Prashant Bhadauiya Project Report

112

Summer training Report On “Recruitment of Financial Advisor at Met Life And Generating Business from Them” UNDER THE GUIDENCE OF SUBMIITED BY: Sudhir Kumar Prashant Singh Bhadauriya (sales manager) MBA 3 rd sem Roll no. 0909470066 GALGOITA INSTITUTE OF MANAGEMENTECHONOLOGY MAHAMAYA TECHNICAL UNIVERSITY

-

Upload

kalabala123 -

Category

Documents

-

view

221 -

download

0

Transcript of Prashant Bhadauiya Project Report

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 1/112

Summer training Report On

“Recruitment of Financial Advisor at Met Life

And Generating Business from Them”

UNDER THE GUIDENCE OF SUBMIITED BY:

Sudhir Kumar Prashant Singh Bhadauriya

(sales manager) MBA 3 rd sem

Roll no. 0909470066

GALGOITA INSTITUTE OF MANAGEMENTECHONOLOGY

MAHAMAYA TECHNICAL UNIVERSITY

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 2/112

DECLARATION

This project report has been undertaken as a fulfilment of the requirement for the award of the

degree of Master Business Administration of GIMT, Gr. NOIDA (UPTU).

This project report was executed during the summer training program of MBA program under

the supervision of Mr. SUDHIR KUMAR.

Further, we declare that this project is our original work and the analysis and finding are for

academic purpose only. This project has not been presented in any seminar elsewhere for the

award of any degree or diploma.

(Under the supervision ) (Submitted by )

Mr. Sudhir Kumar PRASHANT SINGH BHADAURIYA

Sales Manager MBA IIIrd sem.

MetLife Insurance Ltd.

Gr.Noida (U.P)

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 3/112

Acknowledgement

I acknowledge my indebtedness to all who generously helped by sharing their invaluable

experience with me, without which this project would have never been accomplished.

First and the foremost I convey my sincere thanks to Mr Sudhir Kumar under whose able

guidance this project could be accomplished. It was his perspective guidance, constant

encouragement and constructive criticism that was the guiding light during the entire tenure

of this project.

I thankful acknowledge the assistance provided by all the faculty members of GIMT,

Gr.Noida

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 4/112

PREFACE

The business of insurance is related to protection of economic value of assets. Every asset has

a value. In India insurance business is classified primarily as a life insurance or non-life or

general insurance.

In India insurance company MetLife insurance company ltd is one of the major private player

that commenced its.

In this project I was entrusted with the task of recruiting financial advisors for the company

and generating business from them.

The knowledge and the experience generated during the training has provided me with an

opportunity to provide some suggestions that would be of great help for the organisation and

would facilitate the growth.

Prashant Singh Bhadauriya

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 5/112

TABLE OF CONTENT

Introduction

Company Profile

Vision & Mission

Management team

Partners

Product Range

SWOT Analysis

Insurance Agency As A Career

Definition of an Agent

Authority of an Agent

Agent’s Regulation

Other intermediaries

Research Methodology

Study design

Sample size

Aim of the study

Objective of the study

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 6/112

Scope of the study

Data analysis

Recruitment of an advisor

Methods of remunerating Agents

Agency As Profession

Requirements for becoming an agent

Role of an Advisor

Introduction

Prerequisites for success

Importance of Advisor

Profile of an Advisor

Benefits and Support

Career Progression

Training of Advisor

Rewards and Recognition

Promotional strategies

Distribution and channel Management

Conclusion

Recommendations & suggestion

Limitation

Bibliography

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 7/112

Questionnaire

INTRODUCTION

THE HISTORY OF INDIAN INSURANCE INDUSTRY

The story of insurance is probably as old as the story of mankind. The same instinct that

prompts modern businessmen today to secure themselves against loss and disaster existed

in primitive men also. They too sought to avert the evil consequences of fire and flood and

loss of life and were willing to make some sort of sacrifice in order to achieve security.

Though the concept of insurance is largely a development of the recent past, particularly

after the industrial era –past few centuries yet its beginnings date back almost 6000 years.

Life Insurance

In 1818 the British established the first insurance company in India in Calcutta, the

Oriental Life Insurance Company . First attempts at regulation of the industry were made

with the introduction of the Indian Life Assurance Companies Act in 1912 . A number of

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 8/112

amendments to this Act were made until the Insurance Act was drawn up in 1938.

Noteworthy features in the Act were the power given to the Government to collect

statistical information about the insured and the high level of protection the Act gave to the

public through regulation and control. When the Act was changed in 1950, this meant far

reaching changes in the industry. The extra requirements included a statutory requirement

of a certain level of equity capital, a ceiling on share holdings in such companies to

prevent dominant control (to protect the public from any adversarial policies from one

single party), stricter control on investments and, generally, much tighter control. In 1956,

the market contained 154 Indian and 16 foreign life insurance companies. Business was

heavily concentrated in urban areas and targeted the higher echelons of society. “Unethical

practices adopted by some of the players against the interests of the consumers” then led

the Indian government to nationalize the industry. In September 1956, nationalization was

completed, merging all these companies into the so-called Life Insurance Corporation

(LIC). It was felt that “nationalization has lent the industry fairness, solidity, growth and

reach.”

Some of the important milestones in the life insurance business in India

are :

1912: The Indian Life Assurance Companies Act enacted as the first statute to regulate the

life insurance business.

1928: The Indian Insurance Companies Act enacted to enable the government to collect

statistical information about both life and non-life insurance businesses.

1938: Earlier legislation consolidated and amended to by the Insurance Act with the

objective of protecting the interests of the insuring public.

1956: The market contained 154 Indian and 16 foreign life insurance Companies

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 9/112

General Insurance

The General insurance business in India started with the establishment of Triton

Insurance Company Limited in 1850 at Calcutta. In 1907, the first company, The

Mercantile Insurance Ltd . was set up to transact all classes of general insurance business.

General Insurance Council, a wing of the Insurance Association of India in 1957, framed a

code of conduct for ensuring fair conduct

and sound business practices. In 1968 the Insurance Act was amended to regulate

investments and to set minimum solvency margins. In the same year the Tariff Advisory

Committee was also set up. In 1972, The General Insurance Business (Nationalization)

Act was passed to nationalize the general insurance business in India with effect from 1st

January 1973. For these 107 insurers was amalgamated and grouped into four company’s

viz., the National Insurance Company Ltd ., the New India Assurance Company Ltd ., the

Oriental Insurance Company Ltd ., and the United India Insurance Company Ltd .

General Insurance Corporation of India was incorporated as a company.

Some of the important milestones in the general insurance business in

India are :

1907: The Indian Mercantile Insurance Ltd . set up, the first company to transact all

classes of general insurance business.

1957: General Insurance Council , a wing of the Insurance Association of

India, frames a code of conduct for ensuring fair conduct and sound business practices.

1968: The Insurance Act amended to regulate investments and set minimum solvency

margins and the Tariff Advisory Committee set up.

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 10/112

1972: The General Insurance Business (Nationalization) Act, 1972 nationalize the general

insurance business in India with effect from 1st January 1973. 107 insurers amalgamated

and grouped into four companies viz. the National Insurance Company Ltd., the New

India Assurance Company Ltd., the Oriental Insurance Company Ltd. and the

United India Insurance Company Ltd . GIC incorporated as a company.

MAJOR POLICY CHANGES

Insurance sector has been opened up for competition from Indian private insurance

companies with the enactment of Insurance Regulatory and Development Authority Act,

1999 (IRDA Act). As per the provisions of IRDA Act, 1999, Insurance Regulatory and

Development Authority (IRDA) was established on 19th April 2000 to protect the interests

of holder of insurance policy and to regulate, promote and ensure orderly growth of the

insurance industry. IRDA Act 1999 paved the way for the entry of private players into the

insurance market which was hitherto the exclusive privilege of public sector insurance

companies/ corporations. Under the new dispensation Indian insurance companies in

private sector were permitted to operate in India with the following conditions: Company

is formed and registered under the Companies Act, 1956;The aggregate holdings of equity

shares by a foreign company, either by itself or through its subsidiary companies or its

nominees, do not exceed 26%, paid up equity capital of such Indian insurance company;

The company's sole purpose is to carry on life insurance business or general insurance

business or reinsurance business. The minimum paid up equity capital for life or general

insurance business is Rs.100crores.The minimum paid up equity capital for carrying on

reinsurance business has been prescribed as Rs.200crores.The Authority has notified 27

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 11/112

Regulations on various issues which include Registration of Insurers, Regulation on

insurance agents, Solvency Margin, Reinsurance, Obligation of Insurers to Rural and

Social sector, Investment and Accounting Procedure, Protection of policy holders' interest

etc. Applications were invited by the Authority with effect from 15th August, 2000 for

issue of the Certificate of Registration to both life and non-life insurers. The Authority has

its Head Quarter at Hyderabad .

Changing face of Indian insurance industry:

Indian life-insurance market is the target market of all the companies who either want to

extend or diversify their business. To tap the Indian market there has been tie-ups between

the major Indian companies with other International insurance companies to start up their

business. The government of India has set up rules that no foreign insurance company can

set up their business individually here and they have to tie up with an Indian company and

this foreign insurance company can have an investment of only 24% of the total start-up

investment. Indian insurance industry can be featured by:

· Low market penetration.

· Ever growing middle class component in population.

· Growth of customer’s interest with an increasing demand for better insurance products.

· Application of information technology for business.

· Rebate from government in the form of tax incentives to be insured. Today, the Indian

life insurance industry has a dozen private players, each of which are making strides in

raising awareness levels, introducing innovative products and increasing the penetration of

life insurance in the vastly underinsured country. Several of private insurers have

introduced attractive products to meet the needs of their target customers and in line with

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 12/112

their business objectives. The success of their effort is that they have captured over 28% of

premium income in five years. The biggest beneficiary of the competition among life

insurers has been the customer. A wide range of products, customer focused service and

professional advice has become the mainstay of the industry, and the Indian customer’s

forms the pivot of each company’s strategy. Penetration of life insurance is beginning to

cut across socio-economic classes and attract people who have never purchased insurance

before. Life insurance is also now being regarded as a versatile financial planning tool.

Apart from the traditional term and saving insurance policies, industry has seen the entry

and growth of unit linked products. This provides market linked returns and is among the

most flexible policies available today for investment. Now products are priced, flexible,

and realistic and sustain so people in better position to understand the risk and benefits of

the product and they are accepting these innovative products. So it is clear that the face of

life insurance in India is changing, but with the changes come a host of challenges and it is

only the credible players with a long term vision and a robust business strategy that will

survive.

Whatever the developments, the future and the opportunities in this industry will surely be

exciting.

Various types of life insurance policies:-

· Endowment policies: This type of policy covers risk for a specified period, and at the

end of the maturity sum assured is paid back to policyholder with the bonuses during the

term of the policy.

· Money back policies: This type of policy is for periodic payments of partial survival

benefits during the term of the policy as long as the policy holder is alive.

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 13/112

· Group insurance: This type of insurance offers life insurance protection under group

policies to various groups such as employers-employees, professionals, co-operatives etc it

also provides insurance coverage for people in certain approved occupations at the lowest

possible premium cost.

· Term life insurance policies: This type of insurance covers risk only during the selected

term period. If the policy holder survives the term, risk cover comes to an end. These types

of policies are for those people who are unable to pay larger premium required for

endowment and whole life policies. No surrender, loan or paid up values are in such

policies.

Whole life insurance policies: This type of policy runs as long as the policyholder is

alive and is covered for the entire life of the policyholder. In this policy the insured

amount and the bonus is payable only to nominee on the death of policy holder.

· Joint life insurance policies: These policies are similar to endowment policies in

maturity benefits and risk cover, but joint life policies cover two lives simultaneously such

as married couples. Sum assured is payable on the first death and again on the death of

survival during the term of the policy.

· Pension plan: a pension plan or annuity is an investment over a certain number of years

but does not provide any life insurance cover. It offers a guaranteed income either for a life

or certain period.

· Unit linked insurance plan: ULIP is a kind of insurance plan which provides life cover

as well as return on premium paid over a certain period of time. The investment is denoted

as units and represented by the value called as net asset value (NAV).

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 14/112

COMPANY PROFILE

70 million customers in MetLife India Insurance Company Limited (MetLife) is an affiliateof Met Life Inc. And was incorporated as a joint venture between MetLife International

Holdings, Inc., The Jammu and Kashmir Bank, M. Pallonji and Co. Private Limited, and

other private investors.

MetLife is one of the fastest growing life insurance companies in the country. It serves its

customers by offering a range of innovative products to individuals and group customers at

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 15/112

more than 600 locations through its bank partners and company-owned offices. MetLife has

More than 50,000 Financial Advisors, who help customers, achieve peace of mind across the

length and breadth of the country.

MetLife, Inc., through its affiliates, reaches more than The Americas, Asia Pacific and

Europe. Affiliated companies, outside of India, include the number one life insurer in the

United States (based on life insurance enforce), with over 140 years of experience and

relationships with more than 90of the top one hundred FORTUNE 500® companies.

The MetLife companies offer life insurance, annuities, automobile and home insurance, retail

banking and other financial services to individuals, as well as group insurance, reinsurance

and retirement and savings products and services to corporations and other institutions.

MetLife Inc .

Celebrating 140 years, MetLife, Inc. is a leading provider of insurance and financial services

with operations throughout the United States and the Latin America, Europe, and Asia Pacific

regions. Through its domestic and international subsidiaries and affiliates, MetLife, Inc.

reaches more than 70 million customers around the world and MetLife is the largest life

insurer in the United States (based on life insurance in-force).

The MetLife companies offer life insurance, annuities, auto and home insurance, retail

banking and other financial services to individuals, as well as group insurance and retirement

& savings products and services to corporations and other institutions .

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 16/112

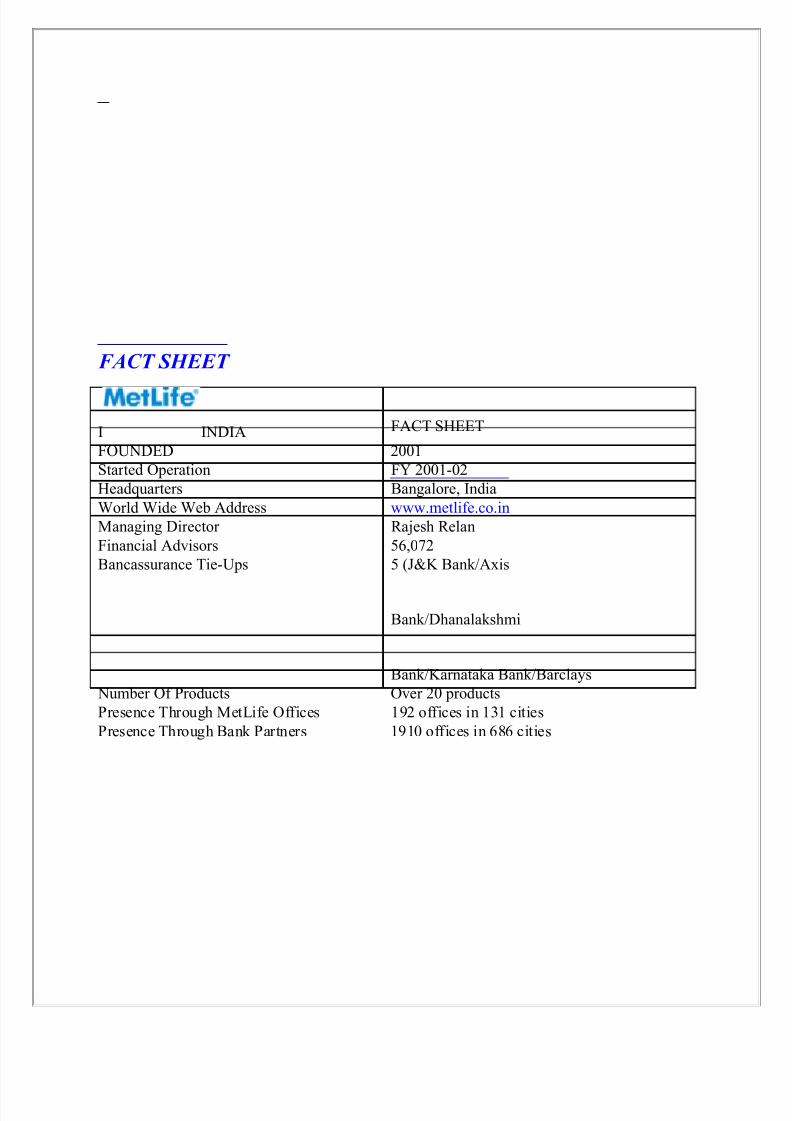

FACT SHEET

I INDIA FACT SHEET

FOUNDED 2001Started Operation FY 2001-02Headquarters Bangalore, IndiaWorld Wide Web Address www.metlife.co.inManaging Director Rajesh RelanFinancial Advisors 56,072Bancassurance Tie-Ups 5 (J&K Bank/Axis

Bank/Dhanalakshmi

Bank/Karnataka Bank/BarclaysNumber Of Products Over 20 productsPresence Through MetLife Offices 192 offices in 131 citiesPresence Through Bank Partners 1910 offices in 686 cities

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 17/112

"Coming into your own", are

performing as a Leader to be really

effective and successful by acting

and making decisions independently

to get results.

It's all about People, MetLife's

key resource. MetLife will

succeed because we are winningfrom within.

Functioning productively inteams towards a common

purpose; realizing the collective

power of diverse work-groups.

Operating with an intense

dedication to managing monetary

resources for strong business

results.

Conducting all business endeavors

with truth, sincerity and fairness.

Continuously creating and

introducing new and original

ideas and ways of doing things.

VISION & MISSION

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 18/112

Build financial freedom for all through leadership in providing financial advice and building

long-term relationships through innovative protection, accumulation and retirement products,

robust underwriting processes and creating world-class customer service experience for our

customers.

We want to provide customers in India with world-class solutions for financial security, and

in the process add significant value to our shareholders, associates and society.

Our Core Values

•

We lead through Innovation to offer world class and competitive products to

our customers.

We build Long Term Relationships with our customers by creating a world

class service experience through operational excellence and the innovative use

of technology.

We create a Customer Centered and Result Focused Vision that inspires each

one of our Associates and has their buy-in.

We are committed to creating a High Performance Organization by creating an

environment that allows each one of our Associates to perform at their peak.

As a result we will also be recognized as an Employer of Choice .

We are committed to Partnering with our internal and external Customers for

mutual success .

We work with Integrity, Fairness and Financial Prudence in all our dealings

keeping the interests of our Shareholders, Customers and Associates

paramount.

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 19/112

Management Team

Rajesh Relan

Managing Director

MSVS Phanesh

Appointed Actuary

Sameer Bansal

Director- Agency

Nitish Asthana

Director- Bancassurance & Business Partnerships

Joydeep Mukherji

Chief Financial Officer

Balachander Sekhar

Director – Marketing

KR Anil Kumar

Director - Legal & Risk and Company Secretary

P. S. Sankaran

Director – Compliance & Internal Controls

KS Raghavan

Chief Administrative Officer

Gaurav Sharma

Director - Customer Service and Operations

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 20/112

Preetinder Chadha

Deputy Director-Training

Kiran yadav

Deputy Director- Human Resources

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 21/112

PARTNERS

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 22/112

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 23/112

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 24/112

Corporate Social Responsibility:-

MetLife has always been committed to making a positive difference in the lives of the

individuals and communities. Today, that commitment drives volunteer work and

philanthropy across the globe. Working with non-profit organizations, MetLife supports

programs that provide young people with the skills they need to succeed in life and create

opportunities for people of all ages.

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 25/112

MetLife’s core values are personal responsibility, people count, partnership, integrity and

honesty, innovation and financial strength. These values also shape the responsibility to the

communities where the organization conducts its business.

Child Plan :-

Met Bhavishya

MetLife offers 'Met Bhavishya' - a guaranteed money back plan that pays out funds to help to

meet the education and career milestones of children. With this plan, the Life Insured is that

of the parent. The plan also has inbuilt guaranteed additions to add value to the policy over its

term.

There are two options to choose from and fixed term benefits, periodic additions & terminal

additions are payable based on the option that select. The policy is suitable for parents with

children between the ages 0-12 and parents in the age group of 20-50 years old.

Met Junior Endowment

MetLife offers 'Met Junior'- a flexible endowment plan that combines savings and security.

Children's well-being is our highest priority. So MetLife offer a plan which offers both timely

and efficient return on investment.

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 26/112

Met Junior - Non Par

On attaining maturity, the Person Insured will receive the Sum Assured.

Met Junior - Par

On attaining maturity, the Person Insured will receive the Sum Assured, the Reversionary

Bonus and the Terminal Bonus, if any.

Met Little Star

When child is born, a star is born in family. And, parents would like to provide their star with

all the building blocks that could develop his or her potential to the fullest. This could mean

special instruction sessions for talented children, unique training gear for exceptional athletes

or qualified training for born singers to provide that extra-edge.

To ensure this, parents would need an investment and protection package that is exclusively

designed to help you plan for financial security, no matter what uncertainties life brings.

'Met Little Star', a Unit-Linked, regular premium, child insurance plan helps parents do justthat. It secures finances for child's educational needs and ensures that plans go as planned, no

matter what the circumstances.

\Met Junior Money Back

MetLife offers 'Met Junior Money Back' - a money back plan that combines savings and

security. Child's well-being is our highest priority. So MetLife offer a money back plan which

provides guaranteed periodic survival benefits at the end of 5, 10 & 15 years, along with

guaranteed growth of savings.

A plan which offers both timely and efficient return on investment with payouts at different

milestones .

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 27/112

Survival Benefit

At the end of 5 years 20% of Sum Assured

At the end of 10 years 20% of Sum Assured

At the end of 15 years 20% of Sum Assured

Upon survival to maturity 40% of Sum Assured plus total Guaranteed

Additions

Met Magic

MetLife offers 'Met Magic', a Unit-Linked (non-medical, regular premium) life insurance

plan (Non Par).

Parents always want their little angel to have the best, in every sphere of life. You don't want

your child to have to compromise. No matter what the circumstances.

Met Magic, a unique life insurance plan, helps you secure the future of your loved one!

(IN THIS POLICY, THE INVESTMENT RISK IN INVESTMENT PORTFOLIO IS

BORNE BY THE POLICY HOLDER )

Retirement :-

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 28/112

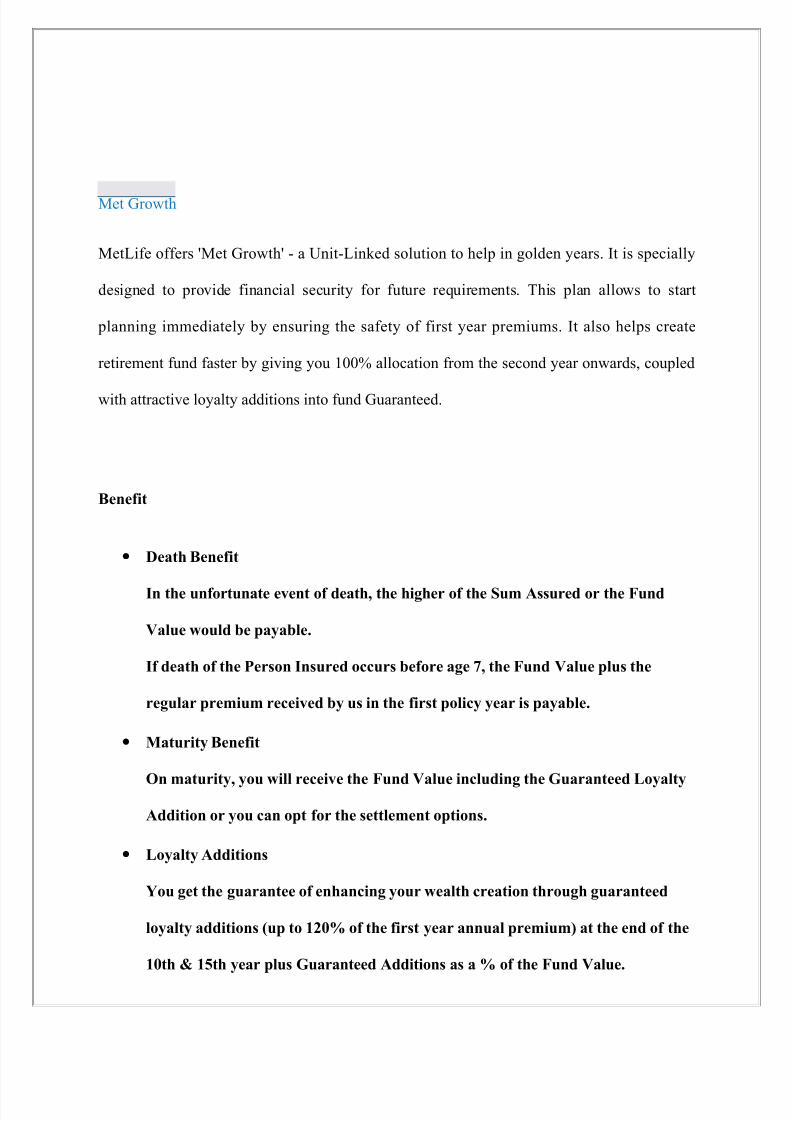

Met Growth

MetLife offers 'Met Growth' - a Unit-Linked solution to help in golden years. It is specially

designed to provide financial security for future requirements. This plan allows to start

planning immediately by ensuring the safety of first year premiums. It also helps create

retirement fund faster by giving you 100% allocation from the second year onwards, coupled

with attractive loyalty additions into fund Guaranteed.

Benefit

• Death Benefit

In the unfortunate event of death, the higher of the Sum Assured or the Fund

Value would be payable.

If death of the Person Insured occurs before age 7, the Fund Value plus the

regular premium received by us in the first policy year is payable.

• Maturity Benefit

On maturity, you will receive the Fund Value including the Guaranteed Loyalty

Addition or you can opt for the settlement options.

• Loyalty Additions

You get the guarantee of enhancing your wealth creation through guaranteed

loyalty additions (up to 120% of the first year annual premium) at the end of the

10th & 15th year plus Guaranteed Additions as a % of the Fund Value.

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 29/112

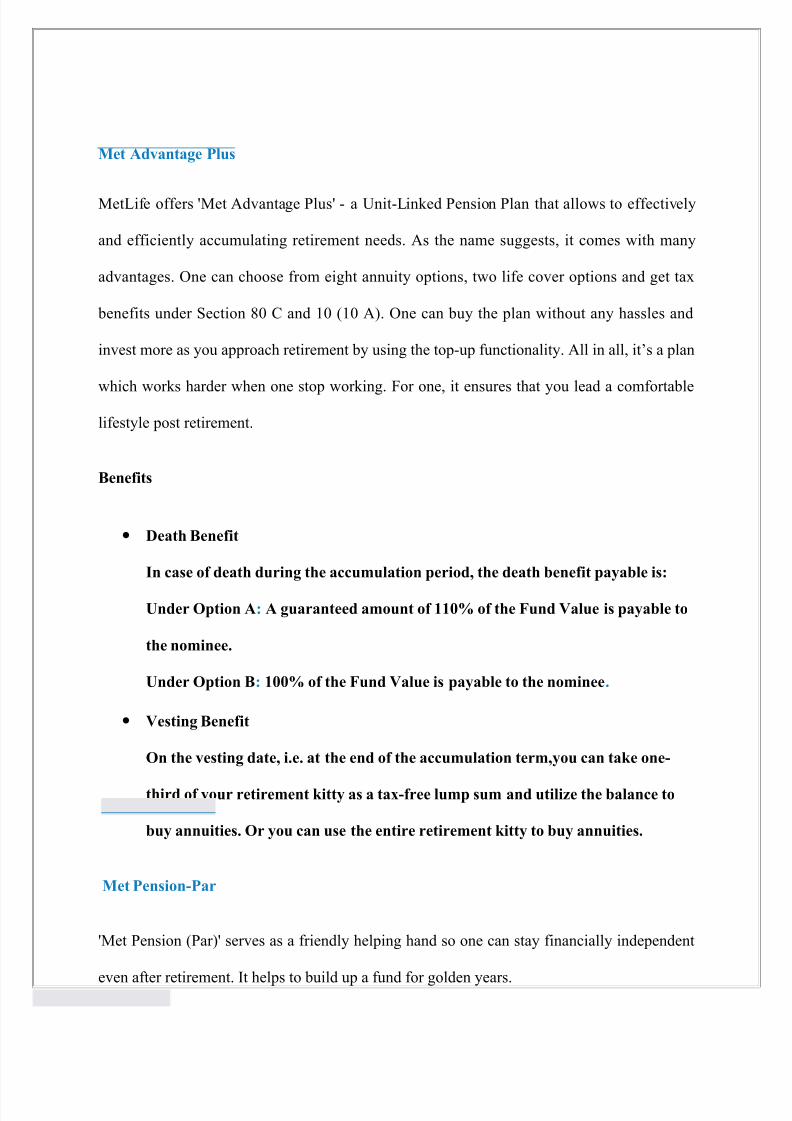

Met Advantage Plus

MetLife offers 'Met Advantage Plus' - a Unit-Linked Pension Plan that allows to effectively

and efficiently accumulating retirement needs. As the name suggests, it comes with many

advantages. One can choose from eight annuity options, two life cover options and get tax

benefits under Section 80 C and 10 (10 A). One can buy the plan without any hassles and

invest more as you approach retirement by using the top-up functionality. All in all, it’s a plan

which works harder when one stop working. For one, it ensures that you lead a comfortable

lifestyle post retirement.

Benefits

• Death Benefit

In case of death during the accumulation period, the death benefit payable is:

Under Option A : A guaranteed amount of 110% of the Fund Value is payable to

the nominee.

Under Option B : 100% of the Fund Value is payable to the nominee .

• Vesting Benefit

On the vesting date, i.e. at the end of the accumulation term,you can take one-

third of your retirement kitty as a tax-free lump sum and utilize the balance to

buy annuities. Or you can use the entire retirement kitty to buy annuities.

Met Pension-Par

'Met Pension (Par)' serves as a friendly helping hand so one can stay financially independent

even after retirement. It helps to build up a fund for golden years.

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 30/112

With this plan,one can ensure his\her enjoy retirement as a happy new chapter.

Benefits

Death Benefit

In case of death while one is saving for retirement, the death benefit payable is:

1. Return of premiums.

2. Accrued reversionary bonus, if any.

3. Any insurance on the life of the Insured that may be provided by riders to this policy.

Vesting Benefit

On the vesting date, you can take one third of your retirement kitty as a tax-free lump

sum and utilize the balance to buy annuities or you can use the entire retirement kitty to

buy annuities. The retirement fund on the date of vesting is equal to the Sum Assured

plus Guaranteed Additions plus the compounded reversionary bonuses plus the

terminal bonus, if any.

Guaranteed Additions

Savings :-

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 31/112

Met Sukh

MetLife offers 'Met Sukh'- a guaranteed money-back policy which provides guaranteed

periodic survival benefits at the end of 5, 10, 15 & 20 years and guaranteed additions of 10%

of the Sum Assured for the entire term. It not only covers your life, but also guarantees you

cash payments at various milestones along with guaranteed growth of your savings.

Benefits

• Death Benefit

In the unfortunate event of death of the Person Insured, the Sum Assured along

with the Guaranteed Additions are payable.

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 32/112

The policyholder is entitled to Guaranteed Additions of Rs. 100 per Rs. 1,000 of

the Sum Assured for each completed year.

• Maturity Benefit

On maturity, the life insured will receive the Survival Benefits plus the

Guaranteed Addition.

Met Suvidha

'Met Suvidha' is a flexible Endowment Plan that combines savings and security. In addition to

providing you rotection till the maturity of the plan, it helps you save for your specific long

term financial objectives. This long term savings-cum-protection plan comes to a customer at

affordable premiums.

Met Suvidha is available in both participating as well as non-participating versions.

Met Saral

MetLife presents 'Met Saral' - a non- participating endowment plan. As the name suggests,

it’s a simple savings plan which gets customer into the savings habit without any medical

tests. All need to do is fill in a simple application form and are ensured a guaranteed maturity

amount of Rs 100,000, even in the case of death during the term. Take the first step towards a

better financial future for customer and his family. Ensure and insure the first Lakh.

Met 100

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 33/112

'Met 100' - a whole life policy where customer pay premiums for 15, 20 or 25 years. It helps

create a legacy for the children, leaving money for a dependant spouse and, more importantly,

provides insurance cover at affordable rates. Met 100 is available in participating as well

as non- participating versions

Death Benefit

Met 100 - Par

In the event of death, the Sum

Assured plus the Reversionary

Bonus and Terminal Bonuses,

if any, are payable.

Met 100 - Non-Par

In the event of death, the Sum

Assured is payable.

Maturity Benefit

Met 100 - Par

On maturity of the policy, the

Sum Assured plus the

Reversionary Bonus and

Terminal Bonuses, if any, are

payable.

Met 100 - Non-Par

On maturity of the policy, the

Sum Assured is payable

Protection :-

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 34/112

Met Suraksha

MetLife offers 'Met Suraksha - Term Assurance (TA)', a non

participating term assurance plan which provides life cover at a nominal

cost. To put it simply, it is a life insurance plan that gives complete

protection to enjoy life to the fullest. Customer can further customize

plan with two riders – Accidental Death Benefit and Critical Illness.

Met Suraksha TROP

MetLife offers 'Met Suraksha - Term with Return of Premium (TROP)', a

non participating term assurance plan which provides life cover at a

nominal cost. To put it simply, it is a life insurance plan that gives

complete protection to enjoy life to the fullest. You can further

customize your plan with two riders – Accidental Death Benefit and

Critical Illness.

Met Mortgage Protector

This plan which provides life cover for home loans taken for any period

above 5 years. It is a decreasing term insurance with single and limited

premium options. The plan covers an amount equal to the outstanding

amount as per the policy schedule.

It ensures the assets that have created stays with family.

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 35/112

Rural :-

None of us can be sure what tomorrow will bring. Shield your families

against the unknown. MetLife’s rural plans protect your loved ones

against financial liabilities and help you save for tomorrow. All at

affordable premiums

Met Vishwas

'Met Vishwas', - a single premium, micro insurance, non- participating

term assurance plan which provides life cover at a nominal cost. On

survival, customers get 110% or 125% of the premium.

Met Suvidha-Rural

Met Suvidha (Rural) is a participating flexible Endowment Plan that

combines savings and security. In addition to providing protection up to

maturity, it helps to save for specific long term financial objectives. This

long term savings-cum-protection plan comes at affordable premiums.

Benefits:

Met Suvidha - Par

In the event of death during

the term of the policy, the

beneficiary will receive the

base Sum Assured, the

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 36/112

accrued reversionary bonus

and terminal bonus if any.

Maturity Benefit

Met Suvidha - Par

On maturity of the policy, you

will receive the base Sum

Assured, the accrued

reversionary bonus and

terminal bonus if any.

• It is an Endowment plan that offers both savings and life

insurance.

• Flexible premium paying options to suit various income cycles.

• A plan which participates in the bonuses declared by the

company.

• Customization possible with Accident Death Benefit, Critical

Illness, Term, Waiver of Premium Riders for comprehensive

protection.

Investment :-

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 37/112

MetLife’s Unit-Linked Insurance Plans ensure systematic enhancement

of wealth. Be it higher returns or the right blend of protection and wealth

optimization, they help to ensure the right choice and peace of mind.

(IN THESE POLICY, THE INVESTMENT RISK IN INVESTMENT

PORTFOLIO IS BORNE BY THE POLICY HOLDER )

Met Easy

A simplified unit-linked plan which offers an opportunity to

systematically build wealth and protection for you and your family.

(The maximum Sum Assured available in this product is based on age, at

the time of buying the policy.)

Benefits-

Death Benefit

In the event of

death:

In the 1st Policy

Year : Higher of

50% of the Sum

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 38/112

Assured or the

Fund Value is

payable.

After the 1st

Policy Year :

Higher of 100%

of the Sum

Assured or Fund

Value. If death of

the Person

Insured occurs

before age 7, the

Fund Value plus

the Regular

Premium received

by us in the first

policy year is

payable.

Maturity Benefit

On maturity, you

will receive the

Fund Value

including the

Loyalty Addition

or you can opt for

the settlement

options.

Loyalty Additions

With Met Easy,

you get the benefit

of potentially

enhancing your

wealth creation

with loyalty

additions that are

added to your

policy on maturity .

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 39/112

Met Smart Gold

MetLife offers 'Met Smart Gold'- a Unit-Linked wealth creation cum protection plan for the well-

heeled. It's specially conceived so that one can get a plan to match his specific financial

requirements.

If you are keen on investing lump sum amounts over a shorter horizon, this is the ideal plan for

you.

Met Smart Plus-Regular Pay

'Met Smart Plus' – a Unit-Linked Whole life plan that matures at age 100. If you want to protect

your family from life’s uncertainties; at the same time, you wish insurance would yield higher

returns on your investments. You want your insurance policy to help realize all your dreams. It’s a

right plan to go with.

Met Smart Plus- Single Pay

Same as Met Smart Plus Regular but premium is payable in a single term or at the time of policy

taken.

Met Smart Premier- Regular Pay

MetLife offers 'Met Smart Premier' – a Unit-Linked Whole life plan that matures at age 100. You

want to protect your family from life’s uncertainties; at the same time, you wish insurance would

39

39

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 40/112

yield higher returns on your investments. You want your insurance policy to help realize all your

dreams.

Met Smart Premier- Single Pay

Payable lump sum at the time of policy taken.

Health :-

Met Health Care

UIN no: 117N048V01

Health problems strike unexpectedly. In addition to causing ill health, it can also scar financial

health. One need to protect himself against such a situation through a health insurance plan. In

order to ensure you are well protected to face any health condition that could befall you, MetLife

presents - Met Health Care, a simple health insurance policy with unique and smart advantages for

you and your family#.

(# Family means spouse and two children. Every additional family member shall be underwritten

as per the underwriting conditions laid by the Company from time to time.)

Met Health Care is a long term health insurance plan from MetLife. This plan covers

1. Hospitalization expenses by providing a Daily Cash benefit as chosen by you.

2. 10 major Critical Illnesses by providing a lump sum benefit.

40

40

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 41/112

3. Total & Permanent Disability due to accident by providing a lump sum benefit.

All the above benefits can be availed without the hassle of undergoing any medical examination.

Just fill up the simple application form and start enjoying the unmatched benefits of Met Health

Care.

Benefits

Death/Maturity Benefit

There is no Death/Maturity Benefit under Met Health Care.Tax Benefits

The premium paid (excluding the service tax) under this plan is eligible for Tax

Benefits under Section 80 D of the Income Tax Act, 1961 as per the provisions

and conditions given therein and are subject to any changes made in the tax laws

in future.

Reasons to Buy1. Coverage for the entire family.

2. No Claim Discounts.

3. Guaranteed Cover* till age 65.

4. Payouts in addition to other Insurance Plans.

5. Multiple Claims.

41

41

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 42/112

SWOT ANALYSIS

Strengths

1) MetLife enjoys good reputation and goodwill in the minds of general public.

2) MetLife has a wide range of products in order to suit the needs of every segment of the

society.

3) The company has also very good distribution network with over 50’000 insurance agents

who are placed in different parts of country.

4) The company has a good customer base and is expanding very fast on it.

5) The bonus rates provided by company are also high.

6) Staffs working at the company are well qualified people. There is less wastage of time that

results in prompt customer service and full attention to the customer.

Weaknesses:

42

42

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 43/112

1. The premium charged by the company on various policies is not at all compatible with

premium offered by other companies.

2. There is less advertising of the products and services offered by the company.

3. The company has less number of insurance policies in comparison to its various competitors.

4. The company has low number of branch offices in comparison to other companies.

Opportunities:

1. Growth in untapped rural market by private players.

2. Purchasing power of both rural and urban customer is increasing significantly.

3. Other private players in insurance industry are doing well in urban market because of

transparency in functioning of the company. So, MetLife also has an opportunity.

4. People are more aware about the importance of life insurance because of growth in

education.

Threats:

43

43

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 44/112

1. The company does not have a proper advertising channel, infect this can be the major

reason that despite having the same kind of services (even better), it is lagging behind.

2. The company is not coming up with more creative ideas.

3. High attrition rate of insurance advisors.

4. High premium charged for sum assured.

INSURANCE AGENCY AS A CAREER

DEFINITION OF AN AGENT OR ADVISOR

1. An agent is the one who acts on the behalf of another. The ‘another’ on whose behalf the

agent acts, is called principal. This is simple definition. The lawyer is the agent of the

client, when he argues the case in the court. An ambassador is the agent of the country. It is

function, which determines the relationship of agency, not the designation.

2. According to section 182 of the Indian Contracts Act, an ‘agent’ is the person employed to

do any act for another or to represent another in dealing with the third person. The person

for whom such act is done or who is so represented is called ‘principal’. In the insurance

industry, the term ‘agent’ is ordinarily applied to a person engaged by the insurer to procure

the new business. The Insurance Act defines an insurance agent as one who is licensed

under sect ion 42 of the act and is paid by the way of commission or otherwise, in

44

44

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 45/112

consideration of this soliciting or procure insurance business, including business relating to

the continuance, renewal or revival of the policies of insurance. He is, for all purpose, an

authorised salesman for insurance.

3. There is legal maxim ‘qui facit alium, facit perse’, which means that he who acts through

others, acts to himself. The principal is bound by what the agent does. Therefore, contracts

enter into through an agent, and obligations arising from acts done by an agent, may be

enforced in the same manner and will have the same legal consequences, as if the contracts

have been into, and the acts done, by the principle himself.

4. Under section 183 of the Contracts Act, any person who is a major, according to the law to

which he is subject, and is of sound mind, can employ an agent. Section 184 provides that as

between the principal and third persons, any person can become an agent. Thus though a

minor may be employed as an agent and the principle would be bound by his actions, the

minor himself will not be liable to his principal. Unlike other contacts, no consideration is

necessary to create an agency contract.

AUTHORITY OF AN AGENT:

While the maxim cited above makes the principal liable for all the acts done by the agent, he

can restrict his liability by specifying the extent of authority granted to the agent. This authority

may be expressed or implied. An authority is said to be expressed when it is stated by the

words, spoken or written. It is implied when it is inferred by the circumstances of the case.

45

45

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 46/112

The L.I.C. does not authorize its agent to collect premium (except first premium along with the

proposal) or the other amounts from policyholders. But if the agent collects such amounts,

remits them to the insurer and gets receipts to be handed over back to the policyholder, implied

authority can be inferred or constructed. The LIC’s stand has been that its agent are not

authorised to collect renewal of premiums and that if they do so, they are acting as agent of

policyholder not LIC. The implication is that if an agent collects premium from the

policyholder and does not remit the same in

the office. The LIC would not be liable for the amount. The courts have upheld this stand. Other

insurance company in India may not follow LIC’s practice. They may grant more or less

authority.

AGENT’S REGULATIONS

The Insurance Regulatory and Development authority (IRDA), constituted by the IRDA act of

1999, issued the IRDA (Licensing of Insurance Agents) Regulation 2000.these regulations

deals with the issue of licences under section 42 of the insurance act, 1938 and other matters

relating to agents.

the regulations are reproduced in full at the end of this course and form part of study material.

46

46

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 47/112

By another notification in October 2002, these regulations were made ineffective for corporate

agents and new IRDA (Licensing of Corporate Agents) Regulations, 2002 were issued. These

regulations deal with the issue of licences and other matters relating to corporate agents. In

terms of these regulations, a licence will not be given if the person is (a) minor, (b) found to be

of unsound mind, (c) found guilty of criminal misappropriation or criminal breach of trust of

cheating or forgery or an abetment of or attempt to commit any such offence (d) found guilty of

or knowingly participating in or conniving any fraud, dishonesty or misrepresentation against

an insurer or insured € not possessing the requisite qualifications and specific training (f) not

passed such examinations as are specified by the regulations (g) found violating the code of

conduct as specified by the regulations.

It is not only an individual who can become an agent. Collective like companies, firms, banks,

cooperative societies, etc., can also become agents. These collective will designate one or more

persons as ‘Corporate Insurance Executives’, who will be required to obtain licences. Other

who may also work for the corporate agent, will be called ‘Specified Persons’ and they will be

required to obtain certificates.

The agent licence as well as corporate agent licence is granted for 3 years. It may be renewed

after three years with renewal fee. The certificate is also valid for three years.

47

47

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 48/112

OTHER INTERMEDIARIES:

Different kinds of agents are recognised under the Contract Act. In the airline industry, for

example, there is the system of general agent, who has authority to act on behalf of principle

on all matters within a specified sphere. Such general agents may represent more than one

principle at the same time. Similar systems of general agents exist also in shipping industry.

They represent foreign shipping companies and are authorised to deal with shippers and local

authorities like the ports or the stevedores, to ensure that the ship’s visit to the port is

profitable and without any problems.

Brokers arrange to place the business of their clients with insurers on terms that ae standard or

negotiated. This becomes necessary when the needs of the proposer are unique and not met by

the benefits under the standard plans of insurance. Brokers understand the nuances of the

business well and also know the policies of insurer. A broker usually does business with more

than one insurance company. He collects commission from the insurer with whom the

business is placed and does not charge the prospect.

In India, till October 2002, only insurance agents licensed by IRDA were permitted to procure

and solicit life insurance business. Brokers only dealt with reinsurance business. The law was

amended

48

48

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 49/112

in September 2002, and the IRDA has issued (Insurance Brokers) Regulations, 2002 providing

for ,

licence of ‘direct brokers’, ‘reinsurance brokers’, and ‘composite brokers’, the last being

authorised to

deal with direct business as well as reinsurance businesses.

49

49

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 50/112

RESEARCH METHODOLOGY

In this study of Recruitment and Development practices of Met Life Insurance Ltd. descriptive

type of research has been done for collecting the primary data. It includes surveys facts, findings,

and enquiries of different kinds.

The major purpose of this descriptive research is the description of the state of affair as it exists at

present. Moreover there is no control over the variables under study; but only reporting of what is

happening or what has happened can be done.

Study design:

Primary data , which has been collected for descriptive research, was based on the telecalling

mainly by hot calling, cold calling, objection handling etc.

For secondary data collection method the help of various reference books have been taken which

are mentioned in bibliography and also by way of surfing through the company’s website.

Sample size:

Out of total universe, 100 respondents have been taken for convenience and were named as

prospective-100 or P-100 . These P-100 were the simultaneously and rigorously approached

50

50

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 51/112

consistently to join the company. Among these P-100, then finally P-15 were selected which were

more of sure and confident to be selected and further developed for joining the business.

AIM OF THE STUDY

Recruitment and development are multifaceted concepts. The relevance of recruitment and

selection is to determine the number of personnel required and development deals with the further

overall grooming of the candidate as an employee. The HR proceeds with the identification of

sources of recruitment and finding suitable candidates for employment. Both internal and external

sources of manpower are used depending upon the types of personnel needed.

The aim of the selection policy is the selection of suitable candidate for a suitable job. The

selection procedure starts only when the recruitments are done, that is, the various suitable

candidate pools are made available. The selections are done from this pool.

Development includes such opportunities as employee training, employee career development,

performance management and development, coaching , mentoring , succession planning , key

employee identification, tuition assistance , and organization development.

This project has the following aims:

1. To understand the nature of Recruitment and Development policy for acquiring suitable

personnel.

2. To understand the variables of Recruitment and Development in Met Life Insurance Ltd.

3. To identify the sources of manpower supply with a view to acquire the best possible

candidate.

4. To understand the procedure of Recruitment and Development in Met Life Insurance Ltd.

51

51

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 52/112

5. To understand the procedure of Recruitment and Development in Met Life Insurance Ltd.

6. Finally to bring out the challenges ahead with respect to recruitment and selection of

advisors.

RESEARCH OBJECTIVE

The objective of the company was to recruit financial advisors for the company and generate work

from them.

In the insurance industry, there are two channels of distribution –Alternate distribution and tied

agency. Advisor recruitment is part of tied agency.

Tied agency is the largest distribution channels of MetLife comprising a large advisor force that

target various customer segments.

With focus on sales and people development, tied agency has emerged as robust, predictable and

sustainable business model.

52

52

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 53/112

SCOPE THE STUDY

The scope of this study is to observe the degree of satisfaction levels of the employer as well as the

employees towards the Recruitment and Development techniques adopted by the company. The

deviations if any, towards this effect have also been studied. Apart from getting an idea of the

techniques and methods in the recruitment procedures a close look will be taken at the insight of

corporate culture prevailing out there in the organization. This would not only help to be familiar

with the corporate environment but it would also enable to get a close look at the various levels

authority-responsibility relationship prevailing in the organization. This study also focuses on

studying the various techniques adopted by the organization to retain the new recruits.

The stipulated time for the project is insufficient to undergo an exhaustive study about the topic

assigned. Moreover the scope of the topic (Recruitment and Development) is wide enough, so it is

difficult to cover the entire topic within the stipulated time, but still whatever could be done

towards .

53

53

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 54/112

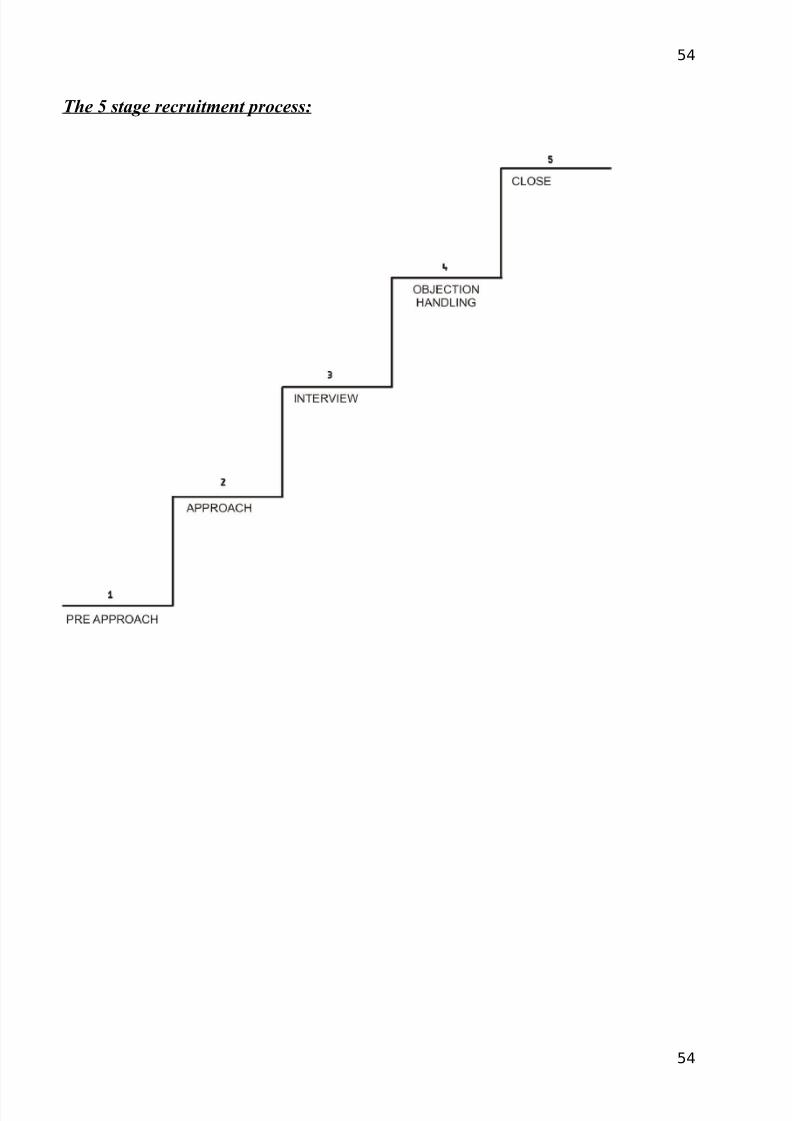

The 5 stage recruitment process:

54

54

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 55/112

PRE APPROACH

1. PRE-APPROACH :

It refers to preparing in order to approach the

prospect. It requires forming some ideas as to how the interview could begin and

proceed.

It involves collection of basic information regarding the prospect’s

Income level

Interests and habits

Present occupation

Family position

To make this stage more effective a script is prepared. A script is nothing but a set

pattern of doing things and responding to the objections.

2. APPROACH

55

55

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 56/112

It involves the meeting with the prospect and explaining him the benefits attached

on becoming an advisor of reputed organisation like MetLife.

3. INTERVIEW:

It begins by making the prospect listen about the proposal that the company is

offering.

It is important that the proposal we make to the prospect should be seen by him as

beneficial and complimentary to existing arrangements.

4. OBJECTION HANDLING:

Prospects raise objections like ‘I do not want to be a financial advisor’, ‘I cannot

attend the training’. These objections can be handled by providing the prospect with

complete and convincing answer.

56

56

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 57/112

5. CLOSE:

It involves helping the client in taking decisions in favour of MetLife insurance.

The various task involved in it are:

Collecting a cheque from client.

Getting the form filled.

Completing the documentation with form filled, cheque collected and date of

birth of proof.

DATA ANALYSIS & INTERPRETATION

QUE.1- ARE YOU EMPLOYED

YES 70 70%

NO 30 30%

TOTAL 100 100%

57

57

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 58/112

no, 30%

yes, 70%

INTERPREATION

70% Respondent say they are employed.

30% Respondent say they are unemployed.

QUE.2- PREFERENCE OF RESPONDENTS OF INSURANCE COMPANIES

COMPANY’S NAME

NO.OF

RESPONDE

NT

SHARE (%)

L.I.C. 74 74

Reliance Life Insurance 3 3

Met life India Ins. Co. Ltd 2 2

58

58

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 59/112

Bajaj Allianz 3 3

ICICI Prudential 9 9

SBI Life 7 7

Max New York Life 2 2

TOTAL 100 100

INTERPRETATION

74% of the people contacted prefer LIC policy to any other and therefore it is ranked no.1

by that percent of respondents.

59

59

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 60/112

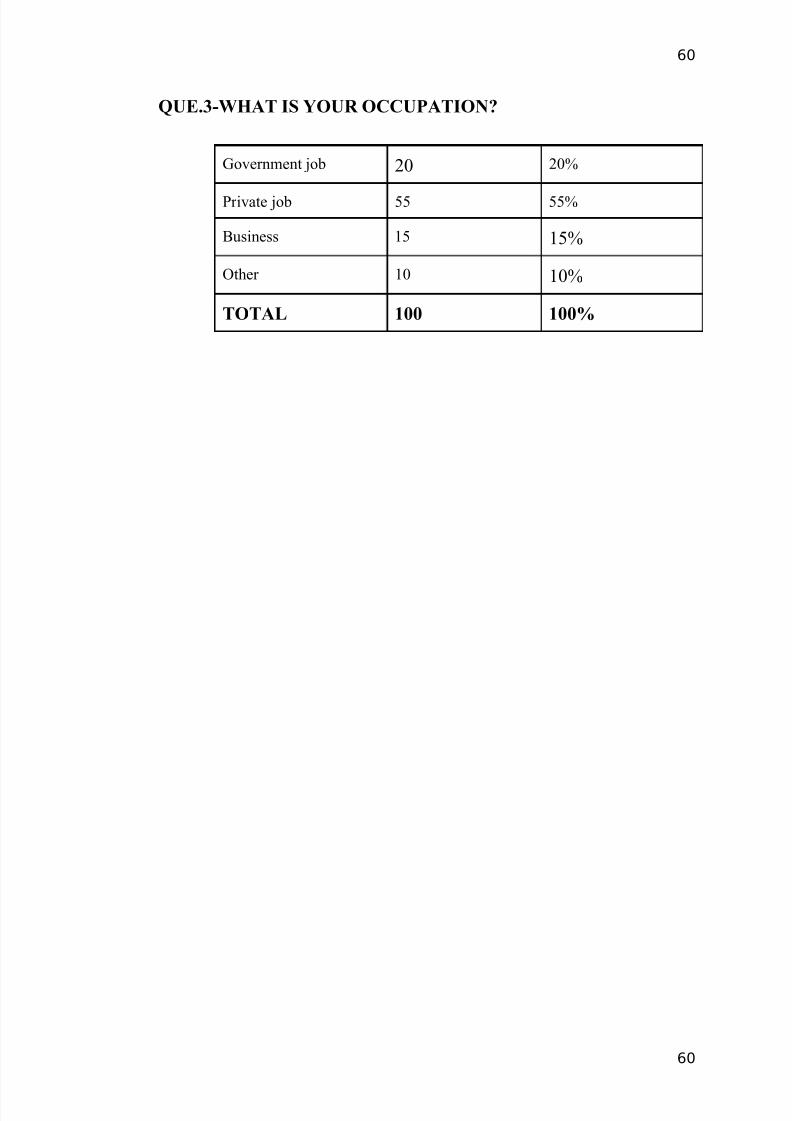

QUE.3-WHAT IS YOUR OCCUPATION?

Government job 20 20%

Private job 55 55%

Business 15 15%

Other 10 10%

TOTAL 100 100%

60

60

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 61/112

Other, 10%Business, 15%

Private job, 55%

Government job ,20%

0%

10%

20%

30%

40%

50%

60%

Government job Private job Business Other

INTERPREATION

20% Responder in government job

55% Respondent are private job

15% Respondent are going business

61

61

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 62/112

10% Respondent other than mention

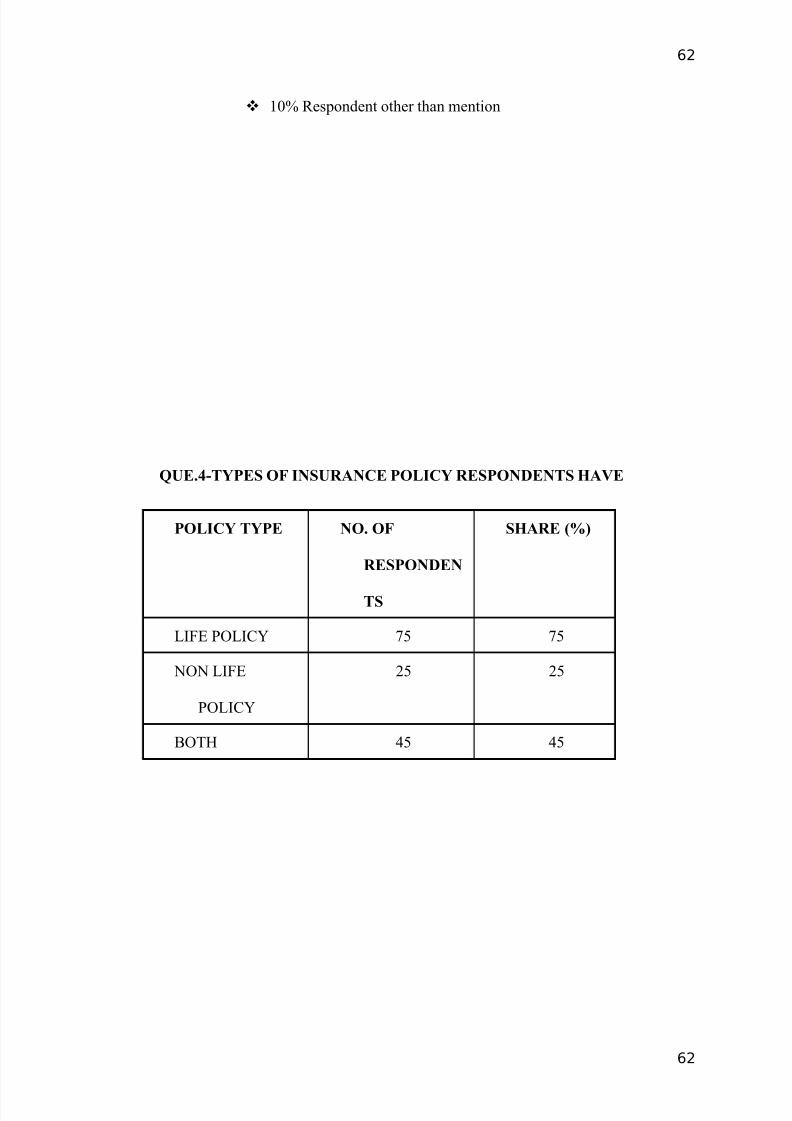

QUE.4-TYPES OF INSURANCE POLICY RESPONDENTS HAVE

POLICY TYPE NO. OF

RESPONDEN

TS

SHARE (%)

LIFE POLICY 75 75

NON LIFE

POLICY

25 25

BOTH 45 45

62

62

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 63/112

Life Policy, 75

Non Life Policy,25

Both, 45

0

10

20

30

40

50

60

70

80

Life Policy Non Life Policy Both

INTERPRETATION

75% of the respondents have only Life Insurance Policy.

While 45% of the respondents have both .

25% of the respondents have only Non- life Policy.

[ Some of the respondents opted for two or more than two items]

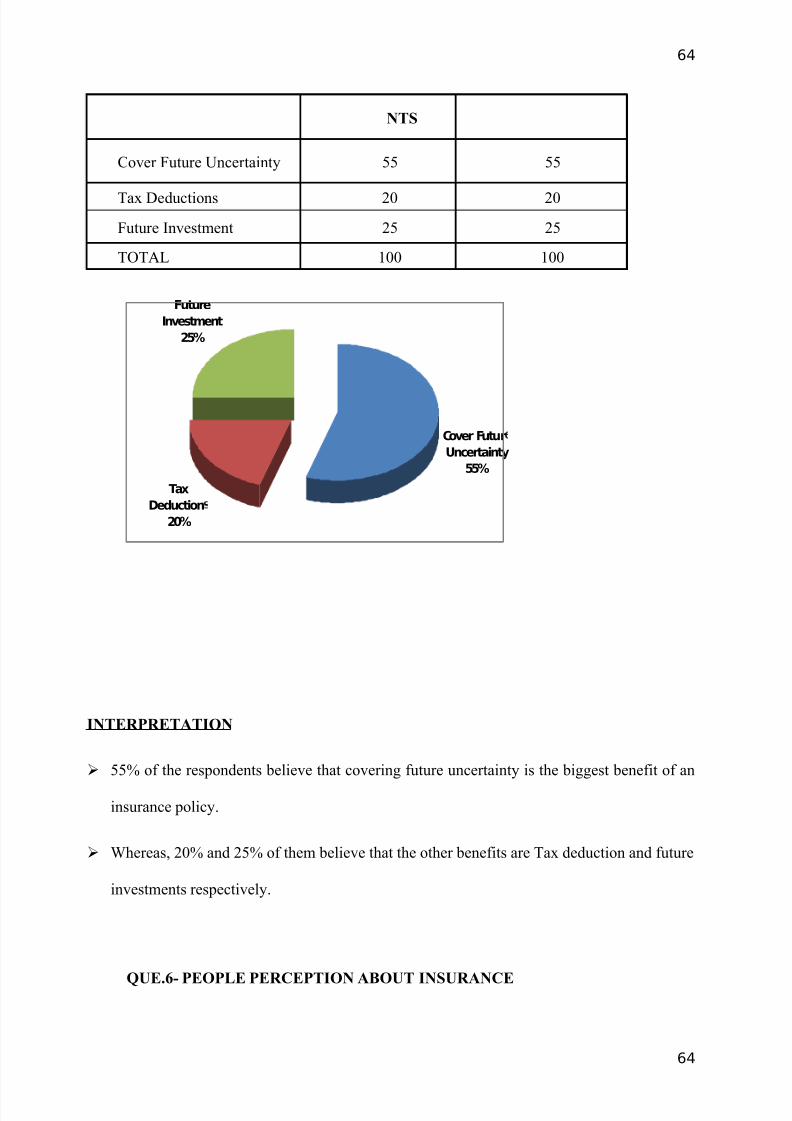

QUE.5-BENEFITS OF INSURANCE PERCEIVED BY RESPONDENTS

BENEFITS NO.OF

RESPONDE

SHARE (%)

63

63

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 64/112

NTS

Cover Future Uncertainty 55 55

Tax Deductions 20 20

Future Investment 25 25

TOTAL 100 100

INTERPRETATION

55% of the respondents believe that covering future uncertainty is the biggest benefit of an

insurance policy.

Whereas, 20% and 25% of them believe that the other benefits are Tax deduction and future

investments respectively.

QUE.6- PEOPLE PERCEPTION ABOUT INSURANCE

64

64

Cover FuturUncertainty

55%

TaxDeduction

20%

FutureInvestment

25%

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 65/112

RESPONSE NO. OF

RESPONDEN

TS

SHARE

(%)

A saving tool 81 81%

A tax saving device 74 74%

A tool to protect your family 100 100%

A savings tool,81 A tax saving

device, 74

A tool toprotect yoour

family, 100

0

20

40

60

80

100

120

A savings tool A tax saving device A tool to protect yoourfamily

INTERPRETATION

• 81% of the respondents have perception of Insurance being a saving tool.

• And 74% of the respondents have perception of Insurance being a tax saving device.

• But 100% of the respondents are with the view that Insurance is a tool to protect your

family.

[Some of the respondents opted for two or more than two items]

65

65

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 66/112

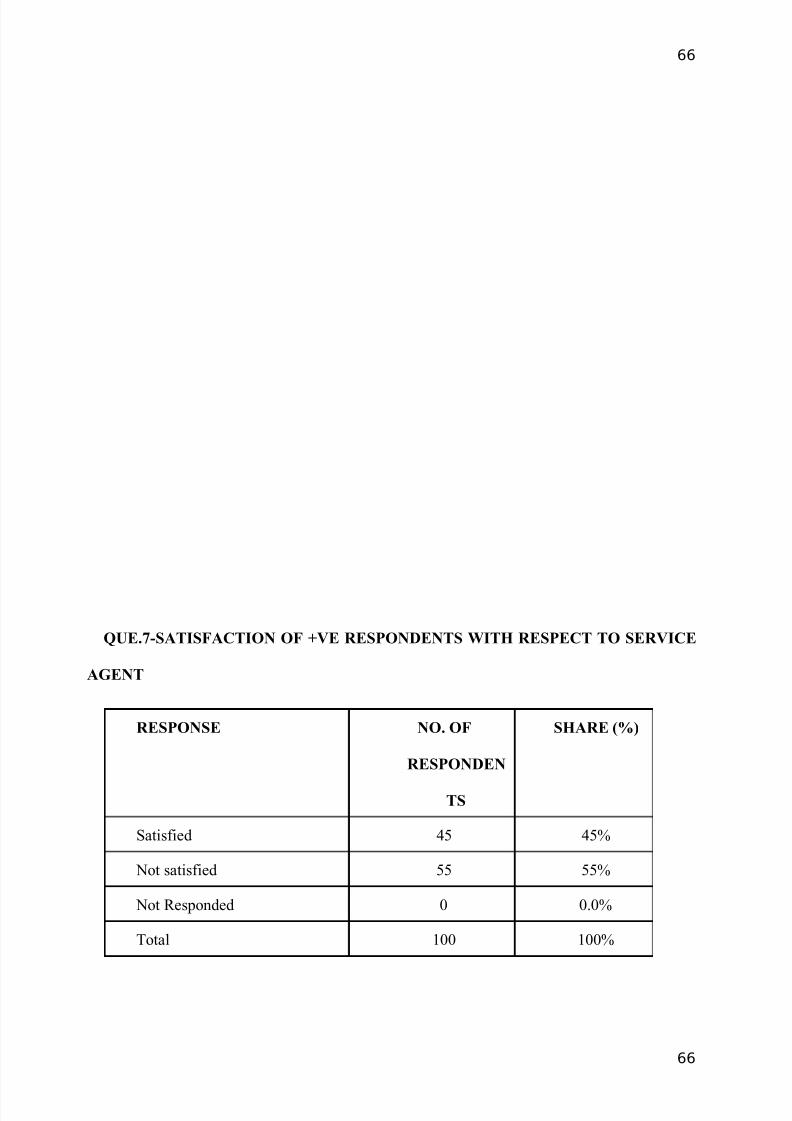

QUE.7-SATISFACTION OF +VE RESPONDENTS WITH RESPECT TO SERVICE

AGENT

RESPONSE NO. OF

RESPONDEN

TS

SHARE (%)

Satisfied 45 45%

Not satisfied 55 55%

Not Responded 0 0.0%

Total 100 100%

66

66

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 67/112

Satisfied45%

Not satisfied55%

INTERPRETATION

• 45% of the respondents are satisfied with their existing service agent.

• 55% of the respondents are not satisfied with their existing insurance agent.

• All of those who have taken a policy have responded.

67

67

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 68/112

QUE.8- NUMBER OF RESPONDENTS PAYING TAX

RESPONSE NO. OF

RESPONDENT

S

SHARE

(%)

Paying tax 91 91%

Not paying tax 9 9%

Total 100 100%

INTERPRETATION

• Of the sample size of 100 respondents, 91 respondents are paying tax.

68

68

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 69/112

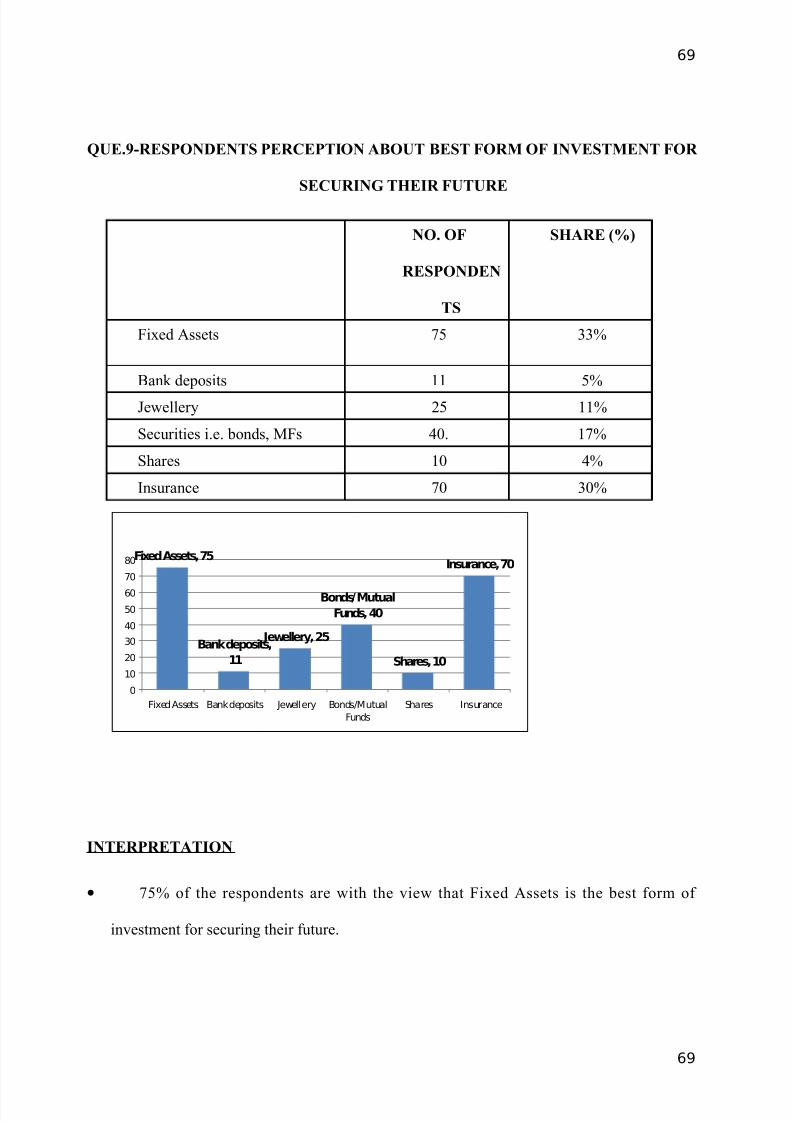

QUE.9-RESPONDENTS PERCEPTION ABOUT BEST FORM OF INVESTMENT FOR

SECURING THEIR FUTURE

NO. OF

RESPONDEN

TS

SHARE (%)

Fixed Assets 75 33%

Bank deposits 11 5%

Jewellery 25 11%

Securities i.e. bonds, MFs 40. 17%

Shares 10 4%

Insurance 70 30%

Fixed Assets, 75

Bank deposits,11

Jewellery, 25

Bonds/MutualFunds, 40

Shares, 10

Insurance, 70

0

10

20

30

40

50

60

70

80

Fixed Assets Bank deposits Jewellery Bonds/MutualFunds

Shares Insurance

INTERPRETATION

• 75% of the respondents are with the view that Fixed Assets is the best form of

investment for securing their future.

69

69

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 70/112

• 70% of the respondents are with the perception that Insurance is the best form of

investment for securing their future, which is 2nd highest and this shows that insurance is

an important key for securing your future.

[Some of the respondents opted for two or more than two items]

QUE.10- PEOPLE OPINION ABOUT INDIAN INSURANCE COMPANIES

RESPONSE NO. OF

RESPONDEN

TS

SHARE (%)

Rigid plans 67 67%

Non user friendly 29 29%

Unsatisfactory services 26 26%

Non Aggressive 35 35%

Satisfactory 24 24%

Good 10 10%

Very good 0 0%

01020304050607080

Rigid

plans

Non us

er frie

ndly

unsat

isfacto

ry ser

vices

Non ag

gressiv

e

Satisfa

ctory

Good

Very g

ood

70

70

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 71/112

INTERPRETATION

• 67% of the respondents have the opinion that Indian Insurance Companies have Rigid

plans.

• 29.5% feel that Indian Insurance companies are Non-user friendly.

• 26.5% feel that services of Indian Insurance companies are Unsatisfactory.

• 35.75% of the respondents are with the view that Indian Insurance companies are Non-

aggressive.

• 24% of the respondents feel that products and services of Indian Insurance companies

is Satisfactory.

• Whereas only 10.25% feel that it is Good enough.

•

And according to the data, no single person has felt that it is very good.

[Some of the respondents opted for two or more than two items]

QUE.11 -DO YOU WANT TO EARN EXTRA INCOME

YES 80 80NO 20 20TOTAL 100 100

71

71

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 72/112

YES

NO

S1

YES, 80%

NO, 20%

0%10%20%30%40%

50%60%70%80%

INTERPREATION

80% say yes

20% say no

QUE-12- DO YOU WANT TO BE A BUSINESS PARTENER

YES 15 15%NO 85 85%

TOTAL 100 100%

72

72

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 73/112

NO, 85%

YES, 15%

INTERPREATION

Only 15% respondent say yes

85% respondent say no

RECRUITMENT OF ADVISOR

Being a MetLife Insurance advisor can be an enriching and exciting career option. It’s an

opportunity to associate with an industry leader, be in touch with the latest and finest insurance

practices from around the globe and grow both professionally and personally.

Some of the benefits of being a MetLife Life Insurance advisor are:

73

73

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 74/112

Unlimited earning potential.

A clear career path

All round support through exclusive advertising.

A comprehensive benefit package.

MetLife believes that its ‘advisors’ are the ‘ambassadors’ to the customers. They are key source of

business for the organisation are continuing link with the clients.

Most financial opportunities are risky, need some financial investment and offer a one-time

income. But, being an MetLife advisor is an ideal opportunity which is neither risky nor does it

require any investment. And above all it offers a trail of future income.

74

74

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 75/112

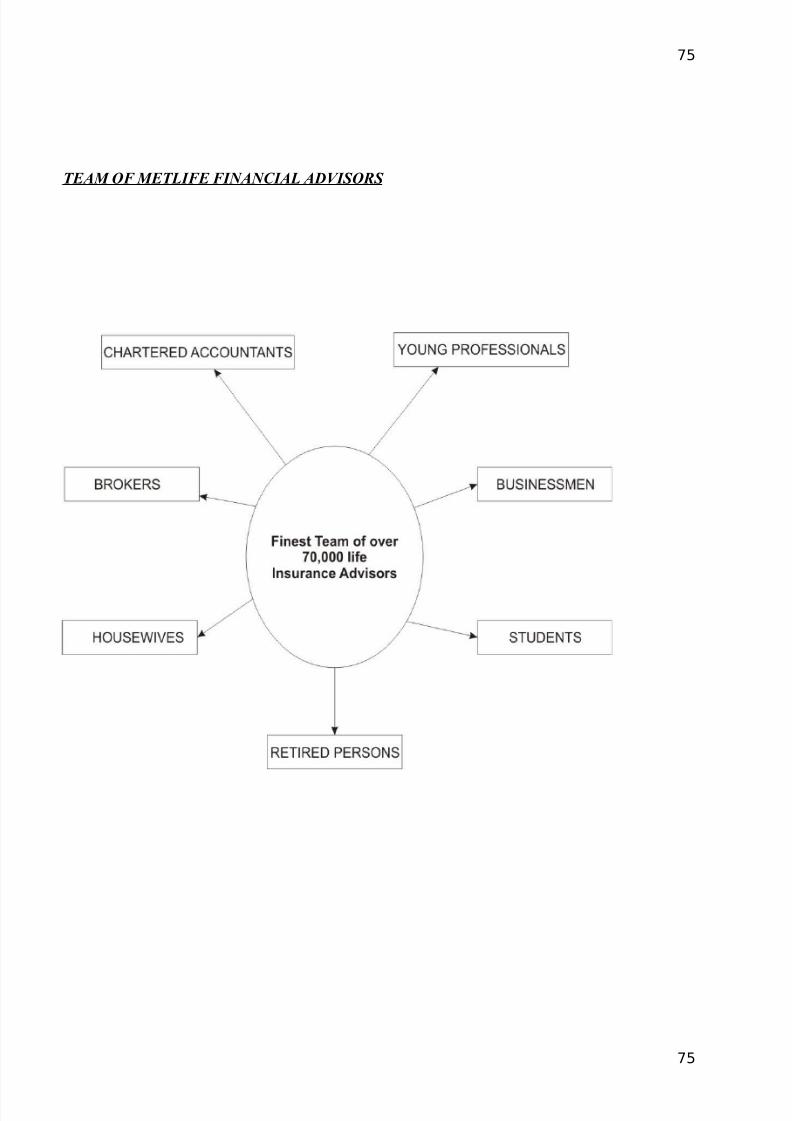

TEAM OF METLIFE FINANCIAL ADVISORS

75

75

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 76/112

METHODS OF REMUNERATING AGENTS

A life insurance agent works on commission basis. He is paid a stated percentage of the

premium collected through his agency. Section 40 (A) (1) of the insurance act stipulates that

the maximum amount which can be paid to a life insurance agent, by way of commission or

remuneration in any form, shall be 35%of the first years premium, 7 and half of the second and

third years renewal premium and 5%of subsequent renewal premium.

There are some exception to this. During the first 10 years of the insurer’s business, he may pay

40% instead of 35% of first years premium. Under certain circumstances, commission of 6%

can be paid on the renewal premium even beyond the third year. Within these limits the manner

of remunerating the FA will be determined by the insurer. Normally, under Term Assurance

Plans, commission rates are less. Similarly, for shorter duration policies, commission rates are

lesser then under long duration plans. Under single premium plans and pension plans rate of

commission is very small.

New agents may be paid stipend to be adjusted against the commission to be earned, as when

business begins to come in. brokers are paid on the totally different basis.

76

76

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 77/112

AGENCY AS A PROFESSION

The insurance agent is bound by the terms of appointment of the insurer and is expected to

procure business for the insurer. It is not the job that he has to do at fixed hours, in prescribed

ways and under close supervision. Once license is appointed, he is an independent professional.

He is the master of his time. He is not prevented from pursuing any other interest or vocation.

Many agents see the agency as the means to earn a living. They may spend only a part of time

on insurance, being busy on other work the rest of the time. Some agents however, try to study

understand the business in great details and to improve their skills. They are trying to become

best in the profession. They would be recognised as experts in the field.

To most persons, life insurance is just one of the many avenues for financial outlays. When an

agent approaches a prospect with a proposal for life insurance, the chances are that the prospect

will no know much about the benefits under various plans. He may be vaguely familiar with the

alternatives available, but it is unlikely to be sure of the details of all of them. He would need

expert advice. If he sees the life insurance agent as one who is keen to divert his money to life

insurance to the exclusion of other alternatives, then that agents intentions and expertise wouldbe suspect. On the contrary, if he sees the agent as one who knows about other alternatives and

who is willing to take note of the needs of the prospect, then the agent would have the better

chance of persuading the prospect one way or the other. In other words, a life insurance agent,

while dealing with the prospect, should be thinking of his interests and requirements and best

financial arrangements that would be appropriate in his situation. Thus the life insurance agent

is an agent of the prospect also.

77

77

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 78/112

As an agent of the insurer, the life insurance agent is expected to obtain life insurance business

and contributes to revenue of the insurer. He is also depended on the bring in business that

would be profitable, to report attempts to commit any fraud, to report on the relevant features

that affect the risk of the subject of insurance. He is in touch with the person to be insured.

Having met him at his place of work or residence and observed his lifestyle and habits, he

would be aware of the nature and characteristics of the risk, beyond what is contained in the

proposal form. He is therefore, called the primary underwriter.

As an agent of the prospect, he is expected to look after the interests of the prospect. Even

people who are generally experts in financial matters, may not be aware of the implications of

the insurance, in relation to terms and conditions, warranties, exclusions, tax provisions, right

of parties, etc. agents have the dual responsibility of being true to the interests of both the

parties in the transaction. He is obliged to reveal to the prospect all the important terms and

conditions of the policy, even if they are restrictive or unpleasant. He is obliged to report to the

insurer all the true facts about the prospect and the subject of insurance. He should not mislead

either.

To be able to advise the prospect on the best financial arrangements appropriate to his situation,

the agent needs to be familiar with the alternatives available in the market. He is also expected

to know in full the benefits and limitations of the various plan being offered by his insurer. A

78

78

8/7/2019 Prashant Bhadauiya Project Report

http://slidepdf.com/reader/full/prashant-bhadauiya-project-report 79/112

good agent is a good financial planner, taking into account not merely the plans offered by the

insurers, but by the innumerable schemes on offer in the market. This needs study on one’s

own it also needs conviction that life insurance policies do not meet all the needs of the people.

Other instruments have their own advantages.

REQUIREMENTS FOR BECOMING AN AGENT

The insurance Act, 1938 lays down that an insurance agent must possess a license under

section 42 of the Act. That licence is to be issued by the IRDA. The IRDA has authorised

designated persons, in each insurance company, to issue the licences on the behalf of IRDA.