Paradox of Prudence Linkage between - South African rand Stability/FinStab_Research... · Paradox...

46

Brunnermeier “Paradox of Prudence” Paradox of Prudence & Linkage between Financial & Price Stability Markus Brunnermeier Reserve Bank of South Africa Pretoria, South Africa, Oct 26 th , 2017

Transcript of Paradox of Prudence Linkage between - South African rand Stability/FinStab_Research... · Paradox...

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Paradox of Prudence&

Linkage betweenFinancial & Price Stability

Markus Brunnermeier

Reserve Bank of South Africa Pretoria, South Africa, Oct 26th, 2017

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Overview

1. From Risk in Isolation to Systemic Risk• Volatility Paradox

• Direct Spillovers – domino effects

• Indirect Spillovers – amplifiers vs. absorbers

• Paradox of Prudence (becoming an amplifier)

2. From Separation Principles to Interlinkagesacross stability concepts• … and redistributive monetary policy

3. International: Safe assets and cross-border capital flowsFrom a Buffer Approach to a Rechanneling Approach

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

The 2 Components of Systemic Risk

1. Systemic risk build-up during (credit) bubble … and materializes in a crisis – time-series

“Volatility Paradox” contemp. measures inappropriate

• Low VaR ⇒ low margins ⇒ high margins ⇒ high leverage ⇒ low risk-weights⇒ less capital ⇒ high leverage

• Shock leads to large adjustment• High VaR ⇒ …

Procyclicality• Countercyclical puffer… See paper

More subtle: better idiosyncratic risk sharing higher endogenous risk

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

The 2 Components of Systemic Risk

1. Systemic risk build-up during (credit) bubble … and materializes in a crisis – time-series

“Volatility Paradox” contemp. measures inappropriate

• Low VaR ⇒ low margins ⇒ high margins ⇒ high leverage ⇒ low risk-weights⇒ less capital ⇒ high leverage

• Shock leads to large adjustment• High VaR ⇒ …

Procyclicality• Countercyclical puffer… See paper

More subtle: better idiosyncratic risk sharing higher endogenous risk

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

The 2 Components of Systemic Risk

1. Systemic risk build-up during (credit) bubble … and materializes in a crisis – time-series

“Volatility Paradox” contemp. measures inappropriate

• Low VaR ⇒ low margins ⇒ high margins ⇒ high leverage ⇒ low risk-weights⇒ less capital ⇒ high leverage

• Shock leads to large adjustment• High VaR ⇒ …

Procyclicality• Countercyclical puffer… See paper

More subtle: better idiosyncratic risk sharing higher endogenous risk

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

The 2 Components of Systemic Risk

1. Systemic risk build-up during (credit) bubble … and materializes in a crisis – time-series• “Volatility Paradox” contemp. measures inappropriate

2. Spillovers/contagion – cross sectional• Direct contractual: domino effect – network

Network effects Bankruptcy of bank A

leads to default of B • 1st, 2nd, 3rd round effects• Random recovery rate

Data implications:• Position data• High frequency• High granularity

6

pre

ven

tive

cris

is m

anag

emen

t

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

The 2 Components of Systemic Risk

1. Systemic risk build-up during (credit) bubble … and materializes in a crisis – time-series• “Volatility Paradox” contemp. measures inappropriate

2. Spillovers/contagion – cross sectional• Direct contractual: domino effect - network• Indirect: price effect (fire-sale externalities)

credit crunch, liquidity spirals

• Adverse GE response amplification, persistence7

Loss of

net worth

Shock to

capital

Precaution

+ tighter

margins

volatility

price

Fire

sales

nonlinearity

pre

ven

tive

cris

is m

anag

emen

t

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Absorbers vs. amplifier

Shock absorber

Shock amplifier

Distributionexogenous endogenous

Direct Indirect

Contractual links “Virtual links”

Loss through bankruptcy/default

Similar exposurethan other levered players

Position data Response indicator- expectations/constraints

8Fat tail

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Absorbers vs. amplifier Response Indicator

Liquidity mismatch – not maturity mismatch

See Brunnermeier, Gorton & Krishnamurthy (2012)

A L

Micro-prudential Macro-prudential

Market Illiquidity exogenous depends on funding structure of other holders

Technological Illiquidity- Irreversibility

Market Illiquidity- Price Impact

Fund Illiquidity- Maturity- Haircut/margin sensitivity

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

From Risk in Isolation to Spillover RiskFrom 𝑉𝑎𝑅 to Δ𝐶𝑜𝑉𝑎𝑅

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

“Paradox of Prudence”

Fallacy of Composition in Risk Space

1. Keynes’ Paradox of Thrift

2. “Paradox of Prudence” Brunnermeier & Sannikov (Handbook chapter 2017)

• Each institution tries to reduce risk exposure (micro-prudent)

• Increases endogenous (systemic) risk (macro-imprudent) Liquidity spirals, fire-sales,…

Disinflationary spirals, …

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Overview

1. From Risk in Isolation to Systemic Risk• Volatility Paradox

• Direct Spillovers – domino effects

• Indirect Spillovers – amplifiers vs. absorbers

• Paradox of Prudence (becoming an amplifier)

2. From Separation Principles to Interlinkagesacross stability concepts• … and redistributive monetary policy

3. International: Safe assets and cross-border capital flowsFrom a Buffer Approach to a Rechanneling Approach

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Separation Principles Perspectives

Separation of task and accountability

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Interlinkages Perspectives

From YouTube video: “Money and Banking” by Markus.Economicus

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Interlinkages Perspectives

From YouTube video: “Money and Banking” by Markus.Economicus

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Interlinkages: MacroPru & MoPo

Liquidity spiral, fire sales

Disinflationary spiralEndogenous systemic risk

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Interlinkages: MacroPru & MoPo

In EME many MacroPru = MoPo measures

Inside money creation by private banks

Central bank balance sheet• Reserve holding due to liquidity regulation (LCR)

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

A L

Ris

ky C

laim

A LR

isky

Cla

im

The “I Theory of Money” Technologies 𝑏

…

Net worth

Inside Money(deposits)

A L

Outside Money Pass through

Ris

ky C

laim

Ris

ky C

laim

Ris

ky C

laim

Outside Money

Intermediaries• Can diversify within sector 𝑏

• Monitoring

• Create inside money

• Maturity/liquidity transformation

A L

𝐵1

Money

Ris

ky C

laim

Insi

de

equ

ity

A LA L

A LA L

𝐴1

Money

HH

Net

wo

rth

Technologies 𝑎

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Technologies 𝑏

A L

Ris

ky C

laim

A L

Shock impairs assets: 1st of 4 steps Technologies 𝑎

…

Net worth

Inside Money(deposits)

A L

Outside Money Pass through

Ris

ky C

laim

Ris

ky C

laim

Ris

ky C

laim

Losses

A L

𝐴1

Money

Ris

ky C

laim

Insi

de

equ

ity

𝐵1

A LA L

A LA L

𝐴1

Money

HH

Net

wo

rth

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Technologies 𝑏

Shrink balance sheet: 2nd of 4 steps

A

Technologies 𝑎

Inside Money(deposits)

…

Net worth

Inside Money(deposits)

A L

Pass through

Losses

Deleveraging Deleveraging

…

Ris

ky C

laim

Ris

ky C

laim

Ris

ky C

laim

Outside Money

Switch

A L

Ris

ky C

laim

A LA L

𝐴1

Money

Ris

ky C

laim

Insi

de

equ

ity

𝐵1

A LA L

A LA L

𝐴1

Money

HH

Net

wo

rth

“Paradox of Prudence”

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Technologies 𝑏

Liquidity spiral: asset price drop: 3rd of 4 Technologies 𝑎

A L

Ris

ky C

laim

A LA L

𝐴1

Money

Ris

ky C

laim

Insi

de

equ

ity

𝐵1

Inside Money(deposits)

Outside Money

…

Net worth

Inside Money(deposits)

A L

Pass through

Ris

ky C

laim

Ris

ky C

laim

Ris

ky C

laim

Losses

Deleveraging Deleveraging

A LA L

A LA L

𝐴1

Money

HH

Net

wo

rth

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

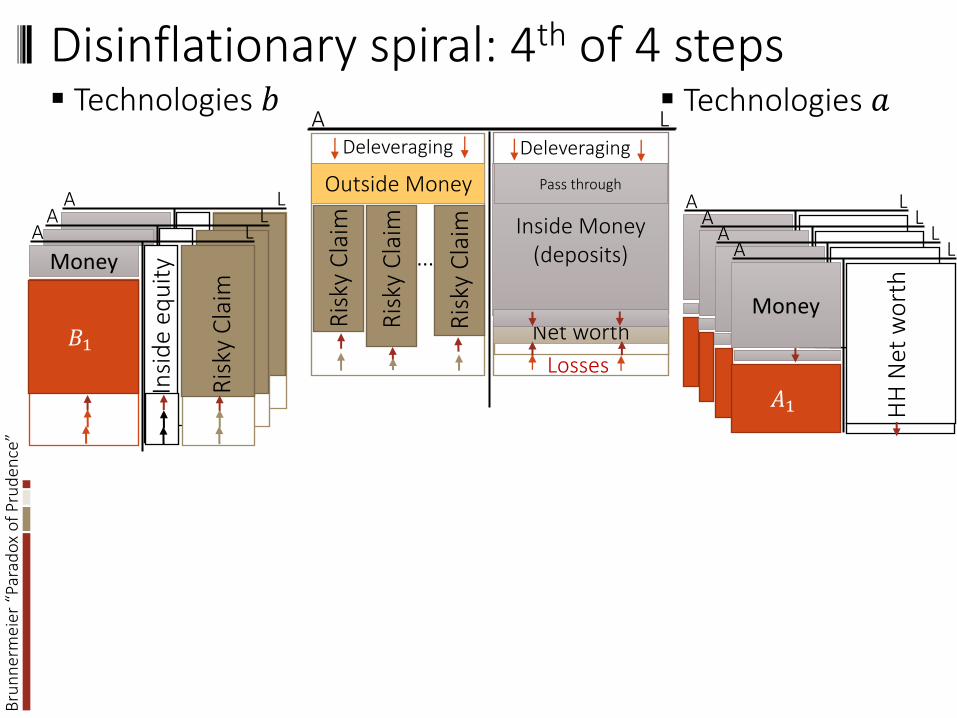

Technologies 𝑎 Technologies 𝑏

Disinflationary spiral: 4th of 4 steps

A LA L

A LA L

𝐴1

Money

HH

Net

wo

rth

A L

Ris

ky C

laim

A LA L

𝐴1

Money

Ris

ky C

laim

Insi

de

equ

ity

𝐵1

Inside Money(deposits)

Outside Money

…

Net worth

Inside Money(deposits)

A L

Pass through

Ris

ky C

laim

Ris

ky C

laim

Ris

ky C

laim

Losses

Deleveraging Deleveraging

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Redistributive MoPo: “I Theory of Money”

Monetary policy• Interest rate cut ⇒ long-term bond price • Asset purchase ⇒ asset price • ⇒ “stealth recapitalization” - redistributive• ⇒ risk premia

Liquidity & Deflationary Spirals are mitigated

…

Net worth

Inside Money(deposits)

A L

Reserves Pass through

𝑁𝑡

Long-term Bonds

Ris

ky C

laim

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Redistributive MoPo: “I Theory of Money”

Adverse shock Liquidity & Deflationary Spirals

Monetary policy• Interest rate cut ⇒ long-term bond price • Asset purchase ⇒ asset price • ⇒ “stealth recapitalization” - redistributive• ⇒ risk premia

Liquidity & Deflationary Spirals are mitigated

…

Net worth

Inside Money(deposits)

A L

Reserves Pass through

𝑁𝑡

Long-term Bonds

Ris

ky C

laim

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Redistributive MoPo: “I Theory of Money”

Adverse shock Liquidity & Deflationary Spirals

Monetary policy• Interest rate cut ⇒ long-term bond price • Asset purchase ⇒ asset price ⇒ “stealth recapitalization” - redistributive

⇒ Liquidity & Deflationary Spirals are mitigated

⇒ risk premia MoPo with risk premium focus

…

Net worth

Inside Money(deposits)

A L

Reserves Pass through

𝑁𝑡

Long-term Bonds

Ris

ky C

laim

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Redistributive MoPo: “I Theory of Money”

Adverse shock Liquidity & Deflationary Spirals

Monetary policy• Interest rate cut ⇒ long-term bond price • Asset purchase ⇒ asset price ⇒ “stealth recapitalization” - redistributive

⇒ Liquidity & Deflationary Spirals are mitigated

⇒ risk premia MoPo with risk premium focus

…

Net worth

Inside Money(deposits)

A L

Reserves Pass through

𝑁𝑡

Long-term Bonds

Ris

ky C

laim

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Difference to New Keynesian View

Consumption Boost approach to “Bottleneck approach”

(New) KeynesianDemand Management

I Theory of MoneyRisk (premium) management

Stimulate aggregate consumptionSubstitution effect

Alleviate balance sheet constraintsIncome/wealth effect

Woodford Tobin (1982) BruSan

Price stickinessPerfect capital markets

Both Financial FrictionsIncomplete markets

Representative Agent Heterogeneous Agents

Cut 𝑖Reduces 𝑟 due to price stickinessConsumption 𝑐 rises

Cut 𝑖Changes bond pricesRedistributes from low MPC to high MPC consumers

- -

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Difference to New Keynesian View

Consumption Boost approach to “Bottleneck approach” (New) Keynesian

Demand ManagementI Theory of Money

Risk (premium) management

Stimulate aggregate consumptionSubstitution effect

Alleviate balance sheet constraintsIncome/wealth effect

Woodford Tobin (1982) BruSan

Price stickinessPerfect capital markets

Both Financial FrictionsIncomplete markets

Representative Agent Heterogeneous Agents

Cut 𝑖Reduces 𝑟 due to price stickinessConsumption 𝑐 rises

Cut 𝑖Changes bond pricesRedistributes from low MPC to high MPC consumers

Cut 𝑖Changes asset pricesEx-post: Redistributesto balance sheet impaired sector

QE

- -

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Difference to New Keynesian View

Consumption Boost approach to “Bottleneck approach” (New) Keynesian

Demand ManagementI Theory of Money

Risk (premium) management

Stimulate aggregate consumptionSubstitution effect

Alleviate balance sheet constraintsIncome/wealth effect

Woodford Tobin (1982) BruSan

Price stickinessPerfect capital markets

Both Financial FrictionsIncomplete markets

Representative Agent Heterogeneous Agents

Cut 𝑖Reduces 𝑟 due to price stickinessConsumption 𝑐 rises

Cut 𝑖Changes bond pricesRedistributes from low MPC to high MPC consumers

Cut 𝑖Changes asset pricesEx-post: Redistributesto balance sheet impaired sector

QE- US: QE1 & QE3: MBS- Japan 1990: corporate bonds

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Difference to Monetarist View

Target broad money supply measure

When private/inside money creation contractsreplace “missing” inside money with outside money

Ignores that • Private financial institutions “diversify” some risk away• If these institutions contract – more risk in the system• Money demand rises

Outside vs. Inside money Inside money allows banks to diversify idiosyncratic risk Outside money doesn’t

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Difference to Monetarist View

Target broad money supply measure

When private/inside money creation contractsreplace “missing” inside money with outside money

Ignores that • Private financial institutions “diversify” some risk away• If these institutions contract – more risk in the system• Money demand rises

Outside vs. Inside money Inside money allows banks to diversify idiosyncratic risk Outside money doesn’t

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Interaction between MoPo & MacroPru

Redistributive MoPo insures ⇒ Moral Hazard

MacroPru complements MoPo• Not substitutes

Good MacroPru enables more aggressive MoPo• More redistribution ex-post

• More risk-transfers/insurance ex-ante

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Overview

1. From Risk in Isolation to Systemic Risk• Volatility Paradox

• Direct Spillovers – domino effects

• Indirect Spillovers – amplifiers vs. absorbers

• Paradox of Prudence (becoming an amplifier)

2. From Separation Principles to Interlinkagesacross stability concepts• … and redistributive monetary policy

3. International: Safe assets and cross-border capital flowsFrom a Buffer Approach to a Rechanneling Approach

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Safe assets

“Good friend analogy” - like reserve assets

• Safe/available at any horizon - “when it counts”

• Precautionary buffer held in addition to more risky assets

Risk ⇒ demand for safe assets

“Safe asset tautology”• safe because it is “perceived to be safe”

• safe independent of fundamentals US Treasury downgrade

by S&P in 2011 ⇒ yield

German CDS spread ⇒ yield during Euro crisis

• Multiple equilibria

• Bubble

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Safe assets

“Good friend analogy” - like reserve assets

• Safe/available at any horizon - “when it counts”

• Precautionary buffer held in addition to more risky assets

Risk ⇒ demand for safe assets

Pool ofRisky assets

Safe asset

Deposits

Equity

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Safe assets

“Good friend analogy” - like reserve assets

• Safe/available at any horizon - “when it counts”

• Precautionary buffer held in addition to more risky assets

Risk ⇒ demand for safe assets

“Safe asset tautology”• safe because it is “perceived to be safe”

• safe independent of fundamentals US Treasury downgrade

by S&P in 2011 ⇒ yield

German CDS spread ⇒ yield during Euro crisis

• Multiple equilibria

• Bubble37

Pool ofRisky assets

Safe asset

Deposits

Equity

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Flight to Safety

Risk-on, Risk-off Flight to safe asset

If asymmetrically supplied by AE

Flight to safety cross-border capital flows

Who insures whom? (rich the poor?)• At times of global crisis issue new debt

- for AE: at inflated prices

- for EME: at depressed prices

• Question: is buffer large (long-term) enough s.t. no new debt issuance needed & sale off safe asset

38

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Flight to Safety

Risk-on, Risk-off Flight to safe asset

If asymmetrically supplied by AE

Flight to safety cross-border capital flows

Who insures whom? (rich the poor?)• At times of global crisis issue new debt

- for AE: at inflated prices

- for EME: at depressed prices

• Question: is buffer large (long-term) enough s.t. no new debt issuance needed & sale off safe asset

39

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Flight to Safety

Risk-on, Risk-off Flight to safe asset

If asymmetrically supplied by AE

Flight to safety cross-border capital flows

At times of global crisis, issuance of new debt• For US at inflated prices eases conditions

• For EME at depressed prices worsens conditions

Question: Who insures whom? (rich the poor OR poor the rich?)

• “Correct” insurance only if buffer is large (and debt long-term) enoughso that no new debt issuance needed & sale off safe asset 40

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Different Approaches to Counter Risks

Buffer Approach (public)

IMF Facilities Approach

Swapline Approach

Rechanneling Approach

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Different Approaches to Counter Risks

Buffer Approach (public)

IMF Facilities Approach

Swapline Approach

Rechanneling Approach

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Buffer Approach

Buffers (public) more private imbalances

• Irrelevance theorem in BruSan2017 “International Monetary Theory: Mundell-Fleming Redux”

• International banks approach central bank as Lender of Last Resort in a Foreign Currency New additional rationale for Central Banks’

foreign reserve (safe asset) holding (in dollar)

Moral Hazard problem: banks hold fewer safe asset (in dollar) and rely on LOLR of CB

43

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Rechanneling Approach

Buffers (public) more private imbalances

Rechannel away from cross-border capital flows

4444

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Rechanneling Approach

Buffers (public) more private imbalances

Rechannel away from cross-border flows

• With ESBies in Europe (SBBS = sovereign backed securities)

4545

sovereign bonds ESBies

Junior Bond

A L

Poo

ling

Tran

chin

g

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Global Safe Asset (GSA) - without a Passport

46

Rechannel flight to safety via GloSBBieS (Global SBBS)• Now, GSA junior bond

• Difference to ESBiesjunior bond also has to absorb currency risk

Both are internationalShift to a new equilibrium

Sovereign Bonds (+ currency swap)

GSA in $

Junior Bond in $

A L

Poo

ling

Tran

chin

g

Bru

nn

erm

eier

“Pa

rad

ox

of

Pru

den

ce”

Conclusion

1. From Risk in Isolation to Systemic Risk• Volatility Paradox

• Direct Spillovers – domino effects

• Indirect Spillovers – amplifiers vs. absorbers

• Paradox of Prudence (becoming an amplifier)

2. From Separation Principles to Interlinkagesacross stability concepts• … and redistributive monetary policy

3. International: Safe assets and cross-border capital flowsFrom a Buffer Approach to a Rechanneling Approach• Global Safe Asset - GloSBBS