Pandox redovisning av affärsverksamheten 2010

92

ONE OF THE LEADING HOTEL PROPERTY COMPANIES IN EUROPE Pandox Report on business operations 2010

-

Upload

pandox -

Category

Real Estate

-

view

130 -

download

18

description

Pandox - Ett av de ledande hotellfastighetsbolagen i Europa

Transcript of Pandox redovisning av affärsverksamheten 2010

o n e o f t h e l e a d i n g

h o t e l p r o p e r t y c o m pa n i e s i n e u r o p e

Pandox Report on business

operations2010

The Company

The Business model . . . . . . . . . . . . . . . . . . . 2

The Development . . . . . . . . . . . . . . . . . . . . . 4

Success factors . . . . . . . . . . . . . . . . . . . . . . 6

Strategy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Value-growth . . . . . . . . . . . . . . . . . . . . . . 10

Types of agreements . . . . . . . . . . . . . . . . 10

Business processes . . . . . . . . . . . . . . . . 11

Success stories . . . . . . . . . . . . . . . . . . . . . . 12

Operated by Pandox . . . . . . . . . . . . . . . . . . 14

Market communication . . . . . . . . . . . . . . . . 15

Hotel property market . . . . . . . . . . . . . . . . . 16

Pandox’ hotels and partners . . . . . . . . . . . . .18

Hotel properties

List of hotel properties . . . . . . . . . . . . . . . . . 40

Other information

CEO commentary 2010 and ahead . . . . . . . 44

Board of Directors and auditors . . . . . . . . . . 48

Senior managers and executives . . . . . . . . . 50

Team Pandox . . . . . . . . . . . . . . . . . . . . . . . . 52

Finances

Financial overview . . . . . . . . . . . . . . . . . . . . 58

Sensitivity analysis . . . . . . . . . . . . . . . . . . . . 62

Valuation and fiscal situation . . . . . . . . . . . . 64

Definitions . . . . . . . . . . . . . . . . . . . . . . . . . . 65

Ten-year overview . . . . . . . . . . . . . . . . . . . . 66

Quarterly data 2009–2010 . . . . . . . . . . . . . . 68

Financial statements 2010

Report of the Board of Directors . . . . . . . . . 70

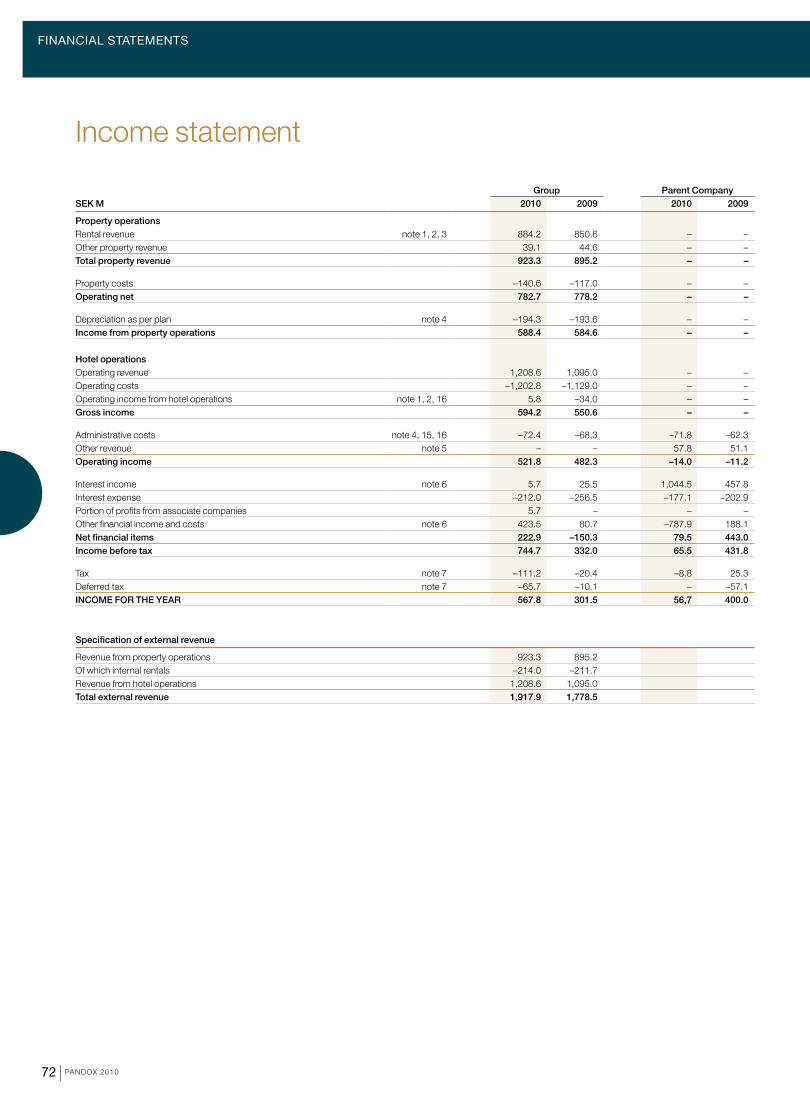

Income statement and comments . . . . . . . . 72

Balance sheet and comments . . . . . . . . . . . 74

Changes in equity . . . . . . . . . . . . . . . . . . . . 76

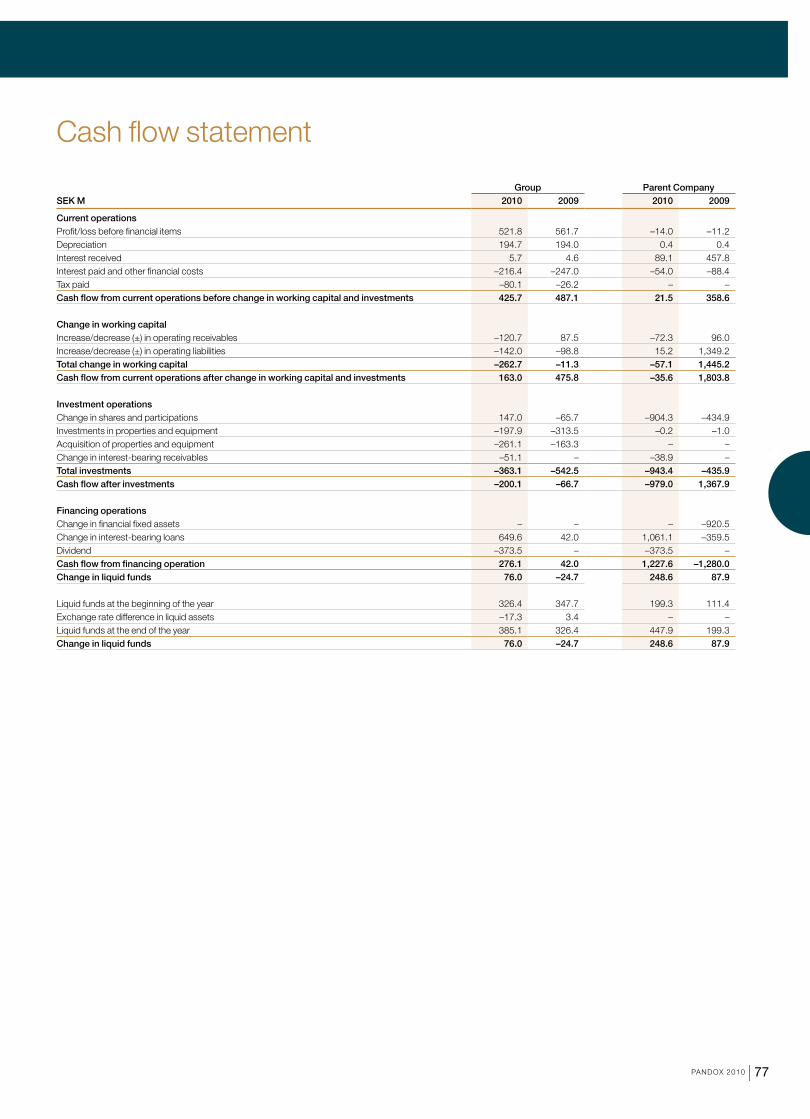

Cash flow statement . . . . . . . . . . . . . . . . . . 77

Accounting principles . . . . . . . . . . . . . . . . . . 78

Notes to the accounts . . . . . . . . . . . . . . . . . 79

Proposed disposition of earnings . . . . . . . . . 84

Auditors’ report . . . . . . . . . . . . . . . . . . . . . . 85

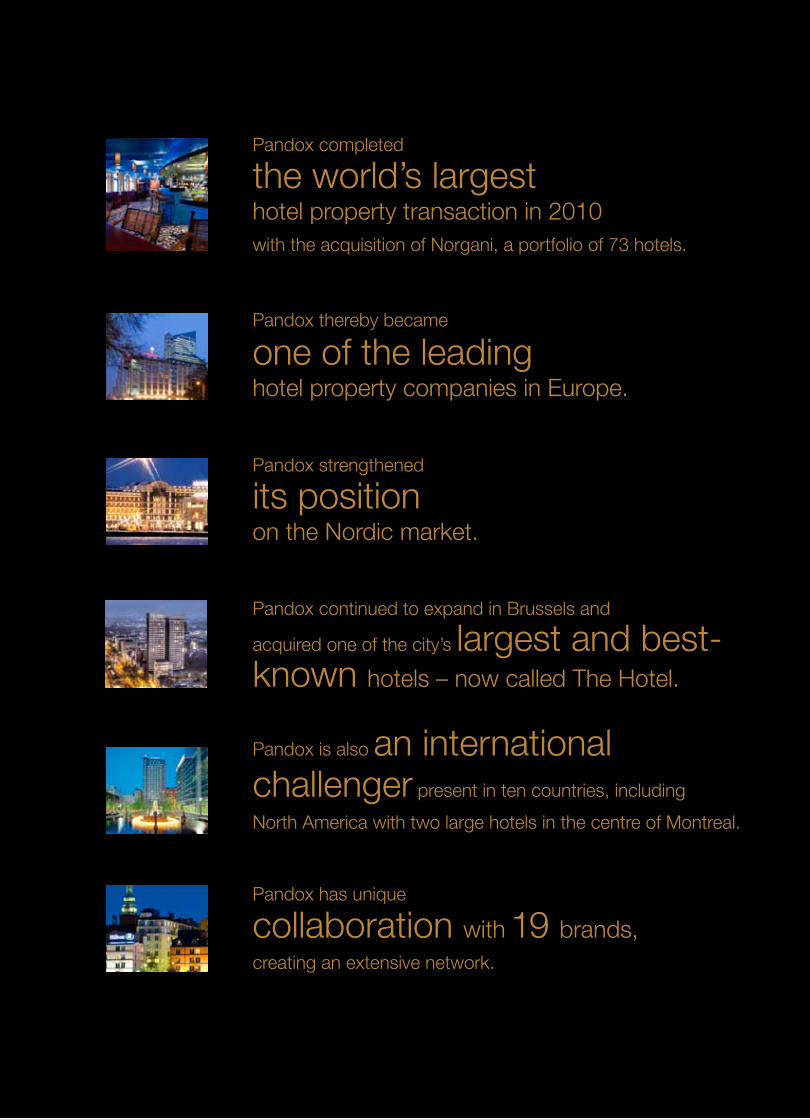

Pandox completed

the world’s largest hotel property transaction in 2010

with the acquisition of Norgani, a portfolio of 73 hotels .

Pandox thereby became

one of the leadinghotel property companies in Europe .

Pandox strengthened

its position on the Nordic market .

Pandox continued to expand in Brussels and

acquired one of the city’s largest and best- known hotels – now called The Hotel .

Pandox is also an international challenger present in ten countries, including

North America with two large hotels in the centre of Montreal .

Pandox has unique

collaboration with 19 brands, creating an extensive network .

4read more on page

Success factors

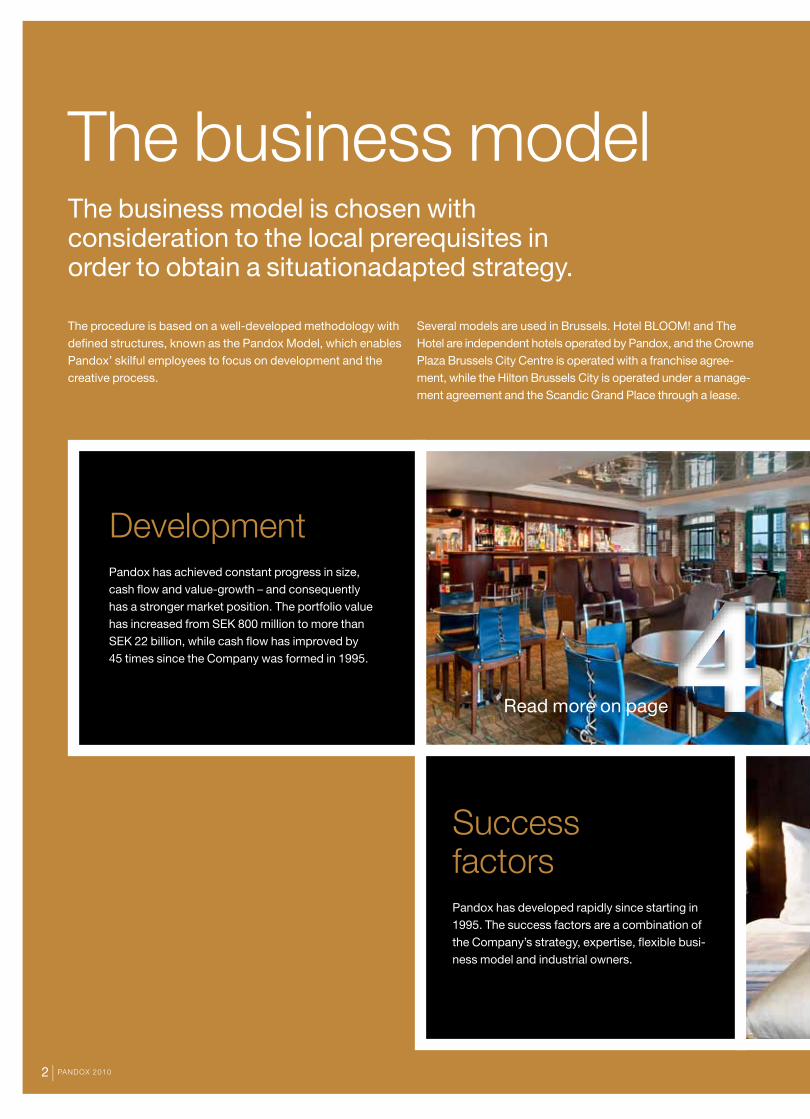

the business model is chosen with consideration to the local prerequisites in order to obtain a situationadapted strategy.

pandox has developed rapidly since starting in 1995. the success factors are a combination of the company’s strategy, expertise, flexible busi-ness model and industrial owners.

Developmentpandox has achieved constant progress in size, cash flow and value-growth – and consequently has a stronger market position. the portfolio value has increased from seK 800 million to more than seK 22 billion, while cash flow has improved by 45 times since the company was formed in 1995.

The business model

the procedure is based on a well-developed methodology with defined structures, known as the pandox model, which enables pandox’ skilful employees to focus on development and the creative process.

several models are used in Brussels. hotel Bloom! and the hotel are independent hotels operated by pandox, and the crowne plaza Brussels city centre is operated with a franchise agree-ment, while the hilton Brussels city is operated under a manage-ment agreement and the scandic grand place through a lease.

2 | PANDOx 2010

8read more on page

Knowledge, network and individual capital

Consistent strategy

one of pandox’ most important cornerstones is to constantly develop the company’s expertise and competences. in order to inspire our employees, an informal leadership style has been devel oped to give each individual considerable freedom and development opportunities. the corporate culture includes an interactive discussion with an extens-ive network, which provides valuable input in both large and small issues.

pandox has a well-defined strategy that is thoroughly embodied with the Board of directors, senior executives and banks – a strategy that has been consistently followed since the company was formed 15 years ago. the point of departure is to acquire under-performing large hotels in strong loca-tions, where the company’s specialist exper-tise can be used to develop the assets. this in turn creates prerequisites for long-term value development and a strong company.

6read more on page

PANDOx 2010 | 3

201814

2831

46*

*hot

ellu

s fö

rvär

vas

med

16

hote

llfas

tighe

ter.

46 44

267266

228

119

97

53

2112

Pandox’ development 1995–2010 Number of hotels

Cash flow SEK M

45

299

272

The DevelopmentFrom financial crisis to successful hotel property company

When Pandox started in 1995, the company consisted of 18 hotels with 3,000 rooms located in nine

swedish towns and cities. the business model was new and untried. the company had weak profita b-

ility and limited capital.

The road to success has since gone via transactions embracing 170 hotel properties to a total value

of seK 20 billion. With a consistent strategy, pandox has shown durable and profitable growth, along

with a greater geographic spread.

At the end of 2010, pandox had 120 hotels with a total of 24,800 rooms

located in 59 towns and cities in 10 different countries in the nordic region,

the rest of europe, and north america. pandox thereby is one of the

leading hotel property companies in the european market.

Acquisitions totalling SEK 20 billion .Founded in 1995. Pandox has its origins in the financial and property crisis

in the beginning of the 1990s . The Company was formed in 1995 by Secu-

rum and Skanska . The mission was to take over and restructure the hotel

portfolio, and prepare it for sale .

The original hotel property portfolio. In the beginning, Pandox consisted

of 18 hotel properties and three small operating units . All of the hotels were

in Sweden, and most of them were small with weak locations and in poor

condition .

Stock-exchange listing. Pandox was floated on the Stockholm Stock

Exchange in 1997 with a new and untried business concept . The Company’s

portfolio was valued at SEK 1 .3 billion and the market capitalisation was SEK

520 million . The listing gave 4,000 new shareholders .

Further to the listing, Pandox expanded substantially with acquisitions of

large hotels in strong locations, while smaller hotels were sold .

Internationalisation. In 2000, Pandox enlarged its geographical strategy to

northern Europe through the acquisition of Hotellus with 16 hotel properties .

Privatised again in 2004. Pandox is bought out from the stock market in

2004, with new industrial owners through Eiendomsspar AS and Sundt AS .

44

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 20101990 – Swedish financialand property crisis

1999/2000 IT and financial crisis

* acq

uisi

tion

of h

otel

lus

with

16

hote

ls.

4 | PANDOx 2010

120*

46

39

445 446

389

318

301

Average annual return

19%

Transactions covering 170 hotels .Stronger in Europe. The transaction tempo increased further to the privat-

isation, and several large hotels were acquired in Berlin, Brussels, Basel,

Copenhagen, Stockholm and Malmö – thus strengthening Pandox as one

of the leading hotel property players in Europe .

Expansion to North America. In 2007–2008, Pandox continued its inter-

national expansion with two acquisitions in Montreal .

Leading in Europe. In August 2010, Pandox announced the acquisition

of Norgani Hotels with a portfolio of 73 hotels in Sweden, Finland, Norway

and Denmark .

Further to the acquisition, Pandox became one of the leading pure hotel

property companies in Europe with regard to geographic spread and number

of hotels and brands . Since starting in 1995, Pandox has carried out acquisi-

tions for a total of SEK 20 billion representing transactions of 170 hotels .

The value of the Company’s hotel property portfolio amounts to approxi-

mately SEK 22 billion further to the acquisition of Norgani – which implies

that the value has increased about 20 times . This has been achieved

through a good hotel market, active ownership, sound expertise and

profitable acquisitions .

Key indicators 2010Pandox proforma including Norgani (before acquisition costs)

Mkr 2010

Number of hotels 120Number of hotel rooms 24,800Property revenues, SEK M 1,700Cash flow, SEK M 700

36*

44 45

700

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

2007/2008 Global finance crisis

* a

cqui

sitio

n of

nor

gani

with

73

hote

ls.

* sal

e of

12

hote

ls to

nor

gani

.

PANDOx 2010 | 5

Expertise and network

Success factors

pandox has a small management organisation, and all members are based at the office in stockholm. in addition, one of the company’s exec-utives is based in Brussels where the largest operational activities are located. the model provides major benefits with rapid decision-making paths, a high level of interactivity, and

considerable individual freedom. in order to maintain all business proc-esses in motion, the organisation is supplemented by a national and inter-national network composed of people with specialist expertise within mar-ket, management, hotel operations, property development, brand names, finance and taxes. pandox works

actively to attract people into the net-work, which is a precondition for the company’s rapid growth. the model places demands on both visionary and operative leadership, as well as an ability to create forms of collabora-tion with individuals with different backgrounds.

International network provides access to unique expertise

Depending on local prerequisites, Pan-dox is able to choose between four operational strategies: through leases with professional operators where Pan-dox remains as a strategic partner; man-

agement agreements where a partner runs the daily operations on behalf of Pandox; by managing one’s own opera-tions through a franchise agreement under a well-known brand or via an inde-

pendent distribution system . The busi-ness model provides excellent opportu-nities to create a situation-adapted strat-egy “asset by asset” .

Flexible business model

Pandox’ shareholders and Board of Directors possess industrial expertise in the Company’s three most important areas: hotel operations, properties and business development . Their knowledge and experience create confidence, which enables us to take rapid decisions within, for example, different acquisition questions . This is a competitive advantage in a significantly slower surrounding world .

Short and rapid decision-making paths

Well-defined and consistent strategyPandox has a well-defined strategy within geography, types of hotel and yield require-ments that have been consistently followed since the Company was formed .

clarion collection hotel Bastion, oslo

6 | PANDOx 2010

The hotel property portfolio is of very high quality . The hotels are located in international and dynamic markets such as London, Brussels, Berlin, Stockholm, Copenhagen and Montreal as well as locations with a high pro-portion of domestic demand, which creates balance in revenues . The hotels have strong locations and are the right size, which provides a critical mass as well as being marketed by the sector’s most prominent brand names . The agreement structure with a combination of leases, management agree-ments and own operations provides good potential with limited risk .

Choice of countries and locationsPandox is establishing in major hotel markets that have good potential and stable demand .

Pandox actively seeks strategic alliances with strong brand names that have an interest in forming a partnership that creates benefits for both par-ties . Pandox currently works with 11 partners under 19 brands .

Acquisition strategy

Portfolio of the highest quality

Strategic alliances

pandox primarily acquires hotels with a potential that can be brought out through active measures and where the compa-ny’s areas of expertise can be utilised.

hyatt regency, montreal

Corporate culture

Pandox Spiritpandox has established an informal leadership style where a high level of expertise is combined with minimum bureaucracy and effective monitoring methods. the catchwords are inspira-tion, simplicity, rapidity, expertise and visible leadership.

PANDOx 2010 | 7

Geographical spread, proportion of hotel rooms

Revenue-based lease, 34%

Franchise agreement, own operation, 4%

Own operation, 5%

Revenue-based lease with guarantee, 52%

Management agreements, own operation, 4%

Other, 1%

Sweden, 51%

International, 49%

Lease structure – Rental revenues

corner-stones in pandox’ strategy

Strategyconsistent strategy enables stability and the spreading of risk

One type of asset – hotel properties

A hotel property has distinctive features

and differs from other types of property,

which demands specialist expertise to be

able to maintain active and successful

ownership . Pandox therefore invests in

just one type of asset: hotel properties .

Business position: Pandox has

120 hotels with a total of 24,800 rooms .

Agreement structure

To maximise value-growth in each hotel

requires a flexible business model that creates

opportunities for a situation-adapted strategy .

Business position: Pandox has a structure

that embraces leases, management agree-

ments, franchise agreements, as well as agree-

ments with independent players . The largest

portion concerns leases, which cover 87

percent of revenues .

Geographical market

Focusing on one type of asset requires a

broad geographic market so as to create

growth prerequisites and be able to benefit

from changes in the hotel economic cycle .

Business position: Pandox is currently

located in ten countries, of which Sweden is

the largest market . Major markets outside the

domestic market are Brussels, Copenhagen,

Helsinki and Montreal . Pandox is represented

in 59 locations that have a mix of national and

international demand .

scandic Kramer, malmö

8 | PANDOx 2010

Pandox’ vision is to be one of the world’s leading hotel property companies with regard to special-ist expertise in both hotel and property opera-tions, and active ownership.

for the vision to become reality, the company must retain its

specialist expertise regarding the value-growth chain, and that

the balance between international and national revenues, brand

names and types of hotel are maintained. another important

aspect is to constantly develop the business model so as to

adapt to each situation and choose the best strategy in relation

to local conditions.

Business concept and strategy

pandox’ business concept, based on expertise within hotel

properties, hotel operations and business development, is to

actively own, develop and lease out hotel properties.

Overall goal

pandox’ overall goal, through specialist expertise within hotels,

hotel properties and business development, is to achieve optimal

yield and value-growth in the hotel property portfolio. specific

goals are set each year for the operating net, return on investment,

value-growth in the existing hotel property portfolio, and the

equity/assets ratio. the goals are then broken down to each indi-

vidual property and act as guidance upon investment decisions.

Location and size

Large hotels with strong locations increase

potential and reduce risks, and are attrac-

tive for both partners and guests . Such

hotels have higher liquidity and are easier

to finance .

Business position: All Pandox hotels

have strong locations with an average size

of 207 rooms, which is significantly larger

than the average hotel in Europe .

Type of hotel

The hotels shall belong to the upper-

medium and high-price segment .

Business position: The portfolio contains

a mix of upper medium and high-priced

hotels . Examples of upper medium-priced

hotels include many Scandic hotels as

well as the Hotel Berlin, Berlin . High-priced

hotels include InterContinental Montreal

and Hilton Stockholm Slussen .

Choice of brand names and partners

Each hotel shall have the best possible brand

name that strengthens the profile . This requires

that Pandox maintains a broad network with

national and international hotel companies .

Business position: Pandox currently works with

11 partners under 19 well-known brand names,

as well as a number of independent distribution

channels, thus providing a unique position and

extensive network .

hotel Berlin, Berlinradisson Blu hotel, Basel

PANDOx 2010 | 9

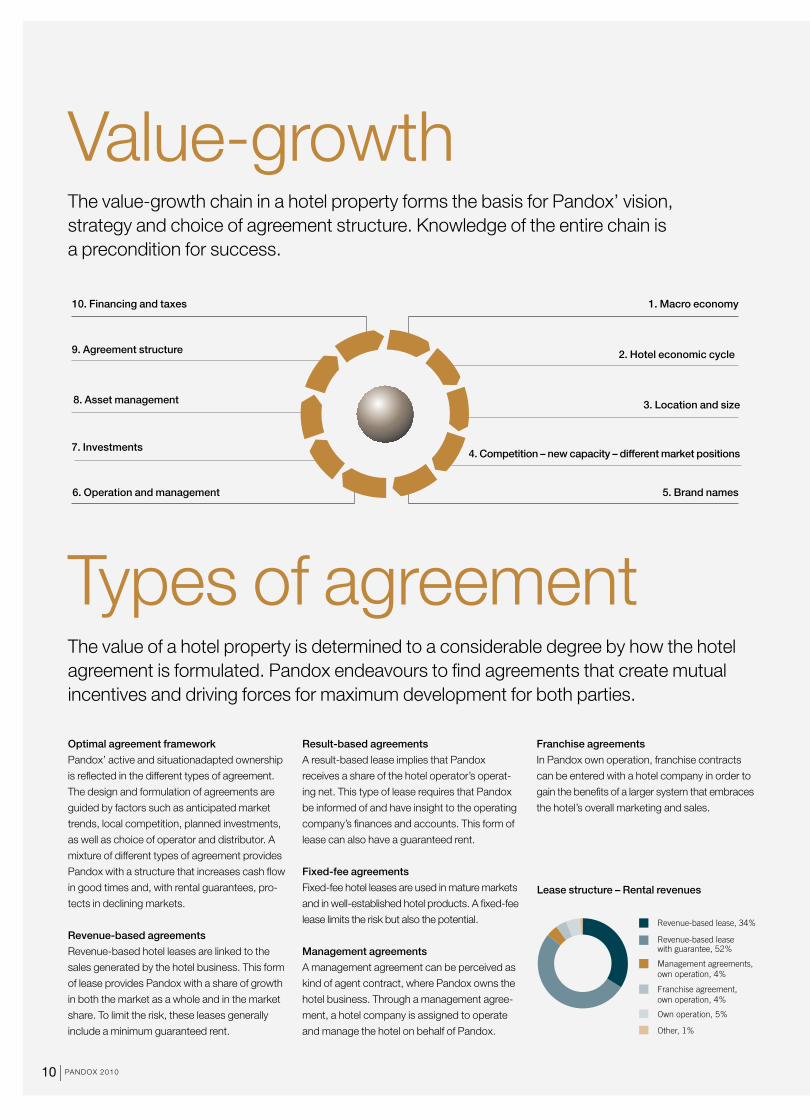

Value-growth

1. Macro economy

2. Hotel economic cycle

3. Location and size

4. Competition – new capacity – different market positions

5. Brand names

10. Financing and taxes

9. Agreement structure

6. Operation and management

8. Asset management

7. Investments

The value-growth chain in a hotel property forms the basis for Pandox’ vision, strategy and choice of agreement structure . Knowledge of the entire chain is a precondition for success .

The value of a hotel property is determined to a considerable degree by how the hotel agreement is formulated . Pandox endeavours to find agreements that create mutual incentives and driving forces for maximum development for both parties .

Types of agreement

Optimal agreement framework

Pandox’ active and situationadapted ownership

is reflected in the different types of agreement .

The design and formulation of agreements are

guided by factors such as anticipated market

trends, local competition, planned investments,

as well as choice of operator and distributor . A

mixture of different types of agreement provides

Pandox with a structure that increases cash flow

in good times and, with rental guarantees, pro-

tects in declining markets .

Revenue-based agreements

Revenue-based hotel leases are linked to the

sales generated by the hotel business . This form

of lease provides Pandox with a share of growth

in both the market as a whole and in the market

share . To limit the risk, these leases generally

include a minimum guaranteed rent .

Result-based agreements

A result-based lease implies that Pandox

receives a share of the hotel operator’s operat-

ing net . This type of lease requires that Pandox

be informed of and have insight to the operating

company’s finances and accounts . This form of

lease can also have a guaranteed rent .

Fixed-fee agreements

Fixed-fee hotel leases are used in mature markets

and in well-established hotel products . A fixed-fee

lease limits the risk but also the potential .

Management agreements

A management agreement can be perceived as

kind of agent contract, where Pandox owns the

hotel business . Through a management agree-

ment, a hotel company is assigned to operate

and manage the hotel on behalf of Pandox .

Franchise agreements

In Pandox own operation, franchise contracts

can be entered with a hotel company in order to

gain the benefits of a larger system that embraces

the hotel’s overall marketing and sales .

Revenue-based lease, 34%

Franchise agreement, own operation, 4%

Own operation, 5%

Revenue-based lease with guarantee, 52%

Management agreements, own operation, 4%

Other, 1%

Lease structure – Rental revenues

10 | PANDOx 2010

Business processes

Market analysisA market analysis is performed in order to assess a hotel’s prof-itability potential and subsequent ability to pay the agreed rent . The local market is identified and analysed with regard to demand, competition and the current and future supply .

Market strategyA strategic plan for each hotel property is established based on the respective hotel’s specific prerequisites, the local market, and its position in the hotel eco-nomic cycle . The property’s con-tinued area of use is uncondi-tionally evaluated while prepar-ing the strategic plan .

Profitability optimisationIn view of that the value of a prop-erty is influenced by the profitabil-ity of the related hotel operations, the operator is Pandox’ most important partner . The hotel operator is constantly assessed in order to ensure positive devel-opments of the hotel’s operations and the value of the property .

Agreement optimisationThe optimal cash flow of each respective hotel property is divided between the operator, Pandox and other related parties . Each agreement is formulated in such a way that all parties involved are given an incentive to continuously improve the hotel property’s overall profitability .

The Pandox Model – and its four phases

Possibility to acquire a hotel property

Action plan with concrete measures

Evaluation of each respective hotel property and the portfolio

market analysis market strategy profitability optimisation

agreement optimisation

sales in accordance with the strategy

Pandox’ five business processes are implemented to describe the business position, the external and internal driving forces, and how these interact with each other .

Market survey

Gains knowledge of the market situation and change-pattern.

2The Pandox Model

the company’s working methodology increases cash flow and limits the risk

for each respective hotel.

Asset managementDaily management plus major invest-

ments with the objective of increasing the value of the properties in the long-term.

Economic and financial reporting

Operations are monitored through estab-lished goals, evaluations and valuations.

Market communication

Pandox regularly performs marketing activities towards target groups.

3

5

1

4

PANDOx 2010 | 11

Pandox has developed a large number of hotel properties and hotel operations during the years . A selection of the past years’ successful repositioning and ongoing projects are here presented .

Crowne Plaza Brussels City Centre was

acquired in 2003, and has for several years been

one of Brussels’ business and meeting hotels –

and indeed continues to strengthen its market

position year after year . The hotel, which has

received several international awards, has the

vision of becoming Brussels’ best meeting hotel

in the city centre .

Holiday Inn Brussels Airport

Vision – the best!Holiday Inn Brussels Airport was acquired in 2006 when the hotel required substantial

refurbishment and development . With the vision of creating the best upper-medium-

priced hotel in the area, the change process has been successfully implemented based

on the catchwords of full service, attractive design and high efficiency .

Crowne Plaza Brussels City Centre

Established in Brussels

Investment program: eur 8 millionAccomplished: completely new design for rooms and lobby, new meeting concept, upgrading of general facilities and major organisational development.

Investment program: cad 7.5 million Accomplished: modernisation and improvement of the banqueting hall and other meeting areas.

Investment program: eur 15 millionAccomplished: repositioning towards the meeting segment with new concept called “Balanced senses”. upgrading of all rooms, as well as new restaurant and bar concept in a classic environment.

Investments in developm ent and repositioning

12 | PANDOx 2010

Investments in developm ent and repositioning

Pandox acquired the InterContinental Mon-

treal in the summer of 2007 . Extensive devel-

opment work has since created a completely

new hotel concept – and reactions have been

nothing less than fantastic with several dis-

tinctions and awards . Work is now continuing

with the vision of becoming RevPAR-leader in

Montreal .

pandox acquired the hyatt regency montreal

in the summer of 2008, and is now investing

in the vision of creating montreal’s best

meeting and festival hotel. and the hotel is

well on the way to becoming outstanding!

the first stage is already completed with the

upgrading of the hotel’s large banqueting

hall and other meeting rooms. Work is now

continuing with the upgrading of the

reception and lobby.

Investment program: cad 14 million Accomplished: new management, new profile and design in all rooms and the lobby, new f&B offer.

SuCCESS STORIES

Pandox acquired the hotel in 2005, which at the

time was considered to be one of the city’s abso-

lutely poorest hotels . During more than two

years, the hotel was refurbished, upgraded and

developed, and a new concept was produced .

Hotel BLOOM! is a unique hotel with a completely

own concept based on art and design . It has

become a challenger in the Brussels hotel market

and now competes with the major hotels .

Hotel BLOOM!, Brussels

Talk of the town

Investment program: eur 13 millionAccomplished: repositioning, upgrading and development of the entire hotel. new management, new concept and new name.

Since acquiring the hotel in 2006, Pandox has

created the meeting place of the future in one of

the city’s largest hotels . Extensive re-profiling has

moved the Hotel Berlin, Berlin back to the top –

and is now established as one of the leading

meeting hotels, as well as one of Berlin’s most

creative meeting places .

Hotel Berlin, Berlin

Meeting place

Investment program: eur 10 million Accomplished: modernisation and improvement of all rooms and meeting product, as well as facade, entrance and lobby. new market profile and new management.

Hyatt Regency Montreal

Outstanding!

InterContinental Montreal

Business and pleasure

PANDOx 2010 | 13

Hotels operated by Pandox

City Hotel Brand name No. rooms Location

Berlin Hotel Berlin, Berlin Independent hotel 701 CentralMontreal Hyatt Regency Hyatt Regency 605 Central InterContinental Montreal InterContinental 357 City centreBrussels Crowne Plaza Brussels City Centre Crowne Plaza 354 City centre Hotel BLOOM! Independent hotel 305 Central Hilton Brussels City Hilton 283 City centre The Hotel Independent hotel 4334 City centre Holiday Inn Brussels Airport Holiday Inn 310 AirportAntwerp Crowne Plaza Antwerp Crowne Plaza 264 CentralBahamas Pelican Bay Independent hotel 184 Central

Operatedby Pandox

A natural part of Pandox’ active ownership is to operate its own hotels . Depending on the local prerequisites, the best strategy can be to develop operations oneself, and to choose another solution at a later stage . This creates a situation adapted strategy – hotel by hotel .

Another reason is that business cultures vary

among different geographical areas . In the

Nordic region, leases dominate while in North

America the most common form is manage-

ment and franchise agreements . Europe has a

mixture of both . It is therefore important to com-

mand different strategies in order to successfully

operate in an international hotel environment .

Having one’s own operational competence also

implies possessing specialist knowledge to

evaluate the hoteloperators, and be able to

carry out acquisitions that include both the

property and operating company .

Further to the growing industry trend of hotel

companies becoming management companies,

it is also natural for Pandox to integrate vertically

and take over operational responsibility .

At the end of 2010, Pandox’ operating com-

panies, including management agreements,

embraced ten hotels with total revenues of SEK

1 .2 billion – located in Berlin, Brussels, Antwerp,

Montreal and the Bahamas .

In recent years, four of the operations that had

been acquired as under-performers and there-

after redeveloped, were leased with long-term

agreements to well-known operators . In turn,

this created prerequisites for new acquisitions .

The philosophy behind Pandox’ operating

companies is to build up each hotel’s strategy

and competence locally . This implies that the main

part of decision-taking is delegated, and report-

ing is made to a board of directors with, normally,

external members who are elected for their spe-

cialist expertise . To be successful with the busi-

ness processes requires an ability to attract the

best management, and that such persons be

given substantial influence over operations .

crowne plaza Brussels city centre

holiday inn Brussels airport

hotel Bloom!, Brussels

hilton Brussels city

the hotel, Brussels

crowne plaza antwerp

hotel Berlin, Berlin

hyatt regency montreal

intercontinental montreal

pelican Bay, Bahamas

14 | PANDOx 2010

Marketcommunication

Pandox organises a Hotel Market Day each year, where current topics that affect the industry and sector are pre-sented and discussed . The event has been held every year since 1997 and interest is constantly growing . Recent years have seen a full house with around 300 people taking part, of which a large part is composed of international guests .

The Hotel Market Day is a dynamic meeting

place where hotel owners, operators, hotel

companies, banks, public opinion lobbyists,

construction companies, politicians and media

come together . They can listen to interesting

presentations that increase knowledge and

insight about the hotel sector’s conditions, and

are given the opportunity to network and obtain

a forecast and prognosis for next year . The

evening always closes with a dinner in a pleas-

ant and relaxed environment . The event is held

in November at the Hilton Stockholm Slussen,

which apart from being owned by Pandox is a

conference hotel of the highest class . In recent

years, themes taken up have included the effect

of low-price airlines on the hotel industry, the

significance of shopping tourism for a destina-

tion, as well as the signification of the term

“brand profitability” and the business models it

offers . The themes for 2010 were the economic

situation and its consequences for the hotel

industry, as well as social media and their effect

on the sector .

The speakers are top-quality . In November

2010, we had the honour of presenting Simon

Johnson, Director EMEA from CBRE Hotels,

Jan Tissera, CEO of TravelClick International,

and Hermine Coyet Ohlén, Chief Editor of

Swedish Elle . Staffan Olsson, well-known hand-

ball profile and Swedish national handball team

manager and Stefan Lövgren, handball icon and

expert commentator for TV4, were also there

and talked about the Handball World Champi-

onship 2011 – a mega event .

Regular information about market trends and acquisitionsWhen Pandox was formed in 1995, the

publication of a newsletter was started in

order to market the Company vis-à-vis the

capital market prior to being listed on the

stock exchange . The newsletter later was

replaced by the public reports distributed

by the Company . In spite of Pandox no

longer being listed on the Stockholm Stock

Exchange, the flow of information was

maintained to people interested in the hotel

sector and the hotel property market,

which is why Pandox upgrade is still

regularly issued . The newsletter contains

topics such as market trends and current

Swedish and international hotel market

questions .

Welcome as a subscriber

Pandox upgrade is free of charge and may

be ordered from Pandox either by tele-

phone at +46 (0)8-506 205 50 or by send-

ing an email to pandox@pandox .se

Pandox upgrade is also available on

www .pandox .com

PANDOx 2010 | 15

Development of the hotel property marketHistorically, hotel properties were perceived as part of the overall property market . Own-ership was often in the hands of institutions and large property companies that lacked hotel expertise and had few contact sur-faces with hotel operators . The relationship between tenant and landlord was in general based on long leases with solid guarantee components where the operator/hotel company took care of all development, maintenance and service of the properties .

The distinctive features of hotel properties

became clear

During the financial and property crisis in the begin-

ning of the 1990s, it became clear that the owners,

often institutions and large property companies,

lacked industrial competence . The economic

downturn hit the hotels, which suddenly could not

afford to pay their rent – which in turn caused far-

reaching problems for the property owners .

The property crisis led to the banks being

forced to take over a number of hotels, and

banks and other passive owners discovered

that hotels have distinctive features that distin-

guish them from, for example, housing and

office buildings . The value growth of a hotel

property is complex in view of that revenues and

results are affected by several factors that

demand extensive knowledge of the sector,

including knowledge of driving forces within the

hotel industry, effects of the choice of brand

name and type of agreement, as well as different

price and product segments, and much more .

Functional and geographical focus

Further to this baptism of fire, the capital market

increased its requirements regarding the strate-

gies of property companies . The companies

started to specialise, and two principal paths

crystallised: functional and geographical focus .

The majority of property companies chose the

latter and concentrated their portfolio around a

few locations, which also led to them selling

special properties such as hotels and shopping

centres . New structures arose from this situation

where companies with a functional strategy

were formed, and the first pure hotel property

companies were established .

At the same time, several of the large hotel

companies changed their strategies and chose

an “asset light” orientation, implying that they

started to sell their property portfolios .

These were the most important driving forces

behind greater liquidity in the hotel property mar-

ket . The new companies were active and in gen-

eral managed by people with considerable hotel

experience – which in turn led to greater dynam-

ics in the market with new contact surfaces and

the spreading of interest in the new players .

Scandinavia led the changes in Europe

Scandinavia was in the forefront of these develop-

ments . Pandox was the first hotel property com-

pany in Europe to be listed on the stock market .

The listing in 1997 in Stockholm led to a more

transparent hotel market further to the improved

availability of information, and the confidence

grew within the capital market . Capona was listed

intercontinental, montreal

Source: The information in the graph is an estimation based on public information and research . Deviations may occur .

10 largest hotel property owners in Europe

Starwood Capital Group

Foncière des Murs

OCPI

Pandox

Moor Park Capital Partners

Westmont Hospitality Group

The Blackstone Group

Prupim/Prudential

Quinland Private Capital

CapMan

0 200 400

No . of hotels

16 | PANDOx 2010

on the Stockholm stock exchange at the end of

the 1990s, and was also founded further to the

reorganisation and industrialisation of the sector .

Over the years that followed, interest in the

hotel industry grew and the number of players

increased . Private equity companies, institutional

owners, high net worth individuals and various

kinds of funds took positions in the market .

Only a few diversified hotel property portfolios

Even if the hotel property market is now estab-

lished and transactions with gigantic amounts are

carried out, ownership is still fragmented and

being restructured . If the point of departure is that

there have been, and still are, functional focus

towards one type of property, the situation should

have led to the market’s players owning hotel

properties in many countries managed by several

brand names, so as to be able to benefit from the

change in the hotel economic cycle and use their

specialist competence . But this is not the situa-

tion today . Few companies have any pronounced

global strategy, and only a minority has opera-

tions in several countries and continents .

At company level, there are only eight com-

panies that have a European property portfolio

with more than 50 hotels . The largest is Starwood

Capital Group that owns close to 1,000 hotel

properties across the world, and where Europe

represents just under 40 percent . Another large

player is Westmont Hospitality Group that owns

about 500 hotels in total, of which 16 percent are

in Europe . Pandox is also a significant player with

120 hotels in 10 countries together with 11 part-

ners under 19 brand names .

Buyers and sellers in 2010

2010 proved to be a year of surprises . The trans-

actions market in Europe touched bottom in

2009 and finished at close to 90 percent under

the peak year of 2007 . The backdrop to the

downturn was strong macro-economic factors,

which were expected to prevent a rapid recov-

ery . But after a cautious, albeit positive, start to

2010 both the underlying hotel market and

transactions within the sector accelerated .

By the end of the year one could see that the

trend of the hotel market showed a pattern of a

very sharp V, with a rapid and strong recovery .

The transaction market in Europe had increased

by 150 percent at the end of the year compared

with 2009 and reached a level of EuR 7 .8 billion .

The transactions completed during the year

were mainly domestic or within Europe, and the

banks’ continued stringent loan requirements

held down the size of the transactions . About 60

percent were less than EuR 35 million and only

17 percent were over EuR 70 million . The larg-

est transaction in Europe was Pandox’ acquisi-

tion of Norgani for just over EuR 1 billion .

The most active buyers in the hotel property

market in 2010 were high net worth individuals

and private equity or investment companies .

The largest sales group was composed of

receivers, companies assigned by banks to sell

distressed assets .

Transaction volume on the hotel property market, EMEA1)

EUR million

0

5,000

10,000

15,000

20,000

25,000

2010200920082007

Single acquisitions Portfolio acquisitions

1) Europe, Middle East, AfricaSource: Hotel Investment Outlook 2011, Jones Lang LaSalle

Buyer and seller net shift analysis, EMEA1) 2010

Other corporates

Developer/Property company

HNWI

Hotel operator

Institutional investor

Investment fund/Private equity

Receiver3)

REIT2)

Sovereign Wealth Fund 2.8

−13.7

−4.5

−5.3

−2.0

0.9

−0.1

9.1

12.8

1) Europe, Middle East, Africa2) Real Estate Investment Trust3) Companies assigned by banks to sell distressed assetsSource: Hotel Investment Outlook 2011, Jones Lang LaSalle

–15 0 15

comfort hotel Børsparken, oslo

%

PANDOx 2010 | 17

120hotels24,800hotel rooms

Pandox – 120 hotel prop erties, one congress centre and 19 well-known brand namesPandox currently works with 11 part-

ners under 19 hotel brand names that

are active within different price and

product segments. our partners are all

well-known, established and success-

ful. these partnerships strengthen

Pandox’ knowledge and network and

enable a unique position in the industry.

the hotels are spread over 10

countries and a total of 59 towns and

cities. Pandox’ most extensive partner-

ship is with scandic, who operate 57 of

the hotels in Pandox’ portfolio, followed

by Quality hotel with 12 hotels. Pandox

also works with international brands

such as hilton, hyatt, radisson BlU,

Crowne Plaza and InterContinental.

each hotel is handled and ana-

lysed based on its individual prerequi-

sites and surroundings. the business

model, form of partnership and agree-

ment are chosen depending on each

situation so as to create optimal pre-

conditions for maximum development

for both parties.

presented on pages 20–39

18 | Pandox 2010

10 CoUntrIes

59 CItIes19 Brandnames

Pandox – 120 hotel prop erties, one congress centre and 19 well-known brand names

Pandox 2010 | 19

strong hotels in good locationsscandic is the leading hotel chain in the nordic

region, and currently has 160 hotels in nine countr-

ies. Pandox and scandic have a long business

relationship and have collaborated closely ever

since Pandox was established. today, Pandox

has 57 hotels and one congress centre under the

scandic brand name, representing 49 percent of

revenues in the total Pandox portfolio.

scandic has two principal product segments:

city-centre hotels and highway hotels. of the

city-centre hotels, Pandox’ portfolio includes for

example scandic Park on Karlavägen and scan-

dic hasselbacken at djurgården in stockholm,

scandic Grand marina and scandic Continental

in helsinki as well as scandic Kna in oslo.

Scandic Ferrum, Kiruna Scandic Hasselbacken, Stockholm

Scandic Grand Marina, Helsinki

Scandic Grand Marina, Helsinki

20 | Pandox 2010

Scandic Highway City centre Resort No. hotels

sweden 25 17 42norway 1 1 2Finland 1 6 2 9denmark 1 1Germany 1 1Belgium 1 1 2

TOTAL 57

scandic Kna, osloscandic rosendal,tammerfors

Scandic KNA, OsloScandic Star, Lund

Scandic Park, Stockholm

Scandic Malmen, Stockholm

CItY CentrehasselBaCKen sCandIC ParKGrand marInaContInentalsCandIC KnasKoGshÖJdFerrUmrosendalmalmenstar

and others

Pandox 2010 | 21

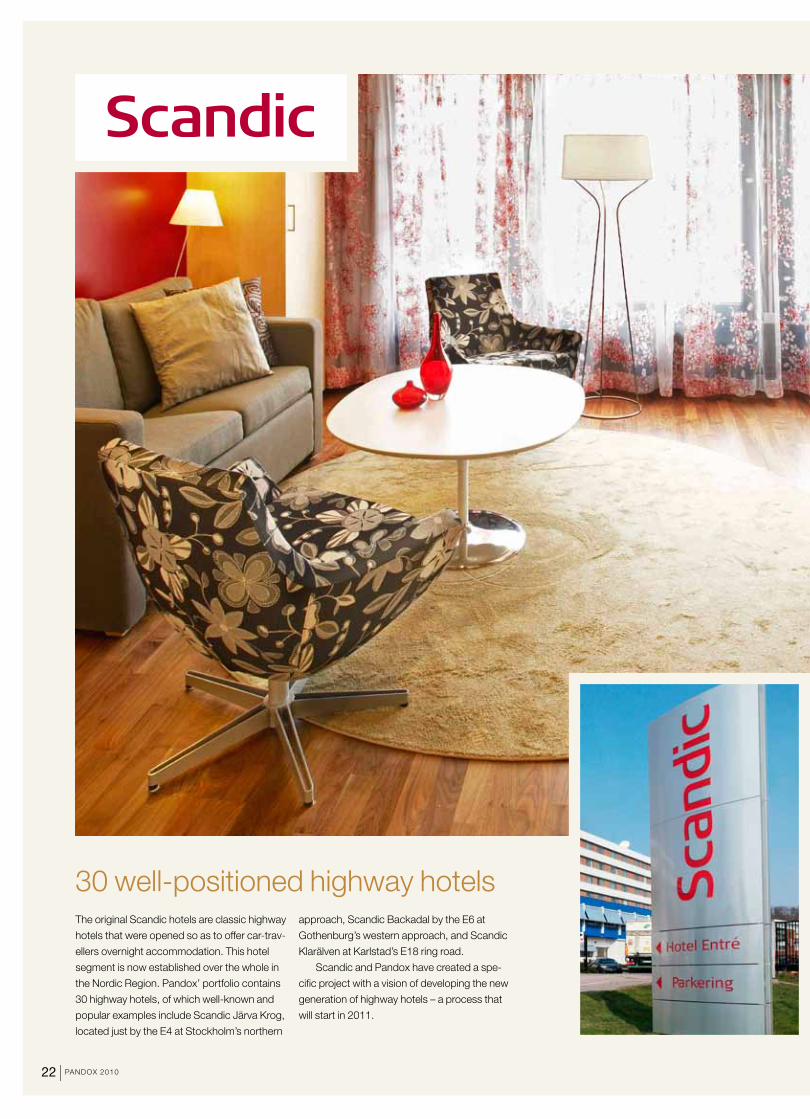

30 well-positioned highway hotelsthe original scandic hotels are classic highway

hotels that were opened so as to offer car-trav-

ellers overnight accommodation. this hotel

segment is now established over the whole in

the nordic region. Pandox’ portfolio contains

30 highway hotels, of which well-known and

popular examples include scandic Järva Krog,

located just by the e4 at stockholm’s northern

approach, scandic Backadal by the e6 at

Gothenburg’s western approach, and scandic

Klarälven at Karlstad’s e18 ring road.

scandic and Pandox have created a spe-

cific project with a vision of developing the new

generation of highway hotels – a process that

will start in 2011.

22 | Pandox 2010

Scandic Örebro Väst

Scandic Norrköping Nord

scandic Backadal, Gothenburg

scandic Bollnäs

scandic Järva Krog, solna

Scandic Linköping Väst

scandic Västerås

scandic Västerås

hIGhwaY hotels

ÖreBro VÄstJÄrVa KroGBaCKadalnorrKÖPInG nordlInKÖPInG VÄst

KlarÄlVenVÄsterÅs

and others

Pandox 2010 | 23

hilton hotels – high class in all locationshilton is a global hotel company, and is to be

found in most major cities across the world.

Pandox has seven hilton hotels in its portfolio.

the locations include london, Brussels,

helsinki and stockholm. Currently a joint refur-

bishment program is in progress at the hilton

stockholm slussen.

Hilton Hotels & Resorts Country City No. rooms

hilton london docklands UK london 365hilton stockholm slussen sweden stockholm 289hilton Brussels City Belgium Brussels 283hilton helsinki Kalastajatorppa Finland helsinki 238hilton helsinki strand Finland helsinki 192hilton Bremen Germany Bremen 235hilton dortmund Germany dortmund 190TOTAL 1,792

Hilton Stockholm Slussen

BrUsselsstoCKholm

londonhelsInKIBremendortmUnd

24 | Pandox 2010

Hilton, Bremen

Hilton Helsinki Kalastajatorppa

Hilton Helsinki Strand

Hilton, Dortmund

Hilton London Docklands

Hilton London Docklands

Pandox 2010 | 25

ClarIonhelsInGBorG

ÖstersUndKarlstadClarIon ColleCtIon CoPenhaGenharstad

osloClarion Collection Hotel Bastion, Oslo

nordic Choice hotels – the portfolio contains all five of the chain’s brandsnordic Choice hotels is the fastest growing hotel com-

pany in the nordic region and is one of Pandox’ larg-

est partners with a total of 22 hotels in the portfolio.

the hotels within the Choice family represent 19

percent of Pandox’ revenues. the hotel company

has several brands, and Pandox has all five in its

portfolio, where Quality is the largest with a total of

12 hotels located in norway and sweden.

26 | Pandox 2010

Nordic Choice Hotels Country No. hotels

Clarion sweden 3Clarion Collection norway, denmark 4Quality norway, sweden 9Quality resort norway 3Comfort norway, denmark 3TOTAL 22

ComFort

osloCoPenhaGen

BerGenQUalItY resortFaGernes

ØYerKrIstIansand

QUalItYmoldelInKÖPInGGothenBUrGstoCKholm KrIstIanstadsÖdertÄlJe

lUleÅsKÖVde

Quality Park Hotel, Södertälje

Clarion Hotel Grand, Helsingborg

Clarion Hotel Mayfair, Copenhagen

Comfort Hotel Børsparken, Oslo

Quality Hotel&Resort, Fagernes

Clarion Hotel Plaza, Karlstad

Pandox 2010 | 27

Centre of attention in the Canadian metropolisInterContinental hotels & resorts is one of the

world’s largest hotel companies, and owns the

InterContinental, Crowne Plaza and holiday Inn

brands. Pandox’ portfolio includes four hotels

located in antwerp, Brussels and montreal. the

InterContinental montreal was acquired in 2007

and has since then been developed and

repositioned. It was named montreal’s best

hotel last year and ranked as one of the 100

best hotels in the world.

BrUsselsantwerPmontreal

Holiday Inn, Brussels

28 | Pandox 2010

leading in BrusselsPandox owns two hotel properties operated

under the Crowne Plaza brand name – both

located in Belgium. Crowne Plaza Brussels City

Centre was acquired in 2003 and thereafter

underwent an important investment program.

the hotel has since become one of Brussels’

leading business and meeting hotels, and is

owned and operated by Pandox under a fran-

chise agreement.

the Crowne Plaza antwerp, acquired in 2007,

is also owned and operated by Pandox under a

franchise agreement. the hotel has 264 rooms

and is strategically located by antwerp’s ring

road just 10 minutes from the airport. It is cur-

rently undergoing an extensive refurbishment

program that will be completed in 2011.

successful change processthe holiday Inn Brussels airport was acquired

in 2006, and needed extensive refurbishment

and development. with the vision of creating

the best upper-medium-priced hotel in the

area, the change process has been

successfully carried out with the catchwords of

full service, attractive design and high efficiency.

today the hotel is runner-up in its market, and is

owned and operated by Pandox under a

franchise agreement.

InterContinental Hotels & Resorts Country City No. hotels

Crowne Plaza Belgium antwerp, Brussels 2holiday Inn Belgium Brussels 1InterContinental Canada montreal 1TOTAL 4

BrUssels

Crowne Plaza Brussels City Centre, Brussels

Crowne Plaza Brussels City Centre, Brussels

Pandox 2010 | 29

Hyatt is an American, stock-market-listed hotel

company with headquarters in Chicago. The

company has eight different brands. Pandox’

hotel in Montreal is operated under the Hyatt

Regency brand.

The Hyatt Regency has a strategically

important position in central Montreal within

walking distance to the Palais des Congrès –

Montreal’s exhibition and congress centre. The

hotel is undergoing refurbishment with the

objective of repositioning as one of Canada’s

best leisure and meeting hotels. The Hyatt

Regency Montreal has 605 rooms and exten-

sive meeting and conference facilities for 1,000

people.

On the way to something big

MONTREAL

Hotel Country City No. rooms

Hyatt Regency Montreal Canada Montreal 605

30 | PANdOx 2010

Rezidor is the fastest growing hotel company in Europe. With Scandi-

navian origins, the company is now listed on the stock market and is

head quartered in Brussels. Pandox has a long relationship with Rezidor

and currently owns six Radisson BLU hotels located in Sweden, Norway

and Switzerland. during 2010, the Radisson BLU hotels in Malmö and

Basel were developed jointly by Rezidor and Pandox with good results

and where the companies’ respective competences could be utilised.

Six hotels, three countries

LiLLEHAMMER

MALMöBOdØSTOCKHOLM

BASELLiNKöPiNg

Rezidor Country City No. rooms

Radisson BLU Arlandia Hotel Sweden Stockholm 335Radisson BLU Hotel, Malmö Sweden Malmö 229Radisson BLU Hotel, Linkoping Sweden Linköping 91Radisson BLU Lillehammer Hotel Norway Lillehammer 303Radisson BLU Hotel, Bodø Norway Bodø 191Radisson BLU Hotel, Basel Switzerland Basel 205TOTAL 1,354

Radisson BLU Lillehammer HotelRadisson BLU Lillehammer Hotel

Radisson BLU Hotel, Basel

Radisson BLU Arlandia Hotel, Arlanda

Radisson BLU Arlandia Hotel, Arlanda

PANdOx 2010 | 31

Elite Hotels is a privately owned hotel chain with 21 hotels, and has specialised in operating

classic hotels. The Pandox portfolio contains the Elite Park Avenue Hotel on gothenburg’s

most well-known avenue, and the Elite Stora Hotellet in Jönköping.

gOTHENBURgJöNKöPiNg

Well-known city profiles

Hotel Country City No. rooms

Elite Park Avenue Hotel Sweden gothenburg 317Elite Stora Hotellet Jönköping Sweden Jönköping 135TOTAL 452

Elite Park Avenue Hotel, GothenburgElite Park Avenue Hotel, Gothenburg

Elite Park Avenue Hotel, Gothenburg

32 | PANdOx 2010

Rica Hotel Bodø

HAMARBOdØ

Rica Hotel Hamar

Rica Hotel Hamar

Rica Hotels has more than 80 hotels in Norway

and Sweden, and two of the Norwegian hotels

are included in Pandox’ portfolio.

The Rica Hotel Bodø is located within walk-

ing distance of the town centre, and has 113

rooms as well as conference facilities for 250

participants.

The Rica Hotel Hamar is a business and

conference hotel located centrally in Østlandet

with 176 rooms and conference facilities for

600 people.

Two Norwegians

Hotel Country City No. rooms

Rica Hotel Bodø Norway Bodø 113Rica Hotel Hamar Norway Hamar 176TOTAL 289

PANdOx 2010 | 33

Central locations

MORAväxJövANTAA

Hotel, other brand names Country City No. rooms

Best Western Mora Hotell & Spa Sweden Mora 135Best Western Royal Corner Sweden växjö 158Best Western Hotel Pilotti Finland vantaa 112ibis Stockholm Hägersten Sweden Stockholm 190Omena Hotel Copenhagen denmark Copenhagen 228Rantasipi imatran valtionhotelli Finland imatra 135

Best Western Mora Hotel & Spa

First Hotels is represented with 46 hotels in Sweden, Norway and denmark. The Pandox portfolio

contains four hotels in Sweden under this brand name, located in älvsjö outside Stockholm and in

Borås, Linköping and Halmstad.

Four First hotels in Sweden

First Hotels Country City No. rooms

First Hotel Royal Star Sweden Stockholm 103First Hotel Linköping Sweden Linköping 133First Hotel grand Borås Sweden Borås 158First Hotel Mårtenson Sweden Halmstad 103TOTAL 497

HALMSTAdLiNKöPiNgSTOCKHOLM

BORÅS

First Hotel Royal Star, Stockholm

Best Western Royal Corner

First Hotel, Linköping

First Hotel Grand, Borås

Best Western Hotels is a global hotel chain with operations

in 80 countries. The hotels are owned and operated

privately but marketed under the joint name of Best

Western. The Pandox portfolio contains three hotels that

are members of Best Western Hotels, of which the Best

Western Mora Hotell & Spa and the Best Western Royal

Corner in växjö are two centrally located four-star hotels.

The Best Western Hotel Pilotti is located in vantaa, Finland.

34 | PANdOx 2010

COPENHAgEN

ibis – budget in southern StockholmAccor is one of the world’s largest hotel companies with operations in 90

countries and 15 different brands in all segments – including the ibis brand

name for low-priced hotels represented in 43 countries. The Pandox portfolio

includes the ibis Stockholm Hägersten, located in southern Stockholm, just

10 minutes from Stockholmsmässan and 15 minutes from central Stockholm.

The hotel has 190 rooms, a restaurant, and several conference rooms.

Centrally located in CopenhagenOmena Hotels has ten hotels, of which nine are in Finland and one in

denmark. The Pandox-owned Omena Hotel Copenhagen is centrally

located in Copenhagen with 228 rooms and a café.

iMATRA

Castle environment in Finland

STOCKHOLM

Rantasipi Imatran Valtionhotelli is a spa hotel in a castle environment close to the town of Imatra in Finland.

The hotel has 135 rooms, conference facilities for 250 people, and a complete spa centre.

PANdOx 2010 | 35

Independent hotels Country City No. rooms

Hotel Berlin, Berlin germany Berlin 701The Hotel Belgium Brussels 433Hotel BLOOM! Belgium Brussels 305

Pelican Bay Bahamasgrand Bahama

island 184Airport Hotel Bonus inn Finland vantaa 211vildmarkshotellet Kolmården Sweden Norrköping 213Mr Chip, Kista Sweden Stockholm 150Stadshotellet Princess Sandviken Sweden Sandviken 84Hotel Korpilampi Finland Espoo 150

A unique and own conceptPandox acquired Hotel BLOOM! in 2005, which

since September 2007 has been totally refur-

bished and has undergone a complete facelift.

Today, the Hotel BLOOM! is a unique hotel

product with its own concept based on art and

design. it is a distinct challenger in the Brussels

hotel market, with 305 rooms and large confer-

ence facilities, in the city centre that competes

with the major hotels. Hotel BLOOM! is both

owned and operated by Pandox.

BRUSSELS

independent hotels

36 | PANdOx 2010

Best location in the EU cityThe Hotel was acquired in 2010 and is one of

the largest and best-known hotels in Brussels.

The hotel property is located on Boulevard

Waterloo next to the city’s most prestigious

shopping street, Avenue Louise. The hotel,

which is a landmark, has 433 rooms on 26

floors with several conference areas, two res-

taurants, as well as a fitness and spa centre.

Pandox’ vision is to recreate the hotel’s histori-

cally strong position as one of the city’s leading

business and meeting hotels in the premium

segment.

BRUSSELS

Hotel BLOOM!, Brussels

Hotel BLOOM!, Brussels

Hotel BLOOM!, Brussels

PANdOx 2010 | 37

BERLiN

independent hotels, continued

Creative meeting place in BerlinSince the acquisition of the hotel in 2006, Pan-

dox has created the meeting place of the future

in one of Berlin’s largest hotels. A comprehensive

repositioning program has brought the Hotel

Berlin, Berlin back to the top. it is now estab-

lished as one of the leading meeting hotels and is

one of Berlin’s most creative meeting places. The

hotel has 701 guest rooms and 22 conference

rooms, as well as several restaurants and bars.

The hotel is owned and operated by Pandox.

38 | PANdOx 2010

KOLMÅRdEN

BAHAMAS

MR CHIp, KIsTA is strategically located in

central Kista, one of Stockholm’s most

expansive areas that is also the centre for

leading companies within the iT and telecom

sectors. The hotel has 150 rooms, conference

facilities, as well as bar and restaurant,

oriented towards business travellers.

Complete resort in the CaribbeanThe Pelican Bay Hotel is located in the beautiful

Bahamas, on grand Bahama island. The hotel has

been repositioned since Pandox took over the man-

agement agreement, and is now one of the leading

business and meeting hotels in the Bahamas.

THe AIRpORT HOTeL bONus INN has 211 rooms

and is located just 5 minutes’ drive from Helsinki-

vantaaa airport and 30 minutes from Helsinki railway

station. The hotel is next to the Leija Business Park –

a shopping and leisure centre.

THe sTAdsHOTeLLeT pRINCess,

sANdvIKeN is located right in the centre of

Sandviken with 84 rooms, conference room

with capacity for 80 people, and a restaurant.

The major family attraction in SwedenVildmarkshotellet is one of the best-known

resort and tourist complexes in Sweden. The

hotel is located outside Norrköping, about

150 kilometres from Stockholm, next to

Scandinavia’s largest wildlife park,

Kolmården. The complex has 213 rooms, of

which most are family-adapted, a large

conference area with capacity for 370 people

in the largest room, a large restaurant and a

lobby bar. A new family spa centre has

recently been completed with waterway,

relaxation areas and treatment room.

PANdOx 2010 | 39

property Operator / brand nameType of agreement Country City Location

Number of rooms

Total area (sqm)

Of which hotels (sqm) property designation

Tax assesment value (seK M)

Scandic Antwerp Scandic O Belgium Antwerp Ring road 204 13,200 13,200 24th div, Borgerhout 1st div, Ar –Scandic grand Place, Brussels Scandic O Belgium Brussels City centre 100 4,500 4,500 –Scandic Copenhagen Scandic O denmark Copenhagen City centre 484 31,500 25,200 99943-2 –Scandic Continental, Helsinki Scandic Og Finland Helsinki City centre 512 30,000 91-14-468-3 178.4Scandic Espoo Scandic Og Finland Espoo Ring road 96 5,245 49-54-17-7 43Scandic grand Marina, Helsinki Scandic Og Finland Helsingfors City centre 462 23,660 91-8-187-8 147.3Scandic Marina Congress Center, Helsinki Scandic O Finland Helsingfors City centre 0 11,500 0 75.8Scandic Jyväskylä Scandic Og Finland Jyväskylä Central 150 7,360 179-3-52-23 78.9Scandic Kajanus, Kajaani Scandic Og Finland Kajaani Exhibition centre 191 10,468 205-14-7-5 77.7Scandic Kuopio Scandic Og Finland Kuopio Central 137 7,113 297-1-41-6-Li 60.6Scandic Luosto Scandic Og Finland Luosto Ski resort 59 4,230 758-893-103-1-L159, L37, L188, L189, L195, L212 11.8Scandic Rosendahl Scandic Og Finland Tampere Central 213 14,662 837-134-495-1-Li Scandic Tampere City Scandic Og Finland Tampere Central 263 14,457 837-112-187-35,837-112-187-37 131.3Scandic Bergen Airport Scandic O Norway Bergen Airport 197 9,654 gnr 114 Bnr 213 33.1Scandic KNA, Oslo Scandic O Norway Oslo City centre 189 11,218 gnr 209 Bnr 275 14.0Scandic Alvik, Stockholm Scandic Og Sweden Stockholm Ring road 325 12,075 Racketen 9 196Scandic Backadal, gothenburg Scandic Og Sweden gothenburg Ring road 232 9,397 Backa 105:1 53.6Scandic Billingen, Skövde Scandic O Sweden Skövde Central 107 7,743 6,844 Fjolner 7 27.6Scandic Bollnäs Scandic Og Sweden Bollnäs Central 111 5,150 Sundsbro 10 20.9Scandic Bromma, Stockholm Scandic Og Sweden Stockholm Ring road 144 6,800 3,970 Pundet 1 38.2Scandic Crown, gothenburg Scandic O Sweden gothenburg City centre 338 24,380 21,800 Stampen 5:5 170Scandic Elmia, Jönköping Scandic O Sweden Jönköping Exhibition centre 220 9,576 Åminne 1 52.2Scandic Ferrum, Kiruna Scandic Og Sweden Kiruna Central 170 11,100 Hovmästaren 1 19.2*Scandic grand, örebro Scandic O Sweden örebro Central 221 12,900 10,900 Mältaren 1 50.6Scandic gävle väst Scandic Og Sweden gävle Ring road 201 7,382 valbo-Backa 6:12 28.4Scandic Hallandia, Halmstad Scandic O Sweden Halmstad Central 154 7,617 6,813 Erik dahlberg 14 & 15 44.8Scandic Hasselbacken, Stockholm Scandic Og Sweden Stockholm City centre 112 10,025 Hasselbacken 1 102Scandic Helsingborg Nord Scandic Og Sweden Helsingborg Ring road 237 9,399 Floretten 1 41Scandic Järva Krog, Stockholm Scandic O Sweden Stockholm Ring road 215 11,300 11,300 Tanken 2 77.6Scandic Kalmar väst Scandic Og Sweden Kalmar Airport 148 5,485 Hammaren 4 24.6Scandic Klarälven, Karlstad Scandic Og Sweden Karlstad Ring road 143 5,694 Sandbäcken 1:3 26.3Scandic Kramer, Malmö Scandic O Sweden Malmö City centre 113 6,913 6,373 gripen 1 73.8Scandic Kungens Kurva, Stockholm Scandic Og Sweden Stockholm Ring road 257 11,581 9,456 Radien 112*Scandic Linköping väst Scandic Og Sweden Linköping Ring road 150 6,105 Osten 2 27.8Scandic Luleå Scandic Og Sweden Luleå Ring road 159 5,565 Mjölkudden 3:45 21Scandic Malmen, Stockholm Scandic Og Sweden Stockholm City centre 327 15,130 gråberget 190Scandic Mölndal, gothenburg Scandic O Sweden gothenburg City centre 208 11,000 11,000 Laken 1 55.2Scandic Norrköping Nord Scandic Og Sweden Norrköping Ring road 150 6,768 Blyet 8 24.2Scandic Park, Stockholm Scandic O Sweden Stockholm City centre 201 12,290 10,290 Lönnen 30 213Scandic Plaza, Borås Scandic Og Sweden Borås Central 135 10,592 7,961 Balder 6 62.8Scandic S:t Jörgen, Malmö Scandic Og Sweden Malmö City centre 288 21,485 14,655 S:t Jörgen 11 222Scandic Segevång, Malmö Scandic Og Sweden Malmö Ring road 161 6,284 Kriseberg 14:95 30.6Scandic Skogshöjd, Södertälje Scandic O Sweden Södertälje Central 225 14,115 14,115 Yxan 8 46.2Scandic Star Sollentuna Scandic Og Sweden Stockholm Ring road 269 18,573 Centrum 12 138*Scandic Star, Lund Scandic Og Sweden Lund Central 196 15,711 15,711 Porfyren 2 102.4Scandic Sundsvall Nord Scandic Og Sweden Sundsvall Ring road 159 4,948 värdshuset 1 23.6Scandic Swania, Trollhättan Scandic O Sweden Trollhättan Central 198 10,399 10,399 Svan 7 48.5Scandic Södertälje Scandic Og Sweden Södertälje Ring road 131 5,630 Reparatören 2 24.4Scandic Umeå Syd Scandic Og Sweden Umeå Ring road 162 5,955 Reparatören 4 26Scandic Uplandia, Uppsala Scandic Og Sweden Uppsala City centre 133 5,402 4,611 dragarbrunn 16:4 51.8Scandic Upplands väsby Scandic O Sweden Stockholm Ring road 150 6,955 6,955 vilunda 6:48 34.6Scandic Uppsala Nord Scandic Og Sweden Uppsala Ring road 184 7,518 6,486 Kvarngärdet 3:2 37Scandic Winn, Karlstad Scandic Og Sweden Karlstad Central 199 10,580 10,580 Negern 2 49Scandic västerås Scandic Og Sweden västerås Ring road 174 7,285 Sågen 1 26.1Scandic växjö Scandic Og Sweden växjö Ring road 123 3,982 Kocken 3 21.74Scandic örebro väst Scandic Og Sweden örebro Ring road 204 7,621 vindmotorn 2 35Scandic östersund Syd Scandic Og Sweden östersund Ring road 129 4,019 Särrimner 1 21.6Scandic Lübeck Scandic O germany Lübeck Ring road 158 9,700 8,800 grundbuch Lübeck, Blatt 54545 – Hilton Brussels City Pandox/Hilton M Belgium Brussels City centre 283 13,850 13,850 Saint-Josseten-Noode (1div) 032 –Hilton Helsinki Kalastajatorppa Scandic/Hilton Og Finland Helsinki Ring road 238 23,291 91-30-1-5,91-30-3-2-Li 164.2Hilton Helsinki Strand Scandic/Hilton Og Finland Helsinki Central 192 10,250 91-11-300-7 146.3Hilton London docklands Hilton O Storbritannien London Central 365 22,800 21,500 HM Land Registry: SgL465779 –Hilton Stockholm Slussen Hilton O Sweden Stockholm City centre 289 18,416 15,725 överkikaren 31 365.9Hilton Bremen Hilton O germany Bremen City centre 235 21,000 15,100 grundbuch Altstadt iv, Blatt 60 –Hilton dortmund Hilton O germany dortmund Exhibition centre 190 12,500 11,300 grundbuch dortmund, Blatt 897 –

* tax assesment value 2007

O = Revenue-based, Og = Revenue-based with guaranteed rent, OR = Revenue and result-based, R = Result-based,

F = Fixed, iO = internal revenue-based, M = Management agreement, FR = Franchise, AM = Asset management agreement

Operated by Pandox (Pandox own hotel operations)

Hotel properties

40 | PANdOx 2010

PANdOx 2009 | 41

property Operator / brand nameType of agreement Country City Location

Number of rooms

Total area (sqm)

Of which hotels (sqm) property designation

Tax assesment value (seK M)

Scandic Antwerp Scandic O Belgium Antwerp Ring road 204 13,200 13,200 24th div, Borgerhout 1st div, Ar –Scandic grand Place, Brussels Scandic O Belgium Brussels City centre 100 4,500 4,500 –Scandic Copenhagen Scandic O denmark Copenhagen City centre 484 31,500 25,200 99943-2 –Scandic Continental, Helsinki Scandic Og Finland Helsinki City centre 512 30,000 91-14-468-3 178.4Scandic Espoo Scandic Og Finland Espoo Ring road 96 5,245 49-54-17-7 43Scandic grand Marina, Helsinki Scandic Og Finland Helsingfors City centre 462 23,660 91-8-187-8 147.3Scandic Marina Congress Center, Helsinki Scandic O Finland Helsingfors City centre 0 11,500 0 75.8Scandic Jyväskylä Scandic Og Finland Jyväskylä Central 150 7,360 179-3-52-23 78.9Scandic Kajanus, Kajaani Scandic Og Finland Kajaani Exhibition centre 191 10,468 205-14-7-5 77.7Scandic Kuopio Scandic Og Finland Kuopio Central 137 7,113 297-1-41-6-Li 60.6Scandic Luosto Scandic Og Finland Luosto Ski resort 59 4,230 758-893-103-1-L159, L37, L188, L189, L195, L212 11.8Scandic Rosendahl Scandic Og Finland Tampere Central 213 14,662 837-134-495-1-Li Scandic Tampere City Scandic Og Finland Tampere Central 263 14,457 837-112-187-35,837-112-187-37 131.3Scandic Bergen Airport Scandic O Norway Bergen Airport 197 9,654 gnr 114 Bnr 213 33.1Scandic KNA, Oslo Scandic O Norway Oslo City centre 189 11,218 gnr 209 Bnr 275 14.0Scandic Alvik, Stockholm Scandic Og Sweden Stockholm Ring road 325 12,075 Racketen 9 196Scandic Backadal, gothenburg Scandic Og Sweden gothenburg Ring road 232 9,397 Backa 105:1 53.6Scandic Billingen, Skövde Scandic O Sweden Skövde Central 107 7,743 6,844 Fjolner 7 27.6Scandic Bollnäs Scandic Og Sweden Bollnäs Central 111 5,150 Sundsbro 10 20.9Scandic Bromma, Stockholm Scandic Og Sweden Stockholm Ring road 144 6,800 3,970 Pundet 1 38.2Scandic Crown, gothenburg Scandic O Sweden gothenburg City centre 338 24,380 21,800 Stampen 5:5 170Scandic Elmia, Jönköping Scandic O Sweden Jönköping Exhibition centre 220 9,576 Åminne 1 52.2Scandic Ferrum, Kiruna Scandic Og Sweden Kiruna Central 170 11,100 Hovmästaren 1 19.2*Scandic grand, örebro Scandic O Sweden örebro Central 221 12,900 10,900 Mältaren 1 50.6Scandic gävle väst Scandic Og Sweden gävle Ring road 201 7,382 valbo-Backa 6:12 28.4Scandic Hallandia, Halmstad Scandic O Sweden Halmstad Central 154 7,617 6,813 Erik dahlberg 14 & 15 44.8Scandic Hasselbacken, Stockholm Scandic Og Sweden Stockholm City centre 112 10,025 Hasselbacken 1 102Scandic Helsingborg Nord Scandic Og Sweden Helsingborg Ring road 237 9,399 Floretten 1 41Scandic Järva Krog, Stockholm Scandic O Sweden Stockholm Ring road 215 11,300 11,300 Tanken 2 77.6Scandic Kalmar väst Scandic Og Sweden Kalmar Airport 148 5,485 Hammaren 4 24.6Scandic Klarälven, Karlstad Scandic Og Sweden Karlstad Ring road 143 5,694 Sandbäcken 1:3 26.3Scandic Kramer, Malmö Scandic O Sweden Malmö City centre 113 6,913 6,373 gripen 1 73.8Scandic Kungens Kurva, Stockholm Scandic Og Sweden Stockholm Ring road 257 11,581 9,456 Radien 112*Scandic Linköping väst Scandic Og Sweden Linköping Ring road 150 6,105 Osten 2 27.8Scandic Luleå Scandic Og Sweden Luleå Ring road 159 5,565 Mjölkudden 3:45 21Scandic Malmen, Stockholm Scandic Og Sweden Stockholm City centre 327 15,130 gråberget 190Scandic Mölndal, gothenburg Scandic O Sweden gothenburg City centre 208 11,000 11,000 Laken 1 55.2Scandic Norrköping Nord Scandic Og Sweden Norrköping Ring road 150 6,768 Blyet 8 24.2Scandic Park, Stockholm Scandic O Sweden Stockholm City centre 201 12,290 10,290 Lönnen 30 213Scandic Plaza, Borås Scandic Og Sweden Borås Central 135 10,592 7,961 Balder 6 62.8Scandic S:t Jörgen, Malmö Scandic Og Sweden Malmö City centre 288 21,485 14,655 S:t Jörgen 11 222Scandic Segevång, Malmö Scandic Og Sweden Malmö Ring road 161 6,284 Kriseberg 14:95 30.6Scandic Skogshöjd, Södertälje Scandic O Sweden Södertälje Central 225 14,115 14,115 Yxan 8 46.2Scandic Star Sollentuna Scandic Og Sweden Stockholm Ring road 269 18,573 Centrum 12 138*Scandic Star, Lund Scandic Og Sweden Lund Central 196 15,711 15,711 Porfyren 2 102.4Scandic Sundsvall Nord Scandic Og Sweden Sundsvall Ring road 159 4,948 värdshuset 1 23.6Scandic Swania, Trollhättan Scandic O Sweden Trollhättan Central 198 10,399 10,399 Svan 7 48.5Scandic Södertälje Scandic Og Sweden Södertälje Ring road 131 5,630 Reparatören 2 24.4Scandic Umeå Syd Scandic Og Sweden Umeå Ring road 162 5,955 Reparatören 4 26Scandic Uplandia, Uppsala Scandic Og Sweden Uppsala City centre 133 5,402 4,611 dragarbrunn 16:4 51.8Scandic Upplands väsby Scandic O Sweden Stockholm Ring road 150 6,955 6,955 vilunda 6:48 34.6Scandic Uppsala Nord Scandic Og Sweden Uppsala Ring road 184 7,518 6,486 Kvarngärdet 3:2 37Scandic Winn, Karlstad Scandic Og Sweden Karlstad Central 199 10,580 10,580 Negern 2 49Scandic västerås Scandic Og Sweden västerås Ring road 174 7,285 Sågen 1 26.1Scandic växjö Scandic Og Sweden växjö Ring road 123 3,982 Kocken 3 21.74Scandic örebro väst Scandic Og Sweden örebro Ring road 204 7,621 vindmotorn 2 35Scandic östersund Syd Scandic Og Sweden östersund Ring road 129 4,019 Särrimner 1 21.6Scandic Lübeck Scandic O germany Lübeck Ring road 158 9,700 8,800 grundbuch Lübeck, Blatt 54545 – Hilton Brussels City Pandox/Hilton M Belgium Brussels City centre 283 13,850 13,850 Saint-Josseten-Noode (1div) 032 –Hilton Helsinki Kalastajatorppa Scandic/Hilton Og Finland Helsinki Ring road 238 23,291 91-30-1-5,91-30-3-2-Li 164.2Hilton Helsinki Strand Scandic/Hilton Og Finland Helsinki Central 192 10,250 91-11-300-7 146.3Hilton London docklands Hilton O Storbritannien London Central 365 22,800 21,500 HM Land Registry: SgL465779 –Hilton Stockholm Slussen Hilton O Sweden Stockholm City centre 289 18,416 15,725 överkikaren 31 365.9Hilton Bremen Hilton O germany Bremen City centre 235 21,000 15,100 grundbuch Altstadt iv, Blatt 60 –Hilton dortmund Hilton O germany dortmund Exhibition centre 190 12,500 11,300 grundbuch dortmund, Blatt 897 –

* tax assesment value 2007

O = Revenue-based, Og = Revenue-based with guaranteed rent, OR = Revenue and result-based, R = Result-based,

F = Fixed, iO = internal revenue-based, M = Management agreement, FR = Franchise, AM = Asset management agreement

Operated by Pandox (Pandox own hotel operations)

PANdOx 2009 | 41

Pandox market segments

SwedenNumber of hotels 69Number of rooms 12,455Property revenues, SEK M 893

Rest of Nordic RegionNumber of hotels 34Number of rooms 6,641Property revenues, SEK M 476

EuropeNumber of hotels 14Number of rooms 4,107Property revenues, SEK M 296

InternationalNumber of hotels 3Number of rooms 1,146Property revenues, SEK M 44

Pandox own hotel operationsNumber of hotels 10Number of rooms 3,796Property revenues, SEK M 1,209Operating net, SEK M 220

Proportion of totalnumber of rooms

51%

Proportion of totalnumber of rooms

17%

Proportion of totalnumber of rooms

27%

Proportion of totalnumber of rooms

16%

Proportion of totalnumber of rooms

5%

PANdOx 2010 | 41

property Operator / brand nameType of agreement Country City Location

Number of rooms

Total area (sqm)

Of which hotels (sqm) property designation

Tax assesment value (seK M)

Clarion Hotel grand, Helsingborg Choice Hotels/Clarion Hotel Og Sweden Helsingborg Central 164 8,555 7,325 Högvakten 8 59.4Clarion Hotel grand, östersund Choice Hotels/Clarion Hotel Og Sweden östersund Central 176 8,766 8,766 Borgens 6 33.8Clarion Hotel Plaza, Karlstad Choice Hotels/Plaza Hotell & Rest Karlstad AB Og Sweden Karlstad Central 131 5,907 5,907 Höken 1 39.6

Clarion Collection Hotel Mayfair, Copenhagen Choice Hotels/Clarion Collection Hotel O denmark Copenhagen City centre 105 3,805 Matr.nr 214 Clarion Collection Hotel Twentyseven, Copenhagen Choice Hotels/Clarion Collection Hotel Og denmark Copenhagen City centre 200 7,568 7,568 169 vester Kvarter København –Clarion Collection Hotel Arcticus, Harstad Choice Hotels/Clarion Collection Hotel O Norway Harstad Ring road 75 3,540 gnr 61 Bnr 331, Snr 12–22 27.2Clarion Collection Hotel Bastion, Oslo Choice Hotels/Clarion Collection Hotel O Norway Oslo City centre 99 4,688 grnr 207 Bnr 262 og 265 28.5

Comfort Hotel Excelsior, Copenhagen Choice Hotels/Comfort Hotel Og denmark Copenhagen City centre 99 3,600 Matr.nr 212-213 seksjon 1–2 Comfort Hotel Børsparken, Oslo Choice Hotels/Comfort Hotel O Norway Oslo City centre 198 7,900 gnr 207 Bnr 343 og 344 101.9Comfort Hotel Holberg, Bergen Choice Hotels/Comfort Hotel O Norway Bergen Central 140 5,720 gnr 165 Bnr 1083 Snr 1 og 2 47.2

Quality Hotel & Resort, Fagernes Choice Hotels/Quality Hotel & Resort O Norway Fagernes Ring road 138 10,310 gnr22 Bnr 177, gnr 25 Bnr 4, 96, 97, 259, gnr 26 Bnr 5 49.8Quality Hotel & Resort Hafjel, Øyer Choice Hotels/Quality Hotel & Resort O Norway Øyer Central 210 9,540 gnr 17 Bnr 25 57.7Quality Hotel & Resort Kristiansand Choice Hotels/Quality Hotel & Resort O Norway Kristiansand Ring road 210 9,940 7,075 gnr 63 Bnr 760, 822 og 823 59.9 Quality Hotel Alexandra, Molde Choice Hotels/Quality Hotel O Norway Molde Central 163 17,033 gnr 24 Bnr 812, 815 og 1312 69.2Quality Hotel Ekoxen, Linköping Choice Hotels/Quality Hotel Og Sweden Linköping Central 190 14,671 12,221 Ekoxen 9 & 11 53.7Quality Hotel grand Kristianstad Choice Hotels/Quality Hotel Og Sweden Kristianstad Central 149 7,524 Hovrätten 41 39.4Quality Hotel Luleå Choice Hotels/Quality Hotel Og Sweden Luleå Central 209 12,166 Tjädern 19 61.4Quality Hotel Park, Södertälje Choice Hotels/Quality Hotel FR Sweden Södertälje City centre 157 10,292 10,110 Herkules 13 35.6Quality Hotel Prince Phillip, Stockholm Choice Hotels/Quality Hotel Og Sweden Stockholm Ring road 201 7,400 Måsholmen 25 57.4Quality Hotel Prisma, Skövde Choice Hotels/Quality Hotel Og Sweden Skövde Central 107 3,687 Liljekonvaljen 14 16.3Quality Hotel Winn, gothenburg Choice Hotels/Quality Hotel Og Sweden gothenburg Ring road 121 5,800 Backa 149:l & 866:39 32.8Quality Hotel, Nacka Choice Hotels/Quality Hotel Og Sweden Stockholm Ring road 164 10,830 8,090 Sicklaön 363:2 84.8 interContinental Montreal Pandox/interContinental M Canada Montreal City centre 357 31,091 31,091 Crowne Plaza Antwerp Pandox/Crowne Plaza FR Belgium Antwerp Central 264 18,340 16,780 Crowne Plaza Brussels City Centre Pandox/Crowne Plaza FR Belgium Brussels City centre 354 28,095 28,095 – Holiday inn Brussels Airport Pandox/Holiday inn FR Belgium Brussels Airport 310 21,072 21,072 Hyatt Regency, Montreal Pandox/Hyatt Hotels M Canada Montreal City centre 605 44,148 29,000 – –