Pension reform: Issues for the future - KWSP

27

Pension reform: Issues for the future Edward Whitehouse Head of Pension Policy Analysis OECD Dynamic Evolution of the Pensions World, Kuala Lumpur, April 2012

Transcript of Pension reform: Issues for the future - KWSP

Pension reform:

Issues for the

future

Edward Whitehouse

Head of Pension Policy Analysis

OECD

Dynamic Evolution of the Pensions World,

Kuala Lumpur, April 2012

Key policy issues

• Coverage

• Early withdrawals

• Annuitisation

• Indexation• Indexation

• Financial sustainability

Coverage

1

Coverage

Coverage

BRNESP

SGP

CHENORCZE

PRT

GRC

ITA

JPN

Active members of pension system, per cent of labour force

75

100BLR

BGRHKG

MDA EGY

UKRBIH

KAZ

BRACHL

RUS

500 1000 2500 5000 10000 25000 50000

SGP

Gross national income per head, USD, 2009, log scale

0

25

50 MYS

IND

TUN

ARG

MEX

PAK

IDN

CHN

MNG

PHLLKA

VNMTHA

MDA EGY BRA TUR

KGZ

LBNVEN

Closing the coverage gap

• Will economic growth and development deal with

the problem?

• Most policies designed to expand coverage have

not succeeded

• Voluntary, matched defined-contribution schemes• Voluntary, matched defined-contribution schemes

• Social pensions

Social pensions

• Currently, play only a small role in Asia/Pacific:

– about 1% of older people in Singapore, 5% in Hong

Kong and maximum of 10-15% in India

Safety-net benefits: recipiency

Spain

Italy

France

Finland

Sweden

Denmark

Portugal

Australia

Greece

0 10 20 30 40 50 60 70 80

Germany

Japan

Hungary

United States

Switzerland

Poland

United Kingdom

Ireland

OECD

Canada

Spain

Safety-net benefits

Contributory minimum

Social pensions

• Currently, play only a small role in Asia/Pacific:

– about 1% of older people in Singapore, 5% in Hong

Kong and maximum of 10-15% in India

• Policy issues with social pensions

– What level?– What level?

– From which age?

– Targeted or not?

Social pension design

• Advantages

• universal benefit is simple

to understand, cheap to

administer and covers all

• incentives to work and

contribute to income-

Retirementincome

contribute to income-

replacement pension

• Disadvantages

• potentially costly,

threatening long-term

financial sustainability

Income-replacement pension

Universal pension(Non-contributory)

Earnings when working

Social pension design

• Advantages

• targeting cuts costs

compared with universal

benefit

• Disadvantages

Retirementincome

10

• Disadvantages

• reduced (but still positive)

incentives to work and

contribute for low earners

• means-testing can be

expensive to administer

correctlyUniversal pension(Non-contributory)

Targeted benefit

Earnings when working

Income-replacement pension

Pension systems in Asia/Pacific

2

Pension systems in Asia/Pacific

Mandatory income-replacement plans

Source: OECD (2012), Pensions at a Glance: Asia/Pacific

Gross pension replacement rates

Source: OECD (2012), Pensions at a Glance: Asia/Pacificper cent of individual earnings

Withdrawals

• ‘Pension’ = periodic payment to most people

• Many Asian countries do not provide ‘pensions’

– purely lump sums (Malaysia, Sri Lanka)

– spread over five years (Indonesia)

– lump-sum option (Hong Kong)– lump-sum option (Hong Kong)

– BUT Singapore moving to mandatory annuities

• Annuities improve welfare: longevity insurance

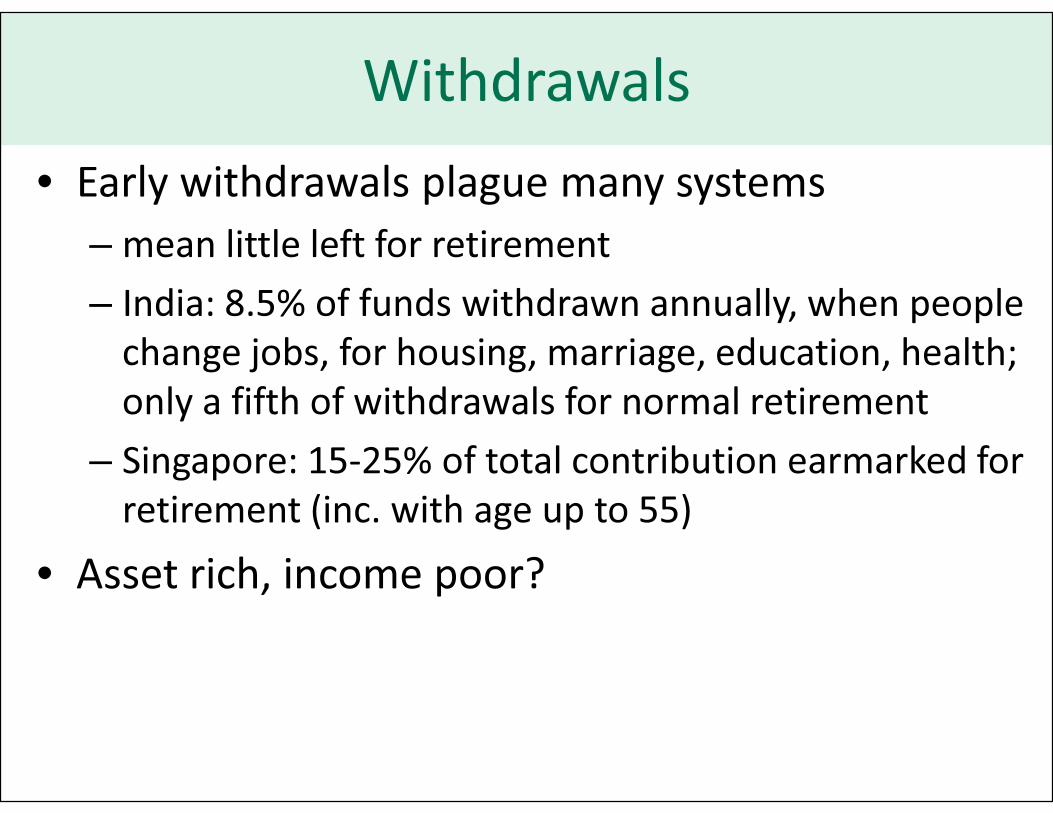

Withdrawals

• Early withdrawals plague many systems

– mean little left for retirement

– India: 8.5% of funds withdrawn annually, when people

change jobs, for housing, marriage, education, health;

only a fifth of withdrawals for normal retirementonly a fifth of withdrawals for normal retirement

– Singapore: 15-25% of total contribution earmarked for

retirement (inc. with age up to 55)

• Asset rich, income poor?

Modernising defined-benefit plans

• Earnings measures:

– final-salary schemes are distortionary, costly and

unnecessary to protect real pension values

– all OECD countries with public/mandatory private

defined-benefit schemes use lifetime average salarydefined-benefit schemes use lifetime average salary

– in Asia/Pacific, only Viet Nam, but not India, Pakistan,

Philippines, Thailand

• Indexation:

– adjustment of pensions needed to preserve adequacy

– China, Philippines and Viet Nam automatically increase

benefits, but not India, Pakistan, Thailand

Financial sustainability

3

Financial sustainability

Public pension spending

EU-27

Sweden

Germany

Greece

France

Italy

Poland

0 5 10 15 20 25

Australia

Ireland

United States

Canada

Netherlands

United Kingdom

OECD-28

Spain

EU-27

Level in 2007

Projected

change,

2007-60

Public expenditure on old-age and survivors’ benefits, per cent of GDPNote: 2050 for Australia

Demographic (in)determinism

15

20

25 Public expenditure on

pensions, per cent of GDP

2010

R2=0.586France

Italy

0 10 20 30 40 50 60 70

0

5

10

Dependency ratio: percentage of adult population aged 65+

Turkey

Mexico

Korea

Austria

France

Sweden

Germany

United Kingdom,

Estonia, Switzerland

Ireland

Poland

Canada, New Zealand,

United States, Australia

Netherlands

Demographic (in)determinism

15

20

25 Public expenditure on

pensions, per cent of GDP

2010

R2=0.586

0 10 20 30 40 50 60 70

0

5

10

Dependency ratio: percentage of adult population aged 65+

Demographic (in)determinism

15

20

25 Public expenditure on

pensions, per cent of GDP

2010

R2=0.586

Luxembourg

Slovenia

Spain

Italy

PortugalNorway

Belgium

Greece

0 10 20 30 40 50 60 70

0

5

10

Dependency ratio: percentage of adult population aged 65+

United

Kingdom

Turkey

United

States

Mexico

Korea

Australia

Canada

Poland

Portugal

Germany

Norway

2050

R2=0.112

Pension ages and life expectancy

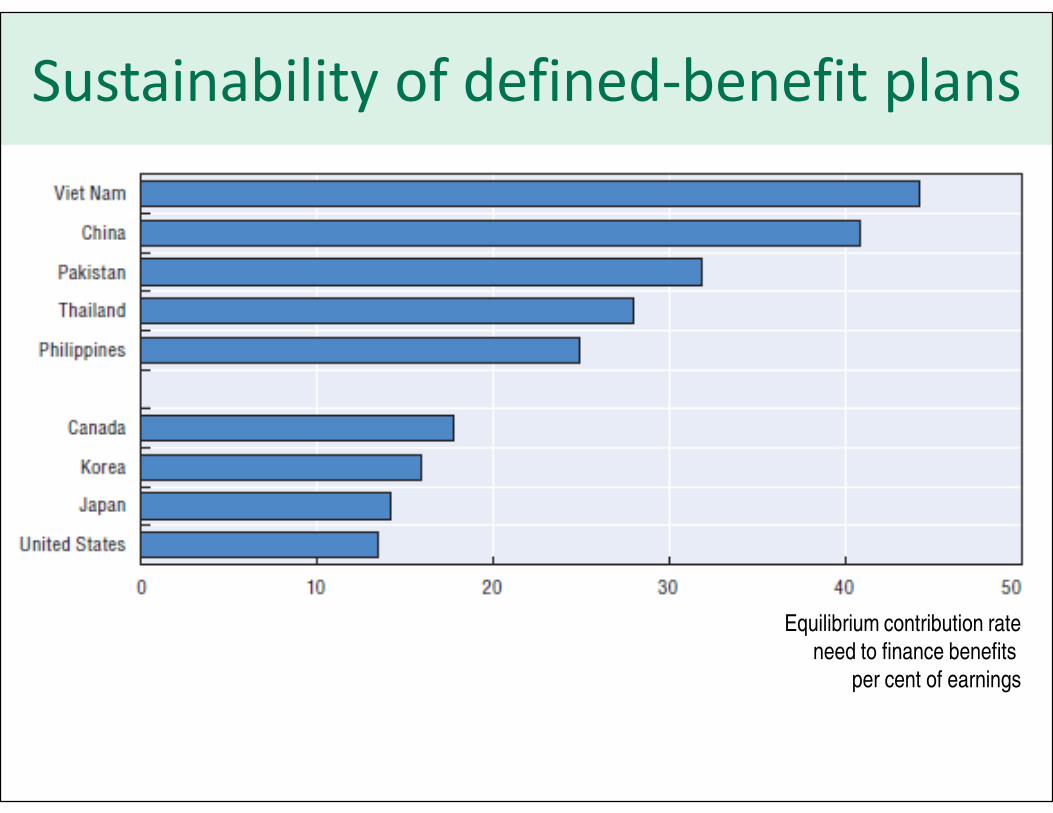

Sustainability of defined-benefit plans

Equilibrium contribution rate

need to finance benefits

per cent of earnings

Conclusions

4

Conclusions

Ageing Asia’s pension problems

• Coverage

• Adequacy

• Sustainability

Pensions at a Glance 2011

RETIREMENT-INCOME SYSTEMS IN

OECD AND G20 COUNTRIES

www.oecd.org/els/social/pensionswww.oecd.org/els/social/pensions

Pensions at a Glance 2011

RETIREMENT-INCOME SYSTEMS IN

OECD AND G20 COUNTRIES

www.oecd.org/els/social/pensionswww.oecd.org/els/social/pensions