Pension reform in SEEspietrom.com/public/admin/immagini/429.pdf · Pension Reform in Small Emerging...

34

Pension Reform in Small Emerging Economies Issues and Challenges Kenroy Dowers Stefano Fassina Stefano Pettinato Inter-American Development Bank Washington, D. C. Sustainable Development Department Technical Papers Series

Transcript of Pension reform in SEEspietrom.com/public/admin/immagini/429.pdf · Pension Reform in Small Emerging...

Pension Reformin Small Emerging Economies

Issues and Challenges

Kenroy DowersStefano Fassina

Stefano Pettinato

Inter-American Development Bank

Washington, D. C.

Sustainable Development DepartmentTechnical Papers Series

Cataloging-in-Publication provided byInter-American Development BankFelipe Herrera Library

Dowers, Kenroy. Pension reform in small emerging economies : issues and challenges / Kenroy Dow-ers, Stefano Fassina, Stefano Pettinato.. p. cm. (Sustainable Development Dept. Technical papers series ; IFM-130) Includes bibliographical references.

1. Pensions— Developing countries. 2. Old age pensions— Developing countries. 3. So-cial security— Developing countries. I. Fassina, Stefano. II. Pettinato, Stefano. III.Inter-American Development Bank. Sustainable Development Dept. Infrastructure and Finan-cial Markets Division. IV. Title. V. Series.

331.252 D6847--dc21

Kenroy Dowers is a financial specialist and Stefano Pettinato is a consultant in the Infra-structure and Financial Markets Division of the Sustainable Development Department.Stefano Fassina is an economist in the Fiscal Affairs Department of the InternationalMonetary Fund. The authors are grateful to Carol Graham, Estelle James, OliviaMitchell, Stefan Queck, Kim Staking and Antonio Vives for their helpful comments andsuggestions, and to Graciela Testa for her help in editing the document.

The opinions expressed in this paper are the responsibility of the authors and do not nec-essarily reflect the official position of the Inter-American Development Bank or the In-ternational Monetary Fund.

December 2001

This publication (Reference No. IFM-130) can be obtained from:

IFM PublicationsInfrastructure and Financial Markets DivisionMail Stop W-0508Inter-American Development Bank1300 New York Avenue, N.W.Washington, D.C. 20577

E-mail: sds/[email protected]: 202-623-2157Web Site: http:www.iadb.org/sds/ifm

Foreword

During the last decade, a consensus has been reached about the need to devise solutions for thelooming old-age crisis. This situation is driven by two sets of phenomena: on one side is thegradual decrease in the share of the working population, which is caused by a mix of decliningfertility rates and increasing life expectancy; on the other, is the widespread mismanagementand/or structural weakness of existing pension systems. Both developing and emerging econo-mies are paying increased attention to the type of pension reform that should be embraced.

While intensive research work has been directed at the reform issues for emerging economies,significantly less attention has been paid to the specific situation of small emerging economies.In this paper the authors examine the crucial issues that shape the types of pension fund reformand the fully funded elements that could be instituted in small emerging economies (SEEs).

This paper examines the issues in light of the constraints generated by the size and economiccharacteristics of many of these countries. In particular small developing states are likely to ex-perience high international labor mobility and domestic informality. Their economic systems areoften volatile, highly unequal, and based on a single-good export-oriented development model.Moreover, their financial markets tend to be small and poorly regulated, retarding the exploitationof economies of scale. Finally, political volatility and institutional weakness can promote cor-ruption and bureaucratic inefficiencies. All these features limit the applicability and success ofthe pension reform alternatives that have been and are currently being proposed.

The paper includes an alternative model that would maximize the efficiency of a pension programbased on fully funded principles, while reducing the costs that such a system would engendergiven the features of SEEs. In particular, the paper proposes the centralized collection of pensioncontributions, new investment management rules, the introduction of a specific regulatoryframework, and the regional integration of institutions and arrangements critical to the manage-ment of the pension system.

The Inter-American Development Bank has worked on pension reform in several Latin Ameri-can countries, including Argentina, Bolivia, Brazil, Honduras, El Salvador and Nicaragua. Pro-grams have included technical assistance and sector loans. The model proposed in this paper isconsistent with the IDB’s strategy for this sector, and can promote economic development andhelp reduce poverty and inequality, within a stable macroeconomic framework and increasingprivate sector participation in the provision of goods and services. Furthermore, the long-termgoals of these reforms, sought by the IDB and the Infrastructure and Financial Markets Divisionof the Sustainable Development Department, are the modernization of states, the advancement ofstructural reforms, and the strengthening of the countries’ financial sectors and capital markets.

Pietro MasciChiefInfrastructure and Financial Markets Division

Contents

I. Introduction 1A Review of Alternatives for Social Security Reform

II. Characteristics of Small Emerging Economies and Implications for Pension Re-form 7

Demographic CharacteristicsLabor MarketStructure of the EconomyFinancial MarketsPolitical Economy

III. A Policy Approach for Pension Reform in Small Emerging Economies 15Centralized CollectionNew Investment ManagementNew Regulatory FrameworkRegional System

IV. Lessons Learned and Conclusion 24

Bibliography 27

I. Introduction

By 2025, nearly 15 percent of the worldpopulation is expected to be over 60 years ofage. With increasing life expectancy thepopulation of developing countries is agingmuch faster than that of industrial countries.It is expected that in 2030, approximately 80percent of the total elderly population willreside in developing countries. A more rele-vant measure of the sustainability of old-agesupport systems is the dependency ratio,which calculates the elderly (normally thoseabove 65) as a percentage of the workingage population (between 15 and 64 yearsold).

As indicated in Table 1, dependency ratiosare likely to increase by more than 50 per-cent between 2000 and 2025 (with the ex-ception of Africa and the transition econo-mies of Central and Eastern Europe). Whilethe transition economies and the OECDcountries will maintain the highest levels ofold-age dependency, the biggest increaseswill occur in the Arab states, Asia and thePacific, and Latin American. The social bur-den from an increasing share of the non-working population is expected to generate

substantial costs that, in turn, are likely to bereflected in government budgets.

In recent years particular attention has beengiven to the need to devise solutions to theold-age crisis. The main concerns pertain tothe ability of existing social security systemsto meet promised benefit levels. In additionto the described demographic trends, mostpension systems around the world sufferfrom systemic flaws and inefficiencies at themanagement level. Overcommitment by thepension institutions, preferential treatmentof some sectors of the population, and near-sightedness in the design of the parameters,are only some of the results of political in-stability, administrative corruption, and bu-reaucratic inefficiency. All these factorshave weakened retirement arrangements andinstitutions in many countries, contributingto the old-age crisis.

Some manifestations and concerns that arisefrom the old-age crisis include:

• Increased deficits crowding out invest-ment in education, health, and infra-structure;

Table 1. Old-age Dependency Ratios*by World Region

1975 2000 2025Africa 6 6 7Arab States 6 5 8Asia and Pacific 7 9 14Central and Eastern Europe and Central Asia 14 17 24Latin America and the Caribbean 8 9 14OECD high-income countries 17 21 32World 10 11 15* Population above 65 years of age as a percentage of those between 15 and 64.

Source: Gillion et al. (2000) based on United Nations data.

2

• Insufficient provision for old-age bene-fits that are not indexed;

• Perverse redistribution from younger toolder generations and from low- to me-dium- and high-income workers;

• Hindered growth as systems mature andbecome a burden on government reve-nues;

• High payroll taxes that encourage eva-sion and informality;

• Reduced savings incentives; and• Incentives for early exit from the labor

market.

Typical policies aimed at correcting the ex-isting problems tend to target either the sys-tem dependency ratio, or the replacementrate.1 Raising the retirement age or theminimum number of years in the contribu-tory period decreases the dependency ratio.Reducing the benefits (either by modifyingthe benefit formula or by loosening the in-dexing mechanisms) or increasing the con-tributory rate (i.e. the payroll tax) takespressure off the replacement rate.

Countries have responded differently to thisimpending crisis depending on their circum-stances. In Africa and most of Asia, infor-mal structures have generally been in placeto deal with old-age income insecurity.2

These have partly compensated for the inef-ficiencies and the low coverage of publicsystems. With the goal of reducing liberalearly retirement provisions and generous

1 The system dependency ratio is the ratio betweenthe number of pensioners in the system and the num-ber of affiliates that contribute to it. The replacementrate is the ratio between the income after retirement(the pension benefit) and that before retiring (the ref-erence or average salary).2 These are usually based on the support given toparents by their children. A broader definition in-cludes family members and communities as the pro-viders of security. World Bank (1994) offers a reviewof the traditional systems for income security acrossgeographical regions.

benefits, several Latin American countrieshave introduced fully funded, defined con-tribution programs that give contributors achoice among different privately managedfunds.

Countries that belong to the Organization forEconomic Cooperation and Development(OECD) appear to be moving toward a sys-tem that combines a mandatory publiclymanaged pension program with mandatoryor voluntary fully funded, privately managedoccupational pensions or saving plans thattarget the needs of middle- and higher-income groups (see Gillion et al., 2000).

Notwithstanding variations in the types ofstructures, most of the recent models for so-cial security reform display elements of amulti-pillar structure. They combine a firstlayer of welfare benefits financed with pub-lic revenues with a second mandatory pay-as-you-go (PAYG) or fully funded layer.Sometimes there is also an optional thirdlayer made up of privately managed individ-ual accounts.

While the major pension reform alternativesin developing countries display these char-acteristics, little attention has been directedat the applicability of these models to solvethe old-age crisis in small emerging econo-mies (SEEs). A notable exception is a studyby Glaessner and Valdés-Prieto (1998), thatexplicitly addresses the major issues of pen-sion reform in small developing nations.They highlight the role of international tradein financial services (e.g. collection, proc-essing, benefits payment) as a condition forsuccessful pension reform in small devel-oping countries.3 While this point is welltaken, we believe that more attention shouldbe given to the initial financial shallownessthat exists in these countries. 3 The authors identify small states as those with lessthan 1 million contributors to the pension system.

3

Small developing states are likely to experi-ence high international labor mobility anddomestic informality. Their economic sys-tems are often volatile, highly unequal, andbased on a single-good export-oriented de-velopment model. Moreover, their financialmarkets tend to be small and poorly regu-lated, retarding the exploitation of econo-mies of scale. Finally, political volatility andinstitutional weakness can promote corrup-tion and bureaucratic inefficiencies.4

The central thesis of this paper is that theseidiosyncratic features of small emergingeconomies have a negative impact on thestructure of an optimal pension policy. Fur-thermore, some of them represent obstaclesto the introduction of funded pension sys-tems, that have been and are currently beingproposed (see World Bank, 1994; Orszagand Stiglitz, 1999).

Most, but not all, of the elements of the cur-rent pension reform agenda are applicable tosmall emerging economies. To illustrate thispoint we propose a new model that is basedon the current approach but that at the sametime tackles the issues unique to many smalldeveloping states.

In particular, to reduce market distortionsand exploit as much as possible the limitedeconomies of scale, we suggest the central-ized collection of contributions and an ini-tially limited pension fund market. Further-more, new investment management rules areneeded, along with the introduction of a spe-cific regulatory framework. Finally, we pro-pose the regional integration of many insti-tutions and arrangements critical to the su-pervision and the management of the pen-sion system.

4 Diamond (1997) stresses the political risk associ-ated with publicly managed PAYG pension plans.

The rest of this section reviews various pen-sion reform alternatives. Section II of thisreport introduces the characteristics of SEEsand the potential problems these countriesface when confronted with pension reform.In section III we posit specific recommen-dations on the policies that are advisable inSEEs, focusing on those aspects that repre-sent a departure from the mainstream modelof reform. Section IV identifies the lessonslearned in some countries that have intro-duced privately managed pension arrange-ments. We draw some concluding remarksin section V.

A Review of Alternatives forSocial Security Reform

Recent approaches to social security reformmay be grouped into two camps, dependingon the scope of reform, as well as its impacton the system. The first is parametric reformand the second is comprehensive reform.

Parametric reform involves changes in oneor more underlying features of the currentsystem, including the pension benefit for-mula, the retirement age, the benefit indexa-tion mechanism, the minimum contributoryperiod, or private fund management rules.

Comprehensive reforms involve significantstructural modification of the retirementsystem. These may affect only part of thepension system, or its entirety. Such reformstypically require a massive political en-deavor and call for particularly carefulanalysis and implementation.5 This is re-quired in most cases to mold the system to 5 It should be noted that parametric reforms may pre-cede or follow a structural reform. Before reformingthe structure of a pension system, authorities maydecide to adjust the parameters of the old system tosmooth out the impact of dismantling it. Conversely,after a reform is implemented and a new system in-troduced various parametric adjustments may be nec-essary as part of a continuous fine-tuning process.

4

the changing characteristics of the demo-graphic, economic, and financial environ-ment where it operates. 6

Countries that are reforming their pensionsystems— or that have done so in the pastdecade— ultimately choose between twobroadly defined models of pension system:the OECD model and the Latin Americanmodel.7

The OECD model has a multi-pillar structurewith a private and a public pillar. The for-mer is a mandatory or quasi mandatory em-ployer-sponsored funded pillar, which canbe either defined benefit or defined contri-bution. By and large, the decision on how toinvest the accumulated assets from workers’contributions is made by the employer orlabor union for the entire company or in-dustry. Pension systems based on the OECDmodel also have a public mandatory, univer-sal, PAYG pillar. With a few exceptions, thepublic pillar is based on a defined-benefit(DB) principle.8 The relevance of the publicpillar in some of the countries that have 6 Various modifications have been introduced to theoriginal Chilean system since its introduction in1981. For details see Vittas and Iglesias (1998).7 What we define as the Latin American model is veryclose to the system suggested by the World Bank(1994) where the public pillar maintains the redis-tributive role through a tax-financed minimum pen-sion guarantee program, and the main pillar is a man-datory privately managed one. Obviously, whenadopted, both of these models need to be adjusted tofit a country’s particular characteristics. For moredetails on this also see James (1998).8 This principle links the benefit to a prescribed for-mula, based on the contributor’s final pay (i.e. theaverage salary during the last years as a contributor).The weight of the public unfunded pillar varieswidely across OECD countries. While the UnitedStates, Great Britain, Switzerland, The Netherlands,and Australia have large privately funded systems(that have recently become mandatory in manycountries), in most OECD countries the public SocialSecurity system dominates old-age pension provi-sions. For the size of the private component see Table2.

adopted this model denotes how public old-age insurance arrangements are an inte-grated component of a broad system of so-cial protection, together with social assis-tance, unemployment insurance, and thelike. This approach gives priority to univer-sal coverage, and the public nature of socialsecurity (Gillion et al., 2000).

Chile implemented a comprehensive reformof its pension system in 1981. Many coun-tries in the region have since adopted ele-ments of the Chilean model, establishingwhat can be referred to as the Latin Ameri-can model.9 A central characteristic of thismodel is the mandatory, privately managed,defined contribution (DC), fully fundedsystem (see World Bank, 1994). In somecases, a PAYG mandatory pillar and a thirdvoluntary pillar are left to coexist with theprivate one.

Some versions of this approach adopt indi-vidual savings accounts, managed by pen-sion fund management companies. Workershave more voice in the choice of where theirassets are invested, and to what degree ofrisk. The funded pillar works on a definedcontribution basis, linking contributionsmade by the worker to the benefit receivedand entitling him or her to a lump sum or toan annuity at the end of the contributing pe-riod. Many countries adopting this modelhave done so by maintaining— or revitaliz-ing— their old public PAYG pillar.

Elements of the Latin American model havealso been introduced in some Eastern Euro-pean transition economies (Hungary, Po-land, Latvia, and Kazakhstan). In the pastfew years, several Central American coun-

9 For an extensive coverage of the history and thecurrent status of the Chilean system see Vittas andIglesias (1998). For a regional analysis of the (secondgeneration) Latin American pension reform trendssee Queisser (2000).

5

tries have expressed their intentions to re-form their pension systems following thedirection chosen by their Southern neigh-bors. However, there are reasons to believethat the development stage and the absolutesize of the economy may incorporate idio-syncratic factors that could make the main-stream Latin American pension reformmodel unsuitable for small emerging coun-tries.

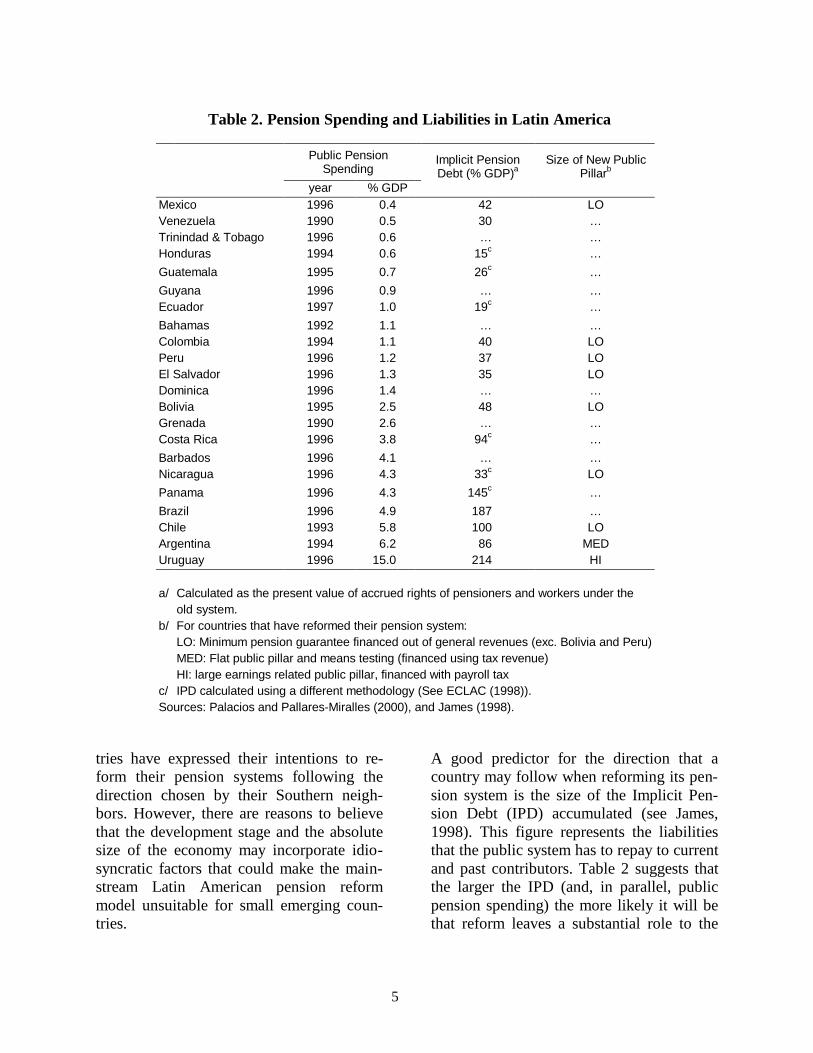

A good predictor for the direction that acountry may follow when reforming its pen-sion system is the size of the Implicit Pen-sion Debt (IPD) accumulated (see James,1998). This figure represents the liabilitiesthat the public system has to repay to currentand past contributors. Table 2 suggests thatthe larger the IPD (and, in parallel, publicpension spending) the more likely it will bethat reform leaves a substantial role to the

Table 2. Pension Spending and Liabilities in Latin America

Public PensionSpending

Implicit PensionDebt (% GDP)a

Size of New PublicPillarb

year % GDPMexico 1996 0.4 42 LOVenezuela 1990 0.5 30 …Trinindad & Tobago 1996 0.6 … …Honduras 1994 0.6 15c …Guatemala 1995 0.7 26c …Guyana 1996 0.9 … …Ecuador 1997 1.0 19c …Bahamas 1992 1.1 … …Colombia 1994 1.1 40 LOPeru 1996 1.2 37 LOEl Salvador 1996 1.3 35 LODominica 1996 1.4 … …Bolivia 1995 2.5 48 LOGrenada 1990 2.6 … …Costa Rica 1996 3.8 94c …Barbados 1996 4.1 … …Nicaragua 1996 4.3 33c LOPanama 1996 4.3 145c …Brazil 1996 4.9 187 …Chile 1993 5.8 100 LOArgentina 1994 6.2 86 MEDUruguay 1996 15.0 214 HI

a/ Calculated as the present value of accrued rights of pensioners and workers under theold system.

b/ For countries that have reformed their pension system:LO: Minimum pension guarantee financed out of general revenues (exc. Bolivia and Peru)MED: Flat public pillar and means testing (financed using tax revenue)HI: large earnings related public pillar, financed with payroll tax

c/ IPD calculated using a different methodology (See ECLAC (1998)).Sources: Palacios and Pallares-Miralles (2000), and James (1998).

6

public pillar, making the transition to thenew system more gradual.

In the next section, after examining the maincharacteristics of countries that are both

small in size and poorer on average, we il-lustrate the way in which some of thesefactors may represent an obstacle to the im-plementation and operation of new pensionsystems.

7

II. Characteristics of Small Emerging Economiesand Implications for Pension Reform

As discussed above, explanations for theold-age crisis are related to demographicfactors as well as to the systemic imbalancesof existing pension arrangements. In most ofthe developing world, these problems areeven more urgent and require adjustments ordrastic changes in pension systems. The cri-sis in emerging economies, however, ismainly a result of systemic problems, as thedemographic strain (i.e. aging populationand high dependency ratios) is not yet amajor issue (see Table 1). In fact, the rela-tively young population of most developingcountries may represent a window of op-portunity for change, making the transitionto more sustainable pension schemes lesspainful.10

Among developing countries, those that aresmaller in terms of population— smallemerging economies (SEEs)— share char-acteristics that can hinder the benefits com-monly attributed to the type of pension sys-tem that is being advocated by many pun-dits.

For this purpose we define an economy assmall if its population is under 8 million. At

10 The window of opportunity for reforming unfundedpension systems incurring in relatively low transitioncosts derives from the small size of the implicit debt.This may reflect the fact that there are fewer workersto compensate for past contributions. Factors thatcontribute to diminishing pension liabilities, thus thecosts of reform, are: a high proportion of young andworking-age population with respect to the more eld-erly workers or benefit recipients, who have contrib-uted throughout their lifetime; limited coverage of thepension system; relative immaturity of the system.For more details on transition cost financing seeQueisser (1998).

the same time, it is emerging if it is a lower-middle income economy in terms of GDPper capita (e.g. 1995 US$5,000). Figure 1and Table 3 show that when using thesethresholds, 13 Latin American countriesqualify as SEEs: Belize, Bolivia, Dominica,El Salvador, Guyana, Haiti, Honduras, Ja-maica, Nicaragua, Panama, Paraguay, St.Lucia, and St. Vincent and the Grenadines.11

In the past decade various initiatives havebeen launched to deal with issues concern-ing small states.12 The Barbados Conferenceof 1994 highlighted the economic and eco-logical vulnerabilities of small island devel-oping states (SIDS). The final report fromthe Conference was the Barbados Pro-gramme of Action for the Sustainable De-velopment of Small Island DevelopingStates, which sets forth specific policies, ac-tions and measures to be taken at the na-tional, regional and international levels insupport of the sustainable development ofSIDS.

Presently, the United Nations Department ofEconomic and Social Affairs is monitoringprogress in the implementation of the Bar-bados Programme of Action in 41 SIDS.Furthermore, various empirical studies havebeen completed to analyze the idiosyncra-sies of small and mainly micro states(population below 1 million).13

11 Although countries like Trinidad and Tobago, theBahamas, or Barbados are small in terms of popula-tion, they have to be excluded from our group ofSEEs because their per capita GDP is aboveUS$8,000.12 Major institutions involved in this effort are theWorld Bank, the United Nations, and the OECD.13 For a review see Easterly and Kray (2001).

8

The Commonwealth Secretariat/World BankJoint Task Force on Small States notes that,besides being small and with low averageincome levels, key features of small statesare:14

• Remoteness and Isolation. Many smallemerging economies are islands, land-locked nations or are far from majormarkets, driving up transport costs.

• Openness. Small economies generallystrive to have intense contacts with theirneighbors and the rest of the world. Onemanifestation is substantial internationallabor mobility.

14 The characteristics listed in the report by theCommonwealth Secretariat/World Bank Joint TaskForce on Small States (April, 2000) refer to countrieswith populations below 1.5 million. However, it islikely that most of these features still apply in coun-tries that have slightly larger populations (e.g. 4 mil-lion).

• Susceptibility to Natural Disasters andEnvironmental Change. Most smalleconomies are located in areas that arefrequently hit by natural disasters (e.g.hurricanes, droughts, and volcanic erup-tions).

• Limited Product Diversification. Due tothe limited size of their domestic mar-kets, small emerging economies tend tolimit export production to a few goods orservices.

• Poverty. Typically, smaller emergingstates tend to have particularly high pov-erty and inequality levels.

• Limited Public and Private Sector Ca-pacity. While this is a problem commonto most emerging economies, it appearsto be more serious in smaller ones. Lowhuman capital endowment and its un-even distribution are a critical factor.

Figure 1. Population and GNP per capitaLatin America and the Caribbean, 1998

1

10

100

1,000

10,000

100,000

1,000,000

1,000 3,000 5,000 7,000 9,000 11,000 13,000

GNP pc (current PPP$)

Pop

ulat

ion

('000

) log

sca

le

HaitiNicaragua

Honduras

Bolivia

Jamaica

Ecuador Guatemala

Dominican R.Paraguay

Panama

GuyanaBelize

St. Vinc. & G.

Dominica

St. Lucia

Grenada

Costa Rica

Venezuela

PeruColombia

BrazilMexico

Chile

Argentina

St. Kitts & N.

Antigua & B.

Trinidad & T.

Uruguay

El Salvador

9

Although many of these characteristics areshared by many larger developing countries,the frequency and incidence of these prob-lems is likely to be higher when a country issmall, poor, and open to external events.

The five critical areas where obstacles mayarise are examined below: the country’sdemographic structure, its labor market, itseconomic structure, its financial system, andits political economy.

Demographic Characteristics

In many developing countries, participationin pension systems is skewed toward theyoungest sectors of the population. Severalstudies point out that this may represent aproblem for pension coverage, especially inmiddle-income countries where povertyrates are higher among the young (James,1997; Whitehouse, 2000).

In SEEs, a set of problems derive from thesmall size of the population in absolute

SEE

Antigua & Barbuda 8,890 65 24.1 157.7 4Argentina 11,728 36,096 17.4 23.3 16.3 6Barbados 11,200 272 16.8 130.4Belize 4,367 236 x 18.9 101.9 13.8 19Bolivia 2,205 7,849 x 10.8 48.6 4.2 15Brazil 6,460 169,306 18.6 17.5 6.9 8Chile 8,507 14,789 25.2 56.4 5.4 7Colombia 5,861 38,340 13.9 33.5 12.0 13Costa Rica 5,812 3,583 26.8 99.8 6.0 15Dominica 4,777 73 x 20.5 115.7 20Dominican Republic 4,337 8,168 16.9 70.1 16.3 12Ecuador 3,003 12,391 19.3 61.5 9.8 13El Salvador 4,008 5,895 x 4.0 58.8 7.9 12Grenada 5,557 90 17.1 99.3 8Guatemala 3,474 11,988 7.7 45.5 23Guyana 3,139 701 x 17.1 203.3 35Haiti 1,379 6,683 x -6.9 40.6 30Honduras 2,338 5,965 x 23.4 97.9 3.8 20Jamaica 3,344 2,624 x 18.4 111.7 16.0 8Mexico 7,450 97,245 22.4 64.5 4.0 5Nicaragua 1,896 4,600 x 1.1 110.5 34Panama 4,925 2,731 x 23.5 76.9 14.3 8Paraguay 4,312 5,296 x 16.6 94.4 8.2 25Peru 4,180 26,049 19.5 28.7 7.4 7St. Kitts & Nevis 9,790 39 19.6 128.5 5St. Lucia 4,897 153 x 16.1 133.1 16.3 8St. Vincent & Grenad. 4,484 114 x 10.7 121.5 11Trinidad & Tobago 7,208 1,187 7.1 97.7 16.2 2Uruguay 8,541 3,284 15.3 44.4 8Venezuela 5,706 22,773 19.6 40.1 5

SEEs LAC Average 3,544 3,301 13.4 101.15 10.55 18.8Other LAC Average 6,924 26,215 18.1 70.52 10.01 8.8

Note: GDS is Gross Domestic Savings.Source: World Bank (2000).

Table 3. Small Emerging Economiesin Latin America and the Caribbean (1998)

1998 GNPpc (PPP)

Total Pop.('000s)

GDS/GDP Trade/GDP Unempl.Agriculture/

GDP

10

terms, and thus of the contributory base.Fewer contributors inevitably limit econo-mies of scale that companies can otherwisebenefit from in large markets, where sub-stantial pools of affiliates exist.15 The sys-tem may not be able to generate the neces-sary economies of scale that reduce admin-istrative costs, which are usually considera-bly higher in a fully funded system than in aPAYG one (see Packard, 1999). There maybe a mutually reinforcing vicious cycle be-tween low participation rates and higheradministrative costs.16

This occurrence can undermine the efficientfunctioning of private pension funds, andthus needs to be taken into account whendesigning pension systems in SEEs.

Labor Market

Owing to high rates of unemployment andunderemployment, young and poor workersare often unable to make regular and con-sistent contributions required to accrue pen-sion rights. In addition, they may be unableto contribute the minimum amount neededto obtain benefits in a defined-contributionsystem with individual accounts. This shiespoorer workers away from participating toofficial pension plans.

In general, large pockets of labor informalityare very common in developing countries.This, coupled with the limited absolutenumber of contributors noted above for

15 This characteristic typically exists in insurancemarkets, where the company, by insuring many indi-viduals can take advantage of the law of large num-bers, where the probability of a substantial loss isminimal given the large number of “events.”16 Fewer workers that regularly contribute to the sys-tem make it harder for the fund managers to lowercosts by exploiting economies of scale, in turn, mak-ing the opportunity cost of joining the system veryhigh for the poorer workers. See Packard (1999).

SEEs, may hinder the achievement of acritical mass of contributors necessary forthe system’s sustainability.

Furthermore, during economic downturns,and/or expansions in larger neighboringcountries, SEE workers may easily seek em-ployment abroad.17 This results in a decreasein the contributors-to-beneficiaries ratio (thesystem’s dependency ratio) as migrants’ re-mittances to the country of origin by-passthe pension system.

One advantage from a fully funded systembased on individual accounts is the link itestablishes between benefits and contribu-tions. This may be an important incentive tojoin the system.18 Finally, the coverage bycurrent systems is largely skewed towardcivil service and the military. New systemswould need to consolidate and enlarge thecontributory base through national partici-patory campaigns.

Structure of the Economy

The structure of the economy plays an im-portant role in the assessment of the bestpension reform. Many emerging economieshave low savings rates, high inequality ofincome, and a high corporate tax rate. Thereare reasons to believe that in many SEEsthese problems are even more serious anddifficult to overcome.

Table 3 highlights some of the characteris-tics of SEEs in Latin American and theCaribbean, defined using a maximum popu-lation threshold of 8 million and a maximum 17 Immigrant workers often belong to the most vigor-ous and hard working portions of the labor force.18 For a view that supports this effect, see Feldstein(1998). Orszag et al.(1999) add that the effect of in-dividual accounts on participation rates is more com-plex, since often additional costs reduce or eliminatethe incentive effect.

11

of $5,000 for GNP per capita (in PPP dol-lars). Thirteen countries fall under thesethresholds. These countries have severalcharacteristics in common that set themapart from the rest of the region.

On average, small emerging economies inthe region display lower gross domesticsaving (as a percentage of GDP), a ratio oftrade flows (imports and exports) to grossdomestic product that is 43 percent higherthan that of the rest of the region, no largedifferences in terms of unemployment rate,and over twice as much economic relianceon the agricultural sector.

These characteristics are likely to discourageparticipation in additional savings mecha-nisms. Given that the national income is de-rived from a one major activity that is basedon traditional agricultural or extractive in-dustries, these countries suffer from the va-garies of external economic pressures.

Because contributors to the system belong,for the most part, to the same industry, thehigh correlation among contributors’wages— thus among their contributingpower— can weaken the pension systemduring economic downturns.19 Moreover,many of the macroeconomic fundamentalstend to be unstable: high fiscal deficit, soar-ing government debt, high interest rates (re-flecting the country risk premium), double-digit inflation rates, and volatile exchangerates.

19 For example, if tourism— country X’s main sourceof revenues— is weak, the country will experiencemacroeconomic difficulties, and the pension systemwill be negatively affected by the weakened con-tributory power of most of its participants. In a coun-try with a more diversified productive structure, con-tributions from workers in stronger sectors can com-pensate for the temporary shortfall in the contribu-tions of those in weaker sectors.

These factors may discourage the involve-ment of sound domestic and (especially)foreign asset management companies in thenew system, and may reduce the returnsyielded by pension funds once they are in-troduced.

Financial Markets

Critical to the efficiency of a privately man-aged pension fund pillar within a multi-pillarmodel— PAYG plus FF— is the existence ofa financial market that permits reasonablereturns on investments. In many SEEs, ifthere is a functioning financial market at all,it is usually embryonic, offering few in-vestment opportunities and lacking an ade-quate legal and regulatory framework.20

In particular, small financial markets tend topresent the following features (see Bossoneand Honohan, 2001, for more details):

• lumpy, with frequent links between bor-rowers and lenders;

• non-competitive, due to polarized re-sources in a few large companies;

• incomplete, lacking ancillary financialservices, securities markets, etc.; and

• expensive, requiring costly regulationand supervision.

Establishing funded pension arrangements isone of the policy options available to poli-cymakers wishing to develop the contractualsavings sector (pension funds and life insur-ance companies) and foster domestic capitalmarkets (see Impavido, Musalem and Vittas,2001).

20 A comprehensive discussion on the constraintsfrom small financial systems have been discussed ina recent workshop held at the World Bank PrivateSector

12

Table 4 shows two common indicators forcapital market maturity.21 The first columnshows market capitalization (as a percentageof GDP, a proxy for overall stock marketsize). The capitalization of capital markets isoften positively correlated with the ability tomobilize capital and diversify risk. The sec-ond column captures the value traded (as apercentage of GDP), or market liquidity.This number can be interpreted as the ca-pacity to easily trade securities.

21 Some of the countries in Table 3 were omittedfrom Table 4 due to lack of data.

In developing regions both figures tend to beconsiderably below average as compared tothe more developed areas of the world. Notsurprisingly, SEEs have the shallowest mar-kets in the region, especially in terms of as-set liquidity. This suggests that introducingfunded pension plans in these countrieswould require specific mechanisms to com-pensate for the limited size and lack of li-quidity of such sectors. Another feature thatstands out is the extraordinary degree ofmarket depth achieved in Chile, where thelevels of market capitalization are compara-ble to those in many OECD countries. Theintroduction of a mandatory funded pension

Table 4. Market Capitalization and Value Traded(1999)

Regional AveragesMcap (% GDP) Valuetr (% GDP)

Central Europe, Central Asia 11.2 3.8East Asia and Pacific 133.1 77.8Latin America & the Caribbean 22.6 2.5Middle East & North Africa 39.1 10.5OECD (high-income countries) 114.7 81.4South Asia 16.3 8.2Sub-Saharan Africa 39.0 7.8

Latin America and the CaribbeanMcap (% GDP) Valuetr (% GDP)

Argentina 29.6 2.7Bolivia 1.4 0.0Brazil 30.3 11.6Chile 101.1 10.2Colombia 13.4 0.8Costa Rica 15.2 1.4Dominican Republic 0.8Ecuador 2.2 0.1El Salvador 17.2 0.4Guatemala 1.2 0.0Honduras 8.7Jamaica 36.7 0.6Mexico 31.8 7.5Panama 37.5 0.5Paraguay 5.5 0.2Peru 25.8 4.4Trinidad and Tobago 63.6 1.4Uruguay 0.8 0.0Venezuela 7.3 0.8Source: The World Bank (2001)

13

plan is a likely contributor to financial ma-turity in this Latin American country.

While capital account constraints limit thepossibility of securing larger returns andportfolio diversification from investment insecurities traded in foreign markets, tightregulations and supervision may be benefi-cial in underdeveloped capital markets giventhe limited financial culture and the high-risk environment.22 Low returns may alsoreduce the incentives to contribute to a pen-sion fund given the higher returns availablefrom alternative investments.

As a consequence investors often look over-seas for alternative investment opportunities.Given a specified amount of diversificationof the funds’ portfolio, these factors couldbe beneficial with a privately managed man-datory program because the risk elementwould be spread among various assets, in-cluding those from overseas.

Political Economy

The political economy of many smallemerging countries also influences thestructure, commitment to, and implementa-tion of reforms. Though many social secu-rity funds in small economies have acquiredsurpluses, a large contingent liability existsfor the unfunded civil service element. Re-form requires the government to recognizethis liability in a transition to a funded sys-tem. This has proven to be a disincentive forimplementing reform.23

22 Vittas (1996) distinguishes between tight or draco-nian regulatory frameworks needed in developingcountries when first introducing a funded system, andrelaxed ones suitable where mature financial andcapital markets already exist. Clearly, as the marketdeepens there should be a gradual relaxation of therules.23 Some Central American countries have approachedthe issue of pension reform, and abandoned it— at

The frequent use of social security funds tofinance the government and state enterprisesis mainly driven by politicians’ short-runexigencies rather than long-run benefits.These produce inertia when the time to im-plement reform comes. Malfeasance result-ing from a history of distortion and politicalinvolvement in the management of contri-butions and provision of benefits are diffi-cult to overcome, even after introducing pri-vate fund managers. When the political andeconomic spheres are shared among fewfigures, as in many SEEs, these distortionsare exacerbated.

An effective argument was posited in thepast by Peter Diamond (1997), when he in-dicated that moving away from a publicPAYG to a private FF system would reducepolitical risk related to episodes of misman-agement and corruption. A private FF sys-tem based on individual accounts wouldgenerate some degree of investment risklinked to financial performance and qualityof regulatory structures. The ultimate chal-lenge is to find out which risk is smaller andmore manageable.24

Finally, given that the success of the a newlyintroduced pension system would largelydepend upon the effective regulation andenforcement of market rules, the weak andinefficient law enforcement and judicialsystems that characterize many SEEs repre-sent serious constraints.

A separate issue that will only be mentionedhere is the political economy of pension re-form. Brooks and James (1999) examinevarious scenarios and reach mixed conclu-sions regarding the conditions for a favor- least temporarily— also due to the large implicit pen-sion debt. See Dowers et al. (2001).24 According to Diamond, the political risk is largeand inevitable in public PAYG systems. Orszag et al.(1999) openly disagree with Diamond on this.

14

able political environment necessary for ashift from public PAYG to private FF.Given the characteristics highlighted above,we can conclude that some SEEs may have

difficulty in reaching such consensus, unlessmultiple parties are involved in the process(i.e. employers organizations, civil societyinstitutions, labor organizations and unions).

15

III. A Policy Approach for Pension Reformin Small Emerging Economies

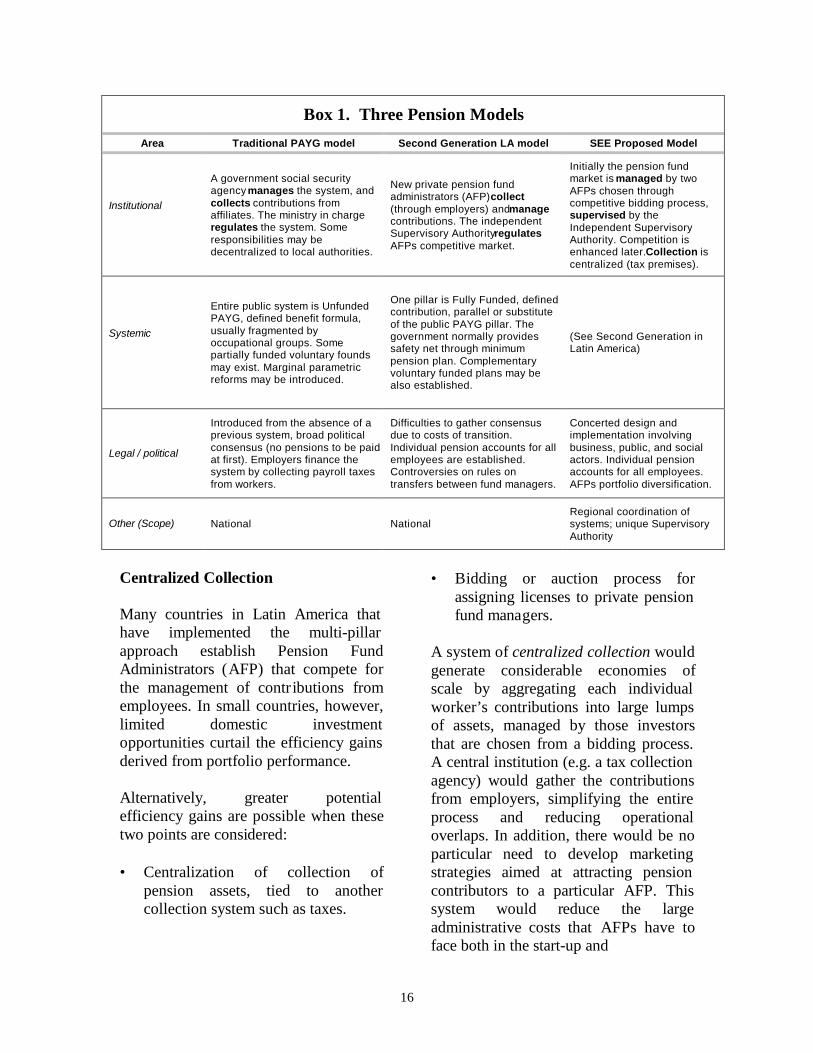

Generally, a pension system can be analyzedby observing four major features: its institu-tional structure, its systemic mechanisms, itslegal and political framework, and all otheraspects. The first column in Box 1 describesthe government-run system typical of manyLatin American countries, observed fromthese four perspectives. The other two col-umns display the major characteristics of theLatin American second-generation reformmodel and the proposed model for smallcountries— the latter a variant of the former.

According to Glaessner and Valdés-Prieto(1998), among others, the systemic aspectsof the second generation pension system aregenerally suitable for small emerging coun-tries. A system based on individual accountscould enhance the savings of its affiliatesand foster saving at the national level.Moreover, the incentive structure linked to adefined contribution system is likely to fa-cilitate the flow of sporadic contributionsfrom affiliates that are working abroad on atemporary basis.25 However, important dif-ferences exist in the institutional, legal, po-litical, and scale dimensions.

In line with the discussion above, some ele-ments of the second generation LatinAmerican pension model are not easily ap-plicable to small emerging economies and 25 It is worth noting that in SEEs, while the favorabledemographic circumstances help to keep the old un-funded systems afloat, the projected structure of thepopulation will represent a problem similar to thatfaced today by countries with older populations. Thishighlights the importance of acting now and changingthe system for a more efficient one, at a lower costgiven the window of opportunity (See note 11).

would require modifications to be more di-rectly relevant. In particular, we identifyfour main areas: approach to collection ofcontributions, investment management crite-ria, regulatory framework, and opportunityof integration at the regional level.

The approach to collection through central-ized institutions, and limited bidding thatwould curtail fees and increase the scale inthe provision of pension services.

Investment management centered on foreignportfolio diversification that also leavesspace for infrastructure-based investment arecritical.

The regulatory framework would be de-signed to maximize efficiency and to makeup for the lack of expertise and financialmarket experience at the domestic level.This may be unified with pre-existing super-visory bodies to optimize use of limited hu-man resources and expertise.

Regional integration of elements of the pen-sion system in order to gain economies ofscale from a centralized system. This wouldexpand considerably the size of the marketreducing the costs that derive from smallcontributory bases, small populations, vola-tility, and shallow financial markets.

Based on these four areas we construct thepolicy discussion over four principles: cen-tralized collection, new investment man-agement, new regulatory framework and re-gional system.

16

Box 1. Three Pension ModelsArea Traditional PAYG model Second Generation LA model SEE Proposed Model

Institutional

A government social securityagency manages the system, andcollects contributions fromaffiliates. The ministry in chargeregulates the system. Someresponsibilities may bedecentralized to local authorities.

New private pension fundadministrators (AFP) collect(through employers) and managecontributions. The independentSupervisory Authority regulatesAFPs competitive market.

Initially the pension fundmarket is managed by twoAFPs chosen throughcompetitive bidding process,supervised by theIndependent SupervisoryAuthority. Competition isenhanced later. Collection iscentralized (tax premises).

Systemic

Entire public system is UnfundedPAYG, defined benefit formula,usually fragmented byoccupational groups. Somepartially funded voluntary foundsmay exist. Marginal parametricreforms may be introduced.

One pillar is Fully Funded, definedcontribution, parallel or substituteof the public PAYG pillar. Thegovernment normally providessafety net through minimumpension plan. Complementaryvoluntary funded plans may bealso established.

(See Second Generation inLatin America)

Legal / political

Introduced from the absence of aprevious system, broad politicalconsensus (no pensions to be paidat first). Employers finance thesystem by collecting payroll taxesfrom workers.

Difficulties to gather consensusdue to costs of transition.Individual pension accounts for allemployees are established.Controversies on rules ontransfers between fund managers.

Concerted design andimplementation involvingbusiness, public, and socialactors. Individual pensionaccounts for all employees.AFPs portfolio diversification.

Other (Scope) National NationalRegional coordination ofsystems; unique SupervisoryAuthority

Centralized Collection

Many countries in Latin America thathave implemented the multi-pillarapproach establish Pension FundAdministrators (AFP) that compete forthe management of contributions fromemployees. In small countries, however,limited domestic investmentopportunities curtail the efficiency gainsderived from portfolio performance.

Alternatively, greater potentialefficiency gains are possible when thesetwo points are considered:

• Centralization of collection ofpension assets, tied to anothercollection system such as taxes.

• Bidding or auction process forassigning licenses to private pensionfund managers.

A system of centralized collection wouldgenerate considerable economies ofscale by aggregating each individualworker’s contributions into large lumpsof assets, managed by those investorsthat are chosen from a bidding process.A central institution (e.g. a tax collectionagency) would gather the contributionsfrom employers, simplifying the entireprocess and reducing operationaloverlaps. In addition, there would be noparticular need to develop marketingstrategies aimed at attracting pensioncontributors to a particular AFP. Thissystem would reduce the largeadministrative costs that AFPs have toface both in the start-up and

17

the operational phases. Furthermore, thecentralization of collection and investmentmanagement does not negate having multi-ple private portfolio managers.

Table 5 indicates that throughout the region,pension fund management companies chargean average old-age coverage commission of1.85 percent of the affiliates’ salary and thisamount varies largely across systems. Thischarge is certainly felt more by poorer con-tributors, and may discourage them fromcontributing to the program. The table alsoindicates that Bolivia is the most cost effi-cient system.

The framework being proposed here wouldhinge on the investment of assets throughthe institutional market with constrainedchoice among investment companies. Se-lected money managers (both local and in-ternational) could be invited to submit bidsto manage particular pension assets. Theauction can either select a predeterminednumber of best performers, or any numberof companies that perform above a certainminimum level. As mentioned, in this sce-nario the portfolio manager would notmaintain an infrastructure for collecting

funds from pension contributors. Under theproposed system, the portfolio managerwould bid for a long-term concession (notless than 5 years) to manage either some orall pension assets.26

This system is particularly suitable in SEEs.In an alternative scenario of free entry andcompetition, the small size of these econo-mies would probably leave space for theAFPs to increase their fees. Bolivia andSweden have utilized this structure. Theyare good examples of limited competitivebidding with efficiency gains from central-ized collection systems in terms of loweradministrative costs and fees (See Box 2 onBolivia).27 A condition for the success ofthis method is the transparency of the entireprocess, avoiding political interference andcollusion.

26 This solution is also advocated for Central Ameri-can countries by Cifuentes and Larraín (1999).27 James et al. ( 2001) advocate this system for coun-tries with small financial sectors. They also indicatethat the U.S. Federal Thrift Saving Plan as a success-ful example of centralized bidding and collection.

Table 5. Average AFP Administrative Fees in Latin America, 1999Select Latin American countries

year of reform Net Fee* Population(1998, ‘000s)

Chile 1981 1.84 14,789Peru 1993 2.36 26,049Colombia 1994 1.64 38,340Argentina 1994 2.30 36,096Uruguay 1996 2.06 3,284Mexico 1997 1.92 97,245Bolivia 1997 0.60 7,849El Salvador 1998 2.13 5,895

* Old-age pension fee, as a percentage of wageSources: James et al. (2001), World Bank (2001).

18

New Investment Management

Listed below are four crucial measures to beconsidered when introducing funded pensionsystems in SEEs,

• Adoption of modern portfolio invest-ment management techniques.

• Focus on diversification of portfolios toinclude foreign assets.

• Compatibility with and support forcapital market development strategies.

• Exploration of virtual links betweenpension fund portfolios and infrastruc-ture finance.

Investment strategy issues cannot be ad-dressed without considering which modernportfolio management techniques are appro-priate for small economies with constrainedcapital and limited investment opportunities.As observed when defining the structure ofthe economy of SEEs, capital account in-

flexibility is one of the factors that keepssmall emerging economies from allowingpension asset managers to have a higher ra-tio of international investment in their port-folios. However, modern investment man-agement techniques, such as asset or stockindex swaps, inflation index bonds and secu-ritization, can provide alternative investmentstrategies for countries with capital con-straints.28

After reaching a minimum critical size, thefinancial system can facilitate the survival ofpension fund managers by providing themwith long term capital investment opportu-nities. At the same time, pension fundscould prove to be crucial clearinghouses forthe flow of domestic and foreign investment, 28 The shift toward funded pension systems encour-ages greater domestic partaking in external bond is-sues through active participation of banks and pen-sion funds. Argentina, Lebanon and Kazakhstan aremajor examples. See Chapter III in Mathieson andSchinasi (2000).

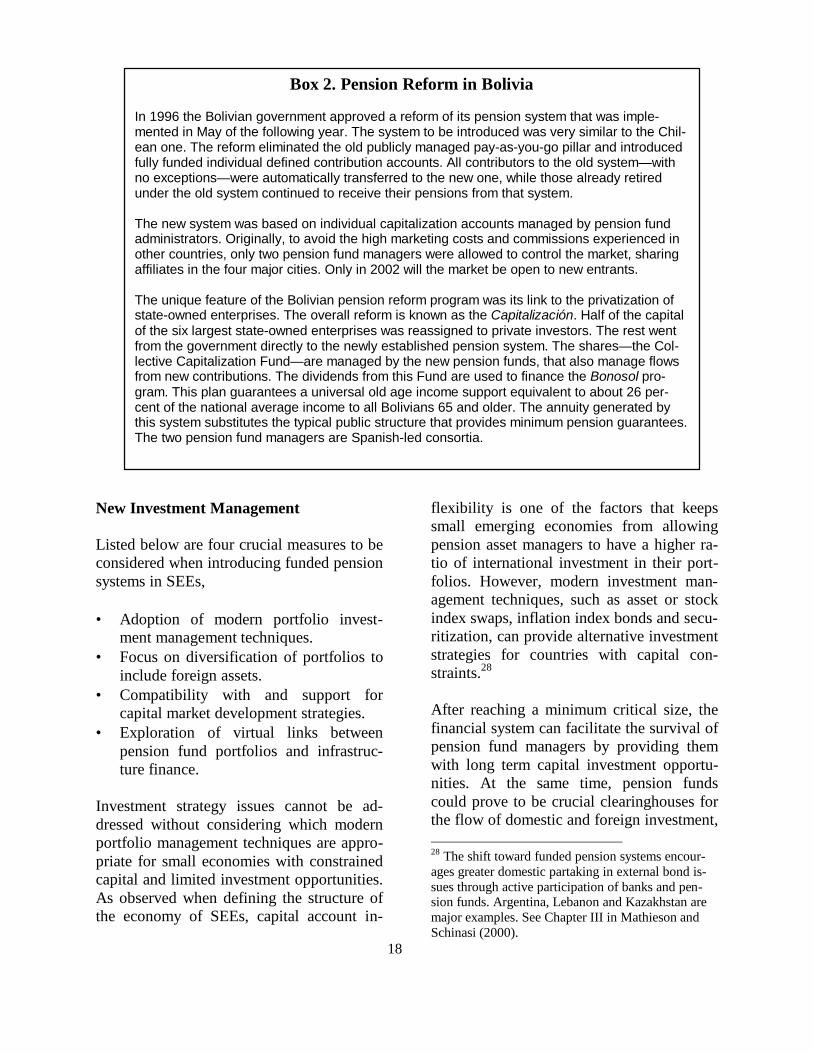

Box 2. Pension Reform in Bolivia

In 1996 the Bolivian government approved a reform of its pension system that was imple-mented in May of the following year. The system to be introduced was very similar to the Chil-ean one. The reform eliminated the old publicly managed pay-as-you-go pillar and introducedfully funded individual defined contribution accounts. All contributors to the old system— withno exceptions— were automatically transferred to the new one, while those already retiredunder the old system continued to receive their pensions from that system.

The new system was based on individual capitalization accounts managed by pension fundadministrators. Originally, to avoid the high marketing costs and commissions experienced inother countries, only two pension fund managers were allowed to control the market, sharingaffiliates in the four major cities. Only in 2002 will the market be open to new entrants.

The unique feature of the Bolivian pension reform program was its link to the privatization ofstate-owned enterprises. The overall reform is known as the Capitalización. Half of the capitalof the six largest state-owned enterprises was reassigned to private investors. The rest wentfrom the government directly to the newly established pension system. The shares— the Col-lective Capitalization Fund— are managed by the new pension funds, that also manage flowsfrom new contributions. The dividends from this Fund are used to finance the Bonosol pro-gram. This plan guarantees a universal old age income support equivalent to about 26 per-cent of the national average income to all Bolivians 65 and older. The annuity generated bythis system substitutes the typical public structure that provides minimum pension guarantees.The two pension fund managers are Spanish-led consortia.

19

allowing the development of capital mar-kets. Tax incentives for the generation ofequity may have a role as a means for fos-tering the growth of a competitive capitalmarket. Dual income tax systems that levylower taxes on profits gained using re-sources collected through the issuing of se-curities should be considered.

Pension Fund Investment inInfrastructure Development

It is worth noting the potential virtuous linksbetween investment in infrastructure proj-ects and pension funds (see Vives, 1999). Inparticular the former can be greatly benefi-cial for the development of the latter. Thistopic is even more relevant when dealingwith small emerging economies that lack thecapital and financial assets needed for thedevelopment of infrastructure investment.

As discussed, when introducing a systembased on pre-funded pension plans in aneconomy with embryonic financial markets,investment regulations are likely to bestrictly focused on safe assets. In these earlystages, infrastructure projects are typicallyexcluded from the investment options avail-able by law for pension funds. Behind theseprovisions are the higher risk and degree ofuncertainty characteristic of such projects,coupled with the lower liquidity of their as-sets. However, after the system reaches aminimum depth, investing in infrastructureassets can prove to be a favorable alternativeto other investments (see Vives, 1999).

Pension fund investment in infrastructuremay also be strictly supply-driven. In otherwords, instead of waiting for regulations tochange, pension funds may be enticed to in-vest in infrastructure projects without par-ticular changes in the investment rules (longrun). Instead, new and specially designed

infrastructure finance instruments couldprovide more liquidity and lower risk.29

The benefits to pension funds from investingin infrastructure result from: a) higher thanaverage returns compared to pension fundportfolios; b) increased diversification withrespect to the portfolios of competing pen-sion funds; and c) indirect benefits from theimpact of infrastructure finance on the econ-omy as a whole (i.e. job creation and eco-nomic growth). These investments have twoserious disadvantages. First, the higher re-turns are achieved in the long run (whilepension funds generally operate in long-terminvestment, competition increases the needfor shorter-term operations). Second, thehigher risk may lead affiliates to switch toother pension fund managers. Coupling in-frastructure finance with the described cen-tralized collection and bidding would reducethese drawbacks.

New Regulatory Framework

A key characteristic of recent approaches topension reform is the enhancement of theregulatory framework. This analysis focuseson the structure of the supervisory body, andon the degree of regulatory constraints im-posed by such entity.

Regulatory Structure

In most instances pension reform implies thecreation of an independent pension supervi-sory authority (PSA) that oversees pensionfund companies and employers and sets cri-teria for participation, contribution levels,conflicts of interests, rules concerning in- 29 For example, investment in many carefully selectedprojects, with some form of credit enhancement (e.g.multilateral participation, credit guarantees) overseveral sectors, covering more than one country,mostly in the operational stage of the project. SeeVives (1999).

20

vestments, switching across funds, funds’corporate governance, and related matters.

For many countries, social security reform isonly one element of a broader developmentstrategy, which occurs alongside the evolu-tion of the capital market and the moderni-zation of the insurance and banking sectors.Though these countries lack the institutionaland technical capacity, they are oftentempted to develop independent and decen-tralized entities for regulating the differentsegments of the financial market.

There are two problems with this approach.First, the countries are typically strapped forresources and thus cannot staff the inde-pendent supervisory entities with knowl-edgeable and well-trained individuals whohave the adequate resources. The secondproblem pertains to the lack of a consoli-dated regulatory framework to mirror theconglomeration that exists in the financialsector. Generally, the primary players in thefinancial sector are not divided by segment,and a few companies dominate the financialmarket. A centralized and consolidatedstructure provides regulators with a holisticview of the activities of these financial con-glomerates.

Finally, there are concerns about the politi-cal instability and bureaucratic murkinessthat exist in some SEEs.30 These may ham-per the creation and effective operation of anautonomous, transparent, and efficientregulatory body. It is thus of paramount im-portance that appropriate mechanisms areintroduced in order for the regulatory bodyto operate autonomously and transparently.Among the numerous alternatives for thestructure of the PSA we favor an integratedapproach, in line with Demaestri and Guer-

30 This applies easily also to medium-sized emergingeconomies.

rero (2001).31 According to this arrange-ment, the supervision and the regulation ofthe pension funds, insurance, and financialmarkets is assigned to a single supervisoryauthority (see Vittas, 1996; and Shah, 1996).This approach is desirable particularly insmall developing countries due to theeconomies of scale and scope generated bythe single authority, the avoidance of over-lapping operations and activities, and theoptimal use of the limited human capital andfinancial expertise available in these coun-tries.

Regulatory Criteria

Key issues that arise when designing regu-latory investment criteria for a fully fundedprivately managed pension system or pillarare both prudential and direct. Prudentialrequirements are financial solvency, avoid-ance of conflicts of interest, custodial safe-guards for managed assets, information dis-closure, fiduciary responsibility, accountkeeping, net asset value calculations, and soforth. The direct regulatory elements aremore specific to a particular system (seeShah, 1996). The major one is the exclusionof certain classes of financial assets (typi-cally equities) when the system is still im-mature. This restriction should be limited tothe initial period, and only where financialmarkets are substantially shallow (see Vit-tas, 1998).

The main reasons for excluding equitiesfrom pension fund investments are illiquid-ity problems, disclosure and corporate gov-ernance standards, and accounting practices.Since the government mandates contributorsto save for their retirement, it is importantthat the resources are deposited in a safe in-

31 Demaestri and Guerrero (2001) discuss the prosand cons of the specialized and integrated approachesto financial and regulatory supervision.

21

vestment. In order to guarantee this safety, atleast until the rules of the game are suffi-ciently transparent, the government has theresponsibility to set the rules for selectingthe best and most sophisticated investmentmanagers. The pension supervisory author-ity covers this function.

Some analysts suggest that the ideal ap-proach to regulation for a small country withan underdeveloped financial system is adraconian one, where strict regulations ap-ply to the management of pension funds andof financial assets in general.32 This regula-tory approach is justified when participationin the system is mandatory, and when affili-ates and fund managers have limited experi-ence and are unfamiliar with the new rules.Typically, under a framework of very strictsupervision, investment by pension funds inoverseas assets is limited to a very smallpercentage of the fund’s overall portfolio.As the financial system matures, these re-strictions are gradually relaxed.33

A dissenting view focuses on the largecountry risk that is generated when all (ormost) assets are invested domestically. In-ternational diversification of pension fundassets is advisable since it reduces the de-pendence of pension funds (and, ultimately,pensioners’ assets) on a single capital mar-ket. This approach has been adopted in therecent reform enacted in Nicaragua, whereAFPs are allowed to invest a maximum of30 percent of their assets internationally (see

32 For a comprehensive analysis see Vittas (1996). Aview more in favor of relaxed regulation of privatepension funds can be found in Shah (1996) andGlaessner and Valdés-Prieto (1998).33 For a recent debate over the merits of restrictions inpension funds investments in equities and foreignsecurities see a favorable argument by Srinivas andYermo (1999), and one against such restrictions byValdés-Prieto (1999).

Mitchell, 1997).34 Economies that are al-ready highly dollarized may benefit morefrom a system that allows for overseas in-vestment options in dollar-denominated as-sets.35

Finally, the global diversification of pensionfund investments promotes the integration ofstock markets. This beneficial outcome islikely to outweigh the disadvantages thatcome from the loss of savings to finance lo-cal investment (see Reisen and Williamson,1997). This conclusion comes from the as-sumption (backed by empirical evidence)that once the country reaches the point ofappearing sufficiently reassuring to foreigninvestors the net savings effect may be fa-vorable to the country.

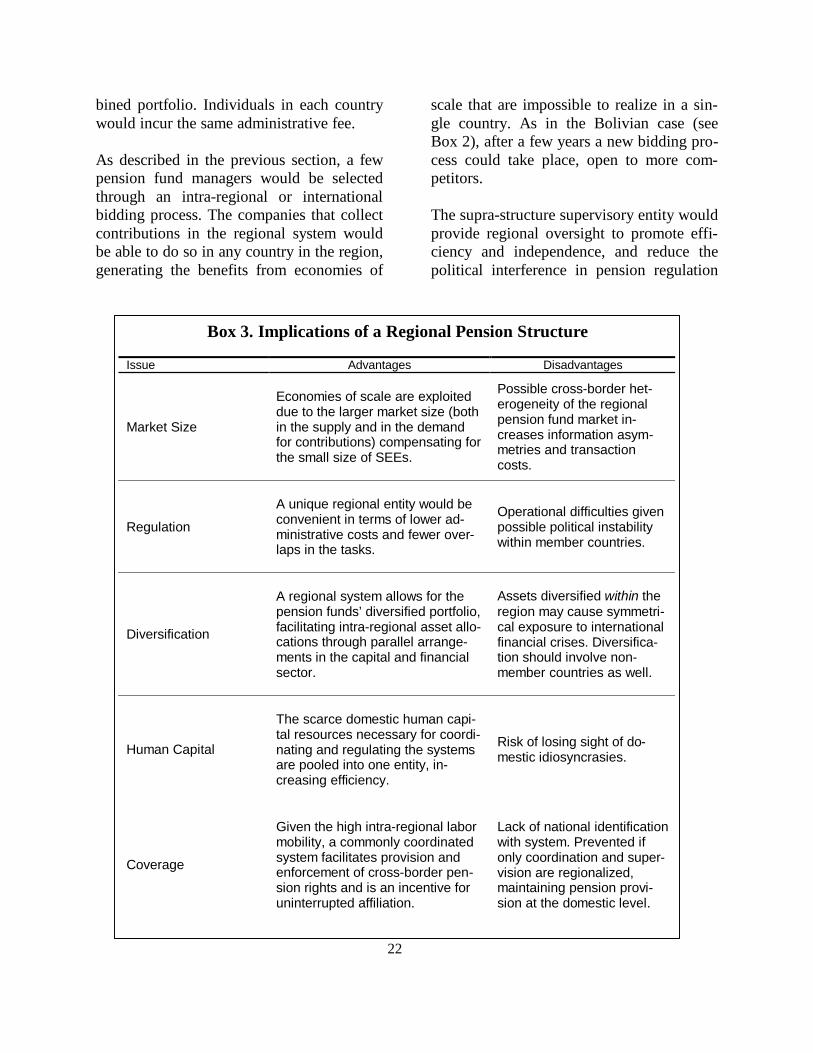

Regional System

Small emerging economies should consideradopting a regional system where a central-ized regulatory or administrative mechanismwould reduce costs through economies ofscale, which are typically very low inSEEs.36 In this structure each country shouldadopt its own pension parameters to fit itsfiscal and demographic realities. Eachcountry could also design and manage itsown tax collection system. The structure ofthe national pension systems would becommon across countries and coordinatedby an ad hoc regional body.

Member countries could come together toform a regional network to solicit interna-tional bidders for the management of a com-

34 Driessen and Laeven (2001) provide empiricalproof of the benefits of international portfolio diversi-fication in SEEs.35 This applies to most Central American and Carib-bean countries, where deposits and other financialand retail transactions occur in US dollars.36 Cifuentes and Larraín (1998) propose a regionalregulatory base for Central American countries.

22

bined portfolio. Individuals in each countrywould incur the same administrative fee.

As described in the previous section, a fewpension fund managers would be selectedthrough an intra-regional or internationalbidding process. The companies that collectcontributions in the regional system wouldbe able to do so in any country in the region,generating the benefits from economies of

scale that are impossible to realize in a sin-gle country. As in the Bolivian case (seeBox 2), after a few years a new bidding pro-cess could take place, open to more com-petitors.

The supra-structure supervisory entity wouldprovide regional oversight to promote effi-ciency and independence, and reduce thepolitical interference in pension regulation

Box 3. Implications of a Regional Pension Structure

Issue Advantages Disadvantages

Market Size

Economies of scale are exploiteddue to the larger market size (bothin the supply and in the demandfor contributions) compensating forthe small size of SEEs.

Possible cross-border het-erogeneity of the regionalpension fund market in-creases information asym-metries and transactioncosts.

Regulation

A unique regional entity would beconvenient in terms of lower ad-ministrative costs and fewer over-laps in the tasks.

Operational difficulties givenpossible political instabilitywithin member countries.

Diversification

A regional system allows for thepension funds’ diversified portfolio,facilitating intra-regional asset allo-cations through parallel arrange-ments in the capital and financialsector.

Assets diversified within theregion may cause symmetri-cal exposure to internationalfinancial crises. Diversifica-tion should involve non-member countries as well.

Human Capital

The scarce domestic human capi-tal resources necessary for coordi-nating and regulating the systemsare pooled into one entity, in-creasing efficiency.

Risk of losing sight of do-mestic idiosyncrasies.

Coverage

Given the high intra-regional labormobility, a commonly coordinatedsystem facilitates provision andenforcement of cross-border pen-sion rights and is an incentive foruninterrupted affiliation.

Lack of national identificationwith system. Prevented ifonly coordination and super-vision are regionalized,maintaining pension provi-sion at the domestic level.

23

that is typical in politically volatile SEEs.Likely results are enhanced efficiency, qual-ity of supervision, and stability of the regu-latory institution. Regional cooperationamong small neighboring countries shouldbe considered on both the demand side(contributors) and the supply side (pensionfunds and supervisory agency).

In formulating the regional oversight entity,it would be necessary to create a centralizedcommission to develop policy and a frame-work for the operations of the regional pen-sion regulator. The commission could bemade up of representatives from the centralbanks and governments of each participatingcountry, and coordinated by some interna-tional agency or organization.

In many cases, it may be politically difficultto introduced or guarantee a regional agree-ment in the medium and long term. How-ever, there are reasons to expect that har-monization in other sectors (i.e. trade, drugenforcement), which is already being pur-sued by groups of countries, could providean appropriate platform for the creation ofthe regional pension architecture.

Clearly, if the countries involved in a re-gional pension initiative already share mem-bership in multilateral bodies and presentlow cross-border transaction costs (e.g. dol-larized economies) the model being pro-posed has a much higher probability of suc-cess.

Hinging on existing regional agreementsmay also be a way to select groups of coun-tries that have demonstrated a willingness toengage in regional accords.

Moreover, this would help to single outcountries that have demonstrated politicaltolerance within and across their borders,thus increasing the likelihood of a successfulaccord on pension harmonization. The par-ticipation of international organizations andmultilateral bodies in the establishment ofsuch regional constituencies could fostercooperation and mutual guarantees.

Box 3 presents a summary of the major is-sues to be considered in the introduction ofregional elements in pension systems, alongwith some of the implications.

24

IV. Lessons Learned and Conclusion

A few conclusions can be drawn from somecases and can be extended to countries thatare considering reforming their pensionsystem. Recent pension reform in Nicaraguacentered on the PAYG pillar (to be phasedout) and introduced a fully funded pillarwith privately managed individual savingsaccounts (for details see Box 4).

One of the most significant tests for the ap-plicability of a pure Chilean-type pensionmodel in a small emerging economy is thecase of El Salvador. In 1996, the congressenacted a comprehensive reform of the pub-lic PAYG system, phasing it out in favor ofa private fully funded system. Only one yearlater, El Salvador experienced a severe fi-nancial crisis ignited by allegations of fraudsurrounding the formation of the new sys-tem.

Due to the loss of confidence by interna-tional investors, this episode delayed the in-

troduction of the system. Today, the Salva-doran pension system appears in bettershape than it was at the time of its introduc-tion, although the bad start may have taken atoll. The Salvadoran example illustrates theimportance of the prerequisites of transpar-ency and financial stability for the soundand successful introduction of a privatelymanaged funded pension plan.

The Bolivian pension reform of 1997 wasmentioned throughout our analysis as an ex-ample of successful pension policy innova-tion, where some aspects of the orthodoxChilean model where maintained, while newones where introduced in line with the needsof the country. In particular, among the lat-ter, the new competition rules for the pen-sion fund management companies haveproven effective in containing fees and gen-erating benefits from scale economies, hardto obtain in a small economy such as Bo-livia.

Box 4. Pension Reform in NicaraguaIn March of 2001 the Nicaraguan parliament approved a comprehensive reform of the country’spension system that entailed the introduction of a new fully funded and privately managed sys-tem on top of the defined-benefit pay-as-you-go existing program, that will eventually be phasedout. The reform is largely driven by concerns regarding the current and projected sustainability ofthe public system, financed largely by government debt and subsidies. Low and unequal cover-age considerations also affected the decision.

Workers who are less than 43 years of age have to join the new system, while those older willremain in the current system. The public pillar will go through some parametric changes (e.g.retirement age, pension minimum period, and prerequisites for minimum pension guaranteed).

As in the general Latin American model, the private pillar will be financed through employees’contributions, deposited in specialized pension fund management companies (AFP). A pensionsupervisory agency will be established in order to monitor the AFP’s profitability, check theirportfolio composition and that they meet the minimum standards set by the system.

25

As is the case for reform processes in otherareas, consultations with other sectors ofsociety when designing a pension systemmay facilitate the transition to a new one.Labor unions, particularly powerful in somecountries, ought to be included in the deci-sion-making process, as Uruguay and Vene-zuela did before introducing new pensionsystems (see Box 5 on Uruguay). It may notbe coincidental that these two pension sys-tems are probably the ones that have de-parted the most from the pure Chileanmodel.

This paper is an attempt to draw attention tothe particular characteristics of smallemerging economies, and how these imply a

revised approach to pension reform. Whilethe old age crisis may be an issue in the fu-ture, small emerging economies present a setof constraints generated by their size andeconomic situation. Thus far, these countrieshave not been treated separately in the dis-cussion on pension reform.

As a general conclusion, the challenge facedby policymakers when introducing privatepension funds in SEEs derives largely fromweak contributory bases (due to limited size,poverty, and informality) and from theshallow financial markets.

We argue that small emerging economieshave a limited ability to reap the intendedgains of recent alternatives for social secu-

Box 5. Pension Reform in Uruguay

A new multi-pillar pension system was introduced in Uruguay in 1996. Like the one introduced twoyears earlier in neighboring Argentina, the Uruguayan pension system is a combination of a pub-licly managed pay-as-you-go pillar and a private fully funded one. A full transition to a privatelymanaged funded system was also considered as an option, but labor groups opposed suchchanges.

The second pillar is modeled after the Chilean pension fund pillar of 1981. Contributions to the firstpillar are mandatory for all workers. However, the rules for joining the second pillar vary. At thetime of the reform only workers below 40 years of age had to join the new system. Moreover, thesecond pillar is mandatory for all workers whose earnings are above a threshold of 5,000 pesos(approximately $850), periodically adjusted for inflation, and optional for everyone else. More spe-cifically:

• Workers that earn less than the threshold can choose to join the new system. If they do, theircontribution will be equally split between the two pillars.

• Workers who earn more than the threshold contribute to the first pillar on the first 5,000 pesosof their earnings while the rest is used towards the private pillar.

As in the Argentine system, contributions to the private pillar come exclusively form employees,while contributions from both employees and employers finance the first pillar.

The structural and operational characteristics of the newly established pension funds in the secondpillar follow closely the Chilean model. One important difference is the supervisory body. Privatepension fund management companies are licensed and supervised by the Central Bank of Uru-guay (as opposed to an ad hoc independent supervisory agency). Affiliates are allowed to switchfunds twice a year, making the system more competitive.

26

rity reform. In particular, policymakersshould consider the following principles:

Principle 1: Centralized Collection. A newapproach to collection and investment man-agement through centralized institutions,and limited bidding. This would reduce feesand increase scale economies.

Principle 2: Assets Diversification. A set ofcriteria that allow pension fund managers toallocate their portfolio using foreign assetsthrough modern portfolio investment man-agement techniques and portfolio diversifi-cation, in part hinging on infrastructure fi-nance.

Principle 3: Integral Regulation. A regula-tory structure based on a pension supervi-sory authority unified with pre-existing su-pervisory bodies to optimize use of limitedhuman resources and expertise.

Principle 4: Regional Integration. Focus ona regional superstructure where elements ofthe pension systems of several countries areintegrated, easing controls, harmonizingcollection and supervision, increasing effi-ciency, and facilitating the cross-border pro-vision of services for affiliates, as well asthe portability of acquired rights.

Small emerging countries usually haveyoung pension systems, with relatively fewcommitments and young populations. If theexisting pension system is not sustainable inthe long term, the opportunity to switch to anew, more efficient and sustainable pensionstructure should be seized now, withoutwaiting for the hard times to come. Unfortu-nately, the apparent lack of urgency reducesthe political leverage of reformers.

Transition costs linked to pension reforms inSEEs deserve closer examination as most ofthese countries may be able to realize certainadvantages if they reform sooner rather thanlater, because the implicit pension debt isrelatively low and the burden of reformingthe system is still contained.

Given the relevance of the topic, more re-search should be done on specific instancesof pension reform in small emerging coun-tries, their successes, and the lessons to belearned.

27

Bibliography

Bossone, Biagio, Patrick Honohan, and Millard Long. 2001. Policy for Small FinancialSystems. Financial Sector Discussion Paper No. 6. The World Bank.

Brooks, Sarah and Estelle James. 1999. The Political Economy of Structural Pension Re-form. World Bank Research Conference on Old Age Security. Washington, D.C.

Cifuentes, Rodrigo, and Felipe Larraín. 1999. Pension Reform in Central America: AProposal. Development Discussion Paper No. 676. HIID. February.

Corsetti, Giancarlo, and Klaus Schmidt-Hebbel. 1997. Pension Reform and Growth. InValdes-Prieto. (1997). The Economics of Pensions. Cambridge: Cambridge Uni-versity Press.

Demaestri, Edgardo, and Federico Guerrero. 2001. The Rationale for Integrating Finan-cial Regulation and Supervision in Latin America and The Caribbean. Mimeo.IDB.

Diamond, Peter. 1997. Insulation of Pensions From Political Risk. In Valdés-Prieto, Sal-vador (ed.). Op. cit.

Dowers, Kenroy, Stefano Fassina, and Stefano Pettinato. 2001. Pension Systems in Gua-temala, Guyana, and Honduras: Evolution, Status, and Possibilities for Reform.Inter-American Development Bank. Mimeo.