Pay for performance? CEO Compensation and Acquirer Returns in BHCs by Kristina Minnick, Haluk Unal...

22

Pay for performance? CEO Compensation and Acquirer Returns in BHCs by Kristina Minnick, Haluk Unal and Liu Yang Discussion by Santiago Carbó-Valverde University of Granada (Spain) Mergers and Acquisitions of Financial Institutions Conference Arlington, Virginia Nov30-Dec1, 2007

-

Upload

jonathan-shaw -

Category

Documents

-

view

218 -

download

1

Transcript of Pay for performance? CEO Compensation and Acquirer Returns in BHCs by Kristina Minnick, Haluk Unal...

Pay for performance?CEO Compensation and Acquirer Returns in BHCsby Kristina Minnick, Haluk Unal and Liu Yang

Discussion by

Santiago Carbó-Valverde

University of Granada (Spain)

Mergers and Acquisitions of Financial Institutions ConferenceArlington, Virginia Nov30-Dec1, 2007

2

OBJETIVES AND MAIN FINDINGS (I)

This paper assesses the role of incentive-based compensation for CEOs in merger decisions.

MAIN FINDINGS:

Banks with higher pay-performance sensitivity are less likely to engage in mergers.

However, when these high PPS managers do undertake mergers, financial markets expect good results and react positively.

We find positive abnormal announcement returns for both bondholders and stockholders for banks with high PPS executives.

Following acquisitions, these banks also experience significantly more improvement in their operating performance as measured by ROA.

3

OBJETIVES AND MAIN FINDINGS (II)

A contribution is the use of a CEO compensation variable as a determinant of merging decisions and ex-post merger value.

Not just compensation but a pay-for-performance compensation (total, stock holdings, option holding).

Nice interpretation of the results and good implications for bank management and for the evaluation of consolidation processes.

4

COMMENTS AND CONCERNS

MAIN COMMENTS

MINOR COMMENTS

- AGENCY THEORY

- ENDOGENEITY CONCERNS AND SELECTION BIAS

- OTHER CONTROLS

- ECONOMETRIC METHODOLOGY

5

AGENCY THEORY (I)

The resolution of the principal-agent problem becomes central to illustrate the extent to which M&As are related to pay-performance measures (Becht et al., 2003, Handbook of the Economics of Finance).

Since Firth (1980, QJE) many studies have shown that mergers and takeovers resulted in benefits to the acquired firms' shareholders and to the acquiring companies' managers, but that losses were suffered by the acquiring companies' shareholders: takeovers are motivated by maximization of management utility reasons, rather than by the maximization of shareholder wealth.

6

AGENCY THEORY (II)

Does compensation depend ultimately on luck? (Exogenous shocks that increase performance? (Bertrand and Mullainathan, 2001, QJE).

In the years following mergers, CEOs of poorly performing firms receive substantial increases in option and stock grants that offset any effect of long-term underperformance on their wealth. As a result, the CEO’s pay and his overall wealth become insensitive to negative stock performance, but his wealth rises in step with positive stock performance (Harford and Li, 2007, JoF)

7

AGENCY THEORY (III)

Can CEOs manipulate their own compensations? In the resolution of the agent-principal problem there are different views: they cannot (contracting view) vs. they can (skimming view). If CEO payments are not the result of an optimal contract then takeover decisions are made on his/her own interest (Bertrand and Mullainathan, 2000, AER)

8

ENDOGENEITY CONCERNS AND SELECTION BIAS (I)

ENDOGENEITY ISSUES: Lessons from agency theory recommend to consider:

Pay-performance affect mergers but there are several explanatory variables (e.g. governance proxies) that may affect both pay-performance and mergers:

The authors acknowledge a positive effect on performance in the mergers that are conducted by high-PPS CEOs.

Is it pay-performance which affects mergers or are mergers affecting pay-performance (reverse causality?).

This may, at least partially, explain the “low” pseudo R2 compared to other studies (the authors are aware of this).

9

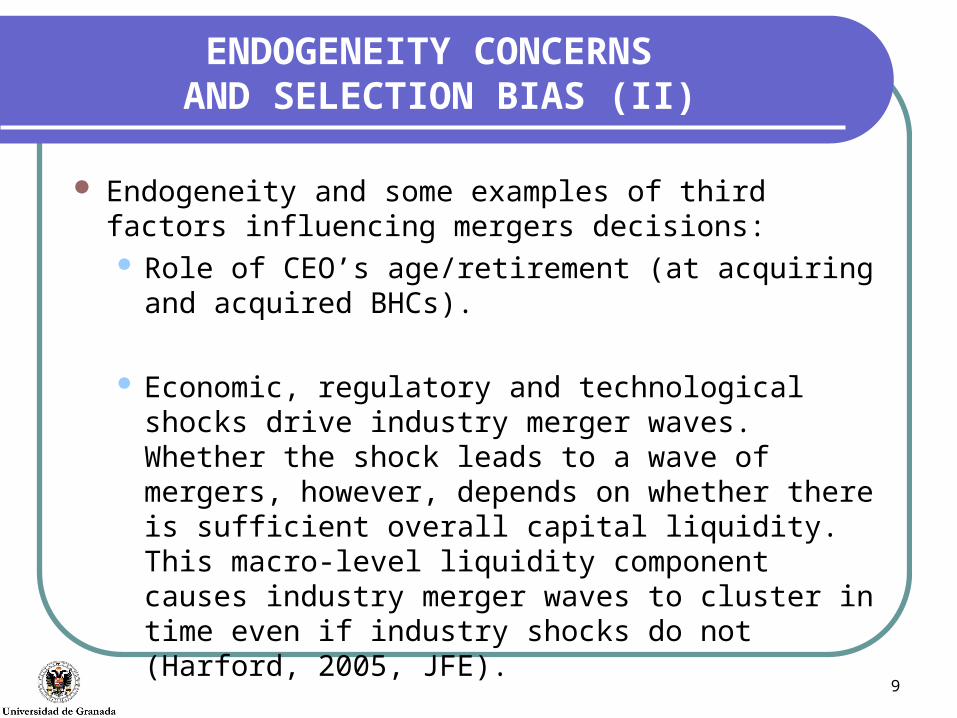

ENDOGENEITY CONCERNS AND SELECTION BIAS (II)

Endogeneity and some examples of third factors influencing mergers decisions: Role of CEO’s age/retirement (at acquiring and

acquired BHCs).

Economic, regulatory and technological shocks drive industry merger waves. Whether the shock leads to a wave of mergers, however, depends on whether there is sufficient overall capital liquidity. This macro-level liquidity component causes industry merger waves to cluster in time even if industry shocks do not (Harford, 2005, JFE).

10

ENDOGENEITY CONCERNS AND SELECTION BIAS (III)

There is a number of factors that can affect merger decisions that the authors, as an assumption, do not consider as relevant:

They assume that “acquisitions are not diversification

driven” but among the primary determinants of merger-related bondholder gains are diversification gains, gains associated with achieving too-big-to-fail status, and, to a lesser degree, synergy gains (Penas and Unal, 2004, JFE).

11

ENDOGENEITY CONCERNS AND SELECTION BIAS (IV)

Selection bias may also be affecting the results:

Merging institutions: employ non-merging institutions as controls? Heckman filters corrections?

Selection problems in the breakdown of mergers between high PPS, medium PPS and low PPS.

12

ECONOMETRIC METHODOLOGY (I)

The estimation seems to be a mixed logit but further details should be helpful to understand the empirical methodology.

How do you include the fixed effects? This does not seem to be purely a panel estimation.

13

ECONOMETRIC METHODOLOGY (II)

The multivariate stock return equations (Table VII) are a bit disappointing even if the pay-performance variables are significant.

The model seems to work much better for bond returns (however, there seems to be too few observations for a logit regression).

The stockholdings compensation (SPPS) does not seem to be significant in the case of the changes in ROA (Table X).

14

Backward aggregation of the data in order to compute pre-merger performance. Should the authors only look at the acquiring bank (B) (pre-merger) when using the pay-performance perspective?

A

B

A + B

B (POST-MERGER?)

Performance

Size

= backward aggregation

15

OTHER CONTROL FACTORS (I)

Adjusting for the impact of earnings management (considering these factors) substantially increases the measured importance of governance variables and dramatically decreases the impact of incentive-based compensation on corporate performance (Cornett et al., JFE forthcoming).

However, variables such as the presence of independent outside directors on the board does not appear to be significant in the paper.

16

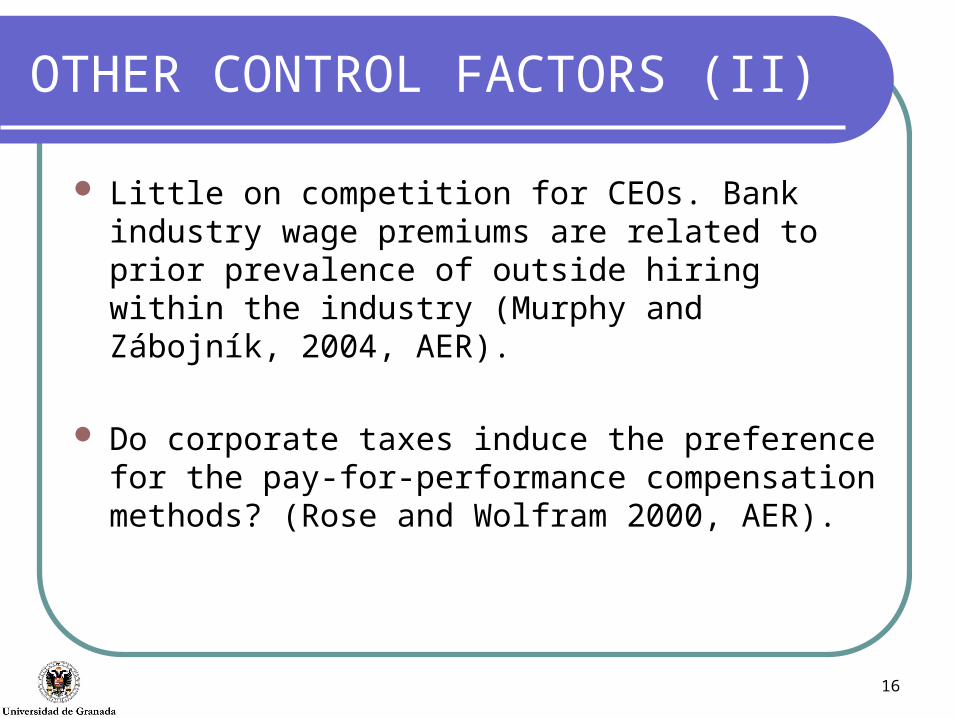

OTHER CONTROL FACTORS (II)

Little on competition for CEOs. Bank industry wage premiums are related to prior prevalence of outside hiring within the industry (Murphy and Zábojník, 2004, AER).

Do corporate taxes induce the preference for the pay-for-performance compensation methods? (Rose and Wolfram 2000, AER).

17

OTHER CONTROL FACTORS (III)

Evidence of a strong relationship between firm performance and CEO compensation explained almost entirely by changes in the value of CEO holdings of stock and stock options (Hall and Liebman, 1998,QJE).

BUT…

There is also evidence that the use of discretionary accruals to manipulate reported earnings is more pronounced at firms where the CEO’s potential total compensation is more closely tied to the value of stock and option holdings (Bergstresser and Philippon, 2006, JFE).

18

OTHER CONTROL FACTORS (IV)

Economic shocks are particularly relevant since they may limit (exacerbate) the merger waves (e.g. current turbulence with subprime mortgages and conduits).

Implications for Europe: Institutional/environmental differences between European and US mergers. The regulatory change towards financial integration and the new merger wave in Europe: is there a role for CEO’s compensation?

Further research: need for more international evidence.

19

Minor comments (I)

The paper claims to be a “natural experiment”. However, this would involve keeping all variables constant excepting those that we want to experiment with.

Thomson financial SIC6020: banks and financial institutions (what does the latter include?)

Is there a role for ROE instead of ROA?

Do the newly awarded and the existing grants have the same weight? (page 5)

20

Minor comments (II)

The bond data only for 18 acquisitions

The effects of returns in the case of bondholders are unclear (page 14)

PAGE 15, First paragraph--- are the univariate results really showing evidence of lower credit risk?

21

References

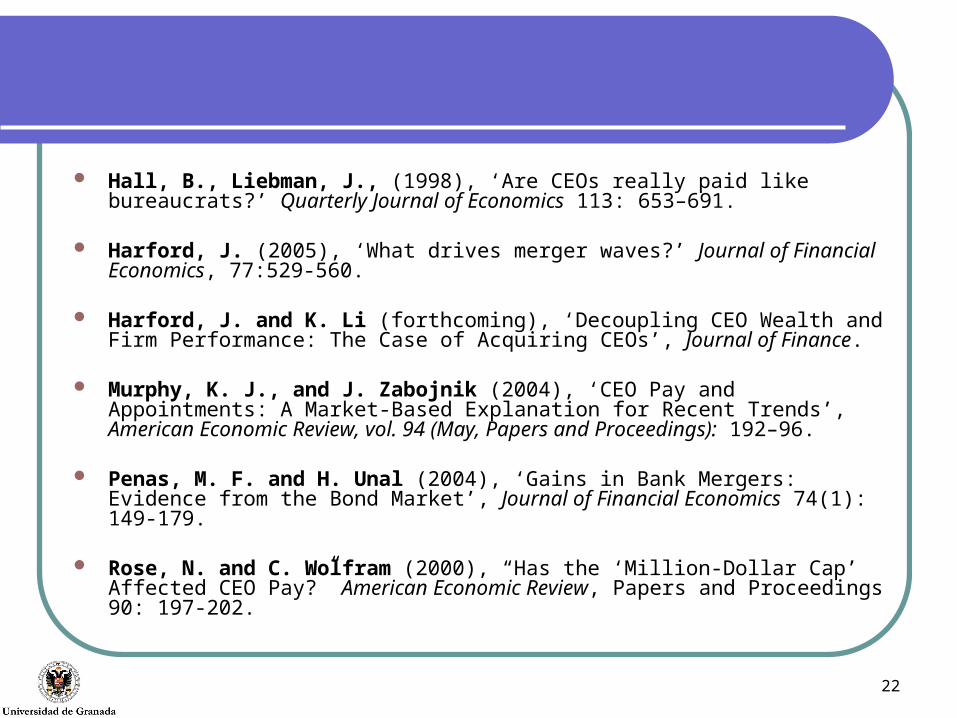

Becht, M., Bolton, P. and A. Röell (2003), ‘Corporate Governance and Control’ in G.M. Constantinides and R.M. Stulz (eds.), Handbook of the Economics of Finance, Volume 1A (Corporate Finance): 3-86.

Bergstresser, D., and T. Philippon (2006), ‘CEO incentives and earnings management: Evidence from the 1990s’, Journal of Financial Economics, 80: 511-529.

Bertrand, M. and S. Mullainathan (2000), ‘Agents with and without Principals’ American Economic Review, Papers and Proceedings of the One Hundred Twelfth Annual Meeting of the American Economic Association, 90: 203-208.

Bertrand, M., and S. Mullainathan (2001), ‘Are CEOs rewarded for luck? The ones without principals are’, Quarterly Journal of Economics 116: 901-932.

Cornett, M.M., Marcus, A.J., and J. Tehranian (forthcoming), ’Corporate governance and pay-for-performance: The impact of earnings management’. Journal of Financial Economics.

Firth, M. (1980), ‘Takeovers, shareholders returns, and the theory of the firm’ Quarterly Journal of Economics, 94: 235-260.

22

Hall, B., Liebman, J., (1998), ‘Are CEOs really paid like bureaucrats?’ Quarterly Journal of Economics 113: 653–691.

Harford, J. (2005), ‘What drives merger waves?’ Journal of Financial Economics, 77:529-560.

Harford, J. and K. Li (forthcoming), ‘Decoupling CEO Wealth and Firm Performance: The Case of Acquiring CEOs’, Journal of Finance.

Murphy, K. J., and J. Zabojnik (2004), ‘CEO Pay and Appointments: A Market-Based Explanation for Recent Trends’, American Economic Review, vol. 94 (May, Papers and Proceedings): 192–96.

Penas, M. F. and H. Unal (2004), ‘Gains in Bank Mergers: Evidence from the Bond Market’, Journal of Financial Economics 74(1): 149-179.

Rose, N. and C. Wolfram (2000), “Has the ‘Million-Dollar Cap’ Affected CEO Pay?” American Economic Review, Papers and Proceedings 90: 197-202.