Positioning for a new financial landscape...Positioning for a new financial landscape 3 While over...

24

Positioning for a new financial landscape

Transcript of Positioning for a new financial landscape...Positioning for a new financial landscape 3 While over...

Positioning for a new financial landscape

Foreword 1

The damage done 2

Positioning for a new financial landscape 7

Contacts 19

Contents

Positioning for a new financial landscape 1

The future of the global financial services industryremains uncertain. While the worst of the financial crisis and economic downturn appears to be past, thecompetitive landscape remains in flux and the debateabout regulatory change continues, with few of thefinal details agreed upon.

What is certain is that the global financial servicesindustry is experiencing a period of transition, leavingbehind many of the practices and products of the pre-crisis era, and moving towards a new financiallandscape. However, there are questions as to whatpreparations institutions are making to positionthemselves for success in this new landscape.

To shed some light on these questions, Deloitteconducted a survey of over 200 financial servicesexecutives from around the world, the results of whichare presented in this report. These executives revealedthe impact of the crisis – the relationships damaged,the performance curtailed, and the strategies disrupted– and highlighted their future focus around customersand products, strategy and operations, risk andregulation, capital and liquidity, and talent andtechnology.

As this industry transition continues, Deloitte’s GlobalFinancial Services Industry network is committed toproviding continued thought leadership, surveys andstudies on the issues most important to global financialinstitutions. Deloitte’s aim is to help guide clients throughthese challenging times and provide them with insightsuseful in preparing for a new financial landscape.

I hope you find this report of interest.

Regards,

Jack RibeiroManaging Partner, Global Financial Services IndustryDeloitte Touche Tohmatsu

Foreword

“It’s tough to make predictions –especially about the future.”

Yogi BerraU.S. Baseball Legend

2

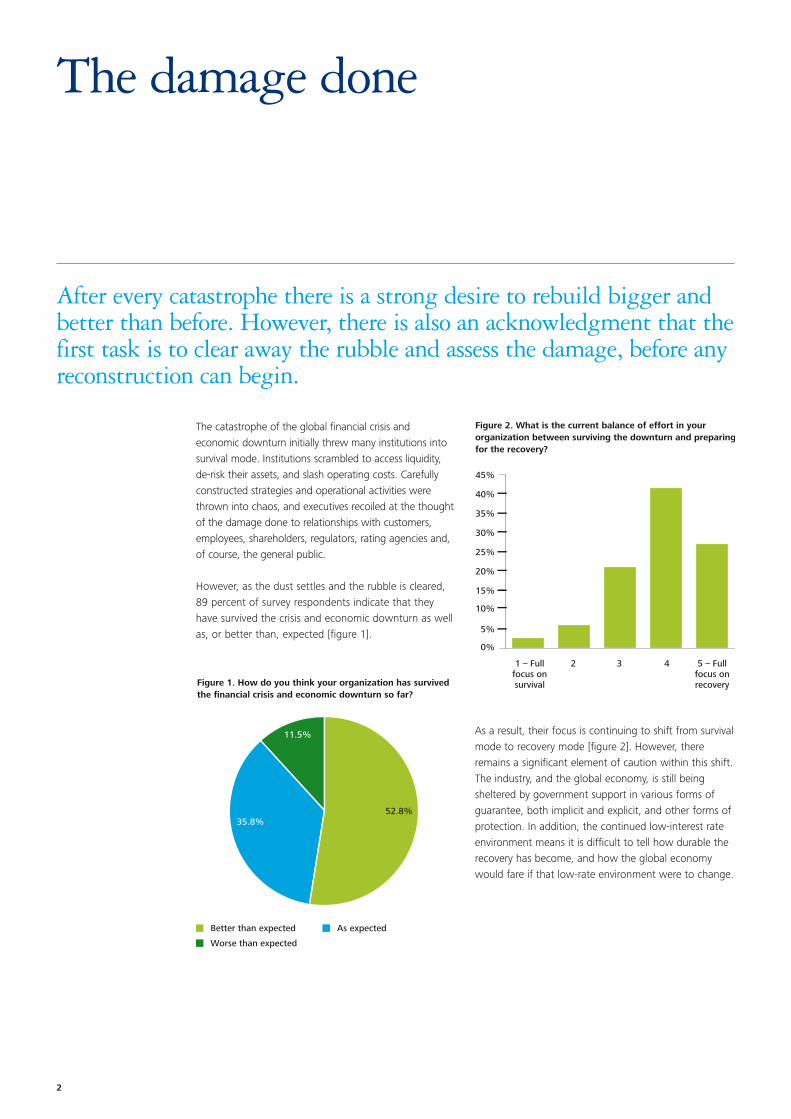

As a result, their focus is continuing to shift from survivalmode to recovery mode [figure 2]. However, thereremains a significant element of caution within this shift.The industry, and the global economy, is still beingsheltered by government support in various forms ofguarantee, both implicit and explicit, and other forms ofprotection. In addition, the continued low-interest rateenvironment means it is difficult to tell how durable therecovery has become, and how the global economywould fare if that low-rate environment were to change.

The damage done

After every catastrophe there is a strong desire to rebuild bigger andbetter than before. However, there is also an acknowledgment that thefirst task is to clear away the rubble and assess the damage, before anyreconstruction can begin.

The catastrophe of the global financial crisis andeconomic downturn initially threw many institutions intosurvival mode. Institutions scrambled to access liquidity,de-risk their assets, and slash operating costs. Carefullyconstructed strategies and operational activities werethrown into chaos, and executives recoiled at the thoughtof the damage done to relationships with customers,employees, shareholders, regulators, rating agencies and,of course, the general public.

However, as the dust settles and the rubble is cleared,89 percent of survey respondents indicate that theyhave survived the crisis and economic downturn as wellas, or better than, expected [figure 1].

Figure 1. How do you think your organization has survivedthe financial crisis and economic downturn so far?

52.8%

Better than expected

Worse than expected

As expected

35.8%

11.5%

Figure 2. What is the current balance of effort in your organization between surviving the downturn and preparingfor the recovery?

1 – Fullfocus onsurvival

2 3 4 5 – Fullfocus onrecovery

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Positioning for a new financial landscape 3

While over half of survey respondents indicated thatthey were optimistic about the prospects for theirindustry over the coming year, the remaining 49 percentpoint to the uncertainty that exists within the industryand the broader economy [figure 3].

The banks led the sectors most concerned about thedamage done to their relationship with the generalpublic. Considering that media attention about the crisishas been heavily focused on the banks – a term looselyused by the media to describe everything frommortgage originators to ‘Wall Street’ traders and hedgefund managers – it is not surprising that publicperception is high on the banks’ list.

Respondents from the investment management industryled the sectors in worries about damage to customerrelationships. While not publically painted as villainsquite to the same extent as the banks, there is nodoubt that there was damage done each time acustomer opened a shrinking investment statementduring the period of the crisis.

Surprisingly, the insurance industry respondents led thevotes for damage done to employee relations. However, this might be explained by the inclusion ofproducers and agents in their perception of the broadterm ‘employees’. As the individuals caught in theturmoil between customers and the insurance companies,it is perhaps not surprising that respondents felt that theseproducer and agent relationships had been damaged.

Figure 3. What is your sentiment about the prospects for your industry over the next 12 months?

51%

Optimistic PessimisticNeutral

37%

12%

RelationshipsWhen respondents considered the damage that thefinancial crisis and economic downturn inflicted on their business relationships, there was a differencebetween the various sectors [figure 4].

Figure 4. What relationships within your business do you think have experienced the most long-term damage from the financial crisis and economic downturn?

Relationship with the general public Relationship with customers Relationship with employees

0%

5%

10%

15%

20%

25%

0%

5%

10%

15%

20%

25%

0%

5%

10%

15%

20%

25%

Banking Inv. mgmtSecurities Insurance

4

PerformanceRespondents indicated that the greatest damage done tothe performance aspects of their business, as a result ofthe financial crisis and economic downturn, was that itleft them with less ability to generate top line revenue[figure 5]. This response reflects the shrinking ordisappearance of a wide range of revenue generatingactivity. Clearly as mortgage originations ground to a haltthere was a corresponding drop in the fees banksexpected to make from those transitions. In addition, thedrop in demand for policies to insure those houses alsoimpacted the insurance industry. Furthermore, the freezein structured products that packaged many of thosemortgages into asset-backed securities also had an impact on the fees generated by the industry.

Banking respondents also indicated an additional area ofperformance damage, leading the sector votes on theissue of weakened balance sheets [figure 6].

This is recognition of the damage done by the historicdrop in equity prices at many institutions, along with thesignificant write-down banks were required to makeagainst many assets that had a mortgage element to them.

StrategyThe final area of damage indicated by surveyparticipants was in relation to disrupted strategic goals.The majority of respondents indicated that their plansto expand into other sectors had to be put on hold as a result of the crisis, with the second and third rankedareas of damage being related to new productdevelopment and the sustainability of business models [figure 7]. Figure 5. What performance aspects of your business do you think have experienced the

most long-term damage from the financial crisis and economic downturn?

Less

ab

ility

to

gen

erat

e to

plin

e re

ven

ue

Wea

ken

ing

of t

he

bal

ance

shee

t

Less

co

nfid

ence

inri

sk m

anag

emen

t

Wea

ken

edco

mp

ensa

tio

nst

ruct

ure

s

Incr

ease

ino

per

atin

g c

ost

s

Oth

er

0%

5%

10%

15%

20%

25%

30%

35%

Figure 6. What performance aspects of your business do youthink have experienced the most long-term damage from the financial crisis and economic downturn?

Weakening of the balance sheet

Banking

0%

5%

10%

15%

20%

25%

Inv. mgmtSecurities Insurance

Figure 7. What strategic objectives of your business do youthink have experienced the most long-term damage from the financial crisis and economic downturn?

Expa

nsio

n in

toot

her

sect

ors

New

pro

duct

deve

lopm

ent

Sust

aina

bilit

y of

your

ope

rati

ngm

odel

Emer

ging

mar

ket

entr

y

Oth

er

0%

5%

10%

15%

20%

25%

30%

Positioning for a new financial landscape 5

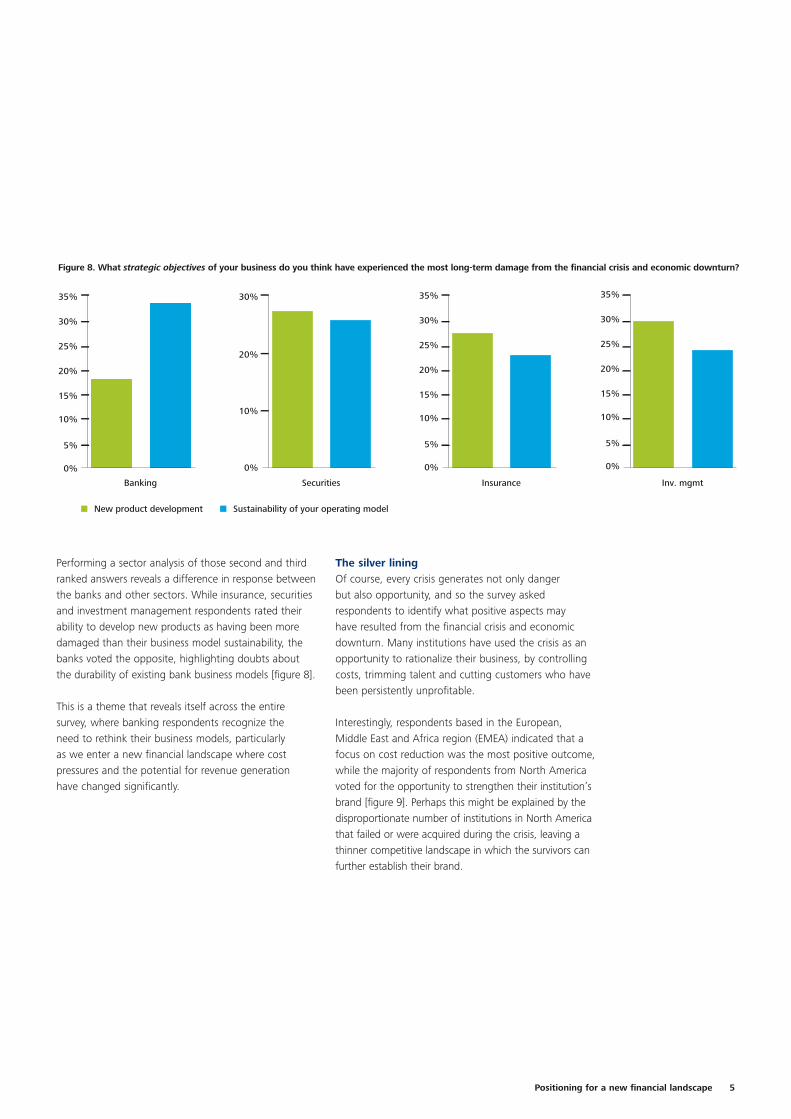

Figure 8. What strategic objectives of your business do you think have experienced the most long-term damage from the financial crisis and economic downturn?

Banking

0%

5%

10%

15%

20%

25%

30%

35%

Insurance

0%

5%

10%

15%

20%

25%

30%

35%

Inv. mgmt

0%

5%

10%

15%

20%

25%

30%

35%

Securities

0%

10%

20%

30%

New product development Sustainability of your operating model

Performing a sector analysis of those second and thirdranked answers reveals a difference in response betweenthe banks and other sectors. While insurance, securitiesand investment management respondents rated theirability to develop new products as having been moredamaged than their business model sustainability, thebanks voted the opposite, highlighting doubts aboutthe durability of existing bank business models [figure 8].

This is a theme that reveals itself across the entiresurvey, where banking respondents recognize the need to rethink their business models, particularly as we enter a new financial landscape where costpressures and the potential for revenue generation have changed significantly.

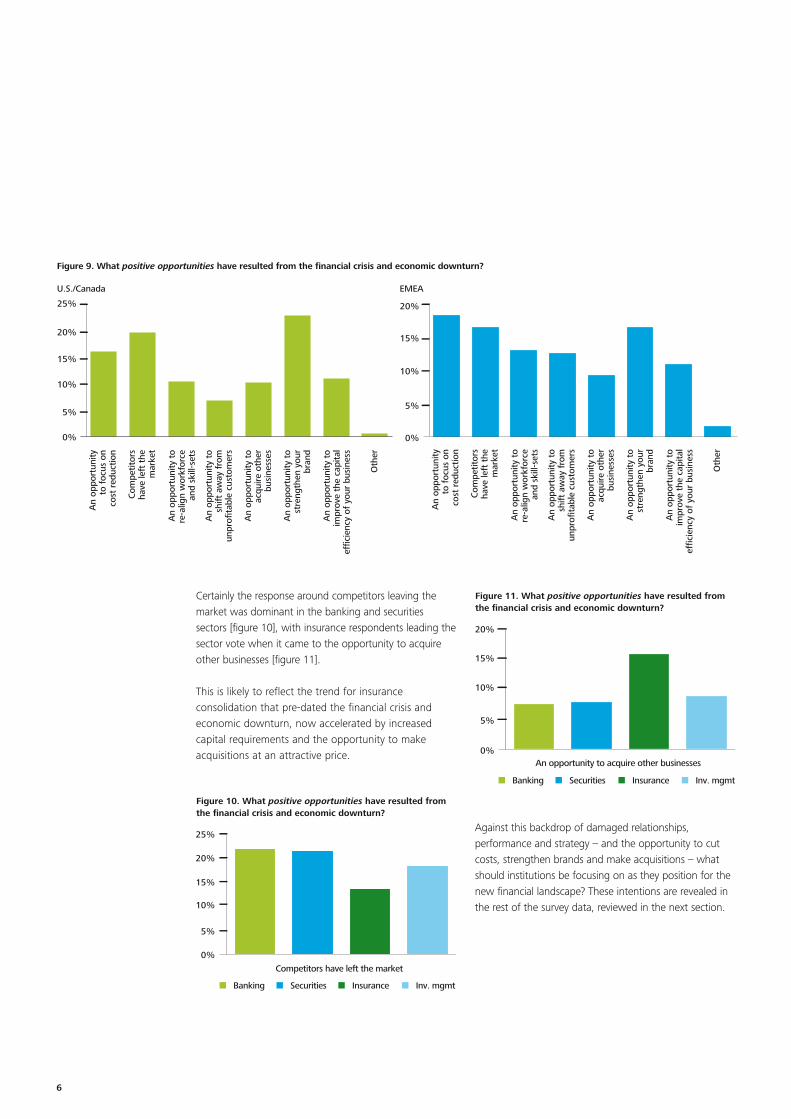

The silver liningOf course, every crisis generates not only danger but also opportunity, and so the survey askedrespondents to identify what positive aspects may have resulted from the financial crisis and economicdownturn. Many institutions have used the crisis as anopportunity to rationalize their business, by controllingcosts, trimming talent and cutting customers who havebeen persistently unprofitable.

Interestingly, respondents based in the European,Middle East and Africa region (EMEA) indicated that afocus on cost reduction was the most positive outcome,while the majority of respondents from North Americavoted for the opportunity to strengthen their institution’sbrand [figure 9]. Perhaps this might be explained by thedisproportionate number of institutions in North Americathat failed or were acquired during the crisis, leaving athinner competitive landscape in which the survivors canfurther establish their brand.

6

Figure 9. What positive opportunities have resulted from the financial crisis and economic downturn?

U.S./Canada

An

oppo

rtun

ityto

foc

us o

nco

st r

educ

tion

Com

petit

ors

have

left

the

mar

ket

An

oppo

rtun

ity t

ore

-alig

n w

orkf

orce

and

skill

-set

s

An

oppo

rtun

ity t

osh

ift a

way

fro

mun

profi

tabl

e cu

stom

ers

An

oppo

rtun

ity t

oac

quire

oth

erbu

sine

sses

An

oppo

rtun

ity t

ost

reng

then

you

rbr

and

An

oppo

rtun

ity t

oim

prov

e th

e ca

pita

lef

ficie

ncy

of y

our

busi

ness

Oth

er

0%

5%

10%

15%

20%

25%

EMEA

An

oppo

rtun

ityto

foc

us o

nco

st r

educ

tion

Com

petit

ors

have

left

the

mar

ket

An

oppo

rtun

ity t

ore

-alig

n w

orkf

orce

and

skill

-set

s

An

oppo

rtun

ity t

osh

ift a

way

fro

mun

profi

tabl

e cu

stom

ers

An

oppo

rtun

ity t

oac

quire

oth

erbu

sine

sses

An

oppo

rtun

ity t

ost

reng

then

you

rbr

and

An

oppo

rtun

ity t

oim

prov

e th

e ca

pita

lef

ficie

ncy

of y

our

busi

ness

Oth

er

0%

5%

10%

15%

20%

Certainly the response around competitors leaving themarket was dominant in the banking and securitiessectors [figure 10], with insurance respondents leading thesector vote when it came to the opportunity to acquireother businesses [figure 11].

This is likely to reflect the trend for insuranceconsolidation that pre-dated the financial crisis andeconomic downturn, now accelerated by increasedcapital requirements and the opportunity to makeacquisitions at an attractive price.

Figure 10. What positive opportunities have resulted fromthe financial crisis and economic downturn?

Competitors have left the market

Banking

0%

5%

10%

15%

20%

25%

Inv. mgmtSecurities Insurance

Figure 11. What positive opportunities have resulted fromthe financial crisis and economic downturn?

An opportunity to acquire other businesses

Banking

0%

5%

10%

15%

20%

Inv. mgmtSecurities Insurance

Against this backdrop of damaged relationships,performance and strategy – and the opportunity to cutcosts, strengthen brands and make acquisitions – whatshould institutions be focusing on as they position for thenew financial landscape? These intentions are revealed inthe rest of the survey data, reviewed in the next section.

Positioning for a new financial landscape 7

The disruption caused by the financial crisis presents a very rareopportunity for institutions to gain competitive position. However, to take advantage of that opportunity, institutions will need to adjust their approach to take account of all the changes thathave occured.

It is hard to think of a single aspect of the financialservices industry that won’t be changed as a result ofthe financial crisis.

Customer perceptions and attitudes are changing.Methods for managing risk are changing. Decisions forthe deployment of capital are changing. Compensationstrategies are changing. And the local regulations bywhich the financial system is governed are also soonlikely to change.

The challenge for financial institutions is how to beginadapting to this new environment long before the finedetail has been confirmed. The Deloitte survey providessome insights to where financial institutions arefocusing their efforts.

Customers and productsIt has been said that trust is like a flower vase. If broken,it can be fixed, but it will never be the same vase again.Working in a service industry that relies so heavily ontrust and reputation, financial executives are likely to beconcerned about the damage done to customer trustand relationships as a result of the crisis.

Confidence in financial products and services wasalmost certainly eroded during the crisis, as customerssaw the value of their properties and investmentsplummet. Despite the fact that investment advisors andfinancial planners didn’t cause this drop in value, it isprobable that customers feel aggrieved that theiradvisors didn’t steer them away from such a crash invalue, and may feel distrustful of advice offered bythese parties in future.

Customer confidence was likely also eroded by theperception that financial institutions were responsible forthe crisis that damaged so much wealth. Customers, afterall, are also members of the general public, and the mediafrenzy that accompanied the crisis will certainly haveimpacted this group’s perception of the industry.

Positioning for a new financial landscape

However, this spotlight on the industry has also createdopportunities for institutions. Customers now have anincreased appreciation about the complexities of theindustry that serves them, and a greater understandingof the innovation necessary to create the products theyrely upon. As a result, there is likely to be a greaterengagement by customers when selecting products and service providers in future.

To leverage this opportunity, and to repair any damagedone to relationships, institutions are focusing greatenergy on customers across the industry [figure 12].This seems like an appropriate focus, since customerswere the group that respondents identified as havingendured the greatest relationship damage as a result of the crisis.

Figure 12. Which of the following groups will your institution focus on in order to rebuild trust and reputation?

Cus

tom

ers

Empl

oyee

s

Shar

ehol

ders

Gen

eral

publ

ic

Reg

ulat

ors

and

over

sigh

t a

utho

riti

es

Inte

rmed

iari

es

Cou

nter

part

ies

0%

10%

20%

30%

40%

50%

8

A large part of this focus is centered on improving thecustomer experience during their interactions withinstitutions [figure 13]. These improvements includebetter communications with customers, as well as more efficient levels of service, particularly in branches.These steps not only repair some of the damage doneto existing customers, but can also be a key factor inattracting new customers.

However, if institutions are trying to steal customersaway from their competitors, it should come as nosurprise that they are also expecting their competitionto target their customers in return [figure 14].Institutions therefore need to carefully balance theirefforts between acquiring new customers, andpreserving existing customers that are in the sights oftheir competitors.

Figure 13. What will be your institution’s focus regarding customers as you prepare for the recovery?

0% 5% 10% 15% 20% 25% 30% 35%

Improving the customer experience

Broadening your customer base

Focus on acquiring dissatisfiedcustomers from competitors

Narrowing your customer base

Aim to pass on more costs tocustomers to maintain margins

Other

The survey confirms this, with evidence that institutionsare focusing energy on acquiring dissatisfied customersfrom their competitors [figure 13]. Convincing customersto switch financial providers is always a difficult task.There is a certain inertia that comes from the ‘hasslefactor’ of having to change financial arrangements,such as scheduled payments or premiums. Therefore, adisruptive event like the financial crisis is a rareopportunity for institutions to acquire customers, whoare either so disillusioned with their current providerthat they are willing to accept the ‘hassle factor’, or arecustomers of an institution that failed or was acquired.

Figure 14. How do you expect your direct competition to respond to the recovery?

0% 10% 20% 30% 40%

Competition will attemptto steal customers

Competition will competethrough lower pricing

Competition will attemptto steal talent

Competition will becomemore local

Competition will becomemore global

Other

Institutions therefore needto carefully balance theirefforts between acquiringnew customers, andpreserving existingcustomers …

Positioning for a new financial landscape 9

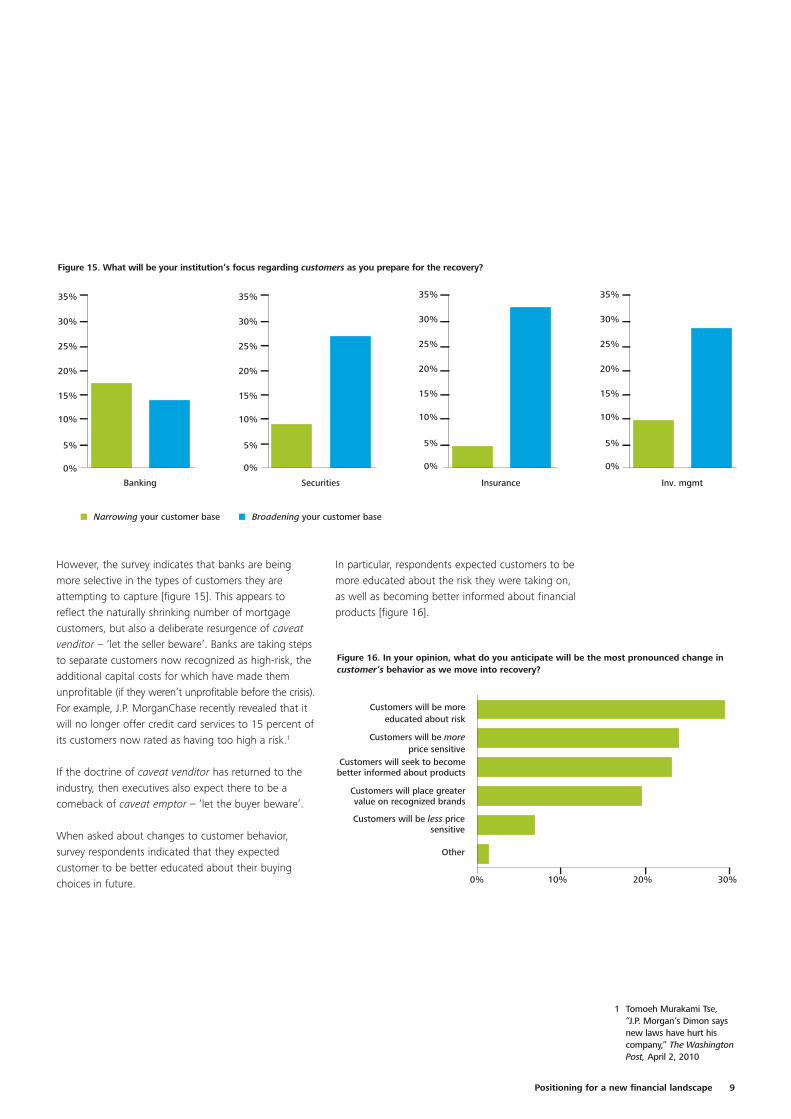

However, the survey indicates that banks are beingmore selective in the types of customers they areattempting to capture [figure 15]. This appears toreflect the naturally shrinking number of mortgagecustomers, but also a deliberate resurgence of caveatvenditor – ‘let the seller beware’. Banks are taking stepsto separate customers now recognized as high-risk, theadditional capital costs for which have made themunprofitable (if they weren’t unprofitable before the crisis).For example, J.P. MorganChase recently revealed that itwill no longer offer credit card services to 15 percent ofits customers now rated as having too high a risk.1

If the doctrine of caveat venditor has returned to theindustry, then executives also expect there to be acomeback of caveat emptor – ‘let the buyer beware’.

When asked about changes to customer behavior,survey respondents indicated that they expectedcustomer to be better educated about their buyingchoices in future.

1 Tomoeh Murakami Tse,“J.P. Morgan’s Dimon saysnew laws have hurt hiscompany,” The WashingtonPost, April 2, 2010

Figure 15. What will be your institution’s focus regarding customers as you prepare for the recovery?

Banking

0%

5%

10%

15%

20%

25%

30%

35%

Insurance

0%

5%

10%

15%

20%

25%

30%

35%

Inv. mgmt

0%

5%

10%

15%

20%

25%

30%

35%

Securities

0%

5%

10%

15%

20%

25%

30%

35%

Narrowing your customer base Broadening your customer base

Figure 16. In your opinion, what do you anticipate will be the most pronounced change incustomer’s behavior as we move into recovery?

0% 10% 20% 30%

Customers will be moreeducated about risk

Customers will be moreprice sensitive

Customers will seek to becomebetter informed about products

Customers will place greatervalue on recognized brands

Customers will be less pricesensitive

Other

In particular, respondents expected customers to bemore educated about the risk they were taking on, as well as becoming better informed about financialproducts [figure 16].

10

This increased diligence by customers is likely to havean impact on the innovation and design of futurefinancial products. Many products that rely uponpromotional rates or other incentives may now actuallyfind it harder to secure a market, as customers becomewiser about the total cost and risk of each package.Conversely, products that are competitive but difficult to promote due to their complexity might now findfavor with a more educated customer base.

This shift in customer engagement sets the scene for a new period of product innovation in the industry, asinstitutions seek to realign their product portfolio withchanging customer expectations. These new productsmight offer the customer greater control at selectingproducts based on their own risk profile, and couldeven be created in a way that allows customers to buildand combine elements of existing products intosomething more in line with their needs.

This resurgence of product innovation is also likely to be driven by the unexpected situations customers findthemselves in. Many customers are now playing ‘catch-up’ on their retirement portfolios, or no longer haveaccess to the types of product and level of returns theywere relying on at retirement. These customers will belooking for new products, innovated to help with this‘catch-up’.

Strategy and operationsDuring the height of the financial crisis thoughts ofstrategy were set aside, as the industry embraced ashort-term focus in order to navigate the stresses andshocks that continued to appear in the market.

However, as some form of stability returns to theindustry, institutions are re-examining their growthstrategies to determine which parts remain relevant inthe new financial landscape, and which will have to be revised.

While the uncertainty around regulatory reform and thestrength of the recovery make this strategy review adifficult task, it is also a great opportunity forinstitutions to exploit the disruption and find ways tojump ahead of the competition. To do this, institutionswill need to identify which attributes may haveemerged as a competitive advantage in the newenvironment, and to re-align their strategic focus toleverage these attributes before the competition can re-orientate themselves to do the same.

Interestingly, the survey reveals that the majority ofrespondents are focusing this strategic re-alignment onproduct development [figure 17]. This is surprising, assurvey respondents earlier indicated that sectorexpansion, not product development, was the aspect of their strategy most damaged by the financial crisisand economic downturn.

Figure 17. What will be your institution’s focus regardingstrategic growth as you prepare for the recovery?

New

pro

duct

deve

lopm

ent

Tran

sfor

mat

ion

ofyo

ur o

pera

ting

mod

el

Expa

nsio

n in

toot

her

sect

ors

Div

ersi

fydi

strib

utio

nch

anne

ls

Emer

ging

mar

ket

entr

y

Oth

er

0%

5%

10%

15%

20%

25%

30%

However, this re-focus on new products can perhaps be explained in part by the changing customer behaviormentioned above, with customers now examiningproducts and risk in a more diligent way. However, theproduct focus may also be a function of the fact thatthe economic basis that made many products profitablebefore the crisis has now vanished. For example,products that relied on an ongoing supply of cheapliquidity to ensure their profitability will need to beredesigned or retired in the new era of increasedliquidity premiums.

Positioning for a new financial landscape 11

Figure 18. What will be your institution’s focus regarding strategic growth as you prepare for the recovery?

20%

22%

24%

26%

28%

New product development

0%

5%

10%

15%

20%

25%

Diversify distribution channels

Banking Securities Insurance Inv. mgmt

Comparing the sectors represented in the survey,investment management and insurance lead the way inthe focus on new product development. Interestinglythese sectors also lead the way in their strategic focus ondiversifying their channels by which they distribute theseproducts [figure 18]. This diversification should delivertwo major advantages to institutions. Firstly, a broadermix of channels is likely to help them capture additionalcustomers, some of whom may not have been touchedthrough previous distribution models. Secondly, thisdiversification should reduce the risk to institutions in theevent that one of their distributors, such as a retail bank,comes under stress or experiences failure.

While the survey suggests that the investmentmanagement and insurance sector strategies arefocused heavily on growth through product expansion,the survey suggests that the banking sector has more ofa split focus in terms of strategy.

While they also have a declared focus in growth throughproduct development, compared to the other sectors thebanking respondents have a stronger focus on emergingmarket entry and sector expansion as growth strategies[figure 19]. This focus has several probable explanations.

Figure 19. What will be your institution’s focus regarding strategic growth as you prepare for the recovery?

0%

5%

10%

15%

Emerging market entry

0%

5%

10%

15%

20%

25%

Expansion into other sectors

Banking Securities Insurance Inv. mgmt

12

As mentioned in the previous section, the financial crisisleft many banks with weakened balance sheets, makingthem vulnerable. This has made for some attractivelypriced acquisition opportunities for those banks thatemerged stronger from the financial crisis and economicdownturn, which may explain the expansion focus.

Another explanation might lie in the wide-rangingpredictions that the emerging markets will make astronger return to economic growth than the moretraditional economies. The International Monetary Fund (IMF) has forecast that growth in emerging anddeveloping economies should top 6.3 percent this year,while reaching only 2.3 percent in more advancedeconomies.2 These forecasts might have been enoughto convince banks to refocus on the emerging marketplans and ambitions that were in place before thefinancial crisis and downturn.

On the operational side, the survey indicates thatinstitutions continue to focus on the issue of cost, as the industry tries to preserve areas of profitability.Respondents are primarily focused on finding ongoingoperational efficiencies, while also taking long-termsteps to shift to a lower cost structure [figure 20]. This pursuit of a lower cost structure is a response tothe expectations of a lower revenue environment goingforward, driven by the ‘commoditization’ of somepreviously higher-margin activities, as well as theexpected increase in costs related to new regulation.Analysts at J.P. Morgan have predicted that if all theproposed regulations were enacted it would requirebanks to add an additional $221billion in capital.3

In addition, only 6.1 percent of survey respondents expectto be able to pass these additional costs onto customers[figure 13]. Almost 23 percent of executives expectcustomers to be more price sensitive [figure 16], and over23 percent expect their competition to try to undercutthem with lower priced offerings [figure 14].

Finally, the survey indicates that institutions in all sectorsare focusing more on centralizing their management thanthey are empowering local business units. The datasuggests a slight reverse of this trend in Asia-Pacificrespondents, where institutions perhaps recognize theneed for a more local approach due to less maturemarkets for some of their products.

Regulation and risk The ongoing regulatory debate, taking place betweengovernments, regulators and industry, has a lot incommon with popular horror movies; you know thatsomething dramatic is going to occur – you just don’tknow when it will happen, or what it will look like.

The regulatory debate began with what appeared to bea strong global consensus to take action. However, asthe discussions proceeded, concerns emerged aboutwhether governments could ensure that any regulatoryaction was consistent across the globe, and this beganto slow the pace of action.

2 Lesley Wroughton andEmily Kaiser, “IMF nudgesup world GDP view,”Reuters, April 21, 2010

3 Steve Slater, “Bank reformmay have $220bln capitalhit,” Reuters, February 17,2010

Figure 20. What will be your institution’s focus regarding operations as you prepare for the recovery?

0% 10% 20% 30% 40%

Identify operationalefficiencies

Pursue a lower coststructure

More centralizedmanagement

Empowering business unitsto be more autonomous

Other

Almost 23 percent ofexecutives expectcustomers to be moreprice sensitive, and over23 percent expect theircompetition to try toundercut them with lowerpriced offerings.

Positioning for a new financial landscape 13

This concern over consistency was an acknowledgementof the skill with which some financial institutions hadnavigated the global regulatory environment in thepast. Politicians appear fearful of the return of‘regulatory arbitrage’, in which institutions abandoncertain countries and move their operations tojurisdictions with more convenient regulatory regimes.However, survey respondents indicate less of anappetite to make such a move than politicians mightfear [figure 21].

This lack of action has left financial institutions in a kindof regulatory ‘limbo’. Despite increasingly detailedproposals emanating from bodies such as the FinancialStability Board (FSB), there remains uncertainty aboutwhat final version of the proposals will be ratified bythe G20 countries – particularly as the early unitybetween members appears to have weakened.However, the survey reveals that the majority ofrespondents are not waiting, and are already changingcompliance procedures in anticipation of newregulation [figure 21].

Figure 21. What will be your institution’s focus regarding regulatory compliance as you prepare for the recovery?

0% 5% 10% 15% 20% 25% 30% 35%

Changing complianceprocedures in

anticipation of newregulation

Influencing publicpolicy on future

regulation

Waiting untilregulations arefinalized before

taking action

Preparing to moveoperations to less

strict regulatorydomains

Other

It is likely that many of these procedure changes willfocus on increasing each institution’s complianceflexibility, such as broadening the data sets reported foreach transaction, so that the institution will have thatinformation available should new regulations require it.This flexibility will be critical in adapting to the newregulations, as they are likely to have a staggered arrival.

Figure 22. What will be your institution’s focus regarding regulatory compliance as youprepare for recovery?

28%

30%

32%

34%

36%

Changing compliance proceduresin anticipation of new regulation

0%

10%

20%

30%

Waiting until regulations are finalizedbefore taking action

Banking Securities Insurance Inv. mgmt

However, the survey shows a difference between thesectors in their willingness to make compliance changesprior to any new regulations being finalized. While thebanking sector appears the most proactive in itscompliance changes, the investment managementsector appears more willing to wait until the regulationsare finalized before taking action [figure 22].

The survey also shows that institutions are not simplymonitoring this regulatory debate – they are also tryingto influence it.

When asked what their current focus is aroundregulatory compliance, the second highest answerrelated to influencing policy decisions. These influenceattempts have led to some tensions with politicians. U.S. President Obama recently warned the financialservices industry about the “the furious efforts ofindustry lobbyists”4, and the 2010 World EconomicForum meeting in Davos was notable for the tensionbetween the politicians and industry executives.

4 Peter Baker, “ObamaIssues Sharp Call forReforms on Wall Street,”The New York Times, April 22, 2010

14

In Davos, many industry executives expressed fears thatregulatory changes might be too extreme, as a result ofpoliticians responding to popular demands for action.However, the politicians made clear their continuingdetermination to keep control of the regulatory agenda.“The big banks, if they think they’re in a position tostop the regulation, they’re deluding themselves.” said Barney Frank, Chairman of the U.S. House ofRepresentatives Financial Services Committee.5

One area of focus almost certain to be included in anyfinal regulations will be risk management. In particular,there is recognition of the need to develop bettertechniques for understanding and managing systemicrisk within the industry.

Prior to the crisis, the industry had recognized the riskof counterparty failure, and many institutions hadprocesses in place to try and mitigate that risk.However, few people could have imaged the scale ofthe systemic risk that existed. The interconnectivity ofthe industry was revealed to be greater than previouslythought, with complex financial instruments linkinginstitutions together in a truly systemic way. The resultof this was that institutions were vulnerable to not onlyfailures of direct counterparties, but failures ofinstitutions across the world to which no direct businessrelations existed.

Armed with these experiences, institutions have beenexamining ways to refine and improve their riskmanagement practices, so that they will be more robustin the new financial landscape. The survey reveals thatthe top priority for institutions in this area is to findbetter ways to measure risk [figure 23].

These measurement improvements are likely to includean expansion of existing risk models to include morerobust variables related to liquidity and systemic risk,which were perhaps missing from previous models.Institutions are also likely to increase the frequency oftheir model validation testing, with some institutionsaiming to validate their pricing models on a daily basis.Institutions are also likely to increase the standardizationof risk measurement across their global business, sothat this risk information can be compared and trendsidentified. To achieve this many institutions are aimingto further centralize their risk management processes.

5 Simon Kennedy andChristine Harper, “DavosDispute Escalates as PolicyMakers, Bankers SquareOff,” BloombergBusinessweek, Jan 29, 2010

Figure 23. What will be your institution’s focus regardingrisk management as you prepare for the recovery?

0% 10% 20% 30%

Better measurementof risk

Ensure better boardfocus on riskmanagement

Strengthening thelink of risk to capital

Further centralize riskmanagement

Push risk responsibilitydown to business units

Increase authority forindividual judgement

of risk

Depend less on riskmodels

Other

The interconnectivity of the industry was revealed to begreater than previously thought, with complex financialinstruments linking institutions together in a trulysystemic way.

Positioning for a new financial landscape 15

Figure 24. What will be your institution’s focus regarding risk management as you prepare for the recovery?

US/Canada

0%

5%

10%

15%

20%

Europe/Middle East/Africa

0%

5%

10%

15%

20%

Asia/Pacific/Australia

0%

5%

10%

15%

20%

Mexico/Central/South America

0%

5%

10%

15%

20%

Further centralize risk management Push risk responsibility down to business units

The survey indicates that further centralizing riskmanagement, including ensuring a better board levelfocus on risk, is a higher priority than pushing riskresponsibility down to business units, again with a slightreverse for Asia-Pacific respondents [figure 24].However, these actions are not mutually exclusive, andit is clear that while institutions are working to improvetheir board level understanding and management ofrisk, this will also require individual business units totake a greater role in managing and measuring thatlocal level of risk.

Capital and liquidityBenjamin Franklin, one of the founding fathers of theUnited States, once said, “If you want to know the truevalue of money, just try to borrow some”.

The financial crisis revealed the dependence that manyinstitutions had developed for easily available liquidity.Some institutions were so dependent on access to thisliquidity, that when credit markets froze it dealt acatastrophic blow to their solvency and operations. As we move into the new financial landscape, institutionshave developed a greater focus on liquidity management,and are recognizing the true value of liquidity.

Survey respondents indicate that their top priority issecuring more stable sources of liquidity [figure 25].Many institutions have boosted their cash holdings, andhave increased the balance of their capital held in amore liquid form, accepting lower returns in exchangefor more stable liquidity. Banks have also focusedattention on deposit accounts as a more diverse andstable source of liquidity.

Figure 25. What will be your institution’s focus regardingliquidity as you prepare for the recovery?

0% 10% 20% 30% 40%

Secure more stablesources of liquidity

Identify cheapersources of liquidity

Manage the cost ofregulatory requirements

for liquidity

Revise treasury andcash operations

Pass on a liquiditypremium to customers

Other

16

Prior to the crisis deposit accounts were viewed largelyas a gateway for drawing customers into an institution,with the aim of selling additional services or chargingoverdraft fees. However, the financial crisis hasreminded the industry of the liquidity benefits of insuredbank deposits. As Michael Carpenter, CEO of GMACFinancial Services, highlighted in his testimony to the U.S. Senate, “Insured bank deposits offer a stableand reliable source of liquidity to fund our business.Previously, GMAC was a wholesale funded financecompany, and as demonstrated by the capital marketdisruption, that model is risky in a financial crisis andneeds to be balanced with access to more stablesources of funding”.6

The cost of these increased liquidity ‘buffers’ will besignificant for many institutions, particularly those thatare active internationally and are therefore likely to besubject to recent requirements proposed by the Bank of International Settlements (BIS).

A notable finding is the lower response from surveyparticipants about the ability to pass on a liquiditypremium to customers [figure 25]. This is in line withthe other survey responses indicating the difficulty inpassing on additional costs to the customer. As a resultit is likely that this increased cost of liquidity will have tobe borne by the institutions themselves. It shouldtherefore be no surprise that survey participantsindicated that their second priority was to identifycheaper sources of liquidity [figure 25].

While cheap liquidity appeared to be a contributingfactor to the crisis, the weakness was that the majority ofthis liquidity came from the wholesale market, creating aconcentration risk. Moving forward institutions will likelywant to balance the efficiency of liquidity with a morediverse range of sources of that liquidity.

Efficiency was also the theme revealed in participants’answers to questions about capital.

When asked about each institution’s priority focusaround capital the top two answers were bettermeasurement on the return on capital, and puttingcapital to better use [figure 26]. Clearly the answers arelinked, as an institution can’t be sure it is putting capitalto better use unless it is confident in its measure of thecapital return.

The methods for measuring the return on capital haveevolved over the last several decades to becomecomplex models, which calculate the risk-adjusted rateof return on capital. The various methodologies forcalculating ‘value at risk’ and economic profit haveenabled institutions to compare risk across theorganizations activities, and therefore enabled them to measure which activities resulted in a better returnon the capital employed.

However, as the financial crisis demonstrated, some of the risk assumptions built into these models wereunderstated, and the true ‘value at risk’ of investingcapital in some activities – such as complex financialinstruments – was greater than previously thought. As we move into the new financial landscape thesemeasurement models will need to be adjusted using the data and experience collected during the marketdisruption.

6 Written Statement ofMichael A. Carpenter,GMAC Chief ExecutiveOfficer GMAC FinancialServices Before theCongressional OversightPanel, February 25, 2010

Figure 26. What will be your institution’s focus regardingcapital as you prepare for the recovery?

Better measurement of‘return on capital’

Put capital to better use

Preserve a higher levelof regulatory andeconomic capital

Identify more diversifiedsources of capital

funding

Other

0% 10% 20%15%5% 25% 30%

Positioning for a new financial landscape 17

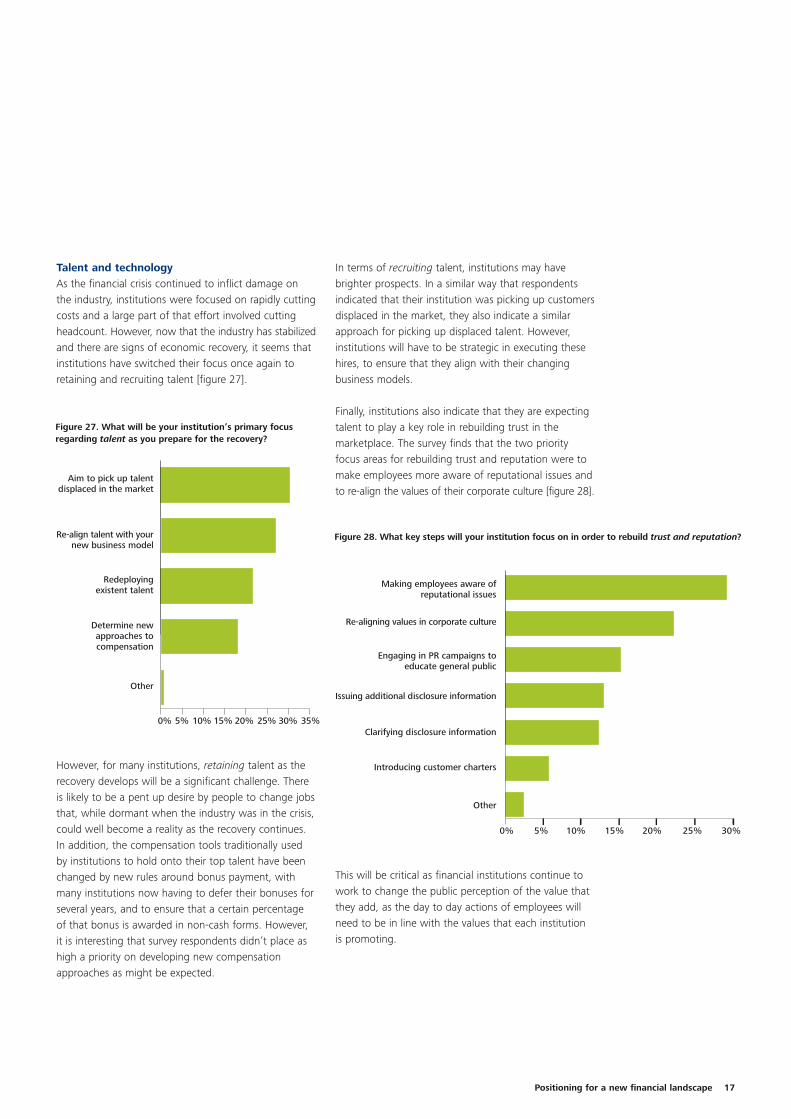

Talent and technologyAs the financial crisis continued to inflict damage on the industry, institutions were focused on rapidly cuttingcosts and a large part of that effort involved cuttingheadcount. However, now that the industry has stabilizedand there are signs of economic recovery, it seems thatinstitutions have switched their focus once again toretaining and recruiting talent [figure 27].

However, for many institutions, retaining talent as therecovery develops will be a significant challenge. Thereis likely to be a pent up desire by people to change jobsthat, while dormant when the industry was in the crisis,could well become a reality as the recovery continues.In addition, the compensation tools traditionally usedby institutions to hold onto their top talent have beenchanged by new rules around bonus payment, withmany institutions now having to defer their bonuses forseveral years, and to ensure that a certain percentageof that bonus is awarded in non-cash forms. However,it is interesting that survey respondents didn’t place ashigh a priority on developing new compensationapproaches as might be expected.

In terms of recruiting talent, institutions may havebrighter prospects. In a similar way that respondentsindicated that their institution was picking up customersdisplaced in the market, they also indicate a similarapproach for picking up displaced talent. However,institutions will have to be strategic in executing thesehires, to ensure that they align with their changingbusiness models.

Finally, institutions also indicate that they are expectingtalent to play a key role in rebuilding trust in themarketplace. The survey finds that the two priorityfocus areas for rebuilding trust and reputation were tomake employees more aware of reputational issues andto re-align the values of their corporate culture [figure 28].

Figure 27. What will be your institution’s primary focus regarding talent as you prepare for the recovery?

Aim to pick up talentdisplaced in the market

Re-align talent with yournew business model

Redeployingexistent talent

Determine newapproaches tocompensation

Other

0% 10% 20%15%5% 25% 30% 35%

Figure 28. What key steps will your institution focus on in order to rebuild trust and reputation?

Making employees aware ofreputational issues

Re-aligning values in corporate culture

Clarifying disclosure information

Engaging in PR campaigns toeducate general public

Issuing additional disclosure information

Introducing customer charters

Other

0% 30%5% 10% 15% 20% 25%

This will be critical as financial institutions continue towork to change the public perception of the value thatthey add, as the day to day actions of employees willneed to be in line with the values that each institution is promoting.

18

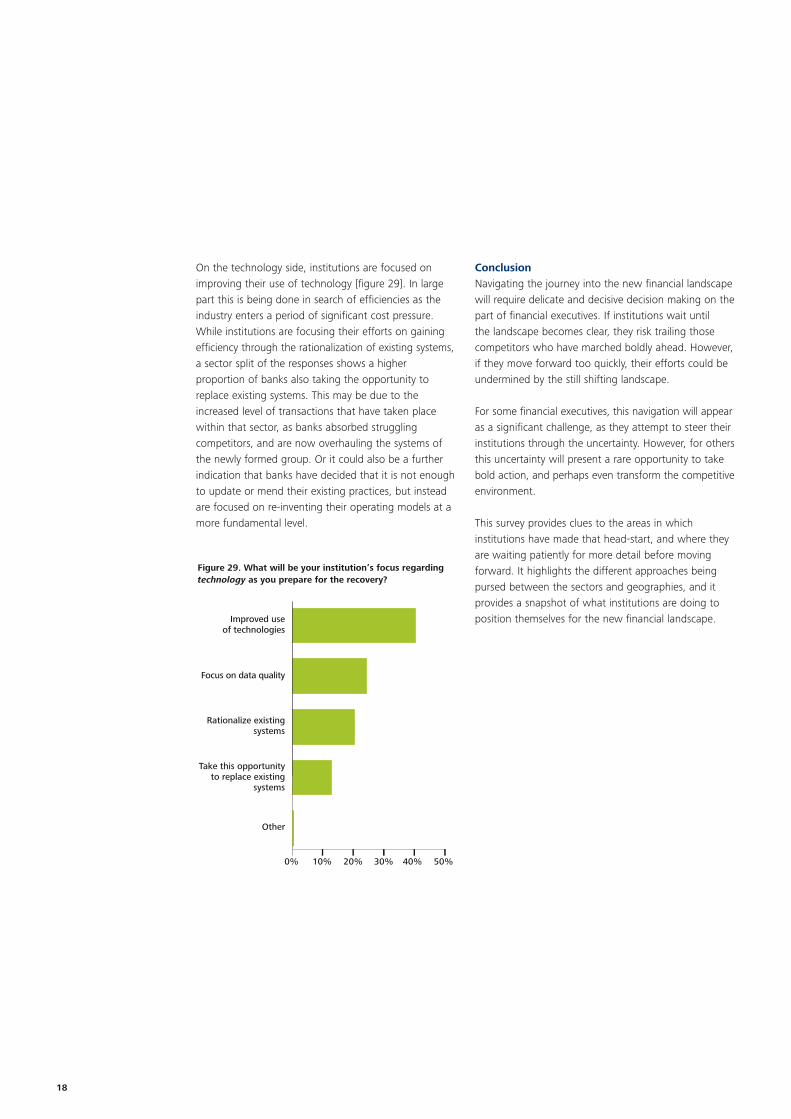

On the technology side, institutions are focused onimproving their use of technology [figure 29]. In largepart this is being done in search of efficiencies as theindustry enters a period of significant cost pressure.While institutions are focusing their efforts on gainingefficiency through the rationalization of existing systems,a sector split of the responses shows a higherproportion of banks also taking the opportunity toreplace existing systems. This may be due to theincreased level of transactions that have taken placewithin that sector, as banks absorbed strugglingcompetitors, and are now overhauling the systems ofthe newly formed group. Or it could also be a furtherindication that banks have decided that it is not enoughto update or mend their existing practices, but insteadare focused on re-inventing their operating models at amore fundamental level.

Conclusion Navigating the journey into the new financial landscapewill require delicate and decisive decision making on thepart of financial executives. If institutions wait until the landscape becomes clear, they risk trailing thosecompetitors who have marched boldly ahead. However,if they move forward too quickly, their efforts could beundermined by the still shifting landscape.

For some financial executives, this navigation will appearas a significant challenge, as they attempt to steer theirinstitutions through the uncertainty. However, for othersthis uncertainty will present a rare opportunity to takebold action, and perhaps even transform the competitiveenvironment.

This survey provides clues to the areas in whichinstitutions have made that head-start, and where theyare waiting patiently for more detail before movingforward. It highlights the different approaches beingpursed between the sectors and geographies, and itprovides a snapshot of what institutions are doing toposition themselves for the new financial landscape.

Figure 29. What will be your institution’s focus regarding technology as you prepare for the recovery?

Improved useof technologies

Focus on data quality

Rationalize existingsystems

Take this opportunityto replace existing

systems

Other

0% 50%10% 20% 30% 40%

Positioning for a new financial landscape 19

Managing PartnerGlobal Financial Services IndustryJack RibeiroNew York+1 212 436 [email protected]

AuthorChris PattersonNew York+1 212 436 [email protected]

Neal BaumannNew York+1 212 618 [email protected]

Leon BloomToronto+1 416 601 [email protected]

Wade DeffenbaughNew York+1 212 436 [email protected]

Peter FirthNew York+1 212 436 [email protected]

Joe GuastellaNew York+1 212 618 [email protected]

Chris HarveyLondon+44 20 7007 [email protected]

Stuart OppLondon+44 20 7303 [email protected]

Johnny Yip Lan YanLuxembourg+352 45145 [email protected]

Contacts

Contributors

20

Americas

ArgentinaClaudio Fiorillo+54 11 [email protected]

BahamasRaymond Winder+1 242 302 [email protected]

BermudaJohn Johnston+1 441 299 [email protected]

BrazilClodomir Félix+55 11 5186 [email protected]

CanadaCathy Bateman+1 416 601 [email protected]

Cayman IslandsDale Babiuk+1 345 814 [email protected]

ChileCarlos H. Munoz+56 2 2703 [email protected]

ColombiaRicardo Rubio Rueda+57 1 635 [email protected]

MéxicoCarlos A. Garcia+52 55 5080 [email protected]

U.S.Jim Reichbach+1 212 436 [email protected]

UruguayJosé Luis Rey+598 2 [email protected]

VenezuelaJosé Antonio López+58 212 [email protected]

Asia Pacific

AustraliaWarren Green+61 2 9322 [email protected]

China – Hong KongGerry Shipper+852 2852 [email protected]

China – MainlandDora Liu+86 21 6141 [email protected]

IndiaSachin Sondhi +91 22 6619 8600 [email protected]

IndonesiaBasar Alhuenius+62 21 2312879 [email protected]

JapanYoriko Goto+81 3 6213 [email protected]

Yukio Ono+81 3 6213 [email protected]

KoreaYun Ho Kim +82 2 6676 1104 [email protected] Lai+60 3 7723 [email protected]

New ZealandRodger Murphy+64 9 303 [email protected]

PhilippinesAvis Manlapaz+63 2 581 [email protected]

SingaporePrakash Desai+65 6530 [email protected]

TaiwanRay Chang +886 2 25459988 x3029 [email protected]

ThailandSuttharug Panya+66 2 676 5700 [email protected]

Vietnam Tom McClelland+84 8 3 910 [email protected]

Europe, Middle East and Africa(EMEA)

Africa – Eastern AfricaJulie Nyangaya +254 20 4441344 [email protected]

Africa – West and CentralOlu Sawyerr+254 1 271 7814 [email protected]

AustriaDominik Damm+43 1 53700 [email protected]

BelgiumFrank Verhaegen+32 3 800 88 [email protected]

Central EuropeMike Jennings+420 2 248 955 [email protected]

CIS (includes Russia)Maxim Lubomudrov +74957870600 [email protected]

CyprusNicos Charalambous+357 25 [email protected]

DenmarkLone Møller Olsen+45 33 76 38 [email protected]

FinlandPetri Heinonen+358 20 755 [email protected]

Deloitte member firm Financial Services Industry leaders

Positioning for a new financial landscape 21

FranceJosé-Luis Garcia+33 1 40 88 28 [email protected]

GermanyFriedhelm Kläs+49 69 75695 [email protected]

GreeceNicos Sofianos+30 210 678 [email protected]

IcelandThorvardur Gunnarsson +354 580 3101 [email protected]

IrelandMary Fulton+353 1 417 [email protected]

IsraelDan Halpern+972 3 608 [email protected]

ItalyRiccardo Motta+39 02 833 22 [email protected]

LuxembourgEric van de Kerkhove+352 451 452 [email protected]

MaltaSteve Paris +356 21 345000 [email protected]

Middle EastJoe El Fadl+961 1 363 [email protected]

NetherlandsJean-Pierre Boelen +31 882887300 [email protected]

NorwayArve Rafteseth+47 23 27 97 [email protected]

PortugalMaria Augusta Francisco+351 21 381 [email protected]

South AfricaRoger Vester+27 0 11 806 5216 [email protected]

SpainFrancisco Celma +34 915145000 [email protected]

SwedenGöran Engquist +48 506 721 94 [email protected]

Switzerland Rolf Schönauer +41 0 44 421 63 [email protected]

TurkeySibel Turker+90 533 583 36 [email protected]

UkraineVictor Lukashuk +38 0444 909000 [email protected]

U.K.Russell Collins+44 20 7303 [email protected]

Deloitte refers to one or more of Deloitte Touche Tohmatsu, a Swiss Verein, and its network of member firms, each of which is alegally separate and independent entity. Please see www.deloitte.com/about for a detailed description of the legal structure ofDeloitte Touche Tohmatsu and its member firms.

Deloitte Global ProfileDeloitte provides audit, tax, consulting, and financial advisory services to public and private clients spanning multiple industries.With a globally connected network of member firms in 140 countries, Deloitte brings world-class capabilities and deep localexpertise to help clients succeed wherever they operate. Deloitte’s 165,000 professionals are committed to becoming the standardof excellence.

Deloitte’s professionals are unified by a collaborative culture that fosters integrity, outstanding value to markets and clients,commitment to each other, and strength from cultural diversity. They enjoy an environment of continuous learning, challengingexperiences, and enriching career opportunities. Deloitte’s professionals are dedicated to strengthening corporate responsibility,building public trust, and making a positive impact in their communities.

© 2010 Deloitte Touche Tohmatsu. All rights reserved.

Item# 100040

Designed and produced by The Creative Studio at Deloitte, London. 3695A