POLISH INFORMATION AND FOREIGN INVESTMENT AGENCY · POLISH INFORMATION AND FOREIGN INVESTMENT...

43

POLISH INFORMATION AND FOREIGN INVESTMENT AGENCY Iwona Chojnowska Director Foreign Investment Department Warsaw, February 7, 2013 Doing Business in Poland

Transcript of POLISH INFORMATION AND FOREIGN INVESTMENT AGENCY · POLISH INFORMATION AND FOREIGN INVESTMENT...

POLISH INFORMATION

AND FOREIGN INVESTMENT AGENCY

Iwona Chojnowska

Director

Foreign Investment Department

Warsaw, February 7, 2013

Doing Business in Poland

Poland - Key Facts

Area: 312 700 sq km – 6th in European Union

Population: 38.5 million – 6th in European Union

Currency: Polish Zloty (1 USD ~ 3.1 PLN, 1 EUR ~ 4.2 PLN)

GDP: USD 771.015 billion (PPP, 2011) – IMF data

USD 801,974 billion (PPP, 2012) – IMF estimates

GDP per capita: USD 20,183 (PPP, 2011) – IMF data

USD 20,976 (PPP, 2012) – IMF estimates

GDP growth: 1.6% (2009), 3.9% (2010), 4.3% (2011), 2.0% (2012),

1.8% (2013, EC forecast), 2.6% (2014, EC forecast)

Membership: EU, NATO, OECD, WTO, Schengen Zone

Competitive Advantages

Location & economic fundamentals

strategic location in continental Europe

part of trans-European transportation corridor

stable economic situation

rapidly growing internal market

Appealing investment incentives

tax exemptions in 14 Special Economic Zones

local tax reliefs

government grants

EU grants

Attractive labor market

young, well-educated workforce

ca 11% of university students in the EU

460 universities & high education schools

language proficiency

increasing labour productivity

1000 km radius

250 m people

2000 km radius

550 m people

ES 0,4%

PT

-1,6%

FR 1,7%

BE 1,8%

NL 1,0%

DE 3,0%

EE 8,3%

LV 5,5%

LT 5,9%

IT

0,4%

TR

8,5%

HU 1,6% AT 2,7% RO 2,2%

SK 3,2%

FI 2,8% SE

3,7%

UK

0,9%

GR

-7,1%

DK

1,1%

BG 1,7%

IR

1,4%

CZ 1,9%

NO

1,2%

PL

+4.3%

Source: Eurostat, 2013

2009

Poland avoided

recession &

experienced the highest

GDP growth in Europe

2010

Poland was the third

fastest growing

economy in the EU

2011

Poland continued to

develop at the pace

three times higher then

the EU average

2012

Poland is expected to

grow by 2.0%, the EU

average is -0.3% (EC)

GDP growth in the EU countries in 2011

European Commission Economic Forecast

Autumn 2012

Source: European Commission, November 2012.

Real GDP growth (%)

2012 2013 2014

EU27 -0.3 0.4 1.6

Eurozone -0.4 0.1 1.4

Germany 0.8 0.8 2.0

Poland 2.4 1.8 2.6

Czech Republic -1.3 0.8 2.0

Slovak Republic 2.6 2.0 3.0

Hungary -1.2 0.3 1.3

Bulgaria 0.8 1.4 2.0

Romania 0.8 2.2 2.7

Unemployment rate

Mazowieckie

10.5%

Podlaskie

14.2%

Lubelskie

13.5%

Podkarpackie

15.6% Małopolskie

11.1%

Śląskie

10.8%

Opolskie

13.7%

Dolnośląskie

13.0%

Lubuskie

15.1%

Świętokrzyskie

15,2%

Łódzkie

13.5%

Wielkopolskie

9.5%

Warmińsko-

-Mazurskie

20.4%

Pomoskie

12.9%

Kujawsko-

-Pomorskie

17.3%

Zachodnio-

-Pomorskie

17.4%

14% >

11-13.9

10.9% <

Source: Central Statistical Office, November 2012

12/2012: 13.4%

2 136 thous.

Year Unemployed Unemployed with

higher education

2005 3 050 000 145 000

2012 1 979 000 235 000

UE: 11.7%

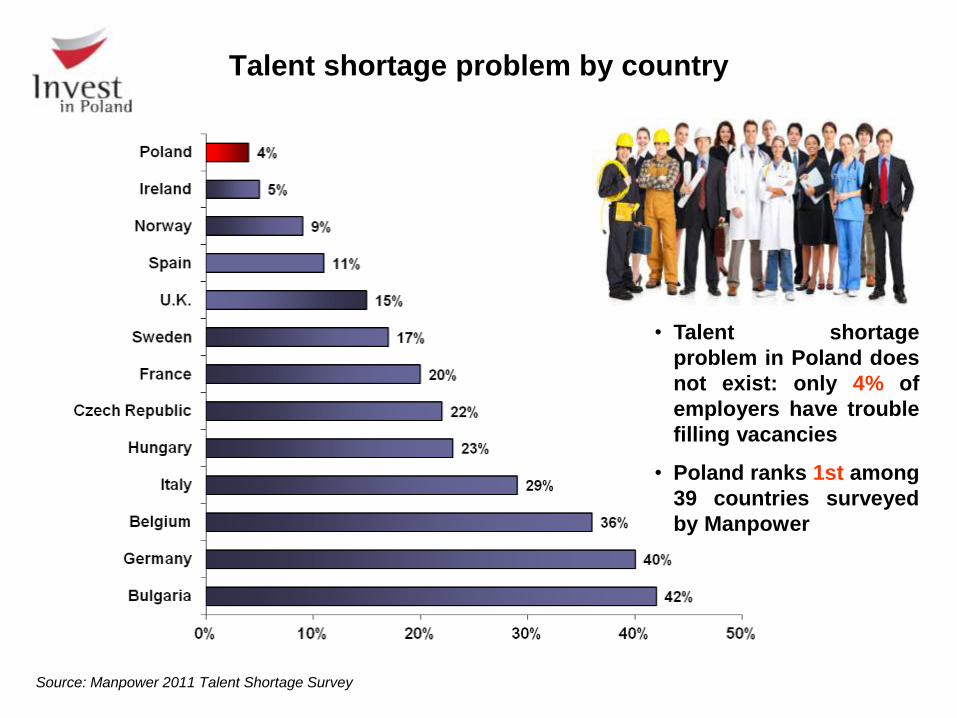

• Talent shortage

problem in Poland does

not exist: only 4% of

employers have trouble

filling vacancies

• Poland ranks 1st among

39 countries surveyed

by Manpower

Talent shortage problem by country

Source: Manpower 2011 Talent Shortage Survey

Source: Eurostat, March 2012

* data available only for 2010

Hourly labour costs in the business economy

in 2011 (in EUR)

Source: Eurostat, January 2013

Hourly labour costs growth in Q3 2011 and Q3 2012

(in %, Q-o-Q)

3,9

3,3

1,8

0,3

0,5

2,4

7,1

6,5

5,1

4

6,8

4,4

-2 -1 0 1 2 3 4 5 6 7 8 9 10 11 12

Germany

Ireland

United Kingdom

Slovenia

Czech Republic

Slovakia

Poland

Hungary

Latvia

Lithuania

Romania

Bulgaria

EU

O3 2011

O2 2012

22.4 m people aged 44 and less (mobility)

almost 2 m students

more than 480 thous. graduates in academic

year 2010/2011

more than 90% of students speak foreign

languages

460 higher education institutions

• 19 universities

• 23 technical universities

• 79 academies of economics

200 different majors taught

growing number of science students

Students and graduates

Source: Central Statistical Office

Academic centers

POZNAN

WROCLAW

WARSZAWA

KRAKOW

LODZ

SZCZECIN

TRI-CITY

KATOWICE

BYDGOSZCZ/TORUN BIALYSTOK

OLSZTYN

ZIELONA GORA

OPOLE KIELCE

LUBLIN

RZESZOW

201 >

151 – 200

101 – 150

51 – 100

50 <

No. of students (thousands)

City Students Graduates

Warszawa 276 000 65 300

Krakow 185 000 35 500

Wroclaw 146 000 30 000

Poznan 137 500 33 000

Lodz 120 500 27 500

Katowice 112 000 23 500

Tricity 95 000 20 500

Students in Poland

Number of students in 2010 (in thous.)

20 428

19 847

3 836

2 556

2 479

2 245

2 149

1 980

1 879

1 000

651

455

445

437

389

384

350

287

241

235

USA

EU 27

Japan

Germany

UK

France

Poland

Italy

Spain

Romania

Netherlands

Sweden

Belgium

Czech Rep.

Hungary

Portugal

Austria

Bulgaria

Denmark

SlovakiaSource: Eurostat, November 2012

• 11% of EU students come from Poland

• Italy and Spain, having larger populations than

Poland, educate fewer students

Imagine Cup is a global competition focused on finding IT solutions to real

world issues

In 2012 students from Technical University in Gdansk and Adam Mickiewicz

University in Poznan took the 2nd and 3rd place respectively.

Students and graduates – achievements

Source: www.microsoft.com, www.us.edu.pl

2011: Polish team from University of Silesia is a special winner of Samsung

Application Contest

Every third student doing internship in Microsoft HQs in Redmond (USA)

comes from Poland

The winners of the International Olympiad in Informatics (IOI) belong to the best

young computer scientists in the world

In 2008 Polish team took 1st place ex-aequo with Chinese one. The third place

individually was won by Pole, too

ACN International Collegiate Programming Contest is an annual multi-tiered

competitive programming competition among the universities of the world. The

contest is sponsored by IBM.

2012 held in Poland, Team from University of Warsaw took 2nd place beatting

110 teams

Average annual hours actually worked

(per person in total employment in 2011)

2 250

2 193

2 047

2 032

1 981

1 980

1 937

1 877

1 793

1 787

1 774

1 774

1 728

1690

1 684

1 644

1 625

1 522

1 475

1 413

1 379

Mexico

Korea*

Chile

Greece

Russian Fed.

Hungary

Poland

Turkey

Slovakia

USA

Czech Rep.

Italy

Japan

Spain

Finland

Sweden

UK

Denmark

France

Germany

Netherlands

Source: OECD Employment Outlook 2012

OECD average: 1 775 hrs

Poles are the 7th hardest

working nation in OECD

*data for 2010

Trade union density in OECD countries

in 2011 (in %)

70

68,8

67,7

54,6

52

35,1

35,6

28,1

25,8

24

18,2

19,3

18,5

19

17,5

17,3

17,2

16,8

15,9

15

11,39,7

Finland*

Denmark**

Sweden

Norway*

Belgium**

Italy*

Ireland

Austria*

UK

Greece***

The Netherlands

Portugal*

Germany*

Japan

OECD area

Czech Rep.**

Slovakia***

Hungary***

Spain**

Poland*

USA

Korea*

Source: OECD, Online OECD Employment database, 2013

Poland has one of the lowest trade

union memberships among OECD

countries

* data for 2010

** data for 2009

*** data for 2008

Modernisation of roads and railroads network

Source: GDDKiA, MT

Till 2006

2007-2013

2014 – 2020

New constructions

After 2020

Railroads Highways and expressways:

existing

under construction

planned

Passengers served by Polish airports (in millions)

Source: The Civil Aviation Office, 2012

Air transport

Direct flights to major European cities

London Warsaw, Gdańsk, Wrocław, Kraków, Rzeszów,

Szczecin, Bydgoszcz, Katowice, Poznan, Łódź

Frankfurt Warsaw, Gdańsk, Wrocław, Poznań, Kraków,

Katowice, Rzeszów

Munich Warsaw, Gdańsk, Wrocław, Kraków, Poznań

Paris Warsaw, Katowice, Kraków, Wroclaw, Poznań,

Gdańsk

Dublin Warsaw, Wrocław, Katowice, Kraków, Poznan,

Gdansk, Bydgoszcz, Szczecin, Łódź, Rzeszów

Oslo Warsaw, Katowice, Kraków, Wroclaw, Poznań,

Gdańsk, Szczecin

Milan Warsaw, Katowice, Kraków

Dortmund Warsaw, Katowice, Wroclaw, Kraków, Poznan,

Łódź

Brussels Warsaw, Katowice, Kraków, Wrocław

Location of main Polish airports

European flights

Domestic flights

Overseas flights

WARSZAWA

SZCZECIN

ZIELONA GÓRA

BYDGOSZCZ

ŁÓDŹ

RZESZÓW

WROCŁAW

KATOWICE

KRAKÓW

GDAŃSK

POZNAŃ

Airports under construction Q

Q

Q

Q Q

Q Q

Q

Q

MODLIN

LUBLIN

KILECE

Corporate Income Tax (CIT) rate: 19%

Personal Income Tax (PIT) rate: 18% and

32%

Value added tax (VAT):

• basic rate: 23%

• reduced rates: 8%, 5%

• export rate: 0%

Social Security Tax paid by employer:

between 19.48% and 22.67%

Tax rates

Source: http://www.worldwide-tax.com/

Entrepreneurs in Poland

pay one of the lowest CIT

in Europe

Corporate income tax rates across Europe

FDI stock in Poland

Geographical sources of FDI

Source: National Bank of Poland, 2012

Cumulative value of FDI (in EUR bn)

82,9 91,3107,0

124,2 134,3 143,7 150,4 153,4

2004 2005 2006 2007 2008 2009 2010 2011

26,8

20,418,7

13,1

10,59,3

5,8 5,6 5,65,3

5,0 3,9 3,7 3,31,3 1,3 1,2

0

5

10

15

20

25

30

Neth

erla

nds

Ger

man

y

France

Luxem

bourg Italy

USA

Switz

erland

Unite

d Kin

gdom

Austr

ia

Swed

en

Spai

n

Irel

and

Belg

ium

Cypru

s

Port

ugal

Finland

Japa

n

Major FDI investors in Poland

(FDI stock as of the end of 2010, in bn EUR)

FDI in Poland

Source: National Bank of Poland, 2012

10,3

6,4

4,4 4,1

10,28,3

15,717,2

10,19,34

10,47

13,6

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

FDI flow into Poland in years 2000 - 2011 (in EUR bn)

Wrocław

AUTOMOTIVE

Source: PAIiIZ compilation, 2012

ELECTRONICS

Services and Manufacturing Hubs in Poland

Gliwice, Tychy Wrocław, Jelcz Laskowice, Wałbrzych Poznań

Other Manufactures

Gorzów Wielkopolski Tczew, Kwidzyn

Other Manufactures

HOUSEHOLD APPLIANCES

Łódź, Radomsko Wrocław, Kobierzyce

Other Manufactures

Wronki

BSS

Wrocław

AEROSPACE

R&D

Rzeszów, Mielec, Świdnik Kalisz

Other Manufactures

Kraków

Other Centers

Wrocław Warszawa

Other Centers

Source: PAIiIZ compilation, 2012

Services and Manufacturing Hubs in Poland

Wrocław Łódź

Sectors of opportunities

• Extraction: shale gas

• Energy: nuclear power plant

• Renewable energy

• Infrastructure

• Food Industry

• Tourism

• Construction

• Research & Development

•

Energy investments

PLN 60 bn for energy investments:

• construction of new power blocks

in Turow, Kozienice, Opole,

Pulawy, Blachownia, Stalowa

Wola, Jaworzno, Wloclawek

• construction of LPG terminal in

Swinoujscie in progress

• construction of new gas pipelines

and magazines

• extension of oil terminal in

Gdansk

Seaport investments

Projects:

sea port Szczecin – Świnoujście

(EUR 530 mn)

sea port Gdynia (EUR 467 mn),

sea port Gdańsk (EUR 270 mn)

EUR 1,3 bn for sea ports infrastructure in years 2013 – 2020

Source: The Ministry of Transport, Construction and Maritime Economy

Road & highway investments

Projects:

ringroad of Poznan,

highways: A1 Tuszyn-

Pyrzowice,

S19 Rzeszow-Lublin,

S7 Gdansk-Warsaw,

S5 Wroclaw-Poznan and

Warsaw-Krakow

PLN 43 bn for roads and highways in years 2012 – 2015

Source: The Ministry of Transport, Construction and Maritime Economy

Source: The Civil Aviation Office, The Ministry of Transport, Construction and Maritime Economy

Location of main Polish airports

European flights

Domestic flights

Overseas flights

WARSZAWA

SZCZECIN

ZIELONA GÓRA

BYDGOSZCZ

ŁÓDŹ

RZESZÓW

WROCŁAW

KATOWICE

KRAKÓW

GDAŃSK

POZNAŃ

Airports under construction Q

Q

Q

Q Q

Q Q

Q

Q

MODLIN

LUBLIN

KILECE

GDYNIA

Airport investments

Planned investments in

modernisation, development

of passenger terminals and

airport infrastructure at

following Polish airports:

Gdańsk,

Kraków,

Katowice,

Poznań,

Wrocław

Rzeszów

Łódź

Szczecin

Bydgoszcz

Zielona Góra

Railway investments

PLN 30 bn for railways in years 2013-2015 (including

new trains purchase)

PKP Polskie Linie Kolejowe S.A. is a company of the

PKP Group and is responsible for maintenance of

railway lines (19 276 km), railway traffic management,

construction of timetables and management of railway

properties

General assessment of the

technical condition of

railway lines

Source: PKP PLK

RAILWAY LINE C-E 59

section Wrocław – Kostrzyn – Szczecin

30

The most important data on railway line C-E 59 section

Wrocław – Kostrzyn – Szczecin:

Total length: 355,6 km railway lines;

Modernization or revitalization of 46 stations;

355,6 km railway lines,

Railway line is fully electrified;

Single-track

from 0,306 km to 2,200 km;

from 348,721 km to 350,355 km;

Double-track

from 2,200 km to 348,721 km;

from 350,355 km to 355,904 km.

Modernization or revitalization of line C-E 59 will increase

the accessibility to Szczecin and Świnoujście Seaport

Szczecin and

Świnoujście

Seaport

Polish investment abroad

29

42

53

45

316

31

16

-90

230

305

955

3392

9168

5664

4613

4562

7484

7335

-4000

-2000

0

2000

4000

6000

8000

10000

Source: PAIiIZ, NBP, 2013

The value of Polish FDI abroad at the end of

2011 amounted to USD 49.6 bn

32 Source: UNCTAD, World Investment Prospects Survey 2009-2011, World Investment Report 2012.

Main advantages of Poland

• Stable economic situation

• Market growth

• Size of internal market

• Access to regional markets

• Cooperation with suppliers and

business

• System of investment incentives

Poland is among 15 most attractive investment locations in the world

World Investment Report UNCTAD

Source: Bloomberg Rankings - Jan 22, 2013

• Poland as best-performing CEE

country

• Factors taken into consideration: - degree of economic integration,

- cost of setting up business,

- cost of labour and material,

- cost of moving goods,

- less tangible costs,

- readiness of the local consumer base.

Best countries for doing business 2013

E&Y 2012 European Attractiveness Survey

Source: Ernst & Young, 2012 European Attractiveness Survey, 2012

According to investors surveyed by E&Y

the strengths of Poland are:

• large domestic market,

• well-qualified and productive workforce,

• stable macroeconomic situation in difficult

times,

• relatively low level of public debt comparing

to Western European countries,

• transparent tax and legal systems,

• favorable conditions both for manufacturing

and services investments

35%

10%

8%

7%

4%

3%

3%

2%

2%

2%

2%

2%

2%

Germany

Poland

UK

Russia

France

Romania

Czech Rep.

Turkey

Switzerland

Netherlands

Italy

Spain

Sweden

What are the most attractive countries for FDI in the next 3 years?

„Poland is already the champion of

Europe - in terms of economic

growth. An estimated GDP growth

for 2011 was revised upwards by

Brussels (to 4.3%) and is nearly

three times bigger than the average

of 27 (1.5 %).

What saved the Polish growth

during the 2009 crisis is that it is

driven by strong domestic demand

(population of 38 million).”

Le Figaro (March 2012) La Pologne, championne

européenne de la croissance

„Poland is the South Korea

of Europe – its economy

moves faster than the

German locomotive.”

La Repubblica (June 2012)

„Poland remains, despite the

crisis, the champion of

economic growth. The state

budget has doubled in the

last decade, the country was

well governed.”

Die Welt (June 2012), Wunderkind Polen

Media about Poland

Tax breaks

CIT exemption in Special Economic Zone

Real estate tax exemption

Cash support

Government grants

Cash grants available through EU Funds

Forms of regional aid

Special Economic Zones

Definition

• a special economic zone (SEZ) is a designated

area in which manufacturing or distribution

activities can be conducted on preferential

terms

• 14 SEZ in Poland, with several subzones

The purpose

• support regional development

Total area

• up to 20 000 hectares

Time of operation

• 31st December 2020

Permits to conduct activities in SEZ

• issued by the authorities of each SEZ

Benefits from obtaining a permit to conduct activities in SEZ :

• eligibility for income tax exemption

• plot of land prepared for an investment project

• free assistance in dealing with formalities relating to the investment project

Production

- automotive

- electronics

- aviation

- biotechnology

- „big investment” in other sectors

Modern

services

- ICT

- SSC

- BPO

- R&D activity

Program of support of investments of considerable importance

for Polish economy

Government grants

Purpose of support

development of innovativeness and competitiveness of Polish economy

Result of support

53 programmes of total amount PLN 900 m (since 2004)

18.9 thous. of new jobs

Source: PAIiIZ, Ministry of Economy

More than EUR 87 billion from the EU Funds

in years 2007-2013

Why Poland? Summary

Availability of skilled human resources

Economic and political stability

Effective incentives system

Strategic location – gateway to the EU

Short list

Investment decision

Long list of countries

Considering of investment

• PM assistance

• site visits

• macroeconomic and sector specific data,

information on financial incentives, SEZ

and EU funds

• assistance in obtaining financial support

from the state government

• co-operation with SEZ

• date base of suppliers and business

partners and real estate data base

• after-care services

• ombudsman for foreign investors

• marketing campaigns, investment

seminars, work-shops, study tours

• co-operation with Polish Embassies

abroad

Investment process Agency’s offer

Agency’s offer

Projekty zakończone pozytywną decyzją inwestycyjną

w 2012 r.

Investments by country of origin

3

4

4

4

4

2

1

2

1 1

2

1

53 INVESTMENT

PROJECTS

The largest investors from the point of view of invested capital

1 236 thousand EUR of investment

The largest investors from the point of wiec of the number of job plces created

9 996 NEW WORK PLACES

Active projects serviced by PAIIIZ

(as of end of January 2013)

PAIIIZ has in the project pipeline 152 potential investments

• Value of investment: EUR 3.8 bn

• Number of new job places: 26 902

• Main sectors:

• modern services (40)

• automotive (23)

• R&D (15)

• machinery (11)

• Major countries-investors:

• USA (45)

• Germany (17)

• China (12)

• Great Britain (12)

Thank you for your attention

00-585 Warszawa, ul. Bagatela 12

tel. (+48 22) 334 98 00, fax (+48 22) 334 99 99

e-mail: [email protected]