Philippine fiscal and expenditure management reforms - Rolando Toledo - Philippines

20

Philippine Fiscal and Expenditure Management Reforms 11 th OECD-Asian Senior Budget Officials Annual Meeting Department of Budget and Management Philippines December 17-18, 2015. Bangkok, Thailand 1

-

Upload

oecd-governance -

Category

Government & Nonprofit

-

view

574 -

download

8

Transcript of Philippine fiscal and expenditure management reforms - Rolando Toledo - Philippines

Philippine Fiscal and Expenditure Management

Reforms

11th OECD-Asian Senior Budget Officials

Annual Meeting

Department of Budget and Management

Philippines

December 17-18, 2015.

Bangkok, Thailand

1

I. Recent Fiscal Performance

II. Key Expenditure Management Reform

III. Climate Budgeting

OUTLINE

2

Strong revenue performance has led to ample fiscal space Revenues continue to grow faster than GDP; BOC led 2014 revenue expansion at 21%

In Billion Pesos

2012 2013 2014

Growth Rate (2014/2013)

Total Revenues 1,534.9 1,716.1 1,908.5 11.2% % of GDP 14.5% 14.9% 15.1%

Tax Revenues 1,361,1 1,535.7 1,720.1 11.9% % of GDP 12.9% 13.3% 13.6%

BIR 1,057.9 1,216.7 1,334.8 9.7% % of GDP 10.0% 10.5% 10.6%

BOC 289.9 304.9 369.3 21.1% % of GDP 2.7% 2.6% 2.9%

Other Offices 13.3 14.1 16.1 5.9% Non-Tax Revenues 173.8 180.4 188.4 5.1%

% of GDP 1.6% 1.5% 1.5% Expenditures 1,777.8 1,880.2 1,981.6 5.4%

% of GDP 16.8% 16.3% 15.7% Surplus/(Deficit) (242.8) (164.1) (73.1) -55.4% % of GDP -2.3% -1.4% -0.6% Nominal GDP 10,561 11,542 12,643 9.5%

3

National Government’s fiscal consolidation efforts are on track Over five years we have increased revenues by 58%, expenditures by 30%,

and narrowed the deficit

Revenues Expenditures Surplus/(Deficit)

PhpBn

1,207.9

1,522.4

(314.5)

1,359.9

1,557.7

(197.8)

1,534.9

1,777.8

(242.8)

1,716.1

1,880.2

(164.1)

1,908.5 1,981.6

(73.1)

-500

0

500

1,000

1,500

2,000

2,500

-3.5% of

GDP -0.6 % of

GDP

2010 2011 2012 2013 2014 2010 2011 2012 2013 2014

2010 2011 2012 2013 2014

+30% 2014 vs 2010

+58% 2014 vs 2010

Contained to

-0.6% of GDP

4

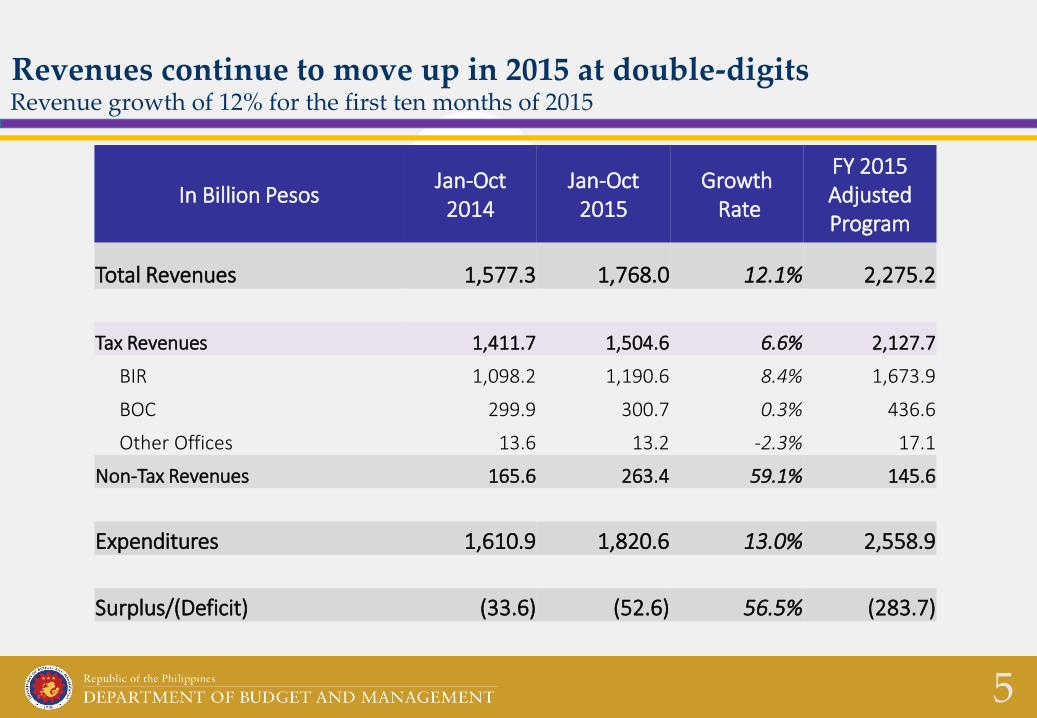

In Billion Pesos

Jan-Oct 2014

Jan-Oct 2015

Growth Rate

FY 2015 Adjusted Program

Total Revenues 1,577.3 1,768.0 12.1% 2,275.2

Tax Revenues 1,411.7 1,504.6 6.6% 2,127.7

BIR 1,098.2 1,190.6 8.4% 1,673.9

BOC 299.9 300.7 0.3% 436.6

Other Offices 13.6 13.2 -2.3% 17.1

Non-Tax Revenues 165.6 263.4 59.1% 145.6

Expenditures 1,610.9 1,820.6 13.0% 2,558.9

Surplus/(Deficit) (33.6) (52.6) 56.5% (283.7)

Revenues continue to move up in 2015 at double-digits Revenue growth of 12% for the first ten months of 2015

5

6

General Government Debt

54.8 52.4 51.0 51.549.2

45.4 44.9

40

45

50

55

2009 2010 2011 2012 2013 2014 2015

National Government Debt

44.3 42.2 41.4 40.639.2

36.4 36.2

35

40

45

2009 2010 2011 2012 2013 2014 2015

% of GDP % of GDP

S1 S1

General Government Debt is composed of the National Government debt (less the debt held by the Bond Sinking Fund), the debt of Social Security Institutions (GSIS, SSS and PhilHealth ) and the Local Government Units (LGU)

Improving debt metrics; lower reliance on foreign debt Further consolidation of debt creating a sustainable fiscal environment

(356.6) (175.1) (162.7)44.8 82.2

(153.5) (129.8)

-4.0%

-1.8% -1.5%

0.4% 0.7%

-1.1% -0.8

-5.0-4.0-3.0-2.0-1.00.01.02.0

-500.0-400.0-300.0-200.0-100.0

0.0100.0200.0

2010 2011 2012 2013 2014 2015 2016

Consolidated Public Sector Financial Position

% of GDP Php bn

Achieved surplus for two consecutive years

Program BESF

BESF – Budget of Expenditures and Sources of Financing

7

8

Social Services Expenditures, FYs 2011-2016 Increased spending and receiving largest portion of the budget

Expenditures for Major Social Programs. The government’s spending for its social services continues its upward trend, increasing by 29.4% in the proposed 2016 Budget as compared to the 2015 level. Overall, the budget for these select social programs has increased by 40% since the start of the Aquino administration, resulting to a 400.4% increase from the P43.1 billion level in 2011 to P215.8 billion come 2016.

Infrastructure Investment, FYs 2010-2016 Nearly 3 times the 1.8% in 2010

9

1.8 %

5.0 %

5.4 %

The government continues to invest in public infrastructures such as road and transport infrastructures, irrigation, farm-to-market roads and other public infrastructures, as one of the key drivers of economic development. In 2016, the government is proposing some P766.5 billion of infrastructure investments, equivalent to 5.0 percent of GDP, nearly three (3) times the 1.8 percent in 2010, and leading the way to the 5.4 percent medium-term target by 2018. These will interconnect growth areas, supporting agriculture and tourism development by providing market access, and accessible routes to tourist destinations, spurring trade, livelihood and investment activities, and at the same time generate employment.

Nominal data from 2010 to 2014 are actual obligations while for 2015 and 2016 are the enacted budget and proposed budget, respectively. Infrastructure Outlays refer to the infrastructure expenditure of the National Government, inclusive of infrastructure subsidies to Government Corporations and infrastructure transfers to Local Government Units. This level however excludes internally generated funds of the Government Corporations and Local Government Units.

• Operating expenditures contained through hard budget ceilings

• Agencies’ absorptive capacity considered in the setting of budget ceilings

• Aligned w/ Budget Priorities Framework

• Implementation-ready proposals prioritized

• Agencies can absorb additional funds

10

Spending Within Our Means Two-Tier Budgeting Approach

TIER 1: OPERATING EXPENDITURES +

ONGOING PROGRAMS

TIER 2: NEW/EXPANDED PROGRAMS

1

1.5

2

2.5

3

2009 2010 2011 2012 2013 2014 2015 2016

Growth of Fiscal Space

Obligation Ceiling Forward Estimates

2016 Fiscal Space = P582.7 billion

1

1.5

2

2.5

3

2009 2010 2011 2012 2013 2014 2015 2016

Growth of Fiscal Space

Obligation Ceiling Forward Estimates

Faster Budget Process via GAA-as-Release Document, Early Bidding, Cashless & Checkless Payments, etc. reforms that streamline processes

Unified Account Codes enables the efficient tracking of each budget item: from enactment to implementation, accounting, and audit.

Agency lump sum funds disaggregated & key Special Purpose Funds reduced

[

Clearer Savings, Augmentation & Realignment rules to strengthen budget integrity while providing sufficient flexibilities for managers

11

Delivering Measurable Results Faster & Better Service Delivery

Full-Time Delivery Units to drive performance, address bottlenecks, and regularly monitor and report on progress

More Bids & Awards Committees & assignment of full-time secretariats

Hiring of key staff: planning, procurement, project management, technical specialists, monitoring & evaluation

Assigning DPWH as government construction agency and making other departments (e.g. DepEd, DoH, DA) focus on core mandates

12

Delivering Measurable Results Addressing Institutional Weaknesses

Transparency Seal sustained in the 2016 Budget; compliance so far at 98% of agencies

Open Data Philippines intensified by requiring all agencies to publish data in open & machine-readable formats & w/ open licenses

Performance in International Fiscal Transparency Standards improved through new budget publications

Bottom-Up Budgeting pursued with P24.7 billion in poverty reduction projects identified by CSOs & communities in 1,514 cities & municipalities

13

Empowerment Through the Budget Fiscal Transparency and Participation

14

Climate Budgeting

in the Philippines

The country’s response to climate change

15

A transformative agenda

Climate Change Commission

and Cabinet Cluster

on Climate Change Adaptation

and Mitigation

Mobilizing the

Budgetary process

National Climate Budgeting Integrating climate response into the budget cycle

16

1. Identify climate change adaptation or mitigation measures.

2. Tag climate change expenditures using a climate change

typology.

3. Submit a list of climate change expenditures to the DBM,

CCC, and DILG (in the case of LGUs).

TYPOLOGY of the climate responses

Climate change expenditure tagging identifies government’s climate response

17

FY 2015 GAA

140.9 billion pesos

programs, projects, and

activities tagged by 55

national government

agencies

National Budget

31 local government

units undertook their

own climate tagging to assess

their climate priorities

Local

Government

361

Climate Budgeting

18

FY 2016 NEP

166.3 billion pesos

FLOOD CONTROL

AND MANAGEMENT

INCREASED

FOREST COVER

MULTI-HAZARD

MAPS

RENEWABLE

ENERGY

MAJOR

RIVER BASINS

P91.6 B (2 billion US dollars)

Risk Resiliency Program

19

11th OECD-Asian Senior Budget Officials Annual Meeting

Department of Budget and Management

Philippines

December 17-18, 2015.

Bangkok, Thailand

20