POWER SECTOR TRANSFORMATION - Energy...

32

1 POWER SECTOR TRANSFORMATION

-

Upload

phungduong -

Category

Documents

-

view

218 -

download

0

Transcript of POWER SECTOR TRANSFORMATION - Energy...

1

POWER SECTOR TRANSFORMATION

2

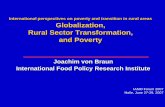

THE U.S. OPPORTUNITY CLEAN ENERGY NO LONGER ‘BOUTIQUE’

$0

$20

$40

$60

$80

$100

$120

$140

$160

0

10

20

30

40

50

60

70

80

2009 2010 2011 2012 2013 2014 2015

LEV

ELI

ZED

CO

ST

OF E

NER

GY

($

/MW

h)*

*

CU

MU

LATI

VE C

AP

AC

ITY

(G

W)

WIND COST & DEPLOYMENT

*Capacity - American Wind Energy Association 2015 Annual Market Report **LCOE - Lazard's Levelized Cost of Energy Analysis 2008-2015, avg. of high/low figures

Prices down

60% since 2009

Capacity more

than doubled

since 2009

3

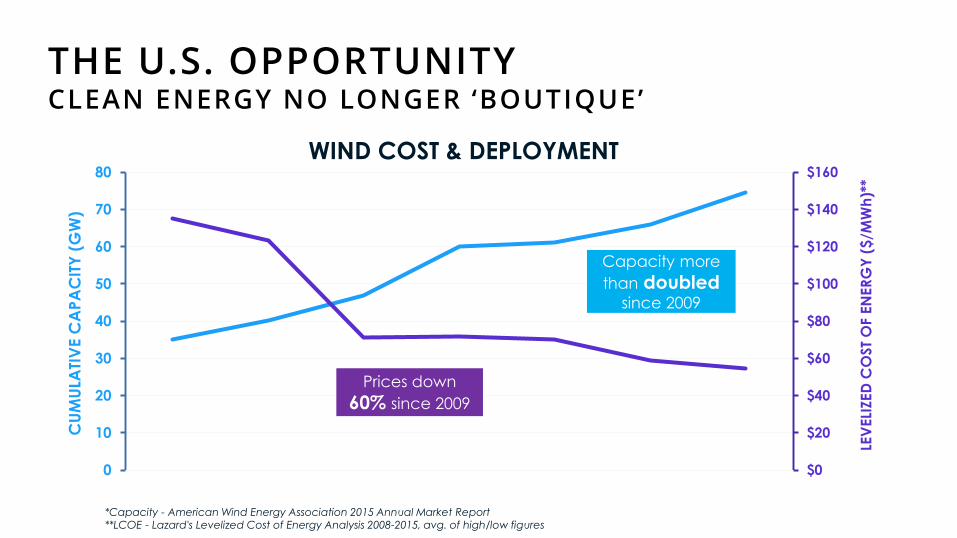

THE U.S. OPPORTUNITY CLEAN ENERGY NO LONGER ‘BOUTIQUE’

$0

$50

$100

$150

$200

$250

$300

$350

$400

0

4

8

12

16

20

24

28

2009 2010 2011 2012 2013 2014 2015

LEV

ELI

ZED

CO

ST

OF E

NER

GY

($

/MW

h)*

*

CU

MU

LATI

VE C

AP

AC

ITY

(G

W)

SOLAR COST & DEPLOYMENT

*Capacity - GTM/SEIA Solar Market Insight Annual Report 2015 **LCOE - Lazard's Levelized Cost of Energy Analysis 2008-2014, technology-weighted avg. of high/low ranges

Prices down

more than 80% since 2009

Capacity

increased 20X

since 2009

4

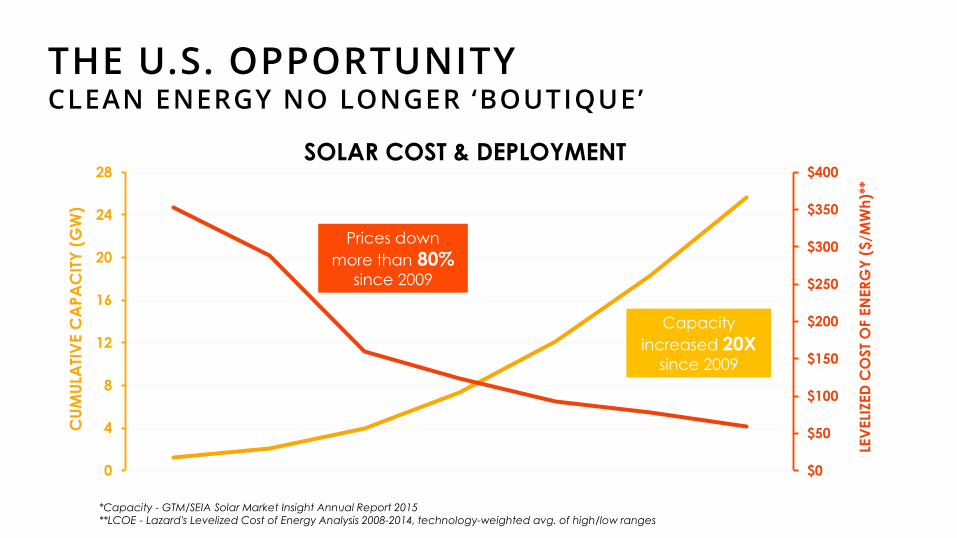

THE U.S. OPPORTUNITY STATE COMMITMENTS

CA: 50% by 2030

HI: 100% by 2045

VT: 75% by 2032

NY: 50% by 2030

5

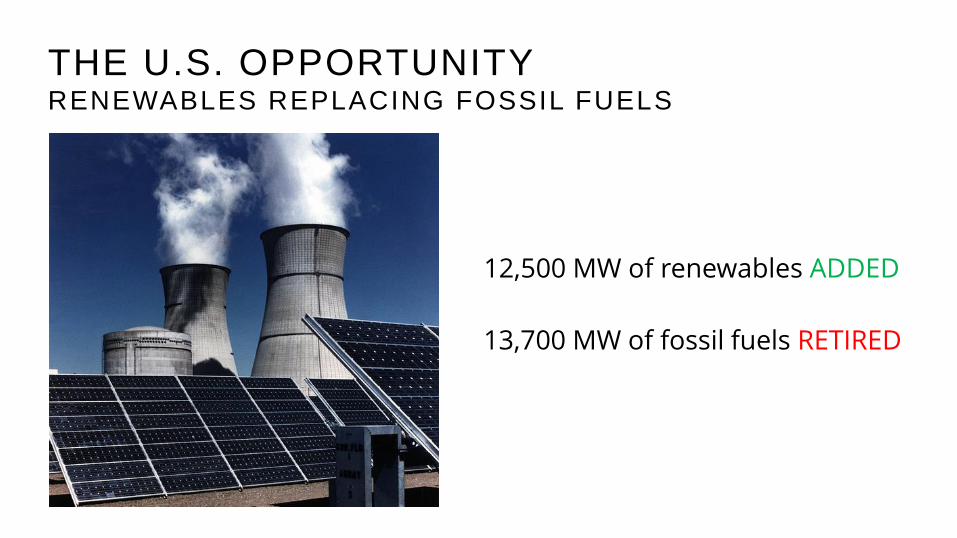

THE U.S. OPPORTUNITY RENEWABLES REPLACING FOSSIL FUELS

12,500 MW of renewables ADDED

13,700 MW of fossil fuels RETIRED

6

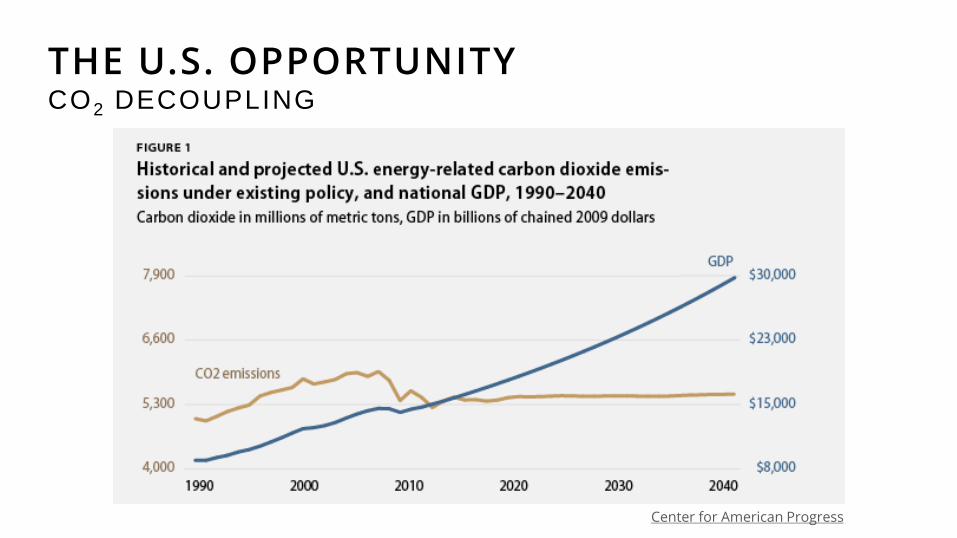

THE U.S. OPPORTUNITY CO2 DECOUPLING

Source: Center for American Progress

7

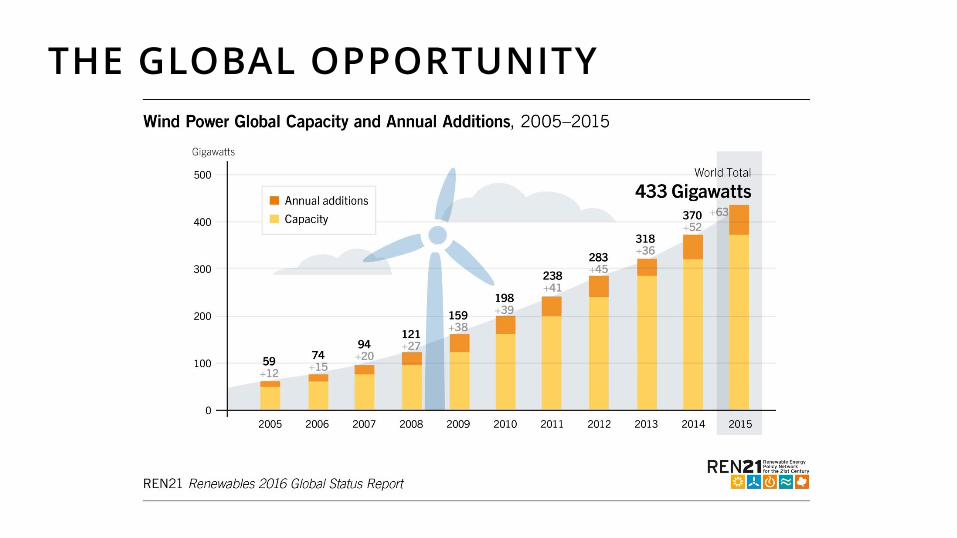

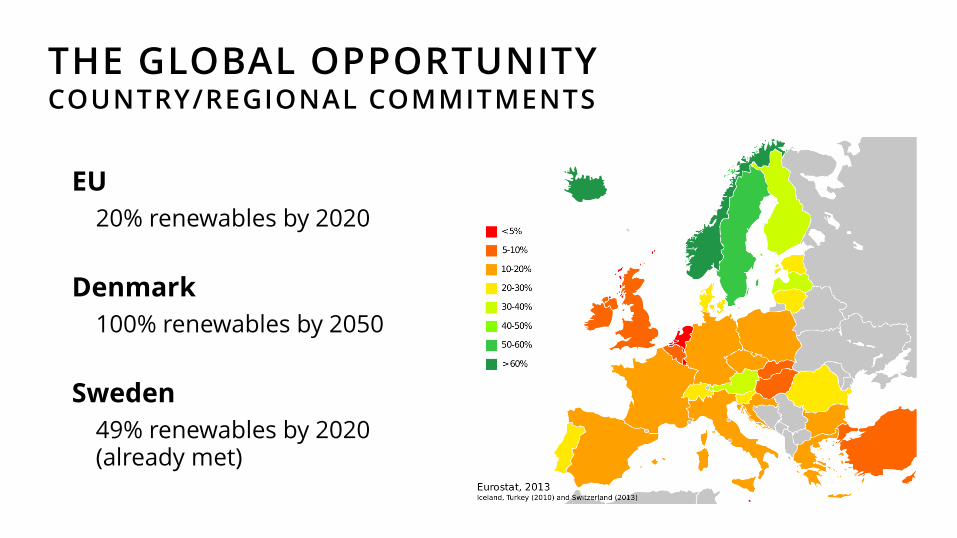

THE GLOBAL OPPORTUNITY

8

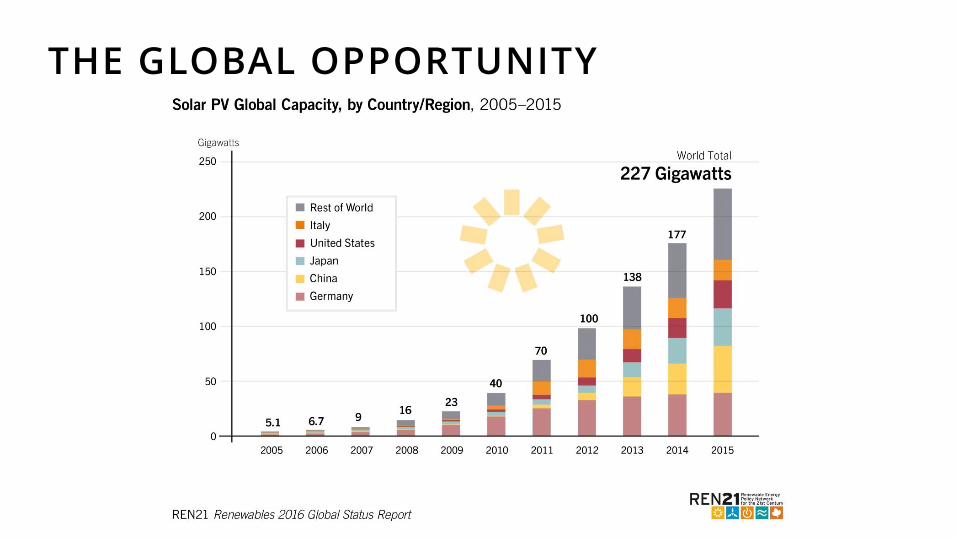

THE GLOBAL OPPORTUNITY

9

THE GLOBAL OPPORTUNITY COUNTRY/REGIONAL COMMITMENTS

EU

20% renewables by 2020

Denmark

100% renewables by 2050

Sweden

49% renewables by 2020 (already met)

10

OPPORTUNITY NEW TECHNOLOGIES UNDERWAY

11

BUT… A CLEAN ENERGY FUTURE REQUIRES A FLEXIBLE GRID

12

How can the electric grid

optimize for this?

13

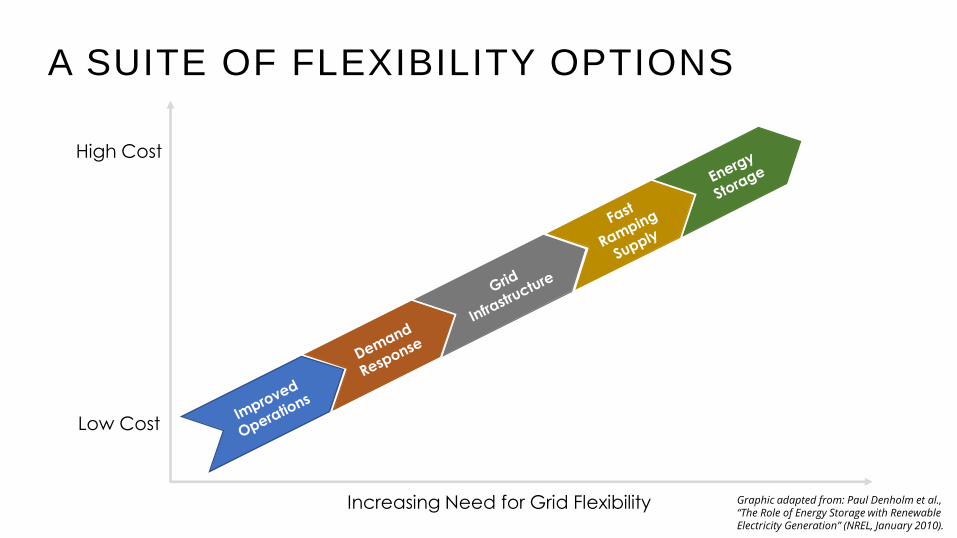

A SUITE OF FLEXIBILITY OPTIONS

Increasing Need for Grid Flexibility

High Cost

Low Cost

Flexibility Resource Supply Curve

Graphic adapted from: Paul Denholm et al., “The Role of Energy Storage with Renewable Electricity Generation” (NREL, January 2010).

High Cost

Low Cost

14

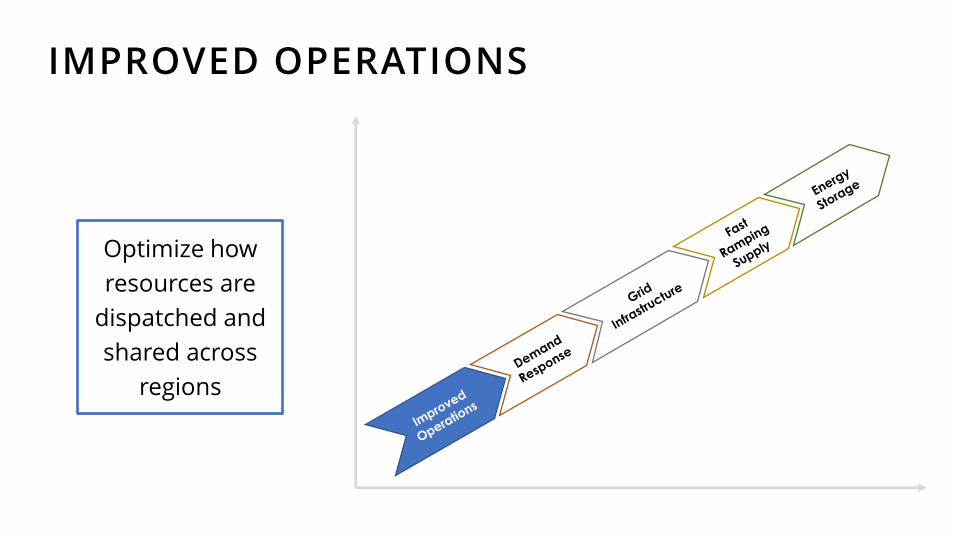

IMPROVED OPERATIONS

Optimize how

resources are

dispatched and

shared across

regions

15

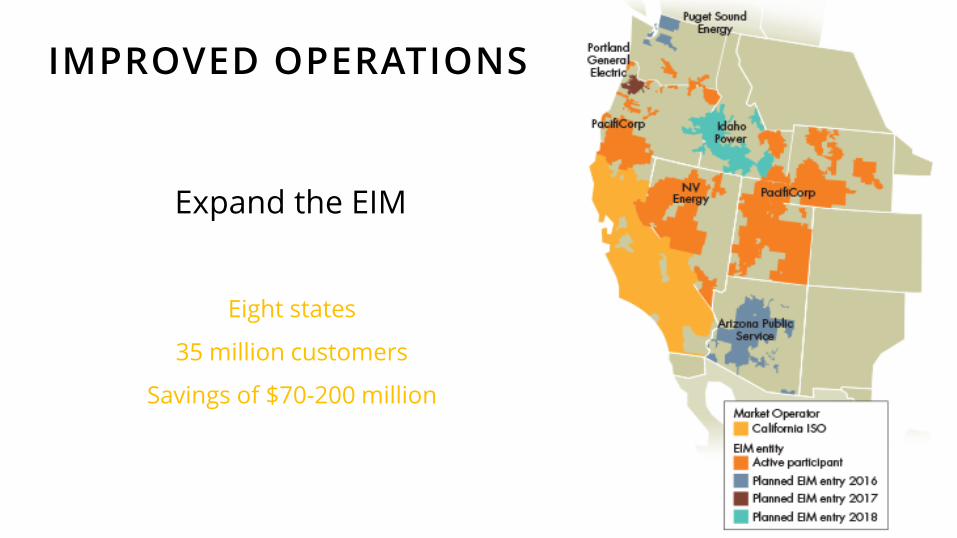

IMPROVED OPERATIONS

Expand the EIM

Eight states

35 million customers

Savings of $70-200 million

16

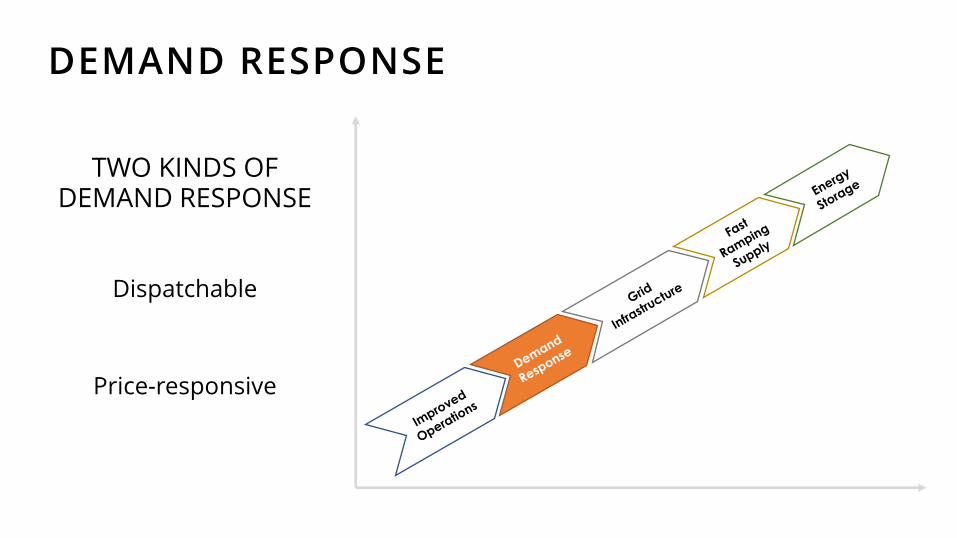

DEMAND RESPONSE

TWO KINDS OF DEMAND RESPONSE

Dispatchable

Price-responsive

17

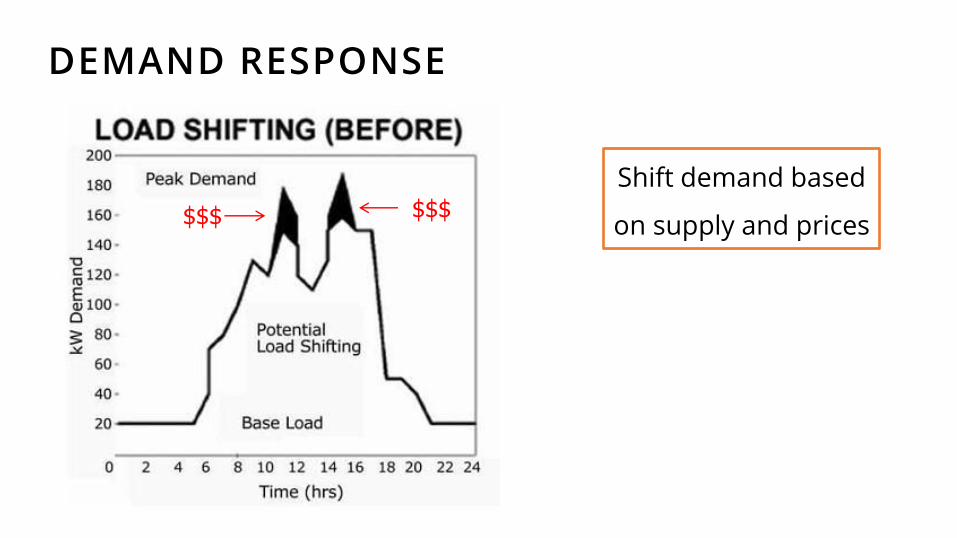

DEMAND RESPONSE

Shift demand based

on supply and prices $$$ $$$

18

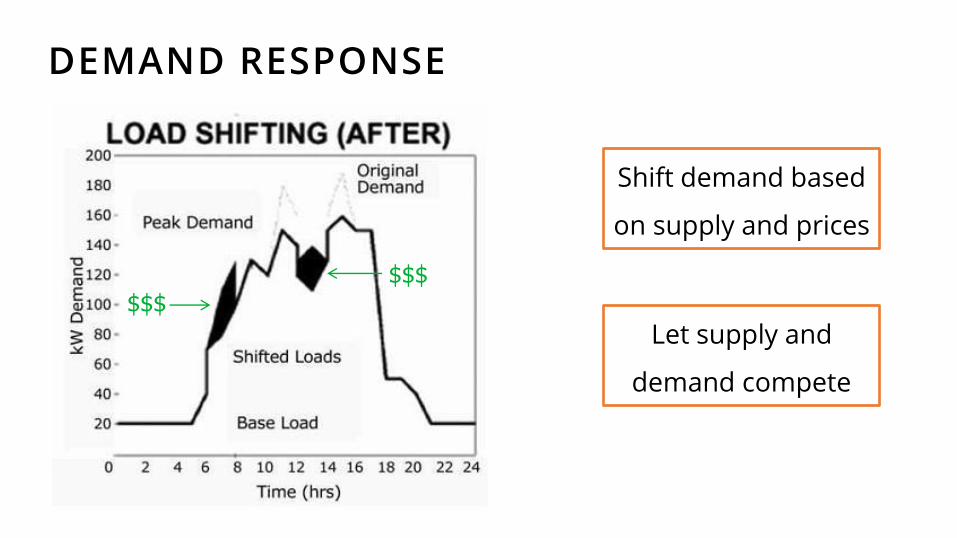

DEMAND RESPONSE

Let supply and

demand compete

Shift demand based

on supply and prices

$$$ $$$

19

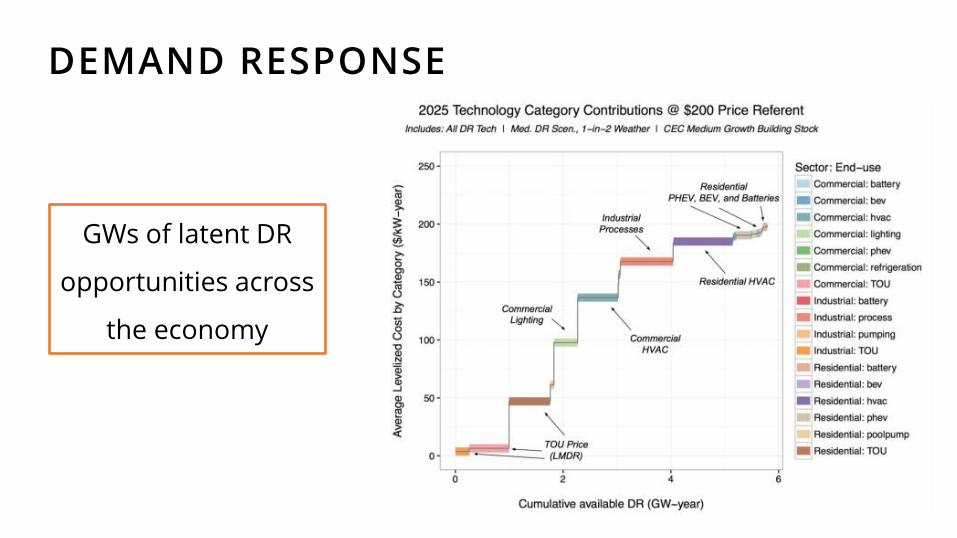

DEMAND RESPONSE

GWs of latent DR

opportunities across

the economy

20

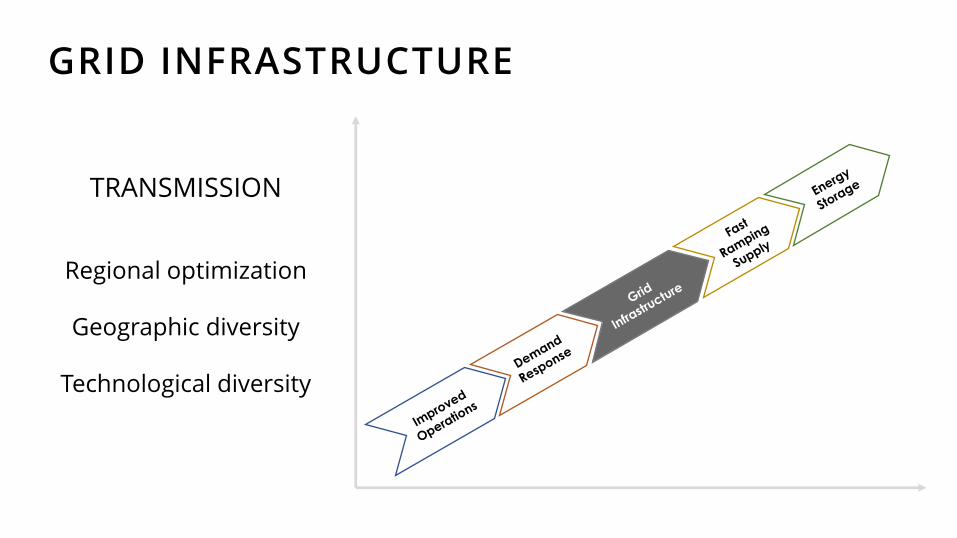

GRID INFRASTRUCTURE

TRANSMISSION

Regional optimization

Geographic diversity

Technological diversity

21

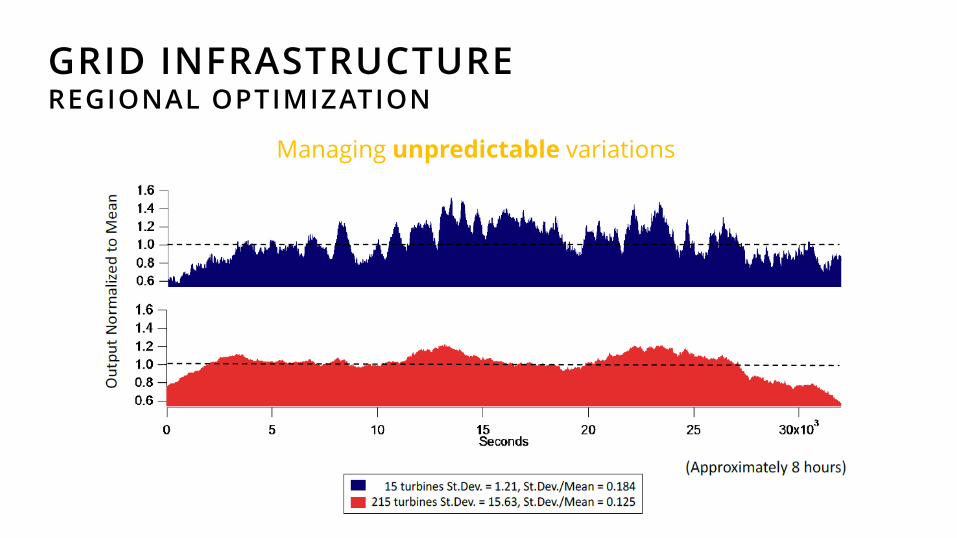

GRID INFRASTRUCTURE REGIONAL OPTIMIZATION

Managing unpredictable variations

22

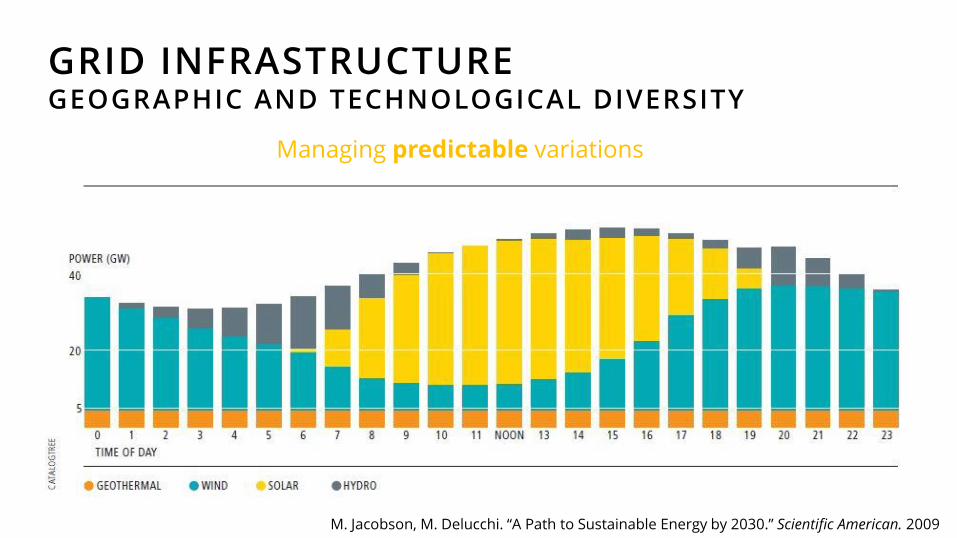

GRID INFRASTRUCTURE GEOGRAPHIC AND TECHNOLOGICAL DIVERSITY

M. Jacobson, M. Delucchi. “A Path to Sustainable Energy by 2030.” Scientific American. 2009

Managing predictable variations

23

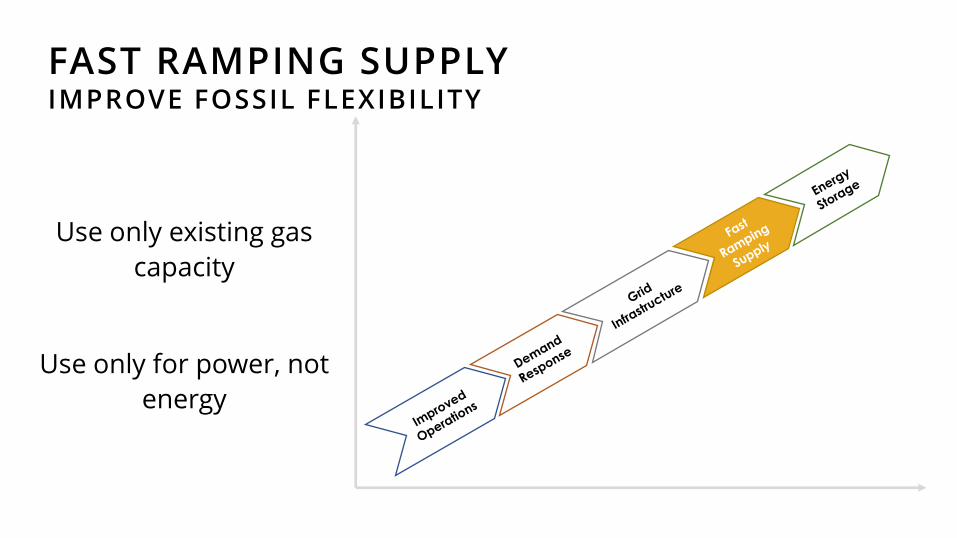

FAST RAMPING SUPPLY IMPROVE FOSSIL FLEXIBILITY

Use only existing gas

capacity

Use only for power, not

energy

24

FAST RAMPING SUPPLY

New natural gas WILL NOT get us to

our emissions reduction goals

Duke Energy (Flickr)

25

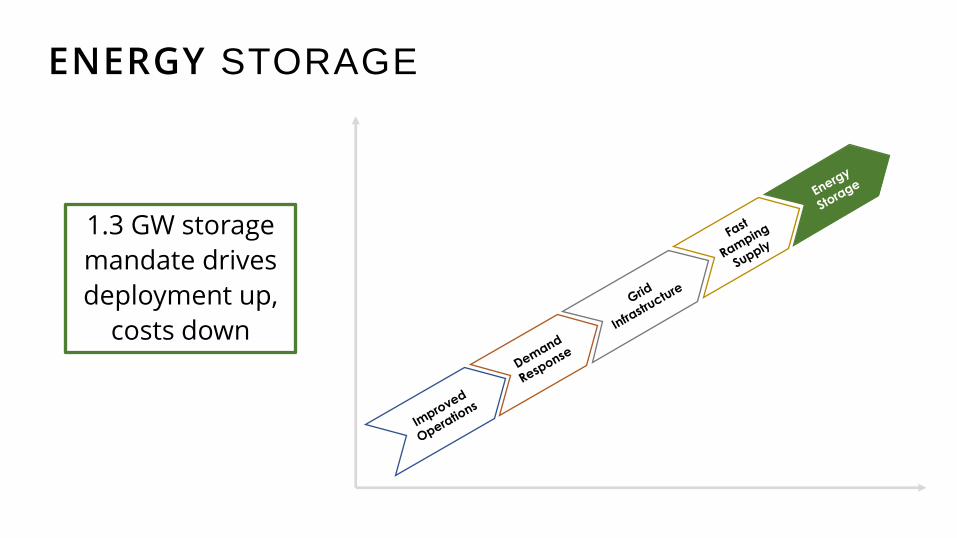

ENERGY STORAGE

1.3 GW storage

mandate drives

deployment up,

costs down

26

ENERGY STORAGE

Pumped hydro Battery storage

27

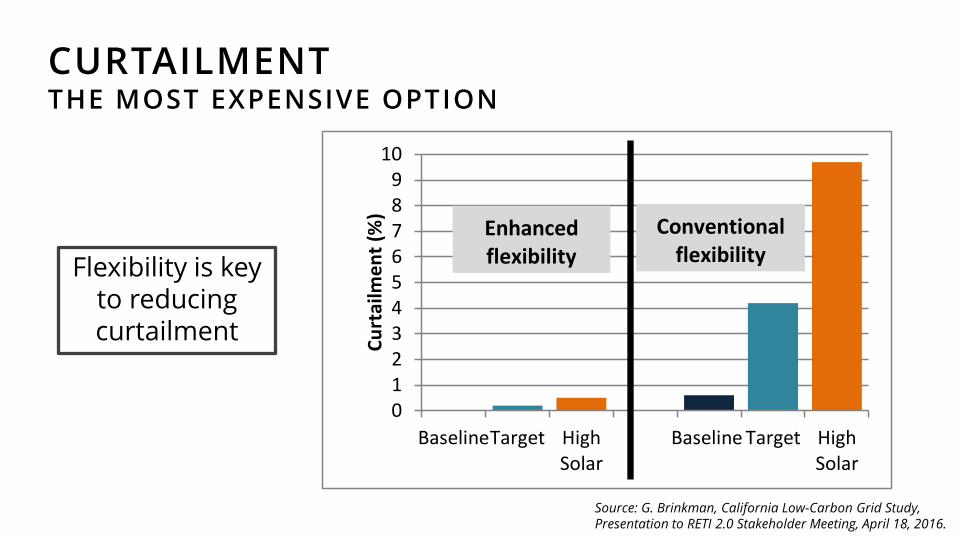

CURTAILMENT THE MOST EXPENSIVE OPTION

0123456789

10

BaselineTarget HighSolar

Baseline Target HighSolar

Cu

rtai

lme

nt

(%)

Enhanced flexibility

Conventional flexibility

Source: G. Brinkman, California Low-Carbon Grid Study, Presentation to RETI 2.0 Stakeholder Meeting, April 18, 2016.

Flexibility is key to reducing curtailment

28

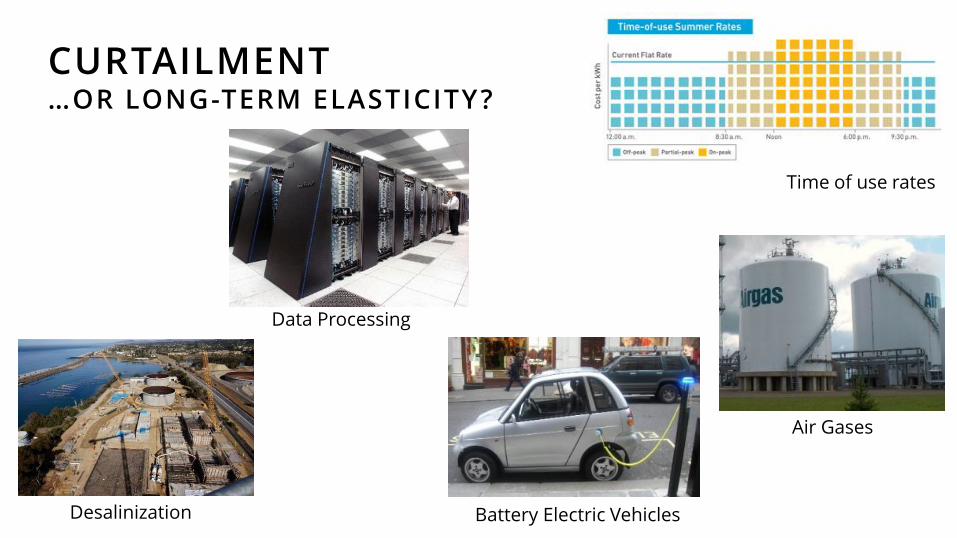

CURTAILMENT …OR LONG -TERM ELASTICITY?

Data Processing

Battery Electric Vehicles

Air Gases

Desalinization

Time of use rates

29

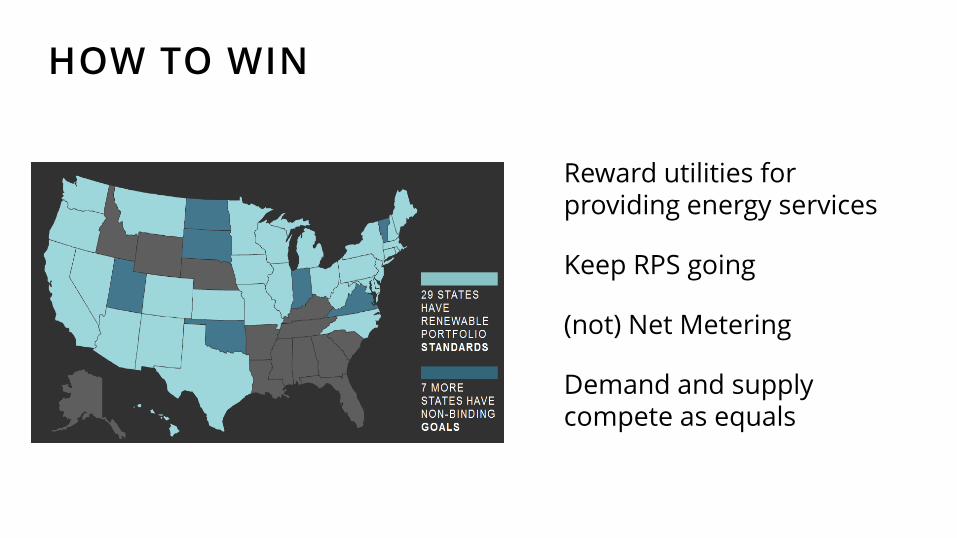

HOW TO WIN

1. Reward utilities for providing energy services

2. Keep RPS going

3. (not) Net Metering

4. Demand and supply compete as equals

Lawrence Berkeley National Lab

30

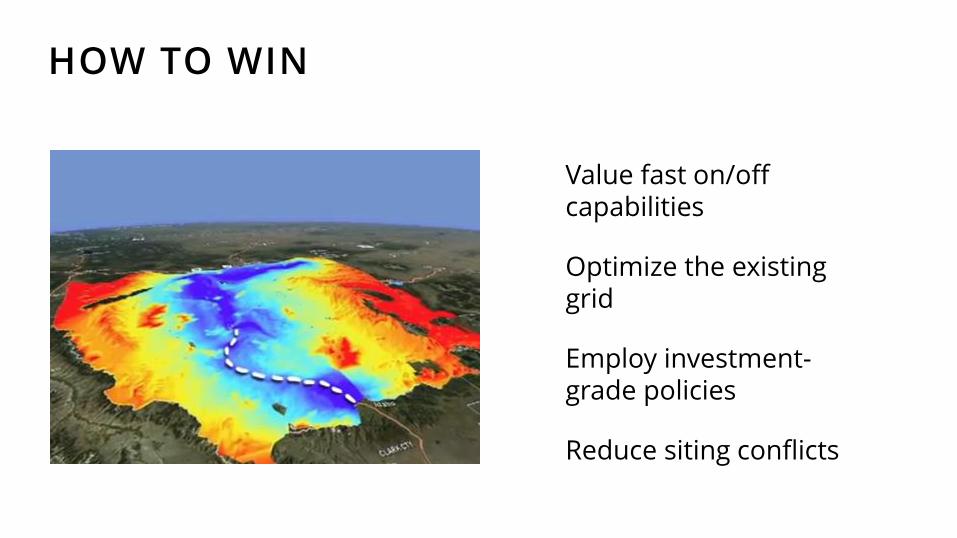

HOW TO WIN

5. Value fast on/off capabilities

6. Optimize the existing grid

7. Employ investment-grade policies

8. Reduce siting conflicts

MSTI Review Project

31 WWW.AMERICASPOWERPLAN.COM

32

THANK YOU

@HAL_HARVEY

@ENERGYINNOVLLC

WWW.ENERGYINNOVATION.ORG