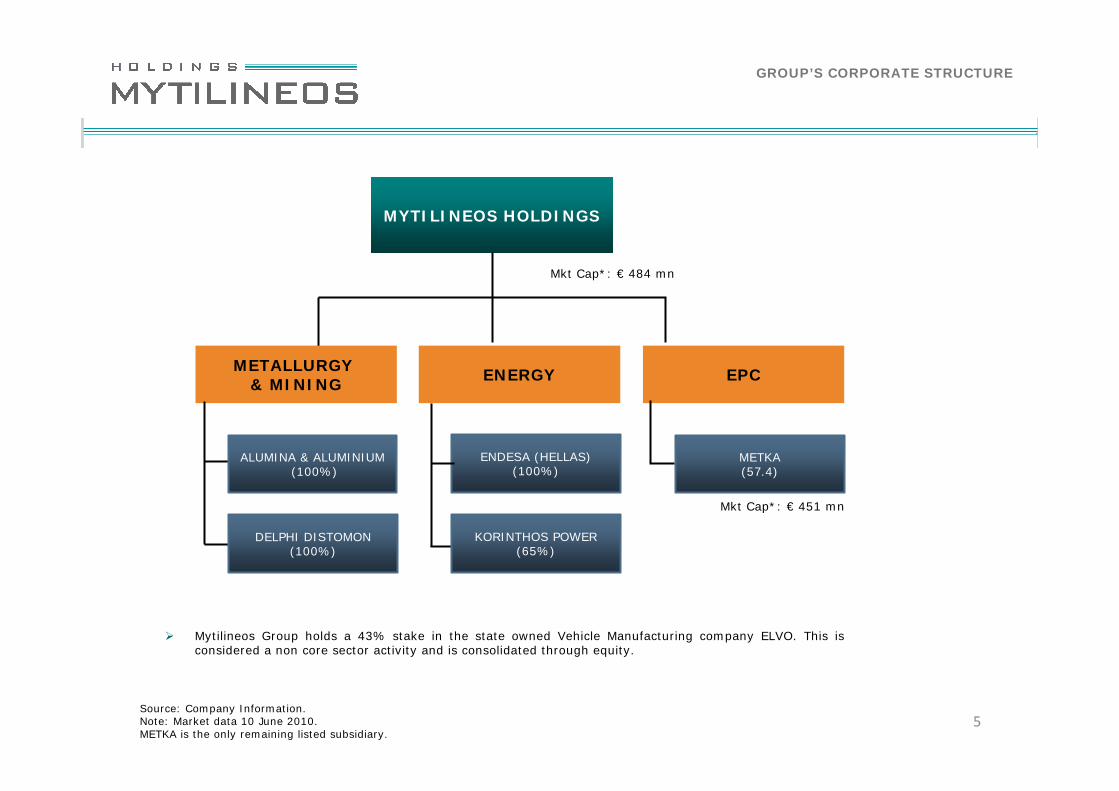

GROUP’S CORPORATE STRUCTURE

Source: Company Information.Note: Market data 10 June 2010.METKA is the only remaining listed subsidiary.

MYTILINEOS HOLDINGS

METKA(57.4)

ALUMINA & ALUMINIUM(100%)

METALLURGY & MINING

ENERGY EPC

ENDESA (HELLAS) (100%)

DELPHI DISTOMON (100%)

Mkt Cap*: € 484 mn

Mkt Cap*: € 451 mn

KORINTHOS POWER (65%)

Mytilineos Group holds a 43% stake in the state owned Vehicle Manufacturing company ELVO. This is considered a non core sector activity and is consolidated through equity.

6

Financial Review

7

Balance Sheet FY09 FY08

Non Current Assets 1,135 902

Current Assets 853 868

Total Assets 1,989 1,770

Debt 650 411

Cash Position 219 44

Marketable Securities 58 42

Equity 764 901

Adj. Equity 896 943

Net Debt 431 367

Adj. Net Debt 373 325

837

913 929

662

154110 119

747

311

18715842

20

256

157211

29 20

22.3%

18.0%

13.5%

21.2%

16.9%

11.8%

0

100

200

300

400

500

600

700

800

900

1,000

2004 2005 2006 2007 2008 20090.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Turnover EBITDA EAT EBITDA%

FINANCIAL REVIEW

Financial Performance

Source: Company Information.

2010 Key Performance Drivers:

Metal and Currency hedges boost top line and profitability.

Favorable $ and commodities prices.

Strong Growth from the EPC sector.

Liberalization of Natural Gas Market (including LNG).

Higher Electricity Pool Prices since the onset of the financial crisis in 2008.

8

Areas of Activity

Metallurgy & Mining

9

M & M – BUSINESS OUTLOOK

Entire complex acquired from Alcan in 2004. Leading industrial producer of alumina and aluminium in South Eastern Europe.

Production facilities occupy an area of 7,035,700m2 and constitute a vertically integrated production unit including bauxite mines, alumina refinery, smelter and self owned port facilities for large tonnage ships.

Low cost production base in Europe both for Alumina and Aluminium – below average global cost.

Enough alumina to cover own aluminium production needs and to export half a million tonnes per annum.

10-year export contract with Glencore AG regarding the majority of excess alumina production.

Steam is produced using Natural Gas by the 334 MW CHP Plant, 100% owned by Mytilineos Group.

Exploitation of bauxite reserves by the 100% owned subsidiary Delphes – Distomon S.A. covering more than half of its Bauxite requirements. Long term contracts with other suppliers (Alcan, S&B, Glencore AG).

Efficient risk management strategy. The Group acting proactively secured Aluminum sales in prices well above current market levels for 2009 and 2010.

Alumina & AluminumBusiness Overview Operational & Financial Overview

Key Strengths

Source: Company Information.

788,900 771,769718,797

164,500 168,000 162,339 134,738

780,000782,000

165,300

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

2005 2006 2007 2008 2009

tn OX AL

471429

73 49 6652 77 37 20 49

469382

471

79110

15.4%

10.4%

23.4%

20.7%

15.5%

0

50

100

150

200

250

300

350

400

450

500

2005 2006 2007 2008 2009

€ mil

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Turnover EBITDA EAT % EBITDA

10

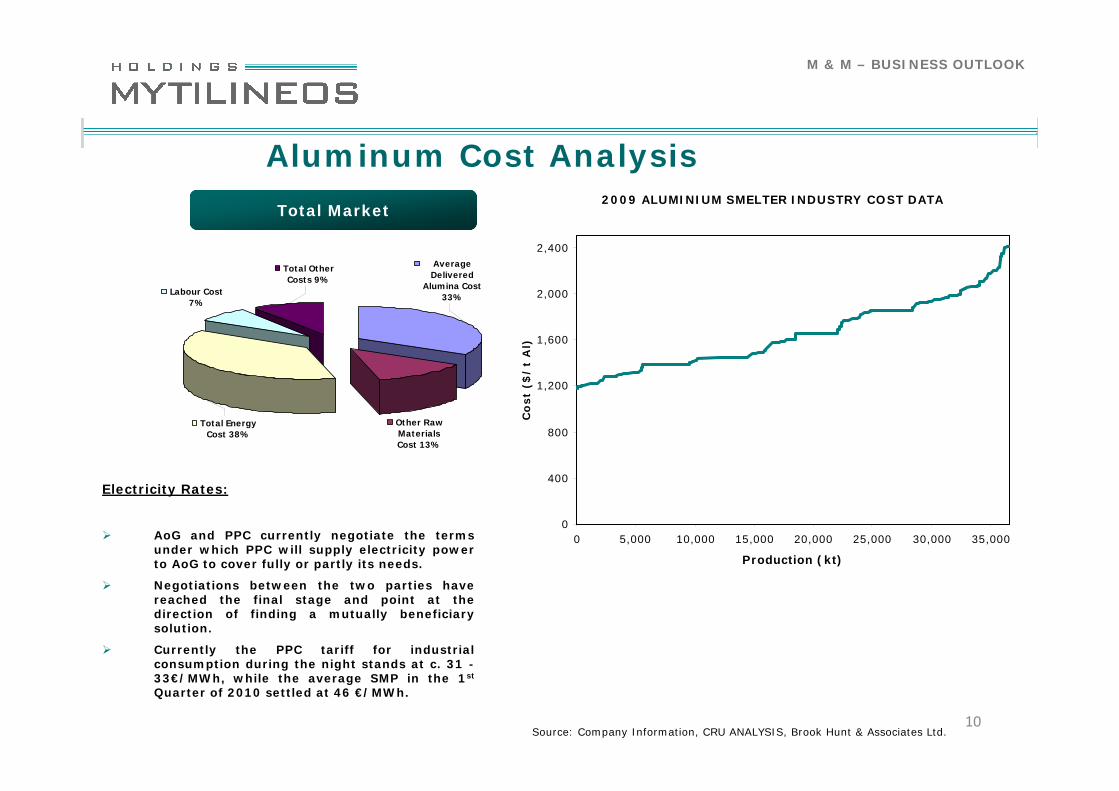

2009 ALUMINIUM SMELTER INDUSTRY COST DATA

0

400

800

1,200

1,600

2,000

2,400

0 5,000 10,000 15,000 20,000 25,000 30,000 35,000

Production (kt)

Co

st

($/

t A

l)

M & M – BUSINESS OUTLOOK

Source: Company Information, CRU ANALYSIS, Brook Hunt & Associates Ltd.

Aluminum Cost Analysis

Total Market

Other Raw Materials Cost 13%

Average Delivered

Alumina Cost 33%

Total Other Costs 9%

Labour Cost 7%

Total Energy Cost 38%

Electricity Rates:

AoG and PPC currently negotiate the terms under which PPC will supply electricity power to AoG to cover fully or partly its needs.

Negotiations between the two parties have reached the final stage and point at the direction of finding a mutually beneficiary solution.

Currently the PPC tariff for industrial consumption during the night stands at c. 31 -33€/MWh, while the average SMP in the 1st

Quarter of 2010 settled at 46 €/MWh.

11

Areas of Activity

Energy

12

Monthly SMP data 2008 – 2010 (EUR)

0

10

20

30

40

50

60

70

80

90

100

110

January

FebruaryMarch April May

June JulyAugust

SeptemberOctob

er

November

December

2008 2009 2010

Source: Company Information, HTSO.

ENERGY - INDUSTRY & MACRO ENVIRONMENT

Electricity Market:

The Greek electricity market (Demand peak c. 10 GW) is under liberalization. Most of the existing capacity is old and inefficient, underlining the need for new capacity and replacements.

Dominant position of PPC to be challenged by IPPs (MYTILINEOS- MOTOR OIL, TERNA - GDF, HELPE – EDISON).

Inefficient fuel supply-mix, over 60% derived from Lignite.

Expensive imports. During the summer the system realizes power shortages.

All the new conventional capacity up to 2014 will be based on Natural Gas. During 2010 IPPs are expected to launch 3 new CCGTs with total capacity of 1.3 GW.

Renewable generation is also set to rise as a very favorable framework has been put into place. Feed-in tariff for the energy and up to 40% subsidy for construction of wind and solar parks.

Natural Gas could become base load post 2013, when CO2 free allowances will be abolished.

AVG 2009: 47.4

AVG 2008: 87.2

13

Energy Market – Developments in 1Q 2010

Total Power demand during 1st Q 2010: 12.7 m MWh (down 3.3% y-o-y).

Lignite production decreased by 17.8% while Hydro production reached 2.6 m MWh (up 112.6% y-o-y).

Natural Gas production also increased at 2 m MWh (up 24.3% y-o-y).

Average SMP decreased at 46.1 €/MWh (down 18.3% y-o-y), however higher Oil prices are expected to put an upward

pressure on the SMP during the rest of the year.

The CHP plant, fully owned by Mytilineos Group, has already supplied the Grid with over 1.3 m MWh since April

2009 – full commercial operation of the plant is imminent and subject only to the completion of the new

electricity codes.

0

10

20

30

40

50

60

70

80

90

1 2 3 4 5

ENERGY - INDUSTRY & MACRO ENVIRONMENT

The Greek Electricity Market

Source: Company Information, HTSO.

Marg

inal

cost

(€

/M

Wh

)

Hydro, RES Lignite Gas CCGT Gas OCGT Fuel oil

Merit Order, 2010Power Production Mix

Total Production 2009: 48.5 m MWh

63.0%3.5%

19.4%

10.2%3.9%

LIGNITE OIL N.G. HYDRO RENEWABLES

1 4.2 9.5 11.8 13.112.3Installed capacity (in GW)

14

Source: Company Information(1) The CHP is under commissioning and commercial operations is expected

to commence as soon as the new electricity code is completed.

Group total installed capacity attributable to

thermal generation assets is expected to

reach c. 1.2GW by 2011

Mytilineos, expects to commission 2 thermal

power plants until 2011 (one in late 2010 and

one in mid 2011)

The Viotia CCGT is under construction, with the EPC c. 80% completed while construction for

the Korinthos Power CCGT started in

September 2009

Thermal Asset Summary

CHP 334MW 20101 Viotia 191 In operation

Korinthos Power 436.6MW August 2011 Korinthos 290

Viotia CCGT 444.4MW November 2010 Viotia 242Final Stage

of construction

RES Asset Summary

Operational

Gross MW

Attr. MW

Installation Licenses

Gross MW

Attr. MW

Production Licenses

Gross MW

Attr. MW

Applications

Gross MW

Attr. MW

Total

Gross MW

Attr. MW

Wind 35.60 32.23 11.50 5.64 166.40 122.45 1,124.90 1,053.17 1,338.40 1,213.49

Hydro 6.06 2.69 1.90 1.71 49.51 44.70 11.29 2.16 68.76 51.26

PV 0 0 0 0 0 0 30.60 27.72 30.60 27.72

Under construction

ENERGY - BUSINESS OUTLOOK

Installed capacity CommentsTotal capex

(Eur mn)LocationCommercial

operation

15Source: Company Information, Bloomberg, Credit Suisse.

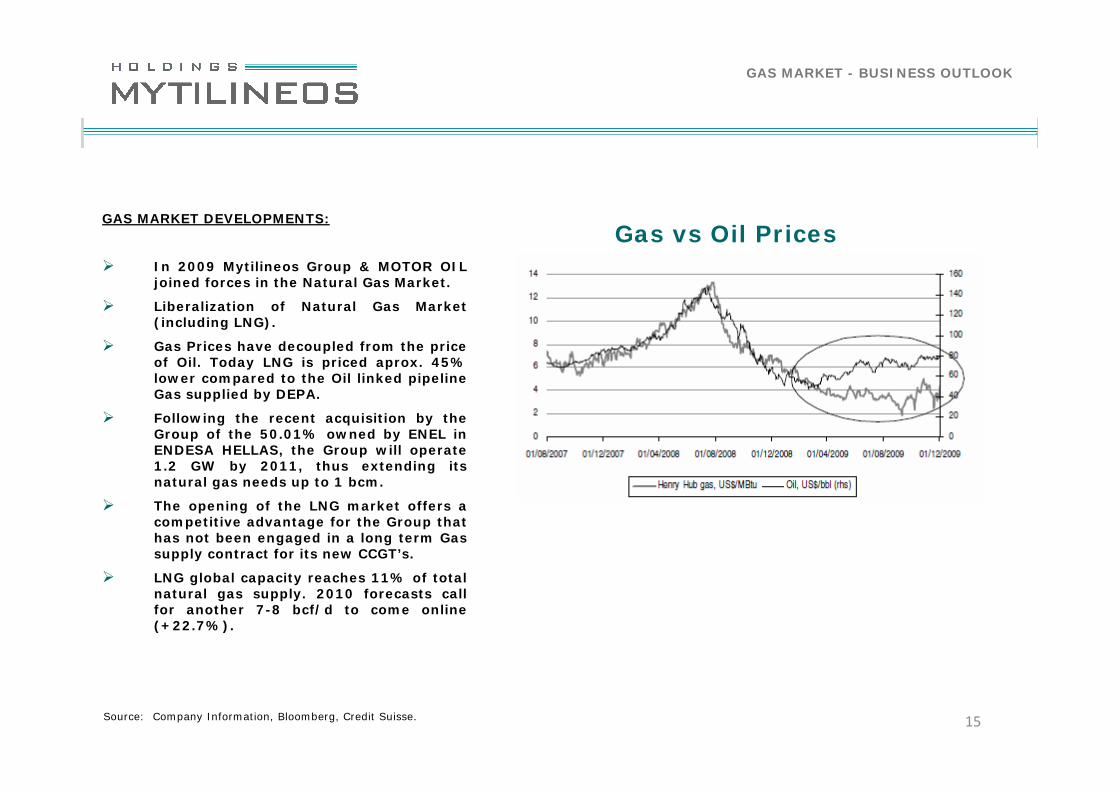

GAS MARKET - BUSINESS OUTLOOK

Gas vs Oil PricesGAS MARKET DEVELOPMENTS:

In 2009 Mytilineos Group & MOTOR OIL joined forces in the Natural Gas Market.

Liberalization of Natural Gas Market (including LNG).

Gas Prices have decoupled from the price of Oil. Today LNG is priced aprox. 45% lower compared to the Oil linked pipeline Gas supplied by DEPA.

Following the recent acquisition by the Group of the 50.01% owned by ENEL in ENDESA HELLAS, the Group will operate 1.2 GW by 2011, thus extending its natural gas needs up to 1 bcm.

The opening of the LNG market offers a competitive advantage for the Group that has not been engaged in a long term Gas supply contract for its new CCGT’s.

LNG global capacity reaches 11% of total natural gas supply. 2010 forecasts call for another 7-8 bcf/d to come online (+22.7%).

16

Areas of Activity

EPC

17

EPC – BUSINESS OUTLOOK

METKABusiness Overview Financial Overview

Key Strengths

• Significant international presence. World class manufacturing capability with high value-added profile.

• Strong demand from developing countries.

• Strong backlog currently at €2.0 bn – Earnings Visibility & Stability.

• High cash flow generation.

• Close ties with all world-class technology providers, including GE, Alstom, Siemens etc.

• Three state-of-the-art industrial facilities with 790 highly skilled and experienced personnel with excellent know-how.

Source: Company Information.

METKA S.A., 57.4% owned by Mytilineos Holdings, is a leading EPC Contractor with international profile.

Listed in the Athens Stock Exchange (ASE) since 1973.

METKA is involved in:

– Energy

» Complete power plants: engineering, procurement, construction (EPC) scope.

» EPC Contractor or consortium with technology suppliers.

– Infrastructure

» Focus on technically demanding infrastructure applications.

» Complex steel structures, mining & minerals, port equipment, refinery & petrochemical.

– Defence

» Manufacturing co-production with defence majors.

» Land defence systems. Major supplier of the Hellenic Armed Forces.

Turnover Analysis

212 196

297 283

48 61 5233 42 40 23 4

165

41270

50

100

150

200

250

300

350

2005 2006 2007 2008 2009

€ milEnergy Infrustructure Defence

284

381339

57 67 6137 41 37 45 37

225

295

54 61

17.9%17.5%

20.7%

24.0%

20.1%

0

50

100

150

200

250

300

350

400

450

2005 2006 2007 2008 2009

€ mil.

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

Turnover EBITDA EAT % EBITDA

18

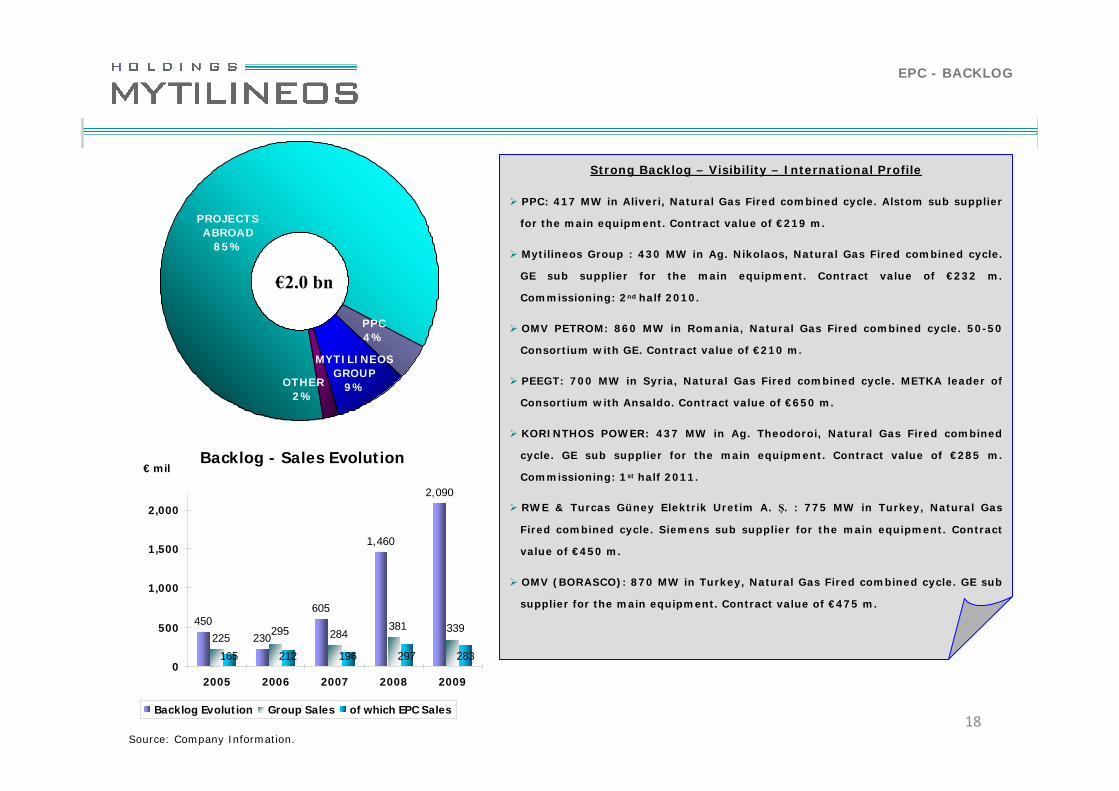

PPC4%

PROJECTS ABROAD

85%

OTHER2%

MYTILINEOS GROUP

9%

EPC - BACKLOG

Source: Company Information.

€2.0 bn

Strong Backlog – Visibility – International Profile

PPC: 417 MW in Aliveri, Natural Gas Fired combined cycle. Alstom sub supplier

for the main equipment. Contract value of €219 m.

Mytilineos Group : 430 MW in Ag. Nikolaos, Natural Gas Fired combined cycle.

GE sub supplier for the main equipment. Contract value of €232 m.

Commissioning: 2nd half 2010.

OMV PETROM: 860 MW in Romania, Natural Gas Fired combined cycle. 50-50

Consortium with GE. Contract value of €210 m.

PEEGT: 700 MW in Syria, Natural Gas Fired combined cycle. METKA leader of

Consortium with Ansaldo. Contract value of €650 m.

KORINTHOS POWER: 437 MW in Ag. Theodoroi, Natural Gas Fired combined

cycle. GE sub supplier for the main equipment. Contract value of €285 m.

Commissioning: 1st half 2011.

RWE & Turcas Güney Elektrik Uretim A. Ş. : 775 MW in Turkey, Natural Gas

Fired combined cycle. Siemens sub supplier for the main equipment. Contract

value of €450 m.

OMV (BORASCO): 870 MW in Turkey, Natural Gas Fired combined cycle. GE sub

supplier for the main equipment. Contract value of €475 m.

Backlog - Sales Evolution

230

605

1,460

2,090

165 212 196 297 283

450339381

284295225

0

500

1,000

1,500

2,000

2005 2006 2007 2008 2009

€ mil

Backlog Evolution Group Sales of which EPC Sales

19

METKA INVESTMENT CASE SUMMARY

Well positioned to benefit from the expansion in new very promising markets such as Turkey & the Middle East.

Strong Backlog - Highly visible cash flows over the next years.

International exposure – neutral investment case against the domestic environment.

The highest EBITDA margin against its peers.

Growth momentum - Sales expected to double over the next couple of years.

Quality Balance Sheet.

METKA Investment Highlights

Source: Company Information.

20

Stock Data

21

STOCK DATA – MYTILINEOS HOLDINGS S.A.

Share Price Information

Market Cap: € 484 mnAvg. Trading Value: € 1.5 mnTotal No of shares: 116,984,338Free Float: 61%Listing FTSE/ASE 20 FTSE

INTERNATIONAL, MSCI Small Cap and HSBC Small Cap

Notes: Data as of 10 June 2010.Source: Company Information.

Stock Symbols

ASE: MYTILReuters: MYTr.ATBloomberg: MYTIL GA

Shareholder Structure

Stock Performance

Mytilineos

Family 30.3% Retail 31.9%

Greek Institutional

Investors 11.4%

Foreign Institutional

Investors 17.5%

Treasury

Stock 8.9%

60

70

80

90

100

110

120

31/12/2009 30/1/2010 1/3/2010 31/3/2010 30/4/2010 30/5/2010

Mytilineos Group Athex Composite

22

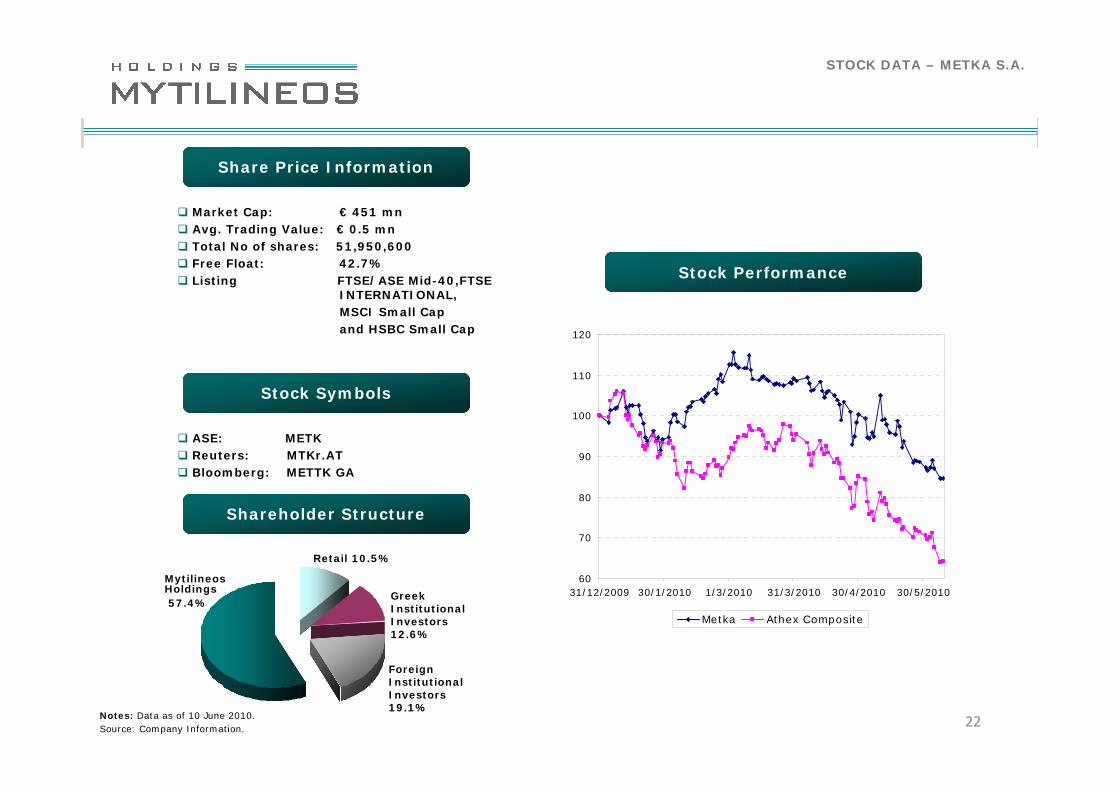

STOCK DATA – METKA S.A.

Share Price Information

Market Cap: € 451 mnAvg. Trading Value: € 0.5 mnTotal No of shares: 51,950,600Free Float: 42.7%Listing FTSE/ASE Mid-40,FTSE

INTERNATIONAL,MSCI Small Capand HSBC Small Cap

Stock Symbols

ASE: METKReuters: MTKr.ATBloomberg: METTK GA

Shareholder Structure

Mytilineos Holdings57.4%

Retail 10.5%

Greek Institutional Investors 12.6%

Foreign Institutional Investors 19.1%

Notes: Data as of 10 June 2010.Source: Company Information.

60

70

80

90

100

110

120

31/12/2009 30/1/2010 1/3/2010 31/3/2010 30/4/2010 30/5/2010

Metka Athex Composite

Stock Performance

23

Summary

24

SUMMARY

The Group is well placed to benefit from:

The liberalization of the domestic energy market.

The establishment of METKA as one of the most reliable EPC players in Europe.

The Recovery of Commodity Prices as the world economy improves.

Strong exposure abroad, neutralizing the impact of the adverse domestic economic environment.

Strong EPC business through METKA, which offers highly visible cash flows and is well positioned to benefit from the expansion in new very promising markets.

Fully Integrated model in Alumina - Aluminium business, self owned bauxite mines and the operation of the CHP plant offer solid control of the main cost parameters.

High Liquidity and secured funding for the execution of the Group’s demanding investment plan.

Effective risk management against FX and Commodities price fluctuations secures medium term profitability supporting also Cash flows.

Successful management’s track record in value creation through a series of value enhancing deals.

Investment Highlights

Source: Company Information.

25

CONTACT INFORMATION

Dimitris KatralisInvestor Relations DepartmentEmail:[email protected]: +30-210-6877476Fax: +30-210-6877400

Mytilineos Holdings S.A.5-7 Patroklou Str.15125 MaroussiAthensGreeceTel: +30-210-6877300Fax: +30-210-6877400

www.mytilineos.grwww.metka.gr