Optimal Ownership of a Public Project, An Application To ... · Optimal Ownership of a Public...

40

Optimal Ownership of a Public Project, An Application To Conservation Concessions Pauline Grosjean 1 LEERNA, University of Toulouse [email protected] Room MF05 Manufacture des Tabacs 21, allées de Brienne 31000 Toulouse December 10, 2003 Abstract This paper studies how the ownership of a project affects the investment incentives of different parties, when the project generates non-excludable bene- fits. The main application is a conservation project, where a conservation NGO and a governmental agency make non contractible investments, which generate an opportunity cost that has to be paid to a third party, typically a local com- munity, in order to prevent her from destroying the value of the public project. It is shown in this context that, contrary to the result of Besley and Ghatak (2001), it is not always true that the project should be granted to the most caring party. In some cases, granting ownership to the least caring party allows both parties to tie their own hands and leads them to maximize their invest- ments. These results have some implications for studying the respective roles of governmental agencies, NGOs and local communities in the management and ownership of conservation concessions, which are an increasingly used tool for conservation in developed as well as developing countries. The insights of the model are applied to a conservation concession project on a communal forest in East Kalimantan, Indonesia. 1 I am grateful to my advisor Paul Seabright, and to Bruno Jullien, Antoine Loeper and Micha Drugov for helpful comments. I thank CIFOR, and particularly Patrice Levang and Sven Wunder, for hosting an internship during summer 2003. Many thanks also to Charles Kole, Ramses Iwan and Rinda Sandayani Kharab. 1

Transcript of Optimal Ownership of a Public Project, An Application To ... · Optimal Ownership of a Public...

Optimal Ownership of a Public Project,An Application To Conservation Concessions

Pauline Grosjean1

LEERNA, University of Toulouse

Room MF05Manufacture des Tabacs21, allées de Brienne31000 Toulouse

December 10, 2003

Abstract

This paper studies how the ownership of a project affects the investmentincentives of different parties, when the project generates non-excludable bene-fits. The main application is a conservation project, where a conservation NGOand a governmental agency make non contractible investments, which generatean opportunity cost that has to be paid to a third party, typically a local com-munity, in order to prevent her from destroying the value of the public project.It is shown in this context that, contrary to the result of Besley and Ghatak(2001), it is not always true that the project should be granted to the mostcaring party. In some cases, granting ownership to the least caring party allowsboth parties to tie their own hands and leads them to maximize their invest-ments. These results have some implications for studying the respective roles ofgovernmental agencies, NGOs and local communities in the management andownership of conservation concessions, which are an increasingly used tool forconservation in developed as well as developing countries. The insights of themodel are applied to a conservation concession project on a communal forest inEast Kalimantan, Indonesia.

1 I am grateful to my advisor Paul Seabright, and to Bruno Jullien, Antoine Loeper andMicha Drugov for helpful comments. I thank CIFOR, and particularly Patrice Levang andSven Wunder, for hosting an internship during summer 2003. Many thanks also to CharlesKole, Ramses Iwan and Rinda Sandayani Kharab.

1

1 Introduction

What is the best way to manage land resources which yield conservationexternalities?Up to recently, the traditional respond to this issue has been to es-

tablish national parks or conservation areas. However, this approachhas revealed a number of shortcomings and is nowadays under question,from the point of view of academics, as well as of active conservationorganizations. In the mean time, a trend towards privately owned con-servation projects, by conservation NGOs, private landholders or evenprivate firms (Earth Sanctuaries Ltd for example in Australia) has beenobserved, with various degrees of success from a conservation viewpoint.What is the current state of the debate? Are privately owned conser-vation areas likely to be a good substitute to national parks? In otherwords, what are the respective incentives of conservation stakeholders inthese various configurations of ownership?To answer that question, one can first look at the shortcomings of the

national parks approach. The establishment of national parks entails atleast a limitation of use rights by local residents and sometimes land ap-propriation and population resettlement. One frequent criticism of thisapproach is the political cost of limiting the property rights of landownersor residents. For example, Innes, Polasky and Tschirhart (1998) exposethe drawbacks of the land appropriation approach on species protectionin the US. This issue is even more dramatic in developing countries.Cernea and Schmidt-Soltau (2003) estimate that between 190,000 and250,000 people were adversely affected by the establishment of nationalparks in nine countries of Central Africa, often without any compen-sation. This overtaking and negation of indigenous peoples’ rights isethically indefensible, and concern about forest dependant people liveli-hood is increasing.Furthermore, beyond aggravating poverty among these highly ex-

posed populations, this approach generally backfires on the security ofthe protected areas. The second critic of the State driven approachindeed concerns its efficacy. A recent report by WWF-Forest Alliancerelates that only 1% of forest protected areas, most of which are underState control, can be considered as fully secure, and 60% are seriouslythreatened. More generally, half to two thirds of all forest are still Statecontrolled and include large deforested areas and degraded forest land(see table in appendix). What is more, the example of Brazil showsthat even though indigenous people’s rights have now been recognizedon large areas of forest, their uses of the resource are largely prohibited.Meanwhile, no reliable monitoring system is provided for, and no ade-quate compensation is offered in exchange of these limitations put on

1

their use rights. Local people thus exploit the resource illegally, sellingfor example mahogany to buyers for a fraction of its commercial price.

Such a State driven approach to forest management is under seriousquestion today, from an ethical as well as an efficacy point of view.These critics also pertain to the general questioning of the logic of publicprovision of public good and a shift in economic policy leading to aretreat of the State from production activities.Some authors (Ferraro and Simpson (2000), Ferraro (2001), Conrad,

Ferraro (2000)) have presented the advantages of a contractual approachover public provision of conservation. Direct payment mechanisms aimat enabling those who benefit from environmental services to reward di-rectly those who provide such services. Providers and demanders can beanyone, individuals or communities, NGOs or governments. Conserva-tion payments are an increasingly used tool for conservation in developedas well as in developing countries. In Europe, 14 nations have spent anestimated $ 11 billion between 1993 and 1997 to divert over 20 millionhectares into long term set aside and forestry contracts (OECD 1997).In the US, the Conservation Reserve Program spends about $1.5 billionper year to contract for 12-15 million hectares. In developing coun-tries, and in particular in Central and South America where they havebeen pioneered by Conservation International, conservation concessionsare a special case of this contractual approach. Under a conservationconcession agreement, national or local authorities or local communi-ties agree to protect natural ecosystems in exchange for a steady streamof structured compensation, which emanates from conservation NGOs,governments or any other investors, including private investors.This contracting approach has two main advantages. The first con-

cerns its efficacy. It has come clear that forest conservation, in the faceof competing land uses, requires that local people obtain some direct orindirect financial benefit from forest resources. This cannot be ignoredby any regulatory policy. The contracting approach acknowledges theimportance of taking into account the incentives of the local stakehold-ers for which conservation must be made more profitable than poachingor illegal logging in order to have a chance to be sustainable.The second advantage derives from a direct application of the theory

of public goods due to Lindahl and Samuelson. These contractual in-struments are additional tools which allow various investors other thangovernments to invest in conservation. Conservation NGOs or other pri-vate investors value the project and they have a willingness to pay thatshould be taken into account in the public good provision decision. Thisis essential, if we consider that biodiversity is a global public good: anational government does not aggregate the World’s preferences, so ad-

2

ditional tools for better taking into account the preferences of the rest ofthe world are needed. A natural question that arises is then: how doesthis feed back on governments’ incentives to invest?

The aim of this paper is then to study the role of public and pri-vate responsibility in conservation. Increased involvement of NGOs inconservation raises two main issues.The first is inherent to public good provision, and is due to the non

excludability of the benefits generated by the investments of NGOs inbiodiversity protection, which shall encourage free riding by the gov-ernment. One can indeed wonder whether the increased participationof NGOs does not crowd out governmental participation. For example,in Indonesia, since 1997, the PKA’s (the government agency for NatureProtection and Preservation) budget has decreased by 40%, while NGOs’involvement has been growing.The second issue is linked to the complexity of investments in conser-

vation. There are many informational problems associated to the protec-tion of biodiversity, because of biological uncertainty, natural variabilityor hidden private information. Moreover, there is an inherent difficulty inmonitoring performance in conservation activities. All of this contributesto contractual incompleteness. The issue of investment incentives in aconservation project is then strikingly similar to the one addressed bythe economic literature on property rights and incomplete contracts inthe context of firms’ organization. This paper will then apply the ideasfrom this literature to the context of conservation.

Contractual incompleteness and the free riding effect are hence twomajor forces shaping the structure of partnerships between NGOs andthe Government in the provision of conservation. How are the investmentincentives of the parties affected in this context?Contractual incompleteness and free riding reinforce each other and

lead to underinvestment. Non excludability of benefits makes breakdownfrom cooperation in a conservation project attractive. This is the freeriding effect. Meanwhile, as contracts are incomplete, agents cannotcommit ex-ante to any investments levels, so that they can easily walkaway from negotiation. Contractual incompleteness also leads them tounderinvest since some of the return of their investment will be dissipatedduring the bargaining over the surplus generated by their investments.

However, there is something specific to conservation projects: localstakeholders exert a pressure on the value of the project. If investorsfree ride, so that local stakeholder do not receive sufficient compensa-tion, conservation is not made an attractive option to them, and theland ends up being converted (illegally or not) to agriculture or logged

3

down. Local stakeholders have the ability to destroy the conservationbenefits of the project to the investors. The existence of this opportunitycost of conservation, which is observable, will then be another major de-terminant of the optimal allocation of property rights over the project.It constitutes an additional instrument, which affects (negatively) thenegotiation break down payoffs and hence the incentives of the partiesto invest in conservation.

The aim of the paper is then to study the role of property rights inthis situation. The general question is: What is the optimal ownershipstructure of an asset, when the value created by the investments con-stitutes a public good, in other words when disagreement payoffs areaffected by the nature of externalities generated by the investments ofboth parties? Investments affect break down payoffs (and hence incen-tives to walk away from the relationship) not only through the privatecost of investment, but also because of the nature of externalities theygenerate. In the case of a private good, granting ownership to a party isthe best way to induce her to invest, because she will get the full benefitof her investment. This may no longer be true with a public good be-cause benefits are not excludable, so that ownership loses this positiveincentive effect.

The property rights issue in the context of incomplete contractingwhen public goods are concerned is studied in section 2 through a reviewof the literature. Section 3 presents the model. The main conclusion ofthe model is that, contrary to what has been stated in the precedingliterature, it is not always optimal to grant ownership of the project tothe most caring party. In some cases, allocating ownership to the partywhich has a lower valuation for the project allows both investors to tietheir own hands and maximize their investments in conservation. Theinsights of the model are applied to the case of conservation concessionsin section 4. Section 5 concludes. The appendix provides for a numericalexample of a conservation project with two investors: a conservationNGO and a governmental agency. There always exists a transfer suchthat the optimal ownership structure is reached, since it is the efficientone. Yet, the example provided tackles the question whether the partieshave enough incentive to reach the efficient ownership structure, in theabsence of an additional transfer between them.

2 Review of the literature

The relation between asset ownership and investment incentives in a pri-vate good context has been largely investigated, in particular by Hart

4

and Moore (1990). These authors consider a situation where two agentsmake complementary investments in a relationship-specific asset. Own-ership of the asset allows the agent to exclude others from the use ofthe asset. The distribution of property rights over the assets determinethe bargaining power of the agents over the returns to investment whichenhances the productivity of theses assets, which in turn determines theincentives to invest. Only the owner gets the full return of his invest-ment, while the others under invest because some of the return of theirinvestment is dissipated during the bargaining process. Asset ownershipraises the outside option of the agent: if the agent-owner walks awayfrom the negotiation, he gets the full benefits of his (and other players’)investments, while the others get zero. Asset ownership of a private as-set always increases the bargaining power of an agent in surplus sharing,and thereby raises his investment incentives. The agent whose invest-ment decision is the most important should always own the asset heworks with.

Besley and Ghatak (1999, 2001) extend the issue of optimal owner-ship of an asset to the case of a public good. Ownership of the assethands over the owner the decision to continue or to abandon the projectin the case negotiation breaks down. This definition will be adopted inthe present paper. Besley and Ghatak (2001) consider that the outsideoption (or equivalently the disagreement payoff) is higher for the ownerthan for the non owner. A key assumption in their model is that themarginal return to a given type of investment is higher in the event ofdisagreement when the party that made this investment is the owner.Following Hart, Shleifer and Vishny (1997), this assumption can be in-terpreted as saying that part of the return of the investment of a player isembodied in her human capital and cannot be realized if she is fired. Inthis context, asset ownership, as in the case of a private good, increasesthe bargaining power of an agent, and hence his investment incentives.It should then be allocated to the agent who values the project more.With transfers being possible between the parties, granting ownership tothe highest valuation party raises the marginal returns to investment ofall players. Nevertheless, assuming that the outside option of the owneris higher than the outside option of the non owner presumes that partof the benefits is excludable, which does not fit with the case of a purepublic good.The impact of asset ownership on investment incentives in the case

of a private good and in the context described by Besley and Ghatak(2001) is the following: ownership of an asset bestows a greater out-side option on the owner, and a greater outside option means a higherbargaining power in surplus sharing, and hence higher incentives to in-

5

vest. However, these two positive relationships: between ownership ofan asset and outside options of the owner; and between outside optionsand higher investment incentives; may fall apart when a public good isconcerned.

A public good is defined by the non excludability and non rivalry ofthe benefits it generates. If benefits are not excludable and non rival, anagent can walk away from the relationship and still enjoy the benefits ofhis, and (more importantly) of his partners’ investments. The outsideoption is then positive for all players (whereas the outside option ofan agent who does not own a private good is zero because there is nobenefit he can capture). Investment in a public good benefits to allagents and increases all agents’ default payoffs. The first consequence ofthis is that the positive relationship between asset ownership and higheroutside option (and higher bargaining power) of the owner falls down.Since costs are, contrary to benefits, excludable, when the owner has tobear more costs than the non owner (which is likely), the relationshipcan even be reversed: asset ownership may decrease the default payoffs.The second consequence is to break the positive relationship between agreater outside option and investment incentives. With non excludablebenefits, a higher disagreement payoff means a higher incentive to freeride, rather than to invest.The core of the problem here comes from the fact that default payoffs

are positive, what induces players to free ride. One way to decrease in-centives to free ride is then to cut down default payoffs (see Matoushek,2002). Default payoffs are minimized when parties can commit to aban-don the project in the case negotiation breaks down.A conservation project generates an opportunity cost for local stake-

holders, which corresponds to the forgone development revenue of theland (in agriculture or logging). If local stakeholders are not compen-sated enough, they may use the asset (the land) in this alternative way,which actually destroys the conservation value of the project. Thisamounts for a third party (the local stakeholders) to exercising an outsideoption and annihilate the value of the default payoffs of the conservationparties, when the latter were unable to make conservation attractive toher.One way to decrease the default payoffs of investors in order to in-

crease their investment incentives is then to rely on the (often de facto)right of a private party to use the project in an alternative way thatdestroys the public value of the project. How can this commitment bemade credible? One way is to allocate ownership to the low valuationparty, since the threat of termination is credible when in her hands. Thiswould mean that it may be socially more efficient for investors to tie their

6

own hands by delegating the project to the least interested party, whatallows them to sharply decrease their break down payoffs and increasestheir investment incentives. Another source of credibility is the powerof the private party to destroy the public project. This actually wouldreinforce the argumentation of those who call for the strengthening ofthe rights of local people and the advocates of community based forestmanagement.

3 The Model

There are two players: the two investors in the public project: the gov-ernment (G) and the NGO (N). The project is ”public” in the sense thatthe benefits it generates, once G and N have invested, are non rival andnonexcludable to G and N.

The project generates an opportunity cost, B, which is borne by thelocal users of the resource. This drives the investors to pay a cost inorder to ensure the compliance of this third party. It is a compensationfor the compliance of a party who does not care about the public valueof the project and who is able to destroy its value. In the example ofa national park, it can be interpreted as the cost which has to be paidto prevent poaching or illegal logging. In the case of a conservationcontract, it is the compensation for the lost development revenues.

At date 1, the players decide on the ownership structure. As inBesley and Ghatak (2001), it is considered that ex ante ownership pro-vides some form of credible commitment to maintain the ownershipstructure ex-post.1 There are two possible ownership structures: own-ership by G, ownership by N.

At date 2, the two investors realize their investments. Let Y =(yG, yN) denote the vector of investment decisions. These investmentsare sunk and cannot be changed.Investments generate a non-verifiable cost: C(yi). Dealing with con-

servation, this could correspond to the cost of the resources affected tothe protection or the restoration efforts of the area (reintroduction ofparticular species, amelioration of the water supply, effort for the pre-vention of fire or salinity...). There is a quality dimension of these efforts

1Since parties will choose the joint-surplus maximizing ownership structure, it isin their interest to make such an ownership comitment. Besley and Ghatak (2001)consider that one way to do so is to consider a design phase at the first stage ofthe game in which the owner undertakes certain actions which require his continuedpresence until the completion of the project.

7

which is not contractible. The size of these investments has also an in-fluence on the amount of the opportunity cost: B(yG, yN), which has tobe paid to the third party.

At date 3, G and N bargain over whether to continue with theproject. Transfers (between G and N, and the transfer to the privateparty) are realized at this stage. If the private party does not receive any,or sufficient transfer, she exercises her outside option, which destroys thevalue of the public project.The opportunity cost is paid at this last stage of the game; whereas

the other investment costs are paid in period 2 and are sunk at date 3.However, the size of this cost is determined by the decisions taken atdate 2.

As usual in the incomplete contract literature, the levels of invest-ment in the project cannot be specified ex-ante. They cannot be guar-anteed by an up-front payment. Following the incomplete contract lit-erature, I consider that the parties bargain over the surplus once theinvestment is sunk using Nash bargaining, and the choice of investmentdepends upon the share of the surplus received by the investing party,who can here be either one of the two investors.

The ownership structure is important in defining the default payoffsin stage 3 because it affects the size of the investments at date 2, thesize of the opportunity cost, and who has to pay for it.As in Besley and Ghatak (2001), it is assumed that the owner has

the residual control rights. Ownership determines who chooses to goahead with the project in the event negotiation breaks down: the ownerdecides whether to continue or to stop the project. This gives the ownersome bargaining power, although this is balanced by the fact that shethen has to pay the outside option, which decreases her disagreementpayoffs and hence her bargaining power. The higher the disagreementpayoff of a party, the stronger is her position in the bargaining game.The party that values the project more has a higher bargaining position,but is hurt more in case the project stops. She will then be ready to givea positive transfer to the low valuation party in order to secure provisionof the public project in the cases where the low valuation party wouldprefer stopping the project, whereas the reverse is not true.

The two investors, G and N, value the project to different degrees.The respective valuations by the government and by the NGO are :

θGV (yG,yN) and θNV (yG,yN)

where θG > 0, θN > 0 are the valuation parameters of G and N.

8

Without loss of generality, it is considered that the NGO values theproject more: θN > θG.

Assumption 1: V (Y ) is a smooth, and increasing function:∂V (yG,yN )

∂yG> 0,

∂V (yG,yN )

∂yN> 0, with

∂2V (yG,yN )

∂yG2< 0,

∂2V (yG,yN )

∂yN 2 < 0

And ∂2V (yG,yN )

∂yi∂yj≷ 0.

The appendix presents the analysis for either substitute or comple-ment investments.

θG and θN are supposed to capture the different preferences of theagents, and V is assumed to be symmetric with respect to both itsarguments.

Assumption 2:Because this public project is non excludable and non rival, each

party benefits from the other’s investment:

θGV (0,yN) > 0 and θNV (yG,0) > 0.

This implies that the default payoff of the non owner is positivesince he benefits from the other’s investment without having to pay theopportunity cost.

Assumption 3:The value of the opportunity cost is positively correlated and convex

with the investment level of the two investors (for example the effortsmade in water supply improvement, against fire or salinity, or moregenerally in restoration of the area will also enhance the agriculturalvalue of the land):

B0yi(yi, yj) > 0

∂2B(yi,yJ )∂y2i

> 0, ∂2B(yi,yJ )∂yi∂yj

> 0 i = G,N.

What is more, B and B0 are assumed to be symmetric with respectto their two arguments.

Two things should be well understood. Firstly, the benefits of in-vestment in terms of conservation and in terms of enhanced agriculturalvalue of the land are mutually exclusive. Secondly, the benefits in landvalue are not externalities generated by the investments; they are ratherwhat has to be bought off to the third part to ensure her compliance (infact they do not come true because at equilibrium, the land is allocated

9

to conservation and not to agriculture). This explains why B appears asa cost.

The first best level of investment is defined by:

MaxyG,yN Max[(θG+θN)V (yG,yN)−C(yG)−C(yN)−B(yG,yN), 0]The public project is then socially efficient as soon as:

(θG + θN)V (yG,yN) ≥ C(yG) + C(yN) +B(yG,yN)that is when the public value of the project (minus the cost of in-

vestment) is higher than the private outside option.

In the absence of any contracting problem, the parties will choosethe level of investments that maximize their joint surplus:

MaxyG,yN (θG + θN)V (yG,yN)− C(yG)− C(yN)−B(yG,yN)

The costs of investment are treated as linear: C(yi) = yi, i =G,N.

Let y∗i denote the joint surplus maximizing level of investment byparty i. It solves the following Lindahl-Samuelson type rule:

(θG + θN)V0yi(y∗G,y

∗N) = B

0yi(y∗G,y

∗N) + 1 i = G,N .

When the parties do not take their investments decisions coopera-tively, the owner follows the program:

Maxyi θiV (yi, yj)−B(yi, yj)− yis.t. yi ≥ 0and the non-owner:

Maxyj θjV (yi, yj)− yjs.t. yj ≥ 0

Lemma 1: If investments are perfect substitute, the non owner con-tributes nothing and totally free rides on the owner of the project.

(See the appendix for a proof).

The individual contribution levels at an interior solution are definedby:

θiV0yi(yG,yN) = B

0yi(yG,yN) + 1 when i is the owner, and

θjV0yj(yG,yN) = 1 for the non-owner.

10

Proposition 1 In general, when the marginal cost is not too high, noncooperative investments levels are suboptimal. With perfect substituteinvestments, non cooperative investment levels are always suboptimal.

Proof. See Appendix.

Underinvestment comes from the fact that each player does not in-ternalize the positive externality of his investment on the other player’swelfare. It is obvious that asset ownership decreases investment incen-tives, because the owner must bear the outside option alone. The twoplayers must then agree on cost sharing to raise efficiency.

The model is solved backwards: the outcome of the bargaining gameat stage 3 is anticipated by the agents and determines their investmentincentives at stage 2. The bargaining game is solved first, and the studyof the investment incentives follows.

3.1 The bargaining gameAccording to the timing of the game, each investor chooses her invest-ment level at date 2. Then, at date 3, the two players bargain on whetherto cooperate and share costs, with transfers being possible at that stage.

Ownership matters because it defines the default payoffs. Indeed, theowner of the project has to pay the opportunity cost, which correspondsto the outside option of the private party. The default payoff (DP) of iwhen j is the owner is denoted by V̄ ji . The default payoffs are the payoffsthe players receive in case the negotiation breaks down. They are differ-ent according to who owns the project since the owner has to bear theopportunity cost. Another source of difference is the different valuationsof the project by the players. In case of break-down in negotiation, theowner decides to go on with the project only if she receives a positivepayoff after having paid for the opportunity cost. In that case, sinceshe receives the benefits of the public good, without having to pay theopportunity cost, the other party receives a positive break-down payoff.The default payoffs are given in the following table:

When the NGO is the owner: When the Government is the owner

DP of theNGO

Max[θNV (yG, yN)−B(yG, yN), 0]θNV (yG, yN)

if θGV (yG, yN)−B(yG, yN) ≥ 00 if not.

DP of theGovernement

θGV (yG, yN)if θNV (yG, yN)−B(yG, yN) ≥ 0

0 if not.Max[θGV (yG, yN)−B(yG, yN), 0]

11

The players adopt Nash bargaining. They split their renegotiationsurplus half, half, over the disagreement point.The transfer from player j to i, when i is the owner is:

tij = argmaxz {θjV (Y )−z−V̄ ij (Y )}{θiV (Y )−B(Y )+z−V̄ ii (Y )}tij =

(θj−θi)V (Y )+B(Y )−V̄ ij (Y )+V̄ ii (Y )2

The transfers are then as follows:

• When N is the owner:- When θNV (Y )−B(Y ) ≥ 0: N is willing to go on with the projectalone and G cannot be induced to contribute, there is no transfer,G free rides on the NGO.

- When θNV (Y )−B(Y ) < 0, both disagreement payoffs of G andN are zero. Since the NGO does not want to go on with the projectalone, the government, if he wants the project to be completed, hasto induce the NGO by giving her a positive transfer. This transferfrom the government to the NGO is: tNG =

(θG−θN )V (Y )+B(Y )2

> 0.

• When G is the owner:- When θGV (Y )−B(Y ) ≥ 0, there is no transfer for similar reasonsas above.

- When θGV (Y ) − B(Y ) < 0, the disagreement payoffs of bothplayers are zero: the government terminates the project if he re-ceives no transfer. The transfer from the NGO to the governmentis: tGN =

(θN−θG)V (Y )+B(Y )2

> 0. The prospect of a positive transferreceived from NGO induces G to invest.

These transfers are credible because the owner has a credible threatof termination in the configuration where those transfers take place.Transfers happen only if the owner has invested. If there is notransfer, the owner decides to terminate the project. It is hence inthe other party’s interest to keep his promise and give the transfer.

Since θG < θN (G is the low valuation party), when made the owner,G is less often willing to undertake the project alone than N is. N hasto induce G to invest, in the cases where G would abandon the projectwhereas N would be willing to continue. This happens whenever the

12

opportunity cost is higher than G0s valuation and lower than N 0s. N caninduce G to invest by giving him a positive transfer in the case he hasinvested. This transfer is credible. Indeed, in this range of values, if Gdoes not receive any transfer, he does not go on with the project and thevalue of the project is destroyed. ConcerningN, she gets sufficient utilityfrom the continuation of the project in this range of values to be willingto give a positive transfer to G. Anticipating the positive transfer, G willinvest at the second stage. In those situations, if N was the owner, shewould undertake the project alone, and G would not participate. UnderG ownership, cooperation and sharing of the surplus occur wheneverB(Y ) > θGV (Y ), whereas under N ownership they occur only whenB(Y ) > θNV (Y ). This means that for all the values of the opportunitycost situated between the two parties’ valuations, G and N cooperatesonly when G is the owner. This brings the first result:

Result 1: Public-NGO partnership occurs more often when the lowvaluation party is the owner, in the sense that it occurs under the sameranges of values of the opportunity cost than under N ownership, andunder all the additional values for which the NGO would have been will-ing to invest alone.

The anticipation of the outcome of this bargaining game determinesthe investment incentives of the agent at the preceding stage.

3.2 Incentives to invest under the different owner-ship structures

Three cases arise depending on the scale of the opportunity cost relativeto the parties’ benefits:

• Case 1: When B(Y ) < θGV (Y ) : the opportunity cost is smallerthan both parties’ valuations. Both parties value the project enoughto be willing to go on with the project even if they are forced toproceed unilaterally.

Transfers are nil, the non-owner will always free ride on the ownerand investment levels are suboptimal (they correspond to the non-cooperative case). NGO ownership is then the best solution, sincethe NGO values the project more and sets a higher level of invest-ment in case she is the owner, than the Government does.

Proposition 2 When the opportunity cost is not so high relative to theproject benefits that either the NGO or the government would want to

13

abandon the project if it is forced to proceed unilaterally, allocation ofownership to the party who has the highest valuation is welfare enhanc-ing.

Proof. See Appendix

• Case 2: When θGV (Y ) < B(Y ) < θNV (Y ). The opportunitycost is situated between the two parties’ valuations of the project.This means that the low valuation party would want to abandonthe project if she was forced to proceed unilaterally, while the highvaluation party would like to continue.

In this ”intermediary” situation, G-ownership improves upon N-ownership. If N is the owner, she invests since B(Y ) < θNV (Y ). Know-ing this, G cannot be made to contribute and then free rides on N . If,on the contrary, the low valuation party is the owner, the high valuationparty has to make a positive transfer in order to induce her to internalizethe positive externality of her investment on the high valuation party’swelfare and thereby induce her to invest.Allocating ownership to the low valuation party strategically compels

both parties to participate, whereas only the high valuation party wouldinvest if she was the owner, while the low valuation party would free ride.Affecting negatively the disagreement payoffs allows reaching a moreefficient level of provision. By granting ownership to the low valuationparty, the disagreement payoffs are nil in a larger number of cases, whatcompels both parties to come more often to an agreement on ex-postsurplus sharing .

Lemma 2: When the opportunity cost lies between the two parties’valuations, allocating ownership to the low valuation party induces par-ties to cooperate and maximize the joint surplus.

The impact on parties’ welfare follows:

Proposition 3 When the opportunity cost is such that only the highvaluation party would be willing to go on with the project if negotiationbreaks down, low valuation party ownership is welfare enhancing.

Proof. See appendix.

14

• Case 3: When (θG+θN)V (Y ) > B(Y ) > θNV (Y ). The opportu-nity cost is so high relative to each party’s benefit, that neither theNGO and the government would want to proceed with the projectunilaterally. Still, it is low enough that the project is socially de-sirable: in that situation, the investment incentives of both partiesare identical under either ownership structures, and are given by:

(θN+θG)V0yi(yG,yN )−B0yi(yG,yN )

2= 1

When N is the owner, she invests if there is a positive transfer fromthe government to the NGO. When G is the owner and invests, there isa positive transfer from N to G.The players have to cooperate in order to reach a positive level of

investment. Who owns the project does not affect the level of investment,it only determines who makes the transfer.

Corollary: In the case where the opportunity cost is so high thatneither party would go on with the project if forced to proceed unilaterally(but still low enough so that provision is socially desirable), the ownershipstructure is irrelevant.

3.3 Incentives for reaching the optimal ownershipstructure

Ownership of the project increases the bargaining position because itconfers on the owner the threat of termination of the project. However,ownership of the project also comes with some liabilities, namely thecost of investment itself, and the opportunity cost that has to be paidto the third party. As the example in section 3 has shown, there mayexist some cases where a party would be better off by free riding than bybeing made the owner. Some additional transfers may then be needed inorder to ensure that the optimal owner actually accepts to become theowner. In particular, in the cases where low valuation party ownershipis optimal, one need to look at the incentives of this party for acceptingownership of the project. If she does not accept, the high valuation partyis the owner, and the low valuation party free rides and invests nothing.In the appendix, it is shown and illustrated with a numerical example

that in the situation where low valuation party ownership is optimal,there always exists an incentive compatible level of transfer such thatthe parties will chose this ownership structure.

4 An Application to Conservation Concessions

The ideas developed in this paper shed some light on two very actualissues. The first issue concerns the relevance of establishing conserva-

15

tion projects negotiated directly between conservation NGOs and pri-vate landholders; and the main message is that these ”direct” deals mayinduce free riding from the government and thereby drive away fromoptimal investment levels. The second issue is related to the debate onlocal communities’ empowerment and on devolution of ownership rightsto communities. The main message is here that these two approacheshave very different implications on the investment incentives of conser-vation investors.

4.1 The impact of conservation concession deals oninvestment incentives

The model developed in this paper can encompass most of the regulatoryinstruments used in conservation. Land appropriation and the establish-ment of national parks would fall in what was considered as case 1: thegovernment is the owner and provider of conservation and the NGO doesnot intervene. Conservation contracts between NGOs and States wouldfall in the ”intermediary case”: G owns the project, and N is the initiatorof the project and provides a transfer to G. Conservation contracts withprivate landholders or communities are a special case, where the thirdparties, which do not value conservation per se, remain the owner of theland to be protected. What is the impact of these new conservation toolson investment incentives of conservationists?

Conservation concessions are a contractual agreement, under whichnational authorities or local resource users agree to protect natural ecosys-tems in exchange for a steady stream of compensation payments fromconservationists or other investors. It requires a negotiated agreementbetween an investor and either a government or resource user.

In the case of a conservation concession with a State, the nationalgovernment remains the owner of the protected area. This case corre-sponds to what is considered in the ”intermediary case” of the model.The government would not undertake the conservation project by itself(otherwise a national park would already be in place), and is assimi-lated to the low valuation party. Conservation concession scheme allowsome NGO, who values conservation more, to invest in order to create aconservation area on a land which would otherwise have been allocatedto different purposes, logging for example. According to the results ofthe model, a transfer should be made from the high valuation party(NGO) to the low valuation one (the government agency) in order toinduce the latter to invest. Existing conservation concessions arrangefor such transfers. Some conservation concessions have for example beennegotiated with the government of Guyana. In July 2002, Conservation

16

International was granted a renewable 30 years Timber Sales Agree-ment to manage 80.000 ha of forest. The agreement involves payment ofacreage fees and royalties comparable to an active timber concession. Italso provides for other payments, namely aimed at community support,rangers training or monitoring, and which are assimilated as the non con-tractible investments in quality in the model above. Similar agreementshave also been negotiated with the governments of Peru and Cameroon,and provide similar payments from the investing NGO to the concernedgovernment.

A few conservation concessions have very recently been negotiatedwith communities. The Centre for International Forestry Research (CIFOR)has proposed to establish such a conservation payments scheme in Setu-lang village in East Kalimantan, Indonesian Borneo. In Indonesia, com-munities have been awarded back their rights over their village forestsduring the decentralization process (revised basic forest law (UU41)). Inmany cases in East Kalimantan, rights have already been sold to loggingcompanies, and forests turned into IPPK2 . The village of Setulang hashowever resisted up to 11 offers by various logging companies to buy therights over its 5.300 ha large village forest reserve to log it down. CIFORhas then proposed to offer some conservation payments to the commu-nity, through the form of a community-based conservation concession,in order to secure the conservation of this forest. The understanding ofthe proposal by CIFOR is that ”for an amount of money somewhat lessthan they are being offered by a logging company, Setulang people wouldagree to maintain the forest and to use it for non timber forest productsextraction, limited timber for subsistence use and eco-tourism”. Theproposal stated on a figure of US $ 30.000 ”to negotiate such a conces-sion and make a conservation payment to the community for the firstfew years”.

The setting developed in this paper can help understanding the roleof the different actors concerned by such a project: the local commu-nity, the conservation NGO and the (local) governmental agency; andthe consequences of this configuration of ownership on the investmentincentives of the investors in conservation. Let us reconsider the modelof section 3 with the new roles of the three agents : the high valuationparty N, the low valuation one G and the private party. The privateparty does not value conservation per se. It acts as an agent whose val-uation parameter for conservation is 0. The NGO and the governmentalagency still value conservation, with: θN > θG > 0. This assumptionmeans that the villagers do not take into account the positive external-

2Ijing Penabang dan Pemeringkan Kayu, the logging licenses.

17

ity of conservation. The local government is more likely to take intoaccount the externality of biodiversity protection, at least at the districtlevel. That explains why the valuation parameter of the governmentis positive but lower than the one of the NGO, which is supposed tointernalize the externalities of conservation at a higher scale than thegovernment.There are now three possible ownership structures: ownership by G,

by N or by the private party. Establishing a conservation concessionon a private land amounts to making the private party owner of theconservation project. The local community remains the owner of theprotected area, and receives a payment from the relevant investors inconservation: NGOs, governments, or both.

According to the analysis developed in this paper, when a NGOnegotiates a conservation concession directly with a community, G isinclined to free ride, which entails an efficiency loss. Indeed, if the NGOis the initiator of the project and decides to invest, the situation isidentical to the case 1 of the model: the NGO invests as long as thebenefits she gets from the project are larger than its costs, and theother party that values conservation less free rides. As investment is notcontractible, no transfer can be made to G to induce him to invest. Ifthe private party is the owner, G loses the threat of termination so thatno transfer between N and G can be made credible. A transfer cannotbe efficient either, since investments are not contractible. G then actsas a free rider.

However, there are some cases where a transfer from N to G mayappear. Often, some specific investments are needed, which only thegovernment is able to make. This is namely the case when security ofland tenure is concerned. The biggest threat on the success of a conser-vation concession in most developing countries is indeed the insecurity oftenure rights. To come back to the example, Setulang village is in con-flict with a logging company that illegally penetrates on its forest; andthe situation with the adjacent villages is much tensed. The core of theconflict is the imprecise delimitation and recognition of the respectivevillages’ forests, and the local government does not seem very eager onresolving the conflict. The security of protected areas cannot be ensuredwithout the support and collaboration of the local government throughits enforcement abilities. This amounts to saying that investments arecomplement: a specific investment by the government is necessary. Localgovernments in Indonesia, which are responsible for forest managementsince the decentralization laws, often back timer companies which rep-resent fiscal (and often corruption-) revenues over conservation, whichmeans forgone tax revenues. Although the central Government of In-

18

donesia displays conservation objectives, the law is hardly enforced bylocal governments which seek to maximize their revenues and for whichconservation is not an attractive option. The role of N if she wants aconservation project to be sustainable, is then to make conservation at-tractive to local governments. A transfer from the investing NGO inorder to induce the government to participate is needed. The questionwhether local governments should receive some money was a big interro-gation during the design phase of the Setulang project. Some criticizedthis approach and claimed that it amounted to corrupting the local gov-ernment. According to the insights of the model developed in this paper,this is not corruption, but rather a necessary transfer in order to inducethe government to take a specific investment in the project. Withoutany transfer, the government will free ride.To illustrate this, let us look at what happens in the model, when

we consider private party ownership and complementary investments bythe NGO and the government. Does it exist a transfer from N to G thatmakes investment of G possible?

When investments are complement: ∂2V (yG,yN )∂yG∂yN

> 0.

If N invests alone, the value of the conservation project is denotedby v(yN) ≡ V (0, yN).When both players invest, the value of the projectis V (yG, yN).If G does not contribute and free rides, his utility is θGv(yN). This

is the outside option of G.The outside option of N is the status quo, that is to say: θNv(yN)−

B(yN).The transfer from the NGO N to the government G is then:

t = argmaxz {θNV (yG, yN)−B(yG, yN)−z−[θNv(yN)−B(yN)]}{θGV (yG, yN)+z − θGv(yN)}t = (θN−θG)(V (yG,yN )−v(yN )]−[B(yG,yN )−B(yN )]

2

There is a positive transfer if the rise in the project benefit accruingto N from G’s investment, discounting what G gets out of it, is higherthan the consecutive increase in the value of the opportunity cost.Considering the net of transfer payoffs, the investment incentives of

the government and of the NGO are respectively:(θN+θG)V

0yG(yG,yN )−B0yG (yG,yN )

2− C 0(yG) = 0

(θN+θG)V0yn(yG,yN )+(θN−θG)v0(yN )−B0yN (yG,yN )−B0(yN )

2− C 0(yN) = 0

Hence, if investments are substitute, only N invests in conservationand compensate the private party for its opportunity cost, while G free

19

rides. If investments are complementary, there exists a possible transferfrom N to G, that induces the latter to invest in conservation and sharethe opportunity cost with N. Hence, if G has some specific investmentsto make, notably in order to make property rights secure, a transfer fromN is necessary (and cannot be assimilated to corruption).

The conclusion here is that establishing conservation concession onprivate land by conservation NGOs, without involving local govern-ments, leads to the free riding of the government, what may raise seriousconcern if the government’s investment is an indispensable prerequisitefor the success of the conservation project. This namely appears tobe the case when the rights of the local community are threatened byconflicts that involve other private parties, for example adjacent com-munities or loggers.

4.2 Some insights on local communities’ empower-ment

There is today a large debate concerning the rights of indigenous peopleon forest land. Facing the poor efficacy of State forestry management,from a point of view of poverty alleviation, commercial exploitation, aswell as conservation, voices are raised to call for a community basedmanagement system. Securing and strengthening rural communities’forest rights do make sense, because it will certainly favor a longer terminvolvement of local communities toward a more sustainable manage-ment. What is more, as the possibility of exploiting the resources oftenexists anyway due to a poor monitoring system, the official recognitionof rural communities’ rights will avoid a number of conflicts and helpalleviate some destructive behavior driven by insecurity. However, itseems that there is some confusion about the ways to get there: trans-ferring or returning ownership of forest areas to the private ownershipof rural communities, strengthening local use and management rights inpublic forests, community based management, or co-management... andthe different consequences of theses approaches.This paper argues that a distinction should be made between the

devolution of ownership and the strengthening and recognition of lo-cal users’ rights. The analysis takes as a prerequisite the necessity ofacknowledging the users’ rights and of offering compensation for anyrestriction of these rights in a conservation goal, should it be under ei-ther private or public ownership. Yet, it was shown that the controlrights over the project should not lie in the hands of the private users.This means that the devolution of ownership rights to communities isnot always the best solution as far as the objective of conservation is

20

concerned. On the contrary, in some cases, granting ownership of theproject to the government is the way to maximize investment incentivesof both the conservation NGO and the government; keeping in mindthat the recognition of the users’ rights and incentives is a necessarycondition for the success of a conservation project.

As a conclusion, although some may argue that local governments arean impediment to conservation, the solution here appears to be some-times to increase the stakes and interest of governmental agencies inconservation, rather than trying to bypass them, especially if they havesome specific investments to take. Indeed, securing conservation as wellas community rights often needs a vastly expended capacity of the Stateto enforce law in forest lands to avoid invasions, squatting and illegal log-ging. In many countries, and particularly in Indonesia, the option is notwhether occupation will continue or not, but whether such penetrationwill take place in an illegal and perhaps violent and chaotic manner, orinstead the government will be willing and able to steer it in an orderlyway. Neither NGOs, nor local communities can be relied upon for theseconflicts to be avoided.

5 Conclusion

The model developed in this paper shows that the optimal ownershipstructure of a conservation project depends on the respective valuationsof the project by the investors, and on the size of the opportunity costit generates.It predicts that negotiating conservation concession with States or

with local communities have different implications. Negotiating a con-servation concession with governments leads to a higher level of invest-ment from both the government and the conservation NGO. However, itis an essential prerequisite for the success of a conservation project thatlocal stakeholders’ rights are recognized. Recognition and strengtheningof local users’ rights is indispensable, but ownership devolution to localcommunities might lead to underinvestment by governmental conserva-tion agencies and hence to a lower level of provision of conservation.

6 Lead for future research

Delegating ownership to the third party may have larger implicationsthan those exposed in the preceding section. One should also considerthe investment incentives of the private party, in the case where she

21

would be made an investor, with the investment yi made part of a con-tract. The increasing use of ”market based instruments” in conservationare equivalent to the delegation of ownership to third parties, but also of-ten delegation of the production of conservation. These ”market basedinstruments” are conservation programs developed on private land, inwhich the private landholders sign a contract with the State or a NGOand are the one that undertake all the investments considered above asyi. Conservation concessions do not exactly fit this case because theyaim at the intact preservation of forest areas. But some other contractsaccount for some specific actions that private landholders should un-dertake in order to increase conservation. These contracts specify thatthe landholder receives a payment based on quality improvement, whichcould corresponds to the investments yi, and is reimbursed his opportu-nity cost and some observable costs (for example fencing costs), whichcan be considered as part of B. This introduces a moral hazard dimen-sion in the non observable effort. These contracts could then have adifferent impact on efficiency, according to their design, and this needsto be studied more closely. The impact on the community’s incentivesof a conservation contract and contract design will be the object of a fu-ture article. There are issues of moral hazard and risk sharing inherentto such contracts, which may have in turn some impacts on the invest-ment incentives of conservationists. An integrated framework would bea very useful tool to study the relevance of different conservation toolsto different institutional situations.

22

7 Appendix:

7.1 Numerical Example

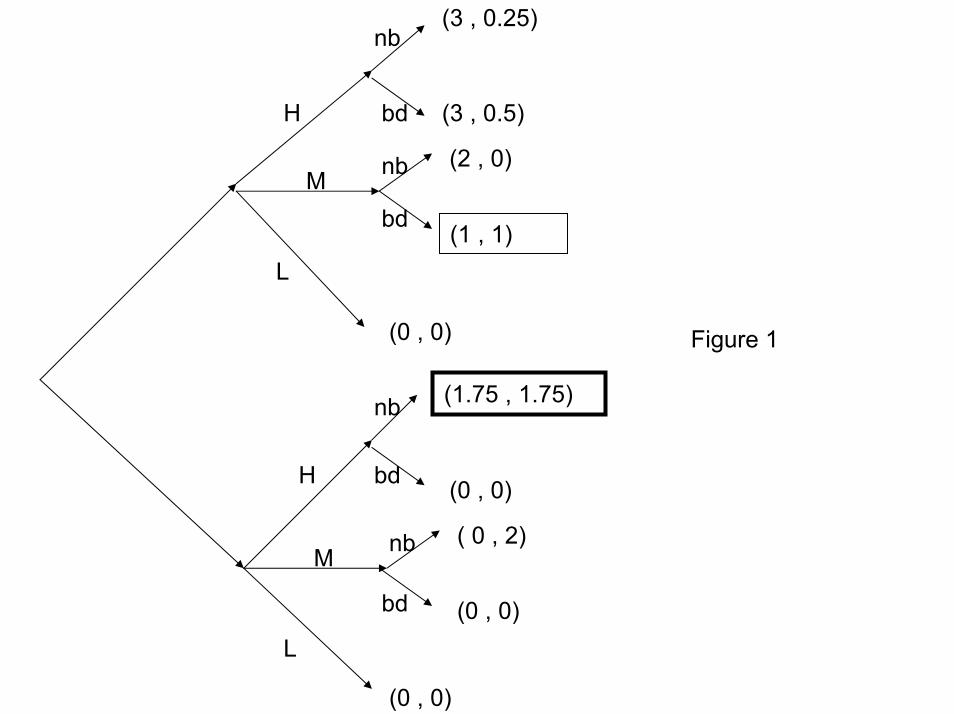

I consider a situation where two investors, the government (he) and aNGO (she) are deciding how much to invest in improving the quality of aconservation project. This project is public in the sense that it generatesnon excludable and non rival benefits to the two investors. I considerhere three investment levels: high, medium and low. The payoffs tothe government from these investment levels are respectively 3, 1 and 0.The NGO values the project more than the government, with respectivevaluation of 7, 5 and 0. (The medium and low situations are identicalto the example of Besley and Ghatak (2001)).The investments of theparties generate two kinds of costs. Firstly, some costs which are noncontractible, for example investment in non verifiable quality, in effortin restoration of the area, or investments to make the property rightssecure. The costs of the high, medium and low levels of investment are,respectively, 3, 2, and 0. Secondly, the project generates an (observable)opportunity cost borne by a third party. This cost is contractible, andincreases with the level of the non contractible investment in quality: itis 3.5 in the high investment project and 2 in the medium one.At the first stage of the game, the players decide on the ownership

structure. Either the government (G) or the NGO (N) is the owner.At stage 2, the players decide on their (non observable) investment lev-els. At stage 3, they bargain over the continuation of the project, withtransfers between the parties being possible. The opportunity cost tothe third party is paid at this last stage. Players adopt Nash bargaining.The private party does not care for the public value of the project and

is concerned only by its forgone outside option when the project is run.Conservation programs have indeed an opportunity cost which is theforegone development revenue (in agriculture or logging for example),and which is borne by local communities. The two investors have tocompensate the third party for this opportunity cost, in order to preventher from destroying the value of the project. In other word, the projectcannot be sustainable if the third party is not compensated, becauseshe would then proceed to illegal logging, poaching or illegal conversionto agriculture. This is a reality in conservation. As reported by theWWF World Bank Alliance (1997), the lack of agreement with localcommunities and undervaluation of their opportunity cost are majorreasons for the insecurity of conservation areas due to illegal poachingor conversion to agriculture. One of the main challenge for managers ofprotected areas is the reconciliation of the local community’s demands

23

for resources and incomes from the protected area with the requirementsof biodiversity conservation.In the context described above, where non contractible investments

generate an additional cost that has to be paid to a third party, two ef-fects will contribute to inefficiencies in the investment level. Firstly, sincethe benefits of investments are not excludable, each party is tempted tofree ride and this leads to underinvestment. Secondly, the size of theopportunity cost has an influence on the investment levels because itaffects the disagreement payoffs of the players, and hence their invest-ment incentives. What is more, the investments are assumed to affectpositively the opportunity cost. For example, investments in the qualityof the water supply affect positively the agricultural value of the land; orinvestments in securing property rights raise the benefits the local com-munity is able to extract from its land (if property rights are correctlyenforced, the loggers will have to pay the full cost of forest extraction,which is not the case if illegal logging is feasible). This opportunity costwhich has to be paid to the third party deters investments if partiesfear to be stuck with the project. However, since it is contractible, thisopportunity cost is an additional tool. I want to show that if the noncontractible investments generate an observable cost, payments condi-tional on the latter allow to recover some efficiency.

The payoffs and costs of the high and medium investment projectsare summarized in the following table:

High investment Medium investmentCost of the sunk investments 3 2Payoff of the Government 3 1Payoff of the NGO 7 5Cost B paid to a third party 3.5 2Total net surplus 3.5 2

The high investment project is the most socially profitable, with anet joint surplus of 3.5 instead of 2 for the medium project.

There are two possible ownership structures: either the NGO or thegovernment is the owner of the project, what confers on them the deci-sion to continue or not with the project.

• Under NGO ownership:

- Concerning the High investment project:

24

At the last stage of the game, when facing the decision to go onor to abandon the project, the NGO gets an ex post surplus of7− 3.5 = 3.5 from continuing the project. She then chooses to goon with the project. G anticipates at the preceding stage that theNGO will go on with the project anyway, and does not contributeanything. G free rides on the NGO. Considering the cost of sunkinvestments, the NGO gets a total net surplus of 3.5 − 3 = 0.5.The government gets 3.

- Concerning the Medium project:

The NGO gets an ex post surplus of 5−2 = 3 from continuing theproject. She then chooses to go on with the project. Anticipatingthis, again, G cannot be made to contribute anything. He choosesto free ride and gets 1. The total net surplus of N (considering thecost of the sunk investment) is 3− 2 = 1.In both cases, the NGO values the project enough to go on with itby herself. There is no threat of termination, G cannot be made tocontribute anything and free rides. The final payoffs for the gov-ernment and the NGO are, respectively (3, 0.5) in the High projectand (1, 1) in the Medium project. The NGO hence prefers under-taking the Medium investment project. No transfer can be madeby G to induce N to choose the High project, although G wouldbenefit from this. As the level of investment is not verifiable, Nwould just cash the transfer and would not change her investmentdecision.

• Under Government ownership:- Concerning the High investment project:

At the last stage of the game, the government faces the decision togo on or to abandon the project. He gets a surplus of 3−3.5 = −0.5from continuing. He would thus prefer to abandon the project,so that he does not invest at the preceding stage. Anticipatingthis, the NGO has an incentive to give G a positive transfer atthe last stage in case G has invested. This transfer is credible.Indeed, if G has not invested, the NGO does not give any transferand the project is abandoned. Both parties get 0-payoff. But incase G has invested, he would abandon the project if N does notgive him a transfer. Hence, N has to give this positive transferbecause the threat of termination by G is credible since G’s expost surplus from continuation, without any transfer, is negative.If they share the surplus from continuation half, half, each player

25

receives: 7+3−3.52

= 3.25 in the example. G is then willing to go onwith the project, and 3.25 is enough to cover the cost of the sunkinvestment (3), so that G invests. The net surpluses for G and Nare then respectively (0.25, 3.25).

- For the Medium project:

G gets a payoff of 1−2 = −1 from continuing the project. He woulddecide to abandon the project if no transfer is received from N, sothat disagreement payoffs are zero. The parties have to cooperatein order to reach a positive level of surplus. Nash bargaining resultsin each player receiving half of the surplus from continuation, here:5+1−22

= 2. Considering the cost of sunk investment, G gets a totalnet surplus of 2 − 2 = 0. Ex post surpluses for G and N arerespectively (0, 2).

G gets a higher payoff when choosing the High level of investment.G-ownership hence results in the High project to be chosen, whichis the total surplus maximizing project.

By making the disagreement payoffs zero, G ownership forces theparties to cooperate and allows to reach the most profitable project. Inthe case of N ownership, N always undertake the project when left byherself: G’s disagreement payoffs are then always positive and he al-ways prefers to free ride. N then chooses the project which maximizesher own payoffs (here the Medium project), which does not necessar-ily correspond to the joint surplus maximizing project (here the Highproject).In both project, one can notice that the value of the observable cost

generated by investments lies between the valuations of the two investors.

However, the game above has two Nash equilibria (see figure 1 inappendix). Under N ownership, the Nash equilibrium is Medium in-vestment and non cooperation. Payoffs are (1,1). Under G ownership,the Nash equilibrium is High investment and cooperation. The cor-responding payoffs are (0.25, 3.25). G’s payoff under G-ownership isthen lower than his payoffs from free riding under N ownership (1). Ghas then a strategic interest in withdrawing and favoring N-ownership.Another bargaining game that aims at favoring G-ownership instead ofN-ownership should be realized, so that the High investment, and not theMedium one, would be picked. N needs to give an additional side pay-ment to G, in order to favor G-ownership. This transfer exists since thereis a net positive surplus of 3.5-2=1.5 to be gained under G-ownership

26

rather than N-ownership. The default payoffs of the bargaining gameare what the players would obtain under N-ownership: (1,1). With Nashbargaining, the value t of this additional side payment between N andG is:

t0 = Argmaxz (3.25− 1− z)(0.25− 1 + z)t0 = 3

2, and the final payoffs of both players are: (1.75, 1.75). The

subgame perfect Nash equilibrium of the game is then cooperation andhigh investment, under G-ownership (see figure 2 in appendix). G own-ership hence leads to a Pareto improvement from N-ownership for bothplayers. Figure 1 represents the tree of this game, with the final payoffs.

7.2 Proofs of the propositionsProof of proposition 1:

The program of the owner is:

Maxyi θiV (yi, yj)−B(yi, yj)− yis.t. yi ≥ 0 (λi)

and of the non-owner:

Maxyj θjV (yi, yj)− yjs.t. yj ≥ 0 (λj)

The first order conditions are:

(FOC)i θiV0yi(yi, yj) = 1 +B

0yi(yi, yj) + λi

(FOC)j θjV0yj(yi, yj) = 1 + λj

• If investments are strong complement, so that the Inada conditionholds, that is to say, if:

V 0yi(0, yj) = +∞V 0yj(yi, 0) = +∞,then there is always an interior solution.

• If investments are perfect substitute, with a weak Inada condition:V 0(0) = +∞, first order conditions can be rewritten as:

27

(FOC)i θiV0yi(s) = 1 +B0yi(s) + λi

(FOC)j θjV0yj(s) = 1 + λj with s = yi + yj

- If λi = λj = 0 (yi > 0, yj > 0), generically, there is no solution.- Let us consider the other possible cases:a) yi = 0, yj = 0 (λi > 0, λj > 0), first order conditions are then:

(FOC)i θiV0yi(s) = 1 +B0yi(s) + λi

(FOC)j θjV0yj(s) = 1,

It is impossible: if θi > θj, and B0(s) > 0, then λi = 0. If θi < θj,there is no solution generically.

b) yj = 0, yi > 0 (λi = 0, λj > 0) , first order conditions are:

(FOC)i θiV0yi(s) = 1 +B0yi(s)

(FOC)j θjV0yj(s) = 1 + λj,

yi solution of θiV 0(yi) = 1 + B0(yi) and yj = 0 are solution of thisproblem. There is a corner solution: the non owner of the project doesnot contribute.

Lemma 1 follows: If investments are perfect substitute, the non ownerdoes not invest in the project and totally free rides on the owner.

Let us now turn to what happens when an interior solution exists.The first best level of investment is given by:

Maxyi,yj (θi + θj)V (yi,yj)− yi − yj −B(yi,yj)s.t. yi ≥ 0, yj ≥ 0λi,λj are the Lagrange multipliers associated with the two constraints.

The first order conditions of this problem are:

(FOC)i (θi + θj)V0yi(yi, yj) = 1 +B

0yi(yi, yj) + λi

(FOC)i (θi + θj)V0yj(yi, yj) = 1 +B

0yj(yi, yj) + λj

For yi > 0, yj > 0 (interior solution), λi = λj = 0, then by com-paring the first order conditions of the non cooperative ,and the coop-erative problems, it is straightforward that the investment incentives ofthe owner i are larger at the optimum than at the equilibrium. The in-vestment incentives of the non owner are (strictly) larger if the followingcondition on the marginal cost holds:

B0yj(y∗i , y

∗j ) <

θi+θjθj

For investments which are (perfect) substitute, the equilibrium levelsof investment are larger at the optimum than at the non cooperativeequilibrium for both players.

28

In the general case, the equilibrium investment levels are suboptimal,with this condition on the marginal cost when investments are comple-ment.

Proof of Proposition 2:

The first order condition of the owner at a non cooperative equilib-rium writes as:

θiV0yi(yi, yj) = 1 +B

0yi(yi, yj)

Differentiating with respect to θi gives:

V 0yi(yi, yj) + θiV00yiyi

∂yi∂θi−B00yiyi ∂yi∂θi

= 0

<=> ∂yi∂θi=

V 0yi(yi,yj)B00yiyi−θiV 00yiyi

B00yiyi(yi, yj)− θiV00yiyi(yi, yj) =

∂2U(yi,yj)

∂y2i, with U(yi, yj) = θiV (yi, yj)−

B(yi, yj)− yi being the general objective function of player i. The prob-lem exhibits concavity, hence B00yiyi(yi, yj) − θiV

00yiyi(yi, yj) < 0. (it was

furthermore assumed that V 00yiyi < 0, and that B00yiyi

> 0), so that:∂yi∂θi> 0.

The level of investment of the owner is therefore an increasing func-tion of his valuation parameter.

Hence, allocating ownership to the high valuation party raises thelevel of investment in the public good.

Proof of Proposition 3:

Under G ownership, the investment level of each player is given bythe maximization of the following program:

Maxyi12[(θi + θj)V (yi, yj)−B(yi, yj)]− yi

s.t. yi > 0

The first order conditions of the maximization of utility by bothplayers i and j are (with λi and λj the Lagrange multipliers associatedwith the positivity constraints in each maximization program) :

(FOC)∗∗i (θi + θj)V0yi(yi, yj) = B

0yi(yi, yj) + 2 + λi

(FOC)∗∗j (θi + θj)V0yj(yi, yj) = B

0yj(yi, yj) + 2 + λj

There exists an interior solution, so that λi = λj = 0. As B and Vare assumed to be symmetric, at this interior solution, the investmentlevels of the players are identical: y∗∗i = y

∗∗j . The concavity of V and the

convexity of B ensure that second order conditions are satisfied.

29

This solution should now be compared with what happens under Nownership (which is according proposition 2 the best non cooperativesolution), in either extreme case of perfect substitute or complementinvestments in the value function.

Under N ownership, investment levels correspond to the non cooper-ative case, and are given by (when i is the owner):

(FOC)i θiV0yi(yi, yj) = 1 +B

0yi(yi, yj) + λi

(FOC)j θjV0yj(yi, yj) = 1 + λj

- If investments are perfect substitute:

The non cooperative solution under N (denoted as i) ownership is:yi > 0 and yj = 0 As the investment level of the non owner j is positiveunder the cooperative solution (y∗∗j > 0) , it is straightforward that theinvestment of the low valuation party is higher under low valuation partyownership and sharing of the surplus.

What about the effect of low valuation ownership on the investmentlevel of the high valuation party and formally owner: i ? There are twoeffects:

1. The cooperative solution implies that imaximizes the joint surplusand not his own. The valuation parameter taken into account in hisinvestment decision is now the sum of the two valuation parametersof both investors (θi + θj) and not only his own θi. This amounts toan increase in the valuation parameter of the player. In the proof ofproposition 2, it was established that:

∂yi∂θi=

V 0yi(yi,yj)B00yiyi−θiV 00yiyi

The increase in the valuation parameter taken into account by theinvestor has a positive effect on his investment level. The increase in thevaluation parameter is exactly θj, so that the subsequent increase in i0sinvestment level is:

dyi =V 0yi(yi,0)

B00yiyi(yi,0)−θiV 00yiyi(yi,0)θj

2. The effect of the increase in the investment of j on the investmentof i has to be taken into account. Differentiating (FOC)i gives:

θi(V00yiyidyi + V

00yiyjdyj)−B00yiyidyi −B00yiyjdyj

so that:dyidyj= −θiV

00yiyj

−B00yiyjθiV 00yiyi−B00yiyi

As B0 is symmetric with respect to its arguments, B00yiyi = B00yiyj

30

If investments are substitute in the value function, then V 00yiyj < 0and V 00yiyi = V

00yiyj

if they are perfect substitute.If investments are perfect substitute in the value function, then there

is complete crowding out of the investment of i by the investment of j :dyidyj= −1

The rise in the investment of j is exactly his investment level sinceyj = 0 under N ownership with perfect substitute investments. The(negative) effect on j0s investment on i0s investment is then:

dyi = −y∗jSince there is perfect crowding out, the effect on the total investment

level is nil.However, the first effect due to the increase in the value parameter

taken into account by i remains and is positive.The total effect on the investment level of i is then positive, and is

just equal to the effect of the increase in the valuation parameter.Both the investments of i and j are higher under low valuation party

ownership than under high valuation party ownership. The problembeing concave, the subsequent increase in the cost of investments due tohigher investment levels do not offset the increase in the utility of theplayers. The total effect on welfare is then positive.

- If investments are complement in the value function:

Let us first look at the effect of the transfer of ownership to thelow valuation party on the investment of the high valuation party (andformal owner) i :If investments are complement, V 00yiyj > 0, whereas V

00yiyi

< 0. Then,dyidyj> −1

With complement investments, the crowding out effect is less strong,so that an increase in yj is not offset by a similar reduction in yj. If thesubsequent increase in B is not taken into account, the effect is strictly

positive for both players: dyidyj= −V

00yiyj

V 00yiyj> 0, i = G,N.

The effect of the increase in the valuation parameter taken into ac-count by i and j is still valid and leads to an increase in the investmentlevels of both players.

The overall effect on total investment is then positive in any case.

31

7.3 Incentives for reaching the optimal ownershipstructure

Let us consider the situation where low valuation party ownership isoptimal, that is to say when: θGV (Y ) < B(Y ) < θNV (Y ).(y∗∗G , y

∗∗N ) denote the vector of investment reached under low valuation

party ownership.(0, y0N) is the level of investment reached under high valuation party

ownership (G free rides and invests nothing).Low valuation party is optimal when the value created by investments

in conservation under this ownership structure is higher than what isobtained under high valuation party ownership, that is to say when:

(E) (θG + θN) [V (y∗∗G , y

∗∗N )−V (0, y0N)] > C(y∗∗G )+C(y∗∗N )−C(y0N)+

B(y∗∗G , y∗∗N )−B(0, y0N)

holds.In case of G ownership, section 4.1. has established that a transfer

will be made from N to G. This transfer is:

tGN(y∗∗G , y

∗∗N ) =

(θN−θG)V (y∗∗G ,y∗∗N )+B(y∗∗G ,y∗∗N )2

The ex post payoffs of the government and the NGO after this trans-fer and the payment to the private party have been made are respec-tively:

θGV (y∗∗G , y

∗∗N )+t

GN(y

∗∗G , y

∗∗N )−B(y∗∗G , y∗∗N )−C(y∗∗G ) = (θN+θG)V (y

∗∗G ,y

∗∗N )−B(y∗∗G ,y∗∗N )2

−C(y∗∗G ), and

θNV (y∗∗G , y

∗∗N ) − tGN(y∗∗G , y∗∗N ) − C(y∗∗N ) = (θN+θG)V (y

∗∗G ,y

∗∗N )−B(y∗∗G ,y∗∗N )2

−C(y∗∗N )

G accepts to become the owner of the project if the benefits receivedfrom the transfer from N and from the increased conservation value ofthe project minus its costs outweighs what he would get by free ridingunder N-ownership, that is to say if the following individual rationalitycondition holds:

(IR)1G(θG+θN )V (y

∗G,y

∗N )−B(y∗G,y∗N )2

− C(y∗G) > θGV (0, y0N)

(E) may hold without (IR)1G being satisfied. However, there is inthat case a positive surplus to be shared in order to induce G-ownership.An additional transfer (from N to G) would then be needed in everycase (IR)1G does not hold. This transfer is always available when lowvaluation party ownership is efficient (that is to say when (E) holds).The outside options of the players in this new bargaining game are what

32

they would obtain under N ownership and non cooperation, that is tosay:

θGV (0, y0N) for the government, and:

θNV (0, y0N)−B(0, y0N)− C(y0N) for the NGO.

The additional transfer from N to G in order to induce G to ac-cept ownership of the project rather than free riding on the NGO hencecorresponds to:

t0 = argmaxz { (θG+θN )V (y∗G,y∗N )−B(y∗G,y∗N )2

−C(y∗N)−z−[θNV (0, y0N)−C(y0N)−B(0, y0N)]}{ (θG+θN )V (y

∗G,y

∗N )−B(y∗G,y∗N )2

−C(y∗G)+ z− [θGV (0, y0N)]}t0 = (θG−θN )V (0,y0N )+C(y0N )+B(0,y0N )+C(y∗G)−C(y∗N )

2

One can now check whether this mechanism respects individual ra-tionality, in the sense that both G and N would be better off underG-ownership with this additional transfer than under N-ownership.The ex-post payoff of the government is:

UG =(θG+θN )V (y

∗G,y

∗N )−B(y∗G,y∗N )−C(y∗G)−C(y∗N )

2+(θG−θN )V (0,y0N )+C(y0N )+B(0,y0N )

2

The transfer t0 does not affect investment incentives; it just entailsa different sharing of the ex-post surplus. Low valuation ownership,together with the transfers t and t0, respects individual rationality if thefinal payoff of G under this ownership structure is higher than whathe would get by free riding on the NGO under high valuation partyownership. The condition for individual rationality writes as:

(IR)2G UG ≥ θGV (0, y0N)

<=>(θG+θN )V (y

∗G,y

∗N )−B(y∗G,y∗N )−C(y∗G)−C(y∗N )