pg 23. INTERVIEW: Dr. Harikishan Koppula Reddy pg 25...

32

1 ST – 15 TH July 2014 . Vol 1 Issue 6 . For Private Circulation Only pg 23. INTERVIEW: Dr. Harikishan Koppula Reddy pg 25. Indian Economy – Trend indicators

Transcript of pg 23. INTERVIEW: Dr. Harikishan Koppula Reddy pg 25...

1ST – 15TH July 2014 . Vol 1 Issue 6 . For Private Circulation Only

pg 23. INTERVIEW: Dr. Harikishan Koppula Reddy

pg 25. Indian Economy – Trend indicators

3GROUND ZERO GROUND ZERO 1 - 15 July 2014 1 - 15 July 2014 2

VOL 1 . ISSUE 5 . 1ST - 15TH JULY 2014

Vineet Bhatnagar- Managing Director and CEO

EDITORIAL BOARD:Naveen Kulkarni Manish AgarwallaKinshuk Bharti Tiwari Dhawal Doshi

COVER & MAGAZINE DESIGN Chaitanya Modak, www.inhousedesign.co.in

FOR EDITORIAL QUERIES:PhillipCapital (India) Private LimitedNo. 1, 2nd Floor, Modern Centre, 101 K.K. Marg, Jacob Circle, Mahalaxmi, Mumbai 400 011

RESEARCH Automobiles Deepak Jain, Priya Ranjan

Banking, NBFCs Manish Agarwalla, Sachit Motwani, Paresh Jain

Consumer, Media, Telecom Naveen Kulkarni, Vivekanand Subbaraman, Manish Pushkar

Cement Vaibhav Agarwal

Economics Anjali Verma

Engineering, Capital Goods Ankur Sharma, Aditya Bahety

Infrastructure & IT Services Vibhor Singhal, Varun Vijayan

Metals Dhawal Doshi, Dharmesh Shah

Mid-caps Vikram Suryavanshi

Oil & Gas, Agri Inputs Gauri Anand, Deepak Pareek

Pharmaceuticals Surya Patra

Retail, Real Estate Abhishek Ranganathan, Neha Garg

Technicals Subodh Gupta

Production Manager Ganesh Deorukhkar

Database Manager Vishal Randive

Sr. Manager – Equities Support Rosie Ferns

SALES & DISTRIBUTION Kinshuk Tiwari, Ashvin Patil, Shubhangi Agrawal, Kishor Binwal, Sidharth Agrawal, Dipesh Sohani, Varun Kumar

GROUND ZERO - PREVIOUS ISSUES

1st June 2014 Issue 4

1st May 2014 Issue 3

16th June 2014 Issue 5

3GROUND ZERO GROUND ZERO 1 - 15 July 2014 1 - 15 July 2014 2

4. COVER STORY: Diesel Gensets - In a sweet spot

Ground Zero explores the dynamics of the Indian diesel genset industry which is entering a sweet spot over the next two years

23. INTERVIEW: Dr. Harikishan Reddy

on the opportunities and challenges in the road sector

25. Indian Economy: Trend indicators

27. PhillipCapital Coverage Universe: Valuation Summary

LETTER FROM THE MANAGING DIRECTORIn his election campaigns, PM Modi promised un-

interrupted electricity supply to millions of house-

holds across India that are currently reeling under

power deficits. This promise is unlikely to be met

over the next two years as significant ramp-up in in

coal production seems remote even as a pickup in

economic activity will lead to higher power deficits.

The industrial power demand deficit will need to

be bridged by alternate sources like diesel-Genset

(DG) based power, which is the most reliable and

time-tested option despite its high per unit costs.

The DG set market in India contracted by 15% in

FY14 and FY15 is likely to be the bottom for this

market.

Our cover story on prognosis for demand of DG

sets written by our capital goods and power sector

analysts Ankur Sharma and Aditya Bahety explores

the changing regulatory environment and its impact

on the industry structure. Further consolidation of

an already concentrated DG set market will have an

incisive impact on profitability, making the segment

more attractive.

This edition also examines the issues and challeng-

es faced by build-operate-transport road develop-

ers, key participants in fulfilling the 30-kilometer/

day road construction target of the transport

ministry.

And finally, the much awaited budget is round the

corner. The government’s reformist agenda will be

put to a stern test as we grapple with a crippling

El Nino and dangerous signals emanating from the

Middle East.

Best Wishes

Vineet

CONTENTS

5GROUND ZERO GROUND ZERO 1 - 15 July 2014 1 - 15 July 2014 4

Cummins genset being used in a remote area

15% - 20% of DG volumes are supplied by the unorganised sector

5GROUND ZERO GROUND ZERO 1 - 15 July 2014 1 - 15 July 2014 4

COVER STORY

After a sharp slowdown in FY14, the Indian diesel genset industry is set for a rebound from

FY16 onwards. This would be lead by a revival in infrastructure spending and get a further

boost as commercial and residential real estate picks up alongside industrial spending.

Stagnant to muted coal production growth is expected to lead to higher power deficits

and increased DG demand. The competitive dynamics of the industry are also set to see

a sea change with the new CPCB II norms – more so in the lower kva (<180kva) where

the unorganized sector has ~15-20% of the market. These players may be forced to exit

the industry and their market share taken by players such as Cummins India, KOEL and

Mahindra.

BY ANKUR SHARMA & ADITYA BAHETY

pg. 6 Diesel Gensets in a sweet spot Increased genset demand amidst short fall in coal production___________________________________________pg.9 Slow down in FY14 a short term blip So what led to the slowdown in demand for DG sets over the last one year?___________________________________________pg.14 Top 5 player have 80% market share Competitive intensity and market share___________________________________________pg.16 New CPCB II norms from July 1, 2014 Are the new CPCB norms really a game changer for the industry in terms of competition?___________________________________________pg.19 Profiles Key players in the Indian Diesel Generator Set market___________________________________________

7GROUND ZERO GROUND ZERO 1 - 15 July 2014 1 - 15 July 2014 6

In 2003, the Indian government had set a

target of “Power for all” by 2012. It was

expected that the Electricity Act would usher

in a new era of private participation in power,

open up access, and cause a sharp reduction in

T&D losses and hence availability of cheap power

to the masses.

While much water has flown under the bridge

since then, India remains a power-starved coun-

try with many states continuing to face severe

power shortages, especially in the summers; this

is particularly true for the Southern states (Tamil

Nadu and Andhra Pradesh — now Telangana and

Seemandhra), Uttar Pradesh, Haryana, and Bihar.

Availability of 24/7 reliable power from the grid

remains a dream in most states even today, and

Increased genset demand amidst short fall in coal production

D I E S E L G E N S E T I N A S W E E T S P O T

Power deficit by region

the poor financial condition of SEBs implies further

power cuts for the consumers and the industry.

This in turn has provided a huge opportunity for

diesel genset manufacturers, who continue to add

around 9GW of capacity every year. To put it in

perspective, over the last three years, India has

added 17-18GW of power capacity every year

(ex-renewables), but a large portion of the new

capacity continues to operate at around 60-65%

utilization levels, not because of lack of demand,

but mainly because there is a shortage of coal

to fire the power plants. We believe that DG

set manufacturers could be in a sweet spot over

the next two years if economic growth revives and

Coal India is unable to ramp up capacity signif-

icantly – this may result in higher power deficits

and increased demand for backup power.

Continued increase in losses has led to higher power cuts by discoms (Rs bn)

7GROUND ZERO GROUND ZERO 1 - 15 July 2014 1 - 15 July 2014 6

Sour

ce: A

mfi

Indi

a, W

orld

Gol

d Co

uncil

, Phi

llipC

apita

l Ind

ia R

esea

rch

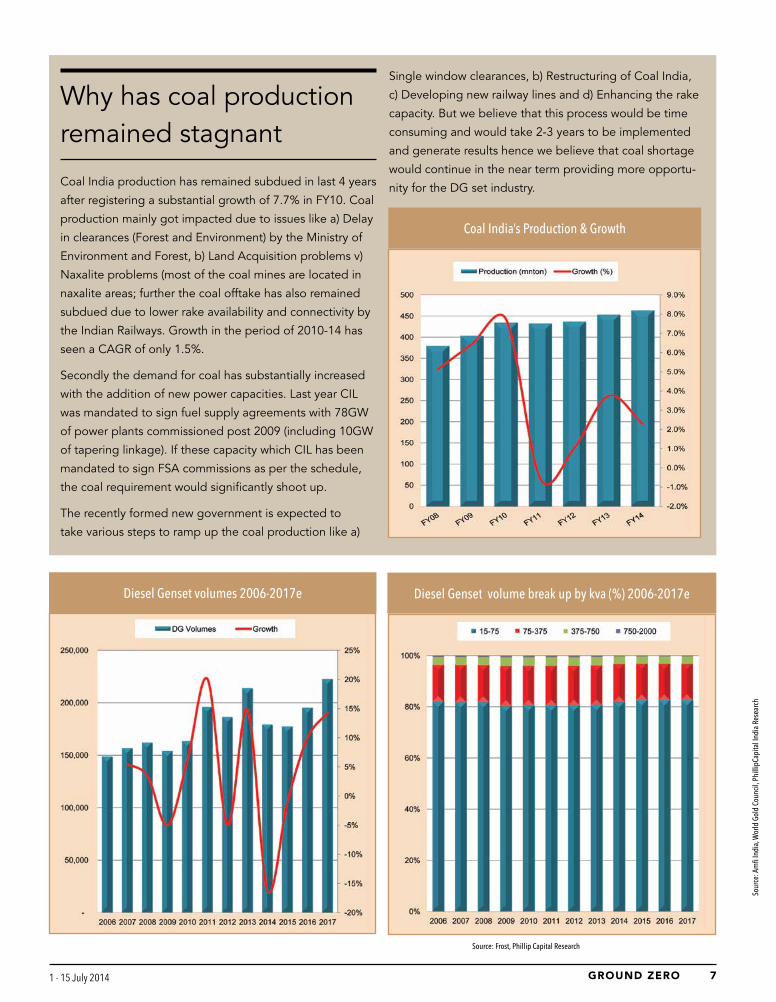

Coal India production has remained subdued in last 4 years

after registering a substantial growth of 7.7% in FY10. Coal

production mainly got impacted due to issues like a) Delay

in clearances (Forest and Environment) by the Ministry of

Environment and Forest, b) Land Acquisition problems v)

Naxalite problems (most of the coal mines are located in

naxalite areas; further the coal offtake has also remained

subdued due to lower rake availability and connectivity by

the Indian Railways. Growth in the period of 2010-14 has

seen a CAGR of only 1.5%.

Secondly the demand for coal has substantially increased

with the addition of new power capacities. Last year CIL

was mandated to sign fuel supply agreements with 78GW

of power plants commissioned post 2009 (including 10GW

of tapering linkage). If these capacity which CIL has been

mandated to sign FSA commissions as per the schedule,

the coal requirement would significantly shoot up.

The recently formed new government is expected to

take various steps to ramp up the coal production like a)

Diesel Genset volumes 2006-2017e

Single window clearances, b) Restructuring of Coal India,

c) Developing new railway lines and d) Enhancing the rake

capacity. But we believe that this process would be time

consuming and would take 2-3 years to be implemented

and generate results hence we believe that coal shortage

would continue in the near term providing more opportu-

nity for the DG set industry.

Coal India’s Production & Growth

Diesel Genset volume break up by kva (%) 2006-2017e

Source: Frost, Phillip Capital Research

Why has coal production remained stagnant

9GROUND ZERO GROUND ZERO 1 - 15 July 2014 1 - 15 July 2014 8

Description Rs per unit

Solar Rs8-9

Domestic Coal Rs3 – 4

Hydro Rs2-3

DG set Rs15-18

Wind Rs5-6

Cost of power generated

Key players operating in the Indian DG industry

include Cummins India, Kirloskar Oil Engines, Ma-

hindra Powerol, Greaves Cotton, Ashok Leyland,

Eicher, and Caterpillar/Perkins. While Cummins

Engine/Generator set supplier 15-75 kVA 75-375 kVA 375-750 kVA Above 750 kVA Brand

Cummins India Ltd u n n n Cummins

Kirloskar Oil Engines Ltd l l l Kirloskar Green

Mahindra n u Mahindra Powerol

Ashok Leyland u l Leypower

Eicher India l Multi-brand

Escorts India u Multi-brand

Greaves Cotton Ltd u l u Greaves Whisper

Kirloskar Electric u u u Kirloskar Bliss

Caterpillar India u l l CAT

MTU India u MTU

l l u nMajor Presence Moderate Presence Low Presence Market Leader Future Focus

Market presence by different nodes of the DG set market

India dominates the mid- to high-kva segments

(ratings >180kva), Kirloskar Oil Engines is a market

leader in the low- to mid-kva segments.

Source: Frost, Phillip Capital Research

With bulk diesel prices linked to the market from

last year, cost of power generation using diesel

gensets has gone up to Rs15-18/unit, which ap-

pears to be quite expensive vs. traditional sources

of power generation such as coal, hydro, wind,

gas, and solar, whose cost of generation is in the

range of Rs3 to Rs9 per unit. However, given the

poor quality of grid power, the dependency on DG

sets for backup power has continued to increase

in India.

High per unit cost not a deterrent for DG set users

9GROUND ZERO GROUND ZERO 1 - 15 July 2014 1 - 15 July 2014 8

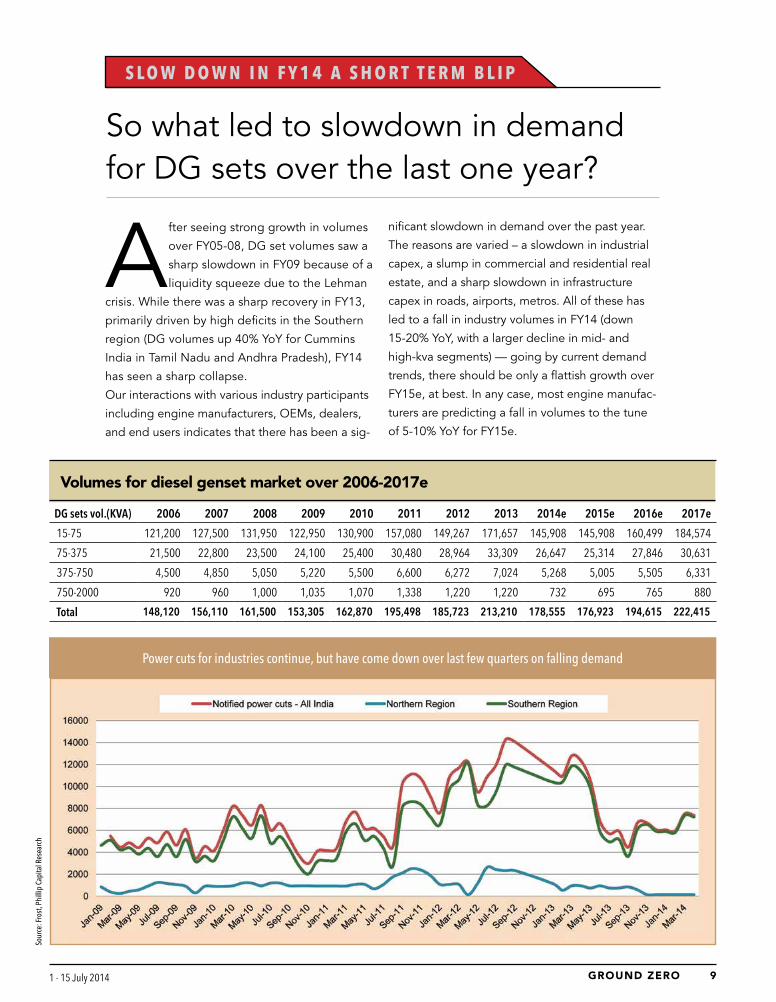

S L O W D O W N I N F Y 1 4 A S H O R T T E R M B L I P

So what led to slowdown in demand for DG sets over the last one year?

A fter seeing strong growth in volumes

over FY05-08, DG set volumes saw a

sharp slowdown in FY09 because of a

liquidity squeeze due to the Lehman

crisis. While there was a sharp recovery in FY13,

primarily driven by high deficits in the Southern

region (DG volumes up 40% YoY for Cummins

India in Tamil Nadu and Andhra Pradesh), FY14

has seen a sharp collapse.

Our interactions with various industry participants

including engine manufacturers, OEMs, dealers,

and end users indicates that there has been a sig-

nificant slowdown in demand over the past year.

The reasons are varied – a slowdown in industrial

capex, a slump in commercial and residential real

estate, and a sharp slowdown in infrastructure

capex in roads, airports, metros. All of these has

led to a fall in industry volumes in FY14 (down

15-20% YoY, with a larger decline in mid- and

high-kva segments) — going by current demand

trends, there should be only a flattish growth over

FY15e, at best. In any case, most engine manufac-

turers are predicting a fall in volumes to the tune

of 5-10% YoY for FY15e.

Power cuts for industries continue, but have come down over last few quarters on falling demand

DG sets vol.(KVA) 2006 2007 2008 2009 2010 2011 2012 2013 2014e 2015e 2016e 2017e

15-75 121,200 127,500 131,950 122,950 130,900 157,080 149,267 171,657 145,908 145,908 160,499 184,574

75-375 21,500 22,800 23,500 24,100 25,400 30,480 28,964 33,309 26,647 25,314 27,846 30,631

375-750 4,500 4,850 5,050 5,220 5,500 6,600 6,272 7,024 5,268 5,005 5,505 6,331

750-2000 920 960 1,000 1,035 1,070 1,338 1,220 1,220 732 695 765 880

Total 148,120 156,110 161,500 153,305 162,870 195,498 185,723 213,210 178,555 176,923 194,615 222,415

Volumes for diesel genset market over 2006-2017e

Sour

ce: F

rost

, Phi

llip

Capi

tal R

esea

rch

11GROUND ZERO GROUND ZERO 1 - 15 July 2014 1 - 15 July 2014 10

Power deficits certainly help revive demand in

the short term (note the current surge in volumes

in North India and the sharp jump in volumes in

Tamil Nadu and Andhra Pradesh in FY13). Howev-

er, a repeat of the sustained growth in volumes (as

seen in 2005-2008) requires a revival of spending

on infrastructure, real estate, and industrial capex.

Ratings Segment End Use Industries

<200 kVA Telecom(15-75kva), Retail sales, Small scale Industries Units

200-375 kVA Real Estate, Healthcare

375-750 kVA Large Industrial Applications, IT, ITES, Hospitals, Hotels, Healthcare

750-3,000 kVA Prime Power

Usage of Diesel Generators by sector and ratings

Segment % share Kva range Main DG suppliers

Telecom 10% 15-75 Mahindra, KOEL, Eicher

Large Industries 20% 375-2000 Cummins, KOEL, CAT, Perkins, Greaves, Leyland

Hospitals 15% 375-750 Cummins, KOEL, CAT, Perkins, Greaves, Leyland

Hotels 15% 75-375 Cummins, KOEL, CAT, Perkins, Greaves,

IT/ITES 12% 375-750 Cummins, KOEL, CAT, Perkins

Residential real Estate 20% 375-750 Cummins, KOEL, CAT, Perkins

Others 13%

Segment-wise end market for diesel gensets

Cummins DG set being used in an industry

Strong correlation between IIP and DG set volumes

Our interaction with various industry participants

indicates that FY15 could be the bottom for

the market and it should revive from FY16. There

is a belief that the new government at the centre

would help revive economic growth via increased

infra spending — this will in turn benefit DG set

manufacturers.

Commercial real estate including hotels, IT/ITES

(amongst the key end-markets for DG players) is

starting to see a fall in vacancy rates and our inter-

action with channel partners indicates that enquiry

levels are starting to improve for developers in

Noida, Bangalore, and parts of Mumbai. The rise

in demand in Bangalore is being led by the IT

sector — Cummins India has a 75-80% share in

the IT/ITES space in Karnataka.

11GROUND ZERO GROUND ZERO 1 - 15 July 2014 1 - 15 July 2014 10

Residential real estate may take longer to recover (likely from mid-FY16 onwards) especially in Tier-1 and Tier-2 cities — high prices coupled with a continued slowdown in new project launches may hinder any fast revival in DG-set demand over the near term.

Perk

ins s

et b

eing

use

d fo

r ind

ustri

al a

pplic

atio

nCu

mm

nis D

G se

t in

use

at a

resid

entia

l site

13GROUND ZERO GROUND ZERO 1 - 15 July 2014 1 - 15 July 2014 12

Cummins DG set being used at the Mumbai monorail site

There is a shift in the nature of the demand for DG sets — while they were previously used as a prime power source, now as much as 70-80% of sets sold in the country are used mainly for standby power. This implies there is a clear shift in usage of DG sets as backup power in case of power failure.

Application-wise usage of DG setsBase Load - 80% of load is usedPrime Load - 100% of load is usedStandby - Once in 12 hrs

A restarting of stalled road projects along with new road projects over the next few quarters coupled with a pickup in metro/mono rail construction could also revive demand for DG sets. Our discussions with NHAI (recently in Delhi) indicated that they have already done a lot of work to bring the road sector back into shape – NHAI is targeting road awards of ~8,500kms in FY15 vs. 1,500kms in FY14. Around 6,000kms of EPC projects are proposed to be awarded — this, along with a restarting of stalled projects will lead to higher spending in road construction.

13GROUND ZERO GROUND ZERO 1 - 15 July 2014 1 - 15 July 2014 12

Description Scale of Ops Sales Model OEM’s Sales to dealers Engine Types

Caterpillar National OEM, Dealer Driven 2 Built Gensets Electronically Controlled

Cummins National OEM Driven, Service is Cummins 5 Engines Mechanically Controlled

Greaves Cotton National Procures engines to make gensets, Service is Greaves 6 Fully Built Gensets Mechanically Controlled

KOEL National OEM Driven, Service is KOEL 13 Engines Mechanically Controlled

MTU National OEM, Dealer driven 5 Engines Electronically Controlled

Perkins National OEM Driven 2 Engines Electronically Controlled

Volvo Penta Regional Direct Selling None Engines Electronically Controlled

Mahindra Powerol South 20 OEM and 3000 Dealer driven Fully Built Gensets Mechanically Controlled

Company-wise scale of operation and distribution channel

Dealer/Distributors End-users3

Diesel Generator SetEngine Manufacturer

Third-party OEMs

GOEM/Own Genset

1

2

1. Engine manufacturers supplies engine to exclusive GOEM, which later integrates engines, alternators and panels and

markets them to end users through its dealer network/distributors (for e.g. Cummins India Ltd, KOEL and Caterpillar.)

2. Engine manufacturers supplies engine to third-party assemblers and OEMs, which later sells the generator sets to

end users through its service dealers/distributor network (for example Mahindra, Eicher, Excorts, Ashok Leyland, and

so on)

3. Engine manufacturers assemble generator sets at their end and sell to the end users either through dealers or direct-

ly to the end-users (for e.g., Greaves Cotton Ltd and also in limited cases suppliers such Mahindra and KOEL)

Distribution channels used for Diesel Gensets

Diesel Generator Set Market (15-2,000 kVA): Distribution Channels (India), 2014

15GROUND ZERO GROUND ZERO 1 - 15 July 2014 1 - 15 July 2014 14

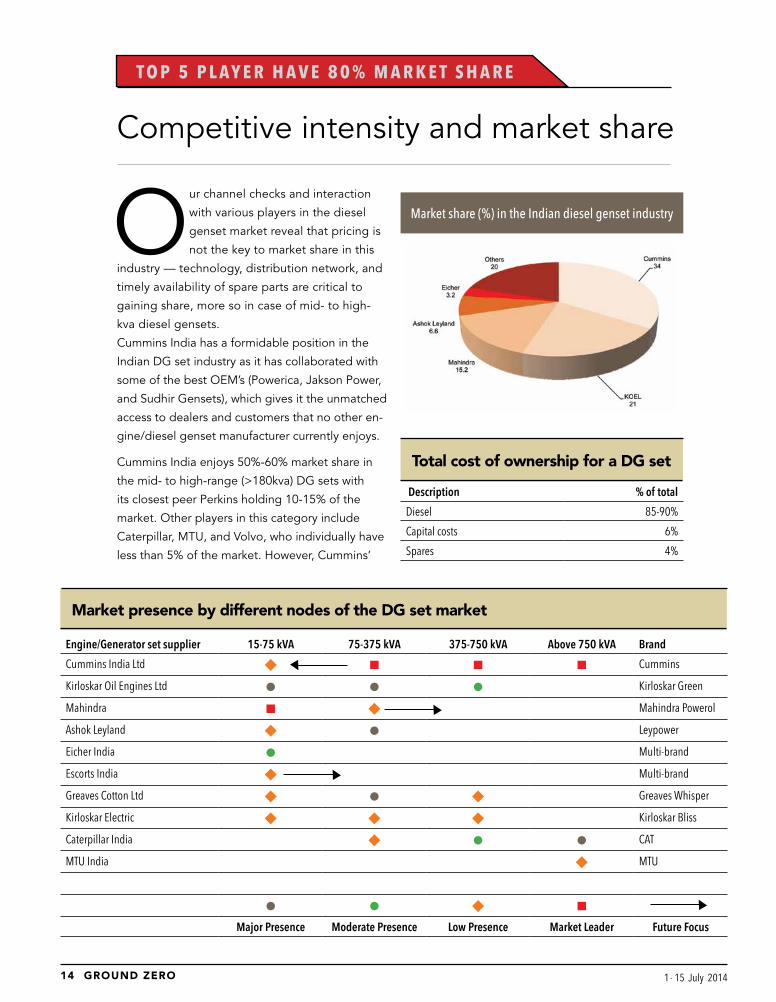

Competitive intensity and market share

T O P 5 P L A Y E R H A V E 8 0 % M A R K E T S H A R E

Our channel checks and interaction

with various players in the diesel

genset market reveal that pricing is

not the key to market share in this

industry — technology, distribution network, and

timely availability of spare parts are critical to

gaining share, more so in case of mid- to high-

kva diesel gensets.

Cummins India has a formidable position in the

Indian DG set industry as it has collaborated with

some of the best OEM’s (Powerica, Jakson Power,

and Sudhir Gensets), which gives it the unmatched

access to dealers and customers that no other en-

gine/diesel genset manufacturer currently enjoys.

Cummins India enjoys 50%-60% market share in

the mid- to high-range (>180kva) DG sets with

its closest peer Perkins holding 10-15% of the

market. Other players in this category include

Caterpillar, MTU, and Volvo, who individually have

less than 5% of the market. However, Cummins’

Market share (%) in the Indian diesel genset industry

Description % of total

Diesel 85-90%

Capital costs 6%

Spares 4%

Total cost of ownership for a DG set

Engine/Generator set supplier 15-75 kVA 75-375 kVA 375-750 kVA Above 750 kVA Brand

Cummins India Ltd u n n n Cummins

Kirloskar Oil Engines Ltd l l l Kirloskar Green

Mahindra n u Mahindra Powerol

Ashok Leyland u l Leypower

Eicher India l Multi-brand

Escorts India u Multi-brand

Greaves Cotton Ltd u l u Greaves Whisper

Kirloskar Electric u u u Kirloskar Bliss

Caterpillar India u l l CAT

MTU India u MTU

l l u nMajor Presence Moderate Presence Low Presence Market Leader Future Focus

Market presence by different nodes of the DG set market

15GROUND ZERO GROUND ZERO 1 - 15 July 2014 1 - 15 July 2014 14

dominance could come under threat with Per-

kins starting a domestic manufacturing plant for

engines in Aurangabad from December2014 —

its aim is to increase its market share to 35-40%

from the current 10-15% it enjoys in the >750kva

segments. Perkins has already started adding to its

dealer network while simultaneously increasing the

indigenized component of its DG sets to suit the

Indian operating environment.

KOEL, along with Mahindra, is amongst the

market leaders in sets below the 75kva range.

Mahindra Powerol is the market leader in the

15-75kva segment with a 40% share followed by

KOEL at 25% share. Within the 75-375kva range,

Cummins India regains its leadership with a 45%

share followed by KOEL at 28%.

In terms of reliability and pricing, Caterpillar, which

operates primarily in 750kva and 1,000kva, is con-

sidered the most reliable and is extensively used

in critical applications in O&G and defense. This

is also the reason that it commands the highest

premium over peers. Next in line are MTU and

Perkins in terms of pricing, followed by Cummins

India whose engines are still mechanical engines

(vs. electronic). KOEL, Mahindra, and Leyland

round off the list of big players in the DG industry

(see table below).

Description Presence Market Share Manufacturing Product Range Distribution & Spares

Caterpillar >20 Year 2% Hosur – Up to 750 KVA 200-3000 KVA 140 Touch points

Cummins >20 Year 34% Pune and Phaltan 7-3000 KVA 400 Touch Points

Greaves Cotton <10 Year NA Aurangabad 30-400 KVA 65 Touch Points

KOEL >15 Year 20% Pune-Up to 750kva Up to 750 KVA 338 Touch Points

MTU <10 Year <5% Imported 200-3000 KVA NA

Perkins >10 Year 10% Imported 200-2500 KVA NA

Volvo Penta >15 Year <5% Imported 200-600 KVA NA

Mahindra Powerol >10 year 15% Domestic 5-500kva 300

Diesel Genset Industry presence and market share

Brand- ranking in the Indian DG set market

l Caterpillar

l MTU / Perkins

l Cummins India

l Kirloskar Oil Engine/ Mahindra/ Leyland

Unorganised player DG set used in fields

17GROUND ZERO GROUND ZERO 1 - 15 July 2014 1 - 15 July 2014 16

Are the new CPCB norms really a game changer for the industry in terms of competition?

N E W C P C B I I N O R M S F R O M J U L Y 1 , 2 0 1 4

The Ministry of Environment and Forests

has notified that the CPCB-2 norms will

be implemented from 1st July 2014

(CPCB stands for Central Pollution

Control Board). These norms have tightened the

existing emission requirements on NOX and HC

(see table).

We are given to understand from our channel

checks that starting from 1st July 2014, engine

manufactures and OEMs will stop shipping and

selling non-compliant engines and DG sets. While

larger players such as Cummins India, KOEL,

Caterpillar/Perkins, MTU, Ashok Leyland, would be

compliant with the new norms, smaller unorgan-

ized players are going to have trouble in achieving

compliance — this should benefit larger players,

more so in the low-kva segments where the unor-

ganized sector has a larger presence. In our view,

Cummins India, which has now started focusing

on the low-kva range (up to 75kva) could be a key

beneficiary as its market share in this segment is

around 10%.

Key changes that need to be made to the ex-

isting mechanical engines would be in terms

of turbochargers, air and fuel filters, and piston

bore — this would increase the cost and price of

the engine by 10-15%. Most engine companies

would not want to convert the existing mechanical

engines to electronic (direct fuel injection) right

away, since it would entail a higher increase in

cost/price, which the market may not be willing to

bear just yet.

Power Category Emission Limits

Description NOx +HC CO PM Smoke Limit

Up to 19 KW 7.5 3.5 0.3 0.7

More than 19 KW up to 75 KW 4.7 3.5 0.3 0.7

More than 75 KW up to 800 KW 4 3.5 0.2 0.7

New emission norms for DG set

Key parts which together constitute an engine

17GROUND ZERO GROUND ZERO 1 - 15 July 2014 1 - 15 July 2014 16

Channel view on ‘pre buying’ and FY15 sales for diesel

gensets

Jakson Power: Our meetings with the top management

of Jakson Power, a Noida-based power solutions company

brought 3 things into focus:

a) Management see Q1FY15 volumes rising as much as 30-

40% QoQ (on very weak volumes in Q3FY14 and Q4FY14),

driven by pre buy and powe r shortages in the North. The

management said they will see the sharp jump not only

because of power shortages, but also pre buying, since

the new CPCB norms are coming into effect from 1st July

2014. Stronger-than-expected pre buying over the past few

months coupled with improvement in demand has led to

lower inventory in the channel (15-30 days) as well. How-

ever, management expects Q2FY15 to be sluggish as most

demand will get pulled in to Q1 because of the pre buying.

b) Management expects volumes for CY14 to be flat (at

best) with the possibility of a single-digit fall. However, they

see CY15 as a far better year, with a recovery in volumes

driven by a pickup in infrastructure and real estate (com-

mercial and residential). With the DG market moving from

continuous-use to standby-use, the need for DG sets is

expected to endure with the industry expected to revive to

a secular growth trend from CY15 onwards.

c) The CPCB-2-compliant engines will be shipped out to

the dealers over the next one month — while the man-

agement did not quantify the price increase, it said it will

continue to maintain the premium it charges over compe-

tition. While Cummins sets are already compliant with the

new norms, some of its peers may not be able to meet the

deadline.

Channel check indicate muted pre buy in South and

West India

We met with the largest distributor of Perkins (key compet-

itor for Cummins India in the >750kva engines segment).

Key takeaways are:

a) Muted prebuy in Q115; inventory now at ~1-1.5 months

in the channel. As per management, DG set volumes

had seen a muted pre buy before the implementation of

the new CPCB II norms which come into effect from 1st

July, 2014. While there had been a rise in enquiries from

customers, the same had not translated into actual sales.

This is in contrast to our recent discussions with one of the

largest OEM’s for Cummins India for North India whose

volumes were up 30% QoQ in Q115 on a strong pre buy

and high power cuts over the past 2 months. Perkins is

present primarily in the >750kva nodes while in our view,

a prebuy is more likely to be evident in the lower and mid

kva nodes which is more price sensitive and where Perkins

has a limited presence. Inventory in the channel had also

come down to a manageable 1-1.5 months from the previ-

ous +2 months seen in Q414.

b) Engines from 400kva -750kva have been certified

compliant; consolidation likely in the lower kva segment.

As per management, Perkins engines in the nodes from

400kva-750kva have been certified compliant for sale in In-

dia; engine prices could increase by 10-15% on the engine

and 6-10% for the diesel genset. These engines would be

electro mechanically controlled and in compliance with the

CPCB II norms. Our discussions with other engines manu-

facturers indicate that engine prices across manufacturers

are expected to see an increase of 10-12%.

c) Perkins plant in Aurangabad to start by Dec’, 2014; fo-

cused on growing market share in >750kva segment. The

Perkins plant for the 4000 series (>750kva) is expected to

be commissioned by Dec’, 2014 (originally to have started

in end CY13). The plant would have an initial capacity of

3,000 engines scalable to 5,000 engines in the second

phase. Note that Perkins already has a plant in China for

lower kva engines (5-200kva, 1100 series) and therefore

there are no plans to set up a lower kva plant in India in

the near future; however, Perkins could look at domestic

manufacturing of the mid range (400-600kva) over the next

few years.

d) Telangana an emerging opportunity for diesel genset

manufacturers on high power cuts. Media reports suggest

strong power cuts across Telangana and Seemandhra over

the past month with full day power cuts for industries since

last week (www.thehindu.com/news/cities/Hyderabad/

power-holidays-for-industries-from-today/article6155974.

ece). We note that the DG market in Andhra Pradesh had

been very muted over the last 1.5 years and could see a

bounce post the recent surge in power cuts. Management

has cited that there was a revival in volumes from the phar-

maceutical sector in Q115 in Andhra Pradesh.

19GROUND ZERO GROUND ZERO 1 - 15 July 2014 1 - 15 July 2014 18

What goes into making a diesel genset? The engine is the heart of the diesel genset

Diesel Engine

Accessories Foundation

Fuel Control

Excitation Control

A.C. Generator Controls Load

5Cs of an Engine: Cylinder block, Cylinder head, Crank shaft, Cam shaft and Connecting rods

Typical layout of a DG set assembly

19GROUND ZERO GROUND ZERO 1 - 15 July 2014 1 - 15 July 2014 18

Key players in the Indian Diesel Generator Set market

P R O F I L E S

Cummins India

Cummins India has an India presence for the past

52 years and has built a very strong reputation

by virtue of its strong dealer network, product

quality, and after-sales support. It supplies engines

to three OEMs — Powerica, Jakson Power, and

Partner Incorporation Areas of Operation Manufacturing

Jaksons 1947 North and North-East India Daman, Jammu

Partner P /Powerica 1984 West and South Daman, Bangalore, Dadra, and Nagar Haveli

Sudhir Gensets 1973 North and North-West India Silvassa, Jammu, Gurgaon

OEMs for Cummins DG sets in India by region

Sudhir Gensets. In turn, the OEMs assemble the

DG sets by adding on alternators, canopies, and

control panels — these are then sent to dealers

across India for sale to customers.

Cummins presence across DG sets

21GROUND ZERO GROUND ZERO 1 - 15 July 2014 1 - 15 July 2014 20

Caterpillar India

In India, Caterpillar sells 200-3,000KVA diesel generator sets,

gas-based generator sets, and also rents out 200-2,000 KVA

gensets. Caterpillar has a manufacturing facility in Hosur,

Tamil Nadu. The unit specializes in the design and manu-

facture of internal combustion engines, genset packages,

and components. The product variants in a wide-ranging

perspective are diesel engines, gas-engine long blocks, and

electric power generator sets. Product ratings range from

200 kVA to 2,000 kVA depending on the various families like

3300, 3400, C series, and 3500. There are more than 300

employees in this facility.

Caterpillar DG set used in industry Factory layout

Hosur currently has an extensive customer base across India,

China, Indonesia, Australia, Europe, and North America. The

unit assembles 200-3000kva engines, makes DG engines

of up to 750kva, and imports/assembles >750kva. It has a

machining shop for marking components that fit into the en-

gine. It produces ~400 engines a month, i.e., ~5000 engines

per annum using a single shift. It has the capacity to double

production by using two shifts.

Perkins India

Starting production in India from October, 2014 onwards.

Perkins is developing manufacturing facility in Aurangabad,

Shendra Industrial Area. The facility will manufacture its 4000

Series engines, with power outputs from 700- to 2000-kVA.

The estimated cost is around Rs 7.5bn with production ca-

pacity of 3,000 units that will be extended to 5,000 units. The

new plant will help meet growing demand for engines from

Asian markets. The 120,000 sq. mt. site (including a 40,000

sq. mt. manufacturing area), will also undertake machining,

assembly and test, paint and packaging.

Channel Partners

In India, Perkins has two distribution partners — GMMCO

Power and Powerparts Private Limited. GMMCO mainly con-

centrates in the Southern and Western states while Power-

parts Pvt Ltd takes care of the Northern and Eastern region.

Gmmco Power

Territories supported — Andaman and Nicobar Islands,

Andhra Pradesh, Chattisgarh, Dadra and Nagar Haveli, Da-

man and Diu, Goa, Gujarat, Karnataka, Kerala, Lakshadweep,

Dealer network

21GROUND ZERO GROUND ZERO 1 - 15 July 2014 1 - 15 July 2014 20

Madhya Pradesh, Maharashtra, Pondicherry, Tamil Nadu.

P owerparts Private Limited

Territories supported — Arunachal Pradesh, Assam, Bihar,

Chandigarh, Delhi, Haryana, Himachal Pradesh, Jammu

and Kashmir, Jharkhand, Manipur, Meghalaya, Mizoram,

Nagaland, Orissa, Punjab, Rajasthan, Sikkim, Tripura, Uttar

Pradesh, Uttarakhand, and West Bengal

Kirloskar Oil Engine (KOEL)

KOEL is one of the major DG set manufacturers in India,

especially in the low- to mid-end segment. It has a presence

in the power generation sector and caters to agriculture and

industrial segments. It also exports engines to the Middle

East and African markets. Kirloskar has four manufacturing

facilities — one each in Nasik, Pune, Rajkot, and Kolhapur.

Agri engines

Power Generation Industrial Engines

Large engines (mainly used in captive power plants)

23GROUND ZERO GROUND ZERO 1 - 15 July 2014 1 - 15 July 2014 22

Mahindra Powerol

Mahindra & Mahindra entered the DG business

under the brand name Mahindra Powerol. It can

produce DG sets from 5kva to 500kva. Mahindra

has a strong presence in the telecom industry

with most of the telecom companies opting for its

gensets. Powerol also has a presence with banks,

buildings, hospitals, hotels, and the manufacturing

segments.

It has OEM’s in major cities of 15 states. Mahindra

diesel gensets are manufactured at two factories

located at Pune and Delhi, with a combined manu-

facturing capacity of over 30,000 sets a year.

Ashok Leyland

It is the genset provider in engines, alternators,

and controllers. Its diesel generating sets meet

latest CPCB norms in India and are made to meet

international norms. AL’s sets are powered by

the compact 4-, 6-, 8-, and 12-cylinder series of

diesel engines. Its DG sets are silent, environ-

ment-friendly, require minimum maintenance, and

are low on operating costs.

Leypower diesel generating sets are manufac-

tured in plants located across six units in the

country. The present range extends from 10-

2,250 kVA with generating sets manufactured to

operate under arduous conditions. It has OEM’s

present across 20+ states in India.

Manufacturing facility

Ashok Leyland DG set

Mahindra Powerol DG set MS Dhoni brand Ambassador

23GROUND ZERO GROUND ZERO 1 - 15 July 2014 1 - 15 July 2014 22

Dr. Harikishan Koppula Reddy,

Dr Harikishan Koppula Reddy is the Managing Director of V R TechNiche Consultants - a leading consulting company in India in the area of travel demand estimation for road projects. It offers advisory services to various stakeholders of a BOT road project (NHAI, developers, lenders and investors) at project conceptualization and planning as well as pre-bid and post-bid stages. Its clientele includes almost all major infrastructure companies in India, along with leading financial institutions. Dr Reddy is a Ph.D. in Trans-portation Systems Engineering from IIT Kanpur, and has over 10 years of experience in the domain.

on the opportunities and challenges in the road sector

BY VIBHOR SINGHALDr Harikishan Koppula Reddy

The advent of the new government at the centre has

created an environment of optimism in the road infra-

structure industry. How do you see this translating, on

the ground, for the road sector? What policy initiatives

would you want to see from the government, in order to

energise the sector?

The new government is definitely trying to create the right

environment for the putting road infrastructure industry,

which has mostly stagnated for the last couple of years, on

the right track. However, a number of policy initiatives and

steps are required to energise as well as sustain the sector:

(i) Creating faster channels in ministries of environment and

railways for timely clearance of road projects and ROBs,

(ii) Bidding only for those projects for which land is available,

(iii) Faster approval of proposals and designs by IEs/NHAI,

(iv) Faster settlement of claims and disputes,

(v) Creating technical groups for faster approval and induc-

tion of new technologies, etc.

An important aspect, which never got any attention, but has

got to be addressed quickly, is toll avoidance by users at

toll plazas. In my opinion, the loss of revenue to developers

on account of toll avoidance at toll plazas ranges anywhere

between 5-10%, which developers never account for while

bidding for projects. Avoiding toll at a toll plaza by a user,

which is increasing by the day, should be treated at par with

avoidance of any other tax, and necessary policies to punish

such offenders should be formulated. Government should

also analyse and assess NHAI’s institutional capacity to han-

dle the amount of workload it is loaded with.

The NHAI fared quite poorly in FY13 and FY14 in terms

of targeted awards to actual achievement. What were

the main reasons?

A large number of projects which were awarded in FY13

never started. It was not NHAI but project developers and

lenders who are largely responsible for this. Developers were

too optimistic about the road sector and therefore they were

very aggressive while bidding for projects. Easier and indis-

criminate financing of road projects before FY13 (to a large

extent) was one of the primary reasons for this optimism.

Is there a chance that the new government can change

the situation and quickly revive the stalled projects?

What does it need to do to achieve that?

To come out of the current situation the government should

first prioritise its decisions. To start with, ongoing projects

with slow or no progress should be sped-up and completed

in a time-bound manner. This requires focussed efforts from

25GROUND ZERO GROUND ZERO 1 - 15 July 2014 1 - 15 July 2014 24

It would be important to learn from mistakes and create

sustainable practices and policies.

Over the last two years, developers have found it

extremely difficult to achieve financial closure for their

projects. Banks now require 100% land acquisition and

clearances, and have started questioning traffic growth

estimates of developers in their bidding. What can NHAI

do (or what is it planning to do / has already done) to ad-

dress these concerns from banks – because if banks don’t

lend, there is no point in NHAI awarding any projects.

In the initial years of PPP lenders were definitely lenient in fi-

nancing and this resulted in too much of optimism. There was

a time when financing a road project was considered a given.

While many of these decisions were based on consultants’

advice, the quality of consulting available in this country has

been very poor. To bring some rationale into the whole pro-

cess, NHAI should review the project costs at which lenders

are financing road projects and lenders should start ranking

consultants based on their previous works.

How would you describe the evolution of the various

players in the sector – in terms of technical capability and

expertise? Are we still quite inferior to the foreign play-

ers like Vinci, Balfour Beatty, and Leighton?

I do not think there are any technical capability issues on de-

velopers’ side. In fact most of the first-generation projects in

India under NHDP Phases 1 and 2 were executed by foreign

players. The space is now mostly crowded by Indian compa-

nies. It is, in fact, faster evolution and stiff competition that

led to the current situation.

Why do you think there hasn’t been much interest in the

road segment from foreign players?

I think red-tape and too much of competition are reasons for

reduced interest from foreign players. The space is already

crowded with too many Indian companies.

Who are the key players in the segment that you feel are

well placed in terms of technical capability and domain

expertise to capture the opportunity in the segment?

Technically, there are a large number of companies that are

capable of implementing road projects efficiently. While it is

quite difficult to comment, with the information that is avail-

able, and the current position, I would say Oriental Structural

Engineers, Sadbhav Engineering, L&T, IRB, and Ashoka Build-

con are doing well (by progressing on projects in hand) and

can take advantage of initiatives by the new government.

the government to obtain all pending clearances and approv-

als, immediately, for such projects. This will increase the cash

flows of the developer and also of the road sector.

To follow up with this, government should decide the fate of

stalled projects quickly, within the parameters of bid doc-

uments/contracts. The path that the government takes will

decide the future course of the road sector. Too much flexibil-

ity from the government could set a bad example and result

in an unrealistically optimistic situation again.

Over and above the stalled projects, how does the pipe-

line for fresh orders look? How can it be ensured that

these projects, if and when awarded, do not meet the

same fate as the ones before?

With expressways and new targets fixed by new government

for implementation of road projects, the future orders should

be good. To avoid FY13 and FY14 situations, it is essential

that the projects come with all approvals and clearances and

lenders need to be rational in financing projects. While lend-

ers were too lenient earlier, they are too pessimistic now.

One of landmark proposals that NHAI took to resolve

the deadlock in the sector was premium rescheduling.

Do you think it was required? Will it not create a moral

hazard with more developers throwing up their hands in

the future?

NHAI should reschedule premiums for only those projects

that are actually feasible. Some of the projects, even af-

ter premium rescheduling, may not be feasible. Premium

rescheduling without a detailed analysis will only shift the

current problems to future. Yes, indiscriminate premium

rescheduling can definitely create moral hazards and set bad

examples. While one-time premium rescheduling may solve

the current situation, continuing with it will not sustain road

sector growth.

NHAI seems to have come full circle, with bulk of the

awards in FY05-08 comprising EPC project, FY09-12

comprising BOT-Toll projects, and now NHAI is looking at

awarding more than 50% of projects on EPC basis. What

is the major reason behind this shift? Does this mean

BOT-Toll project model has been a failure in this country?

No model will be successful unless all stakeholders are ration-

al and responsible. EPC projects might also fail if the NHAI

or ministry does not provide all approvals and clearances in

time or if bidders quote low EPC prices. While the BOT-Toll

model has definitely seen many problems, it has also provid-

ed many opportunities for faster growth of the road sector.

25GROUND ZERO GROUND ZERO 1 - 15 July 2014 1 - 15 July 2014 24

Indian Economy – Trend Indicators

Monthly Economic Indicators

Quarterly Economic Indicators

Growth Rates (%) Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13 Jan-14 Feb-14 Mar-14 Apr-14 May-14

IIP 1.5 (2.5) (1.8) 2.6 0.4 2.7 (1.6) (1.3) 0.1 0.8 (1.8) (0.5) 3.4 3.7

PMI 51.0 50.1 50.3 50.1 48.5 49.6 49.6 51.3 50.7 51.4 52.5 51.3 51.3 51.4

Core sector 2.3 2.3 0.1 3.1 3.7 8.0 (0.6) 1.7 2.1 1.6 4.5 2.5 4.2 2.3

WPI 4.8 4.6 5.2 5.9 7.0 7.0 7.2 7.5 6.4 5.2 5.0 5.7 5.2 6.0

CPI 9.4 9.3 9.9 9.6 9.5 9.8 10.2 11.2 9.9 8.8 8.0 8.3 8.6 8.3

Money Supply 12.4 12.1 12.8 12.5 12.2 12.5 13.0 14.5 14.9 14.5 14.5 14.2 13.9 13.2

Deposit 13.4 13.5 13.8 13.5 13.1 14.1 14.4 16.1 15.8 15.7 15.9 14.6 15.1 13.8

Credit 14.6 14.2 13.7 14.9 17.1 17.8 16.6 15.5 14.5 14.7 14.4 14.3 14.1 12.8

Exports 1.7 (1.1) (4.6) 11.6 13.0 11.2 13.5 5.9 3.5 3.8 (3.7) (3.2) 5.3 12.4

Imports 11.0 7.0 (0.4) (6.2) (0.7) (18.1) (14.5) (16.4) (15.2) (18.1) (17.1) (2.1) (15.0) (11.4)

Trade deficit (USD Bn) (17.8) (20.1) (12.2) (12.3) (10.9) (6.8) (10.6) (9.2) (10.1) (9.9) (8.1) (10.5) (10.1) (11.2)

Net FDI (USD Bn) 2.8 1.9 1.8 1.7 1.7 3.3 1.8 2.4 1.9 0.4 (0.1) 2.9 2.2

FII (USD Bn) 1.6 6.7 (8.7) (4.7) (2.0) 0.2 (0.4) (0.0) 2.9 2.6 1.5 5.4 (0.1)

ECB (USD Bn) 1.1 2.5 2.0 3.7 2.3 3.3 1.9 2.2 4.6 1.8 4.3 3.6 3.2

NRI Deposits (USD Bn) 1.3 1.7 2.5 1.3 1.2 5.9 4.5 14.6 2.0 0.7 0.7 2.5 1.4

Dollar-Rupee 54.4 55.1 58.4 60.6 63.0 63.8 61.6 62.6 61.9 62.1 62.2 61.0 60.4 59.3

FOREX Reserves (USD Bn) 296.4 287.9 284.6 280.2 275.5 276.3 283.0 291.3 295.7 292.2 294.4 303.7 309.9 312.7

Balance of Payment (USD Bn) Q4FY12 Q1FY13 Q2FY13 Q3FY13 Q4FY13 Q1FY14 Q2FY14 Q3FY14 Q4FY14Exports 80.2 75.0 72.6 74.2 84.8 73.9 81.2 79.8 83.7 Imports 131.7 118.9 120.4 132.6 130.4 124.4 114.5 112.9 114.3 Trade deficit (51.5) (43.8) (47.8) (58.4) (45.6) (50.5) (33.3) (33.2) (30.7)Net Invisibles 29.8 26.8 26.7 26.6 27.5 28.7 28.1 29.1 29.3 CAD (21.8) (17.1) (21.1) (31.8) (18.2) (21.8) (5.2) (4.1) (1.3)CAD (% of GDP) 4.4 4.0 5.1 6.5 3.6 4.9 1.2 0.8 0.3 Capital Account 16.6 16.5 20.7 31.5 20.5 20.6 (4.8) 23.8 9.2 BoP (5.7) 0.5 (0.2) 0.8 2.7 (0.3) (10.4) 19.1 7.1

GDP and its Components (YoY, %) Q4FY12 Q1FY13 Q2FY13 Q3FY13 Q4FY13 Q1FY14 Q2FY14 Q3FY14 Q4FY14Agriculture & allied activities 3.9 1.8 1.8 0.8 1.6 4.0 5.0 3.7 6.3 Industry 7.4 (0.6) 0.1 2.0 2.0 (0.9) 1.8 (0.9) (0.5)Mining & Quarrying 6.5 (1.1) (0.1) (2.0) (4.8) (3.9) - (1.2) (0.4)Manufacturing 7.5 (1.1) (0.0) 2.5 3.0 (1.2) 1.3 (1.5) (1.4)Electricity, Gas & Water Supply 7.6 4.2 1.3 2.6 0.9 3.8 7.8 5.0 7.2 Services 6.5 6.7 6.5 6.1 5.8 6.5 6.1 6.4 5.8 Construction 7.6 2.8 (1.9) 1.0 2.4 1.1 4.4 0.6 0.7 Trade, Hotel, Transport and Communications 4.0 4.0 5.6 5.9 4.8 1.6 3.6 2.9 3.9 Finance, Insurance, Real Estate & Business Services 10.9 11.7 10.6 10.2 11.2 12.9 12.1 14.1 12.4 Community, Social & Personal Services 5.5 7.6 7.4 4.0 2.8 10.6 3.6 5.7 3.3 GDP at FC 6.3 4.5 4.6 4.4 4.4 4.7 5.2 4.6 4.6

27GROUND ZERO GROUND ZERO 1 - 15 July 2014 1 - 15 July 2014 26

Annual Economic Indicators and Forecasts Indicators Units FY6 FY7 FY8 FY9 FY10 FY11 FY12 FY13 FY14E FY15E

Real GDP growth % 9.5 9.6 9.3 6.7 8.6 8.9 6.7 4.5 4.6 5.2

Agriculture % 5.1 4.2 5.8 0.1 0.8 8.6 5.0 1.4 4.0 2.4

Industry % 8.5 12.9 9.2 4.1 10.2 8.3 6.7 0.9 0.0 2.9

Services % 11.1 10.1 10.3 9.4 10.0 9.2 7.1 6.2 6.0 6.6

Real GDP Rs Bn 32531 35644 38966 41587 45161 49185 52475 54821 57486 60475

Real GDP US$ Bn 733 787 967 908 953 1079 1096 1008 951 1008

Nominal GDP Rs Bn 36925 42937 49864 56301 64778 77841 90097 101133 113205 126723

Nominal GDP US$ Bn 832 948 1237 1229 1367 1707 1881 1859 1872 2112

Population Mn 1106 1122 1138 1154 1170 1186 1202 1219 1236 1254

Per Capita Income US$ 753 845 1087 1065 1168 1439 1565 1525 1515 1685

WPI (Average) % 4.5 6.6 4.7 8.1 3.8 9.6 8.7 7.4 6.0 5-5.5

CPI (Average) % 4.2 6.8 6.4 9.0 12.4 10.4 8.3 10.2 9.5 7.5-8

Money Supply % 15.5 20.0 22.1 20.5 19.2 16.2 15.8 13.6 13.5 14.0

CRR % 5.0 6.0 7.5 5.0 5.75 6.00 4.75 4.00 4.0 4.0

Repo rate % 6.5 7.50 7.75 5.0 5.00 6.75 8.50 7.50 8.00 8.00

Reverse repo rate % 5.5 6.0 6.0 3.5 3.50 5.75 7.50 6.50 7.00 7.0

Bank Deposit growth % 24.0 23.8 22.4 19.9 17.2 15.9 13.5 14.4 14.6 15.0

Bank Credit growth % 37.0 28.1 22.3 17.5 16.9 21.5 17.0 15.0 14.3 16.0

Centre Fiscal Deficit Rs Bn 1464 1426 1437 3370 4140 3736 5160 5209 5126 5558

Centre Fiscal Deficit % of GDP 4.0 3.3 2.9 6.0 6.4 4.8 5.7 5.2 4.5 4.4

Gross Central Govt Borrowings Rs Bn 1310 1460 1681 2730 4510 4370 5098 5580 5639 6390

Net Central Govt Borrowings Rs Bn 954 1104 1318 2336 3984 3254 4362 4674 4233 4870

State Fiscal Deficit % of GDP 2.4 1.8 1.5 2.4 2.9 2.1 2.3 2.2 2.5 2.5

Consolidted Fiscal Deficit % of GDP 6.4 5.1 4.4 8.4 9.3 6.9 8.1 7.4 7.0 6.9

Exports US$ Bn 105.2 128.9 166.2 189.0 182.4 251.1 309.8 306.6 318.6 328.2

YoY Growth % 23.4 22.6 28.9 13.7 -3.5 37.6 23.4 -1.0 3.9 3.0

Imports US$ Bn 157.1 190.7 257.6 308.5 300.6 381.1 499.5 502.2 466.2 500.2

YoY Growth % 32.1 21.4 35.1 19.7 -2.5 26.7 31.1 0.5 -7.2 7.3

Trade Balance US$ Bn -51.9 -61.8 -91.5 -119.5 -118.2 -129.9 -189.8 -195.6 -147.6 -172.0

Net Invisibles US$ Bn 42.0 52.2 75.7 91.6 80.0 84.6 111.604 107.5 115.2 118.1

Current Account Deficit US$ Bn -9.9 -9.6 -15.7 -27.9 -38.2 -45.3 -78.2 -88.2 -32.4 -54.0

CAD (% of GDP) % -1.2 -1.0 -1.3 -2.3 -2.8 -2.6 -4.2 -4.7 -1.7 -2.6

Capital Account Balance US$ Bn 25.5 45.2 106.6 7.8 51.6 62.0 67.8 89.3 48.8 63.5

Dollar-Rupee (Average) 44.4 45.3 40.3 45.8 47.4 45.6 47.9 54.4 60.5 60.0

Source: RBI, CSO, CGA, Ministry of Agriculture, Ministry of commerce, Bloomberg, PhillipCapital India Research

27GROUND ZERO GROUND ZERO 1 - 15 July 2014 1 - 15 July 2014 26

Note

: For

ban

ks, E

BITD

A is

pre-

prov

ision

pro

fit

Phill

ipC

apita

l Ind

ia C

over

age

Uni

vers

e: V

alua

tio

n Su

mm

ary

CMP

Mkt

Cap

Ne

t Sal

es (R

s mn)

EB

IDTA

(Rs

mn)

PAT (

Rs m

n)EP

S (R

s)

EPS

Grow

th (%

) P

/E (x

) P

/B (x

) EV

/EBI

TDA

(x)

ROE

(%)

ROCE

(%)

Nam

e of

com

pany

Sect

orRs

Rs m

nFY

14E

FY15

EFY

14E

FY15

EFY

14E

FY15

EFY

14E

FY15

EFY

14E

FY15

EFY

14E

FY15

EFY

14E

FY15

EFY

14E

FY15

EFY

14E

FY15

EFY

14E

FY15

E

Cham

bal F

ertil

iser

sAg

ri In

puts

58 2

4,22

1 8

6,90

3 8

7,44

1 6

,120

7

,829

2

,595

3

,260

6.

27.

814

.525

.69.

37.

41.

21.

19.

87.

113

.215

.24.

76.

0

Coro

man

del F

ert

Agri

Inpu

ts26

3 7

5,12

5 1

00,5

32

109

,906

7

,759

9

,899

3

,710

5

,526

13

.019

.5-1

5.1

50.3

20.3

13.5

3.3

2.7

11.3

10.2

16.3

20.0

14.9

19.4

Tata

Che

mica

ls Lt

dAg

ri In

puts

342

87,

127

157

,353

1

53,4

38

18,

094

20,

253

3,8

82

6,0

14

15.2

23.6

-55.

354

.922

.414

.51.

61.

98.

67.

57.

013

.314

.37.

0

Deep

ak Fe

rtilis

ers

Agri

Inpu

ts14

8 1

3,06

3 3

9,20

4 3

2,74

4 5

,636

4

,882

2

,519

2

,309

28

.626

.295

.1-8

.35.

25.

70.

90.

83.

63.

818

.415

.013

.110

.9

Kave

ri Se

eds

Agri

Inpu

ts76

1 5

2,42

0 1

0,11

2 1

2,13

8 2

,213

2

,858

2

,092

2

,681

30

.439

.164

.528

.625

.019

.410

.27.

223

.718

.040

.636

.846

.542

.0

PI In

dust

ries

Agri

Inpu

ts33

3 4

5,32

4 1

5,95

5 1

9,19

4 2

,892

3

,532

1

,884

2

,398

13

.817

.692

.627

.324

.118

.96.

55.

015

.913

.227

.126

.726

.627

.7

Ralli

s Ind

iaAg

ri In

puts

226

43,

960

17,

466

19,

423

2,6

13

3,1

40

1,5

19

1,8

13

7.8

9.3

23.2

19.3

29.0

24.3

6.1

5.2

17.0

14.1

21.2

21.5

20.0

20.5

Unite

d Ph

osph

orus

Agri

Inpu

ts34

1 1

46,1

54

105

,800

1

21,1

45

20,

196

20,

464

10,

145

11,

775

23.7

27.5

29.4

16.1

14.4

12.4

2.8

2.3

8.1

8.0

19.7

19.7

13.1

14.1

Baja

j Aut

oAu

tom

obile

s23

31 6

74,4

57

197

,176

2

14,5

78

41,

057

42,

124

32,

419

34,

242

112.

011

8.3

4.7

5.6

20.8

19.7

7.4

6.2

16.3

15.9

35.4

31.4

35.3

31.7

Bhar

at Fo

rge

Auto

mob

iles

663

154

,378

6

6,43

5 6

7,20

0 1

0,27

1 1

1,46

1 4

,179

5

,444

17

.923

.483

.430

.337

.028

.45.

95.

216

.714

.616

.118

.310

.813

.0

Hero

Mot

oCor

pAu

tom

obile

s26

40 5

27,1

65

251

,249

2

81,9

65

35,

401

40,

708

21,

091

27,

471

105.

613

7.6

-0.4

30.2

25.0

19.2

9.4

7.9

14.8

12.9

37.7

41.0

38.4

43.3

Asho

k Le

ylan

dAu

tom

obile

s37

98,

312

95,

404

107

,936

1

,664

6

,582

(4

,764

) (4

17)

-1.8

-0.2

-431

.2-9

1.2

-20.

6-2

35.8

2.2

2.2

87.1

21.7

-10.

6-0

.9-1

.92.

2

M&M

Auto

mob

iles

1186

730

,140

3

95,9

34

433

,653

4

7,68

0 5

2,26

4 3

6,48

7 3

7,60

9 59

.461

.38.

73.

119

.919

.44.

13.

615

.714

.320

.818

.316

.316

.3

Mar

uti S

uzuk

iAu

tom

obile

s25

17 7

60,3

35

426

,448

4

54,2

13

50,

900

59,

501

27,

831

33,

411

92.1

110.

616

.320

.127

.322

.83.

73.

214

.712

.413

.414

.113

.113

.9

Apol

lo Ty

res

Auto

mob

iles

202

101

,813

1

33,1

27

137

,896

1

7,76

2 1

8,56

1 9

,526

9

,973

18

.919

.864

.84.

710

.710

.22.

31.

96.

86.

124

.520

.616

.715

.9

Tata

Mot

ors

Auto

mob

iles

440

1,3

29,6

69

2,3

06,7

71

2,7

42,0

17

374

,029

4

33,7

13

139

,910

1

80,5

77

43.9

56.6

41.4

29.1

10.0

7.8

2.6

2.0

4.1

3.6

26.1

25.3

16.7

16.2

ABB

Indi

aCa

p Go

ods

1137

240

,908

7

6,31

6 7

8,46

0 4

,036

5

,402

1

,899

3

,228

9.

015

.2-2

8.0

70.0

126.

974

.69.

08.

460

.545

.27.

111

.27.

610

.4

BGR

Ener

gyCa

p Go

ods

214

15,

439

35,

204

40,

640

4,2

81

4,8

20

1,3

29

1,6

22

18.4

22.5

-18.

022

.111

.69.

51.

21.

18.

08.

410

.211

.65.

95.

9

BHEL

Cap

Good

s25

4 6

22,0

58

383

,888

3

41,5

74

47,

064

40,

737

36,

534

31,

809

14.9

13.0

-44.

8-1

2.9

17.0

19.6

1.9

1.8

11.3

11.1

11.1

9.0

8.6

7.0

Alst

om T&

DCa

p Go

ods

346

88,

669

35,

171

41,

100

3,1

02

4,2

35

1,1

42

1,9

27

4.5

7.5

-9.0

68.8

77.7

46.0

7.1

6.4

29.8

21.7

9.1

13.9

10.9

13.3

Crom

pton

Gre

aves

Cap

Good

s20

3 1

27,2

29

134

,806

1

45,3

93

6,8

20

9,3

59

2,4

43

5,1

72

3.9

8.3

195.

711

1.7

52.1

24.6

3.5

3.2

20.7

14.9

6.7

13.0

4.9

8.8

Engi

neer

s Ind

iaCa

p Go

ods

324

109

,218

1

8,23

6 1

7,65

3 3

,766

3

,672

4

,789

4

,670

14

.213

.9-2

3.8

-2.5

22.8

23.4

4.4

4.1

24.3

24.5

19.5

17.3

20.4

18.1

Jyot

i Stru

ctur

esCa

p Go

ods

63 5

,143

3

0,70

3 3

0,85

5 2

,964

2

,947

7

22

641

8.

87.

811

.3-1

1.4

7.1

8.0

0.6

0.6

4.5

4.5

8.9

7.4

10.9

10.9

KEC

Inte

rnat

iona

lCa

p Go

ods

129

33,

190

79,

018

85,

597

4,9

33

6,7

96

849

2

,335

3.

39.

130

.317

5.0

39.1

14.2

2.8

2.4

10.7

7.4

7.1

17.0

7.8

11.0

Lars

en &

Toub

roCa

p Go

ods

1715

1,5

90,5

60

565

,990

6

33,6

86

66,

671

74,

923

49,

047

53,

333

52.9

57.3

18.7

8.2

32.4

29.9

4.7

4.2

24.7

21.8

14.6

14.2

12.6

12.0

Siem

ens

Cap

Good

s95

4 3

39,5

60

111

,452

1

12,3

00

4,8

31

6,7

18

4,3

13

4,4

78

12.1

12.6

-18.

83.

878

.775

.88.

48.

069

.049

.510

.710

.57.

88.

1

Cum

min

s Ind

iaCa

p Go

ods

653

181

,012

3

8,99

1 4

3,58

1 6

,192

7

,297

6

,000

6

,365

21

.623

.0-9

.56.

130

.228

.47.

16.

329

.124

.523

.422

.320

.219

.8

Ther

max

Cap

Good

s94

9 1

13,0

79

51,

000

59,

488

4,1

23

5,3

61

2,8

10

3,5

30

23.6

29.6

-12.

225

.640

.232

.05.

64.

927

.220

.613

.815

.411

.713

.9

VA Te

ch W

abag

Cap

Good

s13

73 3

6,66

7 2

2,30

1 2

8,00

0 1

,800

3

,453

1

,083

2

,438

40

.891

.819

.912

5.1

33.7

15.0

4.3

3.8

18.7

9.9

12.9

25.5

11.7

21.3

Volta

sCa

p Go

ods

221

73,

208

52,

660

54,

241

2,6

56

3,5

46

2,2

43

2,6

06

6.8

7.9

15.0

16.2

32.6

28.1

4.0

3.7

27.5

20.1

12.3

13.0

11.9

13.0

ACC

Cem

ent

1470

275

,986

1

09,0

84

124

,747

1

3,69

0 1

9,90

1 1

0,94

7 1

1,87

6 58

.263

.2-2

1.5

8.5

25.2

23.3

3.5

3.3

18.3

13.6

14.0

14.3

11.7

11.4

Ambu

ja C

emen

tCe

men

t22

3 3

45,4

20

91,

180

231

,471

1

5,68

9 4

3,73

9 1

2,53

8 2

1,58

7 8.

110

.9-2

0.6

34.3

27.5

20.5

3.6

2.4

19.5

7.5

13.3

11.5

11.8

15.7

Indi

a Ce

men

tCe

men

t12

1 3

7,01

5 5

0,84

8 5

7,30

2 5

,914

7

,517

(6

46)

754

-2

.12.

5-1

31.0

-216

.7-5

7.3

49.1

1.0

1.0

11.5

8.6

-1.7

2.0

2.3

4.0

Man

gala

m C

emen

tCe

men

t22

0 5

,859

6

,997

1

0,68

9 5

82

1,4

96

418

6

51

15.7

24.4

-46.

055

.714

.09.

01.

21.

116

.86.

78.

211

.75.

08.

3

Shre

e Ce

men

tCe

men

t72

50 2

52,5

79

61,

817

73,

661

14,

288

19,

555

7,1

02

10,

178

203.

929

2.1

-29.

343

.335

.624

.85.

64.

617

.212

.515

.818

.714

.817

.8

Ultra

tech

Cem

ent

Cem

ent

2632

722

,082

2

14,4

37

268

,219

3

8,26

4 5

6,54

5 2

2,06

0 3

3,94

3 80

.412

3.8

-17.

653

.932

.721

.34.

23.

619

.513

.212

.816

.99.

013

.1

29GROUND ZERO GROUND ZERO 1 - 15 July 2014 1 - 15 July 2014 28

CMP

Mkt

Cap

Ne

t Sal

es (R

s mn)

EB

IDTA

(Rs

mn)

PAT (

Rs m

n)EP

S (R

s)

EPS

Grow

th (%

) P

/E (x

) P

/B (x

) EV

/EBI

TDA

(x)

ROE

(%)

ROCE

(%)

Nam

e of

com

pany

Sect

orRs

Rs m

nFY

14E

FY15

EFY

14E

FY15

EFY

14E

FY15

EFY

14E

FY15

EFY

14E

FY15

EFY

14E

FY15

EFY

14E

FY15

EFY

14E

FY15

EFY

14E

FY15

EFY

14E

FY15

E

OCL I

ndia

Cem

ent

312

17,

750

19,

366

22,

057

2,9

92

3,5

36

1,0

75

1,3

59

18.9

23.9

-32.

626

.416

.513

.11.

51.

47.

56.

09.

410

.98.

89.

2

JK La

kshm

i Cem

ent

Cem

ent

216

25,

358

20,

566

22,

994

3,0

18

4,3

18

1,1

23

2,0

91

9.5

17.8

-41.

386

.222

.612

.11.

91.

711

.78.

88.

614

.46.

19.

6

Heid

elbe

rgCe

men

tCe

men

t65

14,

775

13,

648

17,

256

864

2

,598

(4

07)

591

-1

.82.

6-2

32.1

-245

.0-3

6.3

25.0

1.8

1.7

30.8

10.0

-4.9

6.6

1.3

5.4

JK C

emen

tCe

men

t39

0 2

7,28

9 2

8,17

8 3

8,39

4 3

,449

4

,737

7

58

1,3

63

10.8

19.5

-67.

179

.736

.020

.01.

61.

514

.99.

74.

37.

44.

36.

2

Dalm

ia B

hara

t Ltd

Cem

ent

462

37,

509

28,

670

37,

139

3,2

63

6,0

95

(84)

521

-1

.06.

4-1

04.3

-718

.8-4

45.5

72.0

1.2

1.2

22.2

13.4

-0.3

1.7

2.4

4.4

Andh

ra B

ank

Finan

cials

102

60,

141

37,

373

43,

330

37,

373

43,

330

4,3

56

8,4

59

7.4

14.3

-67.

994

.213

.87.

10.

70.

7NM

NM5.

19.

40.

30.

5

Bank

of B

arod

a Fin

ancia

ls87

9 3

77,6

06

119

,654

1

42,2

89

119

,654

1

42,2

89

46,

033

55,

990

106.

913

0.0

-0.9

21.6

8.2

6.8

1.1

1.0

NMNM

14.0

15.1

0.8

0.8

Bank

of I

ndia

Fin

ancia

ls30

6 1

96,5

32

106

,289

1

28,6

52

106

,289

1

28,6

52

30,

691

37,

211

47.7

57.9

3.6

21.2

6.4

5.3

0.8

0.7

NMNM

12.6

13.6

0.6

0.6

Cana

ra B

ank

Finan

cials

463

213

,471

8

9,44

4 1

08,9

73

89,

444

108

,973

2

4,38

2 3

8,12

5 52

.982

.7-1

8.5

56.4

8.8

5.6

0.9

0.8

NMNM

10.0

14.4

0.5

0.7

Corp

orat

ion

bank

Finan

cials

393

65,

810

38,

502

43,

359

38,

502

43,

359

7,2

90

12,

466

43.5

74.4

-53.

671

.09.

05.

30.

70.

6NM

NM7.

411

.90.

40.

5

HDFC

Ban

kFin

ancia

ls81

8 1

,969

,496

1

84,2

34

222

,367

1

84,2

34

222

,367

8

5,36

4 1

01,9

08

35.9

42.8

26.9

19.4

22.8

19.1

4.5

3.8

NMNM

21.6

21.8

2.0

2.0

ICIC

I Ban

kFin

ancia

ls14

34 1

,657

,721

1

64,7

56

186

,898

1

64,7

56

186

,898

9

8,10

6 1

09,3

57

84.9

94.5

17.7

11.2

16.9

15.2

2.3

2.1

NMNM

14.0

14.3

1.7

1.7

IOB

Finan

cials

81 1

00,0

63

55,

768

64,

783

55,

768

64,

783

6,0

17

6,9

07

5.1

4.9

-16.

5-4

.115

.816

.50.

70.

7NM

NM4.

64.

60.

20.

2

Orie

ntal

Ban

k Fin

ancia

ls32

5 9

7,39

1 5

1,27

1 5

7,71

1 5

1,27

1 5

7,71

1 1

1,39

4 1

4,52

7 38

.048

.4-1

6.5

27.5

8.5

6.7

0.8

0.7

NMNM

9.2

10.9

0.5

0.6

PNB

Finan

cials

996

360

,531

1

61,4

60

179

,825

1

61,4

60

179

,825

3

3,42

6 4

4,72

0 92

.312

3.5

-31.

333

.810

.88.

11.

01.

0NM

NM10

.212

.40.

60.

8

SBI

Finan

cials

2698

2,0

14,3

29

673

,371

7

93,5

49

673

,371

7

93,5

49

136

,339

1

60,7

17

182.

621

5.3

-30.

317

.914

.812

.51.

31.

2NM

NM9.

710

.20.

60.

6

Unio

n Ba

nk

Finan

cials

240

151

,116

7

8,79

4 9

3,14

2 7

8,79

4 9

3,14

2 1

6,96

1 2

1,10

8 26

.933

.5-2

5.6

24.5

8.9

7.2

0.9

0.8

NMNM

10.4

11.9

0.5

0.6

HDFC

Ltd

Finan

cials

985

1,5

43,5

92

70,

030

81,

419

75,

402

87,

013

54,

402

62,

753

34.9

40.2

11.2

15.4

28.3

24.5

5.7

5.0

NMNM

20.5

21.1

2.7

2.7

Indi

an B

ank

Finan

cials

185

85,

997

44,

320

52,

207

44,

320

52,

207

11,

246

13,

504

24.2

31.4

-34.

229

.87.

65.

90.

70.

6NM

NM10

.211

.20.

60.

7

Dev.

Cred

it Ba

nkFin

ancia

ls82

20,

489

3,6

84

4,3

10

3,6

84

4,3

10

1,5

05

1,7

30

6.0

6.9

47.3

15.0

13.6

11.8

1.9

1.6

NMNM

14.7

14.6

1.2

1.2

AXIS

Ban

kFin

ancia

ls19

28 9

08,5

78

119

,516

1

34,9

17

119

,516

1

34,9

17

62,

174

72,

053

132.

315

2.6

19.6

15.3

14.6

12.6

2.4

2.0

NMNM

17.4

17.4

1.7

1.7

Indu

sind

Ban

kFin

ancia

ls57

1 3

00,4

33

28,

907

34,

208

28,

907

34,

208

14,

114

17,

258

26.9

32.8

32.3

22.3

21.3

17.4

3.5

3.0

NMNM

17.6

18.4

1.8

1.8

Shrir

am Tr

ansp

ort

FFin

ancia

ls90

5 2

05,2

27

36,

479

40,

567

28,

574

31,

615

12,

642

14,

377

55.7

63.4

-7.1

13.8

16.2

14.3

2.5

2.3

NMNM

16.3

16.7

2.7

2.7

LIC

Hous

ing

Fina

nce

Finan

cials

326

164

,495

1

8,64

5 2

2,15

8 1

8,25

9 2

1,50

4 1

2,92

7 1

5,40

6 25

.630

.526

.319

.212

.710

.72.

21.

9NM

NM18

.418

.81.

51.

5

Hind

usta

n Un

ileve

rFM

CG61

8 1

,336

,368

2

74,0

83

301

,232

5

0,96

3 5

5,86

0 3

6,98

3 3

8,70

3 17

.117

.910

.54.

736

.134

.540

.828

.125

.823

.411

2.9

81.3

125.

196

.9

Mar

ico In

dust

ries

FMCG

249

160

,831

4

6,76

2 5

5,66

8 7

,480

8

,773

4

,784

5

,420

7.

48.

431

.313

.333

.629

.711

.910

.221

.918

.535

.334