PowerPoint Presentation · for large technology & software consolidators – Apple could bring back...

48

Important disclosures appear at the back of this report GP Bullhound LLP is authorized and regulated by the Financial Conduct Authority GP Bullhound Inc is a member of FINRA Global Software Market Perspectives Q1 2018

Transcript of PowerPoint Presentation · for large technology & software consolidators – Apple could bring back...

Important disclosures appear at the back of this report

GP Bullhound LLP is authorized and regulated by the Financial Conduct Authority GP Bullhound Inc is a member of FINRA

Global Software Market PerspectivesQ1 2018

2

Key Sector Takeaways

Recent Software Transaction Trends

Public Market SaaS Analyses

Key SaaS Metrics

Appendix A: GP Bullhound SaaS Index

Appendix B: Software Public Comps by Category

1

2

3

4

6

7

8Appendix C: GP Bullhound Software Report

Overview, Software Credentials & Team

5 SaaS CEO Commentary

3

▪ Software consolidators are hyper focused on “growth acquisitions”

– SaaS companies with as little as $5 million of ARR have attracted such interest when growing north of 100%

– Acquirers are not evaluating build vs. buy as often in these scenarios

– Targets are being integrated, but left alone to continue momentum and growth

▪ Strategic M&A processes have been catalyzed through “market checks” in parallel to companies’ investment processes

– Companies are weighing the advantages of exiting prior to their next financing as opposed to further dilution and time horizon

– Investor interest and term sheets can often drive strategics to act

– All opportunities should be considered and we have seen founders benefit from exploring and understanding their options

▪ We have also started to see a number of “soft landing” exits for start-ups

– Companies exiting to strategics or PE buyers in lieu of raising fresh capital and continued standalone growth

– This is a trend in difficult sub-sectors (consumer, parts of digital marketing) and with non-category leading companies

▪ Despite the initial tailwinds for a robust IPO market in 2018, volatility could threaten the IPO market in the near-term

– Market volatility spiked dramatically in early February as the Dow had one of its biggest point losses in recent times

– We will look to see if planned IPOs will price below initial guidance and/or last privately marked valuations

▪ Dropbox is a marquee software IPO – fastest SaaS company to $1B in revenue – it will be a bellwether IPO in ‘18

– Dropbox is primarily a consumer-focused SaaS business with much different metrics than most enterprise SaaS companies

– Dropbox’s net revenue retention of 100% is low for a SaaS company; land & expand efforts may not be working as well as others

– S&M expenses are much lower than Box’s S&M spend due to their consumer customer base

Q1 SaaS Market Highlights

4

▪ Large established SaaS companies are focusing on shifting to PaaS for their customers

– Customers want to be able to customize their own applications, add new services and shape their product. They can also integrate new

features and functionalities that are prohibitive to develop on their own, for example AI features

– Salesforce is the best example of a SaaS company shifting to PaaS, with their Force.com platform spawning multiple innovative and

successful companies leveraging their technology

» Financial Force – by being native on Force.com they are able to build cloud ERP apps on the largest customer success platform, making

teams more nimble, the services better, and the cost of synchronizing transactions lower

– Other companies focusing on platform offerings are Google, Microsoft, Oracle, SAP and Workday

▪ Customer acquisition cost for SaaS companies has increased almost 65% over the past 5 years lowering margin

expectations for software companies, and making optimization of sales strategies more difficult

– Competition among SaaS vendors has made the cost of acquiring customers increase quite significantly, particularly larger enterprise

solutions

– While competition is responsible for driving up prices, another factor that inevitably affects SaaS companies of scale is a shrinking number of

sales channels to tap

» As early sales channels become saturated, converting clients from this source becomes increasingly difficult and expensive

» Sales channels further down the continuum usually have a marginally higher cost. Channel sales is the exception, having an existing

customer to sell to or through is much cheaper than a new sale and the upfront friction that comes with it

▪ The newly signed tax bill in the US will lead to repatriation of profits, creating an extremely favorable M&A environment

for large technology & software consolidators

– Apple could bring back cash to the order of $252B, Cisco $65B and Google $55B – the possibilities are numerous, with multiple software

companies at large public valuations, and many more with significant value that could contribute scale to the largest technology acquirers

» E.g. Apple / Tesla, Apple / Netflix, Microsoft / Citrix, Google / Salesforce

Our Views on Current Trends in Software

Source: Redpoint Ventures, Capital IQ

5

Key Sector Takeaways

Recent Software Transaction Trends

Public Market SaaS Analyses

Key SaaS Metrics

Appendix A: GP Bullhound SaaS Index

Appendix B: Software Public Comps by Category

1

2

3

4

6

7

8Appendix C: GP Bullhound Software Report

Overview, Software Credentials & Team

5 SaaS CEO Commentary

6

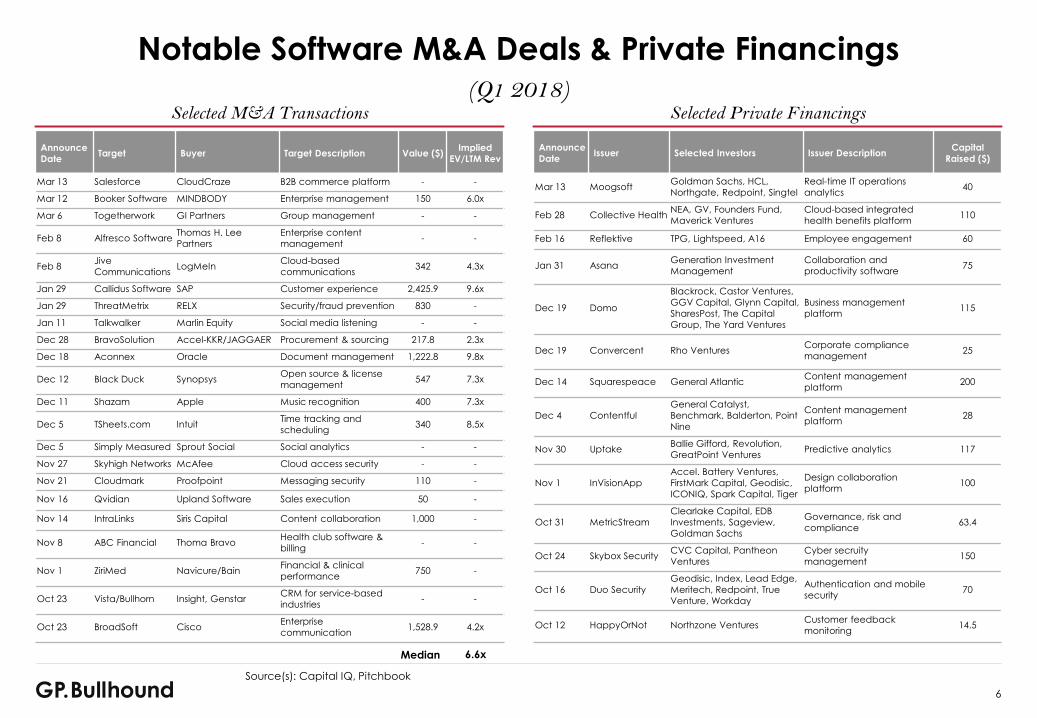

Announce

DateIssuer Selected Investors Issuer Description

Capital

Raised ($)

Mar 13 MoogsoftGoldman Sachs, HCL,

Northgate, Redpoint, Singtel

Real-time IT operations

analytics40

Feb 28 Collective HealthNEA, GV, Founders Fund,

Maverick Ventures

Cloud-based integrated

health benefits platform110

Feb 16 Reflektive TPG, Lightspeed, A16 Employee engagement 60

Jan 31 AsanaGeneration Investment

Management

Collaboration and

productivity software75

Dec 19 Domo

Blackrock, Castor Ventures,

GGV Capital, Glynn Capital,

SharesPost, The Capital

Group, The Yard Ventures

Business management

platform115

Dec 19 Convercent Rho VenturesCorporate compliance

management25

Dec 14 Squarespeace General AtlanticContent management

platform200

Dec 4 Contentful

General Catalyst,

Benchmark, Balderton, Point

Nine

Content management

platform28

Nov 30 UptakeBallie Gifford, Revolution,

GreatPoint VenturesPredictive analytics 117

Nov 1 InVisionApp

Accel. Battery Ventures,

FirstMark Capital, Geodisic,

ICONIQ, Spark Capital, Tiger

Design collaboration

platform100

Oct 31 MetricStream

Clearlake Capital, EDB

Investments, Sageview,

Goldman Sachs

Governance, risk and

compliance63.4

Oct 24 Skybox SecurityCVC Capital, Pantheon

Ventures

Cyber secruity

management150

Oct 16 Duo Security

Geodisic, Index, Lead Edge,

Meritech, Redpoint, True

Venture, Workday

Authentication and mobile

security70

Oct 12 HappyOrNot Northzone VenturesCustomer feedback

monitoring14.5

Announce

DateTarget Buyer Target Description Value ($)

Implied

EV/LTM Rev

Mar 13 Salesforce CloudCraze B2B commerce platform - -

Mar 12 Booker Software MINDBODY Enterprise management 150 6.0x

Mar 6 Togetherwork GI Partners Group management - -

Feb 8 Alfresco SoftwareThomas H. Lee

Partners

Enterprise content

management- -

Feb 8Jive

CommunicationsLogMeIn

Cloud-based

communications342 4.3x

Jan 29 Callidus Software SAP Customer experience 2,425.9 9.6x

Jan 29 ThreatMetrix RELX Security/fraud prevention 830 -

Jan 11 Talkwalker Marlin Equity Social media listening - -

Dec 28 BravoSolution Accel-KKR/JAGGAER Procurement & sourcing 217.8 2.3x

Dec 18 Aconnex Oracle Document management 1,222.8 9.8x

Dec 12 Black Duck SynopsysOpen source & license

management547 7.3x

Dec 11 Shazam Apple Music recognition 400 7.3x

Dec 5 TSheets.com IntuitTime tracking and

scheduling340 8.5x

Dec 5 Simply Measured Sprout Social Social analytics - -

Nov 27 Skyhigh Networks McAfee Cloud access security - -

Nov 21 Cloudmark Proofpoint Messaging security 110 -

Nov 16 Qvidian Upland Software Sales execution 50 -

Nov 14 IntraLinks Siris Capital Content collaboration 1,000 -

Nov 8 ABC Financial Thoma BravoHealth club software &

billing- -

Nov 1 ZiriMed Navicure/BainFinancial & clinical

performance750 -

Oct 23 Vista/Bullhorn Insight, GenstarCRM for service-based

industries- -

Oct 23 BroadSoft CiscoEnterprise

communication1,528.9 4.2x

Notable Software M&A Deals & Private Financings(Q1 2018)

Selected M&A Transactions Selected Private Financings

Source(s): Capital IQ, Pitchbook

Median 6.6x

7

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

$0M

$5B

$10B

$15B

$20B

$25B

$30B

$35B

2015

Q1

2015

Q2

2015

Q3

2015

Q4

2016

Q1

2016

Q2

2016

Q3

2016

Q4

2017

Q1

2017

Q2

2017

Q3

2017

Q4

2018

Q1

Value Deals

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2015

Q1

2015

Q2

2015

Q3

2015

Q4

2016

Q1

2016

Q2

2016

Q3

2016

Q4

2017

Q1

2017

Q2

2017

Q3

2017

Q4

2018

Q1

U.S. & Canada Europe Asia Other

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2015

Q1

2015

Q2

2015

Q3

2015

Q4

2016

Q1

2016

Q2

2016

Q3

2016

Q4

2017

Q1

2017

Q2

2017

Q3

2017

Q4

2018

Q1

U.S. & Canada Europe Asia Other

0

100

200

300

400

500

600

$0M

$20B

$40B

$60B

$80B

$100B

$120B

2015

Q1

2015

Q2

2015

Q3

2015

Q4

2016

Q1

2016

Q2

2016

Q3

2016

Q4

2017

Q1

2017

Q2

2017

Q3

2017

Q4

2018

Q1

M&A Buyout M&A Deals Buyout Deals

Global Software Transaction TrendsM&A and Private Placement Activity by Quarter

Source(s): Pitchbook as of 2/28/2018

Note: Data includes all “SaaS” M&A and private placement deals as defined by Pitchbook regardless of geography or transaction size

M&A Deal Value is Picking Up, Driven by PE Fewer, Larger Private Placements are Still Occurring

The US and Europe Continue to Dominate M&A Deal Volume Private Placement Deal Volume by Region has Stayed Consistent

8

▪ Description (NASDAQ:APPN): Provider of

low-code software development platform

that enables organizations to develop

various applications

▪ Listing Date: 05/25/17

▪ Offering Amount: $75.0m

▪ Offering Price/Share: $12

▪ % Change/IPO Price: 125.3%

▪ LTM Revenue : $176.7m

▪ EV/Revenue1: 9.3x

▪ Selected Metrics:

– Revenue Growth 16/15: 20%

– Subscription Revenue %: 45%

– Average ACV: $475K

– Subscription Revenue Retention Rate:

112%

▪ Description (NYSE:AYX): Provider of self-

service data analytics software that

enables organizations to improve

productivity and business outcomes

▪ Listing Date: 03/24/17

▪ Offering Amount: $126.0m

▪ Offering Price/Share: $14

▪ % Change/IPO Price: 144.2%

▪ LTM Revenue : $131.6m

▪ EV/Revenue1: 14.4x

▪ Selected Metrics:

– Revenue Growth 16/15: 59%

– Subscription Revenue %: >95%

– YoY Customer Growth (16/15): 66%

– $ Based Net Retention Rate: >120%

Software IPOs in 2017

▪ Description (NYSE:CLDR): Developer of a

hybrid open source software (HOSS)

platform for data management, machine

learning and advanced analytics

▪ Listing Date: 05/28/2017

▪ Offering Amount: $225.0m

▪ Offering Price/Share: $15

▪ % Change/IPO Price: 27.0%

▪ LTM Revenue : $336.8m

▪ EV/Revenue1: 6.3x

▪ Selected Metrics:

– Revenue Growth 16/15: 57%

– Subscription Revenue %: 77%

– Net Expansion Rate for Subscription

Revenue: 142%

– Revenue from Cloudera Global 8000:

73%

▪ Description (NYSE:MULE): Developer of an

integration solution for connecting

applications, data, to devices

▪ Listing Date: 03/17/17

▪ Offering Amount: $221.0m

▪ Offering Price/Share: $17

▪ % Change/IPO Price: 81.6%

▪ LTM Revenue : $296.5m

▪ EV/Revenue1: 13.3x

▪ Selected Metrics:

– Revenue Growth 16/15: 70%

– Subscription Revenue %: 81%

– Average ACV 2016: $169K

– YoY Customer Growth (16/15): 27%

– $ Based Net Retention Rate: 117%

▪ Description (NasdaqGS:OKTA): Provider of

identity verification software for the

enterprise

▪ Listing Date: 04/07/2017

▪ Offering Amount: $187.0m

▪ Offering Price/Share: $17

▪ % Change/IPO Price: 127.0%

▪ LTM Revenue: $231.1m

▪ EV/Revenue1: 14.7x

▪ Selected Metrics:

– Revenue Growth 17/16: 87%

– Subscription Revenue %: 89%

– YoY Customer Growth (17/16): 40%

– $ Based Net Retention Rate (2017)2:

123%

▪ Description (NYSE:YEXT): Provider of

platform that lets businesses manage

their digital knowledge in the cloud

▪ Listing Date: 04/13/2017

▪ Offering Amount: $115.5m

▪ Offering Price/Share: $11

▪ % Change/IPO Price: 15.5%

▪ LTM Revenue: $157.9m

▪ EV/Revenue1: 6.1x

▪ Selected Metrics:

– Revenue Growth 17/16: 39%

– $ Based Net Retention Rate (2017):

119%

– Revenue Growth from Existing

Enterprise and Mid Size Customers

(2016): 63%

1. CY 2017E revenue multiple

Source(s): Company SEC filings from Edgar, Capital IQ as of 2/28/2018

▪ Description (NASDAQ:MDB): The leading

modern general purpose database

platform

▪ Listing Date: 10/19/2017

▪ Offering Amount: $192m

▪ Offering Price/Share: $24

▪ % Change/IPO Price: 34.2%

▪ LTM Revenue : $139.4m

▪ EV/Revenue1: 8.8x

▪ Selected Metrics:

– Revenue Growth 17/16: 55%

– Subscription Revenue %: 90%

– ARR expansion rate: 120%

– YoY Customer Growth (17/16): 88%

– Average expansion multiple of top 25

end-customers: 12.3x

▪ Description (NASDAQ:FSCT): Provider of

security software to monitor devices

connected to the network

▪ Listing Date: 04/13/2017

▪ Offering Amount: $115.5m

▪ Offering Price/Share: $11

▪ % Change/IPO Price: 170.7%

▪ LTM Revenue: $220.9m

▪ EV/Revenue1: 4.5x

▪ Selected Metrics:

– Revenue Growth 16/15: 32%

– Average ACV: $200K+

– Average expansion multiple of top 20

end-customers: 4.5x

Listed in 2017

9

▪ Description (NYSE:AYX): Provider of mobile

and cloud-based email service platform

designed to deliver customer

communication that drives engagement

and business growth

▪ Listing Date: 11/15/2017

▪ Offering Amount: $131.2m

▪ Offering Price/Share: $16

▪ % Change/IPO Price: 63.3%

▪ LTM Revenue : $111.9m

▪ EV/Revenue1: 8.7x

▪ Selected Metrics:

– Revenue Growth 16/15: 37%

– Subscription Net Dollar Retention %:

126%

– Email Volume Growth YoY%: 37%

– Customer Growth YoY%: 36%

Software IPOs in 2017

1. CY 2017E revenue multiple

Source(s): Company SEC filings from Edgar, Capital IQ as of 2/28/2018

▪ Description (Nasdaq:DBX): Cloud-based

storage platform designed to store

documents, files, videos and photos

▪ File Date: 10/02/17

▪ LTM Revenue : $1.1bn

▪ Offering:

– 36,000,000

– Price per share: $16-$18

– Market Cap: $7.6-$8.5bn

▪ Selected Metrics:

– Revenue Growth 17/16: 31%

– 500m+ registered users

– 11m+ paying users

– Net revenue retention: ~100%

– ARPU: $111.91

Listed in 2017 To come in 2018

▪ Description (Nasdaq:ZS): Security-as-a-

Service internet security and compliance

platform that acts as a series of check

posts in between the organization and the

public internet, scanning all incoming and

outgoing traffic between any device

▪ File Date: 02/16/18

▪ LTM Revenue: $154.3m

▪ Offering:

– 12,000,000 Shares

– Price per share: $13-$15

– Market Cap: $1.6-$1.8bn

▪ Selected Metrics:

– Revenue Growth FY17/16: 57%

– Net retention rate: 115%

– 2,800+ customers

2017 saw a strong IPO market for SaaS unicorns, highlighted by the performance of

Appian and Forescout; we expect 2018 to be less robust of an environment driven by

choppy public markets and fewer SaaS companies of scale ready to debut

10

Key Sector Takeaways

Recent Software Transaction Trends

Public Market SaaS Analyses

Key SaaS Metrics

Appendix A: GP Bullhound SaaS Index

Appendix B: Software Public Comps by Category

1

2

3

4

6

7

8Appendix C: GP Bullhound Software Report

Overview, Software Credentials & Team

5 SaaS CEO Commentary

11

18.3

14.5

13.2

12.6

9.9

7.3

6.1

5.9

5.6

5.4

4.9

4.5

4.4

4.3

4.2

4.1

4.0

Salesforce

ServiceNow

Workday

Square

j2 Global

Splunk

Atlassian

Veeva

Ultimate Software

LogMeIn

Paycom

athenahealth

Proofpoint

RingCentral

Zendesk

2U

RealPage

HubSpot

MuleSoft

New Relic

GP Bullhound Selected SaaS Index Market Valuations

Source(s): Capital IQ as of 02/28/2018

Note: Includes the 20 largest companies by market cap from the GP Bullhound SaaS index, constituents can be found in Appendix A

(Market Cap Values in $ in billions)

84.0

28.1

26.6

12

3.0x

4.0x

5.0x

6.0x

7.0x

8.0x

9.0x

10.0x

11.0x

12.0x

13.0x

14.0x

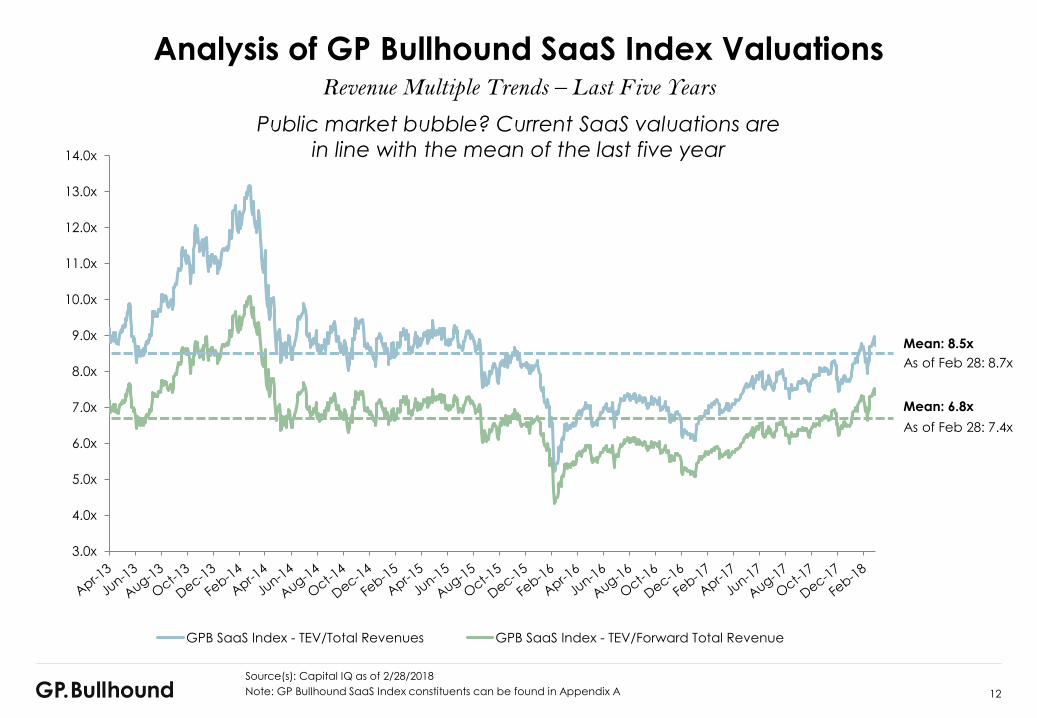

GPB SaaS Index - TEV/Total Revenues GPB SaaS Index - TEV/Forward Total Revenue

Analysis of GP Bullhound SaaS Index ValuationsRevenue Multiple Trends – Last Five Years

Source(s): Capital IQ as of 2/28/2018

Note: GP Bullhound SaaS Index constituents can be found in Appendix A

Mean: 8.5x

Mean: 6.8x

As of Feb 28: 8.7x

As of Feb 28: 7.4x

Public market bubble? Current SaaS valuations are

in line with the mean of the last five year

13

VEEV

BL

PAYC

WDAY

WIX

QTWO

APPF

PFPT

SQ

SPLK

COUP

ZEN

TWLO

HUBS

ULTI

MDSO

MB

CRM

PCTY

NEWR

TLND

MIME

QLYS

EVBG

CALD

FIVN

CSOD

EGHT

RP

RNG

INST

BOX

SPSC

ATHN

BNFT

WK

VIT B

AMBR

CSLT

CARB

APTI

ECOM LPSN

MOBL

BCOVSCWX

AYX

CLDR

YEXT

MULEOKTA

(30%)

(25%)

(20%)

(15%)

(10%)

(5%)

0%

5%

10%

15%

20%

25%

30%

(5%) 0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50% 55% 60% 65%

2018E U

nle

ve

red

FC

F M

arg

in

2018E Revenue Growth

Rule of 40% – Public SaaS2018E Growth and Profitability of Public SaaS Companies in GPB Index

Source(s): Capital IQ as of 02/28/2018

Note: Data based on GP Bullhound SaaS Index, constituents can be found in Appendix A,

excludes outliers and companies with “N/A”

The Rule of

40% Line

14

Comparing the Rule of 40% – Public SaaS2018E Growth and Profitability of Public SaaS Companies in GPB Index is lower than in 2017

Source(s): Capital IQ

Note: Data based on GP Bullhound SaaS Index, constituents can be found in Appendix A,

excludes outliers and companies with “N/A”

VEEV

BL

PAYC

WDAY WIX

QTWO

APPF

PFPT

SQ

SPLK

COUPZEN

TWLO

HUBS

ULTI

MDSO

MB

CRM

PCTY

NEWR

TLND

MIME

QLYS

EVBG

CALD

FIVN

CSOD

EGHT

RP

RNG

INST

BOX

SPSC

ATHN

BNFT

WKVIT B

AMBR

CSLT

CARB

APTI

ECOM LPSN

MOBL

BCOV SCWX

AYX

CLDR

YEXT

MULEOKTA

(30%)

(25%)

(20%)

(15%)

(10%)

(5%)

0%

5%

10%

15%

20%

25%

30%

(5%) 0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50% 55% 60% 65%

2018E U

nle

ve

red

FC

F M

arg

in

2018E Revenue Growth

2018 Revenue Growth + FCF Margin

VEEV

BL

PAYC

WDAY

WIX

QTWOAPPF

SPLK

COUP

ZEN

TWLO

HUBS

ULTIMDSO

MB

CRM

PCTY

NEWR

TLND

MIME

QLYS

EVBG

CALD

FIVN

CSOD

EGHT

RP

RNG

INST

BOX

SPSC

ATHN

BNFT

WKVIT B

AMBR

CSLTCARB

APTI

ECOMLPSN

MOBL

BCOV

SCWX

AYX

CLDR

YEXT

MULE

OKTA

(30%)

(25%)

(20%)

(15%)

(10%)

(5%)

0%

5%

10%

15%

20%

25%

30%

(5%) 0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50% 55% 60% 65%

2017E U

nle

ve

red

FC

F M

arg

in

2017E Revenue Growth

2017 Revenue Growth + FCF Margin

• This interesting comparison of our SaaS Index is telling. SaaS companies are growing quickly, getting larger; thus,

growth rates tend to slow with the law of large numbers

• As SaaS companies mature as public entities, they may be projecting more conservative financial projections.

Moreover, they may be factoring increased competition from SaaS vendors and changes to their market or the

macro economy

15

91%

65%

54%50% 49%

37%

29%

42%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Vertically Focused Cloud SoftwareSignificantly Lower Sales & Marketing Spend as a Percentage of Revenue

However, generally lower growth and valuation multiples

Horizontal Software Vertically-Specific Software

Median: 24%Median: 50%

Source(s): Capital IQ as of 2/28/2018

Note: GP Bullhound SaaS Index constituents can be found in Appendix A

41%

27%24% 24% 24%

20% 21%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

16.1x 13.0x 10.3x 14.2x 7.8x 11.6x 7.6x 8.1x 8.0x 9.2x 7.3x 4.2x 6.8x 13.3x 6.6xEV/LTM

Revenue

CY18/17E

Revenue

Growth

32.5% 41.1% 36.1% 33.3% 21.3% 25.9% 19.2% 26.2% 28.2% 27.9% 25.1% 11.3% 16.8% 20.3% 11.3%

16

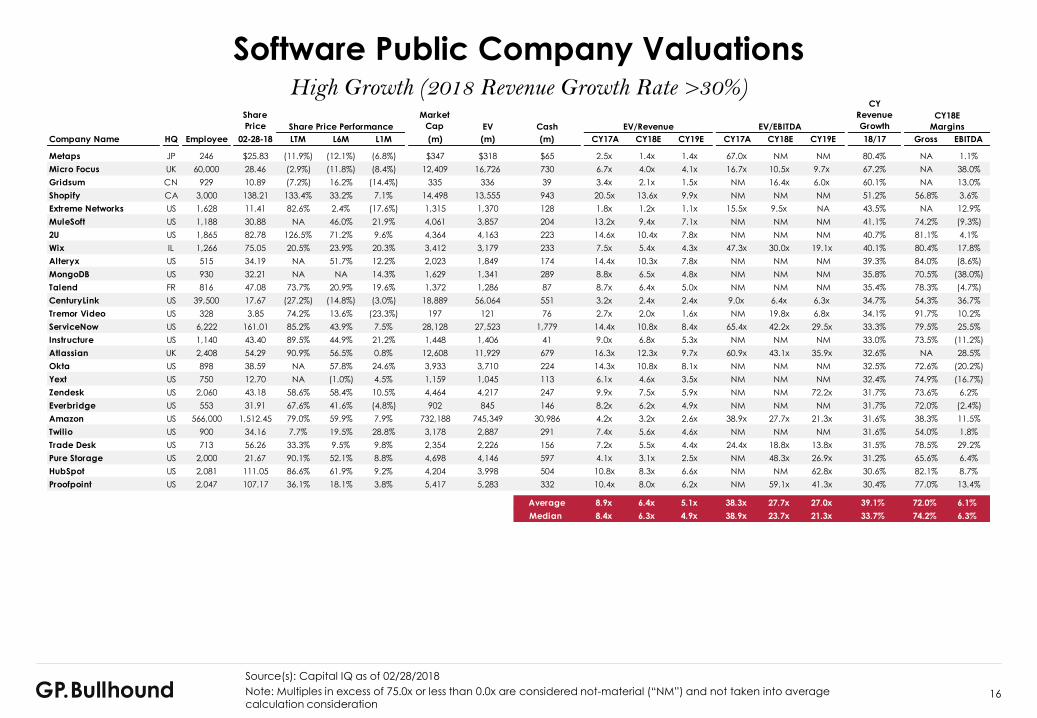

Software Public Company ValuationsHigh Growth (2018 Revenue Growth Rate >30%)

Source(s): Capital IQ as of 02/28/2018

Note: Multiples in excess of 75.0x or less than 0.0x are considered not-material (“NM”) and not taken into average calculation consideration

Share

Price

Market

Cap EV Cash EV/Revenue EV/EBITDA

CY

Revenue

Growth

Company Name HQ Employee 02-28-18 LTM L6M L1M (m) (m) (m) CY17A CY18E CY19E CY17A CY18E CY19E 18/17 Gross EBITDA

Share Price Performance

CY18E

Margins

Metaps JP 246 $25.83 (11.9%) (12.1%) (6.8%) $347 $318 $65 2.5x 1.4x 1.4x 67.0x NM NM 80.4% NA 1.1%

Micro Focus UK 60,000 28.46 (2.9%) (11.8%) (8.4%) 12,409 16,726 730 6.7x 4.0x 4.1x 16.7x 10.5x 9.7x 67.2% NA 38.0%

Gridsum CN 929 10.89 (7.2%) 16.2% (14.4%) 335 336 39 3.4x 2.1x 1.5x NM 16.4x 6.0x 60.1% NA 13.0%

Shopify CA 3,000 138.21 133.4% 33.2% 7.1% 14,498 13,555 943 20.5x 13.6x 9.9x NM NM NM 51.2% 56.8% 3.6%

Extreme Networks US 1,628 11.41 82.6% 2.4% (17.6%) 1,315 1,370 128 1.8x 1.2x 1.1x 15.5x 9.5x NA 43.5% NA 12.9%

MuleSoft US 1,188 30.88 NA 46.0% 21.9% 4,061 3,857 204 13.2x 9.4x 7.1x NM NM NM 41.1% 74.2% (9.3%)

2U US 1,865 82.78 126.5% 71.2% 9.6% 4,364 4,163 223 14.6x 10.4x 7.8x NM NM NM 40.7% 81.1% 4.1%

Wix IL 1,266 75.05 20.5% 23.9% 20.3% 3,412 3,179 233 7.5x 5.4x 4.3x 47.3x 30.0x 19.1x 40.1% 80.4% 17.8%

Alteryx US 515 34.19 NA 51.7% 12.2% 2,023 1,849 174 14.4x 10.3x 7.8x NM NM NM 39.3% 84.0% (8.6%)

MongoDB US 930 32.21 NA NA 14.3% 1,629 1,341 289 8.8x 6.5x 4.8x NM NM NM 35.8% 70.5% (38.0%)

Talend FR 816 47.08 73.7% 20.9% 19.6% 1,372 1,286 87 8.7x 6.4x 5.0x NM NM NM 35.4% 78.3% (4.7%)

CenturyLink US 39,500 17.67 (27.2%) (14.8%) (3.0%) 18,889 56,064 551 3.2x 2.4x 2.4x 9.0x 6.4x 6.3x 34.7% 54.3% 36.7%

Tremor Video US 328 3.85 74.2% 13.6% (23.3%) 197 121 76 2.7x 2.0x 1.6x NM 19.8x 6.8x 34.1% 91.7% 10.2%

ServiceNow US 6,222 161.01 85.2% 43.9% 7.5% 28,128 27,523 1,779 14.4x 10.8x 8.4x 65.4x 42.2x 29.5x 33.3% 79.5% 25.5%

Instructure US 1,140 43.40 89.5% 44.9% 21.2% 1,448 1,406 41 9.0x 6.8x 5.3x NM NM NM 33.0% 73.5% (11.2%)

Atlassian UK 2,408 54.29 90.9% 56.5% 0.8% 12,608 11,929 679 16.3x 12.3x 9.7x 60.9x 43.1x 35.9x 32.6% NA 28.5%

Okta US 898 38.59 NA 57.8% 24.6% 3,933 3,710 224 14.3x 10.8x 8.1x NM NM NM 32.5% 72.6% (20.2%)

Yext US 750 12.70 NA (1.0%) 4.5% 1,159 1,045 113 6.1x 4.6x 3.5x NM NM NM 32.4% 74.9% (16.7%)

Zendesk US 2,060 43.18 58.6% 58.4% 10.5% 4,464 4,217 247 9.9x 7.5x 5.9x NM NM 72.2x 31.7% 73.6% 6.2%

Everbridge US 553 31.91 67.6% 41.6% (4.8%) 902 845 146 8.2x 6.2x 4.9x NM NM NM 31.7% 72.0% (2.4%)

Amazon US 566,000 1,512.45 79.0% 59.9% 7.9% 732,188 745,349 30,986 4.2x 3.2x 2.6x 38.9x 27.7x 21.3x 31.6% 38.3% 11.5%

Twilio US 900 34.16 7.7% 19.5% 28.8% 3,178 2,887 291 7.4x 5.6x 4.6x NM NM NM 31.6% 54.0% 1.8%

Trade Desk US 713 56.26 33.3% 9.5% 9.8% 2,354 2,226 156 7.2x 5.5x 4.4x 24.4x 18.8x 13.8x 31.5% 78.5% 29.2%

Pure Storage US 2,000 21.67 90.1% 52.1% 8.8% 4,698 4,146 597 4.1x 3.1x 2.5x NM 48.3x 26.9x 31.2% 65.6% 6.4%

HubSpot US 2,081 111.05 86.6% 61.9% 9.2% 4,204 3,998 504 10.8x 8.3x 6.6x NM NM 62.8x 30.6% 82.1% 8.7%

Proofpoint US 2,047 107.17 36.1% 18.1% 3.8% 5,417 5,283 332 10.4x 8.0x 6.2x NM 59.1x 41.3x 30.4% 77.0% 13.4%

Average 8.9x 6.4x 5.1x 38.3x 27.7x 27.0x 39.1% 72.0% 6.1%

Median 8.4x 6.3x 4.9x 38.9x 23.7x 21.3x 33.7% 74.2% 6.3%

17

Software Public Company Valuations (Cont'd)Strong Growth (2018 Revenue Growth Rate Between 20% and 30%)

Source(s): Capital IQ as of 02/28/2018

Note: Multiples in excess of 75.0x or less than 0.0x are considered not-material (“NM”) and not taken into average calculation consideration

Share

Price

Market

Cap EV Cash EV/Revenue EV/EBITDA

CY

Revenue

Growth

Company Name HQ Employee 02-28-18 LTM L6M L1M (m) (m) (m) CY17A CY18E CY19E CY17A CY18E CY19E 18/17 Gross EBITDA

Share Price Performance

CY18E

Margins

Park City Group US 77 $10.35 (27.1%) (15.2%) 16.9% $203 $194 $15 9.1x 7.0x 5.3x NA 21.6x 15.4x 30.0% NA 32.4%

Wisetech AU 900 8.30 98.5% 32.8% (32.7%) 2,409 2,365 47 16.5x 12.7x 10.4x 46.1x 34.7x 26.6x 29.7% NA 36.6%

New Relic US 1,253 71.78 104.0% 49.4% 15.9% 3,980 3,747 233 11.4x 8.8x 7.1x NM NM 56.0x 29.5% NA 8.6%

MINDBODY US 1,440 35.65 34.3% 59.5% 1.4% 1,674 1,456 232 8.0x 6.2x 5.0x NM 65.8x 38.5x 28.2% 72.8% 9.5%

AppFolio US 672 40.10 61.4% (4.5%) (8.1%) 1,366 1,320 46 9.3x 7.3x 5.9x 49.0x 35.3x 25.8x 27.9% 61.9% 20.6%

Blackline US 726 44.00 54.2% 47.1% 30.9% 2,326 2,213 113 12.7x 9.9x 7.9x NM NM NM 27.7% 80.3% 4.6%

Hortonworks US 1,150 17.98 80.9% 12.2% (12.4%) 1,305 1,233 73 4.8x 3.8x 3.0x NM 14.1x 6.8x 27.4% 73.7% 26.7%

RingCentral US 1,352 62.65 134.6% 62.1% 13.0% 4,929 4,748 181 9.5x 7.5x 6.1x NM 65.5x 50.2x 27.3% 77.9% 11.4%

Square US 2,338 46.05 165.9% 84.9% 0.2% 18,252 17,751 866 18.3x 13.2x 10.3x NM 70.7x 42.2x 38.7% 85.7% 18.7%

Mimecast UK 957 34.74 76.5% 27.3% 7.8% 2,008 1,920 129 8.1x 6.3x 5.3x NM 59.9x 43.1x 27.1% NA 10.6%

Cloudera US 1,470 19.05 NA 2.6% 1.7% 2,690 2,301 390 6.3x 5.0x 4.1x NM NM NM 26.9% 74.9% (18.7%)

Workday US 7,900 126.67 52.7% 22.4% 6.6% 26,601 24,824 3,268 11.6x 9.2x 7.5x 71.4x 49.7x 36.8x 25.9% 75.2% 18.6%

Paycom US 2,548 98.92 83.8% 36.0% 6.4% 5,854 5,844 46 13.5x 10.8x 8.7x 44.0x 26.8x 21.9x 25.8% 83.6% 40.1%

Upland Software US 251 23.86 98.0% 5.2% (0.1%) 496 534 53 5.5x 4.4x 4.2x 17.9x 12.4x 11.4x 25.5% 67.3% 35.3%

Splunk US 2,700 93.20 51.0% 44.5% 0.8% 13,184 12,203 1,165 9.8x 7.8x 6.1x NM 57.2x 38.8x 25.5% 83.0% 13.7%

RealPage US 5,462 52.25 54.8% 26.7% 6.2% 4,346 4,925 69 7.3x 5.9x 5.3x 30.4x 22.5x 18.8x 25.1% 62.8% 26.1%

Varonis Systems US 1,251 56.15 104.9% 47.0% 1.8% 1,581 1,444 137 6.9x 5.5x 4.7x NM NM NM 24.8% 90.8% 2.9%

Coupa Software US 652 44.60 68.6% 44.4% 16.4% 2,455 2,236 219 12.3x 9.9x 8.0x NM NM NM 24.5% 72.2% (3.5%)

Carbonite US 830 28.15 44.7% 48.5% 9.1% 787 770 128 3.1x 2.5x 2.2x 16.3x 9.9x 8.6x 24.3% 76.5% 25.5%

Box US 1,726 24.06 36.5% 22.6% 7.4% 3,304 3,182 208 6.3x 5.1x 4.1x NM NM 59.2x 23.6% 74.6% 3.1%

ForeScout Technologies US 818 29.78 NA NA (10.1%) 1,143 979 186 4.5x 3.7x 3.0x NM NM NM 23.0% 74.3% (12.5%)

Palo Alto Networks US 4,833 173.37 14.1% 34.1% 8.6% 15,924 14,825 1,636 7.5x 6.1x 5.2x 31.5x 23.5x 18.9x 22.8% NA 26.0%

Sophos UK 3,293 6.88 98.3% 4.3% (24.1%) 3,216 3,444 81 6.1x 4.9x 4.1x 61.5x 48.5x 33.9x 22.5% NA 10.2%

CyberArk IL 823 49.51 (2.1%) 23.7% 13.8% 1,720 1,417 303 5.5x 4.5x 3.8x 25.3x 22.0x 17.8x 22.5% 86.8% 20.5%

Constellation Software CA 12,124 648.36 37.7% 17.4% 0.2% 13,740 13,587 489 5.5x 4.5x 4.0x 21.2x 17.4x 15.1x 22.2% 66.0% 26.0%

Paylocity US 2,115 46.77 32.6% (0.3%) (5.8%) 2,460 2,349 111 7.1x 5.8x 4.7x 35.5x 27.8x 22.1x 22.1% NA 20.8%

Callidus Software US 1,300 35.90 90.5% 48.7% 11.3% 2,386 2,244 150 9.0x 7.4x 6.2x 71.1x 43.0x 29.9x 21.3% 66.0% 17.3%

Q2 Holdings US 844 45.55 26.7% 10.7% 11.2% 1,914 1,815 100 9.4x 7.7x 6.3x NM NM 53.9x 21.3% 52.4% 8.6%

Alphabet US 80,110 1,103.92 30.7% 18.9% (7.0%) 767,836 669,934 101,871 6.1x 5.0x 4.3x 15.3x 13.0x 11.1x 21.2% 61.0% 38.6%

Adobe US 17,973 209.13 76.7% 37.8% 3.9% 102,804 98,867 5,820 13.6x 11.3x 9.6x 32.5x 25.2x 21.2x 21.0% 87.8% 44.8%

Yonyou CN 15,023 5.18 85.1% 59.5% 41.0% 7,582 7,858 439 8.3x 6.8x 5.9x NM 61.5x 52.5x 21.0% 69.2% 11.1%

Ellie Mae US 1,280 88.67 (7.2%) 8.8% (8.9%) 3,035 2,794 241 6.8x 5.6x 4.8x 23.4x 21.4x 16.0x 20.7% 59.4% 26.2%

Qualys US 869 74.05 111.9% 62.6% 15.2% 2,860 2,572 288 11.2x 9.3x 7.9x 30.4x 26.3x 22.2x 20.5% 78.8% 35.3%

Envestnet US 3,197 55.10 42.6% 29.3% 1.3% 2,441 2,622 60 3.9x 3.2x 2.9x 21.6x 17.1x 14.2x 20.4% 64.0% 18.7%

Veeva US 1,794 69.70 59.5% 22.0% 14.3% 9,852 9,090 762 13.4x 11.1x 9.4x 40.0x 34.2x 28.6x 20.3% 72.9% 32.5%

Salesforce US 29,401 116.25 42.9% 24.1% 2.2% 83,967 81,945 4,522 7.8x 6.5x 5.5x 36.5x 29.8x 23.7x 20.2% 76.6% 21.9%

Average 8.8x 7.0x 5.8x 36.0x 34.2x 28.4x 24.7% 73.4% 18.6%

Median 8.0x 6.4x 5.3x 32.0x 27.3x 23.7x 24.4% 74.3% 19.6%

18

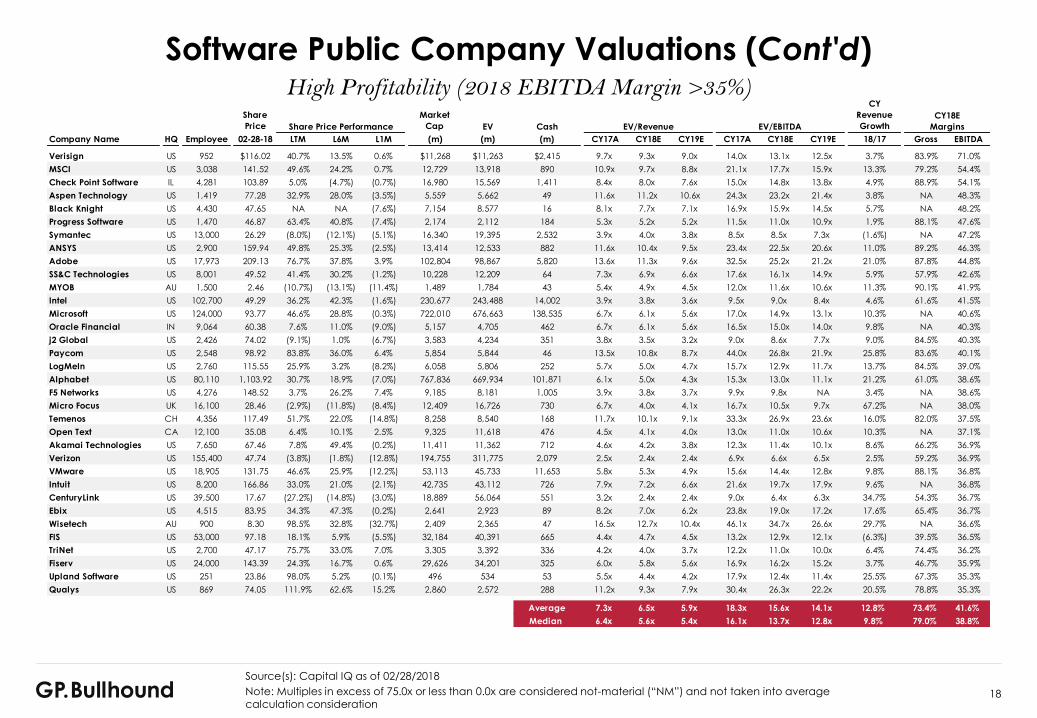

Software Public Company Valuations (Cont'd)High Profitability (2018 EBITDA Margin >35%)

Source(s): Capital IQ as of 02/28/2018

Note: Multiples in excess of 75.0x or less than 0.0x are considered not-material (“NM”) and not taken into average calculation consideration

Share

Price

Market

Cap EV Cash EV/Revenue EV/EBITDA

CY

Revenue

Growth

Company Name HQ Employee 02-28-18 LTM L6M L1M (m) (m) (m) CY17A CY18E CY19E CY17A CY18E CY19E 18/17 Gross EBITDA

Share Price Performance

CY18E

Margins

Verisign US 952 $116.02 40.7% 13.5% 0.6% $11,268 $11,263 $2,415 9.7x 9.3x 9.0x 14.0x 13.1x 12.5x 3.7% 83.9% 71.0%

MSCI US 3,038 141.52 49.6% 24.2% 0.7% 12,729 13,918 890 10.9x 9.7x 8.8x 21.1x 17.7x 15.9x 13.3% 79.2% 54.4%

Check Point Software IL 4,281 103.89 5.0% (4.7%) (0.7%) 16,980 15,569 1,411 8.4x 8.0x 7.6x 15.0x 14.8x 13.8x 4.9% 88.9% 54.1%

Aspen Technology US 1,419 77.28 32.9% 28.0% (3.5%) 5,559 5,662 49 11.6x 11.2x 10.6x 24.3x 23.2x 21.4x 3.8% NA 48.3%

Black Knight US 4,430 47.65 NA NA (7.6%) 7,154 8,577 16 8.1x 7.7x 7.1x 16.9x 15.9x 14.5x 5.7% NA 48.2%

Progress Software US 1,470 46.87 63.4% 40.8% (7.4%) 2,174 2,112 184 5.3x 5.2x 5.2x 11.5x 11.0x 10.9x 1.9% 88.1% 47.6%

Symantec US 13,000 26.29 (8.0%) (12.1%) (5.1%) 16,340 19,395 2,532 3.9x 4.0x 3.8x 8.5x 8.5x 7.3x (1.6%) NA 47.2%

ANSYS US 2,900 159.94 49.8% 25.3% (2.5%) 13,414 12,533 882 11.6x 10.4x 9.5x 23.4x 22.5x 20.6x 11.0% 89.2% 46.3%

Adobe US 17,973 209.13 76.7% 37.8% 3.9% 102,804 98,867 5,820 13.6x 11.3x 9.6x 32.5x 25.2x 21.2x 21.0% 87.8% 44.8%

SS&C Technologies US 8,001 49.52 41.4% 30.2% (1.2%) 10,228 12,209 64 7.3x 6.9x 6.6x 17.6x 16.1x 14.9x 5.9% 57.9% 42.6%

MYOB AU 1,500 2.46 (10.7%) (13.1%) (11.4%) 1,489 1,784 43 5.4x 4.9x 4.5x 12.0x 11.6x 10.6x 11.3% 90.1% 41.9%

Intel US 102,700 49.29 36.2% 42.3% (1.6%) 230,677 243,488 14,002 3.9x 3.8x 3.6x 9.5x 9.0x 8.4x 4.6% 61.6% 41.5%

Microsoft US 124,000 93.77 46.6% 28.8% (0.3%) 722,010 676,663 138,535 6.7x 6.1x 5.6x 17.0x 14.9x 13.1x 10.3% NA 40.6%

Oracle Financial IN 9,064 60.38 7.6% 11.0% (9.0%) 5,157 4,705 462 6.7x 6.1x 5.6x 16.5x 15.0x 14.0x 9.8% NA 40.3%

j2 Global US 2,426 74.02 (9.1%) 1.0% (6.7%) 3,583 4,234 351 3.8x 3.5x 3.2x 9.0x 8.6x 7.7x 9.0% 84.5% 40.3%

Paycom US 2,548 98.92 83.8% 36.0% 6.4% 5,854 5,844 46 13.5x 10.8x 8.7x 44.0x 26.8x 21.9x 25.8% 83.6% 40.1%

LogMeIn US 2,760 115.55 25.9% 3.2% (8.2%) 6,058 5,806 252 5.7x 5.0x 4.7x 15.7x 12.9x 11.7x 13.7% 84.5% 39.0%

Alphabet US 80,110 1,103.92 30.7% 18.9% (7.0%) 767,836 669,934 101,871 6.1x 5.0x 4.3x 15.3x 13.0x 11.1x 21.2% 61.0% 38.6%

F5 Networks US 4,276 148.52 3.7% 26.2% 7.4% 9,185 8,181 1,005 3.9x 3.8x 3.7x 9.9x 9.8x NA 3.4% NA 38.6%

Micro Focus UK 16,100 28.46 (2.9%) (11.8%) (8.4%) 12,409 16,726 730 6.7x 4.0x 4.1x 16.7x 10.5x 9.7x 67.2% NA 38.0%

Temenos CH 4,356 117.49 51.7% 22.0% (14.8%) 8,258 8,540 168 11.7x 10.1x 9.1x 33.3x 26.9x 23.6x 16.0% 82.0% 37.5%

Open Text CA 12,100 35.08 6.4% 10.1% 2.5% 9,325 11,618 476 4.5x 4.1x 4.0x 13.0x 11.0x 10.6x 10.3% NA 37.1%

Akamai Technologies US 7,650 67.46 7.8% 49.4% (0.2%) 11,411 11,362 712 4.6x 4.2x 3.8x 12.3x 11.4x 10.1x 8.6% 66.2% 36.9%

Verizon US 155,400 47.74 (3.8%) (1.8%) (12.8%) 194,755 311,775 2,079 2.5x 2.4x 2.4x 6.9x 6.6x 6.5x 2.5% 59.2% 36.9%

VMware US 18,905 131.75 46.6% 25.9% (12.2%) 53,113 45,733 11,653 5.8x 5.3x 4.9x 15.6x 14.4x 12.8x 9.8% 88.1% 36.8%

Intuit US 8,200 166.86 33.0% 21.0% (2.1%) 42,735 43,112 726 7.9x 7.2x 6.6x 21.6x 19.7x 17.9x 9.6% NA 36.8%

CenturyLink US 39,500 17.67 (27.2%) (14.8%) (3.0%) 18,889 56,064 551 3.2x 2.4x 2.4x 9.0x 6.4x 6.3x 34.7% 54.3% 36.7%

Ebix US 4,515 83.95 34.3% 47.3% (0.2%) 2,641 2,923 89 8.2x 7.0x 6.2x 23.8x 19.0x 17.2x 17.6% 65.4% 36.7%

Wisetech AU 900 8.30 98.5% 32.8% (32.7%) 2,409 2,365 47 16.5x 12.7x 10.4x 46.1x 34.7x 26.6x 29.7% NA 36.6%

FIS US 53,000 97.18 18.1% 5.9% (5.5%) 32,184 40,391 665 4.4x 4.7x 4.5x 13.2x 12.9x 12.1x (6.3%) 39.5% 36.5%

TriNet US 2,700 47.17 75.7% 33.0% 7.0% 3,305 3,392 336 4.2x 4.0x 3.7x 12.2x 11.0x 10.0x 6.4% 74.4% 36.2%

Fiserv US 24,000 143.39 24.3% 16.7% 0.6% 29,626 34,201 325 6.0x 5.8x 5.6x 16.9x 16.2x 15.2x 3.7% 46.7% 35.9%

Upland Software US 251 23.86 98.0% 5.2% (0.1%) 496 534 53 5.5x 4.4x 4.2x 17.9x 12.4x 11.4x 25.5% 67.3% 35.3%

Qualys US 869 74.05 111.9% 62.6% 15.2% 2,860 2,572 288 11.2x 9.3x 7.9x 30.4x 26.3x 22.2x 20.5% 78.8% 35.3%

Average 7.3x 6.5x 5.9x 18.3x 15.6x 14.1x 12.8% 73.4% 41.6%

Median 6.4x 5.6x 5.4x 16.1x 13.7x 12.8x 9.8% 79.0% 38.8%

19

GP Bullhound SaaS Index Performance

L1M L3M

L6M L12M

Source(s): Capital IQ as of 2/28/2018

Note: GP Bullhound SaaS Index constituents can be found in Appendix A

80.0%

85.0%

90.0%

95.0%

100.0%

105.0%

110.0%

115.0%

120.0%

125.0%

12/1/17 12/30/17 1/28/18 2/26/18

Ind

ex V

alu

e

GPB SaaS Index S&P 500 NASDAQ Composite

95.0%

100.0%

105.0%

110.0%

115.0%

120.0%

125.0%

130.0%

9/1/17 10/1/17 10/31/17 11/30/17 12/30/17 1/29/18 2/28/18

Ind

ex

Va

lue

GPB SaaS Index S&P 500 NASDAQ Composite

90.0%

100.0%

110.0%

120.0%

130.0%

140.0%

150.0%

160.0%

2/28/17 5/31/17 8/31/17 11/30/17 2/28/18

Ind

ex

Va

lue

GPB SaaS Index S&P 500 NASDAQ Composite

90.0%

95.0%

100.0%

105.0%

110.0%

2/1/18 2/4/18 2/7/18 2/10/18 2/13/18 2/16/18 2/19/18 2/22/18 2/25/18 2/28/18

Ind

ex V

alu

e

GPB SaaS Index S&P 500 NASDAQ Composite

20

Key Sector Takeaways

Recent Software Transaction Trends

Public Market SaaS Analyses

Key SaaS Metrics

Appendix A: GP Bullhound SaaS Index

Appendix B: Software Public Comps by Category

1

2

3

4

6

7

8Appendix C: GP Bullhound Software Report

Overview, Software Credentials & Team

5 SaaS CEO Commentary

21

Key SaaS MetricsDefinitions & Calculations

Metric Definition Calculation

Normalized measurement of recurring revenue, most frequently

measured with a constant value in each month of the

subscription periodMRR

All S&M expenses for new customers. Sometimes excludes people

management S&M costsCAC =

𝑆&𝑀

# 𝑜𝑓 𝑛𝑒𝑤 𝑐𝑢𝑠𝑡𝑜𝑚𝑒𝑟𝑠

Customer Acquisition Cost (CAC)

Amount of profit a customer is calculated to deliver to the

company over the lifetime of the customerCLV =

𝐴𝑅𝑃𝑈 ∗ 𝐺𝑀

𝐶ℎ𝑢𝑟𝑛 𝑟𝑎𝑡𝑒

Customer Lifetime Value (CLV)

The number of months a company requires to payback its cost of

customer acquisitionPayback Period =

𝐶𝐴𝐶

𝐴𝑅𝑃𝐴 ∗ 𝐺𝑀Payback Period

Churn (Gross & Net)

Gross Churn is the number of customers you lose in a given period

or cohort regardless of account expansion or growth

Net Churn is the number of customers gained or lost in a given

period or cohort after taking into consideration new, reactivated,

or expanded accounts Net Churn =

(𝑐𝑢𝑠𝑡𝑜𝑚𝑒𝑟𝑠 𝑙𝑜𝑠𝑡𝑜𝑣𝑒𝑟 𝑡𝑖𝑚𝑒 𝑝𝑒𝑟𝑖𝑜𝑑 − 𝑐𝑢𝑠𝑡𝑜𝑚𝑒𝑟𝑠 𝑔𝑎𝑖𝑛𝑒𝑑

𝑜𝑣𝑒𝑟 𝑡𝑖𝑚𝑒 𝑝𝑒𝑟𝑖𝑜𝑑)𝑐𝑢𝑠𝑡𝑜𝑚𝑒𝑟𝑠 𝑎𝑡

𝑏𝑒𝑔𝑖𝑛𝑛𝑖𝑛𝑔 𝑜𝑓 𝑡𝑖𝑚𝑒 𝑝𝑒𝑟𝑖𝑜𝑑

Gross Churn = 𝑐𝑢𝑠𝑡𝑜𝑚𝑒𝑟𝑠 𝑙𝑜𝑠𝑡 𝑜𝑣𝑒𝑟 𝑡𝑖𝑚𝑒 𝑝𝑒𝑟𝑖𝑜𝑑

𝑐𝑢𝑠𝑡𝑜𝑚𝑒𝑟𝑠 𝑎𝑡 𝑏𝑒𝑔𝑖𝑛𝑛𝑖𝑛𝑔 𝑜𝑓 𝑡𝑖𝑚𝑒 𝑝𝑒𝑖𝑟𝑜𝑑

MRR= # 𝑜𝑓 𝑝𝑎𝑦𝑖𝑛𝑔 𝑐𝑢𝑠𝑡𝑜𝑚𝑒𝑟𝑠 ∗ 𝐴𝑅𝑃𝐴/𝑚𝑜𝑛𝑡ℎ

22

Key SaaS Metrics (Cont’d)

• Monthly Recurring Revenues (MRR), Annual Recurring Revenue (ARR), Annual Run Rate Revenue (ARRR) are the key

metrics that investors will focus on

– Note: ARRR = ARR + Non-recurring revenue items

– Also important to understand, the % on-demand SaaS vs. traditional license, and the mix between software and

services

• Important to show continued growth in top line revenue (both reported and for the above metrics)

MRR / ARR / ARRR

• Customer Acquisition Cost (CAC) payback period is typically stated in months. Represents the time taken to fully pay

back sales and marketing investments

• Growth is the key target for SaaS companies, but sales and marketing investments should ultimately be profitable. CAC

payback periods:

– For SMEs, CAC payback period should be 6-12 months

– For Enterprise Customers, CAC payback period should be 9-15 months

– A CAC payback period of >24months should be a cause for concern

• Customer Lifetime Value = NPV of recurring gross profit of a customer less the initial cost of customer acquisition

• For SMEs, CLV should be between 3 & 4 years

– For Enterprise Customers, CLV should be between 5 & 7 years

CAC vs. CLV

• Logo Churn: Churn of absolute number of customers. Top companies have a Logo Churn of <7%

• MRR Churn: Churn of customer MRR that has been lost over given period of time. Top companies have a MRR Churn of

<5%, including upgrades/customer expansion, churn is ideally negative

• MRR Renewal: Total MRR of renewed customers/Total MRR of existing customers at year beginning. Top companies

have a MRR Renewal percentage of 105-110% due to upsells to its installed base

• Net Revenue Retention:

– Key metric for performance of SaaS business

– >100% upsells more than make up for churn

– ARR as a Percentage of Upsells: 15%+

Churn & Renewal Rates

• Growth is of paramount importance, with excess cash being used to fuel growth

• Important, therefore, to understand the cash burn in the business and planning for capital efficient hyper-growth

Free Cash Flow / Burn Rate

Source(s): GP Bullhound analysis

Investors focus on key SaaS metrics, long-term business model viability and valuations

23

Key Sector Takeaways

Recent Software Transaction Trends

Public Market SaaS Analyses

Key SaaS Metrics

Appendix A: GP Bullhound SaaS Index

Appendix B: Software Public Comps by Category

1

2

3

4

6

7

8Appendix C: GP Bullhound Software Report

Overview, Software Credentials & Team

5 SaaS CEO Commentary

24

SaaS Company Executive Commentary

Celigo is redefining the future of cloud-based

application integration through an easy-to-use,

next-generation integration Platform-as-a-Service

(iPaaS) that enables companies to integrate almost

anything to anything.

JAN ARENDTSZFounder & CEO

"The phenomenal success of SaaS over the last ten years has

spawned thousands of new cloud applications. The

proliferation of these apps is a direct result of the

consumerization of enterprise software, where clunky

interfaces and complex implementations are a relic of the past.

Today, most mid-market companies use well over 100

specialized cloud-based apps and services that are easy to

purchase by line managers and quick to deploy. That’s the easy

part. They soon find out that to be successful, they need to

integrate the enterprise. These apps need to be connected with a

simplicity that matches the simplicity of the underlying apps

themselves."

25

SaaS Company Executive Commentary (Cont’d)

GERO DECKERCo-Founder & CEO

"Many companies are overwhelmed with the pace, volume and

complexity of change. Faced with disruption in the market,

new technologies and complex regulatory requirements,

organizations are desperate to become more agile. SaaS

offerings like the Signavio suite come at a perfect time to help

these businesses solve their challenges and fundamentally

improve the way they work. With a focus on delivering

customer success, SaaS providers can make a sustainable

difference at scale - and yield fantastic returns for their

investors along the way."

Signavio enables companies to translate between

strategy and execution. Its Business Transformation

Suite helps analyze, improve, reinvent and

automate business processes across the enterprise.

26

SaaS Company Executive Commentary (Cont’d)

JOERG WIEMERCo-Founder & CEO

“As any scrappy entrepreneur will tell you, cash burn rates

provide a very good sense for the steady-state health of the

business. Detailed cash flow metrics are a must have.

However, large organizations rarely use this metrics to run

their business. They still rely on accounting data. This triggers

some problems, because accounting data is an opinion from

yesterday, after the accountant has dome his work. Only cash

tells you the truth in real time. CXO`s have realized that cash

flow is the lifeblood of a business and payment processes are

carrying this lifeblood. We deliver smart payment processes to

help great organizations to make better decisions in real time.”

TIS is a leading global cloud platform for managing

corporate payments and cash flows. The platform

provides bank account management, payments,

business discovery, cash flow, ERP integration, and

certification solutions for treasurers, CFOs, and firms

in the accounting and IT industry.

27

Key Sector Takeaways

Recent Software Transaction Trends

Public Market SaaS Analyses

Key SaaS Metrics

Appendix A: GP Bullhound SaaS Index

Appendix B: Software Public Comps by Category

1

2

3

4

6

7

8Appendix C: GP Bullhound Software Report

Overview, Software Credentials & Team

5 SaaS CEO Commentary

28

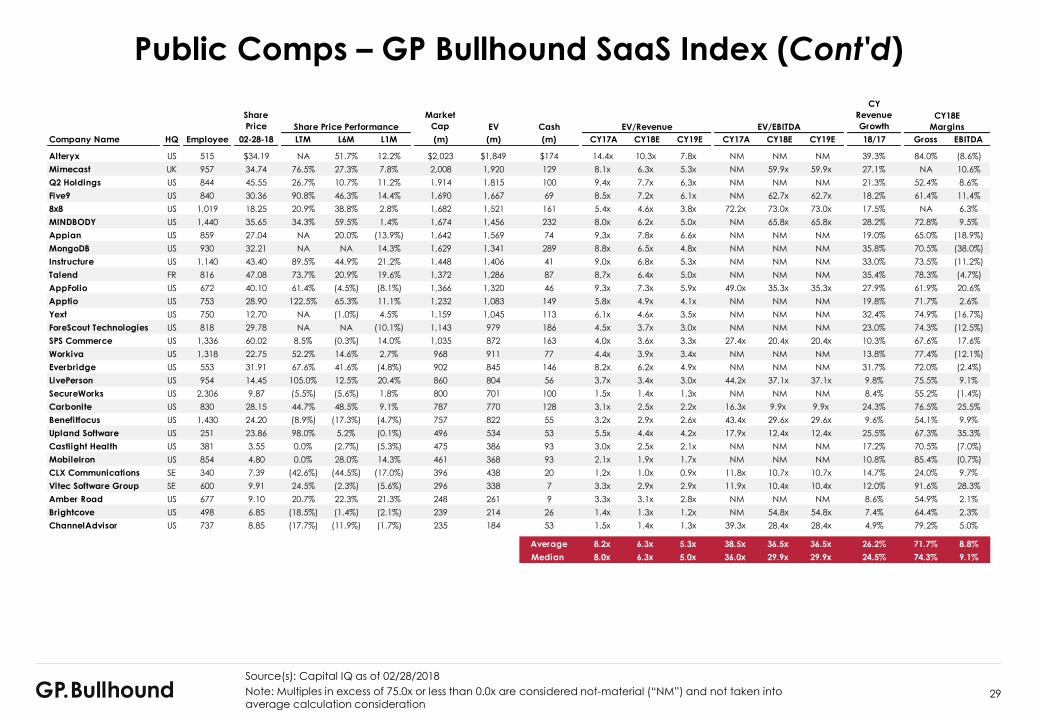

Public Comps – GP Bullhound SaaS Index

Source(s): Capital IQ as of 02/28/2018

Note: Multiples in excess of 75.0x or less than 0.0x are considered not-material (“NM”) and not taken into average calculation consideration

Salesforce US 29,401 $116.25 42.9% 24.1% 2.2% $83,967 $81,945 $4,522 7.8x 6.5x 5.5x 36.5x 29.8x 29.8x 20.2% 76.6% 21.9%

ServiceNow US 6,222 161.01 85.2% 43.9% 7.5% 28,128 27,523 1,779 14.4x 10.8x 8.4x 65.4x 42.2x 42.2x 33.3% 79.5% 25.5%

Workday US 7,900 126.67 52.7% 22.4% 6.6% 26,601 24,824 3,268 11.6x 9.2x 7.5x 71.4x 49.7x 49.7x 25.9% 75.2% 18.6%

Square US 2,338 46.05 165.9% 84.9% 0.2% 18,252 17,751 866 18.3x 6.5x 10.3x NM 70.7x 70.7x 181.1% 85.7% 9.2%

j2 Global CA 3,000 138.21 133.4% 33.2% 7.1% 14,498 13,555 943 20.5x 13.6x 9.9x NM NM NM 51.2% 56.8% 3.6%

Splunk US 2,700 93.20 51.0% 44.5% 0.8% 13,184 12,203 1,165 9.8x 7.8x 6.1x NM 57.2x 57.2x 25.5% 83.0% 13.7%

Atlassian UK 2,408 54.29 90.9% 56.5% 0.8% 12,608 11,929 679 16.3x 12.3x 9.7x 60.9x 43.1x 43.1x 32.6% NA 28.5%

Veeva US 1,794 69.70 59.5% 22.0% 14.3% 9,852 9,090 762 13.4x 11.1x 9.4x 40.0x 34.2x 34.2x 20.3% 72.9% 32.5%

Ultimate Software US 4,208 238.46 23.3% 21.3% 2.6% 7,291 7,135 165 7.6x 6.4x 5.4x 33.2x 25.8x 25.8x 19.2% 65.0% 24.9%

LogMeIn US 2,760 115.55 25.9% 3.2% (8.2%) 6,058 5,806 252 5.7x 5.0x 4.7x 15.7x 12.9x 12.9x 13.7% 84.5% 39.0%

Paycom US 2,548 98.92 83.8% 36.0% 6.4% 5,854 5,844 46 13.5x 10.8x 8.7x 44.0x 26.8x 26.8x 25.8% 83.6% 40.1%

athenahealth US 5,156 139.74 18.5% 0.8% 6.5% 5,603 5,711 165 4.7x 4.2x 3.8x 21.7x 16.3x 16.3x 11.3% 58.3% 26.0%

Proofpoint US 2,047 107.17 36.1% 18.1% 3.8% 5,417 5,283 332 10.4x 8.0x 6.2x NM 59.1x 59.1x 30.4% 77.0% 13.4%

RingCentral US 1,352 62.65 134.6% 62.1% 13.0% 4,929 4,748 181 9.5x 7.5x 6.1x NM 65.5x 65.5x 27.3% 77.9% 11.4%

Zendesk US 2,060 43.18 58.6% 58.4% 10.5% 4,464 4,217 247 9.9x 7.5x 5.9x NM NM NM 31.7% 73.6% 6.2%

2U US 1,865 82.78 126.5% 71.2% 9.6% 4,364 4,163 223 14.6x 10.4x 7.8x NM NM NM 40.7% 81.1% 4.1%

RealPage US 5,462 52.25 54.8% 26.7% 6.2% 4,346 4,925 69 7.3x 5.9x 5.3x 30.4x 22.5x 22.5x 25.1% 62.8% 26.1%

HubSpot US 2,081 111.05 86.6% 61.9% 9.2% 4,204 3,998 504 10.8x 8.3x 6.6x NM NM NM 30.6% 82.1% 8.7%

MuleSoft US 1,188 30.88 NA 46.0% 21.9% 4,061 3,857 204 13.2x 9.4x 7.1x NM NM NM 41.1% 74.2% (9.3%)

New Relic US 1,253 71.78 104.0% 49.4% 15.9% 3,980 3,747 233 11.4x 8.8x 7.1x NM NM NM 29.5% NA 8.6%

Okta US 898 38.59 NA 57.8% 24.6% 3,933 3,710 224 14.3x 10.8x 8.1x NM NM NM 32.5% 72.6% (20.2%)

Medidata Solutions US 1,424 65.66 17.4% (9.5%) (8.5%) 3,841 3,732 484 6.8x 5.9x 5.0x 28.4x 22.8x 22.8x 16.8% 78.5% 25.7%

Wix IL 1,266 75.05 20.5% 23.9% 20.3% 3,412 3,179 233 7.5x 5.4x 4.3x 47.3x 30.0x 30.0x 40.1% 80.4% 17.8%

Box US 1,726 24.06 36.5% 22.6% 7.4% 3,304 3,182 208 6.3x 5.1x 4.1x NM NM NM 23.6% 74.6% 3.1%

Twilio US 900 34.16 7.7% 19.5% 28.8% 3,178 2,887 291 7.4x 5.6x 4.6x NM NM NM 31.6% 54.0% 1.8%

Qualys US 869 74.05 111.9% 62.6% 15.2% 2,860 2,572 288 11.2x 9.3x 7.9x 30.4x 26.3x 26.3x 20.5% 78.8% 35.3%

Cloudera US 1,470 19.05 NA 2.6% 1.7% 2,690 2,301 390 6.3x 5.0x 4.1x NM NM NM 26.9% 74.9% (18.7%)

Paylocity US 2,115 46.77 32.6% (0.3%) (5.8%) 2,460 2,349 111 7.1x 5.8x 4.7x 35.5x 27.8x 27.8x 22.1% NA 20.8%

Coupa Software US 652 44.60 68.6% 44.4% 16.4% 2,455 2,236 219 12.3x 9.9x 8.0x NM NM NM 24.5% 72.2% (3.5%)

Callidus Software US 1,300 35.90 90.5% 48.7% 11.3% 2,386 2,244 150 9.0x 7.4x 6.2x 71.1x 43.0x 43.0x 21.3% 66.0% 17.3%

Cornerstone OnDemand US 1,891 41.00 (1.8%) 19.3% (2.7%) 2,350 2,320 563 4.8x 4.6x 4.2x 35.5x 25.8x 25.8x 4.3% 75.5% 17.8%

Blackline US 726 44.00 54.2% 47.1% 30.9% 2,326 2,213 113 12.7x 9.9x 7.9x NM NM NM 27.7% 80.3% 4.6%

Share

Price

Market

Cap EV Cash EV/Revenue EV/EBITDA

CY

Revenue

Growth

Company Name HQ Employee 02-28-18 LTM L6M L1M (m) (m) (m) CY17A CY18E CY19E CY17A CY18E CY19E 18/17 Gross EBITDA

Share Price Performance

CY18E

Margins

29

Public Comps – GP Bullhound SaaS Index (Cont'd)

Source(s): Capital IQ as of 02/28/2018

Note: Multiples in excess of 75.0x or less than 0.0x are considered not-material (“NM”) and not taken into average calculation consideration

Alteryx US 515 $34.19 NA 51.7% 12.2% $2,023 $1,849 $174 14.4x 10.3x 7.8x NM NM NM 39.3% 84.0% (8.6%)

Mimecast UK 957 34.74 76.5% 27.3% 7.8% 2,008 1,920 129 8.1x 6.3x 5.3x NM 59.9x 59.9x 27.1% NA 10.6%

Q2 Holdings US 844 45.55 26.7% 10.7% 11.2% 1,914 1,815 100 9.4x 7.7x 6.3x NM NM NM 21.3% 52.4% 8.6%

Five9 US 840 30.36 90.8% 46.3% 14.4% 1,690 1,667 69 8.5x 7.2x 6.1x NM 62.7x 62.7x 18.2% 61.4% 11.4%

8x8 US 1,019 18.25 20.9% 38.8% 2.8% 1,682 1,521 161 5.4x 4.6x 3.8x 72.2x 73.0x 73.0x 17.5% NA 6.3%

MINDBODY US 1,440 35.65 34.3% 59.5% 1.4% 1,674 1,456 232 8.0x 6.2x 5.0x NM 65.8x 65.8x 28.2% 72.8% 9.5%

Appian US 859 27.04 NA 20.0% (13.9%) 1,642 1,569 74 9.3x 7.8x 6.6x NM NM NM 19.0% 65.0% (18.9%)

MongoDB US 930 32.21 NA NA 14.3% 1,629 1,341 289 8.8x 6.5x 4.8x NM NM NM 35.8% 70.5% (38.0%)

Instructure US 1,140 43.40 89.5% 44.9% 21.2% 1,448 1,406 41 9.0x 6.8x 5.3x NM NM NM 33.0% 73.5% (11.2%)

Talend FR 816 47.08 73.7% 20.9% 19.6% 1,372 1,286 87 8.7x 6.4x 5.0x NM NM NM 35.4% 78.3% (4.7%)

AppFolio US 672 40.10 61.4% (4.5%) (8.1%) 1,366 1,320 46 9.3x 7.3x 5.9x 49.0x 35.3x 35.3x 27.9% 61.9% 20.6%

Apptio US 753 28.90 122.5% 65.3% 11.1% 1,232 1,083 149 5.8x 4.9x 4.1x NM NM NM 19.8% 71.7% 2.6%

Yext US 750 12.70 NA (1.0%) 4.5% 1,159 1,045 113 6.1x 4.6x 3.5x NM NM NM 32.4% 74.9% (16.7%)

ForeScout Technologies US 818 29.78 NA NA (10.1%) 1,143 979 186 4.5x 3.7x 3.0x NM NM NM 23.0% 74.3% (12.5%)

SPS Commerce US 1,336 60.02 8.5% (0.3%) 14.0% 1,035 872 163 4.0x 3.6x 3.3x 27.4x 20.4x 20.4x 10.3% 67.6% 17.6%

Workiva US 1,318 22.75 52.2% 14.6% 2.7% 968 911 77 4.4x 3.9x 3.4x NM NM NM 13.8% 77.4% (12.1%)

Everbridge US 553 31.91 67.6% 41.6% (4.8%) 902 845 146 8.2x 6.2x 4.9x NM NM NM 31.7% 72.0% (2.4%)

LivePerson US 954 14.45 105.0% 12.5% 20.4% 860 804 56 3.7x 3.4x 3.0x 44.2x 37.1x 37.1x 9.8% 75.5% 9.1%

SecureWorks US 2,306 9.87 (5.5%) (5.6%) 1.8% 800 701 100 1.5x 1.4x 1.3x NM NM NM 8.4% 55.2% (1.4%)

Carbonite US 830 28.15 44.7% 48.5% 9.1% 787 770 128 3.1x 2.5x 2.2x 16.3x 9.9x 9.9x 24.3% 76.5% 25.5%

Benefitfocus US 1,430 24.20 (8.9%) (17.3%) (4.7%) 757 822 55 3.2x 2.9x 2.6x 43.4x 29.6x 29.6x 9.6% 54.1% 9.9%

Upland Software US 251 23.86 98.0% 5.2% (0.1%) 496 534 53 5.5x 4.4x 4.2x 17.9x 12.4x 12.4x 25.5% 67.3% 35.3%

Castlight Health US 381 3.55 0.0% (2.7%) (5.3%) 475 386 93 3.0x 2.5x 2.1x NM NM NM 17.2% 70.5% (7.0%)

MobileIron US 854 4.80 0.0% 28.0% 14.3% 461 368 93 2.1x 1.9x 1.7x NM NM NM 10.8% 85.4% (0.7%)

CLX Communications SE 340 7.39 (42.6%) (44.5%) (17.0%) 396 438 20 1.2x 1.0x 0.9x 11.8x 10.7x 10.7x 14.7% 24.0% 9.7%

Vitec Software Group SE 600 9.91 24.5% (2.3%) (5.6%) 296 338 7 3.3x 2.9x 2.9x 11.9x 10.4x 10.4x 12.0% 91.6% 28.3%

Amber Road US 677 9.10 20.7% 22.3% 21.3% 248 261 9 3.3x 3.1x 2.8x NM NM NM 8.6% 54.9% 2.1%

Brightcove US 498 6.85 (18.5%) (1.4%) (2.1%) 239 214 26 1.4x 1.3x 1.2x NM 54.8x 54.8x 7.4% 64.4% 2.3%

ChannelAdvisor US 737 8.85 (17.7%) (11.9%) (1.7%) 235 184 53 1.5x 1.4x 1.3x 39.3x 28.4x 28.4x 4.9% 79.2% 5.0%

Average 8.2x 6.3x 5.3x 38.5x 36.5x 36.5x 26.2% 71.7% 8.8%

Median 8.0x 6.3x 5.0x 36.0x 29.9x 29.9x 24.5% 74.3% 9.1%

Share

Price

Market

Cap EV Cash EV/Revenue EV/EBITDA

CY

Revenue

Growth

Company Name HQ Employee 02-28-18 LTM L6M L1M (m) (m) (m) CY17A CY18E CY19E CY17A CY18E CY19E 18/17 Gross EBITDA

Share Price Performance

CY18E

Margins

30

Key Sector Takeaways

Recent Software Transaction Trends

Public Market SaaS Analyses

Key SaaS Metrics

Appendix A: GP Bullhound SaaS Index

Appendix B: Software Public Comps by Category

1

2

3

4

6

7

8Appendix C: GP Bullhound Software Report

Overview, Software Credentials & Team

5 SaaS CEO Commentary

31

Public Comps – Large-Cap Consolidator

Source(s): Capital IQ as of 02/28/2018

Note: Multiples in excess of 75.0x or less than 0.0x are considered not-material (“NM”) and not taken into average calculation consideration

Microsoft US 124,000 $93.77 46.6% 28.8% (0.3%) $722,010 $676,663 $138,535 6.7x 6.1x 5.6x 17.0x 14.9x 13.1x 10.3% NA 40.6%

Intel US 102,700 49.29 36.2% 42.3% (1.6%) 230,677 243,488 14,002 3.9x 3.8x 3.6x 9.5x 9.0x 8.4x 4.6% 61.6% 41.5%

Cisco US 72,900 44.78 31.0% 42.0% 5.2% 215,728 181,437 73,683 3.8x 3.6x 3.5x 10.6x 10.5x 10.5x 4.0% NA 34.6%

Oracle US 138,000 50.67 19.0% 2.9% (3.9%) 209,754 199,282 71,580 5.1x 4.9x 4.7x 11.1x 10.6x 10.0x 4.0% NA 46.6%

IBM US 366,600 155.83 (13.3%) 9.3% (6.9%) 143,546 177,953 12,582 2.3x 2.2x 2.2x 9.3x 9.1x 9.0x 1.9% 47.6% 24.3%

SAP DE 88,543 105.56 12.8% 0.7% (7.6%) 126,551 126,629 6,005 4.5x 4.3x 4.0x 12.9x 12.4x 11.4x 5.2% 71.9% 34.3%

Hewlett Packard US 66,000 18.59 (18.5%) 4.5% 11.3% 29,131 35,451 7,673 1.1x 1.2x 1.1x 6.3x 6.7x 6.7x (7.1%) NA 17.2%

Average 3.9x 3.7x 3.5x 10.9x 10.5x 9.9x 3.3% 60.4% 34.2%

Median 3.9x 3.8x 3.6x 10.6x 10.5x 10.0x 4.0% 61.6% 34.6%

Share

Price

Market

Cap EV Cash EV/Revenue EV/EBITDA

CY

Revenue

Growth

Company Name HQ Employee 02-28-18 LTM L6M L1M (m) (m) (m) CY17A CY18E CY19E CY17A CY18E CY19E 18/17 Gross EBITDA

Share Price Performance

CY18E

Margins

32

Public Comps – Advertising Technology

Source(s): Capital IQ as of 02/28/2018

Note: Multiples in excess of 75.0x or less than 0.0x are considered not-material (“NM”) and not taken into average calculation consideration

Alphabet US 80,110 $1,103.92 30.7% 18.9% (7.0%) $767,836 $669,934 $101,871 6.1x 5.0x 4.3x 15.3x 13.0x 11.1x 21.2% 61.0% 38.6%

Adobe US 17,973 209.13 76.7% 37.8% 3.9% 102,804 98,867 5,820 13.6x 11.3x 9.6x 32.5x 25.2x 21.2x 21.0% 87.8% 44.8%

Salesforce US 29,401 116.25 42.9% 24.1% 2.2% 83,967 81,945 4,522 7.8x 6.5x 5.5x 36.5x 29.8x 23.7x 20.2% 76.6% 21.9%

Teradata US 10,615 36.82 18.4% 18.6% (9.9%) 4,492 4,181 1,089 2.0x 1.9x 1.9x 11.3x 10.9x 10.4x 2.0% 53.1% 17.6%

Hubspot US 2,081 111.05 86.6% 61.9% 9.2% 4,204 3,998 504 10.8x 8.3x 6.6x NM NM 62.8x 30.6% 82.1% 8.7%

Callidus Software US 1,300 35.90 90.5% 48.7% 11.3% 2,386 2,244 150 9.0x 7.4x 6.2x 71.1x 43.0x 29.9x 21.3% 66.0% 17.3%

Trade Desk US 713 56.26 33.3% 9.5% 9.8% 2,354 2,226 156 7.2x 5.5x 4.4x 24.4x 18.8x 13.8x 31.5% 78.5% 29.2%

Criteo FR 2,764 29.99 (36.2%) (35.2%) 20.2% 1,982 1,588 414 1.7x 1.6x 1.4x 5.4x 5.2x 4.5x 9.9% 86.7% 29.8%

TechTarget US 659 17.28 88.9% 78.0% 11.5% 475 474 34 4.4x 3.9x 3.4x 21.9x 16.3x 12.8x 13.1% 74.1% 23.7%

ChannelAdvisor US 737 8.85 (17.7%) (11.9%) (1.7%) 235 184 53 1.5x 1.4x 1.3x 39.3x 28.4x 19.8x 4.9% 79.2% 5.0%

Average 6.4x 5.3x 4.5x 28.6x 21.2x 21.0x 17.6% 74.5% 23.7%

Median 6.7x 5.3x 4.3x 24.4x 18.8x 16.8x 20.6% 77.5% 22.8%

Share

Price

Market

Cap EV Cash EV/Revenue EV/EBITDA

CY

Revenue

Growth

Company Name HQ Employee 02-28-18 LTM L6M L1M (m) (m) (m) CY17A CY18E CY19E CY17A CY18E CY19E 18/17 Gross EBITDA

Share Price Performance

CY18E

Margins

33

Public Comps – Business Intelligence/Analytics

Source(s): Capital IQ as of 02/28/2018

Note: Multiples in excess of 75.0x or less than 0.0x are considered not-material (“NM”) and not taken into average calculation consideration

Alphabet US 80,110 $1,103.92 30.7% 18.9% (7.0%) $767,836 $669,934 $101,871 6.1x 5.0x 4.3x 15.3x 13.0x 11.1x 21.2% 61.0% 38.6%

IBM US 366,600 155.83 (13.3%) 9.3% (6.9%) 143,546 177,953 12,582 2.3x 2.2x 2.2x 9.3x 9.1x 9.0x 1.9% 47.6% 24.3%

SAP DE 88,543 105.56 12.8% 0.7% (7.6%) 126,551 126,629 6,005 4.5x 4.3x 4.0x 12.9x 12.4x 11.4x 5.2% 71.9% 34.3%

Adobe US 17,973 209.13 76.7% 37.8% 3.9% 102,804 98,867 5,820 13.6x 11.3x 9.6x 32.5x 25.2x 21.2x 21.0% 87.8% 44.8%

NetApp US 10,100 60.55 44.8% 57.9% (4.4%) 16,223 12,769 5,626 2.2x 2.1x 2.0x 9.8x 9.2x 8.5x 5.8% NA 22.9%

Splunk US 2,700 93.20 51.0% 44.5% 0.8% 13,184 12,203 1,165 9.8x 7.8x 6.1x NM 57.2x 38.8x 25.5% 83.0% 13.7%

Tableau Software US 3,489 81.67 54.9% 13.9% 6.3% 6,659 5,804 855 6.7x 6.0x 5.3x NM NM 63.8x 11.3% 87.4% 5.0%

Fair Isaac US 3,358 169.94 30.7% 22.2% (0.1%) 5,111 5,680 94 6.0x 5.6x 5.2x 24.9x 20.6x 19.1x 7.1% NA 27.1%

Blackbaud US 3,182 102.52 43.3% 21.9% 6.0% 4,800 5,208 30 6.6x 5.9x 5.4x 26.8x 24.6x 21.8x 11.3% 58.3% 24.1%

Teradata US 10,615 36.82 18.4% 18.6% (9.9%) 4,492 4,181 1,089 2.0x 1.9x 1.9x 11.3x 10.9x 10.4x 2.0% 53.1% 17.6%

New Relic US 1,253 71.78 104.0% 49.4% 15.9% 3,980 3,747 233 11.4x 8.8x 7.1x NM NM 56.0x 29.5% NA 8.6%

Cloudera US 1,470 19.05 NA 2.6% 1.7% 2,690 2,301 390 6.3x 5.0x 4.1x NM NM NM 26.9% 74.9% (18.7%)

Verint US 5,000 38.90 3.0% 0.5% (8.9%) 2,481 2,945 319 2.6x 2.4x 2.3x 11.4x 10.4x 9.0x 7.1% 65.3% 23.1%

Alteryx US 515 34.19 NA 51.7% 12.2% 2,023 1,849 174 14.4x 10.3x 7.8x NM NM NM 39.3% 84.0% (8.6%)

Inovalon US 2,119 12.00 0.0% (8.7%) (11.8%) 1,733 1,505 476 3.3x 3.2x 3.0x 13.8x 12.9x 11.7x 4.3% 67.4% 24.8%

MicroStrategy US 2,216 127.98 (33.3%) 1.3% (7.1%) 1,465 790 675 1.6x 1.6x 1.5x 7.7x 12.3x 10.9x 1.4% 80.6% 12.7%

Talend FR 816 47.08 73.7% 20.9% 19.6% 1,372 1,286 87 8.7x 6.4x 5.0x NM NM NM 35.4% 78.3% (4.7%)

Hortonworks US 1,150 17.98 80.9% 12.2% (12.4%) 1,305 1,233 73 4.8x 3.8x 3.0x NM 14.1x 6.8x 27.4% 73.7% 26.7%

Apptio US 753 28.90 122.5% 65.3% 11.1% 1,232 1,083 149 5.8x 4.9x 4.1x NM NM 67.4x 19.8% 71.7% 2.6%

Yext US 750 12.70 NA (1.0%) 4.5% 1,159 1,045 113 6.1x 4.6x 3.5x NM NM NM 32.4% 74.9% (16.7%)

SAS AB SE 9,929 2.57 56.3% 11.4% 3.3% 985 862 1,176 0.2x 0.2x 0.2x 1.8x 1.9x 1.9x (3.6%) NA 8.9%

Workiva US 1,318 22.75 52.2% 14.6% 2.7% 968 911 77 4.4x 3.9x 3.4x NM NM NM 13.8% 77.4% (12.1%)

LivePerson US 954 14.45 105.0% 12.5% 20.4% 860 804 56 3.7x 3.4x 3.0x 44.2x 37.1x 27.3x 9.8% 75.5% 9.1%

SDL UK 3,310 5.74 (4.5%) (3.4%) (13.9%) 472 436 34 1.1x 1.1x 1.0x 13.0x 10.2x 9.2x 7.7% 53.4% 10.3%

Gridsum CN 929 10.89 (7.2%) 16.2% (14.4%) 335 336 39 3.4x 2.1x 1.5x NM 16.4x 6.0x 60.1% NA 13.0%

iSentia AU 1,300 0.80 (33.0%) (39.7%) (29.7%) 159 198 11 1.8x 1.9x 1.8x 7.5x 7.8x 7.2x (6.9%) NA 24.3%

Attunity IL 253 7.33 (16.2%) 14.5% 3.4% 152 123 29 2.0x 1.7x 1.4x 31.8x 23.3x NA 19.3% 85.7% 7.1%

Datawatch US 144 9.35 23.0% (5.1%) (16.5%) 115 86 30 2.3x 2.0x NA NM NM NA 13.1% NA 2.4%

Hottolink JP 88 6.63 50.1% 13.6% (12.7%) 86 89 10 NA NA NA NA NA NA NA NA NA

Mattersight US 265 2.35 (33.8%) 6.8% (17.5%) 78 97 9 2.1x 2.0x 1.8x NM NM 31.2x 8.5% 72.2% 1.2%

Expert System IT 238 1.61 (12.5%) (20.7%) (5.0%) 57 69 13 2.4x 2.1x 2.0x NM 18.2x 9.6x 12.5% NA 11.6%

Marin Software US 437 7.80 (51.6%) 1.3% (17.9%) 44 20 28 NA NA NA NA NA NA NA NA NA

Average 4.9x 4.1x 3.6x 17.1x 17.3x 20.4x 15.7% 72.0% 12.6%

Median 4.0x 3.6x 3.0x 12.9x 12.9x 11.1x 11.9% 74.3% 12.1%

Share

Price

Market

Cap EV Cash EV/Revenue EV/EBITDA

CY

Revenue

Growth

Company Name HQ Employee 02-28-18 LTM L6M L1M (m) (m) (m) CY17A CY18E CY19E CY17A CY18E CY19E 18/17 Gross EBITDA

Share Price Performance

CY18E

Margins

34

Public Comps – Communication

Source(s): Capital IQ as of 02/28/2018

Note: Multiples in excess of 75.0x or less than 0.0x are considered not-material (“NM”) and not taken into average calculation consideration

Microsoft US 124,000 $93.77 46.6% 28.8% (0.3%) $722,010 $676,663 $138,535 6.7x 6.1x 5.6x 17.0x 14.9x 13.1x 10.3% NA 40.6%

Cisco US 72,900 44.78 31.0% 42.0% 5.2% 215,728 181,437 73,683 3.8x 3.6x 3.5x 10.6x 10.5x 10.5x 4.0% NA 34.6%

Atlassian UK 2,408 54.29 90.9% 56.5% 0.8% 12,608 11,929 679 16.3x 12.3x 9.7x 60.9x 43.1x 35.9x 32.6% NA 28.5%

Citrix US 7,500 92.00 16.5% 21.7% (2.9%) 12,526 12,906 1,748 4.6x 4.5x 4.3x 12.7x 13.6x 13.1x 1.9% 87.0% 32.9%

NICE Systems IL 4,930 97.60 40.5% 26.2% 6.7% 5,946 6,001 392 4.5x 4.2x 3.9x 15.8x 14.3x 12.9x 7.3% 70.4% 29.1%

RingCentral US 1,352 62.65 134.6% 62.1% 13.0% 4,929 4,748 181 9.5x 7.5x 6.1x NM 65.5x 50.2x 27.3% 77.9% 11.4%

Nuance US 11,600 16.06 (5.7%) 2.0% (11.5%) 4,717 6,506 511 3.3x 3.1x 3.0x 11.1x 10.5x 9.7x 5.1% NA 29.7%

j2 Global US 2,426 74.02 (9.1%) 1.0% (6.7%) 3,583 4,234 351 3.8x 3.5x 3.2x 9.0x 8.6x 7.7x 9.0% 84.5% 40.3%

Twilio US 900 34.16 7.7% 19.5% 28.8% 3,178 2,887 291 7.4x 5.6x 4.6x NM NM NM 31.6% 54.0% 1.8%

8x8 US 1,019 18.25 20.9% 38.8% 2.8% 1,682 1,521 161 5.4x 4.6x 3.8x 72.2x 73.0x 39.8x 17.5% NA 6.3%

Everbridge US 553 31.91 67.6% 41.6% (4.8%) 902 845 146 8.2x 6.2x 4.9x NM NM NM 31.7% 72.0% (2.4%)

LivePerson US 954 14.45 105.0% 12.5% 20.4% 860 804 56 3.7x 3.4x 3.0x 44.2x 37.1x 27.3x 9.8% 75.5% 9.1%

Synchronoss US 1,765 9.34 (65.5%) (44.1%) 12.3% 444 568 194 1.2x 1.4x 1.5x 4.9x 6.9x 8.7x (14.7%) 62.2% 20.4%

CLX Communications SE 340 7.39 (42.6%) (44.5%) (17.0%) 396 438 20 1.2x 1.0x 0.9x 11.8x 10.7x 9.0x 14.7% 24.0% 9.7%

Cybozu JP 516 5.16 34.2% 13.7% (11.3%) 237 220 16 NA NA NA NA NA NA NA NA NA

V-cube JP 450 4.79 (14.7%) (12.5%) (6.0%) 115 137 30 NA NA NA NA NA NA NA NA NA

Average 5.7x 4.8x 4.2x 24.6x 25.7x 19.8x 13.4% 67.5% 20.9%

Median 4.5x 4.3x 3.8x 12.7x 14.0x 13.0x 10.1% 72.0% 24.4%

Share

Price

Market

Cap EV Cash EV/Revenue EV/EBITDA

CY

Revenue

Growth

Company Name HQ Employee 02-28-18 LTM L6M L1M (m) (m) (m) CY17A CY18E CY19E CY17A CY18E CY19E 18/17 Gross EBITDA

Share Price Performance

CY18E

Margins

35

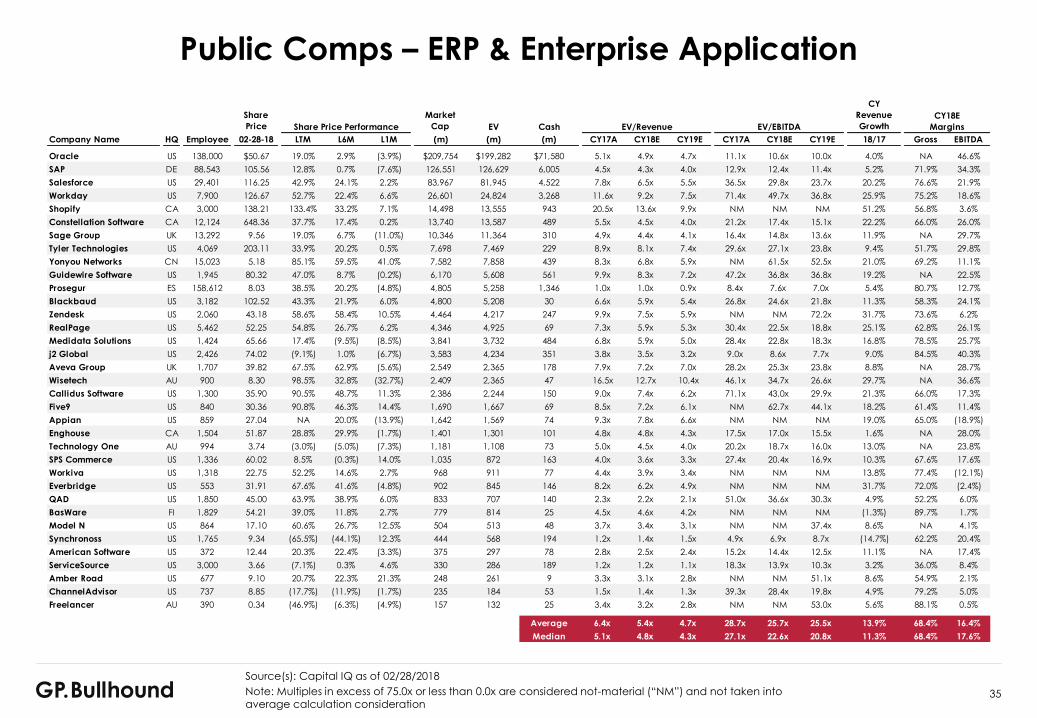

Public Comps – ERP & Enterprise Application

Source(s): Capital IQ as of 02/28/2018

Note: Multiples in excess of 75.0x or less than 0.0x are considered not-material (“NM”) and not taken into average calculation consideration

Oracle US 138,000 $50.67 19.0% 2.9% (3.9%) $209,754 $199,282 $71,580 5.1x 4.9x 4.7x 11.1x 10.6x 10.0x 4.0% NA 46.6%

SAP DE 88,543 105.56 12.8% 0.7% (7.6%) 126,551 126,629 6,005 4.5x 4.3x 4.0x 12.9x 12.4x 11.4x 5.2% 71.9% 34.3%

Salesforce US 29,401 116.25 42.9% 24.1% 2.2% 83,967 81,945 4,522 7.8x 6.5x 5.5x 36.5x 29.8x 23.7x 20.2% 76.6% 21.9%

Workday US 7,900 126.67 52.7% 22.4% 6.6% 26,601 24,824 3,268 11.6x 9.2x 7.5x 71.4x 49.7x 36.8x 25.9% 75.2% 18.6%

Shopify CA 3,000 138.21 133.4% 33.2% 7.1% 14,498 13,555 943 20.5x 13.6x 9.9x NM NM NM 51.2% 56.8% 3.6%

Constellation Software CA 12,124 648.36 37.7% 17.4% 0.2% 13,740 13,587 489 5.5x 4.5x 4.0x 21.2x 17.4x 15.1x 22.2% 66.0% 26.0%

Sage Group UK 13,292 9.56 19.0% 6.7% (11.0%) 10,346 11,364 310 4.9x 4.4x 4.1x 16.4x 14.8x 13.6x 11.9% NA 29.7%

Tyler Technologies US 4,069 203.11 33.9% 20.2% 0.5% 7,698 7,469 229 8.9x 8.1x 7.4x 29.6x 27.1x 23.8x 9.4% 51.7% 29.8%

Yonyou Networks CN 15,023 5.18 85.1% 59.5% 41.0% 7,582 7,858 439 8.3x 6.8x 5.9x NM 61.5x 52.5x 21.0% 69.2% 11.1%

Guidewire Software US 1,945 80.32 47.0% 8.7% (0.2%) 6,170 5,608 561 9.9x 8.3x 7.2x 47.2x 36.8x 36.8x 19.2% NA 22.5%

Prosegur ES 158,612 8.03 38.5% 20.2% (4.8%) 4,805 5,258 1,346 1.0x 1.0x 0.9x 8.4x 7.6x 7.0x 5.4% 80.7% 12.7%

Blackbaud US 3,182 102.52 43.3% 21.9% 6.0% 4,800 5,208 30 6.6x 5.9x 5.4x 26.8x 24.6x 21.8x 11.3% 58.3% 24.1%

Zendesk US 2,060 43.18 58.6% 58.4% 10.5% 4,464 4,217 247 9.9x 7.5x 5.9x NM NM 72.2x 31.7% 73.6% 6.2%

RealPage US 5,462 52.25 54.8% 26.7% 6.2% 4,346 4,925 69 7.3x 5.9x 5.3x 30.4x 22.5x 18.8x 25.1% 62.8% 26.1%

Medidata Solutions US 1,424 65.66 17.4% (9.5%) (8.5%) 3,841 3,732 484 6.8x 5.9x 5.0x 28.4x 22.8x 18.3x 16.8% 78.5% 25.7%

j2 Global US 2,426 74.02 (9.1%) 1.0% (6.7%) 3,583 4,234 351 3.8x 3.5x 3.2x 9.0x 8.6x 7.7x 9.0% 84.5% 40.3%

Aveva Group UK 1,707 39.82 67.5% 62.9% (5.6%) 2,549 2,365 178 7.9x 7.2x 7.0x 28.2x 25.3x 23.8x 8.8% NA 28.7%

Wisetech AU 900 8.30 98.5% 32.8% (32.7%) 2,409 2,365 47 16.5x 12.7x 10.4x 46.1x 34.7x 26.6x 29.7% NA 36.6%

Callidus Software US 1,300 35.90 90.5% 48.7% 11.3% 2,386 2,244 150 9.0x 7.4x 6.2x 71.1x 43.0x 29.9x 21.3% 66.0% 17.3%

Five9 US 840 30.36 90.8% 46.3% 14.4% 1,690 1,667 69 8.5x 7.2x 6.1x NM 62.7x 44.1x 18.2% 61.4% 11.4%

Appian US 859 27.04 NA 20.0% (13.9%) 1,642 1,569 74 9.3x 7.8x 6.6x NM NM NM 19.0% 65.0% (18.9%)

Enghouse CA 1,504 51.87 28.8% 29.9% (1.7%) 1,401 1,301 101 4.8x 4.8x 4.3x 17.5x 17.0x 15.5x 1.6% NA 28.0%

Technology One AU 994 3.74 (3.0%) (5.0%) (7.3%) 1,181 1,108 73 5.0x 4.5x 4.0x 20.2x 18.7x 16.0x 13.0% NA 23.8%

SPS Commerce US 1,336 60.02 8.5% (0.3%) 14.0% 1,035 872 163 4.0x 3.6x 3.3x 27.4x 20.4x 16.9x 10.3% 67.6% 17.6%

Workiva US 1,318 22.75 52.2% 14.6% 2.7% 968 911 77 4.4x 3.9x 3.4x NM NM NM 13.8% 77.4% (12.1%)

Everbridge US 553 31.91 67.6% 41.6% (4.8%) 902 845 146 8.2x 6.2x 4.9x NM NM NM 31.7% 72.0% (2.4%)

QAD US 1,850 45.00 63.9% 38.9% 6.0% 833 707 140 2.3x 2.2x 2.1x 51.0x 36.6x 30.3x 4.9% 52.2% 6.0%

BasWare FI 1,829 54.21 39.0% 11.8% 2.7% 779 814 25 4.5x 4.6x 4.2x NM NM NM (1.3%) 89.7% 1.7%

Model N US 864 17.10 60.6% 26.7% 12.5% 504 513 48 3.7x 3.4x 3.1x NM NM 37.4x 8.6% NA 4.1%

Synchronoss US 1,765 9.34 (65.5%) (44.1%) 12.3% 444 568 194 1.2x 1.4x 1.5x 4.9x 6.9x 8.7x (14.7%) 62.2% 20.4%

American Software US 372 12.44 20.3% 22.4% (3.3%) 375 297 78 2.8x 2.5x 2.4x 15.2x 14.4x 12.5x 11.1% NA 17.4%

ServiceSource US 3,000 3.66 (7.1%) 0.3% 4.6% 330 286 189 1.2x 1.2x 1.1x 18.3x 13.9x 10.3x 3.2% 36.0% 8.4%

Amber Road US 677 9.10 20.7% 22.3% 21.3% 248 261 9 3.3x 3.1x 2.8x NM NM 51.1x 8.6% 54.9% 2.1%

ChannelAdvisor US 737 8.85 (17.7%) (11.9%) (1.7%) 235 184 53 1.5x 1.4x 1.3x 39.3x 28.4x 19.8x 4.9% 79.2% 5.0%

Freelancer AU 390 0.34 (46.9%) (6.3%) (4.9%) 157 132 25 3.4x 3.2x 2.8x NM NM 53.0x 5.6% 88.1% 0.5%

Average 6.4x 5.4x 4.7x 28.7x 25.7x 25.5x 13.9% 68.4% 16.4%

Median 5.1x 4.8x 4.3x 27.1x 22.6x 20.8x 11.3% 68.4% 17.6%

Share

Price

Market

Cap EV Cash EV/Revenue EV/EBITDA

CY

Revenue

Growth

Company Name HQ Employee 02-28-18 LTM L6M L1M (m) (m) (m) CY17A CY18E CY19E CY17A CY18E CY19E 18/17 Gross EBITDA

Share Price Performance

CY18E

Margins

36

Public Comps – Financial Application

Source(s): Capital IQ as of 02/28/2018

Note: Multiples in excess of 75.0x or less than 0.0x are considered not-material (“NM”) and not taken into average calculation consideration

Intuit US 8,200 $166.86 33.0% 21.0% (2.1%) $42,735 $43,112 $726 7.9x 7.2x 6.6x 21.6x 19.7x 17.9x 9.6% NA 36.8%

Fidelity National US 53,000 97.18 18.1% 5.9% (5.5%) 32,184 40,391 665 4.4x 4.7x 4.5x 13.2x 12.9x 12.1x (6.3%) 39.5% 36.5%

Fiserv US 24,000 143.39 24.3% 16.7% 0.6% 29,626 34,201 325 6.0x 5.8x 5.6x 16.9x 16.2x 15.2x 3.7% 46.7% 35.9%

MSCI US 3,038 141.52 49.6% 24.2% 0.7% 12,729 13,918 890 10.9x 9.7x 8.8x 21.1x 17.7x 15.9x 13.3% 79.2% 54.4%

SS&C US 8,001 49.52 41.4% 30.2% (1.2%) 10,228 12,209 64 7.3x 6.9x 6.6x 17.6x 16.1x 14.9x 5.9% 57.9% 42.6%

Jack Henry & Associates US 5,972 117.30 25.1% 16.7% (7.3%) 9,063 9,105 58 6.2x 5.8x 5.5x 17.6x 17.1x 16.0x 6.6% NA 34.1%

Temenos CH 4,356 117.49 51.7% 22.0% (14.8%) 8,258 8,540 168 11.7x 10.1x 9.1x 33.3x 26.9x 23.6x 16.0% 82.0% 37.5%

Black Knight US 4,430 47.65 NA NA (7.6%) 7,154 8,577 16 8.1x 7.7x 7.1x 16.9x 15.9x 14.5x 5.7% NA 48.2%

Oracle Financial IN 9,064 60.38 7.6% 11.0% (9.0%) 5,157 4,705 462 6.7x 6.1x 5.6x 16.5x 15.0x 14.0x 9.8% NA 40.3%

Fair Isaac US 3,358 169.94 30.7% 22.2% (0.1%) 5,111 5,680 94 6.0x 5.6x 5.2x 24.9x 20.6x 19.1x 7.1% NA 27.1%

Ellie Mae US 1,280 88.67 (7.2%) 8.8% (8.9%) 3,035 2,794 241 6.8x 5.6x 4.8x 23.4x 21.4x 16.0x 20.7% 59.4% 26.2%

Ebix US 4,515 83.95 34.3% 47.3% (0.2%) 2,641 2,923 89 8.2x 7.0x 6.2x 23.8x 19.0x 17.2x 17.6% 65.4% 36.7%

SimCorp DK 1,547 62.87 12.7% 5.3% (0.9%) 2,477 2,475 38 6.1x 5.4x 5.0x 23.4x 19.5x 17.7x 13.1% 61.4% 27.6%

Envestnet US 3,197 55.10 42.6% 29.3% 1.3% 2,441 2,622 60 3.9x 3.2x 2.9x 21.6x 17.1x 14.2x 20.4% 64.0% 18.7%

Fidessa UK 1,705 51.74 65.7% 91.3% 50.4% 1,994 1,866 125 3.9x 3.9x 3.8x 17.2x 17.3x 16.0x 0.9% NA 22.5%

Q2 Holdings US 844 45.55 26.7% 10.7% 11.2% 1,914 1,815 100 9.4x 7.7x 6.3x NM NM 53.9x 21.3% 52.4% 8.6%

Bottomline Technologies US 1,600 37.98 52.2% 28.9% 2.2% 1,545 1,621 74 4.5x 4.0x 3.7x 19.5x 17.8x 15.0x 10.7% NA 22.7%

MYOB AU 1,500 2.46 (10.7%) (13.1%) (11.4%) 1,489 1,784 43 5.4x 4.9x 4.5x 12.0x 11.6x 10.6x 11.3% 90.1% 41.9%

IRESS AU 1,881 8.09 (11.2%) (14.9%) (17.2%) 1,372 1,500 22 4.5x 4.1x 3.9x 16.9x 15.1x 13.7x 8.8% 26.7% 27.5%

Apptio US 753 28.90 122.5% 65.3% 11.1% 1,232 1,083 149 5.8x 4.9x 4.1x NM NM 67.4x 19.8% 71.7% 2.6%

Asseco PL 22,364 13.81 0.2% 8.6% (4.3%) 1,147 1,248 134 0.6x 0.5x 0.5x 4.7x 3.9x 4.0x 17.2% 22.8% 12.4%

Average 6.4x 5.7x 5.2x 19.1x 16.9x 19.5x 11.1% 58.5% 30.5%

Median 6.1x 5.6x 5.2x 17.6x 17.1x 15.9x 10.7% 60.4% 34.1%

Share

Price

Market

Cap EV Cash EV/Revenue EV/EBITDA

CY

Revenue

Growth

Company Name HQ Employee 02-28-18 LTM L6M L1M (m) (m) (m) CY17A CY18E CY19E CY17A CY18E CY19E 18/17 Gross EBITDA

Share Price Performance

CY18E

Margins

37

Public Comps – Human Capital Management

Source(s): Capital IQ as of 02/28/2018

Note: Multiples in excess of 75.0x or less than 0.0x are considered not-material (“NM”) and not taken into average calculation consideration

ADP US 58,000 $115.32 12.4% 10.1% (5.7%) $51,118 $51,344 $1,777 4.0x 3.7x 3.5x 19.8x 17.7x 16.0x 7.8% NA 21.2%

ServiceNow US 6,222 161.01 85.2% 43.9% 7.5% 28,128 27,523 1,779 14.4x 10.8x 8.4x 65.4x 42.2x 29.5x 33.3% 79.5% 25.5%

Workday US 7,900 126.67 52.7% 22.4% 6.6% 26,601 24,824 3,268 11.6x 9.2x 7.5x 71.4x 49.7x 36.8x 25.9% 75.2% 18.6%

Ultimate Software US 4,208 238.46 23.3% 21.3% 2.6% 7,291 7,135 165 7.6x 6.4x 5.4x 33.2x 25.8x 21.3x 19.2% 65.0% 24.9%

Paycom US 2,548 98.92 83.8% 36.0% 6.4% 5,854 5,844 46 13.5x 10.8x 8.7x 44.0x 26.8x 21.9x 25.8% 83.6% 40.1%

TriNet US 2,700 47.17 75.7% 33.0% 7.0% 3,305 3,392 336 4.2x 4.0x 3.7x 12.2x 11.0x 10.0x 6.4% 74.4% 36.2%

Paylocity US 2,115 46.77 32.6% (0.3%) (5.8%) 2,460 2,349 111 7.1x 5.8x 4.7x 35.5x 27.8x 22.1x 22.1% NA 20.8%

Callidus Software US 1,300 35.90 90.5% 48.7% 11.3% 2,386 2,244 150 9.0x 7.4x 6.2x 71.1x 43.0x 29.9x 21.3% 66.0% 17.3%

Cornerstone OnDemand US 1,891 41.00 (1.8%) 19.3% (2.7%) 2,350 2,320 563 4.8x 4.6x 4.2x 35.5x 25.8x 18.2x 4.3% 75.5% 17.8%

WageWorks US 1,958 52.45 (31.9%) (11.2%) (14.6%) 2,079 1,431 892 3.0x 2.7x 2.5x 9.8x 8.5x 7.5x 8.9% 65.1% 32.1%

Instructure US 1,140 43.40 89.5% 44.9% 21.2% 1,448 1,406 41 9.0x 6.8x 5.3x NM NM NM 33.0% 73.5% (11.2%)

Benefitfocus US 1,430 24.20 (8.9%) (17.3%) (4.7%) 757 822 55 3.2x 2.9x 2.6x 43.4x 29.6x 21.2x 9.6% 54.1% 9.9%

Upland Software US 251 23.86 98.0% 5.2% (0.1%) 496 534 53 5.5x 4.4x 4.2x 17.9x 12.4x 11.4x 25.5% 67.3% 35.3%

Solium CA 611 8.50 32.8% 3.6% (7.3%) 475 407 70 4.7x 4.1x 3.5x 37.8x 30.3x 18.2x 14.9% NA 13.4%

Freelancer AU 390 0.34 (46.9%) (6.3%) (4.9%) 157 132 25 3.4x 3.2x 2.8x NM NM 53.0x 5.6% 88.1% 0.5%

Average 7.0x 5.8x 4.9x 38.2x 27.0x 22.6x 17.6% 72.3% 20.2%

Median 5.5x 4.6x 4.2x 35.5x 26.8x 21.3x 19.2% 73.9% 20.8%

Share

Price

Market

Cap EV Cash EV/Revenue EV/EBITDA

CY

Revenue

Growth

Company Name HQ Employee 02-28-18 LTM L6M L1M (m) (m) (m) CY17A CY18E CY19E CY17A CY18E CY19E 18/17 Gross EBITDA

Share Price Performance

CY18E

Margins

38

Public Comps – Infrastructure

Source(s): Capital IQ as of 02/28/2018

Note: Multiples in excess of 75.0x or less than 0.0x are considered not-material (“NM”) and not taken into average calculation consideration

VMware US 18,905 $131.75 46.6% 25.9% (12.2%) $53,113 $45,733 $11,653 5.8x 5.3x 4.9x 15.6x 14.4x 12.8x 9.8% 88.1% 36.8%

ServiceNow US 6,222 161.01 85.2% 43.9% 7.5% 28,128 27,523 1,779 14.4x 10.8x 8.4x 65.4x 42.2x 29.5x 33.3% 79.5% 25.5%

Red Hat US 10,500 147.40 78.0% 39.6% 9.0% 26,090 25,137 1,716 9.1x 7.7x 6.8x 33.6x 28.0x 23.0x 17.4% NA 27.7%

Symantec US 13,000 26.29 (8.0%) (12.1%) (5.1%) 16,340 19,395 2,532 3.9x 4.0x 3.8x 8.5x 8.5x 7.3x (1.6%) NA 47.2%

Splunk US 2,700 93.20 51.0% 44.5% 0.8% 13,184 12,203 1,165 9.8x 7.8x 6.1x NM 57.2x 38.8x 25.5% 83.0% 13.7%

Atlassian UK 2,408 54.29 90.9% 56.5% 0.8% 12,608 11,929 679 16.3x 12.3x 9.7x 60.9x 43.1x 35.9x 32.6% NA 28.5%

Citrix US 7,500 92.00 16.5% 21.7% (2.9%) 12,526 12,906 1,748 4.6x 4.5x 4.3x 12.7x 13.6x 13.1x 1.9% 87.0% 32.9%

Micro Focus UK 16,100 28.46 (2.9%) (11.8%) (8.4%) 12,409 16,726 730 6.7x 4.0x 4.1x 16.7x 10.5x 9.7x 67.2% NA 38.0%

Akamai Technologies US 7,650 67.46 7.8% 49.4% (0.2%) 11,411 11,362 712 4.6x 4.2x 3.8x 12.3x 11.4x 10.1x 8.6% 66.2% 36.9%

F5 Networks US 4,276 148.52 3.7% 26.2% 7.4% 9,185 8,181 1,005 3.9x 3.8x 3.7x 9.9x 9.8x NA 3.4% NA 38.6%

Juniper Networks US 9,381 25.66 (8.4%) (6.8%) (9.0%) 8,821 8,004 3,033 1.6x 1.7x 1.6x 5.9x 7.4x 6.6x (5.9%) 59.4% 22.8%

Trend Micro JP 5,627 56.97 29.7% 22.5% 1.8% 7,841 6,413 1,353 4.9x 4.2x 4.0x 14.3x 12.8x 12.0x 16.8% 80.9% 32.7%

LogMeIn US 2,760 115.55 25.9% 3.2% (8.2%) 6,058 5,806 252 5.7x 5.0x 4.7x 15.7x 12.9x 11.7x 13.7% 84.5% 39.0%

Nutanix US 3,009 36.45 21.5% 64.2% 10.5% 5,847 5,482 918 5.6x 4.8x 3.9x NM NM 71.2x 16.9% NA 1.8%

Proofpoint US 2,047 107.17 36.1% 18.1% 3.8% 5,417 5,283 332 10.4x 8.0x 6.2x NM 59.1x 41.3x 30.4% 77.0% 13.4%

Pure Storage US 2,000 21.67 90.1% 52.1% 8.8% 4,698 4,146 597 4.1x 3.1x 2.5x NM 48.3x 26.9x 31.2% 65.6% 6.4%

MuleSoft US 1,188 30.88 NA 46.0% 21.9% 4,061 3,857 204 13.2x 9.4x 7.1x NM NM NM 41.1% 74.2% (9.3%)

New Relic US 1,253 71.78 104.0% 49.4% 15.9% 3,980 3,747 233 11.4x 8.8x 7.1x NM NM 56.0x 29.5% NA 8.6%

Software AG DE 4,596 52.84 NA NA (1.6%) 3,909 3,811 471 3.6x 3.5x 3.3x 11.3x 11.2x 10.4x 3.4% 76.4% 31.0%

Sophos UK 3,293 6.88 98.3% 4.3% (24.1%) 3,216 3,444 81 6.1x 4.9x 4.1x 61.5x 48.5x 33.9x 22.5% NA 10.2%

FireEye US 2,960 16.59 47.3% 14.7% 5.1% 3,178 3,061 897 4.1x 3.7x 3.5x 35.0x 29.3x 23.6x 10.3% 73.5% 12.8%

Qualys US 869 74.05 111.9% 62.6% 15.2% 2,860 2,572 288 11.2x 9.3x 7.9x 30.4x 26.3x 22.2x 20.5% 78.8% 35.3%

Commvault US 2,656 52.05 6.1% (13.0%) (6.9%) 2,339 1,894 445 2.7x 2.5x 2.3x 21.6x 17.8x 13.5x 9.8% NA 14.1%

NetScout Systems US 3,090 26.55 (28.1%) (18.7%) (0.4%) 2,317 2,237 380 2.1x 2.2x 2.2x 8.5x 11.0x 10.1x (7.5%) NA 20.1%

Progress Software US 1,470 46.87 63.4% 40.8% (7.4%) 2,174 2,112 184 5.3x 5.2x 5.2x 11.5x 11.0x 10.9x 1.9% 88.1% 47.6%

Mimecast UK 957 34.74 76.5% 27.3% 7.8% 2,008 1,920 129 8.1x 6.3x 5.3x NM 59.9x 43.1x 27.1% NA 10.6%

Alarm.com US 784 36.14 26.6% (19.1%) (4.0%) 1,706 1,680 96 5.0x 4.4x 3.9x 24.3x 20.5x 16.9x 14.3% 70.2% 21.5%

Talend FR 816 47.08 73.7% 20.9% 19.6% 1,372 1,286 87 8.7x 6.4x 5.0x NM NM NM 35.4% 78.3% (4.7%)

Extreme Networks US 1,628 11.41 82.6% 2.4% (17.6%) 1,315 1,370 128 1.8x 1.2x 1.1x 15.5x 9.5x NA 43.5% NA 12.9%

Hortonworks US 1,150 17.98 80.9% 12.2% (12.4%) 1,305 1,233 73 4.8x 3.8x 3.0x NM 14.1x 6.8x 27.4% 73.7% 26.7%

Rapid7 US 1,000 26.41 74.3% 63.5% 5.6% 1,185 1,094 91 5.5x 4.7x 3.9x NM NM NM 16.2% 73.7% (7.2%)

SecureWorks US 2,306 9.87 (5.5%) (5.6%) 1.8% 800 701 100 1.5x 1.4x 1.3x NM NM 29.9x 8.4% 55.2% (1.4%)

A10 Networks US 837 6.28 (33.6%) (2.3%) (9.6%) 444 320 124 1.4x 1.3x 1.2x 28.7x 25.4x 16.1x 4.5% 76.9% 5.2%

Metaps JP 246 25.83 (11.9%) (12.1%) (6.8%) 347 318 65 2.5x 1.4x 1.4x 67.0x NM NM 80.4% NA 1.1%